Exhibit 99.1

CENTER FINANCIAL

CORPORATION

11th Annual Financial Services Conference

May 7, 2009

Safe Harbor

During the course of this presentation, the Company may make or present forward-looking statements. These forward-looking statements may be subject to the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Such statements, including statements related to the Company’s growth, market position and future performance are predictions based on factors as currently known to the Company. Actual events or results may differ materially. You are referred to the documents the Company files from time to time with the U.S. Securities and Exchange Commission, which review the risks and uncertainties that could cause actual results to differ materially from those contained in the Company’s projections or forward-looking statements. The historical results achieved by the company are not necessarily indicative of its future prospects. The Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

2

Corporate Profile

23 years of service as strong commercial franchise

Leading provider of business-oriented products & services

Recipient of the SBA’s 2006 Excellence in Lending Award

20 offices across the nation

19 full-service branches in Southern California, Seattle, Chicago

One loan production office (LPO) in Seattle

Total assets of $2.09 billion (at 3/31/09)

Headquartered in Los Angeles

Largest Korean concentration outside Republic of Korea

3

Community Business Bank

Core customer base

Small to middle-market closely held businesses

Professional associations

Korean-American and other ethnic niche groups

Centered around relationship banking philosophy Areas of expertise

International trade finance

SBA lending

Cash management services

4 |

|

Resilient Koreatown

Factors supporting influx of Korean immigrants and funds

Ratification of Visa-Waiver status

Ratification of US-Korea FTA

Liberation of currency controls

Mid-Wilshire financial district

Symbolic for growth in LA’s Korean-American community

5

Supporting Our Customers

“We have earned the trust of our patients and the community by taking great care in treating their needs. Our bankers do the same with us, and that is why Center Bank is our financial partner of choice.”

Jae Hong Kim, CEO Samra Acupuncture Spinal Center Los Angeles, CA

6

Supporting Our Customers

“Our motto is ‘Flexible Packaging Made Better.’ Center Bank is our financial partner because we believe they make business banking better.”

Don Kwon, President Osio International, Inc. Anaheim, CA

7

Supporting Our Customers

“We are a strong organization:

Think again. Think Hyundai.

We need a strong financial

partner like Center Bank

to support our growth long term.”

John Lim, President

Hyundai Construction

Equipment U.S.A., Inc.

Elk Grove Village, IL

8

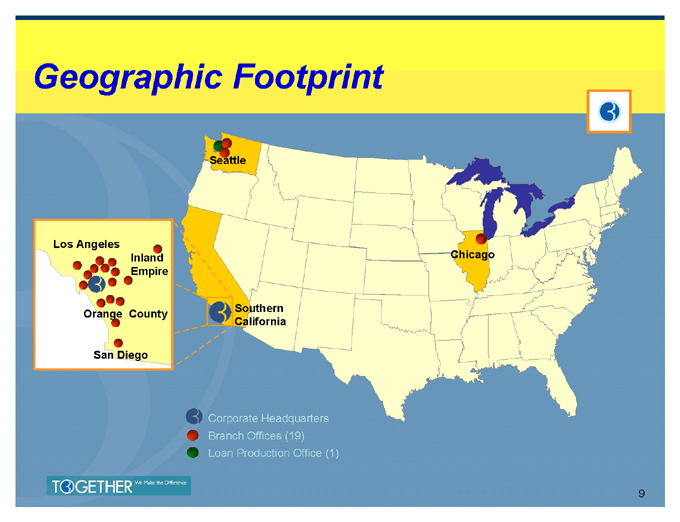

Geographic Footprint

Seattle

Los Angeles Chicago Inland Empire

Southern Orange County California

San Diego

Corporate Headquarters Branch Offices (19) Loan Production Office (1)

