Exhibit 99.2

Table of Content

| | | | |

Letter to Shareholders | | | 2 | |

| |

Management’s Discussion & Analysis of Financial Conditions & Results of Operations | | | 5 | |

| |

Auditors’ Report | | | 28 | |

| |

Financial Statements | | | 29 | |

| |

Notes to Consolidated Financial Statements | | | 33 | |

| |

Corporate Information | | | 69 | |

| |

Shareholder Information | | | 70 | |

| 1 |

Dear Shareholders,

Novadaq® has remained focused on our mission to provide clinically relevant fluorescence imaging solutions to surgeons and other healthcare professionals to enable more informed point of care, clinical decisions. New peer-reviewed publications continue to demonstrate the use of our SPY® technology ultimately leads to clinical benefit for patients and economic value for healthcare providers. Over the past year, our team has achieved a number of significant clinical, product development, strategic and commercial milestones that together resulted in accelerated revenue growth in 2012 and have positioned Novadaq well for long-term growth. On behalf of the team at Novadaq, I am proud to share with you our accomplishments of the past twelve months that continue to give me confidence in the future of our company.

The combined SPY Imaging annualized run rate for procedures performed using SPY, SPYElite® andFireFly™ at the beginning of 2012, was approximately 10,000 procedures. By December 2012, the annualized run rate had doubled to an estimated 20,000 procedures. Over the same period, the combined installed base of SPY Imaging technology systems in the United States also grew from approximately 400 systems in January 2012 to 700 systems as we exited the year. Concurrently, our market penetration rate in our lead application, breast reconstruction, increased to 13% from less than 8% a year ago. As a result of these accomplishments, Novadaq total revenues grew to $23 million in 2012, with SPY Imaging revenues increasing to $19 million, which represents an increase of 85% compared to 2011. At the same time, annual gross margin increased to 63% in 2012 from 57% in 2011.

Healthcare professionals continued to validate the benefits of Novadaq’s SPY fluorescence imaging technologies and in 2012, the use of SPY in either open, minimally invasive or robotic procedures was featured in 21 peer reviewed journal publications—double the number of SPY studies published in 2011, which brings the total number of articles included in the SPY Imaging bibliography to sixty-six. Highlights of the 2012 publications included five breast reconstruction studies, one of which was a level 1 comparative study that demonstrated the use of SPY imaging is superior to clinical judgment alone. While the use of SPYElite in plastic reconstructive surgery was the subject of many published papers for Novadaq during 2012,FireFlyenjoyed substantial recognition at the Clinical Robotic Surgeons Association meeting held in Chicago last September with 19 presentations on the technology including colorectal, general and kidney cancer surgeries. Positive first reports of the use of our new PINPOINT® Endoscopic Fluorescence Imaging System in colorectal surgery and cholecystectomy were also published, as were four articles describing the use of our new LUNA™ System in the treatment of diabetic foot ulcers and other non-healing wounds. Looking forward into 2013, we expect the SPY Imaging bibliography will continue to grow at a rapid pace and that we will continue to benefit from positive reports highlighting the use of our products in both our lead and new applications.

While sales of our existing products continued to fuel our growth in 2012, our product development team did not remain idle. We completed development of the PINPOINT Endoscopic Fluorescence Imaging System, which effectively provides SPY imaging in an endoscope for surgeons performing complex minimally invasive procedures. PINPOINT, like other SPY products, allows surgeons to make more informed decisions based on the quality of blood flow and tissue perfusion; and patient anatomy where it counts—in the operating room. The PINPOINT message resonates with surgeons and their hospital administrators who have experienced serious and costly patient complications that could potentially been avoided through the use of PINPOINT. Our first PINPOINT System sale to Maimonides Medical Center in Brooklyn New York occurred in December 2012. Surgeons at Maimonides had been involved with Novadaq’s clinical development of PINPOINT and that first-hand experience with the system and the associated medical value, prompted the hospital to purchase. Although the value proposition of SPY technology is already strong, to further reinforce the PINPOINT message, Novadaq is sponsoring PILLAR, a multi-center clinical study of the use of PINPOINT in colorectal surgery, which will enroll up to 150 patients. Data from the PILLAR study will be presented in key surgical conferences during 2013 starting with the first presentation, which will occur during the Society of American Gastrointestinal Surgeons Conference in Baltimore and the American Society of Colorectal Surgeons in April 2013.

In addition, Novadaq developed the first generation LUNA Fluorescence Angiography System. LUNA will be used in the outpatient wound care clinic to assess tissue perfusion in foot ulcers and non-healing wounds caused by diseases such as diabetes, that lead to vascular deficiencies. LUNA once again demonstrates the value of Novadaq’s core SPY Imaging technology and our Company’s ability to adapt that technology into a product that meets the needs of specific healthcare professionals working in different treatment settings. LUNA is in commercial use in three United States wound care centers and to-date the feedback related to the clinical benefit it imparts has been positive. It is estimated that approximately 500,000 patients could benefit from the use of LUNA each year in the United States.

| 2 |

Originally, Novadaq had partnered with KCI to commercialize this application. However due to changes in priorities and Novadaq’s proven record of being able to commercialize new applications of SPY technology, we will commence a full direct launch of LUNA at the Diabetic Foot Conference Meeting in Los Angeles, California in March 2013.

While the main driver for the adoption of SPY imaging technology is clinical benefit, Novadaq also made progress in reimbursement, which aligns perfectly with the launch of LUNA. In April 2012, the Centers for Medicare and Medicaid Services (“CMS”) established payment for outpatient facilities performing fluorescence imaging procedures. Effective January 2013, CMS increased the amount of that payment, which will assist facilities wishing to acquire the technology and offer LUNA services.

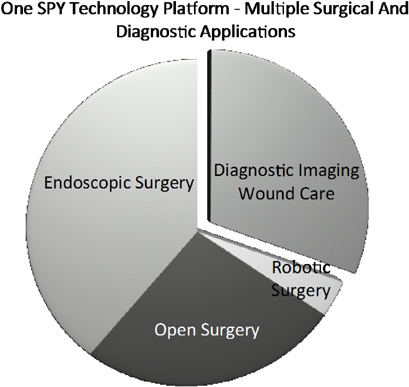

The environment for hospitals and the physicians they employ is becoming dominated by incentives for improving quality of care and penalties for poor practices, as payers increasingly recognize that less than optimal patient outcomes cost our healthcare system billions of dollars each and every year. Clinical publications repeatedly show that SPY Imaging technology supports hospitals as they drive to achieve quality care and reduced costs, which is their number one goal. Likewise, Novadaq’s corporate “ecosystem” fits our diverse customer base which includes physicians and facilities across a broad range of specialties. The figure below shows how Novadaq has adapted to its customer base, by partnering with market leaders, such as LifeCell™ Corporation for “open” surgery and Intuitive Surgical®, for robotics surgery, our first two SPY products, but “going direct” for the sale of PINPOINT and LUNA, now that medical value of our core technology is established.

Novadaq remains steadfast in our application of SPY imaging technology to complex procedures that typically cost the healthcare system $25,000 or more, and those with complication rates that exceed 10 percent. It is here, we believe, that SPY adds the most value. Leveraging our core SPY technology, we will continue to innovate by developing new devices, accessories and imaging agents, which cater to the needs of specific types of surgeries and other procedures and the physicians who performs them. The coming year will also be about introducing SPY technology into a high value outpatient diagnostic setting, wound care clinics. With chronic wounds, each patient visit costs substantially less than $25,000, but as patients require ongoing care the overall economic and personal burden is substantially higher. Numerous published studies have reported fluorescence imaging can be used to guide wound treatment, and to monitor the success of various wound therapies. Combining this clinical support, and the recently increased reimbursement for LUNA, we look forward to its launch in the second half of 2013, when we also expect PINPOINT revenues will start becoming material to our business. As we stated on our fourth quarter

| 3 |

2012 results call, Novadaq’s goal has been to create a business with a sustainable 40%-plus annual growth rate, and we think the Company is positioned to achieve this goal. In 2013, our growth will largely be derived from our partnered products, SPYElite andFireFly, then in 2014 and beyond, LUNA and PINPOINT will become major drivers of our growth.

