Table of Contents

FORM 6-K

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

Commission File Number: 1-15270

For the month of July 2024

NOMURA HOLDINGS, INC.

(Translation of registrant’s name into English)

13-1, Nihonbashi 1-chome

Chuo-ku, Tokyo 103-8645

Japan

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F X Form 40-F

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Table of Contents

On June 26, 2024, Nomura Holdings, Inc. filed its Annual Securities Report for the year ended March 31, 2024 with the Director of the Kanto Local Finance Bureau of the Ministry of Finance pursuant to the Financial Instruments and Exchange Act.

Information furnished on this form:

EXHIBITS

Exhibit Number

| 1. |

| 2. |

Table of Contents

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| NOMURA HOLDINGS, INC. | ||||

| Date: July 19, 2024 | By: | /s/ Yoshifumi Kishida | ||

| Yoshifumi Kishida | ||||

| Senior Managing Director | ||||

Table of Contents

Annual Securities Report Pursuant to the Financial Instruments and Exchange Act for the Fiscal Year Ended March 31, 2024

| Page | ||||

| 2 | ||||

Item 1. Information on the Company and Its Subsidiaries and Affiliates | 2 | |||

| 2 | ||||

2. History and Development of the Company and Its Subsidiaries and Affiliates | ||||

| 4 | ||||

4. Subsidiaries and Affiliates | ||||

| 5 | ||||

| 7 | ||||

| 7 | ||||

| 11 | ||||

| 20 | ||||

4. Operating, Financial and Cash Flow Analyses by Management | 35 | |||

| 66 | ||||

6. Research and Development, Patent and Licenses, etc. | ||||

Item 3. Property, Plants and Equipment | ||||

1. Results of Capital Expenditure | ||||

2. Our Properties | ||||

3. Prospects of New Capital Expenditure, Abandonment and Other | ||||

| 67 | ||||

| 67 | ||||

| 73 | ||||

| 74 | ||||

| 75 | ||||

| 128 | ||||

| 129 | ||||

| 256 | ||||

Item 6. Information on Share Handling, etc. | ||||

Item 7. Reference Information | ||||

PART II Information on Guarantor of the Company | ||||

| 269 | ||||

An English translation of the underlined items above is included in this document.

* Status of Directors and Senior Management in Item 4.4. Status of Corporate Governance and Other is not translated.

1

Table of Contents

Item 1. Information on the Company and Its Subsidiaries and Affiliates

(1) Selected consolidated financial data for the latest five fiscal years.

Year ended March 31 | 2020 | 2021 | 2022 | 2023 | 2024 | |||||||||||||||

Total revenue (millions of yen) | 1,952,482 | 1,617,235 | 1,593,999 | 2,486,726 | 4,157,294 | |||||||||||||||

Net revenue (millions of yen) | 1,287,829 | 1,401,872 | 1,363,890 | 1,335,577 | 1,562,000 | |||||||||||||||

Income before income taxes (millions of yen) | 248,261 | 230,671 | 226,623 | 149,474 | 273,850 | |||||||||||||||

Net income attributable to Nomura Holdings, Inc. | 216,998 | 153,116 | 142,996 | 92,786 | 165,863 | |||||||||||||||

Comprehensive income attributable to NHI shareholders | 219,943 | 141,077 | 309,113 | 283,267 | 307,393 | |||||||||||||||

Total equity (millions of yen) | 2,731,264 | 2,756,451 | 2,972,803 | 3,224,142 | 3,448,513 | |||||||||||||||

Total assets (millions of yen) | 43,999,815 | 42,516,480 | 43,412,156 | 47,771,802 | 55,147,203 | |||||||||||||||

Shareholders’ equity per share (yen) | 873.26 | 879.79 | 965.80 | 1,048.24 | 1,127.72 | |||||||||||||||

Net income attributable to NHI common shareholders per share—basic (yen) | 67.76 | 50.11 | 46.68 | 30.86 | 54.97 | |||||||||||||||

Net income attributable to NHI common shareholders per share—diluted (yen) | 66.20 | 48.63 | 45.23 | 29.74 | 52.69 | |||||||||||||||

Total NHI shareholders’ equity as a percentage of total assets (%) | 6.0 | 6.3 | 6.7 | 6.6 | 6.1 | |||||||||||||||

Return on shareholders’ equity (%) | 8.21 | 5.73 | 5.10 | 3.06 | 5.10 | |||||||||||||||

Price/earnings ratio (times) | 6.76 | 11.60 | 11.04 | 16.52 | 17.78 | |||||||||||||||

Cash flows from operating activities (millions of yen) | (94,709 | ) | 667,610 | (862,832 | ) | (694,820 | ) | 132,640 | ||||||||||||

Cash flows from investing activities (millions of yen) | (180,541 | ) | 257,932 | (593,182 | ) | (233,225 | ) | (887,938 | ) | |||||||||||

Cash flows from financing activities (millions of yen) | 807,705 | (668,725 | ) | 1,112,718 | 1,283,937 | 1,012,850 | ||||||||||||||

Cash, cash equivalents, restricted cash and restricted cash equivalents at end of the year (millions of yen) | 3,192,310 | 3,510,011 | 3,316,408 | 3,820,852 | 4,299,022 | |||||||||||||||

Number of staffs | 26,629 | 26,402 | 26,585 | 26,775 | 26,850 | |||||||||||||||

[Average number of temporary staffs, excluded from above] | [4,313 | ] | [4,224 | ] | [4,339 | ] | [4,420 | ] | [4,234 | ] | ||||||||||

| 1 | The selected financial data of Nomura Holdings, Inc. and its consolidated subsidiaries (“Nomura”) were stated in accordance with the accounting principles generally accepted in the United States of America (“U.S. GAAP”). |

| 2 | Shareholders’ equity per share, Total NHI shareholders’ equity as a percentage of total assets, Return on shareholders’ equity are calculated using Total NHI shareholders’ equity. |

| 3 | The consumption tax and local consumption tax on taxable transaction are accounted for based on the tax exclusion method. |

| 4 | Certain contract employees are included in Number of staffs. |

2

Table of Contents

| (2) | Selected stand-alone financial data for the latest five fiscal years |

Year ended March 31, | 2020 | 2021 | 2022 | 2023 | 2024 | |||||||||||||||

Operating revenue (millions of yen) | 348,003 | 328,625 | 355,487 | 472,321 | 557,326 | |||||||||||||||

Ordinary income (millions of yen) | 119,658 | 88,992 | 114,577 | 121,963 | 83,720 | |||||||||||||||

Net income (loss) (millions of yen) | 281,212 | (1,508 | ) | 176,470 | 174,264 | 90,548 | ||||||||||||||

Common stock (millions of yen) | 594,493 | 594,493 | 594,493 | 594,493 | 594,493 | |||||||||||||||

Number of issued shares (thousands of shares) | 3,493,563 | 3,233,563 | 3,233,563 | 3,233,563 | 3,163,563 | |||||||||||||||

Shareholders’ equity (millions of yen) | 2,598,561 | 2,510,710 | 2,546,193 | 2,578,102 | 2,540,897 | |||||||||||||||

Total assets (millions of yen) | 7,535,957 | 7,891,346 | 8,985,161 | 9,514,679 | 10,626,780 | |||||||||||||||

Shareholders’ equity per share (yen) | 855.09 | 819.55 | 843.62 | 858.21 | 855.20 | |||||||||||||||

Dividend per share (yen) | 20.00 | 35.00 | 22.00 | 17.00 | 23.00 | |||||||||||||||

The first quarter | — | — | — | — | — | |||||||||||||||

The second quarter | 15.00 | 20.00 | 8.00 | 5.00 | 8.00 | |||||||||||||||

The third quarter | — | — | — | — | — | |||||||||||||||

The end of a term (the fourth quarter) | 5.00 | 15.00 | 14.00 | 12.00 | 15.00 | |||||||||||||||

