Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

Table of Contents

As filed with the Securities and Exchange Commission on July 9, 2014

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

INTERFACE SECURITY SYSTEMS

HOLDINGS, INC.

(Exact name of Registrant as Specified in Its Charter)

| | | | |

Delaware

(State or Other Jurisdiction of

Incorporation or Organization) | | 7380

(Primary Standard Industrial

Classification Code Number) | | 04-3583955

(I.R.S. Employer

Identification Number) |

INTERFACE SECURITY SYSTEMS, L.L.C.

(Exact name of Registrant as Specified in Its Charter)

| | | | |

Louisiana

(State or Other Jurisdiction of

Incorporation or Organization) | | 7380

(Primary Standard Industrial

Classification Code Number) | | 72-1310576

(I.R.S. Employer

Identification Number) |

3773 Corporate Center Drive

Earth City, MO 63045

(314) 595-0100

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrants' Principal Executive Offices)

Michael T. Shaw

Chief Executive Officer

3773 Corporate Center Drive

Earth City, MO 63045

(314) 595-0100

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

With a copy to:

Terry M. Schpok, P.C.

Akin Gump Strauss Hauer & Feld LLP

1700 Pacific Avenue, Suite 4100

Dallas, Texas 75201

(214) 969-4085

Approximate date of commencement of proposed sale of the securities to the public:

As soon as practicable on or after the effective date of this Registration Statement.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| | | | | | |

| Large accelerated filer o | | Accelerated filer o | | Non-accelerated filer ý

(Do not check if a

smaller reporting company) | | Smaller reporting company o |

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) o

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) o

CALCULATION OF REGISTRATION FEE

| | | | | | | | |

| | | | | | | | |

| |

Title of Each Class of Securities

to be Registered

| | Amount to be

Registered

| | Proposed Maximum

Offering Price Per

Note

| | Proposed Maximum

Aggregate Offering

Price

| | Amount of

Registration Fee

|

|---|

| |

91/4% Senior Secured Notes due 2018 | | $230,000,000 | | 100%(1) | | $230,000,000(2) | | $29,624 |

|

- (1)

- The proposed maximum offering price per note is based on the book value of the Notes as of July 9, 2014, in the absence of a public market for the Notes, in accordance with Rule 457(f)(2) promulgated under the Securities Act of 1933, as amended (the "Securities Act").

- (2)

- Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457 under the Securities Act.

The Registrants hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrants shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not exchange these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated July 9, 2014

PRELIMINARY PROSPECTUS

Interface Security Systems Holdings, Inc.

and

Interface Security Systems, L.L.C.

Offer to Exchange

All outstanding 91/4% Senior Secured Notes due 2018

($230,000,000 aggregate principal amount)

for

91/4% Senior Secured Notes due 2018

which have been registered under the Securities Act of 1933, as amended

The exchange offer will expire at 5:00 p.m., New York City time, on , 2014, unless we extend the exchange offer. We do not currently intend to extend the expiration date.

- •

- We are offering to exchange up to $230,000,000 aggregate principal amount of new 91/4% Senior Secured Notes due 2018, or Exchange Notes, which have been registered under the Securities Act of 1933, as amended, or the Securities Act, for an equal principal amount of our outstanding 91/4% Senior Secured Notes due 2018, or Initial Notes, issued in a private offering on January 18, 2013. We refer to the Exchange Notes and the Initial Notes collectively as the Notes.

- •

- We will exchange all Initial Notes that are validly tendered and not validly withdrawn prior to the closing of the exchange offer for an equal principal amount of Exchange Notes that have been registered.

- •

- You may withdraw tenders of Initial Notes at any time prior to the expiration of the exchange offer.

- •

- The terms of the Exchange Notes to be issued are identical in all material respects to the Initial Notes, except for transfer restrictions and registration rights that do not apply to the Exchange Notes, and different administrative terms.

- •

- The Exchange Notes, together with any Initial Notes not exchanged in the exchange offer, will constitute a single class of debt securities under the indenture governing the Notes.

- •

- The exchange of Initial Notes will not be a taxable exchange for United States federal income tax purposes. We will not receive any proceeds from the exchange offer.

- •

- No public market exists for the Initial Notes. We do not intend to list the Exchange Notes on any securities exchange and, therefore, no active public market is anticipated.

See "Risk Factors" beginning on page 19 for a discussion of risk factors that you should consider before tendering your Initial Notes.

We are an "emerging growth company" under applicable federal securities laws and will be subject to reduced public company reporting requirements.

Each broker-dealer that receives Exchange Notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such Exchange Notes. The related letter of transmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an "underwriter" within the meaning of the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of Exchange Notes received in exchange for Initial Notes where such Initial Notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of 180 days after the consummation of the exchange offer, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See "Plan of Distribution."

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2014.

Table of Contents

TABLE OF CONTENTS

| | | | |

| | Page | |

|---|

EMERGING GROWTH COMPANY STATUS | | | i | |

INDUSTRY AND MARKET DATA | | |

ii | |

WHERE YOU CAN FIND MORE INFORMATION | | |

ii | |

NON-GAAP FINANCIAL MEASURES | | |

iii | |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS | | |

iv | |

PRESENTATION OF FINANCIAL INFORMATION | | |

v | |

PROSPECTUS SUMMARY | | |

1 | |

RISK FACTORS | | |

19 | |

THE EXCHANGE OFFER | | |

42 | |

USE OF PROCEEDS | | |

52 | |

CAPITALIZATION | | |

53 | |

SELECTED HISTORICAL CONSOLIDATED FINANCIAL DATA | | |

54 | |

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | | |

56 | |

BUSINESS | | |

79 | |

MANAGEMENT | | |

92 | |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | | |

98 | |

CERTAIN RELATIONSHIPS AND RELATED PARTY TRANSACTIONS | | |

100 | |

DESCRIPTION OF OTHER INDEBTEDNESS | | |

105 | |

DESCRIPTION OF EXCHANGE NOTES | | |

107 | |

BOOK-ENTRY SETTLEMENT AND CLEARANCE | | |

169 | |

CERTAIN UNITED STATES FEDERAL INCOME TAX CONSEQUENCES | | |

171 | |

PLAN OF DISTRIBUTION | | |

172 | |

LEGAL MATTERS | | |

174 | |

EXPERTS | | |

174 | |

You should rely only on the information contained in this prospectus. We have not authorized any person to provide you with any information or represent anything about us or this exchange offer that is not contained in this prospectus. If given or made, any such other information or representation should not be relied upon as having been authorized by us. We are not making an offer in any jurisdiction where an offer or sale is not permitted. The information contained in this prospectus is current only as of its date.

EMERGING GROWTH COMPANY STATUS

We are an "emerging growth company" as defined in the Jumpstart Our Business Startups Act ("JOBS Act"), and we are eligible to take advantage of certain exemptions from various reporting

i

Table of Contents

requirements that are applicable to other public companies that are not "emerging growth companies." See "Risk Factors—Risks Related to Our Business and Our Industry—As an "emerging growth company" under the JOBS Act, we are permitted to, and intend to, rely on exemptions from certain disclosure requirements."

Section 107 of the JOBS Act allows us to take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. As a result, we may delay the adoption of such standards until those standards would otherwise apply to private companies. As an "emerging growth company," we have elected to delay adoption of new or revised accounting standards applicable to public companies until such pronouncements are made applicable to private companies.

