REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders and the Board of Directors of Amarc Resources Ltd.,

Opinion on the Consolidated Financial Statements

We have audited the accompanying consolidated financial statements of Amarc Resources Ltd. (‘the Company’), which comprise the consolidated statements of financial position as at March 31, 2022 and 2021 and the consolidated statements of loss, comprehensive income (loss), changes in (deficiency) equity and cash flows for each of the years in the three year period ended March 31, 2022, and a summary of significant accounting policies and other explanatory information (collectively referred to as the ‘consolidated financial statements’). In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Company as at March 31, 2022 and 2021 and its financial performance and its cash flows for each of the years in the three year period ended March 31, 2022, in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board.

Going Concern

The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern. Without modifying our opinion, we draw attention to Note 1 in the consolidated financial statements which indicates that the Company has no current source of revenue, has incurred losses from inception and is dependent upon its ability to secure new sources of financing. These conditions, along with other matters as set forth in Note 1, indicate the existence of a material uncertainty that casts significant doubt as to the Company's ability to continue as a going concern. Management’s plans in regard to these matters are also described in Note 1. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

This issue also constitutes, from our perspective, a critical audit matter that was communicated to the audit committee and that: (i) relates to accounts or disclosures that are material to the consolidated financial statements; and (ii) involved, on our part, especially challenging, subjective, or complex judgements. The communication of a critical audit matter does not alter in any way our opinion on the consolidated financial statements, taken as a whole, and we are not, by communicating this critical audit matter, providing a separate opinion on the critical audit matter or on the accounts or disclosures to which it relates.

The principal considerations for our determination that the going concern uncertainty was a critical audit matter were: (i) that the formal reporting of such uncertainty involves a significant disclosure, the absence of which could constitute a material misstatement to a financial statement reader and, (ii) that, at the same time, it involves on our part the use of a high level of subjective judgement as we are required to consider the possible impact of future events that cannot currently be known and which in all likelihood will not be directly linked to any particular current or future financial results and reporting, or the lack thereof.

Addressing this matter involved performing procedures and evaluating audit evidence in connection with forming our overall opinion on the consolidated financial statements. These procedures also included, among others, (i) obtaining and evaluating management’s assessment of the Company’s ability to remain a going concern; (ii) determining based on all other evidence available to us whether management’s assessment appeared to be fair and reasonable in the circumstances and, (iii) considering whether the resultant disclosure of these matters herein was consistent with the foregoing, in the context of the Company’s overall business activities, objectives and financial history.

Basis for Opinion

These consolidated financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s consolidated financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (‘PCAOB’) and are required to be independent with respect to the Company in accordance with U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance whether the consolidated financial statements are free of material misstatement, whether due to fraud or error. The Company is not required to have, nor were we engaged to perform, an audit of internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.

2 | Page

Our audits included performing procedures to assess the risks of material misstatement of the consolidated financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the consolidated financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that our audits provide a reasonable basis for our opinion.

Critical Audit Matter

A critical audit matter was communicated above under ‘Going Concern’.

CHARTERED PROFESSIONAL ACCOUNTANTS

Vancouver, Canada

July 29, 2022

We have served as the Company’s auditor since 1995.

3 | Page

4 | Page

5 | Page

6 | Page

7 | Page

8 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

1.

NATURE AND CONTINUANCE OF OPERATIONS

Amarc Resources Ltd. (“Amarc” or the “Company”) is a company incorporated under the laws of the Province of British Columbia (“BC”). Its principal business activity is the acquisition and exploration of mineral properties. The Company’s mineral property interests are located in BC. The address of the Company’s corporate office is 14th Floor, 1040 West Georgia Street, Vancouver, BC, Canada V6E 4H1.

The Company is in the process of exploring its mineral property interests and has not yet determined whether its mineral property interests contain economically recoverable mineral reserves. The Company’s continuing operations are entirely dependent upon the existence of economically recoverable mineral reserves, the ability of the Company to obtain the necessary financing to continue the exploration and development of its mineral property interests and to obtain the permits necessary to mine, and the future profitable production from its mineral property interest or proceeds from the disposition of its mineral property interests.

These consolidated financial statements as at and for the year ended March 31, 2022 (the “Financial Statements”) have been prepared on a going concern basis, which contemplates the realization of assets and the discharge of liabilities in the normal course of business for the foreseeable future. As at March 31, 2022, the Company had cash of $370,784, a working capital deficiency of $171,812, and an accumulated deficit of $69,951,679.

The Company will need to seek additional financing to meet its exploration and development objectives. The Company has a reasonable expectation that additional funds will be available when necessary to meet ongoing exploration and development costs. However, there can be no assurance that the Company will continue to be able to obtain additional financial resources or will achieve profitability or positive cash flows. If the Company is unable to obtain adequate additional financing, the Company will be required to re-evaluate its planned expenditures until additional funding can be raised through financing activities. These factors indicate the existence of a material uncertainty that casts significant doubt about the Company’s ability to continue as a going concern.

These Financial Statements do not include any adjustments to the recoverability and classification of recorded asset amounts and classification of liabilities that may be necessary should the Company be unable to continue as a going concern.

The current outbreak of COVID-19, and any future emergence and spread of similar pathogens, could have a material adverse effect on global and local economic and business conditions, which may adversely impact Amarc’s business and results of operations and the operations of contractors and service providers. The extent to which the COVID-19 impacts our operations will depend on future developments, which are highly uncertain and cannot be predicted with confidence, including the duration of the outbreak, new information that may emerge concerning its severity and the actions taken to contain the virus or treat its impact, among others. The adverse effects on the economy, the stock market and Amarc’s share price could adversely impact its ability to raise capital, with the result that our ability to pursue development of the JOY, IKE and DUKE Districts could be adversely impacted, both through delays and through increased costs. Any of these developments, and others, could have a material adverse effect on the Company’s business and results of operation and could delay its plans for development of its districts.

