Exhibit 99.1

Exhibit 99.1

Take Stock in Gold

Wayne W. Murdy

Chairman & Chief Executive Officer

Merrill Lynch Global Metals, Mining & Steel Conference

Boston, MA

May 12, 2004

CAUTIONARY STATEMENT

PRIVATE SECURITIES LITIGATION REFORM ACT SAFE HARBOR STATEMENT

This presentation contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, that are intended to be covered by the safe harbor created by such sections. Such forward-looking statements include, without limitation, (i) statements regarding future earnings, and the sensitivity of earnings to the gold and other metals prices; (ii) estimates of future gold and other metals production and sales; (iii) estimates of future cash costs and total production costs; (iv) statements of future cash flows, and the sensitivity of cash flows to the gold and other metals prices; (v) estimates of future capital expenditures, expenses and tax rates; (vi) estimates regarding timing of future production or closure activities; (vii) statements regarding future exploration results and the replacement of reserves; (viii) statements regarding future asset sales or rationalization efforts; and (ix) estimates of future royalty revenues Where the Company expresses or implies an expectation or belief as to future events or results, such expectation or belief is expressed in good faith and believed to have a reasonable basis. However, forward-looking statements are subject to risks, uncertainties and other factors, which could cause actual results to differ materially from future results expressed, projected or implied by such forward-looking statements. Such risks include, but are not limited to, gold and other metals price volatility, currency fluctuations, increased production costs and variances in ore grade or recovery rates from those assumed in mining plans, political and operational risks in the countries in which we operate, and governmental regulation and judicial outcomes. For a more detailed discussion of such risks and other factors, see the Company’s 2003 Annual Report on Form 10-K, which is on file with the Securities and Exchange Commission, as well as the Company’s other SEC filings. The Company does not undertake any obligation to release publicly revisions to any “forward-looking statement,” to reflect events or circumstances after the date of this news release, or to reflect the occurrence of unanticipated events, except as may be required under applicable securities laws.

