Exhibit 3

DELIVERING ENERGY AROUND THE GLOBE

TABLE OF CONTENTS

Chairman’s Letter | 1 | |

Board of Directors and Officers | 4 | |

Tsakos Energy Navigation Board Committees | 5 | |

Financial Highlights | 7 | |

TEN Growth Charts | 8 | |

Management Review and Analysis | 11 | |

Newbuilding Program in the Year 2003 | 31 | |

General Market Overview - Supply and Demand | 36 | |

World Tanker Fleet | 39 | |

Vessel Prices | 40 | |

Vessel Earnings | 44 | |

Consolidated Financial Statements | 47 | |

TEN Fleet | 80 | |

Internet: www.tenn.gr

CHAIRMAN’S LETTER TO STOCKHOLDERS

April 27, 2004

Dear Fellow Shareowner:

Every year is important, particularly in the life of a young dynamic company. For Tsakos Energy Navigation (TEN), 2003, was very special, as it marked 10 years of continuous growth and sustained profitability.

HIGHLIGHTS OF 2003

| • | Record profits of $59.1 million |

| • | Record earnings per share of $3.45 (basic) |

| • | Record dividends of $1.00 per share |

| • | Six new buildings added to the fleet |

| • | Six new building orders contracted including four ice classed ships |

MILESTONES SINCE INCEPTION

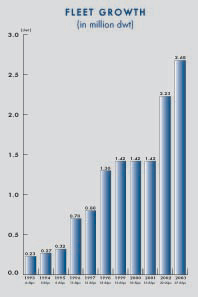

| • | Fleet in operation has grown from four vessels in 1993 to twenty-eight ships currently. |

| • | New building program commenced in 1997 includes sixteen ships currently generating revenues and thirteen vessels to be received in 2004, 2005, 2006, and 2007. |

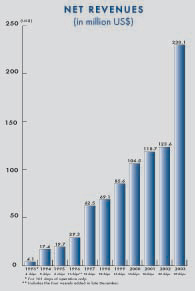

| • | Net revenues have grown to $230.1 million last year from a base of $15.8 million in 1994. |

| • | Net income was $2.6 million in 1994 and last year reached $59.1 million. |

| • | Earnings per share grew from $0.67 in 1994 to $3.45 in 2003. |

TEN takes great pride in its ability to produce these outstanding results while at the same time building a company whose human and physical assets are prepared for the challenges and opportunities of the future. Dynamic organic growth has resulted in a young modern fleet comprised of a diversified group of vessels capable of meeting the breadth of our clients’ requirements.

TEN’s FLEET AND TANKER INDUSTRY CHALLENGES

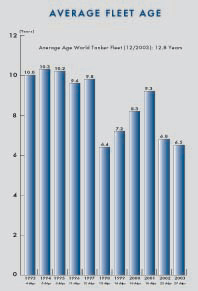

TEN has one of the youngest fleets in the world. Average tonnage age at the end of 2003 was 6.5 years as compared with the world fleet’s age of over 12 years. This key factor has taken on increasing importance.

The impact of shipping tragedies in 1999 and subsequent years has redefined acceptable tanker tonnage. The combination of much tighter regulatory restrictions on vessel ages and survey requirements and charterer vetting standards have resulted in much narrower selectivity among ships and their operators. A strong preference for younger tonnage is increasingly evident in comparative charter rates.

The new regulatory requirements and the overall impact on ownership economics is expected to accelerate vessel retirements. At the same time there is limited availability of new building berths. Thus, the outlook is one of constrained growth in the world’s tanker fleet during early future years.

The tanker industry is highly fragmented. However, the process of consolidation has begun and appears to be accelerating. Among the factors underlying this trend are: tighter vetting standards requiring scale to help moderate rising costs of doing business with first class charterers; limited availability of debt financing for older tonnage; and the significant capital needs to build and maintain a young modern fleet. TEN believes these developments will inure to the benefit of the company, its industry, and the customers it serves.

TEN LIMITED | 1 |

ECONOMIC BACKDROP

The world economy has delivered an erratic but positive performance in the past several months. The locomotion of an expanding U.S. economy has spurred dramatic growth in India, China, and the broader Pacific Rim. Most recently Japan has taken on a much improved tone arising from growing exports to China, Korea, and the U.S. Even domestic consumption appears at long last to be expanding. Unfortunately Europe has failed to keep pace barely avoiding a new recession while Latin America for the most part is burdened with financial and/or political impediments.

Most observers foresee a world economy in an overall growth mode in the foreseeable future. However, the shadow of geopolitical clouds, the pressures of sharply higher commodity prices including oil, and the twin deficits (trade and fiscal) in the U.S. suggest the path will be neither smooth nor riskless.

Growth in energy consumption is heavily dependent on affordability. Demand in the fastest growing economies is the most elastic. The substandard increase in oil demand at the turn of the century mirrored sluggish industrial activity, timid consumer absorption, warmer than normal winters in the northern hemisphere, and aggressive inventory policies. Happily each of these factors reversed last year and demand grew by a full 2%. Recent projections by the International Energy Agency suggest similar demand growth is likely this year although they express caution that a sustained high level of crude oil prices could moderate economic growth prospects with an impact on energy consumption. The principal growth drivers are once again U.S. consumption and the expansion spurts in India, China, and the greater Pacific Rim.

TANKER INDUSTRY

Last year the tanker industry enjoyed one of the strongest chartering markets in modern history. Early months of 2004 have seen a continuation of that environment. The severe temperatures of the winter months in virtually all areas of the northern hemisphere coupled with industrial expansion in India, China, and the Pacific Rim have driven oil demand and consumption to record levels. Much of the growth in consumption developed in markets more distant from the sources of supply with the resulting impact on ton-miles and shipping capacity requirements. This trend is projected to continue even as incremental production derives from Russia and Libya, which are somewhat nearer to consumers. The outlook for tanker capacity in 2004 remains unclear. High charter rates have discouraged scrappage despite the attraction of the sharp increase in steel scrap prices. However, the parallel impact on survey costs and the approaching regulatory deadlines will influence the timing of vessel retirements. The general expectation is that a seasonal dip in charter rates amplified by the likely cutback in OPEC production and a possible adjustment in the U.S.’ strategic reserves could encourage scrappage. On balance, the growth in the supply of tanker capacity could modestly exceed the expanded demand for transport. However, this small gap is likely to be absorbed by longer waiting times for older, less desirable tonnage.

The industry’s earning potential for 2004 is favorable. The solid chartering markets of the first three months are likely to hold up better than usual during the seasonal softness of spring and summer months. Key factors include slim inventories and growing import needs of China, India, and most markets on the Pacific Rim as well as the U.S. However, the revenue side will be offset by higher insurance rates, somewhat higher finance costs, rising maintenance expenses and general operating needs pushed by the soft dollar. On balance, the industry is likely to enjoy a second year of strong profits extending the recovery from the depressed results of 2002.

TEN’s PROSPECTS

TEN’s longer term prospects are very bright. The growth since inception has built a solid platform for future development. In addition to the traditional transport of crude oil and products the company is building the capability to be a key participant in the future growth of ice-bound routes. TEN is also exploring the high growth market of liquefied natural gas (LNG) shipments.

2 | ANNUAL REPORT AND ACCOUNTS 2003 |

The fleet profile was highlighted earlier and is detailed in the MANAGEMENT REVIEW AND ANALYSIS. Key factors include:

| 1) | a young, modern, and growing fleet; |

| 2) | a fleet comprised largely of vessels designed by and built for TEN and its customers identified needs; |

| 3) | a commitment to fleet renewal through sales or retirement of older single-hull vessels; |

| 4) | and embarkation to future growth markets via ice class tankers and LNG carriers. |

Tanker industry tonnage is expected to experience relatively modest growth in early future years as a result of limited shipyard capacity and accelerated scrappage in response to regulatory demands. The latter factor will also speed up the process of consolidation of the tanker industry.

TEN is well positioned to compete in this most demanding environment. TEN’s young and growing fleet is strongly complemented by the human strengths of its commercial and technical managers within the Tsakos group which provide over three decades of experience and strong industry ties. The importance of this heritage has never been more important. Fleet management is supported by a business model which has produced consistent and growing profits through three shipping cycles in the last ten years. The essence of this model is balance. The chartering policy has a bias for term employment but breathing room to participate in rising freight markets. Risk management also tempers financing cost volatility through interest rate hedging positions. The relative stability in profits has built the foundation for the on-going expansion of the fleet, secular earnings growth and higher shareholder value.

ANNUAL GENERAL MEETING

Our shareowners’ annual General Meeting (AGM) will be held in Athens on the 7th of June 2004 at 13:00. The key proposal will be the election of directors including two candidates identified by the nomination committee as valuable additions to your Board of Directors. We will also address directors’ fees as well as our long-term incentive compensation programs. A review of 2003 financial results and the appointment of auditors will be on the agenda. The AGM is where sound corporate governance begins. Your participation by proxy or preferably in person is essential.

As an incentive for your attendance, the AGM is scheduled to coincide with the bi-annual Posidonia Conference which is the premier shipping industry event. It is a great opportunity to meet and visit with leaders in the shipping community.

