Table of Contents

As filed with the Securities and Exchange Commission on April 29, 2015

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Alion Science and Technology Corporation

(Exact name of registrant as specified in its charter)

| Delaware | 8711 | 54-2061691 | ||

(State or other jurisdiction of incorporation or organization) | (Primary standard industrial classification code number) | (I.R.S. employer identification number) |

1750 Tysons Boulevard

Suite 1300

McLean, Virginia 22102

(703) 918-4480

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Bahman Atefi

President, Chairman and Chief Executive Officer

Alion Science and Technology Corporation

1750 Tysons Boulevard

Suite 1300

McLean, Virginia 22102

(703) 918-4480

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Kevin T. Boyle, Esq. Alion Science and Technology Corporation 1750 Tysons Boulevard Suite 1300 McLean, Virginia 22102 (703) 918-4480 | Stuart H. Gelfond, Esq. Joshua Wechsler, Esq. Fried, Frank, Harris, Shriver & Jacobson LLP One New York Plaza New York, New York 10004 (212) 859-8000 | Marc D. Jaffe, Esq. Senet S. Bischoff, Esq. Latham & Watkins LLP 885 Third Avenue New York, New York 10022 (212) 906-1200 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large Accelerated Filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

CALCULATION OF REGISTRATION FEE

| ||||

Title of Each Class of Securities to be Registered | Proposed Maximum Offering Price(1)(2) | Amount of Registration Fee | ||

Common Stock, $0.0001 par value per share | $100,000,000 | $11,620 | ||

| ||||

| ||||

| (1) | Includes offering price of shares of common stock which the underwriters have the option to purchase. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) of the Securities Act of 1933, as amended. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion. Dated April 29, 2015.

Shares

Alion Science and Technology Corporation

Common Stock

This is our initial public offering. We are offering shares of common stock.

Prior to this offering, there has been no public market for the common stock. It is currently estimated that the initial public offering price per share will be between $ and $ . We intend to list the common stock on under the symbol “ ”.

We are an “emerging growth company” and we are eligible for, but have not elected to adopt in this prospectus, reduced reporting requirements. See “Prospectus Summary—Implications of Being an Emerging Growth Company”.

See “Risk Factors” on page 17 to read about the factors you should consider before buying shares of the common stock.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Per | Total | |||

Initial public offering price | $ | $ | ||

Underwriting discount | $ | $ | ||

Proceeds, before expenses, to us | $ | $ |

To the extent that the underwriters sell more than shares of common stock, the underwriters have the option to purchase up to an additional shares from us at the initial price to the public less the underwriting discount.

The underwriters expect to deliver the shares against payment in New York, New York on , 2015.

| Credit Suisse | Jefferies | |

| Wells Fargo Securities | ||

Prospectus dated , 2015.

Table of Contents

| i | ||||

| i | ||||

| i | ||||

| iii | ||||

| 1 | ||||

| 17 | ||||

| 34 | ||||

| 35 | ||||

| 36 | ||||

| 37 | ||||

| 39 | ||||

| 41 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 43 | |||

| 78 | ||||

| 100 | ||||

| 108 | ||||

| 122 | ||||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 124 | |||

| 126 | ||||

| 131 | ||||

| 138 | ||||

| 139 | ||||

| 143 | ||||

| 146 | ||||

| 146 | ||||

| 146 | ||||

| F-1 |

Through and including , 2015 (the 25th day after the date of this prospectus), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus or any free writing prospectus that we, or someone on our behalf, have prepared. Neither we nor any underwriter take responsibility for, or can provide assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares that we are offering in this prospectus, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date.

Table of Contents

We obtained the industry, market and competitive position data used throughout this prospectus from our own research, surveys or studies conducted by third parties and industry or general publications. Industry publications and surveys generally state that they have obtained information from sources believed to be reliable, but do not guarantee the accuracy and completeness of such information. While we believe that each of these studies and publications is reliable, we have not independently verified such data. Similarly, we believe our internal research is reliable but it has not been verified by any independent sources.

This prospectus contains registered and unregistered trademarks and service marks of Alion Science and Technology Corporation and its affiliates, as well as trademarks and service marks of third parties. All brand names, trademarks and service marks appearing in this prospectus are the property of their respective holders. The following terms which may be used in this prospectus are our trademarks and/or trade names: Alion and the Alion logo.

The following are definitions of certain key terms used throughout this prospectus:

| • | “2010 Warrants” means the warrants issued by the Company on March 22, 2010 to holders of Secured Notes; |

| • | “2014 Refinancing” means the series of transactions that occurred on August 18, 2014, as described in the section entitled “Business – 2014 Refinancing”; |

| • | “2014 Warrants” means the warrants issued by the Company on August 18, 2014 to ASOF, Phoenix, and other holders of the Existing Third Lien Notes and the lenders under the Existing Second Lien Term Loan which, immediately prior to consummation of this offering and assuming consummation of the Transactions, will be exercised in full; |

| • | “ASOF” means ASOF II Investments, LLC; |

| • | “Company” means, unless the context requires otherwise, Alion Science and Technology Corporation, a Delaware corporation, and its subsidiaries on a consolidated basis; |

| • | “ESOP” means the Alion Science and Technology Corporation Employee Ownership, Savings and Investment Plan, as amended, which is sometimes referred to as the “Plan”, the “KSOP” or “Alion KSOP”; |

| • | “ESOP Trust” means the Alion Science and Technology Corporation Employee Ownership Savings and Investment Trust; |

| • | “Existing Credit Agreements” means the credit agreements entered into as part of the 2014 Refinancing governing the Existing First Lien Term Loan and the Existing Second Lien Term Loan, and the Existing Revolving Credit Facility, collectively; |

| • | “Existing Debt Instruments” means the Existing Credit Agreements and the indenture governing the Existing Third Lien Notes, collectively, entered into as part of the 2014 Refinancing; |

| • | “Existing First Lien Term Loan” means our first lien term loan in an initial aggregate principal amount of $285 million entered into as part of the 2014 Refinancing, which includes two tranches: Tranche A (in an initial aggregate principal amount of $110 million) and Tranche B (in an initial aggregate principal amount of $175 million); |

i

Table of Contents

| • | “Existing Revolving Credit Facility” means our $65 million (subject to borrowing base limitations) revolving credit facility entered into as part of the 2014 Refinancing, with Wells Fargo Bank, National Association, as administrative agent and the lenders party thereto; |

| • | “Existing Second Lien Term Loan” means our second lien credit agreement entered into as part of the 2014 Refinancing, in an initial aggregate principal amount of $70 million, with ASOF and JLP Credit Opportunity Master Fund Ltd., an affiliate of Phoenix, as lenders; |

| • | “Existing Third Lien Notes” means third lien notes (i) in initial aggregate principal amount of $208.1 million issued by the Company as part of the 2014 Refinancing, in exchange for approximately 90% of the Company’s Unsecured Notes, plus (ii) $2.9 million in aggregate principal amount issued for cash at a discount; |

| • | “Existing Warrants” means the 2010 Warrants and the 2014 Warrants; |

| • | “New Credit Agreement” means that new credit agreement or credit agreements the Company expects to enter into pursuant to the IPO Refinancing; |

| • | “Phoenix” means Phoenix Investment Adviser, LLC; |

| • | “Secured Notes” means the 12% Senior Secured Notes due 2014, which were refinanced in their entirety in 2014; |

| • | “Series A Preferred Stock” means shares of our outstanding Series A Preferred Stock, par value $0.01 per share, issued in August 2014, all of the outstanding shares of which, assuming the consummation of the Transactions, we expect will be eliminated in their entirety; |

| • | “Transactions” means (a) our initial public offering and (b) the refinancing, or the IPO Refinancing, in full of our currently outstanding debt, a portion of which we expect to refinance through committed financing and the remainder of which will be repaid in full with the proceeds of this offering; |

| • | “U.S. GAAP” means accounting principles generally accepted in the United States; and |

