Wonder Auto Technology, Inc1.

Investor Presentation

Roth Capital Partners, New York, September 7, 2006

1: Formerly MGCC Investment Strategies Inc.

1

Safe Harbor Statement

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This presentation includes or incorporates by reference statements that constitute forward-

looking statements within the meaning of Section 27A of the Securities Act of 1933, as

amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These

statements relate to future events or to our future financial performance, and involve known

and unknown risks, uncertainties and other factors that may cause our actual results, levels

of activity, performance, or achievements to be materially different from any future results,

levels of activity, performance or achievements expressed or implied by these forward-looking

statements. These statements include, but are not limited to, information or assumptions

about revenues, gross profit, expenses, income, capital and other expenditures, financing

plans, capital structure, cash flow, liquidity, management’s plans, goals and objectives for

future operations and growth. In some cases, you can identify forward-looking statements by

the use of words such as “may,” “could,” “expect,” “intend,” “plan,” “seek,” “anticipate,”

“believe,” “estimate,” “predict,” “potential,” “continue,” or the negative of these terms or other

comparable terminology. You should not place undue reliance on forward-looking statements

since they involve known and unknown risks, uncertainties and other factors which are, in

some cases, beyond our control and which could materially affect actual results, levels of

activity, performance or

achievements.

We do not intend or assume any obligation to update any of these forward-looking statements

2

Investment Considerations

China’s #2 manufacturer of automotive alternators and starters1

China has become the world’s second largest auto market2 and is

amongst the fastest growing in the world

Additional growth drivers are causing China’s auto parts market to

grow even faster

Diversified, and expanding base of OEM customers

Multiple growth opportunities, both short and long term

The company’s competitive advantage accruing from exceptional

technology, a low cost manufacturing structure and superior quality

Strong financial condition

1: 2005 Economic Analysis of the Automotive Electrical Component Commission, China Automotive

Society

2: China Association of Auto Manufacturers

3

Equity Snapshot

Listed on the OTC Bulletin Board, Ticker: WATG.OB

Price (8/24/2006): $3.00

Market Cap (on 23.96M shares): $71.9 M

Revenues (ttm 6/30/06): $56.1 M

Net Income (ttm 6/30/06): $6.3 M

Shares Outstanding: 23.96 M

Earnings Per Share (ttm 6/30/06): $0.261

1: based on 23.96 million shares

4

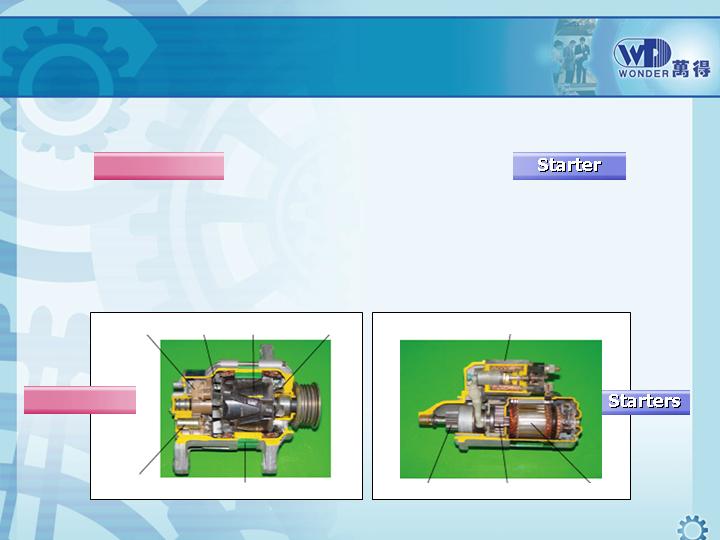

PRODUCTS

Alternator

Critical part of a car

engine’s electrical

system

Starter and engine

solenoid comprise

engine’s starter

system

Alternators

Front Fan

Rotor

Rear Fan

Regulator

Rectifier

Stator

Pinion Gear

Planetary Gear

Armature

Magnetic Switch

China’s #2 Manufacturer of Automotive

Alternators and Starters

5

Facilities

42,196 sq. m manufacturing

facility, Jinzhou City, Northeast

China

2 R&D facilities: Jinzhou and

Beijing

Total employment ~300 people;

including 32 R&D; 30 QC; 158

workers

China’s #2 Manufacturer of Automotive

Alternators and Starters

Highly automated; rapid product

changeover!