Net income (loss) per share (yen) | 87.80 | (0.49 | ) | 57.60 | 57.95 | 30.01 | ||||||||||||||

Net income per share—diluted (yen) | 85.82 | — | 55.86 | 55.95 | 28.79 | |||||||||||||||

Shareholders’ equity as a percentage of total assets (%) | 34.3 | 31.7 | 28.3 | 27.1 | 23.9 | |||||||||||||||

Return on shareholders’ equity (%) | 11.08 | (0.06 | ) | 7.00 | 6.81 | 3.54 | ||||||||||||||

Price/earnings ratio (times) | 5.33 | — | 9.22 | 9.11 | 33.96 | |||||||||||||||

Payout ratio (%) | 22.64 | — | 37.98 | 29.30 | 75.85 | |||||||||||||||

Dividend on shareholders’ equity (%) | 2.46 | 4.28 | 2.64 | 1.98 | 2.70 | |||||||||||||||

Number of staffs | 173 | 154 | 187 | 167 | 185 | |||||||||||||||

[Average number of temporary staffs, excluded from above] | [— | ] | [— | ] | [— | ] | [— | ] | [— | ] | ||||||||||

Total Shareholder Return (%) | 119.4 | 159.0 | 148.0 | 150.8 | 273.5 | |||||||||||||||

[Comparison index with the above : TOPIX Total Return Index] | [90.5 | ] | [128.6 | ] | [131.2 | ] | [138.8 | ] | [196.2 | ] | ||||||||||

Highest stock price (yen) | 586.4 | 721.0 | 614.8 | 573.9 | 1,006.0 | |||||||||||||||

Lowest stock price (yen) | 330.7 | 402.5 | 460.3 | 464.3 | 476.7 | |||||||||||||||

| 1 | Number of staffs represents staffs who work at the Company. |

| 2 | Stock prices are quoted on the Tokyo Stock Exchange (First Section or Prime Market of the Tokyo Stock Exchange). |

| 3 | No net income per share—diluted information was provided, as there was net loss per share, although there are dilutive shares for the years ended March 31, 2021. |

| 4 | No Price/earnings ratio (times) or payout ratio was provided due to the net loss for the years ended March 31, 2021. |

3

Table of Contents

The Company and its 1,529 consolidated subsidiaries and variable interest entities primarily operate investment and financial services business focusing on securities business as their core business. Nomura provides wide-ranging services to customers for both of financing and investment through the operations in Japan and other major financial capital markets in the world. Such services include securities trading and brokerage, underwriting and distribution, arrangement of public offering and secondary distribution, arrangement of private placement, principal investment, asset management and other broker-dealer and financial business. There are also 14 companies accounted for under the equity method as of March 31, 2024.

The reporting of the business operations and results of the Company and its consolidated subsidiaries are based on business segments referred in Note 20 “Segment and geographic information” in our consolidated financial statements included in this annual report. Please refer to the table below in the organizational structure listing the main companies by business segments.

Organizational Structure

The following table lists Nomura Holdings, Inc. and its significant subsidiaries and affiliates by business segments.

Nomura Holdings, Inc.

Retail Division(1)

(Domestic)

Nomura Securities Co., Ltd. and others

Investment Management Division

(Domestic)

Nomura Asset Management Co., Ltd. and others

Wholesale Division

(Domestic)

Nomura Securities Co., Ltd.

Nomura Financial Products & Services, Inc.

Nomura Asia Pacific Holdings Co., Ltd. and others

(Overseas)

Nomura Holding America Inc.

Nomura Securities International, Inc.

Nomura America Mortgage Finance, LLC

Instinet, Incorporated

Nomura Europe Holdings plc

Nomura International plc

Nomura International (Hong Kong) Limited

Nomura Singapore Limited and others

Others

(Domestic)

The Nomura Trust and Banking Co., Ltd.

Nomura Properties, Inc.

Nomura Research Institute, Ltd.(2)

Nomura Real Estate Holdings, Inc.(2)

| (1) | Retail Division has been renamed to Wealth Management Division, effective April 1, 2024. |

| (2) | Affiliates |

4

Table of Contents

(1) Consolidated company

| Year ended March 31, 2024 | ||

| Number of our employees | ||

Total | 26,850 (4,234) |

| 1 | Business segments consist of Retail Division (“Wealth Management Division” since April 2024), Investment Management Division, Wholesale Division and Other. In Japan, we had employees of 7,328 in Retail Division, 1,112 in Investment Management Division, 1,748 in Wholesale Division, and 4,682 in Other. In overseas, we had employees of 11,980, most of which were in Wholesale Division. |

| 2 | Number of our employees consists of full-time employees. The number of non-fulltime employees on annual average is in brackets, not including in number of our employees. |

(2) The Company

| Year ended March 31, 2024 | ||||||

| Number of our employees | Average ages | Average service years | Average annual salary | |||

185 (—) | 45 years and 0 month | 4 years and 8 months | ¥14,089,399 |

| 1 | We had employees of the Company, most of which were in Other in business segments. |

| 2 | Number of our employees consists of full-time employees and the number of non-fulltime employees on annual average is in brackets. |

| 3 | In addition to the employees above, we had employees of 538, who belong to both the Company and Nomura Securities Co., Ltd. |

| 4 | Average annual salary includes bonus and non - standard salary. |

(3) Nomura employees’ union

None

5

Table of Contents

(4) The ratio of females in manager roles and so on

| Subsidiaries | Ratio of female in manager roles (%) (1) (2) | Ratio of male employees taking childcare leave (%) (1) (3) | Gender pay gap (female pay gap) (%) (1) (2) (4) | |||||||||||||||||

| All | Permanent | Fixed Term | ||||||||||||||||||

Nomura Securities Co., Ltd. | 15.7 | 88.3 | 59.9 | 58.6 | 87.6 | |||||||||||||||

Nomura Asset Management Co., Ltd. | 13.3 | 112.0 | 69.2 | 71.0 | 68.8 | |||||||||||||||

The Nomura Trust and Banking Co., Ltd. | 20.8 | 100.0 | 70.2 | 73.3 | 58.0 | |||||||||||||||

Nomura Business Services Co., Ltd. | 24.6 | — | 71.3 | 77.2 | 76.5 | |||||||||||||||

SUGIMURA WAREHOUSE Co., Ltd. | 12.5 | — | 65.1 | 71.7 | 67.6 | |||||||||||||||

SUGIMURA TRANSPORTATION Co., Ltd. | 2.4 | 100.0 | 38.9 | 67.2 | 41.0 | |||||||||||||||

| 1 | The ratio of female in manager roles is as of March 31, 2024, the ratio of male employees taking childcare leave and the gender pay gaps are calculated from April 1, 2023 to March 31, 2024. |

| 2 | The ratio of female in manager roles and the gender pay gaps are calculated according to the Act on the Promotion of Women’s Active Engagement in Professional Life (Act No. 64 of 2015, Japan). |

| 3 | The ratio of male employees taking childcare leave is calculated as the ratio of childcare leave taken according to the Act on Childcare Leave, Caregiver Leave, and Other Measures for the Welfare of Workers Caring for Children or Other Family Members (Act No. 76 of 1991) and Article 71-4 items (ii) of Ordinance for Enforcement of the Act on Childcare Leave, Caregiver Leave, and Other Measures for the Welfare of Workers Caring for Children or Other Family Members (Ordinance of the Ministry of Labor No. 25 of 1991). In companies where the number of male employees who took childcare leave in the current fiscal year exceeded the number of male employees whose spouses gave birth in the current fiscal year, the acquisition rate exceeds 100%. |

| 4 | At our major subsidiaries such as Nomura Securities Co., Ltd., Nomura Asset Management Co., Ltd., The Nomura Trust and Banking Co., Ltd., and Nomura Business Services Co., Ltd., a gender pay gap exists among all employees or permanent employees mainly due to the low percentage of female employees in higher corporate titles or positions which are relatively high in salary. As the percentage of female employees in higher corporate titles or positions increases, it is believed that this wage differential will shrink. Each company sets targets for the ratio of female managerial positions in their action plans to promote the active participation of women. As a common initiative in the group, they incorporate DEI promotion into personnel evaluations. Specifically, for managers, efforts related to the development of female employees’ abilities, the establishment of a workplace environment that accepts diversity, and the promotion of male employees taking childcare leave and the necessary environmental adjustments are identified as essential tasks. The above efforts are yielding tangible results, with Nomura Securities Co., Ltd. achieving the target ratio of female department managers by April 2024, and Nomura Business Services Co., Ltd. achieving the target ratio of female employees in managerial positions ahead of schedule. |

(Reference) Differences in wages between male and female by corporate title at our major subsidiaries.

