Lehman Conference

London

May 16, 2007

Exhibit 99.1

Notices

Forward Looking Statements

Certain statements made in these presentations that are not historical facts may constitute “forward-looking” statements under the Private Securities

Litigation Reform Act of 1995, including those that are signified by words such as “anticipate”, “believe”, “expect”, “estimate”, “target”, and similar

expressions. These forward-looking statements reflect the current views of CIT and its management and are subject to risks, uncertainties, and changes

in circumstances. CIT’s actual results or performance may differ materially from those expressed in, or implied by, such forward-looking statements.

Factors that could affect actual results and performance include, but are not limited to, potential changes in interest rates, competitive factors and

general economic conditions, changes in funding markets, industry cycles and trends, uncertainties associated with risk management, risks associated

with residual value of leased equipment, and other factors described in our Form 10-K for the year ended December 31, 2006 and 10-Q for the quarter

ended March 31, 2007. CIT does not undertake to update any forward-looking statements.

Non-GAAP Financial Measures

The data provided in these presentations have been modified from our previously reported periodic data, including, but not limited to, the exclusion of

certain noteworthy transactions and nonrecurring events, because management believes that the data presented herein better reflects core operating

results. As such, the data will vary from comparable data reported in CIT’s Forms 10-K & 10-Q. The data provided in these presentations have not been

examined by independent accountants and is not presented in accordance with generally accepted accounting principles (“GAAP”).

These presentations include certain non-GAAP financial measures, as defined in Regulation G promulgated by the Securities and Exchange

Commission. Any references to non-GAAP financial measures are intended to provide additional information and insight into CIT’s financial condition

and operating results. These measures are not in accordance with, or a substitute for, GAAP and may be different from or inconsistent with non-GAAP

financial measures used by other companies.

For a reconciliation of these non-GAAP measures to GAAP and a list of the transactions and events excluded from the data herein, please refer to the

appendix within this presentation or access the reconciliations through CIT's Investor Relations website at www.cit.com ..

This presentation is derived from CIT’s publicly available information and is to be used solely as part of CIT management’s continuing

investor communications program. This presentation has not been prepared in connection with, and should not be used in connection with,

any offering of securities by CIT. For the sale of any securities by CIT you are directed to rely only upon the offering document for those

particular securities.

Data as of or for the period ended March 31, 2007 unless otherwise noted.

2

Building on 99 Years of Success

$11 Billion Market Capitalization

Global Servicing Capabilities

Customized Financial Solutions

Strong Credit Culture

Managed Assets $80 Billion

Premium Brand

Diverse Portfolio

3

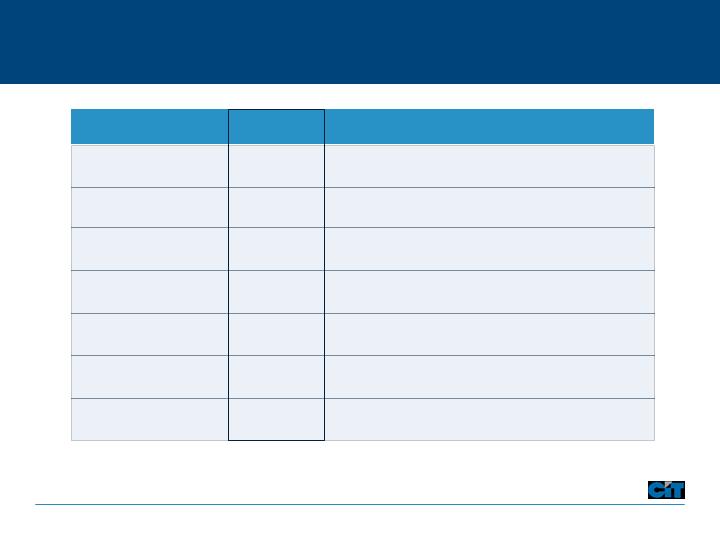

Solid Start to 2007

Increased 22%

$65,503

$79,712

Managed Assets

Increased 15%

$1.13

$1.30

EPS

Increased 60 basis points

14.2%

14.8%

ROE

Improved 140 basis points

45.7%

44.3%

Efficiency Ratio

Continued excellence

0.37%

0.39%

Net Charge-offs

Increased 14%

$707

$809

Revenue

Increased 24%

$8,716

$10,779

Volume

Comment

Q1 2006

Q1 2007

Metric

($ millions, except EPS)