On behalf of the management team and our Board of Directors, I thank you for your confidence in Novadaq. I look forward to updating you on our progress in the months and years to come.

Best Regards,

Arun Menawat, Ph.D, MBA

Chief Executive Officer

| 4 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS

This Management’s Discussion and Analysis [“MD&A”] for Novadaq® Technologies Inc. [“Novadaq” or the “Company”] should be read with the audited consolidated financial statements for the year ended December 31, 2012. The consolidated financial statements for the year ended December 31, 2012 of Novadaq were prepared in accordance with International Financial Reporting Standards [“IFRS”] as issued by the International Accounting Standards Board [“IASB”]. The audited consolidated financial statements and comparative information has been prepared in United States [“U.S.”] dollars, except where another currency has been indicated.

Forward-Looking Information

This MD&A contains certain information that may constitute forward-looking information within the meaning of Canadian securities laws and forward-looking statements within the meaning of U.S. federal securities laws, both of which we refer to as forward-looking information. In some cases, forward-looking information can be identified by the use of terms such as “may”, “will”, “should”, “expect”, “plan”, “anticipate”, “believe”, “intend”, “estimate”, “predict”, “potential”, “continue” or other similar expressions concerning matters that are not statements about the present or historical facts. Forward-looking information may relate to management’s future outlook and anticipated events or results, and may include statements or information regarding the future financial position, business strategy and strategic goals, research and development activities, projected costs and capital expenditures, financial results, research and clinical testing outcomes, taxes and plans and objectives of, or involving, Novadaq®. Without limitation, information regarding future sales and marketing activities, SPY®, SPYElite®, PINPOINT®, FIREFLY™ and LUNA™ Imaging System sales, placements and utilization rates, reimbursement for SPY, SPYElite, PINPOINT, LUNA and FIREFLY procedures, future revenues arising from the sales of the Company’s products, the sales and marketing arrangements with LifeCell™ Corporation and Kinetic Concepts, Inc., the license and supply agreements with Intuitive Surgical®, Inc., the distribution agreement with MAQUET Cardiovascular and future potential partnerships, research and development activities, the Company’s plans to seek further regulatory clearances for additional indications, as well as the Company’s plans to commercialize PINPOINT®, the endoscopic version of the SPY technology, is forward-looking information.

Forward-looking information is based on certain factors and assumptions regarding, among other things, market acceptance and the rate of market penetration of Novadaq’s products, the success of Novadaq’s partnerships, the effect of reimbursement codes for procedures involving use of the SPY, SPYElite, LUNA and FIREFLY Imaging System and/or PINPOINT Endoscopic Fluorescence Imaging System and the clinical results of the use of SPY, SPY Elite, FIREFLY, LUNA and/or PINPOINT Imaging Systems or the CO2 Heart Laser™ System for Transmyocardial Revascularization. While the Company considers these assumptions to be reasonable based on information currently available to it, they may prove to be incorrect.

Forward-looking information is subject to certain factors, including risks and uncertainties, which could cause actual results to differ materially from what we currently expect. These factors include: risks relating to the transition from research and development activities to commercial activities; market acceptance and adoption of the Company’s products; the risk that a recently implemented reimbursement code will not affect acceptance or usage of the SPY System; risks related to third-party contractual performance; dependence on key suppliers for components of the Company’s products; regulatory and clinical risks; risks relating to the protection of intellectual property; risks inherent in the conduct of research and development activities, including the risk of unfavorable or inconclusive clinical trial outcomes; potential product liability, competition and the risks posed by potential technological advances; and, risks relating to fluctuations in the exchange rate between the U.S. and the Canadian dollar. We have included important factors in the cautionary statements included in this MD&A, particularly in the section entitled “Risk and Uncertainties,” that we believe could cause actual results or events to differ materially from the forward-looking statements that we make. A detailed list of the risks and uncertainties affecting us can be found in our Annual Information Form for the year ended December 31, 2011 and our Short Form Base Shelf Prospectus dated April 3, 2012, each filed on SEDAR. Prospective investors should give careful consideration to such risks and uncertainties.

Undue importance should not be placed on forward-looking information, nor should reliance be placed upon this information as of any other date. Unless required by law, Novadaq does not undertake to update this information at any particular time. Unless otherwise indicated, this MD&A was prepared by management from information available through February 6, 2013.

MD&A | 5 |

Overview and Fourth Quarter Events

Novadaq primarily develops, manufactures and markets real-time fluorescence imaging products that are designed for use by surgeons in the operating room and other clinical settings where open, minimally invasive or interventional surgical procedures are performed. The Company was founded in 2000, and initially listed on the TSX under the trading symbol NDQ in June 2005. Additionally, in March 2012, Novadaq listed on the NASDAQ Global Market under the trading symbol NVDQ.

The Company’s SPY Imaging core technology platform provides clinically relevant anatomic and physiologic images of blood flow in vessels and micro-vessels during a wide variety of complex surgical procedures performed in the operating room and outpatient surgery center without exposing the patient or the surgery staff to radiation. The SPY technology platform is flexible and can be used to develop unique imaging devices specifically designed to meet the needs of different surgeons and the specialty procedures they perform. SPY images enable surgeons treating life-threatening illnesses, such as breast, head and neck, colon, kidney and other cancers, complex hernias, diabetes and certain cardiovascular diseases, to effectively visualize blood flow in vessels, co-joined vessels and micro-vessels and to visually assess the quality of blood perfusion in tissue such as skin and organs. The ability to assess blood flow and tissue perfusion in real-time enables surgeons to repair or remove tissue that could, otherwise, lead to post-operative complications if not addressed during the surgical procedure, and which in turn increase overall treatment costs.

More than 65 peer-reviewed publications report experiences using SPY Imaging technologies in a variety of surgical procedures including open, robotic and endoscopic surgeries. Published literature supports the use of SPY Imaging which enables surgeons to make more informed decisions that lead to fewer post-operative complications which, in turn, helps reduce hospital costs. The SPY, SPYElite and LUNA Imaging System are 510(k) cleared by the U.S. Food and Drug Administration [“FDA”] and indicated for use in a variety of surgical applications including coronary artery bypass graft surgery, cardiovascular surgery, plastic, reconstructive and micro-surgery, organ transplant surgery, gastrointestinal surgery, wound care and vascular surgery and minimally invasive surgery. The SPY and SPYElite Systems are also Conformité Européenne [“CE Marked”] for sale in Europe, are licensed by Health Canada, and have regulatory authority approval for sale in Japan and certain other markets outside of the United States. The Company also markets the SPY Analysis Toolkit [“SPY-Q”], companion post-processing software designed to allow surgeons to enhance and apply objective analysis tools to SPY, SPYElite and LUNA images. SPY-Q is also 510(k) cleared by the FDA. The PINPOINT Endoscopic Fluorescence Imaging System [“PINPOINT”] is FDA 510(k) cleared for use in minimally invasive surgical procedures. PINPOINT combines the capabilities of SPY imaging with state-of-the-art high definition [“HD”] visible light visualization offered by conventional endoscopes, providing surgeons with better visualization of important information related to anatomic structures and micro-perfusion during complex minimally invasive procedures.

In addition to marketing SPY Imaging technology products, Novadaq acquired and now manufactures and markets the FDA Premarket Approval [“PMA”] approved CO2 Heart Laser™ System [“TMR Laser System”] for Transmyocardial Revascularization [“TMR”]. TMR is a procedure aimed at improving blood flow to areas of the heart that cannot be successfully treated by alternative standard revascularization techniques and is often performed adjunctively with coronary artery bypass graft [“CABG”] surgery.

Novadaq’s intellectual property consists of 46 patent families representing 130 granted or allowed patents and 89 applications in various stages of review and prosecution.

