UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

(Mark One)

x QUARTERLY REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended: December 31, 2009

o TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT

OF 1934

For the transition period from --- to ---

Commission File Number: 001-31810

______________________________________

Cinedigm Digital Cinema Corp.

(Exact Name of Registrant as Specified in its Charter)

______________________________________

| Delaware | 22-3720962 |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

55 Madison Avenue, Suite 300, Morristown New Jersey 07960

(Address of Principal Executive Offices, Zip Code)

(973-290-0080)

(Registrant’s Telephone Number, Including Area Code)

| Indicate by check mark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | Yes x No o |

| | |

| Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). | Yes o No o |

| | |

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one): |

| | |

Large accelerated filer o | Accelerated filer o |

Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company x |

| | |

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | Yes o No x |

| | |

| As of February 5, 2010, 28,032,875 shares of Class A Common Stock, $0.001 par value, and 733,811 shares of Class B Common Stock, $0.001 par value, were outstanding. |

CINEDIGM DIGITAL CINEMA CORP.

CONTENTS TO FORM 10-Q

PART I -- | FINANCIAL INFORMATION | Page |

Item 1. | Financial Statements (Unaudited) | |

| Condensed Consolidated Balance Sheets at March 31, 2009 and December 31, 2009 (Unaudited) | 1 |

| Unaudited Condensed Consolidated Statements of Operations for the Three and Nine Months ended December 31, 2008 and 2009 | 3 |

| Unaudited Condensed Consolidated Statements of Cash Flows for the Nine Months ended December 31, 2008 and 2009 | 4 |

| Notes to Unaudited Condensed Consolidated Financial Statements | 5 |

Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 30 |

Item 4T. | Controls and Procedures | 43 |

PART II -- | OTHER INFORMATION | |

Item 1. | Legal Proceedings | 44 |

Item 1A. | Risk Factors | 44 |

Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 45 |

Item 3. | Defaults Upon Senior Securities | 46 |

Item 4. | Submission of Matters to a Vote of Security Holders | 46 |

Item 5. | Other Information | 46 |

Item 6. | Exhibits | 46 |

Signatures | | 47 |

| Exhibit Index | 48 |

PART I - FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS (UNAUDITED)

CINEDIGM DIGITAL CINEMA CORP.

CONDENSED CONSOLIDATED BALANCE SHEETS

(In thousands, except for share data)

| | | March 31, 2009 | | | December 31, 2009 | |

| ASSETS | | | | | (Unaudited) | |

Current assets | | | | | | |

| Cash and cash equivalents | | $ | 26,329 | | | $ | 12,118 | |

| Restricted available-for-sale investments | | | — | | | | 5,764 | |

| Accounts receivable, net | | | 13,884 | | | | 13,073 | |

| Deferred costs, current portion | | | 3,936 | | | | 3,013 | |

| Unbilled revenue, current portion | | | 3,082 | | | | 5,061 | |

| Prepaid and other current assets | | | 1,798 | | | | 1,856 | |

| Note receivable, current portion | | | 616 | | | | 165 | |

| Total current assets | | | 49,645 | | | | 41,050 | |

Restricted available-for-sale investments | | | — | | | | 3,492 | |

| Restricted cash | | | 255 | | | | 7,164 | |

| Security deposits | | | 424 | | | | 427 | |

| Property and equipment, net | | | 243,124 | | | | 228,037 | |

| Intangible assets, net | | | 10,707 | | | | 8,452 | |

| Capitalized software costs, net | | | 3,653 | | | | 3,803 | |

| Goodwill | | | 8,024 | | | | 8,024 | |

| Deferred costs, net of current portion | | | 3,967 | | | | 7,295 | |

| Unbilled revenue, net of current portion | | | 1,253 | | | | 966 | |

| Note receivable, net of current portion | | | 959 | | | | 843 | |

| Accounts receivable, net of current portion | | | 386 | | | | 386 | |

| Total assets | | $ | 322,397 | | | $ | 309,939 | |

See accompanying notes to Unaudited Condensed Consolidated Financial Statements

CINEDIGM DIGITAL CINEMA CORP.

CONDENSED CONSOLIDATED BALANCE SHEETS

(In thousands, except for share data)

(continued)

| | | March 31, 2009 | | | December 31, 2009 | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | | (Unaudited) | |

Current liabilities | | | | | | |

| Accounts payable and accrued expenses | | $ | 14,954 | | | $ | 7,333 | |

| Current portion of notes payable, non-recourse | | | 24,824 | | | | 25,791 | |

| Current portion of notes payable | | | 424 | | | | 181 | |

| Current portion of capital leases | | | 175 | | | | 499 | |

| Current portion of deferred revenue | | | 5,535 | | | | 4,916 | |

| Current portion of customer security deposits | | | 314 | | | | 104 | |

| Total current liabilities | | | 46,226 | | | | 38,824 | |

| | | | | | | | | |

| Notes payable, non-recourse, net of current portion | | | 170,624 | | | | 153,637 | |

| Notes payable, net of current portion | | | 55,333 | | | | 67,633 | |

| Capital leases, net of current portion | | | 5,832 | | | | 5,721 | |

| Warrant liability | | | — | | | | 13,695 | |

| Interest rate swap | | | 4,529 | | | | 2,453 | |

| Deferred revenue, net of current portion | | | 1,057 | | | | 1,976 | |

| Customer security deposits, net of current portion | | | 9 | | | | 9 | |

| Total liabilities | | | 283,610 | | | | 283,948 | |

Commitments and contingencies (see Note 7) | | | | | | | | |

Stockholders’ Equity | | | | | | | | |

Preferred stock, 15,000,000 shares authorized; Series A 10% - $0.001 par value per share; 20 shares authorized; 8 shares issued and outstanding at March 31, 2009 and December 31, 2009, respectively. Liquidation preference $4,050 | | | 3,476 | | | | 3,556 | |

| Class A common stock, $0.001 par value per share; 65,000,000 and 75,000,000 shares authorized at March 31, 2009 and December 31, 2009, respectively; 27,544,315 and 28,084,315 shares issued and 27,492,875 and 28,032,875 shares outstanding at March 31, 2009 and December 31, 2009, respectively | | | 27 | | | | 28 | |

| Class B common stock, $0.001 par value per share; 15,000,000 shares authorized; 733,811 shares issued and outstanding, at March 31, 2009 and December 31, 2009, respectively | | | 1 | | | | 1 | |

| Additional paid-in capital | | | 173,565 | | | | 175,596 | |

| Treasury stock, at cost; 51,440 Class A shares | | | (172 | ) | | | (172 | ) |

| Accumulated deficit | | | (138,110 | ) | | | (152,958 | ) |

| Accumulated other comprehensive loss | | | — | | | | (60 | ) |

| Total stockholders’ equity | | | 38,787 | | | | 25,991 | |

| Total liabilities and stockholders’ equity | | $ | 322,397 | | | $ | 309,939 | |

See accompanying notes to Unaudited Condensed Consolidated Financial Statements

CINEDIGM DIGITAL CINEMA CORP.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(In thousands, except for share and per share data)

(Unaudited)

| | For the Three Months Ended December 31, | | For the Nine Months Ended December 31, |

| | | | 2008 | | | | 2009 | | | | 2008 | | | | 2009 | |

| Revenues | | $ | 22,710 | | | $ | 21,769 | | | $ | 65,129 | | | $ | 60,316 | |

Costs and Expenses: | | | | | | | | | | | | | | | | |

| Direct operating (exclusive of depreciation and amortization shown below) | | | 7,068 | | | | 6,585 | | | | 19,597 | | | | 18,113 | |

| Selling, general and administrative | | | 4,691 | | | | 4,158 | | | | 13,711 | | | | 12,100 | |

| Provision for doubtful accounts | | | 98 | | | | 144 | | | | 271 | | | | 408 | |

| Research and development | | | 107 | | | | 47 | | | | 207 | | | | 151 | |

| Stock-based compensation | | | 295 | | | | 346 | | | | 653 | | | | 1,112 | |

| Impairment of goodwill | | | 6,525 | | | | — | | | | 6,525 | | | | — | |

| Depreciation and amortization of property and equipment | | | 8,126 | | | | 8,286 | | | | 24,394 | | | | 24,762 | |

| Amortization of intangible assets | | | 821 | | | | 740 | | | | 2,669 | | | | 2,255 | |

| Total operating expenses | | | 27,731 | | | | 20,306 | | | | 68,027 | | | | 58,901 | |

| Income (loss) from operations | | | (5,021 | ) | | | 1,463 | | | | (2,898 | ) | | | 1,415 | |

