0001167831lbk:InterestRateMemberlbk:DepositsFromCustomersMemberlbk:TheGroupMemberifrs-full:CashFlowHedgesMember2020-01-012020-12-310001167831lbk:PriorToOffsettingOfBalancesWithinSameTaxingJurisdictionMemberlbk:TheBankMember2019-12-310001167831lbk:RetailUKMotorFinanceMemberlbk:TheGroupMemberlbk:ExpectedCreditLossesInRespectOfDrawnExposuresMemberlbk:RMS16Member2020-12-310001167831lbk:CommercialMemberlbk:CMS1518Memberlbk:TheGroupMemberlbk:GrossUndrawnExposuresMember2020-12-310001167831lbk:PurchasedOrOriginatedCreditimpairedMemberlbk:TheGroupMemberlbk:RMSMemberlbk:ExpectedCreditLossesInRespectOfDrawnExposuresMemberlbk:OtherMember2019-12-310001167831lbk:Stage2Memberlbk:RMS14Memberlbk:GrossDrawnExposuresMemberlbk:TheBankMemberlbk:RetailMortgagesMember2020-12-310001167831lbk:CommercialMemberlbk:TheBankMemberlbk:GrossUndrawnExposuresMemberlbk:Stage1Member2020-12-310001167831lbk:RMS79Memberlbk:RetailLoansAndOverdraftsMemberlbk:GrossUndrawnExposuresMemberlbk:TheBankMemberlbk:Stage1Member2019-12-310001167831lbk:UndiscountedFutureCashFlowBasisMemberlbk:OutflowsMemberifrs-full:LaterThanOneYearAndNotLaterThanFiveYearsMemberlbk:TheBankMember2020-12-31

Lloyds Bank plc

2020 Annual Report on Form 20-F

As filed with the Securities and Exchange Commission on 11 March 2021

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

☐ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended 31 December 2020 OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☐ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission file number 001-35079

LLOYDS BANK plc

(Exact name of Registrant as Specified in Its Charter)

England

(Jurisdiction of Incorporation or Organization)

25 Gresham Street

London EC2V 7HN

United Kingdom

(Address of Principal Executive Offices)

Kate Cheetham, Company Secretary

Tel +44 (0) 20 7356 2104, Fax +44 (0) 20 7356 1808

25 Gresham Street

London EC2V 7HN

United Kingdom

(Name, telephone, e-mail and/or facsimile number and address of Company contact person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading symbol | Name of each exchange on which registered |

| $1,250,000,000 3.5% Senior Notes due 2025 | LYG25 | The New York Stock Exchange |

| $1,500,000,000 2.25% Senior Notes due 2022 | LYG22 | The New York Stock Exchange |

| $1,250,000,000 3.3% Senior Notes due 2021 | LYG21A | The New York Stock Exchange |

| $1,000,000,000 Floating Rate Senior Notes due 2021 | LYG21B | The New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

The number of outstanding shares of each of Lloyds Bank plc’s classes of capital or common stock as of 31 December 2020 was:

| | | | | |

| Ordinary shares, nominal value 1 pound each | 1,574,285,752 |

| Preference shares, nominal value 1 pound each | 100 | |

| Preference shares, nominal value 25 pence each | NaN |

| Preference shares, nominal value 25 cents each | NaN |

| Preference shares, nominal value 25 euro cents each | NaN |

| Preference shares, nominal value 25 yen each | NaN |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ☐ Accelerated filer ☐ Non-Accelerated filer ☒ Emerging Growth Company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐ International Financial Reporting Standards as issued by the International Accounting Standards Board ☒ Other ☐

If ‘Other’ has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes☐ No ☒

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

As a wholly-owned subsidiary of Lloyds Banking Group plc, a public company with limited liability incorporated in the United Kingdom and which has its registered office in Scotland, Lloyds Bank plc meets the conditions set forth in General Instructions I(1)(a) and I(1)(b) of Form 10-K, as applied to reports on Form 20-F and is therefore filing its Form 20-F with a reduced disclosure format.

FORM 20-F CROSS REFERENCE SHEET

| | | | | | | | | | | |

| Form 20-F item number | Page and caption references in this document* |

| 1 | | Identity of Directors, Senior Management and Advisers | Not applicable |

| 2 | | Offer Statistics and Expected Timetable | Not applicable |

| 3 | | Key Information | |

| A. | Selected financial data | Omitted |

| B. | Capitalization and indebtedness | Not applicable |

| C. | Reason for the offer and use of proceeds | Not applicable |

| D. | Risk factors | |

| 4 | | Information on the Company | |

| A. | History and development of the company | Omitted |

| B. | Business overview | |

| C. | Organizational structure | |

| D. | Property, plant and equipment | |

| 4A | | Unresolved staff comments | Not applicable |

| 5 | | Operating and Financial Review and Prospects | |

| A. | Operating results | |

| B. | Liquidity and capital resources | Omitted |

| C. | Research and development, patents and licenses, etc. | Not applicable |

| D. | Trend information | Omitted |

| E. | Off-balance sheet arrangements | Omitted |

| F. | Tabular disclosure of contractual obligations | Omitted |

| G. | Safe harbor | |

| 6 | | Directors, Senior Management and Employees | |

| A. | Directors and senior management | Omitted |

| B. | Compensation | Omitted |

| C. | Board practices | |

| D. | Employees | Omitted |

| E. | Share ownership | Omitted |

| 7 | | Major Shareholders and Related Party Transactions | |

| A. | Major shareholders | Omitted |

| B. | Related party transactions | Omitted |

| C. | Interests of experts and counsel | Not applicable |

| 8 | | Financial Information | |

| A. | Consolidated statements and other financial information | |

| B. | Significant changes | Not applicable |

| 9 | | The Offer and Listing | |

| A. | Offer and listing details | |

| B. | Plan of distribution | Not applicable |

| C. | Markets | |

| D. | Selling shareholders | Not applicable |

| E. | Dilution | Not applicable |

| F. | Expenses of the issue | Not applicable |

| 10 | | Additional Information | |

| A. | Share capital | Not applicable |

| B. | Memorandum and Articles of Association | |

| C. | Material contracts | Not applicable |

| D. | Exchange controls | |

| E. | Taxation | |

| F. | Dividends and paying assets | Not applicable |

| G. | Statement by experts | Not applicable |

| H. | Documents on display | |

| I. | Subsidiary information | |

| 11 | | Quantitative and Qualitative Disclosure about Market Risk | |

FORM 20-F CROSS REFERENCE SHEET

| | | | | | | | | | | |

| 12 | | Description of Securities Other than Equity Securities | |

| A. | Debt Securities | Not applicable |

| B. | Warrants and Rights | Not applicable |

| C. | Other Securities | Not applicable |

| D. | American Depositary Shares | Not applicable |

| 13 | | Defaults, Dividends Arrearages and Delinquencies | Not applicable |

| 14 | | Material Modifications to the Rights of Security Holders and Use of Proceeds | Not applicable |

| 15 | | Controls and Procedures | |

| A. | Disclosure controls and procedures | |

| B. | Management’s annual report on internal control over financial reporting | |

| C. | Attestation report of the registered public accounting firm | Not applicable |

| D. | Changes in internal control over financial reporting | |

| 16A | | Audit Committee Financial Expert | Omitted |

| 16B | | Code of Ethics | Omitted |

| 16C | | Principal Accountant Fees and Services | |

| 16D | | Exemptions from the Listing Standards for Audit Committees | Not applicable |

| 16E | | Purchases of Equity Securities by the Issuer and Affiliated Purchasers | Not applicable |

| 16F | | Change in Registrant’s Certifying Accountant | |

| 16G | | Corporate Governance | |

| 17 | | Financial Statements | See Item 8 |

| 18 | | Financial Statements | See Item 8 |

| 19 | | Exhibits | Exhibit Index |

*Certain items are indicated as omitted as Lloyds Bank plc is a wholly owned subsidiary of Lloyds Banking Group plc, which is a reporting company under the Securities Exchange Act of 1934, and meets the conditions set forth in General Instruction I(1)(a) and (b) of Form 10-K, as applied to annual reports on Form 20-F, and is therefore filing this Form 20-F with a reduced disclosure format.