May 12, 2004—Slide 2

Introduction

Outline

•Strategic Overview

•Gold Fundamentals

•Operating & Financial Results

•2004 Guidance

•Reserves and Exploration

•Conclusion

May 12, 2004—Slide 3

Strategic Overview –Introduction

Gold Company

“No Gold Hedging” Philosophy Large

Land Position

Conservative Balance Sheet

Economic Value Drivers

NAV per share

Long-term

Reserve replacement

Free cash flow per share Short-term

EPS

May 12, 2004—Slide 4

Strategic Overview –Global Footprint

Gold

Copper/Other

Midas

Twin Creeks

Carlin

Lone Tree

Phoenix NEVADA

Leeville

May 12, 2004—Slide 5

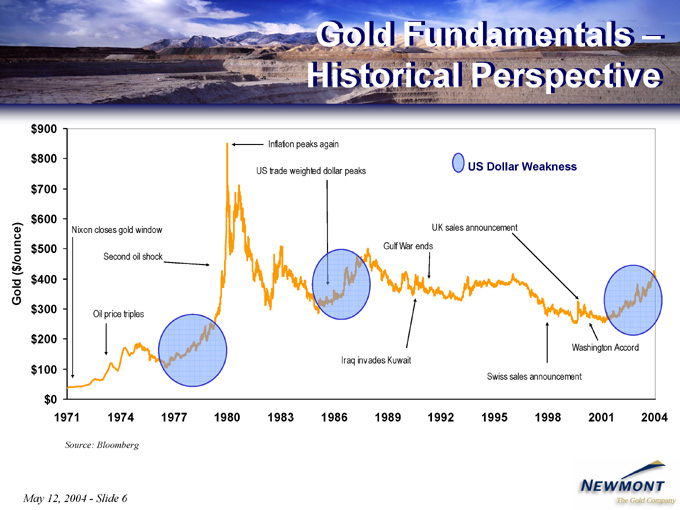

Gold Fundamentals – Historical Perspective

Source: Bloomberg

May 12, 2004—Slide 6

