UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-21055

T. Rowe Price Institutional Income Funds, Inc.

(Exact name of registrant as specified in charter)

100 East Pratt Street, Baltimore, MD 21202

(Address of principal executive offices)

David Oestreicher

100 East Pratt Street, Baltimore, MD 21202

(Name and address of agent for service)

Registrant’s telephone number, including area code: (410) 345-2000

Date of fiscal year end: May 31

Date of reporting period: May 31, 2024

Item 1. Reports to Shareholders

(a) Report pursuant to Rule 30e-1

Annual Shareholder Report

May 31, 2024

Institutional Long Duration Credit Fund

This annual shareholder report contains important information about Institutional Long Duration Credit Fund (the "fund") for the period of June 1, 2023 to May 31, 2024. You can find the fund’s prospectus, financial information on Form N-CSR (which includes required tax information for dividends), holdings, proxy voting information, and other information atwww.troweprice.com/prospectus. You can also request this information without charge by contacting T. Rowe Price at 1-800-638-5660 or info@troweprice.com or contacting your intermediary.

What were the fund costs for the last year? (based on a hypothetical $10,000 investment)

| Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Institutional Long Duration Credit Fund | $45 | 0.45% |

What drove fund performance during the past 12 months?

The U.S. long duration credit market posted positive returns for the reporting period. Despite generally higher U.S. Treasury yields, higher coupon payments and tighter credit spreads benefited bond investors.

In the government-related sector, select taxable municipal holdings and allocations to emerging markets debt performed well for the fund relative to the Bloomberg U.S. Long Credit Bond Index. Taxable municipal bonds benefited from a scarcity premium with investors looking to add yield, while increased demand and falling interest rate volatility helped buoy emerging markets.

An emphasis on intermediate corporate bonds, which can be less volatile compared with longer-term corporates, detracted relative to the Bloomberg U.S. Long Credit Bond Index. Longer-term corporate credit spreads tightened more meaningfully on strong demand for yield.

The fund seeks to provide high income through a diversified portfolio of longer-duration debt instruments issued by corporations as well as certain noncorporate issuers. With high-grade corporate bond yields at attractive levels, the fund increased its holdings in investment-grade corporates as the macroeconomic backdrop remained mostly supportive.

The fund held exposure to derivatives, including credit and interest rate derivatives. Broadly speaking, the fund’s use of derivatives was beneficial, and the use of credit derivatives aided absolute returns. However, interest rate derivatives had a negative impact on absolute performance.

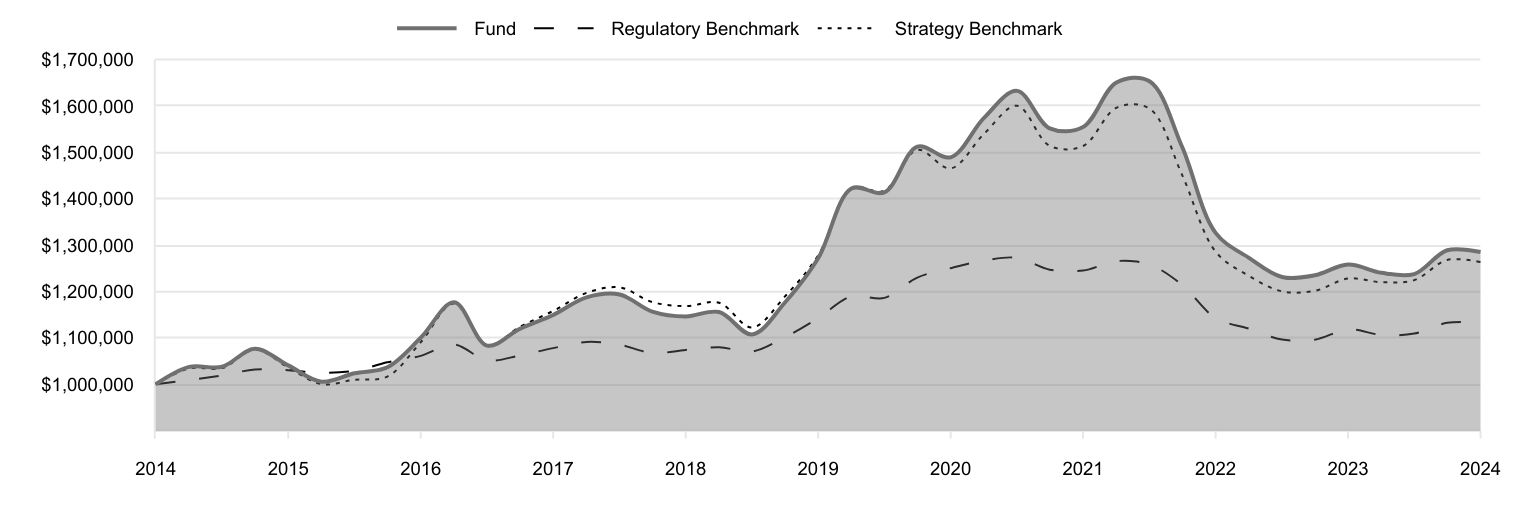

How has the fund performed?