9

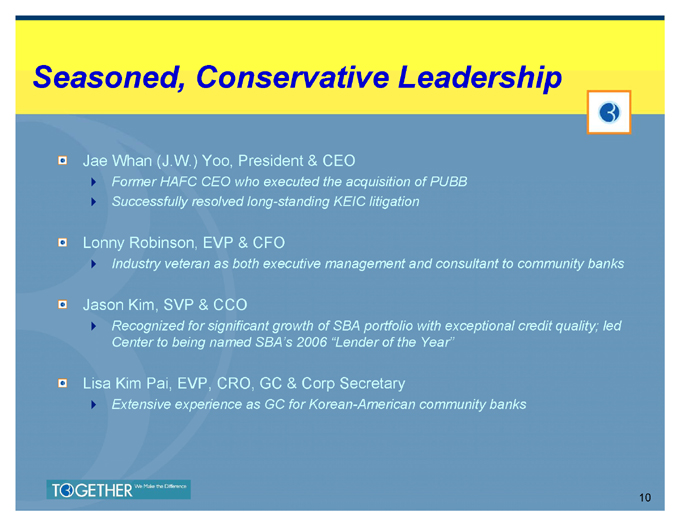

Seasoned, Conservative Leadership

Jae Whan (J.W.) Yoo, President & CEO

Former HAFC CEO who executed the acquisition of PUBB

Successfully resolved long-standing KEIC litigation

Lonny Robinson, EVP & CFO

Industry veteran as both executive management and consultant to community banks

Jason Kim, SVP & CCO

Recognized for significant growth of SBA portfolio with exceptional credit quality; led Center to being named SBA’s 2006 “Lender of the Year”

Lisa Kim Pai, EVP, CRO, GC & Corp Secretary

Extensive experience as GC for Korean-American community banks

10

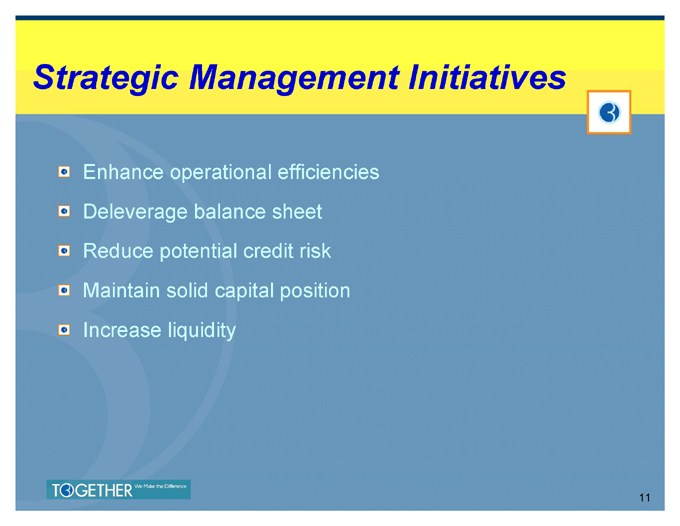

Strategic Management Initiatives

Enhance operational efficiencies Deleverage balance sheet Reduce potential credit risk Maintain solid capital position Increase liquidity

11

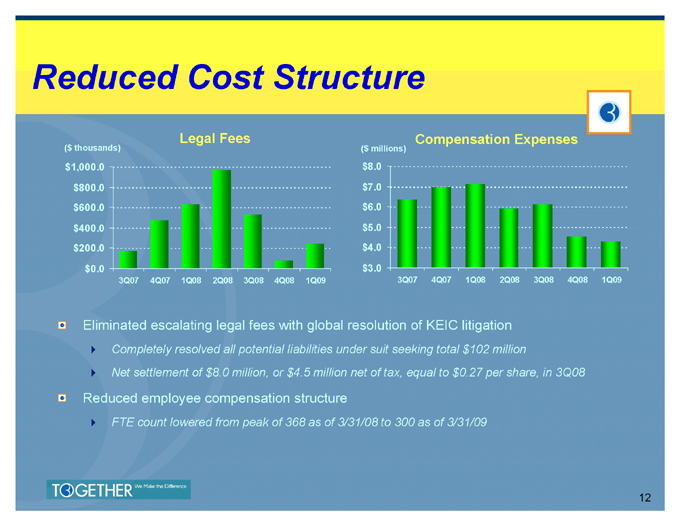

Reduced Cost Structure

($ thousands) Legal Fees Compensation Expenses

($ millions) $1,000.0 $8.0 $800.0 $7.0 $600.0 $6.0 $400.0 $5.0 $200.0 $4.0 $0.0 $3.0