4

2007 Initiatives

Leverage asset manager model

Drive operational excellence

Proactively manage risk and capital

Expand global footprint

5

Expanding the Asset Manager Model

Transportation Finance

Develop

aerospace

investment vehicle

Corporate Finance

Enter CLO market

and launch

Healthcare REIT

Consumer/SBL

Increase

originate-to-sell

activity

Release capital

Manage risk

Common Objectives

Provide ongoing capital source

Build non-spread revenue

Leverage platform

Maintain growth

6

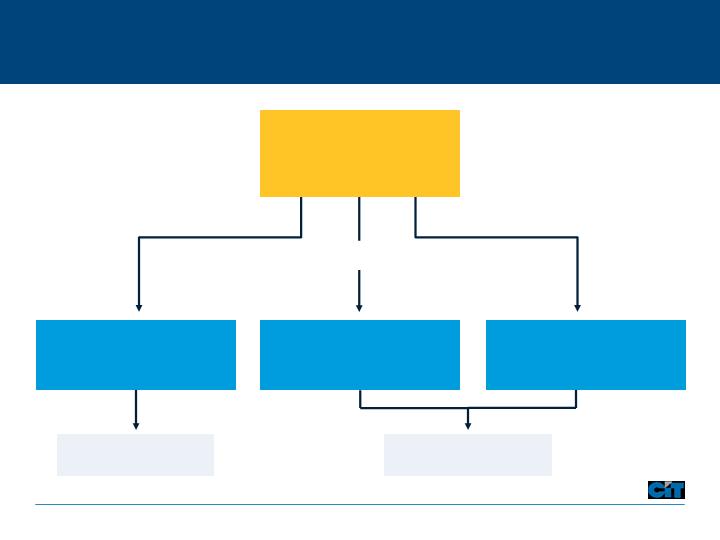

Leveraging Originations

Balance Sheet

74%

Sold / Syndicated

26%

Investment Vehicles

2007 Initiatives

‘Hold’

‘Partner / Invest’

‘Distribute’

2006

Loan / Lease Volume

($41 billion)

Net Finance Income

Non-Spread Revenue

7

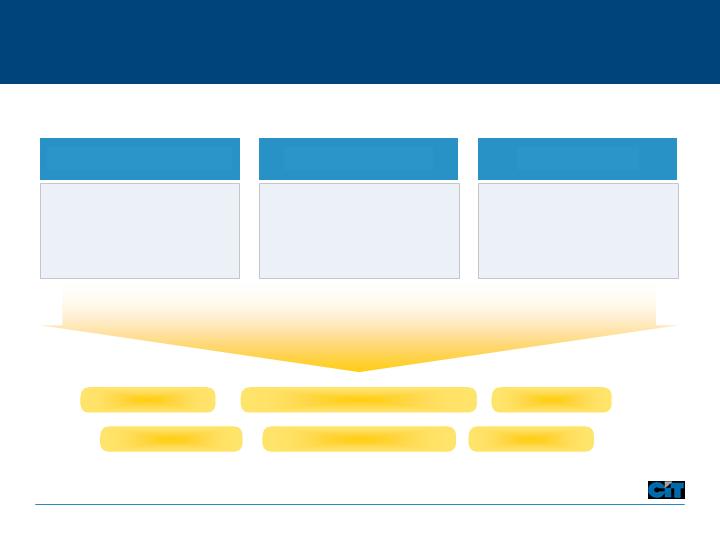

Balancing Revenue Growth

Revenue Composition

($ in Millions)

$2,218

$2,661

$2,452

$3,057

22%

NSR

Growth

$707

$809

26%

NSR

Growth

8

Driving Operational Excellence

*Guidance as presented on November 7, 2006. This should not be construed as an affirmation or update of that guidance.

