SECURITIES AND EXCHANGE COMMISSION

UNDER THE SECURITIES ACT OF 1933

(980) 365-7100

c/o C T Corporation System

28 Liberty Street

New York, NY 10005

(800) 448-5350

Carlton Fields

1025 Thomas Jefferson St., N.W.

Suite 400 West

Washington, DC 20007-5208

Large accelerated filer filer ☐ | Accelerated filer filer ☐ |

Non-accelerated filer ☒ | Smaller reporting company filer ☐ |

Emerging growth company filer ☐ |

6 | |

7 | |

11 | |

12 | |

15 | |

19 | |

20 | |

20 | |

20 | |

20 | |

21 | |

21 | |

21 | |

23 | |

23 | |

24 | |

24 | |

24 | |

25 | |

25 | |

25 | |

25 | |

25 | |

26 | |

26 | |

27 | |

27 | |

28 | |

28 | |

28 | |

33 | |

33 | |

35 | |

36 | |

37 | |

37 | |

37 | |

41 | |

41 | |

43 | |

43 | |

43 | |

46 | |

47 | |

47 | |

48 | |

48 | |

48 | |

48 |

68 | |

69 | |

69 | |

69 | |

69 | |

71 | |

73 | |

74 | |

74 | |

74 | |

75 | |

84 | |

100 | |

100 | |

100 | |

100 | |

100 | |

101 | |

102 | |

102 | |

102 | |

103 | |

103 | |

103 | |

104 | |

110 | |

110 | |

110 | |

113 | |

113 | |

114 | |

117 | |

A-1 | |

B-1 | |

C-1 | |

D-1 | |

E-1 | |

F-1 |

Contract | Individual single premium deferred index-linked separate account annuity contract. |

Purchase Payment | The minimum Purchase Payment: $25,000. Prior approval required for a Purchase Payment of less than $25,000 or $1,000,000 or more. |

Owner and Annuitant Issue Ages | 0-85 |

Contract Periods | The Contract has two periods: •The Accumulation Period, the period prior to the Annuity Date; and •The Annuity Period, which begins on the Annuity Date and during which Annuity Payments are provided. |

Account Value | The total of the Fixed Account Value, the value of the Shield Option(s), and the Holding Account value under the Contract during the Accumulation Period. |

Shield Option | Each Shield Option has an associated Term, Index, Shield Rate and Rate Crediting Type. |

Term | The Term may be 1, 2, 3, or 6 years in length. |

Index | The current Indices are as follows: •S&P 500® Index (Price Return Index); •Russell 2000® Index (Price Return Index); •MSCI EAFE Index (Price Return Index); and •Nasdaq-100 Index® (Price Return Index). |

Shield Rate | We currently offer different levels of protection: Shield 10 — A Shield Rate where negative Index Performance of up to 10% of your Investment Amount is absorbed by us at the Term End Date, which would leave you to absorb any remaining negative Index Performance of up to 90% of your Investment Amount. Shield 15 — A Shield Rate where negative Index Performance of up to 15% of your Investment Amount is absorbed by us at the Term End Date, which would leave you to absorb any remaining negative Index Performance of up to 85% of your Investment Amount. Shield 25 — A Shield Rate where negative Index Performance of up to 25% of your Investment Amount is absorbed by us at the Term End Date, which would leave you to absorb any remaining negative Index Performance of up to 75% of your Investment Amount. |

Rate Crediting Type | A Shield Option can only have one associated Rate Crediting Type: Cap Rate, Step Rate, or Step Rate Edge. |

Performance Lock | For any Shield Option, once during each Term you may elect to lock the Interim Value. Once an Interim Value is locked it is irrevocable for the remainder of that Term. The Performance Lock Value will be used as value of the Shield Option for the remainder of the Term. You can exercise Performance Lock by providing Notice of election on a particular Business Day to lock the Interim Value on that day. (See “PERFORMANCE LOCK.”) |

Interim Value | The Interim Value is designed to represent the fair value of the Shield Option on each Business Day between the Term Start Date and Term End Date, taking into account the potential gain or loss of the applicable Index at the end of the Term. The Interim Value reflects the change in fair value due to economic factors of the investment instruments (including derivatives) supporting the Shield Options. The Interim Value is the amount that is available for annuitization, death benefits, withdrawals, Surrenders, and Performance Lock. For each Shield Option, we assign the value of Interim Value on any Business Day other than the Term Start Date and Term End Date. The Interim Value may be less than the Investment Amount at the time the Interim Value is calculated even when the current Index Value is higher than it was on the Term Start Date. See “Interim Value Calculation.” |

Transfers | During the Accumulation Period you may only make transfers to or from the Fixed Account, to or from the Shield Option(s), and from the Holding Account. If you have not exercised Performance Lock, you may make transfers only during the Transfer Period following the Term End Date. The effective date of such transfer is the first day of the Fixed Account Term and/or the Term(s) in which the transfer is made. If you have exercised Performance Lock, you may transfer on any Contract Anniversary prior to the end of the Term and on the Term End Date. You may only transfer the entire amount of your Performance Lock Value on a Contract Anniversary that is not a Term End Date. On the Term End Date, you have the Transfer Period to transfer all or a portion of your Performance Lock Value. Partial transfers of a Shield Option (with or without Performance Lock) are not permitted, except during the Transfer Period. See “TRANSFERS.” |

Fixed Account | See Appendix D. |

Access to Your Money | You may withdraw some or all of your money at any time prior to the Annuity Date. For any withdrawal taken on a Term End Date, a Performance Rate Adjustment, as of the date of the withdrawal, will apply. For any withdrawal taken between the Term Start Date and the Term End Date, we use an Interim Value calculation, which will reduce the Investment Amount for that Shield Option by the percentage reduction in the Interim Value of that Shield Option. If you have exercised Performance Lock, a withdrawal will reduce your Performance Lock Value by the dollar amount of the withdrawal. The Performance Rate Adjustment and reduction (either proportionate or dollar for dollar) may be substantial. In addition, a withdrawal taken in excess of the Free Withdrawal Amount may be subject to a Withdrawal Charge. |

Withdrawal Charge | A percentage charge applied to withdrawals in excess of the Free Withdrawal Amount.The Free Withdrawal Amount is 0% in the first Contract Year, and 10% of Account Value in each subsequent Contract Year to the extent that amount has not already been withdrawn that Contract Year.The Withdrawal Charge is calculated at the time of each withdrawal in accordance with the following: |

Number of Complete Contract Years since Issue Date | Withdrawal Charge percentage | |||

0 | 7% | |||

1 | 7% | |||

2 | 6% | |||

3 | 5% | |||

4 | 4% | |||

5 | 3% | |||

6 or more | 0% | |||

See “WITHDRAWAL PROVISIONS — When No Withdrawal Charge Applies” for a list of Withdrawal Charge waivers. | ||||

Systematic Withdrawal Program | You may elect the Systematic Withdrawal Program to provide automated processing of amounts withdrawn from your Contract, subject to program terms. We do not assess a charge for the program and you may terminate your participation in the program at any time. Withdrawals under the Systematic Withdrawal Program are subject to the same Withdrawal Charge provisions and risks as any other withdrawals under the Contract. Moreover, since withdrawal amounts from a Shield Option will reduce the Investment Amount for that Shield Option by the percentage reduction in the Interim Value of that Shield Option, a withdrawal when Interim Value is less than the Investment Amount will cause a greater percentage reduction in the Investment Amount that remains in your Shield Option relative to the percentage reduction for the same withdrawal amount when Interim Value is greater than the Investment Amount. If you exercise Performance Lock on any Shield Option, the Performance Lock Value for that Shield Option will be reduced by the dollar amount of any subsequent withdrawals. Since withdrawals under the Systematic Withdrawal Program are automatic, you will have no control over the timing of those withdrawals. See “WITHDRAWAL PROVISIONS – Systematic Withdrawal Program” for availability and other restrictions. |

Death Benefit | For Owners age 81 or older at the Issue Date of the Contract, the standard death benefit is the Account Value. For Owners age 80 or younger at the Issue Date of the Contract, the standard death benefit (known as the Return of Premium death benefit) is the greater of the Account Value or your Purchase Payment (reduced proportionally by the percentage reduction in Account Value of the Shield Option(s), the Fixed Account, and the Holding Account for each partial withdrawal (including any applicable Withdrawal Charge)). The Death Benefit Amount is determined as of the end of the Business Day on which we receive Notice of due proof of death and an acceptable election for the payment method. |

Annuity Options | You can choose an Annuity Option. After Annuity Payments begin, you cannot change the Annuity Option. You can choose one of the following Annuity Options on a fixed payment basis or any other Annuity Option acceptable to us: (i) Life Annuity with 10 Years of Annuity Payments Guaranteed; and (ii)Joint and Last Survivor Annuity with 10 Years of Annuity Payments Guaranteed. The Annuity Options may be limited due to the requirements of the Code. |

Charges and Expenses | You will bear the following charges and expenses: (i)Withdrawal Charges; and (ii)Premium Tax and other taxes. |

Your Right to Cancel | You may cancel the Contract within 10 days after receiving it by mailing or delivering the Contract to either us or the financial representative who sold it. This is known as a “Free Look.” You will receive (i) whatever your Contract is worth, plus (ii) the sum of all fees, taxes and charges deducted from the Purchase Payment during the Free Look period, as of the effective date of the Free Look, on the Business Day we receive your Contract and we will not deduct a Withdrawal Charge. The amount you receive may be more or less than your Purchase Payment depending on the Shield Options you allocated your Purchase Payment to during the Free Look period. |

SHIELD OPTIONS | |

TERM | INDEX |

SHIELD 25 (up to 25% downside protection) | |

1 Year | S&P 500® Index Russell 2000® Index MSCI EAFE Index Nasdaq-100 Index® |

6 Year | S&P 500® Index Russell 2000® Index MSCI EAFE Index Nasdaq-100 Index® |

SHIELD 15 (up to 15% downside protection) | |

1 Year | S&P 500® Index S&P 500® Index Step Rate S&P 500® Index Step Rate Edge Russell 2000® Index Russell 2000® Index Step Rate Russell 2000® Index Step Rate Edge MSCI EAFE Index MSCI EAFE Index Step Rate MSCI EAFE Index Step Rate Edge Nasdaq-100 Index® Nasdaq-100 Index® Step Rate Nasdaq-100 Index® Step Rate Edge |

2 Year | S&P 500® Index Step Rate S&P 500® Index Step Rate Edge Russell 2000® Index Step Rate Russell 2000® Index Step Rate Edge MSCI EAFE Index Step Rate MSCI EAFE Index Step Rate Edge Nasdaq-100 Index® Step Rate Nasdaq-100 Index® Step Rate Edge |

3 Year | S&P 500® Index Russell 2000® Index MSCI EAFE Index Nasdaq-100 Index® |

6 Year | S&P 500® Index Russell 2000® Index MSCI EAFE Index Nasdaq-100 Index® |

SHIELD 10 (up to 10% downside protection) | |

SHIELD OPTIONS | |

TERM | INDEX |

1 Year | S&P 500® Index S&P 500® Index Step Rate S&P 500® Index Step Rate Edge Russell 2000® Index Russell 2000® Index Step Rate Russell 2000® Index Step Rate Edge MSCI EAFE Index MSCI EAFE Index Step Rate MSCI EAFE Index Step Rate Edge Nasdaq-100 Index® Nasdaq-100 Index® Step Rate Nasdaq-100 Index® Step Rate Edge |

