TEMECULA VALLEY BANCORP 2007 Annual Meeting of Shareholders May 22, 2007

TEMECULA VALLEY BANCORP 2007 Annual Meeting of Shareholders May 22, 2007 Safe Harbor Statement Safe Harbor Statement Certain statements contained in this presentation, including, wi Certain statements contained in this presentation, including, without limitation, thout limitation, statements containing the words statements containing the words “believes believes”, “anticipates anticipates”, “intends intends”, and , and “expects expects”, and words of similar import, constitute and words of similar import, constitute “forward forward-looking statements looking statements” within the within the meaning of Section 27A of the Securities Act of 1933 and Section meaning of Section 27A of the Securities Act of 1933 and Section 21E of the 21E of the Securities Exchange Act of 1934. Securities Exchange Act of 1934. Such forward looking statements involve known and unknown risks, Such forward looking statements involve known and unknown risks, uncertainties uncertainties and other factors that may cause the actual results, performance and other factors that may cause the actual results, performance or achievements of or achievements of Temecula Valley Bancorp ( Temecula Valley Bancorp (“the Company the Company”) to be materially different from any future ) to be materially different from any future results, performance or achievements expressed or implied by suc results, performance or achievements expressed or implied by such forward h forward-looking looking statements. Such factors include, among others, the following; g statements. Such factors include, among others, the following; general economic and eneral economic and business conditions in those areas in which the Company operates business conditions in those areas in which the Company operates, demographic , demographic changes, competition, fluctuations in interest rates, changes in changes, competition, fluctuations in interest rates, changes in business strategy or business strategy or development plans, changes in governmental regulation, credit qu development plans, changes in governmental regulation, credit quality, the ality, the availability of capital to fund the expansion of the Company availability of capital to fund the expansion of the Company’s business, and other s business, and other factors referenced in this presentation. factors referenced in this presentation. The Company disclaims any obligation to update any such factors The Company disclaims any obligation to update any such factors or to publicly or to publicly announce the results of any revisions to any of the forward announce the results of any revisions to any of the forward-looking statements looking statements contained herein to reflect future events or developments. contained herein to reflect future events or developments.

???? Founded in December, 1996 Founded in December, 1996 ???? $1.24 billion in assets at Dec. 31, 2006 $1.24 billion in assets at Dec. 31, 2006 ???? 10 branches in Southern California 10 branches in Southern California ???? Market cap Market cap of $203+ million of $203+ million* ???? Our brand evolves as our bank matures Our brand evolves as our bank matures ~ 10 Years of Successful Growth ~ ~ 10 Years of Successful Growth ~ 1996 to 2006 1996 to 2006 * As of May 11, 2007

TVB 2006 Milestones TVB 2006 Milestones ???? January 16 January 16: Named All Star Top 20 Bank by U.S. Banker magazine. : Named All Star Top 20 Bank by U.S. Banker magazine. Ranked No. 7 out of 8,000 banks nationwide based on 24.97% ROE Ranked No. 7 out of 8,000 banks nationwide based on 24.97% ROE ???? April 20 April 20: Received : Received “Five Year Stock Appreciation Award Five Year Stock Appreciation Award” by by Carpenter & Co. for 675% return to shareholders Carpenter & Co. for 675% return to shareholders – 5 yrs ending 12/05 5 yrs ending 12/05 ???? April 21 April 21: Announced record 1 : Announced record 1st st quarter earnings, up 33% above 1Q quarter earnings, up 33% above 1Q 2005 2005 ???? June 27 June 27: Added to NASDAQ : Added to NASDAQ’s Global Select Market, its top tier listing s Global Select Market, its top tier listing ???? July 6 July 6: Recognized as Top Performing Community Bank in U.S. by : Recognized as Top Performing Community Bank in U.S. by U.S. Banker magazine based on 3 U.S. Banker magazine based on 3-year average ROE of 29.39% year average ROE of 29.39% ???? July 20 July 20: Received national recognition as top : Received national recognition as top-performing small cap performing small cap company making Sandler O company making Sandler O’Neill Neill’s Sm s Sm-All Star List All Star List ???? July 24 July 24: Announced record 2 : Announced record 2nd nd quarter earnings, up 1 quarter earnings, up 15% above 2Q 5% above 2Q 2005 2005

