Exelon’s Acquisition of John Deere Renewables August 31, 2010 Exhibit 99.2 |

2 Forward-Looking Statements This presentation includes forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, that are subject to risks and uncertainties. The factors that could cause actual results to differ materially from these forward-looking statements include those discussed herein as well as those discussed in (1) Exelon’s 2009 Annual Report on Form 10-K in (a) ITEM 1A. Risk Factors, (b) ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and (c) ITEM 8. Financial Statements and Supplementary Data: Note 18; (2) Exelon’s Second Quarter 2010 Quarterly Report on Form 10-Q in (a) Part II, Other Information, ITEM 1A. Risk Factors, (b) Part 1, Financial Information, ITEM 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations and (c) Part I , Financial Information, ITEM 1. Financial Statements: Note 12 and (3) other factors discussed in filings with the Securities and Exchange Commission (SEC) by Exelon Corporation and Exelon Generation Company, LLC (Companies). Readers are cautioned not to place undue reliance on these forward-looking statements, which apply only as of the date of this presentation. None of the Companies undertakes any obligation to publicly release any revision to its forward-looking statements to reflect events or circumstances after the date of this presentation. |

3 Transaction Summary Components of purchase price • $860M for operating assets and advanced-stage Michigan development projects • Up to $40M in additional payments contingent on commencement of construction on Michigan development projects • Equivalent to ~$1,000/KW Financing • Exelon will fund transaction with Exelon Generation debt (no equity issuance) • Clean capital structure with no tax equity and project debt (1) • Ability to utilize production tax credits 735 MW operating portfolio spread across 36 projects located in eight states • 75% of the operating portfolio is sold under long-term power purchase arrangements • 86% of contracted portfolio has PPAs through 2026 or beyond 1,468 MW in development pipeline • PPAs have already been executed for 230 MW in Michigan – projects expected to be operational in 2012-2013 Acquisition positions Exelon as a large wind operator, complementing its world-class nuclear fleet (1) Except for $1.8M loan from Illinois Finance Authority for AgriWind project in IL |

4 Strategic Rationale Diversify with additional clean generation • JDR’s proven wind platform provides unique opportunity and entry point into U.S. wind business • Provides diversity in geographic presence and generation type • Supports Exelon 2020 by adding more “clean” generation to our portfolio and positions us for potential federal RPS Contracted portfolio with option for future growth • 75% of operating portfolio sold under long-term PPAs • 1,468 additional MW in pipeline, of which 230 MW have executed PPAs • Only plan further development of contracted assets Attractive economics and good fit • Purchase price compares favorably with other wind transactions • Disciplined investment approach aligned with Exelon’s approach • Addition of strong renewable energy development team Acquisition further enhances Exelon’s strong environmental leadership and provides future opportunities for incremental development |

