UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the fiscal year ended December 31, 2009 | ||

| Or | ||

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from __________ to _________ | ||

Commission file number: 0-33347

Ambassadors Group, Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 91-1957010 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

Dwight D. Eisenhower Building 2001 South Flint Road Spokane, WA | 99224 | |

| (Address of Principal Executive Offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (509) 568-7800 | ||

| Securities registered pursuant to Section 12(b) of the Act: | ||

| Common Stock, $.01 Par Value | The NASDAQ Stock Market | |

| (Title of Class) | (Name of each exchange on which registered) | |

| Securities registered pursuant to Section 12(g) of the Act: | ||

| None | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

o Yes |

ý No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

o Yes |

ý No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

ý Yes |

o No |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

| o | Yes | |

| o | No |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

| o |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer x | ||

Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| o | Yes | |||

| ý | No |

The aggregate market value of the voting stock held by non-affiliates of the registrant, based upon the closing sales price of the Common Stock on the NASDAQ Stock Market on June 30, 2009, was $117.9 million. Shares of Common Stock held by each executive officer and director, and by each individual and entity that owns 5% or more of the outstanding Common Stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of shares of the registrant’s Common Stock, $0.01 par value, outstanding as of February 18, 2010 was 19,018,865.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement relating to the 2010 Annual Meeting of Stockholders are incorporated by reference into Part III of this Annual Report on Form 10-K to the extent stated herein.

TABLE OF CONTENTS

| Page | ||

| PART I | ||

| Item 1. | Business | 1 |

| Item 1A. | Risk Factors | 9 |

| Item 1B. | Unresolved Staff Comments | 13 |

| Item 2. | Properties | 14 |

| Item 3. | Legal Proceedings | 14 |

| Item 4. | Reserved | 14 |

| PART II | ||

| Item 5. | Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 15 |

| Item 6. | Selected Financial Data | 18 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operation | 19 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 31 |

| Item 8. | Financial Statements and Supplementary Data | 31 |

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 31 |

| Item 9A. | Controls and Procedures | 31 |

| Item 9B. | Other Information | 34 |

| PART III | ||

| Item 10. | Directors, Executive Officers and Corporate Governance | 34 |

| Item 11. | Executive Compensation | 34 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 34 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 34 |

| Item 14. | Principal Accountant Fees and Services | 34 |

| PART IV | ||

| Item 15. | Exhibits, Financial Statement Schedules | 35 |

| Signatures | II-1 | |

Forward-Looking Statements

Statements contained in this Annual Report on Form 10-K of Ambassadors Group, Inc., which are not historical in nature, are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended (the “Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These forward-looking statements include, without limitation, statements that relate to expectations concerning matters that are not historical facts. Words such as “projects,” “believes,” “anticipates,” “plans,” “expects,” “intends,” and similar words and expressions are intended to identify forward-looking statements. These forward-looking statements reflect our beliefs or current expectations with respect to, among other things, trends in the travel and education industry, our business and growth strategies, our use of technology, our ability to integrate acquired businesses, and fluctuations in our results of operations.

Forward-looking statements involve certain risks and uncertainties that could cause actual results to differ materially from anticipated results. These risks and uncertainties include factors affecting the travel and education industry generally, competition, dependence on key personnel and vendor relationships, our ability to successfully integrate the operations of existing or acquired companies, and a variety of factors such as periods of international unrest, the outbreak of disease, changes in the direct-mail environment, protection of intellectual rights, unidentified taxation exposure, recession, weather conditions and concerns for passenger safety that could cause a decline in travel demand, as well as the risk factors set forth in Item 1A and other factors as may be identified from time to time in our filings with the Securities and Exchange Commission (the “SEC”) or in our press releases. All forward-looking statements are expressly qualified in their entirety by these factors and all related cautionary statements. We do not undertake any obligation to update any forward-looking statements.

Ambassadors Group, Inc. (“Ambassadors,” “Company,” “we,” “us” or “our”) is a leading educational company that organizes and promotes worldwide travel programs for students, athletes and professionals, and provides over 8 million pages of online research content through www.BookRags.com. We were founded in 1967, reincorporated in Delaware in 1995, and operated as Ambassadors Education Group, a wholly owned subsidiary of Ambassadors International, Inc. (“International”) until February 2002. Effective February 28, 2002, Ambassadors spun off from International by virtue of a special stock dividend to International’s shareholders of all of the outstanding shares of our Company that International owned (the “Distribution”). Beginning March 1, 2002, we began operating as an independent stand-alone company. Trading of our Common Stock on the NASDAQ Stock Market began on March 1, 2002 under the symbol “EPAX.” Our principal offices are located in Spokane, Washington, USA.

Our travel business consists of several specialized private-label educational travel programs, including (i) the “People to People Student Ambassador Programs” (“Student Ambassador Programs”), which provide opportunities for grade school, middle school and high school students to visit domestic and foreign destinations to learn about the history, government, economy and culture of such countries, (ii) the “People to People Sports Ambassador Programs” (“Sports Ambassador Programs”), which provide opportunities for middle school and high school athletes to participate in international sports challenges, (iii) the “People to People Leadership Summit,” and “World Leadership Forum” (“Leadership Programs”), which provide domestic travel experiences for grade school, middle school and high school students emphasizing leadership, community involvement, and government education, (iv) the “People to People Citizen Ambassador Programs” (“Citizen Ambassador Programs”), which provide foreign travel experiences for professionals, with emphasis on meetings and seminars between delegates and persons in similar professions abroad and (v) “Discovery Student Adventures”, which provide opportunities for grade school, middle school and high school students to visit foreign destinations with an emphasis on adventure and scientific exploration.

Since 1995, we have expanded our travel operations primarily through internal growth and three acquisitions of educational or travel related businesses. Since 1963, we have organized programs for nearly 515,000 students, athletes, and adults. Our educational travel programs feature visits abroad, including, but not limited to, Antarctica, Australia, China, France, Germany, Great Britain, Italy, New Zealand, and South Africa. In 2009, 34,248 delegates, including students from 95 different countries, traveled on our programs to 47 countries on seven continents.

We have the exclusive right from People to People International (“People to People”) to develop and conduct student programs for kindergarten through high school students using the People to People name. We also have the non-exclusive right to develop, market and operate programs for professionals, college students and athletes using the People to People name. At the present time, we are the only entity that has been given this right by People to People. These rights, granted pursuant to agreements with People to People, expire in 2020. People to People is a private, non-profit organization dedicated to the promotion of world peace through cultural exchange. We also have the exclusive right from Discovery Education, Inc. (“Discovery Education”) to develop and conduct international student programs for kindergarten through high school students using the Discovery Education marks and the name “Discovery Student Adventures.” In addition, we have the first right of refusal to develop, market and operate programs for students to domestic destinations. These rights, granted pursuant to agreements with Discovery Education, expire in 2014.

People to People was founded by President Dwight D. Eisenhower in 1956 and was originally administered by the U.S. State Department. Eight U.S. presidents since President Eisenhower have served as the honorary chairman of People to People. Mary Eisenhower, the president and chief executive officer of People to People, also continues her grandfather’s legacy by serving the organization.

