Common Stock Offering 2012 Issuer Free Writing Prospectus Dated July 20, 2012 Filed Pursuant to Rule 433 Registration Statement No. 333-180456 |

Forward-Looking Information Certain statements in this presentation may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are statements that include projections, predictions, expectations or beliefs about future events or results or otherwise and are not statements of historical fact. Such statements are often characterized by the use of qualified words (and their derivatives) such as “expect,” “believe,” “estimate,” “plan,” “project,” “anticipate” or other statements concerning opinions or judgments of New Peoples Bankshares, Inc. “the Company” and its management about future events. Although the Company believes that its expectations with respect to forward-looking statements are based upon reasonable assumptions within the bounds of its existing knowledge of its business and operations, there can be no assurance that actual results, performance or achievements of the Company will not differ materially from any future results, performance or achievements expressed or implied by such forward-looking statements. Actual future results and trends may differ materially from historical results or those anticipated depending on a variety of factors, including, but not limited to, the effects of and changes in: general economic conditions, the interest rate environment, legislative and regulatory requirements, competitive pressures, new products and delivery systems, inflation, changes in the stock and bond markets, technology, and consumer spending and savings habits. The Company does not update any forward-looking statements that may be made from time to time by or on behalf of the Company. Other Information The Company has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (the “SEC”) for the offering to which this communication relates, and the registration statement became effective on July 6, 2012. Before you invest, you should read the prospectus in that registration statement and other documents the Company has filed with the SEC for more complete information about the Company and the offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. The final prospectus, dated July 6, 2012, was filed with the SEC on July 16, 2012. Alternatively, the Company will arrange to send you the prospectus if you request it by calling 1-276-873-6288. 1 |

Why Are We Conducting a Common Stock Offering? Why Are We Conducting a Common Stock Offering? • To enable us to fulfill our mission of meeting the expectations of our vested stakeholders, i.e. Shareholders, Regulators, Customers, Employees and Communities by: • Increasing our capital and improving our capital ratios to strengthen our balance sheet as we continue to resolve and manage our elevated level of nonperforming assets and potential future loan losses • Raising sufficient capital to enable compliance with our capital plan as approved by our regulators • We did not participate in TARP funds • We have not solicited out-of-market institutional investors • The Common Stock Offering is the most fair to our exiting shareholders and best source of capital available • Complying with the requirements of the Formal Written Agreement with regulators • Restoring our capital position as impacted by a cumulative net loss of $24.2 million from January 1, 2009 through March 31, 2012 due primarily to increases in our provisions for loan losses and write-downs of our other real estate owned properties • Positioning ourselves for proposed Basel III capital proposals in future years that may impact the bank • Allowing us to return to profitability more quickly 2 |

Offering Overview Offering Overview Issuer: New Peoples Bankshares, Inc. (OTCBB:NWPP) Offering Structure: Common Stock Rights Offering to Existing Shareholders and Standby Public Offering, whereby shares that are not purchased by the existing shareholders may be sold to the public Offering Size: Up to $25.0 Million ($10.0 Million Minimum) Shares Offered: 6,666,667 shares @ minimum offering, or 16,676,845 shares outstanding minimum pro forma 16,666,667 shares @ maximum offering, or 26,676,845 shares outstanding maximum pro forma Offering Price: $1.50 per share, or 57.69% of tangible book value at March 31, 2012 Director Commitment : All of the Directors have collectively committed to a total of $1.0 million, or 666,667 shares, which is applied toward the $10.0 million minimum. Directors Keene and White Debt Conversion Have agreed to the conversion of $5.45 million of holding company debt plus accrued interest to common stock at the same terms as included in the offering, resulting in 3,813,225 shares issued and 762,643 warrants issued Securities Issued: * Rights to acquire 1.665 shares of our common stock for each share held * Nontransferable stock warrant for every 5 shares purchased with a 5 year maturity and an exercise price of $1.75 per warrant. Immediately exercisable. Use of Proceeds: Up to $8.0 million will be applied to increase the Bank’s equity capital as necessary and appropriate, to serve as a buffer for any possible future unanticipated degradation in the Bank’s loan or asset portfolios, and for general corporate purposes. The remaining funds will be used for general corporate purposes, as well as to provide additional capital support to the Bank should that become necessary and appropriate. Expected Closing Rights Offering – August 15, 2012 (may extend to September 15, 2012) - Public Offering – October 15, 2012 3 |

COMPETITIVE STRENGTHS 4 |

Our Mission Our Mission • Our overall mission continues to be to build a high performing community bank focused on providing high quality, state of the art, “golden rule” banking services within our communities, resulting in increased shareholder value 5 |

• New Peoples’ differentiating factors that provide a foundation for a high performing institution built on customer service and franchise value creation through profitable growth: • Leading Deposit Market Share • Core Deposit Base • Historically Strong Net Interest Margin Management • Experienced Management Team • Committed Board of Directors 6 Competitive Strengths Competitive Strengths |

