FORM 10-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

| | |

(Mark One) | | |

x | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2008 |

OR |

¨ | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO |

Commission file number 001-32871

COMCAST CORPORATION

(Exact name of registrant as specified in its charter)

| | |

PENNSYLVANIA (State or other jurisdiction of incorporation or organization) | | 27-0000798 (I.R.S. Employer Identification No.) |

One Comcast Center, Philadelphia, PA (Address of principal executive offices) | | 19103-2838 (Zip Code) |

Registrant’s telephone number, including area code: (215) 286-1700 |

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

| | |

| Title of Each Class | | Name of Each Exchange on which Registered |

Class A Common Stock, $0.01 par value Class A Special Common Stock, $0.01 par value 2.0% Exchangeable Subordinated Debentures due 2029 6.625% Notes due 2056 7.00% Notes due 2055 7.00% Notes due 2055, Series B 8.375% Guaranteed Notes due 2013 9.455% Guaranteed Notes due 2022 | | Nasdaq Global Select Market Nasdaq Global Select Market New York Stock Exchange New York Stock Exchange New York Stock Exchange New York Stock Exchange New York Stock Exchange New York Stock Exchange |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

NONE

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendments to this Form 10-K. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨ Small reporting company ¨

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

As of June 30, 2008, the aggregate market value of the Class A common stock and Class A Special common stock held by non-affiliates of the Registrant was $39.033 billion and $15.656 billion, respectively.

As of December 31, 2008, there were 2,060,982,734 shares of Class A common stock, 810,211,190 shares of Class A Special common stock and 9,444,375 shares of Class B common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III—The Registrant’s definitive Proxy Statement for its annual meeting of shareholders presently scheduled to be held in May 2009.

Comcast Corporation

2008 Annual Report on Form 10-K

Table of Contents

| | | | |

PART I | | |

Item 1 | | Business | | 1 |

Item 1A | | Risk Factors | | 13 |

Item 1B | | Unresolved Staff Comments | | 16 |

Item 2 | | Properties | | 16 |

Item 3 | | Legal Proceedings | | 17 |

Item 4 | | Submission of Matters to a Vote of Security Holders | | 18 |

| |

PART II | | |

Item 5 | | Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | | 19 |

Item 6 | | Selected Financial Data | | 21 |

Item 7 | | Management’s Discussion and Analysis of Financial Condition and Results of Operations | | 22 |

Item 7A | | Quantitative and Qualitative Disclosures About Market Risk | | 36 |

Item 8 | | Financial Statements and Supplementary Data | | 38 |

Item 9 | | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | | 79 |

Item 9A | | Controls and Procedures | | 79 |

Item 9B | | Other Information | | 79 |

| |

PART III | | |

Item 10 | | Directors and Executive Officers of the Registrant | | 80 |

Item 11 | | Executive Compensation | | 81 |

Item 12 | | Security Ownership of Certain Beneficial Owners and Management | | 81 |

Item 13 | | Certain Relationships and Related Transactions | | 81 |

Item 14 | | Principal Accountant Fees and Services | | 81 |

| |

PART IV | | |

Item 15 | | Exhibits and Financial Statement Schedules | | 82 |

Signatures | | 85 |

This Annual Report on Form 10-K is for the year ended December 31, 2008. This Annual Report on Form 10-K modifies and supersedes documents filed before it. The Securities and Exchange Commission (“SEC”) allows us to “incorporate by reference” information that we file with them, which means that we can disclose important information to you by referring you directly to those documents. Information incorporated by reference is considered to be part of this Annual Report on Form 10-K. In addition, information that we file with the SEC in the future will automatically update and supersede information contained in this Annual Report on Form 10-K. Throughout this Annual Report on Form 10-K, we refer to Comcast Corporation as “Comcast;” Comcast and its consolidated subsidiaries as “we,” “us” and “our;” and Comcast Holdings Corporation as “Comcast Holdings.”

Our registered trademarks include Comcast and the Comcast logo. Our trademarks include Fancast and FEARnet. This Annual Report on Form 10-K also contains other trademarks, service marks and trade names owned by us as well as those owned by others.

Part I

Item 1: Business

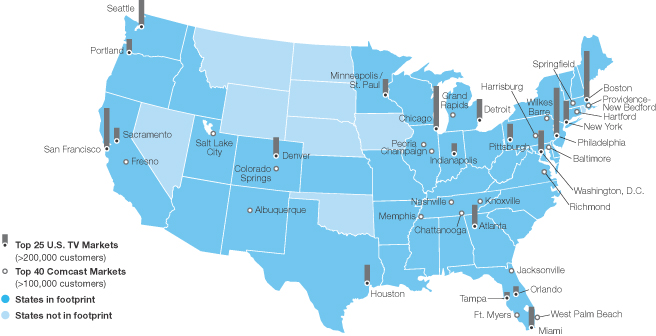

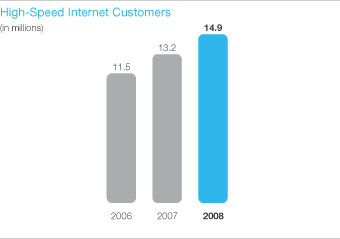

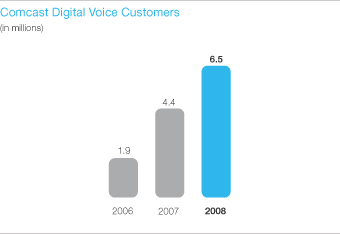

We are the nation’s leading provider of cable services, offering a variety of entertainment, information and communications services to residential and commercial customers. As of December 31, 2008, our cable systems served approximately 24.2 million video customers, 14.9 million high-speed Internet customers and 6.5 million phone customers and passed over 50.6 million homes in 39 states and the District of Columbia. We report the results of these operations as our Cable segment, which generates approximately 95% of our consolidated revenue. Our Cable segment also includes the operations of our regional sports networks. Our other reportable segment, Programming, consists primarily of our national programming networks, including E!, Golf Channel, VERSUS, G4 and Style. We were incorporated under the laws of Pennsylvania in December 2001. Through our predecessors, we have developed, managed and operated cable systems since 1963.

Our other business interests include Comcast Interactive Media and Comcast Spectacor. Comcast Interactive Media develops and operates Comcast’s Internet businesses focused on entertainment, information and communication, including Comcast.net, Fancast, thePlatform, Fandango, Plaxo and DailyCandy. Comcast Spectacor owns two professional sports teams and two large, multipurpose arenas, and manages other facilities for sporting events, concerts and other events. Comcast Interactive Media, Comcast Spectacor and all other consolidated businesses not included in our Cable or Programming segment are included in “Corporate and Other” activities.

For financial and other information about our reportable segments, refer toItem 8, Note 16 to our consolidated financial statements included in this Annual Report on Form 10-K.

Available Information and Web Sites

Our phone number is (215) 286-1700, and our principal executive offices are located at One Comcast Center, Philadelphia, PA 19103-2838. The public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to such reports filed with or furnished to the SEC under Sections 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), are available free of charge on the SEC’s Web site at www.sec.gov and on our Web site at www.comcast.com as soon as reasonably practicable after such reports are electronically filed with the SEC. The information posted on our Web site is not incorporated into our SEC filings.