We believe that our 43 years of continuous experience, relationships arising from organizing travel programs, and our association with People to People have provided the foundation for our Company. This foundation allows us to develop and maintain strong strategic alliances and a competitive edge in the educational and travel industries at a competitive program cost. This foundation also allows us to provide high-quality and unique educational programs and customer service. We intend to continue to grow our business internally through marketing enhancements, new programs and strategic alliances, and may make selective acquisitions of and/or joint agreements with travel, education, and direct marketing related businesses.

On May 15, 2008, we acquired 100 percent of the stock in the educational website BookRags, Inc. (“BookRags”) (www.BookRags.com). BookRags was founded in 1999. It initially started as a source for online book summaries and notes, and has grown to include a wide variety of content, including lesson plans, film summaries, biographies, and literary criticisms. The BookRags’ demographic is similar in nature to that of Ambassador Programs, Inc.(“Ambassador Programs”) and although it is not travel related, BookRags is a complementary fit to our business model in relation to marketing opportunities, as well as the seasonality of our travel business. The results of BookRags have been consolidated into our results of operations since May 15, 2008.

On January 15, 2009, our subsidiary, World Adventures Unlimited, Inc. (“WAU”) (fka ‘Ambassadors Specialty Group, Inc.’), signed a five year license agreement with Discovery Education. The agreement grants us the exclusive right to license all-inclusive land based group travel packages for students in kindergarten through twelfth grade to destinations outside of North America using the Discovery Education marks and the name “Discovery Student Adventures". Pilot programs were operated in the summer of 2009 in preparation for Discovery Student Adventures’ inaugural 2010 travel season. Costs of operating the pilot programs, as well as general start-up costs, have been consolidated into our results of operations since January 15, 2009.

Student Ambassador Programs

Our Student Ambassador Programs provide an educational opportunity for students in grade school, middle school and high school to travel to one or more foreign countries or domestically, and to learn about the history, government, economy and culture of such countries. We market our Student Ambassador Programs predominantly through a combination of direct mail and local informational meetings primarily from August through February. Our representatives review candidate applications and conduct selection interviews throughout the country. Accepted applicants participate in orientation meetings to prepare for their educational travel programs.

Our Student Ambassador Program delegations depart primarily during the summer months, June through August, and generally travel for approximately fourteen to twenty-three days, during which time each delegation visits one or more countries. Each delegation generally consists of approximately 30 to 40 students and is accompanied by several teachers and local guides in each country who assist the delegations for the duration of each program. Teachers and students composing a delegation generally come from the same locale.

Programs are designed by our staff of international planners and researchers to provide an educational and entertaining travel experience by exposing students to the history, government, economy and culture of the country or countries visited. We have contracts with program coordinators to provide day-to-day coordination and oversight of the programs. In many instances, we also provide students with the opportunity for a brief stay with a host family, which gives students a glimpse of daily life in the visited country.

Eligible students who complete certain written assignments and other projects can receive high school and university credit for their participation in the program. Universities recognizing academic credit include, but are not limited to: Stanford University; Princeton University; Yale University; the University of California, Los Angeles; the University of Washington; MIT (Massachusetts Institute of Technology); Brown University; Johns Hopkins University; Columbia University; Cornell University; Dartmouth College and Georgetown University. In addition, high school students who successfully complete the program may be eligible to receive service-learning credits, which have become a high school graduation requirement in many curricula countrywide.

Sports Ambassador Programs

Our Sports Ambassador Programs provide an opportunity for student athletes in middle school and high school to explore the host country’s culture and most participate in international tournaments with teams from across the world in different sports. We market our Sports Ambassador Programs through a combination of direct mail and local informational meetings. We have also partnered with key organizations to promote our programs at local and national tournaments. Interested athletes apply to the program and are interviewed by our representatives, after which the selected athletes are accepted for the program.

Delegates in the Sports Ambassador Programs depart during the summer months, June through August, and travel for approximately nine to fourteen days. Teams are formed based on gender and age, and most teams comprise athletes from several different states. During a three- to four-day training camp, athletes competing in tournaments participate in an individual skill assessment, after which rosters are formed to ensure balanced and competitive teams. After the formation of rosters, the rest of the training camp focuses on team practice and fundamentals in preparation for the ensuing tournament competition. In each tournament, we have contracts with overseas tournament organizers to provide day-to-day coordination and oversight of the programs. Additionally, athletes participate in sports nutrition, psychology, leadership, physical training and international cultural excursions.

Eligible athletes who complete certain written assignments and projects can receive university credit for their participation in the program. Universities recognizing academic credit include, but are not limited to: Stanford University; Princeton University; Yale University; the University of California, Los Angeles; the University of Washington; MIT (Massachusetts Institute of Technology); Brown University; Johns Hopkins University; Columbia University; Cornell University; Dartmouth College and Georgetown University.

Leadership Programs

Our Leadership Programs provide the opportunity for motivated students with academic promise, leadership potential and a desire to serve their communities to travel domestically and internationally to exchange ideas with renowned speakers, field specific experts, professional educators and their peers. These programs are specifically designed for students in fifth through twelfth grades. In addition to the academic coursework, delegates engage in specially designed leadership study, team-building and leadership-building exercises.

We market the Leadership Programs through direct-mail marketing and online efforts throughout the year. Students travel throughout the year for approximately five to ten days. Leadership Programs include group discussions, workshops, educational meetings and other social and recreational activities. Programs originate from our internal marketing and research staff, who identify academic topics, speakers and facilitators. We organize and operate all activities of most of our Leadership Programs, including speakers, facilitators, events, accommodations and transportation.

Delegates traveling on our Leadership Summit programs, grades nine through twelve, may be eligible to receive transferable high school or university credits as part of the academic program. Universities recognizing academic credit include, but are not limited to: Stanford University; Princeton University; Yale University; the University of California, Los Angeles; the University of Washington; MIT (Massachusetts Institute of Technology); Brown University; Johns Hopkins University; Columbia University; Cornell University; Dartmouth College and Georgetown University. In addition, students who successfully complete the program may be eligible to receive service-learning credits, which have become a high school graduation requirement in many curricula countrywide.

Citizen Ambassador Programs

Our Citizen Ambassador Programs provide professionals with common interests the opportunity to travel abroad to meet and exchange ideas with foreign citizens who have similar backgrounds, interests or professions. Citizen Ambassador Programs are developed and travel throughout the year. Direct-mail invitations are sent to candidate delegates approximately six to eight months prior to the travel period for the delegation. Each program is designed to meet the interests of the individual delegates, and travels for eight to twelve days, with an optional additional cultural exchange following each program. Programs originate from our internal development and research staff, who identify potential delegation topics and leaders. Professional programs have been conducted in such areas as agriculture, economics, education, law, medicine and science. Many of our professional programs provide continuing educational credit for the delegates as part of the program experience. Continuing education credits are granted through alliances with professional and academic institutions, including the Wilderness Medical Society, the University of Pittsburgh, the American Bar Association, many state bar associations and other professional associations and societies.

We believe that our Citizen Ambassador Programs provide delegates with enriching experiences and deeper understandings of foreign cultures and people than visits arranged independently or through travel agencies. Unlike travel programs provided by travel agencies, these professional exchanges are intended largely as working programs, with a significant amount of the participant’s time involved in organized meetings, seminars and round-table discussions with their foreign counterparts; visits to significant foreign facilities and institutions; and informal gatherings with foreign counterparts. Each program is led by a delegation leader based upon his or her recognition in the field and expertise regarding the special focus of the particular program.