• Leading Deposit Market Share • #2 in the Tri-State Area Deposit Market • 8.85% of the Tri-State Area deposits • Outpaced deposit growth for our market area which had a 5 year compounded annual rate of 2.3%, our growth was 4.6% • Strong market penetration with 23 convenient branch locations Competitive Strengths Competitive Strengths 7 Note: Information as of June 30, 2011, except branch locations. |

New Peoples Bank New Peoples Bank Branch Locations Branch Locations Virginia Locations Honaker (HQ) Abingdon Big Stone Gap Bland Bluefield Bristol-Linden Square Castlewood Chilhowie Clintwood Gate City Grundy Haysi Jonesville Lebanon Norton Pound Pounding Mill Tazewell Weber City Wise West Virginia Locations Bluewell Princeton Tennessee Locations Kingsport 8 |

• Core Deposit Base • Focused on high quality, “golden rule” banking services within our communities • Provider of superior service through one of the largest branch networks in our market area • Strong core deposit base funding our loan growth • 39.15% of our deposits are in checking, money market and savings accounts • 77.21% of our deposits are core deposits (Total Deposits less time deposits greater than $100,000 and brokered deposits) • Only $2.7 million in brokered deposits which is very favorable to peers Competitive Strengths Competitive Strengths 9 Note: Information as of March 31, 2012. |

Company Statistics Company Statistics New Peoples Bank opened in October 28, 1998 New Peoples Bankshares formed in 2001 Total Shareholders 4,437 ¹ Total Customer Relationships 47,164 ² Total Households 38,023 ² Total # of Deposits 64,099 ² Total # of Loans 11,841 ² Total # of Branches 23 ³ # of Counties Served in VA, TN and WV 12 ³ Market Share of Deposits in Tri-State Area based on June 30, 2011 FDIC Deposit Summary Data # 2 position in Deposit Market Share 8.85% of total deposits 10 1 Information as of Shareholder Record Date, June 26, 2012 2 Information as of May 14, 2012 3 Information as of May 31, 2012 |

• Historically Strong Net Interest Margin Management • Successfully managing a strong net interest margin, a key contributor to delivering consistent profitability resulting in solid returns to shareholders • Historically maintained a net interest margin over 4% • We believe we can continue this trend as we continue to improve asset quality, cultivate and grow core deposits, and effectively position ourselves to maintain or improve our net interest margin in both rising and falling interest rate cycles Competitive Strengths Competitive Strengths 11 |

Net Interest Margin Trend Net Interest Margin Trend December 31, 2007 through March 31, 2012 December 31, 2007 through March 31, 2012 Peer Data Source: Federal Reserve Board of Governors Bank Holding Company Performance Report 12 4.11% 4.13% 4.14% 4.35% 4.29% 3.88% 3.65% 3.61% 3.76% 3.81% 3.72% 0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 2007 2008 2009 2010 2011 3/31/2012 Net Interest Margin Peer Data BHC $500 Million to $1 Billion 4.15% |

• Experienced Management Team • Our executive team consists of 4 officers with over 130 years of combined experience • An average of 33 years experience in the financial services industry • Strongly committed to leading the organization to profitability, strength and shareholder value Competitive Strengths Competitive Strengths 13 Name Position Years of Experience Years with NPB Jonathan H. Mullins President and Chief Executive Officer 31 14 Frank Sexton, Jr. Executive Vice President and Chief Operating Officer 40 14 C. Todd Asbury Executive Vice President, Chief Financial Officer, Secretary and Treasurer 24 8 Stephen W. Trescot Executive Vice President and Chief Credit Officer 39 1 |

• Committed Board of Directors • 11 community leaders native to our market area • Actively involved in local economic development and promotion of our market area • Fully engaged in the oversight of bank management • Committed to investing $1.0 million, or 10% of the minimum offering amount • 2 Directors invested $5.45 million to payoff holding company debt and have agreed to the conversion of the debt plus accrued interest to common stock after the rights offering is complete • Dedicated to increasing shareholder value through enhanced stock value • Devoted to paying dividends as soon as possible Competitive Strengths Competitive Strengths 14 |

Board of Directors Board of Directors 15 Name Position Committees Director Since Michael G. McGlothlin Chairman of the Board Executive (Chair), Compliance, Nominating, Offering 1998 John Cox Vice Chairman of the Board Asset Liability Management, Audit, Compensation (Chair), Compliance, Executive, Nominating, Offering 1998 Tim W. Ball Director n/a 1999 Joe M. Carter Director Asset Liability Management, Director Loan 1998 Charles H. Gent, Jr. Director Audit, Compensation 1998 Eugene Hearl Director Asset Liability Management, Audit, Compensation, Compliance, Director Loan, Executive 2010 Harold Lynn Keene, Jr. Director Asset Liability Management, Audit (Chair), Compliance, Director Loan (Chair), Executive, Nominating, Offering 1998 A. Frank Kilgore Director Compensation 1998 Fred W. Meade Director Compensation, Director Loan, Executive, Nominating 1998 Jonathan H. Mullins Director Asset Liability Management, Compensation, Compliance, Executive 2010 B. Scott White Director Asset Liability Management, Audit, Compliance (Chair), Executive, Nominating, Offering 1998 |