On behalf of the entire Board of Directors I wish to commend our management for a superb performance. The opportunities of 2003 were fully realized. At the same time the platform for increasing shareholder value is well positioned. The support of our shareowners is greatly appreciated.

Yours sincerely,

D. John Stavropoulos

Chairman of the Board

TEN LIMITED | 3 |

BOARD OF DIRECTORS AND OFFICERS

D. JOHN STAVROPOULOS

CHAIRMAN

Executive Vice President and Chief Credit Officer retired in 1990, having served 33 years with The First National Bank of Chicago and its parent, First Chicago Corporation. He chaired the bank’s Credit Strategy Committee, the Country Risk Management Council, and the Economic Council. Professional societies included the Robert Morris Associates (national director), Association of Reserve City Bankers, Financial Analysts Federation. Mr. Stavropoulos was appointed by President George Bush Senior to serve for life on the Presidential Credit Standards Advisory Committee, he was a director of CIPSCO from 1979 to 1992, an instructor of Economics and Finance at Northwestern University from 1962 to 1968 serves as a life member on the Alumni Advisory Board of the Kellogg School of Management and is a Chartered Financial Analyst. He was elected to the TEN Board and Chairmanship on June 1, 1994. Mr. Stavropoulos is member of the Audit Committee.

MICHAEL G. JOLLIFFE

DEPUTY CHAIRMAN

Deputy Chairman since July 2001 and Director of the Company since September 1993. Mr. Jolliffe is also Vice-Chairman of both Klonatex S.A. and Naoussa Spinning Mills SA., two companies quoted on the Athens Stock Exchange that together form the third largest integrated textiles company in Europe. Mr. Jolliffe is also Chairman of Wigham-Richardson Shipbrokers Ltd, one of the oldest established shipbroking companies in the City of London, and of Shipping Spares Repairs and Supplies Ltd, an Agency Company based in Piraeus, Greece. Additionally Mr. Jolliffe is the President of Eurotrans Hermes Hellas S.A., the Greek agent for various manufacturers of trams, buses and trains. Mr. Jolliffe is a member of the Audit Committee and Chairman of the Capital Markets Committee.

TORBEN JANHOLT

DIRECTOR

Torben Janholt has been a member of our board since October 2002. He is President and CEO of J. Lauritzen A/S, a major Danish shipowning and trading company, since 1998. Between 1995 and 1998 he was Director OTS of the UN World Food Programme, based in Rome. In 1992 he took a position as director and executive consultant with the Armada A/S shipping group. Prior to 1992, Mr. Janholt held various senior positions within the Lauritzen Group; including Managing Director of LauritzenNaval Madrid from 1990 - 1992, Senior Vice President J. Lauritzen USA Inc. New York from 1982 - 1989. Mr. Janholt is Vice Chairman of the Danish Shipowners Association.

WILLIAM O’ NEIL

DIRECTOR

William A. O’Neil is Secretary-General Emeritus of the International Maritime Organization, the United Nations agency concerned with maritime safety and the prevention of pollution from ships. Mr. O’Neil was elected Secretary-General of the IMO for a first term of office beginning in 1990, a second term beginning in 1994, a third term beginning in 1998 and a further two-year term beginning in 2002. He graduated in civil engineering from the University of Toronto in his native Canada in 1949 and served in various positions with the Federal Department of Transport and was particularly closely associated with the St. Lawrence Seaway Authority. He was Commissioner of the Canadian Coast Guard from 1975-80 and then became President and Chief Executive Officer of the St. Lawrence Seaway Authority, a position he held until joining IMO. However, his links with the Organization go back to 1972 when he represented Canada at the IMO Council. He became Chairman of the IMO Council in 1980 and was re-elected four times. In 1991 he became Chancellor of the World Maritime University, Malmö, Sweden and Chairman of the Governing Board of the International Maritime Law Institute in Malta.

PETER NICHOLSON

DIRECTOR

Peter Nicholson trained as a naval architect and spent the main part of his working life with Camper & Nicholsons Limited, the world-famous yacht builders. He became Managing Director of the firm and, later, Chairman. When Camper & Nicholsons merged with Crest Securities to form Crest Nicholson Plc. in 1972, he became an executive director of Crest Nicholson, a role he held until 1988, when he became a non executive in order to pursue a wider range of business interests. Since then he has been a non executive director of Lloyds TSB Group Plc (from 1990-2000), chairman of Carisbrooke Shipping Plc (from 1990-1999). He was a director of various companies in the Marsh Group of insurance brokers and remained a consultant to the company until recently. He has sat on the board of a wide variety of small companies and has been very active in the administration of the UK marine industry and is a trustee of the British Marine Federation. He is a Younger Brother of Trinity House, chairman of the Royal National Lifeboat Institution and a trustee of the International Lifeboat Federation. He joined the board of TEN as a founder director in 1993 and is Chairman of the Audit Committee.

FRANCIS T. NUSSPICKEL

DIRECTOR

Retired partner of Arthur Andersen LLP with 35 years of public accounting experience. Served as a member of the Firm’s Transportation Industry Group and worldwide Industry Head for the Ocean Shipping segment. His responsibilities included projects for mergers and acquisitions, fraud investigations, arbitrations and debt and equity offerings. President of the New York State Society of CPA’s in 1996 & 1997, member of the AICPA Council 1992 to 1998, and present Chairman of Professional Ethics Committee of the New York State Society of CPA’s.

ANGELOS PLAKOPITAS

DIRECTOR

Angelos Plakopitas is the Managing Director of Global Finance SA, since 1991, a financial services company based in Athens, with offices throughout the Balkans, and management of several venture capital funds. Between 1979 and 1990, Mr. Plakopitas was General Manager of Shelman Swiss-Hellenique Wood Products Manufacturers SA, a large industrial and trading company in Greece. From 1970 to 1979 he was Vice President with Citibank N.A. based in Athens and Piraeus, during which time he spent six years as Head of the Shipping Department. Mr. Plakopitas started his career with the Hellenic Industrial Development Bank in 1965.

ANTONIO TARAGONI

DIRECTOR

Has been involved in the shipping industry since 1955, initially with Ballestrero, Tuena and Canepa. He spent a year with Galbraith & Pembroke in London. He founded in 1961 and is President of Nolarma Noleggi & Armamento Srl, presently one of the largest Italian ship agents. This company has a long experience of ship management. Mr. Taragoni is also the Founder and President of Nolarma Tankers Srl, a large Italian tanker shipbroking firm. He has been a Council Member of Intertanko from 1973 to 1995 and a Council Member of Porto Petroli SpA of Genoa from 1975 to 1996. Mr. Taragoni has been a director of the Company since inception.

4 | ANNUAL REPORT AND ACCOUNTS 2003 |

BOARD OF DIRECTORS AND OFFICERS

NIKOLAS P. TSAKOS

PRESIDENT

President, CEO, and director of TEN since inception. Shareholder of Tsakos Energy Management. Mr. Tsakos has been involved in ship management since 1981 and has seafaring experience of 36 months. He is President of the Hellenic Marine Environment Protection Agency (HELMEPA). Mr. Tsakos is a member of the council of the Independent Tanker Owners Association (INTERTANKO), a Board member in the Union of Greek Shipowners (UGS), a council member in the Board of the Greek Shipping Co-operation Committee (GSCC), and a council member of the American Bureau of Shipping (ABS), of Bureau Veritas (BV), and of the Greek Committee of Det Norske Veritas (DNV). He graduated from Columbia University, New York in 1985 with a degree in Economics and Political Science and obtained a Masters’ Degree in Shipping, Trade and Finance from the City of London University Business School in 1987. Mr. Tsakos served as an officer in the Hellenic Navy in 1988.

GEORGE V. SAROGLOU

CHIEF OPERATING OFFICER

Chief Operating Officer since May 1996 and director of TEN since July 2001. Mr. Saroglou is a shareholder and director of Pansystems S.A. a leading Greek IT systems integrator where he also worked from 1987 until 1994. From 1995 to 1996 he was employed in the trading department of the Tsakos Group. He graduated from McGill University (Montreal Canada) in 1987 with a Bachelor Degree in Science (Mathematics).

PAUL DURHAM

FINANCE DIRECTOR

Paul Durham joined the Tsakos Group in 1999 and has served as our Finance Director and Chief Accounting Officer since June 2000. Mr. Durham is a U.K. Chartered Accountant. Prior to joining Tsakos Energy Navigation, from 1989 through 1998 Mr. Durham was employed with the Latsis Group, a shipping, refinery and banking enterprise, becoming Financial Director of shipping in 1995. From 1983 to 1989, Mr. Durham was employed by RJR Nabisco Corporation, serving as audit manager for Europe, Asia and Africa until 1986 and then as financial controller of one of their U.K. food divisions. Mr. Durham worked with Ernst & Young (London and Paris) from 1972 to 1979 and Deloitte & Touche (Chicago and Athens) from 1979 to 1983.