ISO9002, QS9000 Qualified

13 Customer Awards for

Excellence Since 1998

6

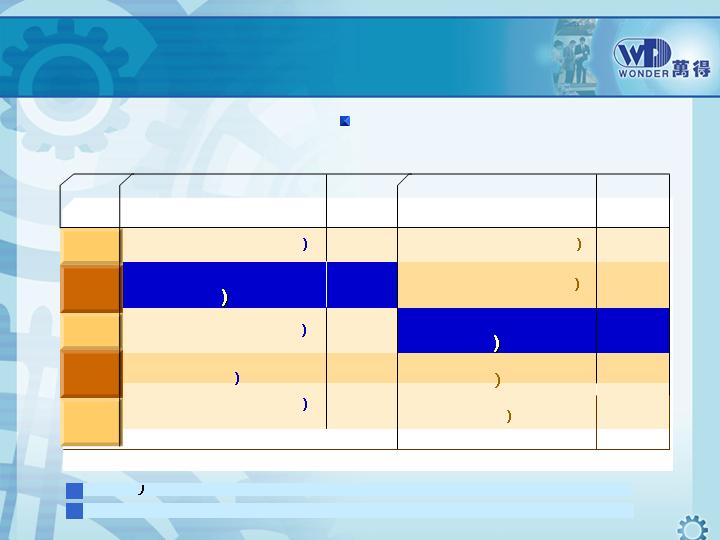

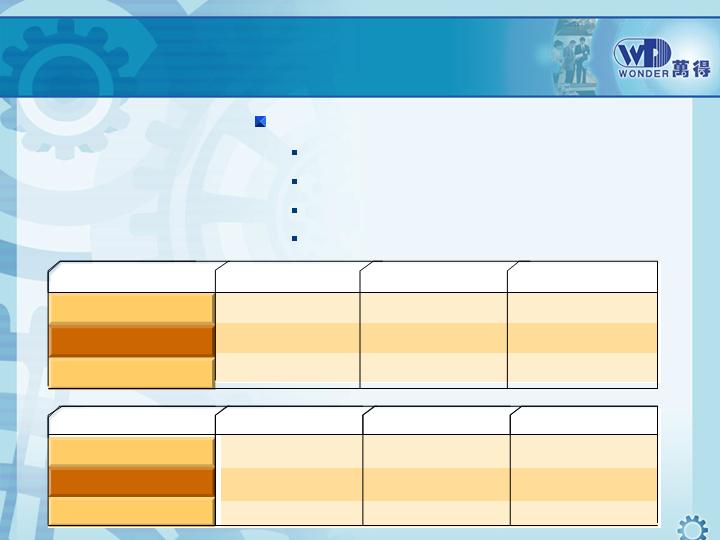

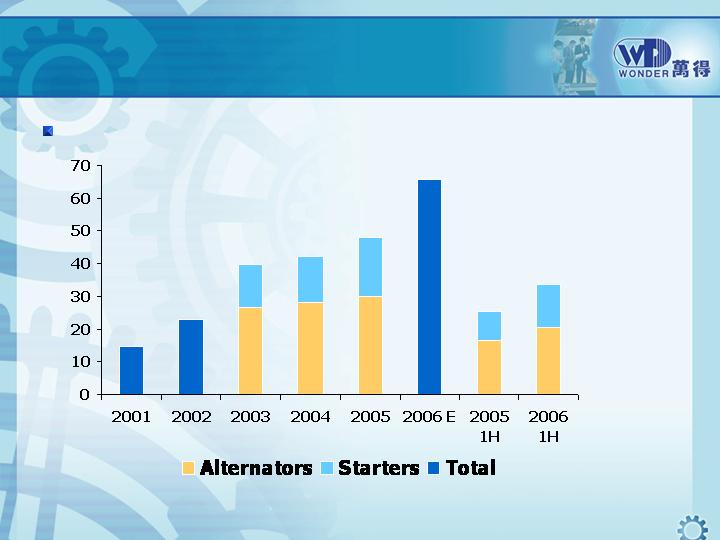

China’s #2 Manufacturer of Automotive

Alternators and Starters

Founded in 1996, as a joint venture with Korean auto parts

manufacturer, rapid growth to #2 position:

Source: Automotive Electrical Component Commission of the China Auto Society, FSSL

Output

(10k)

Starter

manufacturers

20.5

45.0

64.5

71.2

81.5

ZhongQi ChangDian

(3

Xiangfan Dongfeng

(4)

Wonder —JZ Halla

(5)

Shanghai Valeo (2

Hubei Shendian (1

36.5

Huzhou Dehong(5

5

37.9

Chengdu Huachuan

(6

4

52.8

Hubei Shendian(3

3

81.8

Wonder —JZ Halla

(2)

2

111.0

Shanghai Valeo (1

1

Output

(10k)

Alternator

manufacturers

Rank in

1st half

2005

The (* behind names is its rank in 2004; products for agri-vehicles are not included.

7

China is the World’s Second Largest

Auto Market, Fast Growing

Chinese auto market has grown on average 10 to 15% a year since 1990

and the rate is expected to continue1

Growth Drivers:

GDP per capita at the critical point for auto ownership

Low auto ownership per capita compared to ROW

China 19 per 1000; Russia 198 per 1000; South Korea 313 per 1000China is the

World’s Second Largest Auto Market 2, Fast Growing

Increase in urbanization: 43% in 2003 vs. 26% in 19902

78% increase in Class I-IV highways since 19983

Favorable government policies

Small engine segment is the fastest growing. This is an area where

Wonder excels:

Economy in fuel costs and low emissions

Tax Policies: Small engine vehicles 3%; Larger engine vehicles up to

20%

1: Deutsche bank research study, January 6, 2006

2: National Bureau of Statistics, China

3: PRC Ministry of Communication

8

Additional Growth Drivers

Propelling Parts Market

Government imposes up to 25% manufacturer tariff on completed

vehicles with less than 60% local content

Downward pressure on PRC auto prices prompts automobile

manufacturers to adopt cost-saving measures

Growing vehicle population creates aftermarket sales opportunity

US/Japanese/Korean manufacturers have begun parts sourcing

initiatives in China. China is now the 4 th largest exporter of auto arts1

1: Source: CCID Consulting

9

Additional Growth Drivers

Propelling Parts Market

RMB Million

4,362

7,014

8,297

11,593

14,445

15,017

16,878

18,740

20,601

22,463

21,455

31,267

36,819

45,098

52,893

55,423

61,235

67,048

72,860

78,672

Maintenance Products & Services

Electrical Parts

Source: Access Asia Limited

15.53%

98-07

CAGR

19.97%

10

Exceptional Technology Offers

Competitive Advantage

“Co-development” programs with new and existing OEM customers .

R&D Centers in Jinzhou and Beijing

Licensing Agreement with Japanese manufacturer for patented

technology

Co-operation Agreement with Hivron (Korea) for Microchip Research

& Development

11

Exceptional Technology Offers

Competitive Advantage

f70

12V 1.4KW

50

2004

f70

f70

Size

12V 1.5KW

12V 1.2KW

Output Rate

60

33

Number of Models

2005

2003

Starter

f118

14V 120KW

110

2004

f118

f128

Size

14V 135KW

14V 100KW

Output Rate

120

90

Number of Models

2005

2003

Alternator

“Local” R&D drives competitive advantage:

Improved product quality

Lower development cycle times

Broader product range

Design/Function for manufacture at lower cost

12

Diversified Customer Base

77%

$37.2

Total

2.9%

Vehicle Manufacturer

$1.4

Beijing Foton

2.9%

Engine Manufacturer

$1.4

Harbin Dong’an Mitsubishi

4.8%

Engine Manufacturer

$2.3

Shenyang Xinguang

6.0%

Engine Manufacturer

$2.9

Greatwall Baoding

7.0%

Engine Manufacturer

$3.4

Mianyang Xinchen

7.4%

Vehicle Manufacturer

$3.6

Tianjin Automotive Xia Li

9.4%

Vehicle Manufacturer

$4.5

Harbin Dong’an

11.1%

Vehicle Manufacturer

$5.3

Dongfeng Yueda Kia Motor

Co., Ltd

11.3%

Engine Manufacturer

$5.5

Shenyang Aerospace

Mitsubishi

14.4%

Vehicle Manufacturer

$6.9

Beijing Hyundai

% Total Sales

Customer Type

2005 Sales ($M)

Customer

No Customer Accounted for More Than 15% of sales in 2005

13

Multiple Growth Opportunities

Expansion of markets

Create New Products for

Existing Customers

New and Existing Products to

New Customers

Penetrate the Aftermarket

18 New joint development

programs

32 million vehicles in use

Strong business and product

development activity with multiple

OEMs and other manufacturers

Beijing Benz Daimler Chrysler

Shanghai VW

Shanghai GM

South Korea Hyundai

Increase Exports

International sale agreements in

South Korea, USA and Turkey

Detroit sales office planned end ’06

14

Multiple Growth Opportunities

Expansion of capabilities

Enhance R&D capabilities by

employing foreign experts and

purchasing advanced equipment

Build production lines dedicated

to the production of alternators

and/or starters for sedans

Make strategic investments

by way of vertical or

horizontal integration

Strengthen

overall competitiveness

Further expansion improve

quality and cost control

Further increase productivity

and production efficiency

15

Strong Financial Condition

Revenues ($ Millions)