2 Year | S&P 500® Index Step Rate S&P 500® Index Step Rate Edge Russell 2000® Index Step Rate Russell 2000® Index Step Rate Edge MSCI EAFE Index Step Rate MSCI EAFE Index Step Rate Edge Nasdaq-100 Index® Step Rate Nasdaq-100 Index® Step Rate Edge |

3 Year | S&P 500® Index Russell 2000® Index MSCI EAFE Index Nasdaq-100 Index® |

6 Year | S&P 500® Index Russell 2000® Index MSCI EAFE Index Nasdaq-100 Index® |

Shield Rate | Downside Protection |

Shield 10 | up to 10% |

Shield 15 | up to 15% |

Shield 25 | up to 25% |

Minimum Guaranteed Cap Rates | |||

Shield Rate | 1-Year Term | 3-Year Term | 6-Year Term |

Shield 10 | 5% | 15% | 30% |

Shield 15 | 4.5% | 13.5% | 27% |

Shield 25 | 3.5% | N/A | 21% |

Minimum Guaranteed Step Rates | ||

Shield Rate | 1-Year Term | 2-Year Term |

Shield 10 | 5% | 10% |

Shield 15 | 4.5% | 9% |

Minimum Guaranteed Edge Rates | ||

Shield Rate | 1-Year Term | 2-Year Term |

Shield 10 | 5% | 10% |

Shield 15 | 4.5% | 9% |

Shield Option type: | If Index Performance is: | Performance Rate will equal: |

Shield Options with a Cap Rate | less than or equal to zero | the lesser of: zero or the Index Performance increased by the Shield Rate (For example: a -15% Index Performance with Shield 10 will result in a -5% Performance Rate. The Performance Rate can never be greater than zero if the Index Performance is negative.) |

greater than zero and less than the Cap Rate | the Index Performance | |

greater than zero and equals or exceeds the Cap Rate | the Cap Rate | |

Shield Options with a Step Rate | less than zero | the lesser of: zero or the Index Performance increased by the Shield Rate (For example: a -15% Index Performance with Shield 10 will result in a -5% Performance Rate. The Performance Rate can never be greater than zero if the Index Performance is negative.) |

equal to or greater than zero | the Step Rate | |

Shield Options with Step Rate Edge | less than zero and exceeds the Shield Rate | Index Performance increased by the Shield Rate (For example: a -15% Index Performance with Shield 10 will result in a -5% Performance Rate.) |

less than zero but does not exceed the Shield Rate | the Edge Rate | |

zero or positive | the Edge Rate |

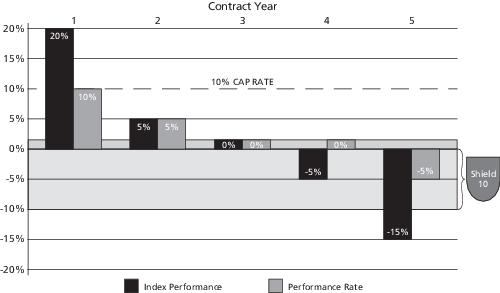

Contract Year | 1 | 2 | 3 | 4 | 5 |

Term Start Date | |||||

Investment Amount(1) | $50,000 | $55,000 | $57,750 | $57,750 | $57,750 |

Index Value | 1,000 | 1,200 | 1,260 | 1,260 | 1,197 |

Term End Date | |||||

Index Value | 1,200 | 1,260 | 1,260 | 1,197 | 1,017 |

Index Performance(2) | 20% | 5% | 0% | -5% | -15% |

Cap Rate | 10% | 10% | 10% | 10% | 10% |

Shield Rate | 10% | 10% | 10% | 10% | 10% |

Performance Rate (one year)(3) | 10% | 5% | 0% | 0% | -5% |

Performance Rate Adjustment(4) | $5,000 | $2,750 | $0 | $0 | -$2,888 |

Investment Amount(5) | $55,000 | $57,750 | $57,750 | $57,750 | $54,862 |

÷ 1,000 [Index Value at Term Start Date] = 20%

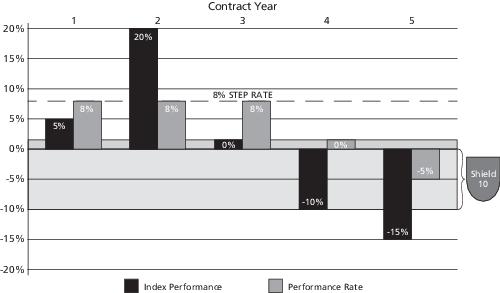

Contract Year | 1 | 2 | 3 | 4 | 5 |

Term Start Date | |||||

Investment Amount(1) | $50,000 | $54,000 | $58,320 | $62,986 | $62,986 |

Index Value | 1,000 | 1,050 | 1,260 | 1,260 | 1,134 |

Term End Date | |||||

Index Value | 1,050 | 1,260 | 1,260 | 1,134 | 964 |

Index Performance(2) | 5% | 20% | 0% | -10% | -15% |

Step Rate | 8% | 8% | 8% | 8% | 8% |

Shield Rate | 10% | 10% | 10% | 10% | 10% |

Performance Rate (one year)(3) | 8% | 8% | 8% | 0% | -5% |

Performance Rate Adjustment(4) | $4,000 | $4,320 | $4,666 | $0 | -$3,149 |

Investment Amount(5) | $54,000 | $58,320 | $62,986 | $62,986 | $59,837 |

÷ 1,000 [Index Value at Term Start Date]) = 5%

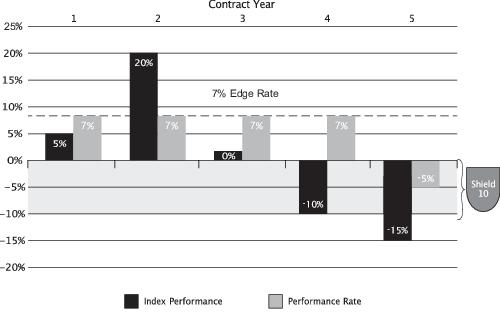

Contract Year | 1 | 2 | 3 | 4 | 5 |

Term Start Date | |||||

Investment Amount(1) | $50,000 | $53,500 | $57,245 | $61,252 | $65,540 |

Index Value | 1,000 | 1,050 | 1,260 | 1,260 | 1,134 |

Term End Date | |||||

Index Value | 1,050 | 1,260 | 1,260 | 1,134 | 964 |

Index Performance(2) | 5% | 20% | 0% | -10% | -15% |

Edge Rate | 7% | 7% | 7% | 7% | 7% |

Shield Rate | 10% | 10% | 10% | 10% | 10% |

Performance Rate (one year)(3) | 7% | 7% | 7% | 7% | -5% |

Performance Rate Adjustment(4) | $3,500 | $3,745 | $4,007 | $4,288 | -$3,277 |

Investment Amount(5) | $53,500 | $57,245 | $61,252 | $65,540 | $62,263 |

÷ 1,000 [Index Value at Term Start Date]) = 5%

Purchase Payment: $200,000.00

Allocated to:

Step Rate Edge | Step Rate | Cap Rate | Cap Rate | |

Term (in months) | 12 | 24 | 36 | 72 |

Months elapsed since Term Start Date | 0 | 0 | 0 | 0 |

Investment Amount | $50,000 | $50,000 | $50,000 | $50,000 |

Shield Rate | 10% | 15% | 10% | 25% |

Shield Option Rate | 8.25% | 18% | 130% | 200% |

Months until Term End Date | 12 | 24 | 36 | 72 |

Market Value Rate on Term Start Date | 2.00% | 4.00% | 6.00% | 8.00% |

Starting Index Value | 1,000 | |||

Total Account Value | $200,000 | |||

Step Rate Edge | Step Rate | Cap Rate | Cap Rate | |

Months elapsed since Term Start Date | 6 | |||

Months until Term End Date | 6 | 18 | 30 | 66 |

Index Value | 1200 | |||

Index Performance on calculation date(1) | 20% | |||

Market Value Rate on calculation date | 3.00% | 5.00% | 7.00% | 9.00% |

Market value of the Fixed Income Asset Proxy | $48,823.16 | $46,519.03 | $42,116.56 | $34,758.31 |

Market value of the Derivative Asset Proxy | $3,848.51 | $6,526.00 | $16,069.42 | $21,946.25 |

Interim Value of each Shield Option(2) | $52,671.67 | $53,045.03 | $58,185.98 | $56,704.57 |

Total Account Value | $220,607.25 | |||

Step Rate Edge | Step Rate | Cap Rate | Cap Rate | |

Months elapsed since Term Start Date | 6 | |||

Months until Term End Date | 6 | 18 | 30 | 66 |

Index Value | 700 | |||

Index Performance on calculation date(1) | -30% | |||

Market Value Rate on calculation date | 3.00% | 5.00% | 7.00% | 9.00% |

Market value of the Fixed Income Asset Proxy | $48,823.16 | $46,519.03 | $42,116.56 | $34,758.31 |

Market value of the Derivative Asset Proxy | -$8,899.83 | -$5,554.28 | -$5,794.44 | $2,103.07 |

Interim Value of each Shield Option(2) | $39,923.32 | $40,964.75 | $36,322.12 | $36,861.38 |

Total Account Value | $154,071.57 | |||

÷ 1000 [Index Value at Term Start Date] = 20%

÷ 1000 [Index Value at Term Start Date] = -30%

Number of Complete Contract Years since Issue Date | Withdrawal Charge percentage |

0 | 7% |

1 | 7% |

2 | 6% |

3 | 5% |

4 | 4% |

5 | 3% |

6 or more | 0% |

Term Start Date | |

Investment Amount | $50,000 |

Shield Rate | Shield 10 |

Cap Rate | 10% |

Index Value | 500 |

Interim Value Calculation Halfway Through Term | |

Index Value | 600 |

Index Performance(1) | 20% |

Time Remaining in Shield Option (in months) | 6 |

Market Value Rate on calculation date | 3% |

Market value of Fixed Income Asset Proxy | $49,452.40 |

Market value of Derivative Asset Proxy | $4,062.37 |

Interim Value of Shield Option(2) | $53,514.77 |

Withdrawal Amount taken | $20,000 |

Investment Amount at Term Start Date adjusted for any withdrawals(3) | $31,313.57 |

Net Proceeds from withdrawal paid to Contract Owner(4) | $20,000 |

Term End Date | |

Index Value | 560 |

Index Performance(5) | 12% |

Performance Rate(6) | 10% |

Performance Rate Adjustment(7) | $3,131.36 |

Investment Amount(8) | $34,444.93 |

÷ 500 [Index Value at Term Start Date]) = 20%

= $53,514.77

x (1-$20,000 [gross withdrawal amount halfway through the Term] ÷ $53,514.77 [Interim Value on date of withdrawal])