FINANCIAL SNAPSHOT 16 |

Consolidated Financial Snapshot Consolidated Financial Snapshot March 31, 2012 and December 31, 2011 17 Balance Sheet March 31, 2012 December 31, 2011 Total Assets $768.4 million $780.4 million Total Loans $573.8 million $597.8 million Total Allowance for Loan Loss $ 18.0 million $ 18.4 million Total Deposits $699.1 million $708.3 million Total Equity Capital $ 26.2 million $ 28.9 million Tangible Book Value $2.60 $2.87 Basic Shares Outstanding 10,010,178 10,010,178 Diluted Shares Outstanding 10,010,178 10,010,178 Equity to Assets Ratio 3.41% 3.70% Tier 1 Leverage Ratio 3.92% 4.23% Total Risk Based Capital Ratio 9.08% 9.15% |

Consolidated Consolidated Financial Financial Snapshot Snapshot (continued) (continued) March 31, 2012 and December 31, 2011 18 Earnings Quarter Ended March 31, 2012 Year Ended December 31, 2011 Net Interest Income $ 7.1 million $ 32.2 million Net Interest Margin % 4.15% 4.29% Provision for Loan Losses $ 2.0 million $ 8.0 million Noninterest Income $ 1.5 million $ 5.5 million Noninterest Expenses $ 9.0 million $ 39.4 million Net (Loss) ($ 2.5 million) ($ 8.9 million) Net (Loss) per Share ($0.25) ($0.89) Asset Quality March 31, 2012 December 31, 2011 Total Non Performing Assets (NPAs) $ 61.4 million $ 58.9 million NPAs/ Total Assets Ratio 7.98% 7.60% ALLL to Total Loans Ratio 3.14% 3.07% |

STRATEGIC INITIATIVES 19 |

Our Strategy Our Strategy • Our immediate business strategy is directed towards building shareholder value by: • Returning to profitability • Improving asset quality • Enhancing our regulatory capital levels • Over the long-term, we want to position ourselves favorably to take advantage of future growth opportunities within our markets and to pay dividends to shareholders 20 |

STRATEGIC INITIATIVES - RETURNING TO PROFITABILITY 21 |

Strategic Actions and Initiatives Taken to Strategic Actions and Initiatives Taken to Improve Profitability, Improve Profitability, Asset Quality, and Capital Asset Quality, and Capital • Improving Profitability • Continuing to maintain a net interest margin in excess of 4.00% and have historically been able to do this • Lowered our cost of deposits over 122 basis points from 2.25% at December 31, 2009 to 1.03% at March 31, 2012 • Reduced total employees from 367 at December 31, 2009 to 295 at March 31, 2012, a total reduction of 72, or 19.62% • Frozen salaries in the year 2012 • Reduced the 100% matching employee 401K contribution from up to 5% to up to 3% in 2012 • Closed/consolidated eight underperforming branch offices since 2010, and will continue to evaluate performance of the branch network • Reduced overhead through aforementioned branch closings and a reduction in full time equivalent employees resulting in estimated annual cost savings of $1.0 million • Stabilizing asset quality issues 22 |

Net Net Income/ Income/ (Loss) (Loss) Trend Trend (In (In thousands) thousands) For Years Ending December 31, 2007 Through December 31, 2011 and For Years Ending December 31, 2007 Through December 31, 2011 and First Quarter March 31, 2012 First Quarter March 31, 2012 23 (1) Includes a one-time non cash Goodwill impairment loss totaling $4 million. -$10,000 -$8,000 -$6,000 -$4,000 -$2,000 $0 $2,000 $4,000 $6,000 Net Income/ (Loss) |

Provision Provision for for Loan Loan Loss Loss Expense Expense and and Net Net Charge Charge Offs Offs (In (In thousands) thousands) For Years Ending December 31, 2007 through December 31, 2011 and For Years Ending December 31, 2007 through December 31, 2011 and First Quarter Ended March 31, 2012 First Quarter Ended March 31, 2012 24 2007 2008 2009 2010 2011 3/31/2012 Provision for Loan Loss $3,840 $1,500 $12,841 $22,328 $7,959 $1,950 Net Charge Offs $2,090 $1,216 $1,157 $15,902 $14,746 $2,299 $0 $2,000 $4,000 $6,000 $8,000 $10,000 $12,000 $14,000 $16,000 $18,000 $20,000 $22,000 $24,000 Provision for Loan Loss compared to Net Charge-Offs |