At Nomura Securities Co., Ltd., looking at the gender pay gap among permanent employees by seniority, it is 89.1% for exempt employees, 82.9% for non-exempt employees, 89.8% for Managing Directors, 101.5% for Executive Directors, 94.0% for Vice Presidents, 78.5% for Senior Associates, 77.0% for Associates, and 91.0% for Analysts.

At Nomura Asset Management Co., Ltd., looking at the gender pay gap among permanent employees by seniority, it is 90.5% for exempt employees and 75.2% for non-exempt employees.

At The Nomura Trust and Banking Co., Ltd., looking at the gender pay gap among permanent employees by seniority, it is 94.7% for exempt employees, 87.7% for non-exempt employees, 94.7% at Manager levels, 86.7% at Shidou-shoku levels, and 98.9% at Gyoumu-shoku / Shokyu-shoku levels.

At Nomura Business Services Co., Ltd., looking at the gender pay gap among permanent employees by seniority, it is 97.4% for exempt employees, 88.4% for non-exempt employees, 95.9% for Managing Directors, 99.1% for Executive Directors, 99.3% for Vice Presidents, 90.2% for Senior Associates, 97.3% for Associates, and 88.7% for Analysts.

6

Table of Contents

Item 2. Operating and Financial Review

1. Management Challenges and Strategies

All matters relating to the future in the sections below are based on the current views as of the date of filing this Securities Report.

(1) Fundamental Management Policy

① Fundamental Management Policy

In Fundamental Management Policy formulated by the Board of Directors, our company has set the following Management Vision and Basic Vision of Group Management.

Fundamental Management Policy of Nomura Holdings, Inc.

(Management Vision)

Nomura Group’s management vision is to enhance its corporate value by deepening society’s trust in the firm and increasing satisfaction of stakeholders, including that of shareholders and clients.

As a global investment bank, the Company will provide high value-added solutions to clients globally, and recognizing its wider social responsibility, the Company will continue to contribute to the economic growth and development of society.

To enhance its corporate value, the Company utilizes return on equity (“ROE”) as a management indicator and will strive for sustainable business transformation.

(Basic Vision of Group Management)

(1) Nomura Group will establish its modernized growth model by itself through realizing expansion of its business in new domains. Nomura Group will also establish an earning structure not subject to market condition with proper cost control and risk management.

(2) Nomura Group will aim to serve its customers at the highest level in every investment, by paying thorough attention to the needs of its customers and the market and by providing its customers with highly value-added solutions in financial and capital markets.

(3) Nomura Group will emphasize compliance with applicable laws and regulations and proper corporate behavior to carry out compliance and conduct risk management in daily business operations. Each company of Nomura Group shall respect customers’ interests and comply with applicable laws and regulations relating to the business.

(4) Nomura Group seeks to ensure effective management oversight and increase management transparency.

(5) Nomura Group will contribute to expanding securities markets through daily business and continuously engage in educational activities regarding investment in order to broaden participation in the securities market. |

② Purpose

Nomura Holdings, Inc. will celebrate its 100th anniversary in December 2025. Nomura is dedicated to the tenets embodied in its Founder’s Principles and the unwavering values ingrained in its Corporate Philosophy. As we look to the next one hundred years, Nomura is pleased to announce its new Group Purpose that will underpin group management:

Purpose

We aspire to create a better world by harnessing the power of financial markets |

Since its founding, Nomura Group has strived to contribute to the development of financial markets. Amid a complex and rapidly changing environment, Nomura will continue to leverage its knowledge and expertise to deliver added value and create a better world through the financial markets. The new Group Purpose articulates Nomura’s strong resolve to work together with various stakeholders to build a better future, and its determination to continue taking on new challenges to become the best company for its clients and other stakeholders.

③ Management Vision

In May 2024, we formulated a new Management Vision for fiscal 2030, “Reaching for Sustainable Growth”, with the aim of promoting management strategies in line with the newly formulated Purpose. Nomura Group continues to engage in the development of the financial and capital markets and the provision of optimal solutions to our clients by facilitating the circulation of risk money through the provision of a wide range of financial services.

7

Table of Contents

(2) Business Environment

During the fiscal year ended March 31, 2024, the global inflation caused by the resumption of economic activities following the COVID-19 pandemic had been somewhat stabilized. Accordingly, some market participants anticipated that the monetary tightening led by the U.S. Federal Reserve (“Federal Reserve”) and other major central banks would come to an end. Toward the end of December 2023, as markets priced in expectations of an early rate cut by the Federal Reserve, and U.S. interest rates declined while U.S. stock prices rose. However, toward the end of the fiscal year ended March 31, 2024, these expectations were somewhat dampened by the strength of the U.S. economy and the persistence of inflationary pressures.

Global economic fundamentals showed resilience, with the U.S. economy growing at an average annual rate of about 4% in the second half of 2023, while stagnation persisted in the Eurozone and China.

In Japan, Kazuo Ueda assumed the post of Governor of the Bank of Japan in April 2023, and expectations for a revision of the large-scale monetary easing policy were further strengthened in May 2023, when the classification of COVID-19 under the Prevention of Infectious Diseases Act was downgraded and economic activity was expected to resume in earnest. On two occasions, in July and October 2023, the Bank of Japan made a decision to more flexibly manage the yield of 10yr JGBs under the policy of controlling long and short term interest rates. Expectations for the realization of a virtuous cycle of wages and prices, which is a condition for the Bank of Japan to lift the monetary easing, and expectations that it may also structurally fortify the earning power of Japanese companies, are gradually growing. Under these circumstances, the Nikkei 225 Stock Average reached the 40,000 yen level for the first time on March 4, 2024, mainly supported by overseas investors buying Japanese stocks.

(3) Management Vision

Our business environment is undergoing significant changes. We will continue to respond to it flexibly while maintaining an appropriate financial standing and effectively utilizing management resources through improved capital efficiency. In addition, we are never satisfied with ourselves and will constantly implement new initiatives with the aim of expanding existing businesses and providing value-added services to clients.

① Medium-to Long-term Priority Issues

We are pursuing sustainable growth across the entire group and working on building a business portfolio that focuses on stable and diversified revenue and improving capital efficiency.

Our vision is to advance Nomura to the next stage. To realize this, we launched a strategy of expanding into private markets to complement our businesses in the public markets. Based on this strategy, we have been working on promoting our asset consulting business, strengthening the Investment Management Division, and fostering growth and stability in the wholesale business. Additionally, we have been exploring and enhancing new areas such as Digital Financial Services including the digital asset business and sustainability sector including sustainable finance. We have also begun to promote company-wide cost control through structural reforms. In addition, we are advancing the sophistication and efficiency of the corporate functions that form the basis of these businesses, strengthening the governance structure, improving operational efficiency using digital technologies, and promoting our own sustainability initiatives such as Diversity, Equity & Inclusion (DEI) and net zero greenhouse gas emissions. For more information on the strategies in each division, please refer to “② Issues in Each Division.”

