Exhibit 99.2

| TransAllied Group Holdings, AG Investor Presentation June 13, 2011 |

| Cautionary Note Regarding Forward-Looking Statements This presentation contains forward-looking statements that involve a number of risks and uncertainties. Statements that are not historical facts, including statements about our beliefs and expectations, are forward-looking statements. Forward-looking statements are based on managements beliefs, as well as assumptions made by, and information currently available to, management. Because such statements are based on expectations as to future economic performance and are not statements of fact, actual results may differ materially from those projected. We undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise. Important factors that could cause our actual results to differ, possibly materially, from those discussed in the specific forward-looking statements may include, but are not limited to, uncertainties relating to economic conditions, financial and credit market conditions, cyclical industry conditions, credit quality, government, regulatory and accounting policies, volatile and unpredictable developments (including natural and man-made catastrophes), the legal environment, legal and regulatory proceedings, failures of pricing models to accurately assess risks, the reserving process, the competitive environment in which we operate, interest rate and foreign currency exchange rate fluctuations and the uncertainties inherent in international operations; and other risks detailed in the Cautionary Statement Regarding Forward-Looking Information, Risk Factors and other sections of the Companies Form 10-K and other filings with the Securities and Exchange Commission. Additional Information about the Proposed Merger and Where to Find It This communication relates to a proposed merger between Transatlantic and Allied World that will become the subject of a registration statement, which will include a joint proxy statement/prospectus, to be filed with the U.S. Securities and Exchange Commission (the "SEC") that will provide full details of the proposed merger and the attendant benefits and risk. This communication is not a substitute for the joint proxy statement/prospectus or any other document that Transatlantic or Allied World may file with the SEC or send to their shareholders in connection with the proposed merger. Investors and security holders are urged to read the registration statement on Form S-4, including the definitive joint proxy statement/prospectus, and all other relevant documents filed with the SEC or sent to shareholders as they become available because they will contain important information about the proposed merger. All documents, when filed, will be available free of charge at the SECs website (www.sec.gov). You may also obtain these documents by contacting Transatlantics Investor Relations department at Transatlantic Holdings, Inc., 80 Pine Street, New York, New York 10005, or via e-mail at investor_relations@transre.com; or by contacting Allied Worlds Corporate Secretary, attn.: Wesley D. Dupont, at Allied World Assurance Company Holdings, AG, Lindenstrasse 8, 6340 Baar, Zug, Switzerland, or via e-mail at secretary@awac.com. This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. Participants in the Solicitation Transatlantic, Allied World and their respective directors and executive officers may be deemed to be participants in any solicitation of proxies in connection with the proposed merger. Information about Transatlantics directors and executive officers is available in Transatlantic’s proxy statement dated April 8, 2011 for its 2011 Annual Meeting of Stockholders. Information about Allied Worlds directors and executive officers is available in Allied Worlds proxy statement dated March 17, 2011 for its 2011 Annual Meeting of Shareholders. Other information regarding the participants in the proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, will be contained in the joint proxy statement/prospectus and other relevant materials to be filed with the SEC regarding the merger when they become available. Investors should read the joint proxy statement/prospectus carefully when it becomes available before making any voting or investment decisions. |

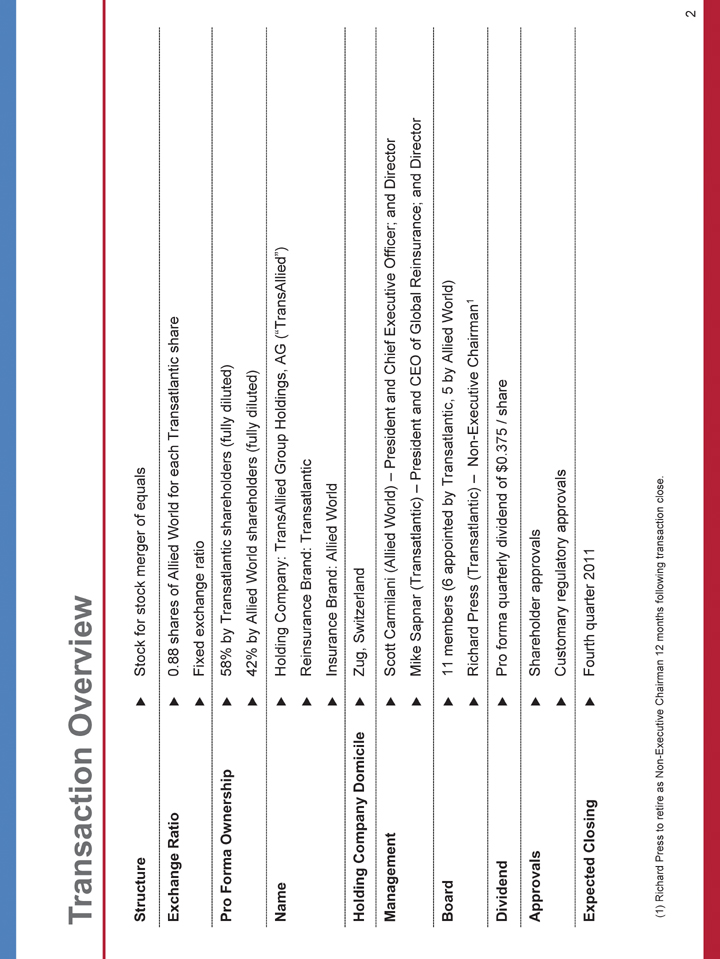

| Transaction Overview Structure Stock for stock merger of equals Exchange Ratio 0.88 shares of Allied World for each Transatlantic share Fixed exchange ratio Pro Forma Ownership 58% by Transatlantic shareholders (fully diluted) 42% by Allied World shareholders (fully diluted) Name Holding Company: TransAllied Group Holdings, AG (“TransAllied”) Reinsurance Brand: Transatlantic Insurance Brand: Allied World Holding Company Domicile Zug, Switzerland Management Scott Carmilani (Allied World) — President and Chief Executive Officer; and Director Mike Sapnar (Transatlantic) — President and CEO of Global Reinsurance; and Director Board 11 members (6 appointed by Transatlantic, 5 by Allied World) Richard Press (Transatlantic) — Non-Executive Chairman1Dividend Pro forma quarterly dividend of $0.375 / share Approvals Shareholder approvals Customary regulatory approvals Expected Closing Fourth quarter 2011 (1) Richard Press to retire as Non-Executive Chairman 12 months following transaction close. 2 |