3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09

Eliminated escalating legal fees with global resolution of KEIC litigation

Completely resolved all potential liabilities under suit seeking total $102 million

Net settlement of $8.0 million, or $4.5 million net of tax, equal to $0.27 per share, in 3Q08

Reduced employee compensation structure

FTE count lowered from peak of 368 as of 3/31/08 to 300 as of 3/31/09

12

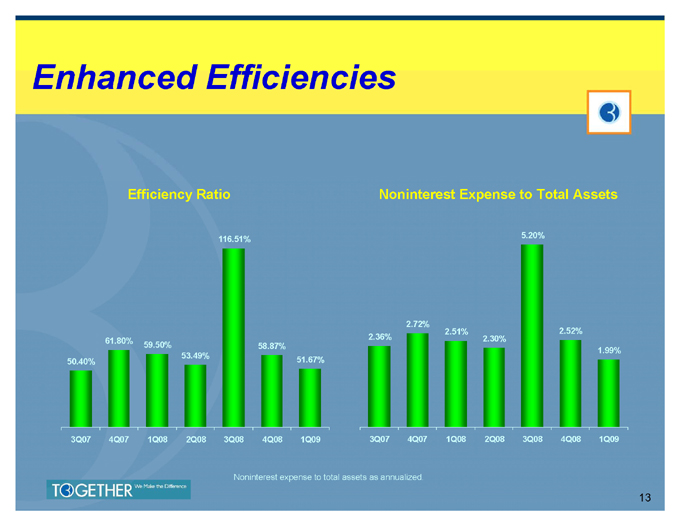

Enhanced Efficiencies

Efficiency Ratio Noninterest Expense to Total Assets

5.20% 116.51%

2.72%

2.51% 2.52% 2.36% 2.30%

61.80%

59.50% 58.87%

1.99%

53.49%

50.40% 51.67%

3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09

Noninterest expense to total assets as annualized.

13

Deleveraged Balance Sheet

Commenced deleveraging strategy at the close of 1Q08

Planned sales of approximately $100 million in loans

Reduce CRE portfolio

Mitigate growing fixed-rate concentration

Forfeit unprofitable growth

Focus on strengthening balance sheet in anticipation of weakening economy

14

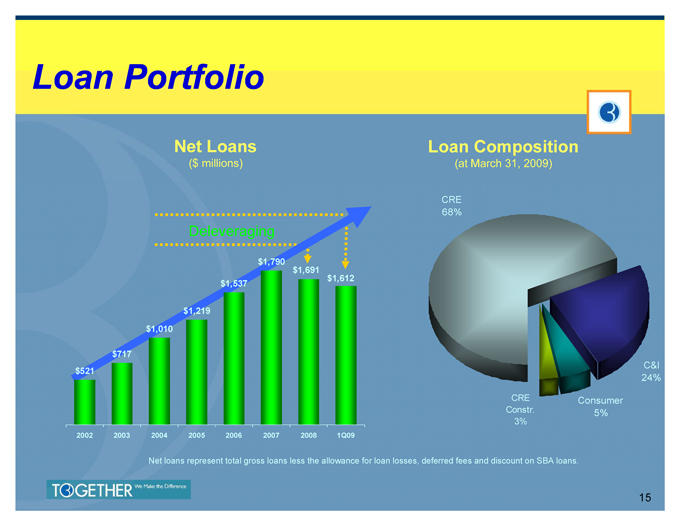

Loan Portfolio

Net Loans Loan Composition

($ millions) (at March 31, 2009)

CRE 68%

Deleveraging

$1,790 $1,691 $1,612 $1,537

$1,219 $1,010

$717

C&I $521

24%

CRE Consumer Constr. 5% 3%

2002 2003 2004 2005 2006 2007 2008 1Q09

Net loans represent total gross loans less the allowance for loan losses, deferred fees and discount on SBA loans.