PAUL B. LABRINAKOS

CHIEF MARINE OFFICER

Paul B. Labrinakos was appointed Chief Marine Officer of TEN in June 2002 with the responsibility of overseeing newbuilding vessels and monitoring the fleet under management. He has served with the Tsakos Group since 1992, firstly as Technical Manager based in New York and later in Athens as Technical Director, responsible for the technical supervision of a fleet of 60 vessels. He created the New Projects Department of the Tsakos Group. Earlier in his career he has worked for other major shipping and industrial companies. He has supervised and has been involved in the design and building of over 50 newbuilding vessels. He has seagoing experience on both bulk carriers and tankers. He is a member of several maritime technical committees both in Europe and the USA. He graduated from the Athens National Technical University as a Naval Architect and Marine & Mechanical Engineer. He has completed technical studies also in Germany and in the United States.

TSAKOS ENERGY NAVIGATION BOARD COMMITTEES

Audit Committee Peter Nicholson - Chairman D. John Stavropoulos Michael G. Jolliffe Angelos Plakopitas | Corporate Governance, Nominating / Compensation Committee Peter Nicholson - Chairman D. John Stavropoulos Michael G. Jolliffe Antonio Taragoni Angelos Plakopitas | |

Chartering Committee Antonio Taragoni - Chairman D. John Stavropoulos Nikolas P. Tsakos | Risk Committee D. John Stavropoulos - Chairman Peter Nicholson Nikolas P. Tsakos Paul Durham | |

Capital Market Committee Michael G. Jolliffe - Chairman D. John Stavropoulos Nikolas P. Tsakos | ||

SECRETARY: EMMANUEL G. PANTELIDES

TEN LIMITED | 5 |

FINANCIAL HIGHLIGHTS

(Expressed in thousands of US Dollars – except share data)

(In accordance with United States Generally Accepted Accounting Principles)

| 2003 | 2002 | |||

NET REVENUE | 230,069 | 123,640 | ||

OPERATING INCOME | 70,525 | 14,430 | ||

NET INCOME | 59,052 | 3,894 | ||

EARNINGS PER SHARE (BASIC) | 3.45 | 0.25 | ||

EARNINGS PER SHARE (DILUTED) | 3.44 | 0.25 | ||

TOTAL ASSETS | 825,507 | 694,545 | ||

TOTAL LIABILITIES | 510,938 | 427,101 | ||

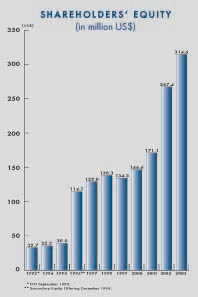

STOCKHOLDERS’ EQUITY | 314,569 | 267,444 | ||

OUTSTANDING SHARES AT YEAR END | 17,151,623 | 17,022,723 | ||

WEIGHTED AVERAGE OUTSTANDING SHARES (BASIC) | 17,134,347 | 15,717,065 | ||

WEIGHTED AVERAGE OUTSTANDING SHARES (DILUTED) | 17,187,859 | 15,854,904 | ||

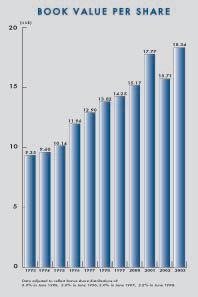

STOCKHOLDERS’ EQUITY PER SHARE OF COMMON STOCK | 18.34 | 15.71 | ||

SHARE PRICE (AS OF DECEMBER 31) (SEE NOTE 1 BELOW) | 18.45 | 15.46 | ||

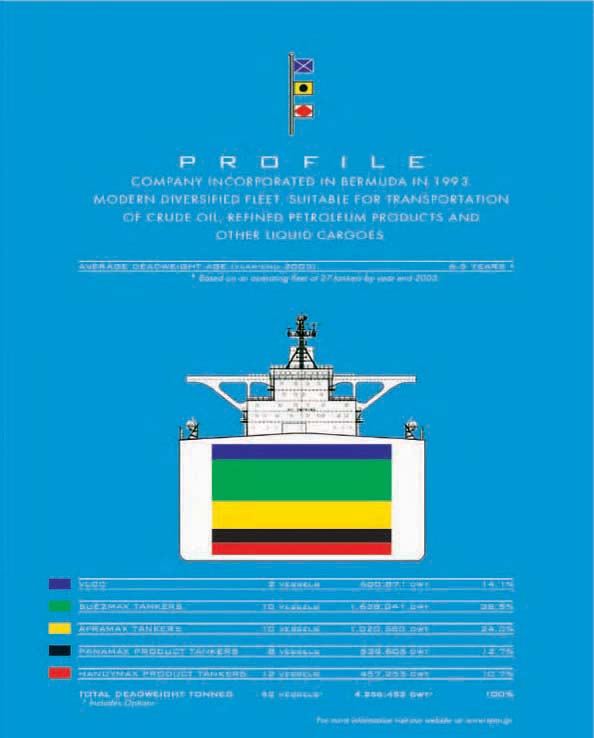

NUMBER OF VESSELS AT YEAR END (SEE NOTE 2 BELOW) | 27 | 22 | ||

TOTAL DWT | 2,681,552 | 2,225,993 | ||

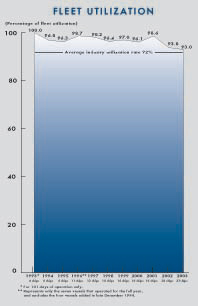

AVERAGE DEADWEIGHT AGE OF VESSELS | 6.5 | 6.8 | ||

| Note | 1: As quoted on the NYSE. |

| Note | 2: The number of vessels at the year end includes: |

| The M/T Olympia, a double hull Aframax tanker of 107,181 dwt. The vessel was sold through a sale and leaseback arrangement in October of 1999 and is time-chartered back from the buyers until October 2007. |

| The M/T Capella (2002 only), a double hull product carrier of 32,396 dwt chartered-in from December 2002 and redelivered to her Owners in September 2003. |

| The M/T Decathlon and M/T Pentathlon, two double hull Suezmax tankers of 164,274 and 164,235 dwt capacity respectively were sold through a sale and leaseback arrangement in October and November 2003 respectively and are time-chartered back by TEN for a minimum period of five years. The vessels have been re-named by the new owner Cape Baker and Cape Balboa. |

TEN LIMITED | 7 |

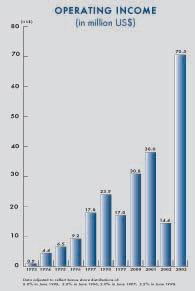

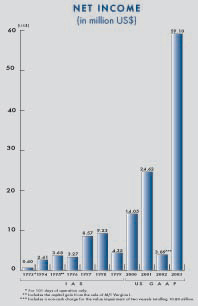

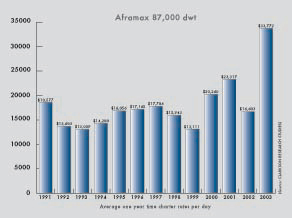

TEN GROWTH CHARTS

The 1993-1999 financial data is in accordance with the International Accounting Standards (IAS)

while 2000-2003 is in accordance with the US Generally Accepted Accounting Principles (US GAAP)

|  | |

|  | |

8 | ANNUAL REPORT AND ACCOUNTS 2003 |

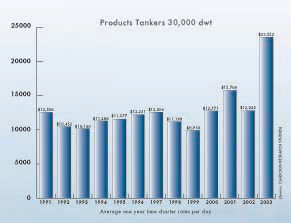

TEN GROWTH CHARTS

The 1993-1999 financial data is in accordance with the International Accounting Standards (IAS)

while 2000-2003 is in accordance with the US Generally Accepted Accounting Principles (US GAAP)

|  | |

|  | |

TEN LIMITED | 9 |

MANAGEMENT REVIEW AND ANALYSIS

The following discussion of our financial condition and results of operations should be read in conjunction with the financial statements and the notes to those statements included later in this Annual Report. This discussion as well as other sections of this Annual Report includes forward-looking statements that involve risks and uncertainties. We have based the forward-looking statements in this Annual Report on our current expectations and projections about future events, including:

| • | general economic and business conditions; |

| • | global and regional political conditions; |

| • | availability of and demand for crude oil and petroleum products; |

| • | demand for crude oil and petroleum product substitutes; |

| • | actions taken by OPEC and major oil producers and refiners; |

| • | competition in the marine transportation industry; |

| • | developments in international trade; |

| • | international trade sanctions; |

| • | changes in seaborne and other transportation industry; |

| • | our ability to find new charters for our vessels at attractive rates; |

| • | capital expenditures; |

| • | meeting our requirements with customers; |

| • | tanker supply and demand; |

| • | interest rate movements; and |

| • | foreign exchange fluctuations. |

The words “anticipate”, “believe”, “estimate”, “expect”, “forecast”, “intend”, “may”, “plan”, “project”, “predict”, “should” and “will” and similar expressions are intended to identify such forward-looking statements. Such statements reflect our current views and assumptions and all forward-looking statements are subject to various risks and uncertainties that could cause actual results to differ materially from expectations. The factors that could affect our future financial results are discussed more fully in our filings with the U.S. Securities and Exchange Commission (“SEC”). Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of their dates. We undertake no obligation to publicly update or revise any forward-looking statements.

