Filed Pursuant to Rule 424(b)(3)

Registration No. 333-154790

43,686,734 SHARES

OF

KAL ENERGY, INC.

COMMON STOCK

This is a resale prospectus for the resale of up to 43,686,734 shares of our common stock by the selling stockholders listed in this prospectus. These shares may be sold by the selling stockholders from time to time in the over-the-counter market or other national securities exchange or automated interdealer quotation system on which our common stock is then listed or quoted, through negotiated transactions at negotiated prices or otherwise at market prices prevailing at the time of sale.

Approximately 28 of our stockholders are offering shares of our common stock to the public by means of this prospectus. As of October 21, 2008, we had 134,416,172 shares of our common stock outstanding. The shares of common stock covered by this prospectus constitute 32.5% of our outstanding common stock.

Pursuant to registration rights granted by us to the selling stockholders, we are obligated to register the shares held by these selling stockholders. The distribution of the shares by the selling stockholders is not subject to any underwriting agreement. We will receive none of the proceeds from the sale of the shares by the selling stockholders. We will bear all expenses of registration incurred in connection with this offering, but all selling and other expenses incurred by the selling stockholders will be borne by them.

Our common stock is quoted on the National Association of Securities Dealers, Inc.’s Over-The-Counter Bulletin Board, or the OTC Bulletin Board, under the symbol “KALG.OB.” The high and low sale prices for shares of our common stock on October 27, 2008, were $0.06 and $0.055 per share, respectively, based upon bids that represent prices quoted by broker-dealers on the OTC Bulletin Board. These quotations reflect inter-dealer prices, without retail mark-up, mark-down or commissions, and may not represent actual transactions.

The selling stockholders and any broker-dealer executing sell orders on behalf of the selling stockholders may be deemed to be ''underwriters'' within the meaning of the Securities Act of 1933, as amended, or the Securities Act, and any commissions or discounts given to any such broker-dealer may be deemed to be underwriting commissions or discounts under the Securities Act. The selling stockholders have informed us that they do not have any agreement or understanding, directly or indirectly, with any person to distribute their common stock.

Brokers or dealers effecting transactions in the shares should confirm registration of these securities under the securities laws of the states in which transactions occur or the existence of our exemption from registration.

Investing in our common stock involves a high degree of risk. We urge you to carefully consider the section entitled ''Risk Factors'' beginning on page 5 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities, or passed on the adequacy or accuracy of the disclosures in the prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is November 17, 2008

TABLE OF CONTENTS

| Prospectus Summary | 3 | |

| Risk Factors | 5 | |

| Use of Proceeds | 10 | |

| Market for Common Equity and Related Stockholder Matters | 10 | |

| Management’s Discussion and Analysis of Financial Condition and Results of Operations | 19 | |

| Business | 11 | |

| Directors, Executive Officers, Promoters and Control Persons | 25 | |

| Executive Compensation | 27 | |

| Security Ownership of Certain Beneficial Owners and Management | 31 | |

| Certain Relationships and Related Transactions | 30 | |

| Description of Securities | 32 | |

| Selling Stockholders | 33 | |

| Plan of Distribution | 34 | |

| Changes In and Disagreements With Accountants on Accounting and Financial Disclosure | 35 | |

| Legal Matters | 35 | |

| Experts | 35 | |

| Where You Can Find Additional Information | 35 | |

| Index to Financial Statements | F-1 |

You should rely only on the information contained in this prospectus. We have not, and the selling stockholders have not, authorized anyone, including any salesperson or broker, to give oral or written information about this offering, our company, or the shares of common stock offered hereby that is different from the information included in this prospectus. If anyone provides you with different information, you should not rely on it.

CAUTION REGARDING FORWARD−LOOKING STATEMENTS

This prospectus contains “forward-looking statements” and information relating to our business that are based on our beliefs as well as assumptions made by us or based upon information currently available to us. When used in this prospectus, the words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “may,” “plan,” “project,” “should” and similar expressions are intended to identify forward-looking statements. These forward-looking statements include, but are not limited to, statements relating to our performance in “Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” These statements reflect our current views and assumptions with respect to future events and are subject to risks and uncertainties. Actual and future results and trends could differ materially from those set forth in such statements due to various factors. Such factors include, among others: general economic and business conditions; industry capacity; industry trends; competition; changes in business strategy or development plans; project performance; the commercial viability of our products; availability, terms, and deployment of capital; and availability of qualified personnel. These forward-looking statements speak only as of the date of this prospectus. Subject at all times to relevant federal and state securities law disclosure requirements, we expressly disclaim any obligation or undertaking to disseminate any update or revisions to any forward-looking statement contained herein to reflect any change in our expectations with regard thereto or any changes in events, conditions or circumstances on which any such statement is based. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

2

PROSPECTUS SUMMARY

This summary highlights selected information contained elsewhere in this prospectus. This summary does not contain all of the information that you should consider before investing in our common stock. You should carefully read the entire prospectus, including the section entitled “Risk Factors” and the financial statements and accompanying notes, before making an investment decision.

Business

We were formed on February 21, 2001 under the laws of the State of Delaware.

On May 10, 2001, we entered into a letter of intent with Tri-Corp. Enterprises Ltd., or Tri-Corp, a privately-held corporation located in British Columbia, Canada, to jointly develop Gateway Falls R.V. Estates, a recreational vehicle community located on Shuswap Lake near Lee Creek, British Columbia, Canada. Under the terms of the agreement with Tri-Corp, we agreed to forward CDN$1,500,000.00 to the joint venture for the purpose of providing clear title to the development property and for use in the development of property infrastructure. We abandoned this business plan in 2001 due to the British Columbia Financial Institutions Commission's issuance of an order preventing the sale of the recreational vehicle sites.

On March 6, 2002, we entered into an option agreement to acquire an interest in the Manchester South Property, a mineral claim located in the Sudbury Mining Division of Ontario, Canada. The agreement, as amended on October 8, 2003, was between us and Terry Loney, doing business as Klondike Bay Resources. Our objective was to conduct mineral exploration activities on the Manchester South Property in order to assess whether the claim possessed commercially exploitable reserves of copper and/or nickel.

Under the terms of the option agreement, we would have been deemed to have exercised the option to acquire a 90% interest in the Manchester South Property when we had:

| · | paid Klondike Bay Resources $7,500 (paid upon the execution of the option agreement); and |

| · | incurred an aggregate of $200,000 of property exploration expenditures on the Manchester South Property within the following periods: |

| · | $25,000 on or before December 31, 2004; and |

| · | a further $175,000 on or before December 31, 2005. |

Due to our inability to raise sufficient funds to meet the exploration expenditure requirements of the option agreement with Klondike Bay Resources, we were unable to exercise the option and our right to acquire an interest in the Manchester South Property was terminated.

On December 29, 2006, we entered into a reorganization agreement with Thatcher Mining Pte Ltd., or Thatcher, a privately-held corporation formed on June 6, 2006 under the laws of Singapore. Thatcher was formed to conduct mining, quarrying and prospecting services and to engage in wholesale and retail sales of certain commodities.

Under the terms of the reorganization agreement, we agreed to acquire all of the issued and outstanding shares of Thatcher in exchange for 32,000,000 shares of our common stock. Upon closing the transactions contemplated by the reorganization agreement, we also agreed to make a cash payment of $10,000 to the former shareholders of Thatcher and to execute a royalty agreement pursuant to which we agreed to pay the former shareholders of Thatcher a royalty of $0.40 per metric ton of coal sold by us. We completed the transactions contemplated by the reorganization agreement on February 9, 2007 and, thereafter, Thatcher became our wholly-owned subsidiary.