We may remain an "emerging growth company" until the earliest of: (i) the last day of the fiscal year during which we have total annual gross revenues of $1 billion or more, (ii) the last day of the fiscal year following the fifth anniversary of the date of the first sale of our common stock pursuant to an effective registration statement, (iii) the date on which we have, during the previous 3-year period, issued more than $1 billion in non-convertible debt or (iv) the date on which we are deemed a "large accelerated issuer" as defined under the federal securities laws.

INDUSTRY AND MARKET DATA

Unless otherwise expressly indicated or noted in this prospectus, all information regarding markets, market size, market share, market position, growth rates and other industry data pertaining to our business contained in this prospectus is based on estimates prepared by us based on certain assumptions and our knowledge of the industry in which we operate as well as data from various market research, publicly available information and industry publications, including information we obtained from The Organization for Economic Co-operation and Development's "OECD Broadband Portal," © OECD (which can be found at http://www.oecd.org/internet/broadband/oecdbroadbandportal.htm and was last updated as of January 9, 2014), Connected Nation, Infonetics Research, Security Distributing and Marketing Magazine, Barnes Associates, TechSci Research, MarketsandMarkets and the Loss Prevention Research Council. Industry publications generally state that the information they contain has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. While management has examined and relied upon certain market or other industry data from external sources as the basis of its estimates, we have not verified that data independently. As such, we cannot assure you of the accuracy and completeness of, and take no responsibility for such data. Similarly, while we believe our internal estimates to be reasonable, these estimates have not been verified by any independent sources and we cannot assure you as to their accuracy. Our estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under the heading "Risk Factors" in this prospectus.

WHERE YOU CAN FIND MORE INFORMATION

We will be required to file annual and quarterly reports and other information with the Securities and Exchange Commission (the "SEC") after the registration statement described below is declared effective by the SEC. You may read and copy any reports, statements and other information that we file with the SEC at the SEC's public reference room located at 100 F Street, N.E. Room 1580, Washington, D.C. 20549. You may request copies of the documents, upon payment of a duplicating fee, by writing the Public Reference Section of the SEC. Please call 1-800-SEC-0330 for further information on the public reference rooms. Our filings with the SEC are also available to the public at the web site maintained by the SEC at http://www.sec.gov.

ii

Table of Contents

We have filed a registration statement on Form S-4 to register with the SEC the Exchange Notes to be issued in exchange for the Initial Notes. This prospectus is part of that registration statement. As allowed by the SEC's rules, this prospectus does not contain all of the information you can find in the registration statement or the exhibits to the registration statement. You should note that where we summarize in the prospectus the material terms of any contract, agreement or other document filed as an exhibit to the registration statement, the summary information provided in the prospectus is less complete than the actual contract, agreement or document. You should refer to the exhibits filed to the registration statement for copies of the actual contract, agreement or document.

NON-GAAP FINANCIAL MEASURES

We use certain financial measures, including EBITDA and Adjusted EBITDA, as supplemental measures of our operating performance that are not required by, or presented in accordance with, generally accepted accounting principles in the United States ("GAAP"). They are not measurements of our financial performance under GAAP and should not be considered as alternatives to net income, operating income or any other performance measures derived in accordance with GAAP or as an alternative to cash flows from operating activities as a measure of our liquidity. These measures are used in the internal management of our business, along with the most directly comparable GAAP financial measures, in evaluating our operating performance. In addition, our presentation of Adjusted EBITDA is consistent with the equivalent measurements that are contained in our Revolving Credit Facility (as defined below) and the indenture governing the Notes.

EBITDA represents net (loss) income attributable to Interface Security Systems Holdings, Inc. before interest expense, interest income, income taxes, depreciation, amortization and net loss attributable to noncontrolling interest. Adjusted EBITDA represents EBITDA as further adjusted for loss on extinguishment of debt, gain or loss on sale of assets (including the Transferred Assets (as defined below)), sales and installation costs, net of sales and installation revenue, related to organic RMR growth, plus 50% of non-capitalized corporate and service center administrative costs related to organic RMR growth, less capitalized subscriber system assets. Our calculation of Adjusted EBITDA does not include any adjustments for expenses related to the Westec Acquisition (as defined below), the sale of the Transferred Assets, the Subsidiaries Merger (as defined below), financing of the Revolving Credit Facility or preparing for the initial registration of the Exchange Notes. These expenses for the years ended December 31, 2013, 2012 and 2011, and the three months ended March 31, 2014 and 2013 were $0.8 million, $4.4 million, $0, $1.9 million and $0.1 million, respectively.

Our measurement of EBITDA and Adjusted EBITDA may not be comparable to similarly titled measures of other companies and are not measures of performance calculated in accordance with GAAP. We have included information concerning EBITDA and Adjusted EBITDA because we believe that such information is used by certain investors as supplemental measures of a company's historical ability to service debt. We believe these measures are frequently used by securities analysts, investors and other interested parties in the evaluation of high yield issuers, many of which present EBITDA and Adjusted EBITDA when reporting their results. Our presentation of EBITDA and Adjusted EBITDA should not be construed as an inference that our future results will be unaffected by unusual or nonrecurring items.

EBITDA and Adjusted EBITDA have limitations as analytical tools, and you should not consider them in isolation, or as a substitute for analysis of, our operating results or cash flows as reported under GAAP. Some of these limitations are:

- •

- they do not reflect our cash expenditures, or future requirements, for capital expenditures or contractual commitments;

- •

- they do not reflect changes in, or cash requirements for, our working capital needs;

iii

Table of Contents

- •

- they do not reflect the significant interest expense, or the cash requirements necessary to service interest or principal payments, on our debt;

- •

- although depreciation is a non-cash charge, the assets being depreciated will often have to be replaced in the future, and EBITDA and Adjusted EBITDA do not reflect any cash requirements for such replacements;

- •

- they are not adjusted for all non-cash income or expense items that are reflected in our statements of cash flows; and

- •

- other companies in our industry may calculate these measures differently than we do, limiting their usefulness as comparative measures.

Because of these limitations, EBITDA and Adjusted EBITDA should not be considered as measures of discretionary cash available to us to invest in the growth of our business. We compensate for these limitations by relying primarily on our GAAP results and using EBITDA and Adjusted EBITDA only for supplemental purposes. Please see our consolidated financial statements contained elsewhere in this prospectus.

For a reconciliation of net (loss) income attributable to Interface Security Systems Holdings, Inc. to EBITDA and Adjusted EBITDA, see "Prospectus Summary—Summary Historical Consolidated Financial Data" and "Management's Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measures."

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements. Statements that are not historical facts, including statements about our beliefs and expectations, are forward-looking statements. Forward-looking statements include statements preceded by, followed by or that include the words "may," "could," "would," "should," "believe," "expect," "anticipate," "plan," "estimate," "target," "project," "intend," "understand," or similar expressions and the negative of such words and expressions, although not all forward-looking statements contain such words or expressions.