General Developments of Our Businesses

The following are the more significant developments in our businesses in 2008:

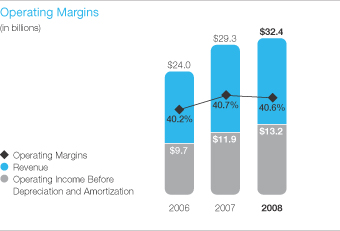

| • | | growth in consolidated revenue of 10.9% to approximately $34.3 billion and an increase in consolidated operating income of 20.7% to approximately $6.7 billion |

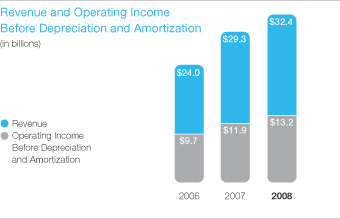

| • | | growth in Cable segment revenue of 10.7% to approximately $32.4 billion and an increase in operating income before depreciation and amortization of 10.5% to approximately $13.2 billion |

| • | | the addition of approximately 1.5 million digital video customers, approximately 1.3 million high-speed Internet customers, approximately 2.0 million digital phone customers and a decrease of approximately 575,000 video customers (excluding in each case customers obtained through acquisitions) |

| • | | a reduction in Cable segment capital expenditures of 7.5% to approximately $5.5 billion |

| • | | the transition of more of our programming to digital transmission rather than analog transmission in order to recapture bandwidth that will allow us to continue to expand our service offerings |

| • | | the initial deployment of DOCSIS 3.0 high-speed Internet technology, also referred to as Wideband |

| • | | the acquisition of cable systems serving Illinois and Indiana (approximately 696,000 video customers), as a result of the dissolution of Insight Midwest, LP (the “Insight transaction”), in January 2008 |

| • | | an investment as part of an investor group in a new entity named Clearwire that is focusing on the deployment of a nationwide 4G wireless network using its significant wireless spectrum holdings and was formed through the combination of the 4G wireless broadband businesses of Clearwire’s legal predecessor and Sprint Nextel (“Sprint”); through related agreements entered into in connection with our investment, we will be able to offer wireless services utilizing Clearwire’s 4G and certain of Sprint’s existing wireless networks |

| • | | the completion of various transactions, including the acquisition of Internet-related businesses, which include Plaxo and DailyCandy, and the purchase of an additional ownership interest in Comcast SportsNet Bay Area |

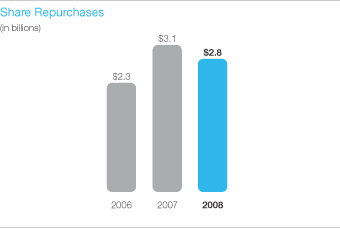

| • | | the repurchase of approximately 141 million shares of our Class A common stock and Class A Special common stock for approximately $2.8 billion under our share repurchase authorization |

| | | | |

| | 1 | | Comcast 2008 Annual Report on Form 10-K |

| • | | the initiation of a quarterly dividend of $0.0625 per share in February 2008; we declared dividends of approximately $727 million in 2008, of which $547 million were paid during 2008 |

We operate our businesses in an intensely competitive environment. Competition for the cable services we offer consists primarily of direct broadcast satellite (“DBS”) operators and phone companies. In 2008, our competitors continued to add features

and adopt aggressive pricing and packaging for services that are comparable to the services we offer and the local phone companies have continued to expand their service areas. A substantial portion of our revenue comes from residential customers whose spending patterns may be affected by prevailing economic conditions. Intensifying competition and a weakening economy affected our net customer additions in 2008 and may, if these conditions continue, adversely impact our results of operations in the future.

Description of Our Businesses

Cable Segment

The table below summarizes certain customer and penetration data for our cable operations as of December 31.

| | | | | | | | | | | | | | | |

| (in millions) | | 2008 | | | 2007 | | | 2006 | | | 2005 | | | 2004 | |

Homes passed(a) | | 50.6 | | | 48.5 | | | 45.7 | | | 38.6 | | | 37.8 | |

Video | | | | | | | | | | | | | | | |

Video customers(b) | | 24.2 | | | 24.1 | | | 23.4 | | | 20.3 | | | 20.5 | |

Penetration(c) | | 47.8 | % | | 49.6 | % | | 51.3 | % | | 52.7 | % | | 54.1 | % |

Digital video customers(d) | | 17.0 | | | 15.2 | | | 12.1 | | | 9.1 | | | 8.1 | |

Digital video penetration(c) | | 70.3 | % | | 63.1 | % | | 51.9 | % | | 44.8 | % | | 39.4 | % |

High-speed Internet | | | | | | | | | | | | | | | |

Available homes(e) | | 50.3 | | | 48.1 | | | 45.2 | | | 38.2 | | | 37.1 | |

Internet customers | | 14.9 | | | 13.2 | | | 11.0 | | | 8.1 | | | 6.6 | |

Penetration(c) | | 29.7 | % | | 27.5 | % | | 24.4 | % | | 21.1 | % | | 17.8 | % |

Phone | | | | | | | | | | | | | | | |

Available homes(e) | | 46.7 | | | 42.2 | | | 31.5 | | | 19.6 | | | 8.9 | |

Phone customers | | 6.5 | | | 4.6 | | | 2.4 | | | 1.2 | | | 1.1 | |

Penetration(c) | | 13.9 | % | | 10.8 | % | | 7.6 | % | | 6.0 | % | | 12.2 | % |

Basis of Presentation: Information related to cable system acquisitions is included from the date acquired. Information related to cable systems sold or exchanged is excluded for all periods presented. All percentages are calculated based on actual amounts. Minor differences may exist due to rounding.

| (a) | | Homes are considered passed (“homes passed”) if we can connect them to our distribution system without further extending the transmission lines. As described in Note (b) below, in the case of certain multiple dwelling units (“MDUs”), such as apartment buildings and condominium complexes, homes passed are counted on an adjusted basis. Homes passed is an estimate based on the best available information. Homes passed and available homes do not include the number of small and medium-sized businesses passed, which cannot be reasonably estimated at this time. |

| (b) | | Generally, a dwelling or commercial unit with one or more television sets connected to our distribution system counts as one video customer. In the case of some MDUs, we count homes passed and video customers on a Federal Communications Commission (“FCC”) equivalent basis by dividing total revenue received from a contract with an MDU by the standard residential rate where the specific MDU is located. |

| (c) | | Penetration is calculated by dividing the number of customers by the number of homes passed or available homes, as appropriate. The number of customers includes our small and medium-sized business customers. |

| (d) | | Digital video customers are those who receive any level of video service via digital transmissions. A dwelling with one or more digital set-top boxes counts as one digital video customer. On average, as of December 31, 2008, each digital video customer had 1.6 digital set-top boxes. |

| (e) | | Homes are considered available (“available homes”) if we can connect them to our distribution system without further upgrading the transmission lines and if we offer the service in that area. Available homes for phone include digital and circuit-switched homes. See also note (a) above. |

| | | | |

| Comcast 2008 Annual Report on Form 10-K | | 2 | | |

Cable Services

We offer a variety of services over our cable systems, including video, high-speed Internet and phone services (“cable services”) and market these services individually and in packages. Substantially all of our customers are residential customers. We have traditionally offered our video services to restaurants and hotels, and we are now offering our cable services to small and medium-sized businesses. Monthly subscription rates and related charges vary according to the service selected and the type of equipment the customer uses, and customers typically pay us on a monthly basis. While residential customers may discontinue services at any time, business customers may only discontinue their services in accordance with the terms of their respective contracts, which typically have one to three year terms.

