UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934

Filed by the Registrant ☒ | Filed by a Party other than the Registrant ☐ |

Check the appropriate box:

☐ | Preliminary Proxy Statement |

☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

☒ | Definitive Proxy Statement |

☐ | Definitive Additional Materials |

☐ | Soliciting Material Pursuant to §240.14a-12 |

CytoDyn Inc.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

☒ | No fee required. |

☐ | Fee paid previously with preliminary materials. |

☐ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a6(i)(1) and 0-11. |

CYTODYN INC.

1111 Main Street, Suite 660

Vancouver, Washington 98660

(360) 980-8524

September 25, 2023

Dear CytoDyn Stockholder:

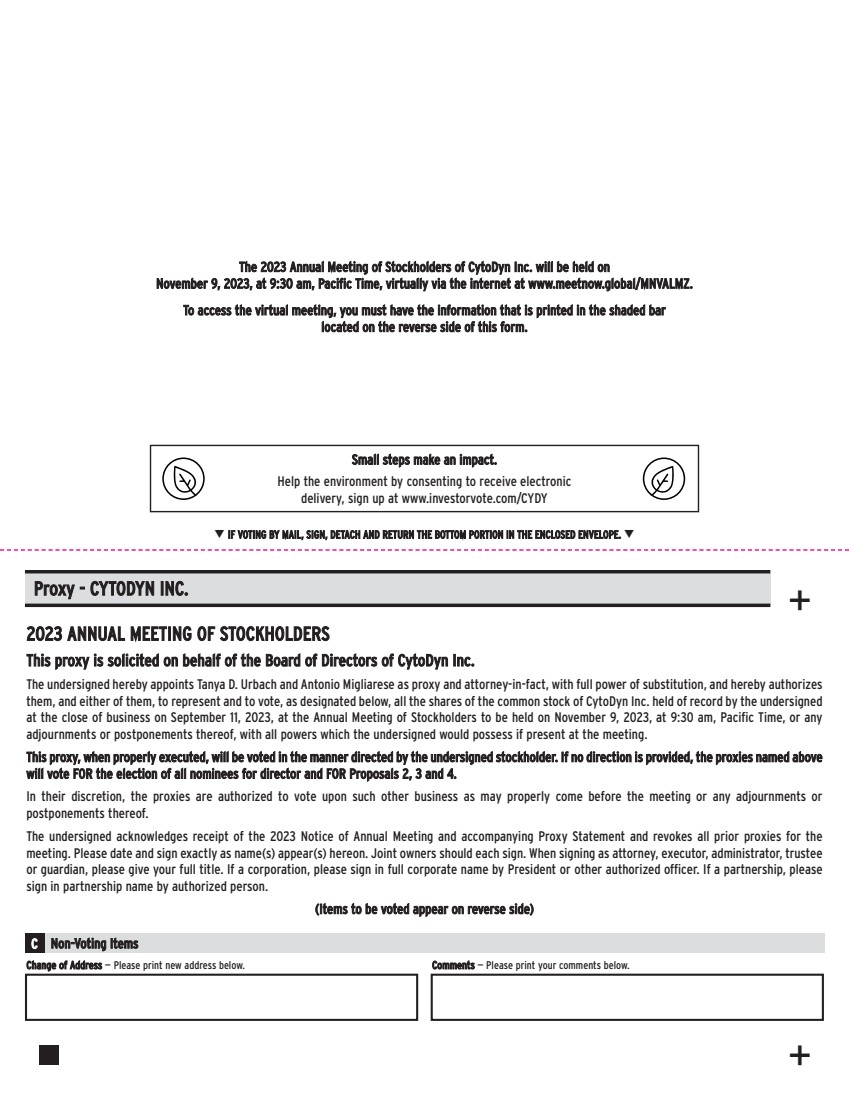

You are cordially invited to virtually attend the 2023 Annual Meeting of Stockholders of CytoDyn Inc. (the “Company”) to be held solely online via a live webcast at 9:30 a.m., Pacific Time, on November 9, 2023 at www.meetnow.global/MNVALMZ. There is no physical location for the Annual Meeting. To attend and vote at the Annual Meeting, you must be a stockholder of record as of the close of business on September 11, 2023, or hold a legal proxy, as explained in the “Voting, Revocation, and Solicitation of Proxies” and “Attendance at the Annual Meeting” sections of the accompanying proxy statement.

The matters to be presented for action at the Annual Meeting are (i) the election of five directors to our Board of Directors; (ii) approval, on an advisory (non-binding) basis, of our named executive officer compensation; (iii) a proposal to increase the total number of authorized shares of common stock from 1,350,000,000 to 1,750,000,000 shares; and (iv) a proposal for the adjournment of the Annual Meeting to solicit additional proxies, if there are insufficient votes at the Annual Meeting to approve the share increase proposal, as further described in the enclosed proxy statement. We may also act on such other business as may properly come before the Annual Meeting.

We are excited about the future of our company. It is vitally important that your shares are represented and voted, whether or not you are able to attend the virtual meeting. We urge you to promptly vote and submit your proxy (1) via the Internet, (2) by phone, or (3) if you received your proxy materials by mail, by signing, dating, and returning the enclosed proxy card or voting instruction form in the envelope provided for your convenience.

Sincerely,

Antonio Migliarese

Chief Financial Officer and Interim President

If you have any questions or require any assistance in voting your shares, please call:

Alliance Advisors LLC

200 Broadacres Drive, 3rd Floor, Bloomfield, NJ 07003

(833) 814-9456

CYTODYN INC.

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

NOVEMBER 9, 2023

You are invited to virtually attend the 2023 Annual Meeting of Stockholders (the “Annual Meeting”) of CytoDyn Inc., a Delaware corporation (the “Company”), to be held at 9:30 a.m., Pacific Time, on November 9, 2023, via a live webcast at www.meetnow.global/MNVALMZ.

The Board of Directors has fixed September 11, 2023 as the record date for the meeting. Only stockholders of record at the close of business on September 11, 2023, or who hold a legal proxy, are entitled to notice of, to vote at, and to virtually attend the Annual Meeting or any postponements or adjournments thereof. Please refer to the “Voting, Revocation, and Solicitation of Proxies” and “Attendance at the Annual Meeting” sections of the accompanying Proxy Statement for additional information.

The Annual Meeting is being held to consider and vote on the following matters:

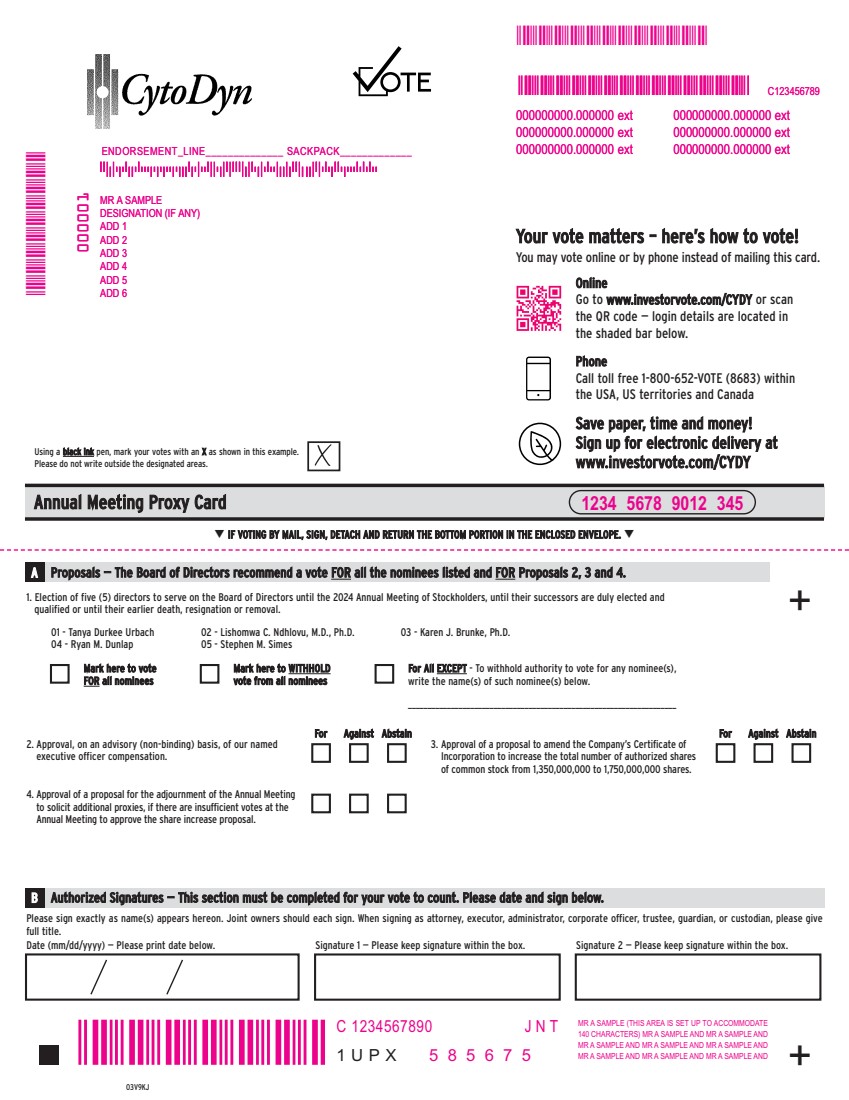

| 1. | Election of five (5) directors to serve on the Board of Directors until the 2024 Annual Meeting of Stockholders, until their successors are duly elected and qualified or until their earlier death, resignation or removal; |

| 2. | Approval, on an advisory (non-binding) basis, of our named executive officer compensation; |

| 3. | Approval of a proposal to amend the Company’s Certificate of Incorporation to increase the total number of authorized shares of common stock from 1,350,000,000 to 1,750,000,000 shares; |

| 4. | Approval of a proposal for the adjournment of the Annual Meeting to solicit additional proxies, if there are insufficient votes at the Annual Meeting to approve the share increase proposal; and |

| 5. | Transaction of any other business as may properly come before the Annual Meeting or any postponements or adjournments thereof. |