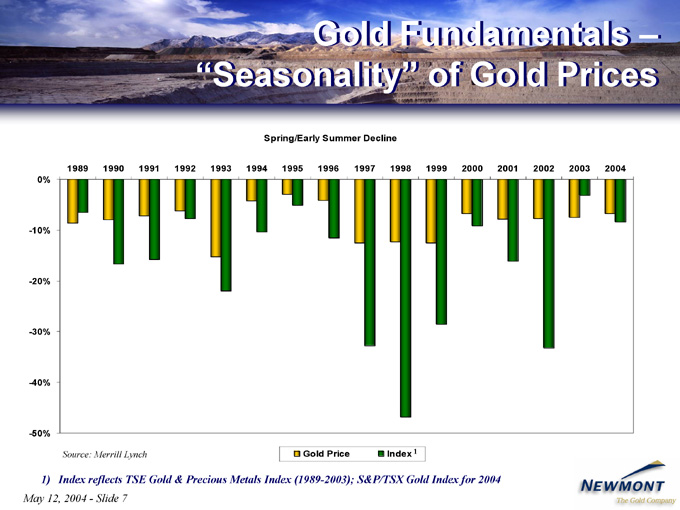

Gold Fundamentals –”Seasonality” of Gold Prices

Spring/Early Summer Decline

Source: Merrill Lynch Gold Price Index 1

1) Index reflects TSE Gold & Precious Metals Index (1989-2003); S&P/TSX Gold Index for 2004

May 12, 2004—Slide 7

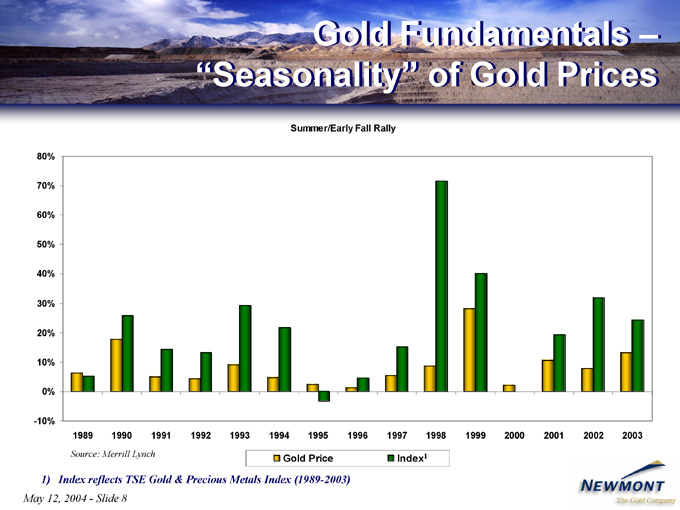

Gold Fundamentals –”Seasonality” of Gold Prices

Summer/Early Fall Rally

Source: Merrill Lynch Gold Price Index1

1) Index reflects TSE Gold & Precious Metals Index (1989-2003)

May 12, 2004—Slide 8

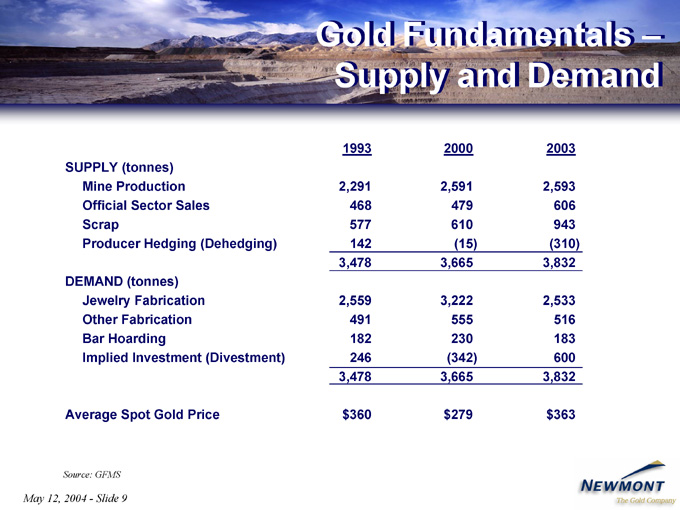

Gold Fundamentals – Supply and Demand

1993 2000 2003

SUPPLY (tonnes)

Mine Production 2,291 2,591 2,593

Official Sector Sales 468 479 606

Scrap 577 610 943

Producer Hedging (Dehedging) 142 (15) (310)