We are focusing our technology initiatives on extending the capacity and efficiency of our networks, increasing the capacity and functionality of advanced set-top boxes, developing and integrating cross-service features and functionality, and developing interactive services.

Video Services

Our video service offerings range from a limited analog service to a full digital service, as well as advanced services, including high-definition television (“HDTV”) and digital video recorder (“DVR”). We tailor our channel offerings for each system serving a particular geographic area according to applicable local and federal regulatory requirements, programming preferences and demographics.

Our video services consist of a limited analog service, which generally includes access to between 20 and 40 channels of programming, an expanded analog service, which generally includes access to between 60 and 80 channels of programming, and digital video services with access to over 250 channels, depending on the level of service selected. Our video services generally include programming provided by national and local broadcast networks, national and regional cable networks, and governmental and public access programming. Our digital video services generally include access to multiple music channels; our On Demand service; and an interactive, on-screen program guide. We also offer some specialty tiers with sports, family or international themes.

Our video customers may also subscribe to premium channel programming. Premium channels include cable networks such as HBO, Showtime, Starz and Cinemax, which generally offer, without commercial interruption, movies, original programming, live and taped sporting events, concerts and other special features.

Our On Demand service allows our digital video customers the opportunity to choose from a selection of more than 10,000 standard-definition and high-definition programs over the course of a month; start the programs at whatever time is convenient; and pause, rewind and fast-forward the programs. The majority of our

On Demand content is available to our digital video customers at no additional charge, with additional content available on a pay-per-view basis. Digital video customers subscribing to premium channels generally have access to the premium channel’s On Demand content without additional fees. Our pay-per-view On Demand service allows our video customers to order, for a separate fee, individual new release and library movies and special-event programs, such as professional boxing, professional wrestling and concerts. We are continuing to expand the number of On Demand choices, including HDTV programming.

Video customers may also subscribe to our advanced services, HDTV and DVR. Our HDTV service provides our video customers with improved, high-resolution picture quality, improved audio quality and a wide-screen format. Our HDTV service offers our digital video customers a broad selection of high-definition programming, including most major broadcast networks, leading national cable networks, premium channels and regional sports networks. In addition, our On Demand service provides over 1,000 HDTV programming choices. We are continuing to expand our HDTV programming choices. Our DVR service lets digital video customers select, record and store programs and play them at whatever time is convenient. Our DVR service also provides the ability to pause and rewind “live” television.

High-Speed Internet Services

We offer high-speed Internet services with Internet access at downstream speeds of up to 24 Mbps, depending on the service selected, and up to 50 Mbps with the introduction of DOCSIS 3.0 technology, also referred to as Wideband, based on geographic market availability. These services also include our interactive portal, Comcast.net, which provides multiple e-mail addresses and online storage, as well as a variety of content and value-added features and enhancements that are designed to take advantage of the speed of the Internet services we provide.

Phone Services

We offer a Voice over Internet Protocol (“VoIP”) digital phone service that provides either usage-based or unlimited local and domestic long-distance calling, including features such as voice mail, caller ID and call waiting. We phased out substantially all of our circuit-switched phone service in 2008.

Advertising

As part of our programming license agreements with programming networks, we often receive an allocation of scheduled advertising time that we may sell to local, regional and national advertisers. We also coordinate the advertising sales efforts of other cable operators in some markets, and in some markets we operate advertising interconnects. These interconnects establish a physical, direct link between multiple cable systems and provide for the sale of regional and national advertising across larger geographic areas than could be provided by a single cable company. We are also in the process of developing technology for interactive advertising.

| | | | |

| | 3 | | Comcast 2008 Annual Report on Form 10-K |

Regional Sports Networks

Our regional sports networks include Comcast SportsNet (Philadelphia), Comcast SportsNet Mid-Atlantic (Baltimore/Washington), Cable Sports Southeast, Comcast SportsNet Chicago, MountainWest Sports Network, Comcast SportsNet California (Sacramento), Comcast SportsNet New England (Boston), Comcast SportsNet Northwest (Portland) and Comcast SportsNet Bay Area (San Francisco). These networks generate revenue from monthly per subscriber license fees paid by multichannel video providers and through the sale of advertising time.

Other Revenue Sources

We also generate revenue from our digital media center, installation services, commissions from electronic retailing networks and fees from other services.

Sources of Supply

To offer our video services, we license from programming networks the substantial majority of the programming channels and the associated On Demand offerings we distribute, and we generally pay a monthly fee for such programming on a per video subscriber, per channel basis. We attempt to secure long-term programming licenses with volume discounts and/or marketing support and incentives. We also license individual programs or packages of programs from programming suppliers for our On Demand service, generally under shorter-term agreements.

Our video programming expenses depend on the number of our video customers, the number of channels and programs we provide, and the programming license fees we are charged. We expect our programming expenses to continue to be our largest single expense item and to increase in the future.

We purchase a significant number of the set-top boxes and network equipment from a limited number of suppliers that we use in providing our video services.

For our high-speed Internet portal, Comcast.net, we license software products (such as e-mail and security software) and content (such as news feeds) from a variety of suppliers under contracts in which we generally pay on a fixed-fee basis, or on a per customer basis in the case of software product licenses, or on a video advertising revenue share basis in the case of content licenses.

To offer our phone services, we license software products (such as voice mail) from a variety of suppliers under multiyear contracts. The fees we pay are based on the consumption of the related services.

In connection with our provision of cable services, we license all of our billing software from two vendors.

Customer and Technical Services

We service our customers through local, regional and national call and technical centers. These call centers provide 24/7 call-answering capability, telemarketing and other services. Our technical services group performs various tasks, including installations, transmission and distribution plant maintenance, plant upgrades, and activities related to customer service.

Technology

Our cable systems employ a network architecture of hybrid fiber coax that we believe is sufficiently flexible and scalable to support our future requirements. This network allows the two-way delivery of transmissions, which is essential to providing interactive video services, such as On Demand, and high-speed Internet and digital phone services.

We continue to work on technology initiatives, including:

| • | | development of cross-platform functionality that will integrate key features of two or more of our services |

| • | | recapture of bandwidth available in our network, both by delivering more of our programming through digital, as opposed to analog, transmission and by exploiting digital optimization |

| • | | development of technology that provides early detection of problems within our network and provides our technicians with enhanced diagnostic tools |

| • | | development of software for our network and for set-top boxes that measures the reliability and quality of our video signals and identifies video problems for particular customers |

| • | | the internal development of strategically important software and technologies, as well as technology specifications that integrate third-party software |

| • | | expanding our use of open technology solutions that allow multiple vendors to more easily integrate with our technology |

| • | | working with members of CableLabs, a nonprofit research and development consortium founded by members of the cable industry, to develop and integrate a common software platform, known as tru2way, that enables cable companies, content developers, network programmers, consumer electronics companies and others to extend interactivity to the TV set and other types of devices |

| • | | exploring wireless options to extend our services outside the home to provide mobility and create new features that integrate with our services, including our November 2008 investment in a new entity named Clearwire that is focusing on the deployment of a nationwide 4G wireless network and our purchase of wireless spectrum, both directly and through a consortium |

| | | | |

| Comcast 2008 Annual Report on Form 10-K | | 4 | | |

Sales and Marketing

We offer our products and services directly to customers through our call centers, door-to-door selling, direct mail advertising, television advertising, local media advertising, telemarketing and retail outlets. We also market our video, high-speed Internet and digital phone services individually and as bundled services.