TVB 2006 Milestones TVB 2006 Milestones ???? August 8 August 8: Announced opening of 9 : Announced opening of 9th th full full-service office in Solana Beach service office in Solana Beach ???? September 14 September 14: Recognized : Recognized by U.S. Banker in Top 100 List as #1 by U.S. Banker in Top 100 List as #1 performer of U.S. banks performer of U.S. banks with assets of $1 with assets of $1-10 billion 10 billion based on 3 based on 3-year year average ROE of 30.40% average ROE of 30.40% ???? October 18 October 18: Announced record 3 : Announced record 3rd rd quarter earnings, up quarter earnings, up 22% above 3Q 22% above 3Q 2005 2005 ???? November 20 November 20: Announced opening of 10 : Announced opening of 10th th full full-service office in Ontario service office in Ontario ???? November 30 November 30: Named No. 1 Independent Bank 7(a) Lender for fifth : Named No. 1 Independent Bank 7(a) Lender for fifth consecutive year consecutive year – ranked 14th overall in SBA 7(a) and SBA 504 loan ranked 14th overall in SBA 7(a) and SBA 504 loan volume among all SBA lenders nationwide volume among all SBA lenders nationwide ???? December 31 December 31: Closed the year with record earnings, up 21% : Closed the year with record earnings, up 21%

Our Mission Remains Unchanged Our Mission Remains Unchanged ???? Superior personal service Superior personal service ???? Set higher standards of professionalism Set higher standards of professionalism ???? Ensure strong organic growth Ensure strong organic growth

