Exhibit 99.1

Investor presentation November 12, 2015

Non-Gaap financial measures / Forward-Looking Statements 2 MarkWest Energy Partners, L.P. is a master limited partnership that owns and operates midstream services related businesses. MarkWest has a leading presence in many natural gas resource plays including the Marcellus Shale, Utica Shale, Huron/Berea Shale, Haynesville Shale, Woodford Shale and Granite Wash formation where it provides midstream services to its producer customers. Cautionary Statement Regarding Forward-Looking Statements This communication includes “forward-looking statements.” All statements other than statements of historical facts included or incorporated herein may constitute forward-looking statements that involve a number of risks and uncertainties. These statements may include statements regarding the proposed acquisition of the Partnership by MPLX, the expected timetable for completing the transaction, benefits and synergies of the transaction, future opportunities for the combined company and any other statements regarding the Partnership’s and MPLX’s future operations, anticipated business levels, future earnings and distributions, planned activities, anticipated growth, market opportunities, strategies and competition. All such forward-looking statements involve estimates and assumptions that are subject to a number of risks, uncertainties and other factors that could cause actual results to differ materially from those expressed or implied in such statements. Factors that could cause or contribute to such differences include: factors relating to the satisfaction of the conditions to the proposed transaction, including regulatory approvals and the required approval of the Partnership’s unitholders; the parties’ ability to meet expectations regarding the timing and tax treatment of the proposed transaction; the possibility that the combined company may be unable to achieve expected synergies and operating efficiencies in connection with the transaction within the expected time-frames or at all; the integration of the Partnership being more difficult, time-consuming or costly than expected; the effect of any changes resulting from the proposed transaction in customer, supplier and other business relationships; general market perception of the proposed transaction; exposure to lawsuits and contingencies associated with MPLX; the ability to attract and retain key personnel; prevailing market conditions; changes in the economic and financial conditions of the Partnership and MPLX; uncertainties and matters beyond the control of management; and the other risks discussed in the periodic reports filed with the SEC, including the Partnership’s and MPLX’s Annual Reports on Form 10-K for the year ended December 31, 2014 and the Partnership’s Report on Form 10-Q for the quarter ended September 30, 2015. These risks, as well as other risks associated with the Partnership, MPLX and the proposed transaction are also more fully discussed in the proxy statement and prospectus included in the registration statement on Form S-4 filed with the SEC by MPLX and declared effective by the SEC on October 29, 2015. The Partnership has mailed the proxy statement/prospectus to its unitholders. The forward-looking statements should be considered in light of all these factors. In addition, other risks and uncertainties not presently known to the Partnership or MPLX or that the Partnership or MPLX considers immaterial could affect the accuracy of the forward-looking statements. The reader is cautioned not to rely unduly on these forward-looking statements. The Partnership and MPLX does not undertake any duty to update any forward-looking statement except as required by law.

Additional Information 3 Additional Information and Where to Find It This communication may be deemed to be solicitation material in respect of the proposed acquisition of the Partnership by MPLX. In connection with the proposed acquisition, the Partnership and MPLX have filed relevant materials with the SEC, including MPLX’s registration statement on Form S-4 that includes a definitive proxy statement and a prospectus and was declared effective by the SEC on October 29, 2015. Investors and security holders are urged to read all relevant documents filed with the SEC, including the definitive proxy statement and prospectus, because they contain important information about the proposed transaction. Investors and security holders are able to obtain the documents free of charge at the SEC’s website, http://www.sec.gov, or for free from the Partnership by contacting Investor Relations by phone at 1-(866) 858-0482 or by email at investorrelations@markwest.com or for free from MPLX LP at its website, http://ir.mplx.com, or in writing at 200 E. Hardin Street, Findlay, Ohio 45840, Attention: Corporate Secretary. Participants in Solicitation This communication is not a solicitation of a proxy from any investor or securityholder. However, the Partnership and its directors and executive officers and certain employees may be deemed to be participants in the solicitation of proxies from the holders of Partnership common units with respect to the proposed transaction. Information about the Partnership’s directors and executive officers is set forth in the proxy statement for the Partnership’s 2015 Annual Meeting of Common Unitholders, which was filed with the SEC on April 23, 2015 and the Partnership’s current reports on Form 8-K, as filed with the SEC on May 5, 2015, May 19, 2015 and June 8, 2015, and in the prospectus filed by MPLX on October 30, 2015 and the related Registration Statement on Form S-4, which was declared effective by the SEC on October 29, 2015. Information about MPLX’s directors and executive officers is available in MPLX’s Annual Report on Form 10-K filed with the SEC on February 27, 2015 and MPLX’s current report on Form 8-K, as filed with the SEC on March 9, 2015. To the extent holdings of Partnership securities have changed since the amounts contained in the definitive proxy statement filed by the Partnership, such changes have been or will be reflected on Statements of Change in Ownership on Form 4 filed with the SEC. Investors may obtain additional information regarding the interest of such participants by reading the joint proxy statement and prospectus regarding the acquisition. These documents may be obtained free of charge from the SEC’s website http://www.sec.gov, or from the Partnership and MPLX using the contact information above. Non-Solicitation This communication shall not constitute an offer to sell or the solicitation of an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended.

