Exhibit 99.1

2012 Interim Report

Wynn Macau, Limited (incorporated in the Cayman island with limited liability) Stock Code:1128

For identification purposes only

2 |

| Corporate Information |

4 |

| Highlights |

5 |

| Management Discussion and Analysis |

28 Directors and Senior Management

Contents

37 Other Information

47 Report on Review of Interim

Financial Information

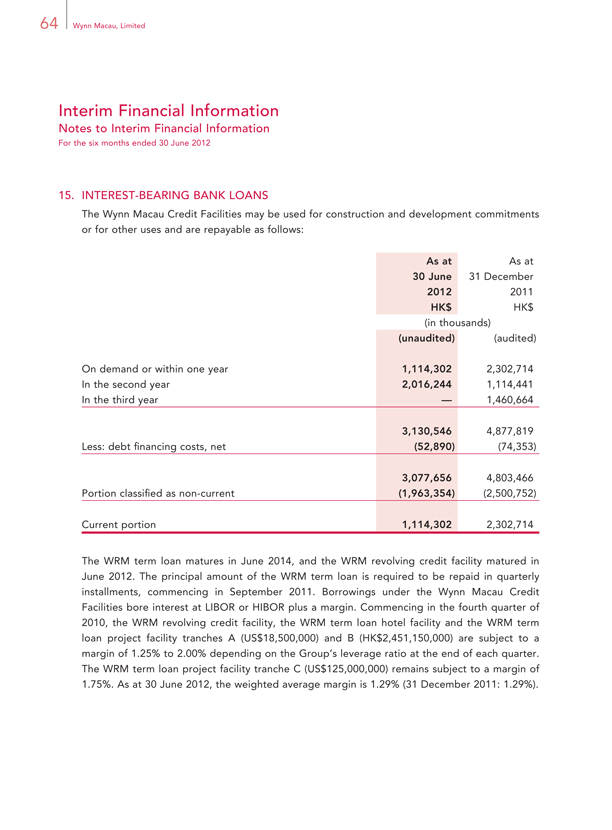

49 Interim Financial Information

79 Definitions

85 Glossary

2 |

| Wynn Macau, Limited |

Corporate Information

BOARD OF DIRECTORS

Executive Directors

Mr. Stephen A. Wynn (Chairman of the Board)

Ms. Linda Chen

Mr. Ian Michael Coughlan

Non-Executive Directors

Mr. Marc D. Schorr

Dr. Allan Zeman, GBM, GBS, JP

(Vice-Chairman of the Board)

Independent Non-Executive Directors

Mr. Jeffrey Kin-fung Lam, GBS, JP Mr. Bruce Rockowitz Mr. Nicholas Sallnow-Smith

AUDIT COMMITTEE

Mr. Nicholas Sallnow-Smith (Chairman) Mr. Bruce Rockowitz Dr. Allan Zeman, GBM, GBS, JP

REMUNERATION COMMITTEE

Mr. Nicholas Sallnow-Smith (Chairman) Mr. Jeffrey Kin-fung Lam, GBS, JP Mr. Bruce Rockowitz Mr. Marc D. Schorr

NOMINATION AND CORPORATE GOVERNANCE COMMITTEE

Mr. Jeffrey Kin-fung Lam, GBS, JP (Chairman) Mr. Nicholas Sallnow-Smith Dr. Allan Zeman, GBM, GBS, JP

COMPANY SECRETARY

Ms. Kwok Yu Ching, FCIS, FCS

AUTHORIZED REPRESENTATIVES

Dr. Allan Zeman, GBM, GBS, JP Ms. Kwok Yu Ching, FCIS, FCS

(Mrs. Seng Sze Ka Mee, Natalia as alternate)

AUDITORS

Ernst & Young

Certified? ed Public Accountants

LEGAL ADVISORS

As to Hong Kong and U.S. laws:

Skadden, Arps, Slate, Meagher & Flom

As to Hong Kong law:

Mayer Brown JSM

As to Macau law:

Dr. Alexandre Correia da Silva

As to Cayman Islands law:

Maples and Calder

Interim Report 2012 3

Corporate Information

REGISTERED OFFICE HONG KONG SHARE REGISTRAR

P.O. Box 309 Computershare Hong Kong Investor

Ugland House Services Limited

Grand Cayman

KY1-1104 STOCK CODE

Cayman Islands 1128

HEADQUARTERS IN MACAU COMPANY WEBSITE

Rua Cidade de Sintra www.wynnmacaulimited.com

NAPE, Macau SAR

PRINCIPAL PLACE OF BUSINESS

IN HONG KONG

Level 28, Three Pacific Place

1 |

| Queen’s Road East |

Hong Kong

PRINCIPAL SHARE REGISTRAR

AND TRANSFER OFFICE

Appleby Trust (Cayman) Limited

4 |

| Wynn Macau, Limited |

Highlights

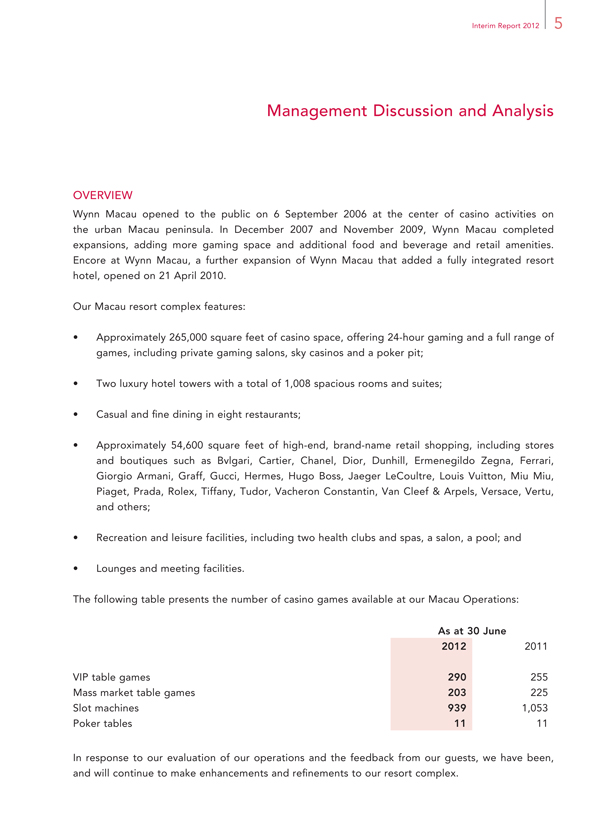

FINANCIAL HIGHLIGHTS

For the Six Months Ended

30 June

2012 2011

HK$ HK$

(in thousands,

except per share amounts

or otherwise stated)

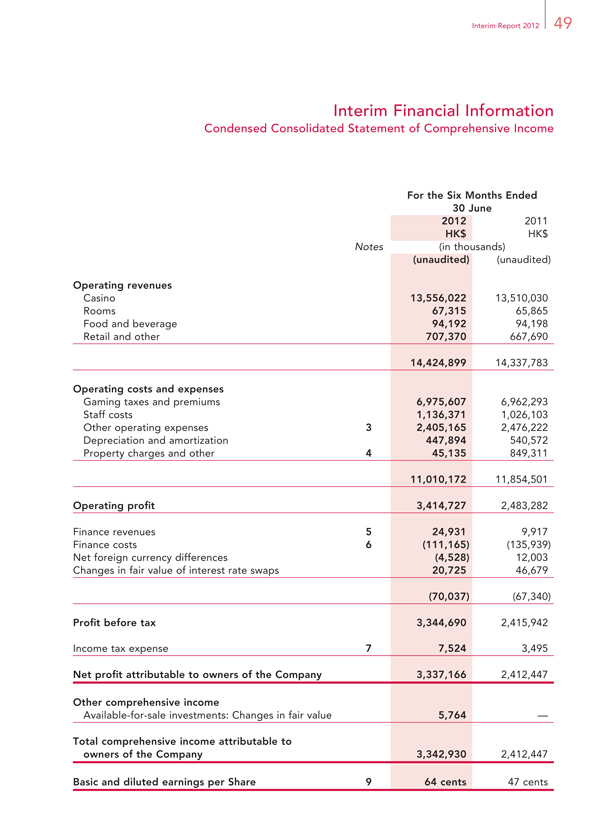

Casino revenues 13,556,022 13,510,030

Other revenues 868,877 827,753

EBITDA 3,932,125 3,909,496

Profit attributable to owners 3,337,166 2,412,447

Earnings per Share — basic and diluted 64 cents 47 cents

Interim Report 2012 5

Management Discussion and Analysis

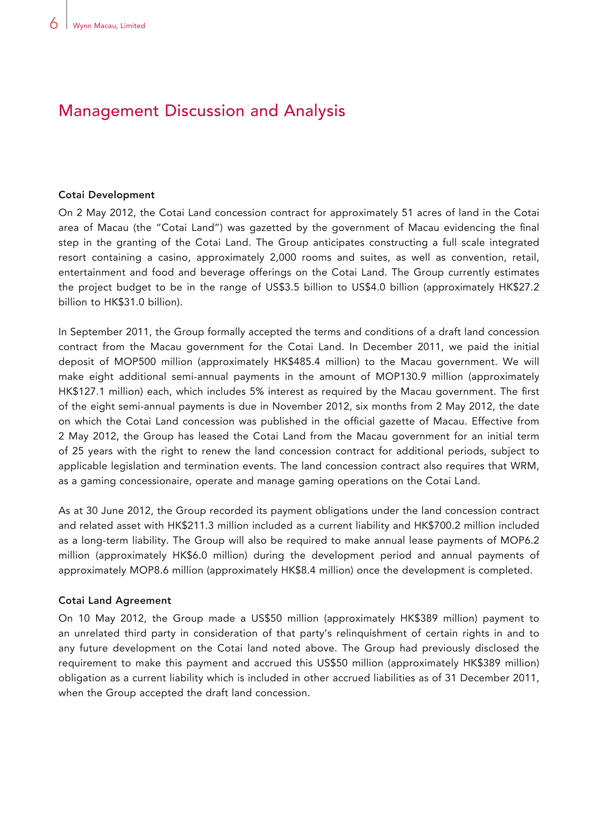

OVERVIEW

Wynn Macau opened to the public on 6 September 2006 at the center of casino activities on the urban Macau peninsula. In December 2007 and November 2009, Wynn Macau completed expansions, adding more gaming space and additional food and beverage and retail amenities. Encore at Wynn Macau, a further expansion of Wynn Macau that added a fully integrated resort hotel, opened on 21 April 2010.

Our Macau resort complex features:

Approximately 265,000 square feet of casino space, offering 24-hour gaming and a full range of games, including private gaming salons, sky casinos and a poker pit;

Two luxury hotel towers with a total of 1,008 spacious rooms and suites;

Casual and fine dining in eight restaurants;

Approximately 54,600 square feet of high-end, brand-name retail shopping, including stores and boutiques such as Bvlgari, Cartier, Chanel, Dior, Dunhill, Ermenegildo Zegna, Ferrari, Giorgio Armani, Graff, Gucci, Hermes, Hugo Boss, Jaeger LeCoultre, Louis Vuitton, Miu Miu, Piaget, Prada, Rolex, Tiffany, Tudor, Vacheron Constantin, Van Cleef & Arpels, Versace, Vertu, and others;

Recreation and leisure facilities, including two health clubs and spas, a salon, a pool; and

Lounges and meeting facilities.

The following table presents the number of casino games available at our Macau Operations:

As at 30 June

2012 2011

VIP table games 290 255

Mass market table games 203 225

Slot machines 939 1,053

Poker tables 11 11

In response to our evaluation of our operations and the feedback from our guests, we have been, and will continue to make enhancements and refinements to our resort complex.

6 |

| Wynn Macau, Limited |

Management Discussion and Analysis

Cotai Development

On 2 May 2012, the Cotai Land concession contract for approximately 51 acres of land in the Cotai area of Macau (the “Cotai Land”) was gazetted by the government of Macau evidencing the final step in the granting of the Cotai Land. The Group anticipates constructing a full scale integrated resort containing a casino, approximately 2,000 rooms and suites, as well as convention, retail, entertainment and food and beverage offerings on the Cotai Land. The Group currently estimates the project budget to be in the range of US$3.5 billion to US$4.0 billion (approximately HK$27.2 billion to HK$31.0 billion).

In September 2011, the Group formally accepted the terms and conditions of a draft land concession contract from the Macau government for the Cotai Land. In December 2011, we paid the initial deposit of MOP500 million (approximately HK$485.4 million) to the Macau government. We will make eight additional semi-annual payments in the amount of MOP130.9 million (approximately HK$127.1 million) each, which includes 5% interest as required by the Macau government. The first of the eight semi-annual payments is due in November 2012, six months from 2 May 2012, the date on which the Cotai Land concession was published in the official gazette of Macau. Effective from

2 May 2012, the Group has leased the Cotai Land from the Macau government for an initial term of 25 years with the right to renew the land concession contract for additional periods, subject to applicable legislation and termination events. The land concession contract also requires that WRM, as a gaming concessionaire, operate and manage gaming operations on the Cotai Land.