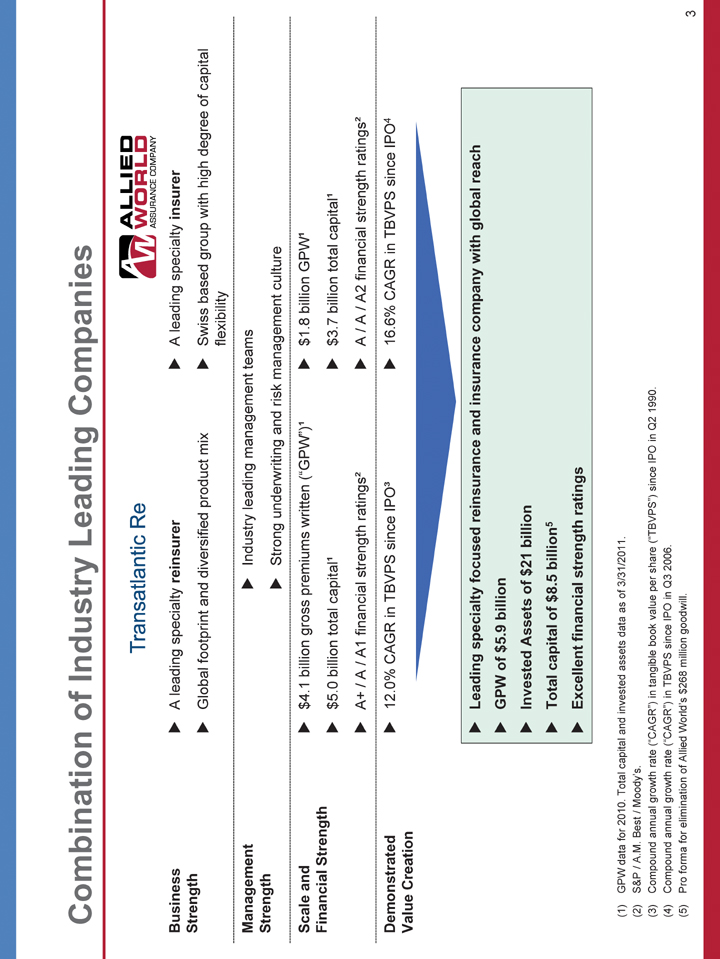

| Combination of Industry Leading Companies Business A leading specialty reinsurer A leading specialty insurer Strength Global footprint and diversified product mix Swiss based group with high degree of capital flexibility Management Industry leading management teams Strength Strong underwriting and risk management culture Scale and $4.1 billion gross premiums written (“GPW”)1 $1.8 billion GPW1 Financial Strength $5.0 billion total capital1 $3.7 billion total capital1 A+ / A / A1 financial strength ratings2 A / A / A2 financial strength ratings2 Demonstrated 12.0% CAGR in TBVPS since IPO3 16.6% CAGR in TBVPS since IPO4 Value Creation Leading specialty focused reinsurance and insurance company with global reach GPW of $5.9 billion Invested Assets of $21 billion Total capital of $8.5 billion5 Excellent financial strength ratings (1) GPW data for 2010. Total capital and invested assets data as of 3/31/2011. (2) S&P / A.M. Best / Moody’s. (3) Compound annual growth rate (“CAGR”) in tangible book value per share (“TBVPS”) since IPO in Q2 1990. (4) Compound annual growth rate (“CAGR”) in TBVPS since IPO in Q3 2006. (5) Pro forma for elimination of Allied World’s $268 million goodwill. 3 |