3,478 3,665 3,832

DEMAND (tonnes)

Jewelry Fabrication 2,559 3,222 2,533

Other Fabrication 491 555 516

Bar Hoarding 182 230 183

Implied Investment (Divestment) 246 (342) 600

3,478 3,665 3,832

Average Spot Gold Price $360 $279 $363

Source: GFMS

May 12, 2004—Slide 9

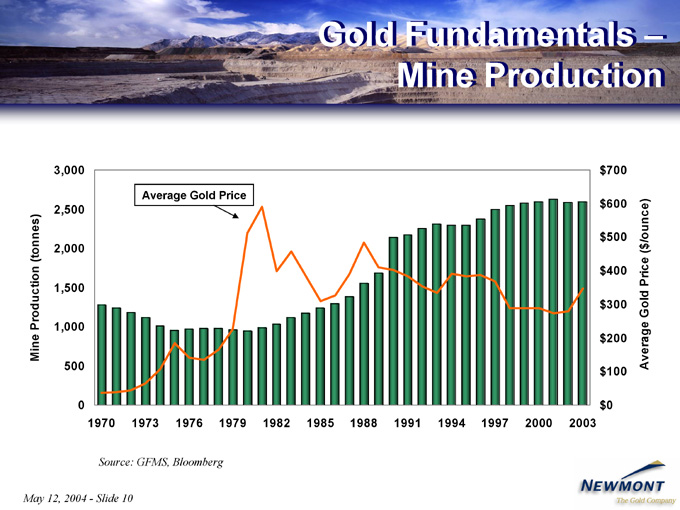

Gold Fundamentals – Mine Production

Source: GFMS, Bloomberg

May 12, 2004—Slide 10

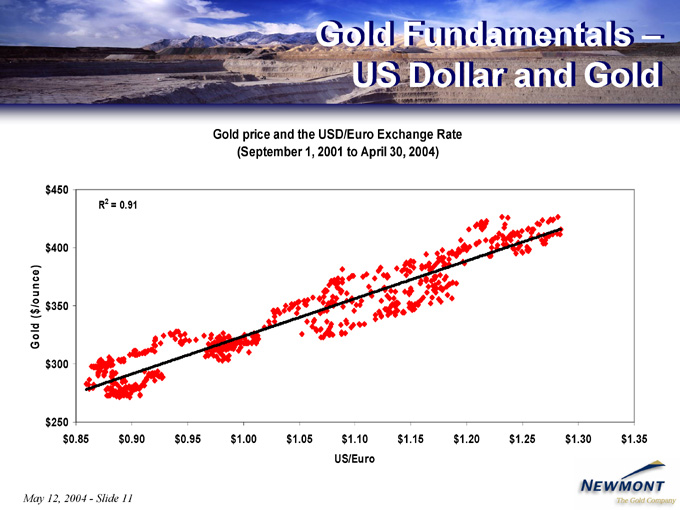

Gold Fundamentals – US Dollar and Gold

Gold price and the USD/Euro Exchange Rate

(September 1, 2001 to April 30, 2004)

US/Euro

May 12, 2004—Slide 11

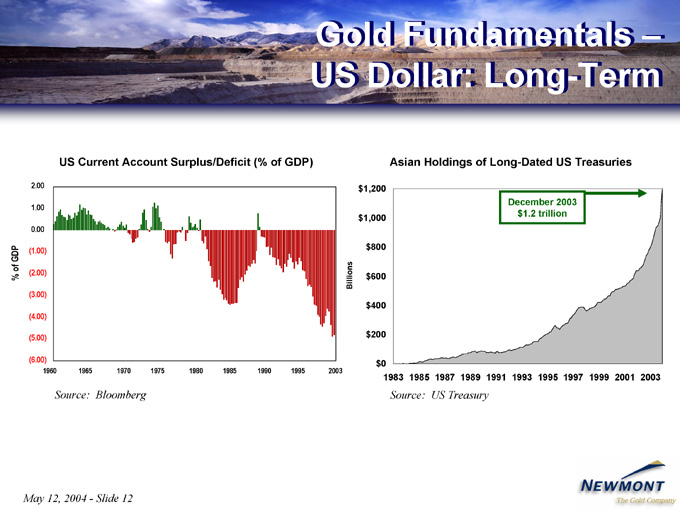

Gold Fundamentals – US Dollar: Long-Term -

US Current Account Surplus/Deficit (% of GDP)