We have established a business model that can consistently achieve an ROE of 8-10% in the medium term through addressing medium- to long-term priority issues. As announced in May 2024, we have set a new management vision, “Reaching for Sustainable Growth”, as an indication of the direction of management toward fiscal 2030, and a management quantitative target of ROE of 8-10%+ and achieving profit before tax of over ¥500 billion. We will focus on the following areas to achieve these goals: (i) deepen global strategy leveraging Japan franchise, (ii) achieve sustainable growth of stable revenues, and (iii) further promote strategy to provide platforms. In addition, we break down the Price Book-value ratio (“PBR”) as shown in the figure below. Maximizing the absolute level of ROE is one of its key elements. Through addressing medium- to long-term priority issues, we aim to enhance our corporate value.

8

Table of Contents

② Issues in Each Division

The challenges and strategies in each division are as follows:

| • | Wealth Management Division |

As a result of the continuous initiatives to overhaul our business model to further help clients manage their assets, the former Retail Division has seen significant changes in its revenue structure, leading to certain achievements in transitioning to the recurring revenue business. The Division has been renamed the “Wealth Management Division” to reflect this transformation of the business model, effective April 1, 2024.

To contribute to the improvement of the ratio of securities among Japanese households, our challenge is to respond to diversifying wealth management needs. By providing comprehensive wealth management services through our nationwide network of branches, as well as our digital services, we aim to assist our clients in achieving their goals. We will continue working on improving the skills of our partners (sales representatives), and enhance our wide range of products and services in order to advance the wealth management business.

| • | Investment Management Division |

Our Investment Management Division provides solutions that meet the diversifying investment needs of our broad clients through a wide range of assets classes and services spanning both traditional and alternative assets. We aim to realize a virtuous cycle of investment that leads to the resolution of social issues by providing high-quality investment products that meet the diverse investment needs of clients. We regard the following trends as growth opportunities: Japan’s abundant individual financial assets and the tailwind of the government’s plan for promoting Japan as a leading asset management center, the growth of investment in private assets, high levels of funding demand for and investor awareness of sustainability-related investments. Amid continued downward pressure on management fees, we are working to improve our investment capabilities, increase our assets under management and increase the value added by our products and services in our public markets businesses, expand our business platforms in alternative assets and other high-fee growth areas, and realize greater efficiency and cost control.

| • | Wholesale Division |

Our Wholesale Division faces challenges presented by increasingly sophisticated client needs and technological advancement, coupled with uncertainty in the market and macroeconomic environment. To ensure continuity of service as well as adding value to clients, we will continue to enhance collaboration across business lines, regions and divisions while further diversifying our business portfolio to stabilize revenues. We will continue to deploy financial resources to selective and high growth opportunities and also focus on cost optimization.

Global Markets aims to provide uninterrupted liquidity to our clients while reinforcing risk control and governance. Additionally, we aim to further diversify our business portfolio, reinforce global connectivity and cross-sell across our global client franchise leveraging our solid business foundation in Japan and competitive global products to pursue growth opportunities such as Structured Financing and Solution business, International Wealth Management business as well as Global Equities, and continue to build on the strength of our Flow Macro businesses.

Investment Banking aims to provide seamless client experiences as we target to accelerate advisory services and financing to domestic as well as cross-border restructurings and industry-wide consolidations, as well as interest rate and foreign exchange solutions as volatile business environments impact our clients’ businesses. We will leverage our Japanese strengths and focus on expanding our global advisory business, while also maintaining focus on sustainability in light of its importance within the industry and to our clients. Additionally, we will accelerate group-wide collaborations as we develop tailored advice for the benefit our clients across a range of products and services.

| • | Risk Management and Compliance, etc. |

We have defined our risk appetite in our Risk Appetite Statement which includes the types and level of risk that the Nomura Group is willing to assume in pursuit of our strategic objectives and business plans. Further, we continue to develop our risk management framework in a way that is strategically aligned to our business plans and incorporates decision-making by senior management, thereby securing capital soundness and enhancing our corporate value.

We have clearly defined in our Risk Appetite Statement that all executives and employees must actively engage in risk management through our Three Lines of Defense framework. Besides, we continuously provide trainings to all executives and employees including those in the group companies to increase our knowledge about risks as financial professionals and develop a corporate culture of correctly recognizing, assessing and managing risks.

9

Table of Contents

With regard to compliance, we continue to focus on improving the management structure to comply with local laws and regulations in the countries where we operate. We also continue to review our internal systems and rules so that all executive management and employees can work autonomously with high ethical standards.

In order to ensure not only compliance with laws and regulations, but also that all directors, officers and employees are able to act in accordance with social norms, we have established the “Nomura Group Code of Conduct” as guidelines for actions to be taken, and through associated trainings and other measures, we are working to promote appropriate actions (“Conduct”) based on the Code of Conduct. At the “Nomura Founding Principles and Corporate Ethics Day” held in every August, we reaffirm the lessons learned from past incidents and renew our determination to prevent similar incidents then to maintain and gain the trust society places in us; discussions are held regarding the proper way to conduct after looking back on past incidents, and a pledge is made to comply with the Code of Conduct. In order for us to be able to respond to the changing demands of society, the Code of Conduct is regularly reviewed to constantly examine ourselves and to ensure that our thinking aligns with society’s norms.

By addressing and resolving the above issues, we will strive for the stability and further development of financial markets as well as the sustainable growth of the Nomura Group.

10

Table of Contents

2. Views on Sustainability and efforts

(1) Nomura’s Basic Views on Sustainability

Since its founding, Nomura has been engaged in the creation of not only economic value but also social value by circulating risk money through the provision of a wide range of financial services, developing financial and capital markets, and providing optimal solutions to customers.

Nomura sees sustainability from two perspectives: “Support the sustainability initiatives of customers and diverse stakeholders as a financial services group” and “Promotes activities such as reducing environmental impact, respecting human rights, and enhancing governance to ensure a sustainable existence for Nomura.”

| • | Supporting the sustainability initiatives of customers and diverse stakeholders as a financial services group |

Our core role as a financial services group is to support customers through the flow of funds and capital. We believe it is important to strengthen our functions to promote the sustainable circulation of funds by underwriting green bonds and social bonds issued by companies and financial institutions, providing strategic advisory services such as M&A advisory, and by developing ESG-related funds as investments and providing them to individual investors in Japan, in order for Nomura to be selected as our customers’ partner. Nomura sees financing of sustainable causes as a business opportunity to expand the range of services and solutions. In particular, in order to strengthen and promote sustainable finance initiatives, we have set a target of engaging $125 billion in sustainable finance projects in Japan and overseas over the five fiscal years ending March 31, 2026.

In addition, we seek to take advantage of the Group’s comprehensive strengths in providing solutions to social issues by leveraging the functions we have cultivated over many years, including support for business succession, promoting innovation in the fields of regional revitalization, agriculture and medical care, and our expertise and knowledge in the field of research and analysis. Nomura has been a frontrunner in providing financial education programs for people of all ages, ranging from children to adults for more than 20 years, dating back to the 1990s. As the Japanese government aims to realize a virtuous cycle of growth and distribution, in which Japan’s household savings flow more into productive investment, and the benefits of increased corporate value are returned to households, leading to further private sector investment and consumption, under its “Policy Plan for Promoting Japan as a Leading Asset Management Center”, improving financial literacy in Japan is an extremely important issue. In addition to financial education centered on school education, we will also actively seek to support asset building through the workplace for working generations, contribute to the improvement of financial literacy throughout society, and work to develop financial and capital markets through sustainable financial circulation.

| • | The Company’s efforts to continue being a sustainable corporate group |

Nomura recognizes that addressing environmental issues and respecting human rights are essential elements in the realization of a sustainable society.

Nomura has announced its goal of achieving net zero greenhouse gas (“GHG”) emissions for its own operations by 2030, and to seek to achieve net zero GHG emissions attributable to its lending and investment portfolios by 2050 and are working on that goal.