General

The Company is a holding company formed under the laws of Bermuda in July 1993 under the name Maritime Investment Fund Limited. In June 1996 it changed its name to MIF Limited and in July 2001 changed its name to Tsakos Energy Navigation Limited (“TEN”). The Company is listed on the stock exchanges of Bermuda and Oslo. Since March 5, 2002, following a public offering of its common shares, it is also listed on the New York Stock Exchange under the symbol TNP.

TEN LIMITED | 11 |

TEN is the sole owner of a number of ship owning companies (those owned at December 31, 2003 are listed in Note 1 of the attached financial statements). Apart from certain subsidiaries with discontinued operations, twenty-four of the remaining companies each own one tanker. Three further companies each charter in a vessel for rechartering out to clients.

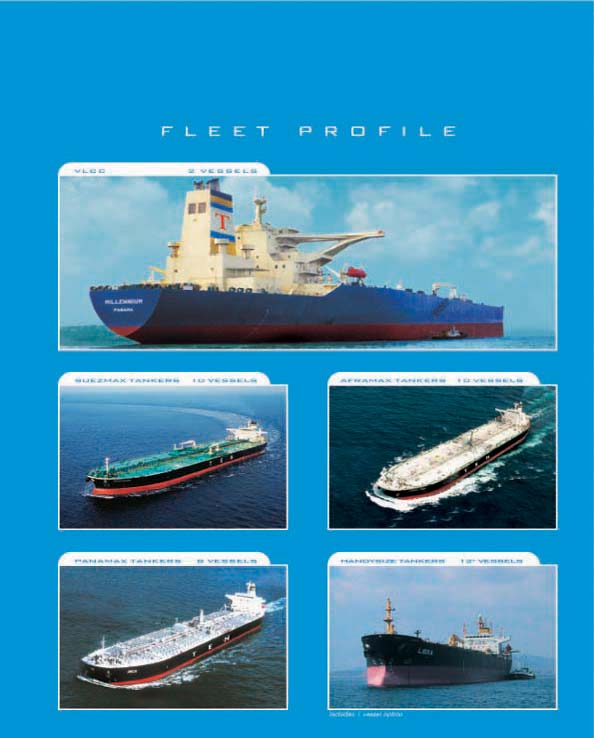

Following the acquisition of a VLCC tanker in January 2004, the Company currently operates a diversified fleet of twenty-eight tankers, consisting of two VLCCs, four Suezmaxes, ten Aframaxes, eight Panamaxes and four Handymax product carriers. A further thirteen tankers (six Suezmaxes and seven product carriers) are on order for delivery from 2004 to 2007.

The primary business of TEN therefore, is to own or charter, through its subsidiaries, carriers of crude oil and petroleum products, which it charters to leading oil companies or refineries or other major chartering enterprises under long, medium and short-term charters. The charter rates obtained are determined in a highly competitive world tanker charter market that has historically exhibited both cyclical and seasonal variations.

The commercial management of these vessels is undertaken through management agreements by a separate company, Tsakos Energy Management S.A. that, in turn, has management agreements with Tsakos Shipping and Trading S.A., a leading ship management company, for the technical management of the Company’s vessels.

Results from Operations

Following a severe depression in freight rates during most of 2002, the market began to see a sharp improvement in the last two months of the year which saw a significant rise in rates brought on by winter demand, low inventories, supply disruptions in Venezuela and Nigeria, prospects of conflict in the Middle East, and the sinking of the Prestige off the Spanish coast. These factors helped to keep the market exceptionally buoyant throughout 2003, modified only by the usual seasonal fluctuations and by new factors that had an impact on the industry, including the high demand for oil imports from China and India, the development of alternative sources for the supply of oil and the passage restrictions in the Bosphorus.

Some of the more significant developments for the Company during 2003 were:

The arrangement of new period charters with leading state-owned oil corporations. While the Company took advantage of the high rates being offered by the spot market, it also sought, in accordance with its overall chartering strategy, to ensure period employment of its vessels, often including in the terms variable rates with minimum floors and profit sharing for the Company to participate in the upside in buoyant markets.

The delivery of six newly constructed vessels:- four Panamax tankers (Maya, Inca, Aztec, Andes) and two Aframax tankers (Marathon, Parthenon). As a result, the dead-weight tonnage of the fleet increased by 20% from 2.23 million tons to 2.68 million tons and the average age (dwt basis) fell from 6.8 years to 6.5 years. Also, an agreement was reached to acquire a VLCC which was delivered in January 2004 and renamedLa Madrina.

The sale of two Suezmaxes acquired in 2002 (Decathlon, Pentathlon), to a German KG organization for $55 million each, thereby achieving a total capital gain of nearly $16 million. The vessels were chartered back for a period of five years over which time the capital gain is amortized. The vessels have been renamedCape Baker andCape Balboa, respectively.

12 | ANNUAL REPORT AND ACCOUNTS 2003 |

The proceeds of new loans with leading European banks relating to the six new vessels amounting to $160 million in total. Repayments amounted to $93 million, including the prepayment on the loans relating to the two sold Suezmaxes. Total debt at the year end amounted to $453 million.

The arrangement of new interest rate swaps, all meeting hedging criteria and providing further coverage of $111 million. Two of the older non-hedging swaps expired during the year. At December 31, 2003, the equivalent of approximately 58% of the outstanding loans were covered by interest rate swap arrangements.

The performance of major surveys on four product carriers (Pella, Dion, Libra, Crux), two Aframaxes (Maria Tsakos, Athens 2004), and three Panamaxes (Hesnes, Victory III, Liberty). In the case of theHesnes, an upgrading was also undertaken with the coating of the ballast tanks.

The ending by mutual accord of the joint venture company, LauriTen Ltd., in accordance with the terms of the original agreement. The original investment made by the Company was returned. Net income earned in 2003 was $0.6 million.

The payment to the Company’s shareholders of two dividends during the year, $0.20 cents per share in April in respect of the fiscal year 2002, and $0.50 cents in November, the first dividend with respect to fiscal year 2003.

The continued adoption and implementation of new corporate governance requirements as required by the Sarbanes-Oxley Act, the SEC, the New York Stock Exchange and the Oslo Stock Exchange. In particular, the Code of Ethics has been revised and is available for viewing on the Company’s website. A firm of public accountants has been appointed to review and document all the internal control procedures relating not only to the Company, but also to the technical managers.

The TEN fleet again achieved record net revenue of $230.1 million, up 86.1% from $123.6 million in 2002. Operating income increased from $14.4 million in 2002 to $70.5 million in 2003, a 388.7% increase. However, in 2002 there was an impairment of $10.8 million on the value of two single-hull vessels. No impairment was considered necessary in 2003.

Net income was $59.1 million in 2003, compared to $3.9 million in the prior year, a 1,416.5% increase. Diluted income per share increased from $0.25 in 2002, based on 15.85 million shares outstanding, to $3.44 in 2003, based on 17.19 million shares outstanding. These results reflect the dramatic improvement in market rates starting in late 2002 and continuing through most of 2003. U.S. interest rates fell in continued efforts to support the U.S. economy, providing reductions in financing costs. Vessel running expenses were held to competitive levels despite increasing costs due to the relative fall in the value of the U.S. Dollar to the Euro and higher insurance premiums.

The Company operated the following types of vessel during 2003:

Vessel Type | VLCC | Suezmax | Aframax | Panamax | Product carriers | ||||||||||||

Average number of vessels | 1 | 4 | 9.4 | 6.6 | 4.7 | ||||||||||||

Number of vessels at end of period | 1 | 4 | 10 | 8 | 4 | ||||||||||||

Dwt at end of period (in thousands) | Dwt | 301.2 | 657.2 | 1,020.7 | 539.6 | 162.9 | |||||||||||

Percentage of total fleet | 11.2 | % | 24.5 | % | 38.1 | % | 20.1 | % | 6.1 | % | |||||||

Average age at end of period | Years | 5.3 | 1.3 | 7.6 | 8.1 | 17.7 |

TEN LIMITED | 13 |

The contribution of the new vessels to the overall results for 2003 was:

| Newbuildings | Acquired | Joint Venture | Other net costs* | Combined | |||||||||||

Average number of vessels | 14.0 | 11.7 | — | — | 25.7 | ||||||||||

Utilization in period | 98 | % | 87 | % | — | — | 93 | % | |||||||

TCE per ship per day | $ | 26,454 | 17,324 | — | — | 22,636 | |||||||||

Operating expenses per ship per day | $ | 5,613 | 6,316 | — | — | 5,949 | |||||||||

Revenue from vessels, net ($ thousand) | $ | 153,856 | 76,213 | — | — | 230,069 | |||||||||

Net income/(loss) - ($ thousand) | $ | 51,853 | 9,398 | 602 | (2,801 | ) | 59,052 | ||||||||

| * | Other net costs include General and Administrative expenses, non-recurring charges, provisions against claims against dormant companies, other costs and interest income. |

(Note - Time Charter Equivalent (TCE): The shipping industry uses time charter equivalent, or TCE, to calculate revenues per vessel in dollars per day for vessels on voyage charters. The industry does this because it does not commonly express charter rates for vessels on voyage charters in dollars per day. TCE allows vessel operators to compare the revenues of vessels that are on voyage charters with those on time charters. For vessels on voyage charters, we calculate TCE by taking revenues earned on the voyage and deducting the voyage costs and dividing by the actual number of net earning days. For vessels on bareboat charters, for which we do not incur either voyage or operating costs, we calculate TCE by taking revenues earned on the charter and adding a representative amount for vessels operating expenses. TCE differs from average daily revenue earned in that TCE is based on revenues before commissions and does not take into account off-hire days.)