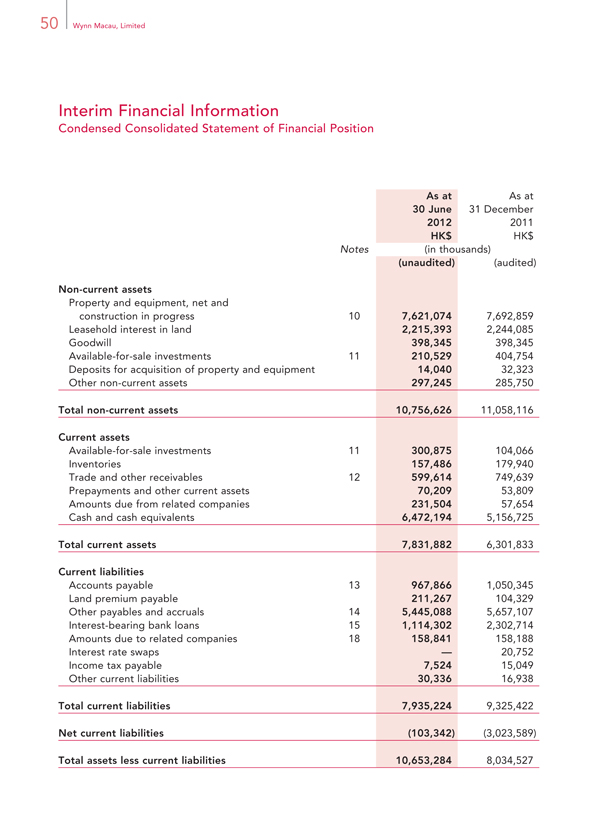

As at 30 June 2012, the Group recorded its payment obligations under the land concession contract and related asset with HK$211.3 million included as a current liability and HK$700.2 million included as a long-term liability. The Group will also be required to make annual lease payments of MOP6.2 million (approximately HK$6.0 million) during the development period and annual payments of approximately MOP8.6 million (approximately HK$8.4 million) once the development is completed.

Cotai Land Agreement

On 10 May 2012, the Group made a US$50 million (approximately HK$389 million) payment to an unrelated third party in consideration of that party’s relinquishment of certain rights in and to any future development on the Cotai land noted above. The Group had previously disclosed the requirement to make this payment and accrued this US$50 million (approximately HK$389 million) obligation as a current liability which is included in other accrued liabilities as of 31 December 2011, when the Group accepted the draft land concession.

Interim Report 2012 7

Management Discussion and Analysis

Macau

Macau, which was a territory under Portuguese administration for approximately 450 years, was transferred from Portuguese to Chinese political control in December 1999. Macau is governed as a special administrative region of China and is located approximately 37 miles southwest of, and approximately one hour away via ferry from, Hong Kong. Macau, which has been a casino destination for more than 40 years, consists principally of a peninsula on mainland China, and two neighboring islands, Taipa and Coloane. We believe that Macau is located in one of the world’s largest concentrations of potential gaming customers. According to Macau statistical information, casinos in Macau generated approximately HK$144.4 billion in gaming revenue during the six months ended

30 June 2012, an increase of approximately 19.8% over the approximate HK$120.5 billion generated in the six months ended 30 June 2011, making Macau the largest gaming market in the world.

Macau’s gaming market is primarily dependent on tourists. Tourist arrivals for the six months ended

30 June 2012 were 13.6 million compared to 13.2 million for the same period last year. The Macau market has experienced tremendous growth in capacity in the last few years. As at 31 May 2012, there were 24,117 hotel rooms and as at 30 June 2012, there were 5,498 table games in Macau, compared to 12,978 hotel rooms and 2,762 table games as at 31 December 2006.

FACTORS AFFECTING OUR RESULTS OF OPERATIONS AND FINANCIAL CONDITION

Tourism

The levels of tourism and overall gaming activities in Macau are key drivers of our business. Both the Macau gaming market and visitation to Macau have grown significantly in the last few years. We have benefited from the rise in visitation to Macau over the past several years.

Gaming customers traveling to Macau typically come from nearby destinations in Asia including mainland China, Hong Kong, Taiwan, South Korea and Singapore. According to the Macau Statistics and Census Service Monthly Bulletin of Statistics, approximately 89.0% of visitors to Macau for the six months ended 30 June 2012 were from mainland China, Hong Kong, and Taiwan.

Tourism levels in Macau are affected by a number of factors, all of which are beyond our control. Key factors affecting tourism levels in Macau may include, among others:

Prevailing economic conditions in mainland China and Asia;

Various countries’ policies on the issuance of travel visas that may be in place from time to time and could affect travel to Macau;

Wynn Macau, Limited 8

Management Discussion and Analysis

Competition from other destinations which offer gaming and leisure activities;

Possible changes to government restrictions on currency conversion or the ability to export currency from mainland China or other countries;

Occurrence of natural disasters and disruption of travel; and

Possible outbreaks of infectious disease.

Economic and Operating Environment

Our operating environment has remained stable during the six months ended 30 June 2012. However, economic conditions can have a significant impact on our business. A number of factors, including a slowdown in the global economy, contracting credit markets, reduced consumer spending, various countries’ policies that affect travel to Macau and any outbreak of infectious diseases can negatively impact the gaming industry in Macau and our business.

Competition

Since the liberalization of Macau’s gaming industry in 2002, there has been a significant increase in the number of casino properties in Macau. Currently, there are six gaming operators in Macau, including WRM. The three concessionaires are WRM, SJM, and Galaxy which opened Galaxy Macau, a major resort in the Cotai area, in May 2011. The three subconcessionaires are Melco Crown, MGM Macau, and Venetian Macau which opened the first phase of Sands Cotai Central, another major resort in the Cotai area, in April 2012. As at 30 June 2012, there were approximately 35 casinos in Macau, including 20 operated by SJM. Each of the current six gaming operators has operating casinos and expansion plans announced or underway.

Wynn Macau also faces competition from casinos primarily located in other areas of Asia, such as Resorts World Sentosa and Marina Bay Sands in Singapore, Genting Highlands Resort located outside of Kuala Lumpur, Malaysia and casinos in the Philippines. Wynn Macau also encounters competition from other major gaming centers located around the world, including Australia and Las Vegas, cruise ships in Asia that offer gaming, and other casinos throughout Asia. Further, if current efforts to legalize gaming in other Asian countries are successful, Wynn Macau will face additional regional competition.

Gaming Promoters

A significant amount of our casino play is brought to us by gaming promoters. Gaming promoters have historically played a critical role in the Macau gaming market and are important to our casino business.

Interim Report 2012 9

Management Discussion and Analysis

Gaming promoters introduce premium VIP players to Wynn Macau and often assist those clients with their travel and entertainment arrangements. In addition, gaming promoters often grant credit to their players. In exchange for their services, Wynn Macau generally pays the gaming promoters a percentage of the gross gaming win generated by each gaming promoter. Approximately 80% of these commissions are netted against casino revenues, because such commissions approximate the amount of the commission returned to the VIP players by the gaming promoters, and approximately 20% of these commissions are included in other operating expenses, which approximate the amount of the commission ultimately retained by the gaming promoters for their compensation. The total amount of commissions paid to these promoters and netted against casino revenues were HK$3.80 billion and HK$3.84 billion for the six months ended 30 June 2012 and 2011, respectively. Commissions decreased 1.2% for the six months ended 30 June 2012 compared to the six months ended 30 June 2011, as VIP gross table games win decreased by 1.1%. We typically advance commissions to gaming promoters at the beginning of each month to facilitate their working capital requirements. These advances are provided to a gaming promoter and are offset by the commissions earned by such gaming promoter during the applicable month. The aggregate amounts of exposure to our gaming promoters, which is the difference between commissions advanced to each individual gaming promoter, and the commissions payable to each such gaming promoter, were HK$626.7 million and HK$361.4 million as at 30 June 2012 and 2011, respectively. Any outstanding commissions are cleared no later than the fifth day of the succeeding month and prior to the advancement of any further funds to a gaming promoter. We believe we have developed strong relationships with our gaming promoters. Our commission percentages have remained stable throughout our operating history.

In addition to commissions, gaming promoters each receive a monthly complimentary allowance based on a percentage of the turnover their clients generate. The allowance is available for room, food and beverage and other products and services for discretionary use with clients.

Premium Credit Play

We selectively extend credit to players contingent upon our marketing team’s knowledge of the players, their financial background and payment history. We follow a series of credit procedures and require from each credit recipient various signed documents that are intended to ensure among other things that, if permitted by applicable law, the debt can be legally enforced in the jurisdiction where the player resides. In the event the player does not reside in a jurisdiction where gaming debts are legally enforceable, we often can assert jurisdiction over assets the player maintains in jurisdictions where gaming debts are recognized. In addition, we typically require a check in the amount of the applicable credit line from credit players, collateralizing the credit we grant to a player.

10 Wynn Macau, Limited

Management Discussion and Analysis

Number and Mix of Table Games and Slot Machines

The mix of VIP table games, mass table games and slot machines in operation at our resort changes from time to time in response to changing market demand and industry competition. The shift in the mix of our games will affect casino profitability.

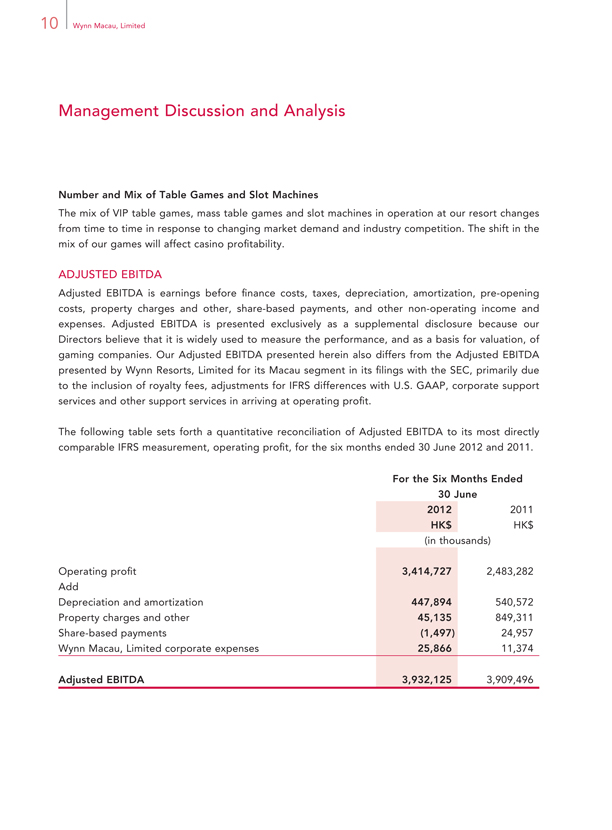

ADJUSTED EBITDA

Adjusted EBITDA is earnings before finance costs, taxes, depreciation, amortization, pre-opening costs, property charges and other, share-based payments, and other non-operating income and expenses. Adjusted EBITDA is presented exclusively as a supplemental disclosure because our Directors believe that it is widely used to measure the performance, and as a basis for valuation, of gaming companies. Our Adjusted EBITDA presented herein also differs from the Adjusted EBITDA presented by Wynn Resorts, Limited for its Macau segment in its Filings with the SEC, primarily due to the inclusion of royalty fees, adjustments for IFRS differences with U.S. GAAP, corporate support services and other support services in arriving at operating profit.

The following table sets forth a quantitative reconciliation of Adjusted EBITDA to its most directly comparable IFRS measurement, operating profit, for the six months ended 30 June 2012 and 2011.