In accordance with the Nomura Group Human Rights Policy, Nomura Group is actively working to improve and enhance its efforts to address human rights issues and promote respect for human rights through the development of various systems and the implementation of training programs. These efforts are regularly discussed by the Sustainability Committee, which is described below, and efforts are made to disclose appropriate information. The Company will further promote its efforts to realize a sustainable society by participating in various initiatives, including the Net Zero Banking Alliance (“NZBA”), an international framework established by the United Nations Environment Program Finance Initiative (“UNEP FI”).

The evolution of human resource management strategies is essential to realize sustainable growth and corporate value improvement through solving social issues. For this reason, Nomura is working to differentiate the human resource management cycle of recruitment, talent development, performance appraisal, and mobility and advancement strategies, promote DEI, create an environment that enables diverse employee working styles, and enhance wellbeing and a sense of belonging. We are working to build a cycle in which people, who are the source of Nomura’s competitiveness, play an active role and provide high added value. (For details, please refer to “(5) Human capital initiatives”.)

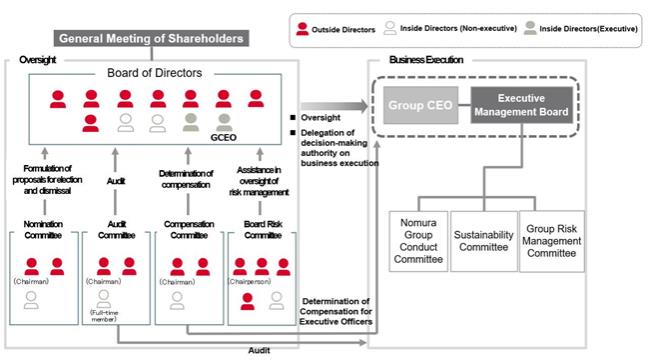

(2) Nomura’s Sustainability-Related Governance

Nomura is a Company with Three Board Committees under Japanese law, separating management oversight and business execution to strengthen corporate governance. The oversight function and the executive side play respective roles in recognizing climate change risks and opportunities, promoting various measures, and managing risks.

11

Table of Contents

① Board of Directors

The Board of Directors offers advice on sustainability related reports prepared by executive officers, based on our basic sustainability policy which states: “Nomura will contribute to the creation of a truly enriched society through our business activities based on the principles embodied in the Nomura Group Corporate Philosophy, and actively pursue initiatives to resolve social issues and create a sustainable world.”

Exchange of opinions regarding sustainability also occur out meetings of our outside directors, which are held periodically in order for outside directors to discuss our business and our corporate governance. Such exchange also occurs at our Internal Controls Committee, which is consisted of multiple directors and executive officers, and at our Audit Committee. In the fiscal year ended March 31, 2024, we dealt with topics such as the establishment of human rights policies and the disclosure of sustainability-related information.

② Sustainability Committee

Nomura has established the Sustainability Committee chaired by the Group CEO and which also consists of other persons designated by the Group CEO including the members of the Executive Management Board to deliberate and make decisions on strategies to promote sustainability. The Chief Sustainability Officer leads discussions in the Sustainability Committee to consolidate the company’s sustainability knowledge and accelerate the formulation and promotion of strategies. In the fiscal year ended March 31, 2024, we covered topics such as the establishment of human rights policies, information disclosure related to sustainability, efforts to achieve net zero and participation in various initiatives.

12

Table of Contents

③ Sustainability Forum

In order to ensure opportunities for more flexible and substantive discussions on sustainability, the Sustainability Forum, as a forum for discussion by executives from across departments and regions, has been established in the fiscal year ended March 31, 2024. This forum is an evolutionary reformation of the Sustainability Council, established in August 2021, and is divided into the Sustainability Business Forum, which deals with topics more closely related to business activities, and the Sustainability Corporate Forum, which deals with information disclosure and policy formulation. The forum has a flexible structure, such as changing the participant member depending on the topics covered. In the fiscal year ended March 31, 2024, we discussed the concept of reducing emissions in our investment and loan portfolio based on the NZBA framework and the content of our human rights policy.

(3) Nomura’s Risk Management on Sustainability

Increasing attention to the management of Sustainability matters makes it imperative that we continue to develop policies and capabilities in these areas, and that we position ourselves in a positive light to interested stakeholders including our shareholders, clients and society at large. Amid rapidly changing circumstances around Sustainability, lack of sufficient focus such as on environmental policies, human rights and diversity, equity & inclusion considerations may also adversely affect our reputation, results of operations and financial condition. In particular, we recognize that climate change risks are likely to have an impact over the medium to long term, and we seek to manage these risks under appropriate management systems.

① Recognition of the Risks Associated with Climate Change

Nomura recognizes risks arising from changes in the environment due to climate change and identifies the potential impact on our business. There are two types of risks associated with climate change: the risk of loss or damage due to extreme weather events such as large typhoons, droughts, and intense heat (physical risk), and the risks associated with decarbonization, such as the inability to respond to changes in government policies or rapid technological innovations (transition risk). Nomura recognizes the following physical and transition risks associated with climate change.

| • | Risk that clients will not adequately respond to climate change, resulting in financial damage, decline in creditworthiness and inability to fulfil their contractual obligations |

| • | Risk that climate change causes market fluctuations and losses are incurred due to fluctuations in the market price of Nomura’s financial assets |

| • | Risk of reputational damage if Nomura and counterparties fail to respond appropriately to climate change |

| • | Risk of financial losses or reputational damage due to inadequate or failed internal processes and employee response to climate change |

| • | Risk of inadequate strategies or failed execution of strategies as compared with competitors, and risk of gap between strategies and resources |

② Our approach on Risks Associated with Climate Change

Climate risk is recognized as one of risks that are understood to potentially impact Nomura adversely if they materialize. Climate risk is not recognized as a standalone risk, but is understood to be a risk factor affecting various risk areas. Nomura has built an integrated risk management framework that manages the risks caused by climate change by adding new responses to the ones into the existing risk management frameworks.

(4) Metrics and Targets

Nomura Group uses metrics related to greenhouse gas emissions to measure and manage the risks and opportunities associated with climate change, with the approval of the Sustainability Committee, as well as to steadily implement initiatives to align with the Paris Agreement and achieve net zero.

The progress is also reported regularly to the board of directors. The result for each metric for the fiscal year ended in March 2024 will be disclosed in the integrated report scheduled to be issued at the end of August 2024.

13

Table of Contents

| # | Metrics | Target | Results (FY2021/22) | Results (FY2022/23) | ||||

| 1 | Greenhouse gas emissions from its own operations (Scopes 1 and 2) (ø1) | Net Zero by 2030 | Scope 1 : 1,924 t-CO2 Scope 2 : 31,710 t-CO2 | Scope 1 : 2,473 t-CO2 Scope 2 : 24,183 t-CO2 | ||||

| 2 | Greenhouse gas emissions from its lending and investment portfolios (Scope 3, Category 15) (based on the NZBA framework) (ø2) | Net Zero by 2050 | Power generation sector GHG emissions: 3,647 (1,250) kt CO2e Economic emission intensity: 3,458 (1,186) t-CO2e/$m

(As of the end of March 2022) | Power generation sector GHG emissions: 4,662 (1,673) kt CO2e Economic emission intensity: 3,422 (1,229) t-CO2e/$m

(As of the end of March 2023) | ||||

| 3 | Sustainable financing (ø3) | US$125bn in sustainable financing over five years by March 2026 | US$21.4 bn | US$25.1 bn |

| (ø1) | Scope 2 emissions are calculated using the market-based method based on the GHG Protocol. The market-based method is a method of calculating Scope 2 emissions reflecting companies’ electricity contract. As the emission factor is based on the contractual terms, if a company purchases low-carbon electricity, such as from renewable energy sources, the effect can be reflected. |

| (ø2) | The values in the parentheses in the chart are consistent with emissions factors used by PCAF before June 2023. |

| (ø3) | This target includes capital raised through Nomura’s debt and equity capital markets businesses, private placements of mezzanine debt and equity securities, and debt financing through its Infrastructure and Power Financing Group. |

