Bank of America Merrill Lynch 2011 Power and Gas Leaders Conference Christopher M Crane – President and COO, Exelon Corp. September 20, 2011 EXHIBIT 99.1 |

Cautionary Statements Regarding Forward-Looking Information 2 Except for the historical information contained herein, certain of the matters discussed in this communication constitute “forward-looking statements” within the meaning of the Securities Act of 1933 and the Securities Exchange Act of 1934, both as amended by the Private Securities Litigation Reform Act of 1995. Words such as “may,” “will,” “anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “believe,” “target,” “forecast,” and words and terms of similar substance used in connection with any discussion of future plans, actions, or events identify forward-looking statements. These forward-looking statements include, but are not limited to, statements regarding benefits of the proposed merger of Exelon Corporation (Exelon) and Constellation Energy Group, Inc. (Constellation), integration plans and expected synergies, the expected timing of completion of the transaction, anticipated future financial and operating performance and results, including estimates for growth. These statements are based on the current expectations of management of Exelon and Constellation, as applicable. There are a number of risks and uncertainties that could cause actual results to differ materially from the forward-looking statements included in this communication regarding the proposed merger. For example, (1) the companies may be unable to obtain shareholder approvals required for the merger; (2) the companies may be unable to obtain regulatory approvals required for the merger, or required regulatory approvals may delay the merger or result in the imposition of conditions that could have a material adverse effect on the combined company or cause the companies to abandon the merger; (3) conditions to the closing of the merger may not be satisfied; (4) an unsolicited offer of another company to acquire assets or capital stock of Exelon or Constellation could interfere with the merger; (5) problems may arise in successfully integrating the businesses of the companies, which may result in the combined company not operating as effectively and efficiently as expected; (6) the combined company may be unable to achieve cost- cutting synergies or it may take longer than expected to achieve those synergies; (7) the merger may involve unexpected costs, unexpected liabilities or unexpected delays, or the effects of purchase accounting may be different from the companies’ expectations; (8) the credit ratings of the combined company or its subsidiaries may be different from what the companies expect; (9) the businesses of the companies may suffer as a result of uncertainty surrounding the merger; (10) the companies may not realize the values expected to be obtained for properties expected or required to be divested; (11) the industry may be subject to future regulatory or legislative actions that could adversely affect the companies; and (12) the companies may be adversely affected by other economic, business, and/or competitive factors. Other unknown or unpredictable factors could also have material adverse effects on future results, performance or achievements of Exelon, Constellation or the combined company. |

Cautionary Statements Regarding Forward-Looking Information (Continued) 3 Discussions of some of these other important factors and assumptions are contained in Exelon’s and Constellation’s respective filings with the Securities and Exchange Commission (SEC), and available at the SEC’s website at www.sec.gov, including: (1) Exelon’s 2010 Annual Report on Form 10-K in (a) ITEM 1A. Risk Factors, (b) ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and (c) ITEM 8. Financial Statements and Supplementary Data: Note 18; (2) Exelon’s Quarterly Report on Form 10-Q for the quarterly period ended June 30, 2011 in (a) Part II, Other Information, ITEM 1A. Risk Factors, (b) Part 1, Financial Information, ITEM 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations and (c) Part I, Financial Information, ITEM 1. Financial Statements: Note 13; (3) Constellation’s 2010 Annual Report on Form 10-K in (a) ITEM 1A. Risk Factors, (b) ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and (c) ITEM 8. Financial Statements and Supplementary Data: Note 12; and (4) Constellation’s Quarterly Report on Form 10-Q for the quarterly period ended June 30, 2011 in (a) Part II, Other Information, ITEM 1A. Risk Factors and ITEM 5. Other Information, (b) Part I, Financial Information, ITEM 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations and (c) Part I, Financial Information, ITEM 1. Financial Statements: Notes to Consolidated Financial Statements, Commitments and Contingencies. These risks, as well as other risks associated with the proposed merger, are more fully discussed in the preliminary joint proxy statement/prospectus included in Amendment No. 1 to the Registration Statement on Form S-4 that Exelon filed with the SEC on August 17, 2011 in connection with the proposed merger. In light of these risks, uncertainties, assumptions and factors, the forward-looking events discussed in this communication may not occur. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this communication. Neither Exelon nor Constellation undertake any obligation to publicly release any revision to its forward-looking statements to reflect events or circumstances after the date of this communication. Additional Information and Where to Find It This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities, or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. On August 17, 2011, Exelon filed with the SEC Amendment No. 1 to its Registration Statement on Form S-4 that included a preliminary joint proxy statement/prospectus and other relevant documents to be mailed by Exelon and Constellation to their respective security holders in connection with the proposed merger of Exelon and Constellation. |

Additional Information and Where to Find It These materials are not yet final and may be amended. WE URGE INVESTORS AND SECURITY HOLDERS TO READ THE PRELIMINARY JOINT PROXY STATEMENT/PROSPECTUS AND THE DEFINITIVE JOINT PROXY STATEMENT/PROSPECTUS AND ANY OTHER RELEVANT DOCUMENTS WHEN THEY BECOME AVAILABLE, BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION about Exelon, Constellation and the proposed merger. Investors and security holders will be able to obtain these materials (when they are available) and other documents filed with the SEC free of charge at the SEC's website, www.sec.gov. In addition, a copy of the preliminary joint proxy statement/prospectus and definitive joint proxy statement/prospectus (when it becomes available) may be obtained free of charge from Exelon Corporation, Investor Relations, 10 South Dearborn Street, P.O. Box 805398, Chicago, Illinois 60680-5398, or from Constellation Energy Group, Inc., Investor Relations, 100 Constellation Way, Suite 600C, Baltimore, MD 21202. Investors and security holders may also read and copy any reports, statements and other information filed by Exelon, or Constellation, with the SEC, at the SEC public reference room at 100 F Street, N.E., Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 or visit the SEC’s website for further information on its public reference room. Participants in the Merger Solicitation Exelon, Constellation, and their respective directors, executive officers and certain other members of management and employees may be deemed to be participants in the solicitation of proxies in respect of the proposed transaction. Information regarding Exelon’s directors and executive officers is available in its proxy statement filed with the SEC by Exelon on March 24, 2011 in connection with its 2011 annual meeting of shareholders, and information regarding Constellation’s directors and executive officers is available in its proxy statement filed with the SEC by Constellation on April 15, 2011 in connection with its 2011 annual meeting of shareholders. Other information regarding the participants in the proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, is contained in the preliminary joint proxy statement/prospectus and will be contained in the definitive joint proxy statement/prospectus. 4 |

Creating Value Through a Strategic Merger Delivers financial benefits to both sets of shareholders Increases scale and scope of the business across the value chain Matches the industry’s premier clean merchant generating fleet with the leading retail and wholesale customer platform Diversifies the generation portfolio Continued upside to power market recovery Maintains a strong regulated earnings profile with large urban utilities Successful integration experience from prior mergers and acquisitions Combining Exelon’s generation fleet and Constellation’s customer-facing businesses creates a strong platform for growth and delivers benefits to investors and customers 5 |