OREO OREO Expenses/ Expenses/ (Gains) (Gains) (In (In thousands) thousands) For Years Ending December 31, 2007 through December 31, 2011 and For Years Ending December 31, 2007 through December 31, 2011 and First Quarter Ended March 31, 2012 First Quarter Ended March 31, 2012 25 ($1,000) ($500) $0 $500 $1,000 $1,500 $2,000 $2,500 $3,000 $3,500 $4,000 $4,500 $5,000 $5,500 $6,000 OREO Expenses/ (Gains) |

STRATEGIC INITIATIVES- IMPROVING ASSET QUALITY 26 |

• Enhanced and Reorganized Management and Board of Directors • Hired a new, outside Chief Credit Officer with over 30 years experience in credit administration and loan portfolio risk • Re-positioned our former Chief Credit Officer to Senior Loan Officer with responsibility for the Bank’s loan production and business development • Appointed a new outside director, Eugene Hearl, who has over 40 years of banking experience • Formed a standing Director Loan Committee to enhance the loan approval process and Board knowledge of loan credits Strategic Actions and Initiatives Taken to Strategic Actions and Initiatives Taken to Improve Profitability, Asset Quality, and Capital Improve Profitability, Asset Quality, and Capital 27 |

• Asset Quality Improvement Initiatives • Adopted new loan policies and procedures with stricter credit underwriting standards, streamlined the loan approval process, and implemented a continuing education program for employees • Formed, fully developed and staffed a special assets department with eight full-time employees concentrating on problem asset resolution • Created and trained a commercial lending division with nine lenders and support staff managed by the Bank’s Senior Lending Officer specialized to serve our commercial business • Enhanced loan concentration identification and implemented new procedures for monitoring and managing loan concentrations • Reduced all loan concentration limits below Federal Reserve guidelines • Established a new allowance for loan loss model and policy and assigned oversight to an employee with significant Allowance for Loan Loss (“ALLL”) experience • Hired an expert outside loan review company to periodically review our loan portfolio resulting in more accurate risk grading of our loan portfolio Strategic Actions and Initiatives Taken to Strategic Actions and Initiatives Taken to Improve Profitability, Asset Quality, and Capital Improve Profitability, Asset Quality, and Capital 28 |

Nonperforming Nonperforming Assets Assets (In (In thousands) thousands) December 31, 2007 through March 31, 2012 December 31, 2007 through March 31, 2012 29 2007 2008 2009 2010 2011 3/31/2012 Total NPAs $5,364 $8,943 $34,231 $59,820 $58,912 $61,355 OREO $2,051 $2,496 $5,643 $12,346 $15,092 $15,009 Nonaccrual Loans $2,946 $6,414 $24,713 $45,781 $42,316 $43,679 90 Days + Accruing Interest $267 $33 $3,875 $1,693 $1,504 $2,667 $0 $10,000 $20,000 $30,000 $40,000 $50,000 $60,000 $70,000 Nonperforming Assets |

Delinquency Delinquency Trends Trends 30+ 30+ days days (In (In thousands) thousands) December 31, 2010 through March 31, 2012 December 31, 2010 through March 31, 2012 30 $0 $10,000 $20,000 $30,000 $40,000 $50,000 $60,000 $70,000 12/31/2010 3/31/2011 6/30/2011 9/30/2011 12/31/2011 3/31/2012 90 Days+ $23,404 $21,185 $31,137 $30,784 $24,820 $33,000 60-89 Days $10,110 $5,836 $6,197 $4,752 $6,609 $3,760 30-59 Days $22,426 $14,754 $22,269 $13,849 $24,328 $12,755 Loan Portfolio Delinquencies |

31 Loan Loan Risk Risk Grades Grades (In (In millions) millions) December 31, 2010 through March 31, 2012 December 31, 2010 through March 31, 2012 $50 $200 $300 $350 $400 $500 $550 $600 $650 $700 $750 Loan Classifications Trend $0 $100 $150 $250 $450 12/31/2010 3/31/2011 6/30/2011 9/30/2011 12/31/2011 3/31/2012 Doubtful $6 $7 $7 $6 $3 $3 Substandard $86 $94 $99 $94 $95 $97 Special Mention $30 $35 $44 $52 $47 $49 Pass $586 $546 $514 $477 $452 $426 |

Allowance for Loan Loss as % of Loans Trend Allowance for Loan Loss as % of Loans Trend December 31, 2007 through March 31, 2012 December 31, 2007 through March 31, 2012 32 |