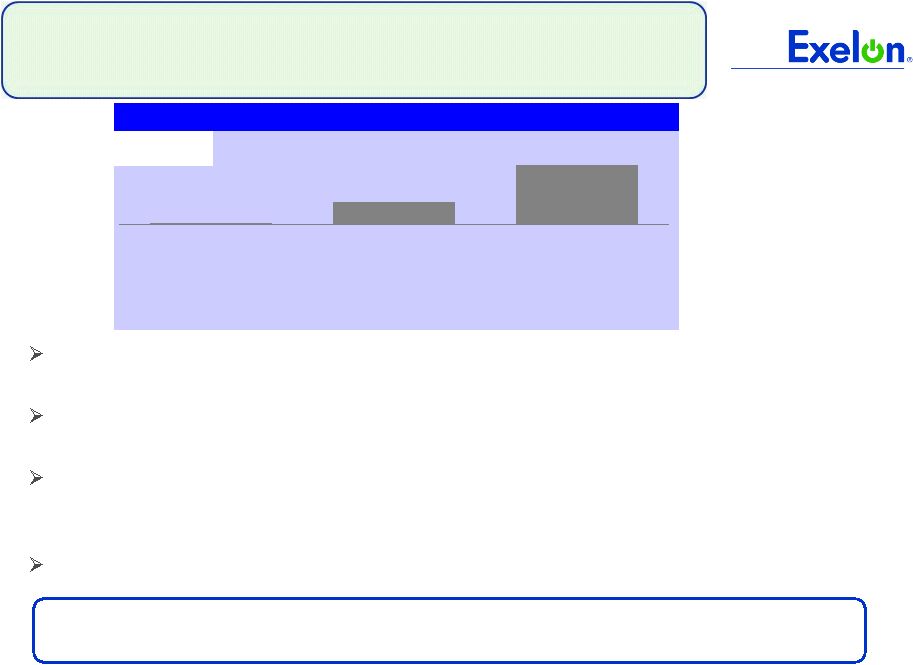

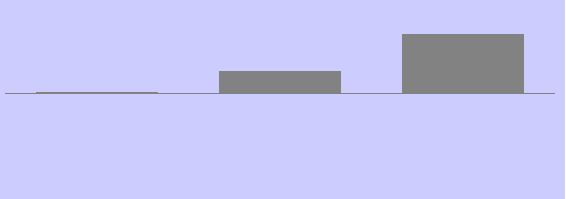

5 Financials Are Attractive Economics for operating and advanced development portfolio are attractive EPS breakeven in 2011, accretive beginning in 2012 • Assumes transaction is funded with 100% debt EBITDA run-rate of ~$150M/year including PTCs (1) (including Michigan development projects) Free cash flow accretive by 2013 • Includes estimated capex (before tax incentives) of $450-$500M in 2011-2012 for Michigan development projects Expect transaction to have minimal impact on credit metrics EPS Accretion / Dilution 0.0% 0.6% 1.5% 2011E 2012E 2013E (1) Production Tax Credits |

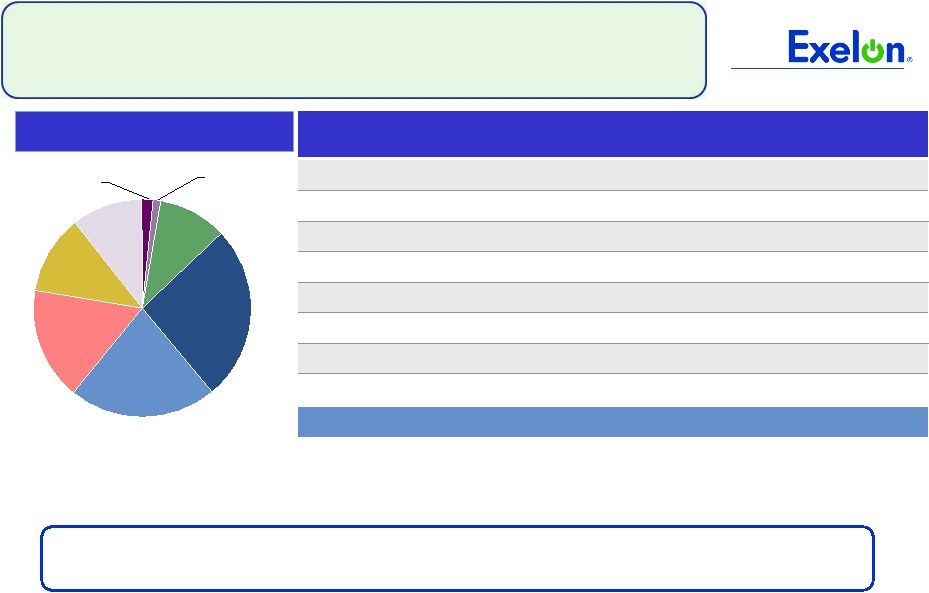

6 6 Asset Profile – Operating The portfolio is largely made up of contracted operating assets Geographic Distribution TX, 26% MO, 22% MI, 17% ID, 12% MN, 11% OR, 10% KS, 2% IL, 1% Note: There is ongoing litigation with Southwest Public Service related to PURPA contracts which could impact the price at which the generation from these units is sold. Cracking issues experienced by Deere on certain Suzlon turbine blades have been addressed to our satisfaction. We have factored both items into our valuation. Project State MW # of Wind Projects Ownership Placed in Service Date PPA End Date Federal Incentive Off-Taker Idaho 88.2 3 100% 2009/2010 2028/2030 ITC Grant Idaho Power Illinois 8.4 1 99% 2008 2018 PTC Wabash Valley Power Kansas 12.5 1 100% 2010 2030 PTC Kansas Power Pool Michigan 121.8 2 100% 2008 2018/2028 PTC Wolverine Power Supply / Consumers Energy Minnesota 77.7 9 94%-100% 2003/2008 2018/2028 PTC Various Missouri 162.5 4 99%-100% 2008 2027 PTC Associated Electric / MO Joint Municipal Oregon 74.5 4 99%-100% 2009 2029 ITC Grant PacifiCorp Texas 189.8 12 100% 2006/2009 N/A PTC Southwest Public Service Total 735.4 36 |

7 7 Asset Profile – Pipeline PPAs already executed for these projects Development pipeline includes wind projects ranging from 20 MW to 300 MW Development of projects to be considered on a case-by-case basis State Project Name MW MI Michigan Wind II 90 MI Harvest II 59 MI Blissfield (MW IV) 81 Total 230 Projects to be developed by Exelon Optional projects for development Ohio 198 Michigan 40 Idaho 20 Texas 760 Maine 50 Colorado 40 Oregon 30 California 100 Total 1,238 Total 1,468 |

8 Regulatory Approval Process FERC approval required DOJ antitrust approval required under the Hart-Scott-Rodino Antitrust Improvements Act Other than Texas, no state approval is necessary Expect to close transaction in 4Q 2010; no material issues expected |