* Excludes acquisitions.

Increase sales force productivity

Scale international operations

Consolidate leasing platforms

Expand shared services model

Offshore select functions

Control headcount

Efficiency Ratio

~ 42%

Target

9

Gaining Global Traction

Europe

Acquired factoring platform in Germany

Expanding global relationship with Microsoft

Acquired vendor business in U.K. and Germany

Canada

Full suite of commercial products and services

Expanding middle-market corporate finance team

Asia Pacific

Largest foreign owned leasing company in China

Centralizing vendor servicing in Shanghai

Servicing aerospace region through Singapore

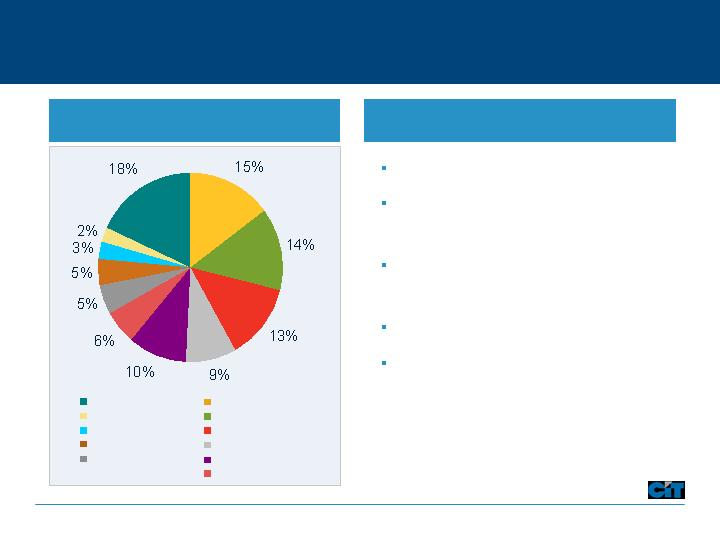

International Portfolio Assets

Canada

Europe

South Pacific

Asia Pacific

Latin America

Other

Recent Initiatives

Approx. $17 billion

24%

45%

8%

5%

10%

8%

10

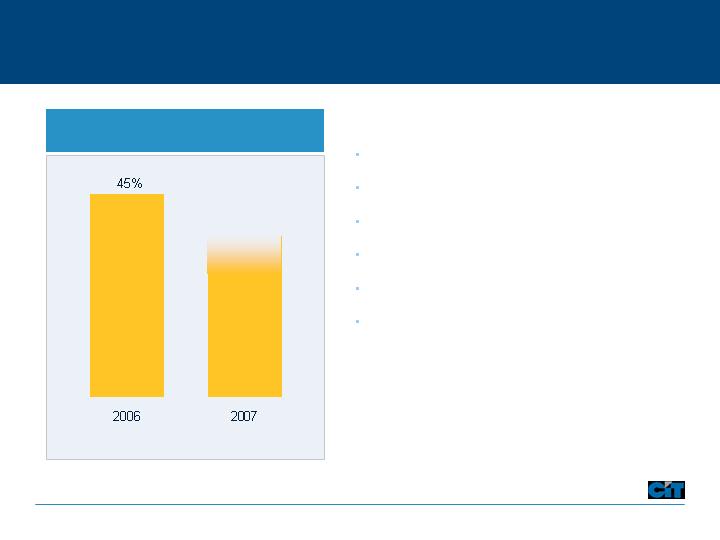

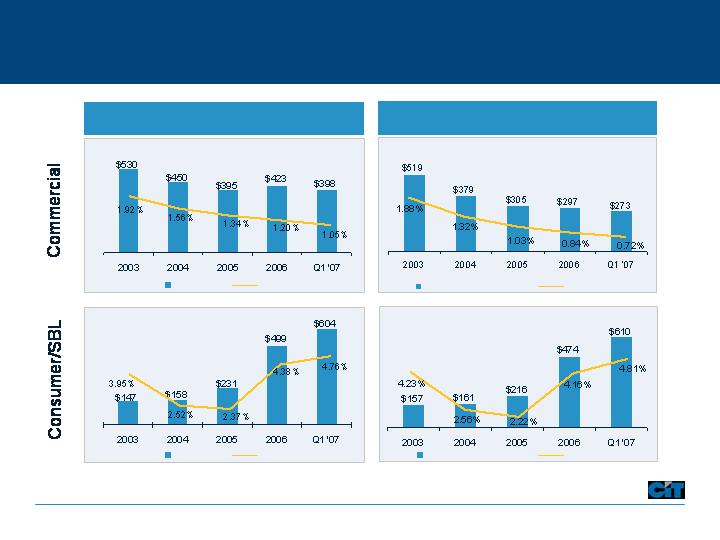

Non-Performing Assets

Monitoring Credit Quality

Delinquency 60+ Days

Owned portfolio statistics; Consumer/SBL excludes Student Loan Xpress