For the Six Months Ended

30 June

2012 2011

HK$ HK$

(in thousands)

Operating profit 3,414,727 2,483,282

Add

Depreciation and amortization 447,894 540,572

Property charges and other 45,135 849,311

Share-based payments (1,497) 24,957

Wynn Macau, Limited corporate expenses 25,866 11,374

Adjusted EBITDA

3,932,125

3,909,496

Interim Report 2012 11

Management Discussion and Analysis

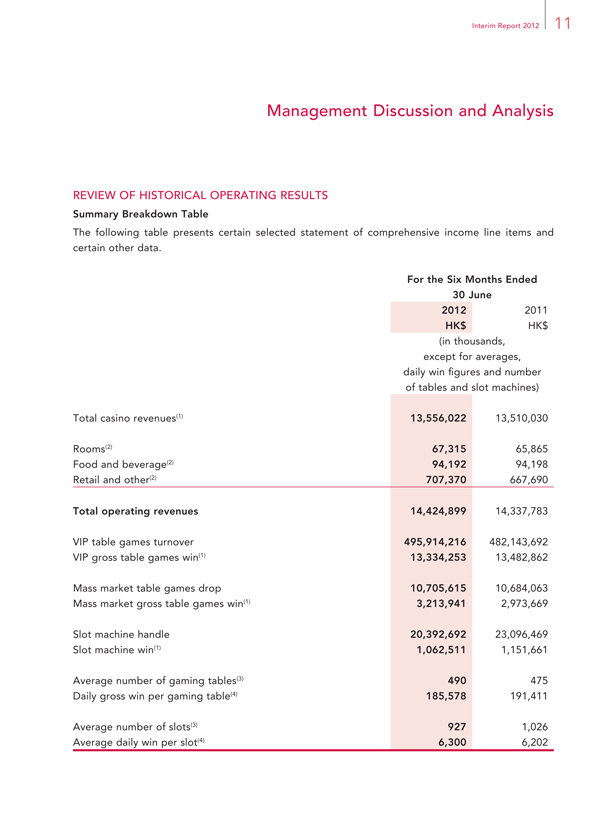

REVIEW OF HISTORICAL OPERATING RESULTS

Summary Breakdown Table

The following table presents certain selected statement of comprehensive income line items and certain other data.

For the Six Months Ended

30 June

2012 2011

HK$ HK$

(in thousands,

except for averages,

daily win figures and number

of tables and slot machines)

Total casino revenues(1) 13,556,022 13,510,030

Rooms(2) 67,315 65,865

Food and beverage(2) 94,192 94,198

Retail and other(2) 707,370 667,690

Total operating revenues 14,424,899 14,337,783

VIP table games turnover 495,914,216 482,143,692

VIP gross table games win(1) 13,334,253 13,482,862

Mass market table games drop 10,705,615 10,684,063

Mass market gross table games win(1) 3,213,941 2,973,669

Slot machine handle 20,392,692 23,096,469

Slot machine win(1) 1,062,511 1,151,661

Average number of gaming tables(3) 490 475

Daily gross win per gaming table(4) 185,578 191,411

Average number of slots(3) 927 1,026

Average daily win per slot(4) 6,300 6,202

12 Wynn Macau, Limited

Management Discussion and Analysis

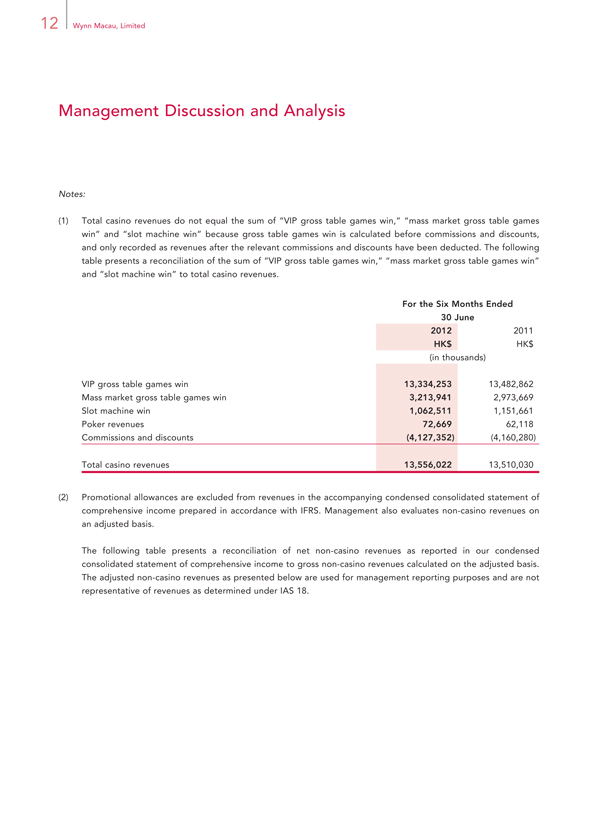

Notes:

(1) Total casino revenues do not equal the sum of “VIP gross table games win,” “mass market gross table games win” and “slot machine win” because gross table games win is calculated before commissions and discounts, and only recorded as revenues after the relevant commissions and discounts have been deducted. The following table presents a reconciliation of the sum of “VIP gross table games win,” “mass market gross table games win” and “slot machine win” to total casino revenues.

For the Six Months Ended

30 June

2012 2011

HK$ HK$

(in thousands)

VIP gross table games win 13,334,253 13,482,862

Mass market gross table games win 3,213,941 2,973,669

Slot machine win 1,062,511 1,151,661

Poker revenues 72,669 62,118

Commissions and discounts (4,127,352) (4,160,280)

Total casino revenues 13,556,022 13,510,030

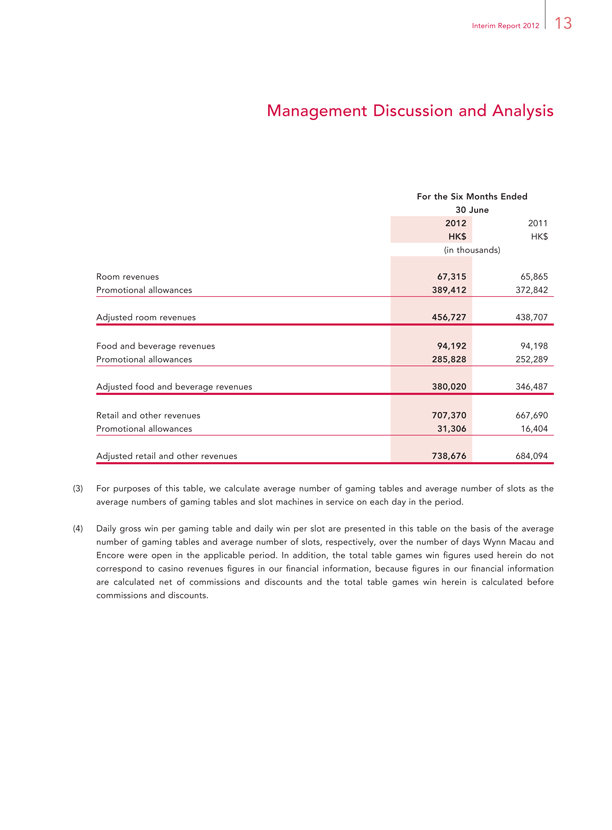

(2)Promotional allowances are excluded from revenues in the accompanying condensed consolidated statement of comprehensive income prepared in accordance with IFRS. Management also evaluates non-casino revenues on an adjusted basis.

The following table presents a reconciliation of net non-casino revenues as reported in our condensed consolidated statement of comprehensive income to gross non-casino revenues calculated on the adjusted basis.

The adjusted non-casino revenues as presented below are used for management reporting purposes and are not representative of revenues as determined under IAS 18.

Interim Report 2012 13

Management Discussion and Analysis

For the Six Months Ended

30 June

2012 2011 HK$ HK$ (in thousands)

Room revenues 67,315 65,865 Promotional allowances 389,412 372,842

Adjusted room revenues 456,727 438,707

Food and beverage revenues 94,192 94,198 Promotional allowances 285,828 252,289

Adjusted food and beverage revenues 380,020 346,487

Retail and other revenues 707,370 667,690 Promotional allowances 31,306 16,404

Adjusted retail and other revenues 738,676 684,094

(3)For purposes of this table, we calculate average number of gaming tables and average number of slots as the average numbers of gaming tables and slot machines in service on each day in the period.

(4)Daily gross win per gaming table and daily win per slot are presented in this table on the basis of the average number of gaming tables and average number of slots, respectively, over the number of days Wynn Macau and Encore were open in the applicable period. In addition, the total table games win figures used herein do not correspond to casino revenues figures in our financial information, because figures in our financial information are calculated net of commissions and discounts and the total table games win herein is calculated before commissions and discounts.

14 Wynn Macau, Limited

Management Discussion and Analysis

Discussion of Results of Operations

Financial results for the six months ended 30 June 2012 compared to financial results for the six months ended 30 June 2011

Operating Revenues

Total operating revenues increased slightly from HK$14.3 billion in the six months ended 30 June 2011 to HK$14.4 billion in the six months ended 30 June 2012.

Casino Revenues

Casino revenues remained basically flat from HK$13.5 billion (94.2% of total operating revenues) in the six months ended 30 June 2011 to HK$13.6 billion (94.0% of total operating revenues) in the six months ended 30 June 2012. The components and reasons are as follows:

VIP casino gaming operations. VIP gross table games win decreased by 1.1%, from HK$13.5 billion in the six months ended 30 June 2011 to HK$13.3 billion in the six months ended 30 June 2012. VIP table games turnover increased by 2.86%, from HK$482.1 billion in the six months ended 30 June 2011 to HK$495.9 billion in the six months ended 30 June 2012. VIP gross table games win as a percentage of turnover (calculated before discounts and commissions) was 2.80% in the six months ended 30 June 2011 compared to 2.69% in the six months ended 30 June 2012, which was below our expected range of 2.7% to 3.0%.

Mass market casino gaming operations. Mass market gross table games win increased by 8.1%, from HK$3.0 billion in the six months ended 30 June 2011 to HK$3.2 billion in the six months ended 30 June 2012. Mass market table games drop remained basically flat, at approximately HK$10.7 billion in both the six months ended 30 June 2012 and 2011. The mass market gross table games win percentage (calculated before discounts) was 27.8% in the six months ended 30 June 2011 compared to 30.0% in the six months ended 30 June 2012, which was higher the expected win percentage range of 26% to 28%.

Slot machine gaming operations. Slot machine win decreased by 7.7% from HK$1.2 billion in the six months ended 30 June 2011 to HK$1.1 billion in the six months ended 30 June 2012. Slot machine handle decreased by 11.7%, from HK$23.1 billion in the six months ended 30 June 2011 to HK$20.4 billion in the six months ended 30 June 2012. Slot machine win and slot machine handle decreased primarily due to increased competition in the premium slot segment. In addition, we removed 99 machines from the gaming floor during the six months ended 30 June 2012. As a result of the decrease in

slot machine count, slot machine win per unit per day increased 1.6% from HK$6,202 in the six months ended 30 June 2011 to HK$6,300 in the six months ended 30 June 2012.

Interim Report 2012 15

Management Discussion and Analysis

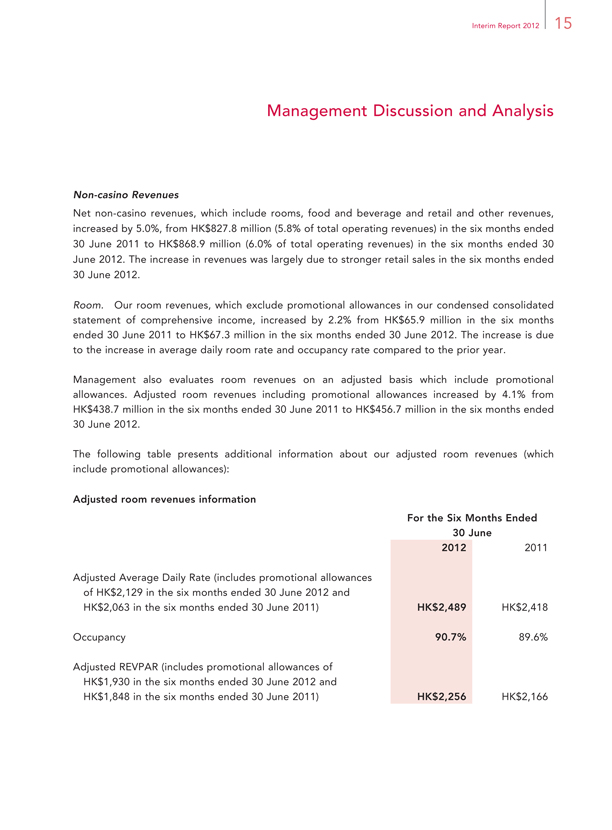

Non-casino Revenues

Net non-casino revenues, which include rooms, food and beverage and retail and other revenues, increased by 5.0%, from HK$827.8 million (5.8% of total operating revenues) in the six months ended

30 June 2011 to HK$868.9 million (6.0% of total operating revenues) in the six months ended 30 June 2012. The increase in revenues was largely due to stronger retail sales in the six months ended

30 June 2012.

Room. Our room revenues, which exclude promotional allowances in our condensed consolidated statement of comprehensive income, increased by 2.2% from HK$65.9 million in the six months ended 30 June 2011 to HK$67.3 million in the six months ended 30 June 2012. The increase is due to the increase in average daily room rate and occupancy rate compared to the prior year.