MWE and MPLX – A Strategic Combination That Will Deliver Enhanced Value Powerful combination with ability to capitalize on significant growth opportunities to deliver increased value to unitholders Multiple platforms with vast opportunities to drive growth and capture commercial synergies Enhanced access to lower cost of debt and equity capital Compelling value to MWE unitholders Significant and immediate premium with recent increase in cash consideration of $400 MM $1.075 Bn cash contribution by MPC represents >70% of incremental IDRs MPC expects to receive in aggregate from 2016 through 2019 Peer-leading distribution growth and substantially lower equity yield will enhance investor returns and deliver long-term value accretion MWE unitholders will own ~73% of MPLX common units after closing Strong sponsor, Marathon Petroleum Corporation (MPC), 4th largest U.S. refiner, is dedicated to the success of the combined partnership Reaffirmed commitment to grow MPLX's distribution at a mid-20% CAGR through 2019 MPC possesses numerous tools to facilitate / achieve such growth Inventory of drop-down assets is ≥$1.6 Bn of EBITDA The MarkWest Board conducted a thorough strategic review process and recommends the combination with MPLX 4

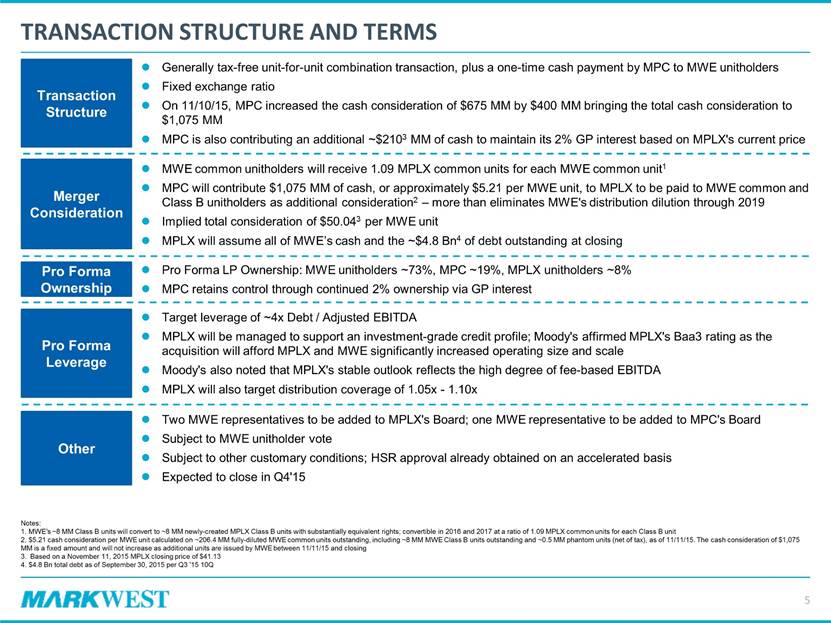

Transaction Structure and Terms Merger Consideration Other Transaction Structure MWE common unitholders will receive 1.09 MPLX common units for each MWE common unit1 MPC will contribute $1,075 MM of cash, or approximately $5.21 per MWE unit, to MPLX to be paid to MWE common and Class B unitholders as additional consideration2 – more than eliminates MWE's distribution dilution through 2019 Implied total consideration of $50.043 per MWE unit MPLX will assume all of MWE’s cash and the ~$4.8 Bn4 of debt outstanding at closing Two MWE representatives to be added to MPLX's Board; one MWE representative to be added to MPC's Board Subject to MWE unitholder vote Subject to other customary conditions; HSR approval already obtained on an accelerated basis Expected to close in Q4'15 Generally tax-free unit-for-unit combination transaction, plus a one-time cash payment by MPC to MWE unitholders Fixed exchange ratio On 11/10/15, MPC increased the cash consideration of $675 MM by $400 MM bringing the total cash consideration to $1,075 MM MPC is also contributing an additional ~$2103 MM of cash to maintain its 2% GP interest based on MPLX's current price Pro Forma Ownership Pro Forma LP Ownership: MWE unitholders ~73%, MPC ~19%, MPLX unitholders ~8% MPC retains control through continued 2% ownership via GP interest Notes: 1. MWE's ~8 MM Class B units will convert to ~8 MM newly-created MPLX Class B units with substantially equivalent rights; convertible in 2016 and 2017 at a ratio of 1.09 MPLX common units for each Class B unit 2. $5.21 cash consideration per MWE unit calculated on ~206.4 MM fully-diluted MWE common units outstanding, including ~8 MM MWE Class B units outstanding and ~0.5 MM phantom units (net of tax), as of 11/11/15. The cash consideration of $1,075 MM