Forward-looking statements are only predictions and are not guarantees of performance. These statements generally relate to our plans, objectives and expectations for future operations and are based on management's beliefs and assumptions, which in turn are based on currently available information. These assumptions could prove inaccurate, which could cause actual results that differ materially from those contained in any forward-looking statement. Forward-looking statements also involve risks and uncertainties. Many of these factors are beyond our ability to control or predict and such incurrence could be material. Such factors include, but are not limited to, the following:

- •

- our inability to maintain compliance with various covenants under the Revolving Credit Facility to borrow funds;

- •

- restrictions in the indenture governing the Master Holdings Notes (as defined below) on our ability to incur additional funded debt, other than amounts available under the Revolving Credit Facility;

- •

- our ability to compete effectively in a highly competitive industry;

- •

- catastrophic events that may disrupt our business;

- •

- our ability to retain customers;

- •

- concentration of RMR in a few top customers and concentration of our business in certain markets;

iv

Table of Contents

- •

- our ability to manage relationships with third-party providers, including telecommunication providers and broadband service providers;

- •

- our ability to obtain or maintain necessary governmental licenses and comply with applicable laws and regulations;

- •

- changes in governmental regulation of communication monitoring;

- •

- our reliance on network and information systems and other technologies and our ability to manage disruptions caused by cyber-attacks, failure or destruction of our networks, systems, technologies or properties;

- •

- macroeconomic factors;

- •

- economic, credit, financial or other risks affecting our customers and their ability to pay us;

- •

- the uncertainty of our future operating results;

- •

- our ability to attract, train and retain an effective sales force;

- •

- our reliance on third party component providers and the risk associated with any failure or interruption in products or services provided by these third parties;

- •

- our reliance on third party software and service providers;

- •

- the loss of our senior management; and

- •

- the other factors discussed under "Risk Factors."

Although we believe the forward-looking statements in this prospectus are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Further, forward-looking statements speak only as of the date of this prospectus and we do not undertake any obligation to update publicly any such statements, except as required by law.

PRESENTATION OF FINANCIAL INFORMATION

In this prospectus, we present the consolidated financial statements of Interface Security Systems Holdings, Inc. and Interface Security Systems, L.L.C., on a consolidated basis, and have not provided separate financial statements for Interface Security Systems, L.L.C. because Interface Security Systems Holdings, Inc. has no material assets other than the equity interests of Interface Security Systems, L.L.C. and conducts substantially all of its operations through Interface Security Systems, L.L.C. Therefore, the revenues and results of operations of Interface Security Systems Holdings, Inc. substantially reflect the revenues and results of operations of Interface Security Systems, L.L.C.

RMR measures contractually obligated recurring monthly revenue attributable to monitoring, service and maintenance contracts. RMR also includes revenue recognized through recurring fees charged to customers under monitoring, management and services contracts and revenue for the provision of managed information technology ("IT") services. The aggregate of all RMR billed to all customers at the end of a given period represents our total RMR. Average revenue per user ("ARPU") measures total RMR divided by the number of total customer sites. The term "total customer sites" is the aggregate number of customer sites for which RMR is being billed at the end of a given period. The term "average net attrition rate" as used in this prospectus refers to the aggregate amount of canceled or reduced RMR during a period divided by the average total RMR during the measurement period. Customers are considered canceled when they terminate in accordance with the terms of their contract or are terminated by us. Certain customer re-signs and relocations are excluded from the attrition calculation. If a customer relocates and continues its service, we consider this as a cancellation but do not include such cancellation in our average net attrition rate calculation. Further, if a customer

v

Table of Contents

discontinues its service at a site and a new customer enters into a contract for service at the same site, we refer to this as a re-sign. We consider re-signs as cancellations, but do not include them in our average net attrition rate calculation. Unless otherwise stated, average net attrition is based on the trailing twelve month period. The term "CAGR" as used in this prospectus refers to the compound annual growth rate over the specified period. The term "creation costs" as used in this prospectus refers to the gross sales and installation costs to generate and install a customer, including 50% of general and administrative costs, net of any sales and installation revenue collected at the time of the contract signing. "Organic RMR growth" refers to new RMR created in a given period from internal sales activity and excluding the effect of new RMR gained through acquisitions. Totals in some tables in this prospectus may differ from the sum of individual amounts in those tables due to rounding. Unless specified otherwise, amounts in this prospectus are presented in U.S. dollars. Defined terms in the financial statements have the meanings ascribed to them in the financial statements.

vi

Table of Contents

PROSPECTUS SUMMARY

This summary highlights selected important information contained elsewhere in this prospectus about us and the exchange offer. This summary does not include all of the information you should consider or that is important to you. Please review this prospectus in its entirety, including the section entitled "Risk Factors" and our consolidated financial statements and the related notes thereto. Unless indicated otherwise, references to "Company," "we," "our," and "us" refer to Interface Security Systems Holdings, Inc. ("Holdings") and Interface Security Systems, L.L.C. ("Interface Systems"), collectively.

Our Company

We are a leading national provider of physical security and secured managed network services to primarily large, commercial multi-site customers and believe that we provide the most comprehensive Internet Protocol ("IP") technology-enabled managed security solution in the market. Our physical security solutions include alarm / event monitoring, interactive video surveillance, managed access control and fire / life safety systems. Our secured network services include secure managed broadband ("SMB"), payment card industry ("PCI") compliance, managed digital voice and other ancillary services. Our comprehensive service offering is designed to meet the needs of commercial enterprises that require a universal and secure IP security platform capable of servicing all of their locations. We combine a complete suite of customized physical and network security services into a fully-integrated bundle, enabling our customers to consolidate services from multiple vendors into a single service provider, significantly enhancing the quality and breadth of their security and reducing their costs.

Our physical security platform is delivered utilizing state-of-the-art IP technology, which enables our alarm / event monitoring to be faster, more reliable and less expensive than digital dialer systems. In addition, our experienced engineering team is able to program the routers on these IP systems to optimize our alarm monitoring and interactive video surveillance services by proactively managing bandwidth in our customers' networks to insure continuity of all critical business systems. Our proprietary video surveillance technology allows for remote event-based monitoring from our central command center ("C3") where highly trained specialists can monitor real-time events taking place at a customer premise through both live video and audio and take appropriate action. We believe our proprietary video surveillance technology provides the most cost-efficient system in the market allowing operators to simultaneously monitor events at multiple customer locations. The unique features of this system include video verification, rapid response, video escorts and snapshot audits. These services, along with our other ancillary IP security applications, are custom-configured through a private, secured network to meet the requirements of our customer's existing software system and infrastructure. We are able to continuously monitor the health of each customer's network remotely through our Security Operations Center ("SOC") / Network Operations Center ("NOC").

We supply and install all of the required hardware and software equipment for our bundled service offering, which enables us to enter into long-term (on average four years or more) contracts with our customers. We have also taken the quality of service and level of urgency that is critical to the life safety / emergency response sector and applied it to monitoring SMB. As a result, we believe we provide the highest quality of customer service in the secured network service space.