The majority of Novadaq’s current revenues comes from alliances formed with leading companies in relevant markets where SPY Imaging and the SPY technology platform have demonstrated improved clinical outcomes in open, minimally invasive and robotic surgery applications. Surgeons performing imaging procedures using SPY technologies are currently reimbursed through the use of existing Current Procedural Terminology [“CPT”] codes. Facilities where procedures are performed using SPY technology in the outpatient environment are reimbursed through the use of Ambulatory Payment Classification [“APC”] codes.

During the fourth quarter of 2012, 135 SPY Elite and FIREFLY systems were shipped to hospitals, and by quarter-end, the number of SPY technology devices installed in hospitals in the United States totaled more than 700. Efforts to increase utilization across the installed bases included sales staff and surgeon training for new applications, and

MD&A | 6 |

this was bolstered by clinical publications in the areas of cholecystectomy, partial nephrectomy, breast reconstruction and colorectal surgeries. Both the training and clinical publications had a positive impact, with shipments of open SPY kits increasing to 4,700, a 81% increase year-over-year, and a 22% increase sequentially. Concurrent with the growth of Novadaq’s partnered businesses, the Company continued to build a direct sales and marketing team for PINPOINT. Recruitment into the multi-center PILLAR™ colorectal surgery study continued at eight active sites. Also, during Q4-2012, the Company has delivered the first PINPOINT device for its order received from Maimonides Medical Center in Brooklyn, New York; however revenue will be recognized when further obligations have been satisfied.

MD&A | 7 |

Overall Performance

Selected Annual Information

The following table sets forth information regarding Novadaq’s revenues, loss from operations and other information for the year presented and should be read in conjunction with the audited consolidated financial statements for the year ended December 31, 2012 and 2011 related notes.

| | | | | | | | | | | | |

| | | Year ended December 31 | |

| | | 2012 | | | 2011 | | | 2010 | |

| | | $ | | | $ | | | $ | |

SPY revenue | | | 16,167,000 | | | | 9,214,000 | | | | 5,560,000 | |

TMR revenue | | | 2,870,000 | | | | 3,712,000 | | | | 2,794,000 | |

Royalty revenue | | | 1,850,000 | | | | 395,000 | | | | — | |

Milestone revenue | | | — | | | | — | | | | 3,959,000 | |

Partnership fee revenue | | | 1,300,000 | | | | 842,000 | | | | 267,000 | |

Service revenue | | | 802,000 | | | | 1,129,000 | | | | 1,291,000 | |

| | | | | | | | | | | | |

Total revenues | | | 22,989,000 | | | | 15,292,000 | | | | 13,871,000 | |

Cost of sales | | | 8,537,000 | | | | 6,634,000 | | | | 5,534,000 | |

| | | | | | | | | | | | |

Gross profit | | | 14,452,000 | | | | 8,658,000 | | | | 8,337,000 | |

| | | 63 | % | | | 57 | % | | | 60 | % |

Operating expenses | | | | | | | | | | | | |

Selling and distribution expenses | | | 4,926,000 | | | | 5,375,000 | | | | 7,067,000 | |

Research and development expenses | | | 5,959,000 | | | | 4,611,000 | | | | 4,916,000 | |

Administration expenses | | | 6,573,000 | | | | 4,551,000 | | | | 4,071,000 | |

Write-down of intangible assets | | | — | | | | — | | | | 4,829,000 | |

Write-down of equipment | | | 58,000 | | | | 314,000 | | | | — | |

Write-down of inventory | | | — | | | | 15,000 | | | | 427,000 | |

| | | | | | | | | | | | |

Total operating expenses | | | 17,516,000 | | | | 14,866,000 | | | | 21,310,000 | |

| | | | | | | | | | | | |

Loss from operations | | | (3,064,000 | ) | | | (6,208000 | ) | | | (12,793,000 | ) |

Interest expense | | | (274,000 | ) | | | (281,000 | ) | | | (279,000 | ) |

Imputed interest expense | | | (433,000 | ) | | | (398,000 | ) | | | (364,000 | ) |

Warrant revaluation adjustment | | | (8,558,000 | ) | | | (3,306,000 | ) | | | (462,000 | ) |

Gain (loss) on investment | | | 25,000 | | | | 25,000 | | | | (125,000 | ) |

Finance income | | | 61,000 | | | | 15,000 | | | | 16,000 | |

| | | | | | | | | | | | |

Loss from operations before income taxes | | | (12,243,000 | ) | | | (10,153,000 | ) | | | (14,187,000 | ) |

| | | | | | | | | | | | |

Income taxes | | | (101,000 | ) | | | — | | | | — | |

| | | | | | | | | | | | |

Net loss and comprehensive loss for the year | | | (12,344,000 | ) | | | (10,153,000 | ) | | | (14,187,000 | ) |

| | | | | | | | | | | | |

Basic and diluted loss and comprehensive loss per share | | | (0.32 | ) | | | (0.32 | ) | | | (0.52 | ) |

| | | |

| Balance Sheet Data | | | | | | | | | | | | |

| | | As at December 31 | |

| | | 2012 | | | 2011 | | | 2010 | |

| | | $ | | | $ | | | $ | |

Cash and cash equivalents | | | 38,954,000 | | | | 9,634,000 | | | | 5,597,000 | |

Working capital | | | 39,944,000 | | | | 9,226,000 | | | | 4,910,000 | |

Total assets | | | 57,587,000 | | | | 22,793,000 | | | | 12,320,000 | |

Total non-current liabilities | | | 21,284,000 | | | | 17,745,000 | | | | 8,292,000 | |

Total liabilities | | | 26,917,000 | | | | 22,167,000 | | | | 13,107,000 | |

Shareholders’ equity (deficiency) | | | 30,670,000 | | | | 626,000 | | | | (787,000 | ) |

MD&A | 8 |

Discussion of Operations—Annual Results

Revenues of $22,989,000 exceeded prior year revenues by $7,697,000, which represents an increase of 50%. SPY product revenues increased by $8,408,000 which included an increase in royalties of $1,455,000. Recurring SPY sales of $10,369,000 more than doubled from 2011. Offsetting were decreases in TMR products and services by $1,169,000, which were a result of the transition of the sales and marketing function of the TMR business to MAQUET.

Gross profit of $14,452,000 exceeded prior year gross profit by $5,794,000. The gross profit increase is due to our product sales growth from our agreements with both LifeCell and Intuitive Surgical, and increased international sales of SPY capital equipment with a partial offset to gross profit from the transitioning of the TMR business to MAQUET.

Selling and distribution expenses of $4,926,000 were $449,000 lower than last year due to the transitioning of sales staff and associated marketing expenditures for both LifeCell and MAQUET; lower stock option costs due to options being fully vested, which was offset by costs associated with recent hiring of sales staff and PINPOINT marketing activities. MAQUET sales staff transitioning has resulted in the reduced costs but is offset by commission expenses due to MAQUET.

Research and development expenses of $5,958,000 were $1,347,000 higher than last year. Increases in expenses mainly comprised of salaries and benefits in the amount of $784,000 to support expanded operations which reduced outsourced product design costs; non-cash stock option expense in the amount of $187,000; clinical trials in the amount of $331,000; and patent and trademark costs in the amount of $53,000 to secure new and existing patents. Offsetting these costs were a reduction in research and consultant expenses in the amount of $206,000 due to in-house staff additions. Various other costs increased by $198,000.

Administration expenses of $6,573,000 were $2,022,000 higher than same period last year. The increased expenses were mainly comprised of the NASDAQ listing fee in the amount of $337,000; increased salary and benefit costs in the amount of $309,000 due to new hires and salary increases; increased professional fees in the amount of $381,000; increased non-cash stock option costs in the amount of $554,000 due to new grants; increased foreign exchange loss in the amount of $96,000; and increased insurance expense in the amount of $238,000. Partially offsetting these costs were decreases in public relations in the amount of $111,000 and bad debt expense accrual in the amount of $57,000. Various other expenses increased by $275,000.