STRATEGIC INITIATIVES – ENHANCING OUR REGULATORY CAPITAL RATIOS 33 |

Strategic Actions and Initiatives Taken to Improve Strategic Actions and Initiatives Taken to Improve Profitability, Asset Quality, and Capital Profitability, Asset Quality, and Capital • Proactively Downsized Balance Sheet and Higher Risk Assets • Reduced total assets $96.6 million from $865.0 million at March 31, 2011 to $768.4 million at March 31, 2012 • Reduced gross loans over $189.8 million from $763.6 million to $573.8 million from December 31, 2009 to March 31, 2012 • Reduced total deposits $83.3 million from $782.4 million at March 31, 2011 to $699.0 million at March 31, 2012, mainly higher cost time deposits • Reduced risk profile of the loan portfolio in compliance with regulatory standards • Reduced higher risk weighted assets overall for the Bank by $164.5 million since December 31, 2009 • Developed a three year strategic and capital plan that incorporates these strategic initiatives including the common stock offering • Paid off Silverton line of credit at the holding company with the proceeds from the unsecured Director Notes (being converted to common stock in this offering) 34 |

35 Strategic Strategic Shrinking Shrinking Trend Trend (In (In Millions) Millions) December 31, 2007- December 31, 2007- March 31, 2012 March 31, 2012 |

Risk Weighted Assets Shrinking Trend (In Millions) Risk Weighted Assets Shrinking Trend (In Millions) December 31, 2007- December 31, 2007- March 31, 2012 March 31, 2012 36 2007 2008 2009 2010 2011 3/31/2012 Total Assets $616.9 $639.8 $645.8 $597.3 $502.4 $481.3 $400 $450 $500 $550 $600 $650 $700 Total Bank Risk Weighted Assets |

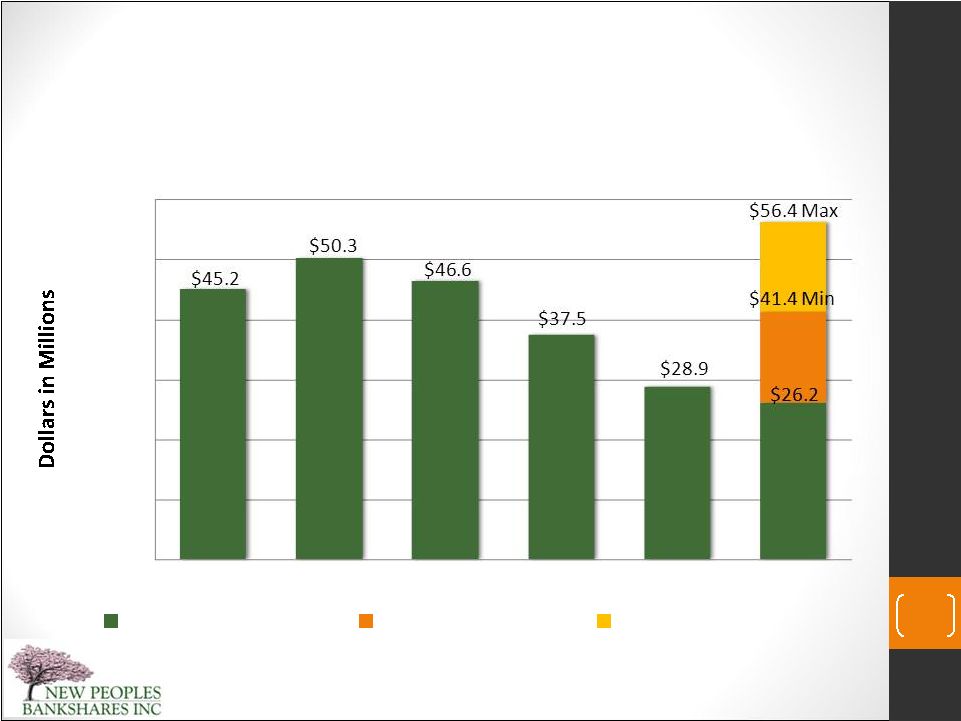

Consolidated Capital Trend – Consolidated Capital Trend – Actual Actual and and Pro Pro Forma Forma (In (In Millions) Millions) December 31, 2007- December 31, 2007- March 31, 2012 March 31, 2012 37 $- $10.0 $20.0 $30.0 $40.0 $50.0 $60.0 2007 2008 2009 2010 2011 3/31/2012 Total Common Equity Proforma Minimum Proforma Maximum |

Capital Ratio Trend – Capital Ratio Trend – Actual and Pro Forma Actual and Pro Forma Consolidated Tier 1 Leverage Ratio Consolidated Tier 1 Leverage Ratio December 31, 2007 through March 31, 2012 December 31, 2007 through March 31, 2012 38 7.22% 7.72% 6.14% 4.62% 4.23% 3.92% 0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 2007 2008 2009 2010 2011 3/31/2012 Leverage Ratio Pro Forma Min Pro Forma Max Minimum Leverage to Remain Well Capitalized 6.44% Min 8.50% Max |