We formed PT Kubar Resources, or Kubar, a limited liability foreign investment (PMA) company under the laws of the Republic of Indonesia on April 12, 2007, and completed its registration on June 6, 2007. Kubar will be our operating company for Indonesia.

On September 12, 2007, we acquired Finchley Resources Pte. Ltd., or Finchley, by assuming its liabilities and expenses, via a transfer of stock from its sole owner. Finchley is a corporation that was formed under the laws of the Republic of Singapore on August 13, 2007. The only expenditures incurred by Finchley were those in association with its formation. We assumed a total of $209 in liabilities from this transaction.

We now carry on the business of Thatcher as our sole line of business and all of our operations are conducted by and through Thatcher or its subsidiaries. All references to the “Company,” “we,” “our” and “us” for periods prior to the closing of the reorganization transaction refer to KAL Energy, and references to the “Company,” “we,” “our” and “us” for periods subsequent to the closing of the reorganization transaction refer to KAL Energy and its subsidiaries.

3

The Offering

| Common stock which may be sold by | 43,686,734 shares | |

| the selling stockholders | ||

| Number of selling stockholders | 28 | |

| Use of proceeds | We will not receive any proceeds from the sale of our common stock by the selling stockholders. Any proceeds from the sale of our common stock offered pursuant to this prospectus will be received by the selling stockholders. | |

| OTC Bulletin Board symbol | KALG.OB | |

| Risk factors | See “Risk Factors” and the other information included in this prospectus for a discussion of factors you should carefully consider before deciding to invest in shares of our common stock. |

4

RISK FACTORS

Investing in our common stock involves a high degree of risk. Prospective investors should carefully consider the risks described below, together with all of the other information included or referred to in this prospectus, before purchasing shares of our common stock. There are numerous and varied risks, known and unknown, that may prevent us from achieving our goals. The risks described below are not the only risks we will face. If any of these risks actually occurs, our business, financial condition and/or results of operations may be materially adversely affected. In such case, the trading price of our common stock could decline and investors in our common stock could lose all or part of their investment. The risks and uncertainties described below are not exclusive and are intended to reflect the material risks that are specific to us, material risks related to our industry and material risks related to companies that undertake a public offering or seek to maintain a class of securities that is registered or traded on any exchange or over-the-counter market.

Risks Related to Us

We are in the exploration stage and have yet to establish our mining operations, which makes it difficult to evaluate our business. There can be no assurance that we will ever generate revenues from operations or ever operate profitably.

We are currently in the exploration stage and have yet to establish our mining operations. Our limited history makes it difficult for potential investors to evaluate our business. We need to complete a drilling program and obtain feasibility studies on the properties in which we have an interest in order to establish the existence of commercially viable coal deposits and proven and probable reserves on such properties. Therefore, our proposed operations are subject to all of the risks inherent in the unforeseen costs and expenses, challenges, complications and delays frequently encountered in connection with the formation of any new business, as well as those risks that are specific to the coal industry in general. Despite our best efforts, we may never overcome these obstacles to financial success. There can be no assurance that our efforts will be successful or result in revenue or profit, or that investors will not lose their entire investment.

As of May 31, 2008, we had approximately $1,944,567 in cash and cash equivalents in our accounts. We estimate that we will need approximately US$5,000,000 in working capital to fund capital and operational costs required to get us through the exploration phase and will need additional working capital following the exploration phase to complete all feasibility and pre production costs to get us to early production. We had subscription agreements for $9,103,010 which were expected to close on a rolling basis through June 15, 2008. We refer to this financing as the June 2008 Financing. We collected $5,803,010 through June 15, 2008. One investor in the June 2008 Financing initially subscribed to purchase 26,666,667 shares of common stock at $0.15 per share for an aggregate purchase price of approximately $4,000,000. Such investor had previously advanced $700,000 to us as part of the outstanding balance for its subscribed shares. We informed such investor that the deadline for payment of the remaining balance of $3,300,000 would be June 13, 2008. On June 13, 2008, such investor informed us that it would be unable to tender payment of the remaining balance on that date. On June 17, 2008, we and the investor amended such investor’s subscription agreement to reduce the number of subscribed shares from 26,666,667 to 4,666,667 for an aggregate purchase price of approximately $700,000. We accepted such investor’s amended subscription for the reduced number of shares and agreed to reduce the total size of the June 2008 Financing from 60,686,732 offered shares to 38,686,732 offered shares for total gross proceeds to us of approximately $5,803,010. We closed the March 2008 Financing on June 17, 2008. We do not have any arrangements for additional financing and we may not be able to obtain financing when required. Obtaining additional financing would be subject to a number of factors, including the market prices for our products, production costs, the availability of credit, prevailing interest rates and the market price for our common stock.

Future sales of our equity securities will dilute existing stockholders.

To fully execute our long-term business plan, we may need to raise additional working capital through future sales of our equity securities. Any such future sales of our equity securities, when and if issued, would result in dilution to our existing stockholders at the time of issuance.

We face numerous uncertainties in confirming the existence of economically recoverable coal reserves and in estimating the size of such reserves, and inaccuracies in our estimates could result in lower than expected revenues, higher than expected costs or failure to achieve profitability.

We have not established the existence of a commercially viable coal deposit on the properties in which we have an interest. Further exploration will be required in order to establish the existence of economically recoverable coal reserves and in estimating the size of those reserves. However, estimates of the economically recoverable quantities and qualities attributable to any particular group of properties, classifications of reserves based on risk of recovery and estimates of net cash flows expected from particular reserves prepared by different engineers or by the same engineers at different times may vary substantially. Actual coal tonnage recovered from identified reserve areas or properties and revenues and expenditures with respect to such reserves may vary materially from estimates. Inaccuracies in any estimates related to our reserves could materially affect our ability to successfully commence profitable mining operations.

Our future success depends upon our ability to acquire and develop coal reserves that are economically recoverable and to raise the capital necessary to fund mining operations.

Our future success depends upon our conducting successful exploration and development activities and acquiring properties containing economically recoverable coal deposits. In addition, we must also generate enough capital, either through our operations or through outside financing, to mine these reserves. Our current strategy includes completion of exploration activities on our current properties and, in the event we are able to establish the existence of commercially viable coal deposits on such properties, continuing to develop our existing properties. Our ability to develop our existing properties and to commence mining operations will depend on our ability to obtain sufficient working capital through financing activities.

5

Our ability to implement our planned development and exploration projects is dependent on many factors, including the ability to receive various governmental permits.

In the event our planned exploration activities confirm the existence of significant coal deposits on our properties, we will then be required to renew our rights in the properties in order to continue with development and mining operations. This may include renewing the existing exploration Kuasa Pertambangan, or KP, on each property, or applying for exploitation KP’s in order to have the right to commence mining operations. We currently intend to maintain interests in the properties described herein by making timely application for renewal of the existing KP’s or by filing applications to obtain the required forms of KP to commence exploitation of the properties. Although we believe that absent unusual circumstances, such as failure to pay rent or fees or the existence of excessive environmental damage, it is common practice for the Indonesian government to approve requests for issuance or renewal of KP’s, there can be no assurance that our applications will be approved. In the event our applications are not approved, we will no longer have any interest in the properties and will be unable to continue with exploration, development or exploitation of those properties. We would be required to resubmit applications or look for other properties to explore, involving additional time and capital. Additionally, the GPK property requires an additional permit from the Forestry department before Phase II can proceed. We are in the process of obtaining this permit.