Combined interest expense and non-cash imputed interest expense of $707,000 is $28,000 higher than last year mainly due to increased non-cash imputed interest expense on the convertible debt.

Finance income of $61,000 increased by $46,000 due to the on-hand cash balances from the April 2012 equity offering.

Warrant revaluation non-cash expense of $8,558,000 exceeded the $3,306,000 prior year expense due to the incremental increase in market share price offset by a slight reduction of expenses for warrants exercised throughout 2012. In December 2012, the share price closed at $8.88 versus $4.91 in December 2011.

Income tax expense of $101,000 is due to income reported in the Company’s subsidiary whereas its operation in the previous year did not result in a taxable income position in the U.S.

Net loss of $12,344,000 increased from the previous year net loss by $2,191,000. The increase in net loss comprises of an increase in the non-cash warrant revaluation adjustment in the amount of $5,252,000 due to an increase in the Company’s share price and an increase in operating expenses of $2,650,000. Offsetting was an increase in gross profit in the amount of $5,794,000 resulting from an increase in revenue from our partnership agreements. The remaining value of increased loss consists primarily of income tax expense.

MD&A | 9 |

Summary of Quarterly Results

The following table sets forth information regarding Novadaq’s revenues, loss from operations and other information for the periods presented and should be read in conjunction with the corresponding unaudited interim condensed consolidated financial statements and related notes.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Q1 | | | Q2 | | | Q3 | | | Q4 | | | Q1 | | | Q2 | | | Q3 | | | Q4 | |

| | | 2011 | | | 2011 | | | 2011 | | | 2011 | | | 2012 | | | 2012 | | | 2012 | | | 2012 | |

| | | $000’s | | | $000’s | | | $000’s | | | $000’s | | | $000’s | | | $000’s | | | $000’s | | | $000’s | |

| | | [restated] | | | [restated] | | | [restated] | | | | | | | | | | | | | | | | |

Revenues | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

SPY revenue | | | 832 | | | | 2,040 | | | | 2,731 | | | | 3,611 | | | | 3,109 | | | | 3,802 | | | | 4,262 | | | | 4,994 | |

TMR revenue | | | 904 | | | | 1,005 | | | | 1,009 | | | | 794 | | | | 545 | | | | 710 | | | | 839 | | | | 776 | |

Royalty revenue | | | — | | | | 139 | | | | 140 | | | | 116 | | | | 608 | | | | 346 | | | | 350 | | | | 546 | |

Partnership fee revenue | | | 200 | | | | 200 | | | | 200 | | | | 242 | | | | 325 | | | | 325 | | | | 325 | | | | 325 | |

Service revenue | | | 405 | | | | 261 | | | | 231 | | | | 232 | | | | 180 | | | | 209 | | | | 208 | | | | 205 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total revenues | | | 2,341 | | | | 3,645 | | | | 4,311 | | | | 4,995 | | | | 4,767 | | | | 5,392 | | | | 5,984 | | | | 6,846 | |

Cost of sales | | | 1,257 | | | | 1,449 | | | | 1,857 | | | | 2,071 | | | | 2,045 | | | | 2,088 | | | | 2,123 | | | | 2,281 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Gross profit | | | 1,084 | | | | 2,196 | | | | 2,454 | | | | 2,924 | | | | 2,722 | | | | 3,304 | | | | 3,861 | | | | 4,565 | |

Gross profit percentage | | | 46 | % | | | 60 | % | | | 57 | % | | | 59 | % | | | 57 | % | | | 61 | % | | | 65 | % | | | 67 | % |

Operating expenses | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Selling and distribution expenses | | | 1,275 | | | | 1,400 | | | | 1,353 | | | | 1,347 | | | | 1,063 | | | | 1,217 | | | | 1,289 | | | | 1,357 | |

Research and development expenses | | | 1,048 | | | | 1,270 | | | | 1,107 | | | | 1,186 | | | | 1,162 | | | | 1,378 | | | | 1,778 | | | | 1,640 | |

Administrative expenses | | | 1,113 | | | | 1,141 | | | | 1,102 | | | | 1,195 | | | | 1,471 | | | | 1,638 | | | | 1,863 | | | | 1,602 | |

Write-down of equipment | | | — | | | | — | | | | 314 | | | | — | | | | — | | | | — | | | | — | | | | — | |

Write-down of inventory | | | — | | | | — | | | | 15 | | | | — | | | | — | | | | — | | | | 58 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total operating expenses | | | 3,436 | | | | 3,811 | | | | 3,891 | | | | 3,728 | | | | 3,696 | | | | 4,233 | | | | 4,988 | | | | 4,599 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Loss from operations before the following | | | (2,352 | ) | | | (1,615 | ) | | | (1,437 | ) | | | (804 | ) | | | (974 | ) | | | (929 | ) | | | (1,127 | ) | | | (34 | ) |

Interest expense | | | (71 | ) | | | (72 | ) | | | (68 | ) | | | (70 | ) | | | (69 | ) | | | (69 | ) | | | (68 | ) | | | (68 | ) |

Imputed interest expense | | | (97 | ) | | | (98 | ) | | | (102 | ) | | | (101 | ) | | | (104 | ) | | | (106 | ) | | | (111 | ) | | | (112 | ) |

Finance income | | | 7 | | | | 4 | | | | 3 | | | | 1 | | | | 1 | | | | 14 | | | | 26 | | | | 20 | |

Warrant revaluation adjustment | | | 4 | | | | (2,607 | ) | | | 326 | | | | (1,029 | ) | | | (3,598 | ) | | | (311 | ) | | | (8,038 | ) | | | 3,389 | |

Gain on investment | | | 25 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 25 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Income (loss) from operations before income taxes | | | (2,484 | ) | | | (4,388 | ) | | | (1,278 | ) | | | (2,003 | ) | | | (4,744 | ) | | | (1,401 | ) | | | (9,293 | ) | | | 3,195 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Income tax expense | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | (101 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net income (loss) and comprehensive income (loss) for the period | | | (2,484 | ) | | | (4,388 | ) | | | (1,278 | ) | | | (2,003 | ) | | | (4,744 | ) | | | (1,401 | ) | | | (9,293 | ) | | | 3,094 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Basic income (loss) and comprehensive income (loss) per share for the period | | | (0.09 | ) | | | (0.13 | ) | | | (0.04 | ) | | | (0.05 | ) | | | (0.15 | ) | | | (0.04 | ) | | | (0.23 | ) | | | 0.08 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Diluted loss and comprehensive loss per share for the period | | | (0.09 | ) | | | (0.13 | ) | | | (0.04 | ) | | | (0.05 | ) | | | (0.15 | ) | | | (0.04 | ) | | | (0.23 | ) | | | (0.00 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

MD&A | 10 |

Discussion of Quarterly Results

Total Q4-2012 revenues of $6,846,000 increased by 37% from $4,995,000 in Q4-2011 due to increased revenue from all SPY products and increased partnership fees. SPY product revenues of $5,540,000 increased by 49% from $3,727,000 in Q4-2011 due to increased capital system sales, increased recurring SPY kit and rental revenues, and increased royalties. Partnership fee revenue increased by $83,000 due to the additional partnership agreement signed in Q4-2011. Q4-2012 recurring SPY revenues of $2,980,000 increased by 67% from $1,789,000 over the same period last year due to our partnership agreements. In comparison to Q3-2012, total revenues increased by $862,000 mainly due to increases in SPY products offset by lower sales of TMR products. Increased SPY product sales of $928,000 included increased recurring SPY product revenues, increased capital sales and increased royalties. TMR products and services combined revenues decreased by $66,000 due to lower CO2 laser sales offset by an increase in consumable kit sales and service work performed.

Gross profit of $4,565,000 in Q4-2012 increased from $2,924,000 for the same period last year mainly due to increased sales from alliances with LifeCell and Intuitive. Increasing SPY product sales continue to produce higher margins while TMR margins were slightly lower. In comparison to Q3-2012, gross profit, is higher by $704,000 due to increased SPY capital sales, increased recurring SPY sales and increased royalty revenue offset by lower TMR capital sales.