| • | “Unsecured Notes” means the 10.25% Senior Notes due 2015, which are no longer outstanding. |

ii

Table of Contents

NON-GAAP FINANCIAL MEASURES AND OTHER FINANCIAL INFORMATION

We have included certain financial measures in this prospectus that are not recognized under U.S. GAAP, including earnings before interest, income taxes, depreciation and amortization, which we refer to as EBITDA, and Consolidated EBITDA, which is defined in the Existing Credit Agreements. We believe that the presentation of EBITDA and Consolidated EBITDA enhances an investor’s understanding of our financial performance. We believe EBITDA is useful in assessing operating performance and in comparing our performance to other companies in the same industry. EBITDA is a common financial metric in the government contracting industry, in part because it excludes from performance the effects of a company’s capital structure, in particular taxes and interest. In addition, we believe Consolidated EBITDA can be useful in evaluating our ability to meet our debt covenants. Consolidated EBITDA information for the trailing four-quarters is used by management and is important to our security holders as our Existing Credit Agreements require that we achieve minimum trailing four-quarter Consolidated EBITDA levels and maintain a minimum one-to-one fixed charge coverage ratio, which is also measured on a trailing four-quarter basis at the end of each quarter. EBITDA and Consolidated EBITDA are not measures under U.S. GAAP and our use of the terms EBITDA and Consolidated EBITDA varies from others in our industry. EBITDA and Consolidated EBITDA should not be considered as alternatives to net income (loss), operating income or any other performance measures derived in accordance with U.S. GAAP, as measures of operating performance or operating cash flows or as measures of liquidity.

EBITDA and Consolidated EBITDA have material limitations as analytical tools and you should not consider them in isolation or as substitutes for analysis of our results as reported under U.S. GAAP. For example, EBITDA and Consolidated EBITDA:

| • | do not reflect any cash capital expenditure requirements for assets being depreciated and amortized that may have to be replaced in the future; |

| • | do not reflect changes in, or cash requirements for, our working capital needs; and |

| • | do not reflect the significant interest expense, or the cash requirements necessary to service interest or principal payments, on our debt. |

In addition, Consolidated EBITDA, as defined in the Existing Credit Agreements, reflects the cash impact relating to the Company’s ESOP and other long-term incentive plans (by adding back non-cash items and subtracting cash items that had been previously included in Consolidated EBITDA in prior periods), while EBITDA does not reflect such adjustments.

Numbers and percentages presented in the tables in this prospectus may not sum to the totals presented due to rounding.

iii

Table of Contents

This summary highlights selected information contained elsewhere in this prospectus, but is not complete and may not contain all of the information that is important to you or that you should consider before making an investment decision. To understand all of the terms of this offering and to attain a more complete understanding of our business and financial situation, you should read the entire prospectus carefully, including the “Risk Factors” section and the financial statements and related notes contained elsewhere in this prospectus.

Our Company

We are a leading provider of engineering solutions and services to the Federal Government for national defense, security and other critical government areas. Founded in 1936 as the Illinois Institute of Technology Research Institute, or IITRI, Alion and its highly skilled and educated employees have consistently been at the forefront of originating, developing and applying innovative scientific, engineering, technology and research and development solutions to our customers’ most complex challenges. Based in McLean, Virginia, we operate in three core business areas:

| • | Naval Architecture and Marine Engineering core business area, in which we provide technical expertise for ship and systems design as well as acquisition and production supervision, testing, delivery and engineering support to naval and commercial markets, both domestically and internationally. |

| • | Systems Analysis, Design and Engineering core business area, in which we provide services and technologies designed to enhance the performance and safety of complex systems and reduce costs. |

| • | Modeling, Simulation, Training and Analysis core business area, in which we leverage our proprietary software, services and technologies to improve mission effectiveness and readiness through the cost effective application of virtual training. |

A significant focus of our solutions and services is our agile engineering work, almost all of which is currently conducted in our systems analysis, design and engineering core business area. Agile engineering is the design, rapid prototyping, testing and limited production of systems and components. This is a substantial and growing part of our business. Within our agile engineering service we provide a broad range of solutions that respond directly to product line managers’ needs, usually on a time-critical basis. Our ability to progressively design, prototype, test and field solutions to emergent problems in close collaboration with (and often embedded in) customer teams results in effective, affordable and timely solutions. We believe our ability to combine traditional services with technological and engineering expertise in a time-critical, cost-efficient manner sets us apart in our industry.

Our solutions and services span the full lifecycle of key programs and provide us with long-standing, entrenched relationships with our customers. The long-term nature of our service offering also allows us to expand our footprint on existing programs and to use our capabilities and relationships to capture new growth opportunities. For fiscal year 2014, which ended on September 30, 2014, we generated revenue of $804.8 million, $68.0 million in Consolidated EBITDA and reported a net loss of $44.0 million. For the three months ended December 31, 2014 and 2013, we generated revenue of $227.9 million and $185.4 million, respectively, $19.2 million and $14.9 million in Consolidated EBITDA, respectively, and reported a net loss of $9.9 million and $18.5 million, respectively. This represents an increase in revenue and Consolidated EBITDA of 22.9% and 28.9%, respectively, and a decrease in net loss of 46.5%. For a discussion of our use of Consolidated EBITDA and a reconciliation to net loss, please refer to “– Summary Historical Consolidated Financial Data”.

We provide high-end research and development capabilities, technical expertise and operational support to a diverse group of U.S. government customers and, to a lesser degree, commercial and international customers. We serve customers in all branches of the U.S. military, a number of Cabinet-level U.S. government agencies, state and foreign governments and commercial customers. As of December 31, 2014, we had more than 200 distinct

1

Table of Contents

customers and over 500 active contracts. For calendar year 2014, U.S. Department of Defense, or DoD, customers represented 93.8% of our revenue and other civilian agencies and commercial customers accounted for 6.2% of our revenue.

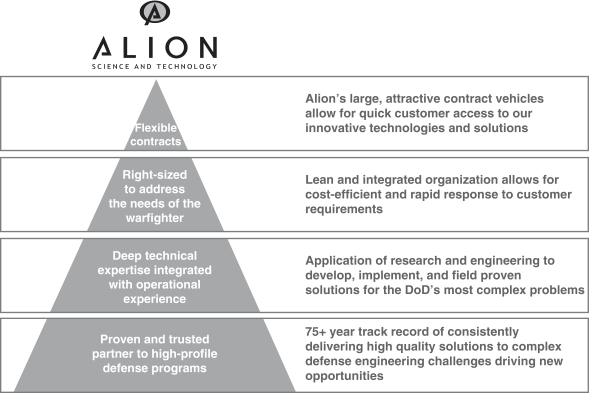

As illustrated in the diagram below, our value proposition is based on the strength of our customer relationships, combined with the quality, depth and skills of our people. This blend of capability and experience enables us to provide innovative and cost-efficient solutions to our customers’ most pressing problems. Our relentless focus on client-centric innovation is rooted in our heritage as a spin-out of IITRI and the passion and commitment of our highly educated workforce. Our business model is built upon a foundation of high-visibility, long-term programs with our long-standing customers, enabling us to continuously expand our presence into high-growth areas, both by responding to our customers’ identified needs as well as current or future challenges that we identify and work to solve for our customers.

We further attribute our growth to being well-aligned with priorities in the Navy, the Army, the Air Force and other DoD customers, which accounted for 54.7%, 16.0%, 15.2% and 8.0%, respectively, of our calendar year 2014 revenues. The overwhelming majority of our revenues are funded by the DoD base budget. Of our calendar year 2014 revenue, 93.7% was generated from cost reimbursable and time and material contracts, which carry lower risk, are more predictable and provide greater revenue visibility than fixed price contracts. With over 88% of our calendar year 2014 revenue generated as a prime contractor, we have direct relationships that provide deep insight into our customers’ priorities.