9 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

2.

SIGNIFICANT ACCOUNTING POLICIES

The principal accounting policies applied in the preparation of these Financial Statements are described below. These policies have been consistently applied for all years presented, unless otherwise stated.

(a)

Statement of compliance

These Financial Statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board (“IASB”) and the International Financial Reporting Interpretations Committee (“IFRIC”), effective for the Company’s reporting year ended March 31, 2022.

The Board of Directors of the Company authorized these Financial Statements for issuance on July 29, 2022.

(b)

Basis of presentation and consolidation

These Financial Statements have been prepared on a historical cost basis, except for certain financial instruments classified as fair value through other comprehensive income, which are reported at fair value. In addition, these Financial Statements have been prepared using the accrual basis of accounting, except for cash flow information.

These Financial Statements include the financial statements of the Company and its wholly-owned subsidiary, 1130346 B.C. Ltd. (the “Subco”), incorporated under the laws of BC. The Subco was incorporated for the purposes of entering into an option agreement related to the JOY District. On March 30, 2021, Subco was dissolved, did not have any assets, liabilities, income or expenses, and all intercompany balances and transactions had been eliminated on consolidation.

Certain comparative amounts have been reclassified to conform to the presentation adopted in the current period.

(c)

Significant accounting estimates and judgements

The preparation of the Financial Statements in conformity with IFRS requires management to make judgments, estimates, and assumptions that affect the application of policies and reported amounts of assets and liabilities, income and expenses. Actual results may differ from these estimates.

The impacts of such estimates are pervasive throughout the Financial Statements, and may require accounting adjustments based on future occurrences. Revisions to accounting estimates are recognized in the period in which the estimate is revised and future periods if the revision affects both current and future periods. These estimates are based on historical experience, current and future economic conditions and other factors, including expectations of future events that are believed to be reasonable under the circumstances. Specific areas where significant estimates or judgments exist are:

•

assessment of the Company’s ability to continue as a going concern;

•

the determination of categories of financial assets and financial liabilities; and

•

the carrying value and recoverability of the Company’s marketable securities.

10 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

(d)

Foreign currency

The functional and presentational currency of the Company is the Canadian Dollar (“CAD”).

Transactions in currencies other than the functional currency of the Company are recorded at the rates of exchange prevailing on the dates of transactions. At each financial position reporting date, monetary assets and liabilities that are denominated in foreign currencies are translated at the rates of exchange prevailing at the date when the fair value was determined. Non-monetary items that are measured in terms of historical cost in a foreign currency are not re-translated. Gains and losses arising on translation are included in profit or loss for the year.

(e)

Financial instruments

A financial asset (unless it is a trade receivable without a significant financing component that is initially measured at the transaction price) is initially measured at fair value plus, for an item not measured at fair value through profit or loss (“FVTPL”), transaction costs that are directly attributable to its acquisition. The directly attributable transaction costs of a financial asset classified at FVTPL are expensed in the period in which they are incurred.

Financial assets measured at amortized cost

A financial asset is measured at amortized cost if it meets both the following conditions and is not designated as at FVTPL:

·

it is held within a business model whose objective is to hold assets to collect contractual cash flows; and,

·

its contractual terms give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

These financial assets are subsequently measured at amortized cost using the effective interest method. The amortized cost is reduced by impairment losses. Interest income, foreign exchange gains and losses, and impairment losses are recognized in profit or loss. Any gain or loss on the derecognition of the financial asset is recognized in profit or loss.

Financial assets measured at fair value through other comprehensive income

A debt investment is measured at fair value through other comprehensive income (“FVTOCI”) if it meets both the following conditions and is not designated as at FVTPL:

·

it is held within a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets; and,

·

its contractual terms give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

On the initial recognition of an equity instrument that is not held for trading, the Company may irrevocably elect to present subsequent changes in the investment’s fair value in other comprehensive income (“OCI”). This election is made on an investment-by-investment basis.

11 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

Debt investments measured at FVTOCI are subsequently measured at fair value. Interest income calculated using the effective interest method, foreign exchange gains and losses, and impairment are recognized in profit or loss. Other net gains and losses are measured in OCI. On de-recognition, gains and losses accumulated in OCI are reclassified to profit or loss.

Equity investments measured at FVTOCI are subsequently measured at fair value. Dividends are recognized as income in profit or loss unless the dividend clearly represents a recovery of part of the cost of the investment. Other net gains and losses are recognized in OCI and are never reclassified to profit or loss.

Financial assets measured at fair value through profit or loss

All financial assets not classified as measured at amortized cost or measured at FVTOCI, as described above, are measured at FVTPL; this includes all derivative financial assets. On initial recognition, the Company may irrevocably designate a financial asset that otherwise meets the requirements to be measured at amortized cost or measured at FVTOCI as FVTPL if doing so eliminates, or significantly reduces, an accounting mismatch that would otherwise arise.

These financial assets are subsequently measured at fair value. Net gains and losses, including any interest or dividend income, are recognized in profit or loss.

Financial liabilities

Classification

Accounts payable and accrued liabilities

Amortized cost

Balance due to related parties

Amortized cost

Financial assets

Classification

Cash

Amortized cost

Marketable securities

FVTOCI

Restricted cash

Amortized cost

Amounts receivable and other assets

Amortized cost

(f)

Exploration and evaluation expenditures

Exploration and evaluation costs are costs incurred to discover mineral resources, and to assess the technical feasibility and commercial viability of the mineral resources found.

Exploration and evaluation expenditures include:

·

costs associated with the acquisition of licences;

·

costs associated with the acquisition of exploration and evaluation assets, including mineral properties; and,

·

costs associated with exploration and evaluation activities.

Exploration and evaluation costs are generally expensed as incurred until the technical feasibility and commercial viability of extracting a mineral resource has been determined and a positive decision to proceed to development has been made. However, if management concludes that future economic benefits are more likely than not to be realized, the costs of property, plant and equipment for use in the exploration and evaluation of mineral resources are capitalized.