(Factors considered in each goal setting)

| • | Regarding the Greenhouse gas emissions from its own operations, targets are set based on comprehensive consideration of the results of energy conservation efforts, the spread of renewable energy, and the ratio of installed renewable energy. |

| • | Regarding the Greenhouse gas emissions from its lending and investment portfolios, based on the NZBA framework, targets are set by referring to the International Energy Agency’s NZE scenarios and the emission factor database provided by PCAF. |

| • | Regarding the Sustainable financing, target is set by referring to the assumed market size of sustainable finance provided by external vendors. |

14

Table of Contents

(5) Human Capital Initiatives

① Embedding Purpose and Maximize Our Corporate Value through the Evolution of Human Resources Management Strategy

We have declared our Group Purpose as “we aspire to create a better world by harnessing the power of financial markets”. In order to further embed our Group Purpose and to maximize our corporate value, we seek to improve our return on equity (ROE) through investing strategically for growth. We believe it is essential to enhance the competitive strength of our employees (human capital) in order to enhance productivity, build value for our clients and shareholders, and enrich our risk management culture by realizing the potential of our dedicated and professional workforce.

Nomura aims to enhance employee engagement by evolving its talent management strategy from a long-term perspective. Nomura seeks to differentiate intellectual capital (*) that our human capital delivers as a team and further enhance the added value provided by the Nomura Group.

* Our intellectual capital refers to the intangibles that are the source of our competitiveness, including organizational capabilities, know-how, customer networks, and branding.

② Nomura Group’s Human Resources Management Strategy

Our human resources management strategy is based on the values of “Entrepreneurial Leadership”, “Teamwork”, and “Integrity” as defined in our corporate philosophy, and these core values set us apart from our competitors in our recruitment, talent development, performance appraisal, and mobility and advancement strategies, as well as our dedication to promoting “Diversity, Equity & Inclusion” (DEI), “Employees’ Ways of Working”, and “Wellbeing”. This strategy forms the core of our recruitment, talent development and retention initiatives.

i Recruitment

We seek to recruit individuals who share our values of “Entrepreneurial Leadership”, “Teamwork”, and “Integrity” and are aligned with our strong risk management culture. In order to attract and develop such individuals who also can demonstrate strong expertise, we recruit individuals in all roles and at all career levels in all regions including Japan, through both new graduate programs and mid-career hiring.

We focus our lateral recruitment on hiring professional talent with advanced knowledge and experience in their specialized fields. In recent years, more than half of Nomura Group’s hires have been mid-career hires.

From January 2023, we have established alumni networks and recruitment strategies to help stay connected and regularly re-engage with our pool of alumni who remain active in the industry and communities. As of March 31, 2024, the number of registrants on the network site has reached approximately 250, showing an increase of approximately 90 compared to the previous year, solidifying the foundation of the network.

ii Talent Development

We are committed to developing our talent under the Basic Policy of Talent Development as listed below.

<Basic Policy of Talent Development>

In order to further embed our Group Purpose, “we aspire to create a better world by harnessing the power of financial markets”, we aim for people in the Nomura Group to differentiate themselves by being professionals that continually take on new challenges to create added value.

When it comes to development of professional talent and leadership talent, we will allocate resources to the following three areas. (i) Hierarchical training for new employees and managerial staff, (ii) self-improvement programs to encourage autonomous learning among employees, and (iii) department-specific training that allows for intensive learning of specialized knowledge and skills. As an example of (ii) the self-improvement program, we launched our Digital IQ University program in the fiscal year ended March 31, 2024. This program enables employees, regardless of whether they are involved in IT operations, to systematically acquire a wide range of knowledge and skills related to digitalization. Additionally, in (iii) department-specific training, for example, in our Investment Banking (Wholesale Division), we provide a knowledge management platform called “M&A University”. By utilizing this platform, employees can learn specialized knowledge in M&A advisory services and apply it in practical work.

Additionally, we are implementing various selective training programs. Specifically, the following programs are available:

15

Table of Contents

Study Abroad Program—For more than 60 years, we have offered tuition assistance programs to employees in Japan in order to support their self-improvement goals through study abroad programs.

Venture company training program—We launched our venture company training program to provide our employees with work experience at venture companies in Japan. Through this program, we encourage employees to gain experience outside of the Nomura Group and promote a culture of accepting diverse values when they return to the Nomura Group.

Nomura Keiei-juku—We have an in-house senior management development program in Japan. The participants are selected from the entire Nomura Group and are given opportunities to have discussions with senior executives. Through these discussions, participants gain direct exposure to senior executive perspectives and are able to deepen their own vision, self-awareness, and determination as candidates of future management.

Nomura Management School—We send senior executives to executive programs operated by external educational institutions. By providing participants with the opportunity to enroll in high-quality executive education programs led by world-class instructors who are experts in various fields, including top-tier instructors from overseas universities, we are focusing on successor development.

iii Performance Appraisal

In all regions including Japan, and across all departments and roles, we are making further efforts to enhance our performance-based compensation system, through ensuring the fairness of performance appraisals and benchmarking employee productivity against external market data. All managers in Japan are paid by job type.

We have also introduced 360-degree feedback globally, and by engaging in dialogue between the target employee and the evaluators regarding the results, we are supporting the growth and leadership development of the employee. Additionally, we have implemented the ERCC (Ethics, Risk Management, Compliance and Conduct) rating, which is a compliance and conduct evaluation, in order to further permeate our code of conduct throughout the organization and sophisticate risk management.

iv Mobility and Advancement

We respect employees’ entrepreneurial mindsets and encourage autonomous career development. While we had a global internal job posting system in place before, we significantly expanded the scope of this system in Japan starting from the fiscal year ended March 31, 2021. Regardless of corporate title, many employees have actively applied to this system across departmental boundaries, enabling them to pursue new career opportunities through job rotations.

Additionally, from the perspective of appointing talent to key positions within the group and developing successors for such positions, we globally manage a talent pool of individuals with the potential to assume critical roles. Assessments are conducted for these talent pools, and various leadership development programs are provided to the respective employees based on their leadership potential.

v DEI (Diversity, Equity & Inclusion)

We believe that diversity helps improve our competitiveness, innovation, and advanced risk management. In July 2016, we adopted our “Declaration on Diversity and Inclusion” initiative, in which we committed to create a work environment where all employees can demonstrate their capabilities and realize their full potential. In October 2022, we further updated this initiative with the addition of the concept of “equity” to become our “Group Diversity, Equity and Inclusion Statement”. Equity from our perspective differs from equality, in that it is less about allocating the exact same resources and opportunities to everyone (equality), but more about providing the best resources and opportunities to each of our employees according to their different circumstances and needs, and therefore creating an equitable space where everyone can meet their objectives. We aim to create a workplace that provides fair and equitable opportunities for our diverse employees and which instills a strong sense of belonging.

Our DEI Working Group, which consists of Executive Officers, Senior Managing Directors, heads of group companies and global regions, aims to create such a work environment across the group using a top-down approach. Additionally, our DEI Employee Network, which consists of voluntary employee networks, engages in diversity awareness-raising activities at Nomura offices worldwide through a bottom-up approach.

16

Table of Contents

In order to further accelerate DEI promotion efforts, NSC made efforts to deepen understanding of and promote DEI as a new evaluation item in the fiscal year ended March 31, 2024. In particular, the following were designated as essential issues for managers: creation of a work environment where diversity is accepted, encouragement of male employees to take childcare leave and creation of an environment for doing so, and efforts to increase the abilities of female employees to promote the advancement of women. In addition, each domestic subsidiary (excluding some joint ventures, etc.) have introduced an incentive program to encourage male employees to take childcare leave. The program provides incentives to employees who take childcare leave for one month or longer regardless of gender.

vi Employees’ Ways of Working

We launched our global “Nomura Ways of Working” project, which aims to create a positive working environment where our employees can maximize their performance without time or location constraints since the fiscal year ended March 31, 2023. We are promoting this project globally across regions based on four key pillars; culture, people, workplace and technology.