2

Table of Contents

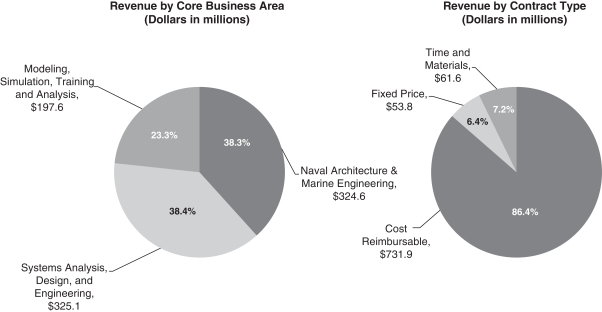

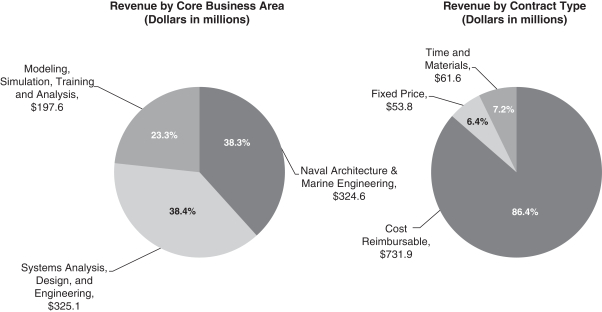

The following charts show our revenue by core business area and contract type for the 2014 calendar year:

Our innovative technology solutions in all of our core business areas are supported by our skilled employee base, which includes engineers, scientists, analysts and former military personnel. As of December 31, 2014, approximately 80% of our employees had security clearances, with approximately 30% of our employees holding clearances at the Top Secret level or above, allowing us access to highly classified DoD information systems and networks. Our workforce is highly educated with approximately 30% of degreed employees having PhDs or Masters degrees, 75% of which are in Engineering, Science or Math / Computer Science. To enhance our technology solutions, we have over 100,000 square feet of laboratory facilities, which we use to conduct customer-funded research and development activities, and to a lesser degree, internally-funded research and development activities.

We have a long operating history of providing a broad range of engineering-based solutions, from requirements development to the actual implementation, maintenance and upgrading of systems. We have supported the Information Analysis Centers for the Defense Technical Information Center for over 45 years and have been providing the U.S. Navy with naval architecture and marine engineering support for over 55 years. Illustrative examples of our engineering and technology solutions include:

| • | Alion provides agile engineering support for the modernization and upkeep of 146 Maritime Patrol and Reconnaissance Aircraft including multiple systems upgrades in the crew, electronics and radar systems. |

| • | Alion is the prime contractor for the in-service support services that lead maintenance and upgrade management for the Navy’s 158 surface combatant and amphibious ships. We coordinate the maintenance periods to ensure these combatants are available to support operational needs. |

| • | Alion provides agile engineering and in-service support to the U.S. Army to upgrade and maintain over 200 ground-based mobile surveillance systems. Our work integrated multiple technologies and upgrades to extend their service life and enhance system effectiveness. |

3

Table of Contents

| • | Alion is the prime contractor providing design, production, and in-service support across all of the Navy’s submarine classes for the Program Executive Officer Submarines. Our work spans design engineering, systems integration, logistics, production support, training, and in-service support across the 70 in-service submarines, six currently under construction, and the ongoing design of the Ohio Replacement Ballistic Missile Submarine Program. |

| • | Alion is the prime contractor responsible for the design, development, integration, test and operation of the Navy Continuous Training Environment, or NCTE. The NCTE integrates simulation and stimulation systems into a single environment, which enables Navy personnel to train and experiment in virtual worldwide locations with realistic weapons, communications, command and control systems operations, and interactions. |

| • | Alion is the developer of the Mobile Technology and Repair Complex for the Special Operations Forces, or SOF. These systems allow SOF to repair, modernize and fabricate equipment and material to execute a broad range of responsive engineering operations that address SOF-specific requirements and improve the effectiveness of deployed SOF mission capabilities in austere environments. |

The Market Opportunity

For U.S. government fiscal year 2015, the approved DoD appropriations totaled $560 billion. Of that amount, $496 billion was for the base budget and the remainder was for what are termed overseas contingency operations. While the Budget Control Act of 2011 is still in effect, lawmakers have made efforts over the past several years to protect U.S. defense appropriations, including the Ryan-Murray Agreement and the Bipartisan Budget Act of 2013. We believe that these efforts will continue to stabilize actual budget allocations.

Note: FY’08 through FY’15 represents actuals. FY’16 through FY’20 represents the President’s FY20l6 Budget request and forecast as submitted to Congress in February 2015.

Source: Department of Defense FY2016 Budget.

The overwhelming majority of Alion’s work and services are performed within the DoD’s base budget and in many cases focus on upgrading or optimizing existing programs and platforms efficiently and cost-effectively.

4

Table of Contents

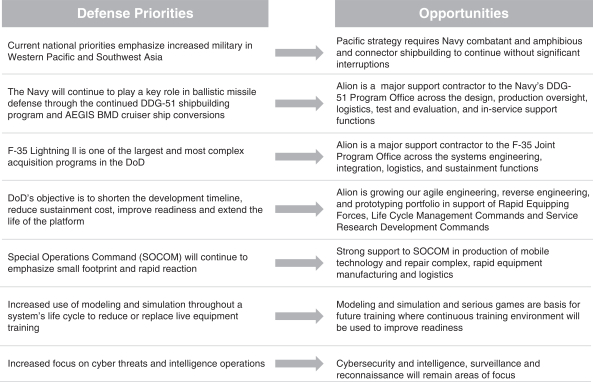

Alion growth opportunities are well-aligned with U.S. defense priorities. As illustrated in the chart below, Alion maintains a strong alignment with U.S. defense priorities. The DoD’s emphasis on an increased presence in the Asia-Pacific region is aligned with our work supporting the DDG-51 AEGIS Destroyer and the Flight III design and integration of Ballistic Missile Defense and the replacement fleet oiler required to support the Pacific region. DoD’s continuous investments to maintain technical superiority are aligned with our current engineering and technical work on critical programs, including F-35 Lightning II and the Ohio Replacement Ballistic Missile Submarine Program. Most importantly, our competency in agile engineering and rapid prototyping align with the DoD’s ongoing investments in existing platforms to address obsolescence, integrate new systems, upgrade legacy systems, extend in-service lives, and improve operational performance.

Attractive addressable market. We believe that the total addressable market for our three core business areas is approximately $68 billion per annum, comprising three main end customers: (1) the DoD, representing approximately $55 billion, (2) the commercial/international market, representing approximately $7 billion and (3) the federal civilian market, representing approximately $6 billion. Based on our size, our market share within each of these three core areas is less than 3%, with an overall market share of approximately 1%. We believe that based on our ability to win and retain business as well as expand our footprint with constantly evolving products and solutions, gains in market share should continue to support Alion’s growth profile.

Innovative science, engineering and technology solutions. We offer innovative science, engineering and technology solutions in all of our core business areas, which have been developed over our 79 year history. For example, our work in agile engineering sets us apart from our peers within the DoD market. Agile engineering is based in an approximately $5 billion per annum market for reset, repair and modernization of mature systems. For example, we are currently involved in upgrading the electronic warfare pod for the F-15 fighter aircraft to allow the radar warning receiver to better identify new threats. We are also involved in upgrading the Apache helicopter blade folding systems to develop an easier, less labor-intensive folding mechanism for helicopter

5

Table of Contents

transport. There is an additional approximately $3 billion per annum addressable market where our competency in agile engineering can be applied to address obsolescence in fielded mature systems. For example, we are currently involved in reverse engineering component designs to upgrade the P-3 radar systems in support of the Naval Air Command because existing spare part inventories were exhausted. We are also supporting the Army’s program manager for electro-optic infrared sensors to reset perimeter monitoring towers that were brought back from Iraq and Afghanistan. This reset includes integrating new full-spectrum sensors and full motion video.