is a fixed amount and will not increase as additional units are issued by MWE between 11/11/15 and closing 3. Based on a November 11, 2015 MPLX closing price of $41.13 4. $4.8 Bn total debt as of September 30, 2015 per Q3 '15 10Q Pro Forma Leverage Target leverage of ~4x Debt / Adjusted EBITDA MPLX will be managed to support an investment-grade credit profile; Moody's affirmed MPLX's Baa3 rating as the acquisition will afford MPLX and MWE significantly increased operating size and scale Moody's also noted that MPLX's stable outlook reflects the high degree of fee-based EBITDA MPLX will also target distribution coverage of 1.05x - 1.10x 5

Thorough Strategic Review and Transaction Process 1 Competitive process and extensive negotiation resulted in best terms for MWE Throughout 2014 and Q1 2015, MWE and MPC / MPLX held discussions regarding potential JV and commercial arrangements In March 2015, MWE asked its financial advisor, Jefferies, to present to the MWE GP Board (the "Board") potential strategic opportunities (e.g., JVs, acquisitions and strategic mergers) available to MWE On March 26, the Board was given an update by MWE management regarding potential JV and commercial arrangements with MPC / MPLX, including the potential for a broader strategic transaction, and the board mandated management to continue discussions MWE's April 2015 negotiations with MPLX began with an initial offer of 1.03x – 1.07x exchange ratio (all equity; no cash), which represented a premium of 21% and 26% respectively; through several weeks of negotiations, MarkWest was able to achieve an increase from the initial offer that culminated with a 1.09x exchange ratio, plus a $675 MM cash contribution by MPC without any additional MPLX equity in exchange, which represented a premium of 31% The Board established a transaction committee on June 22, 2015 consisting solely of independent directors in order to facilitate communication amongst the board members and provide guidance to management In July 2015, MPLX re-affirmed its April merger proposal of a 1.09x exchange ratio and $675 MM cash contribution by MPC, despite the continuing deterioration of market conditions Economic value exceeded the values of other bidders (Company A and B) and other transaction alternatives Competing bidders had the opportunity to improve bids Competing bidders were aware that MWE was undertaking a review of strategic alternatives After completion of thorough negotiations and consideration of all factors the board unanimously voted for approval of the merger on July 11, 2015 Energy Minerals Group, a long-term partner and significant equity holder of MWE, supported the transaction via a voting agreement for its approximate 7.4MM common units (~4%) Since the transaction announcement on 7/13/2015, MarkWest has not received bids from other parties On November 10, 2015, MarkWest, MPC and MPLX agreed to increase the cash consideration by $400 MM payable to MarkWest unitholders Note: 1 Full description can be found in the definitive proxy statement filed on October 30, 2015 6