Management also evaluates room revenues on an adjusted basis which include promotional allowances. Adjusted room revenues including promotional allowances increased by 4.1% from HK$438.7 million in the six months ended 30 June 2011 to HK$456.7 million in the six months ended

30 June 2012.

The following table presents additional information about our adjusted room revenues (which include promotional allowances):

Adjusted room revenues information

For the Six Months Ended

30 June

2012 2011

Adjusted Average Daily Rate (includes promotional allowances

of HK$2,129 in the six months ended 30 June 2012 and

HK$2,063 in the six months ended 30 June 2011) HK$2,489 HK$2,418

Occupancy 90.7% 89.6%

Adjusted REVPAR (includes promotional allowances of

HK$1,930 in the six months ended 30 June 2012 and

HK$1,848 in the six months ended 30 June 2011) HK$2,256 HK$2,166

16 Wynn Macau, Limited

Management Discussion and Analysis

Food and beverage. Food and beverage revenues, which exclude promotional allowances in our condensed consolidated statement of comprehensive income, totaled HK$94.2 million in the six months ended 30 June 2012, which was approximately the same as the six months ended 30 June 2011.

Management also evaluates food and beverage revenues on an adjusted basis including promotional allowances. Food and beverage revenues in the six months ended 30 June 2012, adjusted to include these promotional allowances were HK$380.0 million, a 9.7% increase from the six months ended

30 June 2011 adjusted revenues of HK$346.5 million. A higher portion of our food and beverage services were provided on a complimentary basis in the six months ended 30 June 2012 compared to

30 June 2011 to meet demand from our VIP clients and high-limit mass market customers.

Retail and other. Our retail and other revenues, which exclude promotional allowances in our condensed consolidated statement of comprehensive income, increased by 5.9%, from HK$667.7 million in the six months ended 30 June 2011 to HK$707.4 million in the six months ended 30 June 2012. The increase was due primarily to strong same store sales growth and the addition of new outlets.

Management also evaluates retail and other revenues on an adjusted basis which includes promotional allowances. Adjusted retail and other revenues including promotional allowances increased by 8.0% from HK$684.1 million in the six months ended 30 June 2011 to HK$738.7 million in the six months ended 30 June 2012, reflecting the strong same store sales growth and the addition of new outlets.

Operating Costs and Expenses

Gaming taxes and premiums. Gaming taxes and premiums of HK$7.0 billion in the six months ended 30 June 2012 was approximately the same as the six months ended 30 June 2011 as gross gaming win remained fl at during the six months ended 30 June 2012 compared to the six months ended 30 June 2011. WRM is subject to a 35% gaming tax on gross gaming win. In addition, WRM is required to pay 4% of its gross gaming win as contributions for public development and social facilities.

Staff costs. Staff costs increased by 10.7%, from HK$1.0 billion in the six months ended 30 June 2011 to HK$1.1 billion in the six months ended 30 June 2012. This increase in staff costs is primarily due to general salary increases and an increase in the number of full-time equivalents needed to service our customers.

Interim Report 2012 17

Management Discussion and Analysis

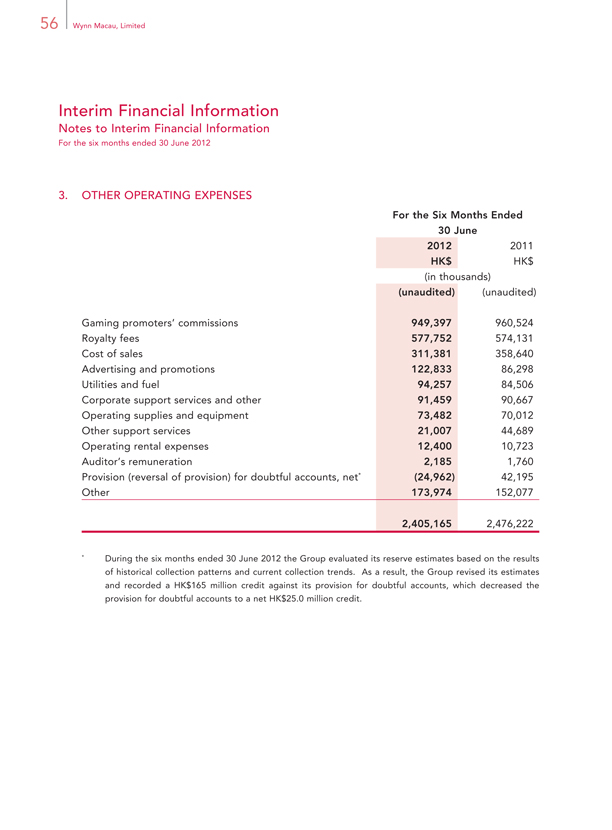

Other operating expenses. Other operating expenses decreased by 2.9% from HK$2.5 billion in the six months ended 30 June 2011 to HK$2.4 billion in the six months ended 30 June 2012, due primarily to a change in the estimate on doubtful accounts receivable. During the six months ended

30 June 2012 the Group evaluated its reserve estimates based on the results of historical collection patterns and current collection trends. As a result, the Group revised its estimates and recorded a HK$165 million credit against its provision for doubtful accounts, which decreased the provision for doubtful accounts to a net HK$25.0 million credit.

Depreciation and amortization. Depreciation and amortization decreased by 17.1% from HK$540.6 million in the six months ended 30 June 2011 to HK$447.9 million in the six months ended 30 June 2012. This decrease is primarily due to assets with a five year life being fully depreciated as of September 2011.

Property charges and other. Property charges and other decreased from HK$849.3 million in the six months ended 30 June 2011 to HK$45.1 million in the six months ended 30 June 2012. Included in property charges and other for the six months ended 30 June 2011 is a charge of HK$831.1 million reflecting the present value of a charitable contribution made by WRM to the University of Macau Development Foundation. This contribution consists of a MOP200.0 million (approximately HK$194.2 million) payment made in May 2011, and a commitment for additional donations of MOP80.0 million (approximately HK$77.7 million) each year for the calendar years 2012 through 2022 inclusive, for a total of MOP1,080.0 million (approximately HK$1,048.5 million). The amount reflected in our accompanying condensed consolidated statement of comprehensive income has been discounted using our current estimated borrowing rate over the time period of the remaining committed payments. Other charges in each period represent gain/loss on the sale of equipment as well as costs related to assets retired or abandoned as a result of renovating certain assets of Wynn Macau in response to customer preferences and changes in market demand.

As a result of the foregoing, total operating costs and expenses decreased by 7.1%, from HK$11.9 billion in the six months ended 30 June 2011 to HK$11.0 billion in the six months ended 30 June 2012.

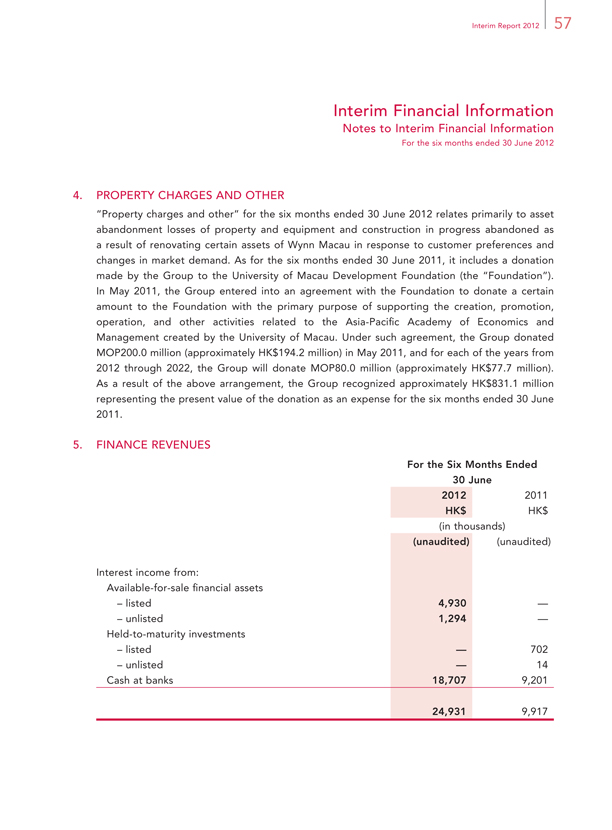

Finance Revenues

Finance revenues increased from HK$9.9 million in the six months ended 30 June 2011 to HK$24.9 million in the six months ended 30 June 2012. During 2012 and 2011, our short-term investment strategy has been to preserve capital while retaining sufficient liquidity. While we have recently invested in certain corporate debt securities which contributed to the increase in interest income, the majority of our short-term investments are primarily in time deposits with a maturity of three months or less.

18 Wynn Macau, Limited

Management Discussion and Analysis

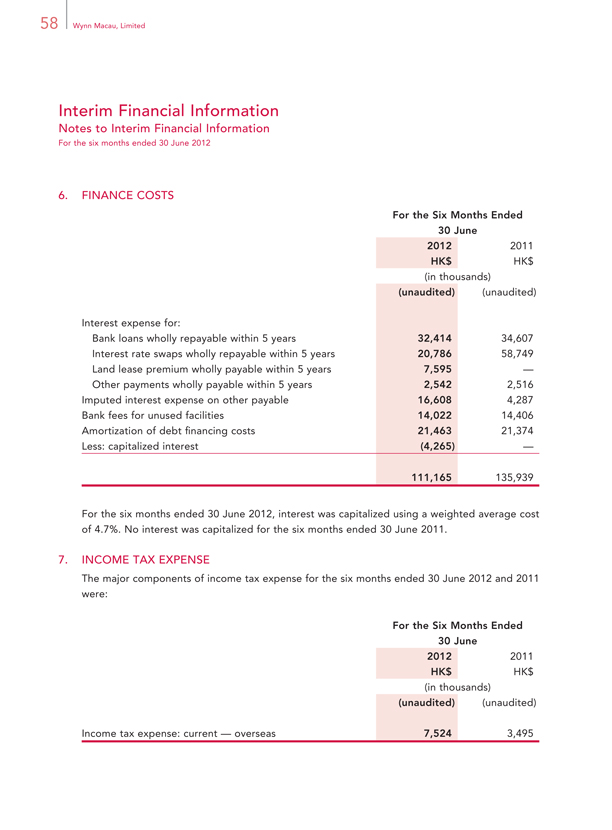

Finance Costs

Finance costs decreased by 18.2%, from HK$135.9 million in the six months ended 30 June 2011 to HK$111.2 million in the six months ended 30 June 2012. Finance costs decreased in the six months ended 30 June 2012 primarily due to the maturity of two interest rate swap agreements in August 2011 which resulted in a higher interest rate. This decrease as well as the increase in capitalized interest was partially offset by the increase in finance cost for the land concession and the charitable contribution payable to the University of Macau Development Foundation for the six months ended

30 June 2012.

Interest Rate Swaps

As required under the terms of the Wynn Macau Credit Facilities, we entered into agreements to swap a portion of the interest on our loans from floating to fixed rates. These transactions did not qualify for hedge accounting.

Changes in the fair value of our interest rate swaps are recorded as an increase or decrease in swap fair value during each period. We recorded a gain of HK$20.7 million for the six months ended 30 June 2012 resulting from the increase in the fair value of our interest rate swaps in the six months ended 30 June 2012. In June 2012, our interest rate swap matured and as of 30 June 2012, we had no outstanding interest rate swaps. We recorded a gain of HK$46.7 million in the six months ended

30 June 2011 resulting from the increase in the fair value of our interest rate swaps in the six months ended 30 June 2011.

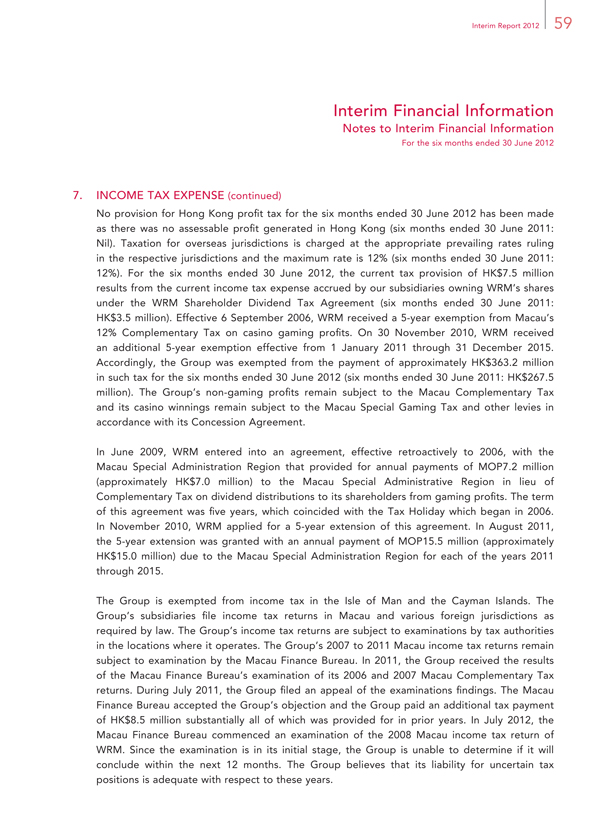

Income Tax Expense

For the six months ended 30 June 2012, our income tax expense was HK$7.5 million compared to an income tax expense of HK$3.5 million in the six months ended 30 June 2011. Our current tax expense for the six months ended 30 June 2012 and 2011 primarily relates to the current tax expense of our subsidiaries owning WRM’s shares under the WRM Shareholder Dividend Tax Agreement.