Interest income | | | 88 | | | | 101 | | | | 311 | | | | 236 | |

| Interest expense | | | (6,935 | ) | | | (9,261 | ) | | | (21,101 | ) | | | (25,602 | ) |

| Extinguishment of debt | | | — | | | | — | | | | — | | | | 10,744 | |

| Other expense, net | | | (162 | ) | | | (153 | ) | | | (488 | ) | | | (454 | ) |

| Change in fair value of interest rate swap | | | (5,411 | ) | | | 853 | | | | (3,846 | ) | | | 2,076 | |

| Change in fair value of warrant liability | | | — | | | | 613 | | | | — | | | | (2,963 | ) |

| Net loss | | $ | (17,441 | ) | | $ | (6,384 | ) | | $ | (28,022 | ) | | $ | (14,548 | ) |

Preferred stock dividends | | | — | | | | (100 | ) | | | — | | | | (300 | ) |

| Net loss attributable to common stockholders | | $ | (17,441 | ) | | $ | (6,484 | ) | | $ | (28,022 | ) | | $ | (14,848 | ) |

Net loss per Class A and Class B common share - basic and diluted | | $ | (0.63 | ) | | $ | (0.23 | ) | | $ | (1.03 | ) | | $ | (0.52 | ) |

| | | | | | | | | | | | | | | | | |

| Weighted average number of Class A and Class B common shares outstanding: | | | | | | | | | | | | | | | | |

| Basic and diluted | | | 27,566,462 | | | | 28,766,686 | | | | 27,324,324 | | | | 28,572,727 | |

See accompanying notes to Unaudited Condensed Consolidated Financial Statements

CINEDIGM DIGITAL CINEMA CORP.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(In thousands) (Unaudited)

| | For the Nine Months Ended December 31, | |

| | | 2008 | | | | 2009 | |

| Cash flows from operating activities | | | | | | | |

| Net loss | $ | (28,022 | ) | | $ | (14,548 | ) |

| Adjustments to reconcile net loss to net cash provided by operating activities: | | | | | | | |

| Loss on disposal of assets | | 164 | | | | 7 | |

| Loss on impairment of goodwill | | 6,525 | | | | — | |

| Depreciation and amortization of property and equipment and amortization of intangible assets | | 27,063 | | | | 27,017 | |

| Amortization of capitalized software costs | | 601 | | | | 486 | |

| Amortization of debt issuance costs included in interest expense | | 1,134 | | | | 1,499 | |

| Provision for doubtful accounts | | 271 | | | | 408 | |

| Stock-based compensation | | 653 | | | | 1,112 | |

| Non-cash interest expense | | 3,937 | | | | 2,398 | |

| Change in fair value of interest rate swap | | 3,846 | | | | (2,076 | ) |

| Change in fair value of warrant liability | | — | | | | 2,963 | |

| Realized loss on available-for-sale investments | | — | | | | 7 | |

| Interest expense added to note payable | | — | | | | 2,333 | |

| Gain on extinguishment of debt | | — | | | | (10,744 | ) |

| Accretion of note payable discount included in interest expense | | — | | | | 837 | |

| Changes in operating assets and liabilities: | | | | | | | |

| Accounts receivable | | 4,823 | | | | 403 | |

| Unbilled revenue | | 1,262 | | | | (1,692 | ) |

| Prepaids and other current assets | | (670 | ) | | | (78 | ) |

| Other assets | | (434 | ) | | | 582 | |

| Accounts payable and accrued expenses | | 472 | | | | (4,493 | ) |

| Deferred revenue | | (23 | ) | | | 265 | |

| Other liabilities | | 13 | | | | (210 | ) |

| Net cash provided by operating activities | | 21,615 | | | | 6,476 | |

| | | | | | | | |

| Cash flows from investing activities | | | | | | | |

| Purchases of property and equipment | | (18,115 | ) | | | (13,045 | ) |

| Purchase of intangible assets | | (550 | ) | | | — | |

| Additions to capitalized software costs | | (825 | ) | | | (637 | ) |

| Sales/maturities of available-for-sale investments | | — | | | | 1,997 | |

| Purchase of available-for-sale investments | | — | | | | (11,265 | ) |

| Restricted cash | | — | | | | (6,909 | ) |

| Net cash used in investing activities | | (19,490 | ) | | | (29,859 | ) |

Cash flows from financing activities | | | | | | | |

| Proceeds from notes payable | | — | | | | 76,513 | |

| Repayment of notes payable | | (1,434 | ) | | | (42,862 | ) |

| Repayment of credit facilities | | (9,676 | ) | | | (26,434 | ) |

| Proceeds from credit facilities | | 569 | | | | 8,884 | |

| Payments of debt issuance costs | | (518 | ) | | | (6,209 | ) |

| Principal payments on capital leases | | (83 | ) | | | (689 | ) |

| Proceeds for subscription of preferred stock | | 2,000 | | | | — | |

| Costs associated with issuance of preferred stock | | (73 | ) | | | (8 | ) |

| Costs associated with issuance of Class A common stock | | — | | | | (23 | ) |

| Net cash (used in) provided by financing activities | | (9,215 | ) | | | 9,172 | |

| Net decrease in cash and cash equivalents | | (7,090 | ) | | | (14,211 | ) |

| Cash and cash equivalents at beginning of period | | 29,655 | | | | 26,329 | |

| Cash and cash equivalents at end of period | $ | 22,565 | | | $ | 12,118 | |

See accompanying notes to Unaudited Condensed Consolidated Financial Statements

CINEDIGM DIGITAL CINEMA CORP.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

December 31, 2009

($ in thousands, except for per share data)

(Unaudited)

Cinedigm Digital Cinema Corp. was incorporated in Delaware on March 31, 2000 (“Cinedigm”, and collectively with its subsidiaries, the “Company”). On September 30, 2009, the Company’s stockholders approved a change in the Company’s name from Access Integrated Technologies, Inc. to Cinedigm Digital Cinema Corp., and such change was effected October 5, 2009. The Company provides technology solutions, financial services and advice, software services, electronic delivery and content distribution services to owners and distributors of digital content to movie theatres and other venues.

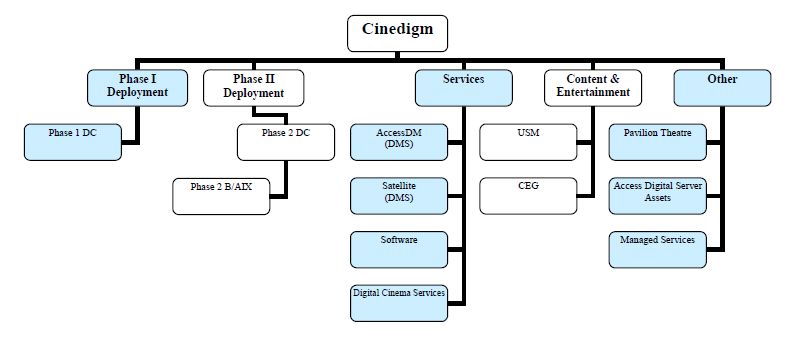

Beginning September 1, 2009, the Company made changes to its organizational structure which impacted its reportable segments, but did not impact its consolidated financial position, results of operations or cash flows. The Company realigned its focus to five primary businesses as follows: the first digital cinema deployment (“Phase I Deployment”), the second digital cinema deployment (“Phase II Deployment”), services (“Services”), media content and entertainment (“Content & Entertainment”) and other (“Other”). The Company’s Phase I Deployment and Phase II Deployment segments are the non-recourse, financing vehicles and administrators for the Company’s digital cinema equipment (the “Systems”) installed in movie theatres nationwide. The Company’s Services segment provides services and support to the Phase I Deployment and Phase II Deployment segments as well as to other third party customers. Included in these services are asset management services for a specified fee via service agreements with Phase I Deployment and Phase II Deployment; software license, maintenance and consulting services; and electronic content delivery services via satellite and hard drive to the motion picture industry. These services primarily facilitate the conversion from analog (film) to digital cinema and have positioned the Company at what it believes to be the forefront of a rapidly developing industry relating to the delivery and management of digital cinema and other content to theatres and other remote venues worldwide. The Company’s Content & Entertainment segment provides content distribution services to alternative and theatrical content owners and to theatrical exhibitors and in-theatre advertising. The Company’s Other segment provides motion picture exhibition to the general public, information technology consulting and managed network monitoring services and hosting services and network access for other web hosting services (“Access Digital Server Assets”). Overall, the Company’s goal is to aid in the transformation of movie theatres to entertainment centers by providing a platform of hardware, software and content choices. Additional information related to the Company’s reporting segments can be found in Note 10.