= $31,313.57

÷ 500 [Index Value at Term Start Date] = 12%

+ $3,131.36 [Performance Rate Adjustment at Term End Date] = $34,444.93

Term Start Date | |

Investment Amount | $50,000 |

Shield Rate | Shield 10 |

Cap Rate | 10% |

Index Value | 500 |

Interim Value Calculation Halfway Through Term | |

Index Value | 400 |

Index Performance(1) | –20% |

Time Remaining in Shield Option (in months) | 6 |

Market Value Rate on calculation date | 3% |

Market value of Fixed Income Asset Proxy | $49,452.40 |

Market value of Derivative Asset Proxy | –$4,661.31 |

Interim Value of Shield Option(2) | $44,791.09 |

Withdrawal Amount taken | $20,000 |

Investment Amount adjusted for any withdrawals(3) | $27,674.13 |

Free Withdrawal Amount(4) | $5,000 |

Withdrawal Charge Amount(5) | $1,050 |

Net Proceeds from Withdrawal paid to Contract Owner(6) | $18,950 |

Term End Date | |

Index Value | 450 |

Index Performance(7) | –10% |

Performance Rate(8) | 0% |

Performance Rate Adjustment(9) | $0 |

Investment Amount(10) | $27,674.13 |

÷ 500 [Index Value at Term Start Date]) = –20%

= $44,791.09

x (1-$20,000 [gross withdrawal amount halfway through the Term]) ÷ $44,791.09 [Interim Value on date of withdrawal]

= $27,674.13

÷ 500 [Index Value at Term Start Date] = –10%

+ $0 [Performance Rate Adjustment at Term End Date] = $27,674.13

Contract Year | 1 |

Term Start Date | |

Investment Amount | $50,000 |

Index Value | 1,000 |

Term End Date | |

Index Value | 1,200 |

Index Performance(1) | 20% |

Cap Rate | 10% |

Shield Rate | Shield 10 |

Performance Rate (one year)(2) | 10% |

Performance Rate Adjustment(3) | $5,000 |

Investment Amount(4) | $55,000 |

÷ 1,000 [Index Value at Term Start Date]) = 20%

Contract Year | 2 | |

1-Year Term / Shield 10 / S&P 500® Index with a Cap Rate of 10% | 1-Year Term / Shield 10 / Russell 2000® Index with a Cap Rate of 12% | |

Investment Amount at Term Start Date (second term)(1) | $27,500 | $27,500 |

Term Start Date | |

Investment Amount | $100,000 |

Shield Rate | Shield 10 |

Cap Rate | 10% |

Index Value | 1,000 |

Interim Value Calculation Halfway Through Term | |

Index Value | 1,200 |

Index Performance(1) | 20% |

Time Remaining in Shield Option (in months) | 6 |

Market Value Rate on calculation date | 3% |

Market value of Fixed Income Asset Proxy | $98,904.80 |

Market value of Derivative Asset Proxy | $8,124.74 |

Interim Value of Shield Option(2) | $107,029.53 |

Performance Lock Value(3) | $107,029.53 |

÷ 1,000 [Index Value at Term Start Date] = 20%

= $107,029.53

Term Start Date | |

Investment Amount | $100,000 |

Shield Rate | Shield 10 |

Cap Rate | 10% |

Index Value | 1,000 |

Interim Value Calculation Halfway Through Term | |

Index Value | 1,200 |

Index Performance(1) | 20% |

Time Remaining in Shield Option (in months) | 6 |

Market Value Rate on calculation date | 3% |

Market value of Fixed Income Asset Proxy | $98,904.80 |

Market value of Derivative Asset Proxy | $8,124.74 |

Time Remaining in Shield Option (in months) | 6 |

Interim Value of Shield Option on day you exercise Performance Lock(2) | $107,029.53 |

Gross Withdrawal Amount | $50,000 |

Free Withdrawal Amount(3) | $10,000 |

Withdrawal Charge Amount(4) | $2,800 |

Net Proceeds from Withdrawal paid to Contract Owner(5) | $47,200 |

Performance Lock Value after Withdrawal(6) | $57,029.53 |

÷ 1,000 [Index Value at Term Start Date] = 20%

= $107,029.53

= $57,029.53 [Performance Lock Value after Withdrawal]

If you… | Your “Applicable Age” is… |

Were born on or before June 30, 1949 | 70½ |

Were born on or after July 1, 1949 (and attain age 72 prior to January 1, 2023) | 72 |

Attain age 72 on or after January 1, 2023 (and attain age 73 on or before December 31, 2032) | 73* |

Attain age 74 on or after January 1, 2033 | 75* |

Plan Type | Elective Contribution | Catch-up Contribution |

IRA | $7,000 | $1,000 |

SIMPLE IRA | $16,000 | $3,500 |

401(k) | $23,000 | $7,500 |

SEP/401(a) | (Employer contributions only) | |

403(b) [TSA] | $23,000 | $7,500 |

457(b) | $23,000 | $7,500 |

Applications when purchasing the Contract, including initial Purchase Payment | P.O. Box 4365 Clinton, IA 52733-4365 Fax: (877) 245-2964 Or through your financial representative |

Death Claims | P.O. Box 4330 Clinton, IA 52733-4330 Fax: (877) 245-8163 |

Annuity Payments |

•Requests to receive regular Annuity Payments | P.O. Box 4365 Clinton, IA 52733-4365 Telephone: (800) 882-1292 Fax: (877) 246-8424 |

•Death Claims for Contracts receiving Annuity Payments | P.O. Box 4364 Clinton, IA 52733-4364 Telephone: (800) 882-1292 Fax: (877) 245-8163 |

•General requests and elections for Contracts receiving Annuity Payments | P.O. Box 4363 Clinton, IA 52733-4363 Telephone: (800) 882-1292 Fax: (877) 246-8424 |

All other requests and elections and general inquiries (except requests for a transaction or other notification related to the Performance Lock must be submitted in writing, by telephone or by fax) | P.O. Box 4301 Clinton, IA 52733-4301 Telephone: (888) 243-1932 Fax: (877) 246-8424 |

FOR SECURITIES ACT LIABILITIES

Name | Position with Brighthouse Life Insurance Company of NY |

David A. Rosenbaum | Director, Chairman of the Board, President and Chief Executive Officer (Principal Executive Officer) (March 24, 2022 - present) |

Kristine H. Toscano | Vice President and Chief Financial Officer (Principal Financial Officer and Principal Accounting Officer) (September 2021 - present) |

Michael J. Inserra | Director (October 12, 2021 - present) |

Edward C. Kosnik | Director (June 6, 2023 - present) |

Mayer Naiman | Director (October 26, 2017 - present) |

Douglas A. Rayvid | Director (September 12, 2019 - present) |

Robert A. Semke | Director (September 21, 2023 - present) |

Kevin D. White | Director (December 8, 2023 - present) |

2023 Director Compensation Table | ||

Name | Fees Earned or Paid in Cash (1) | Total |

David W. Chamberlin (2) | — | — |

Jeffrey P. Halperin (3) | — | — |

Michael J. Inserra | $30,000 | $30,000 |

Edward C. Kosnik | — | — |

Mayer Naiman | — | — |

Richard C. Pearson (4) | $30,000 | $30,000 |

Douglas A. Rayvid (5) | $35,000 | $35,000 |

David A. Rosenbaum | — | — |

2023 Director Compensation Table | ||

Name | Fees Earned or Paid in Cash (1) | Total |

Robert A. Semke (6) | $15,000 | $15,000 |

Kevin D. White | — | — |

Three Months Ended March 31, (unaudited) | Years Ended December 31, | |||||||

2024 | 2023 | 2023 | 2022 | |||||

INCOME | ||||||||

Premiums and annuity considerations | $28 | $190 | $(3,649 ) | $935 | ||||

Considerations for supplementary contracts | 2 | 2 | 12 | 7 | ||||

Net investment income | 23 | (9 ) | (6 ) | 33 | ||||

Reserves adjustments on reinsurance ceded | 232 | (76 ) | 4,039 | (291 ) | ||||

Other income (loss) | (222 ) | (125 ) | (319 ) | 799 | ||||

Total income | 63 | (18 ) | 77 | 1,483 | ||||

BENEFITS AND EXPENSES | ||||||||

Benefit payments | 64 | 92 | 399 | 222 | ||||

Changes to reserves, deposit funds and other policy liabilities | (28 ) | (34 ) | (732 ) | 253 | ||||

Insurance expenses and taxes (other than Federal income and capital gains taxes) | 34 | 32 | 133 | 142 | ||||

Net transfers to (from) Separate Accounts | 8 | 100 | 270 | 617 | ||||

Total benefits and expenses before dividends to policyholders | 78 | 190 | 70 | 1,234 | ||||

Gain (loss) from operations before dividends to policyholders and Federal income tax | (15 ) | (208 ) | 7 | 249 | ||||

Federal income tax expense (benefit) (excluding income tax on capital gains and losses) | — | (1 ) | 2 | 93 | ||||

Gain (loss) from operations | (15 ) | (207 ) | 5 | 156 | ||||

Net realized capital gains (losses), net of Federal income tax and interest maintenance reserve transfer | 1 | 93 | 534 | (308 ) | ||||

NET INCOME (LOSS) | (14 ) | (114 ) | 539 | (152 ) | ||||

CHANGES IN CAPITAL AND SURPLUS | ||||||||

Change in general account net unrealized capital gains (losses) | 26 | 81 | (154 ) | (56 ) | ||||

Change in net deferred income tax | 6 | 25 | (139 ) | 117 | ||||

Change in nonadmitted assets | (7 ) | (11 ) | 115 | (116 ) | ||||

Change in asset valuation reserve | (3 ) | 2 | — | (10 ) | ||||

Change in surplus as a result of reinsurance | (13 ) | (4 ) | 135 | (16 ) | ||||

Change in surplus adjustment paid in | — | 100 | 100 | 100 | ||||

Other - net | (1 ) | — | — | (1 ) | ||||

NET CHANGE IN CAPITAL AND SURPLUS | (6 ) | 79 | 596 | (134 ) | ||||

CAPITAL AND SURPLUS AT BEGINNING OF YEAR | 819 | 223 | 223 | 357 | ||||

CAPITAL AND SURPLUS AT END OF YEAR | $813 | $302 | $819 | $223 | ||||

December 31, 2023 | |||

Notional Amount | Estimated Fair Value (1) | 100 Basis Point Increase in the Yield Curve | |

(In millions) | |||

Financial assets with interest rate risk | |||

Fixed maturity securities | $4,948 | $(261 ) | |

Mortgage loans | $1,084 | (51 ) | |

Increase (decrease) in estimated fair value of assets | (312 ) | ||

Derivative instruments with interest rate risk | |||

Interest rate contracts | $800 | $1 | 10 |

Equity contracts | $874 | $117 | 9 |

Foreign currency contracts | $173 | $12 | (1 ) |

Increase (decrease) in estimated fair value of derivative instruments | 18 | ||

Net change | $(294 ) | ||

Independent Auditor’s Report |

Financial Statements at December 31, 2023 and 2022 and for the Years Ended December 31, 2023, 2022 and 2021: |

Statements of Admitted Assets, Liabilities and Capital and Surplus |

Statements of Operations and Changes in Capital and Surplus |

Statements of Cash Flows |

Notes to the Financial Statements |

Note 1 — Business, Basis of Presentation and Summary of Significant Accounting Policies |