Discovery Student Adventures

Discovery Student Adventures provide students age ten through eighteen and their teachers an opportunity to feed their curiosity about the world and experience rare and adventurous activities. As is suited to programs associated with Discovery Education, the trips provide immersive education in the sciences and personal access to researchers and experts in biology, ecology, geology, and other fields.

Trips are seven to sixteen days in length and take place each spring and summer to destinations from the Arctic to South Africa. Invitations are sent throughout the year to kindergarten through twelfth grade educators to lead travel groups and expand their students’ education. Pilot programs were operated in the summer of 2009 in preparation for Discovery Student Adventures’ inaugural 2010 travel season.

Educators leading the trips may be eligible for continuing education credit, and students in grades nine through twelve may choose to earn transferable high school credit as part of the academic program.

BookRags

The BookRags’ website, www.BookRags.com, is an educational website that attracts millions of users and advertisers each month. Students and teachers are able to “research anything” through over 8 million pages of content, including BookRags-created material, licensed material, user-generated content, and other third party content. BookRags provides book summaries, critical essays, as well as online study guides, biographies and references to encyclopedia articles. Due to the nature of this business and the users of the website, most of BookRags’ revenues are earned during the months of September through June.

Segment Information

Historically, our operations were organized into one operating segment, consisting of out-of-classroom educational travel services to students, professionals and athletes through multiple itineraries within various travel program types. The five types of travel programs have been aggregated as a single reporting segment based on the similarity of their economic characteristics and services provided. Beginning May 15, 2008, with the acquisition of BookRags, our operations were organized into two operating segments, which have been determined to be two reporting segments. These two reporting segments are (1) Ambassador Programs and Other, representing our travel programs and (2) BookRags, an internet research site housing content sales and advertising revenue. The acquisition of BookRags aligns with our mission of bridging cultural and political borders through education See Note 15, Segment Reporting, in our consolidated financial statements in this Form 10-K for further segment information.

Academic Accreditation

Since 2004, we have been academically accredited through the Northwest Association of Accredited Schools. We developed the Washington School of World Studies to provide an opportunity for high school students to earn academic credit through their participation in the Student Ambassador Programs, Sports Ambassador Programs, Leadership Programs, or Discovery Student Adventures. The courses offered by the Washington School of World Studies emphasize the total learning experience of the participant while preparing for and participating in the selected program. In addition to elective academic credit, students are eligible to earn service-learning credits on select programs after successfully completing the course requirements. Since inception, the Washington School of World Studies has granted approximately 182,000 academic and service-learning credits.

Since 2007, we have been able to provide teacher leaders with continuing education units from their study and work as leaders through the International Association for Continuing Education and Training (“IACET”). As an authorized IACET provider, we have granted approximately 2,500 continuing education units.

Our delegates and teacher leaders are also able to earn academic credit through Eastern Washington University’s Eisenhower Center (“EWU”). Student Ambassadors in grades nine through twelve may enroll in EWU courses and earn up to 12 credits. In addition, Student Ambassadors in grades seven and eight are eligible to earn one credit per course. Teacher leaders many enroll in EWU courses and earn up to five credits. Between 1980 and 2009, Student Ambassadors transferred more than 42,500 college credits from EWU to universities of their choice. Since 2006, teacher leaders have earned more than 1,950 college credits from EWU.

Strategic Alliances

Alliances with Students on Ice, Inc. and Full On (Europe) Limited provide adventure and quality for our Student and Citizen Ambassador Programs. These agreements prescribe the nature, scope and pricing of the travel services provided to our delegates. An alliance with Safe Passage Travel I, LLC, provides safety awareness to support the education and support of safe travel practices.

We have also entered into alliances with the American College of Medical Quality, the American Bar Association and the University of Pittsburgh to provide continuing education credits for our Citizen Ambassador Programs.

Service and Trademarks

We have registered or applied for a variety of service and trademarks, including, but not limited to, the names “People to People Ambassador Programs,” “People to People Student Ambassador Programs,” “People to People Sports Ambassador Programs,” “People to People Citizen Ambassador Programs,” “People to People Leadership Programs,” “BookRags” and “Society for Global Citizens.” In addition, we have the right, subject to certain exceptions, to use the People to People and Discovery Education name, service mark and logo for use in our marketing. We believe that the strength of our service and trademarks is valuable to our business and intend to continue to protect and promote our marks as appropriate. We believe that our business is not overly dependent upon any one trademark or service mark.

Insurance

We maintain insurance coverage that we believe is adequate for our business, including, but not limited to, professional and general liability insurance. We also maintain insurance coverage on our leased real property and personal property on a replacement cost basis. There is no assurance that the insurance maintained by us will be adequate in the event of a claim, that such insurance will cover a claim or loss, or continue to be available in the future.

Employees

On December 31, 2009, we employed 251 employees, of which 244 were full-time employees. Of our full-time employees, 223 are located in Spokane, Washington, six are located in Seattle, Washington, seven are located in Washington, D.C, and eight are located in various states across the United States to serve as local field representatives. We have 154 full-time employees engaged in selling and marketing and 90 full-time employees in general and administrative positions. We also employ a temporary workforce on a seasonal basis to assist with our direct marketing efforts in recognition of the fact that our travel programs are seasonal in nature. None of our employees are subject to collective bargaining agreements or are represented by a union. We believe that our labor relations are good.

Competition

The travel industry and the educational segment within the travel industry are highly competitive. Our Student Ambassador Programs, Sports Ambassador Programs, Leadership Programs and Discovery Student Adventures compete with similar educational travel programs operated by other individuals and organizations, as well as independent programs organized and sponsored by local teachers with the assistance of local travel agents. Our Sports Ambassador Programs also compete with independent organizations, which coordinate and travel already intact teams for international competition. Citizen Ambassador Programs compete with independent professional associations and educational institutions, which sponsor and organize their own travel programs through the assistance of local travel agents, and other organizations that design travel programs and continuing professional education for adults.

We believe that the principal basis of competition in the educational travel segment of the market is the quality and uniqueness of the educational program offered, customer service, safety, reputation and program cost. We believe that our 43 years of experience organizing student and professional educational programs and established relationships with public officials, organizations and residents in countries where we provide programs, as well as our agreements with People to People and Discovery Education, allow us to provide an educational opportunity that is not easily duplicated by competitors’ programs.

We believe the barriers to entry are relatively low for any future competitors. Certain organizations engaged in the travel business could have substantially greater financial, marketing and sales resources than we do. There can be no assurance that our present or future competitors will not exert significant competitive pressures on us in the future.

In addition to competition we face in the travel industry, we also face significant competition from a wide variety of content and media Web properties with companies throughout the world. Content and advertising on the internet are intensely competitive and have been rapidly evolving with converging technologies. We compete with many larger Web properties that have larger staff dedicated towards selling and advertising and have more traffic to offer potential advertisers. We anticipate that this competition will increase over time as Internet usage continues to grow. We believe that the internet still offers a more attractive and measurable advertising option than traditional off-line media including television, radio, billboard, magazine, and newspaper.