Combination Will Result in Enhanced Scale, Scope, Flexibility and Financial Strength • $8 billion • $11 billion • 11,980 (Total) • 1,921 (Nuclear) • 1.2 mil. (MD) • 0.7 mil. (MD) • 44 states & D.C. (5) • ~110 TWh/yr • 29% Generation • 44% Utility • 27% NewEnergy Market Value and Enterprise Value (1) Pro forma Standalone Owned Generation (in MW) (2) Regulated Utilities Competitive Retail & Wholesale (4) Business Mix (6) • $28 billion • $41 billion • 26,339 (Total) • 17,047 (Nuclear) Electric customers • 5.4 mil. (IL, PA) Gas customers • 0.5 mil. (PA) • 4 states • ~59 TWh/yr 2011 EBITDA • 61% Generation • 39% Utilities • $35 billion • $52 billion • 44 states & D.C. (5) • ~169 TWh energy sales • Expect >50% pro forma EBITDA from competitive business • 35,671 (Total) (3) • 18,968 (Nuclear) • 6.6 million electric & gas customers in IL, PA and MD Note: Data as of 12/31/10 unless stated otherwise. (1) Market Value as of 9/14/11. Enterprise Value represents Market Value plus Net Debt as of 6/30/11. (2) Exelon data includes 720 MW for Wolf Hollow. Constellation data includes 2,950 MW for Boston Generation assets. (3) Net of physical market mitigation assumed to be 2,648 MW. (4) TWh/yr represents 2011 booked electric sales as of 12/31/2010. Exelon load includes ComEd swap. Data also includes 2011 partial year estimated electric sales from StarTex and MXEnergy (acquired by Constellation). (5) Competitive and wholesale business also active in Alberta, British Columbia and Ontario, Canada. (6) Exelon EBITDA estimates per equity research. Constellation EBITDA estimates per company guidance from Q1 2011. 6 |

On Track for Merger Close in Early Q1 2012 2011 2012 Q3 Q4 Q1 Filed for indirect transfer of Constellation Energy licenses on May 12, 2011 Expect approval in Q4 Filed merger approval application related filings on May 20, 2011 Submitted HSR filing on May 31, 2011 for review under U.S. antitrust laws Filed for approval with the Maryland PSC on May 25, 2011 Approvals Shareholder vote Shareholder vote 1/5/12 Decision deadline SEC NRC Texas PUCT Secured approval from Texas FERC DOJ NY PSC MD PSC Regulatory proceedings are progressing well and we are on track to close in early Q1, 2012 Proxy mailing SEC has completed its review of S-4 7 |

Project Nuclear Uprates Wind Wolf Hollow Acquisition RiteLine Investment $3.3 billion $490 million $305 million $1.1 billion Capacity 1,300 MW 230 MW 720 MW N.A. States IL, PA MI TX IL, IN,OH Committed To Value Driven Growth 8 Capitalize on operational excellence Straight forward regulatory approval process Investment flexibility Efficient tax structure and equity recovery Low risk and stable cash flows Expansion in a new market (MI) Commitment to competitive markets Attractive purchase price and upside opportunity in TX Pre-determined and guaranteed return on equity Enhance reliability and support renewable integration Nuclear Renewables CCGT Transmission These investments further our commitment to Exelon 2020 and a low carbon future, while providing attractive financial returns and diversifying our earnings within the merchant segment of our business |

Three Major Categories of Exelon Uprates Uprates Overnight Cost (1) MUR (Measurement Uncertainty Recapture) • Through the use of advanced techniques and more precise instrumentation, reactor power can be more accurately calculated • Can achieve up to 1.7% additional output • Requires NRC approval 197–233 MW $330M 2-3 years 745–826 MW $2,155M EPU (Extended Power Uprate) • Through a combination of more sophisticated analysis and upgrades to plant equipment, uprates can increase output by as much as 20% of original licensed power level • Requires NRC approval 3 - 6 years 234–255 MW $790M Megawatt Recovery and Component Upgrades • Replacement of major components in the plant occur in the normal life cycle process – with newer technology, replacements result in increased efficiency • Equipment includes generators, turbines, motors and transformers • Megawatt Recovery and Component Upgrades must conform to NRC standards, but do not require additional NRC approval 3-4 years ~1,175–1,300 MW $3,275M Project Duration (1) In 2011 dollars. Overnight costs do not include financing costs or cost escalation. Estimated Internal Rate of Return 12-14% 13-16% 10-14% Refined scenario analysis highlights that uprates continue to be economic 9 |

Wolf Hollow Acquisition and Exelon Wind Diversifies generation portfolio : • Expands geographic and fuel characteristics of fleet • Advances our merger strategy of matching load with generation Creates value for shareholders : • $305M purchase price compares favorably to recent transactions • Free cash flow accretive beginning in 2012 • Opportunity to benefit from future market heat rate expansion in ERCOT ERCOT : Electric Reliability Council of Texas; COD : Commercial Operation Date Wolf Hollow Acquisition – Successfully closed on August 24, 2011 Exelon Wind – Successfully executing on development projects Successfully acquired and integrated a sizeable wind generation portfolio Moving ahead with three development projects • Michigan Wind 2 project (90 MWs) expected COD December 2011 • Harvest II wind project (59.4 MWs) expected COD December 2012 • Blissfield wind project (81 MW) expected COD December 2012 10 |