Cumulative Returns of a Hypothetical $1 Million Investment as of May 31, 2024

| Fund | Regulatory Benchmark | Strategy Benchmark |

|---|

| 2014 | 1,000,000 | 1,000,000 | 1,000,000 |

| 2014 | 1,037,383 | 1,009,025 | 1,034,149 |

| 2014 | 1,037,798 | 1,019,205 | 1,034,714 |

| 2015 | 1,076,678 | 1,031,757 | 1,074,886 |

| 2015 | 1,040,666 | 1,030,342 | 1,036,157 |

| 2015 | 1,005,573 | 1,024,718 | 1,000,203 |

| 2015 | 1,023,683 | 1,029,095 | 1,009,698 |

| 2016 | 1,036,685 | 1,047,261 | 1,016,632 |

| 2016 | 1,100,185 | 1,061,199 | 1,090,455 |

| 2016 | 1,176,729 | 1,085,853 | 1,174,157 |

| 2016 | 1,083,384 | 1,051,443 | 1,082,416 |

| 2017 | 1,119,320 | 1,062,083 | 1,123,849 |

| 2017 | 1,149,443 | 1,077,951 | 1,158,060 |

| 2017 | 1,187,376 | 1,091,201 | 1,197,008 |

| 2017 | 1,193,493 | 1,085,238 | 1,208,776 |

| 2018 | 1,156,759 | 1,067,447 | 1,177,238 |

| 2018 | 1,146,238 | 1,073,913 | 1,168,431 |

| 2018 | 1,155,682 | 1,079,750 | 1,175,731 |

| 2018 | 1,107,463 | 1,070,673 | 1,122,388 |

| 2019 | 1,175,828 | 1,101,283 | 1,188,827 |

| 2019 | 1,271,598 | 1,142,647 | 1,277,609 |

| 2019 | 1,421,988 | 1,189,587 | 1,422,782 |

| 2019 | 1,413,671 | 1,186,211 | 1,417,160 |

| 2020 | 1,512,254 | 1,229,943 | 1,505,453 |

| 2020 | 1,489,317 | 1,250,234 | 1,465,209 |

| 2020 | 1,574,192 | 1,266,595 | 1,539,766 |

| 2020 | 1,632,511 | 1,272,614 | 1,600,435 |

| 2021 | 1,551,702 | 1,246,960 | 1,513,988 |

| 2021 | 1,554,627 | 1,245,172 | 1,513,614 |

| 2021 | 1,650,486 | 1,265,527 | 1,596,135 |

| 2021 | 1,653,159 | 1,257,934 | 1,594,302 |

| 2022 | 1,511,343 | 1,213,988 | 1,450,936 |

| 2022 | 1,326,312 | 1,142,793 | 1,285,982 |

| 2022 | 1,272,607 | 1,119,789 | 1,233,508 |

| 2022 | 1,231,311 | 1,096,421 | 1,200,235 |

| 2023 | 1,234,893 | 1,095,965 | 1,201,387 |

| 2023 | 1,258,176 | 1,118,306 | 1,227,875 |

| 2023 | 1,240,270 | 1,106,428 | 1,220,089 |

| 2023 | 1,237,554 | 1,109,356 | 1,224,600 |

| 2024 | 1,288,961 | 1,132,430 | 1,268,054 |

| 2024 | 1,285,038 | 1,132,905 | 1,263,436 |

202405-3565004, 202407-3567288

Average Annual Total Returns

| 1 Year | 5 Years | 10 Years |

|---|

| Institutional Long Duration Credit Fund | 2.14% | 0.21% | 2.54% |

| Bloomberg U.S. Aggregate Bond Index (Regulatory Benchmark) | 1.31 | | 1.26 |

| Bloomberg U.S. Long Credit Bond Index (Strategy Benchmark) | 2.90 | | 2.37 |

The preceding line graph shows the value of a hypothetical $1,000,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The fund’s performance information included in the line graph and table above is compared with a regulatory required index that represents an overall securities market (Regulatory Benchmark). In addition, the line graph and table may also include one or more indexes that more closely aligns to the fund's investment strategy (Strategy Benchmark(s)). Due to new SEC Rules on shareholder reporting the fund adopted a new broad-based securities market index, referred to as the Regulatory Benchmark. Market index returns do not include expenses, which are deducted from fund returns. The fund's total return figures reflect the reinvestment of dividends and capital gains, if any. Neither the fund’s returns nor the index returns reflect the deduction of taxes that a shareholder would pay on fund distributions or redemptions of fund shares. The fund’s past performance is not a good predictor of the fund’s future performance. Updated performance information can be found at www.troweprice.com.

What are some fund statistics?

| Total Net Assets (000s) | $156,733 |

| Number of Portfolio Holdings | 453 |

| Investment Advisory Fees Paid (000s) | $427 |

| Portfolio Turnover Rate | 59.3% |

What did the fund invest in?

Credit Quality Allocation* (as a % of Net Assets)

| AAA Rated | 1.6% |

| AA Rated | 8.6 |

| A Rated | 34.5 |

| BBB Rated | 42.1 |

| U.S. Treasury Securities | 12.0 |

| Reserves | 1.2 |

*Credit ratings for the securities held in the Fund are provided by Moody’s, Standard & Poor’s, and Fitch and are converted to the Standard & Poor’s nomenclature. A rating of AAA represents the highest-rated securities, and a rating of D represents the lowest rated securities. If the ratings agencies differ, the highest rating is applied to the security. If a rating is not available, the security is classified as Not Rated. The rating of the underlying investment vehicle is used to determine the creditworthiness of credit default swaps and sovereign securities. The Fund is not rated by any agency.

Top Ten Holdings (as a % of Net Assets)

| U.S. Treasury Bonds | 12.0% |

| AT&T | 1.7 |

| CVS Health | 1.3 |

| UnitedHealth Group | 1.3 |

| Bank of America | 1.2 |

| JPMorgan Chase | 1.2 |

| Anheuser-Busch | 1.2 |

| AbbVie | 1.1 |

| Amgen | 1.1 |

| Verizon Communications | 1.0 |

If you invest directly with T. Rowe Price, you can elect to receive future shareholder reports or other important documents through electronic delivery by enrolling at www.troweprice.com/paperless. If you invest through a financial intermediary such as an investment advisor, a bank, retirement plan sponsor or a brokerage firm, please contact that organization and ask if it can provide electronic delivery.

Bloomberg does not accept any liability for any errors or omissions in the indexes or data, and hereby expressly disclaim all warranties of originality, accuracy, completeness, timeliness, merchantability and fitness for a particular purpose. No party may rely on any indexes or data contained in this communication. Visit www.troweprice.com/en/us/market-data-disclosures for additional legal notices & disclaimers.

Institutional Long Duration Credit Fund

(RPLCX)

T. Rowe Price Investment Services, Inc.

100 East Pratt Street

Baltimore, MD 21202

Item 1. (b) Notice pursuant to Rule 30e-3.

Not applicable.

Item 2. Code of Ethics.

The registrant has adopted a code of ethics, as defined in Item 2 of Form N-CSR, applicable to its principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions. A copy of this code of ethics is filed as an exhibit to this Form N-CSR. No substantive amendments were approved or waivers were granted to this code of ethics during the period covered by this report.

Item 3. Audit Committee Financial Expert.

The registrant’s Board of Directors has determined that Mr. Paul F. McBride qualifies as an audit committee financial expert, as defined in Item 3 of Form N-CSR. Mr. McBride is considered independent for purposes of Item 3 of Form N-CSR.

Item 4. Principal Accountant Fees and Services.

(a) – (d) Aggregate fees billed for the last two fiscal years for professional services rendered to, or on behalf of, the registrant by the registrant’s principal accountant were as follows:

| | | | | | | | | | | | | | |

| | | 2024 | | | | | | 2023 | | | |

Audit Fees | | $ | 33,841 | | | | | | | $ | 33,192 | |

Audit-Related Fees | | | - | | | | | | | | - | |

Tax Fees | | | - | | | | | | | | - | |

All Other Fees | | | - | | | | | | | | - | |

Audit fees include amounts related to the audit of the registrant’s annual financial statements and services normally provided by the accountant in connection with statutory and regulatory filings. Audit-related fees include amounts reasonably related to the performance of the audit of the registrant’s financial statements and specifically include the issuance of a report on internal controls and, if applicable, agreed-upon procedures related to fund acquisitions. Tax fees include amounts related to services for tax compliance, tax planning, and tax advice. The nature of these services specifically includes the review of distribution calculations and the preparation of Federal, state, and excise tax returns. All other fees include the registrant’s pro-rata share of amounts for agreed-upon procedures in conjunction with service contract approvals by the registrant’s Board of Directors/Trustees.

(e)(1) The registrant’s audit committee has adopted a policy whereby audit and non-audit services performed by the registrant’s principal accountant for the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant require pre-approval in advance at regularly scheduled audit committee meetings. If such a service is required between regularly scheduled audit committee meetings, pre-approval may be authorized by one audit committee member with ratification at the next scheduled audit committee meeting. Waiver of pre-approval for audit or non-audit services requiring fees of a de minimis amount is not permitted.

(2) No services included in (b) – (d) above were approved pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) Less than 50 percent of the hours expended on the principal accountant’s engagement to audit the registrant’s financial statements for the most recent fiscal year were attributed to work performed by persons other than the principal accountant’s full-time, permanent employees.

(g) The aggregate fees billed for the most recent fiscal year and the preceding fiscal year by the registrant’s principal accountant for non-audit services rendered to the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant were $1,230,000 and $1,521,000, respectively.

(h) All non-audit services rendered in (g) above were pre-approved by the registrant’s audit committee. Accordingly, these services were considered by the registrant’s audit committee in maintaining the principal accountant’s independence.

(i) Not applicable.

(j) Not applicable.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Investments.

(a) Not applicable. The complete schedule of investments is included in Item 7 of this Form N-CSR.

(b) Not applicable.

Item 7. Financial Statements and Financial Highlights for Open-End Management Investment Companies.

(a – b) Report pursuant to Regulation S-X.

Financial

Statements

and

Other

Information

Institutional

Long

Duration

Credit

Fund

For

more

insights

from

T.

Rowe

Price

investment

professionals,

go

to

troweprice.com

.

Financial

Highlights

Portfolio

of

Investments

Financial

Statements

and

Notes

Additional

Fund

Information

T.

ROWE

PRICE

Institutional

Long

Duration

Credit

Fund

Go

Paperless

Going

paperless

offers

a

host

of

benefits,

which

include:

Timely

delivery

of

important

documents

Convenient

access

to

your

documents

anytime,

anywhere

Strong

security

protocols

to

safeguard

sensitive

data

Waive

your

account

service

fee

by

going

paperless.

*

To

Enroll:

˃

If

you

invest

directly

with

T.

Rowe

Price,

go

to

troweprice.com/paperless

.

If

you

invest

through

a

financial

intermediary

such

as

an

investment

advisor,

a

bank,

or

a

brokerage

firm,

please

contact

that

organization

and

ask

if

it

can

provide

electronic

documentation.

Log

in

to

your

account

at

troweprice.com

for

more

information.