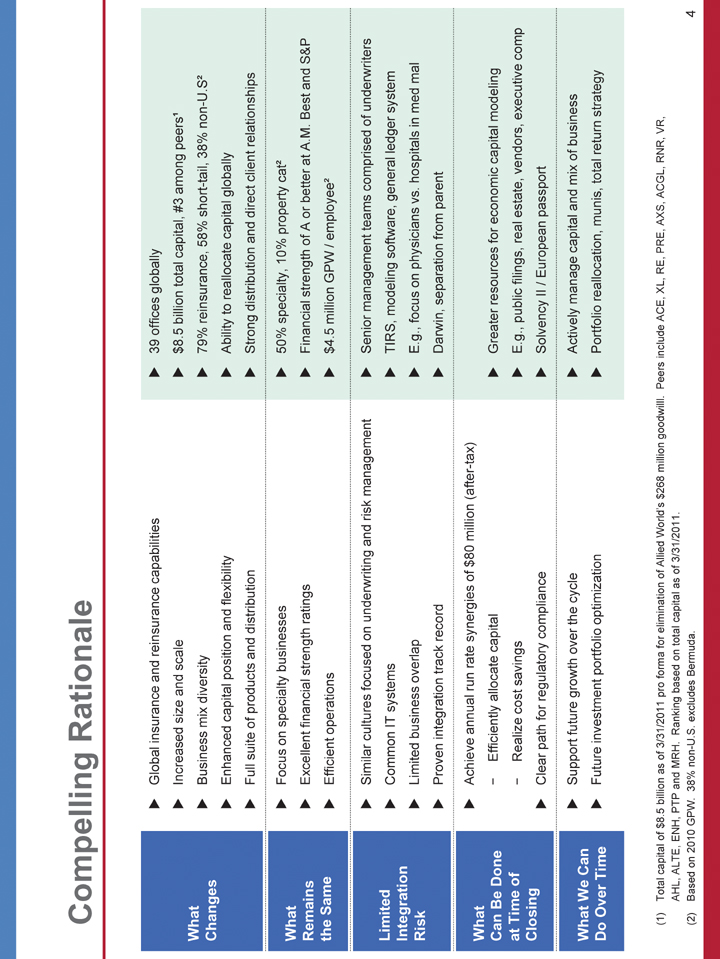

| Compelling Rationale Global insurance and reinsurance capabilities 39 offices globally Increased size and scale $8.5 billion total capital, #3 among peers1 What Business mix diversity 79% reinsurance, 58% short-tail, 38% non-U.S2 Changes Enhanced capital position and flexibility Ability to reallocate capital globally Full suite of products and distribution Strong distribution and direct client relationships Focus on specialty businesses 50% specialty, 10% property cat2 What Remains Excellent financial strength ratings Financial strength of A or better at A.M. Best and S&P the Same Efficient operations $4.5 million GPW / employee2 Similar cultures focused on underwriting and risk management Senior management teams comprised of underwriters Limited Common IT systems TIRS, modeling software, general ledger system Integration Risk Limited business overlap E.g., focus on physicians vs. hospitals in med mal Proven integration track record Darwin, separation from parent Achieve annual run rate synergies of $80 million (after-tax) What Can Be Done - Efficiently allocate capital Greater resources for economic capital modeling at Time of — Realize cost savings E.g., public filings, real estate, vendors, executive comp Closing Clear path for regulatory compliance Solvency II / European passport Support future growth over the cycle Actively manage capital and mix of business What We Can Do Over Time Future investment portfolio optimization Portfolio reallocation, munis, total return strategy (1) Total capital of $8.5 billion as of 3/31/2011 pro forma for elimination of Allied World’s $268 million goodwilll. Peers include ACE, XL, RE, PRE, AXS, ACGL, RNR, VR, AHL, ALTE, ENH, PTP and MRH. Ranking based on total capital as of 3/31/2011. (2) Based on 2010 GPW. 38% non-U.S. excludes Bermuda. 4 |

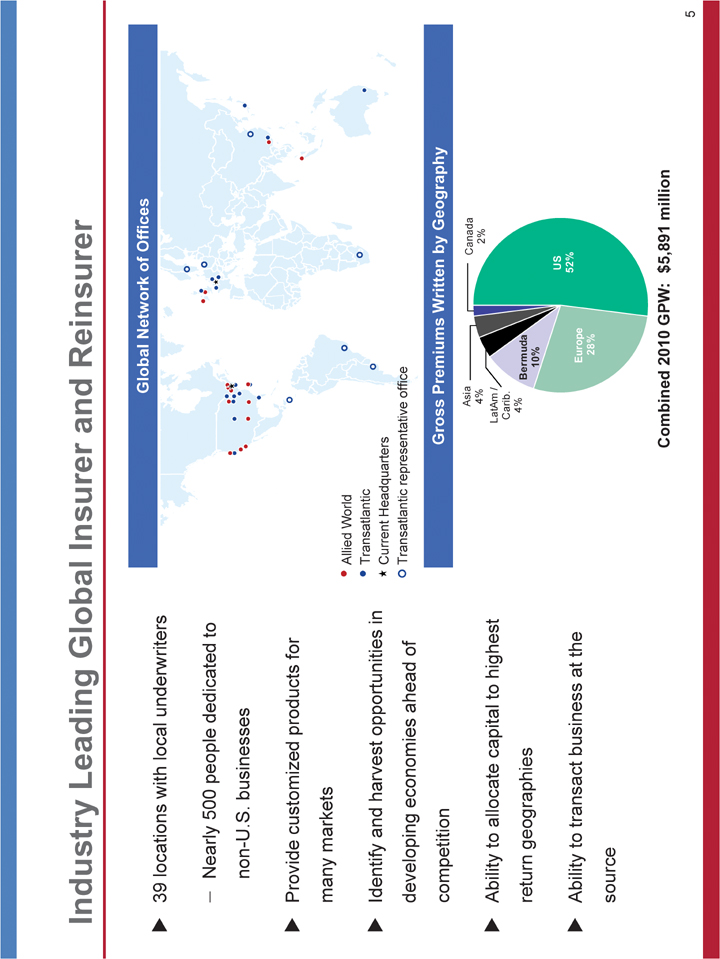

| Industry Leading Global Insurer and Reinsurer Global Network of Offices 39 locations with local underwriters Nearly 500 people dedicated to non-U.S. businesses Provide customized products for many markets Allied World Transatlantic Identify and harvest opportunities in Current Headquarters developing economies ahead of Transatlantic representative office competition Gross Premiums Written by Geography Asia Canada 4% 2% Ability to allocate capital to highest LatAm / Carib. 4% return geographies Bermuda 10% US Ability to transact business at the 52% Europe 28% source Combined 2010 GPW: $5,891 million 5 |

