Table of Contents

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

ANNUAL REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2003

Commission File Number: 333-14168

Petrobras International Finance Company

(Exact name of registrant as specified in its charter)

Cayman Islands

(Jurisdiction of incorporation or organization)

Anderson Square Building

P.O. Box 714

George Town, Grand Cayman

Cayman Islands

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act: None

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

Title of each class:

U.S.$500,000,000 9.125% Senior Notes due 2007

U.S.$450,000,000 9.875% Senior Notes due 2008

U.S.$400,000,000 9.00% Global Step-Up Notes due 2008

U.S.$600,000,000 9.750% Senior Notes due 2011

U.S.$750,000,000 9.125% Global Notes due 2013

U.S.$750,000,000 8.375% Global Notes due 2018

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock

as of the close of the period covered by this Annual Report:

At December 31, 2003, there were outstanding:

50,000 common shares of Petrobras International Finance Company

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ¨ Item 18 x

Table of Contents

| Page | ||||

| 1 | ||||

| 1 | ||||

| 1 | ||||

| 1 | ||||

Item 1. | Identity of Directors, Senior Management, and Advisers | 2 | ||

Item 2. | Offer Statistics and Expected Timetable | 2 | ||

Item 3. | Key Information | 3 | ||

Item 4. | Information on the Company | 15 | ||

Item 5. | Operating and Financial Review and Prospects | 21 | ||

Item 6. | Directors, Senior Management and Employees | 28 | ||

Item 7. | Major Shareholders and Related Party Transactions | 30 | ||

Item 8. | Financial Information | 31 | ||

Item 9. | The Offer and Listing | 32 | ||

Item 10. | Additional Information | 32 | ||

Item 11. | Quantitative and Qualitative Disclosures About Market Risk | 44 | ||

Item 12. | Description of Securities Other than Equity Securities | 45 | ||

Item 13. | Defaults, Dividend Arrearages and Delinquencies | 45 | ||

Item 14. | Material Modifications to the Rights of Security Holders and Use of Proceeds | 45 | ||

Item 15. | Controls and Procedures | 45 | ||

Item 16A. | Audit Committee Financial Expert | 46 | ||

Item 16B. | Code of Ethics | 46 | ||

Item 16C. | Principal Accountant Fees and Services | 46 | ||

Item 17. | Financial Statements | 46 | ||

Item 18. | Financial Statements | 47 | ||

Item 19. | Exhibits | 47 | ||

| 52 | ||||

| 53 | ||||

| 53 | ||||

1

Table of Contents

INCORPORATION OF CERTAIN DOCUMENTS BY REFERENCE

The annual report on Form 20-F of Petróleo Brasileiro S.A.—PETROBRAS (“Petrobras”) for the year ended December 31, 2003, as first filed with the United States Securities and Exchange Commission (the “SEC”) (Commission file No. 1-15106) on June 30, 2004, is incorporated by reference in this annual report.

Many statements made in this annual report under the captions “Item 3. Risk Factors,” “Item 4. History and Development of the Company—Business Overview” relating to the operation and performance of Petrobras International Finance Company, or PIFCo, and Petrobras and under the caption “Item 5. Operating and Financial Review and Prospects” and elsewhere are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, that are not based on historical facts and are not assurances of future results. Many of the forward-looking statements contained in this annual report may be identified by the use of forward-looking words, such as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimate” and “potential,” among others. These forward-looking statements are subject to certain risks and uncertainties, including, but not limited to:

| • | our ability to obtain financing; |

| • | changes in Petrobras’ use of our services for market purchases of crude oil and oil products; |

| • | changes in Brazilian foreign exchange control regulations, which may prevent Petrobras from making payment to us in U.S. dollars; and |

| • | changes in other applicable government regulations. |

All forward-looking statements attributed to us or a person acting on our behalf are expressly qualified in their entirety by this cautionary statement, and you should not place reliance on any forward-looking statement contained in this annual report.

The annual report on Form 20-F of Petrobras for the fiscal year ended December 31, 2003, incorporated herein by reference, also contains forward-looking statements. For a discussion of the factors affecting the forward-looking statements contained in Petrobras’ annual report, see “Forward-Looking Statements” on page one of that document.

Unless the context otherwise requires, the terms “PIFCo,” “we,” “us,” and “our” refer to Petrobras International Finance Company and its subsidiaries. When we refer to Petrobras, we refer to Petrobras and its consolidated subsidiaries, including us.

A glossary of petroleum industry terms, a table of abbreviations and a conversion table are presented beginning on page 52.

PRESENTATION OF FINANCIAL INFORMATION

References to “Real,” “Reais” or “R$” in this annual report are to Brazilian Reais and references to “U.S. dollars” or “U.S.$” are to United States dollars.

Our functional currency is the U.S. dollar. Substantially all of our sales are made in U.S. dollars and all of our debt is denominated in U.S. dollars. Accordingly, our audited consolidated financial statements as of December 31, 2003 and 2002, and for each of the three years in the period ended December 31, 2003, and the accompanying notes contained in this annual report have been presented in U.S. dollars and prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”) and include our wholly-owned subsidiaries: Petrobras Europe Limited, Petrobras Finance Limited, Bear Insurance Company Limited – BEAR (which Brasoil, a Petrobras subsidiary, transferred to us in January 2003) and Petrobras Netherlands B.V. (which we transferred to Petrobras in January 2003). See Item 5. “Operating and Financial Review and Prospects” and Note 1 to our audited consolidated financial statements.

1

Table of Contents

Certain figures included in this annual report have been subject to rounding adjustments; accordingly, figures shown as totals in certain tables may not be an arithmetic aggregation of the figures that precede them.

Item 1. Identity of Directors, Senior Management, and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

2

Table of Contents

SELECTED FINANCIAL DATA

The following table of selected financial data is presented in U.S. dollars and prepared in accordance with U.S. GAAP. The data for each of the five years in the period ended December 31, 2003 have been derived from our audited consolidated financial statements, which were audited by Ernst & Young Auditores Independentes S/S for the year ended December 31, 2003 and by PricewaterhouseCoopers Auditores Independentes for each of the years ended December 31, 2002, 2001, 2000 and 1999.

The information below should be read in conjunction with, and is qualified in its entirety by reference to, our audited consolidated financial statements and the accompanying notes and “Item 5. Operating and Financial Review and Prospects.”

| For the Year Ended December 31, | ||||||||||||||||||||

| 2003 | 2002 | 2001 | 2000 | 1999 | ||||||||||||||||

| (in millions of U.S. dollars) | ||||||||||||||||||||

| Income Statement Data: | ||||||||||||||||||||

Sales of crude oil and oil products and Services | $ | 6,975.5 | $ | 6,390.2 | $ | 6,260.5 | $ | 7,937.0 | $ | 4,728.0 | ||||||||||

Lease income(1) | — | 36.1 | 10.7 | — | — | |||||||||||||||

| 6,975.5 | 6,426.3 | 6,271.2 | 7,937.0 | 4,728.0 | ||||||||||||||||

Cost of sales | (6,920.1 | ) | (6,371.5 | ) | (6,253.0 | ) | (7,912.6 | ) | (4,723.8 | ) | ||||||||||

Lease expense(1) | — | (24.0 | ) | (10.5 | ) | — | — | |||||||||||||

Selling, general and administrative Expenses | (18.6 | ) | (1.2 | ) | (0.1 | ) | — | — | ||||||||||||

| (6,938.7 | ) | (6,396.7 | ) | (6,263.6 | ) | (7,912.6 | ) | (4,723.8 | ) | |||||||||||

Gross profit | 36.8 | 29.6 | 7.6 | 24.4 | 4.2 | |||||||||||||||

Financial income(2) | 442.9 | 219.6 | 158.8 | 221.6 | 158.4 | |||||||||||||||

Financial expense(3) | (482.7 | ) | (314.7 | ) | (187.1 | ) | (219.7 | ) | (142.2 | ) | ||||||||||

Gain on materials and equipment | — | — | 0.4 | — | — | |||||||||||||||

Net income (loss) | $ | (3.0 | ) | $ | (65.5 | ) | $ | (20.3 | ) | $ | 26.3 | $ | 20.4 | |||||||