Source: Bloomberg

Asian Holdings of Long-Dated US Treasuries

December 2003 $1.2 trillion

Source: US Treasury

May 12, 2004—Slide 12

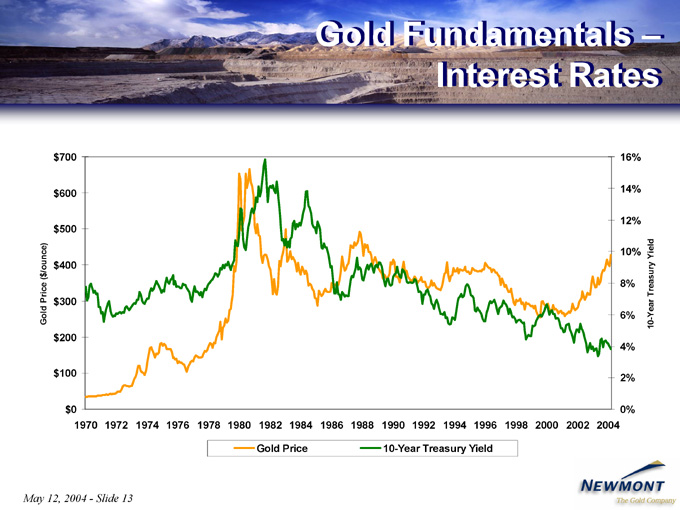

Gold Fundamentals – Interest Rates

Gold Price 10-Year Treasury Yield

May 12, 2004—Slide 13

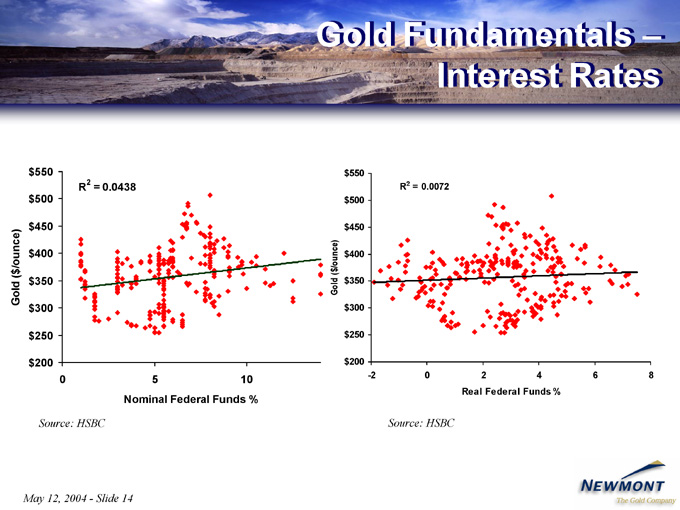

Gold Fundamentals – Interest Rates

Nominal Federal Funds %

Source: HSBC

Real Federal Funds %

Source: HSBC

May 12, 2004—Slide 14

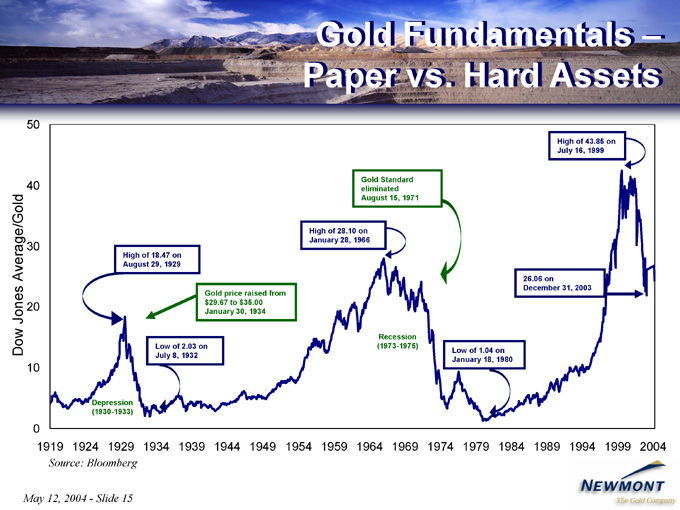

Gold Fundamentals – Paper vs. Hard Assets .