Competition

We operate our businesses in an intensely competitive environment. We compete with a number of different companies that offer a broad range of services through increasingly diverse means. Competition for the cable services we offer consists primarily of DBS operators and local phone companies. In 2008, our competitors continued to add features and adopt aggressive pricing and packaging for services that are comparable to the services we offer, and the local phone companies have continued to expand their service areas. These competitive factors have had an impact on and are likely to continue to affect our results of operations. In addition, we operate in a technologically complex environment where it is likely that new technologies will further increase the number of competitors we face for our video, high-speed Internet and phone services, and for our advertising business. We expect advances in communications technology, such as video streaming over the Internet, to continue in the future, and we are unable to predict what effects these developments will have on our businesses and operations.

Video Services

We compete with a number of different sources that provide news, sports, information and entertainment programming to consumers, including:

| • | | DBS providers that transmit satellite signals containing video programming, data and other information to receiving dishes located on the customer’s premises |

| • | | certain local phone companies that have built and are continuing to build wireline fiber-optic-based networks, in some cases using Internet protocol (“IP”) technology, to provide video and data services in substantial portions of their service areas and in an increasing number of our service areas, in addition to marketing DBS service in certain areas |

| • | | other providers that build and operate wireline communications systems in the same communities that we serve, including those operating as franchised cable operators |

| • | | online services that offer Internet video streaming, downloading and distribution of movies, television shows and other video programming |

| • | | satellite master antenna television systems, known as SMATVs, that generally serve condominiums, apartment and office complexes, and residential developments |

| • | | local television broadcast stations that provide free over-the-air programming |

| • | | wireless and other emerging mobile technologies that provide for the distribution and viewing of video programming |

| • | | video rental services and home video products |

In recent years, Congress has enacted legislation and the FCC has adopted regulatory policies intended to provide a favorable operating environment for existing competitors and for potential new competitors to our cable systems. The FCC adopted rules favoring new investment by local phone companies in networks capable of distributing video programming and rules allocating and auctioning spectrum for new wireless services that may compete with our video service offerings. Furthermore, the FCC and various state governments have adopted measures that reduce or eliminate local franchising requirements for new entrants into the multichannel video marketplace, including local phone companies. Certain of these franchising entry measures have already been adopted in many states in which we operate. We could be materially disadvantaged if FCC and state franchising rules continue to set a different, less burdensome standard for some of our competitors than for ourselves(see “Legislation and Regulation” below).

Direct broadcast satellite systems

According to recent government and industry reports, conventional, medium-power and high-power satellites provide video programming to over 35 million customers in the United States. DBS providers with high-power satellites typically offer more than 250 channels of programming, including programming services substantially similar to those our cable systems provide. Two companies, DIRECTV and DISH Network, provide service to substantially all of these DBS customers.

High-power satellite service can be received throughout the continental United States through small rooftop or side-mounted outdoor antennas. Satellite systems use video compression technology to increase channel capacity and digital technology to improve the quality and quantity of the signals transmitted to their customers. Our digital cable service is competitive with the programming, channel capacity and quality of signals currently delivered to customers by DBS providers.

Federal legislation establishes, among other things, a compulsory copyright license that permits satellite systems to retransmit local broadcast television signals to customers who reside in the local television station’s market. These companies are currently transmitting local broadcast signals in most markets that we serve. Additionally, federal law generally provides satellite systems with access to cable-affiliated video programming services delivered by satellite. DBS providers also have arrangements with local phone companies in which the DBS provider’s video services are sold together with a local phone company’s high-speed Internet and phone services.

| | | | |

| | 5 | | Comcast 2008 Annual Report on Form 10-K |

Local phone companies

Local phone companies, in particular AT&T and Verizon, have built and continue to build fiber-optic-based networks to provide video services in substantial portions of their service areas. These local phone companies have continued to offer video services in an increasing number of our service areas, and we anticipate that local phone companies’ video services will be offered in a substantial portion of our service areas in the near future. In certain areas, video services are being offered in addition to joint marketing arrangements local phone companies have entered into with DBS providers. Local phone companies have taken various positions on the question of whether they need a local cable television franchise to provide video services. Some, like Verizon, have applied for local cable franchises while others, like AT&T, claim that they can provide their video services without a local cable franchise. Notwithstanding their positions, both AT&T and Verizon have filed for video service franchise certificates under state franchising laws(see “Legislation and Regulation” below).

Other providers

We operate our cable systems under nonexclusive franchises that are issued by a local community governing body, such as a city council or county board of supervisors or, in some cases, by a state regulatory agency. Federal law prohibits franchising authorities from unreasonably denying requests for additional franchises, and it permits franchising authorities to operate cable systems. In addition to local phone companies, various other companies, including those that traditionally have not provided cable services and have substantial financial resources (such as public utilities, including those that own some of the poles to which our cables are attached), have obtained cable franchises and provide competing cable services. These and other cable systems offer cable services in various areas where we hold franchises. We anticipate that facilities-based competitors will emerge in other franchise areas that we serve.

Satellite master antenna television systems

Our cable systems also compete for customers with SMATV systems. SMATV system operators typically are not subject to regulation in the same manner as local, franchised cable system operators. SMATV systems offer customers both improved reception of local television stations and much of the programming offered by our cable systems. In addition, some SMATV operators offer packages of video, Internet and phone services to residential and commercial developments.

Local broadcast services

Local broadcast stations have the ability to broadcast multiple streams of free programming in their digital broadcast spectrum, and some broadcasters are providing such services in markets that we serve. The increasing use of such free multicast services could present competitive challenges to our cable service.

High-Speed Internet Services

We compete with a number of other companies, many of which have substantial resources, including:

| • | | Internet service providers (“ISPs”), such as AOL, Earthlink and Microsoft |

| • | | wireless phone companies and other providers of wireless Internet service |

Digital subscriber line (“DSL”) technology allows Internet access to be provided to customers over telephone lines at data transmission speeds substantially greater than those of dial-up modems. Local phone companies and other companies offer DSL service, and several of them have increased transmission speeds, lowered prices or created bundled service packages. In addition, some local phone companies, such as AT&T and Verizon, have built and are continuing to build fiber-optic-based networks that allow them to provide data transmission speeds that exceed those that can be provided with DSL technology and are now offering these higher speed services in many of our markets. The FCC has reduced the obligations of local phone companies to offer their broadband facilities on a wholesale or retail basis to competitors, and it has freed their DSL services of common carrier regulation.

Various wireless phone companies are offering wireless high-speed Internet services. In addition, in a growing number of commercial areas, such as retail malls, restaurants and airports, Wi-Fi Internet service is available. Numerous local governments are also considering or actively pursuing publicly subsidized Wi-Fi and WiMAX Internet access networks, and commercial WiMAX offerings are being rolled out.