Critical Accounting Policies

Our consolidated financial statements are prepared in accordance with accounting principles generally accepted in the United States. The Company’s significant accounting policies are described in Note 2 of the attached financial statements. The application of such policies may require management to make estimates and assumptions. We believe that the following are the more critical accounting estimates used in the preparation of our consolidated financial statements that involve a higher degree of judgment and could have a significant impact on our future consolidated results of operations and financial position:

Revenues from vessels, net. Our vessels are employed under a variety of charter contracts, including time, bare-boat and voyage charters, contracts of affreightment and pool arrangements. Time and bare-boat charter revenues are recorded over the term of the charter as the service is provided. Under a voyage charter (including those under contract of affreightment) the revenues and associated voyage costs are recognized on a pro-rata basis over the duration of the voyage. If a voyage is in progress as at a reporting date, the operating results are estimated and recognized pro-rata on a per day basis. If a loss is forecast for a given voyage, such losses would be provided for in full at the time they can be estimated. Vessel operating expenses are accounted for on an accrual basis. Unearned revenue represents revenue applicable to periods after December 31, of each year. The operating revenues and voyage expenses of all vessels operating under a tanker pool are pooled by the pool manager and net operating revenues are allocated to the pool participants according to an agreed formula. We apply the same revenue and expense principles stated above in determining the pool net operating revenues.

Depreciation. We depreciate our vessels on a straight-line basis over their estimated useful lives, after considering their estimated residual values, based on the assumed value of the scrap steel available for recycling after demolition, calculated at $180 per lightweight ton. In assessing the useful lives of vessels, we have adopted the industry wide accepted practice of assuming a vessel has a useful life of 25 years, given that all classification

14 | ANNUAL REPORT AND ACCOUNTS 2003 |

society rules have been adhered to concerning survey certification and statutory regulations are followed. Useful life is then ultimately dependent on customer demand and if customers were to reject our vessels, either because of new regulations or internal specifications, then the useful life of the vessel will require revision. Actual scrap values are primarily dependent on the demand for steel bars for construction purposes and the availability of vessels for demolition and recycling. Current scrap prices have recently reached a historic high. However, given the volatility in scrap prices in recent years and the average life of the vessels, we have decided not to adjust residual values. If we were to do so in current circumstances, the residual value of vessels would increase and the depreciation charge fall accordingly.

Impairment. The carrying value of the Company’s vessels includes the original cost of the vessels plus capitalized expenses since purchase relating to improvements and upgrading of the vessel, less depreciation. Carrying value also includes the unamortized portion of deferred special survey and dry-docking costs. The carrying value of vessels usually differs from the fair market value applicable to any vessel, as market values fluctuate continuously depending on the market supply and demand conditions for vessels, as determined primarily by prevailing freight rates and newbuilding costs.

In order to identify indicators of impairment, test for recoverability of vessel carrying value and if necessary, measure the required impairment charges, management regularly compares each vessel’s carrying amount with the average of its fair market values as provided by two independent and reputable brokers. In the event that an indicator of impairment exists because a vessel’s carrying value is in excess of its fair market value, management estimates the undiscounted future cash flows to be generated by each of the Company’s vessel’s in order to assess the recoverability of the vessel’s carrying value. These estimates are based on historical industry freight rate averages for each category of vessel taking into account the age, specifications and likely trading pattern of each vessel and the likely condition and operating costs of each vessel. Such estimations are inevitably subjective and actual freight rates, as witnessed during 2002, 2003 and early 2004, may be volatile. As a consequence, estimations may differ considerably from actual results.

The estimations also take into account new regulations regarding the permissible trading of tankers depending on their structure and age. As a consequence of new European Union regulations effective from October 2003, the IMO adopted new regulations in December 2003 regarding early phase out of non-double hull tankers. At December 31, 2003, the Company owned and operated four single-hull tankers, two product carriers with single side and double bottom and two product carriers with double side and single bottom. None of the vessels were deemed Category I vessels, which require phase out by 2005. All eight vessels, providing they complete the newly imposed survey requirements, may continue trading to the end of their assumed economic lives of 25 years.

While management, therefore, is of the opinion that the assumptions it has used in assessing whether there are grounds for impairment are justifiable and reasonable, the possibility remains that conditions in future periods may vary significantly from current assumptions, which may result in a material impairment loss. In the event that the undiscounted future cash flows do not exceed a vessel’s carrying value, an impairment charge is required, and the vessel’s carrying value is written down to the fair market value as determined above. As vessel values are also volatile, the actual market value of a vessel may differ significantly from estimated values within a short period of time.

Allowance for doubtful accounts. Revenue is based on contracted charter parties and although our business is with customers whom we believe to be of the highest standard, there is always the possibility of dispute over terms and payment of freight. In particular, disagreements may arise as to the responsibility for lost time and demurrage revenue due. As such, we periodically assess the recoverability of amounts outstanding and we estimate a provision if there is a possibility of non-recoverability. Although we believe our provisions to be based on fair judgment at the time of their creation, it is possible that an amount under dispute is not ultimately recovered and the estimated provision for doubtful recoverability is inadequate.

TEN LIMITED | 15 |

Amortization of deferred charges. In accordance with Classification Society requirements, a special survey is performed on our vessels every five years. A further intermediate survey takes place in-between special surveys, depending on the age of the vessel. In most cases a dry-docking is necessary with repairs undertaken to bring the vessel up to the condition required for the vessel to be given its classification certificate. The costs include the yard charges for labor, materials and services, plus possible new equipment and parts where required, plus part of the participating crew costs incurred during the survey period. We capitalize these charges and amortize them over the period up to the vessel’s next special survey. These expenses are part of the normal costs we incur in connection with the operation of our fleet.

Financial Analysis

Year ended December 31, 2003 versus year ended December 31, 2002

Net Revenue

Net revenue from vessels (freight less brokerage commission) was $230.1 million during the year ended December 31, 2003 as compared to $123.6 million during the year ended December 31, 2002, an 86.1% increase partly resulting from an increase in the number of vessels from an average of 18.0 in 2002 to an average of 25.7 in 2003, and partly from the improvement in charter markets. The average time charter equivalent rate per vessel for the year 2003 was $22,636 per day compared to $16,676 for the previous year. In 2002, four newly built Suezmaxes were delivered, mostly in the latter part of the year, representing a whole new category of vessel for the Company to operate. A new Aframax,Opal Queen, was also acquired. These vessels operated throughout 2003. In addition, during 2003, four new Panamax tankers plus a further two Aframaxes were delivered. A Handymax product carrier was chartered-in towards the end of 2002 to provide cover in the absence of owned Handymaxes during their scheduled dry-dockings. This vessel was released in the autumn of 2003. The additional contribution in 2003 over 2002 to net revenue of these twelve vessels was $84.3 million. However, the fleet had 92.9% employment compared to 93.8% in the previous year, both years incurring significant dry-docking activity, which involved nine vessels in 2003 and six vessels in 2002.

Voyage Expenses

Voyage expenses include all our costs, other than operating expenses, that are related to a voyage, including port charges, canal dues and bunker or fuel costs. Voyage expenses were $61.3 million during the year ended December 31, 2003 compared to $32.8 million during the prior year, an 86.7% increase. Total operating days on spot charter and contract of affreightment, under which contracts the owner bears voyage expenses, rose from 2,582 days in 2002 to 4,272 in 2003, a 65% increase. The introduction of the larger Suezmaxes into the fleet with new trading routes (primarily West Africa to the U.S.) also contributed to increased voyage expenses. Bunker costs increased during 2003 as a consequence of higher oil prices.

Vessel Operating Expenses

Vessel operating expenses include crew costs, maintenance repairs and spares, stores, lubricants, insurance and sundry expenses such as tonnage tax, registration fees, and communication costs. Total operating costs were $49.9 million during the year ended December 31, 2003 as compared to $32.3 million during year ended December 31, 2002, an increase of 54.4%. This compares with an increase in operating days of approximately 2,462 or 47%, over the previous year, in those vessels bearing operating expenses.

Operating expenses per ship per day for the fleet increased from $5,498 for the year ended December 31, 2002 to $5,949 for the year ended December 31, 2003, an 8.4% increase. For the most part, this increase was due to the approximately 30% fall in value of the dollar against the Euro over the year. Approximately 25% of the Company’s operating expenses are in Euro, mainly in respect to Greek officers on the vessels. Increased insurance costs and extra repairs and spares also contributed to increased running costs.

16 | ANNUAL REPORT AND ACCOUNTS 2003 |

Depreciation

Depreciation was $32.9 million during the year ended December 31, 2003 compared to $24.4 million during the year ended December 31, 2002, an increase of 34.6%, due primarily to the addition in 2003 of, on an average basis, seven new vessels.