Our diverse customer base includes large multi-site commercial enterprises in the luxury retail, dining, quick-service restaurant ("QSR") and hospitality vertical sectors, including Dollar General, Subway, Family Dollar, Michaels Stores, McDonald's, Sterling Jewelers, Zales, Tumi, Panda Express, Sunoco and Edward Jones. As of March 31, 2014, our top ten customers accounted for 46.1% of our total RMR, with an average length of relationship of seven years. As of March 31, 2014, we serviced 76,356 total customer sites across our customer base through our 16 regional service centers and employee field technicians in most of the largest markets in the U.S. The scope and breadth of our services, combined with our significant equipment investment, software system configuration and

1

Table of Contents

long-term contracts make our customer relationships stable and "sticky." In addition, we have established a sales and installation infrastructure capable of managing large-scale national deployments, which we can leverage to add new customers without significantly incurring additional infrastructure costs. We also have mutually-beneficial channel partnership agreements in place with companies such as Cisco and Verizon Wireless to expand our national sales footprint at minimal incremental cost. As a result of our infrastructure, partnerships and focus on large, commercial multi-site customers, our costs to create customers are lower than the industry average and we achieve higher than industry ARPU. We have demonstrated the ability to manage large-scale deployments across customer locations nationwide in a short period of time, as highlighted by our rollout of over 10,000 store locations for Dollar General in 2010 and 2011 (the "Dollar General Deployment").

Our revenue model emphasizes a strong base of high margin RMR with high ARPU. Our customer retention rate is among the highest in the industry (measured by RMR attrition) and, as of March 31, 2014, our average twelve month net attrition rate was 10.8%. We maintain a backlog of new RMR associated with fully executed customer contracts for services that are pending installation ("Contracted Backlog") and a sales pipeline that we believe will generate a steady, significant flow of new RMR in 2014 and beyond. As of March 31, 2014, our sales pipeline included approximately $16.9 million of identified opportunities for multiple, large managed bundled service deployments for future RMR growth. In addition, as of March 31, 2014, our Contracted Backlog was $0.3 million with a majority of the Contracted Backlog expected to be installed in 2014. In April 2014, we converted approximately $2.4 million of our sales pipeline to Contracted Backlog.

For the year ended December 31, 2013, our total revenues, net loss and Adjusted EBITDA were $126.7 million, $47.8 million and $38.1 million, respectively, representing an Adjusted EBITDA margin of 30.1%. For the three months ended March 31, 2014, our total revenues, net income and Adjusted EBITDA were $28.7 million, $27.7 million and $7.2 million, respectively, representing an Adjusted EBITDA margin of 25.1%.

Industry Overview

We believe we are the only nationwide provider of bundled managed IP and physical security services. To date, we do not believe there are any direct competitors capable of offering a similar suite of bundled services on the same scale as we offer. However, we do face competition on an un-bundled basis across the following sectors:

Secure Managed Cloud Services Market. The secure managed cloud services industry encompasses many outsourced and hosted technology-enabled services including security as a service. In security, the market is often referred to as managed security services, particularly as it relates to IT security. Total IT spending and the share of security within IT budgets is expected to increase in 2014 and beyond, as the rising sophistication of computer network attacks and subsequent cost of repairing security breaches will continue to drive IT security demand. The penetration of broadband connections in the U.S. has grown from 9.6% of the population in 2003 to 29.3% in 2013 according to the Organization for Economic Co-operation and Development. Among businesses, the industry trade group Connected Nation estimates in its 2013 Business Survey that 1.8 million U.S. businesses or 24% of all U.S. businesses are still without broadband. Within the retail trade, recreation, food and lodging sectors, approximately 32% of businesses do not utilize broadband services. Infonetics Research, a market research and consulting services firm focused on the communications industry, estimates that in the first half of 2013, global residential and business Voice over Internet Protocol ("VoIP") services revenue rose 3% to $33 billion and is projected to grow to $80 billion by 2017. Similarly, the global market for cloud-based video surveillance is expected to more than double in just four years from $570 million in 2013 to $1.3 billion in 2017, according to TechSci Research.

2

Table of Contents

Electronic Security Monitoring Market. Over the last decade, the security monitoring market has remained highly competitive and fragmented without any material change to market concentration. Competition in the industry is based primarily on services offered, reputation for quality of service, market visibility, price and the ability to identify potential new customers. Technological advances have reduced costs and streamlined installation, which in turn has resulted in higher customer adoption. This trend is expected to drive a migration of customers from security-focused companies to suppliers offering integrated solutions. The electronic security monitoring industry (equipment and monitoring) was estimated by Barnes Associates at $45.8 billion in 2013. According to estimates of Barnes Associates, the market for monitoring and related electronic security services in which we primarily compete generated approximately $21.2 billion in revenue in 2013 and has grown every year for the past nine years. This industry has been growing across economic cycles, driven by increased penetration, higher pricing and overall population, business and home growth. We believe the electronic security monitoring industry tends to be relatively recession resilient as compared to other industries, as heightened security awareness typically occurs during times of economic turmoil due to the higher perceived risk of crime.

Remotely Managed Video Surveillance Market. Remotely managed video monitoring is a rapidly growing segment of commercial security and is evolving from a primary focus on security to a key business intelligence tool. MarketsandMarkets estimates that the global video surveillance as a service market will grow from $474 million in 2011 to $2.4 billion in 2017, representing a CAGR of 31.5%. The projected growth of the remotely managed video surveillance market is largely driven by the replacement of analog equipment with IP-based equipment, general security and terrorism concerns, business intelligence application and IT and physical security convergence. Multi-store and franchised retail sites are emerging as an early adopter of this technology, especially given the migration from analog video to IP video and the new features offered as a result. While retailers have traditionally applied video surveillance for loss prevention and security measures, enhanced video surveillance systems can also help generate information to help retailers optimize store layouts, measure the effectiveness of promotional campaigns, identify customer patterns and address other marketing and operational uses. According to a 2013 survey by the Loss Prevention Research Council, approximately one third of retailers possess analog-only systems, down from approximately two thirds in 2010. However, 64.4% of those retailers currently using analog systems have a plan to or are considering migrating to IP video. If these retailers migrate to IP video, the adoption of intelligent video surveillance services over the next several years would substantially expand.

Business Strengths

Leader in Bundled Physical Security and Secured Network Services. Many years of operational experience, significant investment in infrastructure and the development of proprietary software has enabled us to become a leader in combining physical security and secured network services into a seamless solution. We believe our bundled services improve store operations and deliver material cost savings to our customers. While some of our competitors offer certain overlapping services, we are aware of no competitor that has been able to effectively pair physical security with the broad range of managed IP services we offer over a SMB connection. We believe our ability to combine both physical and data security applications on a national scale is the key differentiator that separates us from our competition. We further believe our ability to integrate services onto a single platform and monitor related events from a centralized location is unparalleled in the market. In addition, our bundled service offering is enhanced by the following:

- •

- Technology Infrastructure. We provide around-the-clock monitoring of managed network and security events through our SOC / NOC located just outside of St. Louis, Missouri, which is Underwriters Laboratories ("UL") listed and Central Station Alarm Association ("CSAA") Five

3

Table of Contents

Operating Model Creates "Stickier" Customers. Through our bundled service offering, we are able to reduce the number of vendors our customers must utilize and consolidate billing and services to a single vendor. We offer standardized contracts and service level agreements for our multi-site customers to reduce administrative costs and internal delays while ensuring uniform service standards. In addition, we supply and install all of the required equipment (both hardware and software) for our bundled service offering, which enables us to enter into long-term (on average four years or more) contracts with our customers. Once in place, our bundled customer relationship becomes more stable due to the custom configuration of each security solution we provide to our customers and the significant cost to migrate to another provider. As of March 31, 2014, 38.7% of our commercial customer sites subscribed to more than one service offering and 29.4% adopted our secured network services bundled offering within the bundled services, demonstrating the appeal of a broad multi-service platform. As of March 31, 2014, our average combined commercial and residential twelve month average net attrition rate was 10.8%. Our national accounts customers with IP related bundled services, which excludes Digital Witness, are our "stickiest" and our twelve month average net attrition rate among these customers as of March 31, 2014 was only 7.6%.