The FCC has adopted an order that prohibits us from engaging in certain high-speed Internet network management practices, and Congress and the FCC are considering creating certain rights for Internet content providers and for users of high-speed Internet services by imposing “net neutrality” requirements on service providers. These requirements, as well as any other measures adopted by Congress or the FCC that impose additional obligations on high-speed Internet service providers, could adversely affect our high-speed Internet business(see “Legislation and Regulation” below).

| | | | |

| Comcast 2008 Annual Report on Form 10-K | | 6 | | |

Phone Services

Our digital phone service competes against local phone companies, wireless phone service providers, competitive local exchange carriers (“CLECs”) and other VoIP service providers. The local phone companies have substantial capital and other resources, longstanding customer relationships, and extensive existing facilities and network rights-of-way. A few CLECs also have existing local networks and significant financial resources.

Advertising

We compete for the sale of advertising against a wide variety of media, including local broadcast stations, national broadcast networks, national and regional programming networks, local radio broadcast stations, local and regional newspapers, magazines and Internet sites.

Programming Segment

The table below presents a summary of our most significant consolidated national programming networks as of December 31, 2008.

| | | | |

| Programming Network | | Approximate U.S. Subscribers (in millions) | | Description |

E! | | 85 | | Pop culture and entertainment-related programming |

Golf Channel | | 73 | | Golf and golf-related programming |

VERSUS | | 66 | | Sports and leisure programming |

G4 | | 57 | | Gamer lifestyle programming |

Style | | 51 | | Lifestyle-related programming |

Revenue for our programming networks is primarily generated from the sale of advertising and from monthly per subscriber license fees paid by multichannel video providers that have typically entered into multiyear contracts to distribute our programming networks. To obtain long-term contracts with distributors, we may make cash payments, provide an initial period in which license fee payments are waived or do both. Our programming networks assist distributors with ongoing marketing and promotional activities to retain existing customers and acquire new customers. Although we believe prospects of continued carriage and marketing of our programming networks by larger distributors are generally good, the loss of one or more of such distributors could have a material adverse effect on our programming networks.

Sources of Supply

Our programming networks often produce their own television programs and broadcasts of live events. This often requires us to acquire the rights to the content that is used in such productions (such as rights to screenplays or sporting events). In other cases, our programming networks license the cable telecast rights to television programs produced by third parties.

Competition

Our programming networks compete with other television programming services for distribution and programming. In addition, our programming networks compete for audience share with

all other forms of programming provided to viewers, including broadcast networks; local broadcast stations; pay and other cable networks; home video, pay-per-view and video on demand services; and Internet sites. Finally, our programming networks compete for advertising revenue with other national and local media, including other television networks, television stations, radio stations, newspapers, Internet sites and direct mail.

Other Businesses

Our other business interests include Comcast Interactive Media and Comcast Spectacor. Comcast Interactive Media develops and operates Comcast’s Internet businesses focused on entertainment, information and communication, including Comcast.net, Fancast, thePlatform, Fandango, Plaxo and DailyCandy. Comcast Spectacor owns two professional sports teams and two large, multipurpose arenas, and manages other facilities for sporting events, concerts and other events.

We also own noncontrolling interests in certain networks and content providers, including MGM, iN DEMAND, TV One, PBS KIDS Sprout, FEARnet, New England Cable News, Pittsburgh Cable News Channel, Music Choice and SportsNet New York. In addition, we have noncontrolling interests in wireless-related companies, including Clearwire and SpectrumCo, LLC.

| | | | |

| | 7 | | Comcast 2008 Annual Report on Form 10-K |

Legislation and Regulation

Our Cable segment is subject to regulation by federal, state and local governmental authorities under federal and state laws and regulations as well as agreements we enter into with franchising authorities. The Communications Act of 1934, as amended (the “Communications Act” or “Act”) and FCC regulations and policies affect significant aspects of our Cable segment, including cable system ownership, video customer rates, carriage of broadcast television stations, the way we sell our programming packages to customers, access to cable system channels by franchising authorities and other parties, the use of utility poles and conduits and the offering of our high-speed Internet and phone services. Our Programming segment is subject to more limited governmental regulation.

Federal regulation and regulatory scrutiny of our Cable and Programming segments have increased over the last three years, even as the cable industry is subject to increasing competition from DBS providers, phone companies and others for video, high-speed Internet and phone services. Meanwhile, the FCC has provided regulatory relief and various regulatory advantages to our competitors, examples of which are provided below. Further, in some areas, the Communications Act treats certain multichannel video programming distributors (“MVPDs”) differently from others. For example, ownership limits, pricing and packaging regulation, must-carry and franchising are not applicable to our DBS competitors. Regulation continues to present significant adverse risks to our businesses.

Regulators at all levels of government frequently consider changing, and sometimes do change, existing rules or interpretations of existing rules, or prescribe new ones. The transition to a new administration under President Obama will likely lead to turnover in the leadership of many federal agencies, including the FCC. We are unable to predict how new leadership in these agencies will ultimately affect regulation of our businesses. In addition, we always face the risk that Congress or one or more states will approve legislation significantly affecting our businesses, such as proposed federal legislation referred to as the Employee Free Choice Act, which would substantially liberalize the procedures for union organization.

The following paragraphs describe existing and potential future legal and regulatory requirements for our businesses.

Video Services

Ownership Limits

The FCC adopted an order in 2007 establishing a 30% limit on the percentage of multichannel video customers that any single cable

provider can serve nationwide. Because we currently serve approximately 26% of multichannel video customers nationwide, the 30% ownership limit constrains our ability to take advantage of future growth opportunities. A federal appellate court struck down a similar 30% limit in a 2001 decision, and we have appealed the new limit in court. The FCC is also assessing whether it should reinstate a limit on the number of affiliated programming networks a cable operator may carry on its cable systems. The FCC’s previous limit of 40% of the first 75 channels was also struck down by the federal appellate court in the 2001 decision. The percentage of affiliated programming networks we currently carry is well below the previous 40% limit. It is uncertain when the FCC will rule on this issue or how any regulation it adopts might affect us.

Pricing and Packaging

The Communications Act and FCC regulations and policies limit the prices that cable operators may charge for limited basic service, equipment and installation, as well as the manner in which cable operators may package premium or pay-per-view services with other tiers of service. These rules do not apply to cable systems that the FCC determines are subject to effective competition. The FCC has made this determination for systems covering 33% of our customers, and, as of December 31, 2008, we have pending before the FCC additional petitions for determination of effective competition for systems covering another 12% of our customers. An additional 35% of our customers are not subject to rate regulation because numerous local franchising authorities have chosen not to make the FCC certification filing necessary to regulate rates. From time to time, Congress and the FCC consider imposing new pricing or packaging regulations on the cable industry, including proposals that would require cable operators to offer programming networks on an a la carte or themed-tier basis instead of, or in addition to, our current packaged offerings. As discussed under “Legal Proceedings” in Item 3, we and others are currently involved in litigation that could force us and other MVPDs to offer programming networks on an a la carte basis. Additionally, uniform pricing requirements under the Communications Act may affect our ability to respond to increased competition through offers, promotions or other discounts that aim to retain existing customers or regain those we have lost. In October 2008, the FCC initiated several inquiries regarding the cable industry’s transition from analog to digital transmission and the potential impact of these transition efforts on pricing and packaging for customers who lack the equipment necessary to receive digital programming. We believe that our product and service offerings will improve as we deliver more of our programming through digital transmission, because we will be able to provide more high-definition programming and video on demand services, better picture quality of our video services, faster Internet speeds and other services. There is a risk that the FCC could pursue regulatory or enforcement actions in this area, which could complicate or delay our transition to digital technology and could have an adverse effect on our business.