Whether or not you are able to virtually attend the meeting, please promptly vote and submit your proxy (1) via the internet, (2) by phone, or (3) if you received your proxy materials by mail, by signing, dating, and returning the enclosed proxy card or voting instruction form in the envelope provided for your convenience. If you are a stockholder of record at the close of business on September 11, 2023, or hold a legal proxy, and virtually attend the Annual Meeting, you may revoke your proxy and vote your shares at the meeting.

The Board of Directors of the Company recommends that you vote “FOR” the election of the Board’s nominees for directors named in this Proxy Statement, as well as “FOR” Proposals 2, 3 and 4 above, using the enclosed proxy card.

We urge you to read this Proxy Statement carefully and to vote promptly through the internet, by telephone, or by mail. This will ensure the presence of a quorum at the meeting. For instructions on voting, please refer to the instructions on the Notice of Internet Availability of Proxy Materials you received in the mail. You can request to receive proxy materials by mail or e-mail as well. Promptly voting your shares via internet, by telephone, or by signing, dating, and returning the proxy card or voting instruction form, will save us the expense and extra work of additional solicitation.

| | |

By Order of the Board of Directors | | |

| | |

Tyler Blok | | |

Secretary | | |

Vancouver, Washington | | |

September 25, 2023 | | |

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF PROXY MATERIALS FOR THE ANNUAL

STOCKHOLDERS’ MEETING TO BE HELD ON NOVEMBER 9, 2023:

This Proxy Statement and our Annual Report on Form 10-K for the fiscal year ended May 31, 2023, are available at www.investorvote.com/CYDY.

PROXY STATEMENT

2023 ANNUAL MEETING OF STOCKHOLDERS

This Proxy Statement is furnished in connection with the solicitation of proxies by the Board of Directors (the “Board”) of CytoDyn Inc., a Delaware corporation (“CytoDyn” or the “Company”), to be voted at our Annual Meeting of Stockholders to be held on November 9, 2023 at 9:30 a.m., Pacific Time, in a solely virtual format (the “Annual Meeting”), and any postponements or adjournments thereof. There is no physical location for the Annual Meeting. Website references throughout this document are provided for convenience only, and the content on the referenced website is not incorporated by reference into this document.

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF PROXY MATERIALS

Our proxy materials are available at www.investorvote.com/CYDY. The following materials are available for review:

| ● | Proxy Statement; |

| ● | Our Annual Report on Form 10-K for the fiscal year ended May 31, 2023; |

| ● | Notice of Internet Availability of Proxy Materials; and |

| ● | Proxy Card. |

We will provide electronic access to our proxy materials on or about September 27, 2023. Also, on or about September 27, 2023, we will begin mailing to our stockholders the Notice of Internet Availability of Proxy Materials, which contains instructions on how to access the Proxy Statement via the internet and how to vote online. The Securities and Exchange Commission (the “SEC”) allows the delivery of proxy materials to stockholders over the internet. We believe that this offers a convenient way for stockholders to review the proxy materials, while also reducing printing and mailing expenses and lessening the environmental impact of paper copies.

VOTING, REVOCATION, AND SOLICITATION OF PROXIES

Solicitation of Proxies. Proxies to vote at the Annual Meeting are being solicited by and on behalf of the Board, with the cost of solicitation borne by the Company. Solicitation may also be made by directors, officers and employees of the Company in person, by telephone or otherwise without additional compensation for such services.

Voting. You may submit a proxy to have your shares of common stock voted at the Annual Meeting in one of three ways: (1) via the internet, (2) by phone, or (3) if you received your proxy materials by mail, by signing, dating, and returning the enclosed proxy card or voting instruction form in the envelope provided for your convenience. When a proxy is properly returned, the shares represented by the proxy will be voted at the Annual Meeting in accordance with the instructions specified in the spaces provided in the proxy. If no instructions are specified, the proxies will be counted for purposes of determining whether or not a quorum is present and will be voted in accordance with the recommendations of our Board, as stated in the Notice of Annual Meeting of Stockholders. If a stockholder of record as of the close of business on September 11, 2023, or a holder of a legal proxy, virtually attends the Annual Meeting, he or she may vote at the Annual Meeting. If you hold shares through a broker or nominee (that is, in “street name”), please follow their directions on how to vote your shares.

1

Banks and brokers acting as nominees are permitted to use discretionary voting authority to vote proxies for proposals that are deemed “routine” by the New York Stock Exchange but are not permitted to use discretionary voting authority to vote proxies for proposals that are deemed “non-routine” by the New York Stock Exchange. Although the New York Stock Exchange may not announce which proposals will be deemed routine until after the date on which this Proxy Statement has been mailed to you, we expect that the election of directors and advisory vote on named executive officer compensation will be deemed non-routine. As such, it is important that you provide voting instructions to your bank, broker or other nominee, if you wish to direct the voting of your shares.

Revocation of Proxies. Proxies may be revoked by written notice delivered in person or mailed to the Secretary of the Company or by submitting a later-dated proxy prior to a vote being taken at the Annual Meeting. Attendance at the Annual Meeting alone will not revoke a previously submitted proxy. If you hold shares through a broker or nominee (that is, in “street name”), please follow their directions on how to revoke previously submitted voting instructions relating to your shares.

ATTENDANCE AT THE ANNUAL MEETING

If you are a registered stockholder (i.e., you hold your shares through our transfer agent, Computershare), you do not need to register to attend the Annual Meeting virtually on the internet. Please follow the instructions on the notice or proxy card that you received.

If you hold your shares through an intermediary, such as a bank or broker, you must obtain a legal proxy and register in advance to attend the Annual Meeting virtually on the internet. To register, you must submit proof of your proxy power (legal proxy) from the broker reflecting your CytoDyn Inc. holdings, along with your name and email address, to our transfer agent, Computershare. Requests for registration must be labeled as “CytoDyn Inc. Legal Proxy” and be received no later than 5:00 p.m., Eastern Time, on November 6, 2023. You will receive a confirmation of your registration by email after we receive your registration materials.

Requests for registration should be directed to us at the following:

By email

Forward the email from your broker, or attach an image of your legal proxy, to

legalproxy@computershare.com

By mail

Send to:

Computershare

CytoDyn Inc. Legal Proxy

P.O. Box 43001

Providence, RI 029403001

The virtual meeting platform is fully supported across browsers (MS Edge, Firefox, Chrome and Safari) and devices (desktops, laptops, tablets and cell phones) running the most up-to-date version of applicable software and plugins. Note: Internet Explorer is not a supported browser. Participants should ensure that they have a strong WiFi and internet connection from wherever they intend to participate in the meeting. We encourage you to access the meeting prior to the start time. For further assistance should you need it, you may call 1-866-641-4276.

OUTSTANDING VOTING SECURITIES AND QUORUM

Under our Amended and Restated Certificate of Incorporation, as amended, only shares of common stock, par value $0.001 per share, of the Company are entitled to vote at the Annual Meeting. Stockholders of record as of the close of business on September 11, 2023, are entitled to one vote at the Annual Meeting for each share of common stock then held by the stockholder. As of that date, the Company had 930,960,097 shares of common stock issued and outstanding. The presence, in person (by attendance at the virtual meeting) or by proxy, of at least a majority of the total number of

2

outstanding shares of common stock entitled to vote will constitute a quorum at the Annual Meeting. Abstentions will be considered present for purposes of determining the presence of a quorum at the Annual Meeting.

A broker “non-vote” occurs when a proposal is deemed “non-routine” and a nominee holding shares for a beneficial owner does not have discretionary voting authority with respect to the matter being considered and has not received instructions from the beneficial owner. Broker non-votes will not be considered present for purposes of determining the presence of a quorum at the Annual Meeting if the New York Stock Exchange (the “NYSE”) determines that none of the proposals are “routine,” but will be considered present for purposes of determining the presence of a quorum at the Annual Meeting if the NYSE determines that one or more of the proposals is routine. As of the date of this Proxy Statement, we believe that the NYSE will determine that Proposals 1 and 2 are non-routine, but that Proposals 3 and 4 are routine.