12 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

Costs incurred before the Company has obtained the legal rights to explore an area are expensed. Costs incurred after the technical feasibility and commercial viability of extracting a mineral resource has been determined and a positive decision to proceed to development has been made are considered development costs and are capitalized.

Costs applicable to established mineral property interests where no further work is planned by the Company may, for presentation purposes only, be carried at nominal amounts.

(g)

Equipment

Equipment is carried at cost, less accumulated depreciation and accumulated impairment losses.

The cost of equipment consists of the purchase price, any costs directly attributable to bringing the asset to the location and the condition necessary for its intended use, and an initial estimate of the costs of dismantling and removing the asset and restoring the site on which it is located.

Depreciation is provided at rates calculated to expense the cost of the equipment, less its estimated residual value, using the declining balance method at various rates ranging from 20% to 30% per annum.

An item of equipment is derecognized upon disposal or when no material future economic benefits are expected to arise from the continued use of the asset. Any gain or loss arising on disposal of the asset, determined as the difference between the net disposal proceeds and the carrying amount of the asset, is recognized in profit or loss.

Where an item of equipment consists of major components with different useful lives, the components are accounted for as separate items of equipment. Expenditures incurred to replace a component of an item of equipment that is account for separately, including major inspection and overhaul expenditures, are capitalized.

As at March 31, 2022, all equipment had been fully depreciated. The Company did not purchase any equipment during the year ended March 31, 2022.

(h)

Share capital

Common shares of the Company are classified as equity. Transaction costs directly attributable to the issuance of common shares and share purchase options are recognized as a deduction from equity, net of any tax effects.

When the Company issues common shares for consideration other than cash, the transaction is measured at fair value based on the quoted market price of the Company’s common shares on the date of issuance.

(I)

Loss per share

Loss per share is computed by dividing the losses attributable to common shareholders by the weighted average number of common shares outstanding during the reporting period. Diluted loss per share is determined by adjusting the losses attributable to common shareholders and the weighted average number of common shares outstanding for the effects of all dilutive potential common shares, such as options granted to employees. The dilutive effect of options assumes that the proceeds to be received on the exercise of share purchase options are applied to repurchase common shares at the average market price for the reporting period. Share purchase options are included in the calculation of dilutive earnings per share only to the extent that the market price of the common shares exceeds the exercise price of the share purchase options. The effect of anti-dilutive factors is not considered when computed diluted loss per share.

13 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

(j)

Equity-settled share-based payments

The share purchase option plan allows employees and consultants of the Company to acquire shares of the Company. The fair value of share purchase options granted is recognized as an employee or consultant expense with a corresponding increase in the share-based payments reserve in equity. An individual is classified as an employee when the individual is an employee for legal and tax purposes (direct employee) or provides services similar to those performed by a direct employee.

For employees, fair value is measured at the grant date and each tranche is recognized on a straight-line basis over the period during which the share purchase options vest. The fair value of the share purchase options granted is measured using the Black-Scholes option pricing model taking into account the terms and conditions upon which the share purchase options were granted. At the end of each financial reporting period, the amount recognized as an expense is adjusted to reflect the actual number of share purchase options that are expected to vest.

Share-based payment transactions with non-employees are measured at the fair value of the goods and services received. However, if the fair value cannot be estimated reliably, the share-based payment transaction is measured at the fair value of the equity instrument granted at the date the entity obtains the goods or the counterparty renders the service.

(k)

Income taxes

Income tax on the profit or loss for the years presented comprises of current and deferred tax. Income tax is recognized in profit or loss except to the extent that it relates to items recognized directly in equity, in which case it is recognized in equity.

Current tax expense is the expected tax payable on taxable income for the year, using tax rates enacted or substantively enacted at year end, adjusted for amendments to tax payable with regards to previous years.

Deferred tax is provided using the balance sheet liability method, providing for temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes.

The following temporary differences are not provided for:

·

goodwill not deductible for tax purposes;

·

the initial recognition of assets or liabilities that affect neither accounting nor taxable profit; and

·

differences relating to investments in subsidiaries, associates, and joint ventures to the extent that they will probably not reverse in the foreseeable future.

The amount of deferred tax provided is based on the expected manner of realization or settlement of the carrying amount of assets and liabilities, using tax rates enacted or substantively enacted at the financial position reporting date applicable to the period of expected realization or settlement.

14 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

A deferred tax asset is recognized only to the extent that it is probable that future taxable profits will be available against which the asset can be utilized.

Additional income taxes that arise from the distribution of dividends are recognized at the same time as the liability to pay the related dividend.

Deferred tax assets and liabilities are offset when there is a legally enforceable right to set off current tax assets against current tax liabilities, when they relate to income taxes levied by the same taxation authority, and the Company intends to settle its current tax assets and liabilities on a net basis.

Flow-through Shares

The Company will, from time-to-time, issue flow-through common shares to finance a portion of its exploration programs. Pursuant to the terms of the flow-through share agreements, these shares transfer the tax deductibility of qualifying resource expenditures to investors. On issuance, the Company bifurcates the flow-through share into i) a flow-through share premium, equal to the estimated premium, if any, investors pay for the flow-through feature, which is recognized as a liability, and ii) share capital. Upon expenses being incurred, the Company derecognizes this liability and recognizes this premium as other income, offsetting any expense associated with the Company’s expenditure of the flow-through proceeds.

(l)

Restoration, rehabilitation and environmental obligations

An obligation to incur restoration, rehabilitation and environmental costs arises when environmental disturbance is caused by the exploration or development of a mineral property interest. Such costs arising from the decommissioning of plant and other site preparation work, discounted to their net present value, are provided for and capitalized at the start of each project to the carrying amount of the asset, along with a corresponding liability at the time the obligation to incur such costs arises. The timing of the actual rehabilitation expenditure is dependent on a number of factors such as the life and nature of the project or asset, the conditions imposed by the relevant permits, and, when applicable, the jurisdiction in which the project or asset is located.