Source: Bloomberg

May 12, 2004—Slide 15

Operating & Financial Results

May 12, 2004—Slide 16

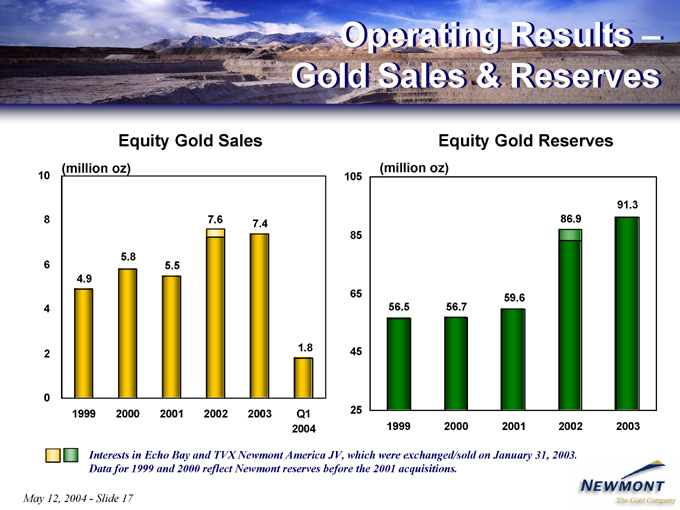

Operating Results –Gold Sales & Reserves

Equity Gold Sales

Equity Gold Reserves

Interests in Echo Bay and TVX Newmont America JV, which were exchanged/sold on January 31, 2003. Data for 1999 and 2000 reflect Newmont reserves before the 2001 acquisitions.

May 12, 2004—Slide 17

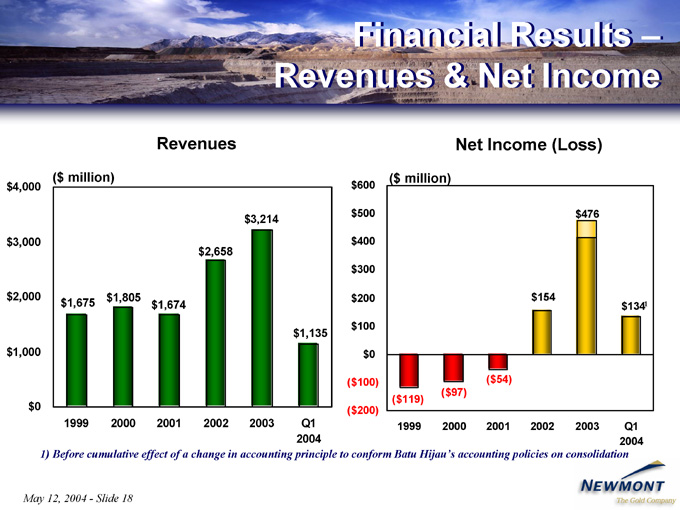

Financial Results –Revenues & Net Income

Revenues

Net Income (Loss)

1) Before cumulative effect of a change in accounting principle to conform Batu Hijau’s accounting policies on consolidation

May 12, 2004—Slide 18

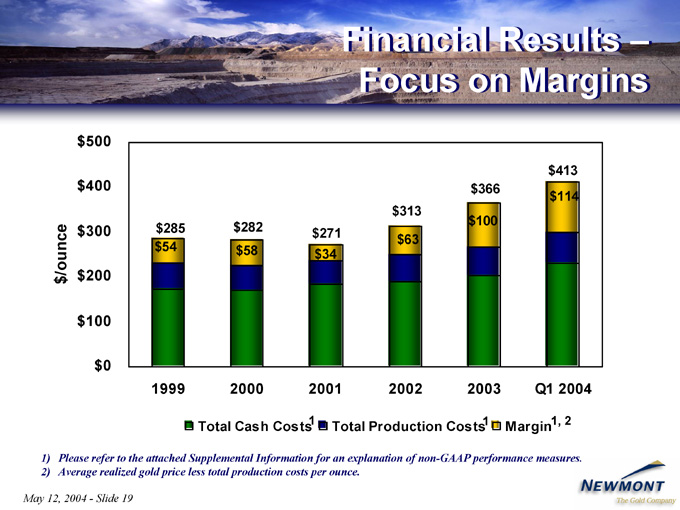

Financial Results –Focus on Margins

Total Cash Costs1 Total Production Costs1 Margin1, 2

1) Please refer to the attached Supplemental Information for an explanation of non-GAAP performance measures.