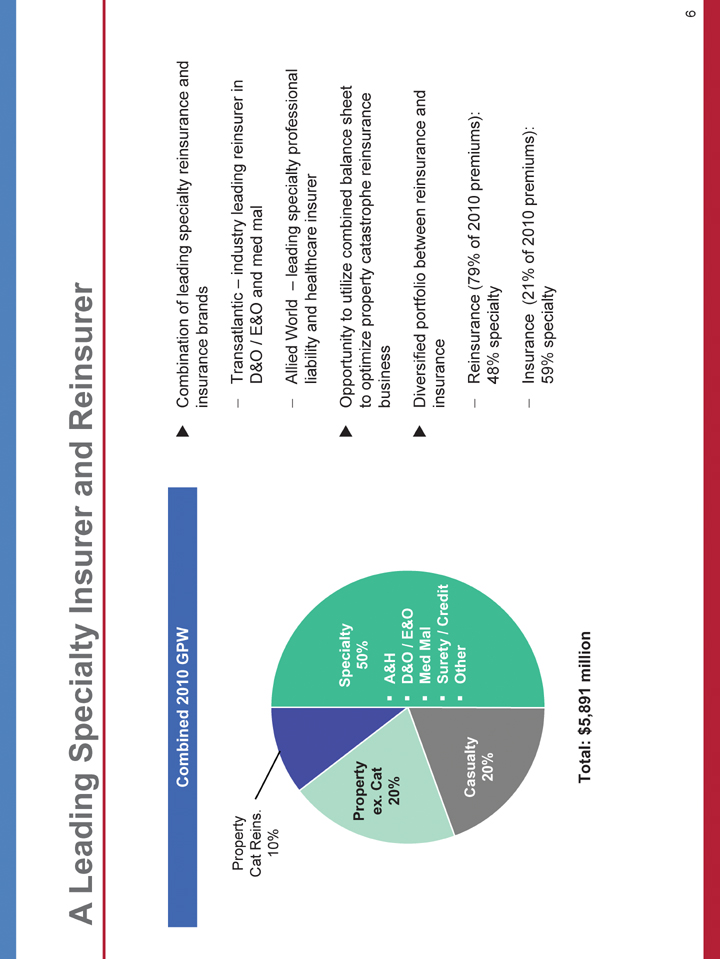

| A Leading Specialty Insurer and Reinsurer Combined 2010 GPW Combination of leading specialty reinsurance and insurance brands Property Transatlantic — industry leading reinsurer in Cat Reins. D&O / E&O and med mal 10% Allied World — leading specialty professional liability and healthcare insurer Specialty Opportunity to utilize combined balance sheet Property 50% to optimize property catastrophe reinsurance ex. Cat A&H business 20% D&O / E&O Med Mal Diversified portfolio between reinsurance and Surety / Credit insurance Other Casualty Reinsurance (79% of 2010 premiums): 20% 48% specialty Insurance (21% of 2010 premiums): 59% specialty Total: $5,891 million 6 |

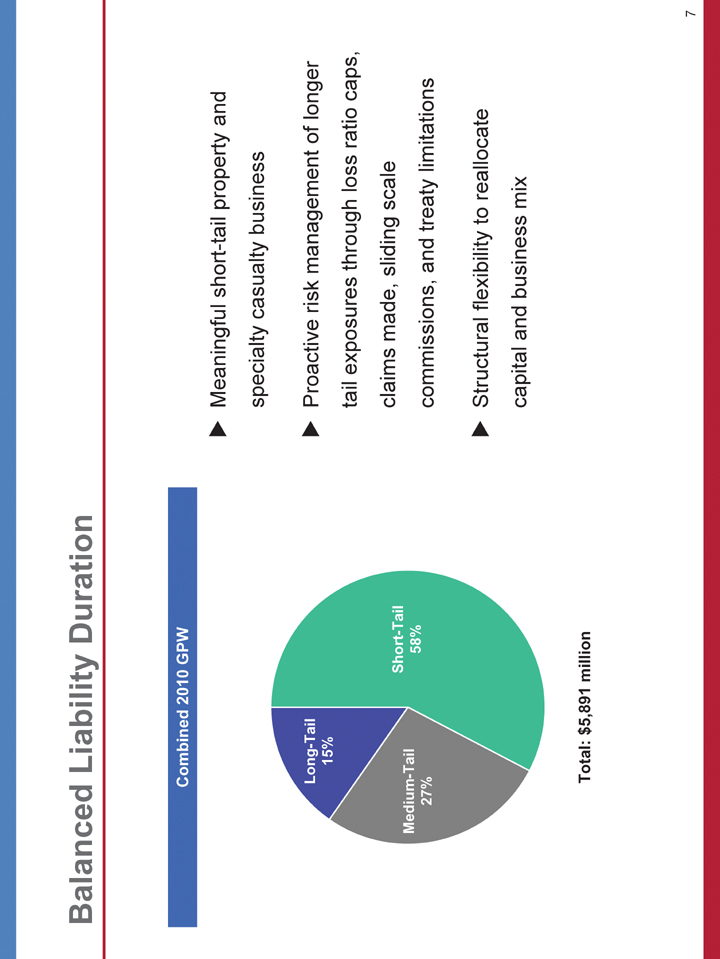

| Balanced Liability Duration Combined 2010 GPW Meaningful short-tail property and specialty casualty business Long-Tail Proactive risk management of longer 15% tail exposures through loss ratio caps, claims made, sliding scale Short-Tail Medium-Tail 58% 27% commissions, and treaty limitations Structural flexibility to reallocate capital and business mix Total: $5,891 million 7 |