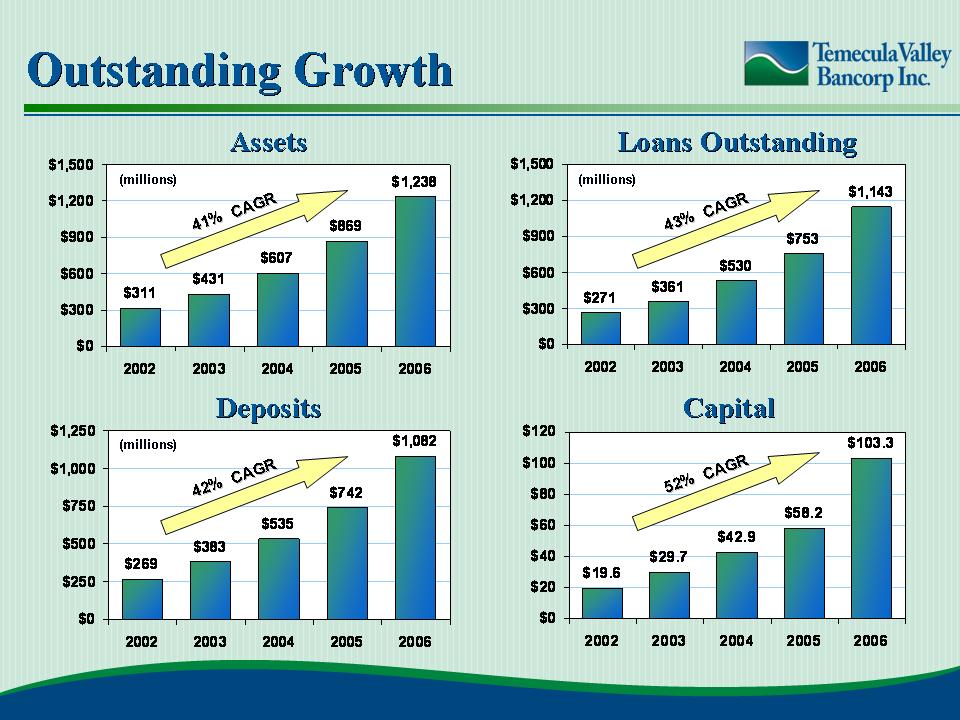

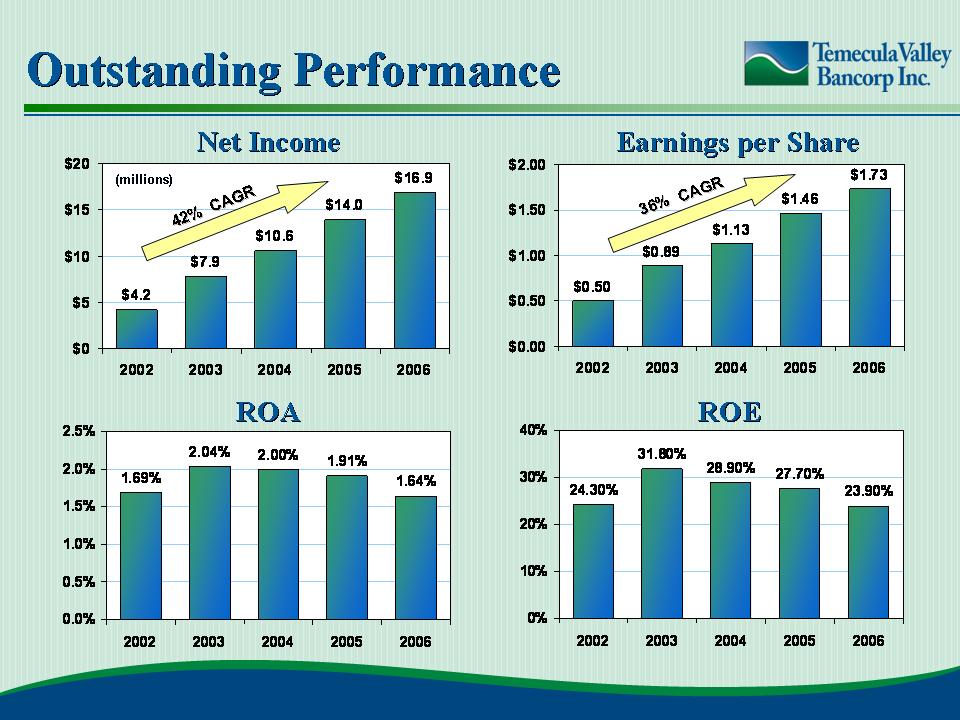

Outstanding Growth Outstanding Growth $269 $383 $535 $742 $1,082 $0 $250 $500 $750 $1,000 $1,250 2002 2003 2004 2005 2006 $19.6 $29.7 $42.9 $58.2 $103.3 $0 $20 $40 $60 $80 $100 $120 2002 2003 2004 2005 2006 Assets Assets xx% CAGR xx% CAGR Loans Outstanding Loans Outstanding Deposits Deposits Capital Capital $311 $431 $607 $869 $1,238 $0 $300 $600 $900 $1,200 $1,500 2002 2003 2004 2005 2006 $271 $361 $530 $753 $1,143 $0 $300 $600 $900 $1,200 $1,500 2002 2003 2004 2005 2006 43% CAGR 43% CAGR 41% CAGR 41% CAGR 42% CAGR 42% CAGR 52% CAGR 52% CAGR (millions) (millions) (millions) $0.50 $0.89 $1.13 $1.46 $1.73 $0.00 $0.50 $1.00 $1.50 $2.00 2002 2003 2004 2005 2006 24.30% 31.80% 28.90% 27.70% 23.90% 0% 10% 20% 30% 40% 2002 2003 2004 2005 2006 1.69% 2.04% 2.00% 1.91% 1.64% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 2002 2003 2004 2005 2006 $4.2 $7.9 $10.6 $14.0 $16.9 $0 $5 $10 $15 $20 2002 2003 2004 2005 2006

Outstanding Performance Outstanding Performance 36% CAGR 36% CAGR 42% CAGR 42% CAGR ROE ROE ROA ROA