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

BASIS OF PRESENTATION, USE OF ESTIMATES AND CONSOLIDATION

The Company has incurred net losses historically and has an accumulated deficit of $152,958 as of December 31, 2009. The Company also has significant contractual obligations related to its recourse and non-recourse debt for the remaining part of fiscal year 2010 and beyond. Management expects that the Company will continue to generate net losses for the foreseeable future. Based on the Company’s cash position at December 31, 2009, and expected cash flows from operations, management believes that the Company has the ability to meet its obligations through December 31, 2010. In August 2009, the Company entered into a private placement of a senior secured recourse note and extinguished its existing senior notes, which provided net proceeds after repayment of existing debt, funding of an interest reserve and transactions fees and expenses of approximately $11,300 of working capital funding. The Company has signed commitment letters for additional non-recourse debt capital, primarily to meet equipment requirements related to the Company’s Phase II Deployment, there is no assurance that financing for the Phase II Deployment will be completed as contemplated or under terms acceptable to the Company or its existing stockholders. Failure to generate additional revenues, raise additional capital or manage discretionary spending could have a material adverse effect on the Company’s ability to continue as a going concern. The accompanying unaudited condensed consolidated financial statements do not reflect any adjustments which may result from the Company’s inability to continue as a going concern.

The condensed consolidated balance sheet as of March 31, 2009, which has been derived from audited financial statements, and the condensed consolidated financial statements were prepared following the interim reporting requirements of the Securities and Exchange Commission (“SEC”). They do not include all disclosures normally

made in financial statements contained in the Form 10-K. In management’s opinion, all adjustments necessary for a fair presentation of financial position, the results of operations and cash flows in accordance with accounting principles generally accepted in the United States (GAAP) for the periods presented have been made. The results of operations for the respective interim periods are not necessarily indicative of the results to be expected for the full year. The accompanying condensed consolidated financial statements should be read in conjunction with the financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the fiscal year ended March 31, 2009 filed with the SEC on June 15, 2009 (the “Form 10-K”).

The Company’s condensed consolidated financial statements include the accounts of Cinedigm, Access Digital Media, Inc. (“AccessDM”), Hollywood Software, Inc. d/b/a AccessIT Software (“Software”), Core Technology Services, Inc. (“Managed Services”), FiberSat Global Services, Inc. d/b/a AccessIT Satellite and Support Services (“Satellite”), ADM Cinema Corporation (“ADM Cinema”) d/b/a the Pavilion Theatre (the “Pavilion Theatre”), Christie/AIX, Inc. d/b/a AccessIT Digital Cinema (“Phase 1 DC”), PLX Acquisition Corp., UniqueScreen Media, Inc. (“USM”), Vistachiara Productions, Inc. f/k/a The Bigger Picture, currently d/b/a Cinedigm Content and Entertainment Group (“CEG”), Access Digital Cinema Phase 2 Corp. (“Phase 2 DC”) and Access Digital Cinema Phase 2 B/AIX Corp. (“Phase 2 B/AIX”). AccessDM and Satellite are together referred to as the Digital Media Services Division (“DMS”). All intercompany transactions and balances have been eliminated.

The preparation of the consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the amounts reported in the condensed consolidated financial statements and accompanying notes. On an on-going basis, the Company evaluates its estimates, including those related to the carrying values of its long-lived assets, intangible assets and goodwill, the valuation of deferred tax assets, the valuation of assets acquired and liabilities assumed in purchase business combinations, stock-based compensation expense, revenue recognition and capitalization of software development costs. The Company bases its estimates on historical experience and on other assumptions that the Company believes to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Because of the uncertainty inherent in such estimates, actual results could differ materially from these estimates under different assumptions or conditions.

The March 31, 2009 consolidated balance sheets were reclassified to break out the recourse and non-recourse notes payable to conform to the current period presentation.

REVENUE RECOGNITION

Phase I Deployment and Phase II Deployment

Virtual print fees (“VPFs”) are earned pursuant to contracts with movie studios and distributors, whereby amounts are payable to Phase 1 DC and to Phase 2 DC, when movies distributed by the studio are displayed on screens utilizing the Company’s digital cinema equipment (the “Systems”) installed in movie theatres. VPFs are earned and payable to Phase 1 DC based on a defined fee schedule with a reduced VPF rate year over year until the sixth year (calendar 2011) at which point the VPF rate remains unchanged through the tenth year. One VPF is payable for every movie title displayed per System. The amount of VPF revenue is therefore dependent on the number of movie titles released and displayed on the Systems in any given accounting period. VPF revenue is recognized in the period in which the movie first opens for general audience viewing in that digitally-equipped movie theatre, as Phase 1 DC’s and Phase 2 DC’s performance obligations have been substantially met at that time.

Phase 2 DC’s agreements with distributors require the payment of VPFs, according to a defined fee schedule, for ten years from the date each system is installed; however, Phase 2 DC may no longer collect VPFs once “cost recoupment,” as defined in the agreements, is achieved. Cost recoupment will occur once the cumulative VPFs and other cash receipts collected by Phase 2 DC have equaled the total of all cash outflows, including the purchase price of all Systems, all financing costs, all “overhead and ongoing costs”, as defined, and including the Company’s service fees, subject to maximum agreed upon amounts during the three-year rollout period and thereafter, plus a compounded return on any billed but unpaid overhead and ongoing costs, of 15% per year. Further, if cost recoupment occurs before the end of the eighth contract year, a one-time “cost recoupment bonus” is payable by the studios to the Company. Any other cash flows, net of expenses, received by Phase 2 DC following the achievement of cost recoupment are required to be returned to the distributors on a pro-rata basis. At this time, the Company cannot estimate the timing or probability of the achievement of cost recoupment.

Alternative content fees (“ACFs”) are earned pursuant to contracts with movie exhibitors, whereby amounts are payable to Phase 1 DC and to Phase 2 DC, generally as a percentage of the applicable box office revenue derived from the exhibitor’s showing of content other than feature films, such as concerts and sporting events (typically referred to as “alternative content”). ACF revenue is recognized in the period in which the alternative content opens for audience viewing.

Services

For software multi-element licensing arrangements that do not require significant production, modification or customization of the licensed software, revenue is recognized for the various elements as follows: revenue for the licensed software element is recognized upon delivery and acceptance of the licensed software product, as that represents the culmination of the earnings process and the Company has no further obligations to the customer, relative to the software license. Revenue earned from consulting services is recognized upon the performance and completion of these services. Revenue earned from annual software maintenance is recognized ratably over the maintenance term (typically one year).

Revenue is deferred in cases where: (1) a portion or the entire contract amount cannot be recognized as revenue, due to non-delivery or pre-acceptance of licensed software or custom programming, (2) uncompleted implementation of application service provider arrangements (“ASP Service”), or (3) unexpired pro-rata periods of maintenance, minimum ASP Service fees or website subscription fees. As license fees, maintenance fees, minimum ASP Service fees and website subscription fees are often paid in advance, a portion of this revenue is deferred until the contract ends. Such amounts are classified as deferred revenue and are recognized as earned revenue in accordance with the Company’s revenue recognition policies described above.

Revenues from the delivery of data via satellite and hard drive are recognized upon delivery, as DMS’ performance obligations have been substantially met at that time.

Content & Entertainment

USM has contracts with exhibitors to display pre-show advertisements on their screens, in exchange for certain fees paid to the exhibitors. USM then contracts with businesses of various types to place their advertisements in select theatre locations, designs the advertisement, and places it on-screen for specific periods of time, generally ranging from three to twelve months. Cinema advertising service revenue, and the associated direct selling, production and support cost, is recognized on a straight-line basis over the period the related in-theatre advertising is displayed, pursuant to the specific terms of each advertising contract. USM has the right to receive or bill the entire amount of the advertising contract upon execution, and therefore such amount is recorded as a receivable at the time of execution, and all related advertising revenue and all direct costs actually incurred are deferred until such time as the in-theatre advertising is displayed.

The right to sell and display such advertising, or other in-theatre programs, products and services, is based upon advertising contracts with exhibitors which stipulate payment terms to such exhibitors for this right. Payment terms generally consist of fixed annual payments or annual minimum guarantee payments, plus a revenue share of the excess of a percentage of advertising revenue over the minimum guarantee, if any. The Company recognizes the cost of fixed and minimum guarantee payments on a straight-line basis over each advertising contract year, and the revenue share cost, if any, in accordance with the terms of the advertising contract.