Indonesian mining regulations do not currently permit KP’s to be held by non-Indonesian companies or by Indonesian companies which are wholly or partly owned by non-Indonesian persons or entities. Therefore, in order for a non-Indonesian entity such as us to have mining rights on properties in Indonesia, it is necessary to establish special contractual arrangements. We believe that the contractual arrangements we have established, which involve selecting and entering into agreements with Indonesian individuals who act as our nominees in acquiring ownership interests in the KP’s, represent a well established and accepted shed procedure which has been used by many other foreign companies which are currently conducting mining operations in Indonesia. However, there is no assurance that the contractual arrangements we have established are adequate to give us rights to explore, develop and exploit the properties or that our rights in such properties would be upheld in the event of a legal challenge by governmental officials or by a third party. Any challenge to the contractual arrangements we have established could delay the exploration or development of the properties and could ultimately result in the loss of any right or interest in such properties.

Due to variability in coal prices and in our cost of producing coal, as well as certain contractual commitments, we may be unable to sell coal at a profit.

In the event we are able to commence coal production from our properties, we will plan to sell any coal we produce for a specified tonnage amount and at a negotiated price pursuant to short-term and long-term contracts. Price adjustment, "price reopener" and other similar provisions in long-term supply agreements may reduce the protection from short-term coal price volatility traditionally provided by such contracts. Any adjustment or renegotiation leading to a significantly lower contract price would result in decreased revenues and lower our gross margins. Coal supply agreements also typically contain force majeure provisions allowing temporary suspension of performance by us or our customers during the duration of specified events beyond the control of the affected party. Most coal supply agreements contain provisions requiring us to deliver coal meeting quality thresholds for certain characteristics such as Btu, sulfur content, ash content, hardness and ash fusion temperature. Failure to meet these specifications could result in economic penalties, including price adjustments, the rejection of deliveries or, in the extreme, termination of the contracts. Consequently, due to the risks mentioned above with respect to long-term supply agreements, we may not achieve the revenue or profit we expect to achieve from any such future sales commitments. In addition, we may not be able to successfully convert these future sales commitments into long-term supply agreements.

The coal industry is highly competitive and includes many large national and international resource companies. There is no assurance that we will be able to effectively compete in this industry and our failure to compete effectively could cause our business to fail or could reduce our revenue and margins and prevent us from achieving profitability.

In the event we are able to produce coal, we will be in competition for sale of our coal with numerous large producers and hundreds of small producers who operate globally. The markets in which we may seek to sell our coal are highly competitive and are affected by factors beyond our control. There is no assurance of demand for any coal we are able to produce, and the prices that we may be able to obtain will depend primarily on global coal consumption patterns, which in turn are affected by the demand for electricity, coal transportation costs, environmental and other governmental regulations and orders, technological developments and the availability and price of competing alternative energy sources such as oil, natural gas, nuclear energy and hydroelectric energy. In addition, during the mid-1970s and early 1980s, a growing coal market and increased demand for coal attracted new investors to the coal industry and spurred the development of new mines and added production capacity throughout the industry. Although demand for coal has grown over the recent past, the industry has since been faced with overcapacity, which in turn has increased competition and lowered prevailing coal prices. Moreover, because of greater competition for electricity and increased pressure from customers and regulators to lower electricity prices, public utilities are lowering fuel costs and requiring competitive prices on their purchases of coal. Accordingly, there is no assurance that we will be able to produce coal at competitive prices or that we will be able to sell any coal we produce for a profit. Our inability to compete effectively in the global market for coal would cause our business to fail.

Our inability to diversify our operations may subject us to economic fluctuations within our industry.

Our limited financial resources reduce the likelihood that we will be able to diversify our operations. Our probable inability to diversify our activities into more than one business area will subject us to economic fluctuations within the coal industry and therefore increase the risks associated with our operations.

6

We rely heavily on our senior management, the loss of which could have a material adverse effect on our business.

Our future success is dependent on having capable seasoned executives with the necessary business knowledge and relationships to execute our business plan. Accordingly, the services of our management team, specifically, William Bloking, our President and the Chairman of our board of directors, and Jorge Nigaglioni, our Chief Financial Officer, who serves pursuant to an employment agreement, and our board of directors are deemed essential to maintaining the continuity of our operations. If we were to lose their services, our business could be materially adversely affected. Our performance will also depend on our ability to find, hire, train, motivate and retain other executive officers and key employees, of which there can be no assurance.

Because our assets and operations are located outside the United States and a majority of our officers and directors are non-United States citizens living outside of the United States, investors may experience difficulties in attempting to enforce judgments based upon United States federal securities laws against us and our directors. United States laws and/or judgments might not be enforced against us in foreign jurisdictions.

All of our operations are conducted through a subsidiary corporation organized and located outside of the United States, and all of the assets of such subsidiary corporation are located outside the United States. In addition, all of our officers and directors, other than Jorge Nigaglioni, our Chief Financial Officer, are foreign citizens. As a result, it may be difficult or impossible for United States investors to enforce judgments of United States courts for civil liabilities against us or against any of our individual directors or officers. In addition, United States investors should not assume that courts in the countries in which our subsidiary is incorporated or where the assets of our subsidiary are located would enforce judgments of United States courts obtained in actions against us or our subsidiary based upon the civil liability provisions of applicable United States federal and state securities laws or would enforce, in original actions, liabilities against us or our subsidiary based upon these laws.

Risks Related to the Coal Business

The international coal industry is highly cyclical, which will subject us to fluctuations in prices for any coal we produce.

In the event we are able to produce coal, we will be exposed to swings in the demand for coal, which will have an impact on the prices for our coal. The demand for coal products and, thus, the financial condition and results of operations of companies in the coal industry, including us, are generally affected by macroeconomic fluctuations in the world economy and the domestic and international demand for energy. In recent years, the price of coal has been at historically high levels, but these price levels may not continue. Any material decrease in demand for coal could have a material adverse effect on our operations and profitability.

The price of coal is driven by the global market. It is affected by changing requirements of customers based on their needs and the price of alternative sources of energy such as natural gas and oil.

In the event that we are able to begin producing coal, our success will depend upon maintaining a consistent margin on our coal sales to pay our costs of mining and capital expenditures. We intend to seek to control our costs of operations, but pressures by government policies and the price of substitutes could drive the price of coal down to make it unprofitable for us. The price of coal is controlled by the global market and we will be dependent on both economic and government policies to maintain the price above our future cost structure.

Logistics costs could increase and limit our ability to sell coal to end customers economically.

Logistics costs represent a significant portion of the total cost of coal and, as a result, the cost of transportation is a critical factor in a customer’s purchasing decision. Increases in transportation costs could make coal a less competitive source of energy or could make some of our operations less competitive than other sources of coal. Our future coal production, if any, will depend upon barge, trucking, pipeline and ocean-going vessels to deliver coal to markets. While coal customers typically arrange and pay for transportation of coal from the mine or port to the point of use, disruption of these transportation services because of weather-related problems, infrastructure damage, capacity restraints, strikes, lock-outs, lack of fuel or maintenance items, transportation delays or other events could temporarily impair our ability to supply coal to our customers and thus could adversely affect our results of operations.

Operating a mine has hazardous risks that can delay and increase the costs of production.

Our mining operations, if any, will be subject to conditions that can impact the safety of the workforce, or delay production and deliveries or increase the full cost of mining. These conditions include fires and explosions from methane gas or coal dust; accidental discharges; weather, flooding and natural disasters; unexpected maintenance problems; key equipment failures; variations in coal seam thickness; variations in the amount of rock and soil overlying the coal deposit; variations in rock and other natural materials and variations in geologic conditions. Despite our efforts, once operational, significant mine accidents could occur and have a substantial impact.