Robust Revenue Growth

*

* Guidance

65.9

48.1

42.3

39.8

22.8

14.7

33.6

25.6

16

Strong Financial Condition

Net Income

Rising Full Year Net Income

*

* Guidance

17

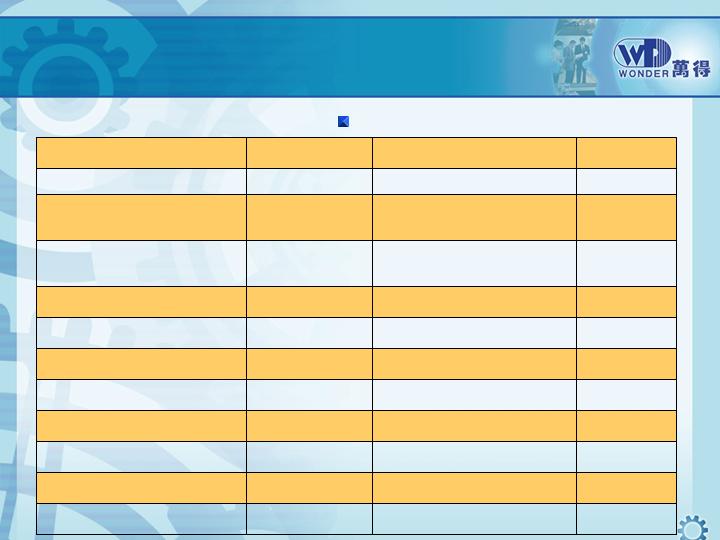

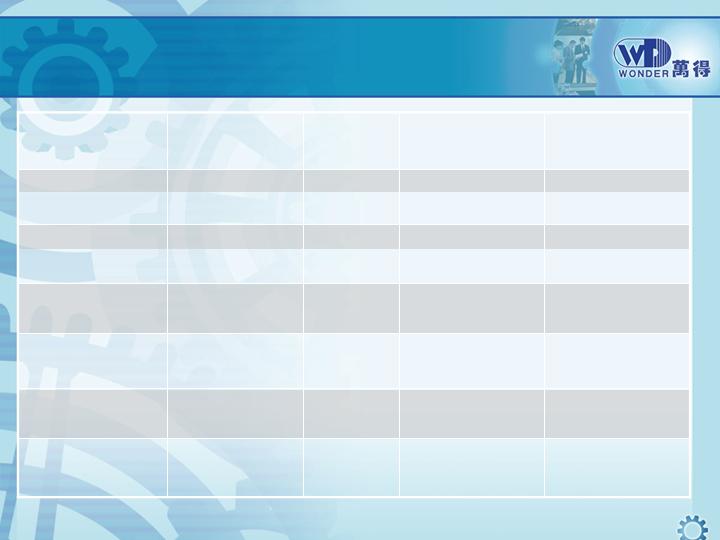

Income Statement

8,231,000

28.6%

3,489,306

6,400,926

14.6%

5,587,455

Net Income

% Growth

778,149

1,570,960

1,199,829

Taxes and

Int/Other Exp

4,267,455

12.7%

7,971,886

16.6%

6,787,284

16.1%

Operating Inc.

% of Revenue

1,844,855

3,303,804

2,404,824

Operating

Expenses

6,112,310

18.2%

11,275,690

23.5%

9,192,108

21.7%

Gross Profit

% of Revenue

65,937,640

37.2%

33,606,328

48,062,805

13.7%

42,265,874

Revenues

% Increase

2006

projected

1st half 2006

2005

2004

USD$

18

Strong Financial Condition

Balance Sheet $ millions

5.00

4.95

Secured Long-term Debt

7.49

7.43

Secured Short-Term Debt

15.53

7.97

Cash and Restricted Cash

69.03

52.09

Total Liabilities and Equity

32.66

18.85

Shareholders’ Equity

5.00

4.95

Non-Current Liabilities

31.38

28.28

Current Liabilities

69.03

52.09

Total Assets

13.88

13.62

Non-Current Assets

55.15

38.47

Current Assets

June 30,

2006

Unaudited

December 31,

2005

Audited

19

Experienced Management Team

Mr. Qingjie Zhao, Chairman and CEO

Chairman of Chinese operating subsidiary since 1997.

Strategic planning, business development, policy development

Previous to private industry, professor and lecturer in advanced automotive

engineering with Liaoning University

Mr. Yuncong Ma, COO

General Manger responsible for all operations

30 years production management experience; 16 in automotive

Mr. Meirong “Ryan” Yuan, CFO

Previously VP Finance for Shenzhen Asphalt Advanced Technology, Ltd.

PhD study at the University of Southern California program in China

Mr. Yuguo Zhao, VP Sales

Jim Groh and Gerry Pascale, US executives

20

Valuation

3.8

2.1

10.6

2.3

4.8%

42.6

164.6

7.07

CAAS

China

Automotive

Systems

1.4

1.3

N/A

1.6

14%

9.7

42.2

0.11

08293.HK

Jinheng

Automotive

1.9

0.9

7.6

1.0

5%

16.7

99.9

12.00

MPAA.PK

Motorcar

Parts of

America

4.3

1.2

10.0

1.3

8%

14.8

89.2

6.68

SORL

SORL Auto

Parts Inc.

2.2

1.3

7.8

1.2

11%

11.3

71.9

3.00

WATG.OB

Wonder

Auto

Company

Price/

Book

(ttm)

Price/

Sales

(ttm)

EV/

EBITDA

(ttm)

EV/

Rev

(ttm)

Profit

Margin

(ttm)

P/E

ttm

Market

Cap ($)

Stock

Price

($)

Ticker

Symbol

Source: Yahoo Finance and Company Reports

21

Investment Considerations

China’s #2 manufacturer of automotive alternators and starters1

China has become the world’s second largest auto market2 and is

amongst the fastest growing in the world

Additional growth drivers are causing China’s auto parts market to

grow even faster

Diversified, and expanding base of OEM customers

Multiple growth opportunities, both short and long term

The company’s crafts competitive advantage accruing from

exceptional technology, a low cost manufacturing structure and

superior quality

Strong financial condition

1: 2005 Economic Analysis of the Automotive Electrical Component Commission, China Automotive

Society

2: China Association of Auto Manufacturers

22