Barter advertising revenue is recognized for the fair value of the advertising time surrendered in exchange for alternative content. The Company includes the value of such exchanges in both Content & Entertainment’s net revenues and direct operating expenses. There may be a timing difference between the screening of alternative content and the screening of the underlying advertising used to acquire the content. The acquisition cost is being recorded and recognized as a direct operating expense by CEG when the alternative content is screened, and the underlying advertising is being deferred and recognized as revenue ratably over the period such advertising is screened by USM. For the three months ended December 31, 2008 and 2009, the Company recorded net revenues and direct operating expenses related to barter advertising of $1,152 and $583, respectively, and $1,152 and $1,124, for the nine months ended December 31, 2008 and 2009, respectively.

CEG has contracts for the theatrical distribution of third party feature films and alternative content. CEG’s distribution fee revenue is recognized at the time a feature film and alternative content is viewed, based on CEG’s participation in box office receipts. CEG has the right to receive or bill a portion of the theatrical distribution fee in

advance of the exhibition date, and therefore such amount is recorded as a receivable at the time of execution, and all related distribution revenue is deferred until the third party feature films’ or alternative content’s theatrical release date.

Other

Movie theatre admission and concession revenues are generated at the Company’s nine-screen digital movie theatre, the Pavilion Theatre. Movie theatre admission revenues are recognized on the date of sale, as the related movie is viewed on that date and the Company’s performance obligation is met at that time. Concession revenues consist of food and beverage sales and are also recognized on the date of sale.

Managed Services’ revenues, which consist of monthly recurring billings pursuant to network monitoring and maintenance contracts, are recognized as revenues in the period the services are provided, and other non-recurring billings are recognized on a time and materials basis as revenues in the period in which the services were provided.

Other revenues, attributable to the Access Digital Server Assets, which consist of monthly recurring billings for hosting and network access fees, are recognized as revenues in the period the services are provided.

Since May 1, 2007, the Company’s three internet data centers (“IDCs”) have been operated by FiberMedia AIT, LLC and Telesource Group, Inc. (together, “FiberMedia”), unrelated third parties, pursuant to a master collocation agreement. Although the Company is still the lessee of the IDCs, substantially all of the revenues and expenses were being realized by FiberMedia and not the Company and since May 1, 2008, 100% of the revenues and expenses are being realized by FiberMedia. In June 2009, one of the IDC leases expired, leaving two IDC leases with the Company as lessee.

RESTRICTED AVAILABLE-FOR-SALE INVESTMENTS

In connection with the $75,000 Senior Secured Note issued in August 2009 (see Note 5), the Company was required to segregate $11,265 of the proceeds into marketable securities which will be used to pay interest over the next two years. The Company classifies the marketable securities as available-for-sale investments and accordingly, these investments are recorded at fair value. The maturity dates of these investments coincide with the quarterly interest payment dates through September 2011. The changes in the value of these investments are recorded in other comprehensive loss in the condensed consolidated financial statements. Realized gains and losses are recorded in earnings when securities mature or are redeemed. During the three and nine months ended December 31, 2009, there were realized losses of $5 and $7, respectively.

The Company held no available-for-sale securities at March 31, 2009. During the three and nine months ended December 31, 2009, the Company has made scheduled quarterly interest payments of $1,327 and $2,041, respectively. Investment securities of $5,764 with a maturity of twelve months or less are classified as short-term and investment securities of $3,492 with a maturity greater than twelve months are classified as long-term. The carrying value and fair value of investment securities available-for-sale at December 31, 2009 were as follows:

| | | Amortized Cost | | | Gross Unrealized Gains | | | Gross Unrealized Losses | | | Fair Value | |

| U.S. Treasury securities | | $ | 3,655 | | | $ | 1 | | | $ | (31 | ) | | $ | 3,625 | |

| Obligations of U.S. government agencies and FDIC guaranteed bank debt | | | 4,651 | | | | — | | | | (28 | ) | | | 4,623 | |

| Corporate debt securities | | | 505 | | | | — | | | | — | | | | 505 | |

| Other interest bearing securities | | | 505 | | | | — | | | | (2 | ) | | | 503 | |

| | | $ | 9,316 | | | $ | 1 | | | $ | (61 | ) | | $ | 9,256 | |

DEFERRED COSTS

Deferred costs primarily consist of the unamortized debt issuance costs related to the credit facility with General Electric Capital Corporation (“GECC”), the $55,000 of 10% Senior Notes issued in August 2007 up to August 2009 (see Note 5) and the $75,000 Senior Secured Note issued in August 2009 (see Note 5), which are amortized on a straight-line basis over the term of the respective debt (see Note 5 for extinguishment of debt). The straight-line basis is not materially different from the effective interest method. As of December 31, 2009 and included in deferred costs are advertising production, post production and technical support costs related to developing and displaying advertising in the amount of $768, which are capitalized and amortized on a straight-line basis over the same period as the related cinema advertising revenues of $4,517 are recognized.

DIRECT OPERATING COSTS

Direct operating costs consist of facility operating costs such as rent, utilities, real estate taxes, repairs and maintenance, insurance and other related expenses, direct personnel costs, film rent expense, amortization of capitalized software development costs, exhibitors payments for displaying cinema advertising and other deferred expenses, such as advertising production, post production and technical support related to developing and displaying advertising.

STOCK-BASED COMPENSATION

For the three months ended December 31, 2008 and 2009, the Company recorded stock-based compensation expense of $295 and $346, respectively, and $653 and $1,112 for the nine months ended December 31, 2008 and 2009, respectively. The Company estimates that the stock-based compensation expense related to current outstanding stock options, using a Black-Scholes option valuation model, and current outstanding restricted stock awards will be approximately $1,485 in fiscal 2010.

The weighted-average grant-date fair value of options granted during the three months ended December 31, 2008 and 2009 was $0.55 and $0.80, respectively, and $0.58 and $0.71, for the nine months ended December 31, 2008 and 2009, respectively. There were no stock options exercised during the three and nine months ended December 31, 2008 and 2009.

The Company estimated the fair value of stock options at the date of each grant using a Black-Scholes option valuation model with the following assumptions:

| | | For the Three Months Ended December 31, | | | For the Nine Months Ended December 31, | |

| | | 2008 | | | 2009 | | | 2008 | | | 2009 | |

| Range of risk-free interest rates | | | 2.5-5.2 | % | | | 2.4 | % | | | 2.5-5.2 | % | | | 2.4-2.7 | % |

| Dividend yield | | | — | | | | — | | | | — | | | | — | |

| Expected life (years) | | | 5 | | | | 5 | | | | 5 | | | | 5 | |

| Range of expected volatilities | | | 52.5-58.7 | % | | | 77.6 | % | | | 52.5-58.7 | % | | | 77.4-77.6 | % |

The risk-free interest rate used in the Black-Scholes option valuation model for options granted under the Company’s stock option plan awards is the historical yield on U.S. Treasury securities with equivalent remaining lives. The Company does not currently anticipate paying any cash dividends on common stock in the foreseeable future. Consequently, an expected dividend yield of zero is used in the Black-Scholes option valuation model. The Company estimates the expected life of options granted under the Company’s stock option plans using both exercise behavior and post-vesting termination behavior, as well as consideration of outstanding options. The Company estimates expected volatility for options granted under the Company’s stock option plans based on a measure of historical volatility in the trading market for the Company’s common stock.

CAPITALIZED SOFTWARE COSTS

Internal Use Software

The Company accounts for internal use software development costs based on three distinct stages to the software development process for internal use software. The first stage, the preliminary project stage, includes the conceptual

formulation, design and testing of alternatives. The second stage, or the program instruction phase, includes the development of the detailed functional specifications, coding and testing. The final stage, the implementation stage, includes the activities associated with placing a software project into service. All activities included within the preliminary project stage are considered research and development and expensed as incurred. During the program instruction phase, all costs incurred until the software is substantially complete and ready for use, including all necessary testing, are capitalized, Capitalized costs are amortized on a straight-line basis over estimated lives ranging from three to five years, beginning when the software is ready for its intended use.

Software to be Sold, Licensed or Otherwise Marketed

Software development costs that are incurred subsequent to establishing technological feasibility are capitalized until the product is available for general release. Amounts capitalized as software development costs are amortized using the greater of revenues during the period compared to the total estimated revenues to be earned or on a straight-line basis over estimated lives ranging from three to five years. The Company reviews capitalized software costs for impairment on a periodic basis with other long-lived assets. Amortization of capitalized software development costs, included in direct operating costs, for the three months ended December 31, 2008 and 2009 amounted to $214 and $163, respectively and $601 and $486 for the nine months ended December 31, 2008 and 2009, respectively. At December 31, 2009, there were no unbilled receivables under such customized software development contracts included in unbilled revenue in the condensed consolidated balance sheets.