Balance Sheet Data (end of period): | ||||||||||||||||||||

Cash and cash equivalents | $ | 1,262.0 | $ | 260.6 | $ | 48.6 | $ | 51.2 | $ | 49.4 | ||||||||||

Accounts receivable | ||||||||||||||||||||

Related parties | 5,064.5 | 4,837.1 | 2,583.7 | 3,011.2 | 2,839.7 | |||||||||||||||

Trade | 109.4 | 57.1 | 44.7 | 39.6 | 2.3 | |||||||||||||||

Notes receivable – related parties | 1,726.4 | 1,631.6 | 283.0 | |||||||||||||||||

Export Prepayment – related parties | 1,479.4 | 751.2 | 751.2 | |||||||||||||||||

Total assets | 10,196.6 | 8,697.3 | 4,277.8 | 3,244.5 | 2,900.0 | |||||||||||||||

Trade accounts payable | ||||||||||||||||||||

Related parties | 271.0 | 292.0 | 288.1 | 70.8 | 148.1 | |||||||||||||||

Other | 349.0 | 281.1 | 231.0 | 593.2 | 306.8 | |||||||||||||||

Notes payable - related parties | 2,442.8 | 3,688.2 | 334.6 | 1,716.6 | 1,628.9 | |||||||||||||||

Short-term financing and current portion of long-term debt | 1,076.4 | 367.5 | 990.4 | 530.4 | 741.5 | |||||||||||||||

Long-term debt | 5,825.3 | 3,248.7 | 2,335.0 | 245.0 | — | |||||||||||||||

Capital lease obligations | — | 601.7 | ||||||||||||||||||

Total stockholders’ equity | 94.8 | 43.9 | 49.4 | 9.7 | 21.5 | |||||||||||||||

Total liabilities and stockholders’ equity | 10,196.6 | 8,697.3 | 4,277.8 | 3,244.5 | 2,900.0 | |||||||||||||||

| (1) | As a result of the transfer of PNBV, our leasing subsidiary, to Petrobras, we had no lease income or lease expense in 2003. |

| (2) | Financial income represents primarily the imputed interest realized from our sales of crude oil and oil products to Petrobras. |

| (3) | Financial expense consists primarily of costs incurred by us in financing our activities in connection with the importation by Petrobras of crude oil and oil products. |

3

Table of Contents

RISK FACTORS

Risks Relating to Our Company

We may not earn enough money from our own operations to meet our debt obligations.

We are a direct wholly-owned subsidiary of Petrobras incorporated in the Cayman Islands as an exempted company with limited liability. Accordingly, our financial position and results of operations are largely affected by decisions of our parent company. We have limited operations consisting principally of the purchase of crude oil and oil products from third parties and the resale of those products to Petrobras, with financing for such operations provided by Petrobras as well as third-party credit providers. We also resell crude oil and oil products to third parties on a limited basis. Our ability to pay interest, principal and other amounts due on our outstanding and future debt obligations will depend upon a number of factors, including:

| • | Petrobras’ financial condition and results of operations; |

| • | the extent to which Petrobras continues to use our services for market purchases of crude oil and oil products; |

| • | Petrobras’ willingness to continue to make loans to us and provide us with other types of financial support; |

| • | our ability to access financing sources, including the international capital markets and third-party credit facilities; and |

| • | our ability to transfer our financing costs to Petrobras. |

In the event of a material adverse change in Petrobras’ financial condition or results of operations or in Petrobras’ financial support of us, we may not have sufficient funds to repay all amounts due on our indebtedness. See “Risks Relating to Petrobras” for a more detailed description of certain risks that may have a material adverse impact on Petrobras’ financial condition or results of operations and therefore affect our ability to meet our debt obligations.

If Brazilian law restricts Petrobras from paying us in U.S. dollars, we may have insufficient U.S. dollar funds to make payments on our debt obligations.

We obtain substantially all of our funds from Petrobras’ payments in U.S. dollars for crude oil that it purchases from us. In order to remit U.S. dollars to us, Petrobras must comply with Brazilian foreign exchange control regulations, including preparing specified documentation to be able to obtain U.S. dollar funds for payment to us. If Brazilian law were to impose additional restrictions, limitations or prohibitions on Petrobras’ ability to convert Reais into U.S. dollars, we may not have sufficient U.S. dollar funds available to make payment on our debt obligations. Such restrictions could also have a material adverse effect on the Brazilian economy or Petrobras’ business, financial condition and results of operations.

We may be limited in our ability to pass on our financing costs.

We are principally engaged in the purchase of crude oil and oil products for resale to Petrobras, as described above. At any time, we may incur indebtedness related to such purchases and/or obtain financing from Petrobras or third-party creditors. At December 31, 2003, approximately 13.8% of our indebtedness was floating-rate debt denominated in U.S. dollars not having the benefit of Petrobras’ standby purchase obligation or other support. Petrobras is in the process of changing its risk management processes, including those which may affect us, but neither Petrobras nor we have yet entered into derivative contracts or made other arrangements to hedge against interest rate risk. We have historically passed on our financing costs to Petrobras by selling crude oil and oil products to Petrobras at a premium to compensate for our financing costs. Although we and Petrobras intend for this practice to continue in the future, we cannot assure you that this practice will continue. Our inability to transfer our financing costs to Petrobras could have a material adverse effect on our business and on our ability to meet our debt obligations.

4

Table of Contents

Risks Relating to Petrobras’ Operations

Substantial or extended declines in the prices of crude oil and oil products may have a material adverse effect on Petrobras’ operations.

Petrobras does not, and will not, have control over the factors affecting international prices for crude oil and oil products. The average prices of Brent crude, an international benchmark oil, were approximately U.S.$28.84 per barrel for 2003, U.S.$25.02 per barrel for 2002 and U.S.$24.44 per barrel for 2001.

Changes in crude oil prices typically result in changes in prices for oil products. Lower crude oil prices have various effects on Petrobras, including decreasing its net operating revenues, net income and cash flows. In comparison, higher crude oil prices generally lead to increases in Petrobras’ net operating revenues, net income and cash flows. However, even during periods of high crude oil prizes, depending on the behavior of demand, Petrobras may not be able to pass through higher prizes to consumers.

Historically, international prices for crude oil and oil products have fluctuated widely as a result of many factors. These factors include:

| • | global and regional economic and political developments in crude oil producing regions, particularly in the Middle East; |

| • | the ability of OPEC and other crude oil producing nations to set and maintain crude oil production levels and prices; |

| • | other actions taken by major crude oil producing or consuming countries; |

| • | global and regional supply and demand for crude oil and oil products; |

| • | competition from other energy sources; |

| • | domestic and foreign government regulations; |

| • | weather conditions; |

| • | war; and |

| • | terrorism. |

Until January 2, 2002, the prices Petrobras was allowed to charge for crude oil and oil products (and, as a result, its recorded prices for the calculation of net operating revenues) were determined on the basis of a pricing formula established by the Brazilian government designed to reflect changes in the Real/U.S. dollar exchange rate and international market prices for relevant benchmark products. As of January 2, 2002, the crude oil and oil products markets in Brazil were deregulated in their entirety.

Petrobras expects continued volatility and uncertainty in international prices for crude oil and oil products. Substantial or extended declines in international crude oil prices may have a material adverse effect on Petrobras’ business, results of operations and financial condition and the value of its proved reserves.

Because of changes in government regulations, Petrobras faces increased competition and may lose market share.

The Brazilian government eliminated all price controls on crude oil and oil products in early 2002. Prices remain regulated, however, for natural gas and electricity. These controls could have an adverse effect on Petrobras’ revenues from these business activities.

The changes in government regulation have enabled multinational and regional oil companies to enter the Brazilian energy market. Competition in Petrobras’ upstream and downstream activities has increased and will increase further, as existing and new participants expand their activities as a result of these regulatory changes.

Although Petrobras’ prices for oil products are based on international prices, in periods of high international prices or sharp devaluations of the Real, Petrobras may not be able to adjust its prices in Reais sufficiently to maintain parity with international prices.