Available Information

We are subject to the informational requirements of the Exchange Act that require us to file reports, proxy and information statements, and other information with the SEC. The public may read and copy our filings at the SEC’s Public Reference Room, 100 F. Street, N.E., Washington, D.C. 20549. The SEC maintains an Internet site that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC at www.sec.gov. Similarly, we maintain a website at www.AmbassadorsGroup.com, where we make available our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports as soon as reasonably practical after, or on the same day as, such material is electronically filed with or furnished to the SEC. We make these available free of charge.

BUSINESS STRATEGY

We believe that high-quality programs and exceptional customer service are and will remain key elements of our success. Our strategy is to maintain our high quality and unique out-of-classroom educational experiences while increasing the volume of business. To grow the business, we intend to (i) introduce new and expand existing marketing channels and to increase volume of current educational travel programs, (ii) introduce new educational travel programs independently and through strategic alliances, (iii) further develop our internet presence, and (iv) pursue acquisition opportunities.

Expand the Marketing and Travel Volume

U.S. Census data projects that there will be more than 42.8 million people in the 10- to 19-year-old age range by 2015, from 41.1 million people in 2010. We believe that a large number of qualified students in this age group are not aware of our youth travel programs. In light of these factors, we intend to further develop our marketing techniques by making greater use of referrals from teachers, parents and past student travelers, targeting strategic partnerships, and expanding and refining our extensive databases of potential customers using more precise business intelligence techniques.

According to U.S. Census data, the number of Americans 45 to 74 years old is expected to grow substantially, increasing to more than 110.4 million people in 2015, from 102.3 million people in 2010. We expect this trend to benefit our program growth, as this population segment historically has been the most likely to participate in one of our professional travel programs. In addition, we believe that American adults interested in traveling abroad will increasingly seek convenient and unique experiences. Consequently, we believe that the opportunity exists to expand the professional educational travel programs by continuing to increase the quality and number of specialty professional programs, including professional education credit opportunities, and by exploring new country destinations. We continue to look for alliances with partners that have strong brand recognition and access to well-defined customer segments.

Introduce New Programs

We continually seek to develop and introduce additional innovative and educational experiences. We intend to maintain our contacts with foreign governmental agencies and officials and utilize these and other foreign contacts to organize opportunities for our program delegates that other travel programs do not currently offer. In addition, we may develop new youth travel programs organized around common extracurricular activities such as science, nature and music.

Expand Website Traffic

According to the U.S. Census, there will be over 48 million people in the United States by 2015 between the ages of 14 and 24. Worldwide, there will be almost 1.4 billion people between the ages of 15 and 24. According to internetworldstats.com, worldwide penetration of the Internet is below 26% at the end of 2009, but is rapidly growing. As we continue to add content, resources, tools and functionality to our websites, we anticipate increasing our appeal to and penetration of these ages as well as other age groups.

Pursue Acquisition Opportunities

We consider the travel and youth education industries encompassed by our business to be large and fragmented, which present attractive acquisition opportunities. We believe acquisitions of businesses that are either compatible with our current business or represent a developing specialty segment may be an opportunity for future growth.

Item 1A. Risk Factors

The following risk factors could materially and adversely affect our future operating results and could cause actual results to differ materially from those predicted in forward-looking statements we make about our business.

A decline in the travel industry could adversely affect our results of operations.

Our results of operations will depend upon factors affecting the travel industry in general. Our enrollments and resulting revenues and earnings are especially sensitive to events that affect domestic and international air travel and the level of hotel reservations. A number of factors, including a rise in fuel prices or other travel costs, excessive inflation, currency fluctuations within the global market, the strength of the dollar, foreign taxation changes, extreme weather conditions and concerns about passenger safety could result in a temporary or longer-term overall decline in demand for our programs. Also, demand for our products and services may be significantly affected by the general level of economic activity and employment levels in the United States and key international markets. Therefore, the economic downturn or a recession in the United States or these other markets could have a material adverse effect on our business, financial condition, cash flows and results of operations. Currently, the United States and other markets are facing these conditions which has impacted the travel industry, the markets in which we operate, our operations and profitability. We expect these conditions will continue to impact our operations and profitability.

Business interruption due to adverse weather conditions or natural disasters, international political climate, armed conflicts, terrorist and threats thereof, and other world events or other incidents affecting the health, safety, security and/or program satisfaction of individuals could have an adverse affect on our profitability.

Demand for our travel programs may be adversely affected by natural occurrences such as hurricanes, earthquakes, epidemics or other disease outbreaks such as influenza, and flooding in geographic regions in which we conduct travel programs. The occurrence of any of the events described above or other unforeseen developments in one or more of these regions would have a material adverse effect on our business, financial condition, cash flows, and results of operations.

Our operations are subject to special risks inherent in doing business internationally, as a substantial portion of our travel programs are conducted outside the United States. Historically, gross program receipts from programs to Europe, the South Pacific (Australia and New Zealand) and China have accounted for a majority of our receipts. Risks inherent in doing business internationally include potential adverse effects on operations from war, U.S. military deployments, international and domestic terrorism, civil disturbances, political instability, foreign currency exchange rates, governmental activities and deprivation of contract rights.

Periods of international and domestic unrest have reduced demand for our travel programs and could have a material adverse effect on our business and results of operations. Examples of such past events include, but are not limited to, war in Iraq in 2003 and various terrorist attacks, such as the attempted airliner terrorist attack on December 25, 2009, the attacks that occurred in India on November 26 through 29, 2008, London on July 7 and 21, 2005, and in the United States on September 11, 2001. A continued U.S. military response and other acts of violence or war have and will affect the travel industry generally, the markets in which we operate, and our operations and profitability. Further terrorist attacks against the United States or U.S. businesses and citizens at home and abroad may occur. The September 11 attacks had a very negative impact on domestic and international air travel and the travel industry in general. The potential long-term effects of these events are uncertain for our customers, the market for our Common Stock, the markets for our services and the U.S. economy. The consequences of any terrorist attacks, or any armed conflicts including war which may result, are unpredictable, and we may not be able to foresee events that could have an adverse effect on our business or operations. Historically, we have experienced increased cancellations for our travel programs during such times.

Our financial results are subject to fluctuations due to the seasonality of our business.

Our business is highly seasonal. The majority of our travel programs are scheduled in June and July of each year, mildly complemented by the majority of content sales which occur during the school year, primarily September to June. We anticipate that this trend will continue for the foreseeable future. We recognize gross program receipts, revenues and program pass-through expenses upon the departure of our program delegates for the majority of our programs. Substantially all of our operating income is generated in the second and third quarters, which historically has offset the operating losses incurred during the rest of the year. Annual results would be adversely affected if our revenues were to be substantially below seasonal norms during the second and third quarters of the year. Furthermore, our operating results may fluctuate as a result of many factors, including the mix among five different travel programs and program destinations offered by us and our competitors, the introduction and acceptance of new programs and program enhancements by us and our competitors, timing of program completions, cancellation rates, competitive conditions in the industry, marketing expenses, extreme weather conditions, international or domestic conflicts, timing of and costs related to acquisitions, changes in relationships with certain travel providers, economic factors and other considerations affecting travel. As a result of the foregoing, annual or quarterly operating results may be below the expectations of public market analysts and investors. In such event, the price of our Common Stock could be materially and adversely affected.