Government focus on efficient, cost-effective solutions and procurement practices. Criticism of government inefficiencies has led to a focus on identifying opportunities to achieve “more with less”. We believe government demand for solutions that enhance, upgrade, sustain and improve existing platforms and programs will continue to increase. Offering holistic packages that combine strong technical and economic solutions with effective, customer-tailored contract structures represents a significant competitive advantage.

Our Value Proposition

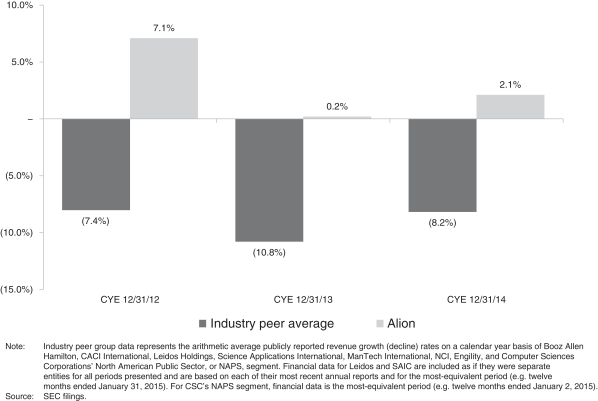

Relative revenue outperformance versus competitors in a challenging defense environment. Alion generated cumulative revenue growth of 9.1% from calendar year 2011 through 2014, and 2.1% from calendar year 2013 through 2014, which favorably compares with the average of our public company industry peers of cumulative revenue declines of (24.2)% and (8.2)%, respectively, as shown below. We believe Alion significantly outperformed that peer group due to our alignment with enduring defense priorities, and our ability to provide high-end, cost-effective services and solutions.

6

Table of Contents

Combining science, engineering and technology. We offer innovative science, engineering and technology solutions in all of our core business areas, which we have developed over our 79-year history. Our innovative solutions are supported by our skilled employee base, which includes engineers, scientists and former military personnel. This allows us to combine engineering capabilities, scientific skills and domain expertise to provide solutions that incorporate current technologies with real-world understanding of and experience with DoD programs, systems and networks. We employ approximately 2,800 people, at least 52% of whom have been with us for more than five fiscal years. Our workforce is highly educated, with approximately 30% of degreed employees having PhDs or Masters degrees, with 75% of those degrees in Engineering, Science or Math / Computer Science. Approximately 34% of our employees are veterans. As of December 31, 2014, approximately 80% of our employees had security clearances, with approximately 30% of our employees holding clearances at the Top Secret level or above, allowing us access to highly classified DoD systems and networks. To further enhance our technology solutions, we have over 100,000 square feet of laboratory facilities, which we use to conduct customer- and internally- funded technology and research and development activities, often times embedded within our customers facilities.

Large contract backlog and significant revenue visibility. As of December 31, 2014, our backlog was approximately $1.5 billion and approximately $499 million of this backlog was funded. The strength of our backlog provides us with longer-term visibility of our future revenue and the long-term nature of our contracts provides an ongoing revenue stream. As a result of our strong backlog, as of December 31, 2014, our fiscal year 2015 revenue forecast was 92% under contract.

Strong free cash flow generation. Our business model generates strong free cash flow as a result of low capital expenditure requirements and modest working capital needs. Our capital expenditures have been less than 1% of revenue on average over the past five fiscal years. We intend to utilize our strong free cash flow to continue to deleverage the business going forward. In addition, as of December 31, 2014, we had net operating loss carryforwards, or NOLs, and other deferred tax assets, of $241 million and $127 million, respectively.

Long-standing customer relationships. As a result of our innovative technology solutions and long operating legacy of superior performance, we have developed a strong reputation within our industry and with our customers for providing quality expertise in our core business areas. Our relationships across the DoD span decades.

Diverse government customer base with multiple contract vehicles. As of December 31, 2014, we perform services for a broad base of more than 200 distinct customers, including Cabinet-level government departments and agencies, and state and foreign governments. We earn revenue from our diverse customer base through a broad array of task orders that are issued under multiple contract vehicles awarded by U.S. government agencies and through other customers. Our multiple contract vehicles provide us with more flexibility to obtain tasking and associated funding from the U.S. government. For calendar year 2014, U.S. government contracts accounted for 97.3% of our revenue, with 93.8% of our revenue derived from DoD contracts. As of December 31, 2014, we had more than 200 distinct customers and over 500 active contracts. We are the prime contractor for 88% of the revenue generated in calendar year 2014 from our contracts. Our largest individual contract (stand-alone contract) accounted for approximately 8.0% of our revenues for calendar year 2014.

Experienced, consistent management team. The six senior members of our management team average more than 30 years of experience in the defense and related industry sectors, and have significant experience in government contracting. Members of senior management hold equity stakes through investment in our common stock through our ESOP.

7

Table of Contents

Our Strategy for Continued Growth

Our engineering capabilities are aligned with DoD budget and mission priorities. A critical part of the DoD’s success in the future will depend on cost-effective, rapid engineering solutions for critical platform and operational programs. Alion’s high-end agile engineering solutions provide a differentiated capability to support the DoD’s missions through modernization and upgrade of platforms and systems. Our design engineering and systems analysis services continue to address the DoD requirements for development of new programs and solutions to maintain the country’s technology edge and to meet the decisive superiority requirements of the 2014 Quadrennial Defense Review, or 2014 QDR. Alion’s deep domain knowledge, turn-key solutions approach, and design, production and in-service support offering directly support our current and continued growth. Our strategy to maintain our growth will leverage our experience and reputation to expand our work for existing and new customers. We will continue to leverage our high-end engineering and agile engineering services to support the modernization and upgrade of existing systems. We will further continue to broaden our core business areas through internal investment and organic growth that complements our customer-funded research and development in new capabilities, technologies, and solutions.

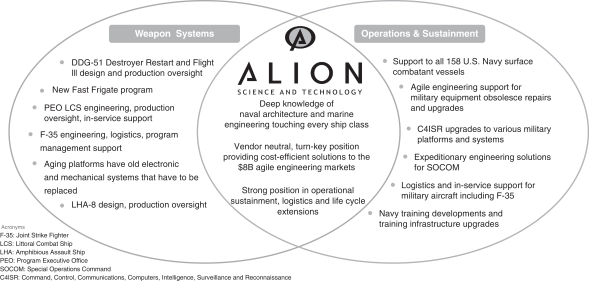

Alion’s technical services span the product life cycle, which allows us to service both new systems and programs as well as deliver agile engineering and in-service support services in the operations and sustainment of existing platforms and equipment, as shown in the following diagram.

Continue to prioritize organic revenue and cash flow growth. We completed our most recent corporate acquisition in calendar year 2007. Subsequently, our revenue has grown at a compounded annual growth rate of 2.2% despite a difficult defense budget environment, from $745.1 million for calendar year 2008 to $847.3 million for calendar year 2014. More recently, our revenue has grown on a sequential basis for each quarter of calendar year 2014. For the three months ended December 31, 2014, revenue increased by 22.9% over the three months ended December 31, 2013. Going forward, we plan to continue to prioritize organic revenue and cash flow growth and to further deleverage our balance sheet. For more than five years,Washington Technology and Defense News has continued to rank us among the top professional services government contractors.Washington Business Journal continues to rank us in its top 20 technology government contractors and government contract awardees.

8

Table of Contents

Multiple engines of growth. Alion will continue to invest in multiple engines of growth, including:

Agile engineering. Our agile engineering business more than doubled over the last three fiscal years, and accounted for approximately 20% of our calendar year 2014 revenue. Our competency in agile engineering and rapid prototyping align with the DoD’s ongoing investments in existing systems to address obsolescence, integrate upgrades, and improve operational performance. Our competency in agile engineering requires a high level of skill, but is cost-efficient, and provides a fast fix for our customers.

Continued growth in engineering services. We are expanding our design engineering, production oversight, test and evaluation and in-service support to the Navy warfare center community and international customers including Canada. We are expanding our systems engineering, logistics and foreign military sales support for the F-35 Lightning II Joint Project Office, multiple Naval Aviation programs, and the Littoral Combat Ship programs.