Since the Brazilian government’s elimination of all price controls on crude oil and oil products in January 2002, there have been periods of high international prices or sharp devaluations of the Real when Petrobras has been unable to increase prices in Reais sufficiently to maintain parity with international prices. While Petrobras does not have an obligation to supply the Brazilian market,

5

Table of Contents

during periods when the local prices of oil products were below prevailing international prices, Petrobras’ competitors were unwilling to supply the local market. In order to ensure adequate supply of oil products in Brazil, Petrobras sold oil products below prevailing international prices.

As a result of deregulation of the Brazilian market, and the elimination of import tariffs in particular, Petrobras’ competitors can sell products in the Brazilian market at parity with international prices. In light of this increased competition, Petrobras has less flexibility to maintain local prices above international prices to compensate for revenues not realized in periods in which it sold oil products below prevailing international market prices.

Petrobras may be required to sell some of its refining capacity in Brazil.

Petrobras presently owns 98.6% of the existing refining capacity in Brazil. Petrobras plans to upgrade its present refineries and may build new refineries in Brazil, sell participation interests in its present refineries to new partners or engage in asset swaps, as it did through its business combination in 2001 involving assets of Repsol-YPF S.A. Although Petrobras is not presently subject to any requirement to divest any assets, and the Brazilian government has not made any proposal in that respect, it is possible that Petrobras will be required to divest a portion of its refining capacity or other assets in the future. Any such divestiture could have a material adverse effect on Petrobras’ financial condition and results of operations.

Petrobras’ ability to achieve its growth objectives depends on its ability to gain access to additional reserves.

Petrobras’ ability to achieve its growth objectives is highly dependent upon its level of success in finding, acquiring or gaining access to additional reserves, as well as successfully developing current reserves. In general, the volume of production from crude oil and natural gas properties declines as reserves are depleted, with the rate of decline depending on reservoir characteristics. Unless Petrobras conducts successful exploration and development activities or acquires properties containing proved reserves, or both, its proved reserves will decline as reserves are extracted.

Exploratory drilling involves numerous risks, including the risk that Petrobras will not discover commercially productive oil or natural gas reserves.

Petrobras’ exploration and development activities expose it to the inherent risks of drilling, including the risk that Petrobras will not discover commercially productive crude oil or natural gas reserves. The costs of drilling, completing and operating wells are often uncertain and numerous factors beyond Petrobras’ control (such as unexpected drilling conditions, equipment failures or accidents and shortages or delays in the availability of drilling rigs and the delivery of equipment) may cause drilling operations to be curtailed, delayed or cancelled. Petrobras’ future drilling, exploration and acquisition activities may not be successful and, if unsuccessful, could harm its future results of operations and financial condition.

Petrobras’ crude oil and natural gas reserve estimates involve some degree of uncertainty and may prove to be incorrect over time.

The proved crude oil and natural gas reserves set forth in Petrobras’ annual report are its estimated quantities of crude oil, natural gas and natural gas liquids that geological and engineering data demonstrate with reasonable certainty to be recoverable from known reservoirs under existing economic and operating conditions (i.e., prices and costs as of the date the estimate is made). Petrobras’ proved developed crude oil and natural gas reserves are reserves that can be expected to be recovered through existing wells with existing equipment and operating methods. Although 91% of Petrobras’ domestic reserves are independently certified, there are uncertainties in estimating quantities of proved reserves related to prevailing crude oil and natural gas prices applicable to Petrobras’ production, which may lead Petrobras to make revisions to its reserve estimates.

Petrobras’ equipment, facilities and operations are subject to numerous environmental and health regulations which have become more stringent in the recent past and may result in increased liabilities and increased capital expenditures.

Petrobras’ activities are subject to a wide variety of federal, state and local laws, regulations and permit requirements relating to the protection of human health and the environment, both in Brazil and in other jurisdictions in which Petrobras operates. In Brazil, Petrobras could be exposed to civil penalties, criminal sanctions and closure orders for non-compliance with these environmental regulations, which, among other things, limit or prohibit emissions or spills of toxic substances produced in connection with its operations. Waste disposal and emissions regulations may require Petrobras to clean up or retrofit its facilities at substantial cost and could result in substantial liabilities. TheInstituto Brasileiro do Meio Ambiente dos Recursos Naturais Renováveis(Brazilian Institute of the Environment and Renewable Natural Resources, or IBAMA) routinely inspects Petrobras’ oil platforms in the Campos Basin, and may impose fines, restrictions on operations or other sanctions in connection with its inspections.

6

Table of Contents

Petrobras spent approximately U.S.$750 million in 2003, U.S.$466 million in 2002 and U.S.$473 million in 2001 to comply with environmental laws and to implement improvements in its environmental practices. Because environmental regulations have become more stringent in Brazil and in other jurisdictions where Petrobras operates, it is probable that Petrobras’ capital expenditures for compliance with environmental regulations and to effect improvements in health, safety and environmental practices may increase substantially in the future. In addition, due to the possibility of unanticipated regulatory or other developments, the amount and timing of future environmental expenditures may vary widely from those currently anticipated. The amount of investments Petrobras makes in any given year is subject to limitations by the Brazilian government. Accordingly, expenditures required for compliance with environmental regulation could result in reductions in other strategic investments that Petrobras has planned, and any such reduction may have a material adverse effect on Petrobras’ results of operations or financial condition.

In the past, significant oil spills have occurred and Petrobras has incurred, and may continue to incur, liabilities in connection with oil spills, including clean up costs, government fines and potential lawsuits.

From time to time, oil spills occur in connection with Petrobras’ operations. In 2003, Petrobras experienced spills totaling 73,000 gallons of crude oil, as compared to 52,000 gallons in 2002 and 691,000 gallons in 2001. As a result of certain of Petrobras’ spills, it was fined by various state and federal environmental agencies, named the defendant in several civil and criminal suits and remains subject to several investigations and potential civil and criminal liabilities. These or any future oil spills may have a material adverse effect on Petrobras’ financial condition or results of operations. Accordingly, if one or more of the potential liabilities resulting from these oil spills were to result in an actual fine or civil or criminal liability, Petrobras’ operations and financial condition could be negatively affected.

Petrobras may incur losses and spend time and money defending pending litigation and arbitration.

Petrobras is currently a party to numerous legal proceedings relating to civil, administrative, environmental, labor and tax claims filed against it. These claims involve substantial amounts of money and other remedies. Several individual disputes account for a significant part of the total amount of claims against Petrobras. Petrobras’ audited financial statements as of December 31, 2003 include reserves totaling U.S.$260 million as of that date, for probable and reasonably estimable losses and expenses it may incur in connection with all of its pending litigation and an additional provision of U.S.$95 million related to various tax assessments received from theInstituto Nacional de Seguridade Social(National Security Institute, or INSS).

In the event that a number of the claims that Petrobras considers to represent remote or reasonably possible risks of loss were to be decided against it, or in the event that the losses estimated turn out to be higher than the reserves made, the aggregate cost of unfavorable decisions could have a material adverse effect on Petrobras’ financial condition and results of operations. Additionally, Petrobras’ management may be required to direct its time and attention to defending these claims, which could preclude them from focusing on its core business. Depending on the outcome, certain litigation, including matters involving its platforms and asset swaps, could result in restrictions on Petrobras’ operations and have a material adverse effect on certain of its businesses.

If a State of Rio de Janeiro law imposing ICMS on oil upstream activities is applied to Petrobras, its results of operations and financial condition may be adversely affected.

In June 2003, the State of Rio de Janeiro enacted a law imposing theImposto sobre Circulação de Mercadorias e Serviços (state sales tax, or ICMS) on upstream activities. Although the law is technically in force, the government of the State of Rio de Janeiro has yet to apply it. Currently, the ICMS is assessed at the point of sale from refineries to distributors but not at the wellhead level. As a result, the tax is mainly collected in the eight states where Petrobras’ refineries are located (Rio de Janeiro, São Paulo, Rio Grande do Sul, Paraná, Minas Gerais, Amazonas, Ceará and Bahia). If the State of Rio de Janeiro applies the law to Petrobras, it would change the point of collection of a portion of the ICMS from the refinery level to the wellhead level of production in the State of Rio de Janeiro. As a result, Petrobras would be unable to utilize part of the taxes imposed at the wellhead level in Rio de Janeiro to offset taxes that are imposed at the refinery level in other states, and therefore would have paid taxes on the same oil products at both production and refining levels. The attorney general has filed a lawsuit with the Brazilian Supreme Court challenging the constitutionality of the ICMS legislation. If the law is declared constitutional and the State of Rio de Janeiro applies the law to Petrobras, the amount of ICMS that Petrobras would be required to pay to the State of Rio de Janeiro could increase by approximately R$5.4 billion (U.S.$1.9 billion) per year. This increase could have a material adverse effect on Petrobras’ results of operations and financial condition.