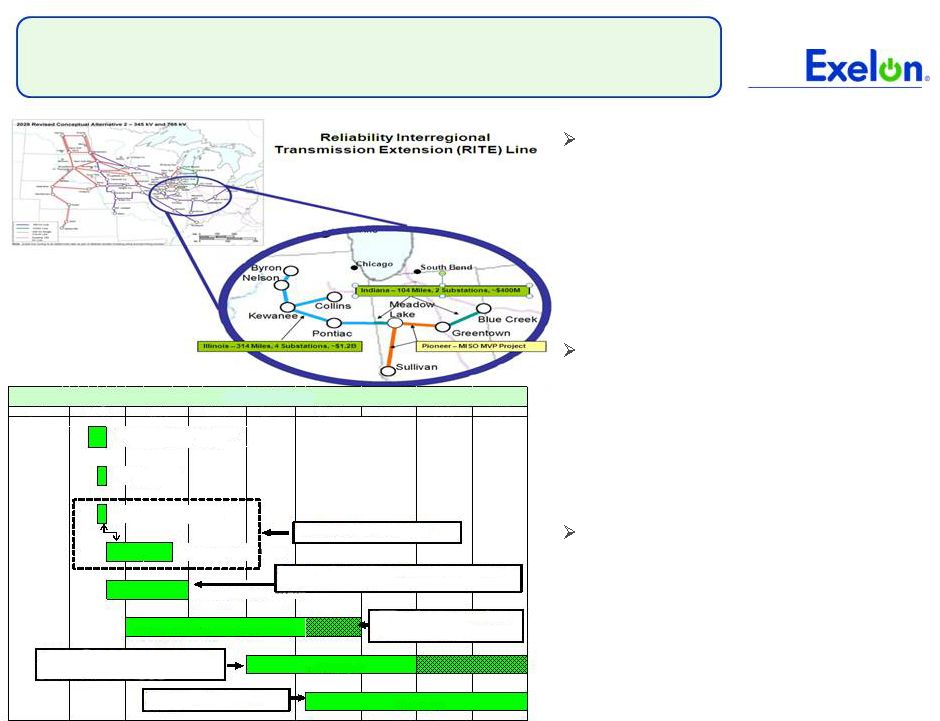

RITE Line Project Update Project Background • 420 miles of 765kV transmission stretches from Northern Illinois to Ohio. The RITE Line will be built from the existing 765kV system in Ohio in the East to the West • Estimated construction to begin 2015 pending regulatory approvals and siting Strategic and Financial Objectives • Ensures reliability, enables states to meet RPS standards, and supports the integration of more renewables • ComEd/Exelon investment ~ $1.1 billion • Requested ROE 12.70% Latest Developments • Signed partnership agreement with ETA on July 13 • Completed FERC incentive rate filing on July 18. Expect FERC ruling by October 2011. Note: ETA = Electric Transmission America RPS = Renewable Portfolio Standards RTEP = Regional Transmission Expansion Planning 11 2016 2017 2018 FERC Final Rule on NOPR PJM Compliance Filing 2010 State Local Outreach & Project Siting Establish Definitive Agreement Between Exelon & ETA 2012 FERC Incentive Construction RITE Line 2013 2011 2015 In-Service Pursue PJM RTEP Approval RTEP Approval expected by 2012, depending on PJM Planning criteria Time length is dependent on: 1. Land negotiations 2. Receipt of State Line can be in-serviced in phases Construction can range from 3-5 yrs depending on the length of time needed to site the project Non Project Specific Events 2014 Filing - |

Exelon Generation Hedging Disclosures (as of June 30, 2011) 12 |

Important Information 13 The following slides are intended to provide additional information regarding the hedging program at Exelon Generation and to serve as an aid for the purposes of modeling Exelon Generation’s gross margin (operating revenues less purchased power and fuel expense). The information on the following slides is not intended to represent earnings guidance or a forecast of future events. In fact, many of the factors that ultimately will determine Exelon Generation’s actual gross margin are based upon highly variable market factors outside of our control. The information on the following slides is as of June 30, 2011. We update this information on a quarterly basis. Certain information on the following slides is based upon an internal simulation model that incorporates assumptions regarding future market conditions, including power and commodity prices, heat rates, and demand conditions, in addition to operating performance and dispatch characteristics of our generating fleet. Our simulation model and the assumptions therein are subject to change. For example, actual market conditions and the dispatch profile of our generation fleet in future periods will likely differ – and may differ significantly – from the assumptions underlying the simulation results included in the slides. In addition, the forward- looking information included in the following slides will likely change over time due to continued refinement of our simulation model and changes in our views on future market conditions. |

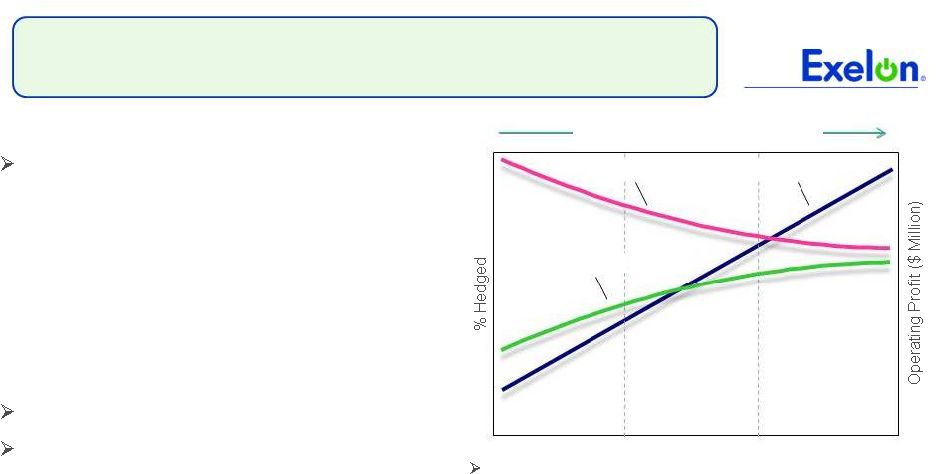

Portfolio Management Objective Align Hedging Activities with Financial Commitments Power Team utilizes several product types and channels to market • Wholesale and retail sales • Block products • Load-following products and load auctions • Put/call options Exelon’s hedging program is designed to protect the long-term value of our generating fleet and maintain an investment-grade balance sheet • Hedge enough commodity risk to meet future cash requirements if prices drop • Consider: financing policy (credit rating objectives, capital structure, liquidity); spending (capital and O&M); shareholder value return policy Consider market, credit, operational risk Approach to managing volatility • Increase hedging as delivery approaches • Have enough supply to meet peak load • Purchase fossil fuels as power is sold • Choose hedging products based on generation portfolio – sell what we own • Heat rate options • Fuel products • Capacity • Renewable credits % Hedged High End of Profit Low End of Profit Open Generation with LT Contracts Portfolio Optimization Portfolio Management Portfolio Management Over Time 14 |

Percentage of Expected Generation Hedged • How many equivalent MW have been hedged at forward market prices; all hedge products used are converted to an equivalent average MW volume • Takes ALL hedges into account whether they are power sales or financial products Equivalent MWs Sold Expected Generation = Our normal practice is to hedge commodity risk on a ratable basis over the three years leading to the spot market • Carry operational length into spot market to manage forced outage and load-following risks • By using the appropriate product mix, expected generation hedged approaches the mid-90s percentile as the delivery period approaches • Participation in larger procurement events, such as utility auctions, and some flexibility in the timing of hedging may mean the hedge program is not strictly ratable from quarter to quarter Exelon Generation Hedging Program 15 |

2011 2012 2013 Estimated Open Gross Margin ($ millions) (1)(2) $5,450 $5,000 $5,600 Open gross margin assumes all expected generation is sold at the Reference Prices listed below Reference Prices (1) Henry Hub Natural Gas ($/MMBtu) NI-Hub ATC Energy Price ($/MWh) PJM-W ATC Energy Price ($/MWh) ERCOT North ATC Spark Spread ($/MWh) (3) $4.37 $33.18 $46.07 $3.77 $4.84 $33.10 $46.02 $1.40 $5.16 $34.45 $47.45 $2.27 Exelon Generation Open Gross Margin and Reference Prices 16 (1) Based on June 30, 2011 market conditions. (2) Gross margin is defined as operating revenues less fuel expense and purchased power expense, excluding the impact of decommissioning and other incidental revenues. Open gross margin is estimated based upon an internal model that is developed by dispatching our expected generation to current market power and fossil fuel prices. Open gross margin assumes there is no hedging in place other than fixed assumptions for capacity cleared in the RPM auctions and uranium costs for nuclear power plants. Open gross margin contains assumptions for other gross margin line items such as various ISO bill and ancillary revenues and costs and PPA capacity revenues and payments. The estimation of open gross margin incorporates management discretion and modeling assumptions that are subject to change. (3) ERCOT North ATC spark spread using Houston Ship Channel Gas, 7,200 heat rate, $2.50 variable O&M. |