| | | | |

| Comcast 2008 Annual Report on Form 10-K | | 8 | | |

Must-Carry/Retransmission Consent

Cable operators are currently required to carry, without compensation, the programming transmitted by most local commercial and noncommercial television stations. Alternatively, local television stations may insist that a cable operator negotiate for retransmission consent, which may enable popular stations to demand cash payments or other significant concessions (such as the carriage of, and payment for, other programming networks affiliated with the broadcaster) as a condition of transmitting the TV broadcast signals that video customers expect to receive. As part of the transition from analog to digital broadcast transmission, Congress and the FCC gave each local broadcast station a digital channel, capable of carrying multiple programming streams, in addition to its current analog channel. After the broadcasters’ transition to digital (the current transition date is June 12, 2009, although broadcasters have the option of making the transition earlier), cable operators will have to carry the primary digital programming stream of local broadcast stations, as well as an analog version of the primary digital programming stream. These requirements will last for at least three years from the date of the digital transition. The FCC has provided a limited exemption from these requirements for cable systems with an activated channel capacity of 552 MHz or less. Under this exemption, which applies to certain of our cable systems, the operator is only obligated to carry the analog version of the broadcaster’s primary digital programming stream. The FCC is also considering proposals to require cable operators to carry, after the 2009 transition date, some or all of the multiple programming streams transmitted in the broadcaster’s digital signal. Such expanded must-carry obligations would further constrain our ability to allocate bandwidth to more high-definition channels, faster Internet speeds and other services. In addition, the FCC is considering proposals that would require cable operators to carry certain low power broadcast television stations that, under current regulations, generally lack must-carry rights.

Program Access/Program Carriage/License Agreements

The Communications Act and the FCC’s program access rules generally prevent video programmers affiliated with cable operators from favoring cable operators over competing MVPDs, such as DBS providers, and limit the ability of such affiliated programmers to offer exclusive programming arrangements to cable operators. The FCC has extended the exclusivity restrictions through October 2012. We have challenged this FCC action in federal court. In addition, the Communications Act and the FCC’s program carriage rules prohibit cable operators and other MVPDs from requiring a financial interest in, or exclusive distribution rights for, any video programming network as a condition of carriage, or from unreasonably restraining the ability of an unaffiliated programming network to compete fairly by discriminating against the network on the basis of its nonaffiliation in the selection, terms or conditions for carriage. The FCC is considering proposals to expand its program access and program carriage regulations that, if adopted, could have an adverse effect on our businesses. In addition, under the FCC’s July 2006 order approving our acquis-

ition of Adelphia cable systems and related Time Warner transactions, until July 2012 our regional sports networks are generally covered by the program access rules, and MVPDs may invoke commercial arbitration against such regional sports networks as an alternative to filing a program access complaint with the FCC. In addition, we are a party to program carriage disputes at the FCC involving three programming networks (NFL Network, WealthTV and Mid-Atlantic Sports Network). Adverse decisions in these disputes could increase our costs and curtail our flexibility to deliver services to our customers.

Leased Access

The Communications Act requires a cable system to make available up to 15% of its channel capacity for commercial leased access by third parties to provide programming that may compete with services offered directly by the cable operator. To date, we have not been required to devote significant channel capacity to leased access. However, the FCC adopted rules in 2007 that dramatically reduce the rates we can charge for leased access channels. Although the lower rates initially will not apply to home shopping or infomercial programmers, the FCC has issued a further notice to determine if such programming should also have the benefit of the lower rates. These new FCC rules, which have been stayed by a federal court pending the outcome of a challenge brought by us and other cable operators and which also have been blocked by the Office of Management and Budget, could adversely affect our business by significantly increasing the number of cable system channels occupied by leased access users and by significantly increasing the administrative burdens and costs associated with complying with such rules.

Cable Equipment

The FCC has adopted regulations aimed at promoting the retail sale of set-top boxes and other equipment that can be used to receive digital video services. Effective July 2007, cable operators were prohibited from acquiring for deployment set-top boxes that perform both channel navigation and security functions. Set-top boxes purchased after that date must rely on a separate security device known as a CableCARD, which adds to the cost of set-top boxes. In addition, the FCC has adopted rules to implement an agreement between the cable and consumer electronics industries aimed at promoting the manufacture of plug-and-play TV sets that can connect directly to a cable network and receive one-way analog and digital video services without the need for a set-top box. The FCC is also considering proposals to establish regulations for plug-and-play retail devices that can access two-way cable services. Some of the proposals, if adopted, would impose substantial costs on us and impair our ability to innovate. In April 2008, we joined major consumer electronics companies, information technology companies and other major cable operators in an agreement to use certain technology to enable retail devices to access two-way cable services. We believe that this inter-industry agreement makes it less likely the FCC will adopt two-way plug-and-play requirements in the near future.

| | | | |

| | 9 | | Comcast 2008 Annual Report on Form 10-K |

MDUs and Inside Wiring

In October 2007, the FCC adopted an order prohibiting the enforcement of exclusive video service access agreements between cable operators and MDUs and other private real estate developments. The order also prohibits the execution of new exclusive access agreements. The order has been appealed by the National Cable & Telecommunications Association (“NCTA”), the cable industry’s trade organization. The FCC is also considering proposals to extend these prohibitions to non-cable MVPDs and to expand the scope of the rules to prohibit exclusive marketing and bulk billing agreements. Because we have a significant number of exclusive access agreements, the FCC’s order to abrogate the exclusivity provisions of those agreements could negatively affect our business, as would adoption of new limits on exclusive marketing and bulk billing. The FCC has also adopted rules facilitating competitors’ access to the cable wiring inside such MDUs. These rules could also have an adverse impact on our business as they allow our competitors to use wiring we have deployed to reach potential customers more quickly and inexpensively.

Pole Attachments

The Communications Act permits the FCC to regulate the rate that pole-owning utility companies (with the exception of municipal utilities and rural cooperatives) charge cable systems for attachments to their poles. States are permitted to preempt FCC jurisdiction and regulate the terms of attachments themselves, and many states in which we operate have done so. Most of these states have generally followed the FCC’s pole rate standards. The FCC or a state could increase pole attachment rates paid by cable operators. Additionally, higher pole attachment rates apply to pole attachments that are subject to the FCC’s telecommunications services pole rates. The applicability of and method for calculating those rates for cable systems over which phone services are transmitted remain unclear, and there is a risk that we could face materially higher pole attachment costs. In November 2007, the FCC initiated a proceeding to consider whether to modify its rules governing prices for pole attachments. Among other issues, the FCC is considering establishing a new unified pole attachment rate that would apply to cable system attachments where the cable operator provides high-speed Internet services and, perhaps, phone services as well. The proposed rate would be higher than the current rate paid by cable service providers but lower than the rate that applies to attachments used to provide telecommunications services. If adopted, this proposal could materially increase our costs by increasing our existing payments for pole attachments.