Competition in the travel and education industries could impact our results of operations.

The travel industry in general and the educational segment of the travel industry are highly competitive and have relatively low barriers to entry. We compete with other companies that provide similar educational travel programs for students and athletes, as well as independent programs organized and sponsored by local teachers and coaches with the assistance of local travel agents. People to People, under the terms of its agreement with us, reserves the right to offer programs to college students for studies abroad and to grant to other individuals or entities, the right to use the People to People name in connection with People to People’s professional education and sports programs. In general, our Citizen Ambassador Programs compete with independent professional organizations that sponsor and organize their own travel programs through the assistance of local travel agents, and other organizations that offer travel programs and continuing education credits for adults. Some of our competitors are larger and have greater brand-name recognition and financial resources than we do. In addition to competition we face in the travel industry, we also face significant competition from a wide variety of content and media Web properties with companies throughout the world. Content and advertising on the internet are intensely competitive and have been rapidly evolving with converging technologies. We compete with many larger Web properties that have larger staff and more traffic to offer potential advertisers. There can be no assurance that we will be able to compete successfully, and the failure to compete successfully may have a material adverse effect on our business, financial condition, cash flows and results of operations.

Our inability to use established brands, such as the “People to People” and “Discovery Education” names, could significantly impact our success in attracting future travelers.

Our agreements with People to People give us the exclusive right to develop and conduct programs for kindergarten through high school students using the People to People name, and the non-exclusive right to develop and conduct programs for professionals, college students and athletes using the People to People name. Our agreements with People to People, however, allow People to People to continue to conduct college and professional seminars and internship programs and to develop other sports and professional programs. Our agreements with People to People expire in 2020. Our agreement with Discovery Education gives us the exclusive right to license all-inclusive programs for kindergarten through high school students using the Discovery Education marks and the name “Discovery Student Adventures." We believe that we derive benefit from our ability to market our programs using the People to People and Discovery Education names. If our agreements with People to People and Discovery Education were terminated or if we were unable to use the branded names to market new programs or destinations, this could have a material adverse effect on our business, financial condition, cash flows and results of operations. Similarly, if our relationship with People to People or Discovery Education is disrupted or is adversely impacted because People to People or Discovery Education experiences interruption, delay or ceases operations in the future for any reason, our business could be harmed and our stock price may decline.

Our dependence on travel suppliers could delay the delivery of our products and services, which would impact our reputation and could reduce our profitability.

We are dependent upon travel suppliers for access to their products and services. Travel suppliers include airlines, hotels, bus lines, overseas coordinators and other participants in the travel industry. Consistent with industry practices, we currently have no long-term agreements with travel suppliers that obligate such suppliers to sell services or products through us on an ongoing basis. Therefore, the travel suppliers generally can cancel or modify their agreements with us upon relatively short notice. In addition, any decline in the quality of travel products and services provided by these suppliers, or a perception by our delegates of such a decline, could adversely affect our reputation. The loss of contracts, changes in our pricing agreements, commission schedules or incentive override commission arrangements, more restricted access to travel suppliers’ products and services or less favorable public opinion of certain travel suppliers, resulting in low demand for the products and services of such travel suppliers and loss of deposits with travel suppliers that could go bankrupt could all have a material adverse effect on our business, financial condition, cash flows and results of operations.

We depend on our ability to attract and retain our key personnel.

Our performance is substantially dependent on the continued services and performances of our senior management and certain other key personnel. The loss of the services of any of our executive officers or other key employees could have a material adverse effect on our business, financial condition and results of operations. Our future success also depends on our ability to identify, attract, hire, train, retain and motivate other highly skilled managerial, marketing and customer service personnel. The failure to retain and attract necessary managerial, sales, marketing and customer service personnel could have a material adverse effect on our business, financial condition, cash flows and results of operations.

We depend on the effectiveness of marketing to obtain individuals to travel on our programs and to use our website.

Our performance in our travel programs is substantially dependent on the effectiveness of our direct and indirect marketing efforts, including but not limited to, names sources used to identify potential participants for our programs, direct mail, online presence and local informational meetings. Failure or underperformance of our marketing efforts, including changes in the direct-mail environment and the Company’s reputation with teachers could have a material adverse effect on our business, financial condition, cash flows and results of operations. Such changes in the direct-mail environment could include, but are not limited to, a threat of disease or bioterrorism within the mail environment and new or different regulatory schemes or changes in costs or services by the United States Postal Service. In addition, the performance of our research segment is dependent on advertising rates. Changes affecting advertising fees and reduced traffic could have an impact on operations.

Government regulation and taxation may adversely affect the travel industry and thus increase our operating expenses.

Many travel suppliers, particularly airlines, are subject to extensive regulation by federal, state and foreign governments. In addition, the travel industry is subject to certain seller of travel laws of certain states and special taxes by federal, state, local and foreign governments, including but not limited to hotel bed taxes, car rental taxes, airline excise taxes and airport taxes and fees. New or different regulatory schemes or changes in tax policy could have an adverse impact on the travel industry in general and could have a material adverse effect on our business, financial condition, cash flows and results of operations.

Fluctuations in foreign currency exchange rates could affect our results of operations.

Many of our arrangements with our foreign-based suppliers require payment to be made in foreign currencies. Any decrease in the value of the U.S. dollar in relation to foreign currencies has the effect of increasing the cost of the services to be provided. Since late 1993, we generally have purchased forward contracts and options with less than two years’ maturity to help manage program costs and hedge against foreign currency valuation increases. While the ability to utilize forward contracts for the delivery of foreign currencies can mitigate the effect of increased program costs and foreign currency exchange fluctuations, there can be no assurance that increased program costs relating to such currency fluctuations will not be substantial in future periods. There can also be no assurance our hedging strategy will mitigate longer-term foreign exchange valuation trends. Depending on the strength of the U.S. dollar at the time the forward contracts and options are entered into and its strength throughout the contracted period, we could end up in an over-hedged position, which may result in a gain or loss that must be recognized in our financial statements immediately. Our contract with delegates in our travel programs provides us the option of passing along to delegates any increase in program costs resulting from currency fluctuations. Although we have exercised this option in the past, there can be no assurance that we will be able to increase program prices to offset any such cost increases in the future and any failure to do so could have a material adverse effect on our business, financial condition, cash flows and results of operations.

Litigation may subject us to significant litigation costs, judgments, fines and penalties that may not be covered by or may be in excess of available insurance coverage, and may divert management’s attention and resources from our business.

Due to the nature of our business and being a publicly held company, we may be subject to liability claims arising out of perceived wrong doing related to management’s decisions, securities claims, governmental investigations, business operations, or accidents or disasters causing injury to delegates on our programs, including claims for serious personal injury or death. We believe that we have adequate liability insurance for risks arising in the normal course of our business. Although we have experienced no claims for which we did not have adequate insurance coverage, there can be no assurance that insurance coverage will be sufficient to cover one or more large claims or that the applicable insurer will be solvent at the time of any covered loss. Further, there can be no assurance that we will be able to obtain insurance coverage at acceptable levels and cost in the future. Successful assertion against us of one or a series of large uninsured claims, or of one or a series of claims exceeding any insurance coverage could have a material adverse effect on our business, financial condition, cash flows and results of operations. In addition, liability claims asserted against us may also divert management’s attention and resources from our business to participation in the litigation process and defense of these asserted claims. See Note 10, Commitments and Contingencies, to the consolidated financial statements for a description of the claims that have been made against us.