Note 2 — Fair Value Information |

Note 3 — Investments |

Note 4 — Related Party Information |

Note 5 — Premium and Annuity Considerations Deferred and Uncollected |

Note 6 — Reinsurance and Other Insurance Transactions |

Note 7 — Reserves for Life Contracts and Deposit-Type Contracts |

Note 8 — Analysis of Actuarial Reserves and Deposit Liabilities by Withdrawal Characteristics |

Note 9 — Separate Accounts |

Note 10 — Federal Income Tax |

Note 11 — Borrowed Money |

Note 12 — Capital and Surplus |

Note 13 — Other Commitments and Contingencies |

Note 14 — Retained Assets |

Note 15 — Subsequent Events |

Financial Statement Schedules at December 31, 2023 and 2022 and for the Years Ended December 31, 2023, 2022 and 2021: |

Schedule I — Statutory Selected Financial Data |

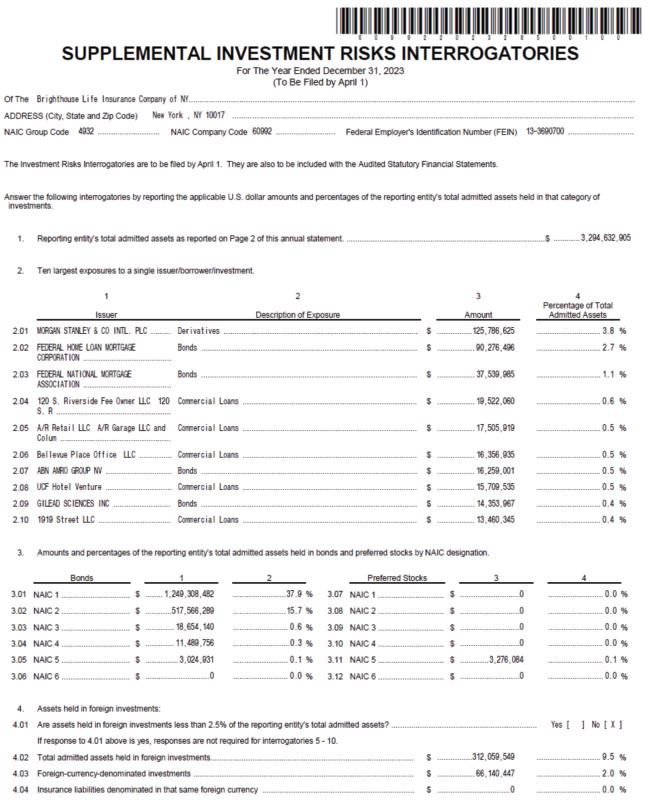

Schedule II — Supplemental Investment Risks Interrogatories |

Schedule III — Statutory Summary Investment Schedule |

Schedule IV — Reinsurance contracts with risk-limiting features |

Brighthouse Life Insurance Company of NY:

March 25, 2024

December 31, 2023 and 2022

2023 | 2022 | |

ADMITTED ASSETS | ||

Bonds | $1,796 | $1,722 |

Preferred stocks | 3 | 3 |

Mortgage loans | 228 | 242 |

Cash, cash equivalents and short-term investments | 242 | 317 |

Derivative assets | 137 | 369 |

Other invested assets | 51 | 124 |

Total invested assets | 2,457 | 2,777 |

Investment income due and accrued | 15 | 15 |

Premiums and annuity considerations deferred and uncollected | 2 | 2 |

Reinsurance recoverable | 778 | 75 |

Net deferred tax asset | 33 | 16 |

Other assets | 10 | 8 |

Total assets excluding Separate Accounts | 3,295 | 2,893 |

Separate Account assets | 8,852 | 7,997 |

Total Admitted Assets | $12,147 | $10,890 |

LIABILITIES AND CAPITAL AND SURPLUS | ||

Liabilities | ||

Reserves for life insurance and annuities | $931 | $1,681 |

Liability for deposit-type contracts | 14 | 14 |

Other policy liabilities | 634 | 96 |

Borrowed money (including interest thereon) | — | 126 |

Asset valuation reserve | 45 | 45 |

Derivative liabilities | 10 | 136 |

Payable for collateral under securities loaned and other transactions | 44 | 194 |

Net transfers to (from) Separate Accounts due and accrued | 141 | (32 ) |

Funds held under reinsurance treaties | 418 | 429 |

Other liabilities | 239 | 347 |

Total liabilities excluding Separate Accounts | 2,476 | 3,036 |

Separate Account liabilities | 8,852 | 7,631 |

Total Liabilities | 11,328 | 10,667 |

Capital and Surplus | ||

Capital stock (par value $10 per share, 200,000 shares authorized, issued and outstanding) | 2 | 2 |

Paid-in surplus | 670 | 570 |

Special surplus fund reserve | 9 | — |

Unassigned surplus (deficit) | 138 | (349 ) |

Total Capital and Surplus | 819 | 223 |

Total Liabilities and Capital and Surplus | $12,147 | $10,890 |

For the Years Ended December 31, 2023, 2022, and 2021

2023 | 2022 | 2021 | |

INCOME | |||

Premiums and annuity considerations | $(3,649 ) | $935 | $965 |

Considerations for supplementary contracts and dividend accumulations | 12 | 7 | 8 |

Net investment income | (6 ) | 33 | 73 |

Reserve adjustments on reinsurance ceded | 4,039 | (291 ) | (351 ) |

Other income (loss) | (319 ) | 799 | (108 ) |

Total income | 77 | 1,483 | 587 |

BENEFITS AND EXPENSES | |||

Benefit payments | 399 | 222 | 202 |

Changes to reserves, deposit funds and other policy liabilities | (732 ) | 253 | (45 ) |

Insurance expenses and taxes (other than Federal income and capital gains taxes) | 133 | 142 | 150 |

Net transfers to (from) Separate Accounts | 270 | 617 | 612 |

Total benefits and expenses before Federal income tax | 70 | 1,234 | 919 |

Gain (loss) from operations before Federal income tax | 7 | 249 | (332 ) |

Federal income tax expense (benefit) (excluding income tax on capital gains and losses) | 2 | 93 | 28 |

Gain (loss) from operations | 5 | 156 | (360 ) |

Net realized capital gains (losses), net of Federal income tax and interest maintenance reserve transfer | 534 | (308 ) | 308 |

NET INCOME (LOSS) | 539 | (152 ) | (52 ) |

CHANGES IN CAPITAL AND SURPLUS | |||

Change in General Account net unrealized capital gains (losses) | (154 ) | (56 ) | 50 |

Change in net deferred income tax | (139 ) | 117 | 40 |

Change in nonadmitted assets | 115 | (116 ) | (27 ) |

Change in asset valuation reserve | — | (10 ) | (9 ) |

Change in surplus as a result of reinsurance | 135 | (16 ) | (16 ) |

Change in surplus adjustment paid in | 100 | 100 | — |

Other – net | — | (1 ) | (2 ) |

NET CHANGE IN CAPITAL AND SURPLUS | 596 | (134 ) | (16 ) |

CAPITAL AND SURPLUS AT BEGINNING OF YEAR | 223 | 357 | 373 |

CAPITAL AND SURPLUS AT END OF YEAR | $819 | $223 | $357 |

(In millions)

2023 | 2022 | 2021 | |

CASH FROM OPERATIONS | |||

Premiums and annuity considerations, net of reinsurance, received | $(3,126 ) | $906 | $979 |

Net investment income received | (8 ) | 57 | 50 |

Other income (loss) received | (129 ) | 193 | 146 |

Total receipts | (3,263 ) | 1,156 | 1,175 |

Benefits paid (other than dividends) | (3,654 ) | 530 | 534 |

Insurance expenses and taxes paid (other than Federal income and capital gains taxes) | 361 | 158 | 166 |

Net transfers to (from) Separate Accounts | 267 | 755 | 705 |

Federal income tax paid (recovered) (net of tax on capital gains and losses) | 95 | 33 | (5 ) |

Total payments | (2,931 ) | 1,476 | 1,400 |

Net cash provided by (used in) operations | (332 ) | (320 ) | (225 ) |

CASH FROM INVESTMENTS | |||

Proceeds from invested assets sold, matured or repaid | 607 | 493 | 788 |

Cost of invested assets acquired | (267 ) | (802 ) | (399 ) |

Net cash provided by (used in) investments | 340 | (309 ) | 389 |

CASH FROM FINANCING AND OTHER SOURCES | |||

Net change in surplus adjustment | — | 100 | — |

Borrowed Money | (125 ) | 125 | — |

Net change in deposit-type contracts | — | (1 ) | (2 ) |

Other-net | 42 | 303 | 37 |

Net cash provided by (used in) financing and other sources | (83 ) | 527 | 35 |

NET CHANGE IN CASH, CASH EQUIVALENTS AND SHORT-TERM INVESTMENTS: | (75 ) | (102 ) | 199 |

CASH, CASH EQUIVALENTS AND SHORT-TERM INVESTMENTS: | |||

BEGINNING OF YEAR | 317 | 419 | 220 |

END OF YEAR | $242 | $317 | $419 |

SUPPLEMENTAL DISCLOSURES OF CASH FLOW INFORMATION FOR NON-CASH TRANSACTIONS: | |||

Bonds, asset in kind transfer in | $100 | $— | $— |

Transfer of assets from mortgages to other invested assets | $— | $6 | $— |

Prior period adjustment-valuation system conversion | $— | $— | $2 |

For the Years Ended December 31, | ||||

SSAP Number(1) | 2023 | 2022 | 2021 | |

Net income (loss), NY SAP | $539 | $(152 ) | $(52 ) | |

State prescribed practices: | ||||

Deferred annuities using continuous CARVM | 51 | — | — | — |

Variable annuities in excess of NY Reg 213 standard scenario over VM 21 stochastic reserves | 51 | 4 | (143 ) | 143 |

NYSDFS Circular Letter No. 11 (2010) impact on deferred premiums | 61 | (2 ) | — | — |

NYSDFS Seventh Amendment to Regulation No. 172 impact on admitted unearned reinsurance premium | 61 | 10 | — | — |

State permitted practices: NONE | — | — | — | |

Net income, NAIC SAP | $551 | $ (295 ) | $91 | |

December 31, | ||||

SSAP Number | 2023 | 2022 | 2021 | |

Statutory capital and surplus, NY SAP | $819 | $223 | $357 | |

State prescribed practices: | ||||

Deferred annuities using continuous CARVM | 51 | 1 | — | 1 |

Variable annuities in excess of NY Reg 213 standard scenario over VM 21 stochastic reserves | 51 | 3 | — | 143 |

NYSDFS Circular Letter No. 11 (2010) impact on deferred premiums | 61 | (2 ) | — | — |

NYSDFS Seventh Amendment to Regulation No. 172 impact on admitted unearned reinsurance premium | 61 | 9 | (1 ) | (1 ) |