Selling and distribution expenses of $1,357,000 for Q4-2012 were $10,000 higher than Q4-2011. Cost for both salaries and other sales disbursements were lower due to our partnership agreements; however higher MAQUET commissions for the TMR business and higher promotional costs related to our new PINPOINT system offset the savings from these partnership agreements. Included in our costs are partial year salaries, benefits and marketing costs for new hires to support our Minimally Invasive Surgery [“MIS”] PINPOINT sales launch. Accordingly, selling and distribution expenses were $68,000 higher in Q4-2012 as compared to Q3-2012 due to increased costs of $316,000 to support the MIS PINPOINT launch partially offset by lower incentive costs.

Research and development expenses of $1,640,000 in Q4-2012 were $454,000 higher than Q4-2011 expenses of $1,186,000 due to higher salaries and fringes, in the amount of $315,000, to support expanded operations; higher non-cash stock option expense in the amount of $55,000 due to additional grants and higher fair value priced option; higher royalties due to previous year credit of $84,000; higher clinical trial costs for pre-clinical nerve imaging development in the amount of $63,000; and higher PINPOINT product design costs in the amount of $259,000. Partially offsetting these costs were lower patents and trademarks costs of $215,000; lower incentive costs in the amount of $88,000 due to increased accrual for previous periods and lower SPY registration costs of $44,000 due to the registry being completed. All other expenses increased by $25,000. In comparison to Q3-2012, research and development expenses were $138,000 lower due mainly to reduced clinical trial costs in the amount by $192,000 as previous clinical funding commitments were complete. Offsetting were cost increases for product development and research in the amount of $111,000; and for salaries, benefits and incentives for new hires in the amount of $22,000. Various other expenses resulted in a decrease of $79,000.

Administrative expenses of $1,602,000 in Q4-2012 were $407,000 higher than Q4-2011 expenses due to higher salary costs in the amount of $100,000 from administrative hiring and salary increases; higher stock option costs, in the amount of $174,000 due to new grants; higher insurance cost in the amount of $110,000 from increased coverage; and higher professional fees in the amount of $82,000 from legal fees. Public relations expenses were lower by $79,000, while all other expenses netted out for a $20,000 increase. In comparison to Q3-2012, total expenses decreased by $261,000 mainly due to lower professional fees of $294,000 and lower foreign exchange losses by $58,000. Offsetting were higher expenses related to incentives, computer and office and various other expenses totaling $91,000.

Interest expense of $68,000 and imputed interest expense of $112,000 for Q4-2012 was comparable to interest expense of $70,000 and imputed interest of $101,000 for Q4-2011. Combined interest and imputed interest expense this quarter was $1,000 higher than Q3-2012.

Finance income of $20,000 is higher than income of Q4-2011 due to on-hand cash balances but lower than Q3-2012 due to lower interest rates.

Q4-2012 warrant revaluation adjustment of $3,389,000 was favorable compared to Q4-2011 warrant revaluation expense of $1,029,000 due to a decrease in the Company’s share price. The Q4-2012 non-cash adjustment swung from a non-cash expense of $8,038,000 in Q3-2012 which also relates to a decrease in the Company’s share price

MD&A | 11 |

Income tax expense of $101,000 compared to nil in comparison to Q4-2011 and Q3-2012.

Net income of $3,094,000 in Q4-2012 increased by $5,097,000 from a loss of $2,003,000 in Q4-2011. The increase in net income was due to a non-cash warrant revaluation adjustment by $4,418,000 due to a decrease in the Company’s share price as compared an increase in the share price for the same time period last year; increased gross profit by $1,641,000 resulting from an increase in sales driven by our partnership agreements and higher finance income by $19,000. Offsetting was higher operating expenses in the amount of $871,000, higher tax expense in the amount of $101,000 and higher combined interest expenses in the amount of $9,000.

In comparison to Q3-2012, net income increased by $12,387,000 mainly due to an increase in the non-cash warrant revaluation adjustment in the amount of $11,427,000; an increase of gross profit in the amount of $704,000 and lower operating expenses in the amount of $389,000. Finance income, gain on investment, combined interest expenses and income taxes netted to an increase of $133,000.

Liquidity and Capital Resources

Novadaq’s principal capital needs are for funds to support scientific research and development activities, including system design and development and clinical trials, and funds to support sales and marketing activities, capital expenditures and working capital. Since inception, Novadaq has financed its cash requirements primarily through the issuances of securities and convertible debt, strategic alliances, licensing and development fees, investment tax credits and government funding and interest income. The Company has a history of continuing losses and has an accumulated deficit. Revenues will need to continue to increase over a sustained period. The Company will also require funding from outside sources which may include working capital financing, funds from strategic alliances or equity placements to realize its plans. However, there can be no assurance that Novadaq will be successful in securing its financing on terms favorable to the Company or at all.

Since March 24, 2011, the Company raised funds from the sources listed below:

Private Placement

On March 24, 2011, the Company closed a private placement of $14,280,000, net of transaction costs of $998,000, in exchange for 4,731,864 units at a price of CDN $3.17 per unit. Each unit consists of one common share and 0.45 of a warrant. Each warrant has a five year term and is exercisable for one common share at an exercise price of CDN $3.18.

Revolver Loan

On August 26, 2011, the Company executed a revolving credit agreement with a Canadian chartered bank entitling the Company to borrow to a maximum limit of $2,500,000, subject to a borrowing base formula, certain financial covenants and reporting requirements. The credit facility is secured by a General Security Agreement constituting a first ranking security interest in all personal property of the Company, with a conventional rate of interest. Since its inception and as at December 31, 2012, the Company has not utilized the credit facility.

Sales Distribution Alliance Agreements

On November 29, 2011, the Company and LifeCell Corporation; LifeCell Medical Resources Limited [“LifeCell MR”]; KCI USA, Inc; KCI Medical Resources Ltd [“KCI MR”] signed exclusive multi-year marketing and sales distribution alliance agreements for the commercialization of Novadaq’s SPY imaging system for additional surgical and wound care applications in North American and certain other markets. As part of the agreements, Novadaq received $3,000,000 on December 1, 2011. There was no further contract payments received in 2012.

Public Offering

On April 9, 2012, Novadaq announced that it had completed the closing of its public offering of 7,015,000 common shares at a price $5.75 per share. Gross proceeds from the offering were approximately $40.3 million resulting in cash proceeds of $36.9 million, net of transaction costs.

MD&A | 12 |

As at December 31, 2012, the Company had cash and cash equivalents of $38,954,000 to support its 2012 cash requirements. In addition to the current cash holdings of $38,954,000, the Company has existing loan availability of $2,500,000. Based on the cash on hand as at the date of this report, the capacity to borrow funds and the sales and margins the Company anticipates to generate from operations in 2013, the Company expects to have adequate resources to meet its forecasted cash requirements for the year ending December 31, 2013. In meeting the daily cash requirements, the Company invests its cash and cash equivalents in daily interest at the Company’s chartered bank in Canada.

Contractual Obligations

The Company’s long-term contractual obligations are as follows:

| | | | | | | | | | | | |

| | | 0-1 year

$ | | | 2-5 years

$ | | | After 5 years

$ | |

Long-term debt convertible debentures | | | — | | | | 5,218,000 | | | | — | |

Operating lease | | | 412,000 | | | | 164,000 | | | | — | |

Cash interest on convertible debentures | | | 261,000 | | | | 35,000 | | | | — | |

Repayable government assistance | | | 203,000 | | | | 18,000 | | | | — | |

Cash interest on repayable government assistance | | | 28,000 | | | | — | | | | — | |

Total contractual obligations | | | 904,000 | | | | 5,435,000 | | | | — | |

The long-term operating lease commitments are for premises located in: Mississauga, ON; Taunton, MA and Richmond, BC. The long-term convertible debentures require cash interest payment or Payment in Kind [“PIK”] interest payable semi-annually. Payment provision for these leases and interest expenses are part of our 2013 forecasted cash requirements. The long-term convertible debt repayment is subject to the terms of the indenture agreement and payment for this amount is expected to be fully satisfied within the terms of the agreement. There is no current year requirement for the repayment of this debt.