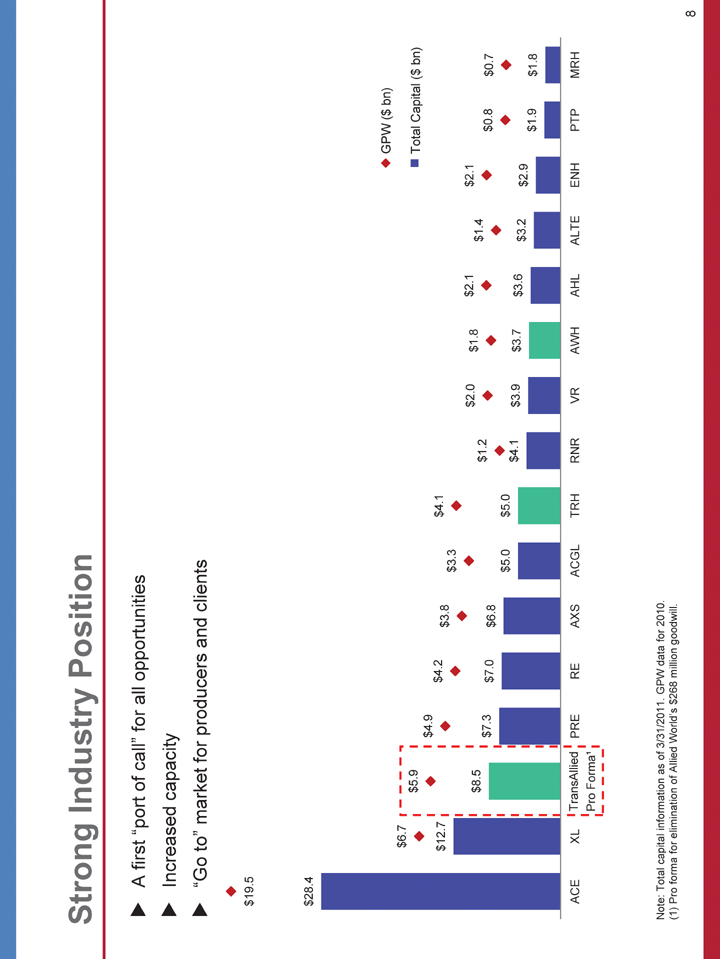

| Strong Industry Position A first “port of call” for all opportunities Increased capacity “Go to” market for producers and clients $19.5 $28 .4 GPW ($ bn) $6.7 $5 .9 Total Capital ($ bn) $4.9 $12.7 $4.2 $4.1 $3.8 $3.3 $2.0 $1.8 $2.1 $2.1 $8.5 $1.4 $7.3 $1.2 $7.0 $6.8 $0.8 $0.7 $5.0 $5.0 $4 .1 $3.9 $3.7 $3.6 $3.2 $2.9 $1.9 $1.8 ACE XL TransAllied PRE RE AXS ACGL TRH RNR VR AWH AHL ALTE ENH PTP MRH Pro Forma1 Note: Total capital information as of 3/31/2011. GPW data for 2010. (1) Pro forma for elimination of Allied World’s $268 million goodwill. 8 |

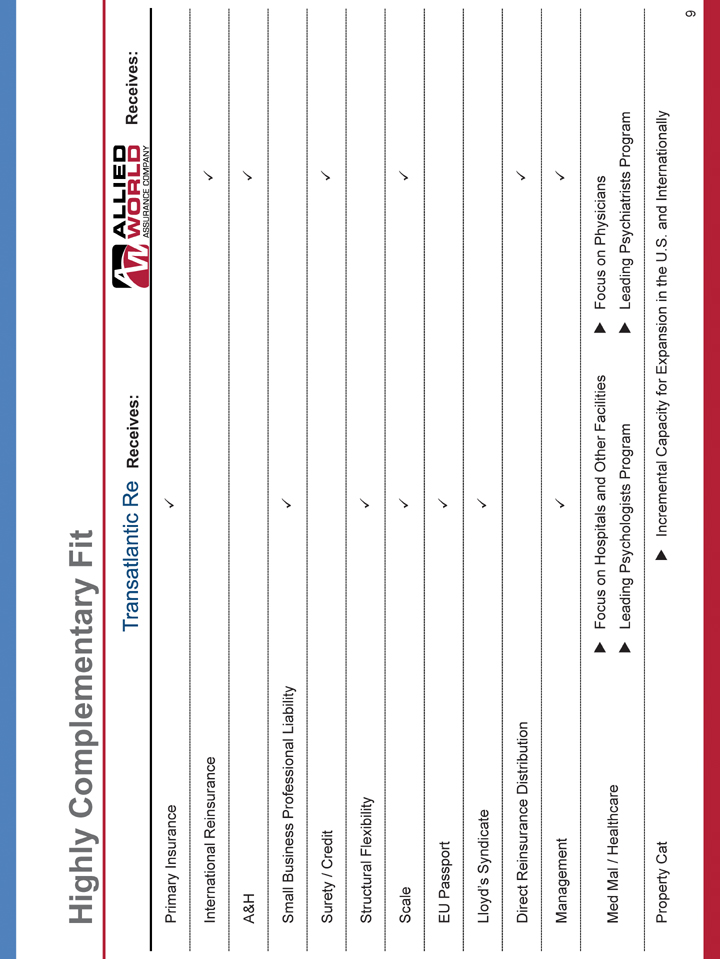

| Highly Complementary Fit Receives: Receives: Primary Insurance International Reinsurance A&H Small Business Professional Liability Surety / Credit Structural Flexibility Scale EU Passport Lloyd’s Syndicate Direct Reinsurance Distribution Management Focus on Hospitals and Other Facilities Focus on Physicians Med Mal / Healthcare Leading Psychologists Program Leading Psychiatrists Program Property Cat Incremental Capacity for Expansion in the U.S. and Internationally 9 |

| Strong Combined Balance Sheet As of March 31, 2011 Pro Forma1 ($ in millions) Cash & Investments $13,483 $7,992 $21,475 Net Loss and LAE Reserves 8,913 4,125 13,038 Debt 1,006 798 1,803 Shareholders’ Equity 4,041 2,951 6,724 Total Capital 5,047 3,749 8,527 Total Debt / Total Capital 19.9% 21.3% 21.1% NPW2 / Total Capital 0.77x 0.38x 0.63x (NPW2+Net Reserves) / Total Capital 2.54 1.48 2.16 (1) Pro forma for elimination of Allied World’s $268 million goodwill. (2) Net premiums written (“NPW”) for the last 12 months ending March 31, 2011. 10 |