7

Table of Contents

A final judicial ruling upholding the view of the Brazilian Revenue Service of Rio de Janeiro that drilling and production platforms may no longer be classified as sea-going vessels will increase the amount of taxes Petrobras’ pays, and such an increase may have a material adverse effect on Petrobras’ results of operations and financial condition.

The Rio de Janeiro branch of the Brazilian Revenue Service (Secretaria de Receita Federal) has asserted that, under Brazilian law, drilling and production platforms may not be classified as sea-going vessels and therefore should not be chartered but leased. Based on this interpretation of Brazilian law, overseas remittances for charter payments would be reclassified as lease payments, and would be subject to withholding tax at the rate of 15%.

The Brazilian Revenue Service has filed two tax assessments against Petrobras in connection with the withholding tax (IRRF) on foreign remittances of payments related to the charter of vessels of movable platform types. On February 17, 2003, the Brazilian Revenue Service served Petrobras with a tax assessment notice for R$93 million (U.S.$32 million) covering disputed taxes for 1998. On June 27, 2003, the Brazilian Revenue Service served Petrobras with a tax assessment notice for R$3,064 million (U.S.$1,066 million) covering disputed taxes for the period from 1999 to 2002. Petrobras recently received two unfavorable rulings from the Brazilian Revenue Service with respect to these tax assessments, and has appealed these rulings to a higher administrative court.

Petrobras believes that Brazilian law supports its view that drilling and production platforms may be classified as sea-going vessels. However, in the event that a final judicial ruling supports the Brazilian Revenue Service’s position, the taxes Petrobras pays in connection with its drilling and production platforms would significantly increase, and such an increase could have a material adverse effect on its level of investments and, therefore, on its results of operations and financial condition.

Labor disputes, strikes, work stoppages and protests could lead to increased operating costs.

All of Petrobras’ employees, other than its maritime employees, are subject to a collective bargaining agreement with the Oil Workers’ Unified Federation, which was signed on November 4, 2003, and is retroactive to September 1, 2003. This collective bargaining agreement will expire on August 31, 2004. Petrobras negotiated a separate collective bargaining agreement with the maritime employees’ union. The agreement was signed on January 30, 2004, is retroactive to November 1, 2003 and will expire on October 31, 2004.

From time to time, Petrobras has been subject to strikes and work stoppages. In 2001, its oil workers began a five-day strike, which led to a decrease in crude oil production of four million barrels of oil equivalent per day. If Petrobras’ workers were to strike, the resulting work stoppages could have an adverse effect on Petrobras, as it does not carry insurance for losses incurred as a result of business interruptions of any nature, including business interruptions caused by labor action. As a result, Petrobras’ financial condition and results of operations could be adversely affected by future strikes, work stoppages, protests or similar activities.

Petrobras’ participation in the domestic power market has generated losses, and the Brazilian regulatory environment for energy remains uncertain.

Consistent with the global trend of other major oil and gas companies and to secure demand for its natural gas, Petrobras participates in the domestic power market. Despite a number of incentives introduced by the former Brazilian government to promote the development of thermoelectric power plants, development of such plants by private investors has been slow to progress. Petrobras has invested in 11 (5 in operation and 6 under construction or development) of the 39 gas-fired power generation plants being built or proposed to be built in Brazil under the program to promote the development of thermoelectric plants, known as thePrograma Prioritário de Termoeletricidade(Thermoelectric Priority Program, or PPT). Petrobras invests in some of these plants with partners, many of whom may have power purchase agreements with the plants. Petrobras has had contractual disputes in connection with these investments and other disputes may occur. Depending on the outcome of any such disputes, they could have an adverse economic impact on Petrobras, including on the profitability of its investments.

In 2002, Congress passed a law increasing government intervention in the domestic power market, and in 2003 the current administration proposed a new regulatory model for the energy sector. The New Industry Model Law was enacted on March 16, 2004, but because the new law remains subject to the enactment of decrees of the Brazilian government and implementing resolutions of the National Electric Energy Agency (ANEEL), many aspects of the regulatory environment for thermoelectric power remain uncertain, and it is not clear that thermoelectric power will remain a priority for the country.

8

Table of Contents

Petrobras has limited its investments in this area, but its participation in the domestic power market may never become profitable and may continue to adversely affect its operating results and financial condition.

Petrobras may not be able to obtain financing for all of its planned investments.

The Brazilian government maintains control over Petrobras’ budget and establishes limits on its investments and long-term debt. As a state-controlled entity, Petrobras must submit its proposed annual budgets to the Ministry of Planning, Budget and Management, the Ministry of Mines and Energy and the Brazilian Congress for approval. Petrobras is endeavoring to obtain financing that does not require Brazilian government approval, such as structured financings, but there can be no assurance that it will succeed. As a result, Petrobras may not be free to make all the investments it envisions, including those it has agreed to make to expand and develop its crude oil and natural gas fields. If Petrobras is unable to make these investments, its operating results and financial condition may be adversely affected. In addition, failure to make its planned investments in Brazil could hurt Petrobras’ competitive position in the Brazilian oil and gas sector, particularly as other companies enter the market.

Currency fluctuations could have a material adverse effect on Petrobras’ financial condition and results of operations, because most of Petrobras’ revenues are in Reais and a large portion of its liabilities are in foreign currencies.

The principal market for Petrobras’ products is Brazil, and over the last three fiscal years over 83% of Petrobras’ revenues have been denominated in Reais. A substantial portion of Petrobras’ indebtedness and some of its operating expenses and capital expenditures are, and are expected to continue to be, denominated in or indexed to U.S. dollars and other foreign currencies. In addition, during 2003, Petrobras imported U.S.$5.7 billion of crude oil and oil products, the prices of which were all denominated in U.S. dollars.

The Real depreciated 18.7% in 2001 and 52.3% in 2002 against the U.S. dollar, before appreciating 18.2% in 2003 against the U.S. dollar. As of June 15, 2004, the exchange rate of the Real to the U.S. dollar was R$3.138 per U.S.$1.00, representing a depreciation of approximately 6.7% in 2004 year-to-date. The value of the Real in relation to the U.S. dollar may continue to fluctuate and may include a significant depreciation of the Real against the U.S. dollar as occurred in 2002. Any future substantial devaluation of the Real may adversely affect Petrobras’ operating cash flows and its ability to meet its foreign currency-denominated obligations. You should consider this risk in light of past devaluations of the Real caused by inflationary and other pressures.

Petrobras is exposed to increases in prevailing market interest rates.

As of December 31, 2003, approximately 57% of Petrobras’ total indebtedness consisted of floating rate debt. Although Petrobras is changing its risk management practices, it has not yet entered into derivative contracts or made other arrangements to hedge against interest rate risk. Accordingly, if market interest rates (principally LIBOR) rise, Petrobras’ financing expenses will increase.

In the aftermath of the U.S. military action in Iraq there may be changes to the international oil markets, some of which could have an adverse effect on Petrobras.

Following the formal declaration of the end of hostilities in Iraq, the United Nations eliminated sanctions that had limited Iraq’s ability to participate in the international oil markets. As a result, it is expected that in the future, Iraq will substantially increase its production and export sales of crude oil and oil products. Given the uncertainty surrounding the circumstances under which Iraq’s oil industry will be managed over the next few years, it is impossible to predict the economic or political goals which the United States government or any other party controlling such industry will seek to achieve. The changes to the international oil markets that could result from Iraq’s full re-entry into such markets could have a material adverse effect on Petrobras’ financial condition and results of operations.

9

Table of Contents

Petrobras is not insured against business interruption for its Brazilian operations and most of Petrobras’ assets are not insured against war and terrorism.