State permitted practices: NONE | — | — | — | |

Statutory capital and surplus, NAIC SAP | $830 | $222 | $500 | |

2023 | |||||

Aggregate Fair Value | Admitted Value | Level 1 | Level 2 | Level 3 | |

Assets | |||||

Bonds | $1,645 | $1,796 | $116 | $1,528 | $1 |

Preferred stocks | 3 | 3 | — | — | 3 |

Mortgage loans | 210 | 228 | — | — | 210 |

Cash, cash equivalents and short-term investments | 242 | 242 | 242 | — | — |

Derivative assets (1) | 140 | 137 | — | 140 | — |

Other invested assets | 15 | 19 | — | 15 | — |

Investment income due and accrued | 15 | 15 | — | 15 | — |

Separate Account assets | 8,429 | 8,808 | 148 | 7,375 | 906 |

Total assets | $10,699 | $11,248 | $506 | $9,073 | $1,120 |

Liabilities | |||||

Investment contracts included in: | |||||

Liability for deposit-type contracts | $14 | $14 | $— | $— | $14 |

Derivative liabilities (1) | 10 | 10 | — | 10 | — |

Borrowed Money (including interest thereon) | — | — | — | — | — |

Payable for collateral received | 44 | 44 | — | 44 | — |

Separate Account liabilities | 2 | 2 | — | 2 | — |

Total liabilities | $70 | $70 | $— | $56 | $14 |

2022 | |||||

Aggregate Fair Value | Admitted Value | Level 1 | Level 2 | Level 3 | |

Assets | |||||

Bonds | $1,520 | $1,722 | $114 | $1,403 | $3 |

Preferred stocks | 3 | 3 | — | — | 3 |

Mortgage loans | 222 | 242 | — | — | 222 |

Cash, cash equivalents and short-term investments | 317 | 317 | 317 | — | — |

Derivative assets (1) | 373 | 369 | — | 373 | — |

Other invested assets | 15 | 20 | — | 15 | — |

Investment income due and accrued | 15 | 15 | — | 15 | — |

Separate Account assets | 7,492 | 7,971 | 258 | 6,341 | 893 |

Total assets | $9,957 | $10,659 | $689 | $8,147 | $1,121 |

Liabilities | |||||

Investment contracts included in: | |||||

Liability for deposit-type contracts | $14 | $14 | $— | $— | $14 |

Derivative liabilities (1) | 136 | 136 | — | 136 | — |

Borrowed Money (including interest thereon) | 126 | 126 | — | 126 | — |

Payable for collateral received | 194 | 194 | — | 194 | — |

Separate Account liabilities | — | — | — | — | — |

Total liabilities | $470 | $470 | $— | $456 | $14 |

2023 | ||||

Fair Value Measurements at Reporting Date Using | ||||

Level 1 | Level 2 | Level 3 | Total | |

Assets | ||||

Derivative assets (1) | ||||

Interest rate | $— | $1 | $— | $1 |

Foreign currency exchange rate | — | 3 | — | 3 |

Equity market | — | 126 | — | 126 |

Total Derivative assets | — | 130 | — | 130 |

Separate Account assets (2) | — | 4,126 | — | 4,126 |

Total assets | $— | $4,256 | $— | $4,256 |

Liabilities | ||||

Derivative liabilities (1) | ||||

Interest rate | $— | $— | $— | $— |

Foreign currency exchange rate | — | — | — | — |

Equity market | — | 10 | — | 10 |

Total liabilities | $— | $10 | $— | $10 |

2022 | ||||

Fair Value Measurements at Reporting Date Using | ||||

Level 1 | Level 2 | Level 3 | Total | |

Assets | ||||

Derivative assets (1) | ||||

Interest rate | $— | $12 | $— | $12 |

Foreign currency exchange rate | — | 4 | — | 4 |

Equity market | — | 343 | — | 343 |

Total Derivative assets | — | 359 | — | 359 |

Separate Account assets (2) | — | 3,922 | — | 3,922 |

Total assets | $— | $4,281 | $— | $4,281 |

Liabilities | ||||

Derivative liabilities (1) | ||||

Interest rate | $— | $— | $— | $— |

Foreign currency exchange rate | — | — | — | — |

Equity market | — | 136 | — | 136 |

Total liabilities | $— | $136 | $— | $136 |

2023 | 2022 | |||||||

Book/ Adjusted | Gross Unrealized | Estimated | Book/ Adjusted | Gross Unrealized | Estimated | |||

Carrying Value | Gains | Losses | Fair Value | Carrying Value | Gains | Losses | Fair Value | |

Bonds | ||||||||

U.S. corporate | $942 | $5 | $100 | $847 | $914 | $1 | $130 | $785 |

RMBS | 195 | 3 | 10 | 188 | 148 | 2 | 10 | 140 |

Foreign corporate | 189 | 1 | 14 | 176 | 188 | — | 19 | 169 |

U.S. government and agency | 176 | — | 10 | 166 | 174 | — | 12 | 162 |

CMBS | 158 | — | 16 | 142 | 168 | — | 18 | 150 |

State and political subdivision | 90 | 2 | 9 | 83 | 83 | 1 | 12 | 72 |

ABS | 40 | — | 2 | 38 | 41 | — | 4 | 37 |

Foreign government | 6 | — | 1 | 5 | 6 | — | 1 | 5 |

Total bonds | $1,796 | $11 | $162 | $1,645 | $1,722 | $4 | $206 | $1,520 |

Preferred Stocks | ||||||||

Preferred | $3 | $— | $— | $3 | $3 | $— | $— | $3 |

Book/Adjusted Carrying Value | Estimated Fair Value | |

Due in one year or less | $28 | $27 |

Due after one year through five years | 406 | 394 |

Due after five years through ten years | 254 | 239 |

Due after ten years | 715 | 617 |

Subtotal | 1,403 | 1,277 |

Loan-backed securities | 393 | 368 |

Total | $1,796 | $1,645 |

2023 | 2022 | |||||||

Less than 12 Months | Equal to or Greater than 12 Months | Less than 12 Months | Equal to or Greater than 12 Months | |||||

Estimated Fair Value | Gross Unrealized Losses | Estimated Fair Value | Gross Unrealized Losses | Estimated Fair Value | Gross Unrealized Losses | Estimated Fair Value | Gross Unrealized Losses | |

U.S. corporate | $16 | $1 | $724 | $99 | $704 | $105 | $63 | $25 |

RMBS | 33 | 1 | 77 | 9 | 95 | 7 | 15 | 3 |

Foreign corporate | 1 | — | 146 | 14 | 153 | 18 | 4 | 1 |

U.S. government and agency | 31 | 1 | 121 | 9 | 149 | 12 | — | — |

CMBS | — | — | 140 | 16 | 132 | 14 | 18 | 4 |

State and political subdivision | 1 | — | 53 | 9 | 50 | 11 | 2 | 1 |

ABS | 3 | — | 32 | 2 | 29 | 3 | 8 | 1 |

Foreign government | — | — | 5 | 1 | 5 | 1 | — | — |

Total bonds | $85 | $3 | $1,298 | $159 | $1,317 | $171 | $110 | $35 |

Total number of bonds in an unrealized loss position | 29 | 549 | 538 | 90 | ||||

CUSIP | Book/Adjusted Carrying Value Amortized Cost Before Current Period OTTI | Present Value of Projected Cash Flows | Recognized OTTI | Amortized Cost after OTTI | Estimated Fair Value at Time of OTTI | Date of Financial Statement Where Reported |

12648WAE2 | $2,543,559 | $1,939,162 | $604,397 | $1,939,162 | $1,623,877 | 9/30/2023 |

23332UEL4 | $119,098 | $118,692 | 405 | $118,692 | $104,473 | 9/30/2023 |

Total | $604,802 |

2023 | 2022 | |||

Amount | Percent | Amount | Percent | |

Commercial | $182 | 80 % | $194 | 80 % |

Agricultural | 46 | 20 | 49 | 20 |

Total mortgage loans | $228 | 100 % | $243 | 100 % |

State | Percent of Total Mortgage Loans |

California | 21 % |

Florida | 14 |

New York | 12 |

Illinois | 10 |

Washington | 9 |

Colorado | 7 |

Total | 73 % |

2023 | |||||

Recorded Investment | |||||

Debt Service Coverage Ratios | |||||

˃ 1.20x | 1.00x - 1.20x | ˂ 1.00x | Total | % of Total | |

Loan-to-value ratios: | |||||

Less than 65% | $84 | $12 | $— | $96 | 52 % |

65% to 75% | 43 | — | 9 | 52 | 29 |

76% to 80% | 29 | — | — | 29 | 16 |

Greater than 80% | 2 | — | 3 | 5 | 3 |

Total | $158 | $12 | $12 | $182 | 100 % |

2022 | |||||

Recorded Investment | |||||

Debt Service Coverage Ratios | |||||

˃ 1.20x | 1.00x - 1.20x | ˂ 1.00x | Total | % of Total | |

Loan-to-value ratios: | |||||

Less than 65% | $136 | $— | $— | $136 | 70 % |

65% to 75% | 42 | — | 12 | 54 | 28 |

76% to 80% | — | — | — | — | — |

Greater than 80% | — | 1 | 3 | 4 | 2 |

Total | $178 | $1 | $15 | $194 | 100 % |

2023 | 2022 | |||||

Total Pledged & Restricted Assets | % of Total Assets | % of Total Admitted Assets | Total Pledged & Restricted Assets | % of Total Assets | % of Total Admitted Assets | |

State deposits | $1 | 0.0 % | 0.0 % | $1 | 0.0 % | 0.0 % |

Derivatives collateral(1) | 1 | 0.0 | 0.0 | 282 | 2.5 | 2.6 |

Total | $2 | 0.0 % | 0.0 % | $283 | 2.5 % | 2.6 % |

2023 | 2022 | ||||||

Primary Underlying Risk Exposure | Instrument Type | Notional Amount | Book/ Adjusted Carrying Value | Estimated Fair Value | Notional Amount | Book/ Adjusted Carrying Value | Estimated Fair Value |

Foreign currency exchange rate | Foreign currency swaps | $93 | $10 | $13 | $100 | $14 | $18 |

Interest rate | Interest rate caps | 800 | 1 | 1 | 800 | 12 | 12 |

Equity market | Equity index options | 874 | 116 | 116 | 2,761 | 182 | 182 |

Total rate of return swaps | — | — | — | 2,392 | 25 | 25 | |

Total | $1,767 | $127 | $130 | $6,053 | $233 | $237 | |

Asset | Liability | |||

2023 | 2022 | 2023 | 2022 | |

Foreign currency swaps | $52 | $55 | $— | $— |

Securities(1) | ||

2023 | 2022 | |

Initial Margin: | ||

OTC-bilateral | $— | $225 |

Variation Margin: | ||

OTC-bilateral | 1 | 57 |

Total OTC | $1 | $282 |

Cash(1) | Securities(2) | Total | ||||

2023 | 2022 | 2023 | 2022 | 2023 | 2022 | |

Initial Margin: | ||||||

OTC-bilateral | $— | $— | $1 | $151 | $1 | $151 |

Variation Margin: | ||||||

OTC-bilateral | 44 | 194 | 2 | 6 | 46 | 200 |

Total OTC | $44 | $194 | $3 | $157 | $47 | $351 |

Fiscal Year | Net Undiscounted Future Settled Premium Payments (Receipts) |

2024 | $11 |

2025 | 20 |

2026 | 23 |

2027 | 14 |

Thereafter | 32 |

Total | $100 |

2023 | 2022 | |

Net undiscounted future premium payments (receipts) | $100 | $92 |

Estimated fair value of derivative net assets (liabilities), including discounted future premiums | $26 | $164 |