(m)

Operating segments

The Company operates as a single reportable segment—the acquisition, exploration and development of mineral properties. All assets are held in Canada.

(n)

Government assistance

When the Company is entitled to receive the BC Mineral Exploration Tax Credit (“BCMETC”) and other government grants, this government assistance is recognized as a cost recovery when there is reasonable assurance of recovery. Any amounts accrued or received typically remain subject to review and revision by government authorities. It is not possible to predict the occurrence or outcome of such actions in advance.

(o)

Adoption of IFRS 16, Leases (“IFRS 16”)

In January 2016, the IASB issued IFRS 16, replacing IAS 17 - Leases. IFRS 16 provides a single lessee accounting model and requires the lessee to recognize assets and liabilities for all leases on its statement of financial position, providing the reader with greater transparency of an entity’s lease obligations.

15 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

The Company elected to use the modified retrospective transition approach, which provides lessees a method for recording existing leases at adoption with no restatement of prior period financial information. Under this approach, a lease liability was recognized at January 1, 2019 in respect of leases previously classified as operating leases, measured at the present value of the remaining lease payments, discounted using the lessee’s incremental borrowing rate at transition. The associated right-of-use assets were measured at amounts equal to the respective lease liabilities, subject to certain adjustments allowed under IFRS 16.

All leases are accounted for by recognizing a right-of-use asset and a lease liability except for:

·

Leases of low value assets; and

·

Leases with a duration of twelve months or less.

Lease liabilities are measured at the present value of the contractual payments due to the lessor over the lease term, with the discount rate determined by the interest rate implicit in the lease, or if that rate cannot be readily determined, the Company’s incremental borrowing rate on commencement of the lease is used. Variable lease payments are only included in the measurement of the lease liability if they depend on an index or rate. In such cases, the initial measurement of the lease liability assumes the variable element will remain unchanged throughout the lease term. Other variable lease payments are expensed in the period to which they relate.

On initial recognition, the carrying value of the lease liability also includes:

·

Amounts expected to be payable under any residual value guarantee;

·

The exercise price of any purchase option granted if it is reasonable certain to assess that option;

·

Any penalties payable for terminating the lease, if the term of the lease has been estimated on the basis of termination option being exercised.

·

Right-of-use assets are initially measured at the amount of the lease liability, reduced for any lease incentives received, and increased for:

·

Lease payments made at or before commencement of the lease;

·

Initial direct costs incurred; and

·

The amount of any provision recognized where the Company is contractually required to dismantle, remove or restore the leased asset.

Lease liabilities, on initial measurement, increase as a result of interest charged at a constant rate on the balance outstanding and are reduced for lease payments made.

Right-of-use assets are amortized on a straight-line basis over the remaining term of the lease or over the remaining economic life of the asset if this is judged to be shorter than the lease term.

When the Company revises its estimate of the term of any lease, it adjusts the carrying amount of the lease liability to reflect the payments to make over the revised term, which are discounted at the same discount rate that applied on lease commencement. The carrying value of lease liabilities is similarly revised when the variable element of future lease payments dependent on a rate or index is revised. In both cases, an equivalent adjustment is made to the carrying value.

16 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

3.

CASH

The Company’s cash is invested in business and savings accounts, which are available on demand by the Company.

4.

MARKETABLE SECURITIES

As at March 31, 2022, the fair value of its current holdings was $311,293 (March 31, 2021 - $1,026,418) and the negative change of fair value adjustment of $715,125 for the year ended March 31, 2022 (March 31, 2021 –change of fair value adjustment of $626,438). The marketable securities include 5.5 million units (shares and warrants) of Carlyle Commodities Corp., a Canadian public company listed on TSX-V exchange.

As at March 31, 2022, the Company held the following marketable securities:

5.

RESTRICTED CASH

Restricted cash represents amounts held in support of exploration permits. The amounts are refundable subject to the consent of regulatory authorities upon completion of any required reclamation work on the related projects.

6.

AMOUNTS RECEIVABLE AND OTHER ASSETS

17 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

7.

EXPLORATION AND EVALUATION EXPENSES AND COST RECOVERIES

Below is a summary of the Company’s major exploration property interests, together with the material property transactions relating to the three year period ended March 31, 2022.

(a)

IKE District

The IKE Property claims carry a Net Smelter Return (“NSR”) royalty obligation of 1%, subject to a $2 million cap and with the Company able to purchase the royalty at any time by payment of the same amount. These claims carry an additional NSR royalty of 2%, subject to the Company retaining the right to purchase up to the entire royalty amount by the payment of up to $4 million. The Company has also agreed to make annual advance royalty payments of $50,000 to the holders of the 2% NSR royalty interest and, upon completion of a positive feasibility study, to issue to these same parties 500,000 common shares.

The Granite Property claims are subject to a 2% NSR royalty which can be purchased for $2 million. In addition, there is an underlying 2.5% NSR royalty on certain mineral claims within the Granite Property, which can be purchased at any time for $1.5 million less any amount of royalty already paid.

The entire project is subject to a 1% NSR royalty from mine production capped at a total of $5 million.

(b)

JOY District

The JOY District, located in north-central BC, comprises the JOY and PINE Properties, and also the “Staked Claims” acquired directly by the Company. In November 2016, the Company entered into a purchase agreement with a private company wholly-owned by one of its directors to purchase 100% of the JOY Property for the reimbursement of the vendor’s direct acquisition costs of $335,299. The property is subject to an underlying NSR royalty held by a former owner which is capped at $3.5 million.

In addition, the Company concluded agreements with each of Gold Fields Toodoggone Exploration Corporation (“GFTEC”) and Cascadero Copper Corporation (“Cascadero”) in mid-2017 pursuant to which the Company can purchase 100% of the PINE Property.