A shortage of skilled labor in the mining industry could pose a risk to achieving optimal labor productivity and competitive costs, which could adversely affect our profitability.

Efficient coal mining using modern techniques and equipment requires skilled laborers, preferably with at least a year of experience and proficiency in multiple mining tasks. In order to support our planned production opportunities, we intend to sponsor both in-house and vocational coal mining programs at the local level in order to train additional skilled laborers. In the event the shortage of experienced labor continues or worsens or we are unable to train the necessary amount of skilled laborers, there could be an adverse impact on our future labor productivity and costs and our ability to commence production and therefore have a material adverse effect on our earnings.

7

The coal industry could have overcapacity which would affect the price of coal and in turn, would impact our ability to realize a profit from future coal sales.

Current prices of alternative fuels such as oil are at high levels, spurring demand and investment in coal. This can lead to over investment and over capacity in the sector, dropping the price of coal to unprofitable levels. Such an occurrence would adversely affect our ability to commence mining operations or to realize a profit from any future coal sales we may seek to make.

Environmental pressures could increase and accelerate requirements for cleaner coal or coal processing.

Environmental pressures could drive potential purchasers of coal to either push the price of coal down in order to compete in the energy market or move to alternative energy supplies therefore reducing demand for coal. Requirements to have cleaner mining operations could lead to higher costs for us which could hamper our ability to make future sales at a profitable level. Coal plants emit carbon dioxide, sulfur and nitrate particles to the air. Various countries have imposed cleaner air legislations in order to minimize those emissions. Some technologies are available to do so, but also increase the price of energy derived by coal. Such an increase will drive customers to make a choice on whether or not to use coal as their driver for energy production.

Risks Related to Doing Business in Indonesia

We face the risk that changes in the policies of the Indonesian government could have a significant impact upon the business we may be able to conduct in Indonesia and the profitability of such business.

Indonesia’s economy as it relates to coal is in a transition. Indonesia has recently reduced taxation on the import of mining equipment and on the export of coal. Those changes make doing business in Indonesia more favorable, but such regulations can change in the future, and could have the effect of limiting the financial viability of our operations. Other-in country regulations could increase costs of operations, limit export quotas or net trade.

Inflation in Indonesia could negatively affect our profitability and growth.

Indonesia’s rapid climb amongst the world exporters of coal can drive increased competition and access to resources can lead to higher costs. Indonesia has kept inflation in the 6% range per annum, but constant interest rate cuts by the central bank to spur investment can lead to quicker inflation hikes. We will monitor inflation and adjust cost structures as necessary, but market pressures on resources could possibly result in operating delays.

We may experience currency fluctuation and longer exchange rate payment cycles.

The local currencies in the countries in which we intend to seek to sell our products may fluctuate in value in relation to other currencies. Such fluctuations may affect the cost of our product sold and the value of our local currency profits. While we are not conducting any operations in countries other than Indonesia at the present time, we may expand to other countries and may then have an increased risk of exposure of our business to currency fluctuation.

Terrorist threats and civil unrest in Indonesia may negatively affect our business, financial condition and results of operations.

Our business is affected by general economic conditions, fluctuations in consumer confidence and spending, and market liquidity, which can decline as a result of numerous factors outside of our control, such as terrorist attacks and acts of war. Our business also may be affected by civil unrest and individuals who engage in activities intended to disrupt our business operations. Future terrorist attacks against Indonesia or the interests of the United Kingdom or other Western nations in Indonesia, rumors or threats of war, actual conflicts involving Indonesia, the United Kingdom, or their allies, or military or trade disruptions affecting our customers may materially adversely affect our operations. As a result, there could be delays or losses in future transportation and deliveries of coal to our customers, decreased future sales of our coal and extension of time for payment of accounts receivable from our customers. Strategic targets such as energy-related assets may be at greater risk of future terrorist attacks than other targets in Indonesia. In addition, disruption or significant increases in energy prices could result in government-imposed price controls. It is possible that any, or a combination, of these occurrences could have a material adverse effect on our business, financial condition and results of operations.

Environmental disasters like earthquakes and tsunamis in Indonesia may negatively affect our business, financial condition and results of operations.

The coal concessions which we intend to operate in Indonesia are subject to natural disasters that can delay our drilling efforts to get certified measurements of the properties coal reserves, destroy infrastructure required for production and create delays in delivering product to our end customers. These impacts will require us to adjust our operations and may be financially detrimental to our success.

Risks Relating to Public Company Compliance Requirements

Public company compliance may make it more difficult to attract and retain officers and directors.

The Sarbanes-Oxley Act of 2002 and rules subsequently implemented by the Securities and Exchange Commission, or the Commission, have required changes in corporate governance practices of public companies. As a public entity, we expect these new rules and regulations to increase compliance costs and to make certain activities more time consuming and costly. As a public entity, we also expect that these rules and regulations may make it more difficult and expensive for us to obtain director and officer liability insurance in the future and we may be required to accept reduced policy limits and coverage or incur substantially higher costs to obtain the same or similar coverage. As a result, it may be more difficult for us to attract and retain qualified persons to serve as directors or as executive officers.

8

Risks Relating to Our Common Stock

Our stock price may be volatile.

The market price of our common stock is likely to be highly volatile and could fluctuate widely in price in response to various factors, many of which are beyond our control, including the following:

| · | technological innovations or new products and services by us or our competitors; |

| · | additions or departures of key personnel; |

| · | limited “public float” following the reorganization transaction, in the hands of a small number of persons whose sales or lack of sales could result in positive or negative pricing pressure on the market price for the common stock; |

| · | our ability to execute our business plan; |

| · | operating results that fall below expectations; |

| · | loss of any strategic relationship; |

| · | industry developments; |

| · | economic and other external factors; and |

| · | period-to-period fluctuations in our financial results. |

In addition, the securities markets have from time to time experienced significant price and volume fluctuations that are unrelated to the operating performance of particular companies. These market fluctuations may also materially and adversely affect the market price of our common stock.

There is currently no liquid trading market for our common stock and we cannot ensure that one will ever develop or be sustained.

Our common stock is currently approved for quotation on the Over-The-Counter Bulletin Board maintained by the National Association of Securities Dealers, Inc., or the OTC Bulletin Board, trading under the symbol “KALG.OB.” However, there is limited trading activity and not currently a liquid trading market. There is no assurance as to when or whether a liquid trading market will develop, and if such a market does develop, there is no assurance that it will be maintained. Furthermore, for companies whose securities are quoted on the OTC Bulletin Board, it is more difficult to obtain accurate quotations, to obtain coverage for significant news events because major wire services generally do not publish press releases about such companies, and to obtain needed capital. As a result, purchasers of our common stock may have difficulty selling their shares in the public market, and the market price may be subject to significant volatility.

Offers or availability for sale of a substantial number of shares of our common stock may cause the price of our common stock to decline or could affect our ability to raise additional working capital.

If our current stockholders seek to sell substantial amounts of common stock in the public market either upon expiration of any required holding period under Rule 144 or pursuant to an effective registration statement, it could create a circumstance commonly referred to as “overhang,” in anticipation of which the market price of our common stock could fall substantially. The existence of an overhang, whether or not sales have occurred or are occurring, also could make it more difficult for us to raise additional financing in the future through sale of securities at a time and price that we deem acceptable.

Our common stock is currently deemed to be “penny stock”, which makes it more difficult for investors to sell their shares.