Estimated fair value of derivative net assets (liabilities), excluding discounted future premiums | $116 | $247 |

2023 | 2022 | 2021 | |

Bonds | $69 | $65 | $69 |

Mortgage loans | 9 | 10 | 12 |

Cash and cash equivalents | 22 | 5 | — |

Derivatives | (89 ) | (37 ) | (4 ) |

Other invested assets | 4 | 1 | 1 |

Gross investment income | 15 | 44 | 78 |

Less: investment expenses | 21 | 12 | 6 |

Net investment income, before IMR amortization | (6 ) | 32 | 72 |

IMR amortization | — | 1 | 1 |

Net investment income | $(6 ) | $33 | $73 |

2023 | 2022 | 2021 | |

Bonds | $(3 ) | $(2 ) | $1 |

Derivatives | 534 | (309 ) | 308 |

Other | — | (1 ) | — |

Net realized capital gains (losses), before Federal income tax | 531 | (312 ) | 309 |

Less: Federal income tax expense (benefit) | (1 ) | (2 ) | — |

Net realized capital gains (losses), before IMR transfer | 532 | (310 ) | 309 |

IMR transfer, net of Federal income tax expense (benefit) of less than $1 million, $1 million and less than $(1) million, respectively | (2 ) | (2 ) | 1 |

Net realized capital gains (losses), net of Federal income tax and IMR transfer | $534 | $(308 ) | $308 |

2023 | 2022 | 2021 | |

Proceeds from sales and disposals | $90 | $418 | $141 |

Gross realized capital gains on sales | $— | $7 | $2 |

Gross realized capital losses on sales | $(2 ) | (9 ) | $(1 ) |

OTTI losses - bonds | $(1 ) | $— | $— |

2023 | 2022 | 2021 | |

Number of CUSIPs | 2 | 9 | 22 |

Aggregate Amount of Investment Income(1) | $— | $1 | $2 |

1 Gross | $15 |

2 Nonadmitted | — |

3 Admitted | $15 |

2023 | 2022 | 2021 | |

Premiums and annuity considerations | $(4,640 ) | $(172 ) | $(251 ) |

Reserve adjustments on reinsurance ceded | $4,039 | $(291 ) | $(351 ) |

Benefit payments | $(471 ) | $(337 ) | $(489 ) |

Changes to reserves, deposit funds and other policy liabilities | $(1,131 ) | $(366 ) | $29 |

2023 | 2022 | |

Reserves for life insurance, annuities and deposit-type contracts | $(2,133 ) | $(1,002 ) |

2023 | 2022 | |

Balance at beginning of year | $138 | $144 |

Capitalization of deferred gain on reinsurance | 160 | — |

Amortization of deferred gains on reinsurance | (15 ) | (6 ) |

Balance at end of year | $283 | $138 |

2023 | 2022 | 2021 | |

Reserves for life insurance, annuities and deposit-type contracts | $638 | $933 | $567 |

Premiums and annuity considerations | $83 | $126 | $206 |

Reserve adjustments on reinsurance ceded | $332 | $291 | $351 |

Benefit payments | $339 | $301 | $449 |

2023 | 2022 | 2021 | |

Reserves for life insurance, annuities and deposit-type contracts | $1,425 | $— | $— |

Premiums and annuity considerations | $4,511 | $— | $— |

Reserve adjustments on reinsurance ceded | $(4,371 ) | $— | $— |

Benefit payments | $100 | $— | $— |

2023 | 2022 | |||

Type | Gross | Net of Loading | Gross | Net of Loading |

Ordinary renewal | $2 | $2 | $2 | $2 |

2023 | 2022 | 2021 | |

Premiums and annuity considerations | $(4,636 ) | $(180 ) | $(265 ) |

Reserve adjustments on reinsurance ceded | $4,039 | $(291 ) | $(351 ) |

Benefit payments | $(482 ) | $(359 ) | $(491 ) |

Changes to reserves, deposit funds and other policy liabilities | $(1,100 ) | $(350 ) | $29 |

2023 | 2022 | |

Reserves for life insurance, annuities and deposit-type contracts | $(3,035 ) | $(1,920 ) |

Funds held under reinsurance treaties | $(418 ) | $(429 ) |

2023 | 2022 | |

Balance at beginning of year | $420 | $436 |

Capitalization of deferred gain on reinsurance | 160 | — |

Amortization of deferred gains on reinsurance | (26 ) | (16 ) |

Balance at end of year | $554 | $420 |

Ordinary | |||

Item | Total | Life Insurance | Individual Annuities |

Reg 213 Stocastic Excess over Standard | $667 | $— | $667 |

Miscellaneous Annuity Reserves | (210 ) | — | (210 ) |

Reinsurance ceded | (883 ) | — | (883 ) |

Total | $(426 ) | $— | $(426 ) |

Individual Annuities: | 2023 | ||||

General Account | Separate Account with Guarantees | Separate Account Nonguaranteed | Total | Percent of Total | |

Subject to discretionary withdrawal: | |||||

With market value adjustment | $339 | $— | $— | $339 | 3.4 % |

At book value less current surrender charge of 5% or more(1) | 153 | 2,702 | — | 2,855 | 28.3 % |

At fair value | — | — | 4,087 | 4,087 | 40.4 |

Total with market value adjustment or at fair value | 492 | 2,702 | 4,087 | 7,281 | 72.1 |

At book value without adjustment | 421 | 2,199 | — | 2,620 | 26.0 |

Not subject to discretionary withdrawal: | 193 | — | 3 | 196 | 1.9 |

Total (gross) | 1,106 | 4,901 | 4,090 | 10,097 | 100.0 % |

Reinsurance ceded | (318 ) | — | — | (318 ) | |

Total (net) | $788 | $4,901 | $4,090 | $9,779 | |

Individual Annuities: | 2022 | ||||

General Account | Separate Account with Guarantees | Separate Account Nonguaranteed | Total | Percent of Total | |

Subject to discretionary withdrawal: | |||||

With market value adjustment | $396 | $— | $— | $396 | 4.5 % |

At book value less current surrender charge of 5% or more | 183 | 2,279 | — | 2,462 | 28.1 |

At fair value | — | — | 3,884 | 3,884 | 44.4 |

Total with market value adjustment or at fair value | 579 | 2,279 | 3,884 | 6,742 | 77.0 |

At book value without adjustment | 438 | 1,399 | — | 1,837 | 21.0 |

Not subject to discretionary withdrawal: | 172 | — | 3 | 175 | 2.0 |

Total (gross) | 1,189 | 3,678 | 3,887 | 8,754 | 100.0 % |

Individual Annuities: | 2022 | ||||

General Account | Separate Account with Guarantees | Separate Account Nonguaranteed | Total | Percent of Total | |

Reinsurance ceded | (71 ) | — | — | (71 ) | |

Total (net) | $1,118 | $3,678 | $3,887 | $8,683 | |

Deposit-Type Contracts: | 2023 | ||||

General Account | Separate Account with Guarantees | Separate Account Nonguaranteed | Total | Percent of Total | |

Subject to discretionary withdrawal: | |||||

With market value adjustment | $— | $— | $— | $— | — % |

At book value less current surrender charge of 5% or more | — | — | — | — | — |

At fair value | — | — | — | — | — |

Total with market value adjustment or at fair value | — | — | — | — | — |

At book value without adjustment | 5 | — | — | 5 | 26.5 |

Not subject to discretionary withdrawal: | 14 | — | 1 | 15 | 73.5 |

Total (gross) | 19 | — | 1 | 20 | 100.0 % |

Reinsurance ceded | (5 ) | — | — | (5 ) | |

Total (net) | $14 | $— | $1 | $15 | |

Individual Annuities: | 2022 | ||||

General Account | Separate Account with Guarantees | Separate Account Nonguaranteed | Total | Percent of Total | |

Subject to discretionary withdrawal: | |||||

With market value adjustment | $— | $— | $— | $— | — % |

At book value less current surrender charge of 5% or more | — | — | — | — | — |

At fair value | — | — | — | — | — |

Total with market value adjustment or at fair value | — | — | — | — | — |

At book value without adjustment | 17 | — | — | 17 | 83.6 |

Not subject to discretionary withdrawal: | 3 | — | 1 | 4 | 16.4 |

Total (gross) | 20 | — | 1 | 21 | 100.0 % |

Reinsurance ceded | (6 ) | — | — | (6 ) | |

Total (net) | $14 | $— | $1 | $15 | |

2023 | 2022 | |

General Account: | ||

Annuities (excluding supplementary contracts with life contingencies) | $743 | $1,073 |