*

An

account

service

fee

will

be

charged

annually

for

each

T.

Rowe

Price

mutual

fund

account

unless

you

meet

criteria

for

a

fee

waiver.

Go

to

troweprice.com/personal-investing/help/fees-and-minimums.html

to

learn

more

about

this

account

service

fee,

including

other

ways

to

waive

it.

T.

ROWE

PRICE

Institutional

Long

Duration

Credit

Fund

For

a

share

outstanding

throughout

each

period

The

accompanying

notes

are

an

integral

part

of

these

financial

statements.

..

Year

..

..

Ended

.

5/31/24

5/31/23

5/31/22

5/31/21

5/31/20

NET

ASSET

VALUE

Beginning

of

period

$

7

.77

$

8

.59

$

10

.70

$

11

.00

$

10

.68

Investment

activities

Net

investment

income

(1)(2)

0

.37

0

.34

0

.33

0

.36

0

.40

Net

realized

and

unrealized

gain/loss

(

0

.21

)

(

0

.79

)

(

1

.76

)

0

.15

1

.35

Total

from

investment

activities

0

.16

(

0

.45

)

(

1

.43

)

0

.51

1

.75

Distributions

Net

investment

income

(

0

.41

)

(

0

.37

)

(

0

.38

)

(

0

.41

)

(

0

.43

)

Net

realized

gain

–

–

(

0

.27

)

(

0

.40

)

(

1

.00

)

Tax

return

of

capital

–

–

(

0

.03

)

–

–

Total

distributions

(

0

.41

)

(

0

.37

)

(

0

.68

)

(

0

.81

)

(

1

.43

)

NET

ASSET

VALUE

End

of

period

$

7

.52

$

7

.77

$

8

.59

$

10

.70

$

11

.00

Ratios/Supplemental

Data

Total

return

(2)(3)

2

.14

%

(

5

.14

)

%

(

14

.69

)

%

4

.39

%

17

.12

%

Ratios

to

average

net

assets:

(2)

Gross

expenses

before

waivers/payments

by

Price

Associates

0

.45

%

0

.45

%

0

.45

%

0

.45

%

0

.46

%

Net

expenses

after

waivers/payments

by

Price

Associates

0

.45

%

0

.45

%

0

.45

%

0

.45

%

0

.46

%

Net

investment

income

4

.87

%

4

.26

%

3

.21

%

3

.19

%

3

.56

%

Portfolio

turnover

rate

59

.3

%

46

.7

%

59

.9

%

50

.9

%

70

.5

%

Net

assets,

end

of

period

(in

thousands)

$

156,733

$

55,544

$

24,849

$

19,168

$

23,979

(1)

Per

share

amounts

calculated

using

average

shares

outstanding

method.

(2)

Includes

the

impact

of

expense-related

arrangements

with

Price

Associates.

(3)

Total

return

reflects

the

rate

that

an

investor

would

have

earned

on

an

investment

in

the

fund

during

each

period,

assuming

reinvestment

of

all

distributions,

and

payment

of

no

redemption

or

account

fees,

if

applicable.

T.

ROWE

PRICE

Institutional

Long

Duration

Credit

Fund

May

31,

2024

Par/Shares

$

Value

(Amounts

in

000s)

‡

CORPORATE

BONDS

78.4%

Banking

12.3%

Australia

&

New

Zealand

Banking

Group,

6.742%,

12/8/32 (1)

200

212

Banco

Bilbao

Vizcaya

Argentaria,

VR,

6.033%,

3/13/35 (2)

400

401

Banco

Santander,

6.921%,

8/8/33

200

211

Bank

of

America,

5.00%,

1/21/44

500

472

Bank

of

America,

VR,

2.676%,

6/19/41 (2)

200

140

Bank

of

America,

VR,

2.687%,

4/22/32 (2)

200

167

Bank

of

America,

VR,

3.824%,

1/20/28 (2)

100

96

Bank

of

America,

VR,

4.078%,

4/23/40 (2)

300

254

Bank

of

America,

VR,

4.33%,

3/15/50 (2)

455

379

Bank

of

America,

VR,

5.468%,

1/23/35 (2)

210

209

Bank

of

America,

Series N,

VR,

2.651%,

3/11/32 (2)

250

209

Bank

of

New

York

Mellon,

VR,

6.474%,

10/25/34 (2)

230

247

Barclays,

5.25%,

8/17/45 (3)

250

238

Barclays,

VR,

6.036%,

3/12/55 (2)

200

204

Barclays,

VR,

7.437%,

11/2/33 (2)

200

219

BNP

Paribas,

VR,

2.871%,

4/19/32 (1)(2)

200

168

CaixaBank,

VR,

6.84%,

9/13/34 (1)

(2)

230

244

Capital

One

Financial,

VR,

3.273%,

3/1/30 (2)

250

224

Capital

One

Financial,

VR,

6.051%,

2/1/35 (2)

150

151

Capital

One

Financial,

VR,

6.377%,

6/8/34 (2)

300

307

Citigroup,

4.65%,

7/30/45

530

470

Citigroup,

VR,

5.827%,

2/13/35 (2)

500

495

Citigroup,

VR,

6.174%,

5/25/34 (2)

115

116

Credit

Agricole,

5.365%,

3/11/34 (1)

500

493

Danske

Bank,

VR,

5.705%,

3/1/30 (1)(2)

200

200

Fifth

Third

Bancorp,

8.25%,

3/1/38

300

351

Goldman

Sachs

Group,

2.60%,

2/7/30

100

87

Goldman

Sachs

Group,

4.75%,

10/21/45

515

464

Goldman

Sachs

Group,

5.15%,

5/22/45

200

188

Goldman

Sachs

Group,

6.25%,

2/1/41

700

752

HSBC

Holdings,

7.625%,

5/17/32

155

169

HSBC

Holdings,

VR,

5.719%,

3/4/35 (2)

275

277

HSBC

Holdings,

VR,

6.332%,

3/9/44 (2)

400

421

Par/Shares

$

Value

(Amounts

in

000s)

‡

HSBC

Holdings,

VR,

7.399%,

11/13/34 (2)

290

315

ING

Groep,

VR,

5.55%,

3/19/35 (2)

500

495

ING

Groep,

VR,

6.114%,

9/11/34 (2)

200

206

Intesa

Sanpaolo,

6.625%,

6/20/33 (1)

330

341

JPMorgan

Chase,

5.625%,

8/16/43

1,005

1,029

JPMorgan

Chase,

VR,

3.882%,

7/24/38 (2)

730

622

JPMorgan

Chase,

VR,

5.336%,

1/23/35 (2)

185

182

Lloyds

Banking

Group,

4.344%,

1/9/48

200

156

Lloyds

Banking

Group,

VR,

5.679%,

1/5/35 (2)

225

224

Morgan

Stanley,

4.30%,

1/27/45

450

385

Morgan

Stanley,

VR,

3.217%,

4/22/42 (2)

450

335

NatWest

Group,

VR,

6.016%,

3/2/34 (2)

250

255

PNC

Financial

Services

Group,

VR,

4.626%,

6/6/33 (2)

250

231

Santander

Holdings

USA,

VR,

6.342%,

5/31/35 (2)

560

561

Societe

Generale,

VR,

6.066%,

1/19/35 (1)(2)

365

364

Standard

Chartered,

VR,

5.905%,

5/14/35 (1)(2)

650

650

Standard

Chartered,

VR,

6.301%,

1/9/29 (1)(2)

200

204

State

Street,

VR,

5.159%,

5/18/34 (2)

305

299

Sumitomo

Mitsui

Financial

Group,

5.766%,

1/13/33

200

205

U.S.