VOTES REQUIRED

Pursuant to the General Corporation Law of the State of Delaware and our Amended and Restated By-laws (our “By-laws”), the five nominees for election as directors at the Annual Meeting who receive the highest number of affirmative votes will be elected, provided that a quorum is present at the Annual Meeting. Proposal 2 will be approved, on an advisory basis, if a quorum exists and the votes cast “for” the proposal exceed the votes cast “against” the proposal. Proposal 3 will be approved only if it receives the affirmative votes of a majority of the outstanding shares of common stock of the Company entitled to vote at the Annual Meeting. Proposal 4 will be approved if a quorum exists and the votes cast favoring the proposal exceed the votes cast opposing the proposal. If a quorum is present, shares that are not represented at the Annual Meeting, shares that abstain from voting, and broker non-votes, if any, will have no effect on the outcome of voting on Proposals 1, 2, and 4 but will have the effect of a vote against Proposal 3.

3

SUMMARY TERM SHEET

The following is only a summary of certain material information contained in this document. You should carefully review this entire document to understand the proposals fully.

| ● | Time and Place of Annual Meeting (see Notice of Annual Meeting of Stockholders): 9:30 a.m., Pacific Time, on November 9, 2023, solely in virtual format. Stockholders of record as of the close of business on September 11, 2023, or holding a legal proxy, may access the Annual Meeting virtually at www.meetnow.global/MNVALMZ. See “Attendance at the Annual Meeting” above for additional information on how to access the Annual Meeting. |

| ● | Record Date (see page 2): You are entitled to vote on the proposals to be presented at the Annual Meeting if you owned common stock of the Company as of the close of business on September 11, 2023, either of record or in street name. |

| ● | Proposals to be Voted on (see Notice of Annual Meeting of Stockholders): Matters to be presented for action at the meeting include (i) election of five (5) directors to serve on the Board until the 2024 Annual Meeting of Stockholders, until their successors are duly elected and qualified or until their earlier death, resignation or removal; (ii) approval, on an advisory (non-binding) basis, of our named executive officer compensation; (iii) approval of a proposal to amend the Company’s Certificate of Incorporation to increase the total number of authorized shares of common stock from 1,350,000,000 to 1,750,000,000 shares; and (iv) a proposal for the adjournment of the Annual Meeting to solicit additional proxies, if there are insufficient votes at the Annual Meeting to approve Proposal 3. |

| ● | Recommendation of the Board (see pages 13-18): The Board recommends that you vote “FOR” the election of the Board’s nominees for director named in this Proxy Statement, as well as “FOR” Proposals 2, 3 and 4 above. |

| ● | Vote Required: Pursuant to the General Corporation Law of the State of Delaware and our By-laws, the five nominees for election as directors at the Annual Meeting who receive the highest number of affirmative votes will be elected, provided that a quorum is present at the Annual Meeting. Proposal 2 will be approved, on an advisory basis, if a quorum exists and the votes cast “for” the proposal exceed the votes cast “against” the proposal. Proposal 3 will be approved only if it receives the affirmative votes of a majority of the outstanding shares of common stock of the Company entitled to vote at the Annual Meeting. Proposal 4 will be approved if a quorum exists and the votes cast favoring the proposal exceed the votes cast opposing the proposal. If a quorum is present, shares that are not represented at the Annual Meeting, shares that abstain from voting, and broker non-votes, if any, will have no effect on the outcome of voting on Proposals 1, 2, and 4 but will have the effect of a vote against Proposal 3. |

| ● | How to Vote Your Shares (see page 1): You may submit a proxy to have your shares of common stock voted at the Annual Meeting in one of three ways: (1) via the internet, (2) by phone, or (3) if you received your proxy materials by mail, by signing, dating, and returning the enclosed proxy card or voting instruction form in the envelope provided for your convenience. In order to assure that your vote is recorded, please submit your proxy even if you are a stockholder of record as of the close of business on September 11, 2023, and currently plan to virtually attend the Annual Meeting. |

| ● | How to Revoke Your Proxy (see page 2): Proxies may be revoked by written notice delivered in person or mailed to the Secretary of the Company or by submitting a later-dated proxy prior to a vote being taken at the Annual Meeting. Attendance at the Annual Meeting alone will not be sufficient to revoke a previously submitted proxy. If you hold shares through a broker or nominee (that is, in “street name”), please follow their directions on how to revoke previously submitted instructions relating to your shares. |

4

| ● | Voting of Shares Held in “Street Name” (see pages 1-2): Your broker is permitted to use discretionary voting authority to vote proxies for proposals that are deemed “routine” by the NYSE but is not permitted to use discretionary voting authority to vote proxies for proposals that are deemed “non-routine” by the NYSE. The determination of which proposals are deemed routine versus non-routine may not be made by the NYSE until after the date on which this Proxy Statement has been mailed to you. As such, it is important that you provide voting instructions to your bank, broker or other nominee, if you wish to direct the voting of your shares. |

| ● | Whom You Should Contact with Questions: If you have further questions, you may contact the Company’s proxy solicitor, Alliance Advisors LLC, at: |

Alliance Advisors LLC

200 Broadacres Drive, 3rd Floor, Bloomfield, NJ 07003

(833) 814-9456

5

INFORMATION ABOUT OUR BOARD OF DIRECTORS

Directors and Board Committees

The following table lists each of our five current directors and sets forth information about their committee memberships:

| | | | | | Board committees | ||||

Director name | | Age | | Independent | | Audit | | Compensation | | Nom/Gov |

Tanya D. Urbach, Board Chair |

| 56 |

| Yes |

| M |

| M |

| C |

Lishomwa C. Ndhlovu, M.D., Ph.D. | | 53 | | Yes | | | | | | M |

Karen J. Brunke, Ph.D. | | 71 | | Yes | | | | M | | |

Ryan M. Dunlap | | 53 | | Yes | | C | | | | M |

Stephen M. Simes | | 71 | | Yes | | M | | C | | |

Cindicates chair of respective board committee.

Mindicates member of respective board committee.

Board Meetings and Executive Sessions

The Board held 13 meetings during the Company’s fiscal year ended May 31, 2023. During fiscal year 2023, each of the then-current directors attended at least 75 percent of the total number of the meetings of the Board and the meetings held by each committee of the Board on which they served during their tenure on such committee or the Board.

It is our policy that our Board members attend our Annual Meeting. At our 2022 Annual Meeting, all then-current Board members participated in the virtual Annual Meeting.

Board Leadership Structure

Our Board is currently chaired by our non-employee independent director Tanya D. Urbach. Ms. Urbach has served as Board Chair since January 2022. The Board believes its current Board leadership structure, which reflects the separation of the Chair and Principal Executive Officer position, enables the Board to govern in the best interests of the Company and its stockholders.

The Board’s Role in Risk Oversight

Our management is responsible for identifying, assessing, and managing the material risks we face. The Board generally oversees risk management practices and processes and, both as a whole and through the Audit Committee, periodically discusses with management strategic and financial risks associated with our operations, their potential impact on us, and the steps taken to manage these risks.

While the Board is ultimately responsible for risk oversight, the Board’s committees assist the Board in fulfilling its oversight responsibilities in certain areas of risk. In particular, the Audit Committee focuses on financial and enterprise risks and discusses with management and our independent registered public accounting firm our policies and practices with respect to risks and particular areas of risk exposure. The Nominating and Corporate Governance Committee oversees recruitment of potential director nominees and succession planning for our executive positions. The Compensation Committee monitors our incentive compensation programs to assure that management is not encouraged to take actions involving excessive risk.

6

Code of Ethics and Business Conduct

We have adopted a Code of Ethics and Business Conduct and a Statement of Insider Trading Policy and Related Trading Procedures. Copies of these governing documents, as well as the committee charters described below, are available on our website at www.cytodyn.com under the Investors/Corporate Governance tabs. The Company intends to disclose any amendments to its Code of Ethics and Business Conduct, or any waivers of the requirements thereof, on its website at the address and location specified above, to the extent permitted or required by applicable SEC rules.

Director Independence

We are not a “listed issuer” as that term is used in Regulation S-K Item 407 adopted by the SEC. However, in determining director independence, we use the definition of independence in Rule 5605(a)(2) and Rule 5605(c)(2) of the listing rules of The Nasdaq Stock Market (the “Nasdaq Rules”).

The Board has determined that all of our current directors, Ms. Urbach, Drs. Brunke and Ndhlovu, and Messrs. Dunlap and Simes, are independent as defined in the Nasdaq Rules and none of them otherwise has a relationship that, in the opinion of the Board, would interfere with their exercise of independent judgment in carrying out the responsibilities of a director. See also “Related Person Transactions” below.

Dr. Ndhlovu served on the Company’s Scientific Advisory Board for a period of time. As compensation for that service, Dr. Ndhlovu was granted an option to purchase 50,000 shares of common stock with an exercise price of $3.36 per share that will expire on August 31, 2030, and an option to purchase an additional 50,000 shares of common stock with an exercise price of $0.50 per share that will expire on September 6, 2032. The awards were not subject to disclosure under Regulation S-K Item 404(a), but the Board took them into consideration in determining that Dr. Ndhlovu is independent under the Nasdaq Rules.