Petrobras does not maintain coverage for business interruption for its Brazilian operations and does not insure most of its assets against war and terrorism. A terrorist attack or an operational incident could therefore have a material adverse effect on Petrobras’ financial condition or results of operations.

Petrobras is subject to substantial risks relating to its business and operations in Argentina and other South American countries.

Petrobras operates in Argentina through its subsidiary, Petrobras Energia Participaciones S.A. (PEPSA). Approximately 5.9% of Petrobras’ total crude oil and natural gas production and 3.5% of its proved crude oil and natural gas reserves were located in Argentina at December 31, 2003. As a result, PEPSA’s results of operations and financial condition, and consequently, Petrobras’ results of operations and financial condition, may be adversely affected by fluctuations in the Argentine economy, Argentine political instability, and governmental actions concerning the economy, including:

| • | the imposition of exchange controls, which could restrict the flow of capital out of Argentina and make it more difficult for PEPSA to service its non-Peso denominated debt, totaling U.S.$1,960 million at December 31, 2003; |

| • | the imposition of restrictions on hydrocarbon exports, which could decrease PEPSA’s U.S. dollar cash receipts and limit PEPSA’s ability to make payment on its foreign-currency denominated debt; |

| • | the devaluation of the Argentine Peso, which could adversely affect PEPSA’s results of operations, financial condition and ability to make payment on its foreign-currency denominated debt; |

| • | increases in export tax rates for crude oil and oil products, which could lead to a reduction in PEPSA’s export margins and cash flows; |

| • | the imposition of price controls restricting PEPSA’s ability to increase the price of energy and natural gas sold in the Argentine market, which could adversely affect PEPSA’s results of operations, financial condition and ability to make payment on its foreign-currency denominated debt; and |

| • | the pesification of utility rates, which combined with the devaluation of the Argentine Peso, resulted in payment defaults by three of PEPSA’s affiliated utility companies, TGS, CIESA (the parent of TGS), and Transener, and which could lead to defaults by other affiliated utility companies. |

Petrobras is also active in Venezuela, Ecuador, Colombia, Bolivia and Peru. Petrobras’ operations in Venezuela and Bolivia are its most significant international operations outside of Argentina. Petrobras’ operations in Venezuela represented 2.1% of its total production in barrels of oil equivalent in 2003 and 2.6% of its proved crude oil and natural gas reserves at December 31, 2003. Petrobras’ operations in Bolivia represented 1.5% of its total production in barrels of oil equivalent in 2003 and 2.9% of its proved crude oil and natural gas reserves at December 31, 2003. Accordingly, its operations may be negatively affected by:

| • | political, social and economic instability in Venezuela and Bolivia, including strikes and other forms of political protest, similar to those experienced by Venezuela during the first quarter of 2003 and by Bolivia during the third quarter of 2003; |

| • | increases in royalty payments from production in its Venezuelan fields; |

| • | any decisions by OPEC to decrease production volumes, as Venezuela is a member of OPEC, and Petrobras is subject to any decisions by OPEC to reduce production; |

| • | any decision by the Venezuelan government to modify the terms and conditions of PEPSA’s operating agreements in Venezuela; and |

| • | any decision by the Bolivian government to modify the existing energy regulatory framework, including the regulation and taxation of the oil and natural gas industry. |

10

Table of Contents

If one or more of the risks described above were to materialize, Petrobras may not achieve its strategic objectives in South America, resulting in a material adverse effect on its results of operations and financial condition.

The current Argentine economic, political and social crisis could adversely affect Petrobras’ Argentine operations.

From the last quarter of 1998 until 2003, the Argentine economy was in a recession marked by reduced levels of consumption and investment, increased unemployment, declining gross domestic product, capital flight and a suspension of payments on its approximately U.S.$95 billion of sovereign debt owed to private creditors. Argentina’s GDP contracted by 4.4% in 2001 and 10.9% in 2002.

On December 1, 2001, the Argentine government led by President Fernando de la Rúa effectively froze bank deposits and introduced exchange controls restricting capital outflows. The measures were perceived as further paralyzing the economy for the benefit of the banking sector and caused a sharp rise in social discontent, ultimately triggering public protests, outbreaks of violence and the looting of stores throughout Argentina. On December 20, 2001, President Fernando de la Rúa resigned, and since then, Argentina has had several presidents, including President Eduardo Duhalde, who held office from January 2002 to May 2003. During his term, President Duhalde and his government undertook a number of far-reaching initiatives, including:

| • | ratifying the suspension of payment of certain of Argentina’s sovereign debt; |

| • | amending Argentina’s Convertibility Law to allow the exchange rate of the Argentine Peso to float, breaking the Peso’s decade-old one-to-one relationship to the U.S. dollar, and resulting in a 66.4% decline in the value of the Peso against the U.S. dollar from January 7, 2002 to March 31, 2003; |

| • | converting certain U.S. dollar-denominated debts into peso-denominated debts at a one-to-one exchange rate and U.S. dollar-denominated bank deposits into peso-denominated bank deposits at an exchange rate of 1.4 Argentine Pesos per U.S.$1.00; |

| • | restructuring bank deposits and maintaining restrictions on bank withdrawals; |

| • | enacting an amendment to the Argentine Central Bank’s charter to (i) allow it to print currency in excess of the amount of the foreign reserves it holds, (ii) make short-term advances to the Argentine federal government and (iii) provide financial assistance to financial institutions with liquidity constraints or solvency problems; |

| • | imposing restrictions on transfers of funds abroad subject to certain exceptions; and |

| • | requiring the deposit into the banking system of foreign currency earned from exports, subject to certain exceptions. |

On May 25, 2003, a new president, Néstor Kirchner, took office. His current term will expire on December 10, 2007. There remains uncertainty as to the nature and scope of the measures to be adopted by Mr. Kirchner’s government to address many of the country’s unresolved economic problems, including the ongoing renegotiation of the country’s public debt.

During 2003, some economic indicators of the Argentine economy began to stabilize. In 2003, GDP grew by approximately 8.7%, inflation remained below 4%, consumption and investment increased and the peso appreciated significantly against the U.S. dollar. Nevertheless, this return to growth and partial stabilization are recent developments and may not be sustainable. These developments must be viewed against the significant declines preceding 2003 and against the substantial continuing uncertainties in Argentina’s economic and legal environment, including the renegotiation of the country’s external public debt and public utility contracts, restructuring of the financial system and redesigning of the federal fiscal regime. We cannot be certain that the economy will not suffer additional shocks.

Over the last few years, Argentina has also been afflicted by an energy crisis. In May 2002, the Argentine government declared a state of emergency in the supply of hydrocarbons in Argentina. Subsequently, in March 2004, Argentina’s Secretary of Energy issued a resolution pursuant to which limits on natural gas exports may be imposed and, in fact, some limits have already been imposed. Further Argentine political instability, fluctuations in the Argentine economy and governmental actions concerning the economy could adversely affect Petrobras’ operations in Argentina and may have a material adverse impact on its results of operations and financial condition.

11

Table of Contents

Risks Relating to the Relationship between Petrobras and the Brazilian Government

The Brazilian government, as Petrobras’ controlling shareholder, may cause Petrobras to pursue certain macroeconomic and social objectives that may have an adverse effect on its results of operations and financial condition.

The Brazilian government, as Petrobras’ controlling shareholder, has pursued, and may pursue in the future, certain of its macroeconomic and social objectives through Petrobras. Brazilian law requires the Brazilian government to own a majority of Petrobras’ voting stock, and so long as it does, the Brazilian government will have the power to elect a majority of the members of Petrobras’ board of directors and, through them, a majority of the executive officers who are responsible for Petrobras’ day-to-day management. As a result, Petrobras may engage in activities that give preference to the objectives of the Brazilian government rather than to its own economic and business objectives. In particular, Petrobras continues to assist the Brazilian government to ensure that the supply of crude oil and oil products in Brazil meets Brazilian consumption requirements. Accordingly, Petrobras may continue to make investments, incur costs and engage in sales on terms that may have an adverse effect on its results of operations and financial condition.

If the Brazilian government reinstates controls over the prices Petrobras can charge for crude oil and oil products, such price controls could affect Petrobras’ financial condition and results of operations.