Strong Sponsor has Many Options to Support MPLX Capacity to incubate growth projects at the parent Balance sheet strength for large projects Minimizes upfront dilution of projects at MPLX GP cash flows enhance flexibility GP IDR give-backs, caps or other modifications to distributions/cash flows Consideration around purchase price / multiple for drops Receive units as consideration in drop-downs from MPC to MPLX Intercompany funding through debt or equity Commercial arrangements with parent: Minimum volume commitments – provide stability of cash flows Commodity risk retained by parent – reduces volatility MLPs that are owned by strong sponsors with robust drop-down inventory have outperformed the broader MLP market Many sponsors have recently “de-risked” their underlying MLPs’ business growth plan and MPC offers the pro-forma MLP the same benefits 7 MPC is a Fortune 25 Company with ~$30 Bn market cap that has a large, investment grade balance sheet and significant liquidity/free cash flow

Stand-Alone and Pro Forma Comparison Baa2 / BBB Baa3 / BBB- Enterprise Value 2016E Coverage Yield Current / Expected Debt Leverage 2016 – 2019 LP Distribution CAGR Pro Forma Ba3 / BB ~$15.2 Bn ~$4.0 Bn ~$34.5 Bn ~$19.2 Bn 1.05x – 1.10x ~1.00x 1.05x – 1.10x 8.2% 4.6% 3.5% - 4.5% ~8.0% - 10.0% ~20.0% - 25.0% ~20.0% - 25.0% Baa3 / BBB- Current / Expected Credit Rating Target Leverage of ~4.0x Debt / Adjusted EBITDA ~3.0x ~4.6x MWE’s largest competitors benefit from greater financial flexibility to fund investment due to their investment grade profile, high trading multiples and ability to retain earnings The combined MWE/MPLX entity will have higher distribution coverage, lower debt leverage, a lower debt and equity cost, and an investment grade credit profile The enhanced financial profile provides the flexibility to more adequately fund the pro forma entity’s growth projects, including the additional $6.0 Bn - $9.0 Bn of identified future organic growth projects that would not otherwise be available to MarkWest on a stand-alone basis 8 Pro Forma entity has significantly more Financial Flexibility 2015-2016 LP Distribution CAGR 4.3% 25.0% 25.0%

3.1 Bcf/d Total Gathering Volumes Markwest is one of the largest midstream service providers Total Processed Volumes 5.2 Bcf/d 275 MBbl/d Total Fractionated Volumes 9 Volumes represent 3Q2015 Average MarkWest processes approximately 75% of total rich-gas production from the Marcellus and Utica Total NGL Production 325 MBbl/d #2 Processor in U.S. #4 Transmission Capacity 1.4 Bcf/d 10% Total U.S. NGLs Fractionator in U.S. #4

And When Combined with MPC’s Large Downstream Asset Base Global Markets High Performance Resource Plays Being well positioned in premier shale plays drives the opportunity for new midstream and downstream projects to complete the value chain 10 Significant Synergies and Opportunities Are Created Across the Value Chain Upstream Continued production growth in key basins drives midstream infrastructure requirements Improving efficiency and productivity Midstream Gathering, processing, and fractionation Connecting the wellhead to downstream markets Downstream Feedstock supply from midstream assets Growing blendstock and refined product demand