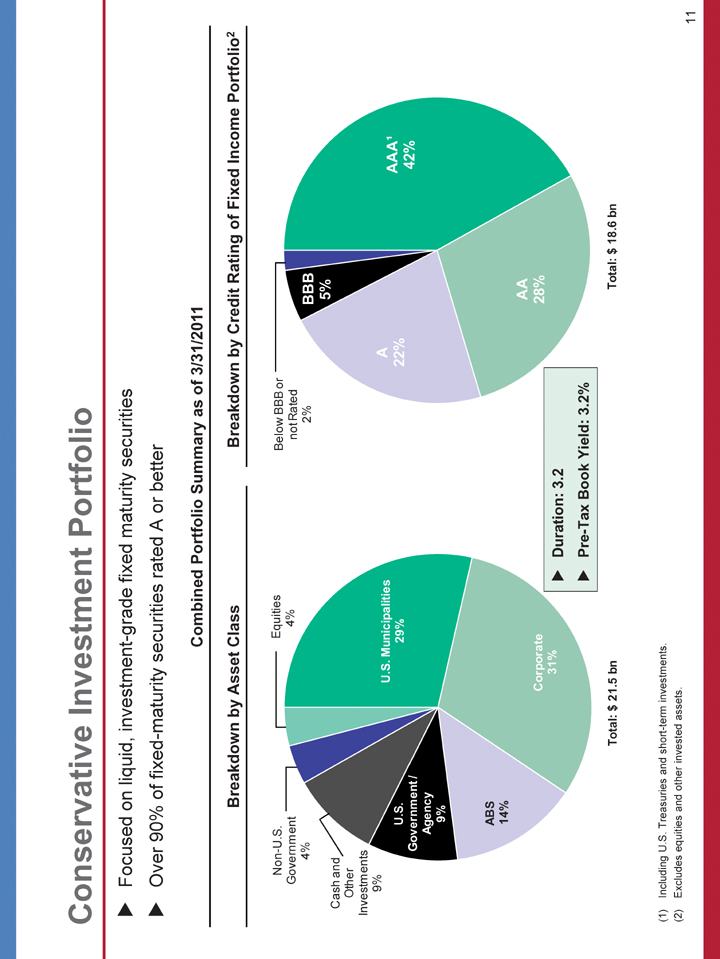

| Conservative Investment Portfolio Focused on liquid, investment-grade fixed maturity securities Over 90% of fixed-maturity securities rated A or better Combined Portfolio Summary as of 3/31/2011 Breakdown by Asset Class Breakdown by Credit Rating of Fixed Income Portfolio2 Non-U.S. Equities Below BBB or Government 4% not Rated 4% 2% BBB 5% Cash and Other Investments 9% A U.S. Municipalities AAA1 U.S. 29% 22% Government / 42% Agency 9% ABS 14% AA Corporate 28% 31% Duration: 3.2 Pre-Tax Book Yield: 3.2% Total: $21.5 bn Total: $18.6 bn (1) Including U.S. Treasuries and short-term investments. (2) Excludes equities and other invested assets. 11 |

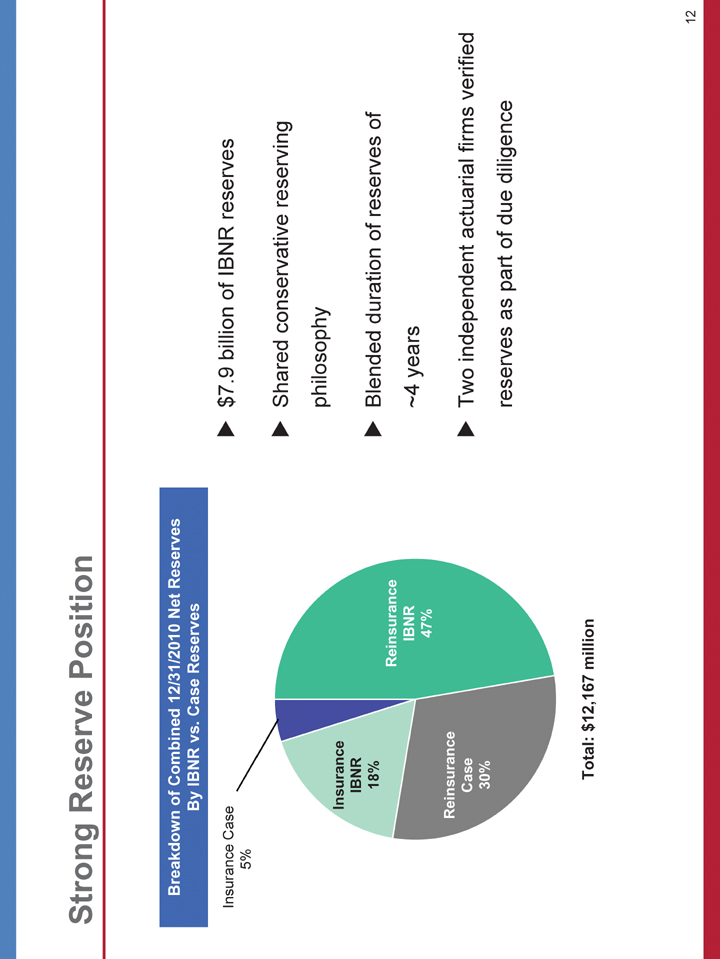

| Strong Reserve Position Breakdown of Combined 12/31/2010 Net Reserves By IBNR vs. Case Reserves Insurance Case $7.9 billion of IBNR reserves 5% Shared conservative reserving philosophy Insurance IBNR 18% Blended duration of reserves of Reinsurance IBNR ~4 years 47% Reinsurance Case Two independent actuarial firms verified 30% reserves as part of due diligence Total: $12,167 million 12 |

