| News Release | NYSE-AMEX, TSX Symbol: NG |

NovaGold Strongly Endorses Barrick’s Comments on the Donlin Gold Project

September 9, 2011 - Vancouver, British Columbia - NovaGold Resources Inc.(NYSE-AMEX: NG, TSX: NG) During its Investor Day, which took place on September 7, 2011, Barrick Gold Corporation (“Barrick”) expressed its view of the Donlin Gold Project (“Donlin Gold”) located in Alaska. Donlin Gold is owned equally by a wholly-owned subsidiary of NovaGold Resources Inc. (“NovaGold” or “the Company”) and a wholly-owned subsidiary of Barrick. NovaGold strongly endorses Barrick’s stated position regarding Donlin Gold. In highlighting Donlin Gold, Barrick emphasized the following:

- Donlin Gold is one of the world’s largest undeveloped gold deposits and among the premier projects in Barrick’s portfolio;

- Donlin Gold is located in the United States, one of the world’s safest geo-political jurisdictions and one in which Donlin Gold is well equipped to permit;

- Over the last five years, Donlin Gold’s mineral endowment has more than doubled;

- Donlin Gold has the potential for a mine life of over 25 years on the basis of present mineral endowment, with significant exploration upside to extend the mine life;

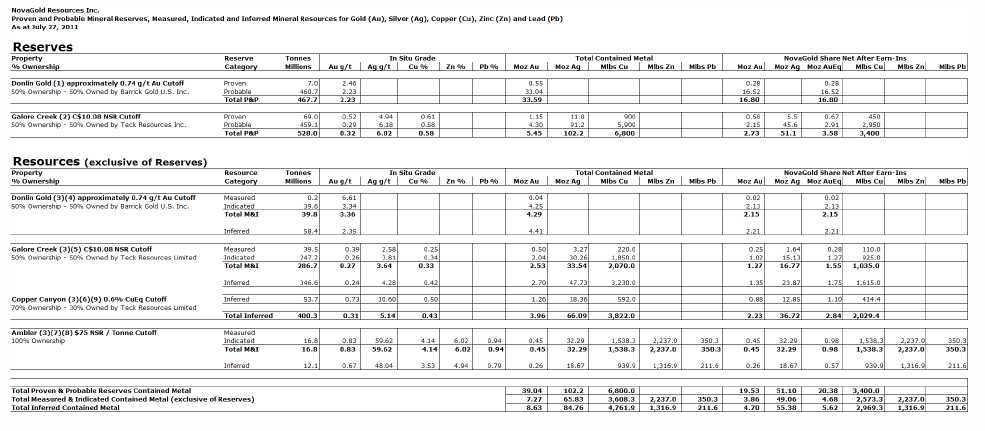

- With 38 million ounces of gold resources already identified (See the attached Appendix for details), the deposit remains open at depth as well as to the north and east with strong surface anomalies extending for an additional five kilometers along strike;

- Building a gas pipeline, expected to cost approximately US$1 billion, would result in lower power costs than in a diesel option, and provides the Project with an environmentally sound, long-term socially responsible alternative;

- The revised feasibility study, including the natural gas pipeline, is expected to be completed before the end of the year;

- Permitting is expected to begin in the first half of 2012.

“With the potential to produce well over a million ounces of gold a year from one of the safest mining jurisdictions, Donlin Gold is among the most important gold development projects in the world today. We are pleased that our partner Barrick's presentation highlights this profile. The fact that the headline capital increase from US$4.5 billion to US$6 billion is in-line with other projects being developed by Barrick and other major producers is most encouraging. It should also be recognized that with the increase in the price of gold from approximately US$900/oz in 2009 when the previous study was conducted, to US$1,800/oz now, the value of the 38 million ounce gold resource has increased substantially,” said Rick Van Nieuwenhuyse, NovaGold’s President and CEO. “From that standpoint, the increase in the projected capital cost represents a fraction of the increase in the intrinsic value of the gold endowment at Donlin Gold, without regard to the potential expansion of the resource that Barrick referenced. The addition of the gas pipeline is especially good news, as we believe this will add long-term benefits to the Project.”