Interim Report 2012 19

Management Discussion and Analysis

Net Profit Attributable to Owners of the Company

As a result of the foregoing, net profit attributable to owners of the Company increased by 38.3%, from HK$2.4 billion in the six months ended 30 June 2011 to HK$3.3 billion in the six months ended

30 June 2012.

LIQUIDITY AND CAPITAL RESOURCES

Capital Resources

Since Wynn Macau opened in 2006, we have generally funded our working capital and recurring expenses as well as capital expenditures from cash flow from operations and cash on hand.

Our cash balances as at 30 June 2012 were HK$6.5 billion. Such cash is available for operations, new development activities, enhancements to Wynn Macau and Encore and general corporate purposes. On 27 June 2012, the WRM revolving credit facility matured with no outstanding balance. On 31 July 2012, WRM expanded its availability under the senior secured bank facility to US$2.3 billion (approximately HK$17.9 billion) equivalent consisting of a US$750 million (approximately HK$5.8 billion) equivalent fully funded senior secured term loan facility and a US$1.55 billion (approximately HK$12.1 billion) equivalent senior secured revolving credit facility. WRM also has the ability to upsize the total senior secured facilities by an additional US$200 million (approximately HK$1.6 billion) pursuant to the terms and provisions of the Amended Wynn Macau Credit Facilities. Borrowings under the Amended Wynn Macau Credit Facilities will be used to refinance WRM’s existing indebtedness, to fund the design, development, construction and pre-opening expenses of Wynn Cotai and for general corporate purposes.

Investments

As at 30 June 2012, the Group had net investments in Offshore RMB denominated debt securities with maturities of up to two years that amounted to Offshore RMB419.4 million (approximately HK$511.4 million) compared to RMB415.6 million (approximately HK$508.8 million) as at 31 December 2011.

20 Wynn Macau, Limited

Management Discussion and Analysis

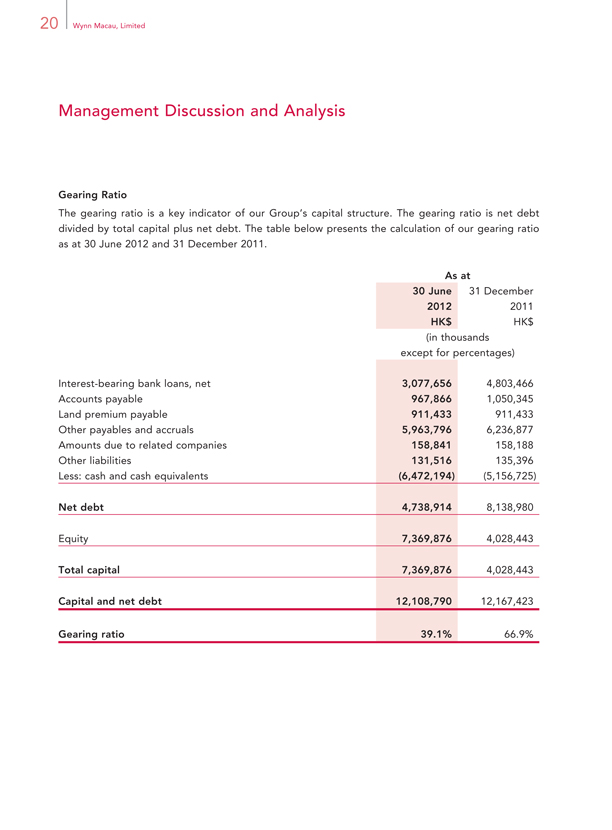

Gearing Ratio

The gearing ratio is a key indicator of our Group’s capital structure. The gearing ratio is net debt divided by total capital plus net debt. The table below presents the calculation of our gearing ratio as at 30 June 2012 and 31 December 2011.

As at

30 June 31 December

2012 2011

HK$ HK$

(in thousands

except for percentages)

Interest-bearing bank loans, net 3,077,656 4,803,466

Accounts payable 967,866 1,050,345

Land premium payable 911,433 911,433

Other payables and accruals 5,963,796 6,236,877

Amounts due to related companies 158,841 158,188

Other liabilities 131,516 135,396

Less: cash and cash equivalents (6,472,194) (5,156,725)

Net debt 4,738,914 8,138,980

Equity 7,369,876 4,028,443

Total capital 7,369,876 4,028,443

Capital and net debt 12,108,790 12,167,423

Gearing ratio 39.1% 66.9%

Interim Report 2012 21

Management Discussion and Analysis

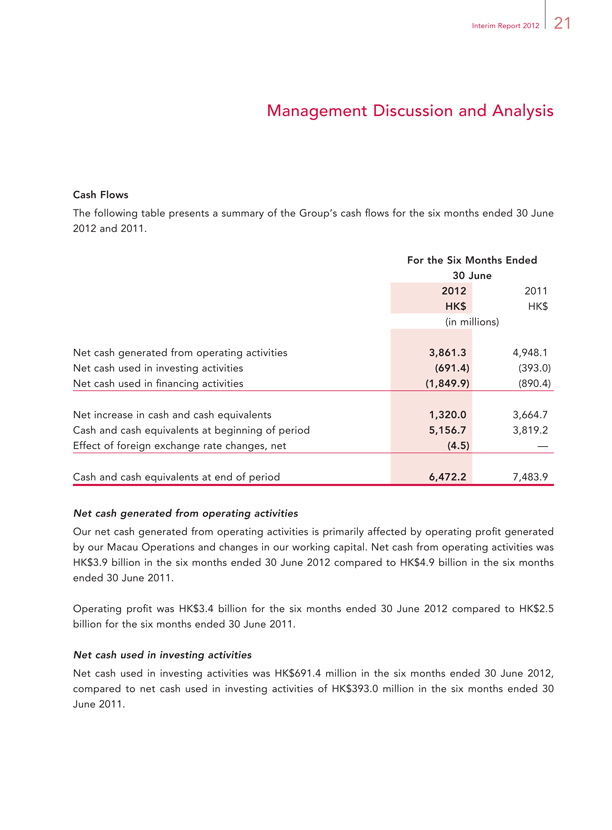

Cash Flows

The following table presents a summary of the Group’s cash flows for the six months ended 30 June 2012 and 2011.

For the Six Months Ended

30 June

2012 2011

HK$ HK$

(in millions)

Net cash generated from operating activities 3,861.3 4,948.1

Net cash used in investing activities (691.4) (393.0)

Net cash used in financing activities (1,849.9) (890.4)

Net increase in cash and cash equivalents 1,320.0 3,664.7

Cash and cash equivalents at beginning of period 5,156.7 3,819.2

Effect of foreign exchange rate changes, net (4.5) —

Cash and cash equivalents at end of period 6,472.2 7,483.9

Net cash generated from operating activities

Our net cash generated from operating activities is primarily affected by operating profit generated by our Macau Operations and changes in our working capital. Net cash from operating activities was HK$3.9 billion in the six months ended 30 June 2012 compared to HK$4.9 billion in the six months ended 30 June 2011.

Operating profit was HK$3.4 billion for the six months ended 30 June 2012 compared to HK$2.5 billion for the six months ended 30 June 2011.

Net cash used in investing activities

Net cash used in investing activities was HK$691.4 million in the six months ended 30 June 2012, compared to net cash used in investing activities of HK$393.0 million in the six months ended 30 June 2011.

22 Wynn Macau, Limited

Management Discussion and Analysis

Capital expenditures were HK$323.1 million for the six months ended 30 June 2012, and related primarily to renovation projects to enhance and refine the Macau Operations and land improvement costs for Cotai. Capital expenditures for the six months ended 30 June 2011 were HK$141.0 million and related primarily to renovation projects to enhance and refine the Macau Operations. Also during the six months ended 30 June 2012, the Group made a HK$389.0 million payment to an unrelated third party in consideration of that party’s relinquishment of certain rights in and to any future development of the Cotai Land.

Net cash used in financing activities

Net cash used in financing activities was HK$1.8 billion during the six months ended 30 June 2012 compared to HK$890.4 million during the six months ended 30 June 2011.

The difference between net cash flow used in the six months ended 30 June 2012 compared to the six months ended 30 June 2011 is primarily due to a HK$779.5 million repayment of the senior revolving credit facility under the Wynn Macau Credit Facilities made in the six months ended 30 June 2011 compared to a HK$1.7 billion repayment of the Wynn Macau Credit Facilities made in the six months ended 30 June 2012.

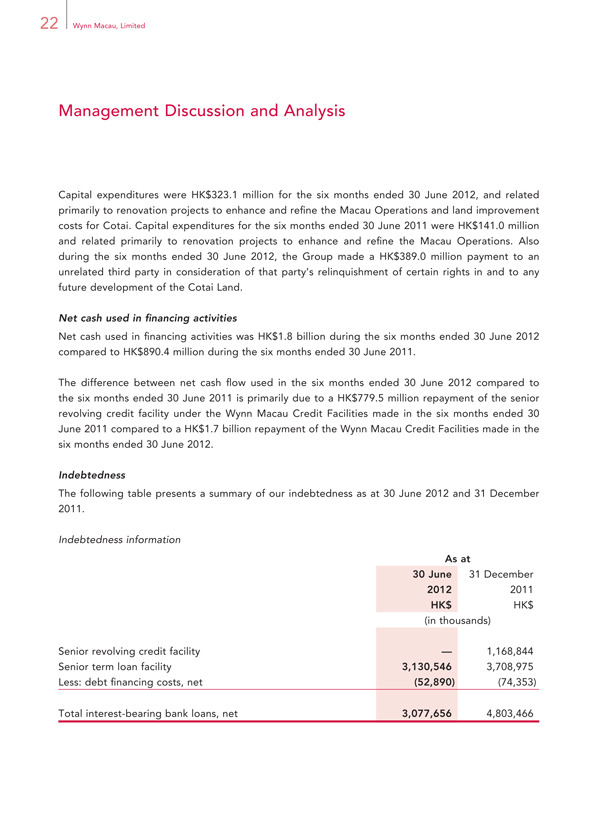

Indebtedness

The following table presents a summary of our indebtedness as at 30 June 2012 and 31 December 2011.

Indebtedness information

As at

30 June 31 December

2012 2011

HK$ HK$

(in thousands)

Senior revolving credit facility — 1,168,844

Senior term loan facility 3,130,546 3,708,975

Less: debt financing costs, net (52,890) (74,353)

Total interest-bearing bank loans, net

3,077,656

4,803,466

Interim Report 2012 23

Management Discussion and Analysis

Wynn Macau Credit Facilities

Overview

As at 30 June 2012, WRM’s credit facility consisted of a HK$4.3 billion fully funded senior term loan in a combination of Hong Kong dollar and U.S. dollar. The facility was permitted to be used for a variety of purposes, including further enhancements at our resort, investments in other projects in Macau and general corporate purposes. On 27 June 2012, WRM’s HK$7.7 billion senior revolving credit facility in a combination of Hong Kong and U.S. dollars matured with no outstanding balance (see “Recent Developments” section below for details of the Amended Wynn Macau Credit Facilities).

As at 30 June 2012, we had total bank and other borrowings under the previously in place Wynn Macau Credit Facilities of HK$3.1 billion, of which HK$1.1 billion was denominated in U.S. dollars and HK$2.0 billion was denominated in Hong Kong dollars.

The term loans under the previously in place Wynn Macau Credit Facilities were due to mature in June 2014, but were refinanced as part of the Amended Wynn Macau Credit Facilities. The revolving loans under the Wynn Macau Credit Facilities matured in June 2012.

Security and Guarantees

Collateral for the previously in place Wynn Macau Credit Facilities consisted of substantially all of the assets of WRM. Certain of our direct and indirect subsidiaries have executed guarantees and pledged their interests in WRM in support of the obligations under the Wynn Macau Credit Facilities. With respect to the Concession Agreement, the WRM lenders had certain cure rights and consultation rights with the Macau government upon an enforcement by the lenders.