2011 2012 2013 Expected Generation (GWh) (1) 166,100 165,600 163,000 Midwest 99,000 97,900 95,800 Mid-Atlantic 56,300 57,100 56,500 South & West 10,800 10,600 10,700 Percentage of Expected Generation Hedged (2) 95-98% 82-85% 49-52% Midwest 95-98 81-84 48-51 Mid-Atlantic 96-99 85-88 50-53 South & West 86-89 63-66 45-48 Effective Realized Energy Price ($/MWh) (3) Midwest $43.00 $41.00 $40.00 Mid-Atlantic $57.00 $50.00 $50.50 South & West $4.50 $0.00 ($2.00) Generation Profile 17 (1) Expected generation represents the amount of energy estimated to be generated or purchased through owned or contracted for capacity. Expected generation is based upon a simulated dispatch model that makes assumptions regarding future market conditions, which are calibrated to market quotes for power, fuel, load following products, and options. Expected generation assumes 12 refueling outages in 2011 and 10 refueling outages in 2012 and 2013 at Exelon-operated nuclear plants and Salem. Expected generation assumes capacity factors of 93.0%, 93.4% and 93.2% in 2011, 2012 and 2013 at Exelon-operated nuclear plants. These estimates of expected generation in 2012 and 2013 do not represent guidance or a forecast of future results as Exelon has not completed its planning or optimization processes for those years. (2) Percent of expected generation hedged is the amount of equivalent sales divided by the expected generation. Includes all hedging products, such as wholesale and retail sales of power, options, and swaps. Uses expected value on options. Reflects decision to permanently retire Cromby Station and Eddystone Units 1&2 as of May 31, 2011. (3) Effective realized energy price is representative of an all-in hedged price, on a per MWh basis, at which expected generation has been hedged. It is developed by considering the energy revenues and costs associated with our hedges and by considering the fossil fuel that has been purchased to lock in margin. It excludes uranium costs and RPM capacity revenue, but includes the mark-to- market value of capacity contracted at prices other than RPM clearing prices including our load obligations. It can be compared with the reference prices used to calculate open gross margin in order to determine the mark-to-market value of Exelon Generation's energy hedges. |

Gross Margin Sensitivities with Existing Hedges ($ millions) (1) Henry Hub Natural Gas + $1/MMBtu - $1/MMBtu NI-Hub ATC Energy Price +$5/MWH -$5/MWH PJM-W ATC Energy Price +$5/MWH -$5/MWH Nuclear Capacity Factor +1% / -1% 2011 $5 $(5) $5 $(5) $5 $(5) +/- $25 2012 $85 $(35) $95 $(75) $55 $(55) +/- $45 2013 $340 $(290) $250 $(245) $155 $(150) +/- $50 Exelon Generation Gross Margin Sensitivities (with Existing Hedges) 18 (1) Based on June 30, 2011 market conditions and hedged position. Gas price sensitivities are based on an assumed gas-power relationship derived from an internal model that is updated periodically. Power prices sensitivities are derived by adjusting the power price assumption while keeping all other prices inputs constant. Due to correlation of the various assumptions, the hedged gross margin impact calculated by aggregating individual sensitivities may not be equal to the hedged gross margin impact calculated when correlations between the various assumptions are also considered. |

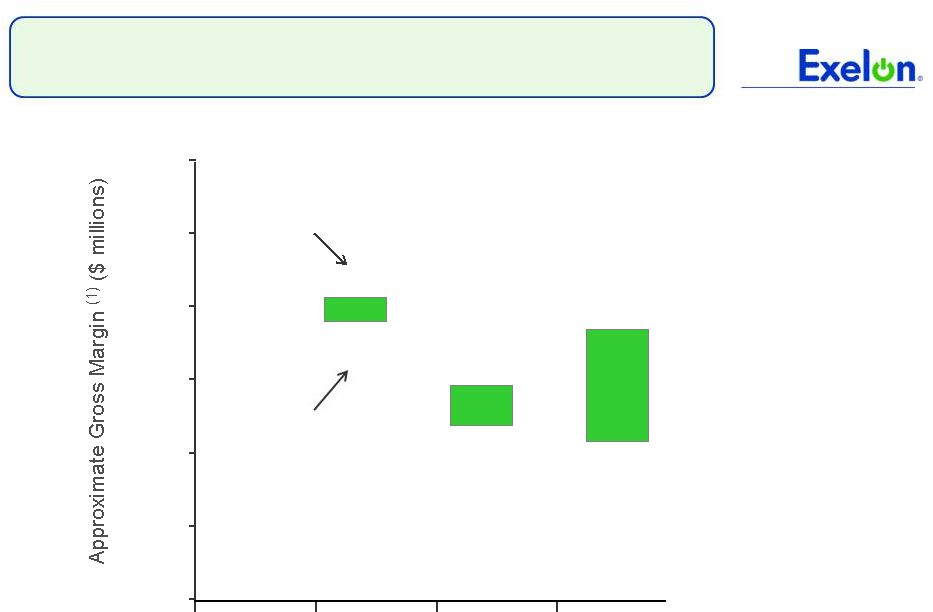

95% case 5% case $5,500 $7,100 $6,900 $6,000 Exelon Generation Gross Margin Upside / Risk (with Existing Hedges) $3,000 $4,000 $5,000 $6,000 $7,000 $8,000 $9,000 2011 2012 2013 $6,800 $5,200 19 (1) Represents an approximate range of expected gross margin, taking into account hedges in place, between the 5th and 95th percent confidence levels assuming all unhedged supply is sold into the spot market. Approximate gross margin ranges are based upon an internal simulation model and are subject to change based upon market inputs, future transactions and potential modeling changes. These ranges of approximate gross margin in 2012 and 2013 do not represent earnings guidance or a forecast of future results as Exelon has not completed its planning or optimization processes for those years. The price distributions that generate this range are calibrated to market quotes for power, fuel, load following products, and options as of June 30, 2011. |

Illustrative Example of Modeling Exelon Generation 2011 Gross Margin (with Existing Hedges) 20 Midwest Mid-Atlantic South & West Step 1 Start with fleetwide open gross margin $5.45 billion Step 2 Determine the mark-to-market value of energy hedges 99,000GWh * 96% * ($43.00/MWh-$33.18MWh) = $0.93 billion 56,300GWh * 97% * ($57.00/MWh-$46.07MWh) = $0.60 billion 10,800GWh * 87% * ($4.50/MWh-$3.77MWh) = $0.00 billion Step 3 Estimate hedged gross margin by adding open gross margin to mark-to- market value of energy hedges Open gross margin: $5.45 billion MTM value of energy hedges: $0.93 billion + $0.60 billion + $0.00 billion Estimated hedged gross margin: $6.98 billion |