Bancorp,

VR,

5.678%,

1/23/35 (2)

325

324

UBS

Group,

VR,

3.179%,

2/11/43 (1)

(2)

200

143

UBS

Group,

VR,

5.699%,

2/8/35 (1)

(2)

200

199

UBS

Group,

VR,

6.301%,

9/22/34 (1)

(2)

200

208

Wells

Fargo,

3.90%,

5/1/45

350

279

Wells

Fargo,

VR,

2.393%,

6/2/28 (2)

150

138

Wells

Fargo,

VR,

3.068%,

4/30/41 (2)

850

627

Wells

Fargo,

VR,

5.499%,

1/23/35 (2)

250

248

Wells

Fargo,

VR,

5.557%,

7/25/34 (2)

200

198

Wells

Fargo

Bank,

6.60%,

1/15/38

250

271

Westpac

Banking,

VR,

2.668%,

11/15/35 (2)

500

410

19,339

Basic

Industry

2.1%

BHP

Billiton

Finance

USA,

5.50%,

9/8/53

35

34

Celanese

U.S.

Holdings,

6.70%,

11/15/33

60

63

Dow

Chemical,

4.80%,

5/15/49

490

418

Dow

Chemical,

5.60%,

2/15/54

350

336

Ecolab,

2.70%,

12/15/51

300

186

Ecolab,

3.70%,

11/1/46

30

22

T.

ROWE

PRICE

Institutional

Long

Duration

Credit

Fund

Par/Shares

$

Value

(Amounts

in

000s)

‡

Freeport-McMoRan,

5.45%,

3/15/43

300

283

International

Paper,

4.35%,

8/15/48

139

112

LYB

International

Finance

III,

5.625%,

5/15/33

250

253

LyondellBasell

Industries,

4.625%,

2/26/55

400

318

Newmont,

5.45%,

6/9/44

195

188

Nucor,

4.40%,

5/1/48 (3)

75

64

Southern

Copper,

5.25%,

11/8/42

200

186

Southern

Copper,

7.50%,

7/27/35

200

231

Vale

Overseas,

6.875%,

11/21/36

300

318

Westlake,

3.125%,

8/15/51

500

315

3,327

Brokerage

Assetmanagers

Exchanges

1.2%

BlackRock

Funding,

5.00%,

3/14/34

750

741

Intercontinental

Exchange,

4.95%,

6/15/52

300

274

Intercontinental

Exchange,

5.25%,

6/15/31

345

346

Nasdaq,

3.95%,

3/7/52

220

164

Nasdaq,

5.95%,

8/15/53

340

345

1,870

Capital

Goods

3.8%

Amphenol,

5.25%,

4/5/34

270

269

Boeing,

5.705%,

5/1/40

300

274

Boeing,

5.805%,

5/1/50

500

447

Carrier

Global,

6.20%,

3/15/54

400

428

CRH

America

Finance,

5.40%,

5/21/34

750

743

Honeywell

International,

5.25%,

3/1/54

500

482

Ingersoll

Rand,

5.70%,

6/15/54

170

172

Johnson

Controls

International,

4.50%,

2/15/47

250

209

L3Harris

Technologies,

4.854%,

4/27/35

280

264

Martin

Marietta

Materials,

4.25%,

12/15/47

305

247

Masco,

4.50%,

5/15/47

360

296

Owens

Corning,

5.95%,

6/15/54

550

552

Republic

Services,

5.00%,

12/15/33

530

515

Republic

Services,

5.00%,

4/1/34

25

24

Stanley

Black

&

Decker,

2.75%,

11/15/50

800

456

Vulcan

Materials,

4.50%,

6/15/47

130

109

Waste

Connections,

2.95%,

1/15/52

175

111

Waste

Management,

4.875%,

2/15/34

350

342

5,940

Communications

10.1%

American

Tower,

5.45%,

2/15/34

265

262

American

Tower,

5.90%,

11/15/33

300

307

AT&T,

3.50%,

6/1/41

1,150

873

AT&T,

3.80%,

12/1/57

2,228

1,545

AT&T,

5.40%,

2/15/34

200

198

Bell

Canada,

5.10%,

5/11/33

250

243

Par/Shares

$

Value

(Amounts

in

000s)

‡

Charter

Communications

Operating,

3.70%,

4/1/51

600

365

Charter

Communications

Operating,

5.75%,

4/1/48

425

357

Charter

Communications

Operating,

6.484%,

10/23/45

300

276

Charter

Communications

Operating,

6.65%,

2/1/34 (3)

280

284

Comcast,

2.45%,

8/15/52

350

195

Comcast,

3.90%,

3/1/38

150

126

Comcast,

4.049%,

11/1/52

755

584

Cox

Communications,

2.95%,

10/1/50 (1)

230

136

Cox

Communications,

5.70%,

6/15/33 (1)

500

495

Crown

Castle,

2.90%,

4/1/41

250

172

Crown

Castle,

4.75%,

5/15/47

185

157

Interpublic

Group

of

Companies,

5.375%,

6/15/33

340

335

Meta

Platforms,

4.95%,

5/15/33 (3)

170

170

Meta

Platforms,

5.60%,

5/15/53

380

384

NBCUniversal

Media,

4.45%,

1/15/43

1,700

1,462

Rogers

Communications,

4.35%,

5/1/49

175

138

Rogers

Communications,

4.50%,

3/15/42

160

134

Rogers

Communications,

4.55%,

3/15/52

250

203

Rogers

Communications,

5.00%,

3/15/44

350

313

Rogers

Communications,

5.30%,

2/15/34

225

219

T-Mobile

USA,

5.05%,

7/15/33

250

243

T-Mobile

USA,

5.75%,

1/15/34

300

307

T-Mobile

USA,

5.75%,

1/15/54

680

677

Telefonica

Emisiones,

5.52%,

3/1/49

500

465

Time

Warner

Cable,

5.875%,

11/15/40

700

605

TWDC

Enterprises

18,

4.125%,

6/1/44

700

584

Verizon

Communications,

2.65%,

11/20/40

1,000

690

Verizon

Communications,

2.987%,

10/30/56

1,536

937

Videotron,

5.125%,

4/15/27 (1)

70

68

Vodafone

Group,

4.875%,

6/19/49

230

200

Warnermedia

Holdings,

5.05%,

3/15/42

1,285

1,061

15,770

Consumer

Cyclical

4.6%

Amazon.com,

4.95%,

12/5/44

400

387

AutoZone,

4.75%,

2/1/33

250

238

AutoZone,

5.20%,

8/1/33

200

196

Best

Buy,

1.95%,

10/1/30

200

164

CBRE

Services,

5.95%,

8/15/34 (3)

245

247

Cummins,

5.45%,

2/20/54

1,000

980

Daimler

Truck

Finance

North

America,

5.375%,

1/18/34 (1)

450

445

T.

ROWE

PRICE

Institutional

Long

Duration

Credit

Fund

Par/Shares

$

Value

(Amounts

in

000s)

‡

Dollar

General,

5.45%,

7/5/33 (3)

250

247

eBay,

4.00%,

7/15/42

500

400

Ford

Motor,

4.75%,

1/15/43

200

161

Ford

Motor

Credit,

7.122%,

11/7/33

215

229

General

Motors,

6.60%,

4/1/36

600

627

Home

Depot,

4.20%,

4/1/43

500

422

Home

Depot,

4.40%,

3/15/45

200

172

Lowe's,

4.65%,

4/15/42

250

220

Lowe's,

5.625%,

4/15/53

400

386

Lowe's,

5.85%,

4/1/63

300

293

Magna

International,

5.50%,

3/21/33

270

274

McDonald's,

4.20%,

4/1/50

90

72

McDonald's,

5.45%,

8/14/53

250

242

Mercedes-Benz

Finance

North

America,

5.05%,

8/3/33 (1)

300

295

Tractor

Supply,

5.25%,

5/15/33

250

247

Volkswagen

Group

of

America

Finance,

5.90%,

9/12/33 (1)

250

253

7,197

Consumer

Non-Cyclical

12.2%

AbbVie,

4.05%,

11/21/39

500

433

AbbVie,

4.25%,

11/21/49

735

611

AbbVie,

4.50%,

5/14/35

400

376

AbbVie,

5.50%,

3/15/64

335

329

Altria

Group,

5.80%,

2/14/39

140

139

Amgen,

4.95%,

10/1/41

600

556

Amgen,

5.65%,

3/2/53

1,125

1,109

Anheuser-Busch,

4.90%,

2/1/46

1,980

1,814

Anheuser-Busch

InBev

Worldwide,

5.45%,

1/23/39

305

306

Anheuser-Busch

InBev

Worldwide,

5.55%,

1/23/49

400

399

Astrazeneca

Finance,

4.875%,

3/3/33

200

197

Banner

Health,

2.913%,

1/1/51

115

75

BAT

Capital,

6.00%,

2/20/34

110

111

BAT

Capital,

7.079%,

8/2/43

180

192

Bayer

U.S.