The Foundation of Our Strategy is Exceptional People The Foundation of Our Strategy is Exceptional People ???? Entrepreneurship Entrepreneurship ???? Pay for performance Pay for performance We Build the Business Around the Bankers We Build the Business Around the Bankers Experienced Management Team Experienced Management Team ???? Average 25 years industry experience Average 25 years industry experience ???? Experience with various economic cycles Experience with various economic cycles ???? Strong credentials Strong credentials ???? Empowerment Empowerment ???? Delegation of authority Delegation of authority ???? Results Results

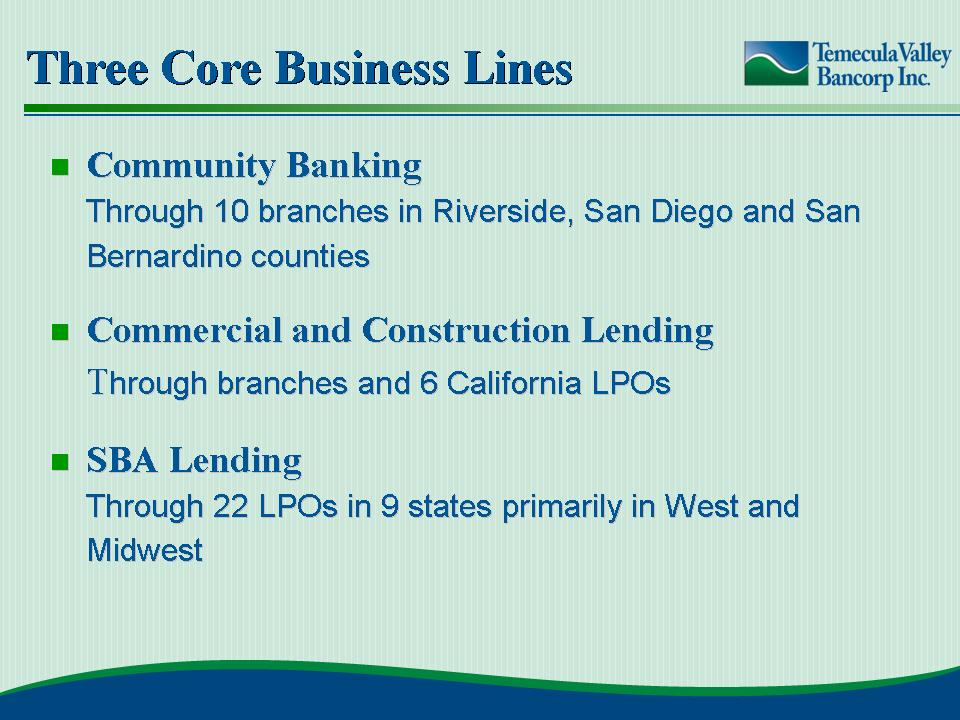

Three Core Business Lines ???? Community Banking Community Banking Through 10 branches in Riverside, San Diego and San Through 10 branches in Riverside, San Diego and San Bernardino counties Bernardino counties ???? Commercial and Construction Lending Commercial and Construction Lending Through branches and 6 California LPOs hrough branches and 6 California LPOs ???? SBA Lending SBA Lending Through 22 LPOs in 9 states primarily in West and Through 22 LPOs in 9 states primarily in West and Midwest Midwest

Source: SNL Financial 16.4% 16.4% ~16.0% ~16.0% 7.1 7.1 10 10 Total 1 6 3 # of TMCV # of TMCV Branches Branches 17.3% 17.3% 17.3% 17.3% 2.0 2.0 San Bernardino 6.5% 6.5% 9.0% 9.0% 3.1 3.1 San Diego 6.66% 6.66% 7.87% 7.87% 303.6 303.6 U.S. 8.0% 8.0% 9.9% 9.9% 37.2 37.2 California 25.9% 25.9% 30.6% 30.6% 2.0 2.0 Riverside Proj. Proj. % ? Pop. Pop. 2006 2006 – 2011 2011 % Pop. % Pop. Growth Growth 2000 2000 – 2006 2006 2006 2006 Pop. Pop. (MM) (MM) Our market is one of the fastest growing in the U.S. Our market is one of the fastest growing in the U.S.