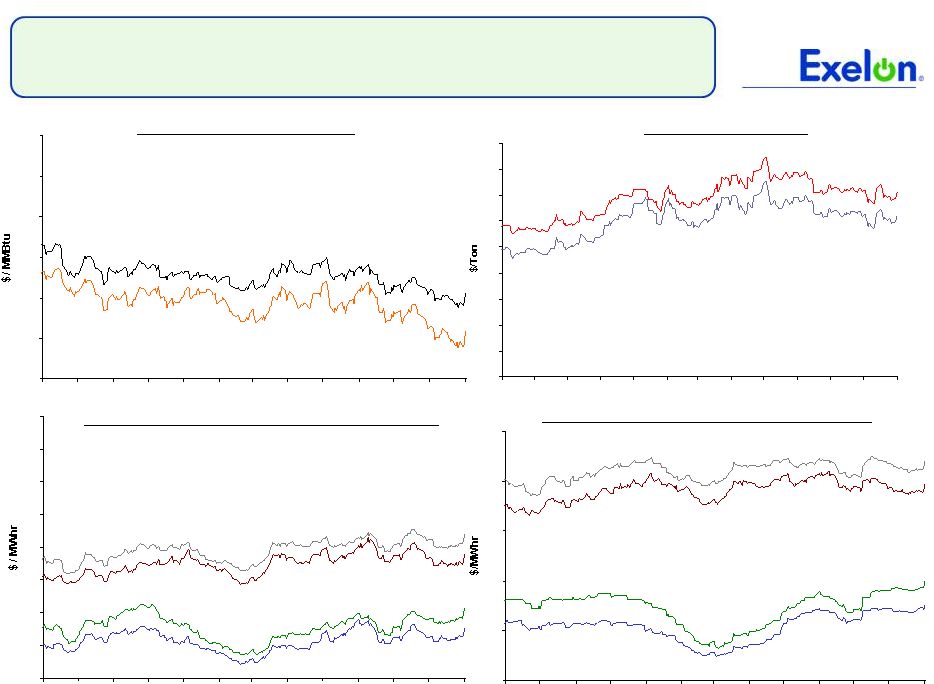

20 25 30 35 40 45 8/10 9/10 10/10 11/10 12/10 1/11 2/11 3/11 4/11 5/11 6/11 7/11 8/11 35 40 45 50 55 60 65 70 75 8/10 9/10 10/10 11/10 12/10 1/11 2/11 3/11 4/11 5/11 6/11 7/11 8/11 4.0 4.5 5.0 5.5 6.0 6.5 7.0 8/10 9/10 10/10 11/10 12/10 1/11 2/11 3/11 4/11 5/11 6/11 7/11 8/11 50 55 60 65 70 75 80 85 90 95 8/10 9/10 10/10 11/10 12/10 1/11 2/11 3/11 4/11 5/11 6/11 7/11 8/11 Market Price Snapshot Forward NYMEX Natural Gas PJM-West and Ni-Hub On-Peak Forward Prices PJM-West and Ni-Hub Wrap Forward Prices 2012 $4.58 2013 $5.05 Forward NYMEX Coal 2012 $81.06 2013 $85.51 2012 Ni-Hub $42.62 2013 Ni-Hub $45.58 2013 PJM-West $56.91 2012 PJM-West $53.84 2012 Ni-Hub $27.61 2013 Ni-Hub $30.00 2013 PJM-West $42.07 2012 PJM-West $39.62 21 Rolling 12 months, as of August 31 2011. Source: OTC quotes and electronic trading system. Quotes are daily. st |

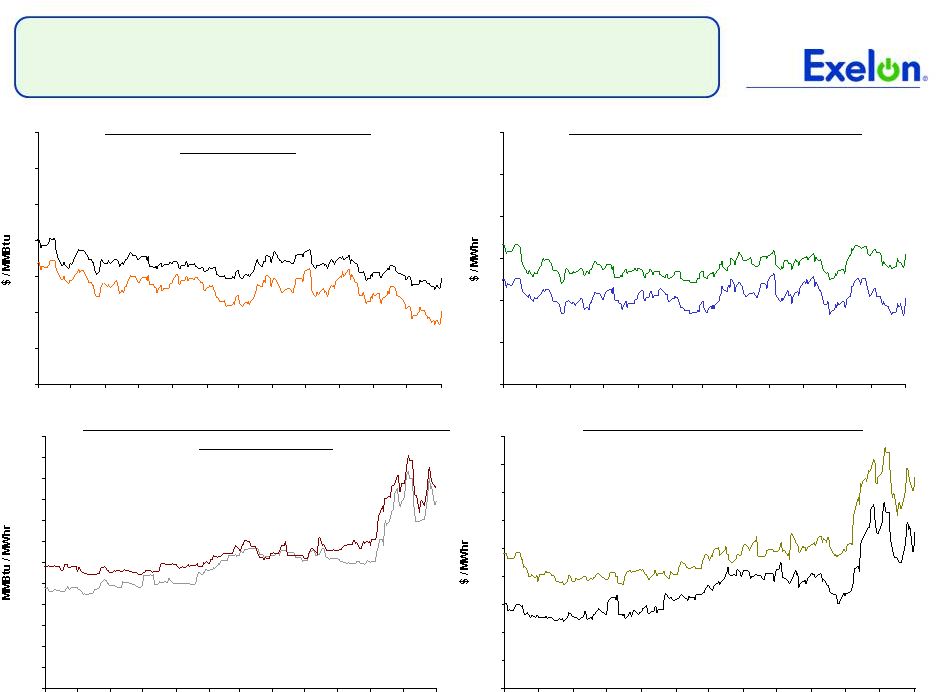

4.5 5.5 6.5 7.5 8.5 9.5 10.5 11.5 12.5 13.5 8/10 9/10 10/10 11/10 12/10 1/11 2/11 3/11 4/11 5/11 6/11 7/11 8/11 8.2 8.4 8.6 8.8 9.0 9.2 9.4 9.6 9.8 10.0 10.2 10.4 10.6 8/10 9/10 10/10 11/10 12/10 1/11 2/11 3/11 4/11 5/11 6/11 7/11 8/11 35 40 45 50 55 60 65 8/10 9/10 10/10 11/10 12/10 1/11 2/11 3/11 4/11 5/11 6/11 7/11 8/11 3.5 4.0 4.5 5.0 5.5 6.0 6.5 7.0 8/10 9/10 10/10 11/10 12/10 1/11 2/11 3/11 4/11 5/11 6/11 7/11 8/11 Market Price Snapshot 2013 10.14 2012 10.00 2012 $45.27 2013 $50.53 2012 $4.53 2013 $4.99 Houston Ship Channel Natural Gas Forward Prices ERCOT North On-Peak Forward Prices ERCOT North On-Peak v. Houston Ship Channel Implied Heat Rate 2012 $10.09 2013 $12.06 ERCOT North On Peak Spark Spread Assumes a 7.2 Heat Rate, $1.50 O&M, and $.15 adder 22 Rolling 12 months, as of August 31 2011. Source: OTC quotes and electronic trading system. Quotes are daily. st |