Critical Accounting Estimates

The preparation of the consolidated financial statements requires the use of estimates and assumptions to be made in applying the accounting policies that affect the reported amounts of assets, liabilities, revenue, expenses and the disclosure of contingent assets and liabilities. The estimates and related assumptions are based on previous experience and other factors considered reasonable under the circumstances, the results of which form the basis of making the assumptions about carrying values of assets and liabilities that are not readily apparent from other sources.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimate is revised if the revision affects only that period or in the period of the revision and future periods if the revision affects both current and future periods. Judgments made by management in the application of IFRS that have a significant effect on the consolidated financial statements relate to the following:

Impairment of non-financial assets

The Company’s impairment test is based on value-in-use calculations that use a discounted cash flow model. The cash flows are derived from the projections for the next three to five years and are sensitive to the discount rate used as well as the expected future cash inflows and the growth rate used for extrapolation purposes.

Development costs

Initial capitalization of costs is based on management’s judgment that technical and economical feasibility is confirmed, usually when a project has reached a defined milestone according to an established project management model.

MD&A | 13 |

Useful lives of key property and equipment and intangible assets

The depreciation method and useful lives reflect the pattern in which management expects the asset’s future economic benefits to be consumed by the Company.

Accounts receivable

The Company reviews its individually significant receivables at each reporting date to assess whether an impairment loss should be recorded in the consolidated statements of loss and comprehensive loss. In particular, judgment by management is required in the estimation of the amount and timing of future cash flows when determining the impairment loss. In estimating these cash flows, the Company makes judgments about the borrower’s financial situation and the net realizable value of collateral, if any. These estimates are based on assumptions about a number of factors and actual results may differ, resulting in future changes to the allowance.

Fair value of financial instruments

Where the fair value of financial assets and financial liabilities recorded in the consolidated statements of financial position cannot be derived from active markets, they are determined using valuation techniques including the discounted cash flow models. The inputs to these models are taken from observable markets. Changes in input from observable market factors could affect the reported fair value of financial instruments.

Share-based compensation

The Company measures the cost of equity-settled transactions with employees by reference to the fair value of equity instruments at the date at which they are granted. Estimating fair value for share-based compensation requires determining the most appropriate valuation model for a grant of these instruments, which is dependent on the terms and conditions of the grant. This also requires determining the most appropriate inputs to the valuation model, including the risk-free interest rate expected life of the option, volatility and dividend yield.

Shareholder warrants

In determining the fair value of the shareholder warrants, the Company used the Black-Scholes option pricing model with the following assumptions: average volatility rate; market price as at the reporting date; risk-free interest rate; the remaining expected life of the warrant; and an exchange rate as at the reporting date. The inputs used in the Black-Scholes model are taken from observable markets. In particular, changes in estimates of the fair value of the shareholder warrants can have a material impact on the reported loss and comprehensive loss for a given period.

Significant Accounting Policies

Revenue Recognition

Revenue is recognized to the extent that it is probable that the economic benefits will flow to the Company and the revenue can be reliably measured, regardless of when the payment is being made. Revenue is measured at the fair value of the consideration received or receivable, taking into account contractually defined terms of payment and excluding taxes or duty. The Company assesses its revenue arrangements with all of its customers and partners against specific criteria to determine if it is acting as principal or agent. The Company has concluded that it is acting as a principal in all of its revenue arrangements. The specific recognition criteria described below must also be met before revenue is recognized.

Product sales

Product sales to customers

Revenue from the sale of medical devices and consumables is recognized when significant risks and rewards of ownership of the products have passed or transferred to the customer, usually when the products are picked up by the shipper for delivery, collection of the related receivable is probable, persuasive evidence of an arrangement exists and the sales price is fixed or determinable.

Products sales under partnership agreements

Revenue is recognized on sale of capital devices or consumable products when they are picked up by the shipper for delivery to the partners, as at that point-of-time the Company has transferred all relevant risks of ownership [inventory risks for the delivered products, credit risk for the transaction with the end customer and price risk for the transaction with the end customer] to the partners, who maintains the business relationship with the end customer. Under the current partnership agreements, the Company shares on-going revenues from its partners’ sales to end

MD&A | 14 |

customers, net of contracted minimum pricing retained by the Company upon initial shipments to its partners, related to the SPY imaging system and the disposable products required to perform the SPY imaging procedure. The Company records any additional amounts when its partners sell to the end customer.

Rental income

Rental income arising from the rental of capital devices is recognized on a straight-line basis over the lease terms and included in product sales.

Multiple element arrangements

The Company may enter into arrangements in which it commits to provide multiple products and services to its customers occurring at different points in time. Revenue recognition for these arrangements is determined based on evaluation of the individual elements of the arrangements. If the element delivered has stand-alone value to the customer and the fair value associated with the element can be measured reliably, the amount recognized as revenue for that element is the fair value of the element in relation to the fair value of the arrangement as a whole. Otherwise, the entire arrangement is treated as one unit of accounting and revenue is deferred and recognized ratably over the remaining term of the arrangements, commencing when all elements are delivered.

Royalty revenue

The Company earns and recognizes royalties upon sale of its products to the end user by its partner.

Partnership fee revenue

Partnership fee revenue relates to upfront payments received from partners for exclusive sales and marketing rights. Upfront payments are deferred and recognized on a straight-line basis over the exclusive sales and marketing terms.

Service revenue

Service revenue primarily relates to extended warranty services agreements in connection with capital sales. Revenue from these agreements are deferred and recognized on a straight-line basis over the extended warranty services term.

Impairment of non-financial assets

The Company assesses at each reporting date whether there is an indication that an asset may be impaired. If such an indication exists, the Company estimates the asset’s recoverable amount. The recoverable amount is the higher of an asset’s or cash-generating unit’s [“CGU”] fair value less costs to sell and its value-in-use. Where the carrying amount of an asset or CGU exceeds its recoverable amount, the asset is considered impaired and is written down to its recoverable amount.

Value-in-use is determined by discounting estimated future cash flows using a pre-tax discount rate that reflects the current market assessment of the time value of money and the specific risks of the asset. In determining fair value less costs to sell, recent market transactions are taken into account, if available. If no such transactions can be identified, an appropriate valuation model has to be used. The recoverable amount of assets that do not generate independent cash flows is determined based on the CGU to which the asset belongs.

The Company bases its impairment calculation on detailed budgets and forecast calculations which are prepared separately for each of the Company’s CGUs to which the individual assets are allocated. These budgets and forecast calculations are generally cover a period of three to five years.

An impairment loss is recognized in the consolidated statements of loss and comprehensive loss if an asset’s carrying amount or that of the CGU to which it is allocated is higher than its recoverable amount. Impairment losses of CGUs are charged against the carrying value of assets in a CGU, in proportion to their carrying amount. In the consolidated statements of loss and comprehensive loss, the impairment losses are recognized in the expense categories consistent with the function of the impaired asset.

An assessment is made at each reporting date as to whether there is any indication that previously recognized impairment losses may no longer exist or may have decreased. For purposes of impairment testing, the Company determined that it has two CGUs, namely the SPY Imaging Technology business and the TMR business.

MD&A | 15 |

The calculation of value-in-use for the CGU would be most sensitive to the following assumptions:

| • | | Price development for the consumables and medical devices; and |

| • | | Market share assumptions. |

Gross margins—Gross margins are based on historical and forecasted values.

Discount rates—Discount rates reflect the current market assessment of the risks specific to each CGU. The discount rate was estimated based on the average percentage of a weighted average cost of capital for the medical device industry.

Price development for the consumables and medical devices—Estimates are obtained from published forecasts about the future development of applicable procedures in North America during the detailed forecast period, as well as management’s own judgments.

Market share assumptions—These assumptions are important because management assesses how the CGU’s position, relative to its competitors, might change over the budget period.