Also, we launched a program called COMPASS to support both new employees joining Nomura Group and existing employees in the fiscal year ended March 31, 2024. We provide useful tools and support to help employees smoothly integrate into us and fully demonstrate their abilities from the first day of joining to the 100th day.

vii Wellbeing

Under the Fundamental Approach of an Employee-friendly Work Environment listed below, we are fully committed to development of employee wellbeing.

< Fundamental Approach of an Employee-friendly Work Environment >

Nomura Group recognizes the importance of our employees’ physical, emotional, mental and financial wellbeing so that they can realize their full potential, stay motivated and excel in the performance of their duties.

We seek to improve employee welfare programs, such as childcare and nursing care support, as well as to maintain and promote employee health, so that employees can continue to work with enthusiasm, including the development of appropriate working conditions and a comfortable working environment.

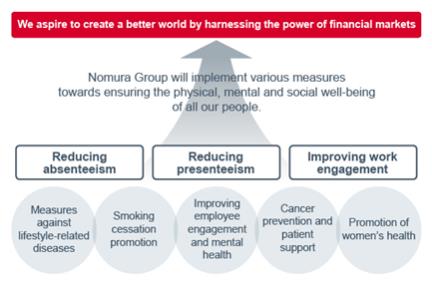

We also recognize the need to reduce Absenteeism (1) and Presenteeism (2), and improve Work Engagement (3) in order for employees to achieve complete physical, mental and social well-being, and have set the following measurements in order to monitor employee wellbeing:

17

Table of Contents

| Measurements (4) | Targets (4) (Year ending March 31, 2026) | |||||||||||||||

| Year ended March 31, 2022 | Year ended March 31, 2023 | Year ended March 31, 2024 | ||||||||||||||

Absenteeism (millions of yen) | 1109.7 | 794.7 | 794.7 | — | ||||||||||||

Presenteeism (%) | 15.2 | 16.1 | 16.4 | 10 | ||||||||||||

Work Engagement | 53.4 | 53.7 | 53.3 | 60 | ||||||||||||

| (1) | Absenteeism: The impact of absenteeism is measured by financial losses due to absence from work caused by injury or illness, calculated by multiplying the average compensation of employees per financial year by the number of employees and the utilization rate of sick leave during that year. |

| (2) | Presenteeism: A condition in which individuals go to work despite being ill or experiencing symptoms of illness, with a negative impact on business execution and productivity. The figure is calculated based on responses to the SPQ (Single-Item Presenteeism Question, Tokyo University 1-Item Version). |

| (3) | Work Engagement: A positive, fulfilling, work-related state of mind. This is measured based on deviation from the results of the national average of annual stress assessment, which is an annual mandatory workplace program in Japan to screen for mental health issues in workers. |

| (4) | The Target figures are for the Nomura Group, and the Measurement figures are for NSC, our major consolidated subsidiary. |

18

Table of Contents

We also support the financial wellbeing of our employees globally by offering various programs and advice including the granting of compensation awards through employee share ownership plans, a defined contribution pension plan and posting financial wellbeing information on our intranet. Since the fiscal year ended March 31, 2024, at NSC, we are providing video content (Nomura Financial Wellness Program) that allows for a quick understanding of retirement benefits and pension systems, as well as holding workshops on defined contribution pensions.

viii Engagement Survey

As part of our ongoing efforts to evaluate and improve our various human resource strategies, we have conducted our Nomura Group Employee Survey annually since the fiscal year ended March 31, 2014. We believe that the survey provides valuable insights regarding employee engagement and perceptions about Nomura. The results are reviewed by our senior management and used for refinement or planning of our human resource strategies, programs and practices. In the fiscal year ended March 31, 2024, over 80% of our employees who participated in the Survey gave a positive response to the question “I am proud to work for the firm”.

In addition, starting from the fiscal year ended March 31, 2024, we have begun conducting a “Pulse Check Survey” every quarter with randomly selected employees, aiming to hear employees’ voices on a regular basis, with the goal of increasing the frequency to help improve working conditions and employee satisfaction.

ix Retention

In recent years, the mobility of human resources has increased globally in many industries, including in financial services, and our global employee turnover rate has also increased. To enhance engagement, we have established a system to discuss and implement solutions for the issues identified in the results of the surveys mentioned above.

19

Table of Contents

You should carefully consider the risks described below before making an investment decision. If any of the risks described below actually occurs, our business, financial condition, results of operations or cash flows could be adversely affected. In that event, the trading prices of shares of NHI could decline, and you may lose all or part of your investment. In addition to the risks listed below, risks not currently known to us or that we now deem immaterial may also harm us and affect your investment.

INDEX

● Risks Relating to the Business Environment

| 1 | Our business may be materially affected by financial markets, economic conditions and market fluctuations in Japan and elsewhere around the world, including the ones caused by geopolitical events |

| (1) | Governmental fiscal and monetary policy changes in Japan, or in any other countries or regions where we conduct business may affect our business, financial condition and results of operations |

| (2) | Extended market declines and decreases in market participants can reduce liquidity and lead to material losses |

| (3) | Natural disaster, terrorism, military dispute and infectious disease could adversely affect our business |

| 2 | The financial services industry faces intense competition |

| (1) | Competition with other financial firms and financial services by non-financial companies is increasing |

| (2) | Increased consolidation, business alliance and cooperation in the financial services industry mean increased competition for us |

| (3) | Our global business continues to face intense competition and may require further revisions to its business model |

| 3 | Event risk, including the ones caused by geopolitical events, may cause losses in our trading and investment assets as well as market and liquidity risk |

| 4 | Sustainability factors including climate change and broader associated policy changes in each jurisdiction could adversely affect our business |

● Risks Relating to Our Businesses

| 5 | Our business may incur losses due to various factors in the conduct of its operations |

| (1) | We may incur significant losses from our trading and investment activities |

| (2) | Holding large and concentrated positions of securities and other assets may expose us to significant losses |

| (3) | Our hedging strategies may not prevent losses |

| (4) | Our risk management policies and procedures may not be fully effective in managing risk |

| (5) | Market risk may increase other risks that we face |

| (6) | Our brokerage and asset management revenues may decline |

| (7) | Our investment banking revenues may decline |

| 6 | We may be exposed to losses when third parties do not perform their obligations to us |

| (1) | Defaults by a large financial institution could adversely affect the financial markets generally and us specifically |

| (2) | There can be no assurance as to the accuracy of the information about our credit risk, or the sufficiency of the collateral we use in managing it |

| (3) | Our clients and counterparties may be unable to perform their obligations to us as a result of political or economic conditions |

| 7 | We are exposed to model risk, i.e., risk of financial loss, incorrect decision making, or damage to our credibility arising from model errors or incorrect or inappropriate model application |

| 8 | NHI is a holding company and depends on payments from its subsidiaries |

| 9 | We may not be able to realize gains we expect, and may even suffer losses, on our investments in equity securities and non-trading debt securities |

| 10 | We may face an outflow of clients’ assets due to losses incurred within cash reserve funds or debt securities we offer to clients |

20

Table of Contents

● Risks Relating to Our Financial Position

| 11 | We may have to recognize impairment losses with regard to the amount of goodwill, tangible and intangible assets recognized on our consolidated balance sheets |