Premier Positions Drive $6 bn to $9 bn of potential investment Investment Opportunities in Marcellus & Utica: Expansion of dry-gas gathering systems Expansion of Ohio condensate facility Long-haul pipelines, storage, and terminal facilities Developing “Mont Belvieu” capabilities in the region, i.e. alkylation & gasoline blending, PDH & BDH, etc. Infrastructure to support ethane cracker development Investment Opportunities in Northeast: Development of additional midstream infrastructure to support the emerging Rogersville Shale Investment Opportunities in the Gulf Coast and Southwest: Midstream infrastructure to support MPC’s refinery operations Olefin projects at Javelina Complex Development of NGL pipelines and transportation infrastructure Opportunity in other resource plays Strategic combination allows pursuit of multiple incremental investment opportunities 11

Gathering & Processing MLPs – Yield and TEV Refined Products / Crude MLPs – Yield and TEV Sponsor Sponsor TEV $188 $37 $54 $35 Sponsor Sponsor TEV $12 $15 $4 $53 $6 / $23 Sponsored Drop-Down MLPs Across the sector trade at better valuations than independent / non-drop-down MLps Source: Wall Street research and company filings. Pricing as of 11/11/2015. Listed as non-drop-down MLP because, not withstanding sponsorship from DVN, there is no remaining drop-down inventory Sponsored by utilities and/or private equity firms but have limited/no market-ready drop-downs. Includes implied equity value of GP. ($Billions) Avg. Drop-Down Yield: 3.1% Avg. Independent Yield: 7.0% Avg. Drop-Down Yield: 5.2% Avg. Independent Yield: 10.9% Drop-Down Independent / Non-Drop-Down TEV ($Bn) (3) 12 ($Billions) $34 (1) (2) (2) Drop-Down Independent / Non-Drop-Down TEV ($Bn) (3) 2.4% 2.5% 2.8% 4.6% 4.7% 6.3% 7.0% 10.1% $- $4 $8 $12 $16 $20 0% 2% 4% 6% 8% 10% 12% SHLX VLP PSXP MPLX MMP GEL BPL NS 3.5% 3.8% 5.3% 6.3% 7.3% 8.2% 9.2% 11.4% 11.8% 12.5% 12.7% $- $4 $8 $12 $16 $20 0% 2% 4% 6% 8% 10% 12% 14% AM EQM RMP WES CNNX MWE ENLK DPM ENBL SMLP NGLS

Current Yields of Drop-Down MLPs Correlation Between Growth and Yield MLps with Substantial, visible growth achieve higher valuation Key Points MLPs with “embedded growth” in the form of identified drop-downs from parent companies or other highly visible growth outperform peers with lower near-term growth prospects The tightest yielding MLPs – on average – have the highest expected distribution growth CAGRs; indicating that investors are rewarding growth in the MLP sector Median: 4.2% Consensus Estimate 2015 – 2018 LP Distribution CAGR Current Yield Source: Market data and Wall Street research consensus estimates as of 11/11/15. MLPs with “embedded growth” in the form of identified drop-downs from parent companies or other highly visible growth outperform peers with lower near-term growth prospects The tightest yielding MLPs – on average – have the highest expected distribution growth CAGRs; indicating that investors are rewarding growth in the MLP sector 13 R² = 0.7713 0% 2% 4% 6% 8% 10% 12% 14% 0% 5% 10% 15% 20% 25% 30% 35% 2.4% 2.5% 2.5% 2.8% 3.5% 3.8% 4.6% 4.8% 5.3% 5.6% 6.3% 7.3% SHLX VLP DM PSXP AM EQM MPLX CPPL RMP TLLP WES CNNX