High ARPU Customers with Low Creation Costs. Our portfolio of products and services and industry vertical focus emphasizes high ARPU and provides high dollar margins while minimizing capital requirements associated with customer acquisition. While traditional alarm customers typically generate $25 to $50 of monthly ARPU, our average customer site generates an ARPU of $97.45 per month ($134.90 for commercial and $30.14 for residential) as of March 31, 2014. We have made significant investments in our infrastructure and ability to manage and install large-scale deployments in recent years. This ability is highlighted by the Dollar General Deployment. We have invested time and resources in recent years to purpose-build a technology infrastructure that is highly scalable and enables us to continue to expand our diversified customer base. Because of the scalability of our business model, adding services to an established customer platform is a highly cost-efficient way to increase RMR at very low creation costs. Our SOC / NOC and C3 give us the ability to monitor additional accounts without investing capital to expand those facilities. This allows us to not only add new customers at low creation costs, but also improves our monitoring gross margins as we leverage our fixed monitoring overhead and add incremental customer sites.

Blue Chip Customer Base. Our diverse customer base includes large multi-site commercial enterprises in the luxury retail, dining, QSR and hospitality vertical sectors, including many leading national companies including Dollar General, Subway, Family Dollar, Michaels Stores, McDonald's, Sterling Jewelers, Zales, Tumi, Panda Express, Sunoco and Edward Jones. We primarily focus on industry verticals where there is a significant base of national accounts with multi-site operations, both company operated and franchised. Our customers in the luxury retail, QSR, convenience store and restaurant industries have been responsive to our service offerings and are rolling out installations at a strong pace, showing excellent near and long- term growth potential. Our business model focuses on

4

Table of Contents

industry verticals with high adoption rates leading to higher "win rates" that achieve scale and build reputation through strong word-of-mouth referrals. These verticals remain largely under-penetrated and provide a strong organic growth pipeline. We have benefited from the shift to adopting corporate-wide security and IP service standards among large commercial customers with national accounts. Whereas in the past, vendor selection was a function typically relegated to the store manager, more retail and franchise chains are assuming corporate-wide policies and are therefore seeking vendors that already have the experience and scale to service a national customer base. Corporate-mandated standards are typically more stringent and tend to incorporate more effective technologies that require expertise and experience on the part of the vendor, which we believe is a significant advantage and point of differentiation for us. Our focus on large, established commercial customers with national accounts helps reduce our exposure to attrition as a result of customer locations closing or customers going out of business.

Significant Contracted Backlog and Pipeline. We maintain a substantial Contracted Backlog and sales pipeline that we believe will generate a steady and significant flow of new RMR in 2014 and beyond. As of March 31, 2014, our Contracted Backlog was $0.3 million with a majority of the Contracted Backlog expected to be installed in 2014. In addition, as of March 31, 2014, our sales pipeline included approximately $16.9 million of identified opportunities for multiple, large managed bundled service deployments for future RMR growth. In April 2014, we converted approximately $2.4 million of our sales pipeline to Contracted Backlog. We believe there is also an additional $0.8 million of near-term, high probability RMR opportunities within our sales pipeline that will be converted to Contracted Backlog in 2014.

Strong Financial Performance and Organic Growth. We have been able to increase total revenues by 87.7% from $67.5 million in 2009 to $126.7 million for the year ended December 31, 2013, and Adjusted EBITDA by more than 62.1%, from $23.5 million to $38.1 million over the same period through organic growth and acquisitions. For the three months ended March 31, 2014, our total revenues, net income and Adjusted EBITDA were $28.7 million, $27.7 million and $7.2 million, respectively. From January 1, 2002 through March 31, 2014, we have created $9.1 million of new RMR from internal growth activity, excluding the impact of attrition. From January 1, 2009 through March 31, 2014, including the impact of the Westec Acquisition and the sale of the Transferred Assets, we have grown RMR internally from $3.9 million to $7.4 million, representing a CAGR of 16.3%.

Knowledgeable and Experienced Management Team. Our senior management team has significant industry experience (approximately 113 years combined) and strong technical expertise. We have grown organically and through 42 acquisitions since 1998 to reach total RMR of $7.4 million as of March 31, 2014, which would make us one of the top 15 largest alarm companies in the U.S. based on RMR as of December 31, 2013, according to a 2014 report issued by Security Distributing and Marketing Magazine.

Business Strategy

Target National Accounts. We believe that our key growth opportunity is in the multi-site regional and national account market segment. Customers in this segment represent an attractive source of RMR because they are continuously seeking to increase security while reducing operating expenses and improving store operations.

- •

- Internal Sales. We plan to continue to grow our customer base in both new and existing geographic regions through our internal sales infrastructure. We have a nationwide presence through our 16 regional service centers and a national account sales team consisting of 39 team members. Our sales team is responsible for sourcing new business and for supporting our largest customers that typically have national footprints. In addition, we believe our ability to manage all customer relations from our corporate headquarters and SOC / NOC in St. Louis, Missouri

5

Table of Contents

and our C3 in Plano, Texas and deliver same day / next day service nationwide is a key differentiator in winning large multi-site national accounts that require centralized support and consistent service levels across all locations. Since the beginning of 2011, we have installed $3.0 million of new national account RMR as of March 31, 2014 and believe that by December 31, 2014, we will have installed an additional $1.7 million of new national account RMR.

- •

- Cisco Partnership, Verizon VSP Partnership, Ideacom Partnership and Other Channel Partners. We have established significant channel partnerships that we believe will become a more significant source of new business in 2014 and beyond. We are among the first managed service providers to become certified under Cisco's new Channel Partner program. The certification is awarded by invitation only and there are fewer than 100 certified Cisco Managed Service Channel Partners ("MSCP") worldwide. The certification earns higher Cisco discounts, a dedicated team for sales and technical support and Cisco marketing resources, including target telemarketing and success documentaries. We and Verizon established a strategic marketing partnership in 2012 under the Verizon Partner Program ("VPP"). As a VPP partner, we benefit from Verizon's lead sharing, co-marketing efforts and sales management tools. We have access to a dedicated webpage, internal to Verizon sales representatives, that provides a company overview of us, how to contact us for help with deals, white papers, key wins and additional detailed information. By being included in the lead sharing portal, Verizon sales representatives can enter leads into their CRM system which automatically emails them to us. Our partnership currently includes a nationwide alignment of go-to-market resources and has resulted in our participation in over 50 Verizon local marketing events. The latest program was our invitation to participate in Verizon's Connected Technology Tour ("CTT"), a series of 20 local shows across the major Verizon markets. We were one of only approximately 20 Verizon partners (5% of all Verizon partners) that were invited to participate in all 20 CTT programs across the nation. We also have expanded our channel partner program to include vertically focused companies such as telecom and broadband service providers, including Ideacom Solutions Group, a national association of 90 independent telecom and IT service providers. As of March 31, 2014, as a result of these relationships, we have identified over 8,000 new potential sites, with total potential RMR of approximately $0.8 million, and we believe this number will increase over the next several years.