% of FR

Non-Accrual

Delinquent

% of FR

% of FR

Non-Accrual

Delinquent

% of FR

11

Responding to a Challenging Home Lending Market

Softening housing market

Reduced prepayment speeds

Tighter secondary market pricing

Industry consolidation

Market Trends

Initiatives

Tightened underwriting criteria

Added loss mitigation resources

Closed offices

Targeted collection efforts

Raised pricing

Increased reserves

Rising delinquencies

12

Performing Through The Business Cycles

Entered non-cyclical industries

Expanded risk management

capabilities

Managing capital in more cyclical

industries

Building international franchises

Expanding non-spread revenue

sources

Initiatives

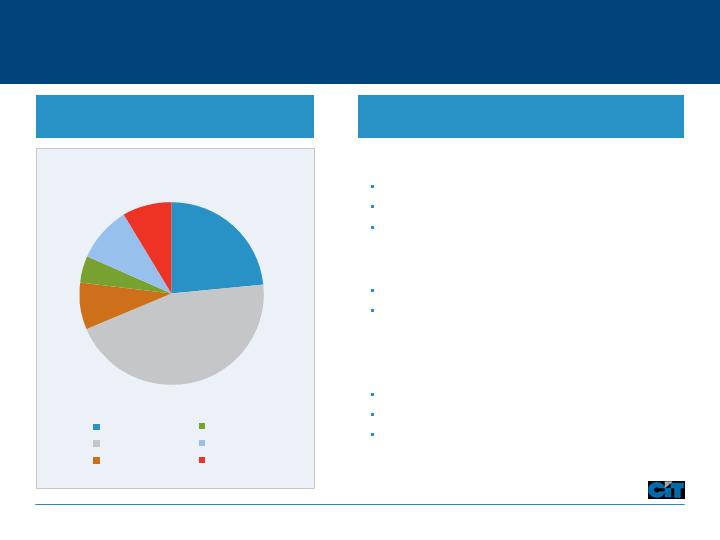

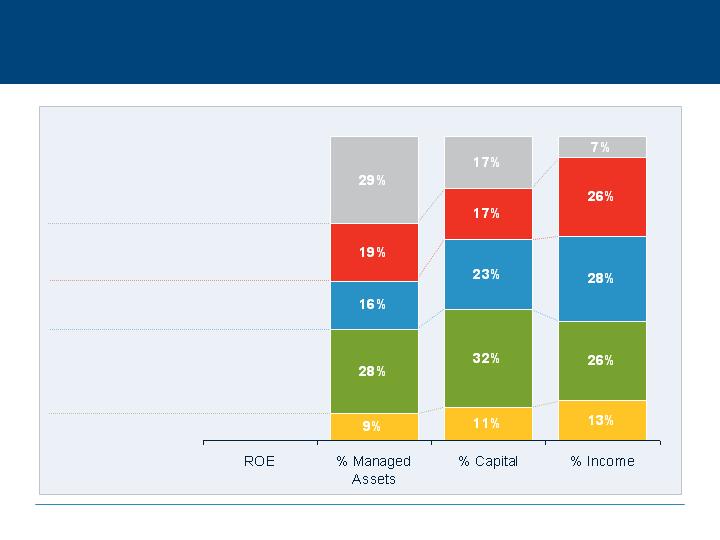

Balanced Portfolio

(% Financing and Leasing Assets)

Home Lending

Manufacturing

Educational Lending

Retail

Commercial Air

Services

Other*

Consumer-Other

Wholesale

Transportation

Healthcare

*No other industry served greater than 2%.

