Lehman Financial

Services Conference

New York

September 11, 2007

Notices

Forward Looking Statements

Certain statements made in these presentations that are not historical facts may constitute “forward-

looking” statements under the Private Securities Litigation Reform Act of 1995, including those that are

signified by words such as “anticipate”, “believe”, “expect”, “estimate”, “target”, and similar expressions.

These forward-looking statements reflect the current views of CIT and its management and are subject

to risks, uncertainties, and changes in circumstances. CIT’s actual results or performance may differ

materially from those expressed in, or implied by, such forward-looking statements. Factors that could

affect actual results and performance include, but are not limited to, potential changes in interest rates,

competitive factors and general economic conditions, changes in funding markets, industry cycles and

trends, uncertainties associated with risk management, risks associated with residual value of leased

equipment, and other factors described in our Form 10-K for the year ended December 31, 2006 and 10-

Q for the quarter ended June 30, 2007. CIT does not undertake to update any forward-looking

statements.

This presentation is derived from CIT’s publicly available information and is to be used solely as

part of CIT management’s continuing investor communications program. This presentation has

not been prepared in connection with, and should not be used in connection with, any offering of

securities by CIT. For the sale of any securities by CIT you are directed to rely only upon the

offering document for those particular securities.

Data as of or for the period ended June 30, 2007 unless otherwise noted.

2

Building on Nearly 100 Years of Success

$7 Billion Market Capitalization

Global Servicing Capabilities

Customized Financial Solutions

Strong Credit Culture

Managed Assets $80 Billion

Premium Brand

Diverse Portfolio

3

Agenda

What’s New?

What’s the Same?