Increase Sales from Base of Existing Customers. We believe the potential to up-sell additional services to our existing customers presents a significant opportunity. As businesses regularly review budgets to determine how to achieve cost savings, increase security and improve operations, we are able to leverage our existing relationship with our customers to generate new sales. As of March 31, 2014, 38.7% of our commercial customer sites subscribed to more than one service offering and 29.4% adopted our secured network services bundled offering within the bundled services. We believe that we will be able to increase the adoption rate of our bundled service offering as our customers' existing contracts with other providers expire. Since the completion of the Westec Acquisition, our customers, including our customers that were acquired in the Westec Acquisition, have shown strong interest in cross-purchasing services. As a result of the Westec Acquisition, we have identified $6.2 million of potential cross-selling opportunities in our pipeline and continue to work to identify more opportunities to sell our existing customers incremental services.

Recent Developments

Disposition of Hawk Security Services Assets

Pursuant to an Asset Purchase Agreement (the "Asset Purchase Agreement"), dated as of January 9, 2014 (the "Closing Date"), by and among My Alarm Center, LLC, d/b/a Alarm Capital Alliance ("Buyer"), and Interface Systems, we sold certain residential customer contracts and related assets and liabilities used exclusively in, or necessary to conduct, the alarm system sales, installation,

6

Table of Contents

repair, maintenance and monitoring services of our Hawk Security Services brand ("Hawk") in the State of Texas (the "Transferred Assets") to the Buyer. The total purchase price for the Transferred Assets was approximately $42.8 million, of which approximately $40.7 million was paid in cash to us on the Closing Date and approximately $2.1 million was deposited in an escrow account on the Closing Date. The funds will remain in escrow for six months following the Closing Date and will serve as the exclusive source of recovery for customary indemnification obligations with respect to our representations, warranties and covenants under the Asset Purchase Agreement and certain adjustments to the purchase price in the event the customer attrition rate applicable to the Transferred Assets differs from specified targets. We have agreed to provide Buyer with certain specified transition services to allow for the efficient transition of the Transferred Assets to Buyer for six months following the Closing Date, unless extended by mutual agreement. We continue to operate in the residential alarm monitoring business and the Hawk branded services were not clearly distinguishable operationally or for financial reporting purposes. We used a portion of the net proceeds to redeem all of the issued and outstanding shares of our Class G Preferred Stock and Class F Preferred Stock and part of our Class E Preferred Stock and to pay a cash dividend in an aggregate amount of approximately $27.3 million to the stockholders as permitted under the indenture governing the Notes. For purposes of the "Asset Sales" covenant in the indenture governing the Notes, a portion of the sale of the Transferred Assets constituted a "Permitted Hawk Disposition" under such indenture, and therefore did not constitute an "Asset Sale." The remainder of the sale, which generated gross proceeds of $13.2 million, did constitute an "Asset Sale" under such indenture, and we intend to apply such Asset Sale proceeds as required under such indenture.

Subsidiary Roll-up

On September 30, 2013, Holdings completed a series of transactions by which all of its then-existing subsidiaries, other than Interface Systems, ultimately merged with and into Interface Systems (the "Subsidiaries Merger"). Westec Intelligent Surveillance, Inc., a Delaware corporation, merged with and into Westec Acquisition Corp., a Delaware corporation, which subsequently merged with and into Interface Systems. The Greater Alarm Company, Inc., a California corporation ("Greater Alarm"), effected a reverse stock split, whereby every 100 shares of common stock of Greater Alarm were combined into 1 share of common stock of Greater Alarm. No fractional shares were issued, and Holdings and a shareholder with a 0.8% ownership in Greater Alarm were paid for their fractional shares resulting from the reverse stock split. Subsequent to this reverse stock split, Greater Alarm merged with and into Interface Systems.

Westec Intelligent Surveillance, Inc., Westec Acquisition Corp. and Greater Alarm were initial guarantors under the Initial Notes. Following the Subsidiaries Merger, we no longer have any subsidiaries. Accordingly, the Initial Notes are not currently, and the Exchange Notes will initially not be, guaranteed. The Notes may in the future be guaranteed by any future domestic restricted subsidiaries under certain circumstances. See "Description of Exchange Notes."

Corporate Reorganization

On May 30, 2014, we completed a corporate reorganization with a newly formed holding company, Interface Master Holdings, Inc. ("Master Holdings"), in connection with the closing of a $115.0 million offering of 12.50% / 14.50% Senior Contingent Cash Pay Notes (the "Master Holdings Notes") issued by Master Holdings. Pursuant to the reorganization, each of SunTx, the management investors (as defined below) and certain other stockholders of Holdings exchanged all of their shares of each class of common stock of Holdings and each class of preferred stock of Holdings for an equal number of shares of common stock and preferred stock of Master Holdings with substantially similar terms as the shares of Holdings. In addition, Master Holdings used $71.6 million of the proceeds of the offering to purchase shares of Class A Common Stock and Class B Common Stock of Holdings. Holdings and

7

Table of Contents

Interface Systems intend to use the consideration from the sale of shares of Holdings common stock to Master Holdings to make cash interest payments on the Notes and for general corporate purposes, including to fund growth initiatives. The foregoing transactions described in this "Corporate Reorganization" section are referred to collectively as the "Reorganization Transactions." Immediately following the consummation of the Reorganization Transactions, Master Holdings owned approximately 99% of each class of common stock of Holdings and at least 99% of each class of Holdings' preferred stock. Subsequent to the Reorganization Transactions, the remaining stockholders of Holdings exchanged all of their shares of each class of common stock and preferred stock of Holdings for an equal number of shares of common stock and preferred stock of Master Holdings. As a result, Master Holdings now owns 100% of the common stock and preferred stock of Holdings.

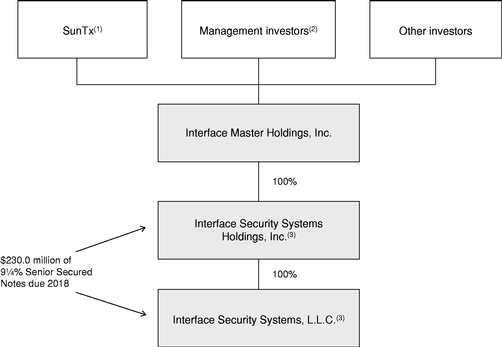

Corporate Structure

The chart below summarizes our corporate structure and principal indebtedness as of July 9, 2014.

- (1)

- Includes certain investment funds affiliated with SunTx Capital Partners, L.P. (together with its affiliates, "SunTx").

- (2)

- Includes shares held by Michael Shaw, our chief executive officer, Kenneth Obermeyer, our chief financial officer, and Michael McLeod, our chief operating officer (collectively, the "management investors").

- (3)

- Holdings and Interface Systems are also parties to a $45.0 million revolving credit facility (as amended, the "Revolving Credit Facility"), dated January 18, 2013, as amended on September 30, 2013 and May 16, 2014, among Interface Systems and its then-existing subsidiaries, as borrowers, Holdings, as guarantor, and Capital One, N.A. ("Capital One"), as administrative agent and lender. Holdings and Interface Systems entered into the Revolving Credit Facility concurrently with the closing of the offering of the Initial Notes.