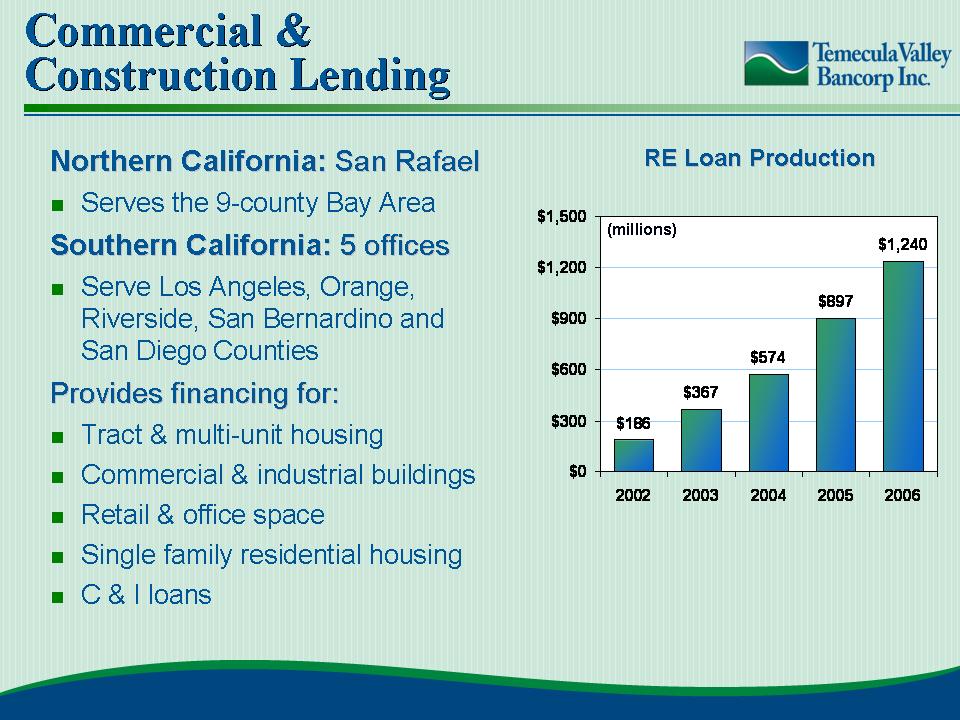

Community Banking Community Banking SOUTHERN CALIFORNIA SOUTHERN CALIFORNIA Northern California: Northern California: San Rafael San Rafael ?? Serves the 9-county Bay Area Southern California: Southern California: 5 offices 5 offices ?? Serve Los Angeles, Orange, Riverside, San Bernardino and San Diego Counties Provides financing for: Provides financing for: ?? Tract & multi-unit housing ?? Commercial & industrial buildings ?? Retail & office space ?? Single family residential housing ?? C & I loans Commercial & Construction Lending Commercial & Construction Lending RE Loan Production RE Loan Production $186 $367 $574 $897 $1,240 $0 $300 $600 $900 $1,200 $1,500 2002 2003 2004 2005 2006 (millions) $205 $216 $298 $300 $353 $0 $100 $200 $300 $400 2002 2003 2004 2005 2006