Amortization

We amortize the cost of dry-docking and special surveys over the period to the next special survey and this amortization is included as part of the normal costs we incur in connection with the operation of our vessels. During the year ended December 31, 2003, amortization of deferred dry-docking charges was $7.8 million as compared to $4.3 million during the year ended December 31, 2002, an increase of 81.6%, due to the major dry-docking and special survey work in the two year period since January 1, 2002.

Management Fees

Management fees are the fixed fees per vessel the Company pays to Tsakos Energy Management Ltd. under a management agreement between the companies. Since January 1, 2002 each vessel (excluding temporarily chartered-in vessels) bears a management fee of $15,000 per month, payable by the Company to Tsakos Energy Management Ltd., of which $10,000 per month is forwarded to Tsakos Shipping and Trading S.A. under a management contract for the technical management of the fleet. We believe this to be a very competitive fee to pay for such services. The remaining $5,000 per vessel is retained by Tsakos Energy Management Ltd. to cover the running costs associated with the administration of TEN. Management fees totalled $4.5 million during the year ended December 31, 2003, compared to $3.2 million for the year ended December 31, 2002, an increase of 38.0%, in line with the increase in available days provided by the newly acquired vessels to the fleet.

General and Administrative Expenses

General and administrative expenses consist primarily of professional fees, office supplies, advertising costs, directors’ fees, directors’ liability insurance, and reimbursement of our directors’ and officers’ travel-related expenses. General and administrative expenses were $2.4 million during the year ended December 31, 2003 compared to $1.3 million during the year 2002, an increase of 91.5% primarily due to additional expenditures relating to investor relations, advertising, travel, staff bonuses, SEC filing fees, legal and audit fees.

The sum of general and administrative expenses plus management fees payable to Tsakos Energy Management Ltd. represents the overheads of the Company. On a per vessel basis, daily overhead costs increased from $683 in 2002 to $734 in 2003, due to the factors mentioned above.

Operating Income

Income from vessel operations therefore was $70.5 million during the year ended December 31, 2003 versus $14.4 million during the year ended December 31, 2002, representing a 388.7% increase.

Interest and Finance Costs

Net interest and finance costs increased from $11.4 million during the year ended December 31, 2002 to $12.4 million during the year ended December 31, 2003, an 8.7% increase. Total average bank loans were approximately $473 million for 2003 compared to $271 million for 2002, an increase of 75%. Actual loan interest costs increased from $11.2 million to $13.2 million, only an 18% increase as the average interest rate for 2003 borne on the Company’s loans (taking into account actual interest payable on interest rate swaps) was approximately 3.5% compared to 4.5% for 2002. The actual interest payable on the swaps amounted to $4.5 million in 2003 compared to $2.7 million in 2002, the increase being due to the reduction in long term interest rates.

There was a positive movement of $3.5 million in the fair value (mark-to-market) of the non-hedging interest rate swaps in 2003, which is accounted for through the income statement and is included as part of interest costs,

TEN LIMITED | 17 |

compared to a negative movement of $3.8 million in 2002. This was primarily due to the reduction in the remaining life of the four swaps, including the expiry of two of them. The positive movement would have been greater if not for the unexpected reduction of long term interest rates mentioned above.

Capitalized interest in 2003 was only $0.8 million compared to $3.2 million in the previous year, due to the number of vessels completing construction during the past year and the reduction in average interest rates.

Interest income was $0.4 million during 2003 as compared to $0.7 million during the year ended December 31, 2002, due to lower time deposit interest rates in 2003 compared to 2002, despite much higher average bank deposits. Foreign exchange losses amounted to $0.4 million in 2003 compared to $0.1 million in 2002, due to the devaluation of the U.S. dollar compared to the Euro.

Joint Venture Income

The share of net income due to TEN Ltd. from the joint venture, LauriTen Ltd., for the year ended December 31, 2003 was $0.6 million after the write-off of $0.3 million expenses on cessation of the joint venture, compared to $0.2 million in 2002. The Company acquired a 50% participating interest in LauriTen Ltd. in 2002. The joint venture owned four separate companies each of which owned a small LPG carrier. The joint venture was accounted for using the equity method whereby the investment was carried at the Company’s original cost plus its share of undistributed earnings. A mutual decision was taken in August 2003 by the partners not to extend the joint venture agreement and consequently, in accordance with the original agreement, the joint venture expired on August 31, 2003.

Gain on the Sale of Vessels

The Company sold two Suezmaxes in a sale and leaseback transaction in the fourth quarter of 2003. The total gain of $15.8 million has been deferred and is being amortized over the five year minimum charter period. The initial part of this amortization amounted to $0.5 million in 2003.

Net Income

As a result of the foregoing, net income for the year ended December 31, 2003 was $59.1 million, or $3.45 per share, basic, versus $0.25 per share, basic, during the year ended December 31, 2002, an increase of 1,279%.

Year ended December 31, 2002 versus year ended December 31, 2001

Net Revenue

Net revenue from vessels, net, was $123.6 million during 2002 as compared to $118.7 million during the year ended December 31, 2001, a 4.2% increase primarily resulting from expansion of our fleet from an average of 16 vessels operating in 2001 to an average of 18 vessels operating in 2002. This increase in fleet size offset the weakness in charter markets for all types of tankers during 2002, the average time charter equivalent rate per vessel for 2002 being $16,676 per day compared to $19,002 for 2001. However, the fleet had 93.8% employment in 2002 compared to 98.6% in the previous year, so that total days employed were equivalent to a little over one extra vessel in the year. The primary reason for the reduced productivity was increased dry-docking activity, which involved six vessels during the course of the year. Certain of these vessels had been scheduled for drydock in 2003, but the timing was brought forward to take advantage of the soft freight market.

Voyage Expenses

Voyage expenses were $32.8 million during the year ended December 31, 2002 as compared to $21.4 million during the year ended December 31, 2001, representing a 53.2% increase primarily due to the operation of two extra vessels on spot charter during 2002 compared to 2001. Total operating days on spot charter and contract of affreightment, under which contracts the owner bears voyage expenses, rose from 1,731 days in 2001 to 2,582 in 2002, a 49% increase. Bunker costs, an important component of voyage expenses also increased significantly during 2002.

18 | ANNUAL REPORT AND ACCOUNTS 2003 |

Vessel Operating Expenses

Vessel operating expenses were $32.3 million during the year ended December 31, 2002 as compared to $28.7 million during the year ended December 31, 2001. The increase of 12.7% was due to the addition, on average, of two extra vessels during the year compared to the previous year. This represented an increase in operating days of approximately 14% in vessels bearing operating expenses. Vessel operating expenses per ship per day for the fleet decreased from $5,622 for the year ended December 31, 2001 to $5,498 for the year ended December 31, 2002, despite increased insurance costs, additional required vessel repairs and a rising Euro. The decrease in average daily vessel operating expenses is also partly attributable to reduced running costs during dry-docking activities and the cost efficiencies achieved through the addition of new vessels to the fleet.

Depreciation

Depreciation was $24.4 million during the year ended December 31, 2002 compared to $21.3 million during the year ended December 31, 2001, an increase of 15.0% due to the addition on average for the year of two new vessels to the fleet.

Impairment

The carrying values of two 21-year old single hull vessels, Panos G and Liberty, were written-down to their fair market values, resulting in an impairment loss of $10.8 million. Values of single hull tankers had fallen as a result of the incident involving the Prestige, an aged single hull oil tanker which sank in rough seas and resulted in proposed restrictions on the operation of such vessels. In addition, it was estimated on the basis of industry data that the cash flow expected to be generated by the future use of these vessels would also be less than the carrying values. In such circumstances, accounting principles require the write-down of the difference between the carrying value of the asset and the fair market value.

Amortization

During the year ended December 31, 2002, amortization of deferred dry-docking charges amounted to $4.3 million as compared to $5.1 million during the year ended December 31, 2001, a decrease of 15.7%. The total charges for the previous year included $1.3 million relating to an adjustment of the amortization period for the remaining unamortized deferred dry-docking costs on two vessels undergoing special surveys within 2001 and 2002 to ensure full amortization before the new special surveys. Excluding this adjustment from 2001, the resulting increase in amortization of dry-docking charges of approximately $0.5 million is primarily due to amortization of significant new expenditure relating to dry dock work on four vessels during 2001 and 2002.

Management Fees

Management fees were $3.2 million during the year ended December 31, 2002, a $0.1 million increase from the year ended December 31, 2001. The monthly fee payable to Tsakos Energy Management decreased from $16,500 per month per vessel to $15,000 commencing January 1, 2002. The savings offset the additional management fees resulting from the addition of two vessels on average to the fleet.

Stock Option Compensation Expenses

Stock option compensation expenses represent changes in the fair value of the stock options granted. As all such expenses were fully accounted by December 31, 2001, there were no further charges during the year ended December 31, 2002. The expense during the year ended December 31, 2001 was $0.3 million.

General and Administrative Expenses

General and administrative expenses were $1.3 million during the year ended December 31, 2002 as compared to $0.8 million during the year ended December 31, 2001. This represents a 59.3% increase, which is primarily attributable to increased expenditures with respect to investor relations, advertising, directors’ and officers’ insurance and legal and audit fees relating to our completion in early 2002 of a public offering of our common shares in the United States and our on-going reporting obligations as a publicly traded company.