Appendix 23 |

MISO (TWh) PJM (TWh) South (1) (TWh) ISO-NE & NY ISO (2) (TWh) West (TWh) The combination establishes an industry-leading platform with regional diversification of the generation fleet (1) Represents load and generation in ERCOT, SERC and SPP. (2) Constellation load includes ~0.7TWh of load served in Ontario. 31.8 147.3 Load 102.1 43.4 58.7 Generation 179.1 Constellation Exelon Load 6.3 5.8 0.5 Generation 9.1 9.1 29.5 Load Generation 14.2 4.8 9.4 2.4 Load Generation 0.8 0.4 0.4 28.5 23.2 Load Generation 24 Portfolio Matches Generation with Load in Key Competitive Markets Data for Exelon and Constellation represents expected generation (owned and contracted) and booked electric sales for 2011 as of 12/31/10. This data also includes 2011 partial year generation from Wolf Hollow (acquired by Exelon). Data also includes 2011 partial year estimated electric sales from StarTex and MXEnergy (acquired by Constellation). Exelon load includes ComEd Swap, load sold through affiliates, fixed and indexed load sales and load sold through POLR auctions. Constellation load includes load sold through affiliates, fixed and indexed load sales and load sold through POLR auctions. Note: |

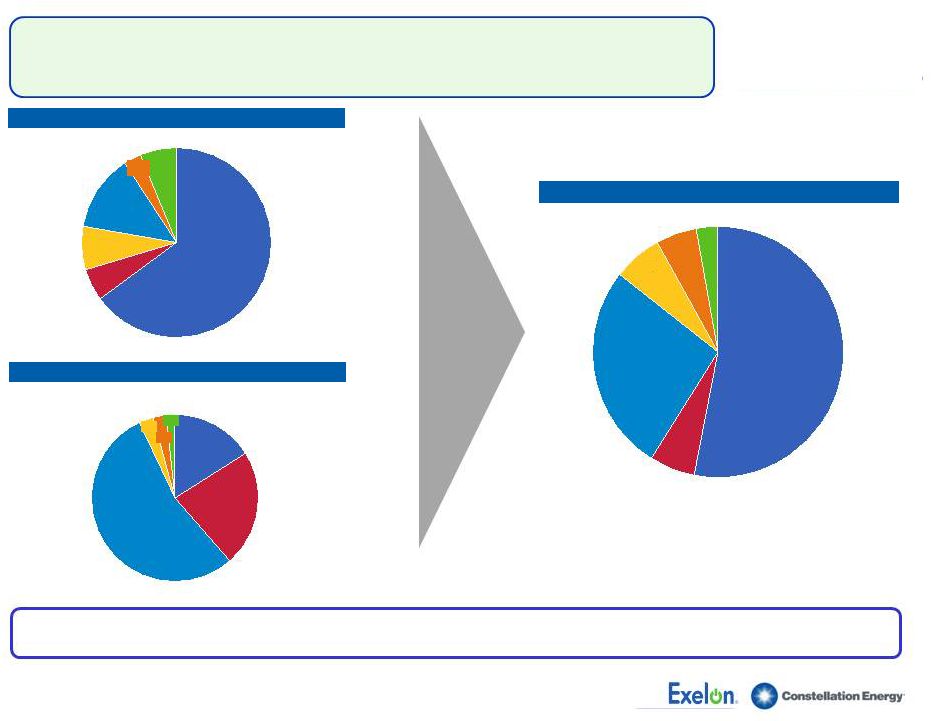

A Clean Generation Profile Creates Long- Term Value in Competitive Markets (1) Exelon generation includes Wolf Hollow acquisition (720 MW of natural gas). Constellation generation includes Boston Generation acquisition (2,950 MW of natural gas). Constellation nuclear reflects 50.01% interest in Constellation Energy Nuclear Group LLC. Generation capacity doesn’t reflect contracted capacity. (2) Net of physical market mitigation assumed to be 2,648 MW. Exelon Standalone (1) Total Generation: 26,339 MW Constellation Standalone (1) Total Generation: 11,980 MW Pro forma Company (Net of Mitigation) (2) Total Generation: 35,671 MW Hydro 6% Wind/Solar/Other Gas 13% Oil Coal 5% Nuclear 65% Wind/Solar/Other Hydro Oil Gas 54% Coal 23% Nuclear 16% Wind/Solar/Other 3% Hydro 5% Oil Gas 27% Coal 6% Nuclear 53% 25 Combined company remains the premier low-cost generator 7% 6% 3% 3% 2% 2% |

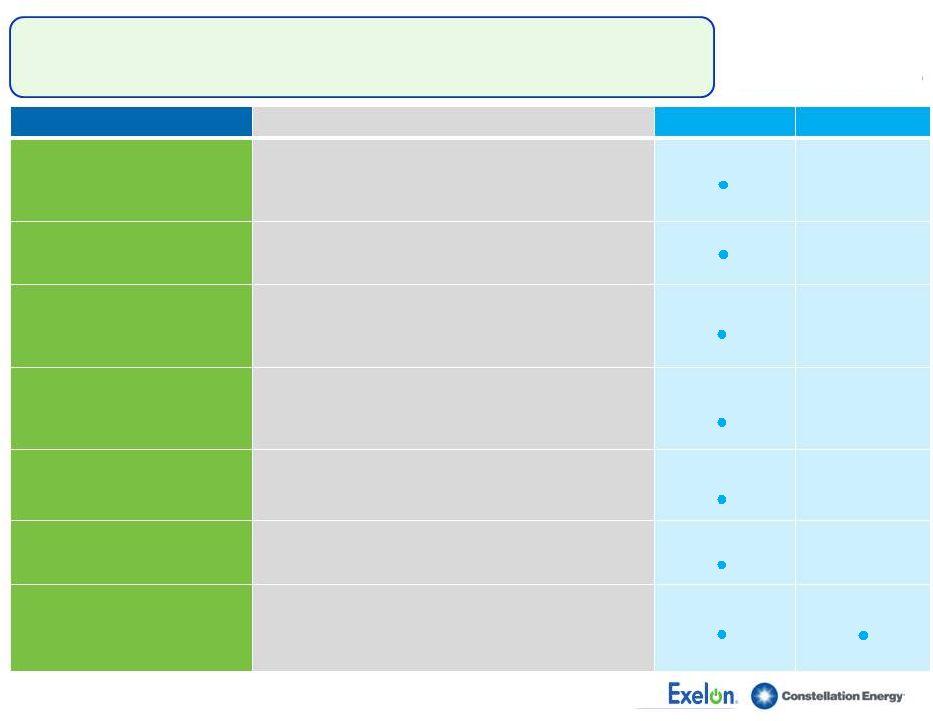

Merger Approvals Process on Schedule (as of 9/15/11) 26 Stakeholder Status of Key Milestones Filed Approved • SEC has completed its review of the amended S-4 Registration Statement • Shareholder approval anticipated in mid November 2011 • Submitted Hart-Scott-Rodino filing on May 31, 2011 for review under U.S. antitrust laws • Approval expected by January 2012 • Filed merger approval application and related filings on May 20, 2011, which assesses market power- related issues • Approval expected in Q4 2011 • Filed for indirect transfer of Constellation Energy licenses on May 12, 2011 • Approval expected by January 2012 • Filed for approval with the Maryland Public Service Commission on May 25, 2011 • Approval expected by January 5, 2012 • Filed for approval with the New York State Public Service Commission on May 17, 2011 • Approval expected in Q4 2011 • Filed for approval with the Public Utility Commission of Texas on May 17, 2011 • Approval received on August 3, 2011 Securities and Exchange Commission (SEC) (File No. 333-175162) Department of Justice (DOJ) Federal Energy Regulatory Commission (FERC) (Docket No. EC 11-83) Nuclear Regulatory Commission (Docket Nos. 50-317, 50-318, 50-220, 50-410, 50-244, 72-8, 72-67) Maryland PSC (Case No. 9271) New York PSC (Case No. 11-E-0245) Texas PUC (Case No. 39413) |