Evolving business environment

Decisions on home lending

Migration of funding strategy

Strong business franchises

Strategic initiatives

Core value proposition

4

Evolving Business Environment

Re-pricing

of

Risk

Reduced

Market

Competition

Fragile

Investor

Sentiment

Reduced

Market

Liquidity

Weakened

Housing

Sector

5

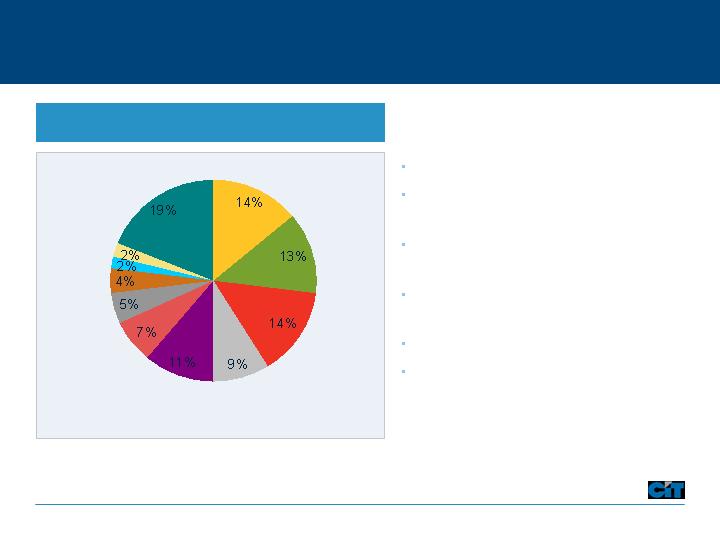

Diverse and Liquid Asset Base

High quality and liquid portfolio

Strong asset cash flows support

franchise

No industry represents more than

15% of asset base

Less than 20% of assets are

encumbered

Broad geographic spread of risk

Prudent loan loss reserves

Portfolio Assets

Other*

Manufacturing

Home Lending

Educational

Lending

Retail

Commercial Air

Consumer-Other

Wholesale

Transportation

Healthcare

Services

*No other industry greater than 2%

6

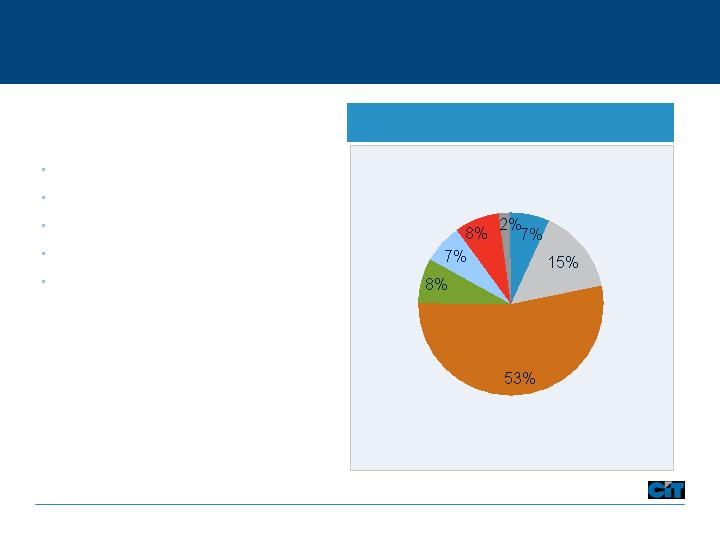

Flexible Funding Model

Match-funded portfolio

Resilient liability structure

Proven secured programs

Strong capital generation

Solid credit ratings

Capital Structure

Commercial Paper

Secured –

on B/S

LTD –

Due < 1year

LTD – Due > 1 year

Secured – off B/S

Common Equity

Preferred &

Sub Debt

Data as of June 30, 2007

7

Funding Plan Progressing

~$5 billion of unsecured commercial paper outstanding

Continue to issue commercial paper daily

Costs have increased with overall market

Short-term Financing

Long-term Financing

Second half 2007 term funding needs of approximately $6-8 billion

Completed about half of that funding in the secured markets since June 30, 2007

$1.8B Student lending

$1.5B Trade Finance

$0.3B Equipment

Opportunistically tap the capital markets if economics are right

Data as of August 31, 2007

8

Strong Alternate Liquidity

$12B of committed and available liquidity

$7.5B unsecured facilities available

No material adverse change clause

1 financial covenant: Net worth >$4B

$4.5B secured facilities available

Bank sponsored multi-issuer conduits

Diverse asset classes (equipment, vendor, trade and student loans)

Ability to fund against other portfolio assets (asset based loans, mortgages,

SBA loans, airplanes and railcars)

Data as of August 31, 2007

9

Continued Progress on Home Lending

Announced intent to exit home lending business on July 18, 2007

Classified assets as held for sale

Recorded a $731M pre-tax charge reflecting fair-value adjustment

Established task force to evaluate strategic options

Announced closing of origination operations on August 28, 2007

Analyzing optimal liquidation strategy and related accounting treatment

Maximizing loan collection and servicing efforts to ensure best performance

Monitoring results in Q3 and Q4:

Portfolio to generate $40-$50 million of pre-tax earnings per quarter which will

bolster the home lending equity base (excludes $35M restructuring charge in Q3)

Expected losses of ~$50 million per quarter largely factored into 6/30 fair value

adjustment

Completed Actions

On-going Initiatives

10

Home Lending Portfolio Statistics

~ 90% 1st liens and owner occupied

Geographically diverse portfolio

Limited ‘interest only’ exposure

No ‘negative am’ or ‘option ARMS’

59% fully documented loans

43% fixed rate

50% of reset risk in 2009 or beyond

Better than sub-prime industry stats:

129 bps losses (YTD)

6.5% delinquency (60+)

2.1% foreclosure rate

82%

Loan-to-value

41%

Debt to Income

20 Months

Seasoning*

8 years

Employment

6 years

Residence

$128K

Loan Size

636

FICO

Portfolio averages at June 30, 2007

Demographics

Characteristics

* Weighted Average

Industry data cited from: LoanPerformance, A Subsidiary of First American Real Estate Solutions