In the past, the Brazilian government set prices for crude oil and oil products in Brazil, often below prevailing prices on the world oil markets. These prices involved elements of cross-subsidy among different oil products sold in various regions in Brazil. The cumulative impact of this price regulation system on Petrobras is recorded as an asset on Petrobras’ balance sheet under the line item “Petroleum and Alcohol Account-Receivable from the Brazilian government.” The balance of the account at December 31, 2003 was U.S.$239 million. Effective January 2, 2002, all price controls for crude oil and oil products ended, and while no price controls were imposed on crude oil and oil products in 2002 or 2003, the Brazilian government could decide to reinstate price controls in the future as a result of market instability or other conditions. If this were to occur, Petrobras’ financial condition and results of operations could be adversely affected.

Historical Brazilian government control of Petrobras’ sales prices and regulation of its operating revenues mean that Petrobras’ results of operations cannot be easily compared from year to year.

One of the tools available to the Brazilian government to control inflation and pursue other economic and social objectives has been the regulation of oil product prices. The method by which the Brazilian government has controlled Petrobras’ prices has varied from year to year. Until December 31, 2001, the Brazilian government regulated the prices at which Petrobras was permitted to sell its oil products. The Brazilian government also established freight subsidies to ensure uniform oil product prices throughout Brazil, but these subsidies have since been phased out. Beginning in July 1998, and until the institution of price deregulation on January 2, 2002, the Brazilian government established a new methodology for calculating the price of oil products based on fluctuations in exchange rates and international market prices for relevant benchmark products.

Because of this government price control and the change in methodology:

| • | the various line items in Petrobras’ financial statements are not necessarily comparable from period to period; and |

| • | Petrobras’ results of operations reflect not only its consolidated operations, but also the results of economic activity undertaken on behalf of the Brazilian government. |

Additionally, from time to time, the Brazilian government may impose specific taxes or other special payment obligations on Petrobras’ operations that may affect its results of operations.

Petrobras does not own any of the crude oil and natural gas reserves in Brazil.

A guaranteed source of crude oil and natural gas reserves is essential to an oil and gas company’s sustained production and generation of income. As a result, many oil and gas companies own crude oil and natural gas reserves in other countries. Under Brazilian law, the Brazilian government owns all crude oil and natural gas reserves in Brazil. Petrobras possesses the exclusive right to develop its reserves pursuant to concession agreements awarded to it by the Brazilian government, but if the Brazilian government were to restrict or prevent Petrobras from exploiting these crude oil and natural gas reserves, its ability to generate income would be adversely affected.

12

Table of Contents

Risks Relating to Brazil

The Brazilian government has historically exercised, and continues to exercise, significant influence over the Brazilian economy. Brazilian political and economic conditions have a direct impact on Petrobras’ business and may have a material adverse effect on Petrobras.

The Brazilian economy has been characterized by significant involvement by the Brazilian government, which often changes monetary, credit and other policies to influence Brazil’s economy. The Brazilian government’s actions to control inflation and other economic policies have often involved wage and price controls, modifications to the Central Bank’s base interest rates, and other measures, such as the freezing of bank accounts, which occurred in 1990.

The Brazilian government’s economic policies may have important effects on Brazilian corporations and other entities, including Petrobras, and on market conditions and prices of Brazilian securities. Petrobras’ financial condition and results of operations may be adversely affected by the following factors and the Brazilian government’s response to these factors:

| • | devaluations and other exchange rate movements; |

| • | inflation; |

| • | exchange control policies; |

| • | social instability; |

| • | price instability; |

| • | energy shortages; |

| • | interest rates; |

| • | liquidity of domestic capital and lending markets; |

| • | tax policy; and |

| • | other political, diplomatic, social and economic developments in or affecting Brazil. |

Inflation and government measures to curb inflation may contribute significantly to economic uncertainty in Brazil and to heightened volatility in the Brazilian securities markets and, consequently, may adversely affect Petrobras’ financial condition and results of operations.

Petrobras’ principal market is Brazil, which has, in the past, periodically experienced extremely high rates of inflation. Inflation, along with recent governmental measures to combat inflation and public speculation about possible future measures, has had significant negative effects on the Brazilian economy. The annual rates of inflation, as measured by the National Consumer Price Index (Índice Nacional de Preços ao Consumidor), have decreased from 2,489.1% in 1993 to 929.3% in 1994, to 8.4% in 1999 and to 5.3% in 2000. The same index increased to 9.4% during 2001 and to 14.7% in 2002, before decreasing to 10.4% in 2003.

Brazil may experience high levels of inflation in the future. The lower levels of inflation experienced since 1994 may not continue. Future governmental actions, including actions to adjust the value of the Real, could trigger increases in inflation.

Fluctuations in the value of the Real against the U.S. dollar may result in uncertainty in the Brazilian economy and the Brazilian securities market and could negatively impact Petrobras’ business.

Over the last three fiscal years, approximately 83% of Petrobras’ revenues have been denominated in Reais, although prices for crude oil and oil products have been based on international prices. A substantial portion of Petrobras’ indebtedness and some of its operating expenses and capital expenditures are, and are expected to continue to be, denominated in or indexed to the U.S. dollar and other foreign currencies. In addition, during the year ended December 31, 2003, Petrobras imported approximately U.S.$5.7 billion of crude oil and oil products, the prices of which were all denominated in U.S. dollars.

13

Table of Contents

As a result of inflationary pressures, the Real and its predecessor currencies have been devalued periodically during the last four decades. Throughout this period, the Brazilian government has implemented various economic plans and utilized a number of exchange rate policies, including sudden devaluations, periodic mini-devaluations during which the frequency of adjustments has ranged from daily to monthly, floating exchange rate systems, exchange controls and dual exchange rate markets. From time to time, there have been significant fluctuations in the exchange rates between the Real and the U.S. dollar and other currencies. For example, the Real declined in value against the U.S. dollar by 18.7% in 2001 and by 52.3% in 2002, before appreciating 18.2% against the U.S. dollar in 2003.

Devaluation of the Real relative to the U.S. dollar could create additional inflationary pressures in Brazil by generally increasing the price of imported products and requiring recessionary governmental policies to curb aggregate demand. On the other hand, appreciation of the Real against the U.S. dollar may lead to a deterioration of the country’s current account and the balance of payments, as well as dampen export-driven growth. The potential impact of the floating exchange rate and of measures by the Brazilian government aimed at stabilizing the Real is uncertain. In addition, a substantial increase in inflation may weaken investor confidence in Brazil. Policies pursued by the Brazilian government, and investors’ reactions to actual or potential governmental policies, may contribute to economic uncertainty in Brazil and adversely affect Petrobras’ financial condition and results of operations.

Risks Relating to our Debt Securities

The market for our notes may not be liquid.

Our notes are not listed on any securities exchange and are not quoted through an automated quotation system. We can make no assurance as to the liquidity of or trading markets for our notes. We cannot guarantee that the holders of our notes will be able to sell their notes in the future. If a market for our notes does not develop, holders of our notes may not be able to resell the notes for an extended period of time, if at all.

Enforcement of Petrobras’ obligations under the standby purchase agreement might take longer than expected.

Petrobras will enter into a standby purchase agreement in support of our obligation under the notes and an indenture. Petrobras’ obligation to purchase from the noteholders any unpaid amounts of principal, interest and other amounts due under the notes and the indenture applies, subject to certain limitations, irrespective of whether any such amounts are due at maturity of the notes or otherwise. See “Senior Notes—Standby Purchase Agreements” and “Global Notes—Standby Purchase Agreements.”

Petrobras has been advised by its counsel that the enforcement of the standby purchase agreement in Brazil against Petrobras, if necessary, will occur under a form of judicial process that, while similar, has certain procedural differences from those applicable to enforcement of a guarantee and, as a result, the enforcement of the standby purchase agreement may take longer than would otherwise be the case with a guarantee.

Restrictions on the movement of capital out of Brazil may impair your ability to receive payments on the standby purchase agreement.

The Brazilian government may impose restrictions on the conversion of Reais into foreign currencies and on the remittance to foreign investors of proceeds from their investments in Brazil. Brazilian law permits the government to impose these restrictions whenever there is a serious imbalance in Brazil’s balance of payments or there are reasons to foresee a serious imbalance.