Finance,

6.875%,

11/21/53 (1)

200

207

Becton

Dickinson

&

Company,

4.669%,

6/6/47

200

174

Biogen,

3.15%,

5/1/50

270

175

Bristol-Myers

Squibb,

4.125%,

6/15/39

800

693

Bristol-Myers

Squibb,

5.65%,

2/22/64

225

220

Centra

Health,

4.70%,

1/1/48

190

161

Cigna

Group,

3.875%,

10/15/47

370

280

CommonSpirit

Health,

3.91%,

10/1/50

170

129

CommonSpirit

Health,

4.187%,

10/1/49

135

107

CVS

Health,

4.125%,

4/1/40

330

266

CVS

Health,

5.05%,

3/25/48

765

661

CVS

Health,

5.25%,

2/21/33

170

165

CVS

Health,

6.00%,

6/1/44

750

736

CVS

Health,

6.00%,

6/1/63

250

240

Eli

Lilly,

5.00%,

2/9/54

350

333

Par/Shares

$

Value

(Amounts

in

000s)

‡

Hackensack

Meridian

Health,

4.211%,

7/1/48 (3)

170

143

HCA,

4.375%,

3/15/42

580

478

HCA,

4.625%,

3/15/52

400

311

HCA,

5.90%,

6/1/53

250

243

Icon

Investments

Six,

6.00%,

5/8/34

200

203

IQVIA,

6.25%,

2/1/29

95

97

Mars,

4.75%,

4/20/33 (1)

225

217

Merck,

5.00%,

5/17/53

340

319

Nestle

Holdings,

4.85%,

3/14/33 (1)

300

298

Pfizer

Investment

Enterprises,

5.11%,

5/19/43

1,300

1,234

Pfizer

Investment

Enterprises,

5.30%,

5/19/53

190

182

Philip

Morris

International,

5.25%,

2/13/34

500

489

Reynolds

American,

5.70%,

8/15/35

150

146

Reynolds

American,

5.85%,

8/15/45

600

559

Roche

Holdings,

5.218%,

3/8/54 (1)

500

486

Solventum,

5.90%,

4/30/54 (1)

750

720

Sutter

Health,

5.547%,

8/15/53

95

97

Sysco,

6.00%,

1/17/34

400

418

Thermo

Fisher

Scientific,

5.404%,

8/10/43

350

351

Tyson

Foods,

5.10%,

9/28/48

195

170

Utah

Acquisition

Sub,

5.25%,

6/15/46

250

205

Viatris,

4.00%,

6/22/50

400

271

West

Virginia

United

Health

System

Obligated

Group,

Series 2018,

4.924%,

6/1/48

95

84

Zoetis,

4.70%,

2/1/43

300

267

19,182

Electric

10.0%

AEP

Texas,

5.40%,

6/1/33

220

214

Ameren

Illinois,

4.50%,

3/15/49 (3)

500

427

American

Electric

Power,

5.625%,

3/1/33

250

248

Appalachian

Power,

6.375%,

4/1/36

145

150

Appalachian

Power,

7.00%,

4/1/38

200

218

Baltimore

Gas

&

Electric,

5.40%,

6/1/53

95

91

Berkshire

Hathaway

Energy,

3.80%,

7/15/48

1,000

737

Berkshire

Hathaway

Energy,

6.125%,

4/1/36

300

312

Commonwealth

Edison,

5.30%,

2/1/53

40

38

Commonwealth

Edison,

5.65%,

6/1/54

500

498

Consolidated

Edison

of

New

York,

6.15%,

11/15/52

400

424

Constellation

Energy

Generation,

5.75%,

3/15/54

500

483

Constellation

Energy

Generation,

6.25%,

10/1/39

300

309

Consumers

Energy,

3.75%,

2/15/50

500

382

DTE

Energy,

5.85%,

6/1/34

360

364

T.

ROWE

PRICE

Institutional

Long

Duration

Credit

Fund

Par/Shares

$

Value

(Amounts

in

000s)

‡

Duke

Energy,

3.75%,

9/1/46

130

96

Duke

Energy,

6.10%,

9/15/53

250

256

Duke

Energy

Indiana,

5.40%,

4/1/53

70

66

Duke

Energy

Ohio,

5.55%,

3/15/54

750

724

Duke

Energy

Progress,

5.35%,

3/15/53

200

190

El

Paso

Electric,

5.00%,

12/1/44

110

92

Exelon,

4.10%,

3/15/52

170

131

Exelon,

5.60%,

3/15/53

285

275

FirstEnergy

Pennsylvania

Electric,

6.15%,

10/1/38

165

168

Florida

Power

&

Light,

2.875%,

12/4/51

130

83

Florida

Power

&

Light,

5.60%,

6/15/54

500

503

Georgia

Power,

4.95%,

5/17/33

140

136

Indianapolis

Power

&

Light,

5.70%,

4/1/54 (1)

740

722

IPALCO

Enterprises,

5.75%,

4/1/34 (1)

825

811

ITC

Holdings,

5.65%,

5/9/34 (1)

1,000

1,001

Kentucky

Utilities,

4.375%,

10/1/45

200

165

Louisville

Gas

&

Electric,

4.375%,

10/1/45

100

83

Nevada

Power,

6.00%,

3/15/54

300

303

New

York

State

Electric

&

Gas,

5.85%,

8/15/33 (1)

90

91

NextEra

Energy

Capital

Holdings,

3.00%,

1/15/52

45

28

NextEra

Energy

Capital

Holdings,

5.25%,

2/28/53

585

544

Niagara

Mohawk

Power,

5.29%,

1/17/34 (1)

500

485

Pacific

Gas

&

Electric,

4.95%,

7/1/50

250

209

Pacific

Gas

&

Electric,

6.15%,

1/15/33

150

153

Pacific

Gas

&

Electric,

6.75%,

1/15/53

390

411

Pacific

Gas

&

Electric,

6.95%,

3/15/34

410

442

PECO

Energy,

4.90%,

6/15/33

300

294

Public

Service

Company

of

Colorado,

5.25%,

4/1/53

100

92

San

Diego

Gas

&

Electric,

Series TTT,

4.10%,

6/15/49

55

43

Southern,

4.25%,

7/1/36

430

381

Southern,

4.40%,

7/1/46

600

504

Southern,

5.70%,

3/15/34

140

142

Southern

California

Edison,

5.75%,

4/15/54

500

494

Southern

California

Edison,

5.875%,

12/1/53

250

250

Southern

California

Edison,

Series C,

4.125%,

3/1/48

150

117

Vistra

Operations,

4.30%,

7/15/29 (1)

225

210

Vistra

Operations,

6.95%,

10/15/33 (1)

90

96

15,686

Par/Shares

$

Value

(Amounts

in

000s)

‡

Energy

6.1%

Canadian

Natural

Resources,

6.25%,

3/15/38

300

308

Cheniere

Energy,

5.65%,

4/15/34 (1)

250

248

Cheniere

Energy

Partners,

5.75%,

8/15/34 (1)

820

813

ConocoPhillips,

5.55%,

3/15/54

350

344

Diamondback

Energy,

4.25%,

3/15/52

170

132

Enbridge,

5.95%,

4/5/54

500

495

Enbridge,

6.70%,

11/15/53

120

131

Enbridge

Energy

Partners,

7.375%,

10/15/45

120

137

Energy

Transfer,

5.95%,

5/15/54

425

408

Energy

Transfer,

6.50%,

2/1/42

595

613

Eni,

5.95%,

5/15/54 (1)