11

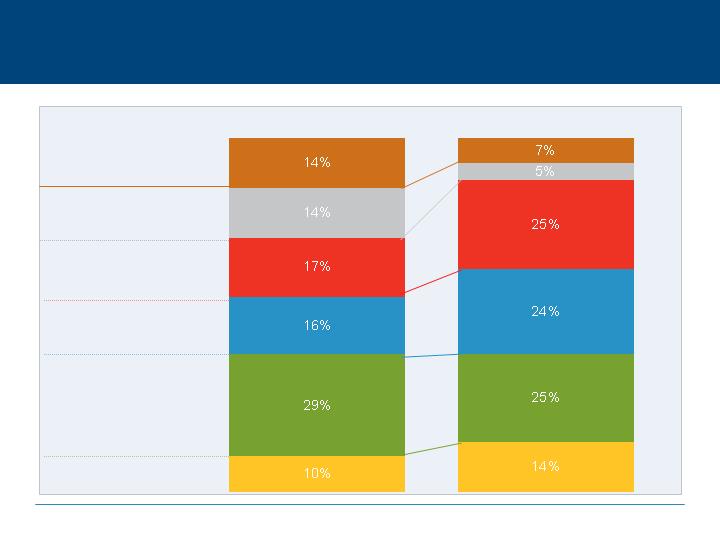

Franchise Businesses Drive Earnings and Growth

Transportation Finance

Trade Finance

Corporate Finance

Vendor Finance

Student / SBL

Home Lending

Based on full year 2006

% Managed Assets

% Income

12

Market leader with global presence

Thousands of vendor relationships including

Dell, Microsoft, Avaya and Snap-on-Tools

Efficient and scalable platforms

Collateral and residual management expertise

Vendor Finance: Remains Strong

Continuing to invest capital in high growth / high ROE segment

Maintaining strong credit performance and residual realization

Strong organic originations off-setting lower Dell Financial Services volumes

Focused on realizing synergies from recent Barclays and Citi acquisitions

Microsoft roll-out remains on schedule

Studying feasibility of funding vendor assets in CIT Bank

17%

0.58%

51%

$452M

$17.0B

YTD

6/30/07

ROE

Charge-offs

Efficiency

Revenue

Managed Assets

Business Profile

Financial Profile

Business Update

13

Leading factoring business in the U.S.

Long-term client relationships with thousands

of customer credit profiles

Track record of navigating retail credit cycles

and highly efficient processing

Annuity-like earnings and consistent returns

Trade Finance: A Recognized Leader

Commission rates poised to recover following dip on benign credit

Seasonal build-up in inventories/volume in progress

Focused on expanding international presence

Further efficiency studies underway

17%

0.51%

38%

$199M

$6.9B

YTD

6/30/07

ROE

Charge-offs

Efficiency

Revenue

Managed Assets

Business Profile

Financial Profile

Business Update

14

Top 3 global aerospace and North American

railcar lessor

Attractive and modern fleets

Experts in managing and maximizing collateral

values and residual realization

Strong relationships with deep market penetration

Transportation Finance: Utilization Remains High

Air:

Full economic utilization at strong lease rates and good returns

Robust and attractively priced order book will benefit near-term returns

Rail:

Strong utilization continues - around 95%

Lease rates solid, although coming off cyclical highs

17%

-2.02%

34%

$227M

$12.7B

YTD

6/30/07

ROE

Charge-offs

Efficiency

Revenue

Managed Assets

Business Profile

Financial Profile

Business Update

15

Preeminent lender to middle-market companies

Long-standing referral relationships

Re-invigorated sales culture

Industry focused teams in healthcare,

communications, media, entertainment,

energy, commercial and industrial.

Corporate Finance: Leveraging Deep Relationships

Balancing liquidity between existing clients and attractive market opportunities

Improved pricing for lenders with a return to more conventional covenants

Slow syndications market impacting fees, but restructuring business gearing up

Originations in less cyclical industries continue strong

13%

0.25%

47%

$457M

$19.8B

YTD

6/30/07

ROE*

Charge-offs

Efficiency*

Revenue*

Managed Assets

Business Profile

Financial Profile

Business Update

* Excludes $229 million (pre-tax) gain on construction sale

16

Top 15 originator

Complete front to back end operation

Preferred Lender at over 1,400 schools

Predominantly govt. guaranteed FFELP collateral

Student Lending: An Evolving Story

Operating performance exceeding expectations

New legislation does not impact current portfolio

Evaluating impact of legislation on profitability of future originations

Business Profile

Financial Profile

Business Update

NM

Charge-offs

10%

ROE

61%

Efficiency

$76M

Revenue

$10.3B

Managed Assets

YTD

6/30/07

17

Underlying Financial Performance Solid

$2.48

NM

NM

$0.34

EPS

NM

NM

NM

$.194

NM

NM

NM

$38

Other

Items*

48%

32%

42%

Efficiency Ratio

0.28%

2.99%

$1.4

$69

$18

16%

$488

Adjusted

Results

1.27%

2.11%

$.131

$11

$ 4

NM

$(460)

Home

Lending

$22

Volume ($ Billion)

$1.7

Net Revenue ($ Billion)

2%

ROE

0.46%

Net Charge-offs

2.85%

Net Margin

$80

Managed Assets ($ Billion)

$66

Net Income ($ Million)

Reported

Results

Metric

Data as of or for the six months ended June 30, 2007

* Excludes the following pre-tax items: gain on constructions sale ($229), cost of early debt extinguishment ($139) and MH write-down ($34).