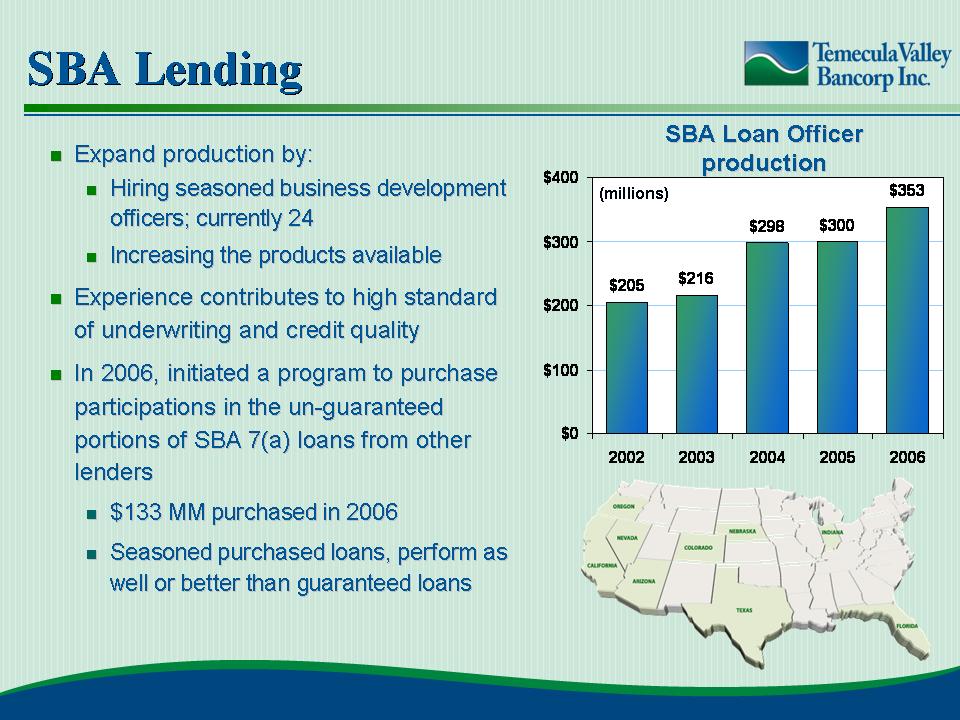

???? Expand production by: Expand production by: ???? Hiring seasoned business development Hiring seasoned business development officers; currently 24 officers; currently 24 ???? Increasing the products available Increasing the products available ???? Experience contributes to high standard Experience contributes to high standard of underwriting and credit quality of underwriting and credit quality ???? In 2006, initiated a program to purchase In 2006, initiated a program to purchase participations in the un participations in the un-guaranteed guaranteed portions of SBA 7(a) loans from other portions of SBA 7(a) loans from other lenders lenders ???? $133 MM purchased in 2006 $133 MM purchased in 2006 ???? Seasoned purchased loans, perform as Seasoned purchased loans, perform as well or better than guaranteed loans well or better than guaranteed loans SBA Lending SBA Lending SBA Loan Officer SBA Loan Officer production production (millions)