2) Average realized gold price less total production costs per ounce.

May 12, 2004—Slide 19

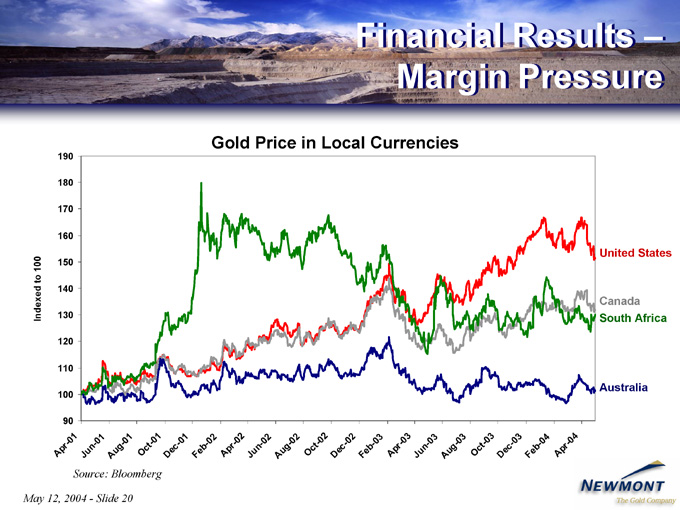

Financial Results –Margin Pressure

Gold Price in Local Currencies

United States

Canada

South Africa

Australia

Source: Bloomberg

May 12, 2004—Slide 20

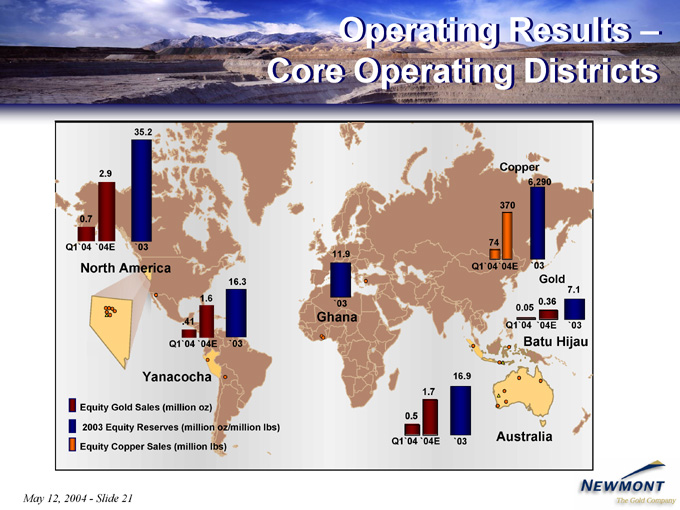

Core Operating Districts

35.2

2.9

0.7

Q1`04 `04E `03

North America

16.3 1.6

.41

Q1`04 `04E `03

Yanacocha

11.9

`03

Ghana

Copper

6,290

370

74

Q1`04`04E `03

Gold

7.1 0.05 0.36 Q1`04 `04E `03

Batu Hijau

16.9

1.7

0.5

Q1`04 `04E `03 Australia

May 12, 2004—Slide 21

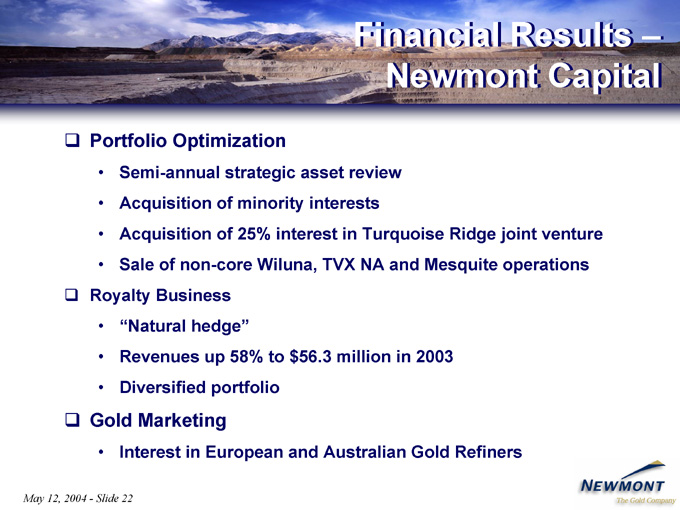

Financial Results –Newmont Capital

Portfolio Optimization

• Semi-annual strategic asset review

• Acquisition of minority interests

• Acquisition of 25% interest in Turquoise Ridge joint venture

• Sale of non-core Wiluna, TVX NA and Mesquite operations

Royalty Business

• “Natural hedge”

• Revenues up 58% to $56.3 million in 2003

• Diversified portfolio

Gold Marketing

• Interest in European and Australian Gold Refiners

May 12, 2004—Slide 22

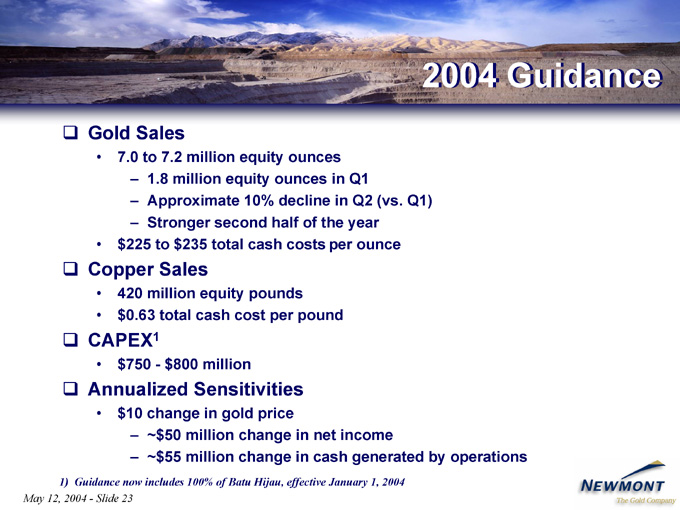

2004 Guidance

Gold Sales

• 7.0 to 7.2 million equity ounces

– 1.8 million equity ounces in Q1

– Approximate 10% decline in Q2 (vs. Q1)