PRESENTATION OF INFORMATION

In this annual report, references to the ‘Bank’ are to Lloyds Bank plc; references to ‘Lloyds Bank Group’ or the ‘Group’ are to Lloyds Bank plc and its subsidiary and associated undertakings; and references to the ‘consolidated financial statements’ or ‘financial statements’ are to Lloyds Bank consolidated financial statements included in this annual report. References to ‘Lloyds Banking Group’ and ‘Parent Group’ are to Lloyds Banking Group plc, the parent company of Lloyds Bank plc, and its subsidiaries and associated undertakings. References to LBCM are to Lloyds Bank Corporate Markets plc, a fellow subsidiary of Lloyds Banking Group, and its subsidiaries. References to the ‘Financial Conduct Authority’ or ‘FCA’ and to the ‘Prudential Regulation Authority’ or ‘PRA’ are to the United Kingdom (the UK) Financial Conduct Authority and the UK Prudential Regulation Authority. References to the ‘Financial Services Authority’ or ‘FSA’ are to their predecessor organisation, the UK Financial Services Authority.

The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB). Certain disclosures required by IFRS have been included in sections highlighted as ‘Audited’ within the Operating and financial review and prospects section of this Annual Report on Form 20-F on pages 13 to 76. Disclosures marked as audited indicate that they are within the scope of the audit of the financial statements taken as a whole; these disclosures are not subject to a separate opinion.

Lloyds Bank Group publishes its consolidated financial statements expressed in British pounds (‘pounds sterling’, ‘sterling’ or ‘£’), the lawful currency of the UK. In this annual report, references to ‘pence’ and ‘p’ are to one-hundredth of one pound sterling; references to ‘US dollars’, ‘US$’ or ‘$’ are to the lawful currency of the United States (the US); references to ‘cent’ or ‘c’ are to one-hundredth of one US dollar; references to ‘euro’ or ‘€’ are to the lawful currency of the member states of the European Union (EU) that have adopted a single currency in accordance with the Treaty establishing the European Communities, as amended by the Treaty of European Union; references to ‘euro cent’ are to one-hundredth of one euro; and references to ‘Japanese yen’, ‘Japanese ¥’ or ‘¥’ are to the lawful currency of Japan. Solely for the convenience of the reader, this annual report contains translations of certain pounds sterling amounts into US dollars at specified rates. These translations should not be construed as representations by Lloyds Bank Group that the pounds sterling amounts actually represent such US dollar amounts or could be converted into US dollars at the rate indicated or at any other rate. Unless otherwise stated, the translations of pounds sterling into US dollars have been made at the noon buying rate in New York City for cable transfers in pounds sterling as certified for customs purposes by the Federal Reserve Bank of New York (the Noon Buying Rate) in effect on 31 December 2020. The Noon Buying Rate on 31 December 2020 differs from certain of the actual rates used in the preparation of the consolidated financial statements, which are expressed in pounds sterling, and therefore US dollar amounts appearing in this annual report may differ significantly from actual US dollar amounts which were translated into pounds sterling in the preparation of the consolidated financial statements in accordance with IFRS.

The information included in the consolidated financial statements presented in this Form 20-F for the two comparative years differs from the information provided in Lloyds Bank Group’s UK results for the year ended 31 December 2020. As reported in the Bank’s 2018 Form 20-F, an adjusting post balance sheet event that occurred between the signing of the Bank’s 2018 UK Annual Report and Accounts and its 2018 Form 20-F resulted in the charge recognised in respect of PPI complaints in the 2018 Form 20-F being £649 million greater than that recorded in the 2018 UK Annual Report and Accounts. Consequently, the charge recognised by the Lloyds Bank Group in its UK basis results for 2019 was £649 million greater than on a US basis. The Lloyds Bank Group has reported the same net assets on a US basis and on a UK basis since 30 June 2019.

The Lloyds Bank Group is a leading provider of financial services to individual and business customers in the UK. At 31 December 2020, Lloyds Bank Group had 60,672 employees (on a full-time equivalent basis) and its total assets were £599,939 million. The Lloyds Bank Group reported a profit before tax for the 12 months to 31 December 2020 of £1,329 million, and its capital ratios at that date were 23.5 per cent for total capital, 19.8 per cent for tier 1 capital and 15.5 per cent for common equity tier 1 capital.

Set out below is the Lloyds Bank Group’s summarised income statement for each of the last two years:

| | | | | | | | |

| 2020 | 2019 |

| £m | £m |

| Net interest income | 10,770 | | 12,220 | |

| Other income | 3,815 | | 4,388 | |

| Total income | 14,585 | | 16,608 | |

| Total operating expenses | (9,196) | | (11,123) | |

| Impairment | (4,060) | | (1,362) | |

| Profit before tax | 1,329 | | 4,123 | |

The Lloyds Bank Group’s main business activities are retail and commercial banking and it operates primarily in the UK. Services are offered through a number of well recognised brands including Lloyds Bank, Halifax and Bank of Scotland, and through a range of distribution channels including the largest branch network and digital bank in the UK.

At 31 December 2020, the Lloyds Bank Group’s two primary operating divisions, which are also reporting segments, were Retail and Commercial Banking. Retail provides current accounts, savings, mortgages, credit cards, motor finance and unsecured loans to personal and business banking customers. Commercial Banking provides lending, transactional banking, working capital management, risk management and debt capital markets services to commercial customers.

Profit before tax is analysed on pages 15 and 16 and the table below shows the results of the Lloyds Bank Group’s segments in the last two fiscal years.

| | | | | | | | |

| 2020 | 20191 |

| £m | £m |

| Retail | 1,856 | | 2,204 | |

| Commercial Banking | 20 | | 1,430 | |

| Other | (547) | | 489 | |

| Profit before tax | 1,329 | | 4,123 | |

1Segmental analysis restated, as explained on page F-31.

Lloyds Bank plc was incorporated as a public limited company and registered in England under the UK Companies Act on 20 April 1865 with the registered number 2065. Lloyds Bank plc’s registered office and its principal executive offices in the UK are located at 25 Gresham Street, London EC2V 7HN, United Kingdom, telephone number + 44 (0) 20 7626 1500. Lloyds Bank maintains a website at www.lloydsbank.com.

STRATEGY OF LLOYDS BANK GROUP

The Lloyds Bank Group is a leading provider of financial services to individual and business customers in the UK. The Lloyds Bank Group’s main business activities are retail and commercial banking. Services are provided through a number of well recognised brands including Lloyds Bank, Halifax and Bank of Scotland and through a range of distribution channels, including the largest branch network and digital bank in the UK. The Lloyds Bank Group strategy is directly aligned to the strategy of its parent, Lloyds Banking Group plc.

Today's environment continues to evolve and provide new challenges. The macroeconomic environment remains uncertain, whilst Lloyds Banking Group is witnessing increasing societal expectations, an accelerated shift to digital and new technology capabilities in the context of the pandemic driving a step change in ways of working.

Throughout 2020 the management team, in conjunction with the Board, have worked on developing an evolution of Lloyds Banking Group's strategy to address these issues. The Group has made significant progress in recent years, leveraging its unique strengths and assets, including its purpose driven and customer focused business model, low risk approach to business, market leading efficiency and leading multi-channel propositions, including the largest digital bank and branch network in the UK. This has created the platform for Strategic Review 2021, the next stage of the Group's journey.

Strategic Review 2021 is focused on Helping Britain Recover and building the UK’s preferred financial partner for personal customers and the best bank for business. Strategic Review 2021 will deliver co-ordinated growth opportunities in the Group’s two core customer segments, supported by enhanced capabilities in four areas:

•Preferred financial partner for personal customers, through leveraging the Group’s unique competitive advantages to significantly deepen customer relationships

•Best bank for business, through building a leading digital SME proposition, with a disciplined and strengthened business for Corporate and Institutional clients

•Further develop and leverage the Group’s core capabilities, including delivering a modernised technology architecture, building integrated payment solutions, creating a data driven organisation and implementing reimagined ways of working

Clear execution outcomes for the coming year are outlined for all these areas and underpinned by long-term strategic vision. Strategic Review 2021 will thus enable the Group to deliver revenue generation and diversification whilst unlocking further efficiency gains, within the Group’s low risk and capital efficient business. Lloyds Banking Group's purpose, unique business model and ambitious strategy will allow the Group to Help Britain Recover and deliver long-term sustainable returns for its shareholders.

BUSINESS AND ACTIVITIES OF LLOYDS BANK GROUP

The Lloyds Bank Group’s activities are organised into two financial reporting segments: Retail and Commercial Banking. During 2020, the Group migrated certain customer relationships from the SME business within Commercial Banking to Business Banking within Retail; the Group has also revised its approach to internal funding charges, including the adoption of the Sterling Overnight Index Average (SONIA) interest rate benchmark in place of LIBOR. Comparatives have been restated accordingly.