295

292

Enterprise

Products

Operating,

3.30%,

2/15/53

1,400

940

Kinder

Morgan

Energy

Partners,

6.95%,

1/15/38

195

212

Marathon

Oil,

5.20%,

6/1/45

300

277

MPLX,

5.65%,

3/1/53

300

282

Occidental

Petroleum,

4.40%,

4/15/46

350

275

ONEOK,

6.625%,

9/1/53

295

316

ONEOK

Partners,

6.85%,

10/15/37

250

266

Ovintiv,

6.25%,

7/15/33

75

77

Patterson-UTI

Energy,

7.15%,

10/1/33

85

89

Raizen

Fuels

Finance,

6.45%,

3/5/34 (1)

200

203

Southern

Natural

Gas,

4.80%,

3/15/47 (1)

205

167

Spectra

Energy

Partners,

5.95%,

9/25/43

115

113

Suncor

Energy,

4.00%,

11/15/47

310

233

Targa

Resources,

4.95%,

4/15/52

80

68

Targa

Resources,

6.50%,

2/15/53

100

105

TotalEnergies

Capital,

5.488%,

4/5/54

800

791

TransCanada

PipeLines,

6.10%,

6/1/40

450

456

Transcanada

Trust,

VR,

5.30%,

3/15/77 (2)

120

112

Transcontinental

Gas

Pipe

Line,

4.60%,

3/15/48

575

491

Williams,

4.85%,

3/1/48

100

86

9,480

Finance

Companies

1.3%

AerCap

Ireland

Capital,

3.40%,

10/29/33

300

249

AerCap

Ireland

Capital,

5.30%,

1/19/34

500

485

AerCap

Ireland

Capital,

6.15%,

9/30/30

150

154

GATX,

5.45%,

9/15/33

250

243

GATX,

6.90%,

5/1/34

270

291

T.

ROWE

PRICE

Institutional

Long

Duration

Credit

Fund

Par/Shares

$

Value

(Amounts

in

000s)

‡

SMBC

Aviation

Capital

Finance,

5.55%,

4/3/34 (1)

600

585

2,007

Insurance

5.4%

Aetna,

3.875%,

8/15/47

500

364

Aflac,

4.75%,

1/15/49

550

482

AIA

Group,

5.375%,

4/5/34 (1)

365

357

American

International

Group,

5.125%,

3/27/33

425

415

Arch

Capital

Group,

7.35%,

5/1/34

200

226

Arthur

J

Gallagher,

5.75%,

7/15/54

750

721

Chubb,

Series 1,

6.50%,

5/15/38

200

221

Chubb

INA

Holdings,

2.85%,

12/15/51

100

65

Corebridge

Financial,

4.40%,

4/5/52

300

234

Elevance

Health,

4.375%,

12/1/47

355

297

Elevance

Health,

5.125%,

2/15/53

100

92

Equitable

Holdings,

5.594%,

1/11/33

100

100

Humana,

5.50%,

3/15/53

75

70

Humana,

5.75%,

4/15/54 (3)

260

251

Humana,

5.95%,

3/15/34

185

188

Jackson

Financial,

4.00%,

11/23/51

300

200

Liberty

Mutual

Group,

4.85%,

8/1/44 (1)

180

154

Marsh

&

McLennan,

5.45%,

3/15/53

200

193

Marsh

&

McLennan,

5.70%,

9/15/53

155

156

Metropolitan

Life

Global

Funding

I,

5.05%,

1/8/34 (1)

500

489

Principal

Financial

Group,

6.05%,

10/15/36

235

244

Reinsurance

Group

of

America,

6.00%,

9/15/33

250

255

Teachers

Insurance

&

Annuity

Assn.

of

America,

4.90%,

9/15/44 (1)

200

178

UnitedHealth

Group,

3.25%,

5/15/51

500

344

UnitedHealth

Group,

3.50%,

8/15/39

300

241

UnitedHealth

Group,

5.35%,

2/15/33

160

162

UnitedHealth

Group,

5.375%,

4/15/54

315

305

UnitedHealth

Group,

5.875%,

2/15/53

900

938

Voya

Financial,

5.70%,

7/15/43

500

483

8,425

Miscellaneous

0.2%

Ally

Financial,

8.00%,

11/1/31

200

218

218

Natural

Gas

1.9%

Boston

Gas,

6.119%,

7/20/53 (1)

215

212

Engie,

5.875%,

4/10/54 (1)

750

735

NiSource,

3.95%,

3/30/48

260

195

NiSource,

5.35%,

4/1/34

750

731

NiSource,

5.40%,

6/30/33

75

74

Piedmont

Natural

Gas,

5.40%,

6/15/33

250

248

Sempra,

4.00%,

2/1/48

120

91

Sempra,

5.50%,

8/1/33 (3)

250

249

Par/Shares

$

Value

(Amounts

in

000s)

‡

Sempra

Energy,

3.80%,

2/1/38

600

490

3,025

Real

Estate

Investment

Trusts

1.4%

Alexandria

Real

Estate

Equities,

4.75%,

4/15/35

70

65

Alexandria

Real

Estate

Equities,

5.25%,

5/15/36

110

105

Essex

Portfolio,

4.50%,

3/15/48 (3)

130

107

Kilroy

Realty,

2.65%,

11/15/33 (3)

350

256

NNN

REIT,

4.80%,

10/15/48

235

197

Prologis,

5.00%,

3/15/34

500

488

Public

Storage

Operating,

5.35%,

8/1/53

55

53

Regency

Centers,

5.25%,

1/15/34

520

506

Simon

Property

Group,

5.85%,

3/8/53

200

197

Simon

Property

Group,

6.65%,

1/15/54

250

275

2,249

Technology

3.6%

Apple,

2.95%,

9/11/49

400

271

Apple,

3.75%,

9/12/47

400

318

Apple,

4.85%,

5/10/53 (3)

200

191

Broadcom,

4.926%,

5/15/37 (1)

400

372

Fiserv,

4.40%,

7/1/49

185

151

Fiserv,

5.45%,

3/15/34

715

709

Fiserv,

5.60%,

3/2/33

85

85

Foundry

JV

Holdco,

6.40%,

1/25/38 (1)

495

507

Intuit,

5.50%,

9/15/53

115

115

Micron

Technology,

3.366%,

11/1/41

400

292

Motorola

Solutions,

5.40%,

4/15/34

140

138

NXP,

3.25%,

5/11/41

400

293

Oracle,

3.60%,

4/1/40

1,000

769

Oracle,

3.95%,

3/25/51

350

257

Oracle,

5.55%,

2/6/53

630

594

Texas

Instruments,

5.00%,

3/14/53

250

233

Texas

Instruments,

5.05%,

5/18/63

180

167

Workday,

3.80%,

4/1/32

200

179

5,641

Transportation

2.2%

Burlington

Northern

Santa

Fe,

5.05%,

3/1/41

75

71

Burlington

Northern

Santa

Fe,

5.20%,

4/15/54

300

284

Canadian

National

Railway,

5.85%,

11/1/33

270

283

Canadian

Pacific

Railway,

3.10%,

12/2/51

125

83

Canadian

Pacific

Railway,

4.70%,

5/1/48

500

430

CSX,

4.30%,

3/1/48

140

117

CSX,

4.50%,

11/15/52

400

341

ERAC

USA

Finance,

5.20%,

10/30/34 (1)

500

491

T.

ROWE

PRICE

Institutional

Long

Duration

Credit

Fund

Par/Shares

$

Value

(Amounts

in

000s)

‡

ERAC

USA

Finance,

5.40%,

5/1/53 (1)

250

241

FedEx,

4.55%,

4/1/46

800

664

Norfolk

Southern,

4.837%,

10/1/41

250

228

Norfolk

Southern,

5.35%,

8/1/54

250

238

3,471

Total

Corporate

Bonds

(Cost

$128,544)

122,827

FOREIGN

GOVERNMENT

OBLIGATIONS

&

MUNICIPALITIES

2.8%

Owned

No

Guarantee

0.9%

Corp.