Committees of Our Board

Our Board’s committee structure currently consists of three principal committees: the Audit Committee, the Compensation Committee, and the Nominating and Corporate Governance Committee. Our Board has adopted a written charter for each of its committees. A copy of each committee’s charter is available on our website at www.cytodyn.com under the Investors/Corporate Governance tabs. A brief description of the composition and the primary responsibilities of our committees is set forth below.

Audit Committee

The primary role of the Audit Committee is to oversee the Company’s financial reporting and disclosure process. The Audit Committee is responsible for overseeing the work done by our independent auditors and reviewing and discussing with management and the independent auditors the adequacy and effectiveness of our financial reporting process, the annual audited financial statements, and the results of the annual audit. The Audit Committee is also responsible for reviewing and approving in advance all contemplated related-party transactions such as those described under “Related Person Transactions” below. The Audit Committee held five meetings during fiscal year 2023, of which four meetings were held to review our financial statements with the auditors following the end of each fiscal quarter prior to their inclusion in reports filed with the SEC.

The members of our Audit Committee are currently Mr. Dunlap, Chair, Ms. Urbach, and Mr. Simes, each of whom is an independent director. For a portion of fiscal year 2023, Ms. Brunke and Dr. Ndhlovu also served on the Audit Committee, each of whom is also an independent director.

The Board has determined that each current member of the Audit Committee is financially sophisticated under the Nasdaq Rules. The Board has also determined that Mr. Dunlap is an “audit committee financial expert” as defined in Regulation S-K Item 407(d)(5)(ii) adopted by the SEC. All current members of the Audit Committee are considered independent because they satisfy the independence requirements prescribed by the Nasdaq Rules, including those set forth in Rule 10A-3 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

7

Compensation Committee

The Compensation Committee reviews and approves our overall compensation philosophy and determines base salaries and other forms of compensation to be paid to executive officers, including cash incentive compensation and grants of options and other stock-based awards. The Compensation Committee is also responsible for making recommendations to the Board with respect to new compensation plans, including incentive compensation plans and equity-based plans, and changes in director compensation. The Compensation Committee held eight meetings during fiscal year 2023.

Our Compensation Committee currently consists of Mr. Simes, Chair, Ms. Urbach, and Dr. Brunke, each of whom is an independent director. Dr. Ndhlovu, who is also an independent director, served on the Compensation Committee for a portion of fiscal year 2023.

The Board has reviewed the source of compensation received by each director currently serving on the Compensation Committee and determined that no director receives compensation from any person or entity that would impair their ability to make independent judgments about our Company’s executive compensation. The Board has also reviewed all affiliations of the directors currently serving on the Compensation Committee with our Company and its affiliates, and determined that there is no relationship that would impair their ability to make independent judgments about our Company’s executive compensation.

Nominating and Corporate Governance Committee

The Nominating and Corporate Governance Committee identifies individuals qualified to become members of the Board, makes recommendations to the Board with regard to the size and composition of the Board and committees thereof, and evaluates the Board and its members. The Nominating and Corporate Governance Committee also assists the Board in recruiting and developing succession and continuity plans for principal officer positions. The Nominating and Corporate Governance Committee held three meetings during fiscal year 2023.

The current members of the Nominating and Corporate Governance Committee are Ms. Urbach, Chair, Dr. Ndhlovu, and Mr. Dunlap, each of whom is an independent director. Dr. Brunke, who is also an independent director, served on the Nominating and Corporate Governance Committee for a portion of fiscal year 2023.

The Nominating and Corporate Governance Committee does not have any specific, minimum qualifications for director candidates. In evaluating potential director nominees, the Nominating and Corporate Governance Committee will consider, among other factors:

| ● | demonstration of ethical behavior; |

| ● | positions of leadership that demonstrate the ability to exercise sound judgment in a wide variety of matters; |

| ● | the candidate’s ability to commit sufficient time to the position; |

| ● | the candidate’s understanding of our business and operations; and |

| ● | the need to satisfy independence requirements relating to Board composition. |

The Nominating and Corporate Governance Committee evaluates all candidates for director thoroughly, whether they are recommended by the management team, stockholders, or third parties, in accordance with the needs of the Board and the qualifications of the candidate. Stockholders who have recommendations for future director candidates may contact the Board at the Company’s address, 1111 Main Street, Suite 660, Vancouver, Washington 98660.

Prior to each annual meeting of stockholders, the Nominating and Corporate Governance Committee evaluates the current composition of the Board in determining whether to recommend the nomination of current directors for re-election. As authorized under its charter, the Nominating and Corporate Governance Committee, as deemed necessary, engages and works with a third-party search firm to assist the committee in locating, recruiting, and vetting potential candidates for election or appointment as directors.

8

The Nominating and Corporate Governance Committee considers diversity in identifying nominees for director, and recognizes that maintaining a diverse membership with varying backgrounds, perspectives, skills, experiences, and other differentiating personal characteristics promotes inclusiveness, enhances the Board’s deliberations, and enables the Board to better serve as effective, engaged stewards of our stockholders’ interests.

When considering directors and nominees, the Nominating and Corporate Governance Committee and the Board focus primarily on the information disclosed in each individual’s resume, references, questionnaire, background check, and personal interview. See “Proposal 1 Election of Directors” for information regarding our five current directors, who have been recommended for re-election as directors by the Nominating and Corporate Governance Committee.

Anti-Hedging Policy

The Board has adopted a policy that prohibits our employees (including officers) and directors, or any of their designees, from engaging in transactions in our capital stock that could create the appearance of misalignment between an employee or director and stockholders and/or create a heightened compliance risk. Engaging in transactions or purchasing financial instruments that hedge or offset, or are designed to hedge or offset, any decrease in the market value of any securities of the Company held by our employees or directors is prohibited. Prohibited transactions include, but are not limited to, zero-cost collars and forward sale contracts.

Director Compensation

During fiscal year 2023, our non-employee director compensation program provided for: (i) $40,000 in annual cash retainer; (ii) an additional annual cash retainer of $30,000 for service as Lead Independent Director or independent Board Chair, (iii) additional annual cash retainers for committee chairs equal to $20,000 for the Audit Committee, $15,000 for the Compensation Committee, and $10,000 for the Nominating and Governance Committee, (iv) annual cash retainers for committee members of $10,000 for the Audit Committee, $7,500 for the Compensation Committee, and $5,000 for the Nominating and Governance Committee, and (v) an annual grant of a non-qualified stock option with a grant date fair value of $100,000 and a 10-year term and vesting in equal monthly installments through the end of the applicable fiscal year. Ryan M. Dunlap and Stephen M. Simes were appointed to the Board after May 31, 2022, and therefore received pro-rated compensation for fiscal year 2023.

2023 Director Compensation Table

The following table sets forth certain information regarding the compensation earned by or awarded to each non-employee director for services during fiscal year 2023:

| | | | | | | | | |

| | | | Stock option | | | |||

Name of non-employee director |

| Cash fees |

| awards (1)(2) |

| Total | |||

Tanya D. Urbach (3) | | $ | 100,389 | | $ | 100,000 | | $ | 200,389 |

Lishomwa C. Ndhlovu, M.D., Ph.D. | | $ | 52,748 | | $ | 100,000 | | $ | 152,748 |

Karen J. Brunke, Ph.D. | | $ | 62,077 | | $ | 100,000 | | $ | 162,077 |

Ryan M. Dunlap (4) | | $ | 47,703 | | $ | 75,000 | | $ | 122,703 |

Stephen M. Simes (4) | | $ | 34,180 | | $ | 62,500 | | $ | 96,680 |

| (1) | Stock option awards represent the grant date fair value of the awards pursuant to Financial Accounting Standards Board Accounting Standards Codification Topic 718, Compensation – Stock Compensation (“ASC 718”), as described in Note 7 to the audited consolidated financial statements included in our Annual Report on Form 10-K for the fiscal year ended May 31, 2023 (the “2023 Form 10-K”), to which reference is hereby made. |

| (2) | The total shares of common stock underlying stock options held by the non-employee directors as of May 31, 2023 are shown in the table below: |

9

| | |

|

| Number of shares underlying |

Name of non-employee director | | outstanding stock option awards |

Tanya D. Urbach | | 359,611 |

Lishomwa C. Ndhlovu, M.D., Ph.D. | | 459,611 |

Karen J. Brunke, Ph.D. | | 284,611 |

Ryan M. Dunlap | | 185,334 |

Stephen M. Simes | | 178,012 |

| (3) | Cash fees include annual fees for service as independent Board Chair. |

| (4) | Mr. Dunlap was appointed to the Board on August 25, 2022. Mr. Simes was appointed to the Board on October 13, 2022. |

10

PROPOSAL 1

ELECTION OF DIRECTORS

Introduction

Under our Certificate of Incorporation and By-laws, the Board is authorized to set the number of directors of the Company. The Board has fixed the number of directors at five. The Board currently consists of five directors.