Offer premium Key Points MLPs with “embedded growth” in the form of identified drop-downs from parent companies or other highly visible growth outperform peers with lower near-term growth prospects The tightest yielding MLPs – on average – have the highest expected distribution growth CAGRs; indicating that investors are rewarding growth in the MLP sector Source: Market data as of 11/11/15; Implied offer price includes $5.21 / unit cash consideration. G&P Peers include the following MLPs: WES, NGLS, ENLK, EQM, DPM, AM, CNNX, SMLP, ENBL Crude Oil & Refined Products Peers include the following MLPs: TLLP, PSXP, VLP, HEP, MMP, SXL, BPL, NS, SHLX Drop-Down MLPs include the following MLPs: PSXP, VLP, SHLX, SMLP, WES, AM, CPPL, CNXC, RMP, DM MLPs with “embedded growth” in the form of identified drop-downs from parent companies or other highly visible growth outperform peers with lower near-term growth prospects The tightest yielding MLPs – on average – have the highest expected distribution growth CAGRs; indicating that investors are rewarding growth in the MLP sector 14 Offer Performance: (16.3%) Crude Oil & Refined Products Peers : (13.2%) (2) G&P MLPs : (24.9%) Drop-Down MLPs : (24.1%) (3) (2) Alerian MLP Index: (21.6%) (50%) (40%) (30%) (20%) (10%) 0% 10% 20% 10-Jul 14-Jul 18-Jul 22-Jul 26-Jul 30-Jul 3-Aug 7-Aug 11-Aug 15-Aug 19-Aug 23-Aug 27-Aug 31-Aug 4-Sep 8-Sep 12-Sep 16-Sep 20-Sep 24-Sep 28-Sep 2-Oct 6-Oct 10-Oct 14-Oct 18-Oct 22-Oct 26-Oct 30-Oct 3-Nov 7-Nov 11-Nov G&P Peers Crude Oil & Refined Products Peers Implied Offer Drop-Down MLPs Alerian MLP Index Illustrative Premium Sensitivity Analysis MPLX Median Low Average Best-in- MWE Unaffected Unit Price (As of 7/10/15) $59.75 Yield as of Drop-Down Drop-Down Crude/Refined Class % Decline of G&P Peers (1) Since Announcement (24.9%) 11/11/2015 MLP Yield MLP Yield MLP Yield MLP Yield Implied Unaffected Unit Price - Adjusted Peers 44.88 $ MPLX Unit Price (As of 11/11/15) $41.13 Illustrative Yield 4.57% 4.00% 3.50% 3.00% 2.50% Exchange Ratio 1.090x Implied Pro Forma MPLX Unit Price 41.13 $ 47.00 $ 53.71 $ 62.67 $ 75.20 $ Equity Consideration Per MWE Unit $44.83 Adjusted for 1.090x Exchange Ratio 44.83 51.23 58.55 68.31 81.97 Plus: Cash Consideration Per Unit 5.21 $ Cash Consideration Per Unit 5.21 5.21 5.21 5.21 5.21 Offer Price 50.04 $ Illustrative Offer Price 50.04 $ 56.44 $ 63.75 $ 73.51 $ 87.17 $ Implied Premium to Adjusted Unaffected Price 11.5% Illustrative Premium to Adjusted Unaffected Price 11.5% 25.7% 42.0% 63.8% 94.2%

Distributions to MWE unitholders Distribution Growth Guidance: MPLX expects compound annual distribution growth rate of ≥25% through 2017 and approximately 20% annual distribution growth in years 2018 and 2019 MWE forecasts a 4.3% distribution growth rate in 2016 and also expects to be able to achieve an 8% to 10% annual distribution growth rate from 2017 to 2020 Upfront cash payment of ~$5.21 per unit more than offsets the difference between MWE’s standalone distribution and MPLX’s forecasted distribution through 2019 15 Upfront cash payment of ~$5.21 per unit more than addresses dilution concerns and provides additional accretion of ~$1.00 - ~$1.50 per unit

Combination Benefits to MarkWest Unitholders Substantial economic value offered to unitholders through upfront cash consideration of ~$5.21 per unit, and potential for meaningful equity value accretion given 1.09x exchange ratio Peer-leading distribution growth profile anchored by combined organic growth prospects and MPC's substantial drop-down inventory Greater operational diversification and enhanced fee-based cash flows provide enhanced stability in this environment Access to substantially lower cost equity and debt capital $6 Bn - $9 Bn of incremental commercial growth opportunities to be executed together Strong sponsorship in MPC that is committed to the growth and success of the combined partnership 16

1515 Arapahoe Street Tower 1, Suite 1600 Denver, Colorado 80202 Phone: 303-925-9200 Investor Relations: 866-858-0482 Email: investorrelations@markwest.com Website: www.markwest.com