Our common stock is currently subject to the “penny stock” rules adopted under Section 15(g) of the Securities Exchange Act or 1934, as amended, or the Exchange Act. The penny stock rules apply to companies whose common stock is not listed on the Nasdaq Stock Market or other national securities exchange and trades at less than $5.00 per share or that have tangible net worth of less than $5,000,000 ($2,000,000 if the company has been operating for three or more years). These rules require, among other things, that brokers who trade penny stock to persons other than “established customers” complete certain documentation, make suitability inquiries of investors and provide investors with certain information concerning trading in the security, including a risk disclosure document and quote information under certain circumstances. Many brokers have decided not to trade penny stocks because of the requirements of the penny stock rules and, as a result, the number of broker-dealers willing to act as market makers in such securities is limited. If we remain subject to the penny stock rules for any significant period, it could have an adverse effect on the market, if any, for our securities. If our securities are subject to the penny stock rules, investors will find it more difficult to dispose of our securities.

The elimination of monetary liability against our directors, officers and employees under Delaware law and the existence of indemnification rights to our directors, officers and employees may result in substantial expenditures by us and may discourage lawsuits against our directors, officers and employees.

Our certificate of incorporation, as amended, does not contain any specific provisions that eliminate the liability of our directors for monetary damages to us and our stockholders. However, we are prepared to give such indemnification to our directors and officers to the fullest extent provided by Delaware law. We may also have contractual indemnification obligations under its employment agreements with its executive officers. The foregoing indemnification obligations could result in us incurring substantial expenditures to cover the cost of settlement or damage awards against directors and officers, which we may be unable to recoup. These provisions and resultant costs may also discourage us from bringing a lawsuit against directors and officers for breaches of their fiduciary duties and may similarly discourage the filing of derivative litigation by our stockholders against our directors and officers even though such actions, if successful, might otherwise benefit us and our stockholders.

9

USE OF PROCEEDS

We will not receive any proceeds from the sale of our common stock by the selling stockholders. Any proceeds from the sale of our common stock offered pursuant to this prospectus will be received by the selling stockholders.

MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

Our common stock is currently quoted on the OTC Bulletin Board, under the symbol “KALG.OB.” Our common stock has been quoted on the OTC Bulletin Board since December 22, 2004. Because we are quoted on the OTC Bulletin Board, our securities may be less liquid, receive less coverage by security analysts and news media, and generate lower prices than might otherwise be obtained if they were listed on a national securities exchange.

The following table sets forth the high and low bid quotations for our common stock as reported on the OTC Bulletin Board for the periods indicated.

Fiscal Year Ending | High | Low | |||||

May 31, 2007 | |||||||

| First Quarter | 0.48 | 0.38 | |||||

| Second Quarter | 0.51 | 0.36 | |||||

| Third Quarter | 1.35 | 0.40 | |||||

| Fourth Quarter | 1.51 | 0.80 | |||||

May 31, 2008 | |||||||

| First Quarter | 1.48 | 0.46 | |||||

| Second Quarter | 0.64 | 0.17 | |||||

| Third Quarter | 0.45 | 0.25 | |||||

| Fourth Quarter | 0.40 | 0.19 | |||||

May 31, 2009 | |||||||

| First Quarter | 0.31 | 0.08 | |||||

Information for the periods referenced above has been furnished by the OTC Bulletin Board. The quotations furnished by the OTC Bulletin Board reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not reflect actual transactions.

As of September 30, 2008, we had approximately 144 holders of record of our common stock.

We have never declared or paid any cash dividends on our common stock nor do we intend to do so in the foreseeable future. Any future determination to pay cash dividends will be at the discretion of our board of directors and will depend upon our financial condition, operating results, capital requirements, any applicable contractual restrictions and such other factors as our board of directors deems relevant.

The following table summarizes the securities authorized for issuance under our equity compensation plans as of May 31, 2008.

| Plan category | Number of securities to be issued upon exercise of outstanding options, warrants and rights | Weighted average exercise price of outstanding options, warrants and rights | Number of securities remaining available for future issuance | |||||||

| Equity compensation plans approved by security holders | 12,000,000 | $ | 0.38 | 2,441,667 | ||||||

| Equity compensation plans not approved by security holders | - | - | - | |||||||

| Total | 12,000,000 | $ | 0.38 | 2,441,667 | ||||||

10

BUSINESS

Background

We were formed on February 21, 2001 under the laws of the State of Delaware.

On May 10, 2001, we entered into a letter of intent with Tri-Corp. Enterprises Ltd., or Tri-Corp, a privately-held corporation located in British Columbia, Canada, to jointly develop Gateway Falls R.V. Estates, a recreational vehicle community located on Shuswap Lake near Lee Creek, British Columbia, Canada. Under the terms of the agreement with Tri-Corp, we agreed to forward CDN$1,500,000.00 to the joint venture for the purpose of providing clear title to the development property and for use in the development of property infrastructure. We abandoned this business plan in 2001 due to the British Columbia Financial Institutions Commission's issuance of an order preventing the sale of the recreational vehicle sites.

On March 6, 2002, we entered into an option agreement to acquire an interest in the Manchester South Property, a mineral claim located in the Sudbury Mining Division of Ontario, Canada. The agreement, as amended on October 8, 2003, was between us and Terry Loney, doing business as Klondike Bay Resources. Our objective was to conduct mineral exploration activities on the Manchester South Property in order to assess whether the claim possessed commercially exploitable reserves of copper and/or nickel.

Under the terms of the option agreement, we would have been deemed to have exercised the option to acquire a 90% interest in the Manchester South Property when we had:

| · | paid Klondike Bay Resources $7,500 (paid upon the execution of the option agreement); and |

| · | incurred an aggregate of $200,000 of property exploration expenditures on the Manchester South Property within the following periods: |

| · | $25,000 on or before December 31, 2004; and |

| · | a further $175,000 on or before December 31, 2005. |

Due to our inability to raise sufficient funds to meet the exploration expenditure requirements of the option agreement with Klondike Bay Resources, we were unable to exercise the option and our right to acquire an interest in the Manchester South Property was terminated.

On December 29, 2006, we entered into a reorganization agreement with Thatcher Mining Pte Ltd., or Thatcher, a privately-held corporation formed on June 6, 2006 under the laws of Singapore. Thatcher was formed to conduct mining, quarrying and prospecting services and to engage in wholesale and retail sales of certain commodities.

Under the terms of the reorganization agreement, we agreed to acquire all of the issued and outstanding shares of Thatcher in exchange for 32,000,000 shares of our common stock. Upon closing the transactions contemplated by the reorganization agreement, we also agreed to make a cash payment of $10,000 to the former shareholders of Thatcher and to execute a royalty agreement pursuant to which we agreed to pay the former shareholders of Thatcher a royalty of $0.40 per metric ton of coal sold by us. We completed the transactions contemplated by the reorganization agreement on February 9, 2007 and, thereafter, Thatcher became our wholly-owned subsidiary.

We formed PT Kubar Resources, or Kubar, a limited liability foreign investment (PMA) company under the laws of the Republic of Indonesia on April 12, 2007, and completed its registration on June 6, 2007. Kubar will be our operating company for Indonesia.

On September 12, 2007, we acquired Finchley Resources Pte. Ltd., or Finchley, by assuming its liabilities and expenses, via a transfer of stock from its sole owner. Finchley is a corporation that was formed under the laws of the Republic of Singapore on August 13, 2007. The only expenditures incurred by Finchley were those in association with its formation. We assumed a total of $209 in liabilities from this transaction.

We now carry on the business of Thatcher as our sole line of business and all of our operations are conducted by and through Thatcher or its subsidiaries. All references to the “Company,” “we,” “our” and “us” for periods prior to the closing of the reorganization transaction refer to KAL Energy, and references to the “Company,” “we,” “our” and “us” for periods subsequent to the closing of the reorganization transaction refer to KAL Energy and its subsidiaries.