GOODWILL AND INTANGIBLE ASSETS

Goodwill is the excess of the purchase price paid over the fair value of the net assets of the acquired business. The Company assesses its goodwill for impairment at least annually, and in interim periods if certain triggering events occur indicating that the carrying value of goodwill may be impaired. The Company also reviews possible impairment of finite lived intangible assets annually. The Company recorded an impairment charge of $6,525 in the quarter ended December 31, 2008 related to the Company’s Content and Entertainment segment and the Pavilion Theatre, in the Other segment, based on the results of an impairment evaluation since the Company had concluded that one or more triggering events had occurred during the three months ended December 31, 2008.

As of December 31, 2009, the Company’s finite-lived intangible assets consisted of customer relationships and agreements, theatre relationships, covenants not to compete, trade names and trademarks and Federal Communications Commission licenses (for satellite transmission services), which are estimated to have useful lives ranging from two to ten years. No intangible assets were acquired during the three and nine months ended December 31, 2009. During the nine months ended December 31, 2009, no impairment charge was recorded.

| Balance at March 31, 2008 | | $ | 14,549 | |

| Goodwill impairment – USM | | | (4,401 | ) |

| Goodwill impairment – The Pavilion Theatre | | | (1,960 | ) |

| Goodwill impairment – CEG | | | (164 | ) |

| Balance at December 31, 2009 | | $ | 8,024 | |

PROPERTY AND EQUIPMENT

Property and equipment are stated at cost, less accumulated depreciation and amortization. Depreciation expense is recorded using the straight-line method over the estimated useful lives of the respective assets. Leasehold improvements are being amortized over the shorter of the lease term or the estimated useful life of the improvement. Maintenance and repair costs are charged to expense as incurred. Major renewals, improvements and additions are capitalized. Upon the sale or other disposition of any property and equipment, the cost and related accumulated depreciation and amortization are removed from the accounts and the gain or loss is included in the condensed consolidated statement of operations.

IMPAIRMENT OF LONG-LIVED ASSETS

The Company reviews the recoverability of its long-lived assets when events or conditions exist that indicate a possible impairment exists. The assessment for recoverability is based primarily on the Company’s ability to recover the carrying value of its long-lived assets from expected future undiscounted net cash flows. If the total of expected future undiscounted net cash flows is less than the total carrying value of the assets the asset is deemed not to be

recoverable and possibly impaired. The Company then estimates the fair value of the asset to determine whether an impairment loss should be recognized. An impairment loss will be recognized if for the difference between the fair value (computed based upon) and the carrying value of the asset exceeds its fair value. Fair value is estimated by computing the expected future discounted cash flows. During the nine months ended December 31, 2008 and 2009, no impairment charge for long-lived assets was recorded.

NET LOSS PER COMMON SHARE

Basic and diluted net loss per common share has been calculated as follows:

| Basic and diluted net loss per common share = | Net loss – preferred dividends |

| | Weighted average number of Common Stock outstanding during the period |

Shares issued and any shares that are reacquired during the period are weighted for the portion of the period that they are outstanding.

The Company incurred net losses for each of the three and nine months ended December 31, 2008 and 2009 and, therefore, the impact of dilutive potential common shares from outstanding stock options, warrants, restricted stock, and restricted stock units, totaling 4,335,382 shares and 24,407,770 shares as of December 31, 2008 and 2009, respectively, were excluded from the computation as it would be anti-dilutive.

ACCOUNTING FOR DERIVATIVE ACTIVITIES

In April 2008, the Company executed an interest rate swap agreement (the “Interest Rate Swap”) (see Note 5) to limit the Company’s exposure to changes in interest rates. Changes in fair value of derivative financial instruments are either recognized in other comprehensive income (a component of stockholders' equity) or in the condensed consolidated statement of operations depending on whether the derivative is being used to hedge changes in cash flows or fair value. The Company has determined that this is not a hedging transaction and changes in the value of its Interest Rate Swap were recorded in the condensed consolidated statements of operations (see Note 5).

FAIR VALUE OF FINANCIAL INSTRUMENTS

The fair value measurement disclosures are grouped into three levels based on valuation factors:

| · | Level 1 – quoted prices in active markets for identical investments |

| · | Level 2 – other significant observable inputs (including quoted prices for similar investments, market corroborated inputs, etc.) |

| · | Level 3 – significant unobservable inputs (including the Company’s own assumptions in determining the fair value of investments) |

Assets and liabilities measured at fair value on a recurring basis use the market approach, where prices and other relevant information are generated by market transactions involving identical or comparable assets or liabilities.

The following table summarizes the levels of fair value measurements of the Company’s financial assets:

| | | Financial Assets at Fair Value as of December 31, 2009 | |

| | | Level 1 | | | Level 2 | | | Level 3 | |

| Cash and cash equivalents | | $ | 12,118 | | | $ | — | | | $ | — | |

| Investment securities, available-for-sale | | $ | 97 | | | $ | 9,159 | | | $ | — | |

| Restricted cash | | $ | 7,164 | | | $ | — | | | $ | — | |

| Interest rate swap | | $ | — | | | $ | (2,453 | ) | | $ | — | |

| 3. | RECENT ACCOUNTING PRONOUNCEMENTS |

Effective July 1, 2009, the Financial Accounting Standards Board’s (“FASB”) Accounting Standards Codification (“ASC”) became the single official source of authoritative, nongovernmental generally accepted accounting principles (“GAAP”) in the United States. The historical GAAP hierarchy was eliminated and the ASC became the only level of authoritative GAAP, other than guidance issued by the SEC. Our accounting policies were not affected by the conversion to ASC. However, references to specific accounting standards in the footnotes to our condensed consolidated financial statements have been changed to refer to the appropriate section of ASC.

In October 2009, the FASB issued Accounting Standards Update (“ASU”) No. 2009-13, “Revenue Recognition (Topic 605): Multiple-Deliverable Revenue Arrangements (a consensus of the FASB Emerging Issues Task Force)” (“ASU 2009-13”), which amends ASC 605-25, “Revenue Recognition: Multiple-Element Arrangements.” ASU 2009-13 addresses how to determine whether an arrangement involving multiple deliverables contains more than one unit of accounting and how to allocate consideration to each unit of accounting in the arrangement. ASU 2009-13 replaces all references to fair value as the measurement criteria with the term selling price and establishes a hierarchy for determining the selling price of a deliverable. ASU 2009-13 also eliminates the use of the residual value method for determining the allocation of arrangement consideration. Additionally, ASU 2009-13 requires expanded disclosures. ASU 2009-13 will become effective for the Company for revenue arrangements entered into or materially modified on or after April 1, 2011. Earlier application is permitted with required transition disclosures based on the period of adoption. The Company does not believe that ASU 2009-13 will have a material impact on the Company’s consolidated financial statements.

In October 2009, the FASB issued ASU No. 2009-14, “Software (Topic 985): Certain Revenue Arrangements That Include Software Elements (a consensus of the FASB Emerging Issues Task Force)” (“ASU 2009-14”). ASU 2009-14 amends ASC 985-605, “Software: Revenue Recognition,” such that tangible products, containing both software and non-software components that function together to deliver the tangible product’s essential functionality, are no longer within the scope of ASC 985-605. It also amends the determination of how arrangement consideration should be allocated to deliverables in a multiple-deliverable revenue arrangement. ASU 2009-14 will become effective for the Company for revenue arrangements entered into or materially modified on or after April 1, 2011. Earlier application is permitted with required transition disclosures based on the period of adoption. The Company does not believe that ASU 2009-14 will have a material impact on the Company’s consolidated financial statements.

In June 2009, the FASB issued SFAS No. 167 “Amendments to FASB Interpretation No. 46(R)” (“SFAS 167”) (which will be codified in ASC 810-10). Revisions to ASC 810-10 improves financial reporting by enterprises involved with variable interest entities and to address (1) the effects on certain provisions of FASB Interpretation No. 46 (revised December 2003), “Consolidation of Variable Interest Entities”, as a result of the elimination of the qualifying special-purpose entity concept in SFAS 166 and (2) constituent concerns about the application of certain key provisions of Interpretation 46(R), including those in which the accounting and disclosures under the Interpretation do not always provide timely and useful information about an enterprise’s involvement in a variable interest entity. Revisions to ASC 810-10 is effective as of the beginning of each reporting entity’s first annual reporting period that begins after November 15, 2009, for interim periods within that first annual reporting period, and for interim and annual reporting periods thereafter. The Company is currently evaluating the impact of adoption and application of revisions to ASC 810-10 will have on the Company’s consolidated financial statements.