Further information on the Lloyds Bank Group’s segments is set out in note 4 to the financial statements.

MATERIAL CONTRACTS

The Bank and its subsidiaries are party to various contracts in the ordinary course of business.

ENVIRONMENTAL MATTERS

Lloyds Banking Group sets the environmental goals and measures the environmental achievements of the Lloyds Banking Group as a whole. Accordingly, the disclosures below are for Lloyds Banking Group as a whole and not specific to the Group.

Helping Britain transition to a sustainable low carbon economy

This section contains certain disclosures in alignment with the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD).

The Group’s unique position within the UK economy means that the successful transition to a more sustainable, low carbon economy is of strategic importance. The Group supports the aims of the 2015 Paris Agreement, the UK Government’s Net Zero target and Ten Point Plan for a Green Industrial Revolution and the recommendations of the TCFD.

The economic recovery required post COVID-19 provides a critical opportunity to drive clean growth and ensure that the UK’s decarbonisation requirements sit at the heart of the UK’s policy framework. In 2020, the Group joined over 200 businesses, investors, and business organisations in calling on the Government to deliver a clean, inclusive, and resilient recovery plan. The Group has produced a separate document outlining its belief that prioritising a green recovery is critical and the priority areas that the Group thought should feature within any economic stimulus plan.

Lloyds Banking Group Strategy

Lloyds Banking Group’s goal and approach

As a signal of commitment, the Group set an ambitious goal in 2020: working with customers, Government, and the market to help reduce the emissions that the Group finances by more than 50 per cent by 2030, on the path to net zero by 2050 or sooner, which will support the UK Government's ambition and the 2015 Paris Agreement. During the course of 2020, the Group has calculated an initial estimate of its 2018 financed emissions baseline and has developed its first emission intensity reduction ambition for the power sector, the decarbonisation of which is critical to the UK achieving its climate targets. The Group will continue to develop additional sector specific ambitions throughout 2021.

In addition, the Insurance and Wealth division (excluding Wealth Private Banking) has published a target to reach net zero across the full portfolio of investments by 2050, halving the investments’ carbon footprint by 2030.

In order to meet its overall 2030 and 2050 goals, the Group will continue to:

•Identify new ways to support customers and clients with the management of opportunities and risks associated with climate change, and the transition to a low carbon economy.

•Identify, manage, and disclose material sustainability and climate-related risks across the Group and their impacts on the Group and its financial planning processes, in line with the TCFD framework. This includes working with industry bodies, specialist consultancies and leading academics to develop a robust climate risk measurement capability.

•Use the scale and reach of the Group to help drive progress towards a sustainable and resilient UK economy through engagement with customers, communities, industry, Government, shareholders, and suppliers.

•Embed sustainability into the way the Group does business and manages its own operations in a more sustainable way. To support this the Group has updated the operational climate pledges, setting a new net zero goal for 2030.

The Group participates in several industry initiatives and has signed up to key principles that drive action on climate change and sustainability.

The Lloyds Banking Group Ambitions

The Group set seven leadership ambitions to support the UK’s transition to a sustainable future. In 2020, the Group has focused on enhancing its green finance products and services to achieve its ambitions. Examples of this include the following:

| | | | | |

| Lloyds Banking Group Ambition | How the Group are delivering against the ambitions |

Business Become a leading UK commercial bank for sustainable growth, supporting clients to transition to sustainable business models and operations, and to pursue new clean growth opportunities | •Since 2018 the Group has supported renewable energy projects that power the equivalent of 10.1 million homes, significantly exceeding the Helping Britain Prosper Plan 2020 target. •The Group launched several new green finance products, tools, and services: a Lloyds Bank and Bank of Scotland Green Buildings Tool; a Sustainability Fixed Term Deposit and 95 Day Notice Account; and the Group also structured and co-ordinated the first Sterling Overnight Index Average (SONIA) Sustainability Linked Loan for Affinity Water |

| |

| |

Homes Be a leading UK provider of customer support for energy efficient, sustainable homes | •The Group launched the Green Living and Eco Home Hub for Halifax and Lloyds customers •To support Halifax customers with the cost of green home improvements, the Group has also introduced a Green Living Reward under the UK Department for Business, Energy, and Industrial Strategy (BEIS) Green Home Finance Innovation Fund |

| |

| |

Vehicles Be a leading UK provider of low emission/green vehicle fleets | •In 2020, the Group more than doubled the number of electric vehicles financed through its Motor Finance and Leasing subsidiaries, Lex Autolease and Blackhorse |

| |

| |

Pensions and investments Be a leading UK pension provider that offers customers and colleagues sustainable investment choices, and challenges the companies the Group invest in to behave more sustainably and responsibly | •Scottish Widows has launched a Responsible Investment Framework in March 2020 and supporting Stewardship Policy. •The Scottish Widows Exclusions Policy focuses on companies that have failed to meet Scottish Widows environmental, social and governance standards, namely manufacturers of controversial weapons, UN Global Compact violators and those deriving more than 10 per cent of their revenue from thermal coal and tar sands extraction. Scottish Widows is currently divesting an initial £440 million from these companies, starting with those investments where Scottish Widows has direct control and is working to expand the application of this policy into external pooled funds that underpin the multi-asset funds as well. Early success of engagement activity with one of the partner asset managers has led the investment manager to introduce an exclusions policy for all its Europe-domiciled passive funds totalling over £20 billion, leading to an additional divestment of approximately £280 million within customer pension portfolios. •Through shareholder investments, Scottish Widows provides direct loans for renewable energy, including for offshore wind and solar energy. •Scottish Widows is also investing £2 billion of Pension and Retirement Portfolio Pension Funds capital into a new fund, the ACS Climate Transition World Equity Fund, co-created with BlackRock that looks to increase investment in companies that are well prepared for the low carbon transition and to reduce exposure to those that are less so |

| |

| |

Insurance Be a leading UK insurer in improving the resilience of customers’ lives against extreme weather exacerbated by climate change | •The Group continues to partner with RedArc to operate a trauma helpline that aids customers needing extra help after a traumatic claim such as a fire or flood •The Group is also investing in ways to minimise the impact of flooding on customers. For example, the Group continues to provide a Rapid Response Vehicle to quickly assess claims and release funds to customers in the worst affected areas |

| |

| |

Green bonds Be a leading UK bank in the green/sustainable bonds market | •Since the launch of this ambition in 2016, the Group has maintained the role as a leader for UK corporate clients between 2016 and 2020, raising around £2.9 billion. |

| |

| |

Lloyds Banking Group’s own footprint Be a leading UK bank in reducing Lloyds Banking Group’s own carbon footprint and challenging our suppliers to ensure Lloyds Banking Group’s own consumption of resources, goods and services is sustainable | •The Group continues to improve the sustainability of its own operations and has recently updated the Group’s operational climate pledges. •This year, the Group has calculated and disclosed the emissions associated with increased homeworking as a result of COVID-19 and sponsored a white paper in this area. •The Group has continued to reduce the energy and carbon intensity of its properties and has supported low carbon travel •Lloyds Banking Group’s overall location-based carbon emissions were 159,487 tonnes CO2e; a 24 per cent decrease since 2019 and 72 per cent since its 2009 baseline (legacy scope). |

| |

Governance

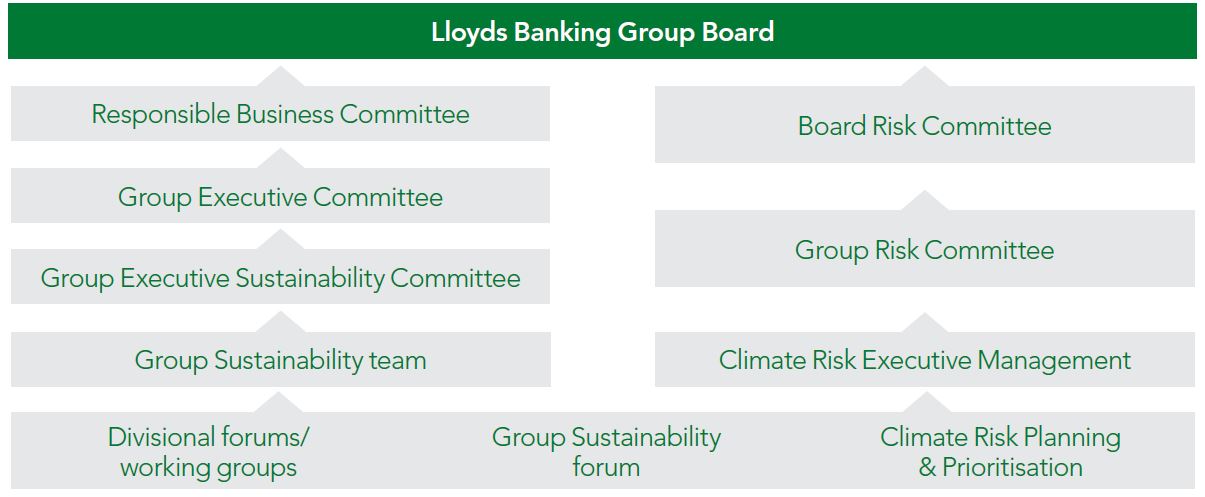

Lloyds Banking Group’s governance structure provides clear oversight and ownership of the Group’s sustainability strategy and management of climate-related risks. Governance for climate-related risks is embedded into the Group’s existing governance structure and is complementary to governance of the sustainability strategy.