Barrick’s view on the future development of Donlin Gold comes on the heels of the successful completion of the Company’s Prefeasibility Study on its 50%-owned Galore Creek project located in northwestern British Columbia, which the Company announced on July 27, 2011, and the positive PEA on the wholly-owned Ambler project, which was announced on April 14, 2011. NovaGold believes that the escalating copper price environment and the increasing value of its copper assets provide a natural hedge against rising capital and input costs for its projects and indeed should underpin the share value of NovaGold. To this end, NovaGold retained J.P. Morgan Securities LLC and RBC Capital Markets to explore various alternatives that could bridge the market valuation gap for our copper holdings.

“The fact that Barrick has expressed its desire to proceed with the permitting process to advance the Project is a major plus for our company and our shareholders. We are proud to be a partner of Barrick,

1

a company with a solid operating track record and financial strength,” concluded Mr. Van Nieuwenhuyse. “We look forward to developing Donlin Gold into one of the largest and best gold mines in the world.”

The technical information contained in this press release was reviewed by Kevin Francis, SME Registered Member, VP, Resources for NovaGold and a Qualified Person as defined by NI 43-101.

About NovaGold

NovaGold is a precious metals company engaged in the exploration and development of mineral properties located principally in Alaska, U.S.A. and British Columbia, Canada. The Company is focused on advancing its two core properties, Donlin Gold and Galore Creek, with the objective of becoming a low-cost, million-ounce-a-year gold producer, and offers superior leverage to gold and copper with one of the largest mineral reserve and mineral resource bases of any junior or mid-tier gold company. NovaGold has a strong track record of expanding deposits through exploration success and forging collaborative partnerships, both with local communities and with major mining companies. The Donlin Gold project in Alaska, one of the world’s largest undeveloped gold deposits, is held by a limited liability company owned equally by wholly-owned subsidiaries of NovaGold and Barrick Gold Corporation. The Galore Creek project in British Columbia, a large copper-gold-silver deposit, is held by a partnership owned equally by wholly-owned subsidiaries of NovaGold and Teck Resources Limited. NovaGold also owns a 100% interest in the high-grade Ambler copper-zinc-lead-gold-silver deposit in northern Alaska and has other earlier-stage exploration properties. NovaGold trades on the TSX and NYSE-AMEX under the symbol NG. More information is available at www.novagold.net or by emailing info@novagold.net.

# # #

NovaGold Contact

Rick Van Nieuwenhuyse

President & CEO

Greg Martin

Vice President, Business Development & Treasurer

604-669-6227 or 1-866-669-6227

Cautionary Note Regarding Forward-Looking Statements

This press release includes certain“forward-looking statements” and“forward-looking information” within the meaning of the applicable securities legislation industry United States Private Securities Litigation Reform Act of 1995. All statements, other than statements of historical fact, included herein including, without limitation, statements relating to NovaGold’s future operating or financial performance, are forward-looking statements. Forward-looking statements are frequently, but not always, identified by words such as“expects”,“anticipates”,“believes”,“intends”,“estimates”,“potential”,“possible”, and similar expressions, or statements that events, conditions, or results“will”,“may”,“could”, or“should” occur or be achieved. These forward-looking statements may include statements regarding perceived merit of properties; exploration results and budgets; mineral reserves and resource estimates; work programs; capital expenditures; timelines; strategic plans; completion of transactions; market prices for precious and base metals; or other statements that are not statements of fact. Forward-looking statements involve various risks and uncertainties. There can be no assurance that such statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. Important factors that could cause actual results to differ materially from NovaGold’s expectations include the uncertainties involving the need for additional financing to explore and develop properties and availability of financing in the debt and capital markets; uncertainties involved in the interpretation of drilling results and geological tests and the estimation of reserves and resources; the need for continued cooperation with Barrick and other third parties for development of the Donlin Gold Project; the need for cooperation of government agencies and native groups in the development and operation of properties; the need to obtain permits and governmental approvals;; risks of construction and mining projects such as accidents, equipment breakdowns, bad weather, non-compliance with environmental and permit requirements, unanticipated variation in geological structures, ore grades or recovery rates; unexpected cost