Capital Ratio Trend – Capital Ratio Trend – Actual and Pro Forma Total Actual and Pro Forma Total Risk Based Capital Ratio – Risk Based Capital Ratio – Consolidated Consolidated December 31, 2007 through March 31, 2012 December 31, 2007 through March 31, 2012 39 10.29% 10.78% 9.83% 8.87% 9.15% 9.08% 0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00% 16.00% 18.00% 2007 2008 2009 2010 2011 3/31/2012 Leverage Ratio Pro Forma Min Pro Forma Max Minimum Leverage to Remain Well Capitalized 12.20% Min 15.32% Max |

INVESTMENT SUMMARY 40 |

• Competitive Strengths • Attractive retail deposit franchise and proven ability to grow market share to further develop and enhance our position • Provider of quality banking services to our customers through innovative products, community involvement and excellent customer service in which we have proven success • Effective management of a strong net interest margin that historically has outpaced our peers and is the key driving force to strong core earnings • Committed Board of Directors and Management that have been instrumental to resolve issues through collaborative efforts involving talents, time, experience and finances Investment Summary Investment Summary 41 |

• Strategic Initiatives Taken • Returning to profitability • Instituted efficiencies that will produce immediate and long term cost savings • Tied employee compensation with the interest of investors • Identified and managing credit problems and expecting loan related losses to be less than in the past • Improving asset quality • Stabilized asset quality issues • Implemented numerous policies and procedures to ensure the quality of new loans going forward • Learned valuable lessons during this extended economic recession and have implemented necessary changes to weather future similar situations, should they arise, more favorably Investment Summary Investment Summary 42 |

• Enhancing our regulatory capital levels • Reduced balance sheet risk resulting in stronger asset quality and lower capital requirements due to lower concentrations in certain industries and loan sectors • This stock offering is the best solution available to successfully enhance our regulatory capital levels • The Offering • First rights to purchase are to our loyal shareholders who have supported us faithfully • Priced attractively below book value • Added value, warrants offer the potential for future investment possibly at a discount • The success of this stock offering helps us to move forward and fulfill our mission and purpose • We believe the offering price and accompanying warrants provide good upside potential to investors in the offering Investment Summary - Investment Summary - continued continued 43 |

Appendix 1 -Financial Trends and Ratios Appendix 1 -Financial Trends and Ratios 44 At and for the Three Months ended March 31, At and for the Years ended December 31, 2012 2011 2011 2010 2009 2008 2007 (Dollars in thousands and shares in whole numbers) Balance Sheet Total Assets............................................. $ 768,447 $ 864,665 $ 780,384 $ 852,627 $ 857,910 $ 807,898 $ 765,951 Gross Loans............................................. 573,752 683,025 597,816 707,794 763,570 721,174 682,260 Allowance for Loan Losses..................... (18,031) (19,660) (18,380) (25,014) (18,588) (6,904) (6,620) Other Real Estate Owned........................ 15,009 13,553 15,092 12,346 5,643 2,496 2,051 Deposits................................................... 699,085 782,411 708,315 766,080 760,714 705,688 657,033 Total Borrowings..................................... 39,629 40,829 39,929 45,829 46,779 47,991 58,930 Shareholders’ Equity............................... 26,170 38,086 28,873 37,523 46,619 50,323 45,249 Summary of Operations Interest Income........................................ $ 9,022 $ 10,984 $ 41,769 $ 48,028 $ 50,378 $ 52,317 $ 51,447 Interest Expense...................................... 1,897 2,814 9,606 13,898 18,563 23,095 25,738 Net Interest Income................................. 7,125 8,170 32,163 34,130 31,815 29,222 25,709 Provision for Loan Losses....................... 1,950 1,145 7,959 22,328 12,841 1,500 3,840 Noninterest Income................................. 1,467 1,311 5,524 5,934 5,449 5,550 4,651 Noninterest Expense................................ 8,987 7,613 39,422 31,894 29,847 26,619 23,674 Net Income before Taxes........................ (2,345) 723 (9,694) (14,158) (5,424) 6,653 2,846 Income Tax Expense (Benefit)................ 190 174 (784) (5,093) (1,738) 1,916 (24) Net Income (Loss)................................... $ (2,535) $ 549 $ (8,910) $ (9,065) $ (3,686) $ 4,737 $ 2,870 Per Share Data Book Value.............................................. $ 2.61 $ 3.83 $ 2.88 $ 3.75 $ 4.66 $ 5.03 $ 4.54 Tangible Book Value............................... 2.60 3.40 2.87 3.31 4.21 4.56 4.06 Net Income (Loss), Basic........................ (0.25) 0.05 (0.89) (0.91) (0.37) 0.47 0.29 Net Income (Loss), Diluted..................... (0.25) 0.05 (0.89) (0.91) (0.37) 0.46 0.28 Basic Shares Outstanding........................ 10,010,178 10,010,178 10,010,178 10,009,468 10,008,943 9,980,348 9,957,949 Diluted Shares Outstanding..................... 10,010,178 10,010,178 10,010,178 10,009,468 10,008,943 10,234,909 10,371,577 Profitability Return (Loss) on Average Assets............ (1.32%) (1.96%) (1.07%) (1.05%) (0.44%) 0.61% 0.42% Return (Loss) on Average Equity............ (36.09%) (39.76%) (24.35%) (19.60%) (7.37%) 9.98% 6.60% Net Interest Margin (1)............................ 4.15% 4.12% 4.29% 4.35% 4.14% 4.13% 4.11% Efficiency Ratio....................................... 105.06% 86.16% 104.63% 79.28% 80.10% 76.55% 77.98% |