Risk management

The Group has adopted a comprehensive approach to embedding climate-related risks into its Enterprise Risk Management Framework through:

•Creation of a new principal risk for climate risk, in order to drive dedicated focus and a consistent approach, whilst enhancing Board-level insight.

•Integration of climate risk into the Group’s existing principal risks, to ensure comprehensive consideration across all aspects of its business activity.

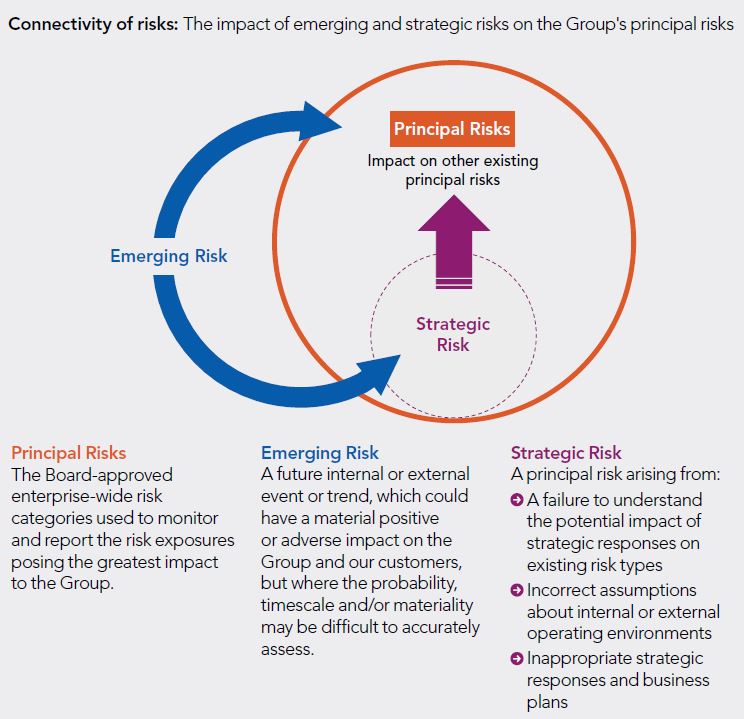

Climate Risk is included as both a principal and emerging risk this year given it is such a new and fast-moving area. The Group continues to ensure its approach for climate risk management has suitable Board- level visibility. The Board has approved a Risk Appetite Statement for climate risk, as well as an interim metric to ensure the Group continues to progress activities at pace, supported by Board-level risk reporting.

As the understanding and importance of climate risk progresses, climate scenario analysis is becoming an essential capability and risk management tool. Scenario analysis assists the identification, measurement, and ongoing assessment of climate risks over the longer-term, and the potential threats to the Group’s strategic objectives. In 2020, the Group has developed its climate scenario analysis framework and will see outputs from this in 2021.

To further accelerate progress, the Group has engaged with third-party consultants to support the development of its climate risk management framework and high priority sector analysis, thereby extending its modelling and assessment capabilities for quantifying climate risk.

Climate risk and sustainability has been a key consideration in the credit assessment process in recent years, and in 2020 the Group has deepened the integration of sustainability into its credit risk processes and appetite statements. Lloyds Banking Group continues to refine the Group’s external sector statements, which help articulate appropriate areas of climate-related risk appetite and the Group’s approach to the risk assessment of its customers.

As part of the Group's credit risk policy, the Group has mandatory requirements to consider environmental risks in key risk management activities. In Commercial Banking, Relationship Managers must continue to ensure that sustainability risk is considered for all new and renewal facilities, and specifically commented on where credit limits exceed £500,000. The Group has also developed and is piloting a tool in Commercial Banking to help qualitatively assess clients’ physical and transition risks.

In Retail, the Group considers exposure to physical risks, such as flooding, in mortgages origination criteria and the Group has also introduced sustainability related criteria into its motor finance businesses. Within Insurance, an assessment of climate-related risks to General Insurance (GI) liabilities is integrated into the internal model governance process. The Group further developed its weather modelling capabilities in 2020 through completion of a research partnership between the Group's GI Weather Modelling Team and the University of Reading on extreme wind and flood risk in the UK.

Sectors with increased climate risk

The Group has identified those sectors where it has lending to customers that may likely contribute a higher share of Lloyds Banking Group’s financed emissions (see Table 1). Not all customers in these sectors have high emissions or are exposed to significant transition risks.

The Group continues to enhance and refine this work at both counterparty and sector level, considering both risks and opportunities as it looks to support customers' responses to climate change.

| | | | | | | | | | | | | | | | | | | | |

Table 1. Lending1 to customers in sectors at increased risk from the impacts of climate change |

Commercial Banking Sector4 | Lending to Commercial Banking customers (£m)2 | | Percentage of total Group loans and advances to customers3 |

| Dec 2020 | Dec 2019 | | Dec 2020 | Dec 2019 |

| Energy Use in Buildings | Real Estate (including Housing Associations) | 25,426 | | 27,124 | | | 5.04% | 5.44% |

| Agriculture | Agriculture, Forestry & Fishing5 | 7,464 | | 7,219 | | | 1.48% | 1.45% |

| Transport | Passenger Transport | 1,135 | | 1,120 | | | 0.22% | 0.22% |

| Industrial Transport | 1,374 | | 1,674 | | | 0.27% | 0.34% |

Automotives6 | 1,485 | | 1,272 | | | 0.29% | 0.26% |

| Energy Use in Industry | Housebuilders | 870 | | 1,168 | | | 0.17% | 0.23% |

Construction7 | 1,210 | | 1,179 | | | 0.24% | 0.24% |

| Cement, Construction Materials, Chemicals & Steel Manufacture | 317 | | 391 | | | 0.06% | 0.08% |

| General Manufacturing | 1,301 | | 1,285 | | | 0.26% | 0.26% |

| Food Manufacturing and Wholesalers | 1,312 | | 1,844 | | | 0.26% | 0.37% |

| Energy Supply | Oil & Gas8 | 1,099 | | 1,393 | | | 0.22% | 0.28% |

| Utilities | 1,638 | | 1,779 | | | 0.32% | 0.36% |

| Coal Mining | 8 | | 21 | | | 0.002% | 0.004% |

| Total | 44,639 | | 47,469 | | | 8.85% | 9.53% |

| | | | | | |

| | Loans and advances to

customers (£m) | | Percentage of total Group loans and advances to customers3 |

Retail Division areas9 | Dec 2020 | Dec 2019 | | Dec 2020 | Dec 2019 |

| UK Mortgages | 294,806 | | 289,198 | | | 58.42% | 58.04% |

| UK Motor Finance | 15,201 | | 15,976 | | | 3.01% | 3.21% |

| Total | 310,007 | | 305,174 | | | 61.44% | 61.25% |

1Commercial Banking and Retail divisions only. Excludes Insurance and Wealth division.

2Commercial Banking division only, excludes Commercial Finance. Drawn lending is gross of significant risk transfers. Excludes Business Banking lending, which sits within Retail division. 2019 restated on a consistent basis with 2020.

3Percentages calculated using total Group loans and advances to customers, before allowance for impairment losses (£504,603 million at 31 December 2020 and £498,247 million at 31 December 2019).

4Commercial lending classified using ONS SIC codes at legal entity level.

5Agriculture lending includes Agricultural Mortgage Corporation (AMC) based on loans and advances to customers £4,186 million (2019: £3,998 million).

6Includes Automotive manufacture, retail and wholesale trade, rentals and parts but excludes finance captives and securitisations.

7Construction excludes 41100 Development of building projects (included within Real Estate) and 41202 Construction of domestic buildings (reported separately as Housebuilders).

8Excludes Commodity Traders.