If we are unable to successfully manage the growth in our business, our prospects may be limited and our future profitability will be decreased.

Our performance is dependent on our ability to grow our business and expand the marketing and volume of our educational travel programs, increase the number of website visitors and unique users, and develop our brands. In addition, our ability to grow is dependent on our ability to find and integrate acquisitions or strategic alliances. Failure to meet growth strategies or any minimum volume requirements pertaining to vendor or strategic alliance agreements could have a material adverse effect on our business, financial condition, cash flows and results of operations.

We are exposed to concentration of credit risk that could affect our results of operations.

Cash, cash equivalents and available-for-sale securities are exposed to concentrations of credit risk. We place our cash and temporary cash investments with high credit quality institutions. At times, such balances may be in excess of the federal depository insurance limit or may be on deposit at institutions which are not covered by this insurance. If such institutions were to become insolvent while holding our cash, cash equivalents or available-for-sale securities in excess of the insurance limit, we could suffer losses or it could be necessary to obtain credit financing to operate our travel programs.

Our short-term investments primarily consist of municipal bonds and our long-term investments consist of auction rate securities ("ARS"). The credit markets are currently experiencing significant uncertainty, however our investments are in high-quality, tax-exempt municipal obligations and our ARS are insignificant compared to our total investment portfolio. See Note 4, Investments and Fair Value Measurements, in our consolidated financial statements in this Form 10-K for further information.

If we are unable to protect our intellectual property, we may lose a competitive advantage or incur substantial litigation costs to protect our rights.

Substantially all of our publications are protected by copyright, held either in our name, in the name of the author of the work, or in the name of the sponsoring professional society. Such copyrights protect our exclusive right to publish the work in the United States and in many countries abroad for specified periods. Our ability to obtain and continue to obtain access to existing and new content, as well as our ability to continue to achieve expected results depends, in part, upon our ability to protect our intellectual property rights. Our results may be adversely affected by lack of legal or technological protections for our intellectual property in some jurisdictions and markets that we operate in.

We depend on our ability to successfully integrate key acquisitions.

One of our growth strategies is to acquire businesses that complement our existing businesses. Target acquisitions may have an impact on costs, revenues, cash flows, and our financial position, such as the acquisition of BookRags, on May 15, 2008. Acquisitions involve risks and uncertainties, including difficulties in integrating acquired operations and in realizing expected opportunities, diversions of management resources and loss of key employees, challenges with respect to operating new businesses, and other unanticipated risks and liabilities.

Our revenues and results of operations may fluctuate unexpectedly from quarter to quarter, which may cause our stock price to decline.

The market price of our Common Stock could be subject to significant fluctuations. Some of the factors that could affect our stock price include:

| • Quarterly variations in operating results; |

| • Changes in revenue or earnings estimates or publication of research reports by analysts; |

| • Speculation in the press or investment community; |

| • Strategic actions by us or our competitors, such as acquisitions or restructurings; |

| • Actions by institutional shareholders; |

| • General market conditions; |

| • Fair value adjustments associated with impairment of investments, goodwill, intangible assets or fixed assets; |

| • Change in key employees; |

| • Domestic or international social and economic factors unrelated to our performance; |

| • Terrorist activities, and |

| • Limited shares of Common Stock available for trading |

The stock markets have experienced extreme volatility that has often been unrelated to the operating performance of particular companies. These broad market fluctuations may adversely affect the trading price of our Common Stock. In particular, we cannot make assurances that our stock will sell at any particular price, or at all.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

We own an office building, approximating 132,000 square feet, in which our headquarters are located in Spokane, Washington. Our facilities are well maintained, in good operating condition and provide adequate capacity for our needs. We have the ability to expand our capacity for growth if we should need to in the future. At December 31, 2009, Ambassadors Group, Inc. and its subsidiaries are the occupants of this property.

We also occupy two additional office spaces. One space totals approximately 2,400 square feet in Arlington, Virginia, pursuant to a lease which expires April 30, 2011 and is occupied by Ambassador Programs. The other totals approximately 2,200 square feet in Seattle, Washington, pursuant to a lease which expires on February 28, 2011 and is occupied by both Ambassador Programs and BookRags. Both facilities are well maintained, in good operating condition and provide adequate capacity for our needs.

On July 14, 2009, a securities class action was filed against us and certain of our executive officers on behalf of all persons or entities who purchased our Common Stock between February 8, 2007 and October 23, 2007. The class action was filed in the United States District Court for the Eastern District of Washington by plaintiff Plumbers Union Local No. 12 Pension Fund (“Plumbers Union”). On October 22, 2009, the Court appointed International Brotherhood of Electrical Workers Local 351 (“IBEW 351)” as lead plaintiff. On November 23, 2009, lead plaintiff IBEW 351 filed a motion to withdraw as lead plaintiff and sought appointment of Plumbers Union as substitute lead plaintiff. On January 7, 2010, a hearing was held and the Court appointed Plumbers Union as lead plaintiff and required any amended complaint shall be served and filed on or before January 11, 2010. Plumbers Union filed its amended complaint on January 11, 2010. The amended complaint alleges that the defendants violated federal securities laws by making untrue statements of material fact and/or omitting to state material facts, thereby artificially inflating the price of our Common Stock. We have reviewed the amended complaint and deny the allegations contained therein. We have tendered our defense and indemnity under applicable insurance coverage and defense counsel in Seattle, Washington has been retained to represent us. We believe that the likelihood that our Company will ultimately incur a loss in connection with this litigation is remote. We cannot estimate the possible loss to our Company, if any, at this time. The actual cost to resolve this case will depend upon many factors such as the outcome of mediation, pre-trial motions, trial and any appeals. However, we believe any loss incurred will not have a material adverse effect on our business, financial condition, cash flows or results of operations. We intend to vigorously defend this lawsuit and any alleged claims for damages.

On October 27, 2009, the Company was informed by the SEC that it had issued a formal order of investigation with respect to trading in the Company's securities. The Company believes that the investigation is for the period August through December, 2007. In connection with the investigation, the Company, certain of its officers, directors and employees, as well as other persons, have received subpoenas from the SEC requesting information. The SEC has indicated that the investigation should not be construed as an indication that any violation of law has occurred or as an adverse reflection upon any person, entity or security. The Company intends to cooperate fully with the investigation.

Other than the disclosed, we are not a party to any other material pending legal proceedings other than ordinary routine litigation incidental to our business, the outcome of which we believe will not have a material adverse effect on our business, financial condition, cash flows or results of operations. These matters are subject to inherent uncertainties and management’s view of these matters may change in the future. Adverse outcomes in some or all of the matters described in this section may result in significant monetary damages or injunctive relief against us that would adversely affect our operations.

Not applicable.

PART II

Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Market Information

Our Common Stock has been traded on the NASDAQ Stock Market under the symbol “EPAX” since March 1, 2002.