13

Defining Success

Strategy

2007 Performance Measures

Advance sales culture

Double digit revenue growth

Achieve balanced asset manager model

Broad based asset growth and higher fee income

Expand global footprint

Generate 25% of income/assets internationally

Drive operational excellence

Single digit expense growth, ~ 42% efficiency ratio

Maintain credit discipline

Losses < 70 basis points

Optimize capital structure

Reduce cost of capital

Improve profitability

EPS $5.40-5.50 (13-15% growth)

Enhance returns

ROE 15% (achieve target set in 2004)

14

Q1 Headwinds and Tailwinds

Margin Compression

Home Lending

Asset Growth

Commercial Credit Quality

Capital Initiatives

15

Long-term Growth Agenda

EPS Growth

Low – Mid

Teens

The leading global finance company for the middle market

ROE

Mid - Upper

Teens

16

Keys to Enhancing Long-term Profitability

Leverage originations platform

Drive capital allocation and efficiency

Further credit and cost disciplines

Balance revenue streams

17

Appendix

Managed Assets - $80B

Business Overview

Aerospace & Railcar Leasing

Asset Based Lending

Equipment Lending & Leasing

Factoring & Trade Finance

Financial Advisory Services

Project Financing

SBA Lending

Student Lending

Vendor Finance

Trade

Finance

Transportation

Finance

Vendor

Finance

Consumer/

Small

Business

Lending

Corporate

Finance

Leadership Positions

Data as of December 31, 2005

19

Trade Finance

Leading factoring business in the U.S.

Vital credit bridge between vendors and retailers

Provide credit insurance, loans and back-office processing

Superb track record of navigating retail credit cycles

Long-term client relationships – average 10+ years

Expanding international presence

Highly efficient processor

Annuity-like earnings

Value

Drivers

Low-cost

provider

International

capabilities

Innovative

technology

Relationship

oriented

20

20

Transportation Finance

Top 3 global aerospace and North American railcar lessor

Attractive and modern fleets

Aerospace – own over 300 commercial and regional aircraft

Rail – manage over 100,000 railcar fleet

Full product offering with flexible deal terms

Four decades of experience

Strong relationships with deep market penetration

Experts in managing and maximizing collateral values

Seasoned equipment managers with proven residual

realization

21

Data as of December 31, 2005

Value

Drivers

Industry

knowledge

Collateral

expertise

Structuring

flexibility

Remarketing

capability

21

Corporate Finance

Leading provider of working capital to the middle market

Unique go-to-market strategy

Asset based lender to multiple industries

Healthcare, communications, media, entertainment, energy,

infrastructure, construction and industrial

Strong debtor-in-possession (DIP), turn around and

expansion financing capabilities

Deal-oriented and collateral protected

Long-standing referral relationships

Significant fee generator

22

Value

Drivers

Client

focus

Life-cycle

financing

Committed

presence

Industry

expertise

Trusted

advisors

22

Vendor Finance

Leading provider of global vendor finance solutions

Thousands of vendor relationships in the US and abroad

Preferred provider relationships with Dell, Microsoft,

Avaya, Snap-on-Tools, and other Fortune 500 companies

Efficient and scalable platforms

State-of-the-art transaction processing technology

Disciplined underwriting supplemented by behavioral

analysis

Collateral and residual management expertise

Global sales coverage (34 countries) with regional

servicing centers

23

Value

Drivers

Structuring

expertise

Global

capabilities

Integrated

systems

Low-cost

provider

23

Consumer / Small Business Lending

Home Lending:

Broker-driven origination network

Disciplined lending standards

Conservative product set

Centralized servicing

Student Lending:

Top player in student loan market

Preferred Lender at over 1,400 schools

Government guaranteed FFELP collateral

SBA Lending:

#1 provider of government backed 7(a) small

business loans for seven consecutive years

24

Value

Drivers

Intermediary

relationships

Efficient

servicing

Brand

recognition

Consistent

underwriting

24

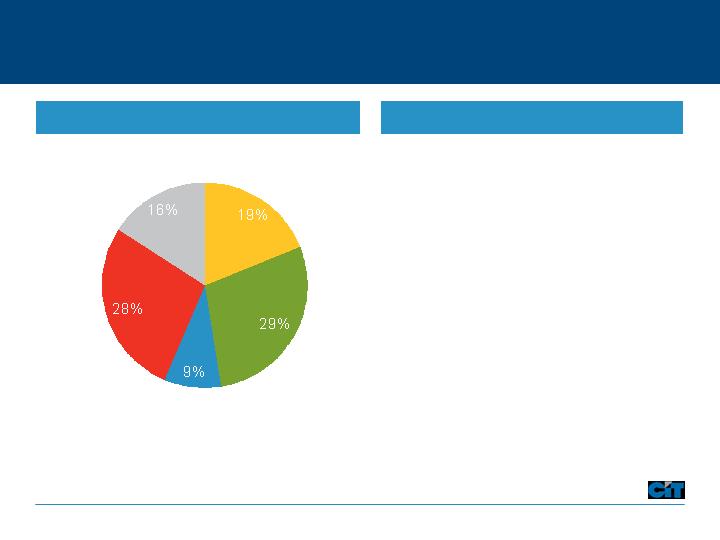

Segment Performance

Transportation Finance

Trade Finance

Corporate Finance

Vendor Finance

Consumer/SBL

$80 B

$8 B

$258 M

19%

17%

13%

20%

6%

25

Proven Acquisition Strategy

Doubled assets

Q1

4,300

Education Loans

EDLG

Solid returns

Q1

860

Factoring

SunTrust

Accelerated build out

Q3

500

Healthcare

HBCC

Closed April 30

Q2

2,000

Vendor Finance (US)

Citigroup

Realized synergies

Q3

700

Vendor Finance

CitiCapital

Strong volume

Q2

520

Technology Leasing

GATX

Completed integration Q107

Q4

700

Diversified equipment

RBS/Citizens

Included serviced fleet

Q4

90

Rail

Bombardier

Established foothold

Hit the ground running

Comments

165

2,000

Assets ($mm)

Q2

Factoring (Germany)

Enterprise Finance

Q1

Vendor Finance (Europe)

Barclays

Closed

Asset Type

Seller

26

Board of Directors

President & CEO

Martha Stewart Living

Chairman & CEO New

York Life Insurance Co.

Chairman & CEO

C.R. Bard Inc.

President & CEO

ADP

Managing Partner

McCarter & English LLP

Chancellor SUNY

Maritime College

EVP& CFO International

Paper Company

Chairman

TerreStar Networks Inc

Retired

CEO & Chairman

CIT Group Inc.