In October 2018, Amarc acquired a 100% interest in Cascadero’s 49% interest in the PINE Property by completing total cash payments of $1,000,000 and issuing 5,277,778 common shares.

In November 2019 Amarc entered into a purchase agreement with two prospectors to acquire 100% of a single mineral claim, called the Paula property, located internal to the wider JOY District tenure. The claim is subject to a 1% NSR royalty payable from commercial production that is capped at $0.5 million (completed).

In December 2019, the Company amended the GFTEC Agreement to purchase GFTEC’s 51% interest in the PINE property. Under the terms of the amendment Amarc will purchase outright GFTEC’s 51% interest in the 323 km2 Property by issuing to GFTEC 5,000,000 common shares of the Company. As such Amarc now holds a 100% interest in the PINE mineral claims.

The PINE Property is subject to a 3% underlying NSR royalty payable to a former owner. The Company has reached an agreement with the former owner to cap the 3% NSR royalty at $5 million payable from production for consideration totaling $100,000 and 300,000 common shares payable in stages through to January 31, 2019 (completed).

18 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

GFTEC retains a 2.5% net profits interest (“NPI”) royalty on mineral claims comprising approximately 96% of the PINE Property, which are subject to a NSR royalty payable to a former owner (“Underlying NSR”) and a 1% NSR royalty on the balance of the claims that are not subject to the Underlying NSR royalty. The NPI royalty can be reduced to 1.25% at any time through the payment to GFTEC of $2.5 million in cash or shares. The NSR royalty can be reduced to 0.5% through the payment to GFTEC of $2.5 million in cash or shares.

JOY District Agreement with Freeport

On May 11, 2021, the Company and Freeport-McMoRan Mineral Properties Canada Inc. (“Freeport”), a wholly-owned subsidiary of Freeport-McMoRan Inc. (NYSE:FCX) entered into a Mineral Property Earn-in Agreement (the “Agreement”) whereby Freeport may acquire up to a 70% ownership interest of the Company’s JOY porphyry Cu-Au District Property.

Under the terms of the Agreement, Freeport has a two-stage option to earn up to a 70% ownership interest in the mineral claims comprising the JOY District, plus other rights and interests, over a 10 year period.

To earn an initial 60% interest, Freeport is required to fund $35 million of work expenditures over a 5- year term. During the first year of the earn-in, a $4 million work program was planned in the JOY District.

These optional earn-in expenditures can be accelerated by Freeport at its discretion. Amarc will be operator during the initial earn-in period. Once Freeport has acquired such 60% interest, Amarc and Freeport will proceed to operate the JOY District through a jointly owned corporation with Freeport assuming project operatorship.

Upon Freeport earning such 60% interest, it can elect, in its sole discretion, to earn an additional 10% interest, for a total 70% interest by sole funding a further $75 million within the following five years.

Once Freeport has finalized its earned ownership interest at either the 60% or 70% level, each party will be responsible for funding its own pro-rata share of project costs on a 60:40 or 70:30 basis.

During the year ended March 31, 2022, the Company incurred eligible and recoverable project costs of $5,333,085 included as expenses in the Consolidated Statements of Loss and Comprehensive Loss.

During the year ended March 31, 2022, the Company also earned a fee of $409,487 as the project operator.

(c)

DUKE District

The DUKE District is located in central BC. In November 2016, the Company entered into a purchase

agreement with a private company wholly-owned by one of its directors (note 11(c)) to purchase a 100% interest in the DUKE property for the reimbursement of the vendor’s direct acquisition costs of $168,996.

(d)

Other property transactions

During the comparative year, Amarc operated programs on two exploration properties owned by a related party, Jake and Mack (the “Operated Properties”), for the claim optionee on a cost recovery basis (note 11(c)).

19 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

During the comparative year, Amarc received a non-refundable payment of US$200,000 (CDN$260,115) pursuant to an option agreement whereby an arms-length third party optionee had the right to earn an initial 51% interest in the Windfall Project, comprised of 25 mineral claims located within the IKE district (note 7(a)), by spending US$4.2 million on exploration by October 21, 2022. On May 25, 2021, this option agreement was terminated by mutual consent of both Amarc and the optionee.

Included in cost recoveries are BCMETC refunds totaling $265,929 received in the year ended March 31, 2022 ($820,075 – March 31, 2021; $Nil – March 31, 2020).

On December 16, 2020 (the “Closing Date”), the Company closed the sale of its Newton property (“Newton”) located in south-central British Columbia (“BC”) to Isaac Mining Corp.(“IMC”), an arms- length private company and a wholly-owned subsidiary of Carlyle Commodities Corp. (“Carlyle”) (CSE:CCC, FSE:1OZ, OTC:DLRYF). Amarc has received consideration comprising total cash of $300,000 from IMC and 5.5 million equity units (common share plus warrant) in Carlyle. The 5.5 million warrants are exercisable at $0.50 per warrant with an expiry date of December 8, 2025. The fair value of the 5.5 million shares of Carlyle on the Closing Date was recorded at $907,500, based on a per share value of $0.165, the closing quote of Carlyle’s common shares on December 16, 2020. The fair value of the 5.5 million warrants of Carlyle on the Closing Date is recorded was $727,000 using the Black-Scholes option pricing model. The fair value was calculated based on the following weighted average assumptions: Risk free-interest rate – 0.38%; Dividend yield – 0.00%; Expected volatility – 139.0%; Expected life – 4.98 years.

8.