The Brazilian government imposed remittance restrictions for approximately six months in 1990. Similar restrictions, if imposed, would impair or prevent the conversion of payments under the standby purchase agreement from Reais into U.S. Dollars and the remittance of the U.S. Dollars abroad. We cannot assure you that the Brazilian government will not take similar measures in the future.

14

Table of Contents

Petrobras may not be able to pay its obligations under the standby purchase agreement in U.S. Dollars.

Payments by Petrobras to us for the import of oil, the expected source of our cash resources to pay our obligations under the notes, will not require approval by or registration with the Central Bank of Brazil. There may be other regulatory requirements that Petrobras will need to comply with in order to make funds available to us. If Petrobras is required to make payments under the standby purchase agreement, Central Bank of Brazil approval will be required to make such payments. Any approval from the Central Bank of Brazil may only be requested when such payment is to be remitted abroad by Petrobras, and will be granted by the Central Bank of Brazil on a case-by-case basis. It is not certain that any such approvals will be obtainable at a future date. In case the noteholders receive payments in Reais corresponding to the equivalent U.S. Dollar amounts due under our notes, it may not be possible to convert these amounts into U.S. Dollars. Petrobras will not need any prior or subsequent approval from the Central Bank of Brazil to use funds it holds abroad to comply with its obligations under the standby purchase agreement.

Petrobras would be required to pay judgments of Brazilian courts enforcing its obligations under the standby purchase agreement only in Reais.

If proceedings were brought in Brazil seeking to enforce Petrobras’ obligations in respect of the standby purchase agreement, Petrobras would be required to discharge its obligations only in Reais. Under the Brazilian exchange control limitations, an obligation to pay amounts denominated in a currency other than Reais, which is payable in Brazil pursuant to a decision of a Brazilian court, may be satisfied in Reais at the rate of exchange, as determined by the Central Bank of Brazil, in effect on the date of payment.

A finding that Petrobras is subject to U.S. bankruptcy laws and that the standby purchase agreement executed by Petrobras was a fraudulent conveyance could result in noteholders losing their legal claim against Petrobras.

Our obligation to make payments on the notes is supported by Petrobras’ obligation under the standby purchase agreement to make payments on our behalf. Petrobras has been advised by its external U.S. counsel that the standby purchase agreement is valid and enforceable in accordance with the laws of the State of New York and the United States. In addition, Petrobras has been advised by its general counsel, Mr. Nilton de Almeida Maia, that the laws of Brazil do not prevent the standby purchase agreement from being valid, binding and enforceable against Petrobras in accordance with its terms. In the event that U.S. federal fraudulent conveyance or similar laws are applied to the standby purchase agreement, and Petrobras, at the time it entered into the standby purchase agreement:

| • | was or is insolvent or rendered insolvent by reason of its entry into the standby purchase agreement; |

| • | was or is engaged in business or transactions for which the assets remaining with Petrobras constituted unreasonably small capital; or |

| • | intended or intends to incur, or believed or believes that Petrobras would incur, debts beyond its ability to pay such debts as they mature; and |

| • | in each case, received or receives less than reasonably equivalent value or fair consideration therefor, |

then Petrobras’ obligations under the standby purchase agreement could be avoided, or claims in respect of the standby purchase agreement could be subordinated to the claims of other creditors. Among other things, a legal challenge to the standby purchase agreement on fraudulent conveyance grounds may focus on the benefits, if any, realized by Petrobras as a result of our issuance of these notes. To the extent that the standby purchase agreement is held to be a fraudulent conveyance or unenforceable for any other reason, the holders of the notes would not have a claim against Petrobras under the standby purchase agreement and will solely have a claim against us. We cannot assure you that, after providing for all prior claims, there will be sufficient assets to satisfy the claims of the noteholders relating to any avoided portion of the standby purchase agreement.

Item 4. Information on the Company

HISTORY AND DEVELOPMENT OF THE COMPANY

We were established on September 24, 1997 as a wholly-owned subsidiary of Braspetro Oil Services Company, or Brasoil, a wholly-owned subsidiary of Petrobras Internacional S.A. (Braspetro), which has since been absorbed by Petrobras. We were initially incorporated under the name Brasoil Finance Company, which was changed by special resolution of our shareholders to Petrobras International Finance Company on September 25, 1997. On January 14, 2000, the board of directors of Braspetro and Petrobras approved the transfer of 100% of our voting shares from Brasoil to Petrobras. Since April 1, 2000, we have operated as a wholly-owned subsidiary of Petrobras.

15

Table of Contents

We are a tax exempt company incorporated with limited liability under the laws of the Cayman Islands. Our registered office is located at Anderson Square Building, P.O. Box 714, George Town, Grand Cayman, Cayman Islands, and our telephone number is 55-21-2534-1410.

BUSINESS OVERVIEW

We were incorporated in order to facilitate and finance the import of crude oil and oil products by Petrobras into Brazil. Accordingly, our primary function is to act as an intermediary between third-party oil suppliers and Petrobras by engaging in crude oil and oil product purchases from international suppliers and reselling crude oil and oil products in U.S. dollars to Petrobras on a deferred payment basis, at a price which represents a premium to compensate us for our financing costs. We are generally able to obtain credit to finance purchases on the same terms granted to Petrobras, and we buy crude oil and oil products at the same price that suppliers would charge Petrobras directly.

As part of Petrobras’ strategy to expand its international operations and facilitate its access to international capital markets, we engage in borrowings in international capital markets supported by Petrobras, primarily through standby purchase agreements.

In addition, we also engage in a number of activities that are conducted by three wholly-owned subsidiaries:

| • | Petrobras Europe Limited, or PEL, a United Kingdom company which acts as an agent and advisor in connection with Petrobras’ activities in Europe, the Middle East, the Far East and North Africa; |

| • | Petrobras Finance Limited, or PFL, a Cayman Islands company, which facilitates an exports prepayment program linked to the resale of fuel oil and bunker fuel bought from Petrobras; and |

| • | Bear Insurance Company Limited – BEAR, a company incorporated in Bermuda that contracts insurance for Petrobras subsidiaries. |

In January 2003, we transferred Petrobras Netherlands B.V., or PNBV, a Dutch company engaged in leasing activities of primarily offshore equipment to be used by Petrobras for exploration and production of crude oil and natural gas, to Petrobras as part of Petrobras’ restructuring of its international business segment. PNBV became a wholly-owned subsidiary of Petrobras, effective as of January, 2003.

Beginning in 2004, as part of a Petrobras restructuring of its offshore subsidiaries in order to centralize trading operations, we have engaged in limited exports of oil and oil products.

Our Principal Commercial Activities

Our principal activity is the purchase of crude oil and oil products for resale to Petrobras and, to a limited extent, third parties. We acquire the crude oil and oil products either through purchases on the spot market or long-term supply contracts. Our crude oil and oil product purchase obligations are, in most instances, guaranteed by Petrobras. We sell the products to Petrobras at our purchase price, plus a premium, determined in accordance with a formula designed to pass on our average costs of capital to Petrobras.

In addition, we finance our oil trading activities principally from commercial banks, including lines of credit and commercial paper programs, as well as through inter-company loans from Petrobras and the issuance of notes in the international capital markets.

16

Table of Contents

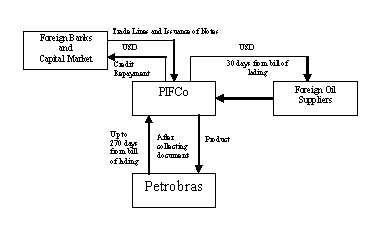

The following chart illustrates how we act as the intermediary between international crude oil suppliers and Petrobras.

We purchase crude oil and oil products from international oil suppliers on a free-on-board (F.O.B.) basis under standard terms that traditionally require payment within 30 days from the bill of lading. Petrobras buys crude oil and oil products from us under terms that allow for payment up to 270 days from the date of the bill of lading. Petrobras would typically be unable to meet the 30-day payment term imposed by international suppliers because of the complexity of producing a full set of documents for a single bill of lading when, for example, the shipment to which that bill of lading relates must be delivered to different parts of Brazil and different sets of documents must be delivered to each delivery point. Depending on the unloading ports’ locations, this process may be completed up to 120 days from the vessel’s departure. Because we are not subject to the Brazilian regulations applicable to Petrobras, we can pay the international supplier on time without having to produce these different sets of documents. To cover our financing costs, we include a premium when we sell crude oil and oil products to Petrobras.