Current Activities

Our business plan is to engage in the exploration, extraction and distribution of coal. We are currently considered to be an exploration stage corporation because we are engaged in the search for coal deposits and are not engaged in the exploitation of a coal deposit. We have not engaged in the preparation of an established commercially mineable coal deposit for extraction or in the exploitation of a coal deposit. We will be in the exploration stage until we discover commercially viable coal deposits on one of our properties, if ever. In an exploration stage company, management devotes most of its activities to acquiring and exploring mineral properties.

We have the rights to two large coal concessions situated near the Mahakam River in North Eastern Kalimantan, Indonesia. Further exploration will be required before a final evaluation as to the economic feasibility of coal extraction on these properties can be determined. We have completed phase 1 drilling and obtained a Joint Ore Reserves Committee, or JORC, compliant resource measurement on one of the properties and require additional work to determine the economic viability of the deposit. The result of the programme is an inferred resource of 204 million tons of thermal coal. See item 2 for a further description of the results of the phase I programme.

11

There is no assurance that a commercially viable coal deposit exists on the unexplored portion of either of our current properties. Furthermore, there is no assurance that we will be able to successfully develop our current properties or identify, acquire or develop other coal properties that would allow us to profitably extract and distribute coal and to emerge from the exploration stage.

Products

Coal is a combustible, sedimentary, organic rock, which is composed mainly of carbon, hydrogen and oxygen. Coal goes through the process of coalification as it matures, affecting its chemical and physical properties. There are various grades of coal, ranging from low rank coals (lignite& sub-bituminous) to hard coals (bituminous & anthracite). Bituminous coal is used as either thermal coal or coking coal, depending on its properties. The properties of the coal determine its value in the market, and include but are not limited to calorific value, sulphur, moisture and ash content.

In the event that our coal concessions are found to contain commercially viable coal deposits, they are expected to yield thermal coal, which is primarily used for power generation and industrial uses. According to the World Coal Institute, or the WCI, coal accounts for approximately 39% of the world’s electricity production. Coal is a lower cost fossil fuel, helping it maintain this sizable share of energy consumption. Coal is also used for iron, steel and cement manufacture.

International Coal Market

According to the WCI, the international coal market is led by the world’s top five national producers: China, United States, India, Russia and Australia, and 16% of global hard coal production, or approximately 775 million tons, is traded internationally. The WCI also estimates that the amount of seaborne traded steam coal has increased by an average of approximately 7% per year over the past 20 years and, according to the WCI, the Pacific Rim market currently accounts for approximately 57% of the total amount of steam coal traded annually. Thermal coal is the largest contributor of this trade and Indonesia is currently the number two world exporter of thermal coal.

According to the WCI, Asia is the largest consumer of coal, accounting for approximately 54% of the total global consumption of coal, and China is the leading user of coal in the region. The Energy Information Association, or the EIA, estimates that the world coal trade should reach approximately 901 million tons by 2015, and 1,122 million tons by 2030. EIA estimates that world coal consumption will grow 74% from 2004 to 2030 and that coal’s share of energy consumption will grow from 24% to 28% from 2004 to 2030. During that period, the EIA estimates that China’s coal consumption will double from 2004 to 2015 and triple from 2004 to 2030, with 50%-60% used in electricity production and close to 40% in industrial uses. The EIA further estimates that total coal imports in Asia should increase from under 200 million tons in 2004 to approximately 500 million tons in 2030. According to Platts, the energy information division of McGraw-Hill, power generation is expected to increase in China and India, with the addition of 562 and 213 coal fired power plants from 2004-2012, respectively.

The WCI estimates that global coal demand is expected to grow by 60% through 2030, pushing electrification rates from 66% in 2002 to 78% in 2030. The WCI further estimates that coal supplies 49% to 72% of the energy production in Asian markets. The price of coal as compared to natural gas and oil drives that increased use in the region.

Employees

As of May 31, 2008, we employed 32 people, each on a full-time basis. To the best of our knowledge, we are compliant with local prevailing wage, contractor licensing and insurance regulations, and have good relations with our employees.

Property

Property Location and Access

We have rights to two coal concessions located near the Mahakam River in North Eastern Kalimantan, on the Indonesian island of Borneo. The following map illustrates the location of the properties:

12

13

The area of interest is in the vicinity of Melak, close to Senadawar, the capital of the district of Kutai Barat in the province of East Kalimantan. Melak is located approximately 100 miles northwest of the city of Balikpapan. Block 16 is approximately 6 miles southeast of Melak. Block 24 is approximately 22 miles northwest of Melak. The rivers provide the principal means of transport to bring in goods and heavy equipment and export coal and timber. The road network in Kutai Barat varies from metalled to unmade and generally requires constant repair. Access into concession areas is by four-wheel drive vehicles or trail bikes on the old logging roads or by motorized boat. The blocks lie close to the Mahakam River. Each block is10,000 hectares, approximately 24,700 acres.

The following map shows a close up view of the Block 16 claim held by PT Bunyut Bara Mandiri:

14

The following map shows a close up view of the Block 24 claim held by PT Graha Panca Karsa:

15

Claim Status

Indonesia’s natural resources are controlled by the Indonesian Government. As a result, there is no title to particular mineral deposits granted by the Indonesian government to private companies or individuals, but rather the Indonesian government will only grant the right to exploit and sell the mineral deposits. Domestic investment in mining is conducted through a KP, a license issued by the Head of Regency, the regional governor and the Indonesian Minister of Energy and Mineral Resources, depending on the location of the mining area. There are several types of KPs, which may be issued depending on the stage of development of the mining area itself, including a General Survey KP, an Exploration KP, an Exploitation KP, a Transportation and Selling KP and a Processing and Refining KP.

Indonesian mining regulations do not permit KPs to be held by non-Indonesian companies or by Indonesian companies, which are wholly or partly owned by non-Indonesian persons or entities. We have established a series of contractual arrangements, which give us an economic benefit in relation to certain mining properties in Indonesia, as further described below.

The KPs for the two properties in which we have economic rights are held by limited liability companies formed under the laws of Indonesia. PT Graha Panca Karsa, or GPK, holds an Exploration KP on Kampung Tukul Kecamatan Tering in the Kutai Barat district of East Kalimantan, and PT Bunyut Bara Mandiri, or BBM, holds an Exploration KP on Kecamatan Melak and Kecamatan Muara Lawa in the Kutai Barat district of East Kalimantan. The KPs are extendable by the company under agreement and obligations and both currently run until September 14th, 2008 unless and until extended. Applications for the extensions of the KP's have been submitted and await approval by the Regency.

Pursuant to share purchase agreements dated September 14, 2006, as amended, Thatcher agreed, in the name of its designated purchasers, to purchase all of the issued and paid up share capital of GPK for a purchase price of $175,000 and BBM for a purchase price of $150,000. The transactions contemplated by the share purchase agreements were completed on December 4, 2006, and at the closing of such transactions, two Indonesian citizens selected by Thatcher to acquire the shares in BBM and GPK, purchased all of the issued shares of both GPK and BBM.

Contemporaneously with the closing of the transactions contemplated by the share purchase agreements, (i) GPK and BBM and the shareholders of GPK and BBM executed a cooperation and investment agreement with Thatcher pursuant to which Thatcher agreed to provide all required funding and certain services in relation to the exploration work, development, construction and operation necessary to develop the mining properties and in return GPK and BBM agreed to pay Thatcher all of the net proceeds from coal sales, and (ii) GPK and BBM executed a power of attorney in favor of Thatcher giving Thatcher the authority to sign any and all documents relating to mining operations on behalf of GPK and BBM.