Our Sponsor

SunTx is a Dallas, Texas based private equity firm that invests in middle-market manufacturing, distribution and services companies. SunTx specializes in supporting talented management teams in

8

Table of Contents

industries where SunTx can apply its operational experience and financial expertise to build leading middle-market companies with operations typically located in the Sun Belt region of the United States. Since the firm's inception in 2001, SunTx has invested over $600 million in a variety of sectors including manufacturing, broadcasting, business services, consumer products and food and beverage.

The capital committed by SunTx comes from its principals, as well as from institutional investors, including leading university endowments, financial institutions and corporate and public pension funds.

Our Corporate Information

Interface Security Systems Holdings, Inc. is a Delaware corporation formed in 2001. Interface Security Systems, L.L.C., formerly known as Louisiana Security Holdings, L.L.C., is a Louisiana limited liability company formed in 1995. Our principal offices are located at 3773 Corporate Center Drive, Earth City, Missouri 63045. Our telephone number is (314) 595-0100 and our website is www.interfacesystems.com. Information on, or accessible through, our website is not part of this prospectus, nor is such content incorporated by reference herein.

9

Table of Contents

Summary of the Terms of the Exchange Offer

In connection with the issuance of the Initial Notes, we entered into a registration rights agreement with the initial purchasers of the Initial Notes. Under that agreement, we agreed to use commercially reasonable efforts to cause a registration statement related to the exchange of Initial Notes for Exchange Notes to become effective under the Securities Act on or prior to the 545th day after January 18, 2013 and to consummate the exchange offer within 30 business days of effectiveness of the registration statement.

The registration statement of which this prospectus forms a part was filed pursuant to our obligations under this registration rights agreement.

You are entitled to exchange in this exchange offer your Initial Notes for Exchange Notes which are identical in all material respects to the Initial Notes except that:

- •

- the Exchange Notes have been registered under the Securities Act and will be freely tradable by persons who are not affiliated with us;

- •

- the Exchange Notes are not entitled to registration rights which are applicable to the Initial Notes under the registration rights agreement; and

- •

- our obligation to pay additional interest on the Initial Notes as described in the registration rights agreement does not apply to the Exchange Notes.

For purposes of this and other sections in this prospectus, we refer to the Initial Notes and the Exchange Notes together as the "Notes."

| | |

Senior Notes | | We are offering to exchange up to $230,000,000 aggregate principal amount of our 91/4% Senior Secured Notes due 2018 which have been registered under the Securities Act for up to $230,000,000 aggregate principal amount of our Initial Notes which were issued on January 18, 2013. Initial Notes may be exchanged only in initial minimum denominations of $2,000 and any integral multiple of $1,000 in excess thereof. |

Resales | | Based on interpretations by the staff of the Securities and Exchange Commission (the "SEC") set forth in no-action letters issued to unrelated third parties, we believe that the Exchange Notes issued pursuant to this exchange offer in exchange for Initial Notes may be offered for resale, resold and otherwise transferred by you (unless you are our "affiliate" within the meaning of Rule 405 under the Securities Act) without compliance with the registration and prospectus delivery provisions of the Securities Act, provided that you |

| | • are acquiring the Exchange Notes in the ordinary course of business, and |

| | • have not engaged in, do not intend to engage in, and have no arrangement or understanding with any person to participate in, a distribution of the Exchange Notes. |

| | Each participating broker-dealer that receives Exchange Notes for its own account pursuant to this exchange offer in exchange for the Initial Notes that were acquired as a result of market-making or other trading activities must acknowledge that it will deliver a prospectus in connection with any resale of the Exchange Notes. See "Plan of Distribution." |

10

Table of Contents

| | |

| | Any holder of Notes who |

| | • is our affiliate, |

| | • does not acquire the Exchange Notes in the ordinary course of business, or |

| | • tenders in this exchange offer with the intention to participate, or for the purpose of participating, in a distribution of Exchange Notes, |

| | cannot rely on the position of the staff of the SEC expressed in Exxon Capital Holdings Corporation, Morgan Stanley & Co. Incorporated or similar no-action letters and, in the absence of an exemption, must comply with the registration and prospectus delivery requirements of the Securities Act in connection with the resale of the Exchange Notes. |

Expiration; Withdrawal of Tenders | | This exchange offer will expire at 5:00 p.m., New York City time, on , 2014, or such later date and time to which we extend it. We do not currently intend to extend the expiration date. A tender of Initial Notes pursuant to this exchange offer may be withdrawn at any time prior to the expiration date. Any Initial Notes not accepted for exchange for any reason will be returned without expense to the tendering holder after the expiration or termination of this exchange offer. |

Delivery of the Exchange Notes | | The Exchange Notes issued pursuant to this exchange offer will be delivered to the holders who validly tender Initial Notes promptly following the expiration date. |

Conditions to this Exchange Offer | | This exchange offer is subject to customary conditions, some of which we may waive. See "The Exchange Offer—Certain Conditions to this Exchange Offer." |

Procedures for Tendering Initial Notes | | If you wish to accept this exchange offer, you must complete, sign and date the accompanying letter of transmittal, or a copy of the letter of transmittal, according to the instructions contained in this prospectus and the letter of transmittal. You must also mail or otherwise deliver the letter of transmittal, or the copy, together with the Initial Notes and any other required documents, to the exchange agent at the address set forth on the cover of the letter of transmittal. If you hold Initial Notes through The Depository Trust Company ("DTC") and wish to participate in this exchange offer, you must comply with the Automated Tender Offer Program procedures of DTC, by which you will agree to be bound by the letter of transmittal. |

| | By signing or agreeing to be bound by the letter of transmittal, you will represent to us that, among other things: |

| | • Any Exchange Notes that you will receive will be acquired in the ordinary course of your business; |

11

Table of Contents

| | |

| | • You have no arrangement or understanding with any person to participate in the distribution (within the meaning of the Securities Act) of the Exchange Notes to be received in the exchange offer; |

| | • If you are a broker-dealer that will receive Exchange Notes for your own account in exchange for Initial Notes, that the Initial Notes to be exchanged for Exchange Notes were acquired as a result of market-making or other trading activities, and that you will deliver a prospectus in connection with any resale of such Exchange Notes; and |

| | • You are not our "affiliate" as defined in Rule 405 under the Securities Act. |

Effect on Holders of Initial Notes | | As a result of the making of, and upon acceptance for exchange of all validly tendered Initial Notes pursuant to the terms of, this exchange offer, we will have fulfilled a covenant contained in the registration rights agreement and, accordingly, additional interest on the Initial Notes, if any, shall no longer accrue and we will no longer be obligated to pay additional interest as described in the registration rights agreement. If you are a holder of Initial Notes and do not tender your Initial Notes in this exchange offer, you will continue to hold such Initial Notes and you will be entitled to all the rights and limitations applicable to the Initial Notes in the indenture, except for any rights under the registration rights agreement that by their terms terminate upon the consummation of this exchange offer. |

Consequences of Failure to Exchange | | All untendered Initial Notes will continue to be subject to the restrictions on transfer provided for in the Initial Notes and in the indenture governing the Notes. In general, the Initial Notes may not be offered or sold unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with this exchange offer, or as otherwise required under certain limited circumstances pursuant to the terms of the registration rights agreement, we do not currently anticipate that we will register the Initial Notes under the Securities Act. |