18

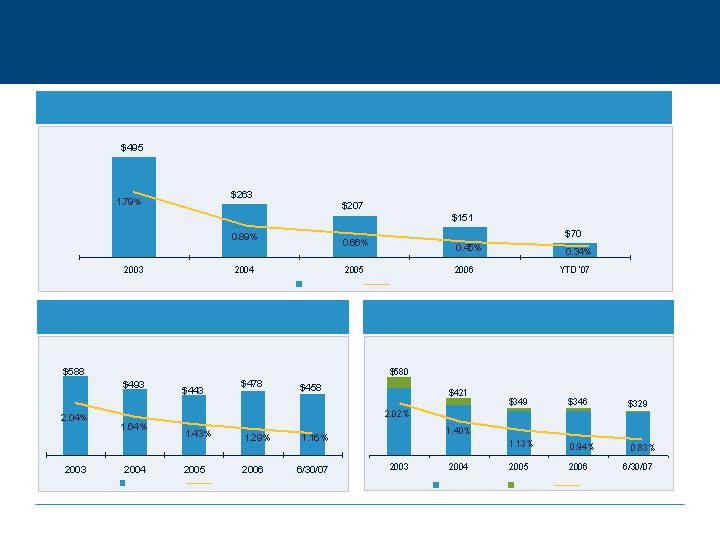

Non-Performing Assets

Commercial Credit Quality Remains Excellent

% of FR

Repo

Non-Accrual

Credit Losses

Delinquent

% of FR

Charge-offs

% of AFR

Delinquency 60+ Days

Owned portfolio statistics: excludes home lending and student lending

19

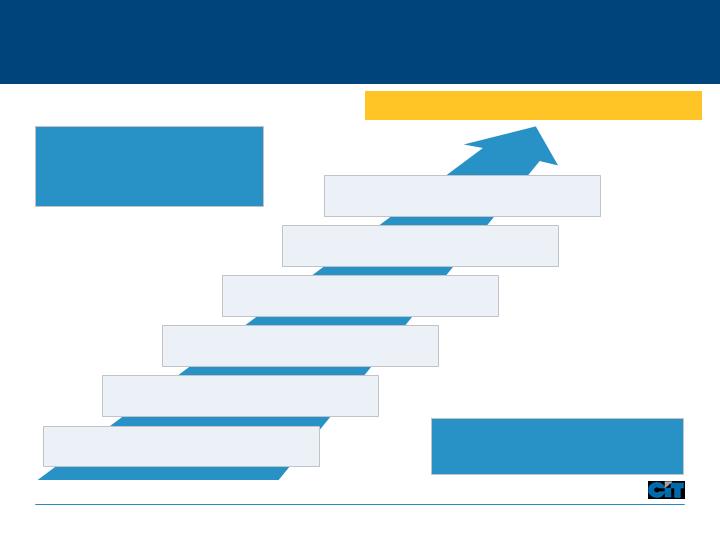

Model Designed to Deliver Earnings Through All Cycles

Strong Economy

Growth Capital

Mergers and Acquisitions

Real Estate Packages

Equipment Utilization

Vendor Sales Financing

Competitors enter,

margins decline

Weak Economy

Factoring

Restructuring / DIP

Distressed Debt

Advisory Services

Vendor Renewals

Competitors exit,

margins improve

Performance Improves

Performance Improves

20

Progress on 2007 Strategic Initiatives

Leverage asset

manager model

Executed first CLO in May

Completed Healthcare REIT IPO in June

Aerospace offering in registration

Proactively manage

risk and capital

Managing portfolio investments

Proceeds from construction sale

Invested in vendor and corporate finance

Completed $500M share repurchase program

Expand global

footprint

Acquired Barclays UK/German vendor business

Opened aerospace operation in China

Expanded our European leveraged finance team

Drive operational

excellence

Reduced second quarter headcount

Eliminated the operating group structure

Driving acquisition synergies

21

CIT: Proven Value Proposition

Leading provider of

capital to middle-

market…

… with 100 years of

success

Diverse Portfolio

Broad-based Revenues

Disciplined Credit Culture

Global Operations

Long-Standing Relationships

Deep Industry Expertise

Sustainable Earnings Growth & Returns

22

23