15

Conservative Credit Management

Stringent underwriting guidelines Proactive loan portfolio management

Semi-annual external loan review Annual internal stress testing

16

Vigilance to Credit Quality

Fully understanding the market

Extensive management experience directly in marketplace

Balancing marketing and credit quality Investing in resources

Credit Administration Department

Review and Monitoring Team

Semi-annual external loan review Ongoing credit training

Stringent underwriting standards and guidelines

17

Stringent Underwriting Standards

Commercial Real Estate: Commercial Loans & Lines:

Loan-to-value ratio 65% Detailed cash flow analysis Minimum debt coverage ratio in Evaluate trade cycle, analyze excess of 125% industry and performance Stricter guidelines for cash-out projections refinancing Other key considerations Sensitivity analysis ` Credit history, experience, Other key considerations financial analysis, terms & conditions and others

Customary personal guarantees

Credit history, experience, collateral, terms & conditions and others

18

Mounting Headwinds

Historical low interest rates Declining equity values Higher FDIC premiums

Weakening economy – significant deterioration from 4Q08

19

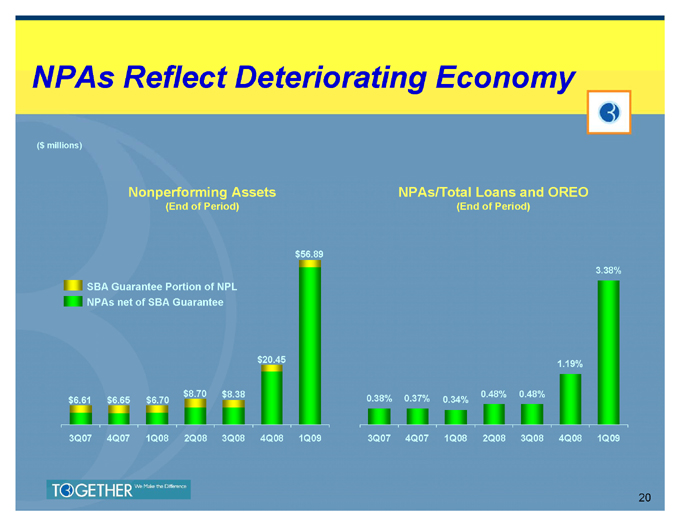

NPAs Reflect Deteriorating Economy

($ millions)

Nonperforming Assets NPAs/Total Loans and OREO

(End of Period) (End of Period)

$56.89

3.38% SBA Guarantee Portion of NPL

NPAs net of SBA Guarantee

$20.45 1.19%

$8.70 $8.38 0.48% 0.48% $6.61 $6.65 $6.70 0.38% 0.37% 0.34%

3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09

20

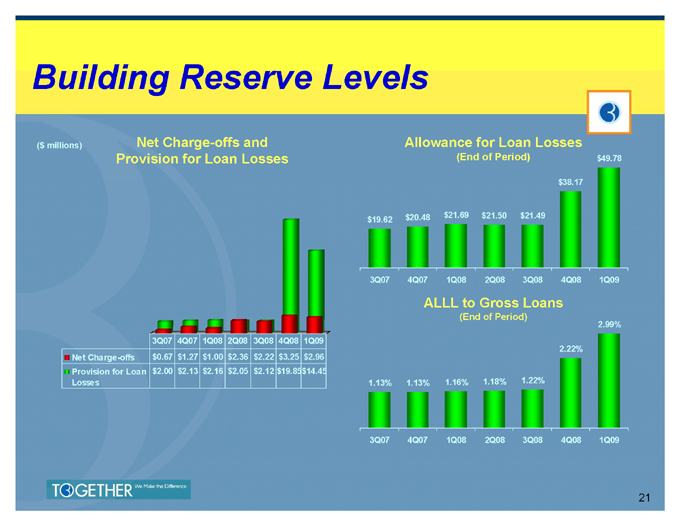

Building Reserve Levels

($ millions) Net Charge-offs and Allowance for Loan Losses Provision for Loan Losses (End of Period) $49.78