In January 2010, the FASB issued ASU No. 2010-06, “Improving Disclosures about Fair Value Measurements” (“ASU 2010-06”). ASU 2010-06 requires some new disclosures and clarifies some existing disclosure requirements about fair value measurements codified within ASC 820, “Fair Value Measurements and Disclosures.” ASU 2010-06 is effective for interim and annual reporting periods beginning after December 15, 2009. Early application of the provisions of this update is permitted. The Company is currently evaluating the impact the adoption of ASU 2010-06 will have on the Company’s consolidated financial statements disclosures.

Notes receivable consisted of the following:

| | | As of March 31, 2009 | | | As of December 31, 2009 | |

| Note Receivable (as defined below) | | Current Portion | | | Long Term Portion | | | Current Portion | | | Long Term Portion | |

| Exhibitor Note | | $ | 54 | | | $ | 37 | | | $ | 51 | | | $ | — | |

| Exhibitor Install Notes | | | 118 | | | | 908 | | | | 90 | | | | 840 | |

| FiberMedia Note | | | 431 | | | | — | | | | — | | | | — | |

| Other | | | 13 | | | | 14 | | | | 24 | | | | 3 | |

| | | $ | 616 | | | $ | 959 | | | $ | 165 | | | $ | 843 | |

In March 2006, in connection with Phase 1 DC’s deployment, the Company issued to a certain motion picture exhibitor a 7.5% note receivable for $231 (the “Exhibitor Note”), in return for the Company’s payment for certain financed digital projectors. The Exhibitor Note requires monthly principal and interest payments through September 2010. As of December 31, 2009, the outstanding balance of the Exhibitor Note was $51.

In connection with Phase 1 DC’s deployment, the Company agreed to provide financing to certain motion picture exhibitors upon the billing to the motion picture exhibitors by Christie Digital Systems USA, Inc. (“Christie”) for the installation costs associated with the placement of Systems in movie theatres. In April 2006, certain motion picture exhibitors agreed to issue to the Company two 8% notes receivable for an aggregate of $1,287 (the “Exhibitor Install Notes”). Under the Exhibitor Install Notes, the motion picture exhibitors are required to make monthly interest only payments through October 2007 and quarterly principal and interest payments thereafter through August 2009 and August 2017, respectively. As of December 31, 2009, the aggregate outstanding balance of the Exhibitor Install Notes was $930.

In November 2008, FiberMedia issued to the Company a 10% note receivable for $631 (the “FiberMedia Note”) related to certain expenses FiberMedia is required to repay to the Company under a master collocation agreement of the IDCs. FiberMedia was required to make monthly principal and interest payments beginning in January 2009 through July 2009. As of December 31, 2009, the FiberMedia Note was repaid in full.

The Company has not experienced a default by any party to any of their obligations in connection with any of the above notes.

Notes payable consisted of the following:

| | | As of March 31, 2009 | | | As of December 31, 2009 | |

| Note Payable (as defined below) | | Current Portion | | | Long Term Portion | | | Current Portion | | | Long Term Portion | |

| First USM Note | | $ | 221 | | | $ | — | | | $ | — | | | $ | — | |

| SilverScreen Note | | | 20 | | | | — | | | | — | | | | — | |

| 2007 Senior Notes | | | — | | | | 55,000 | | | | — | | | | — | |

| NEC Facility | | | 168 | | | | 333 | | | | 181 | | | | 195 | |

| 2009 Note, net of debt discount | | | — | | | | — | | | | — | | | | 67,438 | |

| Other | | | 15 | | | | — | | | | — | | | | — | |

| Total recourse notes payable | | $ | 424 | | | $ | 55,333 | | | $ | 181 | | | $ | 67,633 | |

| | | | | | | | | | | | | | | | | |

| Vendor Note | | $ | — | | | $ | 9,600 | | | $ | — | | | $ | 9,600 | |

| GE Credit Facility | | | 24,824 | | | | 161,024 | | | | 24,444 | | | | 135,094 | |

| KBC Related Facility | | | — | | | | — | | | | 1,269 | | | | 7,616 | |

| P2 Vendor Note | | | — | | | | — | | | | 49 | | | | 741 | |

| P2 Exhibitor Notes | | | — | | | | — | | | | 29 | | | | 586 | |

| Total non-recourse notes payable | | $ | 24,824 | | | $ | 170,624 | | | $ | 25,791 | | | $ | 153,637 | |

| Total notes payable | | $ | 25,248 | | | $ | 225,957 | | | $ | 25,972 | | | $ | 221,270 | |

Non-recourse debt is generally defined as debt whereby the lenders’ sole recourse with respect to defaults by the Company is limited to the value of the asset collateralized by the debt. The Vendor Note and the GE Credit Facility are not guaranteed by the Company or its other subsidiaries, other than Phase 1 DC. The KBC Related Facility, the

P2 Vendor Note and the P2 Exhibitor Notes are not guaranteed by the Company or its other subsidiaries, other than Phase 2 DC.

As part of the consideration for the purchase price of USM in 2006, the Company issued an 8% note payable in the principal amount of $1,204 (the “USM Note”) The First USM Note was payable in twelve equal quarterly installments commencing on October 1, 2006 until July 1, 2009. During the nine months ended December 31, 2008 and 2009, the Company repaid principal of $414 and $221, respectively, on the First USM Note. As of December 31, 2009, the First USM Note was repaid in full.

Prior to the Company’s acquisition of USM, USM had purchased substantially all the assets of SilverScreen Advertising Incorporated (“SilverScreen”) and issued a 3-year, 4% note payable in the principal amount of $333 (the “SilverScreen Note”) as part of the purchase price for SilverScreen. The SilverScreen Note was payable in equal monthly installments until May 2009. During the nine months ended December 31, 2008 and 2009, the Company repaid principal of $86 and $20, respectively, on the SilverScreen Note. As of December 31, 2009, the SilverScreen Note was repaid in full.

In August 2007, the Company entered into a securities purchase agreement (the “Purchase Agreement”) with the purchasers party thereto (the “Purchasers”) pursuant to which the Company issued 10% Senior Notes (the “2007 Senior Notes”) in the aggregate principal amount of $55,000 (the “August 2007 Private Placement”). The term of the 2007 Senior Notes was three years which may be extended for one 6 month period at the discretion of the Company if certain conditions were met. Interest on the 2007 Senior Notes was payable on a quarterly basis in cash or, at the Company’s option and subject to certain conditions, in shares of its Class A Common Stock (“Interest Shares”). In addition, each quarter, the Company issued shares of Class A Common Stock to the Purchasers as payment of additional interest owed under the 2007 Senior Notes based on a formula (“Additional Interest”). The Company may prepay the 2007 Senior Notes in whole or in part following the first anniversary of issuance of the 2007 Senior Notes, subject to a penalty of 2% of the principal if the 2007 Senior Notes are prepaid prior to the two year anniversary of the issuance and a penalty of 1% of the principal if the 2007 Senior Notes are prepaid thereafter, and subject to paying the number of shares as Additional Interest that would be due through the end of the term of the 2007 Senior Notes. The Company and its subsidiaries, other than Phase 1 DC and its subsidiaries, were prohibited from paying dividends under the terms of the 2007 Senior Notes. Interest expense on the 2007 Senior Notes for the three months ended December 31, 2008 and 2009 amounted to $1,375 and $0, respectively and $4,092 and $1,996 for the nine months ended December 31, 2008 and 2009, respectively. In August 2009, in connection with the consummation of the 2009 Private Placement (as defined below), the Company consummated purchase agreements (the “Note Purchase Agreements”) with the holders of all of its outstanding 2007 Senior Notes pursuant to which the Company purchased all of the 2007 Senior Notes, in satisfaction of the principal and any accrued and unpaid interest thereon, for an aggregate purchase price of $42,500 in cash. The source of such aggregate cash payment was the proceeds of the 2009 Private Placement discussed below. Upon such purchase, the 2007 Senior Notes were canceled and the remaining principal of $12,500 along with unamortized debt issuance costs of $(2,377) and accrued interest of $621 resulted in a $10,744 gain on extinguishment of debt included in the condensed consolidated statements of operations.