Franchising

Cable operators generally operate their cable systems under nonexclusive franchises granted by local or state franchising authorities. While the terms and conditions of franchises vary materially from jurisdiction to jurisdiction, franchises typically last for a fixed term; obligate the franchisee to pay franchise fees and

meet service quality, customer service and other requirements; and are terminable if the franchisee fails to comply with material provisions. The Communications Act permits franchising authorities to establish reasonable requirements for public, educational and governmental access programming, and many of our franchises require substantial channel capacity and financial support for this programming. The Communications Act also contains provisions governing the franchising process, including, among other things, renewal procedures designed to protect incumbent franchisees against arbitrary denials of renewal. We believe that our franchise renewal prospects generally are favorable.

There has been considerable activity at both the federal and state levels addressing franchise requirements imposed on new entrants. This activity is primarily directed at facilitating local phone companies’ entry into cable services. In December 2006, the FCC adopted new rules designed to ease the franchising process and reduce franchising burdens for new entrants by, among other things, limiting the range of financial, construction and other commitments that franchising authorities can request of new entrants, requiring franchising authorities to act on franchise applications by new entrants within 90 days, and preempting certain local “level playing field” franchising requirements. The FCC subsequently adopted more modest franchising relief for existing cable operators. We could be materially disadvantaged if the rules continue to set a different, less burdensome standard for some of our competitors than for ourselves. From time to time, Congress has also considered proposals to eliminate or streamline local franchising requirements for local phone companies and other new entrants. We cannot predict whether such legislation will be enacted or what effect it would have on our business.

In addition, approximately half of the states in which we operate have enacted legislation to provide statewide franchising or to simplify local franchising requirements for new entrants, thus relieving new entrants of many of the local franchising burdens faced by incumbent operators. Some of these statutes also allow new entrants to operate on more favorable terms than our current operations, for instance by not requiring that the applicant provide service to all parts of the franchise area or permitting the applicant to designate only those portions it wishes to serve. Certain of these state statutes allow incumbent cable operators to opt into the new state franchise where a competing state franchise has been issued for the incumbent’s franchise area. However, even in those states where incumbent cable operators are allowed to opt into a state franchise, we often are required to retain certain franchise obligations that are more burdensome than the new entrant’s state franchise.

Copyright Regulation

In exchange for filing reports and contributing a percentage of revenue to a federal copyright royalty pool, cable operators can obtain blanket permission to retransmit copyrighted material contained in broadcast signals. The possible modification or

| | | | |

| Comcast 2008 Annual Report on Form 10-K | | 10 | | |

elimination of this copyright license is the subject of ongoing legislative and administrative review. In June 2008, the Copyright Office issued a report to Congress in which it recommended eliminating the compulsory copyright license in favor of free market negotiations between cable operators and copyright owners. If adopted, this proposal could adversely affect our ability to obtain certain programming and substantially increase our programming costs. In May 2008, the Copyright Office rejected a cable industry request to clarify that copyright fees associated with the retransmission of out-of-market broadcast signals should be limited to system customers who actually receive those signals. The Copyright Office concluded it did not have authority under the governing statute to adopt that interpretation. There is a risk that the Copyright Office’s determination on this issue could materially increase the copyright royalty fees that we and other cable operators pay to retransmit out-of-market broadcast signals. Further, in June 2008, the Copyright Office issued a Notice of Proposed Rulemaking addressing how the compulsory license will apply to digital broadcast signals and services. In this notice, the Copyright Office proposed to require royalty fees from cable operators for carriage of each digital multicast stream of programming from an out-of-market television broadcast station. If adopted, this proposal could significantly increase our royalty fees for the carriage of out-of-market television stations. In addition, we pay standard industry licensing fees to use music in the programs we create, including our Cable segment’s local advertising and local origination programming, and our Programming segment’s original programs. These licensing fees have been the source of litigation with music performance rights organizations in the past and we cannot predict with certainty whether license fee disputes may arise in the future.

High-Speed Internet Services

We provide high-speed Internet services by means of our existing cable systems. In 2002, the FCC ruled that this was an interstate information service that is not subject to regulation as a telecommunications service under federal law or to state or local utility regulation. However, our high-speed Internet services are subject to a number of regulatory obligations, including compliance with the Communications Assistance for Law Enforcement Act (“CALEA”) requirement that high-speed Internet service providers must implement certain network capabilities to assist law enforcement in conducting surveillance of persons suspected of criminal activity.

Several parties are advocating that Congress and the FCC adopt so-called “net neutrality” rules that would define certain rights for users of high-speed Internet services and regulate or restrict some types of commercial agreements between service providers and providers of Internet content. In 2005, the FCC issued what was characterized at the time as a nonbinding policy statement identifying four principles that will guide its policymaking regarding high-

speed Internet and related services. These principles provide that consumers are entitled to: (i) access lawful Internet content of their choice; (ii) run applications and services of their choice, subject to the needs of law enforcement; (iii) connect their choice of legal devices that do not harm the network; and (iv) enjoy competition among network providers, application and service providers, and content providers. Some have proposed that Congress and the FCC adopt these principles as formal rules and also impose nondiscrimination and disclosure requirements on high-speed Internet service providers. Congress has rejected similar proposals in the past, but such proposals may be revisited and possibly broadened. Any such rules or statutes could limit our ability to manage our cable systems (including use for other services), obtain value for use of our cable systems or respond to competitive conditions. We cannot predict whether “net neutrality” rules or statutes will be adopted.

All networks must be managed to provide high-quality, consistent and safe high-speed Internet services. In August 2008, the FCC found that we had violated “federal Internet policies” by engaging in certain network management practices intended to address congestion on our high-speed Internet network. As a result, we were ordered to disclose certain information about our network management practices to the FCC, and to cease the practices at issue by December 31, 2008. We are challenging that decision in federal court. In the interim, we complied with the disclosure requirements imposed by the FCC. In addition, as of December 31, 2008, we stopped using our earlier techniques in favor of a new set of protocol-agnostic network management congestion practices, and we have so informed the FCC. Continued FCC regulation of our high-speed Internet network management practices could adversely affect our business by impairing our ability to manage our network efficiently.

A federal program known as the Universal Service program generally requires telecommunications service providers to collect and pay a fee based on their revenue from telecommunications services (in recent years, roughly 10% of revenue) into a fund used to subsidize the provision of telecommunications services in high-cost areas and Internet and telecommunications services to schools, libraries and certain health care providers. Congress is considering proposals that could result in high-speed Internet services being subject to Universal Service fees. We cannot predict whether or how the Universal Service funding system might be extended to cover high-speed Internet services or, if that occurs, how it will affect us.

Congress and federal regulators have adopted a wide range of measures affecting Internet use, including, for example, consumer privacy, copyright protection, defamation liability, taxation, obscenity and unsolicited commercial e-mail. State and local governments have also adopted Internet-related regulations. Furthermore, Congress, the FCC and certain state and local governments are also considering proposals to impose customer

| | | | |

| | 11 | | Comcast 2008 Annual Report on Form 10-K |

service, quality of service, taxation, child safety, privacy and standard pricing regulations on high-speed Internet service providers. It is uncertain whether any of these proposals will be adopted. The adoption of new laws or the application of existing laws to the Internet could have a material adverse effect on our high-speed Internet business.

Phone Services

We currently offer phone services using interconnected VoIP technology. Upon receipt of requested approvals for two remaining service areas, we will no longer provide circuit-switched phone service. The FCC has adopted a number of orders addressing regulatory issues relating to providers of nontraditional voice services such as ours, including regulations relating to customer proprietary network information, local number portability duties and benefits, disability access, E911, CALEA, and contributions to the federal Universal Service Fund, but has not yet ruled on the appropriate classification of the specific type of voice services that we provide. The regulatory environment for interconnected VoIP services therefore remains uncertain at both the federal and state level. Until the FCC definitively classifies interconnected VoIP services for state and federal regulatory purposes, state regulatory commissions and legislatures may continue to investigate imposing regulatory requirements on such services.