2

increases, which could include significant increases in estimated capital and operating costs; fluctuations in metal prices and currency exchange rates; uncertainties and risks regarding permitting for the Project and permitting and construction of the proposed natural gas pipeline and other risk and uncertainties disclosed in NovaGold’s Annual Information Form for the year-ended November 30, 2010, filed with the Canadian securities regulatory authorities, and NovaGold’s annual report on Form 40-F filed with the United States Securities and Exchange Commission and in other NovaGold reports and documents filed with applicable securities regulatory authorities from time to time. NovaGold’s forward-looking statements reflect the beliefs, opinions and projections on the date the statements are made. NovaGold assumes no obligation to update the forward-looking statements of beliefs, opinions, projections, or other factors, should they change.

Cautionary Note Regarding Reserve and Resource Estimates

This press release has been prepared in accordance with the requirements of the securities laws in effect in Canada, which differ from the requirements of U.S. securities laws. Unless otherwise indicated, all resource and reserve estimates included in this press release have been prepared in accordance with National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy, and Petroleum Definition Standards on Mineral Resources and Mineral Reserves. NI 43-101 is a rule developed by the Canadian Securities Administrators which establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. Canadian standards, including NI 43-101, differ significantly from the requirements of the United States Securities and Exchange Commission (“SEC”), and resource and reserve information contained herein may not be comparable to similar information disclosed by U.S. companies. In particular, and without limiting the generality of the foregoing, the term“resource” does not equate to the term“reserves”. Under U.S. standards, mineralization may not be classified as a“reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. The SEC’s disclosure standards normally do not permit the inclusion of information concerning “measured mineral resources”,“indicated mineral resources” or “inferred mineral resources” or other descriptions of the amount of mineralization in mineral deposits that do not constitute“reserves” by U.S. standards in documents filed with the SEC. U.S. investors should also understand that “inferred mineral resources” have a great amount of uncertainty as to their existence and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an“inferred mineral resource” will ever be upgraded to a higher category. Under Canadian rules, estimated “inferred mineral resources” may not form the basis of feasibility or pre-feasibility studies except in rare cases. Investors are cautioned not to assume that all or any part of an“inferred mineral resource” exists or is economically or legally mineable. Disclosure of “contained ounces” in a resource is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers to report mineralization that does not constitute“reserves” by SEC standards as in-place tonnage and grade without reference to unit measures. The requirements of NI 43-101 for identification of“reserves” are also not the same as those of the SEC, and reserves reported by the Company in compliance with NI 43-101 may not qualify as“reserves” under SEC standards. Accordingly, information concerning mineral deposits set forth herein may not be comparable with information made public by companies that report in accordance with U.S. standards.

3

Appendix– Reserve & Resource Table

4

2. See numbered footnotes below on resource information. Resources shown in blue are reported as net values to NovaGold after all project earn-ins.

3. AuEq - gold equivalent is calculated using gold and silver in the ratio of gold + silver ÷ (US$1023 Au ÷ US$17 Ag) 2008 - 2010 average metal prices.

4. Rounding as required by reporting guidelines may result in apparent summation differences between tonnes, grade and contained metal content

5. Tonnage and grade measurements are in metric units. Contained gold and silver ounces are reported as troy ounces, contained copper, zinc, and lead pounds as imperial pounds

Resource Footnotes:

(1) The basis for the cut-off grade was an assumed gold price of US$825/oz. The new reserve estimate represents a 15% increase over the 29.3 million ounce reserve estimate contained in the 2009 technical report referenced below , and is based on the inclusion of additional drilling and a US$100/oz increase in long-term gold price assumptions from that used in 2009. The increase in reserves is expected to extend the mine life from 21 years to 25 years at the feasibility production rate, and does not materially change the information contained in the technical report. It is believed that the additional storage capacity provided for in the 2009 feasibility study will accommodate the increase in tailings and that the w aste rock storage facility can be modified to contain the additional unmineralized rock material. The Qualified Person for this reserve estimate is Kevin Francis, P.Geo., NovaGold Resources Inc.