Supplementary contracts with life contingencies | 45 | 45 |

Deposit-type contracts | 14 | 14 |

Subtotal | 802 | 1,132 |

Separate Account: | ||

Annuities (excluding supplementary contracts) | 8,988 | 7,562 |

Supplementary contracts with life contingencies | 3 | 3 |

Other deposit-type contracts | 1 | 1 |

Total | $9,794 | $8,698 |

2023 | ||||||

General Account | Separate Account - Nonguaranteed | |||||

Account Value | Cash Value | Reserve | Account Value | Cash Value | Reserve | |

Subject to discretionary withdrawal: | ||||||

Term policies with cash value | $— | $— | $— | $— | $— | $— |

Universal life | 4 | 4 | 4 | — | — | — |

Universal life with secondary guarantees | — | — | 6 | — | — | — |

Indexed universal life | 3 | 3 | 5 | — | — | — |

Indexed universal life with secondary guarantees | — | — | — | — | — | — |

Indexed life | — | — | — | — | — | — |

Other permanent cash value life | — | 1 | 2 | — | — | — |

Variable life | — | — | — | — | — | — |

Variable universal life | — | — | — | — | — | — |

Miscellaneous reserves | — | — | — | — | — | — |

Not subject to discretionary withdrawal: | ||||||

Term policies without cash value | XXX | XXX | 1,064 | XXX | XXX | — |

Accidental death benefits | XXX | XXX | — | XXX | XXX | — |

Disability - active lives | XXX | XXX | 9 | XXX | XXX | — |

Disability - disabled lives | XXX | XXX | 6 | XXX | XXX | — |

Miscellaneous reserves | XXX | XXX | 1 | XXX | XXX | — |

Total (gross: direct + assumed) | 7 | 8 | 1,097 | — | — | — |

Reinsurance ceded | 4 | 4 | 965 | — | — | — |

Total (Net) | $3 | $4 | $132 | $— | $— | $— |

2022 | ||||||

General Account | Separate Account - Nonguaranteed | |||||

Account Value | Cash Value | Reserve | Account Value | Cash Value | Reserve | |

Subject to discretionary withdrawal: | ||||||

Term policies with cash value | $— | $— | $— | $— | $— | $— |

Universal life | 4 | 4 | 4 | — | — | — |

Universal life with secondary guarantees | 1 | 1 | 5 | — | — | — |

Indexed universal life | — | — | — | — | — | — |

Indexed universal life with secondary guarantees | — | — | — | — | — | — |

Indexed life | — | — | — | — | — | — |

Other permanent cash value life | — | — | 2 | — | — | — |

Variable life | — | — | — | — | — | — |

Variable universal life | — | — | — | — | — | — |

Miscellaneous reserves | — | — | — | — | — | — |

Not subject to discretionary withdrawal: | ||||||

Term policies without cash value | XXX | XXX | 1,079 | XXX | XXX | — |

Accidental death benefits | XXX | XXX | — | XXX | XXX | — |

Disability - active lives | XXX | XXX | 9 | XXX | XXX | — |

Disability - disabled lives | XXX | XXX | 5 | XXX | XXX | — |

Miscellaneous reserves | XXX | XXX | 1 | XXX | XXX | — |

Total (gross: direct + assumed) | 5 | 5 | 1,105 | — | — | — |

Reinsurance ceded | 4 | 4 | 979 | — | — | — |

Total (Net) | $1 | $1 | $126 | $— | $— | $— |

2023 | 2022 | |

General Account: | ||

Life insurance | $116 | $111 |

Accidental death benefits | — | — |

Active lives | 9 | 9 |

Disability - disabled lives | 6 | 5 |

Miscellaneous reserves | 1 | 1 |

Subtotal | 132 | 126 |

Separate Account: | ||

Life insurance | — | — |

Accident and health contracts | — | — |

Miscellaneous reserves | — | — |

Total | $132 | $126 |

Nonindexed Guarantee Less than/Equal to 4% | |||

2023 | 2022 | 2021 | |

Premiums, considerations or deposits | $815 | $917 | $939 |

Reserves at December 31 | |||

For accounts with assets at: | |||

Fair value | $— | $— | $— |

Amortized cost | 4,901 | 3,678 | 3,361 |

Total reserves | $4,901 | $3,678 | $3,361 |

By withdrawal characteristics: | |||

With market value adjustment | $— | $— | $— |

At book value without market value adjustment and with current surrender charge of 5% or more | 2,702 | 2,279 | 2,512 |

At fair value | — | — | — |

At book value without market value adjustment and with current surrender charge less than 5% | 2,199 | 1,399 | 849 |

Subtotal | 4,901 | 3,678 | 3,361 |

Not subject to discretionary withdrawal | — | — | — |

Total reserves | $4,901 | $3,678 | $3,361 |

Nonguaranteed Separate Accounts | |||

2023 | 2022 | 2021 | |

Premiums, considerations or deposits | $78 | $116 | $194 |

Reserves at December 31 | |||

For accounts with assets at: | |||

Fair value | $4,090 | $3,887 | $5,137 |

Amortized cost | — | — | — |

Total reserves | $4,090 | $3,887 | $5,137 |

By withdrawal characteristics: | |||

With market value adjustment | $— | $— | $— |

At book value without market value adjustment and with current surrender charge of 5% or more | — | — | — |

At fair value | 4,087 | 3,884 | 5,134 |

At book value without market value adjustment and with current surrender charge less than 5% | — | — | — |

Subtotal | 4,087 | 3,884 | 5,134 |

Not subject to discretionary withdrawal | 3 | 3 | 3 |

Total reserves | $4,090 | $3,887 | $5,137 |

2023 | 2022 | 2021 | |

Transfers to Separate Accounts | $893 | $1,033 | $1,133 |

Transfers from Separate Accounts | 623 | 416 | 521 |

Net transfers to Separate Accounts | 270 | 617 | 612 |

Reconciling difference | — | — | — |

Transfers as reported in the statements of operations of the General Account | $270 | $617 | $612 |

2023 | 2022 | |||||

Ordinary | Capital | Total | Ordinary | Capital | Total | |

Gross DTA | $203 | $6 | $209 | $298 | $4 | 302 |

Less: Statutory valuation allowance adjustments | — | — | — | 1 | — | 1 |

Adjusted gross DTA | 203 | 6 | 209 | 297 | 4 | 301 |

Less: DTA nonadmitted | 97 | 6 | 103 | 214 | 4 | 218 |

Subtotal net admitted DTA | 106 | — | 106 | 83 | — | 83 |

Less: DTL | 73 | — | 73 | 67 | — | 67 |

Net admitted DTA/(Net DTL) | $33 | $— | $33 | $16 | $— | $16 |

Change | |||

Ordinary | Capital | Total | |

Gross DTA | $(95 ) | $2 | $(93 ) |

Statutory valuation allowance adjustments | (1 ) | — | (1 ) |

Adjusted gross DTA | (94 ) | 2 | (92 ) |

DTA nonadmitted | (117 ) | 2 | (115 ) |

Subtotal net admitted DTA | 23 | — | 23 |

DTL | 6 | — | 6 |

Net admitted DTA/(Net DTL) | $17 | $— | $17 |

2023 | 2022 | |||||

Ordinary | Capital | Total | Ordinary | Capital | Total | |

Federal income taxes paid in prior years recoverable through loss carrybacks | $— | $— | $— | $— | $— | $— |

Adjusted gross DTA expected to be realized (excluding the amount of DTA from above) after application of the threshold limitation (the lesser of 1 and 2 below) | 33 | — | 33 | 16 | — | 16 |

1. Adjusted gross DTA expected to be realized following the balance sheet date | 33 | — | 33 | 16 | — | 16 |

2. Adjusted gross DTA allowed per limitation threshold | XXX | XXX | 118 | XXX | XXX | 31 |

Adjusted gross DTA (excluding the amount of DTA from above) offset by gross DTL | 73 | — | 73 | 67 | — | 67 |

DTA admitted as the result of application of SSAP 101 total | $106 | $— | $106 | $83 | $— | $83 |

Change | |||

Ordinary | Capital | Total | |

Federal income taxes paid in prior years recoverable through loss carrybacks | $— | $— | $— |

Adjusted gross DTA expected to be realized (excluding the amount of DTA from above) after application of the threshold limitation (the lesser of 1 and 2 below) | 17 | — | 17 |

1. Adjusted gross DTA expected to be realized following the balance sheet date | 17 | — | 17 |

2. Adjusted gross DTA allowed per limitation threshold | XXX | XXX | 87 |

Adjusted gross DTA (excluding the amount of DTA from above) offset by gross DTL | 6 | — | 6 |

DTA admitted as the result of application of SSAP 101 total | $23 | $— | $23 |

December 31, 2023 | December 31, 2022 | |

RBC percentage used to determine recovery period and threshold limitation amount | 3999 % | 615 % |

Amount of total adjusted capital used to determine recovery period and threshold limitation | $831 | $252 |

2023 | 2022 | 2021 | |

1. Current Income Tax | |||

(a) Federal | $2 | $93 | $28 |

(b) Foreign | — | — | — |

(c) Subtotal (1a + 1b) | 2 | 93 | 28 |

(d) Federal income tax on net capital gains | (1 ) | (2 ) | — |

(e) Utilization of capital loss carry-forwards | — | — | — |

(f) Other | — | — | — |

(g) Federal and foreign income taxes incurred (1c +1d +1e + 1f) | $1 | $91 | $28 |

2023 | 2022 | Change | |

2. Deferred Tax Assets | |||

(a) Ordinary: | |||

(1) Discounting of unpaid losses | $— | $— | $— |

(2) Unearned premium reserve | — | — | — |

(3) Policyholder reserves | 11 | 112 | (101 ) |

(4) Investments | 53 | 79 | (26 ) |

(5) Deferred acquisition costs | 4 | 9 | (5 ) |

(6) Policyholder dividends accrual | — | — | — |

(7) Fixed assets | — | — | — |

(8) Compensation and benefits accrual | — | — | — |

(9) Pension accrual | — | — | — |

(10) Receivables - nonadmitted | — | — | — |

(11) Net operating loss carryforward | 99 | 61 | 38 |

(12) Tax credit carryforwards | 8 | 8 | — |

(13) Other | 28 | 29 | (1 ) |

(99) Subtotal (sum of 2a1 through 2a13) | 203 | 298 | (95 ) |

(b) Statutory valuation allowance adjustment | — | 1 | (1 ) |

(c) Nonadmitted | 97 | 14 | (117 ) |

(d) Admitted ordinary deferred tax assets (2a99 -2b -2c) | 106 | 83 | 23 |

(e) Capital: | |||

(1) Investments | 6 | 4 | 2 |

(2) Net capital loss carry-forward | — | — | — |

(3) Real estate | — | — | — |

(4) Other | — | — | — |

(99) Subtotal (2e1+2e2+2e3+2e4) | 6 | 4 | 2 |

(f) Statutory valuation allowance adjustment | |||

(g) Nonadmitted | 6 | 4 | 2 |

(h) Admitted capital DTA (2e99-2f-2g) | — | — | — |

(i) Admitted deferred tax assets (2d+2h) | $106 | $83 | $23 |

3. Deferred Tax Liabilities | |||

(a) Ordinary: | |||

(1) Investments | $63 | $50 | $13 |

(2) Fixed assets | — | — | — |

(3) Deferred and uncollected premiums | 1 | 1 | — |

(4) Policyholder reserves | 9 | 16 | (7 ) |

(5) Other | — | — | — |

(99) Subtotal (3a1+3a2+3a3+3a4+3a5) | 73 | 67 | 6 |

(b) Capital: | |||

(1) Investments | — | — | — |

(2) Real estate | — | — | — |

(3) Other | — | — | — |

(99) Subtotal (3b1+3b2+3b3) | — | — | — |

(c) Deferred tax liabilities (3a99+3b99) | 73 | 67 | 6 |

4. Net deferred tax assets/liabilities (2i -3c) | $33 | $16 | 17 |

Change in nonadmitted deferred tax assets | (115 ) | ||

Tax effect of unrealized gains (losses) | (41 ) | ||

Change in net deferred tax assets | $(139 ) |

2022 | 2021 | Change | |

2. Deferred Tax Assets | |||

(a) Ordinary: | |||

(1) Discounting of unpaid losses | $— | $— | $— |

(2) Unearned premium reserve | — | — | — |

(3) Policyholder reserves | 112 | 56 | 56 |

(4) Investments | 79 | — | 79 |

(5) Deferred acquisition costs | 9 | 10 | (1 ) |

(6) Policyholder dividends accrual | — | — | — |

(7) Fixed assets | — | — | — |

(8) Compensation and benefits accrual | — | — | — |

(9) Pension accrual | — | — | — |

(10) Receivables -nonadmitted | — | — | — |

(11) Net operating loss carryforward | 61 | 61 | — |

(12) Tax credit carryforwards | 8 | 6 | 2 |

(13) Other | 29 | 36 | (7 ) |

(99) Subtotal (sum of 2a1 through 2a13) | 298 | 169 | 129 |

(b) Statutory valuation allowance adjustment | 1 | 1 | — |

(c) Nonadmitted | 214 | 102 | 112 |

(d) Admitted ordinary deferred tax assets (2a99 -2b -2c) | 83 | 66 | 17 |

(e) Capital: | |||

(1) Investments | 4 | — | 4 |

(2) Net capital loss carry-forward | — | — | — |

(3) Real estate | — | — | — |

(4) Other | — | — | — |

(99) Subtotal (2e1+2e2+2e3+2e4) | 4 | — | 4 |

(f) Statutory valuation allowance adjustment | — | — | — |

(g) Nonadmitted | 4 | — | 4 |

(h) Admitted capital deferred tax assets (2e99-2f-2g) | — | — | — |

(i) Admitted deferred tax assets (2d+2h) | $83 | $66 | $17 |

3. Deferred Tax Liabilities | |||

(a) Ordinary: | |||

(1) Investments | $50 | $65 | $(15 ) |

(2) Fixed assets | — | — | — |

(3) Deferred and uncollected premiums | 1 | 1 | — |

(4) Policyholder reserves | 16 | — | 16 |

(5) Other | — | — | — |

(99) Subtotal (3a1+3a2+3a3+3a4+3a5) | 67 | 66 | 1 |

(b) Capital: | |||

(1) Investments | — | — | — |

(2) Real estate | — | — | — |

(3) Other | — | — | — |

(99) Subtotal (3b1+3b2+3b3) | — | — | — |

(c) Deferred tax liabilities (3a99+3b99) | 67 | 66 | 1 |

4. Net deferred tax assets/liabilities (2i -3c) | $16 | $— | $16 |

Change in nonadmitted deferred tax assets | 116 | ||

Tax effect of unrealized gains (losses) | (15 ) | ||

Change in net deferred tax assets | $117 |

Year of expiration | Net Operating Loss Carryforwards |

Indefinite | $474 |

Year of Expiration | Tax Credit Carryforwards |

2027-2031 | $6 |

2032-2033 | 2 |

$8 |

2023 | 2022 | 2021 | |

Net gain (loss) from operations after dividends to policyholders and before Federal income tax @ 21% | $2 | $52 | $(70 ) |

