UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21128

Smith Barney Multiple Discipline Trust

(Exact name of registrant as specified in charter)

125 Broad Street, New York, NY 10004

(Address of principal executive offices) (Zip code)

Robert I. Frenkel, Esq.

Legg Mason & Co., LLC

300 First Stamford Place, 4th Floor

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 451-2010

Date of fiscal year end: December 31

Date of reporting period: December 31, 2005

ITEM 1. REPORT TO STOCKHOLDERS.

The Annual Report to Stockholders is filed herewith.

EXPERIENCE

ANNUAL REPORT

DECEMBER 31, 2005

Smith Barney

Multiple Discipline Trust

Multiple Discipline Portfolio — All Cap Growth and Value

Multiple Discipline Portfolio — Large Cap Growth and Value

Multiple Discipline Portfolio — Global All Cap Growth and Value

Multiple Discipline Portfolio — Balanced All Cap Growth and Value

INVESTMENT PRODUCTS: NOT FDIC INSURED Ÿ NO BANK GUARANTEE Ÿ MAY LOSE VALUE

Smith Barney Multiple Discipline Trust

Annual Report • December 31, 2005

What’s

Inside

Under a licensing agreement between Citigroup and Legg Mason, the names of funds, the names of any classes of shares of funds, and the names of investment managers of funds, as well as all logos, trademarks and service marks related to Citigroup or any of its affiliates (“Citi Marks”) are licensed for use by Legg Mason. Citi Marks include, but are not limited to, “Smith Barney,” “Salomon Brothers,” “Citi” and “Citigroup Asset Management”. Legg Mason and its affiliates, as well as the Fund’s investment manager, are not affiliated with Citigroup.

All Citi Marks are owned by Citigroup, and are licensed for use until no later than one year after the date of the licensing agreement.

Letter from the Chairman

R. JAY GERKEN, CFA

Chairman, President and Chief Executive Officer

Dear Shareholder,

Despite numerous obstacles, including rising short-term interest rates, surging oil prices, a destructive hurricane season, and geopolitical issues, the U.S. economy continued to expand at a healthy pace during the reporting period. After a 3.8% advance in the first quarter of 2005, gross domestic product (“GDP”)i growth was 3.3% during the second quarter and 4.1% in the third quarter. While fourth quarter figures have not yet been released, another slight gain is anticipated.

Given the strength of the economy and inflationary pressures, the Federal Reserve Board (“Fed”)ii continued to raise interest rates throughout the period. After raising rates five times from June 2004 through December 2004, the Fed increased its target for the federal funds rateiii in 0.25% increments eight additional times over the reporting period. This represents the longest sustained Fed tightening cycle since the 1970s. All told, the Fed’s thirteen rate hikes have brought the target for the federal funds rate from 1.00% to 4.25%. After the end of the Funds’ reporting period, at its January meeting, the Fed once again raised its target for the federal funds rate by 0.25% to 4.50%.

For the one-year period ended December 31, 2005, the U.S. stock market generated positive results, with the S&P 500 Indexiv returning 4.91%. While corporate profits remained strong during the year, they were often overshadowed by rising interest rates and higher oil prices. Looking at the fiscal year as a whole, mid-cap stocks outperformed their large- and small-cap counterparts, with the Russell Midcapv , Russell 1000vi , and Russell 2000vii Indexes returning 12.65%, 6.27%, and 4.55%, respectively. From an investment style perspective, value stocks outperformed growth stocks for the sixth consecutive calendar year, with the Russell 3000 Valueviii and Russell 3000 Growthix Indexes returning 6.85% and 5.17%, respectively, in 2005.

As the year began, it was widely expected that both short- and long-term yields would rise. This panned out with short-term rates, as two-year Treasury yields rose from 3.08% to 4.41% over the 12-month period ended December 31, 2005.