At the recommendation of the Nominating and Corporate Governance Committee, the Board has nominated for election at the Annual Meeting the following five individuals: Tanya D. Urbach, Lishomwa C. Ndhlovu, M.D., Ph.D., Karen J. Brunke, Ph.D., Ryan M. Dunlap, and Stephen M. Simes, to hold office until next year’s annual meeting of stockholders, and until their successors are duly elected and qualified or until their earlier death, resignation or removal. If a director retires, resigns or is otherwise unable to serve before the end of his or her one-year term, the Board may appoint a director to fill the remainder of such term, reduce the size of our Board, or leave the position vacant.

The Board has affirmatively determined that each of the Board’s nominees qualifies as an independent director. None of our Board’s nominees is being elected pursuant to any arrangement or understanding between any of the Board’s nominees and any other person or persons. All of the Board’s nominees have consented to serving as a nominee, being named in this Proxy Statement, and serving as a director if elected. If all of the Board’s nominees are elected at the Annual Meeting, two of our directors will be female and one of our directors will be racially or ethnically diverse.

Nominees and their Qualifications

The following table sets forth information with respect to each person who is nominated for election as a director, including their current principal occupation or employment and age as of September 25, 2023:

| | | | | | | | | | | | |

| | | | | | | | Board committees | ||||

Director name |

| Age |

| Principal occupation |

| Independent |

| Audit |

| Compensation |

| Nom/Gov |

Tanya D. Urbach, Board Chair | | 56 | | Partner, Eagle Bay Advisors | | Yes | | M | | M | | C |

Lishomwa C. Ndhlovu, M.D., Ph.D. | | 53 | | Professor, Immunology in Medicine and Neuroscience, Cornell University | | Yes | | | | | | M |

Karen J. Brunke, Ph.D. | | 71 | | Executive Vice President, Corporate and Business Development, Jaguar Health, Inc. (NASDAQ: JAGX) | | Yes | | | | M | | |

Ryan M. Dunlap | | 53 | | Chief Financial Officer, Gurobi Optimization | | Yes | | C | | | | M |

Stephen M. Simes | | 71 | | Independent advisor to companies and organizations in the pharmaceutical industry | | Yes | | M | | C | | |

C | indicates chair of respective board committee. |

M | indicates member of respective board committee. |

11

Tanya D. Urbach. Ms. Urbach has been a director since November 24, 2021, and has served as our Board Chair since January 24, 2022. She is currently Partner/Head of Family Office for Eagle Bay Advisors, which provides family office and investment advisory services, and also provides corporate governance and corporate finance advice to Dynepic, Inc., which provides an integrated platform to power immersive training programs for companies and U.S. military forces. From November 2020 through March 31, 2021, Ms. Urbach was a sole practitioner advising broker-dealers, investment advisers and their professionals. From January 2019 through October 2020, she was a shareholder at the law firm Markun, Zusman, Freniere & Compton in Portland, Oregon. She served as General Counsel for Paulson Investment Company, LLC, a registered broker-dealer that provides investment banking services to the Company from time to time, from July 2015 until January 2019, providing advice regarding corporate governance, securities regulatory compliance, corporate finance, and other legal and securities-related issues. Ms. Urbach earned her bachelor’s degree at University of Oregon and her law degree at Lewis & Clark Law School. She served on the Executive Committee of the Oregon State Bar Securities Regulation Section from 2007 through 2015 and 2019 to 2021. She brings extensive training and expertise in the conduct of securities offerings, securities litigation, corporate finance and business growth, corporate governance, and other corporate business and legal issues to the Board.

Lishomwa C. Ndhlovu, M.D., Ph.D. Dr. Ndhlovu has been a director since November 24, 2021, and previously served on the Company’s Scientific Advisory Board. He was appointed to Weill Cornell Medicine in 2019 as Professor of Immunology in Medicine and Neuroscience. Before joining Weill Cornell Medicine, Dr. Ndhlovu was on the faculty at the University of Hawaii and University of California San Francisco from 2010 to 2019. As co-leader of the $26.5 million NIH-supported Martin Delaney Collaboratory, “HOPE”, testing novel approaches towards an HIV cure, and the $11 million “SCORCH” consortium, investigating how substances that can lead to addition modify effects of HIV in the brain, he is a recognized expert in basic and complex translational immunology and engineered immunotherapy research. He has focused much of his work on confronting the challenges of HIV and aging, addressing molecular mechanism of HIV pathogenesis, complications, and persistence. Dr. Ndhlovu received his M.D. from the University of Zambia and his Ph.D. from Tohoku University in Japan and is an elected Fellow of the American Academy of Microbiology and Chair of the American foundation for AIDS (amfAR) Research Scientific Advisory Committee. He brings a deep understanding of the central nervous system aspects of HIV and research expertise in major arenas in which the Company is studying its drug product to the Board.

Karen J. Brunke, Ph.D. Dr. Brunke was appointed as a director effective April 1, 2022. Dr. Brunke has over 30 years of scientific, operational, clinical, senior executive, and corporate/business development managerial experience with large and small biotechnology companies. She is currently the Executive Vice President of Corporate and Business Development at Jaguar Health, Inc. (JAGX), a position she has held since September 2021, following seven months as an independent consultant to Jaguar. Jaguar is a commercial stage pharmaceuticals company focused on developing novel, sustainably derived gastrointestinal products on a global basis. As of January 2023, Dr. Brunke also serves as acting CEO of Magdalena Biosciences, Inc., a joint venture of Jaguar and Filament Health Corp (FH.NE and FLHLF) funded by OneSmallPlanet. During her career, Dr. Brunke has been a business development and strategy consultant to multiple companies and was instrumental in the initiation of several startup companies, including during the period from 2017 through 2020. Dr. Brunke was part of the executive team that merged Mercator Genetics Inc. with Progenitor, a subsidiary of Interneuron Pharmaceuticals, in 1999 and helped take the resulting company public. Dr. Brunke was Chief Operating Officer of Anexus Pharmaceuticals, a subsidiary of the Japanese public company MediBic, responsible for in- and out-licensing assistance for Japanese companies, from 2004 through June 2006, and was founding Chief Executive Officer of Cardeus Pharmaceuticals, a neuroscience company, from 2011 through March 2014. Dr. Brunke received her BA in Biochemistry as well as a Ph.D. in Microbiology from the University of Pennsylvania. Her many years of service in executive management, business development, operations, and corporate development roles at biotechnology companies will be of valuable assistance to the Board.

Ryan M. Dunlap. Mr. Dunlap was appointed as a director effective August 24, 2022. Mr. Dunlap has over 25 years’ experience in finance and operations leadership, developing significant expertise in strategy setting, improving operational efficiency and effectiveness, fundraising and investor relations, financial reporting and compliance, and risk management. Mr. Dunlap joined Gurobi Optimization, a company that offers customers a mathematical optimization solver to address business problems, in October 2019. Prior to that, he was CFO beginning in January 2016, as well as COO beginning in December 2017, at MolecularMD (now ICON Specialty Labs), a growth equity-backed molecular diagnostics company. Mr. Dunlap also previously served as the CFO of Galena Biopharma, Inc., a publicly traded

12

biotechnology and pharmaceutical sales company. Earlier in his career, Mr. Dunlap held various financial and operational leadership roles in large, multinational organizations, and spent 11 years with public accounting firms such as PricewaterhouseCoopers LLP (“PwC”), KPMG, and Moss Adams, where he provided business assurance and advisory services to both public and private companies predominately in the software, technology, and life sciences industries. Mr. Dunlap earned a B.S. degree in Accounting from the University of Oregon and is an active licensed CPA in the state of Oregon. His expertise as an “audit committee financial expert,” particularly in matters faced by the audit committee of a biotechnology company as well as his significant experience in executive management, finance, operations, and strategic planning, is of valuable assistance to the Board.

Stephen M. Simes. Mr. Simes was appointed as a director effective October 13, 2022. Mr. Simes brings extensive experience to our Board through his service as CEO or a director of a number of pharmaceutical companies, both public and private. His career in the pharmaceutical industry started over 40 years ago with G.D. Searle & Co. (now a part of Pfizer Inc.). He has been an independent advisor to companies and organizations in the pharmaceutical industry since 2016 and is currently Entrepreneur in Residence at Helix 51 and the Innovation and Research Park of Rosalind Franklin University of Medicine and Science in North Chicago, Illinois. Mr. Simes also serves as a director of BioLife4D Corporation, a private company developing a patient-specific, fully functioning human heart using 3D bioprinting and the patient’s own cells and currently preparing for an IPO. Mr. Simes is also chairman of the board of Bio-XL Limited, an Israeli company developing products in oncology. Mr. Simes was the CEO of RestorGenex Corporation from 2014 to 2016, when it was acquired by Diffusion Pharmaceuticals. From 1998 to 2013, Mr. Simes was the President and CEO of BioSante Pharmaceuticals, which was acquired by ANI Pharmaceuticals Inc. in June 2013. He previously served on the boards of directors of Therapix Biosciences (2016-2020), RestorGenex Corporation (2014-2016), Ceregene, Inc. (2009-2013), BioSante Pharmaceuticals (1998-2013), Unimed Pharmaceuticals, Inc. (1994-1997), Bio-Technology General (1993-1995), and Gynex Pharmaceuticals, Inc. (1989-1993). Stephen has a BSc in Chemistry from Brooklyn College of the City University of New York and an MBA from New York University. Simes brings substantial biotech experience to the board, including in the realms of corporate governance, executive management, operations, business development, drug development and capital markets. He also has substantial experience serving on boards of both privately owned and publicly traded entities.