(2) Mineral Reserves are contained within Measured and Indicated pit designs using metal prices for copper, gold and silver of US$2.50/lb, US$1,050/oz, and US$16.85/oz, respectively. 2. Appropriate mining costs, processing costs, metal recoveries and inter ramp pit slope angles varing from 42º to 55º were used to generate the pit phase designs. Mineral Reserves have been calculated using a ’cashflow grade’ ($NSR/SAG mill hr) cut-off which was varied from year to year to optimize NPV. The net smelter return (NSR) was calculated as follow s: NSR = Recoverable Revenue – TCRC (on a per tonne basis), where: NSR = Net Smelter Return; TCRC = Transportation and Refining Costs; Recoverable Revenue = Revenue in Canadian dollars for recoverable copper, recoverable gold, and recoverable silver using metal prices of US$2.50/lb, US$1,050/oz, and US$16.85/oz for copper, gold, and silver, respectively, at an exchange rate of CDN$1.1 to US$1.0; Cu Recovery = Recovery for copper based on mineral zone and total copper grade; for Mineral Reserves this NSR calculation includes mining dilution. SAG throughputs were modeled by correlation with alteration types. Cashflow grades were calculated as the product of NSR value in $/t and throughput in t/hr. 4. The life of mine strip ratio is 2.16.

(3) Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. Inferred Resources are in addition to Measured and Indicated Resources. Details of Measured and Indicated Resources and other NI 43-101 information can be found by following the links below to the relevant Technical Report. Inferred Resources have a great amount of uncertainty as to their existence and w hether they can be mined legally or economically. It cannot be assumed that all or any part of the Inferred Resources will ever be upgraded to a higher category. See "Cautionary Note Concerning Reserve & Resource Estimates".

(4)A variable cut-off grade has been estimated based on recent estimates of mining costs, processing costs (dependent upon sulfur content), selling costs and royalties. Resources are constrained within a Lerchs-Grossman (LG) open-pit shell using the long-term metal price assumption of US$900/oz of gold, w hich is a US$50/oz increase over the long-term gold price assumption used in the 2009 technical report. Assumptions for the LG shell included pit slopes variable by sector and pit area: mining cost is variable w ith depth, averaging US$2.08/t mined; process cost is calculated as the percent sulfur grade x US$2.7948 + US$12.82; general and administrative costs, gold selling cost and sustaining capital are reflected on a per tonne basis. Based on metallurgical testing, gold recovery is assumed to be 89.5% . The Qualified Person for this resource estimate is Kevin Francis, P.Geo., NovaGold Resources Inc.

(5) Mineral resources are contained within a conceptual Measured, Indicated and Inferred optimized pit shell using the same economic and technical parameters as used for Mineral Reserves. Tonnages are assigned based on proportion of the block below topography. The overburden/bedrock boundary has been assigned on a whole block basis. 4) Mineral resources have been estimated using a constant NSR cut-off of C$10.08/t milled. The Net Smelter Return (NSR) was calculated as follows: NSR = Recoverable Revenue – TCRC (on a per tonne basis), where: NSR = Diluted Net Smelter Return; TCRC = Transportation and Refining Costs; Recoverable Revenue = Revenue in Canadian dollars for recoverable copper, recoverable gold, and recoverable silver using silver using the economic and technical parameters mentioned above. 5) The mineral resource includes material within the conceptual M&I pit that is not scheduled for processing in the mine plan but is above cutoff.

(6) The copper-equivalent grade was calculated as follow s: CuEq = Recoverable Revenue ÷ 2204.62 * 100 ÷ 1.55. Where: CuEq = Copper equivalent grade; Recoverable Revenue = Revenue in US dollars for recoverable copper, recoverable gold and recoverable silver using metal prices of US$1.55/lb, US$650/oz, and US$11/oz for copper, gold, and silver, respectively; Cu Recovery = 100%.