Significant Events Date of Event • Filing of Application May 25, 2011 • Intervention Deadline June 24, 2011 • Prehearing Conference June 28, 2011 • Filing of Staff, Office of People Counsel and Intervenor Testimony September 16, 2011* • Filing of Rebuttal Testimony October 12, 2011* • Filing of Surrebuttal Testimony October 26, 2011 • Status Conference October 28, 2011 • Evidentiary Hearings October 31, 2011 - November 10, 2011 • Public Comment Hearings November 29, December 1 & December 5, 2011 • Filing of Initial Briefs December 1, 2011 • Filing of Reply Briefs December 15, 2011 • Decision Deadline January 5, 2012 Maryland PSC Review Schedule 27 * Initial intervenor testimony with respect to market power is due on September 23 rd for all parties except for the Independent Market Monitor, and rebuttal testimony with respect to market power is due on October 17 th . |

EPA Regulations Are Moving Forward Develop Toxics Rule EPA regulations will provide regulatory certainty and significant environmental benefits Pre Compliance Period Compliance With Toxics Rule Develop Cross- State Air Pollution Rule Compliance With Cross-State Air Pollution Rule (CSAPR) Develop 316(b) Regulations Pre Compliance Period Phase In Of Compliance 28 2010 2011 2012 2013 2014 2015 2016 Hazardous Air Pollutants Criteria Pollutants Cooling Water For definition of the EPA regulations referred to on this slide, please see the EPA’s Terms of Environment (http://www.epa.gov/OCEPAterms/). |

Multi-Regional Nuclear Uprate Program Station Base Case MW Max Potential MW MW Online to Date Year of Full Operation by Unit MW Recovery & Component Upgrades: Quad Cities 97 104 99 2011 / 2010 Dresden 3 3 2013 / 2012 Peach Bottom 25 32 2011 / 2012 Dresden 103 110 19 2012 / 2013 Limerick 4 4 2012 / 2013 Peach Bottom 2 2 2014 / 2015 MUR: LaSalle 35 39 39 2011 / 2011 Limerick 33 41 30 2011 / 2011 Braidwood 34 42 2012 / 2012 Byron 34 42 2012 / 2012 Quad Cities 21 23 2014 / 2014 Dresden 28 31 2014 / 2015 TMI 12 15 2014 EPU: Clinton 2 2 2 2010 Peach Bottom 134 148 2015 / 2016 LaSalle 303 336 2016 / 2015 Limerick 306 340 2016 / 2017 Total 1,176 1,314 189 TMI Limerick Peach Bottom Total Midwest Uprates: 660-732 MW Total Mid-Atlantic Uprates: 516-582 MW Quad Cities Dresden Byron LaSalle Clinton Braidwood Notes: MW shown at ownership. An additional 11 MW expected to come online by end of 2011 at Peach Bottom 3. Executing uprate projects across our geographically diverse nuclear fleet 29 |

Exelon Nuclear Fleet Overview - IL Plant Location Type/ Containment Water Body License Extension Status / License Expiration (1) Ownership Spent Fuel Storage/ Date to lose full core discharge capacity (2) Braidwood, IL (Units 1 and 2) PWR Concrete/Steel Lined Kankakee River Expect to file application in 2013/ 2026, 2027 100% Dry Cask (Fall 2011) Byron, IL (Units 1 and 2) PWR Concrete/Steel Lined Rock River Expect to file application in 2013/ 2024, 2026 100% Dry Cask Clinton, IL (Unit 1) BWR Concrete/Steel Lined Clinton Lake 2026 100% 2018 Dresden, IL (Units 2 and 3) BWR Steel Vessel Kankakee River Renewed / 2029, 2031 100% Dry cask LaSalle, IL (Units 1 and 2) BWR Concrete/Steel Lined Illinois River 2022, 2023 100% Dry Cask Quad Cities, IL (Units 1 and 2) BWR Steel Vessel Mississippi River Renewed / 2032 75% Exelon, 25% Mid-American Holdings Dry cask 30 Exelon pursues license extensions well in advance of expiration to ensure adequate time for review by the NRC (1) Operating license renewal process takes approximately 4-5 years from commencement until completion of NRC review. (2) The date for loss of full core reserve identifies when the on-site storage pool will no longer have sufficient space to receive a full complement of fuel from the reactor core. Dry cask storage will be in operation at those sites prior to losing full core discharge capacity in their on-site storage pools. |

Exelon Nuclear Fleet Overview – PA and NJ Plant, Location Type, Containment Water Body License Extension Status / License Expiration (1) Ownership Spent Fuel Storage/ Date to lose full core discharge capacity (2) Limerick, PA (Units 1 and 2) BWR Concrete/Steel Lined Schuylkill River Filed application in June 2011 (decision expected in 2013)/ 2024, 2029 100% Dry cask Oyster Creek, NJ (Unit 1) BWR Steel Vessel Barnegat Bay Renewed / 2029 (3) 100% Dry cask Peach Bottom, PA (Units 2 and 3) BWR Steel Vessel Susquehanna River Renewed / 2033, 2034 50% Exelon, 50% PSEG Dry cask TMI, PA (Unit 1) PWR Concrete/Steel Lined Susquehanna River Renewed / 2034 100% 2023 Salem, NJ (Units 1 and 2) PWR Concrete/Steel Lined Delaware River Renewed / 2036, 2040 42.6% Exelon, 57.4% PSEG Dry Cask Exelon pursues license extensions well in advance of expiration to ensure adequate time for review by the NRC 31 (1) Operating license renewal process takes approximately 4-5 years from commencement until completion of NRC review. (2) The date for loss of full core reserve identifies when the on-site storage pool will no longer have sufficient space to receive a full complement of fuel from the reactor core. Dry cask storage will be in operation at those sites prior to losing full core discharge capacity in their on-site storage pools. (3) On December 8, 2010, Exelon announced that Generation will permanently cease generation operations at Oyster Creek by December 31, 2019. The current NRC license for Oyster Creek expires in 2029. |