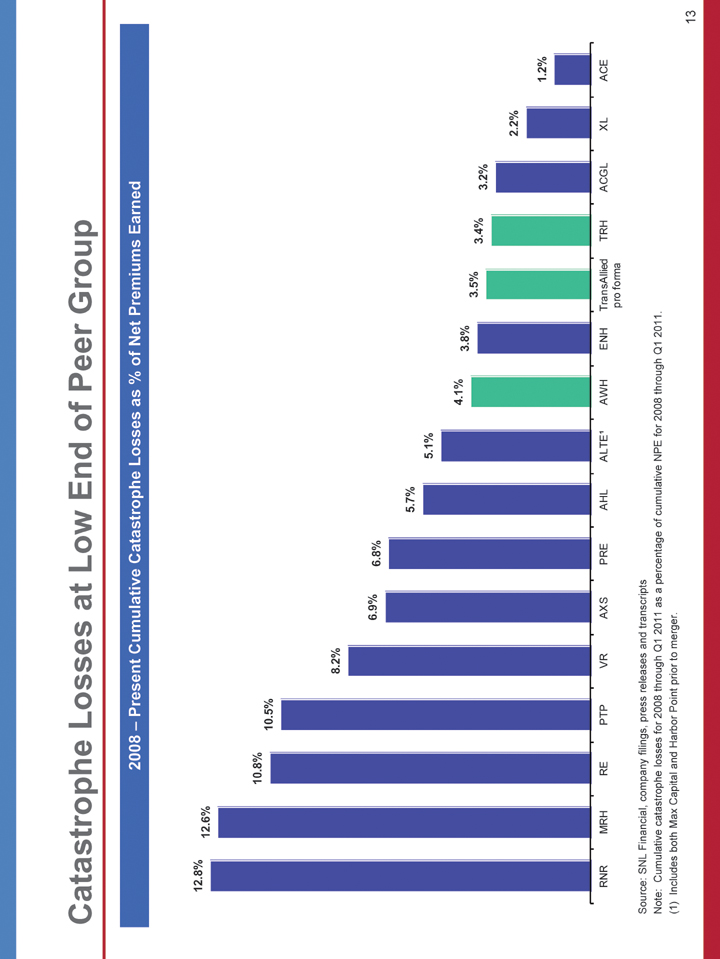

| Catastrophe Losses at Low End of Peer Group 2008 — Present Cumulative Catastrophe Losses as % of Net Premiums Earned 12.8% 12.6% 10.8% 10.5% 8.2% 6.9% 6.8% 5.7% 5.1% 4.1% 3.8% 3.5% 3.4% 3.2% 2.2% 1.2% RNR MRH RE PTP VR AXS PRE AHL ALTE1 AWH ENH TransAllied TRH ACGL XL ACE pro forma Source: SNL Financial, company filings, press releases and transcripts Note: Cumulative catastrophe losses for 2008 through Q1 2011 as a percentage of cumulative NPE for 2008 through Q1 2011. (1) Includes both Max Capital and Harbor Point prior to merger. 13 |

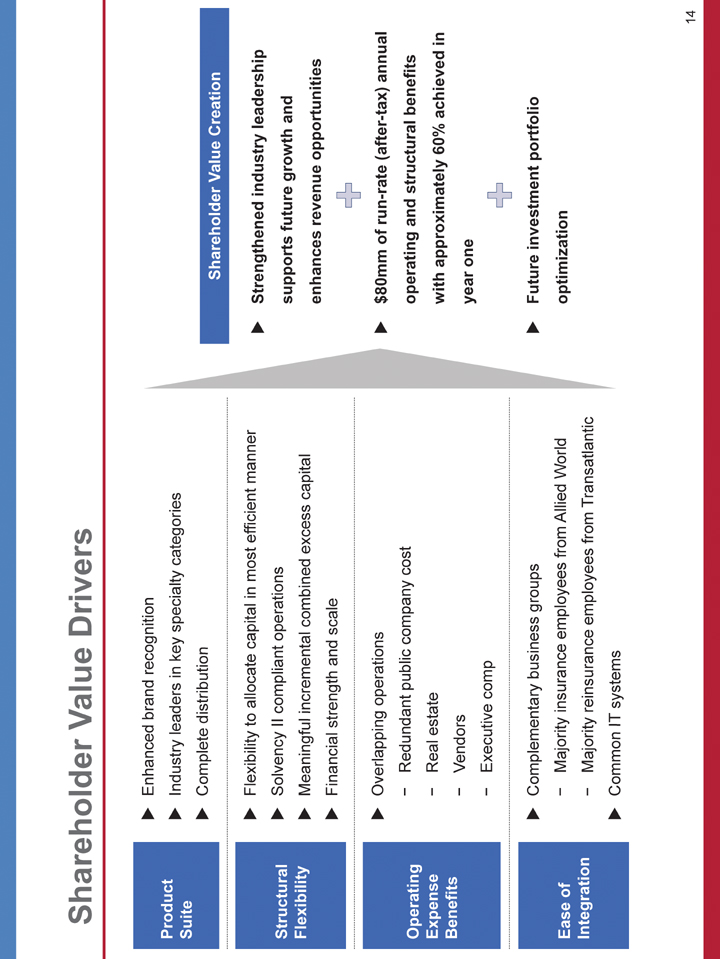

| Shareholder Value Drivers Enhanced brand recognition Product Industry leaders in key specialty categories Suite Complete distribution Shareholder Value Creation Flexibility to allocate capital in most efficient manner Strengthened industry leadership Structural Solvency II compliant operations supports future growth and Flexibility Meaningful incremental combined excess capital enhances revenue opportunities Financial strength and scale d Overlapping operations $80mm of run-rate (after-tax) annual — Redundant public company cost operating and structural benefits Operating Expense — Real estate with approximately 60% achieved in Benefits — Vendors year one - Executive comp Complementary business groups Future investment portfolio Ease of — Majority insurance employees from Allied World optimization Integration — Majority reinsurance employees from Transatlantic Common IT systems 14 |

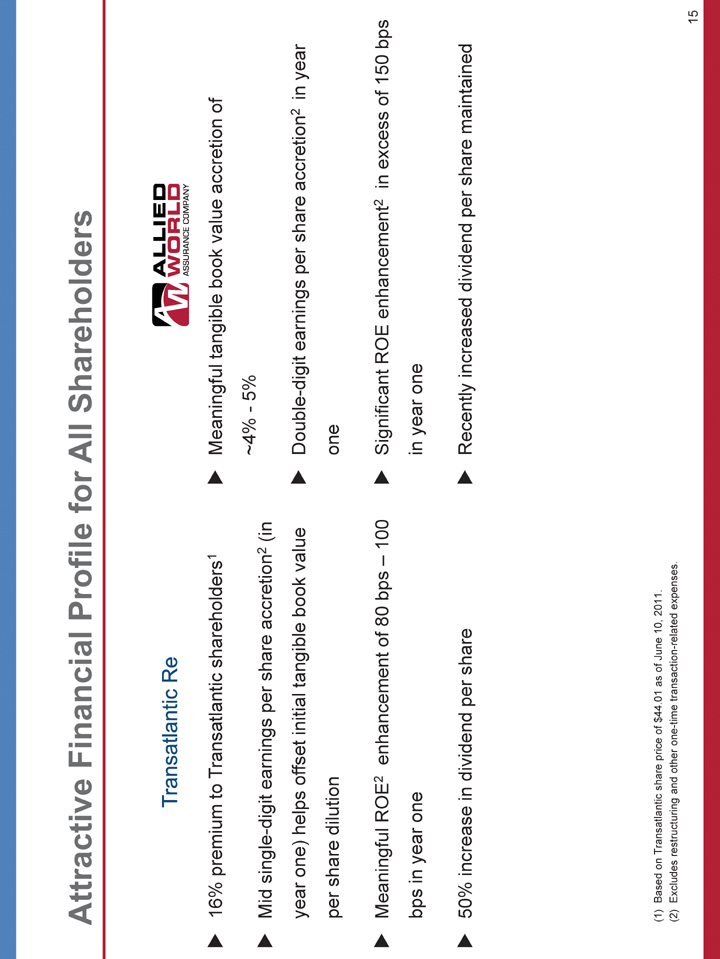

| Attractive Financial Profile for All Shareholders 16% premium to Transatlantic shareholders1 Meaningful tangible book value accretion of ~4% — 5% Mid single-digit earnings per share accretion2(in year one) helps offset initial tangible book value Double-digit earnings per share accretion2in year per share dilution one Meaningful ROE2enhancement of 80 bps — 100 Significant ROE enhancement2in excess of 150 bps bps in year one in year one 50% increase in dividend per share Recently increased dividend per share maintained (1) Based on Transatlantic share price of $44.01 as of June 10, 2011. (2) Excludes restructuring and other one-time transaction-related expenses. 15 |