– Stronger second half of the year

•$ 225 to $235 total cash costs per ounce

Copper Sales

• 420 million equity pounds

•$ 0.63 total cash cost per pound

CAPEX1

•$ 750—$800 million

Annualized Sensitivities

•$ 10 change in gold price

– ~$50 million change in net income

– ~$55 million change in cash generated by operations

1) Guidance now includes 100% of Batu Hijau, effective January 1, 2004

May 12, 2004—Slide 23

Reserves & Exploration

May 12, 2004—Slide 24

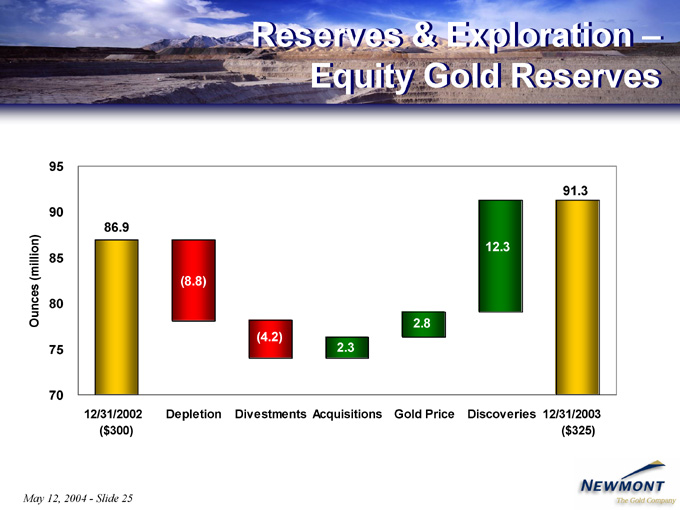

Reserves & Exploration –Equity Gold Reserves

May 12, 2004—Slide 25

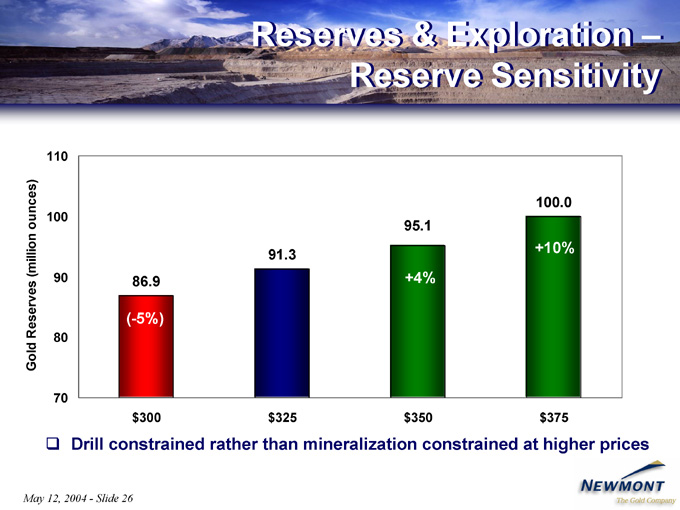

Reserves & Exploration –Reserve Sensitivity

Drill constrained rather than mineralization constrained at higher prices

May 12, 2004—Slide 26

Conclusion

Gold Market Fundamentals Remain Positive

Strong Operating and Financial Results

Record 91.3 Million Reserve Ounces (at $325 gold)

Large, Prospective Land Position

Strengthened Balance Sheet

Merger Integration Complete

Only S&P 500 Gold Stock

May 12, 2004—Slide 27

Take Stock in Gold

Wayne W. Murdy

Chairman & Chief Executive Officer

Merrill Lynch Global Metals, Mining & Steel Conference

Boston, MA

May 12, 2004

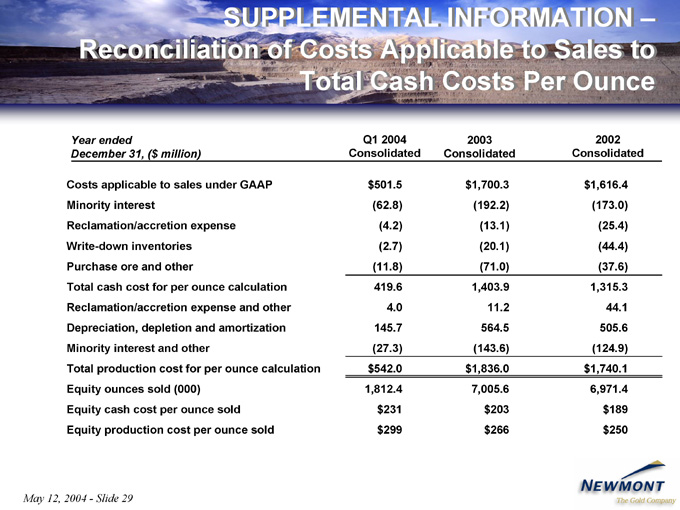

SUPPLEMENTAL INFORMATION – Reconciliation of Costs Applicable to Sales to Total Cash Costs Per Ounce

Year ended Q1 2004 2003 2002

December 31, ($ million) Consolidated Consolidated Consolidated

Costs applicable to sales under GAAP $ 501.5 $ 1,700.3 $ 1,616.4

Minority interest (62.8) (192.2) (173.0)

Reclamation/accretion expense (4.2) (13.1) (25.4)

Write-down inventories (2.7) (20.1) (44.4)

Purchase ore and other (11.8) (71.0) (37.6)

Total cash cost for per ounce calculation 419.6 1,403.9 1,315.3

Reclamation/accretion expense and other 4.0 11.2 44.1

Depreciation, depletion and amortization 145.7 564.5 505.6

Minority interest and other (27.3) (143.6) (124.9)

Total production cost for per ounce calculation $ 542.0 $ 1,836.0 $ 1,740.1

Equity ounces sold (000) 1,812.4 7,005.6 6,971.4

Equity cash cost per ounce sold $ 231 $ 203 $ 189

Equity production cost per ounce sold $ 299 $ 266 $ 250

May 12, 2004—Slide 29