2011 Projected Sources and Uses of Cash 32 ($ millions) Exelon (8) Beginning Cash Balance (1) $800 Cash Flow from Operations (2) 375 875 3,175 4,350 CapEx (excluding Nuclear Fuel, Nuclear Uprates, Exelon Wind, Utility Growth CapEx and Wolf Hollow) (725) (325) (850) (1,950) Nuclear Fuel n/a n/a (1,050) (1,050) Dividend (3) (1,400) Nuclear Uprates and Exelon Wind (4) n/a n/a (625) (625) Wolf Hollow Acquisition n/a n/a (300) (300) Utility Growth CapEx (5) (300) (125) n/a (425) Net Financing (excluding Dividend): Planned Debt Issuances (6) 1,000 -- -- 1,000 Planned Debt Retirements (6) (350) (250) -- (600) Other (7) 300 (125) 200 550 Ending Cash Balance (1) $350 (1) Excludes counterparty collateral activity. (2) Cash Flow from Operations primarily includes net cash flows provided by operating activities and net cash flows used in investing activities other than capital expenditures. (3) Assumes 2011 dividend of $2.10/share. Dividends are subject to declaration by the Board of Directors. (4) Includes $400 million in Nuclear Uprates and $225 million for Exelon Wind spend. (5) Represents new business, smart grid/smart meter investment and transmission growth projects. (6) Planned Issuances of $1B at ComEd reflect the $600M January 18, 2011 issuance and $400M of ComEd’s $600M September 7, 2011 issuance. Incremental $200M of financing was primarily utilized to retire $191M of tax-exempt debt at ComEd. (7) “Other” includes proceeds from options and expected changes in short-term debt. (8) Includes cash flow activity from Holding Company, eliminations, and other corporate entities. . Note: Projected cash flows are as of 6/30/2011 |

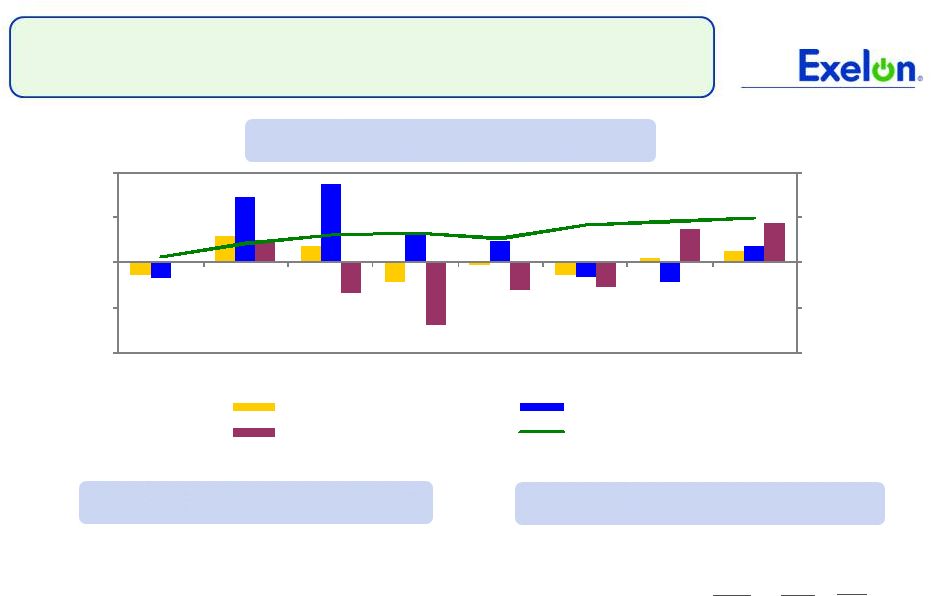

ComEd Load Trends Chicago U.S. Unemployment rate (1) 9.3% 9.2% 2011 annualized growth in gross domestic/metro product (2) 2.5% Note: C&I = Commercial & Industrial Weather-Normalized Load Year-over-Year Key Economic Indicators Weather-Normalized Load 2010 2Q11 2011E Average Customer Growth 0.2% 0.4% Average Use-Per-Customer (1.4)% (2.0)% Total Residential (1.2)% (1.6)% Small C&I (0.6)% (0.2)% Large C&I 2.6% (0.9)% All Customer Classes 0.2% (0.8)% (1) Source: U.S. Dept. of Labor (June 2011) and Illinois Department of Security (June 2011) (2) Source: Global Insight (May 2011) -6.0% -3.0% 0.0% 3.0% 6.0% -6.0% -3.0% 0.0% 3.0% 6.0% 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 All Customer Classes Large C&I Residential Gross Metro Product 33 0.4% 0.0% 0.4% (0.3)% 0.0% 0.0% 2.7% |

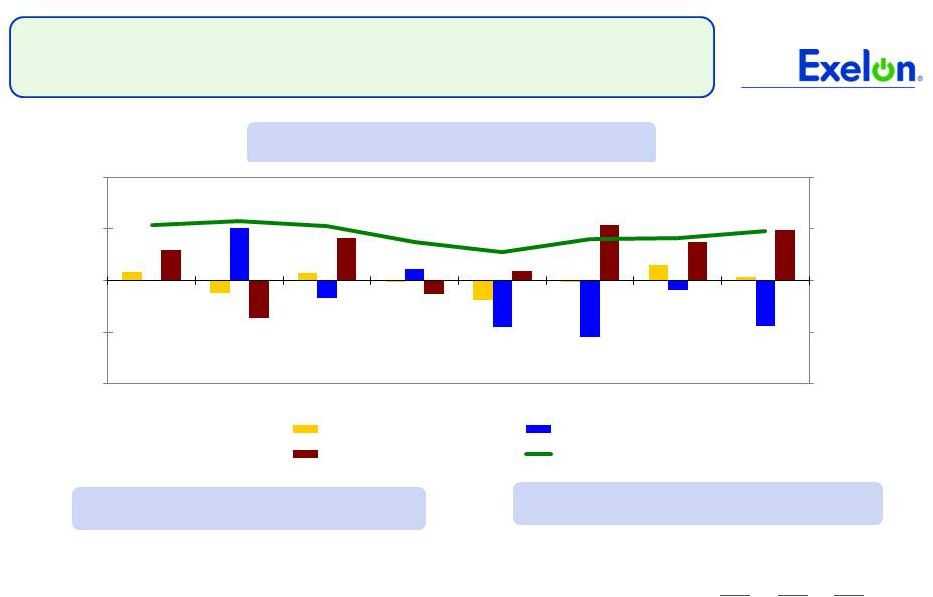

PECO Load Trends Philadelphia U.S. Unemployment rate (1) 7.9% 9.2% 2011 annualized growth in gross domestic/metro product (2) 2.4% 2.7% Note: C&I = Commercial & Industrial Weather-Normalized Load Year-over-Year Key Economic Indicators Weather-Normalized Load 2010 2Q11 2011E Average Customer Growth 0.3% 0.5% 0.4% Average Use-Per-Customer 0.3% 2.8% 1.7% Total Residential 0.5% 3.2% 2.2% Small C&I (1.9)% 1.7% 0.7% Large C&I 0.8% (3.3)% (2.3)% All Customer Classes 0.1% (0.1)% (0.0)% (1) Source: U.S Dept. of Labor data June 2011 - US U.S Dept. of Labor prelim. data May 2011 - Philadelphia (2) Source: Global Insight May 2011 34 -6.0% -3.0% 0.0% 3.0% 6.0% - 6.0% - 3.0% 0.0% 3.0% 6.0% 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 All Customer Classes Large C&I Residential Gross Metro Product |