In addition, the shareholders of GPK and BBM executed (i) a loan agreement with Thatcher to record the terms upon which Thatcher loaned them the funds needed to purchase the shares of GPK and BBM, (ii) a share pledge agreement issued to Thatcher pledging their shares as collateral security for their obligations under their respective loan agreements, cooperation and investment agreements, and any related agreements, and (iii) a power of attorney in favor of Thatcher giving Thatcher the power to vote the shares in GPK and BBM. We have included the results of GPK and BBM in our financial statements as of May 31, 2008, as a variable interest entity, as we currently stand to absorb the majority of the variable interest entity’s expected losses. We have commenced a change in the ownership of GPK and BBM in accordance with the terms of the aforementioned agreements. Article 127 of Company Law requires that any change of more than 50% shareholding requires a newspaper announcement, with closing to occur no earlier than 30 days following the announcement. We expect to complete these transactions in the next 45 days.

In the event that coal is produced and delivered to customers from either of these properties, we will be obligated to pay production sharing fees under production share agreements dated as of December 4, 2006 as follows:

| · | a share of the proceeds of production totaling $0.45 per ton pursuant to production share agreements entered into among GPK, Ferdinandus Hanye, Eko Purwanto, Rudiansyah and Laurensius Hajang, and between GPK and Laurensius Hajang, for production under the KP held by GPK. This share of production proceeds will be paid to the recipients in return for providing assistance to GPK relating to the development of the mining project (particularly in the area of local community relations); and |

| · | a share of the proceeds of production totaling $0.45 per ton pursuant to production share agreements entered into among BBM, Kristiana Neny, Eko Purwanto and Laurensius Hajang, and between BBM and Laurensius Hajang, for production under the KP held by BBM. This share of production proceeds will be paid to the recipients in return for providing assistance to BBM relating to the development of the mining project (particularly in the area of local community relations). |

Depending on the quality of the coal delivered, royalties of between 3% and 7% will be paid to the Indonesian government.

In addition to the production sharing fees described above, we will be obligated to pay a royalty of $0.40 per ton to the former shareholders of Thatcher pursuant to a royalty agreement dated December 29, 2006, entered into between the us, Thatcher and the former shareholders of Thatcher, which include Essendon Capital Ltd., a privately-held company incorporated under the laws of Samoa, Carlton Corp., a privately-held company incorporated under the laws of the Republic of the Seychelles, and Concord International, Inc., a privately-held company incorporated under the laws of the Bahamas.

Pursuant to the terms of a cooperation and investment agreement, GPK and BBM are required to maintain their respective KPs in full force and effect, and to apply for any extensions or renewals of their respective KPs at our direction. We have instructed GPK and BBM to apply for extensions of their respective KPs prior to their expiration. The applications have been submitted and are awaiting approval by the Regency. Although we anticipate that the KPs will be renewed prior to their expiration, there is no assurance that the governing body will grant such renewal. Additionally, the GPK property requires an additional permit from the Forestry department before Phase II can proceed. We are in the process of obtaining this permit.

16

History

We are not aware of any previous mining activities, which have taken place on either of the properties in which we have rights. However, there have been logging operations in the area.

Geology

A field exploration program was conducted on Block 16 and Block 24 in July 2006. Based on that study, the following information is available:

The rocks of Kutai Barat are mostly contained within the Kutai Basin. A summary of the stratigraphy in the Kutai Basin is given in the Table below.

Epoch | Division | Map Ref | Facies | Formation | |

Holocene | Qa | Alluvium | |||

Pleistocene | Tpkb | Mixed with lignite | Kampung Baru | ||

Pliocene | — | — | — | ||

| Late | Tmbp | Mixed with lignite/coal | Balikpapan | ||

| Unconformity | |||||

Miocene | Middle | Tmpb Tmm | Sandstone and mixed, with coal. Tmm – andesite | Palau Balang | Tmm Maragoh |

| Unconformity | |||||

| Early | Tomp | Sandstone and mixed, with coal | Pamaluan | ||

Oligocene | Late | Unconformity | |||

| Early | Toty | Mixed with lignite/coal | Tuyu | ||

Eocene | — | — | — | ||

The regional structural trend of fold axes and major faulting is northeast-east northeast, a trend easily picked out on the satellite images. Other important structural features trend approximately north-south. The area can be divided into three areas based on the topography and the underlying geology.

The floodplain of the Mahakam River and its tributaries

The area is characterized by very low relief and dominated by swamps. Solid geology outcrops of the coal bearing sediments are rare, the area being mostly covered by late Holocene/Quaternary alluvium.

Intermediate ground

This is underlain by the main coal bearing strata of the Pamalauan, Palau Balang and Balikpapan Formations. These formations are of mixed facies with sandstone, siltstones and mudstones/clays with coal seams. These formations form low, undulating hills that have been eroded to form numerous small, V-shaped gullies and valleys.

High ground

Mostly located 200m above sea level, these areas contain the volcanic rocks, andesites and tuffs of the Maragoh Formation and, in the northwest, small areas of the quartzitic Haloq Sandstone Formation of the neighboring basin.

In Block 24, coal seams up to 8 m thick have been recorded. Some 92% of the outcrops recorded in the block have dips under 10 degrees. Gently rolling topography combined with shallow dips (dip-slope) will ensure favorable stripping ratios. The program yielded a collection of coal samples that were analyzed for moisture, ash, sulphur and calorific values of the coal in the property.

Infrastructure

There are approximately 130 kilometers of unsealed roads on the properties, which were built by legacy logging operators operating on the properties. Both of the properties are situated close to the Mahakan River, which is used for barge transportation. In addition, both properties are situated near Melak, a small rural town, which provides a logistic base for operations.

Coal

We completed our Phase I Drilling Programme and obtained a JORC, code compliant resource statement for the GPK site on June 11, 2007. The competent persons reported Inferred Resources of 204 million tons of thermal coal. The coal properties are as below:

Graha Seam Quality | ||||||||||||||||||||

| Stats | TM ar % | IM ad % | Ash ad % | VM ad % | FC ad % | RD ad | TS ad % | CV ad kcal/kg | CV db kcal/kg | CV daf kcal/kg | ||||||||||

Average | 39.9 | 19.4 | 4.9 | 40.9 | 34.8 | 1.33 | 0.18 | 5,189 | 6,415 | 6,856 | ||||||||||

| Minimum | 33.9 | 12.9 | 1.4 | 35.4 | 29.4 | 1.29 | 0.03 | 4,346 | 5,536 | 6,499 | ||||||||||

| Maximum | 43.3 | 27.6 | 15.1 | 47.1 | 40.0 | 1.42 | 0.37 | 5,873 | 6,945 | 7,242 | ||||||||||

(ar = as received, ad = air dried, db = dry basis, daf = dry ash free basis)

Relative Density (RD) of 1.31 used for conservative estimates.

17

Legal Proceedings.

None.

18

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

You should read the following discussion of our financial condition and results of operations together with our financial statements and related notes included elsewhere in this prospectus. This discussion may contain forward-looking statements that involve risks and uncertainties. Our actual results may differ materially from those anticipated in these forward-looking statements due to known and unknown risks, uncertainties and other factors, including those risks discussed under “Risk Factors” and elsewhere in this prospectus.

Results of Operations

Three-month period ended August 31, 2008 compared to the three-month period ended August 31, 2007

Revenue

We have not earned any revenue from our operations from the date of our inception on February 21, 2001 through August 31, 2008. Our activities have been financed from the proceeds of private placement offerings of our common stock. We do not anticipate earning any revenue until we have obtained additional capital to fund early production from our coal concessions.