Current

Position

2006

Susan Lyne

2005

Seymour Sternberg

2005

Timothy M. Ring

2004

Gary Butler

2003

Lois M. Van Deusen

Chair

2003

John R. Ryan

2003

Marianne Miller Parrs

Chair

2003

William M. Freeman

Chair

Lead

2002

Peter J. Tobin

2003

Jeffery M. Peek

Nominating &

Governance

Compensation

Audit

Board Member

Board Committees

Independent

Directors

Member

Since

27

Noteworthy Items

28

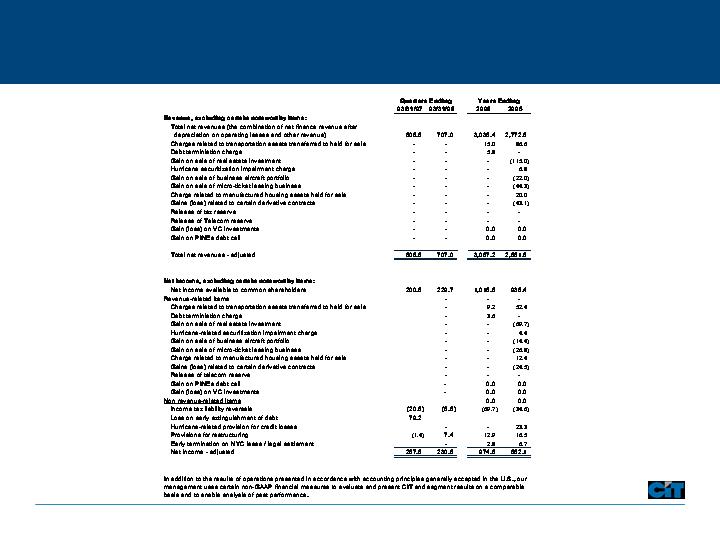

Non-GAAP Reconciliation

*The preferred capital securities were called on April 10, 2007. On March 16, 2007, $250 million of additional junior subordinated notes were issued in anticipation

of the preferred capital securities call. Accordingly only $500 million of the junior subordinated notes were included in our March 31, 2007 capitalization ratios.

*

29

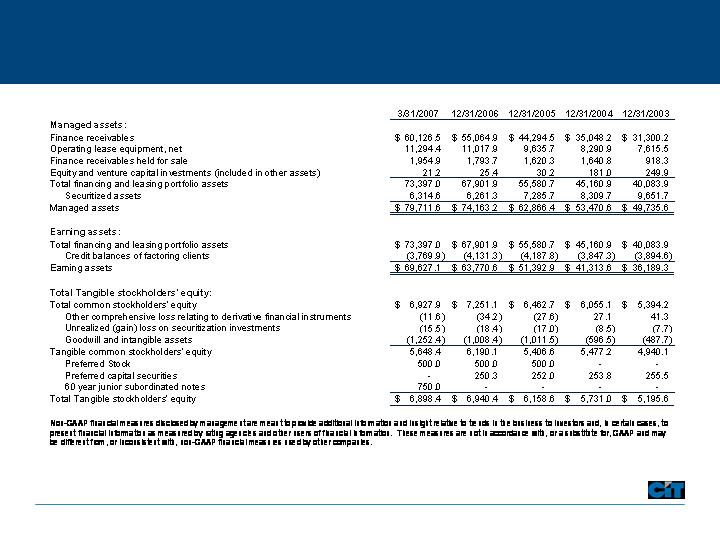

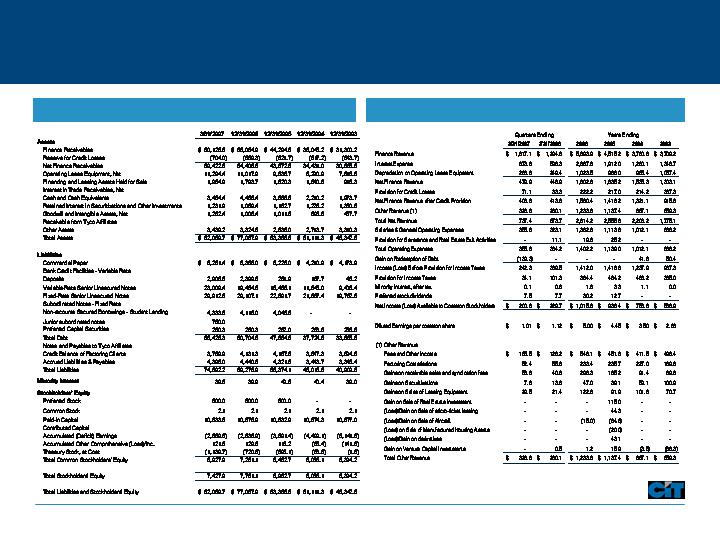

Financial Statements

Balance Sheet

Income Statement

$11 Billion Market Capitalization

30