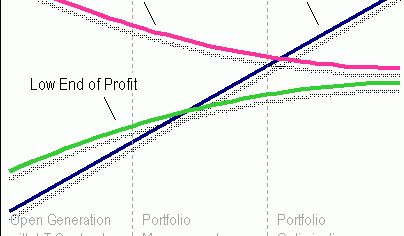

3 Important Information This presentation is intended to provide additional information regarding the hedging program at Exelon Generation and to serve as an aid for the purposes of modeling Exelon Generation’s gross margin (operating revenues less purchased power and fuel expense). The information in this presentation is not intended to represent earnings guidance or a forecast of future events. In fact, many of the factors that ultimately will determine Exelon Generation’s actual gross margin are based upon highly variable market factors outside of our control. The information in this presentation is as of February 28, 2009. Going forward, we plan to update the information on a quarterly basis. Certain information in this presentation is based upon an internal simulation model that incorporates assumptions regarding future market conditions, including power and commodity prices, heat rates and demand conditions, in addition to operating performance and dispatch characteristics of our generating fleet. Our simulation model and the assumptions therein are subject to change. For example, actual market conditions and the dispatch profile of our generation fleet in future periods will likely differ – and may differ significantly – from the assumptions underlying the simulation results included in this presentation. In addition, the forward-looking information included in this presentation will likely change over time due to continued refinement of our simulation model and changes in our views on future market conditions. |