Expenses

Exploration Expenses

Exploration expenses for the three month period ended August 31, 2008 decreased to $379,916, as compared to $1,425,746 for the three month period ended August 31, 2007. The decrease is related to the high expenditure rate from the finish of the Phase I exploration phase of the PT Graha Panca Karsa concession and the continued work on site. Our operations in 2008 have focused on preparation work for the PT Bunyut Bara Mandiri concession.

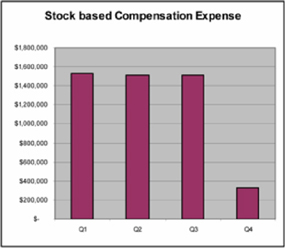

Stock-based Compensation Expense

Stock-based compensation expense for the three month period ended August 31, 2008 decreased to $209,992, as compared to $1,527,396 for the three month period ended August 31, 2007. The decrease is mainly due to the cancellation of 8,145,417 stock option and restricted stock grants since August 31, 2008 against grants of only 4,115,000 issued under our equity compensation plan. The Company recorded a one time credit of $343,585 during the quarter ended August 31, 2008 for unvested grants cancelled during the quarter. The Company has expensed $2,219,764 for cancelled grants that vested but were not exercised since the inception of the plan.

19

General and Administrative Expense

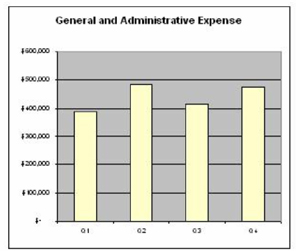

General and administrative expense for the three month period ended August 31, 2008 increased to $411,760, as compared to $376,317 for the three month period ended August 31, 2007. The increase is mainly due to an increase in executive salaries and relocation costs related to the relocation of our principal executive offices.

Professional and Consulting Fees

Professional and consulting fees for the three month period ended August 31, 2008 increased to $398,051, as compared to $210,277 for the three month period ended August 31, 2007. The increase is mainly due to expenses related to the search fees for a new chief executive officer and other personnel, consulting fees related to the resolution of our June 2008 private placement offering of common stock and ongoing legal and accounting fees.

Loss

Net loss for the three month period ended August 31, 2008 decreased to $1,335,997, as compared to a net loss of $3,526,901 for the three month period ended August 31, 2007. The increase in income was mostly due to reductions in exploration expenditures, reductions in the administrative costs of the company and the reductions due to the cancellation of stock option and restricted stock grants issued under our equity compensation plan as described above. We have not attained profitable operations and are dependent upon obtaining additional financing to move from our exploration activities to our initial production. Our proforma losses increased to $16,390,008 due primarily to continued spending on our exploration programmes.

Capital Resources

As of August 31, 2008, we had current assets of $1,512,450, consisting of $1,190,573 in cash and cash equivalents, $75,450 in other receivables and $246,427 in prepaid expenses and deposits. This is a decrease of $631,368 from May 31, 2008. We have not completed our fundraising efforts and have used our cash reserves during the quarter to fund our operations.

Liabilities

As of August 31, 2008, we had liabilities of $983,525, consisting of accounts payable of $462,597 and accrued liabilities of $520,928. This is a decrease of $313,934 from May 31, 2008. We issued $700,000 of shares of our common stock during the quarter that were recorded as a liability as of May 31, 2008. That was partially offset by an increase in liabilities from operations at the quarter end.

20

Results Of Operations

References in the discussion below to 2008 are to our fiscal year ended May 31, 2008, while references to 2007 are to our fiscal year ended May 31, 2007.

Year ended May 31, 2008 compared to the year ended May 31, 2007

Revenue

We have not earned any revenue from operations from our incorporation on February 21, 2001 to May 31, 2008. Our activities have been financed from the proceeds of private placement offerings of our common stock. We do not anticipate earning any revenue until such time as we complete the property exploration and complete activities relating to the preparation of coal extraction, of which there is no assurance.

Expenses

Exploration Expenses

During our fiscal year ended May 31, 2008, we incurred $3,140,838 of exploration expenses, as compared to $1,228,807 of exploration expenses for the year ended May 31, 2007. This increase in exploration expense is due primarily to the work performed on the Graha concession to bring it to a JORC Compliant inferred resource of 204 million tons in June 2007, the exploration of a coal concession in Mongolia and the follow up work in the southwest and eastern blocks of the Graha Concession to further define the resource, including its coal quality and resource mineability.

We incurred significant manpower expense of approximately $1,552,421 for the year ended May 31, 2008 versus $500,325 for the year ended May 31, 2007. This increase in manpower expense is due primarily to the difference in months under exploration of twelve in 2008 as compared to four in 2007. Site expenses incurred were approximately $816,333 for the year ended May 31, 2008 as compared to $407,740 for the year ended May 31, 2007. These include on site facilities, catering, paving and telecommunications. Equipment expense of approximately $481,205 was incurred for the year ended May 31, 2008 as compared to $178,899 for the year ended May 31, 2007. We incurred travel expense of approximately $290,879 for the year ended May 31, 2008 as compared to $141,843 for the year ended May 31, 2007. This includes the travel to and within Kalimantan, Indonesia, as well as travel to Mongolia and other prospective properties under evaluation.

We spent $2,768,948 in coal concessions in Indonesia and $371,890 in due diligence exploration in Mongolia. These expenses were related to the coal concessions in Indonesia under exploration that started after the reorganization transaction. These expenses were part of our Phase I drilling programme to establish a JORC-compliant inferred resource. This included equipment rentals, fuel costs, third party manpower and site maintenance costs.

21

Stock Based Compensation Expense

We incurred stock based compensation expense of $4,883,059 for the year ended May 31, 2008 as compared to $1,301,372 for the year ended May 31, 2007. This increase resulted from operating under the 2007 Stock Incentive Plan for a full year versus one month in 2007. We reduced the number of our employees and consultants as part of our ongoing efforts to reduce operating costs during the last two quarters of 2008. Those efforts resulted in a reduction of stock based compensation. A one time reduction of $1,115,798 was recorded in the fourth quarter to reflect the impact of the grant cancellations. The net fourth quarter expense of $330,788 is not indicative of the ongoing expense. The recurring expense in the fourth quarter was $1,243,713.

General and Administrative Expense

We incurred general and administrative expense of $1,980,357 for the year ended May 31, 2008 as compared to $552,025 for the year ended May 31, 2007, with the increase resulting from a full year of operations in 2008 as compared to four months of operations in 2007. The primary expense was related to salaries and fees for our officers and directors. We also leased offices in London, Singapore and Jakarta during the year ended May 31, 2008. The expense also covers the amortization of intangible assets of $88,571 per quarter. Travel also contributed to the high run rate, although we curtailed travel in the later quarters of 2008 as part of our cost controls.

Professional Expenses

Professional and consulting fees for the year ended May 31, 2008 increased to $732,921, as compared to $642,835 for the year ended May 31, 2007. This increase in professional fees reflects our operations over the course of an entire year as compared to four months in 2007. We use the services of legal counsel and accountants in all the countries in which we operate to ensure compliance with applicable laws and regulatory filings. We also used the services of Mining House Ltd during the year ended May 31, 2008.

22

Loss

Net loss for the year ended May 31, 2008 increased to $10,647,276, as compared to $3,693,152 for the year ended May 31, 2007. The increased loss was due to an increase in expenses, as discussed above. We have not attained profitable operations and are dependent upon obtaining additional financing to move from our exploration activities to our initial production.

Capital Resources