9Based on loans and advances to customers within Retail Division.

Metrics and targets

Financed emissions

Lloyds Banking Group believes it is appropriate to provide more financial information on its financed emissions, although the Group also recognises this is a rapidly developing area, with evolving and sometimes limiting data availability, data completeness and calculation methodologies. The Group expects these to continue to improve in 2021 and beyond, helping it to refine the Group's approaches, estimates and understanding of the climate risk within its portfolios. However, in order to enhance disclosure, whilst recognising these limitations, the Group details in Table 2 an initial estimated view of the 2018 financed emissions baseline across the Group’s own lending activity (excluding Insurance and Wealth).

This will serve as an initial basis for the Group’s goal of helping to reduce the emissions that the Group finances by more than 50 per cent by 2030 and to help it better support customers in their transition plans to a low-carbon economy (see Table 2). The Group selected 2018 as there is more comprehensive company emissions reporting and UK Government Office of National Statistics (ONS) emissions data available at that time.

The Group has used the emerging industry standard for calculating financed emissions developed by the Partnership for Carbon Accounting Financials (PCAF). The baseline is an estimate, as client or asset level emissions data is currently not available in all cases and where appropriate, the Group has used internal and external data and proxies to fill these data gaps. Given this is a new discipline that will continue to develop and evolve, it is expected that its baseline will change in the future (perhaps materially), which may require restatement. The Group expects methodologies for calculating financed emissions to mature, with data availability and quality also improving from clients and Government sources.

The initial estimated view of the 2018 financed emissions baseline covers approximately 70 per cent of the Group’s balance sheet (excluding Insurance and Wealth)1 comprised of:

•Motor vehicle loans (Lex and Black Horse) – at individual vehicle level, vehicle emission intensity and contracted (or estimated) miles driven per annum

•Mortgages (Retail UK Mortgages) – from Energy Performance Certificates (EPCs) where available with estimates used for properties without EPC ratings

•Business loans (Commercial Banking only) – on client-level emissions data and asset-based estimates using ONS UK sector emissions

•Cash balances – with no associated emissions

For the remaining balance sheet, 26 per cent currently have no method for calculating emissions and 4 per cent do not have data readily available to enable emissions to be calculated.2

As currently recommended by PCAF, the baseline only includes Scope 1 and 2 emissions of clients and does not include undrawn lending commitments, off balance sheet contingents or areas where there is no methodology.

Insurance and Wealth financed emissions

The financed emissions for the Insurance and Wealth division are not included in the Group’s total financed emissions or the Group’s target to reduce financed emissions by 50 per cent by 2030. Due to the different nature of banking and investment activity, the Insurance and Wealth division will be further developing its approach to reporting appropriate climate metrics and targets during 2021.

| | | | | | | | |

Table 2. Initial estimated view of the 2018 financed emissions baseline for the Group’s own lending (excluding the Insurance and Wealth division) |

| Asset Class | Estimated MtCO2e (Scope 1 & 2 emissions) | Equivalent share of UK total emissions by sector/asset class6 |

Motor vehicle loans3 | 3.2 | c.4% |

Mortgages4 | 6.3 | c.6% |

Business loans5 | 15.9 | c.6% |

| Total | 25.41,2 | c.5.6% |

Notes to table:

1Includes Nil emissions for cash balances,which accounted for 8 per cent of the Group's balance sheet.

2Examples of areas where there is no current method for calculating emissions include: government securities, derivatives, personal loans, credit cards and reverse repos. Areas where data was not readily available, but coverage may be expanded in the future include: business banking, non-UK mortgages, loans and advances to banks and some assets at fair value through profit and loss.

3Covers 95 per cent of motor vehicle loans and operating lease assets. Excludes assets that do not have a motor , specialist vehicles and vehicles where mileage is difficult to estimate. Currently does not apply a loan-to-value ratio for emissions.

4Covers 97 per cent of mortgages. Excludes non-UK mortgages. Uses EPC emissions estimates for 45% of properties and average emission intensity profiles of EPC C to G properties to calculate emissions for the balance of properties where EPCs are not available. Property index value as at end 2018 is used for current property value in PCAF emission attribution calculations.

5Includes 99 per cent of Commercial Banking business loans, based on drawn lending. The PCAF sector-based approach has been used for the majority of the business loans baseline, using Office of National Statistics (ONS) UK emissions. The business loans method has been applied to project finance (excluding Power project finance) and commercial real estate assets, which will be refined in the future as better data becomes available.

6Total UK emissions in 2018 were: 88 MtCO2e from cars and vans; c.100 MtCO2e from homes, including emissions from both electricity and heating; and 263 MtCO2e from business (excluding emissions from electricity used in residential property). Source: Department for Business, Energy and Industrial Strategy - 2018 UK Greenhouse Gas Emissions, Final Figures.

Power sector ambition

In Commercial Banking, the Group has been working to develop a power sector ambition as power sector decarbonisation is critical for the UK to achieve its Net Zero goal.

The Group has determined that its power generation portfolio, comprising Commercial Banking large corporate and project finance portfolio facilities, generated financed emissions of 0.7MtCO2e in 2018, with an emission intensity of 141gCO2e/kWh on a drawn basis, covering both UK and EU exposures. This is lower than the UK average grid emissions intensity of 283 gCO2e/kWh in 2018, due to market leading support for UK offshore and renewable energy.

Having assessed the Commercial Banking large corporate and project finance power generation portfolio against decarbonisation plans and its commitment to Help Britain Prosper, the Group is now setting an ambition to reduce the portfolio’s emission intensity to less than 75gCO2e/kWh by 20301 This is in line with the UK’s net zero ambition but takes into account the combination of UK and European clients in its portfolio.

Achieving the Group’s ambition will be dependent on the UK and European countries putting in place the policy frameworks to meet decarbonisation goals and major utilities achieving their decarbonisation objectives. The Group will work with the Government and its clients to help support this transition.

1The Group has followed the PCAF recommendation to only account for drawn lending exposure in our financed emission disclosure. It is important to highlight that the undrawn portion of the power generation portfolio could result in fluctuations to the emission and power intensity baseline.

Green finance

In 2020, the Group provided over £2.3 billion of green finance in Commercial Banking, through its Clean Growth Finance Initiative, Commercial Real Estate Green Lending Initiative, Renewable Energy Financing and Green Bond facilitation. This increased the Group’s total green finance to over £7.3 billion since 2016. In addition, the Group has supported clients with over £1.8 billion of Sustainability Linked Loans since 2017.

New climate pledges for Lloyds Banking Group’s own operations

In 2019 the Group announced achievement of its 2030 carbon emission reduction goal for its own operations, 11 years early, having reduced carbon emissions by 63 per cent between 2009 and 2019, and exceeding its 60 per cent reduction target. The Group is now able to announce three new operational climate pledges which accelerate the Group’s plan to tackle climate change and apply across its operations.

•The Group expects to achieve net zero carbon operations by 2030. The Group plans to reduce its direct emissions (known as Scope 1 and 2 emissions) by at least 75 per cent (compared to 2018/9 levels)

•The Group expects to reduce its total energy consumption by 50 per cent by 2030 (compared to 2018/9). Whilst the Group already procures zero carbon electricity, it remains crucial that the Group reduces the amount of power it consumes to support the UK in meeting an increasing demand for renewable energy

•The Group expects to maintain travel carbon emissions below 50 per cent of pre COVID-19 (2018/9) levels, embedding for the long-term the reduced levels of commuting and business travel seen during the pandemic and supporting colleagues to switch to low carbon transport.

Achieving these goals will not be easy, and the Group will need to invest in its buildings over the next decade, supporting the UK to make a green recovery. The Group will continue to deploy energy efficient technology including LED lighting and improved building controls. The Group will remove all use of natural gas from its estate, replacing its gas boilers with zero carbon heating technologies and creating more sustainable branches in communities across the UK. Many of the technologies that the Group will need to use are still new and it will need to work closely with its partners and supply chain to innovate.

Scope 1,2 and 3 Greenhouse gas emissions

The Group has reported greenhouse gas emissions and environmental performance since 2009, and since 2013 this has been reported in line with the requirements of the Companies Act 2006 and its applicable regulations. The Group’s total emissions, in tonnes of CO2 equivalent, are reported in the table below. Deloitte LLP has provided limited level ISAE 3000 (Revised) assurance over selected non-financial indicators as noted by ☑ . Deloitte's full, independent assurance statement is available online in the 2020 ESG Report at https://www.lloydsbankinggroup.com/who-we-are/responsible-business/downloads.html

Methodology

The Group follows the principles of the Greenhouse Gas (GHG) Protocol Corporate Accounting and Reporting Standard to calculate Scope 1, 2 and 3 emissions from its worldwide operations. The reporting period is 1 October 2019 to 30 September 2020. Emissions are reported based on the operational control approach.