Expansion of our modeling & simulation, information technology and cybersecurity solutions. We will carry our prime role on NCTE across the fleet and shore-side infrastructure. We continue to grow our cyber capabilities to support training of cyber warriors by emulating the effects and remediation of cyber attacks. We are expanding our work across the cyber domain including electronic warfare, cyberspace operations, and military information support operations.

Continue to focus on operational efficiency and profitability. We remain focused on growing our business and continuously achieving operating efficiencies that will benefit our performance directly through increased profitability and indirectly through our increased competitiveness vis-à-vis our customers. In the past two fiscal years, we reduced annual operating costs by approximately $8.0 million. These operational improvements and cost reductions have enabled us to improve our competitive position by delivering cost effective solutions to the Federal Government. In addition, in the first quarter of fiscal year 2015, we began to implement additional cost reductions that we expect to reduce our annual operating costs by approximately $13.0 million.

Continue to attract and retain highly experienced employees. We plan to continue to expand our expertise, in particular in the areas of technological developments, where we believe we have a significant advantage over our competition. We hire skilled employees, engage in business development initiatives and invest in projects to expand our employees’ skill sets within our strong culture of innovation. We increase our employees’ technological and program management skills through training, internally funded projects and mentoring. We offer our employees non-degree programs in information technology, business, and desktop applications through “Alion University” to maintain and enhance our employees’ skills and advance our reputation in the commercial technology solutions markets. Additionally for the past four years,Military Times EDGE has voted us a “Best for Vets Employer”.

Contracting tools promote growth. Our Information Analysis Centers, or IAC, contracts provide an agile contracting mechanism across the Federal Government for best value for highly technical services. IAC vehicles are growing in popularity as our customers across the Federal Government use the IAC vehicles to rapidly access the most effective and advanced technologies and services. Our award values under the IAC programs grew 52% from fiscal year 2013 to fiscal year 2014 and our current pipeline of identified new business is over $2 billion.

Refinancing and Operational Initiatives

In August 2014, we completed a series of refinancing transactions in order to extend our debt maturities, reduce our cash interest expense and provide institutional sponsorship (as described more fully in “Business—2014 Refinancing”. Following the 2014 Refinancing, we reorganized by shifting to a matrix structure with four P&L centers reporting directly to the CEO, which eliminated management layers and associated indirect costs. We also

9

Table of Contents

engaged external consultants to conduct industry benchmarking, which has resulted in identifying meaningful cost-savings opportunities that enhance our competitive position on new bids. We continue to focus on gross margin expansion through improved program execution, diversification of our customer and contract mix and increasing of our labor content, as well as increased investment in and efficiency of our business development efforts.

IPO Refinancing

In connection with this offering, we intend to refinance all of our currently outstanding debt, a portion of which we expect to refinance through committed financing and the remainder of which will be repaid in full with the proceeds of this offering. See “Use of Proceeds”, “Capitalization” and “Description of Certain Indebtedness”.

Risks Relating to Our Business and This Offering

Participating in this offering involves substantial risk. Our ability to execute our strategies is also subject to certain risks. The risks described under the heading “Risk Factors” immediately following this summary may cause us not to realize the full benefits of our strengths or may cause us to be unable to successfully execute all or part of our strategies. Some of the more significant challenges and risks include the following:

| • | we depend on U.S. government contracts for substantially all of our revenue. Changes in the contracting or fiscal policies of the U.S. government could adversely affect our business, financial condition, results of operations and ability to satisfy our financial obligations, and grow our business; |

| • | delays in the federal budget process, including actions related to the need to raise the debt ceiling and any future Federal Government shutdown, could delay procurement of, and payment for, the products, services and solutions we provide and materially and adversely affect our revenue, gross margin, operating results and cash flow; |

| • | the Budget Control Act of 2011 caused significant delays or reductions in Federal Government appropriations for our current and future programs and may negatively affect our revenue and materially and adversely affect our financial condition, operating results, cash flows and ability to satisfy our financial obligation, and grow our business; |

| • | we face intense competition from many companies that have greater resources than we do. This could cause price reductions, reduced contract profitability, and loss of market share; |

| • | historically, a few contracts have provided most of our revenue. If we do not retain or replace these contracts our operations and financial condition will suffer; |

| • | if we are unable to achieve or manage growth, our business could be materially adversely affected; |

| • | we may lose one or more members of our senior management team or fail to develop new leaders, which could cause the disruption of the management of our business; |

| • | our business could suffer if we fail to attract, train and retain skilled employees; |

| • | our subcontractors’ failure to perform contractual obligations could damage our reputation as a prime contractor and our ability to obtain future business; |

| • | further adverse changes in market conditions, the stock market, the merger and acquisition environment in our industry or Federal Government budget constraints could adversely affect the value of our operating businesses which could cause us to recognize a goodwill impairment charge in the future; |

| • | our employees may engage in misconduct or other improper activities, which could harm our business; |

| • | many of our U.S. government customers produce goods and services through multiple delivery order type contracts under which we must compete for post-award orders; |

| • | U.S. government contracts contain termination provisions that are unfavorable to us; |

10

Table of Contents

| • | as a U.S. government contractor, we must comply with complex procurement laws and regulations and our failure to do so could result in suspension or debarment from doing business with the U.S. government or otherwise have a negative impact upon our business; |

| • | we derive significant revenue from U.S. government contracts awarded through competitive bidding, which is an inherently unpredictable process; |

| • | our business could be materially negatively impacted by security threats and breaches, including cybersecurity threats, and other disruptions; |

| • | our failure to maintain necessary security clearances may limit our ability to carry our confidential work for U.S. government customers, which could cause our revenue to decline; and |

| • | the other factors set forth under the “Risk Factors” in this prospectus. |

Before you participate in this offering, you should carefully consider all of the information in this prospectus, including those matters set forth under the heading “Risk Factors”.

Implications of Being an Emerging Growth Company

As a company with less than $1.0 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or JOBS Act. An emerging growth company may take advantage of specified reduced reporting and other requirements that are otherwise applicable generally to public companies. These provisions include:

| • | we are required to have only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations disclosure; |

| • | we are not required to engage an auditor to report on our internal controls over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002; |

| • | we are not required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements (i.e., an auditor discussion and analysis); |

| • | we are not required to submit certain executive compensation matters to stockholder advisory votes, such as “say-on-pay”, “say-on-frequency” and “say-on-golden parachutes”; and |

| • | we are not required to disclose certain executive compensation related items such as the correlation between executive compensation and performance and comparisons of the chief executive officer’s compensation to median employee compensation. |

We may take advantage of these provisions until the last day of our fiscal year following the fifth anniversary of the completion of this offering or such earlier time that we are no longer an emerging growth company. We would cease to be an emerging growth company if we have more than $1.0 billion in annual revenue, have more than $700 million in market value of our common stock held by non-affiliates, or issue more than $1.0 billion of non-convertible debt over a three-year period. We may choose to take advantage of some but not all of these reduced burdens. We have not elected to adopt the reduced disclosure in this prospectus other than with respect to the reduced disclosure in the section entitled “Selected Consolidated Financial Data”.

The JOBS Act permits an emerging growth company like us to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. We are choosing to “opt out” of this provision and, as a result, we will comply with new or revised accounting standards as required when they are adopted. This decision to opt out of the extended transition period is irrevocable.

11

Table of Contents

Corporate Information

We are a Delaware corporation. Our executive offices are located at 1750 Tysons Boulevard, Suite 1300, McLean, VA 22102, and our telephone number is (703) 918-4480. Our corporate website address is http://www.alionscience.com. Our website and the information contained on our website are not part of the prospectus, and information contained therein should not be relied upon when making an investment decision.