Appendix 1 (continued) – Appendix 1 (continued) – Financial Trends and Ratios Financial Trends and Ratios 45 Liquidity Ratios Total Loans to Deposits........................... 82.07% 87.30% 84.40% 92.39% 100.38% 102.19% 103.84% Noninterest Bearing Deposits to Total Deposits....................................... 16.14% 13.14% 15.48% 11.46% 11.61% 13.53% 12.74% Nonbrokered Deposits to Total Deposits....................................... 99.61% 97.47% 98.46% 97.41% 96.68% 98.96% 100.00% Capital Adequacy Ratios Total Equity to Total Assets.................... 3.41% 4.44% 3.70% 4.40% 5.43% 6.23% 5.91% Leverage Ratio........................................ 3.92% 4.58% 4.23% 4.62% 6.14% 7.72% 7.22% Tier 1 Capital........................................... 6.23% 6.75% 6.57% 6.54% 8.12% 9.50% 8.73% Total Risk-Based Capital......................... 9.02% 9.08% 9.15% 8.87% 9.83% 10.78% 10.29% Asset Quality Ratios Net Charge-Offs to Average Loans......... 1.57% 1.58% 2.24% 2.14% 0.15% 0.17% 0.34% Nonperforming Loans to Total Loans..... 8.08% 6.37% 7.33% 6.71% 3.74% 0.89% 0.47% Nonperforming Assets to Total Assets.... 7.98% 6.59% 7.60% 7.02% 3.99% 1.11% 0.69% Allowance for Loan Losses to Gross Loans........................................... 3.14% 2.75% 3.07% 3.53% 2.43% 0.96% 0.97% Allowance for Loan Losses to Nonperforming Loans........................... 38.91% 43.14% 41.94% 52.69% 65.02% 107.09% 206.04% Other Data Number of Branch Offices...................... 27 27 27 27 31 31 30 Number of Employees............................. 295 341 312 362 367 377 371 (1) Net interest margin is calculated as tax-equivalent net interest income divided by average earning assets and represents our net yield on our earning asset At and for the Three Months ended March 31, At and for the Years ended December 31, 2012 2011 2011 2010 2009 2008 2007 (Dollars in thousands and shares in whole numbers) |

Appendix 2 - Appendix 2 - Pro Forma Capital Table Pro Forma Capital Table As of March 31, 2012 ($ in thousands, except per share amounts) As Adjusted Actual Minimum $10,000,000.50 Maximum $25,000,000.50 Short-Term Debt: Capital Notes $ 5,450 $ - $ - Long-Term Debt: Trust Preferred Securities 16,496 16,496 16,496 Stockholders' Equity: Common Stock, $2.00 par value; authorized 50,000,000 shares; 10,010,178 shares issued and outstanding at March 31, 2012; 20,310,178 pro forma for minimum; 30,310,178 pro forma for maximum 20,020 40,980 60,980 Additional Paid-in Capital and Warrants 21,689 15,974 10,974 Accumulated Other Comprehensive Loss 81 81 81 Retained Earnings (15,620) (15,620) (15,620) Total Stockholders' Equity $ 26,170 $ 41,415 $ 56,415 Total Capitalization $ 48,116 $ 57,911 $ 72,911 Per Share: Book Value per Share $ 2.61 $ 2.02 $ 1.85 Tangible Book Value per Share $ 2.60 $ 2.02 $ 1.85 Capital Ratios: Tier 1 Leverage Ratio 3.92% 6.44% 8.50% Tier 1 Risk-Based Capital Ratio 6.27% 10.43% 14.04% Total Risk-Based Capital Ratio 9.08% 12.20% 15.32% Tangible Equity to Tangible Assets (period-end) 3.39% 5.31% 7.10% (1) The closing date of the offering is not known as of the date of this prospectus. Consequently, the amount of accrued interest on the capital notes that will be outstanding as of the closing date, and the number of Conversion Shares into which that interest will be convertible, are also not known as of the date of this prospectus. Therefore, the portion of the Conversion Shares related to accrued interest is calculated based on interest accrued through September 15, 2012 in this table. (2) Assumes proceeds invested in cash with a zero risk-weightings. (3) Assumes proceeds added to average assets at period-end. 46 |