Intangible Assets

The Company owns intangible assets consisting of licenses, SPY software and Xillix patent rights.

Intangible assets acquired separately are measured on initial recognition at cost. The cost of intangible assets acquired in a business combination is its fair value at the date of acquisition. Following initial recognition, intangible assets are carried at cost less accumulated amortization and impairment losses, if any. The useful lives of intangible assets are assessed as either finite or indefinite.

The Company currently does not hold any intangible assets with indefinite lives.

Intangible assets with finite useful lives are amortized over the useful economic life and assessed for impairment whenever there is an indication that the intangible asset may be impaired. The amortization method and amortization period of an intangible asset with a finite useful life is reviewed at least annually. Changes in the expected useful life or the expected pattern of consumption of future economic benefits embodied in the asset is accounted for by changing the amortization period or method, as appropriate, and are treated as changes in accounting estimates. The amortization expense on intangible assets with finite lives is recognized in the consolidated statements of loss and comprehensive loss in the expense category consistent with the function of the intangible assets.

Internally generated intangible assets, such as deferred development costs, are capitalized when the product or process is technically and commercially feasible and the Company has sufficient resources to complete development. The cost of an internally generated intangible asset comprises all directly attributable costs necessary to create, produce and prepare the asset to be capable of operating in the manner intended by management. Amortization of the internally generated intangible assets begins when the development is complete and the asset is available for use. It is amortized over the period of expected future benefit. Amortization is recorded in cost of sales.

Intangible assets are amortized on a straight-line basis over the lesser of their useful lives and the life of the patents, or the term of the patent rights:

| | |

TMR manufacturing license | | 2 years |

| |

SPY software | | 2 years |

| |

Xillix patent rights | | 5-15 years |

MD&A | 16 |

Common share warrants derivatives

The Company’s common share warrants are considered to be derivative liabilities due to the warrants being exercisable in a currency (Canadian dollar) other than the functional currency of the Company (U.S. dollar). Accordingly, the warrants are measured at fair value at each reporting date, with changes in fair value included in the statement of loss and comprehensive loss for the applicable reporting period. A change in the inputs utilized to calculate the fair value such as the Company’s share price, volatility, remaining life and interest rate can have a material impact on the reported loss and comprehensive loss for the period.

Stock-based Compensation Plan

Employees [including senior executives and Board members] of the Company receive remuneration in the form of stock options. In situations where stock options are issued and some or all of the goods or services received by the entity as consideration cannot be specifically identified, the unidentified goods or services received are measured as the difference between the fair value of the share-based compensation transaction and the fair value of any identifiable goods or services received at the grant date. This is then capitalized or expensed as appropriate. The cost of equity-settled transactions with employees is measured by reference to the fair value at the date on which they are granted. The cost of stock option transactions is recognized, together with a corresponding increase in contributed surplus, over the period in which the performance and/or service conditions are fulfilled.

The cumulative expense recognized for share-based compensation transactions at each reporting date until the vesting date reflects the extent to which this vesting period has expired and the Company’s best estimate of the number of shares that will ultimately vest. The expense or credit recognized for a period represents the movement in cumulative expense recognized as at the beginning and end of that period and is recognized in the consolidated statements of loss and comprehensive loss in the respective function line. When options are exercised, the amounts previously credited to contributed surplus are reversed and credited to shareholders’ equity. The amount of cash, if any, received from participants is also credited in share capital in shareholders’ equity. Where the terms of stock options are modified, the minimum expense recognized is the expense as if the terms had not been modified, if the original terms of the award are met. An additional expense is recognized for any modification that increases the total fair value of the share-based compensation transaction, or is otherwise beneficial to the employee as measured at the date of modification. The dilutive effect, if any, of outstanding options is reflected as additional share dilution in the computation of diluted loss per share.

Financial instruments

The Company classifies its financial instruments as either [i] financial assets at fair value through profit or loss, [ii] loans and receivables or [iii] available-for-sale, and its financial liabilities as either [i] financial liabilities at fair value through profit or loss or [ii] other financial liabilities. Appropriate classification of financial assets and liabilities is determined at the time of initial recognition or when reclassified in the consolidated statements of financial position.

All financial instruments are recognized initially at fair value plus, in the case of investments and liabilities not at fair value through profit or loss, directly attributable transaction costs. Financial instruments are recognized on the trade date, which is the date on which the Company commits to purchase or sell the asset. There are currently no financial instruments classified as available-for-sale.

Financial assets at fair value through profit or loss:

Financial assets at fair value through profit or loss include financial assets held for trading and financial assets designated upon initial recognition at fair value through profit or loss. Financial assets are classified as held for trading if they are acquired for the purpose of selling or repurchasing in the near term. Financial assets at fair value through profit or loss are carried at fair value. Related realized and unrealized gains and losses are included in the consolidated statements of loss and comprehensive loss in finance income or finance costs. The Company has currently not designated any financial assets upon initial recognition as at fair value through profit or loss.

Loans and receivables:

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. Loans and receivables are initially recognized at fair value plus transaction costs. They are subsequently measured at amortized cost using the effective interest method less any impairment. The losses arising from impairment are recognized in the consolidated statements of loss and comprehensive loss in finance costs.

MD&A | 17 |

De-recognition:

A financial asset is derecognized when the rights to receive cash flows from the asset have expired or when the Company has transferred its rights to receive cash flows from the asset.

Impairment of financial assets:

The Company assesses at each reporting date whether there is any objective evidence that a financial asset or a group of financial assets is impaired. A financial asset is deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more events that have occurred after the initial recognition of the asset [an incurred ‘loss event’] and that loss event has an impact on the estimated future cash flows of the financial asset or the group of financial assets that can be reliably estimated.

For financial assets carried at amortized cost, the Company first assesses individually whether objective evidence of impairment exists individually for financial assets that are individually significant, or collectively for financial assets that are not individually significant. If the Company determines that no objective evidence of impairment exists for an individually assessed financial asset, it includes the asset in a group of financial assets with similar credit risk characteristics and collectively assesses them for impairment. Assets that are individually assessed for impairment and for which an impairment loss is, or continues to be, recognized are not included in a collective assessment of impairment.

If there is objective evidence that an impairment loss has occurred, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows.

The carrying amount of the asset is reduced through the use of an allowance account and the amount of the loss is recognized in profit or loss. Loans and receivables together with the associated allowance are written off when there is no realistic prospect of future recovery. If, in a subsequent year, the amount of the estimated impairment loss increases or decreases because of an event occurring after the impairment was recognized, the previously recognized impairment loss is increased or reduced by adjusting the allowance account. If a write-off is later recovered, the recovery is credited to finance costs in profit or loss.

Financial liabilities at fair value through profit or loss:

Financial liabilities at fair value through profit or loss include financial liabilities held for trading and financial liabilities designated upon initial recognition at fair value through profit or loss.

Because the Company’s shareholder warrants are denominated in Canadian dollars [a currency different from the Company’s functional currency] they are recognized as a financial liability and are re-measured at fair value through profit or loss.

Other financial liabilities:

Financial liabilities are measured at amortized cost using the effective interest rate method. Financial liabilities include long-term debt issued, which is initially measured at fair value, which is the consideration received, net of transaction costs incurred. Transaction costs related to the long-term debt instruments are included in the value of the instruments and amortized using the effective interest rate method. The effective interest expense is included in finance costs in the consolidated statements of loss and comprehensive loss.

De-recognition:

A financial liability is derecognized when the obligation under the liability is discharged or cancelled or expires.

When an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a de-recognition of the original liability and the recognition of a new liability, and the difference in the respective carrying amounts is recognized in the consolidated statements of loss and comprehensive loss.

Offsetting of financial instruments

Financial assets and financial liabilities are offset and the net amount reported in the consolidated statements of financial position if, and only if, there is a currently enforceable legal right to offset the recognized amounts and there is an intention to settle on a net basis, or to realize the assets and settle the liabilities simultaneously.