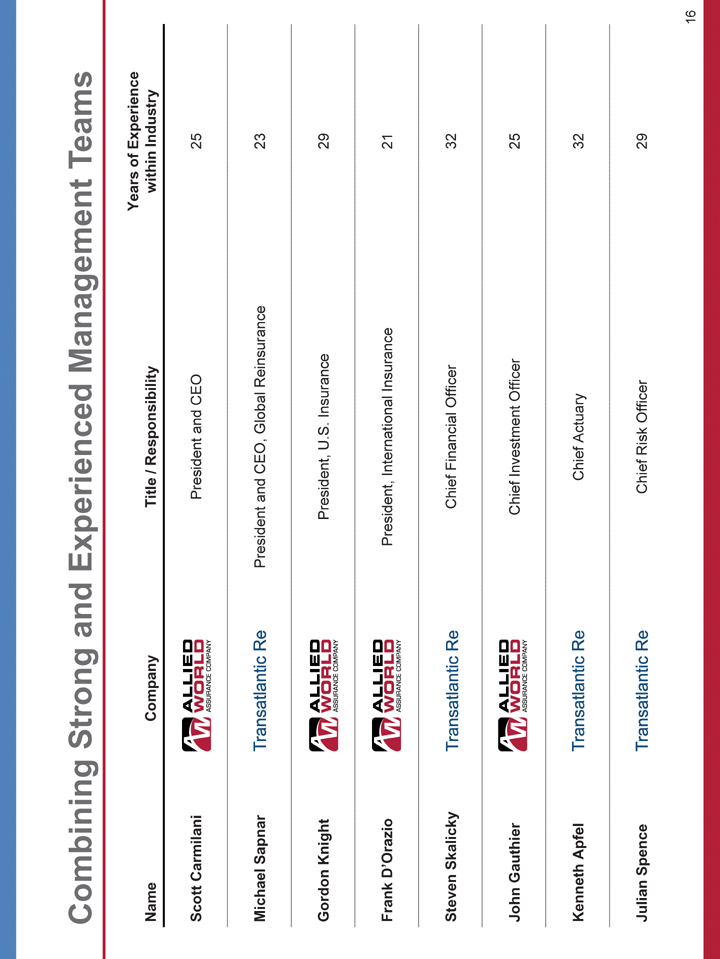

| Combining Strong and Experienced Management Teams Years of Experience Name Company Title / Responsibility within Industry Scott Carmilani President and CEO 25 Michael Sapnar President and CEO, Global Reinsurance 23 Gordon Knight President, U.S. Insurance 29 Frank D’Orazio President, International Insurance 21 Steven Skalicky Chief Financial Officer 32 John Gauthier Chief Investment Officer 25 Kenneth Apfel Chief Actuary 32 Julian Spence Chief Risk Officer 29 16 |

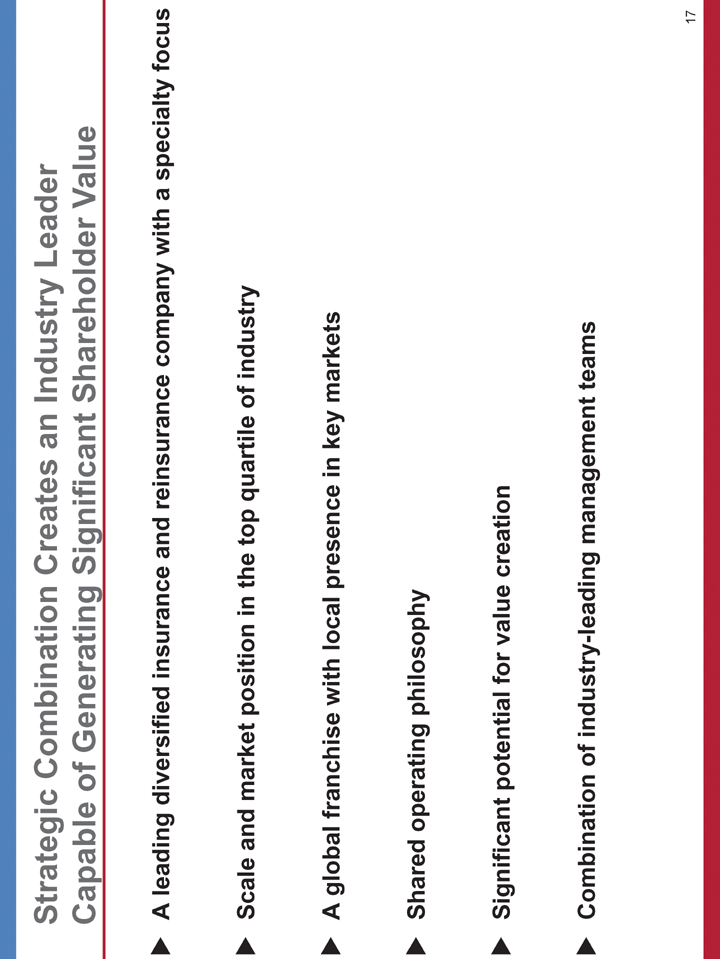

| Strategic Combination Creates an Industry Leader Capable of Generating Significant Shareholder Value A leading diversified insurance and reinsurance company with a specialty focus Scale and market position in the top quartile of industry A global franchise with local presence in key markets Shared operating philosophy Significant potential for value creation Combination of industry-leading management teams 17 |