ACCOUNTS PAYABLE AND ACCRUED LIABILITIES

20 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

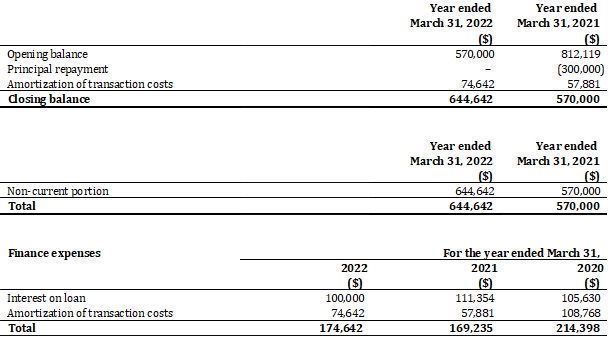

9.

DIRECTOR’S LOAN

In December 2019, the Company entered into a loan extension and amendment agreement (the “Loan”) with a director and significant shareholder of the Company (the “Lender”), pursuant to which a previous loan agreement with a maturity date of November 26, 2019 was extended for five years or earlier pending the achievement of certain financing milestones. The Loan has a principal sum of $1,000,000, is unsecured and bears interest at a rate of 10% per annum. On December 13, 2021, a total of $160,000 in interest was paid.

Pursuant to the Loan, the Company issued to the Lender a loan bonus comprising of 16,000,000 common share purchase warrants (the “Warrants”) with an expiry of five years and an exercise price of $0.05 per share. Refer to note 16.

10.

SHARE CAPITAL AND RESERVES

(a)

Authorized and outstanding share capital

The Company’s authorized share capital consists of an unlimited number of common shares without par value (“Common Shares”) and an unlimited number of preferred shares. All issued Common Shares are fully paid. No preferred shares have been issued.

On August 20, 2020, 3,000,000 flow-through shares were issued pursuant to the exercise of warrants for gross proceeds of $150,000.

On October 2, 2020, 2,000,000 flow-through shares were issued pursuant to the exercise of warrants for gross proceeds of $100,000. $100 related to flow-through tax filing has been deducted from the gross proceeds as issuance costs.

21 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

Approximately $167,000 of the flow-through proceeds received were renounced to the shareholder as at December 31, 2020. The Company recognized no flow-through premium in excess of the fair value of these common shares at their dates of issuance.

On December 2, 2021, 6,000,000 flow-through shares were issued pursuant to the exercise of warrants for gross proceeds of $300,000. The Company recognized no flow-through premium in excess of the fair value of these common shares at their dates of issuance.

As at March 31, 2022, the amount of flow-through proceeds remaining to be expended is approximately $383,000 (March 31, 2021 - $83,000; March 31, 2020 - $nil), which in total must be incurred on or before December 31, 2023. The BCMETC cannot be claimed by the Company on mineral exploration expenses related to meeting expenditure commitments pursuant to the issue of flow-through shares; however, the BCMETC itself, once received, may be used for any purpose.

As at March 31, 2022, there were 186,602,894 (March 31, 2021 – 180,602,894; March 31, 2020 – 175,602,894) Common Shares issued and outstanding.

(b)

Share purchase options

On March 9, 2022, the Company granted 3.48 million incentive stock options to its service providers to acquire an aggregate of 3.48 million common shares at $0.12 per share, for a period of three to five years of which 50% are being granted to insiders. All of the options are subject to required TSXV acceptance and customary vesting provisions over 24 months. The fair value of these warrants at issue was determined to be $366,912 using the Black-Scholes pricing model and based on the following assumptions: risk-free rate of 1.65%; expected volatility of 139%; underlying market price of $0.12; strike price of $0.12; expiry term of 3 - 5 years; and, dividend yield of nil.

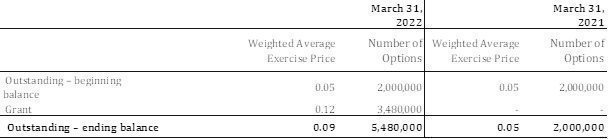

The following summarizes changes in the Company’s share purchase options (the “Options”):

22 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

The following summarizes information on the options outstanding and exercisable as at March 31, 2022:

(c)

Share purchase warrants

The following common share purchase warrants were outstanding at March 31, 2022 and 2021:

(i)

2019 loan bonus warrants

In December 2019, 16,000,000 share purchase warrants were issued pursuant to the Loan (note 9). The fair value of these warrants at issue was determined to be $490,449 at $0.03 per warrant using the Black-Scholes pricing model and based on the following assumptions: risk-free rate of 1.57%; expected volatility of 144%; underlying market price of $0.035; strike price of $0.05; expiry term of 5 years; and, dividend yield of nil.

11.

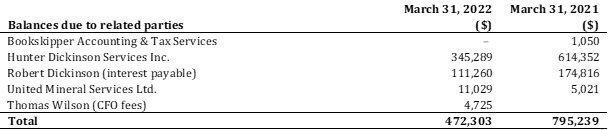

RELATED PARTY TRANSACTIONS

(a)

Transactions with key management personnel

Key management personnel (“KMP”) are those persons that have the authority and responsibility for planning, directing, and controlling the activities of the Company, directly and indirectly, and by definition include all the directors of the Company.

Note 9 includes the details of a director’s loan. Note 7(b) and 7(c) includes the details of the acquisition of mineral property interests from a private entity wholly-owned by one of the directors of the Company.

23 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

During the year ended March 31, 2022 and 2021, the Company’s President, Chief Executive Officer and Director; and Corporate Secretary provided services to the Company under a service agreement with Hunter Dickinson Services Inc. (note 11(b)).

During the year ended March 31, 2022, the Company incurred fees totaling $35,500 (2021 -$10,000) in respect of services provided by Chief Financial Officer.

During the year ended March 31, 2022, the Company recorded share-based compensation expense of $32,747 (March 31, 2021 - $nil; March 31, 2020 - $nil) in relation to 850,000 (March 31, 2021 - nil; March 31, 2020 - nil) stock options issued to directors and officers of the Company.

(b)

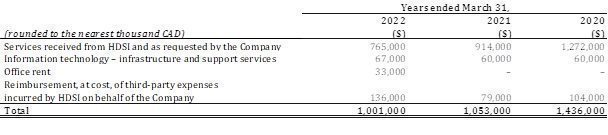

Hunter Dickinson Services Inc.