12

Table of Contents

The Offering

Issuer | Alion Science and Technology Corporation. |

Common stock offered by us | shares. |

Option to purchase additional shares of common stock from us | shares. |

Common stock outstanding immediately after the offering | shares, assuming no exercise of the underwriters’ option to purchase up to an additional shares of common stock from us. |

Use of proceeds | We estimate that the net proceeds we will receive from the sale of shares of our common stock in this offering, after deducting underwriter discounts and commissions and estimated offering expenses payable by us (assuming the shares are sold at the midpoint of the range on the cover of the prospectus), will be approximately $ , million, or $ million if the underwriters’ exercise their option to purchase additional shares in full. We intend to use the net proceeds from this offering to repay debt. See “Use of Proceeds”. |

Dividend policy | Alion has never declared any cash dividends. Following the completion of this offering, we do not expect to pay any dividends in the future and the terms of our debt instruments will limit our ability to do so. See “Dividend Policy”. |

Risk factors | See “Risk Factors” beginning on page 17 of this prospectus for a discussion of factors that you should carefully consider before deciding to invest in shares of our common stock. |

Listing | We intend to apply to have our common shares listed on the , under the symbol “ ”. |

Unless otherwise indicated, all information in this prospectus assumes or gives effect to:

| • | the IPO Refinancing; |

| • | the elimination of all of our outstanding Series A Preferred Stock as described in “Description of Capital Stock – Preferred Stock”; |

| • | full exercise of the 2014 Warrants as described in “Description of Capital Stock – 2014 Warrants”; |

| • | no exercise by the underwriters of their option to purchase additional shares of our common stock; and |

| • | an assumed initial public offering price of $ per share, the midpoint of the estimated offering price range set forth on the cover of this prospectus. |

13

Table of Contents

Summary Historical Consolidated Financial Data

The following tables present summary historical condensed consolidated financial data for each of our last three fiscal years ended September 30, 2014, 2013 and 2012, for the three months ended December 31, 2014 and 2013, for the twelve months ended December 31, 2014, and as of September 30, 2014 and 2013 and December 31, 2014. The summary historical condensed consolidated financial data for the fiscal years ended September 30, 2014, 2013 and 2012 and as of September 30, 2014 and 2013 have been derived from our audited financial statements which are included elsewhere in this prospectus. The summary historical condensed consolidated financial data for the three months ended December 31, 2014 and 2013 and as of December 31, 2014 has been derived from our unaudited condensed consolidated interim financial statements which are included elsewhere in this prospectus. The summary historical condensed consolidated financial data for the twelve months ended December 31, 2014 was calculated by adding amounts from our financial statements for the fiscal year ended September 30, 2014 to amounts from our unaudited financial statements for the three months ended December 31, 2014 and subtracting amounts from our unaudited financial statements for the three months ended December 31, 2013. In management’s opinion, the unaudited condensed consolidated financial statements reflect all adjustments and reclassifications that are necessary for a fair presentation of the periods presented.

The results presented below are not necessarily indicative of results that may be expected for any future period. The following information should be read in conjunction with “Capitalization”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, “Business” and our audited annual and unaudited interim financial statements and notes included elsewhere in this prospectus.

| Twelve Months Ended December 31, 2014 |

Three Months Ended | Fiscal Years Ended September 30, | ||||||||||||||||||||||

| 2014 | 2013 | 2014 | 2013 | 2012 | ||||||||||||||||||||

| (Dollars in thousands except per share data) | ||||||||||||||||||||||||

Consolidated Statement of Operations and Comprehensive Loss: | ||||||||||||||||||||||||

Contract revenue | $ | 847,301 | $ | 227,871 | $ | 185,380 | $ | 804,809 | $ | 848,972 | $ | 817,204 | ||||||||||||

Direct contract expense | 665,907 | 181,870 | 145,275 | 629,311 | 669,504 | 632,831 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Gross profit | 181,394 | 46,001 | 40,105 | 175,498 | 179,468 | 184,373 | ||||||||||||||||||

Operating expenses | 78,240 | 19,043 | 18,864 | 78,061 | 84,128 | 91,494 | ||||||||||||||||||

General and administrative expenses | 45,113 | 12,947 | 18,993 | 51,159 | 53,139 | 52,441 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Operating income | 58,041 | 14,011 | 2,248 | 46,278 | 42,201 | 40,438 | ||||||||||||||||||

Other income (expense) | ||||||||||||||||||||||||

Interest income | 58 | 14 | 11 | 55 | 55 | 78 | ||||||||||||||||||

Interest expense | (85,068 | ) | (22,353 | ) | (18,948 | ) | (81,661 | ) | (75,700 | ) | (74,934 | ) | ||||||||||||

Other | (105 | ) | (10 | ) | (28 | ) | (123 | ) | (84 | ) | (55 | ) | ||||||||||||

Change in warrant value | 10,095 | 201 | — | 9,894 | — | — | ||||||||||||||||||

Gain (loss) on debt extinguishment | (11,458 | ) | — | — | (11,458 | ) | 3,913 | — | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total other expense | (86,478 | ) | (22,148 | ) | (18,965 | ) | (83,294 | ) | (71,816 | ) | (74,911 | ) | ||||||||||||

Loss before income taxes | (28,435 | ) | (8,137 | ) | (16,717 | ) | (37,016 | ) | (29,615 | ) | (34,473 | ) | ||||||||||||

Income tax expense | (6,980 | ) | (1,746 | ) | (1,745 | ) | (6,980 | ) | (6,977 | ) | (6,974 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Net loss | $ | (35,417 | ) | $ | (9,883 | ) | $ | (18,462 | ) | $ | (43,996 | ) | $ | (36,592 | ) | $ | (41,447 | ) | ||||||

Post-retirement actuarial gains (loss) | (149 | ) | — | — | (149 | ) | �� | 279 | 26 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Comprehensive loss | $ | (35,566 | ) | $ | (9,883 | ) | $ | (18,462 | ) | $ | (44,145 | ) | $ | (36,313 | ) | $ | (41,421 | ) | ||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Loss Per Share Data: | ||||||||||||||||||||||||

Net loss per share of common stock | ||||||||||||||||||||||||

Basic | $ | (0.75 | ) | $ | (2.41 | ) | $ | (5.53 | ) | $ | (5.39 | ) | $ | (6.74 | ) | |||||||||

Diluted(a) | $ | (0.75 | ) | $ | (2.41 | ) | $ | (5.53 | ) | $ | (5.39 | ) | $ | (6.74 | ) | |||||||||

Weighted average shares of common stock outstanding | ||||||||||||||||||||||||

Basic | 13,106,777 | 7,659,817 | 7,952,248 | 6,787,660 | 6,148,438 | |||||||||||||||||||

Diluted(a) | 13,106,777 | 7,659,817 | 7,952,248 | 6,787,660 | 6,148,438 | |||||||||||||||||||

Pro Forma Earnings (Loss) Per Share Data(b): | ||||||||||||||||||||||||

Net income (loss) per share of common stock (unaudited) | ||||||||||||||||||||||||

Basic | $ | $ | ||||||||||||||||||||||

Diluted(c) | $ | $ | ||||||||||||||||||||||

Weighted average shares of common stock outstanding used in computing pro forma net income (loss) per share of common stock (unaudited) | ||||||||||||||||||||||||

Basic | ||||||||||||||||||||||||

Diluted(c) | ||||||||||||||||||||||||

14

Table of Contents

| Twelve Months Ended December 31, 2014 | Three Months Ended December 31, | Fiscal Years Ended September 30, | ||||||||||||||||||||||

| 2014 | 2013 | 2014 | 2013 | 2012 | ||||||||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||||||

Other Financial Data: | ||||||||||||||||||||||||

Capital expenditures | $ | (1,461 | ) | $ | (552 | ) | $ | (273 | ) | $ | (1,182 | ) | $ | (1,869 | ) | $ | (2,731 | ) | ||||||