We and two other cable operators filed a complaint with the FCC against Verizon in 2008 claiming that Verizon had violated a statutory carrier proprietary information requirement in processing requests from us to transfer Verizon customers who had selected us to be their voice provider. The FCC subsequently upheld the complaint, and a federal appellate court rejected Verizon’s appeal of the FCC’s order. Verizon could seek additional judicial review and, if the order were overturned on further appeal, our ability to increase our voice services customer base could be adversely affected.

The FCC and Congress also are considering how nontraditional voice services should interconnect with local phone companies’ phone networks. Since the FCC has not determined the appropriate classification of these services, the precise scope of local phone company interconnection rules applicable to providers of nontraditional voice services is not entirely clear. As a result, some local phone companies may resist interconnecting directly with these providers. In light of these concerns, providers of these services typically either secure CLEC authorization or obtain interconnection to local phone company networks by contracting with an existing CLEC, whose right, as a telecommunications carrier, to request and obtain interconnection with local phone companies is set forth in the Communications Act. We have arranged for such interconnection rights through our own CLECs and through third party CLECs, however certain parties have chal-

lenged our interconnection rights at the FCC and various state commissions and these proceedings remain unresolved.

It is uncertain whether and when the FCC or Congress will adopt further rules regarding interconnection rights and arrangements and how such rules would affect our voice services.

Other Areas

The FCC actively regulates other aspects of our Cable segment and limited aspects of our Programming segment, including the mandatory blackout of syndicated, network and sports programming; customer service standards; political advertising; indecent or obscene programming; Emergency Alert System requirements for analog and digital services; closed captioning requirements for the hearing impaired; commercial restrictions on children’s programming; origination cablecasting (i.e., programming locally originated by and under the control of the cable operator); sponsorship identification; equal employment opportunity; lottery programming; recordkeeping and public file access requirements; telemarketing; technical standards relating to operation of the cable network; and regulatory fees. We are unable to predict how these regulations might be changed in the future and how any such changes might affect our Cable and Programming businesses. In addition, while we believe that we are in substantial compliance with FCC rules, we are occasionally subject to enforcement actions at the FCC, which can result in our having to pay fines to the agency.

State and Local Taxes

Some states and localities have imposed or are considering imposing new or additional taxes or fees on the services we offer, or imposing adverse methodologies by which taxes or fees are computed. These include combined reporting or other changes to general business taxes, central assessments for property tax, and taxes and fees on video and voice services. We and other cable industry members are challenging certain of these taxes through administrative and court proceedings.In addition, in some situations our DBS competitors do not face similar state tax and fee burdens. Congress has also considered, and may consider again, proposals to bar states from imposing taxes on DBS providers that are equivalent to the taxes or fees that we pay.

Privacy and Security Regulation

The Communications Act generally restricts the nonconsensual collection and disclosure to third parties of cable customers’ personally identifiable information by cable operators. There are exceptions that permit the collection and disclosure of this information for rendering service, conducting legitimate business activities related to the service, and responding to legal requests. The Telecommunications Act of 1996 provides additional privacy protections for customer proprietary network information, commonly known as CPNI, related to our digital phone services.

| | | | |

| Comcast 2008 Annual Report on Form 10-K | | 12 | | |

A handful of states and the District of Columbia have enacted privacy laws that apply to cable services.

We are also subject to state and federal rules and laws regarding information security. Most of these rules and laws apply to customer information that could be used to commit identity theft. Forty-five states and the District of Columbia have enacted security breach notification laws. These laws generally require that a business give notice to its customers whose financial account information has been disclosed because of a security breach. The Federal Trade Commission (“FTC”) is applying the “red flag rules” in the Fair and Accurate Credit Transactions Act of 2003 to both financial institutions and creditors. Because we permit customers to pay us for services usually 30 days after they receive them, we are considered a creditor according to the FTC’s interpretation of the rules. We intend to comply with these rules, which become effective for us on May 1, 2009, by using an identity theft prevention program to identify, detect and respond to patterns, practices or specific activities that could indicate identity theft.

We are also subject to state and federal “do not call” laws regarding telemarketing and state and federal laws regarding unsolicited commercial e-mails. Additional and more restrictive requirements may be imposed if and to the extent that state or local authorities establish their own privacy or security standards or if Congress enacts new privacy or security legislation.

Employees

As of December 31, 2008, we employed approximately 100,000 employees, including part-time employees. Of these employees, approximately 89,000 were associated with our Cable business and the remainder were associated with our Programming and other businesses. Approximately 6,000 of our employees (including part-time employees) are covered by collective bargaining agreements or have organized but are not covered by collective bargaining agreements. We believe we have good relationships with our employees.

Caution Concerning Forward-Looking

Statements

The SEC encourages companies to disclose forward-looking information so that investors can better understand a company’s future prospects and make informed investment decisions. In this Annual Report on Form 10-K, we state our beliefs of future events and of our future financial performance. In some cases, you can identify these so-called “forward-looking statements” by words such as “may,” “will,” “should,” “expects,” “believes,” “estimates,”

“potential,” or “continue,” or the negative of these words, and other comparable words. You should be aware that those statements are only our predictions. In evaluating those statements, you should specifically consider various factors, including the risks and uncertainties listed in“Risk Factors” under Item 1A and in other reports we file with the SEC. Actual events or our actual results may differ materially from any of our forward-looking statements.

Additionally, we operate in a highly competitive, consumer-driven and rapidly changing environment. The environment is affected by government regulation; economic, strategic, political and social conditions; consumer response to new and existing products and services; technological developments; and, particularly in view of new technologies, the ability to develop and protect intellectual property rights. Our actual results could differ materially from management’s expectations because of changes in such factors. Other factors and risks could adversely affect our operations, business or financial results of our businesses in the future and could also cause actual results to differ materially from those contained in the forward-looking statements. We undertake no obligation to update any forward-looking statements.

Item 1A:Risk Factors

All of the services offered by our cable systems face a wide range of competition that could adversely affect our future results of operations.

We operate in an intensely competitive industry. Our cable systems compete with a number of different sources that provide news, information and entertainment programming to consumers. We compete directly with other programming distributors, including DBS companies, phone companies, companies that build competing cable systems in the same communities we serve and companies that offer programming and other communications services to our customers and potential customers, including high-speed Internet and voice service providers. Our business and results of operations could be adversely affected if we do not compete effectively.

We may face increased competition because of technological advances and new regulatory requirements, which could adversely affect our future results of operations.

In addition to marketing DBS services in certain areas, local phone companies have built and are continuing to build wireline, fiber-optic-based networks and, in some cases, are using IP technology to provide video services in substantial portions of their service areas. Local phone companies and various other companies also offer DSL and other Internet services. We expect other advances in communications technology, as well as changes in the marketplace, to occur in the future. If we choose technology that is not as

| | | | |

| | 13 | | Comcast 2008 Annual Report on Form 10-K |

effective, cost-efficient or attractive to customers as that employed by our competitors, our business and results of operations could be adversely affected.