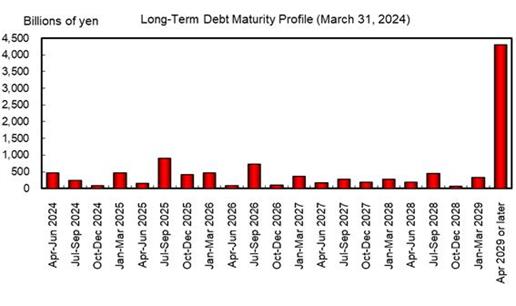

| 12 | Liquidity risk could impair our ability to fund operations and jeopardize our financial condition |

| (1) | We may be unable to access unsecured or secured funding |

| (2) | We may be unable to sell assets |

| (3) | Lowering of our credit ratings could impact our funding |

| 13 | Equity investments in affiliates and other investees accounted for under the equity method in our consolidated financial statements may decline significantly over a period of time and result in us recognizing impairment losses |

● Risks Relating to Legal, Compliance and Other Operational Issues

| 14 | Operational risk could adversely affect our business |

| 15 | We identified a material weakness in our internal control over financial reporting and, despite our efforts to remediate, may identify further material weaknesses in the future |

| 16 | Misconduct or fraud by an employee, director or officer, or any third party, could occur, and our reputation in the market and our relationships with clients could be harmed |

| 17 | A failure to identify and appropriately address conflicts of interest could adversely affect our business |

| 18 | Our business is subject to substantial legal, regulatory and reputational risks |

| (1) | Legal liability related to our business may occur and could adversely affect our business, financial condition and results of operations |

| (2) | Extensive regulation of our businesses limits our activities and may subject us to significant penalties and losses |

| (3) | Tightening of regulations applicable to the financial system and financial industry could adversely affect our business, financial condition and results of operations |

| (4) | Deferred tax assets may be impacted due to a change in business condition or in laws and regulations, resulting in an adverse effect on our operating results and financial condition |

| (5) | Defects in our anti-money laundering and counter-terrorism financing measures could have serious consequences such as, administrative penalties or punitive fines |

| 19 | Unauthorized disclosure or misuse of personal information held by us may adversely affect our business |

| 20 | System failure, information leakage and cost of maintaining sufficient cybersecurity could adversely affect our business, financial condition and results of operations |

| 21 | Our business may be adversely affected if we are unable to hire, retain and develop qualified personnel |

21

Table of Contents

● Risks Relating to the Business Environment

1. Our business may be materially affected by financial markets, economic conditions and market fluctuations in Japan and elsewhere around the world, including the ones caused by geopolitical events

Our business and revenues may be affected by any adverse changes or volatility in the Japanese and global economic environments and financial markets. In addition, not only purely economic factors but also military dispute, acts of terrorism, economic or political sanctions, pandemics, forecasts of geopolitical risks and geopolitical events which have actually occurred, natural disasters or other similar events could have an effect on the financial markets and economies of each country. Geopolitical events include cases such as tensions between the United States and China, the invasion of Ukraine by the Russian Federation, and the geopolitical tensions in the Middle east and in Asia. If any adverse events including those discussed above were to occur, a market or economic downturn may last for a long period of time, which could adversely affect our business and can result in us incurring substantial losses. In addition to conditions in financial markets, social conditions such as the long-term trends of population aging and population decline faced by Japan are expected to continue to put downward pressure on demand in the businesses in which we operate, including, in particular, our retail business. The following are certain risks related to the financial markets and economic conditions for our specific businesses.

(1) Governmental fiscal and monetary policy changes in Japan, or in any other countries or regions where we conduct business may affect our business, financial condition and results of operations

We engage in our business globally through domestic and international offices. Governmental fiscal, monetary and other policy changes in Japan, or in any other countries or regions where we conduct business may affect our business, financial condition and results of operations. In addition, any changes to the monetary policy of the Bank of Japan or central banks in major economies worldwide, which could potentially lead to volatility of interest rate or yields may negatively affect our ability to provide asset management products to our clients as well as our trading and investment activities. For example, on March 19, 2024, the Bank of Japan ended its negative interest rate policy. While so far such change has not materially affected our business, the future of the Bank of Japan’s policies and the potential effect of such changes on our business remain uncertain.

(2) Extended market declines and decreases in market participants can reduce liquidity and lead to material losses

Extended market declines can reduce the level of market activity and the liquidity of the assets traded in those markets in which we operate. Market liquidity may also be affected by decreases in market participants, for example, if financial institutions scale back market-related businesses due to increasing regulation or other reasons. As a result, it may be difficult for us to sell, hedge or value such assets. In the event that a market fails in pricing such assets, it will be difficult to estimate their values. If we cannot properly close out or hedge our associated positions in a timely manner or in full, particularly with respect to Over-The-Counter (“OTC”) derivatives, we may incur substantial losses. Further, if the liquidity of a market significantly decreases and the market becomes unable to price financial instruments held by us, this could lead to unanticipated losses.

We have established a risk management system that measures these market risk and liquidity risk on a daily basis and takes immediate actions if the pre-set limits are exceeded.

(3) Natural disaster, terrorism, military dispute and infectious disease could adversely affect our business

We have developed a contingency plan for addressing unexpected situations and conduct crisis management exercises which include employee notification tests. We also continue to ensure that we can maintain operational resilience (which refers to the ability to continue to provide critical services at a minimum level that should be maintained in the event of a system failure, cyberattack or natural disaster). This includes the establishment of an emergency command center in the event of an actual disaster to account for the safety of our employees and their families. However, disaster, terrorism, military disputes or pandemics or other widespread infectious diseases could exceed the assumptions of our plan and our framework, and we may not always be able to respond to every situation, afflicting our management and employees, facilities and systems, which could adversely affect our business. For example, the COVID-19 pandemic that began in 2020, and governmental measures to respond to it, have significantly affected the market environment such as causing volatility in global equity prices, interest rates and elsewhere and a widening of credit spreads.

22

Table of Contents

2. The financial services industry faces intense competition

Our businesses are intensely competitive, and are expected to remain so. We compete on the basis of a number of factors, including transaction execution capability, our products and services, innovation, reputation and price. We continue to experience intense price competition, particularly in brokerage, investment banking and other businesses.

(1) Competition with other financial firms and financial services by non-financial companies is increasing

We face intense competition in the financial services sector from a wide variety of competitors. We compete with other independent securities firms as well as securities firms affiliated with commercial banks and with firms that have broad footprints across regions. As a result, our market shares and commissions earned in the sales and trading, investment banking and retail businesses in particular have been affected. We face intense competition beyond the traditional financial sector based on the increasing digitalization of the industry, not only with the rise of online securities firms but also FinTech companies and the entry of non-financial companies into the financial services sector. In order to address such changes in the competitive landscape, we continue to adopt and transform our business models through various measures. However, these measures may not be successful in growing or maintaining our market share in this increasingly fierce competitive environment, and we may lose business or transactions to our competitors, harming our business and results of operations.

(2) Increased consolidation, business alliance and cooperation in the financial services industry mean increased competition for us

There has been substantial consolidation and convergence among companies in the financial services industry. In particular, a number of large commercial banks and other broad-based large financial services groups have established or acquired broker-dealers or have consolidated with other financial institutions. These large financial services groups have developed business linkage within their respective groups in order to provide comprehensive financial services to clients, offering a wide range of products, including loans, deposit-taking, insurance, brokerage, asset management and investment banking services within their group, which may enhance their competitive position compared with us. They also have the ability to supplement their investment banking and brokerage businesses with commercial banking and other financial services revenues in an effort to gain market share. In addition, the financial services industry has seen collaboration beyond the borders of businesses and industries, such as alliances between commercial banks and securities companies outside of framework of existing corporate groups and recent alliances with non-financial companies including emerging companies. Our competitiveness may be adversely affected if our competitors are able to expand their businesses and improve their profitability through such business alliances. We also enter into strategic alliances, make investments and launch new businesses. However, if the development and implementation of these business strategies do not proceed as expected, we may not be able to achieve the expected synergies and other benefits or recoup related investments. These new business initiatives and acquisitions may subject us to increased risk as we engage in new activities, transact with a broader array of clients and counterparties and expose us to new asset classes and new markets.

(3) Our global business continues to face intense competition and may require further revisions to its business model