Regulatory Approvals | | Other than compliance with the Securities Act and qualification of the indenture governing the notes under the Trust Indenture Act of 1939, as amended (the "Trust Indenture Act" or "TIA"), there are no federal or state regulatory requirements that must be complied with or approvals that must be obtained in connection with the exchange offer. |

Certain U.S. Federal Income Tax Consequences | | The exchange of Initial Notes for Exchange Notes in this exchange offer should not be a taxable event for U.S. federal income tax purposes. See "Certain United States Federal Income Tax Consequences." |

Use of Proceeds | | We will not receive any cash proceeds from the issuance of the Exchange Notes in this exchange offer. |

Exchange Agent | | Wells Fargo Bank, N.A., the trustee under the indenture governing the Notes, is serving as exchange agent in connection with the exchange offer. The mailing address of the exchange agent is set forth on the cover page of the letter of transmittal. |

12

Table of Contents

Summary of Terms of the Exchange Notes

The summary below describes the principal terms of the Exchange Notes. Certain of the terms and conditions described below are subject to important limitations and exceptions. The "Description of Exchange Notes" section of this prospectus contains a more detailed description of the terms and conditions of the Notes. The Initial Notes were initially guaranteed by our subsidiaries, Westec Intelligent Surveillance, Inc., Westec Acquisition Corp. and Greater Alarm, each existing at the time of the issue date. Following the Subsidiaries Merger, we no longer have any subsidiaries. Accordingly, the Initial Notes are not currently, and the Exchange Notes will initially not be, guaranteed. The Notes may in the future be guaranteed by certain future domestic restricted subsidiaries under certain circumstances. See "Description of Exchange Notes."

| | |

Issuers | | Interface Security Systems Holdings, Inc., a Delaware corporation, and Interface Security Systems, L.L.C., a Louisiana limited liability company, will co-issue the Exchange Notes on a joint and several basis. |

Notes Issued | | $230,000,000 aggregate principal amount of 91/4% Senior Secured Notes due 2018, registered under the Securities Act. |

Maturity Date | | January 15, 2018. |

Interest Rate | | Interest on the Notes will accrue at an annual rate of 91/4% per annum and will be payable in cash. |

Interest Payment Dates | | We will make interest payments on the Notes semi-annually, in arrears, on July 15 and January 15 of each year. |

Guarantees | | The Notes are not currently guaranteed. Any future domestic restricted subsidiaries will be required to fully and unconditionally guarantee, jointly and severally, on a senior secured basis the Notes. |

Security Interest | | The Notes and any guarantees will be secured by second priority liens on substantially all of our and any guarantors' assets, subject to certain exceptions. Pursuant to the terms of the intercreditor agreement, the liens on the collateral securing the Notes and any guarantees will be contractually subordinated to the liens on the collateral that secure the Revolving Credit Facility and certain other obligations. See "Description of Exchange Notes—Security" and "Description of Exchange Notes—Intercreditor Agreement." |

13

Table of Contents

| | |

Intercreditor Agreement | | The administrative agent (on behalf of the secured parties under the Revolving Credit Facility) and the collateral agent (on behalf of the holders of the Initial Notes offered) have entered into an intercreditor agreement, which, among other things, defines the relative priorities of their respective security interests in the assets securing the Notes and the obligations under the Revolving Credit Facility and certain other matters relating to the administration of security interests, exercise of remedies, certain bankruptcy-related provisions and other intercreditor matters. The intercreditor agreement also provides, among other things, that in the event of a foreclosure on the collateral or of insolvency proceedings, the holders of the Notes and any other pari passu indebtedness will receive proceeds from the collateral only after obligations under the Revolving Credit Facility and certain other obligations have been paid in full. See "Description of Exchange Notes—Intercreditor Agreement." |

Ranking | | The Notes will be our and any guarantors' senior secured obligations and will: |

| | • rank equal in right of payment with all of our and any guarantors' existing and future senior indebtedness; |

| | • rank senior in right of payment to all of our and any guarantors' future subordinated indebtedness; |

| | • be effectively subordinated to any of our and any guarantors' future secured indebtedness that is secured by a first priority lien (including indebtedness under the Revolving Credit Facility) to the extent of the value of the assets securing such indebtedness; |

| | • be effectively senior to all of our and any guarantors' existing and future unsecured indebtedness to the extent of the value of the collateral securing the Notes after payment in full of all obligations secured by a first priority lien on such collateral; and |

| | • be structurally junior to all existing and future indebtedness and other liabilities of any non-guarantor subsidiaries. |

| | As of March 31, 2014, we had $261.2 million of secured indebtedness outstanding and the ability to borrow up to $5.6 million under our $45.0 million Revolving Credit Facility. |

Optional Redemption | | On or after July 15, 2015, we may redeem all or a part of the Notes at a premium that will decrease over time as set forth under "Description of Exchange Notes—Optional Redemption," plus accrued and unpaid interest, if any, to the date of redemption. |

14

Table of Contents

| | |

| | Prior to July 15, 2015, we may, at our option, redeem up to 35% of the aggregate principal amount of the Notes using an amount of cash equal to the net cash proceeds of certain equity offerings at a price equal to 109.250% of the principal amount thereof, plus accrued and unpaid interest, if any, to the date of redemption; provided that, following any and all such redemptions, at least 65% of the aggregate principal amount the Notes originally issued under the indenture remains outstanding and the redemption occurs within 90 days of the closing of such equity offering. |

| | In addition, at any time prior to July 15, 2015, we may, at our option, redeem all or a part of the Exchange Notes, upon not less than 30 nor more than 60 days' notice, at a redemption price equal to 100% of the principal amount of the Exchange Notes redeemed plus a specified make-whole premium, plus accrued and unpaid interest, if any, to the applicable date of redemption. See "Description of Exchange Notes—Optional Redemption." |

Change of Control Offer | | If we experience certain kinds of changes of control, the holders of the Notes will have the right to require us to purchase all or a portion of their Notes at an offer price in cash equal to 101% of the aggregate principal amount thereof, plus accrued and unpaid interest, if any, to the date of purchase. |

Asset Sale Offer | | Upon certain asset sales, we may be required to offer to use an amount of cash equal to the net cash proceeds of such asset sale to purchase the Notes at 100% of the aggregate principal amount thereof, plus accrued and unpaid interest, if any, to the date of purchase. See "Description of Exchange Notes—Certain Covenants." |

Covenants | | The indenture governing the Notes contains covenants that limit our ability and the ability of any restricted subsidiaries to, among other things: |

| | • transfer or sell assets or use asset sale proceeds; |

| | • pay dividends or make distributions, redeem subordinated debt or make other restricted payments; |

| | • make certain investments; |

| | • incur or guarantee additional debt or issue redeemable or preferred equity securities; |

| | • create or incur certain liens on our assets; |

| | • incur dividend or other payment restrictions affecting any future restricted subsidiaries; |

| | • merge, consolidate or transfer all or substantially all of our assets; and |

| | • enter into certain transactions with affiliates. |

| | These covenants are subject to a number of important exceptions and qualifications and are described in more detail in "Description of Exchange Notes—Certain Covenants." |

Risk Factors | | You should consider carefully all of the information set forth in this prospectus and, in particular, you should evaluate the risks described under "Risk Factors." |

15

Table of Contents

Summary Historical Consolidated Financial Data