Vote Required

The five nominees for election as directors at the Annual Meeting who receive the highest number of affirmative votes properly cast will be elected, provided that a quorum is present at the Annual Meeting. Stockholders are not permitted to cumulate their votes for the election of directors. Votes may be cast for or withheld from the nominees for election as directors listed below as a group, or for or withheld from each individual nominee. Shares that are not represented at the Annual Meeting, shares that are withheld, and broker non-votes will have no effect on the outcome of the election. If for some unforeseen reason a Board nominee should become unavailable for election, the proxy may be voted for the election of such substitute nominee as may be designated by the Board.

The Board recommends that stockholders vote “FOR” the election of the five nominees named above.

13

Click or tap here to enter text.

PROPOSAL 2

ADVISORY VOTE ON EXECUTIVE COMPENSATION

Introduction

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the “Dodd-Frank Act”) includes a provision that requires public companies to hold an advisory stockholder vote to approve or disapprove the compensation of their named executive officers. The Dodd-Frank Act also includes a provision providing stockholders of a public company the opportunity to vote, on an advisory basis, on how frequently they would like the company to hold an advisory vote on the compensation of executive officers. At the 2019 Annual Meeting, our stockholders approved the Board’s recommendation that an advisory vote on executive compensation be conducted annually. Accordingly, we are conducting an advisory vote to approve the compensation of our executive officers again this year. This vote is intended to consider the overall compensation of executive officers and the policies and practices described in this Proxy Statement.

A detailed description of the compensation paid to the executive officers named in the compensation tables included in this Proxy Statement appears below under the heading “Executive Compensation”.

Our philosophy is that executive compensation should align with stockholders’ interests, without encouraging excessive and unnecessary risk. During fiscal year 2023, the main components of executive compensation, as shown in the Summary Compensation Table in this Proxy Statement, included base salary and time-vested stock options. Cyrus Arman, Ph.D., received awards of restricted stock units (“RSUs”) and performance share units (“PSUs”) pursuant to his employment agreement executed in July 2022 when he was elected by the Board as the Company’s President. The awards were forfeited on July 7, 2023, in connection with his acceptance of the part time, nonexecutive position of Senior Vice President, Business Operations.

This vote is advisory and therefore not binding on us, the Compensation Committee, or the Board. The Board and the Compensation Committee value the opinions of stockholders and will take into account the outcome of the vote when considering future executive compensation arrangements. The next stockholder advisory vote to approve executive compensation will be held at our 2024 Annual Meeting.

Vote Required

Provided that a quorum is present, this proposal will be approved if the votes cast “for” the proposal exceed the votes cast “against” the proposal. Shares that are not represented at the Annual Meeting, abstentions, and broker non-votes will have no effect on the outcome of the voting on this proposal.

The Board recommends that stockholders vote, on an advisory basis, “FOR” the following resolution:

“RESOLVED, that the compensation paid to named executive officers, as disclosed in this Proxy Statement pursuant to Item 402 of Regulation S-K adopted by the SEC, including the executive compensation tables and accompanying footnotes and narrative discussion, is hereby approved on an advisory basis.”

The above-referenced disclosures appear under the heading “Executive Compensation” in this Proxy Statement.

14

PROPOSAL 3

APPROVAL OF AN INCREASE IN THE TOTAL NUMBER OF SHARES OF AUTHORIZED COMMON

STOCK TO 1,750,000,000 SHARES

Background

The Board believes it is in the best interests of the Company to increase the number of shares of common stock authorized for issuance by 400,000,000 shares of common stock, bringing the total number of shares of common stock authorized from 1,350,000,000 shares to 1,750,000,000 shares. These shares do not offer any preemptive rights. The text of the proposed certificate of amendment to the Company’s Certificate of Incorporation is attached hereto as Exhibit A. This proposal to increase the number of shares of common stock authorized for issuance, if approved at the Annual Meeting, will become effective, and the number of authorized shares of common stock will be increased to 1,750,000,000 shares, upon the filing of the certificate of amendment with the Secretary of State of the State of Delaware. The following discussion is qualified in its entirety by the full text of the certificate of amendment, which is attached to this Proxy Statement as Exhibit A and is incorporated herein by reference.

Reasons for the Increase

The Board believes that it is essential to the Company’s continued operations to have additional authorized shares of common stock available for future issuance, as discussed in more detail below. The authorization of a pool of additional shares of common stock at the Special Meeting will provide the Company with the immediate ability to use these shares to meet the Company’s business and financial needs. These needs include: (i) future financings to raise the capital needed to continue to operate the Company’s business and pursue its strategic goals; (ii) potential negotiations with third parties to satisfy the Company’s existing payment obligations in shares of common stock rather than cash; (iii) future equity awards as compensation for employees, officers, directors, consultants and advisors, including equity incentives for performance; (iv) possible strategic transactions or partnerships; and (v) other general corporate purposes. Although such issuances of additional shares would dilute existing stockholders, management believes that such transactions would increase the overall value of the Company to its stockholders. In addition, the Board believes the Company’s successful implementation of its strategic goals depends in part on its continued ability to attract, retain, and motivate highly qualified management and clinical and scientific personnel and advisors, as well as independent directors with requisite skills and experience.

As of the date of this Proxy Statement, the Company has approximately 308,000,000 shares of common stock reserved for issuance upon the exercise of outstanding convertible notes, warrants and stock options, including warrants and stock options held by the Company’s directors, executive officers, employees and scientific advisory board members.

As of the date of this Proxy Statement, less than two percent of the 1,350,000,000 shares of common stock authorized for issuance under our Certificate of Incorporation remain available and unreserved for issuance as of the date of this Proxy Statement. Thus, without an increase in authorized shares of common stock, the Company will not be able to issue additional shares for any of the purposes described above.

There are certain advantages and disadvantages of an increase in our authorized common stock. The advantages include having shares of common stock available:

| ● | To raise additional capital by issuing capital stock in various types of financing transactions, including public offerings or private placements of common stock, preferred stock convertible into common stock, warrants or convertible notes, to finance the Company’s ongoing working capital requirements to advance the Company’s lead product candidate, leronlimab, towards regulatory approval, and to pursue other potential business expansion opportunities, if any. |

| ● | To satisfy the Company’s current payment obligations to third parties in shares rather than cash if the Company is able to negotiate acceptable terms. |

15

| ● | To attract, retain and motivate highly qualified management, clinical and scientific personnel, and our outside directors. |

The disadvantages include:

| ● | Stockholders will experience dilution of their ownership. |

| ● | Stockholders do not have any preemptive or similar rights to subscribe for or purchase any additional shares of common stock that may be issued in the future and, therefore, future issuances of common stock may, depending on the circumstances, have a dilutive effect on the voting power, share value and other interests of existing stockholders of the Company. |

| ● | The additional shares of common stock for which authorization is sought in this proposal would be part of the existing class of common stock and, if and when issued, would have the same rights and privileges as the shares of common stock presently outstanding. The Company intends to use the proceeds from any future capital raises for the purposes described above. The Board does not intend to issue any common stock or securities convertible into common stock in the future other than on terms that the Board deems to be in the best interests of the Company and its stockholders under the circumstances facing the Company at the time of issuance. |

| ● | The issuance of authorized but unissued stock could be used to deter a potential takeover of the Company that may otherwise be beneficial to stockholders by diluting the shares held by a potential suitor or issuing shares to a stockholder that will vote in accordance with the Board’s preferences. A takeover may be beneficial to independent stockholders because, among other factors, a potential suitor may offer such stockholders a premium for their shares of stock compared to the then-existing market price. The Company does not have any plans or proposals to adopt additional provisions or enter into agreements that may have material anti-takeover consequences. |

Although an increase in the authorized shares of common stock could, under certain circumstances, have an anti-takeover effect, this proposal to adopt the amendment is not in response to any effort of which the Company is aware to accumulate common stock or obtain control of the Company. It also is not part of a plan by management to recommend a series of similar amendments to the Board and stockholders. The Company has no arrangements, agreements, or understandings in place at the present time to enter into any merger, consolidation, acquisition, or similar business transaction.

Approval Required

Pursuant to the General Corporation Law of the State of Delaware, this proposal must be approved by the affirmative vote of a majority of the outstanding shares of common stock of the Company entitled to vote on the proposal. Shares that are not represented at the Annual Meeting and abstentions (as well as broker non-votes if this proposal is deemed to be “non-routine” as described above under “Voting, Revocation and Solicitation of Proxies”), will have the same effect as a vote against this proposal.

The Board recommends that stockholders vote “FOR” the proposal to increase the Company’s authorized capital to 1,750,000,000 shares of common stock.