In August 2009, the Company entered into a securities purchase agreement (the “Purchase Agreement”) with an affiliate of Sageview Capital LP (the “Purchaser”) pursuant to which the Company agreed to issue a Senior Secured Note (the “2009 Note”) in the aggregate principal amount of $75,000 and warrants (the “Sageview Warrants”) to purchase 16,000,000 shares of its Class A Common Stock (the “2009 Private Placement”). The remaining proceeds of the 2009 Private Placement after the repayment of existing indebtedness of the Company and one of its subsidiaries, the funding of a cash reserve to pay the cash interest amount required under the 2009 Note for the first two years, the payment of fees and expenses incurred in connection with the 2009 Private Placement and related transactions, and other general corporate purposes was approximately $11,300. The 2009 Note has a term of five years, which may be extended for up to one 12 month period at the discretion of the Company if certain conditions are satisfied. Subject to certain adjustments set forth in the 2009 Note, interest on the 2009 Note is 8% per annum to be accrued as an increase in the aggregate principal amount of the 2009 Note (“PIK Interest”) and 7% per annum paid in cash. The Company may prepay the 2009 Note (i) during the initial 18 months of their term, in an amount up to 20% of the original principal amount of the 2009 Note plus accrued and unpaid interest without penalty and (ii) following the second anniversary of issuance of the 2009 Note, subject to a prepayment penalty equal to 7.5% of the principal amount prepaid if the 2009 Note is prepaid prior to the three-year anniversary of its issuance, a prepayment penalty of 3.75% of the principal amount prepaid if the 2009 Note is prepaid after such third anniversary but prior to the fourth anniversary of its issuance and without penalty if the 2009 Note is prepaid thereafter, plus cash in an amount equal to the accrued and unpaid interest amount with respect to the principal

amount through and including the prepayment date. The Company is obligated to offer to redeem all or a portion of the 2009 Note upon the occurrence of certain triggering events described in the 2009 Note. Subject to limited exceptions, the Purchaser may not assign the 2009 Note until the earliest of (a) August 11, 2011, (b) the consummation of a change in control as defined in the 2009 Note or (c) an event of default as defined under the 2009 Note. The Purchase Agreement also requires the 2009 Note to be guaranteed by each of the Company’s existing and future subsidiaries, other than AccessDM, Phase 1 DC and its subsidiaries and Phase 2 DC and its subsidiaries and subsidiaries formed after August 11, 2009 which are primarily engaged in the financing or deployment of digital cinema equipment (the "Guarantors"), and that the Company and each Guarantor pledge substantially all of their assets to secure payment on the 2009 Note, except that AccessDM and Phase 1 DC are not required to become Guarantors until such time as certain indebtedness is repaid. Accordingly, the Company and each of the Guarantors entered into a guarantee and collateral agreement (the “Guarantee and Collateral Agreement”) pursuant to which each Guarantor guaranteed the obligations of the Company under the 2009 Note and the Company and each Guarantor pledged substantially all of their assets to secure such obligations. The Company agreed to register the resale of the shares of Class A Common Stock underlying the Sageview Warrants (the “Registration Rights Agreement”). The Purchase Agreement, Note Purchase Agreement, 2009 Note, Warrants, Registration Rights Agreement and Guarantee and Collateral Agreement contain representations, warranties, covenants and events of default as are customary for transactions of this type and nature.

The 2009 Note is shown net of the discount associated with the issuance of the Sageview Warrants (see Note 6) and the PIK Interest. As of December 31, 2009, the net balance of the 2009 Note was as follows:

| | | As of March 31, 2009 | | | As of December 31, 2009 | |

| 2009 Note, at issuance | | $ | — | | | $ | 75,000 | |

| Discount on 2009 Note | | | — | | | | (9,895 | ) |

| PIK Interest | | | — | | | | 2,333 | |

| 2009 Note, net | | $ | — | | | $ | 67,438 | |

| Less current portion | | | — | | | | — | |

| Total long term portion | | $ | — | | | $ | 67,438 | |

In August 2007, Phase 1 DC obtained $9,600 of vendor financing (the “Vendor Note”) for equipment used in Phase 1 DC’s deployment. The Vendor Note bears interest at 11% and may be prepaid without penalty. Interest is due semi-annually commencing February 2008. The balance of the Vendor Note, together with all unpaid interest is due on the maturity date of August 1, 2016. As of December 31, 2009, the outstanding balance of the Vendor Note was $9,600.

In September 2009, Phase 2 DC obtained $898 of vendor financing (the “P2 Vendor Note”) for equipment used in Company’s Phase II Deployment. The P2 Vendor Note bears interest at 7% and requires quarterly interest-only payments through January 2010. Quarterly installments commencing in April 2010 are to be repaid with 92.5% of the VPFs and ACFs received on this equipment with the payments being applied to accrued and unpaid interest first and any remaining amounts be applied to the principal. The balance of the P2 Vendor Note, together with all accrued and unpaid interest is due on the maturity date of December 31, 2018. The P2 Vendor Note may be prepaid at any time without penalty and is not guaranteed by the Company or its other subsidiaries, other than Phase 2 DC. During the three and nine months ended December 31, 2009, the Phase 2 DC repaid principal of $108 on the P2 Vendor Note. As of December 31, 2009, the outstanding balance of the Vendor Note was $790.

During the three months ended September 30, 2009, Phase 2 DC obtained $615 of financing from certain exhibitors (the “P2 Exhibitor Notes”) for equipment used in the Company’s Phase II Deployment. The P2 Exhibitor Notes bear interest at 7% and may be prepaid without penalty. The P2 Exhibitor Notes requires quarterly interest-only payments through June 2010. Principal is to be repaid in thirty-two equal quarterly installments commencing in September 2010. The P2 Exhibitor Notes may be prepaid at any time without penalty and are not guaranteed by the Company or its other subsidiaries, other than Phase 2 DC. As of December 31, 2009, the outstanding balance of the P2 Exhibitor Notes was $615.

CREDIT FACILITIES

In August 2006, Phase 1 DC entered into an agreement with GECC pursuant to which GECC and certain other lenders agreed to provide to Phase 1 DC a $217,000 Senior Secured Multi Draw Term Loan (the “GE Credit

Facility”). Proceeds from the GE Credit Facility were used for the purchase and installation of up to 70% of the aggregate purchase price, including all costs, fees or other expenses associated with the purchase acquisition, receipt, delivery, construction and installation of Systems in connection with Phase 1 DC’s deployment and to pay transaction fees and expenses related to the GE Credit Facility, and for certain other specified purposes. The remaining cost of the Systems was funded from other sources of capital including contributed equity. Each of the borrowings by Phase 1 DC bears interest, at the option of Phase 1 DC and subject to certain conditions, based on the bank prime loan rate in the United States or the Eurodollar rate, plus a margin ranging from 2.75% to 4.50%, depending on, among other things, the type of rate chosen, the amount of equity contributed into Phase 1 DC and the total debt of Phase 1 DC. Under the GE Credit Facility, Phase 1 DC paid interest only through July 31, 2008. Beginning August 31, 2008, in addition to the interest payments, Phase 1 DC must repay approximately 71.5% of the principal amount of the borrowings over a five-year period with a balloon payment for the balance of the principal amount, together with all unpaid interest on such borrowings and any fees incurred by Phase 1 DC pursuant to the GE Credit Facility on the maturity date of August 1, 2013. In addition, Phase 1 DC may prepay borrowings under the GE Credit Facility in whole or in part, after July 31, 2007 and before August 1, 2010, subject to paying certain prepayment penalties ranging from 3% to 1%, depending on when the prepayment is made. The GE Credit Facility is required to be guaranteed by each of Phase 1 DC’s existing and future direct and indirect domestic subsidiaries (the “Guarantors”) and secured by a first priority perfected security interest on all of the collective assets of Phase 1 DC and the Guarantors, including real estate owned or leased, and all capital stock or other equity interests in Phase 1 DC and its subsidiaries, subject to specified exceptions. The GE Credit Facility is not guaranteed by the Company or its other subsidiaries, other than Phase 1 DC. During the nine months ended December 31, 2008 and 2009, the Company repaid principal of $9,644 and $26,310, respectively, on the GE Credit Facility. The 2009 payments include a prepayment of $5,000 in accordance with the GE Fifth Amendment described below, and a additional voluntary prepayments of $3,616 during the nine months ended December 31, 2009. As of December 31, 2009, the outstanding principal balance of the GE Credit Facility was $159,538 at a weighted average interest rate of 10.7%.

In May 2009, Phase 1 DC entered into the fourth amendment (the “GE Fourth Amendment”) with respect to the GE Credit Facility to (1) increase the interest rate from 4.5% to 6% above the Eurodollar Base Rate; (2) set the Eurodollar Base Rate floor at 2.5%; (3) reduce the required amount to be reserved for the payment of interest from 9 months of forward cash interest to a fixed $6,900 (which is included in restricted cash in the accompanying consolidated financial statements), and permitted a one-time payment of $2,600 to be made from Phase 1 DC to its parent Company, AccessDM; (4) increase the quarterly maximum consolidated leverage ratio covenants that Phase 1 DC is required to meet on a trailing 12 months basis; (5) increase the maximum consolidated senior leverage ratio covenants that Phase 1 DC is required to meet on a trailing 12 months basis; (6) reduce the quarterly minimum consolidated fixed charge coverage ratio covenants that Phase 1 DC is required to meet on a trailing 12 months basis and (7) add a covenant requiring Phase 1 DC to maintain a minimum unrestricted cash balance of $2,000 at all times. All of the changes contained in the GE Fourth Amendment are effective as of May 4, 2009 except for the covenant changes in (4), (5) and (6) above, which were effective as of March 31, 2009. In connection with the GE Fourth Amendment, Phase 1 DC paid an amendment fee to GE and the other lenders of approximately $1,000. The amendment fee was recorded as debt issuance costs and is being amortized over the remaining term of the GE Credit Facility. At December 31, 2009, the Company was in compliance with all covenants contained in the GE Credit Facility, as amended.