Second Ranking Lender

WRM is also party to a bank guarantee reimbursement agreement with Banco National Ultramarino S.A. to secure a guarantee in favor of the Macau government as required under the Concession Agreement. The amount of this guarantee is MOP300 million (approximately HK$291.3 million) and it lasts until 180 days after the end of the term of the Concession Agreement. The guarantee assures WRM’s performance under the Concession Agreement, including the payment of certain premiums, fines and indemnities for breach. The guarantee is secured by a second priority security interest in the same collateral package securing the Wynn Macau Credit Facilities. This bank guarantee reimbursement agreement remains in place with the Amended Wynn Macau Credit Facilities.

Other Terms

The previously in place Wynn Macau Credit Facilities contained covenants, terms, restrictions and events of default customary for casino development financings in Macau.

24 Wynn Macau, Limited

Management Discussion and Analysis

Recent developments

On 31 July 2012, WRM entered into the Amended Wynn Macau Credit Facilities and appointed Bank of China Limited, Macau Branch as facilities agent, intercreditor agent and security agent. The Amended Wynn Macau Credit Facilities and related agreements took effect on 31 July 2012 and expand availability under WRM’s senior bank facility to US$2.3 billion equivalent (approximately HK$17.9 billion), consisting of a US$750 million equivalent (approximately HK$5.8 billion) fully funded senior term loan facility and a US$1.55 billion equivalent (approximately HK$12.1 billion) senior revolving credit facility. There is also an option to upsize the total senior secured facilities by an additional US$200 million (approximately HK$1.6 billion) under the Amended Wynn Macau Credit Facilities.

Borrowings under the Amended Wynn Macau Credit Facilities, which consist of both Hong Kong dollar and United States dollar tranches, will be used to refinance WRM’s existing indebtedness, to fund the design, development, construction and pre-opening expenses of Wynn Cotai and for general corporate purposes.

The term loan facility matures in July 2018 with the principal amount of the term loan to be repaid in two equal installments in July 2017 and July 2018. The final maturity for the revolving credit facility is July 2017, by which date any outstanding revolving loans must be repaid. The senior secured facilities will bear interest for the first six months after closing at LIBOR or HIBOR plus a margin of

2.50% and thereafter will be subject to LIBOR or HIBOR plus a margin of between 1.75% to 2.50% based on WRM’s leverage ratio.

Customary fees and expenses were paid by WRM in connection with the Amended Wynn Macau Credit Facilities.

Borrowings under the Amended Wynn Macau Credit Facilities are guaranteed by Palo and by certain subsidiaries of the Company that own equity interests in WRM, and are secured by substantially all of the assets of WRM, the equity interests in WRM and, subject to certain post-closing matters, substantially all of the assets of Palo.

The Amended Wynn Macau Credit Facilities contains representations, warranties, covenants and events of default customary for casino development financings in Macau.

The Directors confirm that there is no non-compliance with the financial covenants or general covenants contained in the Amended Wynn Macau Credit Facilities.

The Company is not a party to the credit facilities agreement and related agreements and has no rights or obligations thereunder.

Interim Report 2012 25

Management Discussion and Analysis

QUANTITATIVE AND QUALITATIVE DISCLOSURE ABOUT MARKET RISK

Market risk is the risk of loss arising from adverse changes in market rates and conditions, such as inflation, interest rates, and foreign currency exchange rates.

Foreign Exchange Risks

The financial statements of foreign operations are translated into Hong Kong dollars, the Group’s functional and presentation currency, for incorporation into the condensed consolidated financial information. The majority of our assets and liabilities are denominated in U.S. dollars, Hong Kong dollars, Macau patacas and Offshore RMB, and there are no significant assets and liabilities denominated in other currencies. Assets and liabilities are translated at the prevailing foreign exchange rates in effect at the end of the reporting period. Income, expenditures and cash flow items are measured at the actual foreign exchange rates or average foreign exchange rates for the period. The Hong Kong dollar is linked to the U.S. dollar and the exchange rate between these two currencies has remained relatively stable over the past several years. The Macau pataca is pegged to the Hong Kong dollar, and in many cases the two currencies are used interchangeably in Macau. However, the exchange linkages of the Hong Kong dollar and the Macau pataca, and the Hong Kong dollar to the U.S. dollar, are subject to potential changes due to, among other things, changes in governmental policies and international economic and political developments. In particular, our Group is exposed to foreign exchange risk arising primarily with respect to the Offshore RMB, which does not have pegged exchange linkages to the U.S. dollar, Hong Kong dollar or Macau pataca.

Interest Rate Risks

One of our primary exposures to market risk is interest rate risk associated with our credit facilities, which bear interest based on floating rates. We attempt to manage interest rate risk by managing the mix of long-term fixed rate borrowings and variable rate borrowings supplemented by hedging activities as considered necessary. We cannot assure you that these risk management strategies will have the desired effect, and interest rate fluctuations could have a negative impact on our results of operations.

The Group had one interest rate swap agreement to manage a portion of the underlying interest rate risk on borrowings under the Wynn Macau Credit Facilities which matured in June 2012.

Under this swap agreement, the Group paid a fixed interest rate of 2.15% on borrowings of approximately HK$2.3 billion incurred under the Wynn Macau Credit Facilities in exchange for receipts on the same amount at a variable interest rate based on the applicable HIBOR at the time of payment. This interest rate swap agreement fixed the interest rate on such borrowings at 3.4%.

26 Wynn Macau, Limited

Management Discussion and Analysis

The carrying values of these interest rate swaps on the condensed consolidated statement of financial position approximated their fair values. The fair value approximated the amount the Group would pay if these contracts were settled at the respective valuation dates. Fair value was estimated based upon current, and predictions of future interest rate levels along a yield curve, the remaining duration of the instruments and other market conditions and, therefore, was subject to significant estimation and a high degree of variability of fluctuation between periods. We adjusted this amount by applying a non-performance valuation, considering our creditworthiness or the creditworthiness of our counterparties at each settlement date, as applicable. These transactions did not qualify for hedge accounting. Accordingly, changes in the fair values during the six months ended 30 June 2012 and 2011, were charged to the condensed consolidated statement of comprehensive income.

OFF BALANCE SHEET ARRANGEMENTS

We have not entered into any transactions with special purpose entities nor do we engage in any transactions involving derivatives except for interest rate swaps. We do not have any retained or contingent interest in assets transferred to an unconsolidated entity.

OTHER LIQUIDITY MATTERS

We expect to fund our operations and capital expenditure requirements from operating cash flows, cash on hand and availability under the Amended Wynn Macau Credit Facilities. However, we cannot be sure that operating cash flows will be sufficient for those purposes. We may refinance all or a portion of our indebtedness on or before maturity. We cannot be sure that we will be able to refinance any of the indebtedness on acceptable terms or at all.

New business developments (including our development of Wynn Cotai) or other unforeseen events may occur, resulting in the need to raise additional funds. There can be no assurances regarding the business prospects with respect to any other opportunity. Any other development would require us to obtain additional financing.

In the ordinary course of business, in response to market demands and client preferences, and in order to increase revenues, we have made and will continue to make enhancements and refinements to our resort. We have incurred and will continue to incur capital expenditures related to these enhancements and refinements.

Taking into consideration our financial resources, including our cash and cash equivalents, internally generated funds and availability under the Amended Wynn Macau Credit Facilities, we believe that we have sufficient liquid assets to meet our working capital and operating requirements for the following 12 months.

Interim Report 2012 27

Management Discussion and Analysis

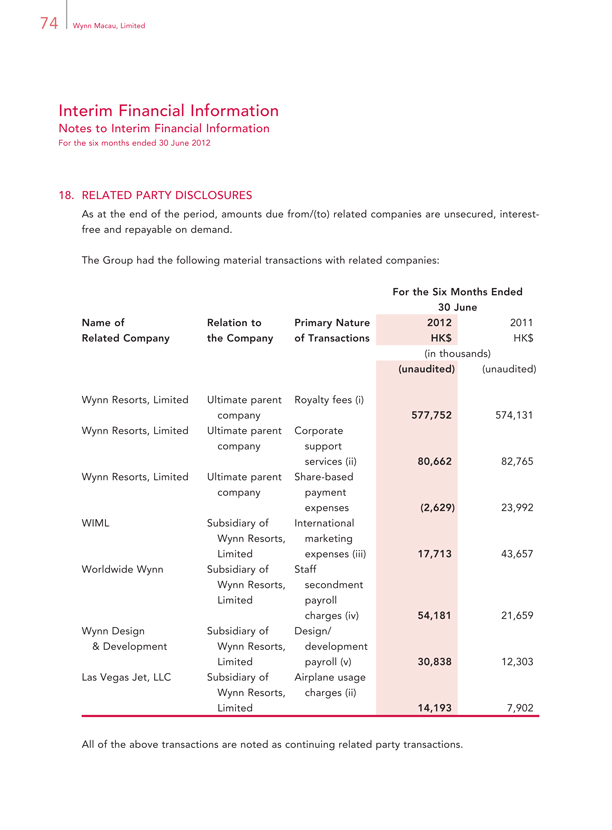

RELATED PARTY TRANSACTIONS

For details of the related party transactions, see note 18 to the Interim Financial Information. Our Directors confirm that all related party transactions are conducted on normal commercial terms, and that their terms are fair and reasonable.

28 Wynn Macau, Limited

Directors and Senior Management

OUR DIRECTORS

The following table presents certain information in respect of the members of our Board.

Members of our Board

Name Age Position Date of Appointment

Stephen A. Wynn 70 Chairman of the Board, 16 September 2009

Executive Director,

Chief Executive Officer

and President

Linda Chen 45 Executive Director and 16 September 2009

Chief Operating Officer

Ian Michael Coughlan 53 Executive Director 16 September 2009

Marc D. Schorr 64 Non-executive Director 16 September 2009

Allan Zeman, GBM, GBS, JP 64 Vice-chairman of the Board 16 September 2009

and Non-executive Director

Jeffrey Kin-fung Lam, GBS, JP 60 Independent 16 September 2009

Non-executive Director

Bruce Rockowitz 53 Independent 16 September 2009

Non-executive Director

Nicholas Sallnow-Smith 62 Independent 16 September 2009

Non-executive Director

The biography of each Director during the six months ended 30 June 2012 is set out below:

Executive Directors

Mr. Stephen A. Wynn, aged 70, has been a Director of the Company since its inception and an executive Director, the Chairman of the Board of Directors, Chief Executive officer and President of the Company since 16 September 2009. Mr. Wynn has served as Director, Chairman and Chief Executive Officer of WRM since October 2001. Mr. Wynn has also served as Chairman and Chief Executive Officer of Wynn Resorts, Limited since June 2002. Mr. Wynn has over 40 years of experience in the gaming casino industry. From April 2000 to September 2002, Mr. Wynn was the managing member of Valvino Lamore, LLC, the predecessor and a current wholly owned subsidiary of Wynn Resorts, Limited. Mr. Wynn also serves as an officer and/or director of several subsidiaries

Interim Report 2012 29

Directors and Senior Management

of Wynn Resorts, Limited. Mr. Wynn served as Chairman, President and Chief Executive Officer of Mirage Resorts, Inc. and its predecessor, Golden Nugget Inc., between 1973 and 2000. Mr. Wynn developed and opened The Mirage, Treasure Island and Bellagio in 1989, 1993 and 1998, respectively. In 2011, Barron’s ranked Mr. Wynn as one of the world’s 30 best CEOs.

Ms. Linda Chen, aged 45, has been an executive Director and the Chief Operating officer of the Company since 16 September 2009 and Chief Operating Officer of WRM since June 2002. Ms. Chen is responsible for the marketing and strategic development of WRM. Ms. Chen is also a director of Wynn Resorts, Limited and President of WIML. In these positions, she is responsible for the setup of international marketing operations of Wynn Resorts, Limited. Prior to joining the Group, Ms. Chen was Executive Vice President — International Marketing at MGM Mirage, a role she held from June 2000 until May 2002, and was responsible for the international marketing operations for MGM Grand, Bellagio and The Mirage. Prior to this position, Ms. Chen served as the Executive Vice President of International Marketing for Bellagio and was involved with its opening in 1998. She was also involved in the opening of the MGM Grand in 1993 and The Mirage in 1989. Ms. Chen is also a member of the Nanjing Committee of the Chinese People’s Political Consultative Conference (Macau). Ms. Chen holds a Bachelor of Science Degree in Hotel Administration from Cornell University in 1989 and completed the Stanford Graduate School of Business Executive Development Program in 1997.

Mr. Ian Michael Coughlan, aged 53, has been an executive Director of the Company since 16 September 2009. Mr. Coughlan is also the President of WRM, a position he has held since July 2007. In this role, he is responsible for the entire operation and development of Wynn Macau. Prior to this role, Mr. Coughlan was Director of Hotel Operations — Worldwide for Wynn Resorts, Limited. Mr. Coughlan has over 30 years of hospitality experience with leading hotels across Asia, Europe and the United States. Before joining Wynn Resorts, Limited, he spent ten years with The Peninsula Group, including posts as General Manager of The Peninsula Hong Kong from September 2004 to January 2007, and General Manager of The Peninsula Bangkok from September 1999 to August 2004. His previous assignments include senior management positions at The Oriental Singapore, and a number of Ritz-Carlton properties in the United States. Mr. Coughlan holds a Diploma from Shannon College of Hotel Management, Ireland.