As of February 18, 2010, the last reported sale price of our Common Stock was $11.44. The following table sets forth the high and low sale prices of a share of our Common Stock as reported on the NASDAQ Stock Market on a quarterly basis for our fiscal years ended December 31, 2009 and 2008.

| High | Low | ||||||

| Quarter ended March 31, 2009 | $ | 11.47 | $ | 6.20 | |||

| Quarter ended June 30, 2009 | $ | 14.06 | $ | 7.56 | |||

| Quarter ended September 30, 2009 | $ | 17.29 | $ | 12.01 | |||

| Quarter ended December 31, 2009 | $ | 17.09 | $ | 11.28 | |||

| Quarter ended March 31, 2008 | $ | 20.80 | $ | 16.40 | |||

| Quarter ended June 30, 2008 | $ | 20.42 | $ | 14.90 | |||

| Quarter ended September 30, 2008 | $ | 19.99 | $ | 13.31 | |||

| Quarter ended December 31, 2008 | $ | 16.35 | $ | 7.42 | |||

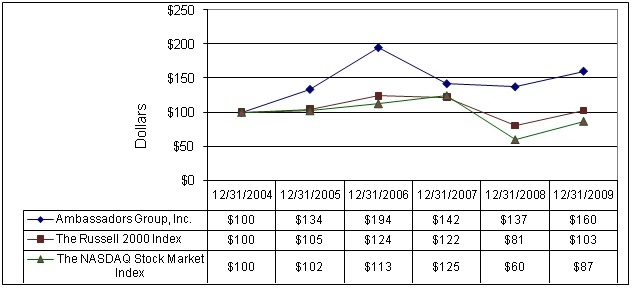

Performance Graph

The following graph compares our cumulative total shareholder return with the NASDAQ Stock Market Index and the Russell 2000 Index. The graph assumes that $100 was invested on December 31, 2004 in our Common Stock and in each of the indexes mentioned above and that all dividends were reinvested.

The performance graph is being furnished by us and shall not be deemed “filed” for purposes of Section 18 of the Exchange Act, or otherwise subject to the liabilities of that section, nor shall it be deemed to be incorporated by reference in any filing under the Act, or the Exchange Act.

Holders of Record

As of February 18, 2010, there were approximately 54 holders of record of our Common Stock, according to our registrar. This number does not include beneficial owners holding shares through nominee or street name.

Dividends

In November 2003, the Board of Directors initiated a dividend policy, payable on a quarterly basis. Each quarter, our Board of Directors reviews the dividend payment, assessing the amount, timing and alignment with its strategic direction.

On August 12, 2005, our Board of Directors declared a two-for-one stock split of our Common Stock in the form of a 100-percent common stock dividend, payable on September 15, 2005, to shareholders of record on August 31, 2005.

During 2008 and 2009, and through February 2010, our Board of Directors declared the following dividend payments:

| Declaration Date | Record Date | Payment Date | DividendPer Share | ||

| February 13, 2008 | February 27, 2008 | March 12, 2008 | $ | 0.115 | |

| May 8, 2008 | May 22, 2008 | June 5, 2008 | $ | 0.115 | |

| August 26, 2008 | September 9, 2008 | September 23, 2008 | $ | 0.115 | |

| November 13, 2008 | November 26, 2008 | December 10, 2008 | $ | 0.115 | |

| February 26, 2009 | March 12, 2009 | March 26, 2009 | $ | 0.06 | |

| May 7, 2009 | May 21, 2009 | June 4, 2009 | $ | 0.06 | |

| August 13, 2009 | August 27, 2009 | September 10, 2009 | $ | 0.06 | |

| November 12, 2009 | November 25, 2009 | December 9, 2009 | $ | 0.06 | |

| February 16, 2010 | March 2, 2010 | March 16, 2010 | $ | 0.06 | |

Transfer Agent and Registrar

BNY Mellon Shareowner Services serves as transfer agent and registrar of our Common Stock.

Equity Compensation Plan Information

The following tables provide information as of December 31, 2009 about our Common Stock that may be issued upon the exercise of options, warrants and rights under all of our existing equity compensation plans.

| (a) | (b) | (c) | |||||||||

| Plan category | Number of securities to be issued upon exercise of outstanding options, warrants and rights | Weighted-average exercise price of outstanding options, warrants and rights | Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) | ||||||||

Equity compensation plans approved by security holders | 2,018,896 | $ | 11.17 | 1,077,675 | |||||||

Equity compensation plans not approved by security holders | N/A | N/A | N/A | ||||||||

| Total | 2,018,896 | $ | 11.17 | 1,077,675 | |||||||

Issuer Purchases of Equity Securities

Between May 2004 and December 2006, our Board of Directors authorized the repurchase of up to $25.0 million of our Common Stock in the open market or through private transactions. On November 8, 2007, our Board of Directors increased the authorized Common Stock repurchase plan amounts to $45.0 million. On November 13, 2008, our Board of Directors, again, increased the authorized Common Stock repurchase plan amounts to $55.0 million. There is no expiration date to repurchase Common Stock. During the quarter ended December 31, 2009, we repurchased 16,337 shares of our Common Stock for $0.2 million. Since inception through December 31, 2009, we have repurchased approximately 1,902,550 shares of our Common Stock, adjusted to reflect the effect of our two-for-one stock split of our Common Stock, for an approximate total of $35.9 million. As of December 31, 2009, approximately $19.1 million remained available for repurchase under the plan. Subsequent to December 31, 2009, no Common Stock has been repurchased. The following is a summary of issuer purchases of equity securities during the quarter ended December 31, 2009:

Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number (or Approximate Dollar Value) of Shares that May Yet Be Purchased Under the Plans or Program | |||||||||||

| Available for repurchase at September 30, 2009 | $ | 19,297,975 | |||||||||||||

| October 1 – October 31, 2009 | — | — | — | 19,297,975 | |||||||||||

| November 1 – November 30, 2009 | 16,337 | $ | 12.25 | 16,337 | 19,097,847 | ||||||||||

| December 1 – December 31, 2009 | — | — | — | 19,097,847 | |||||||||||

| 16,337 | $ | 12.25 | 16,337 | $ | 19,097,847 | ||||||||||

Independent of this share repurchase plan, during the first quarter of 2007, our Board of Directors approved a single repurchase of 1.2 million shares of common stock for approximately $33.0 million.

Recent Sales of Unregistered Securities

During the fiscal year ended December 31, 2009, we sold no equity securities that were not registered under the Act.