EBITDA(d) | 61,164 | 15,266 | 3,536 | 49,435 | 53,433 | 52,178 | ||||||||||||||||||

Consolidated EBITDA(d) | 72,316 | 19,234 | 14,895 | 67,978 | 71,000 | 71,754 | ||||||||||||||||||

| As of December 31, 2014 | As of September 30, | |||||||||||

| 2014 | 2013 | |||||||||||

| (Dollars in thousands) | ||||||||||||

Consolidated Balance Sheet Data: | ||||||||||||

Cash and cash equivalents | $ | 12,984 | $ | 10,732 | $ | 25,613 | ||||||

Working capital | (2,554 | ) | 1,412 | 42,569 | ||||||||

Total assets | 607,674 | 604,269 | 624,626 | |||||||||

Total debt(e) | 575,875 | 569,028 | 556,118 | |||||||||

| (a) | Does not reflect the impact of the exercise of any warrants for any period. |

| (b) | Pro Forma net income (loss) per share data reflects the Transactions, including the issuance of shares of common stock in this offering and the IPO Refinancing, and the use of proceeds therefrom, full exercise of the 2014 Warrants, and the elimination of the Series A Preferred Stock, as if they had occurred on October 1, 2013. |

| (c) | Does not reflect the impact of the exercise of the 2010 Warrants for any period. |

| (d) | We have included certain financial measures in this prospectus that are not recognized under U.S. GAAP, including earnings before interest, income taxes, depreciation and amortization, which we refer to as EBITDA and Consolidated EBITDA, which is defined in our Existing Credit Agreements. We believe that the presentation of EBITDA and Consolidated EBITDA enhances an investor’s understanding of our financial performance. We believe EBITDA is useful in assessing operating performance and in comparing our performance to other companies in the same industry. EBITDA is a common financial metric in the government contracting industry, in part because it excludes from performance the effects of a company’s capital structure, in particular taxes and interest. In addition, we believe Consolidated EBITDA can be useful in evaluating our ability to meet our debt covenants. Consolidated EBITDA information for the trailing four-quarters is used by management and is important to our security holders as our Existing Credit Agreements require that we achieve minimum trailing four-quarter Consolidated EBITDA levels and maintain a minimum one-to-one fixed charge coverage ratio, which is also measured on a trailing four- quarter basis at the end of each quarter. EBITDA and Consolidated EBITDA are not measures under U.S. GAAP and our use of the terms EBITDA and Consolidated EBITDA varies from others in our industry. EBITDA and Consolidated EBITDA should not be considered as alternatives to net income (loss), operating income or any other performance measures derived in accordance with U.S. GAAP, as measures of operating performance or operating cash flows or as measures of liquidity. |

EBITDA and Consolidated EBITDA have material limitations as analytical tools and you should not consider them in isolation or as substitutes for analysis of our results as reported under U.S. GAAP. For example, EBITDA and Consolidated EBITDA:

| • | do not reflect any cash capital expenditure requirements for assets being depreciated and amortized that may have to be replaced in the future; |

| • | do not reflect changes in, or cash requirements for, our working capital needs; and |

| • | do not reflect the significant interest expense, or the cash requirements necessary to service interest or principal payments, on our debt. |

In addition, Consolidated EBITDA, as defined in the Existing Credit Agreements, reflects the cash impact relating to the Company’s ESOP and other long-term incentive plans (by adding back non-cash items and subtracting cash items that had been previously included in Consolidated EBITDA in prior periods), while EBITDA does not reflect such adjustments.

15

Table of Contents

The following table provides a reconciliation of our net loss to EBITDA and Consolidated EBITDA for the periods presented:

| Twelve Months Ended December 31, 2014 | Three Months Ended December 31, | Fiscal Years Ended September 30, | ||||||||||||||||||||||

| 2014 | 2013 | 2014 | 2013 | 2012 | ||||||||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||||||

Net loss | $ | (35,417 | ) | $ | (9,883 | ) | $ | (18,462 | ) | $ | (43,996 | ) | $ | (36,592 | ) | $ | (41,447 | ) | ||||||

Interest expense | 85,068 | 22,353 | 18,948 | 81,662 | 75,700 | 74,934 | ||||||||||||||||||

Income tax expense | 6,980 | 1,746 | 1,745 | 6,980 | 6,977 | 6,974 | ||||||||||||||||||

Depreciation and amortization | 4,533 | 1,050 | 1,305 | 4,789 | 7,348 | 11,717 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

EBITDA | $ | 61,164 | $ | 15,266 | $ | 3,536 | $ | 49,435 | $ | 53,433 | $ | 52,178 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Gain on asset sales | (1,500 | ) | — | — | (1,500 | ) | (157 | ) | (104 | ) | ||||||||||||||

Debt extinguishment gain | 11,458 | — | — | 11,458 | (3,913 | ) | — | |||||||||||||||||

Change in fair value of warrants(1) | (10,094 | ) | (201 | ) | — | (9,894 | ) | — | — | |||||||||||||||

Non-cash stock-based compensation expense (credit) | (21 | ) | 1 | 1 | (21 | ) | (219 | ) | (90 | ) | ||||||||||||||

Non-cash LTIP expense (credit) | 1,744 | 626 | 804 | 1,922 | 2,281 | 1,400 | ||||||||||||||||||

Non-cash ESOP and 401(k) contributions | 14,174 | 3,555 | 3,576 | 14,195 | 13,844 | 13,735 | ||||||||||||||||||

Employee salary deferrals used to purchase Alion common stock | — | — | — | — | 1,968 | 2,427 | ||||||||||||||||||

Cash paid for ESOP obligations | (457 | ) | (13 | ) | (238 | ) | (682 | ) | (1,636 | ) | (857 | ) | ||||||||||||

Cash paid for stock-based compensation | — | — | — | — | — | — | ||||||||||||||||||

Cash paid for LTIP grants | (1,858 | ) | — | — | (1,858 | ) | (1,843 | ) | (1,869 | ) | ||||||||||||||

Non-recurring expenses | (2,293 | ) | — | 7,216 | 4,923 | 7,242 | 4,934 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Consolidated EBITDA | $ | 72,316 | $ | 19,234 | $ | 14,895 | $ | 67,978 | $ | 71,000 | $ | 71,754 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Consolidated EBITDA margin | 8.5 | % | 8.4 | % | 8.0 | % | 8.4 | % | 8.4 | % | 8.8 | % | ||||||||||||

| (1) | The 2014 Warrants are derivative instruments measured at fair value. Their initial fair value was $16.4 million. From August 2014 to September 2014 the estimated value of the shares underlying the 2014 Warrants declined. From October 2014 through December 2014, the risk free interest rate used to value the 2014 Warrants declined. |

Our Existing Credit Agreements define Consolidated EBITDA. Each quarter the Company must achieve $50 million in minimum Consolidated EBITDA (on a trailing twelve-month basis) in order to maintain access to the Existing Revolving Credit Facility and avoid potential cross default under Alion’s other debt instruments. Alion exceeded the requirement by approximately $22.3 million for the twelve months ended December 31, 2014. Neither EBITDA nor Consolidated EBITDA is a measure of financial performance in accordance with generally accepted accounting principles. The Existing Credit Agreements permit Alion to exclude certain expenses and requires it to exclude certain one-time gains when computing Consolidated EBITDA.

| (e) | Total debt as of December 31, 2014 and September 30, 2014 consisted of obligations under the Existing Debt Instruments, as well as that portion of our Unsecured Notes that remained outstanding after the 2014 Refinancing, which were repaid in January 2015, and is net of unamortized debt issue costs and original issue discount. Total debt as of September 30, 2013 consisted of obligations under our prior revolving credit facility, our Secured Notes and our Unsecured Notes, as well as accrued PIK interest, and is net of unamortized debt issue costs and original issue discount. |

16

Table of Contents

An investment in our common stock involves a high degree of risk. You should carefully consider the following risks as well as the other information included in this prospectus, including under “Selected Consolidated Financial Data”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated and combined financial statements, as applicable, and related notes included elsewhere in this prospectus, before investing in our common stock. Any of the following risks could materially and adversely affect our business, financial condition or results of operations. In such a case, the trading price of our common stock could decline, and you may lose all or part of your investment in us.