30 Wynn Macau, Limited

Directors and Senior Management

Non-executive Directors

Mr. Marc D. Schorr, aged 64, has been a non-executive Director of the Company since 16 September 2009, and also a director of WRM. He is also the Chief Operating Officer of Wynn Resorts, Limited, a position he has held since June 2002, and a director of WRL since 29 July 2010. Mr. Schorr has over 32 years of experience in the casino gaming industry. From June 2000 through April 2001, Mr. Schorr served as Chief Operating Officer of Valvino Lamore, LLC. Prior to joining the Group, Mr. Schorr held various positions including President of The Mirage Casino-Hotel from January 1997 until May 2000 and Chief Executive Officer of Treasure Island at The Mirage from August 1992. In 1989, as President and Chief Executive Officer of the Golden Nugget in Laughlin, Nevada, he managed its multi-million dollar expansion program. Preceding that in 1984, as director of Casino Marketing for the Golden Nugget in Las Vegas, he established a casino marketing department and a branch office network throughout the United States.

Dr. Allan Zeman, GBM, GBS, JP, aged 64, has been a Director of the Company since its inception and a non-executive Director of the Company since 16 September 2009 and is the Vice Chairman of the Company. He is also a non-executive director of Wynn Resorts, Limited, a position he has held since October 2002. Dr. Zeman founded The Colby International Group in 1975 to source and export fashion apparel to North America. In late 2000, The Colby International Group merged with Li & Fung Limited. Dr. Zeman is the Chairman of Lan Kwai Fong Holdings Limited. He is also the owner of Paradise Properties Group, a property developer in Thailand. Dr. Zeman is also Chairman of Ocean Park, a major theme park in Hong Kong.

Dr. Zeman is Vice Patron of Hong Kong Community Chest and serves as a director of the “Star” Ferry Company, Limited. Dr. Zeman also serves as an independent non-executive director of Pacifi c Century Premium Developments Limited, Sino Land Company Limited and Tsim Sha Tsui Properties Limited, all of which are listed on the Hong Kong Stock Exchange.

Dr. Zeman is a member of the Food Business Task Force for Business Facilitation Advisory Committee, the Committee on the Commission on Strategic Development, the West Kowloon Cultural District Authority (“WKCDA”), the Consultation Panel of the WKCDA, WKCDA Development Committee, WKCDA Investment Committee, and WKCDA Performing Arts Committee (of which Dr. Zeman is the Chairman). In 2001, Dr. Zeman joined the Richard Ivey School of Business’ Asian Advisory Board.

In 2001, Dr. Zeman was appointed a Justice of the Peace. He was awarded the Gold Bauhinia Star in 2004 and the Grand Bauhinia Medal in 2011.

Interim Report 2012 31

Directors and Senior Management

Independent non-executive Directors

Mr. Jeffrey Kin-fung Lam, GBS, JP, aged 60, has been an independent non-executive Director of the Company since 16 September 2009. Mr. Lam is a member of the National Committee of the Chinese People’s Political Consultative Conference, a member of the Hong Kong Legislative Council, the Chairman of the Assessment Committee of Mega Events Funds, a member of the board of the West Kowloon Cultural District Authority, a member of the board of Hong Kong Airport Authority, a member of the Independent Commission Against Corruption’s Advisory Committee on Corruption, and a member of the Fight Crime Committee in Hong Kong. Mr. Lam is also a General Committee Member of the Hong Kong General Chamber of Commerce and the Vice-Chairman of The Hong Kong Shippers’ Council. In addition, Mr. Lam is an independent non-executive director of CC Land Holdings Limited, Hsin Chong Construction Group Ltd., China Overseas Grand Oceans Group Limited, Sateri Holdings Limited and Chow Tai Fook Jewellery Group Limited, all of which are listed on the Hong Kong Stock Exchange.

In 1996, Mr. Lam was appointed Justice of the Peace and became a member of the Most Excellent Order of the British Empire. He was awarded the honor of the Gold Bauhinia Star in July 2011 and the Silver Bauhinia Star in 2004. Mr. Lam was conferred University Fellow of Tufts University in the United States and Hong Kong Polytechnic University in 1997 and in 2000, respectively.

Mr. Bruce Rockowitz, aged 53, has been an independent non-executive Director of the Company since 16 September 2009. Mr. Rockowitz is also the Group President and Chief Executive Officer of Li & Fung Limited, a company listed on the Hong Kong Stock Exchange. Mr. Rockowitz has been an executive director of Li & Fung Limited since 2001 and was the co-founder and Chief Executive Officer of Colby International Limited, a large Hong Kong buying agent, prior to the sale of Colby International Limited to Li & Fung Limited in 2000. He is a member of the Advisory Board for the Wharton School’s Jay H Baker Retailing Center, an industry research center for retail at the University of Pennsylvania. He is also a board member of the Education Foundation for Fashion Industries, the private fund-raising arm of the Fashion Institute of Technology, New York. In March 2012, he became a member of the Global Advisory Council of the Women’s Tennis Association (WTA). In addition to his position at Li & Fung, Mr. Rockowitz is the non-executive Chairman of The Pure Group, a lifestyle, fi tness and yoga group operating in Hong Kong, Singapore and Taiwan and soon to be opening in mainland China. In December 2008, Mr. Rockowitz was ranked first by Institutional Investor for Asia’s Best CEOs in the consumer category. In the years 2010 and 2011, he was also ranked as one of the world’s 30 best CEOs by Barron’s. In 2011, he was presented with the Alumni Achievement Award by the University of Vermont. In 2012, Mr. Rockowitz was named Asia’s Best CEO at Corporate Governance Asia’s

Excellence Recognition Awards, and he was also presented with an Asian Corporate Director Recognition Award by the same organization.

32 Wynn Macau, Limited

Directors and Senior Management

Mr. Nicholas Sallnow-Smith, aged 62, has been an independent non-executive Director of the Company since 16 September 2009. Mr. Sallnow-Smith has also served as the Chairman and an independent non-executive director of The Link Management Limited since April 2007 and is also Chairman of the Link Management Limited’s Finance and Investment, and Nominations Committees. The Link Management Limited is the manager to the Link Real Estate Investment Trust, a company listed on the Hong Kong Stock Exchange. Mr. Sallnow-Smith is also a non-executive director of Unitech Corporate Parks Plc., a company listed on the London Stock Exchange in the Alternative Investment Market (“AIM”); a non-executive director of Aviva Life Insurance Limited (Hong Kong); and a member of the Advisory Board of Winnington Group. Prior to joining The Link Management Limited, Mr. Sallnow-Smith was Chief Executive of Hongkong Land Holdings Limited from February 2000 to March 2007. He has a wide ranging finance background in Asia and the United Kingdom for over 30 years, including his roles as Finance Director of Hongkong Land Holdings Limited from 1998 to 2000 and as Group Treasurer of Jardine Matheson Limited from 1993 to 1998.

Mr. Sallnow-Smith’s early career was spent in the British Civil Service, where he worked for Her Majesty’s Treasury in Whitehall, London from 1975 to 1985. During that time, he was seconded for two years to Manufacturers Hanover London, working in export finance and in their merchant banking division, Manufacturers Hanover Limited. He left the Civil Service in 1985, following a period working in the International Finance section of H. M. Treasury on Paris Club and other international debt policy matters, and spent two years with Lloyds Bank before moving into the corporate sector in 1987. Mr. Sallnow-Smith served as the Convenor of the Hong Kong Association of Corporate Treasurers in 1996 to 2000 and as Chairman of the Matilda Child Development Centre. He is a director of the Hong Kong Philharmonic Society, Chairman of the Hong Kong Youth Arts Foundation, a member of the Council of the Treasury Markets Association (Hong Kong Association of Corporate Treasurers Representative). He is currently Chairman of the General Committee of The British Chamber of Commerce in Hong Kong and Chairman of the Earth Champions, Hong Kong. He is also the Director of AFS Intercultural Exchanges Ltd. in Hong Kong; a Councillor of the Foundation for the Arts and Music Ltd.; and a Director of The Photographic Heritage Foundation Ltd.

Mr. Sallnow-Smith was educated at Gonville & Caius College, Cambridge, and the University of Leicester and is a Fellow of the Association of Corporate Treasurers. He holds M.A. (Cantab) and M.A. (Soc. of Ed.) Degrees.

Interim Report 2012 33

Directors and Senior Management

OUR SENIOR MANAGEMENT

The following table presents certain information concerning the senior management personnel of the Group (other than our Executive Directors).

Senior management

Name Age Position

Frank Xiao 44 Senior Executive Vice President — Premium Marketing#

Charlie Ward 63 Executive Vice President — Casino Operations#

Doreen Marie Whennen 57 Executive Vice President — Hotel Operations#

Jay M. Schall 39 Senior Vice President and General Counsel##,

Senior Vice President — Legal#

Robert Alexander Gansmo 42 Senior Vice President — Chief Financial Officer#

Andre Mung Dick Ong 42 Senior Vice President — Technology and

Chief Information Officer#

Mo Yin Mok 51 Vice President — Human Resources#

Notes:

## Position held in the Company.

# Position held in WRM.

The biography of each member of the senior management team (other than our executive Directors) is set out below:

Mr. Frank Xiao, aged 44, is the Senior Executive Vice President — Premium Marketing of WRM, a position he has held since August 2006. Mr. Xiao is responsible for providing leadership and guidance to the marketing team and staff, developing business and promoting Wynn Macau. Prior to this position, Mr. Xiao was the Senior Executive Vice President — China Marketing for WIML and Worldwide Wynn between 2005 until 2006. Prior to joining the Group, Mr. Xiao was the Senior Vice President of Far East Marketing at MGM Grand Hotel. During his 12 years at the MGM Grand Hotel, he was promoted several times from his fi rst position as Far East Marketing Executive in 1993. Mr. Xiao holds a Bachelor of Science Degree in Hotel Administration and a Master’s Degree in Hotel Administration from the University of Nevada, Las Vegas.

34 Wynn Macau, Limited

Directors and Senior Management

Mr. Charlie Ward, aged 63, is the Executive Vice President — Casino Operations of WRM, a position he has held since 1 March 2012. Mr. Ward is responsible for providing leadership and operational direction for WRM gaming operations. Mr. Ward has more than 40 years experience in the gaming industry, having served at gaming companies including MGM and Wynn. Over his career Mr. Ward has gained experience in a wide range of assignments including customer/VIP relations, game protection and casino set up, opening and operations. Prior to this position, Mr. Ward held the position of Vice President of Table Games at Wynn | Encore Las Vegas between 2008 and 2012. Prior to joining the Group, Mr. Ward was at MGM Grand Hotel and Casino for 14 years and in 2007 was promoted to the pre-opening team of MGM Grand Macau as Vice President of VIP Gaming.

Ms. Doreen Marie Whennen, aged 57, is the Executive Vice President — Hotel Operations of WRM, a position she has held since May 2007. Ms. Whennen is responsible for overseeing the hotel operations of Wynn Macau. Ms. Whennen has over 20 years of experience in the hospitality industry. She joined Valvino Lamore, LLC in 2000 and prior to joining the Group, she held various positions at The Mirage, which she joined in 1989, including Front Offi ce Manager, Director of Guest Services and Vice President of Hotel Operations.

Mr. Jay M. Schall, aged 39, is the Senior Vice President and General Counsel of the Company and Senior Vice President — Legal of WRM. He has held senior legal positions with WRM since May 2006. Mr. Schall has over twelve years of experience in the legal fi eld, including eight years in Macau and Hong Kong. Prior to joining the Group, Mr. Schall practiced United States law at a major law firm in the United States and in Hong Kong. Mr. Schall is a member of the State Bar of Texas. Mr. Schall holds a Bachelor of Arts Degree from Colorado College, an MBA from Tulane University, Freeman School of Business and a Juris Doctor (magna cum laude, Order of the Coif) from Tulane University School of Law.

Mr. Robert Alexander Gansmo, aged 42, is the Senior Vice President — Chief Financial Offi cer of WRM, a position he has held since April 2009. Prior to taking this position, Mr. Gansmo was the Director — Finance of WRM, a position he assumed in January 2007. Mr. Gansmo is responsible for the management and administration of WRM’s fi nance division. Before joining WRM, Mr. Gansmo worked at Wynn Resorts, Limited, where he served as the Director of Financial Reporting from November 2002. Prior to joining the Group, Mr. Gansmo practiced as a certified public accountant with firms in Las Vegas, Washington and California, including KPMG Peat Marwick, Arthur Andersen, and Deloitte and Touche. Mr. Gansmo graduated in 1993 from California State University, Chico, where he obtained a Bachelor of Science Degree in Business Administration with a focus on accounting.