Hunter Dickinson Inc. (“HDI”) and its wholly-owned subsidiary Hunter Dickinson Services Inc. (“HDSI”) are private companies established by a group of mining professionals. HDSI provides contract services for a number of mineral exploration and development companies, and also to companies that are outside of the mining and mineral development space. Amarc acquires services from a number of related and arms-length contractors, and it is at Amarc’s discretion that HDSI provides certain contract services.

The Company has one director in common with HDSI, namely Robert Dickinson. Also, the Company’s President, Chief Executive Officer and Director, and Corporate Secretary are employees of HDSI and are contracted to work for the Company under an employee secondment agreement between the Company and HDSI.

Pursuant to an agreement dated July 2, 2010, HDSI provides certain cost effective technical, geological, corporate communications, regulatory compliance, and administrative and management services to the

Company, on a non-exclusive basis as needed and as requested by the Company. As a result of this relationship, the Company has ready access to a range of diverse and specialized expertise on a regular basis, without having to engage or hire full-time employees or experts. The Company benefits from the economies of scale created by HDSI which itself serves several clients both within and external to the exploration and mining sector.

The Company is not obligated to acquire any minimum amount of services from HDSI. The monetary amount of the services received from HDSI in a given period of time is a function of annually set and agreed charge-out rates for and the time spent by each HDSI employee engaged by the Company.

HDSI also incurs third-party costs on behalf of the Company. Such third-party costs include, for example, capital market advisory services, communication services and office supplies. Third-party costs are billed at cost, without markup.

There are no ongoing contractual or other commitments resulting from the Company’s transactions with HDSI, other than the payment for services already rendered and billed. The agreement may be terminated upon 60 days’ notice by either the Company or HDSI.

24 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

The following is a summary of transactions with HDSI that occurred during the reporting period:

(c)

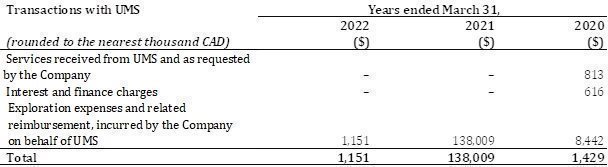

United Mineral Services Ltd.

United Mineral Services Ltd. (“UMS”) is a private company wholly-owned by one of the directors of the Company. UMS is engaged in the acquisition and exploration of mineral property interests. The following is a summary of transactions with UMS that occurred during the reporting period:

Refer also to note 9.

12.

SUPPLEMENTARY INFORMATION TO THE CONSOLIDATED STATEMENTS OF LOSS

(a)

Employees’ salaries and benefits

The employees’ salaries and benefits included in exploration and evaluation expenses and administration expenses are as follows:

(1) rounded to the nearest thousand dollar

(2) includes salaries and benefits included in office and administration expenses (note 12(b)) and other salaries and benefits expenses classified as administration expenses

25 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

(b)

Office and administration expenses

Office and administration expenses include the following:

(1) rounded to the nearest thousand dollar

13.

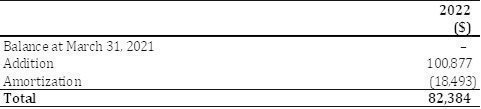

OFFICE LEASE – RIGHT OF USE ASSET AND LEASE LIABILITY

The Company subleases corporate offices in Vancouver, BC from HDSI under a lease agreement dated May 1, 2021, and the lease expires on April 29, 2026. Refer to Note 2 (o) for details regarding the 2019 adoption of IFRS 16.

Right-of-use asset

A summary of the changes in the right-of-use asset for the year ended March 31, 2022 and 2021 is as follows:

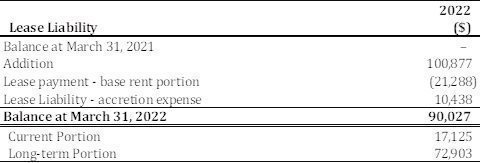

Lease liability

On May 1, 2021, the Company entered into lease agreement which resulted in the lease liability of

$100,877 (undiscounted value of $134,766, discount rate used is 12.00%). This liability represents the monthly lease payment from May 1, 2021 to April 29, 2026, the end of the lease term less abatement granted by HDSI.

A summary of changes in the lease liability during the year ended March 31, 2022 and 2021 are as follows:

26 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

The following is a schedule of the Company’s future lease payments (base rent portion) under

lease obligations:

14.

INCOME TAXES

(a)

Provision for current tax

No provision has been made for current income taxes as the Company has no taxable income.

(b)

Provision for deferred tax

As future taxable profits of the Company are uncertain, no deferred tax asset has been recognized.

At March 31, 2022, the Company has unused non-capital loss carry forwards of approximately $11,00,000 (March 31, 2021 - $10.7 million; March 31, 2020 - $9.8 million).

At March 31, 2022, the Company has resource tax pools of approximately $31,000,000 (March 31, 2021 - $31 million; March 31, 2020 - $31.3 million) available in Canada, which may be carried forward and utilized to offset future taxes related to certain resource income.

(c)

Reconciliation of effective tax rate

March 31,

2022

March 31,

2020

Income (loss) for the year

$

1,078,937

$

1,360,699

Total income tax expense

–

–

Loss excluding income tax

1,078,937

1,360,699

Income tax expense (recovery) using the Company’s tax rate

(291,000

)

367,000

Non-deductible expenses and other

107,000

(577,000

)

Temporary difference booked to reserve

(199,000

)

16,000

Deferred income tax assets not recognized

383,000

194,000

The Company’s statutory tax rate was 27% (2021 – 27%; 2020 – 27%) and its effective tax rate is nil (2021 – nil; 2020 – nil).