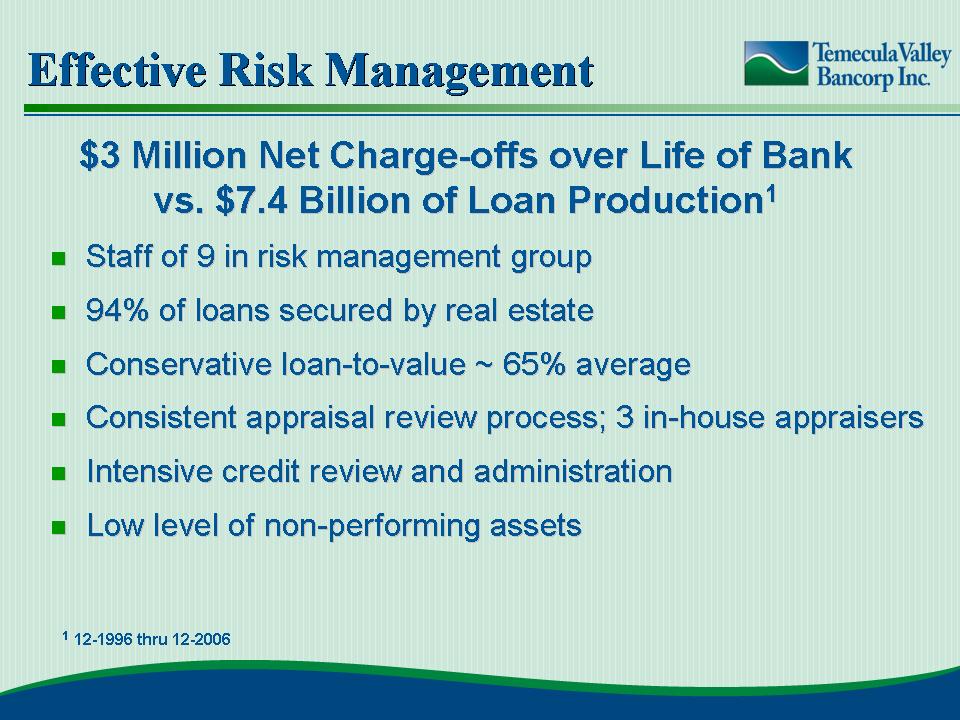

Effective Risk Management Effective Risk Management ???? Staff of 9 in risk management group Staff of 9 in risk management group ???? 94% of loans secured by real estate 94% of loans secured by real estate ???? Conservative loan Conservative loan-to to-value ~ 65% average value ~ 65% average ???? Consistent appraisal review process; 3 in Consistent appraisal review process; 3 in-house appraisers house appraisers ???? Intensive credit review and administration Intensive credit review and administration ???? Low level of non Low level of non-performing assets performing assets 1 12-1996 thru 12-2006 $3 Million Net Charge $3 Million Net Charge-offs over Life of Bank offs over Life of Bank vs. $7.4 Billion of Loan Production vs. $7.4 Billion of Loan Production1

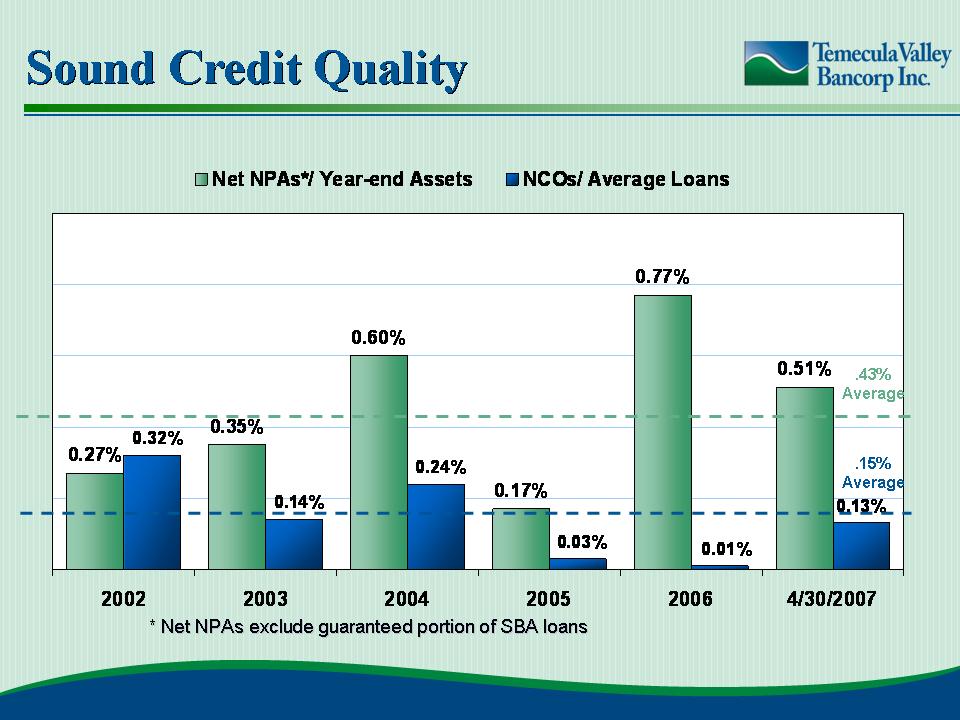

Sound Credit Quality Sound Credit Quality * Net NPAs exclude guaranteed portion of SBA loans * Net NPAs exclude guaranteed portion of SBA loans .43% Average .15% Average