16

PROPOSAL 4

APPROVAL OF THE ADJOURNMENT OF THE ANNUAL MEETING TO SOLICIT ADDITIONAL

PROXIES

Adjournment of the Annual Meeting

In the event that the number of shares of common stock present in person or represented by proxy at the Annual Meeting and voting “FOR” the adoption of Proposal 3 are insufficient to approve Proposal 3, we may move to adjourn the Annual Meeting in order to enable the Board to solicit additional proxies in favor of the adoption of Proposal 3. In that event, we will ask stockholders to vote only upon the adjournment proposal and not on any other proposal discussed in this proxy statement when the Annual Meeting is initially convened. If the adjournment is for more than thirty (30) days, a notice of the adjourned meeting will be given to each stockholder of record entitled to vote at the meeting.

Vote Required and Board Recommendation

If a quorum is present, approval of the proposal to adjourn the Annual Meeting to a later date requires that the votes cast favoring the proposal exceed the votes cast opposing the proposal.

Assuming a quorum is present, abstentions and broker non-votes, if applicable, with respect to this proposal will not be counted for the purpose of determining the number of votes cast and therefore will not have any effect with respect to this adjournment proposal.

The Board recommends that stockholders vote “FOR” the proposal to adjourn the Annual Meeting to solicit additional proxies, if there are insufficient votes at the Annual Meeting to approve Proposal 3.

17

MATTERS RELATING TO THE COMPANY’S

INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

On September 19, 2023, CytoDyn Inc. (the "Company") received notice from the Company’s current independent registered public accounting firm, Macias Gini & O’Connell LLP (“MGO”), informing the Company that MGO declined to stand for re-election as the Company’s fiscal year 2024 registered public accounting firm. The Company’s Audit Committee had considered, but had not formally taken action regarding, a change in the Company’s independent registered public accounting firm prior to September 19, 2023.

The audit reports of MGO on the Company’s financial statements for the fiscal years ended May 31, 2022 and May 31, 2023, included in its Annual Reports on Form 10-K filed on August 15, 2022, and September 14, 2023, respectively, did not contain an adverse opinion or disclaimer of opinion, and were not qualified or modified as to uncertainty, audit scope or accounting principles, except for the expression, in MGO’s audit reports dated August 15, 2022, and September 14, 2023, that there was substantial doubt as to the Company’s ability to continue as a going concern. During the fiscal years ended May 31, 2022 and May 31, 2023, as well as the subsequent interim period, there have been no disagreements (as defined in Item 304(a)(1)(iv) of Regulation S-K), between the Company and MGO on any matter of accounting principles or practices, financial statement disclosure, or auditing scope or procedure, which disagreements, if not resolved to the satisfaction of MGO, would have caused MGO to make reference to the subject matter of the disagreements in connection with its reports.

Other than the material weaknesses described in MGO’s opinion on the Company’s internal control over financial reporting dated August 15, 2022, that was included in the Company’s Annual Report on Form 10-K for the fiscal year ended May 31, 2022, which report concluded that the Company’s internal control over financial reporting was ineffective as of that date, and as further described in Item 9A of the Company’s Annual Report on Form 10-K for the fiscal year ended May 31, 2023, in which the Company’s management concluded that, following remediation efforts during the 2023 fiscal year, the Company’s internal control over financial reporting was effective as of May 31, 2023, there were no “reportable events” under Item 304(a)(1)(v) of Regulation S-K that occurred or were identified during the Company’s two most recent fiscal years ended May 31, 2022 and May 31, 2023, or during the subsequent interim period through September 19, 2023. The material weaknesses related to the accounting treatment of certain equity transactions and the design and operating effectiveness of the Company’s information technology general controls.

The Company’s Audit Committee is in the process of selecting our new independent registered public accounting firm and will disclose the selection when made.

On April 13, 2022, the Company received a letter from the Company’s then-current independent registered public accounting firm, Warren Averett, LLC (“Warren Averett”), informing the Company that, effective April 13, 2022, Warren Averett was resigning as the Company’s independent registered public accounting firm. The Company’s Audit Committee had not recommended a change in the Company’s auditors. On April 18, 2022, the Audit Committee appointed and engaged Macias Gini & O’Connell LLP (“MGO”) as the Company’s independent registered public accounting firm to perform the audit of the Company’s financial statements for the fiscal year ended May 31, 2022, subject to the completion of client acceptance procedures. Subsequently, MGO was engaged to audit the adjustments that were applied to restate the fiscal 2021 consolidated financial statements.

The audit report of Warren Averett on the Company’s consolidated financial statements for the fiscal year ended May 31, 2021, did not contain an adverse opinion or disclaimer of opinion, and was not qualified or modified as to uncertainty, audit scope or accounting principles, except for the expression in such audit report that there was substantial doubt as to the Company’s ability to continue as a going concern and the revision described in Note 2 to the audited consolidated financial statements included in the Company’s Annual Report on Form 10-K for the fiscal year ended May 31, 2022. During the fiscal year ended May 31, 2021, as well as the subsequent interim period through April 13, 2022, there were no disagreements (as defined in Item 304(a)(1)(iv) of Regulation S-K), between the Company and Warren Averett on any matter of accounting principles or practices, financial statement disclosure, or auditing scope or procedure, which disagreements, if not resolved to the satisfaction of Warren Averett, would have caused Warren Averett to make reference to the subject matter of the disagreements in connection with its reports. Other than the material weakness reported in the Company’s Form 10-Q for the quarter ended November 30, 2021, there were no

18

“reportable events” under Item 304(a)(1)(v) of Regulation S-K that occurred or were identified during the Company’s fiscal year ended May 31, 2021, or during the subsequent interim period through April 13, 2022. The material weakness caused the Company’s management to conclude that the Company’s internal control over financial reporting was not effective as of November 30, 2021.

Board Pre-Approval Process, Policies and Procedures

The Audit Committee’s policy is to pre-approve all engagements for audit and non-audit services provided by our independent registered public accounting firm. The Audit Committee pre-approved 100% of the audit-related fees described below.

Fees Paid to Principal Independent Registered Public Accounting Firm

MGO invoiced our Company the approximate amounts shown in the table below for professional services related to fiscal years 2023 and 2022:

| | | | | | |

Services rendered |

| 2023 |

| 2022 | ||

Audit Fees (1) | | $ | 561,928 | | $ | 717,974 |

Audit-Related Fees | | | — | | | — |

Total Audit and Audit-Related Fees | | $ | 561,928 | | $ | 717,974 |

Tax Fees (2) | | | — | | | — |

All Other Fees (3) | | | — | | | — |

Total Fees | | $ | 561,928 | | $ | 717,974 |

(1) | The audit fees covered the annual audit of our financial statements and Sarbanes-Oxley compliance work for fiscal years 2023 and 2022, as well as quarterly reviews for the 2023 fiscal year. |

(2) | The tax fees cover tax returns, year-end tax planning and tax advice. No tax fees were invoiced during fiscal years 2023 or 2022. |

(3) | MGO did not invoice us for any other professional services rendered during fiscal years 2023 or 2022, and it did not provide any professional services described in paragraph (c)(4) of Rule 201 of Regulation S-X. |

19

REPORT OF THE AUDIT COMMITTEE

For the fiscal year ended May 31, 2023, the Audit Committee met with management and our independent auditors, MGO, to review our accounting functions and the audit process and to review and discuss the audited financial statements for the fiscal year ended May 31, 2023. The Audit Committee discussed and reviewed with MGO the matters required to be discussed by the applicable requirements of the Public Company Accounting Oversight Board (“PCAOB”) and the SEC, as well as the Company’s internal control over financial reporting. MGO also provided the written disclosures and the letter required by applicable requirements of the PCAOB regarding communications with the Audit Committee concerning MGO’s independence to the Audit Committee, and the Audit Committee has discussed with MGO its independence.

Based on its review and discussions with management and MGO, the Audit Committee recommended that the audited financial statements be included in our Annual Report on Form 10-K for the fiscal year ended May 31, 2023, for filing with the Securities and Exchange Commission.

Submitted by the Audit Committee of the Board of Directors:

Ryan M. Dunlap, Chair

Stephen M. Simes

Tanya D. Urbach

September 25, 2023

20

INFORMATION ABOUT OUR EXECUTIVE OFFICERS

Information about our current executive officers is set forth below:

| | |||

Name |

| Age |

| Position |

Antonio Migliarese | | 40 | | Interim President, Chief Financial Officer, and Treasurer |

Tyler Blok | | 36 | | Executive Vice President of Legal Affairs and Secretary |

Antonio Migliarese. Mr. Migliarese has served as the Company’s Chief Financial Officer since May 18, 2021, and has also been serving as the Company’s Interim President since May 18, 2023. Mr. Migliarese has held various positions since joining the Company in January 2020, including Corporate Controller, from April 24, 2020 to December 16, 2020, Vice President, Corporate Controller, from December 16, 2020 until May 17, 2021, and Interim President from January 24, 2022 until July 9, 2022. Prior to joining the Company, Mr. Migliarese was the Controller for Domaine Serene Vineyards and Winery, Inc., from 2018 to 2020, and Corporate Controller for Lightspeed Technologies, Inc., an R&D company and supplier of high-tech audio and video solutions to schools and similar organizations, from 2015 to 2018. Mr. Migliarese earned a B.S. degree in Accounting from Oregon State University, began his career in the assurance group of PricewaterhouseCoopers LLP (“PwC”), and is a Certified Public Accountant.

