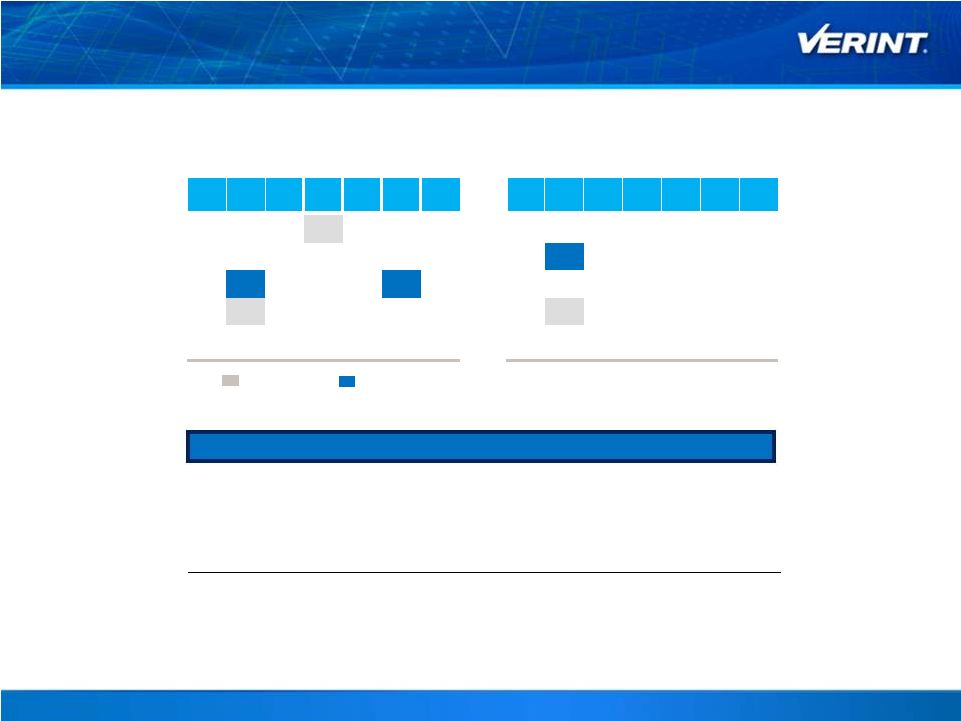

23 Compelling Combination Favorable Industry Reaction to the Transaction…. …And Industry Experts …From Wall Street Analysts… “ Kana enhances VRNT's SaaS capabilities and call center technologies and deepens its reach into customer experience and workforce optimization solutions. ” “ We believe this acquisition is a significant enhancement for Verint, as it augments the company's existing solution suite to include significant online/e-business capabilities, such as response management for e-mail, chat, and social media, as well as KANA's agent desktop solution. ” “ We like the transaction as it could accelerate the adoption of customer engagement suites through the deployment of a solution set from a single vendor and increase the company's importance as a strategic supplier. KANA Software should add ~800 employees (200 in R&D) and ~900 customers to Verint. We believe the move could be an important part in helping the overall growth rate accelerate into the double-digits. ” “ We like this acquisition as it is expected to be accretive to FY 2015 earnings (FYE January) and see it expanding the Company’s service suite in its fastest growing area – actionable intelligence. ” “ Big data and analytics meet customer experience. Verint expects to expand its customer engagement optimization offering with the acquisition of Kana. Verint's core capabilites, Vovici's voice of the customer assets, and Kana's multichannel customer experience solutions allow customers to move from data to information to insight to action or decisions. ” “ The acquisition provides greater gains than just complementary product lines, and a venue for both companies to expand their current footprints by cross-and upselling into their respective installed base. The acquisition provides a vision for deeply personalized customer service interactions which are delivered with maximum efficiency for a contact center. ” “ By offering a ‘best of breed’ customer support suite, with pre- integrated EFM capabilities, Verint should not only be able to sell the entire stack, and have infinite upsell opportunities with existing customers, but they also can better partner with companies to create a vision for EFM, and then enable the entire vision from phone calls to final analysis. ” “ Kana enhances VRNT's SaaS capabilities and call center technologies and deepens its reach into customer experience and workforce optimization solutions. ” |