Nacional

del

Cobre

de

Chile,

6.44%,

1/26/36 (1)

390

398

Petroleos

Mexicanos,

5.50%,

6/27/44

175

108

Petroleos

Mexicanos,

6.50%,

6/2/41

1,000

691

Petroleos

Mexicanos,

7.69%,

1/23/50

200

146

1,343

Sovereign

1.9%

Kingdom

of

Saudi

Arabia,

5.75%,

1/16/54 (1)

370

358

Republic

of

Colombia,

4.125%,

5/15/51

200

119

Republic

of

Colombia,

8.75%,

11/14/53

200

210

Republic

of

Panama,

4.50%,

4/16/50

400

266

Republic

of

Panama,

4.50%,

1/19/63

200

126

Republic

of

Panama,

7.875%,

3/1/57

200

206

Republic

of

Peru,

3.00%,

1/15/34 (3)

400

321

State

of

Qatar,

4.40%,

4/16/50 (1)

200

171

United

Mexican

States,

4.40%,

2/12/52

400

296

United

Mexican

States,

4.75%,

3/8/44

600

487

United

Mexican

States,

6.00%,

5/7/36

310

305

United

Mexican

States,

6.338%,

5/4/53

200

191

3,056

Total

Foreign

Government

Obligations

&

Municipalities

(Cost

$4,584)

4,399

MUNICIPAL

SECURITIES

5.2%

California

1.2%

Bay

Area

Toll

Auth.,

Series S-10,

3.276%,

4/1/50

400

293

Bay

Area

Toll

Auth.,

Series S-3,

Build

America,

6.907%,

10/1/50

350

405

California,

Build

America,

GO,

7.50%,

4/1/34

500

575

California,

Various

Purpose,

GO,

5.20%,

3/1/43

350

343

Par/Shares

$

Value

(Amounts

in

000s)

‡

Los

Angeles

Dept.

of

Water

&

Power,

Build

America,

6.574%,

7/1/45

200

220

1,836

District

of

Columbia

0.2%

Metropolitan

Washington

Airports

Auth.,

Dulles

Toll

Road

Revenue,

Build

America,

7.462%,

10/1/46

200

242

242

Florida

0.3%

Florida

Dev.

Finance,

Nova

Southeastern

Univ.,

Series B,

4.109%,

4/1/50

375

296

Miami-Dade

County

Transit

System,

Series B,

Build

America,

5.624%,

7/1/40

200

202

498

Georgia

0.8%

Fulton

County,

Build

America,

GO,

5.148%,

7/1/39

505

491

Municipal

Electric

Auth.

of

Georgia,

Build

America,

Vogtle

Units,

6.655%,

4/1/57

633

712

1,203

Illinois

0.1%

Illinois

Municipal

Electric

Agency,

Build

America,

6.832%,

2/1/35

190

202

202

Louisiana

0.0%

Louisiana

Local

Government

Environmental

Fac.,

CDA,

Series A,

4.475%,

8/1/39

90

83

83

Maryland

0.1%

Maryland

Economic

Development,

Seagirt

Marine

Terminal,

Series B,

4.75%,

6/1/42

150

129

129

Massachusetts

0.2%

Massachusetts

Bay

Transportation

Auth.,

Build

America,

5.869%,

7/1/40

115

119

Massachusetts

Water

Resources

Auth.,

Series C,

2.823%,

8/1/41

200

155

274

Michigan

0.4%

Gerald

R

Ford

Int'l.

Airport

Auth.,

Series A,

5.435%,

1/1/43

220

222

Michigan

Fin.

Auth.,

Trinity

Health

Credit

Group,

3.084%,

12/1/34

500

431

653

Minnesota

0.1%

Western

Minnesota

Municipal

Power

Agency,

Series A,

3.156%,

1/1/39

150

123

123

Ohio

0.3%

American

Municipal

Power,

Series C,

Build

America,

6.053%,

2/15/43

500

514

514

T.

ROWE

PRICE

Institutional

Long

Duration

Credit

Fund

Par/Shares

$

Value

(Amounts

in

000s)

‡

Tennessee

0.0%

Metropolitan

Government

Nashville

&

Davidson

County

Health

&

Ed.

Facs,

Vanderbilt

Univ.

Medical,

Series B,

3.235%,

7/1/52

85

53

53

Texas

1.3%

Board

of

Regents

of

the

Univ.

of

Texas

System,

Series D,

Build

America,

5.134%,

8/15/42

200

199

Central

Texas

Regional

Mobility

Auth.,

Series E,

3.167%,

1/1/41

150

113

Central

Texas

Turnpike

System,

Series C,

3.029%,

8/15/41

305

228

Dallas/Fort

Worth

Int'l.

Airport,

Series A,

2.994%,

11/1/38

630

521

Dallas/Fort

Worth

Int'l.

Airport,

Series A,

4.507%,

11/1/51

150

132

Dallas/Fort

Worth

Int'l.

Airport,

Series A,

5.045%,

11/1/47

250

240

Texas

Natural

Gas

Securitization

Fin.,

Series 2023-1,

Class

A2,

5.169%,

4/1/41

545

540

Texas

Private

Activity

Bond

Surface

Transportation,

North

Tarrant

Express,

Series B,

3.922%,

12/31/49

125

101

2,074

Virginia

0.2%

Univ.

of

Virginia,

Series B,

2.584%,

11/1/51

300

187

Virginia

Commonwealth

Univ.

Health

System

Auth.,

Series A,

4.956%,

1/1/44

105

99

286

Total

Municipal

Securities

(Cost

$8,651)

8,170

NON-U.S.

GOVERNMENT

MORTGAGE-BACKED

SECURITIES

0.4%

Commercial

Mortgage-Backed

Securities

0.4%

Federal

Home

Loan

Mortgage

Multifamily

Structured

PTC

Series K137,

Class

A2,

ARM

2.347%,

11/25/31

460

386

Federal

Home

Loan

Mortgage

Multifamily

Structured

PTC

Series K150,

Class

A2,

ARM

3.71%,

9/25/32

265

243

Total

Non-U.S.

Government

Mortgage-Backed

Securities

(Cost

$668)

629

Par/Shares

$

Value

(Amounts

in

000s)

‡

U.S.

GOVERNMENT

AGENCY

OBLIGATIONS

(EXCLUDING

MORTGAGE-BACKED)

12.0%

U.S.

Treasury

Obligations

12.0%

U.S.

Treasury

Bonds,

2.375%,

2/15/42 (4)

75

54

U.S.

Treasury

Bonds,

2.50%,

2/15/45 (4)

16,885

11,894

U.S.

Treasury

Bonds,

3.125%,

5/15/48

3,300

2,534

U.S.

Treasury

Bonds,

3.625%,

2/15/53

55

46

U.S.

Treasury

Bonds,

4.125%,

8/15/53

530

486

U.S.

Treasury

Bonds,

4.625%,

5/15/54

1,000

999

U.S.

Treasury

Bonds,

4.75%,

11/15/53

2,730

2,782

Total

U.S.

Government

Agency

Obligations

(Excluding

Mortgage-

Backed)

(Cost

$19,266)

18,795

SHORT-TERM

INVESTMENTS

0.2%

Money

Market

Funds

0.2%

T.

Rowe

Price

Government

Reserve

Fund,

5.39% (5)(6)

244

244

Total

Short-Term

Investments

(Cost

$244)

244

SECURITIES

LENDING

COLLATERAL

2.1%

INVESTMENTS

IN

A

POOLED

ACCOUNT

THROUGH

SECURITIES

LENDING

PROGRAM

WITH

JPMORGAN

CHASE

BANK 0.2%

Money

Market

Funds 0.2%

T.

Rowe

Price

Government

Reserve

Fund,

5.39% (5)(6)

312

312

Total

Investments

in

a

Pooled

Account

through

Securities

Lending

Program

with

JPMorgan

Chase

Bank

312

T.

ROWE

PRICE

Institutional

Long

Duration

Credit

Fund

Par/Shares

$

Value

(Amounts

in

000s)

‡

INVESTMENTS

IN

A

POOLED

ACCOUNT

THROUGH

SECURITIES

LENDING

PROGRAM

WITH

STATE

STREET

BANK

AND

TRUST

COMPANY 1.9%

Money

Market

Funds 1.9%

T.