$38.17

$20.48 $21.69 $21.50 $21.49 $19.62

3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09

ALLL to Gross Loans

(End of Period) 2.99% 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2.22% Net Charge-offs $0.67 $1.27 $1.00 $2.36 $2.22 $3.25 $2.96 Provision for Loan $2.00 $2.13 $2.16 $2.05 $2.12 $19.85 $14.45 Losses 1.13% 1.13% 1.16% 1.18% 1.22%

3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09

21

Tightened FAS 5 Reserve Methodology

Heightened risk ratios for special mention and substandard credits Shortened loss experience evaluation period

` Better reflects current portfolio stresses and recent losses

Designed to more adequately assess true directional

consistency – given severity and swiftness of economic deterioration

22

Heightened Credit Risk Management

Asset quality task force

` Proactive executive management involvement

` Bi-weekly review of delinquent loans greater than $500,000

` Action plan initiated from day one of delinquency

Internal stress testing mechanisms

` Deployment of new software enabling more regular testing

` Capital burn down analysis assuming significant CRE devaluation

Minimizing portfolio risk

` Strategic sales and run-off of construction and CRE portfolios

` Revitalize SBA lending pipeline

• Allows for growth with minimal risk given 90% guarantee

• Low levels of loan loss provision needed

23

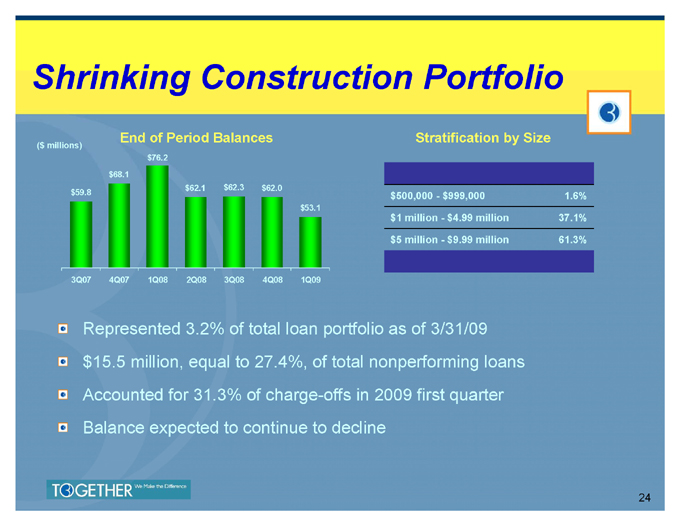

Shrinking Construction Portfolio

End of Period Balances Stratification by Size

($ millions) $76.2 $68.1 $62.1 $62.3 $62.0

$59.8 $500,000—$999,000 1.6%

$53.1

$1 million—$4.99 million 37.1%

$5 million—$9.99 million 61.3%

3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09

Represented 3.2% of total loan portfolio as of 3/31/09 $15.5 million, equal to 27.4%, of total nonperforming loans Accounted for 31.3% of charge-offs in 2009 first quarter Balance expected to continue to decline

24

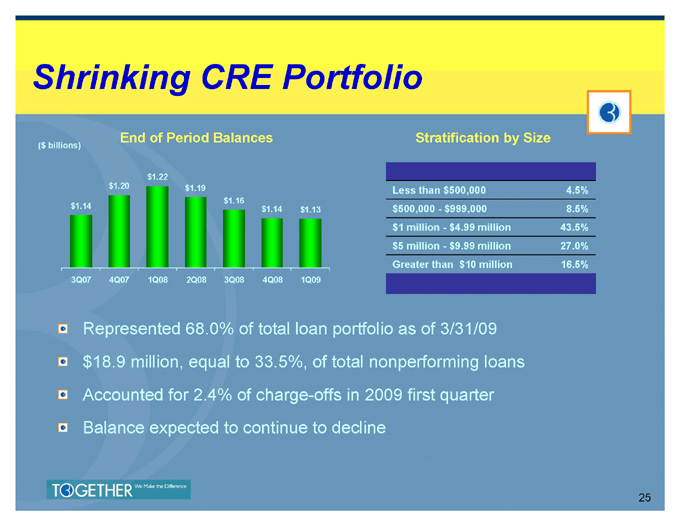

Shrinking CRE Portfolio

End of Period Balances Stratification by Size

($ billions)