27 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

(d)

Deductible temporary differences

At March 31, 2022, the Company had the following deductible temporary differences for which no deferred tax asset was recognized:

Expiry

Tax losses

(capital)

��

Tax losses (non-capital)

Resources

pools

Other

Within one year

$

–

$

–

$

–

$

–

One to five years

–

–

–

–

After five years

–

11,423,000

–

1,011,000

No expiry date

2,030,000

–

31,210,000

77,000

$

2,030,000

$

11,423,000

$

31,210,000

$

1,088,000

15.

FINANCIAL RISK MANAGEMENT

(a)

Capital management objectives

The Company’s primary objectives when managing capital are to safeguard the Company’s ability to continue as a going concern so that it can continue to provide returns for shareholders, and to have sufficient liquidity available to fund ongoing expenditures and suitable business opportunities as they arise.

The Company considers the components of shareholders’ equity as well as its cash as capital. The Company manages its capital structure and makes adjustments to it in light of changes in economic conditions and the risk characteristics of the underlying assets. In order to maintain or adjust the capital structure, the Company may issue equity, sell assets, or return capital to shareholders as well as issue or repay debt.

The Company’s investment policy is to invest its cash in highly liquid, short-term, interest-bearing investments having maturity dates of three months or less from the date of acquisition, which are readily convertible into known amounts of cash.

The Company is not subject to any imposed equity requirements.

There were no changes to the Company’s approach to capital management during the year ended March 31, 2022.

(b)

Carrying amounts and fair values of financial instruments

The Company’s marketable securities are carried at fair value based on quoted prices in active markets.

As at March 31, 2022 and 2021, the carrying values of the Company’s financial assets and financial liabilities approximate their fair values.

(c)

Financial instrument risk exposure and risk management

28 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

The Company is exposed in varying degrees to a variety of financial instrument-related risks. The Board of Directors approves and monitors the risk management processes, inclusive of documented treasury policies, counterparty limits, and controlling and reporting structures. The type of risk exposure and the way in which such exposure is managed is provided as follows:

Credit risk

Credit risk is the risk of potential loss to the Company if a counterparty to a financial instrument fair to meet its contractual obligations. The Company’s credit risk is primarily attributable to its liquid financial assets, including cash, and amounts receivable and other assets. The carrying values of these financial assets represent the Company’s maximum exposure to credit risk.

The Company limits the exposure to credit risk by only investing its cash in high-credit quality financial institutions in business and savings accounts, which are available on demand by the Company for its programs.

Liquidity risk

Liquidity risk is the risk that the Company will encounter difficulty in meeting the obligations associated with its financial liabilities that are settled by delivering cash or other financial assets. The Company ensures that there is sufficient cash in order to meet its short-term business requirements after taking into account the Company’s holdings of cash.

The Company has sufficient cash to meet its commitments associated with its financial liabilities in the near term, other than the amounts payable to related parties.

Interest rate risk

The Company is subject to interest rate risk with respect to its investments in cash. The Company’s policy is to invest cash at variable rates of interest and cash reserves are to be maintained in cash in order to maintain liquidity, while achieving a satisfactory return for shareholders. Fluctuations in interest rates when cash matures impact interest income earned.

As at March 31, 2022 and 2021, the Company’s exposure to interest rate risk was nominal. Price risk

Equity price risk is defined as the potential adverse impact on the Company’s earnings due to movements in individual equity prices or general movements in the level of the stock market. The Company is subject to price risk in respect of its investments in marketable securities.

As at March 31, 2022 and 2021, the Company’s exposure to price risk was not significant in relation to these Financial Statements.

16.

EVENTS AFTER THE REPORTING PERIOD

The Company entered into a Second Loan Amendment Agreement dated May 25, 2022, pursuant to which it has agreed to a $100,000 increase to an existing $ 1 million loan (the “Loan”) with the related party lender disclosed at note 9 (the “Lender”). The Loan is unsecured, will bear interest at a rate of 10% per annum and is repayable on or before the earlier of November 26, 2024, the occurrence of a default or on achievement of financing milestones.

29 | Page

AMARC RESOURCES LTD.

Notes to the Consolidated Financial Statements

For the years ended March 31, 2022, 2021 and 2020

In connection with this Loan, Amarc will issue to the Lender a loan bonus in the form of 1,176,470 warrants (the "Bonus Warrants"), each entitling the holder to acquire one common share of Amarc until November 26, 2024 at a price of $0.085 per share. The Bonus Warrants will be subject to a four month hold period commencing from the date of issuance thereof. The Loan and Bonus Warrants are subject to acceptance by the TSX Venture Exchange.

The Loan proceeds are being used to pay the initial option requirement of $100,000 for a five BC mineral claims group option dated May 16, 2022, from an arm’s length optionor. Total additional option payments are a further $900,000 at $100,000 per year, payable on or before May 31 of each year (total option payments are $1,000,000). The property is subject to a 2% NSR royalty, of which 1.5% is capped at $10 million.

On June 15, a separate 6-month facility 12% interest was included in the Loan Amendment, which can be accessed by the Company upon the determination of the Company’s entitlement to near-term receipt of BCMETC.

On July 8, 2022, the Company announced that it had engaged Kin Communications Inc. (“Kin”) to assist with its investor relations activities. Under the terms of the Investor Relations Agreement with Kin, Kin has agreed to assist Amarc with investor relations, including communicating with and marketing to potential investors, shareholders and media contacts for a period of twelve months and on a month-to-month basis thereafter. In consideration for the services, the Company has agreed to pay Kin $12,500 per month for the initial 12-month period. In addition, the Company has granted Kin stock options entitling it to purchase 1,000,000 of the Company’s common shares at a price of $0.11 per share with a five-year term, vesting in three instalments of 33%, 33% and 34%, with the first instalment vesting 90 days after the Effective Date of the Investor Relations Agreement.

30 | Page

We use cookies on this site to provide a more responsive and personalized service. Continuing to browse, clicking I Agree, or closing this banner indicates agreement. See our Cookie Policy for more information.