Interim Report 2012 35

Directors and Senior Management

Mr. Andre Mung Dick Ong, aged 42, is the Senior Vice President — Technology and Chief Information Offi cer of WRM, a position he has held since June 2012. Mr. Ong is responsible for the strategic planning, development and overall operation of information systems and technology services for WRM. Prior positions held by Mr. Ong include Vice President — Information Technology

& Chief Information Officer and Executive director, Chief Information Officer between June 2003 and May 2012. Before joining the Group, Mr. Ong served at Shangri-La Hotels & Resorts where, from August 2001 until May 2003, he was the Director of Corporate Information Technology and was responsible for the planning and deployment of information technology for the group of 40 hotels and five regional sales offices. Prior to this role, he was Director of Technology Support as well as Systems Support Manager since 1993. Mr. Ong has more than 19 years of experience in the hospitality/gaming industry and extensive skills in technology consultation and execution, vendor management, operation management and software development. Mr. Ong was educated in Western Australia and obtained a Bachelor of Engineering Degree in Computer Systems from Curtin University of Technology in 1991.

Ms. Mo Yin Mok, aged 51, is the Vice President — Human Resources of WRM, a position she has held since June 2008. Ms. Mok has an extensive 20-year background in hospitality and human resources, primarily in the luxury hotel sector at The Regent Four Seasons Hong Kong and The Peninsula Hong Kong. Prior to joining the Group, she led The Peninsula Group’s worldwide human resources team and, in her position, supported eight Peninsula hotels with more than 5,000 staff, and orchestrated human resources activities for the opening of The Peninsula Tokyo. Ms. Mok also served at the front lines of the hospitality industry as the Director of Rooms Division at The Peninsula Hong Kong with responsibility for front office, housekeeping, security and spa departments. Ms. Mok currently serves on the Future Students and Placement Advisory Committee of the University of Macau and is a panel member of the Hong Kong Council for Accreditation of Academic and Vocational Qualifications.

Ms. Mok holds a Bachelor of Science Degree in Hospitality Management from Florida International University in the United States, where she received a Rotary International Ambassadorial Scholarship. She also obtained an MBA from the Chinese University of Hong Kong.

36 Wynn Macau, Limited

Directors and Senior Management

OUR COMPANY SECRETARY

Ms. Kwok Yu Ching, aged 47, is the company secretary of the Company. Ms. Kwok has been a company secretary of the Company since September 2009. She is a director of Corporate Services Division of Tricor Services Limited. Ms. Kwok, a Chartered Secretary, is a Fellow of both The Hong Kong Institute of Chartered Secretaries and The Institute of Chartered Secretaries and Administrators. She has been providing professional services to companies listed on the Hong Kong Stock Exchange for over 20 years. Prior to joining Tricor Services Limited in 2002, Ms. Kwok was the Senior Manager of Company Secretarial Services at Ernst & Young and Tengis Limited in Hong Kong.

Interim Report 2012 37

Other Information

DIVIDENDS

The Board has recommended that no interim dividend be paid in respect of the six months ended 30 June 2012.

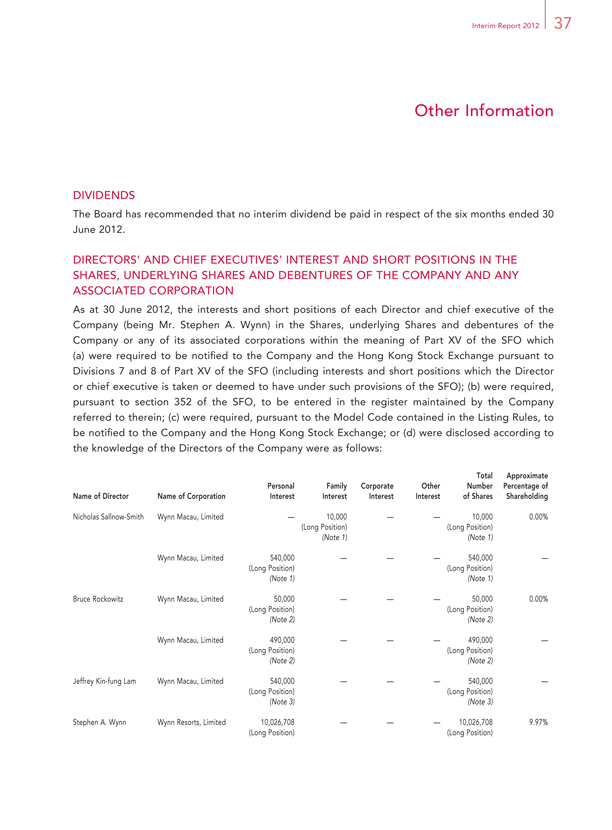

DIRECTORS’ AND CHIEF EXECUTIVES’ INTEREST AND SHORT POSITIONS IN THE SHARES, UNDERLYING SHARES AND DEBENTURES OF THE COMPANY AND ANY ASSOCIATED CORPORATION

As at 30 June 2012, the interests and short positions of each Director and chief executive of the Company (being Mr. Stephen A. Wynn) in the Shares, underlying Shares and debentures of the Company or any of its associated corporations within the meaning of Part XV of the SFO which (a) were required to be notified to the Company and the Hong Kong Stock Exchange pursuant to Divisions 7 and 8 of Part XV of the SFO (including interests and short positions which the Director or chief executive is taken or deemed to have under such provisions of the SFO); (b) were required, pursuant to section 352 of the SFO, to be entered in the register maintained by the Company referred to therein; (c) were required, pursuant to the Model Code contained in the Listing Rules, to be notified to the Company and the Hong Kong Stock Exchange; or (d) were disclosed according to the knowledge of the Directors of the Company were as follows:

Total Approximate

Personal Family Corporate Other Number Percentage of

Name of Director Name of Corporation Interest Interest Interest Interest of Shares Shareholding

Nicholas Sallnow-Smith Wynn Macau, Limited — 10,000 — — 10,000 0.00%

(Long Position) (Long Position)

(Note 1) (Note 1)

Wynn Macau, Limited 540,000 — — — 540,000 —

(Long Position) (Long Position)

(Note 1) (Note 1)

Bruce Rockowitz Wynn Macau, Limited 50,000 — — — 50,000 0.00%

(Long Position) (Long Position)

(Note 2) (Note 2)

Wynn Macau, Limited 490,000 — — — 490,000 —

(Long Position) (Long Position)

(Note 2) (Note 2)

Jeffrey Kin-fung Lam Wynn Macau, Limited 540,000 — — — 540,000 —

(Long Position) (Long Position)

(Note 3) (Note 3)

Stephen A. Wynn Wynn Resorts, Limited 10,026,708 — — — 10,026,708 9.97%

(Long Position) (Long Position)

38 Wynn Macau, Limited

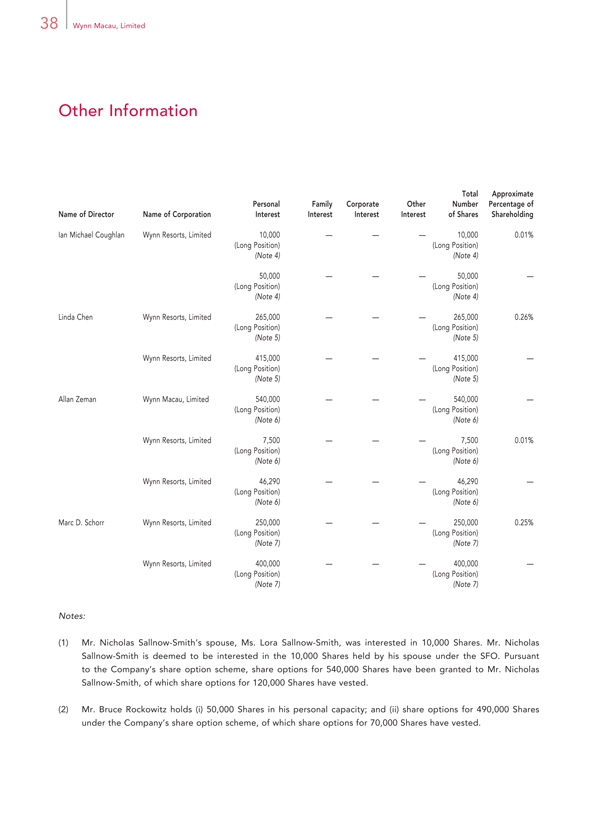

Other Information

Total Approximate

Personal Family Corporate Other Number Percentage of

Name of Director Name of Corporation Interest Interest Interest Interest of Shares Shareholding

Ian Michael Coughlan Wynn Resorts, Limited 10,000 — — — 10,000 0.01%

(Long Position) (Long Position)

(Note 4) (Note 4)

50,000 — — — 50,000 —

(Long Position) (Long Position)

(Note 4) (Note 4)

Linda Chen Wynn Resorts, Limited 265,000 — — — 265,000 0.26%

(Long Position) (Long Position)

(Note 5) (Note 5)

Wynn Resorts, Limited 415,000 — — — 415,000 —

(Long Position) (Long Position)

(Note 5) (Note 5)

Allan Zeman Wynn Macau, Limited 540,000 — — — 540,000 —

(Long Position) (Long Position)

(Note 6) (Note 6)

Wynn Resorts, Limited 7,500 — — — 7,500 0.01%

(Long Position) (Long Position)

(Note 6) (Note 6)

Wynn Resorts, Limited 46,290 — — — 46,290 —

(Long Position) (Long Position)

(Note 6) (Note 6)

Marc D. Schorr Wynn Resorts, Limited 250,000 — — — 250,000 0.25%

(Long Position) (Long Position)

(Note 7) (Note 7)

Wynn Resorts, Limited 400,000 — — — 400,000 —

(Long Position) (Long Position)

(Note 7) (Note 7)

Notes:

Mr. Nicholas Sallnow-Smith’s spouse, Ms. Lora Sallnow-Smith, was interested in 10,000 Shares. Mr. Nicholas Sallnow-Smith is deemed to be interested in the 10,000 Shares held by his spouse under the SFO. Pursuant to the Company’s share option scheme, share options for 540,000 Shares have been granted to Mr. Nicholas Sallnow-Smith, of which share options for 120,000 Shares have vested.

Mr. Bruce Rockowitz holds (i) 50,000 Shares in his personal capacity; and (ii) share options for 490,000 Shares under the Company’s share option scheme, of which share options for 70,000 Shares have vested.

Interim Report 2012 39

Other Information

Pursuant to the Company’s share option scheme, share options for 540,000 Shares have been granted to Mr. Jeffrey Kin-fung Lam, of which share options for 120,000 Shares have vested.

Pursuant to the 2002 Stock Incentive Plan of Wynn Resorts, Limited (the “Stock Plan”), Mr. Ian Michael Coughlan holds (i) 10,000 non-vested shares which vested on 1 January 2012, and became 10,000 shares in common stock of Wynn Resorts, Limited; and (ii) 50,000 stock options in the common stock of Wynn Resorts, Limited of which share options for 15,000 shares have vested.

Pursuant to the Stock Plan, Ms. Linda Chen holds (i) 100,000 shares in common stock of Wynn Resorts, Limited which were vested on 31 July 2012; (ii) 100,000 non-vested shares; and (iii) 415,000 stock options in the common stock of Wynn Resorts, Limited of which share options for 30,000 shares have vested and 385,000 remain unvested. 65,000 shares in the common stock of Wynn Resorts, Limited are held by Ms. Linda Chen in her personal capacity.

Pursuant to the Company’s share option scheme, share options for 540,000 Shares have been granted to Dr. Allan Zeman, of which share options for 120,000 Shares have vested. Pursuant to the Stock Plan, Dr. Allan Zeman holds (i) 5,000 shares in common stock of Wynn Resorts, Limited which were non-vested shares which had vested in the year ended 31 December 2011 and the six months ended 30 June 2012; (ii) 2,500 non-vested shares; and (iii) in aggregate of 46,290 stock options in the common stock of Wynn Resorts, Limited of which share options for 25,720 shares have vested.

Pursuant to the Stock Plan, Mr. Marc D. Schorr holds (i) 250,000 non-vested shares; and (ii) 400,000 unvested stock options in the common stock of Wynn Resorts, Limited of which share options for 50,000 shares have vested.

40 Wynn Macau, Limited

Other Information

SUBSTANTIAL SHAREHOLDERS’ INTERESTS AND SHORT POSITIONS IN THE SHARES AND UNDERLYING SHARES OF THE COMPANY