$1.22

$1.20 $1.19 Less than $500,000 4.5%

$1.16

$1.14 $1.14 $500,000—$999,000 8.5%

$1.13

$1 million—$4.99 million 43.5% $5 million—$9.99 million 27.0% Greater than $10 million 16.5%

3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09

Represented 68.0% of total loan portfolio as of 3/31/09 $18.9 million, equal to 33.5%, of total nonperforming loans Accounted for 2.4% of charge-offs in 2009 first quarter Balance expected to continue to decline

25

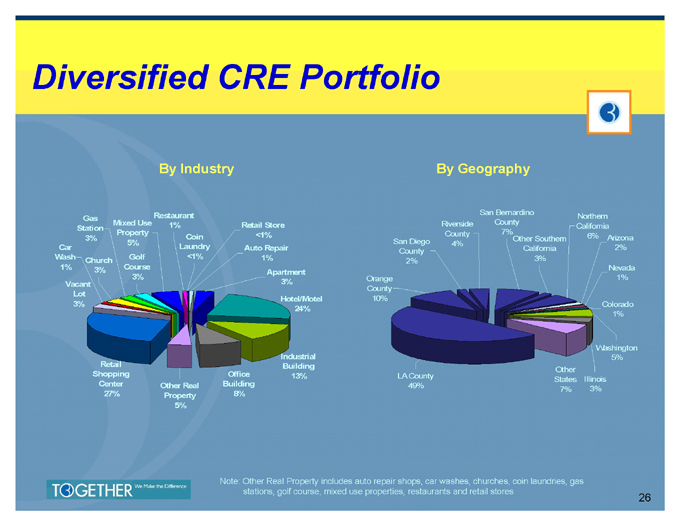

Diversified CRE Portfolio

By Industry By Geography

Restaurant San Bernardino

Gas Northern

Mixed Use 1% Retail Store Riverside County

Station California

Property <1% County 7%

3% Coin Other Southern 6% Arizona

5% San Diego 4%

Car Laundry Auto Repair California 2% County

Wash Golf <1% 1% 3% Church 2%

1% 3% Course Nevada Apartment

3% Orange 1%

Vacant 3% County Lot Hotel/Motel 10%

3% Colorado

24%

1%

Washington

Industrial 5% Retail Building

Other

Shopping Office 13% LA County

States Illinois

Center Other Real Building 49%

7% 3%

27% Property 8% 5%

Note: Other Real Property includes auto repair shops, car washes, churches, coin laundries, gas stations, golf course, mixed use properties, restaurants and retail stores

26

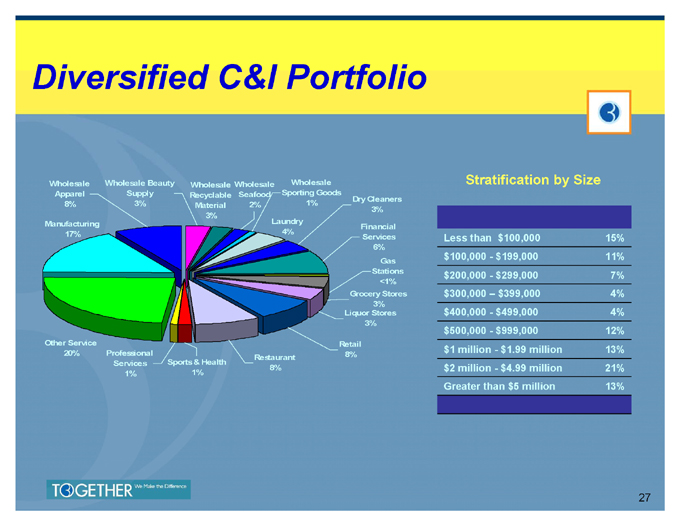

Diversified C&I Portfolio

Wholesale Wholesale Beauty Wholesale Wholesale Wholesale Stratification by Size Apparel Supply Recyclable Seafood Sporting Goods Dry Cleaners