Reported Scope 1 emissions are those generated from gas and oil used in buildings, emissions from fuels used in UK company owned vehicles used for business travel and fugitive emissions from the use of air conditioning and chiller/refrigerant plant. Reported Scope 2 emissions are generated from the use of electricity and are calculated using both the location and market-based methodologies. Reported Scope 3 emissions relate to business travel and commuting undertaken by colleagues, waste and the extraction and distribution of each of the Group’s energy sources – electricity, gas, and oil. This year, in light of the coronavirus pandemic’s impacts on Group operations, the Group has included the emissions of colleagues working from home before and during the pandemic in the Group’s Scope 3 totals.

Intensity ratio

| | | | | | | | | | | |

| Legacy Scope | Oct19-

Sep20 | Oct18-

Sep19 | Oct17-

Sep18 |

GHG emissions (CO2e) per £m of underlying income (Location Based)1 | 10.4 | 11.5 | 13 |

GHG emissions (CO2e) per £m of underlying income (Market Based)1 | 4.7 | 5.6 | 6.2 |

| | | | | | | | | | | |

| Expanded Scope | Oct19-

Sep20 | Oct18-

Sep19 | Oct17- Sep181 |

GHG emissions (CO2e) per £m of underlying income (Market Based) - expanded scope2 | 13.6 | 15.8 | 17.3 |

GHG emissions (CO2e) per £m of underlying income (Location Based) - expanded scope2 | 7.9 | 9.9 | 10.6 |

1Intensities have been restated for 2017-2018 and 2018-2019 to reflect changes to emissions data only, replacing estimated data with actuals; underlying income figures for those years have not changed.

2Scope 3 emissions have been expanded to include additional elements within the Group’s own operations including emissions from waste, colleague commuting and additional elements of business travel, (including taxis, tube, well to tank emissions of business travel and hotels). We have disclosed these figures parallel to legacy scope numbers to allow fairer comparison to numbers previously disclosed and to demonstrate performance versus our previous targets. Additionally, October 19-September 20 scope 3 figures include an allowance for emissions from homeworkers not previously accounted for, owing to the significant increase in materiality year to year due to the impacts of coronavirus. Previous years have not been restated.

This year, the Group’s overall location-based carbon emissions were 159,487 tCO2e; a 24 per cent decrease since 2019 and 72 per cent against its 2009 baseline (legacy scope). Significant reductions were achieved between October and March of this reporting year. These are attributable to the Group’s programme of environmental action since 2010, which has delivered a reduction in gas and electricity consumption through extensive energy management, alongside decarbonisation of the UK electricity grid from October to March 2020. Further reductions have been caused by the impact of coronavirus on the Group’s operations and reported emissions. A large proportion of the Lloyds Banking Group colleagues worked from home in 2020 in line with travel restrictions and advice, which has led to a considerable reduction in both scope 1 and 3 business travel numbers reported. Group building energy, gas, and electricity, also reduced in part due to the impacts of this operational shift, though impacts are not as significant.

The Group scope 2 market-based emissions figure is zero tCO2e, as it has procured renewable energy certificates equal to its total electricity consumption in each of the markets in which the Group operates since January 2019.

Omissions

Emissions associated with joint ventures and investments are not included in this disclosure as they fall outside the scope of the Lloyds Banking Group operational boundary. The Group does not have any emissions associated with imported heat, steam or imported cooling and is not aware of any other material sources of omissions from its reporting.

Carbon Emissions (tonnes CO2e)

| | | | | | | | | | | |

| Legacy Scope | Oct19-

Sep20 | Oct18- Sep191 | Oct17- Sep181 |

Total CO2e (market-based) ☑ | 71,704 | 101,856 | 116,100 |

Total CO2e (location-based) ☑ | 159,487 | 208,495 | 243,028 |

| Total Scope 1 & 2 (location-based) ☑ | 126,890 | 155,270 | 178,378 |

–Of Which UK Scope 1 & 2 (location-based) | 126,209 | 152,893 | 176,676 |

| Total Scope 1 & 2 (market-based) ☑ | 39,107 | 48,631 | 51,450 |

–Of Which UK Scope 1 & 2 (market-based) | 38,806 | 47,946 | 49,213 |

| Total Scope 1☑ | 39,107 | 48,246 | 49,505 |

| Total Scope 2 (market-based) ☑ | — | 385 | 1,945 |

| Total Scope 2 (location-based) ☑ | 32,597 | 53,225 | 64,650 |

| | | |

| Expanded scope | Oct19-

Sep20 | Oct18- Sep191 | Oct17- Sep181 |

Total CO2e (market-based) ☑ | 120,308 | 180,153 | 197,623 |

Total CO2e (location-based) ☑ | 208,092 | 286,792 | 324,551 |

| Total Scope 3 ☑ | 81,202 | 131,522 | 146,173 |

| | | |

| Global Energy Use (kWhs) | Oct19-

Sep20 | Oct18- Sep191 | Oct17- Sep181 |

| Total Global Energy Use ☑ | 524,024,822 | 591,341,929 | 623,467,500 |

–Of Which UK Energy Use | 518,717,523 | 585,136,101 | 617,185,723 |

| Total Building Energy | 503,709,548 | 551,778,914 | 577,606,213 |

| Total Company Owned Vehicle Energy | 14,436,436 | 29,987,906 | 34,889,251 |

Total Grey Fleet Vehicle Energy2 | 5,878,838 | 9,575,109 | 10,972,036 |

1Restated 2018/2017 emissions data to improve the accuracy of reporting, using actual data to replace estimates.

2Grey fleet refers to colleague and hired road vehicles being used for a business purpose. Emissions in tonnes CO2e in line with the GHG Protocol Corporate Standard (2004). We are reporting to the revised Scope 2 guidance, disclosing a market-based figure in addition to the location-based figure.

The measure and report Scope 1, 2, 3 emissions is provided in the Lloyds Banking Group Reporting Criteria statement available online at www.lloydsbankinggroup.com/who-we-are/responsible-business.html

Scope 1 emissions include mobile and stationary combustion of fuel and operation of facilities.

Scope 2 emissions have been calculated in accordance with GHG Protocol guidelines, in both location and market based methodologies.

Scope 3 emissions reported are disclosed in line with our legacy target, per the expanded to include additional elements within the Group’s own operations including emissions from waste, colleague commuting and additional elements of business travel (including taxis, tube, well to tank emissions of business travel and hotels). We have also disclosed legacy scope numbers to allow fairer comparison to numbers previously disclosed and to demonstrate performance versus our previous targets.

☑ Indicator is subject to Limited ISAE3000 (revised) assurance by Deloitte LLP for the 2020 Annual Responsible Business Reporting. Deloitte’s 2020 assurance statement and the 2020 Reporting Criteria are available online at www.lloydsbankinggroup.com/who-we-are/responsible-business.html

Energy Efficiency

Whilst coronavirus has significantly impacted Lloyds Banking Group's energy performance year on year, the Group did see a 4 per cent year to year energy consumption reduction achieved in a 6-month period prior to the impacts of coronavirus, largely due to the Group’s energy reduction initiatives. These initiatives include an energy optimisation programme; an energy intervention scheme that includes remote and on-site optimisation and strategic alterations of building management systems and controls systems to match the run hours of plant to core operating hours and ensure temperature settings are aligned with Group comfort guidelines. In 2020, 89 deep-dives, 88 on-site optimisations, 13 remote optimisations and 550 bank holiday programming were completed, which resulted in a 105 GWh saving. Additionally, Lloyds Banking Group saw a 14 per cent year to year energy reduction in our company owned vehicles energy usage in the 6-month period prior to April 2020, due to our ongoing focus on reducing business travel.

Looking forward

In 2021, Lloyds Banking Group will continue to develop additional sector-based ambitions to support its goal to help reduce the emissions it finances by more than 50 per cent by 2030. The Group will continue to enhance its methodologies and framework for reporting climate risks and opportunities, taking into account relevant industry guidelines and regulatory reporting requirements. This will further advance the Group disclosures and respond to the evolving needs of both its shareholders and other stakeholders.