Appendix 3 Appendix 3 March 31, 2012 $10 Million Minimum- Less Cost Notes Converted Total New Minimum Effect Tangible Capital $ 26,069,336 $ 9,525,000.50 $ 5,719,839.04 $ 15,244,839.54 $ 41,314,176 # of Shares 10,010,178 6,666,667 3,813,225 10,479,892 20,490,070 Book Value Per Share $ 2.60 $ 1.43 $ 1.50 $ 1.45 $ 2.02 Dilution to existing shareholder $ (0.58) March 31, 2012 All Exercised Subscription Rights $25.0 Million Maximum - Less Cost Notes Converted Total New Effect Tangible Capital $ 26,069,336 $ 24,525,000.50 $ 5,719,839.04 $ 30,244,839.54 $ 56,314,176 # of Shares 10,010,178 16,666,667 3,813,225 20,479,892 30,490,070 Book Value Per Share $ 2.60 $ 1.47 $ 1.50 $ 1.48 $ 1.85 Dilution to Existing Shareholders $ (0.75) Assuming Minimum Amount is Raised Assuming All Subscription Rights are Exercised - Maximum 47 Dilution Dilution Effect Effect if if Existing Existing Shareholders Shareholders Do Do Not Not Participate Participate |

Glossary of terms 48 Allowance for Loan Losses - The allowance for loan losses is maintained at a level that, in management’s judgment, is adequate to absorb credit losses inherent in the loan portfolio. The loan portfolio is analyzed periodically and loans are assigned a risk rating. Allowances for impaired loans are generally determined based on collateral values or the present value of expected cash flows. A general allowance is made for all other loans not considered impaired as deemed appropriate by management. In determining the adequacy of the allowance, management considers the following factors: the nature of the portfolio, credit concentrations, trends in historical loss experience, specific impaired loans, the estimated value of any underlying collateral, prevailing environmental factors and economic conditions, and other inherent risks. While management uses available information to recognize losses on loans, further reductions in the carrying amounts of loans may be necessary based on changes in collateral values and changes in estimates of cash flows on impaired loans. This evaluation is inherently subjective as it requires estimates that are susceptible to significant revision as more information becomes available. Efficiency ratio - The allowance is increased by a provision for loan losses, which is charged to expense and reduced by charge-offs, net of recoveries. Loans are charged against the allowance for loan losses when management believes that collectability of all or part of the principal is unlikely. Past due status is determined based on contractual terms. This ratio indicates the percentage of each dollar of revenue spent to support the entity. It is computed by dividing Non-Interest Expense by Total revenues (Noninterest expense/ (Net interest income + other income)). It indicates how efficiently a bank is spending the revenues generated. Items not included in this calculation include, provision for loan losses, nonrecurring items and income taxes. Net interest margin - This ratio is the average yield earned on average earning assets. It is computed by annualizing net interest income for the period shown and dividing by average earning assets for the period shown. It is one of the most telling indicators of a bank’s profitability as it accounts generally for 90% of pretax income. Loan Risk Ratings: • Pass - Loans in this category are considered to have a low likelihood of loss based on relevant information analyzed about the ability of the borrowers to service their debt and other factors. • Special Mention - Loans in this category are currently protected but are potentially weak, including adverse trends in borrower’s operations, credit quality or financial strength. Those loans constitute an undue and unwarranted credit risk but not to the point of justifying a substandard classification. The credit risk may be relatively minor yet constitute an unwarranted risk in light of the circumstances. Special mention loans have potential weaknesses which may, if not checked or corrected, weaken the loan or inadequately protect the Company’s credit position at some future date. • Substandard - A substandard loan is inadequately protected by the current sound net worth and paying capacity of the obligor or of the collateral pledged, if any. Loans classified as substandard must have a well-defined weakness or weaknesses that jeopardize the liquidation of the debt; they are characterized by the distinct possibility that the institution will sustain some loss if the deficiencies are not corrected. • Doubtful - Loans classified Doubtful have all the weaknesses inherent in loans classified Substandard, plus the added characteristic that the weaknesses make collection or liquidation in full on the basis of currently existing facts, conditions, and values highly questionable and improbable. Other Real Estate Owned – Other real estate owned represents properties acquired through foreclosure or deed taken in lieu of foreclosure. At the time of acquisition, these properties are recorded at the lower of cost or fair value less estimated costs to sell. Expenses incurred in connection with operating these properties and subsequent write-downs, if any, are charged to expense. Subsequent to foreclosure, management periodically considers the adequacy of the reserve for losses on the property. Gains and losses on the sales of these properties are credited or charged to income in the year of the sale. Risk weighted assets - Risk-weighted assets are computed by adjusting each asset class for risk in order to determine a bank's real world exposure to potential losses. Regulators then use the risk weighted total to calculate how much loss-absorbing capital a bank needs to sustain it through difficult markets. |