8% 3% Material 2% 1%

3% 3% Manufacturing Laundry Financial 17% 4%

Services Less than $100,000 15% 6% $100,000—$199,000 11% Gas Stations $200,000—$299,000 7% <1% Grocery Stores $300,000 – $399,000 4%

3% $400,000—$499,000 4% Liquor Stores 3% $500,000—$999,000 12% Other Service Retail 20% Professional $1 million—$1.99 million 13% Restaurant 8% Services Sports & Health

8% $2 million—$4.99 million 21%

1% 1%

Greater than $5 million 13%

27

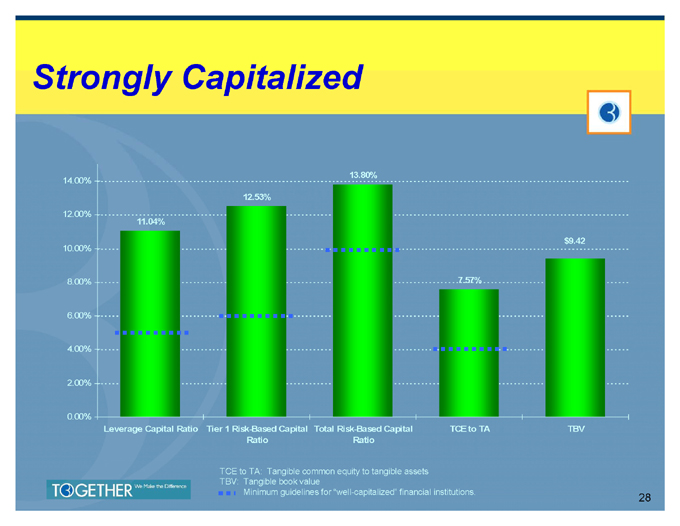

Strongly Capitalized

13.80%

14.00%

12.53%

12.00% 11.04%

10.00% $9.42 8.00% 7.57%

6.00%

4.00%

2.00%

0.00%

Leverage Capital Ratio Tier 1 Risk-Based Capital Total Risk-Based Capital TCE to TA TBV Ratio Ratio

TCE to TA: Tangible common equity to tangible assets TBV: Tangible book value

Minimum guidelines for “well-capitalized” financial institutions.

28

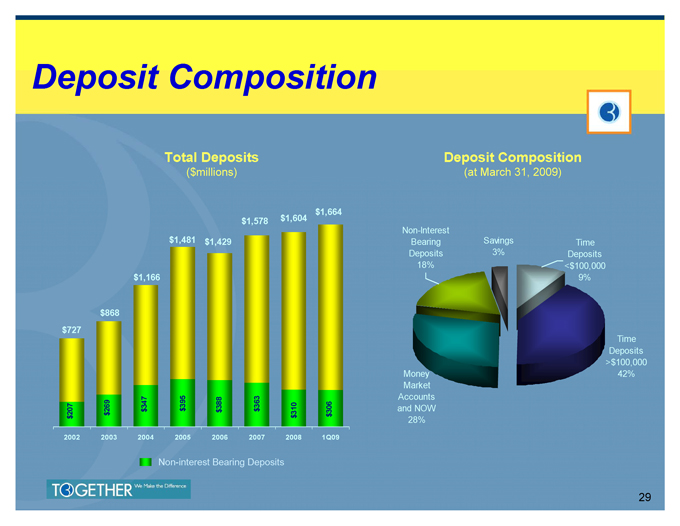

Deposit Composition

Total Deposits Deposit Composition

($millions) (at March 31, 2009)

$1,664 $1,578 $1,604

Non-Interest $1,481 $1,429 Bearing Savings Time Deposits 3% Deposits 18% <$100,000 $1,166 9%