PROPERTIES

At 31 December 2020, Lloyds Bank Group occupied 1,724 properties in the UK. Of these, 367 were held as freeholds and 1,357 as leasehold. The majority of these properties are retail branches, widely distributed throughout England, Scotland, Wales and Northern Ireland. Other buildings include the Lloyds Bank’s head office in the City of London with other customer service and support centres located to suit business needs but clustered largely in eight core geographic conurbations – London, Edinburgh, Glasgow, Midlands (Birmingham), Northwest (Chester and Manchester), West Yorkshire (Halifax and Leeds), South (Brighton and Andover) and Southwest (Bristol and Cardiff).

In addition, there are 103 properties which are either sub-let or vacant. There are also a number of Automated Teller Machine (ATM) units situated throughout the UK, the majority of which are held as leasehold. The Group also has business operations elsewhere in the world, primarily holding property on a leasehold basis.

LEGAL ACTIONS AND REGULATORY MATTERS

During the ordinary course of business the Lloyds Bank Group is subject to threatened or actual legal proceedings and regulatory reviews and investigations both in the UK and overseas. Set out below is a summary of the more significant matters.

PROVISIONS FOR FINANCIAL COMMITMENTS AND GUARANTEES

Provisions are recognised for expected credit losses on undrawn loan commitments and financial guarantees.

PAYMENT PROTECTION INSURANCE (EXCLUDING MBNA)

The Group has made provisions for PPI costs totalling £21,906 million; of which £85 million was recognised in the final quarter of the year ended 31 December 2020. Of the approximately six million enquiries received pre-deadline, more than 99 per cent have now been processed. The £85 million charge in the fourth quarter was driven by the impact of coronavirus delaying operational activities during 2020, the final stages of work to ensure operational completeness ahead of an orderly programme close and final validation of information requests and complaints with third parties that resulted in a limited number of additional complaints to be handled. A small part of the costs incurred during the year also reflect the costs associated with litigation activity to date.

At 31 December 2020, a provision of £198 million remained unutilised relating to complaints and associated administration costs excluding amounts relating to MBNA. Total cash payments were £1,459 million during the year ended 31 December 2020.

PAYMENT PROTECTION INSURANCE (MBNA)

As announced in December 2016, the Group's exposure continues to remain capped at £240 million under the terms of the MBNA sale and purchase agreement. No additional charge has been made by MBNA to its PPI provision in the year ended 31 December 2020; total cash payments in the year were £241 million and the remaining provision at 31 December 2020 was £61 million (31 December 2019: £302 million).

OTHER PROVISIONS FOR LEGAL ACTIONS AND REGULATORY MATTERS

In the course of its business, the Group is engaged in discussions with the PRA, FCA and other UK and overseas regulators and other governmental authorities on a range of matters. The Group also receives complaints in connection with its past conduct and claims brought by or on behalf of current and former employees, customers, investors and other third parties and is subject to legal proceedings and other legal actions. Where significant, provisions are held against the costs expected to be incurred in relation to these matters and matters arising from related internal reviews. During the year ended 31 December 2020 the Group charged a further £329 million in respect of legal actions and other regulatory matters, and the unutilised balance at 31 December 2020 was £261 million (31 December 2019: £395 million). The most significant items are as follows.

HBOS Reading – review

The Group completed its compensation assessment for those within the Customer Review in 2019 with more than £109 million of compensation paid, in addition to £15 million for ex-gratia payments and £6 million for the reimbursement of legal fees. The Group is applying the recommendations from Sir Ross Cranston’s review, issued in December 2019, including a reassessment of direct and consequential losses by an independent panel, an extension of debt relief and a wider definition of de facto directors. Further details of the panel were announced on 3 April 2020 and the panel's full scope and methodology was published on 7 July 2020. The panel’s stated objective is to consider cases via a non-legalistic and fair process, and to make their decisions in a generous, fair and common-sense manner. Details of an appeal process for the further assessments of debt relief and de facto director status have also been announced. The Group continues to make progress on its assessment of claims for further debt relief and de facto director status, completing preliminary assessments for 98 per cent of claims on both debt relief and de facto directors. As part of these activities the Group has recorded charges in relation to compensation payments and associated costs (projected to the fourth quarter of 2021) in 2020 in applying the recommendations, in respect of debt relief and de facto director status. During 2021, decisions from the independent panel re-review on direct and consequential losses will start to be issued, which is likely to result in further charges but it is not possible to estimate the potential impact at this stage. The Group is committed to implementing Sir Ross' recommendations in full.

The Dame Linda Dobbs review, which is considering the Group’s handling of HBOS Reading between January 2009 and January 2017, is now expected to complete towards the end of 2021. The cost of undertaking the review is included in the revised provision.

The 2020 charge of £159 million, and lifetime cost of £435 million, includes both compensation payments and operational costs.

Arrears handling related activities

The Group has provided an additional £35 million in the year ended 31 December 2020 for arrears handling related activities, bringing the total provided to date to £1,016 million; the unutilised balance at 31 December 2020 was £62 million.

INTERCHANGE FEES

With respect to multi-lateral interchange fees (MIFs), the Lloyds Banking Group is not involved in the ongoing litigation which involves card schemes such as Visa and Mastercard (as described below). However, the Group is a member/licensee of Visa and Mastercard and other card schemes. The litigation in question is as follows:

–litigation brought by retailers against both Visa and Mastercard continues in the English Courts (and includes a judgment of the Supreme Court in June 2020 upholding the Court of Appeal's finding in 2018 that historic interchange arrangements of Mastercard and Visa infringed competition law); and

–litigation brought on behalf of UK consumers in the English Courts against Mastercard, which the Supreme Court has now confirmed can proceed.

Any impact on the Group of the litigation against Visa and Mastercard remains uncertain at this time, such that it is not practicable for the Group to provide an estimate of any potential financial effect. Insofar as Visa is required to pay damages to retailers for interchange fees set prior to June 2016, contractual arrangements to allocate liability have been agreed between various UK banks (including the Lloyds Banking Group) and Visa Inc, as part of Visa Inc’s acquisition of Visa Europe in 2016. These arrangements cap the maximum amount of liability to which the Lloyds Banking Group may be subject and this cap is set at the cash consideration received by the Lloyds Banking Group for the sale of its stake in Visa Europe to Visa Inc in 2016. In 2016, the Group received Visa preference stock as part of the consideration for the sale of its shares in Visa Europe. In 2020, some of these Visa preference shares were converted into Visa Inc Class A common stock (in accordance with the provisions of the Visa Europe sale documentation) and they were subsequently sold by the Group. The sale had no impact on this contingent liability.

LIBOR AND OTHER TRADING RATES

Certain Lloyds Banking Group companies, together with other panel banks, have been named as defendants in private lawsuits, including purported class action suits, in the US in connection with their roles as panel banks contributing to the setting of US Dollar, Japanese Yen and Sterling London Interbank Offered Rate and the Australian BBSW reference rate. Certain of the plaintiffs' claims have been dismissed by the US Federal Court for the Southern District of New York (subject to appeals).

Certain Lloyds Banking Group companies are also named as defendants in (i) UK based claims; and (ii) two Dutch class actions, raising LIBOR manipulation allegations. A number of the claims against the Lloyds Banking Group in relation to the alleged mis-sale of interest rate hedging products also include allegations of LIBOR manipulation.

Furthermore, the Swiss Competition Commission concluded its investigation against Lloyds Bank plc in June 2019. However, the Lloyds Banking Group continues to respond to litigation arising out of the investigations into submissions made by panel members to the bodies that set LIBOR and various other interbank offered rates.

It is currently not possible to predict the scope and ultimate outcome on the Lloyds Banking Group of the various outstanding regulatory investigations not encompassed by the settlements, any private lawsuits or any related challenges to the interpretation or validity of any of the Lloyds Banking Group's contractual arrangements, including their timing and scale. As such, it is not practicable to provide an estimate of any potential financial effect.

TAX AUTHORITIES

The Lloyds Banking Group has an open matter in relation to a claim for group relief of losses incurred in its former Irish banking subsidiary, which ceased trading on 31 December 2010. In 2013, HMRC informed the Lloyds Banking Group that its interpretation of the UK rules means that the group relief is not available. In 2020, HMRC concluded their enquiry into the matter and issued a closure notice. The Lloyds Banking Group's interpretation of the UK rules has not changed and hence it has appealed to the First Tier Tax Tribunal, with a hearing expected in early 2022. If the final determination of the matter by the judicial process is that HMRC’s position is correct, management estimate that this would result in an increase in current tax liabilities of approximately £700 million (including interest) and a reduction in deferred tax assets of approximately £270 million. The Lloyds Banking Group, having taken appropriate advice, does not consider that this is a case where additional tax will ultimately fall due.