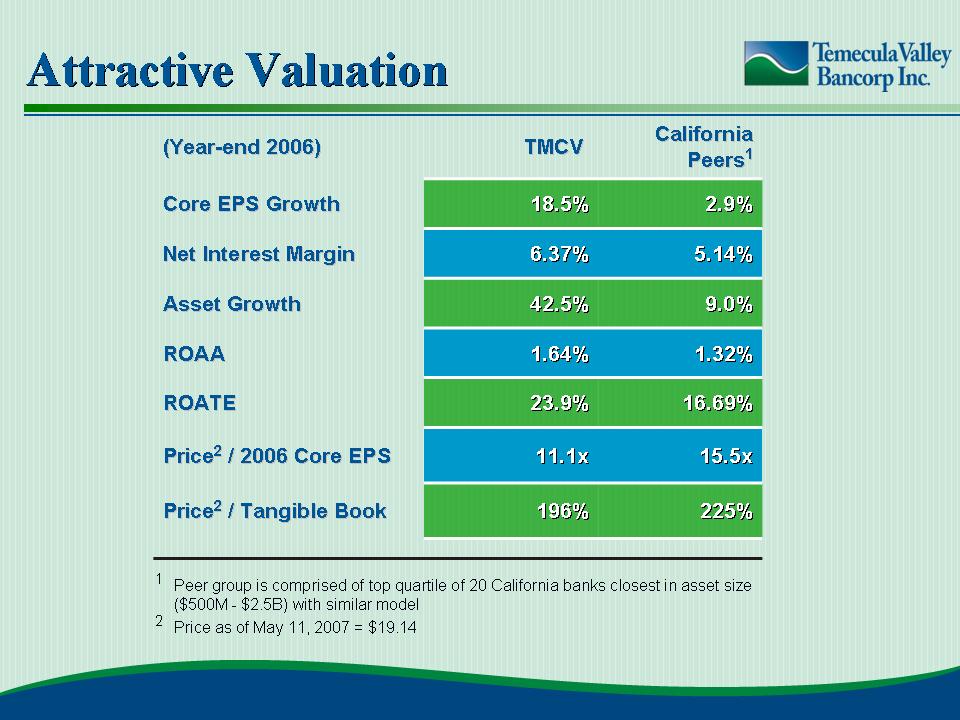

TMCV Investment Highlights TMCV Investment Highlights ???? Attractive, high Attractive, high-growth market for community banking growth market for community banking ???? Market leader in construction and SBA lending Market leader in construction and SBA lending ???? Exceptional combination of profitability and growth Exceptional combination of profitability and growth ???? Exceptional credit quality over extended term Exceptional credit quality over extended term ???? Proven, experienced & nimble management team Proven, experienced & nimble management team ???? Strong long Strong long-term EPS, asset, loan and deposit growth term EPS, asset, loan and deposit growth ???? Attractive valuation Attractive valuation Attractive Valuation Attractive Valuation

1 Peer group is comprised of top quartile of 20 California banks closest in asset size ($500M - $2.5B) with similar model 2 Price as of May 11, 2007 = $19.14 9.0% 9.0% 42.5% 42.5% Asset Growth Asset Growth 5.14% 5.14% 6.37% 6.37% Net Interest Margin Net Interest Margin 225% 225% 196% 196% Price Price2 / Tangible Book / Tangible Book 15.5x 15.5x 11.1x 11.1x Price Price2 / 2006 Core EPS / 2006 Core EPS 2.9% 2.9% 18.5% 18.5% Core EPS Growth Core EPS Growth 16.69% 16.69% 23.9% 23.9% ROATE ROATE 1.32% 1.32% 1.64% 1.64% ROAA ROAA California California Peers Peers1 TMCV TMCV (Year (Year-end 2006) end 2006) TEMECULA VALLEY BANCORP TEMECULA VALLEY BANCORP

TEMECULA VALLEY BANCORP