In August 2009, in connection with the 2009 Private Placement (see Note 5), Phase 1 DC entered into a fifth amendment (the “GE Fifth Amendment”) with respect to the GE Credit Facility, whereby $5,000 of the proceeds of the 2009 Private Placement were used by the Company to purchase capital stock of AccessDM, which in turn used such amount to purchase capital stock of Phase 1 DC. Phase 1 DC then funded the prepayment with respect to the GE Credit Facility. The prepayment is being applied ratably to each of the next 24 successive regularly scheduled monthly amortization payments due under the GE Credit Facility beginning in August 2009.

In October 2009, in connection with the Company’s Phase II Deployment, Phase 2 DC has received commitment letters from GECC’s Media, Communications & Entertainment business (“GE Capital”) and Société Générale Corporate & Investment Banking (“Soc Gen”) for senior credit facilities totaling up to $100 million. GE Capital’s commitment covers the financing of up to about 1,600 Systems and Soc Gen’s commitment covers the financing of up to an additional 533 Systems.

In April 2008, Phase 1 DC executed the Interest Rate Swap with a counterparty for a notional amount of approximately 90% of the amounts outstanding under the GE Credit Facility or an initial amount of $180,000. Under the Interest Rate Swap, Phase 1 DC will effectively pay a fixed rate of 7.3%, to guard against Phase 1 DC’s

exposure to increases in the variable interest rate under the GE Credit Facility to remain in effect until August 2010. As principal repayments of the GE Credit Facility occur, the notional amount will decrease by a pro rata amount, such that approximately 90% of the remaining principal amount will be covered by the Interest Rate Swap at any time.

Upon any refinance of the GE Credit Facility or other early termination or at the maturity date of the Interest Rate Swap, the fair value of the Interest Rate Swap, whether favorable to the Company or not, would be settled in cash with the counterparty. As of December 31, 2009, the fair value of the Interest Rate Swap liability was $2,453. The change in fair value of the interest rate swap for the three months ended December 31, 2008 and 2009 amounted to a loss of $5,411 and a gain of $853, respectively and loss of $3,846 and a gain of $2,076 for the nine months ended December 31, 2008 and 2009, respectively.

In May 2008, AccessDM entered into a credit facility with NEC Financial Services, LLC (the “NEC Facility”) to fund the purchase and installation of equipment to enable the exhibition of 3-D live events in movie theatres as part of the Company’s CineLiveSM product offering. The NEC Facility provides for maximum borrowings of up to approximately $2,000, repayments over a 47 month period, and interest at annual rates ranging from 8.25-8.44%. As of December 31, 2009, AccessDM has borrowed $569 and the equipment purchased therewith is included in property and equipment. During the nine months ended December 31, 2008 and 2009, the Company repaid principal of $0 and $125, respectively, on the NEC Credit Facility. As of December 31, 2009, the outstanding principal balance of the NEC Credit Facility was $376.

In December 2008, Phase 2 B/AIX, a direct wholly-owned subsidiary of Phase 2 DC and an indirect wholly-owned subsidiary of the Company, entered into a credit facility with KBC Bank NV (the “KBC Related Facility”) to fund the purchase of Systems from Barco, Inc. (“Barco”), to be installed in movie theatres as part of the Company’s Phase II Deployment. The KBC Related Facility provides for borrowings of up to a maximum of $8,900 through December 31, 2009 (the “Draw Down Period”) and requires interest-only payments at 7.3% per annum during the Draw Down Period. For any funds drawn, the principal is to be repaid in twenty-eight equal quarterly installments commencing in March 2010 (the “Repayment Period”) at an interest rate of 8.5% per annum during the Repayment Period. The KBC Related Facility may be prepaid at any time without penalty and is not guaranteed by the Company or its other subsidiaries, other than Phase 2 DC. As of December 31, 2009, $8,885 has been drawn down on the KBC Related Facility. Interest expense on the KBC Related Facility for the three months ended December 31, 2008 and 2009 amounted to $0 and $166, respectively and $0 and $384 for the nine months ended December 31, 2008 and 2009, respectively. As of December 31, 2009, the outstanding principal balance of the KBC Related Facility was $8,885.

At December 31, 2009, the Company was in compliance with all of its debt covenants.

STOCKHOLDERS’ RIGHTS

On August 10, 2009, the Company entered into a tax benefit preservation plan (the "Tax Preservation Plan"), dated August 10, 2009, between the Company and American Stock Transfer & Trust Company, LLC, as rights agent. The Company’s board of directors (the "Board") adopted the Tax Preservation Plan in an effort to protect stockholder value by attempting to protect against a possible limitation on its ability to use net operating loss carryforwards (the "NOLs") to reduce potential future federal income tax obligations.

On August 10, 2009, the Board declared a dividend of one preferred share purchase right (the "Rights") for each outstanding share of the Company’s Class A Common Stock and each outstanding share of the Company’s Class B Common Stock, (the "Class B Common Stock," and together with the Class A Common Stock, the "Common Stock") under the terms of the Tax Preservation Plan. The dividend is payable to the stockholders of record as of the close of business on August 10, 2009. Each Right entitles the registered holder to purchase from the Company one one-thousandth of a share of the Company’s Series B Junior Participating Preferred Stock, par value $0.001 per share, (the "Preferred B Stock") at a price of $6.00, subject to adjustment. The Rights are not exercisable, and would only become exercisable when any person or group has acquired, subject to certain conditions, beneficial ownership of 4.99% or more of the Company’s outstanding shares of Class A Common Stock. As of December 31, 2009, the Company did not record the dividends as a 4.99% or more change in the beneficial ownership of the Company’s outstanding shares of Class A Common Stock had not occurred.

CAPITAL STOCK

In August 2004, the Board authorized the repurchase of up to 100,000 shares of Class A Common Stock, which may be purchased at prevailing prices from time-to-time in the open market depending on market conditions and other factors. Under the terms of the 2007 Senior Notes (see Note 5), the Company was previously precluded from purchasing shares of its Class A Common Stock. In a prior year, the Company repurchased 51,440 shares of Class A Common Stock for an aggregate purchase price of $172, including fees, which have been recorded as treasury stock.

Pursuant to the 2007 Senior Notes, in August 2007 the Company issued 715,000 shares of Class A Common Stock (the “Advance Additional Interest Shares”) covering the first 12 months of Additional Interest (see Note 5). The Company registered the resale of these shares of Class A Common Stock and also registered an additional 1,249,875 shares of Class A Common Stock for future Interest Shares and Additional Interest. The Company filed a registration statement on Form S-3 on September 26, 2007, which was declared effective by the SEC on November 2, 2007. The Company is recording the value of the Advance Additional Interest Shares of $4,676 to interest expense over the 36 month term of the 2007 Senior Notes. For the three months ended December 31, 2008 and 2009, the Company recorded $401 and $134, respectively, and $802 and $534 for the nine months ended December 31, 2008 and 2009, respectively, to interest expense in connection with the Advance Additional Interest Shares. See Note 5 on extinguishment of debt.

Commencing with the quarter ended December 31, 2008 and through the maturity of the previous 2007 Senior Notes in the quarter ended September 30, 2010, the Company was obligated to issue a minimum of 132,000 shares or a maximum of 220,000 shares of Class A Common Stock per quarter as Additional Interest (the “Additional Interest Shares”). The Company estimated the initial value of the Additional Interest Shares to be $5,244 and is amortizing that amount over the 36 month term of the 2007 Senior Notes. For the three months ended December 31, 2008 and 2009, the Company recorded $437 and $0, respectively, and $874 and $0 for the nine months ended December 31, 2008 and 2009, respectively, to interest expense in connection with the Additional Interest Shares. In March 2009 and June 2009, the Company issued 220,000 shares of Class A Common Stock, each period, as Additional Interest Shares with a value of $136 and $220, respectively. No Additional Interest Shares were issued in September 2009, as the 2007 Senior Notes were cancelled in August 2009.