Rowe

Price

Government

Reserve

Fund,

5.39% (5)(6)

3,057

3,057

Total

Investments

in

a

Pooled

Account

through

Securities

Lending

Program

with

State

Street

Bank

and

Trust

Company

3,057

Total

Securities

Lending

Collateral

(Cost

$3,369)

3,369

Total

Investments

in

Securities

101.1%

of

Net

Assets

(Cost

$165,326)

$

158,433

‡

Par/Shares

and

Notional

Amount

are

denominated

in

U.S.

dollars

unless

otherwise

noted.

(1)

Security

was

purchased

pursuant

to

Rule

144A

under

the

Securities

Act

of

1933

and

may

be

resold

in

transactions

exempt

from

registration

only

to

qualified

institutional

buyers.

Total

value

of

such

securities

at

period-end

amounts

to

$17,433

and

represents

11.1%

of

net

assets.

(2)

Security

is

a

fix-to-float

security,

which

carries

a

fixed

coupon

until

a

certain

date,

upon

which

it

switches

to

a

floating

rate.

Reference

rate

and

spread

are

provided

if

the

rate

is

currently

floating.

(3)

See

Note

4

.

All

or

a

portion

of

this

security

is

on

loan

at

May

31,

2024.

(4)

At

May

31,

2024,

all

or

a

portion

of

this

security

is

pledged

as

collateral

and/or

margin

deposit

to

cover

future

funding

obligations.

(5)

Seven-day

yield

(6)

Affiliated

Companies

ARM

Adjustable

Rate

Mortgage

(ARM);

rate

shown

is

effective

rate

at

period-end.

The

rates

for

certain

ARMs

are

not

based

on

a

published

reference

rate

and

spread

but

may

be

determined

using

a

formula

based

on

the

rates

of

the

underlying

loans.

CDA

Community

Development

Administration/Authority

GO

General

Obligation

PTC

Pass-Through

Certificate

VR

Variable

Rate;

rate

shown

is

effective

rate

at

period-end.

The

rates

for

certain

variable

rate

securities

are

not

based

on

a

published

reference

rate

and

spread

but

are

determined

by

the

issuer

or

agent

and

based

on

current

market

conditions.

T.

ROWE

PRICE

Institutional

Long

Duration

Credit

Fund

(Amounts

in

000s)

SWAPS

0.8%

Description

Notional

Amount

$

Value

Initial

$

Value

**

Unrealized

$

Gain/(Loss)

CENTRALLY

CLEARED

SWAPS

0.8%

Credit

Default

Swaps,

Protection

Sold

0.8%

Protection

Sold

(Relevant

Credit:

Markit

CDX.NA.HY-S41,

5

Year

Index),

Receive

5.00%

Quarterly,

Pay

upon

credit

default,

12/20/28

8,415

663

295

368

Protection

Sold

(Relevant

Credit:

Markit

CDX.NA.HY-S42,

5

Year

Index),

Receive

5.00%

Quarterly,

Pay

upon

credit

default,

6/20/29

3,300

257

228

29

Protection

Sold

(Relevant

Credit:

Markit

CDX.NA.IG-S41,

5

Year

Index),

Receive

1.00%

Quarterly,

Pay

upon

credit

default,

12/20/28

7,100

176

122

54

Protection

Sold

(Relevant

Credit:

Markit

CDX.NA.IG-S42,

10

Year

Index),

Receive

1.00%

Quarterly,

Pay

upon

credit

default,

6/20/34

5,000

48

29

19

Protection

Sold

(Relevant

Credit:

Markit

CDX.NA.IG-S42,

5

Year

Index),

Receive

1.00%

Quarterly,

Pay

upon

credit

default,

6/20/29

2,750

67

62

5

Total

Centrally

Cleared

Credit

Default

Swaps,

Protection

Sold

474

Total

Centrally

Cleared

Swaps

474

Net

payments

(receipts)

of

variation

margin

to

date

(

447

)

Variation

margin

receivable

(payable)

on

centrally

cleared

swaps

$

27

**

Includes

interest

purchased

or

sold

but

not

yet

collected

of

$10.

T.

ROWE

PRICE

Institutional

Long

Duration

Credit

Fund

FUTURES

CONTRACTS

($000s)

Expiration

Date

Notional

Amount

Value

and

Unrealized

Gain

(Loss)

Long,

134

U.S.

Treasury

Long

Bond

contracts

9/24

15,552

$

(

113

)

Short,

29

U.S.

Treasury

Notes

five

year

contracts

9/24

(3,068)

2

Short,

30

U.S.

Treasury

Notes

ten

year

contracts

9/24

(3,264)

4

Long,

76

Ultra

U.S.

Treasury

Bonds

contracts

9/24

9,305

(

115

)

Short,

144

Ultra

U.S.

Treasury

Notes

ten

year

contracts

9/24

(16,132)

56

Net

payments

(receipts)

of

variation

margin

to

date

231

Variation

margin

receivable

(payable)

on

open

futures

contracts

$

65

T.

ROWE

PRICE

Institutional

Long

Duration

Credit

Fund

The

accompanying

notes

are

an

integral

part

of

these

financial

statements.

AFFILIATED

COMPANIES

($000s)

The

fund

may

invest

in

certain

securities

that

are

considered

affiliated

companies.

As

defined

by

the

1940

Act,

an

affiliated

company

is

one

in

which

the

fund

owns

5%

or

more

of

the

outstanding

voting

securities,

or

a

company

that

is

under

common

ownership

or

control.

The

following

securities

were

considered

affiliated

companies

for

all

or

some

portion

of

the

year

ended

May

31,

2024.

Net

realized

gain

(loss),

investment

income,

change

in

net

unrealized

gain/loss,

and

purchase

and

sales

cost

reflect

all

activity

for

the

period

then

ended.

Affiliate

Net

Realized

Gain

(Loss)

Change

in

Net

Unrealized

Gain/Loss

Investment

Income

T.

Rowe

Price

Government

Reserve

Fund,

5.39%

$

—

$

—

$

76

++

Totals

$

—

#

$

—

$

76

+

Supplementary

Investment

Schedule

Affiliate

Value

05/31/23

Purchase

Cost

Sales

Cost

Value

05/31/24

T.

Rowe

Price

Government

Reserve

Fund,

5.39%

$

1,278

^

^

$

3,613

Total

$

3,613

^

#

Capital

gain

distributions

from

underlying

Price

funds

represented

$0

of

the

net

realized

gain

(loss).

++

Excludes

earnings

on

securities

lending

collateral,

which

are

subject

to

rebates

and

fees

as

described

in

Note

4

.

+

Investment

income

comprised

$76

of

dividend

income

and

$0

of

interest

income.

^

Purchase

and

sale

information

not

shown

for

cash

management

funds.

^

The

cost

basis

of

investments

in

affiliated

companies

was

$3,613.

T.

ROWE

PRICE

Institutional

Long

Duration

Credit

Fund

May

31,

2024

Statement

of

Assets

and

Liabilities

($000s,

except

shares

and

per

share

amounts)

The

accompanying

notes

are

an

integral

part

of

these

financial

statements.

Assets

Investments

in

securities,

at

value

(cost

$165,326)

$

158,433

Interest

receivable

1,942

Receivable

for

shares

sold

526

Variation

margin

receivable

on

futures

contracts

65

Variation

margin

receivable

on

centrally

cleared

swaps

27

Cash

9

Other

assets

10

Total

assets

161,012

Liabilities

Obligation

to

return

securities

lending

collateral

3,369

Payable

for

investment

securities

purchased

499

Payable

for

shares

redeemed

364

Investment

management

and

administrative

fees

payable

47

Total

liabilities

4,279

NET

ASSETS

$

156,733

Net

Assets

Consist

of:

Total

distributable

earnings

(loss)

$

(

11,309

)

Paid-in

capital

applicable

to

20,841,013

shares

of

$0.0001

par

value

capital

stock

outstanding;

4,000,000,000

shares

of

the

Corporation

authorized

168,042

NET

ASSETS

$

156,733

NET

ASSET

VALUE

PER

SHARE

$

7.52

T.

ROWE

PRICE

Institutional

Long

Duration

Credit

Fund

The

accompanying

notes

are

an

integral

part

of

these

financial

statements.

Year

Ended

5/31/24

Investment

Income

(Loss)

Income