Net realized capital gains (losses) @ 21% | 112 | (66 ) | 65 |

Tax effect of: | |||

Separate Account dividend received deduction | (1 ) | (1 ) | (2 ) |

Valuation allowance | (1 ) | — | 1 |

Other | (1 ) | — | 1 |

Uncertain tax positions | — | (1 ) | — |

Tax credits | (1 ) | (1 ) | (1 ) |

Change in nonadmitted assets | — | — | — |

Tax exempt income | — | — | — |

Prior years adjustments and accruals | — | (5 ) | (3 ) |

Interest maintenance reserve | 1 | (2 ) | (1 ) |

Reinsurance Ceding Commission | 29 | (2 ) | (2 ) |

Prior period adjustment in surplus | — | — | — |

Total statutory income taxes (benefit) | $140 | $(26 ) | $(12 ) |

Federal and foreign income taxes incurred including tax on realized capital gains | $1 | $91 | $28 |

Change in net DTA | 139 | (117 ) | (40 ) |

Prior years adjustments in surplus | — | — | — |

Total statutory income taxes (benefit) | $140 | $(26 ) | $(12 ) |

2023 | 2022 | |

Balance at beginning of year | $— | $1 |

Net change for tax positions of current year | — | — |

Net change for tax positions of prior years | — | — |

Settlements with tax authorities | — | — |

Lapses of statutes of limitations | — | (1 ) |

Balance at end of year | $— | $— |

Debt Type | Classification | Issue Year | Maturity Year | Carrying Value | Interest Rate | Interest Paid | Effective Interest Rate |

Affiliated Note | Short-Term | 2022 | 2023 | $125 | 5.450% | $2 | 5.450% |

2023 | 2022 | 2021 | |

Unrealized capital gains (losses) | $13 | $167 | $223 |

Nonadmitted asset values | $(104 ) | $(219 ) | $(103 ) |

Provision for reinsurance | $— | $— | $— |

Asset valuation reserve | $(46 ) | $(46 ) | $(36 ) |

(1) | (2) | (3) | (4) | (5) |

Nature and circumstances of guarantee and key attributes, including date and duration of agreement | Liability recognition of guarantee. (Include amount recognized at inception. If no initial recognition, document exception allowed under SSAP 5R.) | Ultimate financial statement impact if action under the guarantee is required. | Maximum potential amount of future payments (undiscounted) the guarantor could be required to make under the guarantee. If unable to develop an estimate, this should be specifically noted. | Current status of payment or performance risk of guarantee. Also provide additional discussion as warranted. |

The Company is obligated to indemnify the proprietary mutual fund, offered by the Separate Accounts, and the fund’s directors and officers as provided in certain Participation Agreements. | Intercompany and related party guarantees that are considered “unlimited” and as such are excluded from recognition. | Expense | Since this obligation is not subject to limitations, the Company does not believe that it is possible to determine the maximum potential amount that could become due under these guarantees in the future. | The Company has made no payments on the guarantee since inception. |

The Company has provided certain indemnities, guarantees and/or commitments to affiliates and third parties in the ordinary course of its business. In the context of acquisitions, dispositions, investments and other transactions, the Company has provided indemnities and guarantees that are triggered by, among other things, breaches of representations, warranties or covenants provided by the Company. | No liability has been established as the indemnification is for future events for which neither a probability of occurrence nor a reasonable estimate can be established at this time. | Expense | Since this obligation is not subject to limitations, the Company does not believe that it is possible to determine the maximum potential amount that could become due under these guarantees in the future. | The Company has made no payments on the guarantee since inception. |

The Company indemnifies its directors and officers as provided in its charters and by-laws. | No liability has been established as the indemnification is for future events for which neither a probability of occurrence nor a reasonable estimate can be established at this time. | Expense | Since this obligation is not subject to limitations, the Company does not believe that it is possible to determine the maximum potential amount that could become due under these guarantees in the future. | The Company has made no payments on the guarantee since inception. |

The Company indemnifies its agents for liabilities incurred as a result of their representation of the Company’s interests. | No liability has been established as the indemnification is for future events for which neither a probability of occurrence nor a reasonable estimate can be established at this time. | Expense | Since this obligation is not subject to limitations, the Company does not believe that it is possible to determine the maximum potential amount that could become due under these guarantees in the future. | The Company has made no payments on the guarantee since inception. |

Total | $ — | $ — |

In Force | ||||

2023 | 2022 | |||

Number | Balance | Number | Balance | |

Up to and including 12 Months | — | $— | — | $— |

13 to 24 Months | — | — | — | — |

25 to 36 Months | — | — | — | — |

37 to 48 Months | — | — | — | — |

49 to 60 Months | — | — | — | — |

Over 60 Months | 42 | 5 | 47 | 6 |

Total | 42 | $5 | 47 | $6 |

Individual | ||

Number | Balance/ Amount | |

Beginning of year | 47 | $6 |

Accounts issued/added | — | — |

Investment earnings credited | N/A | — |

Fees and other charges assessed* | N/A | — |

Transferred to state unclaimed property funds | — | — |

Closed/withdrawn | 5 | 1 |

End of year | 42 | $5 |

As of and for the Year Ended December 31, 2023 | |

Investment Income Earned | |

U.S. government bonds | $4,686,509 |

Other bonds (unaffiliated) | 64,133,188 |

Bonds of affiliates | — |

Preferred stocks (unaffiliated) | — |

Preferred stocks of affiliates | — |

Common stocks (unaffiliated) | — |

Common stocks of affiliates | — |

Mortgage loans | 8,922,729 |

Real estate | — |

Contract loans | 9,239 |

Cash and cash equivalents | 21,653,395 |

Derivative instruments | (89,011,308 ) |

Other invested assets | 4,133,631 |

Aggregate write-ins for investment income | 853 |

Gross investment income | $14,528,236 |

Real Estate Owned - Book Value Less Encumbrances | $— |

Mortgage Loans - Book Value | |

Agricultural mortgages | $46,216,034 |

Residential mortgages | — |

Commercial mortgages | 182,012,977 |

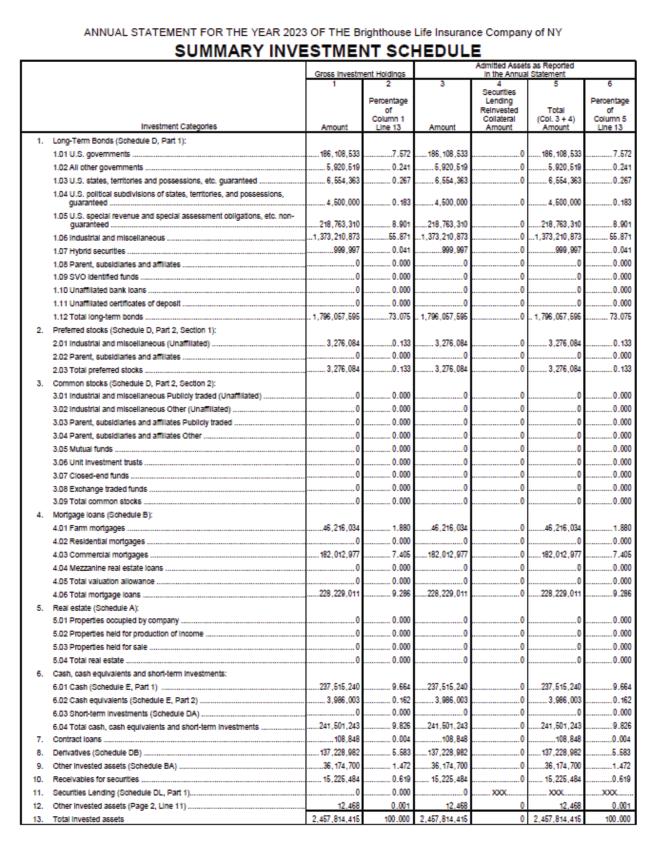

Total mortgage loans | $228,229,011 |

Mortgage Loans by Standing - Book Value | |

Good standing | $228,229,011 |

Good standing with restructured terms | $— |

Interest overdue more than three months, not in foreclosure | $— |

Foreclosure in process | $— |

Other Long Term Invested Assets - Statement Value | $36,174,700 |

Bonds and Stocks of Parents, Subsidiaries and Affiliates - Book Value: | |

Bonds | $— |

Preferred Stocks | $— |

Common Stocks | $— |

Bonds by Class and Maturity: | |

Bonds by Maturity - Statement Value | |

Due within one year or less | $59,057,338 |

Over 1 year through 5 years | 638,951,169 |

Over 5 years through 10 years | 348,240,819 |

Over 10 years through 20 years | 324,586,182 |

Over 20 years | 429,208,090 |

No maturity date | — |

Total by Maturity | $1,800,043,598 |

As of and for the Year Ended December 31, 2023 | |

Bond by Class - Statement Value | |

Class 1 | $1,249,308,482 |

Class 2 | 517,566,289 |

Class 3 | 18,654,140 |

Class 4 | 11,489,756 |

Class 5 | 3,024,931 |

Class 6 | — |

Total by Class | $1,800,043,598 |

Total Bonds Publicly Traded | $1,260,648,371 |

Total Bonds Privately Placed | $539,395,227 |

Preferred Stocks - Book/Adjusted Carrying Value | $3,276,084 |

Common Stocks - Fair Value | $— |

Short Term Investments - Book/Adjusted Carrying Value | $— |

Options, Caps and Floors Owned - Book/Adjusted Carrying Value | $126,171,957 |

Options, Caps and Floors Written and In-force - Book/Adjusted Carrying Value | $(10,081,000 ) |

Collar, Swap and Forward Agreements Open - Book/Adjusted Carrying Value | $10,802,613 |

Futures Contracts Open - Book/Adjusted Carrying Value | $— |

Cash on Deposit | $237,515,240 |

Life Insurance In-Force (000’s) | |

Industrial | $— |

Ordinary | $535,208 |