TEN LIMITED | 19 |

Operating Income

As a result of the foregoing, income from vessel operations was $14.4 million during the year ended December 31, 2002 versus $38.0 million during the year ended December 31, 2001, representing a 62.0% decrease. A significant factor in the decrease in operating income for 2002 versus 2001 was the $10.8 million impairment loss described above.

Interest and Finance Costs

Interest and finance costs decreased from $14.5 million during the year ended December 31, 2001 to $11.4 million during the year ended December 31, 2002, representing a 21.7% decrease. Although total bank loans increased from $244.5 million as at January 1, 2002 to $386.0 million by the year end, average interest rates fell from approximately 5.6% in 2001 to 3.5% in 2002. The decrease in overall interest expense was due also to the increase in capitalization of interest relating to the new building program from $1.6 million in 2001 to $3.2 million during 2002. The reduction in interest and finance costs was offset by a negative $3.8 million fair value adjustment at December 31, 2002 on four open interest rate swap arrangements which we entered into in July 2001. Because these swaps were entered into for non-hedging purposes, the fair value (mark-to-market) of these swap agreements and changes in their fair value are recognized in our financial statements. As at December 31, 2001 these same swaps incurred a $3.4 million negative fair value adjustment, but this had been offset by the termination in June 2001 of two other interest rate swaps entered into in March 2001, which gave rise to a $1 million gain.

Interest income was $0.7 million during the year ended December 31, 2002 as compared to $1.2 million during the year ended December 31, 2001, representing a decrease of 39.4%. This decrease resulted primarily from lower time deposit interest rates in 2002 compared to 2001, notwithstanding that the Company had higher cash balances on deposit during 2002 compared to 2001.

Joint Venture Income

The Company entered into a joint venture, named LauriTen Ltd., with Lauritzen A/S of Denmark in October 2002. The joint venture owns four small LPG carriers which are on bare-boat charter to Lauritzen A/S for one year. The joint venture is accounted for as an investment on an equity basis. The net income of the joint venture is derived after deducting depreciation, bank interest and administrative expenses from the bare-boat charter income and is distributed in equal amounts to the Company and Lauritzen A/S. The share of net income due to TEN Ltd. for the year ended December 31, 2002 is $0.2 million and is included in other income.

Net Income

As a result of the foregoing, net income for the year ended December 31, 2002 was $3.9 million, or $0.25 per share, basic, versus $24.6 million or $2.56 per share, basic, during the year ended December 31, 2001, a decrease of 84.2%.

Liquidity and Capital Resources

Our liquidity requirements relate to servicing our debt, funding the equity portion of investments in vessels, funding working capital and controlling fluctuations in cash flow. Net cash flow generated by continuing operations is our main source of liquidity. Apart from the possibility of securing further equity, additional sources of cash include proceeds from asset sales and borrowings, although all borrowing arrangements to date have specifically related to the acquisition of vessels. There is no off balance sheet financing.

We believe that, unless there is a major and sustained downturn in market conditions, our financial resources are sufficient to meet our liquidity needs through January 1, 2005, taking into account both our existing capital commitments and the minimum debt service requirements as defined by our bank loan covenants.

20 | ANNUAL REPORT AND ACCOUNTS 2003 |

Working capital (non-restricted net current assets) amounted to approximately $33 million at December 31, 2003 compared to approximately $3 million as at December 31, 2002, primarily a reflection of the increase in unrestricted cash holdings from $39.7 million to $86.8 million, most of the increase being due to the sale proceeds arising from the sale of two Suezmaxes in the last quarter. Current assets increased from $75.7 million at December 31, 2002 to $117.0 million at December 31, 2003 due to the increased cash balances and to increased trade and other receivables. Current liabilities increased from $66.2 million to $83.5 million at December 31, 2003 due mainly to increases in the current portion of the long term debt and deferred income and trade accounts payable offset against decreases in accrued liabilities and the fair market valuation of the existing interest rate financial instruments.

Net cash provided by operating activities was $84.2 million in the year ended December 31, 2003 compared to $32.7 million in the previous year, a 157.1% increase. The increase is due mainly to the record income generated by the increase in fleet size and the substantial improvement in the freight market as described in the preceding sections.

Expenditure on dry-dockings is deducted from cash generated by operating activities. Total expenditure during 2003 on dry-dockings amounted to $15.1 million compared to $8.3 million in 2002. Programmed expenditure on dry-dockings has been higher than previous years due to the timing of special and intermediate surveys on the older vessels and the requirement for the newer vessels, delivered since 1997, to undertake their first special survey. A part of the scheduled work was brought forward into 2002, when the freight market was considerably softer. In 2003, special survey work was performed on the Handymax product carriersPella,Libra,Dion andCrux. During much of the period that these vessels were undergoing work, they were substituted in part by the chartered-in Handymax product carrier,Capella which was released by TEN in September 2003. The dry-docking of all the Company’s product carriers has resulted in reduced earnings for this category of vessel during the year. Work was also performed on the PanamaxHesnes relating to its intermediate survey and the coating of its ballast tanks, as performed on its sister vesselBregen in 2002. The vessel returned to pool service in September with the ability to generate more income in its upgraded state. The PanamaxLiberty also completed an extensive intermediate dry-docking and the second of the new Aframaxes, theAthens 2004, delivered in 1998, underwent its first special survey in the second quarter. For the last quarter of the year, the third of the new Aframaxes,Maria Tsakos, undertook its first special survey and the PanamaxVictory III had an intermediate survey.

In contrast, there are four major dry-dockings scheduled for 2004, relating to theOlympia (paid for by the owner),Tamyra,Bregen andLiberty. There is a strong possibility that theLiberty, the oldest vessel in the fleet will be disposed of before its scheduled dry-docking in August.

Net cash used in investing activities was $91.8 million for the year 2003, compared to $257.0 million for the year 2002. Almost all the use of cash in 2003, amounting to $218.9 million, relates to the ongoing new building program. During the year, an amount of $185.8 million was paid for the delivery from Imabari yards in Japan of the PanamaxesMaya (January 24),Inca (March 20),Aztec (May 29),Andes (September 12) and the AframaxesMarathon (January 22) andParthenon (July 23). A further $26.9 million was expended as advances (contract instalments, construction supervisory fees and interest capitalized) on the four Suezmaxes (delivery October 2005, December 2005, February 2006 and May 2006) and the three Handysize product carriers ordered from Hyundai (delivery June 2004, December 2004, June 2005). The cost of upgrading theHesnes was a further $1.1 million. $5.2 million was paid as a deposit for the purchase of the VLCC, delivered in January 2004 at a total purchase price of $51.5 million and renamedLa Madrina.

TEN LIMITED | 21 |

During the period between January 1, 2004 and March 31, 2004, the Company entered into contracts to construct a further six vessels, four ice-class product carriers and two ice-class suezmaxes, bringing the total number of vessels on order to thirteen (see below section on fleet development). The anticipated payment schedule on these vessels, which is subject to change if there are delays or advanced work, is as follows (amounts in $ million):

| Prior to 2004 | 2004 | 2005 | 2006 | 2007 | Total | |||||||

Quarter 1 | 36.3 | 12.2 | 76.1 | 58.4 | ||||||||

Quarter 2 | 23.7 | 25.5 | 35.5 | 55.5 | ||||||||

Quarter 3 | 20.1 | 4.8 | 11.7 | 0 | ||||||||

Quarter 4 | 20.6 | 70.3 | 27.0 | 0 | ||||||||

Total Year | 27.0 | 100.7 | 112.8 | 150.3 | 113.9 | 477.7 |

Net sale proceeds from the sale of the two Suezmaxes,Decathlon andPentathlon, amounted to $108.9 million. The Company received an amount of $11.2 million from Lauritzen Kosan S.A., our Danish partners in the joint venture LauriTen Ltd. for the return of the initial investment in the joint venture LauriTen Ltd. Also, $7.0 million restricted cash in collateral was released.

Net cash from financing activities was $54.8 million in 2003 compared to $230.6 million in 2002. Proceeds from new bank loans in 2003 amounted to $159.9 million with repayments of $93.2 million compared to proceeds of $185.4 million less repayments of $43.9 million in the previous year. 2002 also saw the public offering of our common shares, together with the gross proceeds from the concurrent private placement of one million common shares sold to Sea Consolidation S.A. providing total net proceeds of $100.4 million.

The Company has effectively a continuous program to repurchase a limited number of shares with the primary aim of enhancing share liquidity. The transactions were open market based through the New York Stock Exchange with a maximum price set by the Board of Directors. During 2003, the Company purchased 140,100 shares in the open market in a buy-back program at a cost of approximately $1.8 million. The shares were cancelled in accordance with Bermudan regulations. During the year, the staff of the Tsakos Group exercised 269,000 options at $10 each which provided $2.7 million.