There are a number of other open matters on which the Group is in discussions with HMRC (including the tax treatment of certain costs arising from the divestment of TSB Banking Group plc), none of which is expected to have a material impact on the financial position of the Group.

CONTINGENT LIABILITIES RELATING TO OTHER LEGAL ACTIONS AND REGULATORY MATTERS

In addition, during the ordinary course of business the Group is subject to other complaints and threatened or actual legal proceedings (including class or group action claims) brought by or on behalf of current or former employees, customers, investors or other third parties, as well as legal and regulatory reviews, challenges, investigations and enforcement actions, both in the UK and overseas. All material such matters are periodically reassessed, with the assistance of external professional advisers where appropriate, to determine the likelihood of the Group incurring a liability. In those instances where it is concluded that it is more likely than not that a payment will be made, a provision is established to management's best estimate of the amount required at the relevant balance sheet date. In some cases it will not be possible to form a view, for example because the facts are unclear or because further time is needed properly to assess the merits of the case, and no provisions are held in relation to such matters. In these circumstances, specific disclosure in relation to a contingent liability will be made where material. However the Group does not currently expect the final outcome of any such case to have a material adverse effect on its financial position, operations or cash flows.

OPERATING AND FINANCIAL REVIEW AND PROSPECTS

The results discussed below are not necessarily indicative of Lloyds Bank Group’s results in future periods. The following information contains certain forward looking statements. For a discussion of certain cautionary statements relating to forward looking statements, see Forward looking statements.

The following discussion is based on and should be read in conjunction with the consolidated financial statements and the related notes thereto included elsewhere in this annual report. For a discussion of the accounting policies used in the preparation of the consolidated financial statements, see Accounting policies in note 2 to the financial statements.

TABLE OF CONTENTS

OPERATING AND FINANCIAL REVIEW AND PROSPECTS

CRITICAL ACCOUNTING POLICIES

The preparation of financial statements requires management to make estimates and assumptions that affect amounts reported therein. Due to the inherent uncertainty involved in making estimates, actual results reported in future periods may be based upon amounts which differ from those estimates.

The accounting policies that are deemed critical to the Lloyds Bank Group’s results and financial position, based upon materiality and significant judgements and estimates, are set out in note 3 to the financial statements.

FUTURE ACCOUNTING DEVELOPMENTS

Future developments in relation to the Lloyds Bank Group’s IFRS reporting are discussed in note 47 to the financial statements.

OPERATING AND FINANCIAL REVIEW AND PROSPECTS

RESULTS OF OPERATIONS – 2020 AND 2019

SUMMARY

| | | | | | | | |

| 2020 | 2019 |

| £m | £m |

| Net interest income | 10,770 | | 12,220 | |

| Other income | 3,815 | | 4,388 | |

| Total income | 14,585 | | 16,608 | |

| Total operating expenses | (9,196) | | (11,123) | |

| Impairment | (4,060) | | (1,362) | |

| Profit before tax | 1,329 | | 4,123 | |

| Tax credit (expense) | 137 | | (1,287) | |

| Profit for the year | 1,466 | | 2,836 | |

| | |

| Profit attributable to ordinary shareholders | 1,023 | | 2,515 | |

| Profit attributable to other equity holders | 417 | | 281 | |

| Profit attributable to equity holders | 1,440 | | 2,796 | |

| Profit attributable to non-controlling interests | 26 | | 40 | |

| Profit for the year | 1,466 | | 2,836 | |

INCOME STATEMENT COMMENTARY

During the year ended 31 December 2020, the Lloyds Bank Group recorded a profit before tax of £1,329 million, a reduction of £2,794 million, or 68 per cent, compared with £4,123 million in 2019; the decrease reflected, in particular, the Group's revised economic outlook for the UK following the outbreak of the coronavirus pandemic.The Lloyds Bank Group profit before tax for the year ended 31 December 2020 included a profit before tax of £1,856 million from its Retail division, a 16 per cent decrease compared to 2019, as lower income and a higher impairment charge have more than offset reduced provisions for conduct risk; and a profit before tax of £20 million from its Commercial Banking division.

Total income decreased by £2,023 million, or 12 per cent, to £14,585 million in 2020 compared with £16,608 million in 2019, reflecting reductions in both net interest income and other income.

Net interest income was £10,770 million in 2020, a decrease of £1,450 million, or 12 per cent compared to £12,220 million in 2019. Average interest earning banking assets increased by £19,263 million, or 3 per cent, to £573,514 in 2020 compared to £554,251 million in 2019 as a result of increased placings with central banks and growth in reverse repurchase agreement balances. Average customer lending was stable; the impact of increased balances due from SMEs under the UK Government-backed coronavirus support schemes and growth in the open mortgage book was offset by lower balances in the closed mortgage book and credit cards, as well as the continued optimisation of the Corporate and Institutional book within Commercial Banking. The net interest margin decreased, reflecting the lower rate environment, actions taken during the year to support customers and a change in asset mix, largely as a result of reduced levels of customer demand during the coronavirus pandemic.

Other income was £573 million, or 13 per cent, lower at £3,815 million in 2020 compared to £4,388 million in 2019.

Fee and commission income was £439 million, or 19 per cent, lower at £1,924 million compared to £2,363 million in 2019 as a result of decreases across most categories of fees reflecting reductions in business and transaction volumes as a result of the coronavirus pandemic as well as the impact of the transfer of business into the Lloyds Banking Group’s wealth management joint venture in 2019. Fee and commission expense decreased by £118 million, or 11 per cent, to £909 million compared with £1,027 million in 2019; interchange fees were lower as a result of reduced customer usage of ATMs during the pandemic and there were reductions in card and other fees payable. Net trading income was £390 million higher at £750 million in 2020 compared with £360 million in 2019, reflecting the change in fair value of interest rate derivatives and foreign exchange contracts in the banking book not mitigated through hedge accounting. Other operating income was £642 million, or 24 per cent, lower at £2,050 million in 2020 compared to £2,692 million in 2019, reflecting a lower level of operating lease rental income, following a reduction in the Lex vehicle fleet size, increased losses on liability management exercises and a lower level of cost recharges to other Lloyds Banking Group entities.

Operating expenses decreased by £1,927 million, or 17 per cent to £9,196 million in 2020 compared with £11,123 million in 2019 reflecting a decrease of £1,776 million in charges for redress payments to customers in respect of PPI and other conduct related matters . Excluding these charges from both years, operating expenses were £151 million, or 2 per cent, lower at £8,782 million in 2020 compared to £8,933 million in 2019. Staff costs were £370 million, or 9 per cent, lower at £3,615 million in 2020 compared with £3,985 million in 2019. This reflects a reduction in staff numbers, significantly lower accruals in respect of staff bonuses and reduced levels of agency staff only partly offset by higher redundancy costs. Premises and equipment costs were £21 million lower at £425 million in 2020 compared with £446 million in 2019 reflecting increased gains on the disposal of tangible fixed assets, only partly offset by the cost of making the Group's premises COVID-secure. Other expenses were £168 million, or 9 per cent, higher at £2,068 million in 2020 compared with £1,900 million in 2019 mainly reflecting increased investment spend and cost recharges from Lloyds Banking Group plc. Depreciation and amortisation costs were £68 million, or 3 per cent, higher at £2,670 million in 2020 compared to £2,602 million in 2019 due to increased levels of software capitalisation.

The Group incurred a regulatory provisions charge in operating expenses of £414 million in 2020 compared to £2,190 million in 2019. Of this amount £85 million related to payment protection insurance; this charge was driven by the impact of coronavirus delaying operational activities during 2020, the final stages of work to ensure operational completeness and final validation of information requests and complaints with third parties that resulted in a limited number of additional complaints to be handled. Of the approximately six million enquiries received pre-deadline, more than 99 per cent have now been processed. A small part of the costs incurred during the year also reflect the costs associated with litigation activity to date. The unutilised provision, excluding MBNA, at 31 December 2020 was £198 million The charge in relation to other conduct issues was £329 million in 2020, compared to £395 million in 2019. During the year additional charges, both redress and operational costs of £159 million, have been taken in relation to HBOS Reading, as well as further costs in relation to arrears handling, packaged bank account complaints and various settlements in relation to historic claims. A number of programmes are now close to conclusion. Others, such as HBOS Reading, including the conclusion of the recommendations from the Cranston Review, are still ongoing and further costs are likely to be incurred.

OPERATING AND FINANCIAL REVIEW AND PROSPECTS