MD&A | 18 |

Fair value of financial instruments

Fair value is the estimated amount that the Company would pay or receive to dispose of the financial instrument contracts in an arm’s length transaction between knowledgeable, willing parties who are under no compulsion to act. The fair value of financial instruments that are traded in active markets at each reporting date is determined by reference to quoted market prices, without any deduction for transaction costs.

For financial instruments not traded in an active market, the fair value is determined using appropriate valuation techniques that are recognized by market participants. Such techniques may include using recent arm’s length market transactions, reference to the current fair value of another instrument that is substantially the same, discounted cash flow analysis or other valuation models.

The Company’s financial instruments are comprised of the following as at December 31, 2012: cash and cash equivalents of $38,954,000; accounts receivable of $4,057,000; accounts payable and accrued liabilities of $3,407,000; convertible debentures of $4,657,000; shareholder warrants of $13,003,000 and, repayable government assistance of $221,000. The Company invested its cash and cash equivalents in daily interest savings accounts. Accounts receivable of $4,057,000 (net of $228,000 bad debts reserves), based in the United States and Canada, are subject to minimal credit risk based on the nature of our customers. The receivables are being carried at amortized cost. Accounts payable and accrued liabilities of $3,407,000 carried at amortized cost, is comprised of short-term obligations owing to suppliers relative to the Company’s operations. The convertible debentures have a principal value of $5,068,000 and PIK debentures of $150,000. The shareholder warrants are re-valued quarterly utilizing the Black-Scholes model to determine fair value. The repayable government assistance comprises an Industrial Research and Assistance Program loan, received from the National Research Council, with principal repayment terms over 30 months, commenced in August 2011.

Changes in Accounting Policies Including Initial Adoption

Standards Issued But Not Yet Effective

Standards issued but not yet effective up to the date of issuance of the Company’s consolidated financial statements are listed below. This listing is of standards and interpretations issued, which the Company reasonably expects to be applicable at a future date. The Company intends to adopt those standards when they become effective.

IFRS 9Financial Instruments: Classification and Measurement

In November 2009, the IASB issued IFRS 9, which covers classification and measurement as the first part of its project to replace IAS 39. In October 2010, the Board of Directors also incorporated new accounting requirements for liabilities. The standard introduces new requirements for measurement and eliminates the current classification of loans and receivables, available-for-sale and held-to-maturity, currently in IAS 39. There are new requirements for the accounting of financial liabilities as well as a carryover of requirements from IAS 39. The standard is effective for annual periods beginning on or after January 1, 2015. The Company does not anticipate early adoption and will adopt the standard when it is mandated by the IASB. The Company is currently assessing the impact of the standard on the consolidated financial statements.

IFRS 13Fair Value Measurement

IFRS 13 is a comprehensive standard for fair value measurement and disclosure requirements for use across all IFRS standards. IFRS 13 defines fair value and establishes disclosures about fair value measurement. The effective date of this amendment is for annual periods beginning on or after January 1, 2013. The Company is currently assessing the impact of the standard on the consolidated financial statements.

IAS 32Offsetting Financial Assets and Financial Liabilities

IAS 32Financial Instruments: Presentationand IFRS 7Financial Instruments: Disclosures

In December 2011, the IASB publishedOffsetting Financial Assets and Financial Liabilitiesand issued new disclosure requirements in IFRS 7Financial Instruments: Disclosures. The effective date for the amendments to IAS 32Financial Instruments: Presentationis for annual periods beginning on or after January 1, 2014.

MD&A | 19 |

IFRS 7Financial Instruments: Disclosures

In October 2010, the IASB issued amendments to IFRS 7Financial Instruments: Disclosures”, which increase the disclosure requirements for transactions involving transfers of financial assets. The effective date for the amendments to IFRS 7 is for annual periods beginning on or after January 1, 2013. The Company does not expect implementation of these amendments to have a significant impact on its disclosures or presentation.

Risks and Uncertainties

The Company’s ability to generate revenue and profit from its technologies is dependent on a number of factors, and the risks identified below, if they were to occur, could have a material impact on the Company’s business, financial condition, and liquidity, results of operation or prospects. The risks and uncertainties outlined below do not constitute an exhaustive list. Additional risks and uncertainties not presently known to the Company or that the Company believes to be immaterial may also adversely affect the Company’s business.

The Company has Incurred and Continues to Incur Losses

The Company has incurred substantial losses since its inception in 2000 and continues to incur losses and experience negative cash flows. The Company cannot predict if or when it will operate profitably, generate positive cash flows or if it will be able to implement its business strategy successfully. Pursuing its strategy requires the Company to incur significant expenditures for research and product development, marketing and general administrative activities. As a result, the Company needs to continue to grow its revenues and gross margins to achieve and sustain profitability and positive operating cash flows, and it may need to raise additional capital.

Ability to Obtain Sufficient Funding

The Company does not yet generate sufficient operational cash flows to meet the Company’s planned growth and to fund development activities. The Company has forecasted cash requirements for 2013, and funding from sources currently in place will permit the Company to meet its 2013 operating requirements. However, in the long-term, the Company will require funding from outside sources to complete its business development plans; therefore, the Company is dependent on the willingness of investors or strategic partners to continue to invest in the Company or enter into strategic relationships to continue further development of the Company’s products. There is no assurance that the Company will secure additional funding sources or partnerships. Currently, the Company has no committed sources of capital other than a revolving credit agreement, dated August 26, 2011, with a Canadian chartered bank entitling the Company to borrow a maximum limit of $2,500,000, subject to certain conditions. Since its inception, the Company has not utilized its credit facility.

Shift from Research and Development to Commercialization

Having been founded in 2000, the Company has a limited operating history. Historically, the focus of its operations had been on research and development. However, in mid-2005 the Company shifted its focus towards commercialization with the commercial launch of its system for use during cardiac surgery. In 2009 through 2012, the Company formed certain alliances with four market leading companies for the broad commercialization of Novadaq’s leading products. The successful commercialization of any one of Novadaq’s products will depend on a number of financial, logistical, technical, legal, regulatory, competitive, economic and other factors, the outcome of which cannot be predicted, some of which will be out of the Company’s control. The Company has incurred losses to date and expects to incur losses in the future. In addition, despite the Company’s current focus on the commercialization of its products, the Company continues to invest in additional research and development in order to expand the applications of its imaging platform, and these activities may require significant cash commitments which may affect the profitability of the Company. There can be no assurance that the Company will be able to achieve or sustain profitability in the future.

Successful Commercialization of the Products

The Company’s future success will depend in large part on its own ability to commercialize PINPOINT and the ability of its partners to market and sell SPYElite, FIREFLY and LUNA for use in wound care, and TMR Laser System [together, the “Products”]. Successful commercialization of the Products will depend on a number of factors, including achieving widespread adoption of the Products among the targeted surgeons and hospitals,

MD&A | 20 |

maintaining the Company’s relationships with its suppliers and partners, obtaining sufficient quantities of components for the Products, including fluorescence agent, the performance of Novadaq’s partnering sales organization, the ability of the Company and its partners to successfully market the Products at projected selling prices, and the ability of the Company and its partners to commercially launch Products that are currently in development phase, in a timely manner. In addition, the Company’s success will depend on its ability to supply the key FIREFLY components of da Vinci Surgical Robotic System and the successful commercialization of that Product. There can be no assurance that the Company will be successful in these endeavors. Successful commercialization will also depend on whether any unanticipated adverse effects result from use of the Products, or unfavorable publicity develops in respect of the Products, as well as the emergence of new or existing products as competition for the Products, which are proven to be more clinically or cost-effective.

Dependence on Relationships with Strategic Partners

Execution of the Company’s current strategy is dependent on cooperation with strategic partners for sales and marketing and research and development. The Company can offer no guarantee that existing partnership agreements will be renewed or that its strategic partners will not seek to renegotiate or amend those agreements before or after a product has been commercialized. In addition, there can be no assurance of the commercial success of any joint ventures in which the Company is, or will become, involved.