$868 $727

Time Deposits

>$100,000 Money 42% Market 395 363 Accounts 347 388 and NOW

207 269 $ $ $ $ $ 310 306 $ $ $ 28% 2002 2003 2004 2005 2006 2007 2008 1Q09

Non-interest Bearing Deposits

29

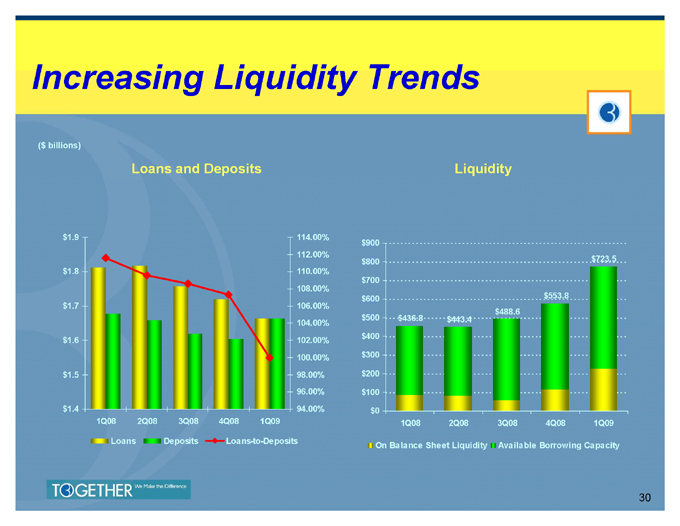

Increasing Liquidity Trends

($ billions)

Loans and Deposits Liquidity

$1.9 114.00% $900 112.00% $800 $723.5 $1.8 110.00% $700 108.00% $600 $553.8 $1.7 106.00% $488.6 $500 $436.8 $443.4 104.00% $400 $1.6 102.00% 100.00% $300 $1.5 98.00% $200

96.00% $100 $1.4 94.00% $0

1Q08 2Q08 3Q08 4Q08 1Q09 1Q08 2Q08 3Q08 4Q08 1Q09 Loans Deposits Loans-to-Deposits On Balance Sheet Liquidity Available Borrowing Capacity

30

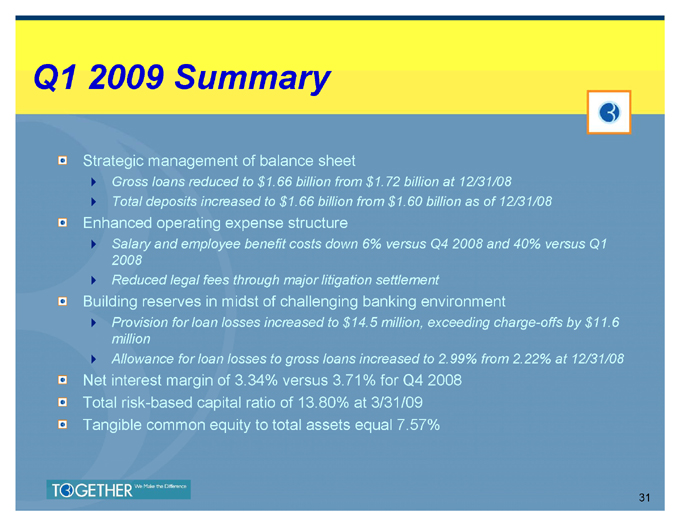

Q1 2009 Summary

Strategic management of balance sheet

` Gross loans reduced to $1.66 billion from $1.72 billion at 12/31/08

` Total deposits increased to $1.66 billion from $1.60 billion as of 12/31/08

Enhanced operating expense structure

` Salary and employee benefit costs down 6% versus Q4 2008 and 40% versus Q1 2008

` Reduced legal fees through major litigation settlement

Building reserves in midst of challenging banking environment

` Provision for loan losses increased to $14.5 million, exceeding charge-offs by $11.6 million

` Allowance for loan losses to gross loans increased to 2.99% from 2.22% at 12/31/08

Net interest margin of 3.34% versus 3.71% for Q4 2008 Total risk-based capital ratio of 13.80% at 3/31/09 Tangible common equity to total assets equal 7.57%

31

Investment Highlights

Strong, cohesive executive team with extensive experience managing through financial crises Focused on balanced growth in recessionary environment Strong capital positioning Proactive risk recognition and management Building reserve levels against significant headwinds

With the right team doing the right things … Together We Make the Difference

32

33