Item 6. Selected Financial Data

This section presents our historical financial data, which should be read carefully with the financial statements included in this Form 10-K, including the notes to the consolidated financial statements and Management’s Discussion and Analysis of Financial Condition and Results of Operations. The statement of operations data for each of the years in the three-year period ended December 31, 2009, and the consolidated balance sheet data as of December 31, 2009 and 2008 have been derived from audited consolidated financial statements included elsewhere in this Form 10-K. The consolidated statement of operations data for the years ended December 31, 2006 and 2005 and the consolidated balance sheet data as of December 31, 2007, 2006 and 2005 have been derived from the audited consolidated financial statements, which are not included in this Form 10-K. Historical results are not necessarily indicative of future results.

| December 31, | ||||||||||||||||||||

| 2009 (C)(D) (E) | 2008 (C) (D) | 2007 | (C) | 2006 | (C) | 2005 | ||||||||||||||

| (in thousands, except per share data) | ||||||||||||||||||||

| Statement of Operations data: | ||||||||||||||||||||

| Net revenue, non-directly delivered programs (A) | $ | 69,279 | $ | 65,656 | $ | 84,512 | $ | 69,554 | $ | 64,321 | ||||||||||

| Gross revenue, directly delivered programs (A) | $ | 26,036 | $ | 30,374 | $ | 30,021 | $ | 19,401 | $ | 4,969 | ||||||||||

| Internet content and advertising revenue | $ | 3,300 | $ | 1,897 | $ | — | $ | — | $ | — | ||||||||||

| Total revenue | $ | 98,615 | $ | 97,927 | $ | 114,533 | $ | 88,955 | $ | 69,290 | ||||||||||

| Cost of sales, directly delivered programs | $ | 14,422 | $ | 18,856 | $ | 18,488 | $ | 11,473 | $ | 2,841 | ||||||||||

| Cost of sales, internet content and advertising | $ | 389 | $ | 192 | $ | — | $ | — | $ | — | ||||||||||

| Gross margin | $ | 83,804 | $ | 78,879 | $ | 96,045 | $ | 77,482 | $ | 66,449 | ||||||||||

| Selling and marketing expenses | $ | 39,021 | $ | 40,842 | $ | 38,943 | $ | 31,638 | $ | 27,574 | ||||||||||

| General and administrative expenses | $ | 14,604 | $ | 12,568 | $ | 15,274 | $ | 11,721 | $ | 8,185 | ||||||||||

| Operating income | $ | 30,179 | $ | 25,469 | $ | 41,828 | $ | 34,123 | $ | 30,690 | ||||||||||

| Operating margin | 36 | % | 32 | % | 44 | % | 44 | % | 46 | % | ||||||||||

| Net income | $ | 20,337 | $ | 18,546 | $ | 31,047 | $ | 26,692 | $ | 22,410 | ||||||||||

| Earnings per share – basic (B) | $ | 1.06 | $ | 0.97 | $ | 1.58 | $ | 1.29 | $ | 1.10 | ||||||||||

| Earnings per share – diluted (B) | $ | 1.05 | $ | 0.95 | $ | 1.53 | $ | 1.24 | $ | 1.05 | ||||||||||

| Balance sheet data: | ||||||||||||||||||||

| Cash, cash equivalents and short-term available-for-sale securities | $ | 81,184 | $ | 74,425 | $ | 84,994 | $ | 133,134 | $ | 116,604 | ||||||||||

| Total assets | $ | 128,095 | $ | 124,277 | $ | 121,704 | $ | 153,953 | $ | 125,046 | ||||||||||

| Total stockholders’ equity | $ | 91,006 | $ | 67,233 | $ | 72,400 | $ | 84,047 | $ | 66,502 | ||||||||||

| Other key financial measures: | ||||||||||||||||||||

| Cash flow from operating activities (C) | $ | 16,138 | $ | 24,732 | $ | 16,436 | $ | 37,207 | $ | 37,792 | ||||||||||

| Cash flow provided by (used in) investing activities | $ | (11,200 | ) | $ | (16,181 | ) | $ | 9,677 | $ | (12,923 | ) | $ | (15,592 | ) | ||||||

| Cash flow used in financing activities (C) | $ | (4,271 | ) | $ | (18,843 | ) | $ | (45,616 | ) | $ | (14,416 | ) | $ | (6,320 | ) | |||||

| Cash dividends declared and paid | $ | (4,581 | ) | $ | (8,801 | ) | $ | (8,940 | ) | $ | (7,655 | ) | $ | (5,729 | ) | |||||

Cash dividends declared and paid, per common share | $ | 0.24 | $ | 0.46 | $ | 0.46 | $ | 0.37 | $ | 0.28 | ||||||||||

| Return on stockholders' equity (F) | 26 | % | 27 | % | 40 | % | 35 | % | 39 | % | ||||||||||

| (A) | Net revenues are a function of gross program receipts from non-directly delivered programs, less program pass-through expenses from non-directly delivered programs. Program pass-through expenses include all direct costs associated with our programs, including, but not limited to, costs related to airfare, hotels, meals, ground transportation, guides, professional exchanges and changes in currency exchange rates. Gross revenues, directly delivered programs are a function of the gross program receipts for those programs we directly organize and operate, including all activities such as speakers, facilitators, events, accommodations and transportation. Gross receipts for both directly delivered programs, non-directly delivered programs and internet content and advertising revenue during the years ended December 31, 2009, 2008, 2007, 2006 and 2005 were $203.7 million, $229.2 million, $277.3 million, $219.5 million, and $180.0 million, respectively. Gross margin as a percent of gross program receipts during the years ended December 31, 2009, 2008, 2007, 2006, and 2005 was 41%, 34%, 35%, 35%, and 37%, respectively. |

| (B) | During September 2005, we implemented a two-for-one stock split in the form of a 100-percent stock dividend. The earnings per share ("EPS") calculations for all periods presented reflect the increase in the number of shares of Common Stock outstanding as a result of the stock split. On January 1, 2009, we adopted a new accounting principle, which requires the inclusion of participating securities in the two class method of computing earnings per share. Participating securities are unvested share-based payment awards that contain nonforfeitable rights to receive dividends or divided equivalents (whether paid or unpaid). Participating securities under this statement include our unvested employee restricted stock awards with time-based vesting and common stock granted in the acquisition of BookRags that will be issued in 2010. As a result of this adoption, all prior period EPS data have been adjusted retrospectively. The effect of this adoption was a decrease in basic EPS of $0.02, $0.02, $0.01 and $0.00 for 2008, 2007, 2006 and 2005, respectively, and a decrease in diluted EPS of $0.02, $0.02, $0.02 and $0.00 for 2008, 2007, 2006, and 2005, respectively. |

| (C) | We adopted accounting principles relating to stock based compensation as of January 1, 2006. During 2009, 2008, 2007, and 2006 stock option expense was $0.9 million, $0.9 million, $1.0 million, and $1.3 million. In addition to stock option expenses we recorded expense related to restricted stock grants in all years presented. Short-fall (excess) tax benefit from stock-based compensation is included in net cash provided by operating activities and net cash used in financing activities of $(0.1) million, $0.1 million, $(2.7) million, and $(2.4) million for 2009, 2008, 2007, and 2006 respectively. |

| (D) | We acquired BookRags on May 15, 2008, therefore our 2008 and 2009 consolidated financial data includes BookRags’ results of operations since this date. |

| (E) | We entered into a license agreement with Discovery Education during the first quarter of 2009. Pilot programs were operated in the summer of 2009, therefore no revenue was generated, and costs associated with those programs and start-up costs are included in the 2009 consolidated financial data. |

| (F) | Calculated as net income divided by average stockholders' equity. |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) is designed to provide a reader of our consolidated financial statements with a narrative from the perspective of our management on our financial condition, results of operations, liquidity and certain other factors that may affect our future results. Our MD&A is presented in ten sections:

| - | Executive Overview |

| - | Results of Operations |

| - | Results of Operations by Segment |

| - | Key Performance Non-GAAP Financial Indicators |

| - | Liquidity and Capital Resources |

| - | Contractual Obligations |

| - | Off-Balance-Sheet Arrangements |

| - | Market Risk |

| - | Critical Accounting Estimates |

| - | Recent Accounting Pronouncements |