Risks Related to Our Business and Operations

We depend on U.S. government contracts for substantially all of our revenue. Changes in the contracting or fiscal policies of the U.S. government could adversely affect our business, financial condition, results of operations and ability to satisfy our financial obligations, and grow our business.

For the calendar year 2014, U.S. government contracts accounted for 97.3% of our revenue, with 93.8% of our revenue derived from DoD contracts. The U.S. Navy is our largest single customer, generating 54.7% of our calendar year 2014 revenue. Changes in U.S. government contracting policies could directly affect our financial performance. Factors that could materially adversely affect our U.S. government contracting business include:

| • | budgetary constraints affecting U.S. government spending generally, or specific departments or agencies in particular; |

| • | changes in U.S. government fiscal policies or available funding; |

| • | U.S. government shutdowns, threatened shutdowns or budget delays; |

| • | changes in U.S. government defense and homeland security priorities; |

| • | changes in U.S. government programs or requirements; |

| • | U.S. government curtailment of its use of technology services firms; |

| • | adoption of new laws, regulations, or enforcement policies; |

| • | technological developments; |

| • | competition and consolidation in our industry; and |

| • | general economic conditions. |

These or other factors could cause U.S. government departments or agencies to reduce their purchases under contracts, to exercise their right to terminate contracts or fail to exercise options to renew contracts, any of which could have a material adverse effect on our business, financial condition, operating results and ability to meet our financial obligations.

Many of our U.S. government customers are subject to tightened constraints. We have substantial contracts in place with many U.S. government departments and agencies. Our continuing performance under these contracts, or the possibility of new contracts from these agencies, could be materially adversely affected by agency spending reductions or budget cutbacks. Such reductions or cutbacks could materially adversely affect our business, financial condition, operating results and ability to meet our financial obligations.

17

Table of Contents

Delays in the federal budget process, including actions related to the need to raise the debt ceiling and any future Federal Government shutdown, could delay procurement of, and payment for, the products, services and solutions we provide and materially and adversely affect our revenue, gross margin, operating results and cash flow.

We derive a significant portion of our revenue from the Federal Government and from prime contractors to the Federal Government. We expect to continue to do so. Funding under those contracts is conditioned upon the continuing availability of Congressional appropriations and agency budgets. Congress usually appropriates funds on a fiscal year basis even though contract performance may extend over many years. The programs in which we participate must compete with other Federal Government programs and policies for funding during the budget and appropriation process. Concerns about increased deficit spending, along with continued economic challenges, continue to place pressure on federal customer budgets. While we believe that our programs are well aligned with national defense and other priorities, legislative shifts in domestic spending and tax policy, changes in security, defense, and intelligence priorities, the affordability of our products and services, general economic conditions and developments, and other factors may affect a decision to fund or the level of funding for existing programs under which we perform contracts or proposed programs under which we might bid for future work. In addition, a continuing resolution allows U.S. government agencies to operate only at spending levels equal to or less than levels approved in the prior budget cycle, which can delay or even cancel new initiatives which could adversely affect our business, financial condition, operating results, cash flows and our ability to meet our financial obligations. Even if our contracts are fully funded, full or partial furloughs of government employees may also result in delays in our customers approving or paying our invoices.

Congress’ failure to agree on deficit reduction goals and disputes on whether to increase the debt ceiling create constraints on and uncertainties about the level of future federal spending. While specific budgetary decisions for the Federal Government’s next fiscal year are not yet known, such constraints could delay or cancel key programs in which we are involved and could materially and adversely affect our cash flows, liquidity and operating results. If the federal budget process were to result in a prolonged Federal Government shutdown, we could incur substantial unreimbursed labor or other costs, or it could delay or cancel key programs, which could materially and adversely affect our operating results, cash flow and liquidity.

In addition, when the U.S. government requires supplemental appropriations to operate or fund specific programs, and legislation to approve any supplemental appropriation bill is delayed, credit markets can react adversely to the uncertainty. Budgetary uncertainties and our lower credit rating could materially and adversely affect our access to credit and our overall liquidity. If we were to use our revolving credit facility to a greater extent and for greater amounts than we have in the recent past, this could also increase the cost of credit to us if our floating interest rates were to rise.

The Budget Control Act of 2011 caused significant delays or reductions in Federal Government appropriations for our current and future programs and may continue to negatively affect our revenue and materially and adversely affect our financial condition, operating results, cash flows and ability to satisfy our financial obligations, and grow our business.

In August 2011, Congress enacted the Budget Control Act intended to significantly reduce the federal deficit over ten years. The Budget Control Act established discretionary spending caps through 2021 and a Joint Committee of Congress to identify additional deficit reductions.

Although we believe we are well-positioned in areas the DoD has indicated are the focus for future defense spending, the Budget Control Act may continue to have a negative impact on our business and industry.

Management cannot forecast whether government shutdowns will disrupt our business or adversely affect timing of collection of our receivables in the future, but we did experience significant payment delays as a result of the government shutdown that occurred immediately after the end of fiscal year 2013. Earlier in fiscal year

18

Table of Contents

2013, the Federal Government altered some of its accelerated payment practices which affected the overall payment cycle of our invoices. It took us until the fourth quarter of fiscal year 2013 to recover from most of the effects of these changes.

We face intense competition from many companies that have greater resources than we do. This could cause price reductions, reduced contract profitability, and loss of market share.

We operate in highly competitive markets and often encounter intense competition to win contracts. If we are unable to successfully compete for new business, our revenue may not grow and operating margins may decline. Many of our competitors have greater financial, technical, marketing, and public relations resources, have larger client bases and have greater brand or name recognition than we do. Main competitors include, but are not limited to, U.S. federal systems integrators and service providers such as Booz Allen Hamilton, CACI International, Leidos Holdings, Science Applications International Corporation, ManTech International, NCI, Engility and the NAPS segment of Computer Sciences Corporation.

Our main competitors may be able to vie more effectively for very large-scale government contracts. Our main competitors also may be able to provide clients with different or greater capabilities or benefits than we can provide in areas such as technical qualifications, past performance on large-scale contracts, geographic presence, price, and availability of key professional personnel. Our competitors have established relationships among themselves or with third parties, including through mergers and acquisitions, to increase their ability to address client needs. They may establish new relationships, and new competitors or competitive alliances may emerge.

Our ability to compete for desirable contracts will depend in large part on the effectiveness of our internal and customer-funded research and development programs, our ability to offer better performance than our competitors at lower or comparable cost, the readiness of our facilities, equipment and personnel to perform the programs for which we compete, our ability to attract and retain key personnel, our financial viability as assessed by government contracting officers and our ability to write superior proposals. If we do not continue to compete effectively and win contracts, our future business, financial condition, results of operations and our ability to meet our financial obligations will be materially compromised.

Historically, a few contracts have provided most of our revenue. If we do not retain or replace these contracts, our operations and financial condition will suffer.

The following five Federal Government contracts (contract vehicles and stand-alone contracts) accounted for more than half of our revenue in fiscal years 2014, 2013 and 2012.

| 1. | Weapons System Technology Information Analysis Center for the Defense Technical and Information Center (26%, 28%, 17%) (Defense Technical Information Center Indefinite Delivery, Indefinite Quantity (IDIQ) contract vehicle); |

| 2. | Seaport-E Multiple Award Contract for the Naval Sea Systems Command (21%, 21%, 20%) (IDIQ contract vehicle); |

| 3. | Technical and Analytical Support for the U.S. Air Force (9%, 8%, 10%) (stand-alone contract); |

| 4. | Naval Sea Systems Command Surface Ships Life Cycle Program Management and Engineering Support (7%, 7%, 6%) (stand-alone contract); and |

| 5. | Software, Networks, Information, Modeling and Simulation for the Defense Technical and Information Center (6%, 2%, 0.2%) (IDIQ contract vehicle). |