Our Principal Suppliers

Our eight principal suppliers represented 63.7% of our total imports for 2003, as compared to 65.7% of our total imports for 2002 and 69.1% of our total imports for 2001. The chart below sets forth information with respect to our principal suppliers for 2003, 2002 and 2001.

17

Table of Contents

OUR PRINCIPAL SUPPLIERS(1)

Year Ended December 31, 2003 | Year Ended December 31, 2002 | Year Ended December 31, 2001 | ||||||||||||||||||

Supplier | Country of | Imports (in millions of U.S. | % of Total Imports | Imports (in millions of U.S. | % of Total Imports | Imports (in millions of U.S. | % of Total Imports | |||||||||||||

Saudi Aramco | Saudi Arabia | $ | 888.5 | 16.8 | % | $ | 534.1 | 10.3 | % | $ | 587.3 | 9.4 | % | |||||||

Petrobras America, Inc. (PAI) | United States | 767.9 | 14.5 | 947.1 | 18.3 | 1,320.8 | 21.2 | |||||||||||||

Sonatrach Group | Algeria | 647.1 | 12.3 | 604.0 | 11.7 | 970.8 | 15.6 | |||||||||||||

Shell | England | 362.5 | 6.9 | 279.5 | 5.4 | — | — | |||||||||||||

Mega | Argentina | 235.9 | 4.5 | 158.1 | 3.1 | — | — | |||||||||||||

AGIP | Italy | 160.7 | 3.0 | — | — | 318.3 | 5.1 | |||||||||||||

Somo | Iraq | 159.5 | 3.0 | — | — | — | — | |||||||||||||

PDVSA Petróleo | Venezuela | 141.9 | 2.7 | 413.6 | 8.0 | 515.9 | 8.2 | |||||||||||||

Sinochem | England | 240.9 | 4.7 | — | — | |||||||||||||||

Reliance | India | 217.7 | 4.2 | 224.2 | 3.6 | |||||||||||||||

Ryttsa (Repsol-YPF) | Argentina | — | — | — | — | 248.8 | 4.0 | |||||||||||||

Chevron San Jorge | Argentina | — | — | — | — | 126.5 | 2.0 | |||||||||||||

Total | $ | 3,364.0 | 63.7 | % | $ | 3,395.0 | 65.7 | % | $ | 4,312.6 | 69.1 | % | ||||||||

| (1) | Excluding suppliers to our subsidiaries |

Our Principal Customers

In 2003, Petrobras conducted 99.8% of its crude oil and oil products import activities through us in order to give it the flexibility it needs to meet various delivery and funding requirements. During 2003, we sold crude oil and oil products with a total value of U.S.$ 5,332.1 million, as compared to U.S.$5,191.1 million in 2002 and U.S.$6,250.0 million in 2001.

Our sales of crude oil and oil products to Petrobras and the Alberto Pasqualini refinery (“Refap,” which is 70% owned by Petrobras) represented U.S.$4,408.7 million (82.7%) of our total sales in 2003 and U.S.$ 4,884.7 million (94.1%) of our total sales in 2002. Our sales of crude oil and oil products to third parties and other related parties (excluding Petrobras and Refap) totaled U.S.$923.8 million for 2003, U.S.$306.4 million for 2002 and U.S.$407.6 million for 2001. Our nine principal clients, excluding Petrobras and Refap, represented 67.0% of our sales to third parties and related parties at December 31, 2003, as compared to 80.5% at December 31, 2002 and 68.0% at December 31, 2001.

18

Table of Contents

THIRD PARTY AND RELATED PARTY SALES(1)

Year Ended December 31, 2003 | Year Ended December 31, 2002 | Year Ended December 31, 2001 | ||||||||||||||||

| Sales | % of Total Sales | Sales | % of Total Sales | Sales | % of Total Sales | |||||||||||||

| (in millions of U.S. dollars) | (in millions of U.S. dollars) | (in millions of U.S. dollars) | ||||||||||||||||

Petrobras America, Inc. | $ | 196.7 | 21.3 | % | $ | 104.3 | 34.0 | % | $ | 6.3 | 1.6 | % | ||||||

BP | 98.7 | 10.7 | 28.8 | 9.4 | 30.5 | 7.5 | ||||||||||||

Shell | 88.8 | 9.6 | — | — | ||||||||||||||

Ipiranga | 61.3 | 6.6 | 12.5 | 4.1 | 60.5 | 14.8 | ||||||||||||

Gasmar | 52.3 | 5.7 | ||||||||||||||||

Manguinhos | 38.6 | 4.2 | ||||||||||||||||

Unipec | 29.1 | 3.1 | ||||||||||||||||

Geogas | 28.2 | 3.0 | ||||||||||||||||

Repsol | 25.7 | 2.8 | ||||||||||||||||

Gases y Graneles | 24.6 | 8.0 | — | — | ||||||||||||||

Ancap | 19.2 | 6.3 | — | — | ||||||||||||||

Vitol | 16.4 | 5.4 | — | — | ||||||||||||||

EG3 | 14.6 | 4.8 | — | — | ||||||||||||||

Ferrel | 14.0 | 4.5 | 20.5 | 5.3 | ||||||||||||||

Gazocean | 12.2 | 4.0 | — | — | ||||||||||||||

Glencore | — | — | — | — | 56.4 | 13.8 | ||||||||||||

Cargill | — | — | — | — | 39.0 | 9.6 | ||||||||||||

Contigroup | — | — | — | — | 25.7 | 6.3 | ||||||||||||

Trafigura | — | — | — | — | 22.5 | 5.5 | ||||||||||||

Hin Leong | — | — | — | — | 14.8 | 3.6 | ||||||||||||

Total | $ | 619.4 | 67.0 | % | $ | 246.6 | 80.5 | % | $ | 276.2 | 68.0 | % | ||||||

| (1) | Excludes Petrobras and Refap, as we do not generate profits from sales to Petrobras and Refap. For each year, includes only our nine principal clients during that year. |

Petrobras Europe Limited (PEL)

In May 2001, we established PEL, a wholly-owned subsidiary incorporated and based in the United Kingdom, to consolidate Petrobras’ trade and finance activities in Europe, the Middle East, the Far East and North Africa. These activities consist of advising on, and negotiating the terms and conditions for, crude oil and oil products supplied to us and Petrobras, as well as marketing Brazilian crude oil and crude oil products exported to the geographic areas in which PEL operates. PEL plays an advisory role in connection with these activities and undertakes no direct or additional commercial or financial risk. PEL provides these advisory and marketing services as an independent contractor, pursuant to a services agreement between PEL and Petrobras. In exchange, Petrobras compensates PEL for all costs incurred in connection with these activities, plus a margin.

Petrobras Finance Limited (PFL)

In December 2001, we established PFL, a wholly-owned subsidiary incorporated and registered in the Cayman Islands. PFL primarily purchases bunker and fuel oil from Petrobras and sells the products in the international market in order to generate export receivables to cover its obligations to transfer these receivables to a trust under an exports prepayment program. The exports prepayment program helps provide PFL with the funding necessary to purchase oil products from Petrobras, as described below.

Bear Insurance Company Limited (BEAR)

In January 2003, we received BEAR from Brasoil. This transaction took place as part of the restructuring of Petrobras’ international business segment. Bear currently serves as an intermediary for Petrobras, advising on, and negotiating the terms and conditions of, certain of Petrobras’ insurance policies.

19

Table of Contents

Exports Prepayment Program

Petrobras sells and delivers bunker fuel and fuel oil and, subject to certain conditions, other oil products (collectively, the “Eligible Products”) to PFL under two principal agreements: the Master Export Contract and the Prepayment Agreement. The PF Export Receivables Master Trust (the “Trust”) was formed under the laws of the Cayman Islands to provide PFL with the funding necessary to purchase Eligible Products from Petrobras and resell these products through the arrangements described below.