(7)Resources stated as contained w ithin a potentially economically minable underground shapes above a US$75.00/t NSR cut-off

(8)NSR calculation is based on assumed metal prices of US$2.50/lb for copper, US$1,000/oz for gold, US$16.00/oz for silver, US$1.00/lb for zinc and US$1.00/lb for lead. A mining cost of US$45.00/t and combined processing and G&A costs of US$31.00 w ere assumed to form the basis for the resource NSR cut-off determination.

(9)NovaGold Canada Inc. has agreed to transfer its 60% joint venture interest in the Copper Canyon property to the Galore Creek Partnership, w hich is equally owned by NovaGold Canada Inc.and a subsidiary of Teck Resources Limited. The remaining 40% joint venture interest in the Copper Canyon property is owned by another wholly owned subsidiary of NovaGold."

Cautionary Note Concerning Reserve & Resource Estimates

This summary table uses the term “resources”, “measured resources”, “indicated resources” and “inferred resources”. United States investors are advised that, while such terms are recognized and required by Canadian securities laws, the United States Securities and Exchange Commission (the “SEC”) does not recognize them. Under United States standards, mineralization may not be classified as a “reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. Mineral resources that are not mineral reserves do not have demonstrated economic viability. United States investors are cautioned not to assume that all or any part of measured or indicated resources will ever be converted into reserves. Further, inferred resources have a great amount of uncertainty as to their existence and as to whether they can be mined legally or economically. It cannot be assumed that all or any part of the inferred resources will ever be upgraded to a higher category. Therefore, United States investors are also cautioned not to assume that all or any part of the inferred resources exist, or that they can ounces be mined ” is permitted disclosure under Canadian regulations, however, the SEC normally only permits issuers to reportlegally or economically. Disclosure of “contained “resources” as in place tonnage and grade without reference to unit measures. Accordingly, information concerning descriptions of mineralization and resources contained in this release may not be comparable to information made public by United States companies subject to the reporting and disclosure requirements of the SEC.

National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”) is a rule developed by the Canadian Securities Administrators, which established standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. Unless otherwise indicated, all resource estimates contained in this circular have been prepared in accordance with NI 43-101 and the Canadian Institute of Mining, Metallurgy and Petroleum Classification System.

| Technical Reports and Qualified Persons | |||

| The documents referenced below provide supporting technical information for each of NovaGold's projects. | |||

| Project | Qualifed Person(s) | Most Recent Disclosure & Filing Date | Link to Most Recent Disclosure |

| Donlin Gold | Kirk Hanson P.E., AMEC Gordon Seibel M.AusIMM, AMEC Simon Allard, P.Eng. Gregory Wortman P.Eng., AMEC Alexandra Kozak P.Eng., AMEC | Donlin Creek Gold Project, Alaska, USA NI 43-101 Technical Report - April 1, 2009 | http://www.novagold.com/upload/technical_reports/DonlinCreekFS.pdf |

| Donlin Gold | Kevin Francis, P.Geo., NovaGold Resources Inc. | March 2010 reserve and resource updates: NovaGold press release - March 22, 2010 | http://novagold.com/section.asp?pageid=13238 |

| Galore Creek | Robert Gill, P.Geo., AMEC Jay Melnyk, P.Eng., AMEC Greg Kulla, P.Geo., AMEC Greg W ortman, P.Eng., AMEC Dana Rogers, P.Eng., AMEC | NovaGold Resources Inc., Galore Creek Copper–Gold Project, British Columbia, NI 43-101 Technical Report on Pre-Feasibility Study,to be filed w ith 45 days of July 27, 2011 | http://www.novagold.com/section.asp?pageid=15854 |

| Copper Canyon | Erin Workman, P.Geo., NovaGold Resources Inc. | Not publicly released - updated March 2008 | http://www.novagold.net/upload/technical_reports/CopperCanyonFebruary2005.pdf |

| Ambler | Russ W hite, P.Geo., SRK Consulting Neal Rigby, C.Eng., MIMMM, Ph.D., SRK Consulting | NI 43-101 Preliminary Economic Assessment, Ambler Project - May 9, 2011 | http://www.novagold.com/upload/pdf/Ambler_PEA_May2011.pdf |

5