Tyler Blok. Mr. Blok has served as the Company’s legal counsel since July 25, 2022, and was appointed by the Board as Executive Vice President of Legal Affairs effective August 15, 2023. Prior to joining the Company, Mr. Blok was an attorney at Buckley Law P.C., from 2021 to 2022, working in the firm’s business and transactional practice group, representing corporate clients in the mergers and acquisitions process, and advising business clients in relation to corporate governance matters. From 2013 to 2021, Mr. Blok worked at Markun Zusman Freniere & Compton LLP as both a law clerk and an attorney, later associating with TT&E Law Group LLP (2020-2021), where he represented various corporate clients in arbitration matters, complex commercial disputes, securities litigation, and regulatory examination and enforcement matters. Mr. Blok earned his bachelor’s degree at Western Oregon University and his law degree at Lewis & Clark Law School.

21

EXECUTIVE COMPENSATION

The following tables provide information regarding the compensation awarded to, earned by, or paid to Cyrus Arman, Ph.D., who served as President and Principal Executive Officer (“PEO”) during the fiscal year ended May 31, 2023, Antonio Migliarese, our Chief Financial Officer, who also served as Interim President and PEO during the 2023 fiscal year, and two other individuals who served as executive officers during the 2023 fiscal year, Scott A. Kelly, M.D., and Nitya G. Ray, Ph.D. We refer to these four individuals as our “named executive officers.” Other executive officers who served during the 2023 fiscal year received total compensation less than the amounts paid or awarded to our named executive officers.

Executive Compensation Tables

The following table sets forth information regarding the compensation of our named executive officers for our fiscal years ended May 31, 2023 and 2022.

2023 Summary Compensation Table

| | | | | | | | | | | | | | | | |

|

| |

| |

| |

| |

| |

| |

| |

| |

| | | | | | | | | | Stock | | Non-equity | | | | |

| | | | | | | | Stock | | option | | incentive plan | | All other | | |

| | | | Salary | | Bonus | | awards | | awards | | compensation | | compensation | | |

Name and Principal Position (1) | | Year | | ($)(2) | | ($)(3) | | ($)(4) | | ($)(5) | | ($)(6) | | ($)(7) | | Total ($) |

Cyrus Arman, Ph.D. President | | 2023 | | 394,700 | | — | | 375,000 | | 750,000 | | — | | 8,711 | | 1,528,411 |

Antonio Migliarese | | 2023 | | 428,418 | | — | | — | | 1,318,800 | | — | | 10,065 | | 1,757,283 |

Chief Financial Officer | | 2022 | | 433,182 | | — | | — | | 1,302,000 | | — | | 12,347 | | 1,747,529 |

Scott A. Kelly, M.D. | | 2023 | | 299,822 | | — | | — | | 665,920 | | — | | 2,227 | | 967,969 |

Chief Medical Officer | | 2022 | | 585,001 | | — | | — | | 1,877,750 | | — | | 16,636 | | 2,479,387 |

Nitya G. Ray, Ph.D. | | 2023 | | 249,375 | | — | | — | | — | | — | | 2,588 | | 251,963 |

Chief Technology Officer | | 2022 | | 497,656 | | — | | 27,345 | | 501,000 | | — | | 14,390 | | 1,040,931 |

| (1) | Dr. Arman was appointed President on July 9, 2022 and was on medical leave beginning May 18, 2023 through July 6, 2023, when he resigned from that position. He was appointed as the Company’s Senior Vice President, Business Operations, a part time, nonexecutive position, effective July 7, 2023. Mr. Migliarese also served as Interim President from January 24, 2022 through July 9, 2022, and has been serving in that position since May 18, 2023. Dr. Kelly resigned from his position on December 19, 2022, and Dr. Ray resigned from his position on November 21, 2022. |

| (2) | Beginning March 31, 2022 through November 30, 2022 (November 15, 2022, in the case of Dr. Ray), 25% of the salaries of each of Mr. Migliarese, Dr. Kelly, and Dr. Ray were paid in the form of shares of common stock instead of cash. The amounts reflecting the value of shares of common stock included in the Salary column in fiscal 2023 and fiscal 2022, respectively, were as follows: Mr. Migliarese, $51,875 and $21,615; Dr. Kelly, $70,854 and $30,470; and Dr. Ray $89,010 and $27,343. In September 2022, Mr. Migliarese’s salary was increased by $25,000 in recognition of his dual service as CFO and Interim President from January 24, 2022, until July 9, 2022, resulting in additional salary awarded for services in fiscal 2023 and 2022 of $18,182 and $6,818, respectively. |

| (3) | No bonuses were awarded for services in fiscal year 2022 or 2023. |

| (4) | The amount shown for stock awards represents the aggregate grant date fair value of an award of restricted stock units (“RSUs”) to Dr. Arman in 2023. The RSUs were scheduled to vest in four equal annual installments, subject to continued employment through the applicable vesting date. Awards subject to performance conditions (“PSUs”) that were made to Dr. Arman in fiscal 2023 were deemed to have zero fair value based on the probable outcome of the performance conditions on the grant date. The value of the PSUs at the grant date, assuming the performance conditions were met at the maximum level (100%), was $375,000. In connection with Dr. Arman’s appointment as Senior Vice President, Business Operations as of July 7, 2023, the RSUs and PSUs were forfeited. |

22

| (5) | Stock option awards represent the aggregate grant date fair value of the awards pursuant to ASC 718, as described in Note 7 to the consolidated financial statements for the fiscal year ended May 31, 2023, included in the 2023 Form 10-K. |

| (6) | No non-equity incentive plan compensation was paid to the named executive officers for services in fiscal years 2022 or 2023. |

| (7) | Represents our qualified non-elective contributions to the Company’s 401(k) employee savings plan. The total value of all personal benefits received by any named executive officer in fiscal years 2022 and 2023 was less than $10,000. |

Outstanding Equity Awards at 2023 Fiscal Year-End

The table below shows equity awards held by our named executive officers as of May 31, 2023. The awards were granted under our Amended and Restated 2012 Equity Incentive Plan (the “2012 Plan”).

| | | | | | | | | | | |||||||

|

| |

| |

| |

| |

| |

| |

| Number of |

| Value of | |

| | Number of | | Number of | | | | | | Number of | | Value of | | unearned | | unearned | |

| | securities | | securities | | | | | | shares or | | shares or | | shares or | | shares or | |

| | underlying | | underlying | | | | | | units of | | units of | | units of | | units of | |

| | unexercised | | unexercised | | Option | | Option | | stock that | | stock that | | stock | | stock | |

| | options (#) | | options (#) | | exercise | | expiration | | have not | | have not | | that have not | | that have not | |

Name | | exercisable | | unexercisable | | price ($) | | date | | vested (#)(1) | | vested ($)(2) | | vested (#)(3) | | vested ($)(2) | |

Cyrus Arman, Ph.D. | | — | | 1,575,557 | (4) | $ | 0.58 | | 9/20/2032 | | | | | | | ||

| | | | | | | | | | | 646,552 | | 168,104 | | | | |

| | | | | | | | | | | | | | | 646,552 | | 168,104 |

Antonio Migliarese | | 50,000 | | — | | $ | 1.03 | | 1/16/2030 | | | | | | | ||

| | 50,000 | | — | | $ | 1.10 | | 2/21/2030 | | | | | | | | |

| | 66,600 | | 33,400 | (5) | $ | 5.57 | | 7/22/2030 | | | | | | | | |

| | 33,300 | | 16,700 | (6) | $ | 5.54 | | 2/17/2031 | | | | | | | | |

| | 333,000 | | 667,000 | (7) | $ | 1.32 | | 8/6/2031 | | | | | | | | |

| | 210,074 | | 420,148 | (8) | $ | 0.58 | | 9/20/2032 | | | | | | | | |

| | 1,146,384 | | 3,439,152 | (9) | $ | 0.35 | | 11/28/2032 | | | | | | | | |

Scott A. Kelly, M.D. | | — | | — | | | | | | | | | | | | | |

Nitya G. Ray, Ph.D. | | — | | — | | | | | | | | | | | | | |

Note: All awards in the table are subject to forfeiture in the event Continuous Service, as the term is defined in the 2012 Plan, terminates prior to the applicable vesting date.

| (1) | Represents awards of RSUs scheduled to vest in four equal annual installments beginning on July 9, 2023. The RSUs were forfeited as of July 7, 2023, in connection with Dr. Arman’s appointment as Senior Vice President, Business Operations. |

| (2) | Based on the closing sale price of the common stock on May 31, 2023, the last trading day of the Company’s 2023 fiscal year, of $0.26 per share. |