A cash dividend of 20 cents was paid in April 2003 representing the final dividend for the fiscal year 2002 and a 50 cent dividend was paid in November 2003 as the first dividend for the fiscal year 2003. In total, the two dividends amounted to $12.0 million. A further dividend of $ 0.50 cents per share for the fiscal year 2003 has been declared, to be paid on April 29, 2004. The dividend policy of the Company is to pay between 25% and 50% of the net income in any given year, payable in two instalments, the first prior to the end of the year based on expected earnings and cash requirements, and the final portion in the early part of the following year based on final earnings and cash requirements. The payment and the amount is subject to the discretion of our board of directors and depends, among other things, on available cash balances, anticipated cash needs, our results of operations, our financial condition, and any loan agreement restrictions binding us or our subsidiaries, as well as other relevant factors.

We operate in a capital-intensive industry requiring extensive investment in revenue-producing assets. We raise the funds for investments in newbuildings mainly from borrowings and partly out of internally generated funds. Newbuilding contracts generally provide for multiple staged payments of 5% to 10%, with the balance of the vessel purchase price paid upon delivery. For the equity portion of an investment in a newbuilding or a secondhand vessel the Company usually pays from its own cash approximately 30% of the contract price. Repayment of the debt incurred to purchase the vessel is made from vessel operating cash flow, typically over eight to twelve years, compared to the vessel’s asset life of approximately 25 years.

As of December 31, 2003, we were committed to seven newbuilding orders totaling approximately $270 million, of which $27 million had been paid by December 31, 2003 and $49 million had been paid by March 31, 2004. Between January 1, 2004 and March 31, 2004, the Company ordered six further vessels. Of the thirteen vessels that were on order at March 31, 2004, with a total contract value of $505 million, there was still $441 million remaining to be paid.

22 | ANNUAL REPORT AND ACCOUNTS 2003 |

As is customary in our industry, we anticipate financing the majority of our commitments on the new buildings with bank debt. We do not usually finalize financing arrangements for the new buildings until shortly before we take delivery of the vessels. We have not yet completed arrangements for the financing of the construction of the thirteen vessels, although discussions with several banks in each case are in progress. We have established relationships with various major international banks that have previously financed our vessel acquisitions and new buildings. We intend to raise at least 70% of the vessel purchase price with bank debt, although our ability to do so will depend upon the commercial loan market for shipping companies and our perceived prospects at the time.

With regards to the new debt financing, $27.4 million for the part financing of theMarathon was drawn on a $129 million facility arranged with Deutsche Schiffsbank in 2002. (The remaining $101.6 million previously received related to three Suezmaxes delivered in 2002). $55 million was received from HSH Nordbank (previously LandesbankKiel) for the PanamaxesMaya andInca and in the second quarter $26 million was received from the Danish Ship Finance Bank for the PanamaxAztec. A loan of $25.6 million has been received from Credit Suisse for the part financing of the AframaxParthenon delivered in July and a loan of $26 million has been received with the Royal Bank of Scotland for the PanamaxAndes delivered in September. No further financing occurred in the fourth quarter. $93.3 million was repaid during the year including a prepayment of $59.4 million relating to the loan for theDecathlon andPentathlon.

In December 2003, the Company entered into a contract to acquire the double hull VLCCMaersk Estelle (299,700 dwt), built in January 1994, for an amount of $51.5 million. An amount of $5.2 million was paid as an advance. The balance of $46.3 million was paid on delivery in January 2004 and the vessel was renamedLa Madrina.

SUMMARY OF LOAN MOVEMENTS THROUGHOUT 2003 (in $ million):

Loan | Vessel | Balance at January 1, 2003 | New Loans | Repaid | Balance at December 31, 2003 | |||||

Syndicated credit facility | 15 vessels | 174.4 | 0 | 20.4 | 154.0 | |||||

Syndicated credit facility | Millennium | 48.1 | 0 | 3.2 | 44.9 | |||||

12-year term loan | Opal Queen | 29.6 | 0 | 1.7 | 27.9 | |||||

10-year term loan | Silia T. | 32.2 | 0 | 1.9 | 30.4 | |||||

Syndicated credit facility | Triathlon, Marathon | 101.6 | 27.4 | 63.3 | 65.7 | |||||

10-year term loan | Maya | 0 | 27.5 | 1.0 | 26.5 | |||||

10-year term loan | Inca | 0 | 27.5 | 1.0 | 26.5 | |||||

10-year term loan | Aztec | 0 | 26.0 | 0.8 | 25.2 | |||||

10-year term loan | Parthenon | 0 | 25.5 | 0 | 25.6 | |||||

10-year term loan | Andes | 0 | 26.0 | 0 | 26.0 | |||||

Total | 386.0 | 159.9 | 93.3 | 452.6 |

There were no undrawn amounts relating to the above facilities as at December 31, 2003.

As a result of such financing activities, long-term debt increased in 2003 by a net amount of $66.6 million, compared to a net increase of $141.5 million in 2002. The average debt to capital ratio was approximately 59% at December 31, 2003. Interest rate swap instruments currently cover approximately 62% of the outstanding debt, and further coverage is being arranged with major banks. The two remaining swaps which do not meet hedging criteria and cover a notional $100 million will expire in July 2004.

TEN LIMITED | 23 |

In January 2004, the Company obtained a term loan facility for $40.0 million from Citibank to partially finance the acquisition of the VLCCLa Madrinaon delivery. The loan will be repaid in sixteen variable instalments with a balloon payment of $13.5 million to be paid together with the last instalment. The interest rate is based on LIBOR plus a spread. The loan is secured with a first preferred mortgage over the vessel, an assignment of earnings and insurance of the vessel and a corporate guarantee of the ship-owning company.

As at March 31, 2004, after including the new $40.0 million debt and deducting repayments made in the first quarter of 2004 of $8.1 million, total net debt outstanding was $484.5 million. Annual principal payments scheduled from April 1, 2004, are as follow (these will change depending on possible prepayments and new loan arrangements):

Year | Principal Payment (in millions) | ||

2004 | $ | 35.7 | |

2005 | 47.7 | ||

2006 | 166.4 | ||

2007 | 19.7 | ||

2008 | 19.6 | ||

2009 and thereafter | 195.4 | ||

Total | $ | 484.5 | |

During 2002 the Company took delivery of the newly constructed SuezmaxesDecathlonandPentathlon.In October and November 2003, the Company sold and time-chartered the vessels (re-namedCape BakerandCape Balboarespectively) back from the buyer for a minimum period of five years, with options to extend the charters for a further three years. In addition, at the end of the first five years, or until the end of the end of the seventh year if the charter is extended, the Company has the option to buy the vessels at specified amounts. The charter back agreements are accounted for as operating leases and the gains on the sale of $8.3 million and $7.5 million respectively were deferred and are amortized over the five year lease period. During 2003, lease payments relating to the time charters of theCape BakerandCape Balboawere $1.8 million and $1.0 million respectively.

Contractual Obligations as of December 31, 2003 were:

| 2004 | 2005 | 2006 | 2007 | 2008 and thereafter | Total | |||||||

Long-Term Debt Obligations | 41.6 | 43.5 | 162.6 | 16.3 | 188.6 | 452.6 | ||||||

Operating Lease Obligations | 24.3 | 24.4 | 24.5 | 23.0 | 13.9 | 110.1 | ||||||

Purchase Obligations (newbuildings) | 65.7 | 109.8 | 67.4 | — | — | 242.9 | ||||||

Purchase Obligations (vessel acquisition) | 46.4 | — | — | — | — | 46.4 | ||||||

Total | 178.0 | 177.7 | 254.5 | 39.3 | 202.5 | 852.0 |

24 | ANNUAL REPORT AND ACCOUNTS 2003 |

Fleet Development

The current fleet, as described in more detail in the table below, consists of two VLCCs, four Suezmaxes, tenAframaxes, eight Panamaxes and four Handymaxes. All vessels are owned by subsidiaries of TEN with the exception of the AframaxOlympia, acquired in March 1999 and sold in October 1999 and time chartered back from the owners for an initial period of approximately eight years and the two Suezmaxes,Decathlonand Pentathlon(renamedCape BakerandCape Balboa), acquired in 2002 and sold in October and November2003 respectively and time chartered back from the owners for five years.

Name | Built-DWT-Design | Date Acquired | ||

Millennium | 1998–301,171 dwt – VLCC Double Hull | September 22, 1998 | ||

La Madrina | 1994–299,700 dwt – VLCC Double Hull | January 28, 2004 | ||

Silia T. | 2002-164,286 dwt-Suezmax Crude Carrier Double Hull | June 29, 2002 | ||

Cape Baker | 2002-164,274 dwt-Suezmax Crude Carrier Double Hull | August 19, 2002 | ||

Cape Balboa | 2002-164,236 dwt-Suezmax Crude Carrier Double Hull | October 10, 2002 | ||

Triathlon | 2002-164,445 dwt-Suezmax Crude Carrier Double Hull | December 2, 2002 | ||

Parthenon | 2003-107,018 dwt-Aframax Crude Carrier Double Hull | July 23, 2003 | ||

Marathon | 2003-107,181 dwt-Aframax Crude Carrier Double Hull | January 22, 2003 | ||

Opal Queen | 2001-107,181 dwt-Aframax Crude Carrier Double Hull | March 15, 2002 | ||

Olympia | 1999-107,181 dwt-Aframax Crude Carrier Double Hull | March 25, 1999 | ||