Smith Barney Multiple Discipline Trust I

Within this environment, the Funds performed as follows1:

| | | | |

| Performance Snapshot as of December 31, 2005 (unaudited) |

| | |

| | | 6 Months | | 12 Months |

| | | | | |

Multiple Discipline Portfolio—All Cap Growth and Value | | 7.13% | | 5.25% |

|

Russell 3000 Index | | 6.13% | | 6.12% |

|

S&P 500 Index | | 5.76% | | 4.91% |

|

Lipper Variable Multi-Cap Core Funds Category Average | | 7.41% | | 6.66% |

|

Multiple Discipline Portfolio—Large Cap Growth and Value | | 5.15% | | 3.55% |

|

Russell 1000 Index | | 6.15% | | 6.27% |

|

S&P 500 Index | | 5.76% | | 4.91% |

|

Lipper Variable Large-Cap Core Funds Category Average | | 6.56% | | 5.77% |

|

Multiple Discipline Portfolio—Global All Cap Growth and Value | | 8.58% | | 6.54% |

|

Russell 3000 Index | | 6.13% | | 6.12% |

|

MSCI EAFE Index | | 14.88% | | 13.54% |

|

MSCI World Index | | 10.25% | | 9.49% |

|

S&P 500 Index | | 5.76% | | 4.91% |

|

Lipper Variable Large-Cap Core Funds Category Average | | 6.56% | | 5.77% |

|

Multiple Discipline Portfolio—Balanced All Cap Growth and Value | | 5.29% | | 4.25% |

|

Russell 1000 Index | | 6.15% | | 6.27% |

|

Russell 3000 Growth Index | | 7.19% | | 5.17% |

|

Russell 3000 Value Index | | 5.07% | | 6.85% |

|

Lehman Brothers Intermediate Treasury Bond Index | | 0.01% | | 1.56% |

|

S&P 500 Index | | 5.76% | | 4.91% |

|

Lipper Variable Balanced Funds Category Average | | 4.29% | | 4.78% |

|

| The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value and investment returns will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost. |

| Current reimbursements and/or fee waivers are voluntary, and may be reduced or terminated at any time. Absent these reimbursements or waivers, performance would have been lower. |

| Fund returns assume the reinvestment of all distributions, including returns of capital, if any, at net asset value and the deduction of all fund expenses. |

| Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the period ended December 31, 2005 and include the reinvestment of all distributions, including returns of capital, if any. Returns for the variable multi-cap core funds category were calculated among the 177 funds for the 6-month period and among the 167 funds for the 12-month period. Returns for the variable large-cap core funds category were calculated among the 223 funds for the 6-month period and among the 220 funds for the 12-month period. Returns for the variable balanced funds category were calculated among the 114 funds for the 6-month period and among the 105 funds for the 12-month period. |

| 1 | | The Funds are underlying investment options of various variable annuity and variable life insurance products. The Funds’ performance returns do not reflect the deduction of initial sales charges and expenses imposed in connection with investing in variable annuity or variable life insurance contracts, such as administrative fees, account charges, and surrender charges, which, if reflected, would reduce the performance of the Funds. Past performance is no guarantee of future results. |

II Smith Barney Multiple Discipline Trust

However, while there were periods of volatility, over the same period long-term yields experienced only a modest increase, moving from 4.24% to 4.37%. In late December, the yield curve inverted, as the yield on two-year Treasuries surpassed that of 10-year Treasuries. This anomaly has historically foreshadowed an economic slowdown or recession. Looking at the municipal market, its yield curve flattened during the reporting period but it did not invert.

Please read on for a more detailed look at prevailing economic and market conditions during the Portfolios’ fiscal year and to learn how those conditions have affected Portfolio performance.

Special Shareholder Notices

On December 1, 2005, Citigroup Inc. (“Citigroup”) completed the sale of substantially all of its asset management business, Citigroup Asset Management (“CAM”), to Legg Mason, Inc. (“Legg Mason”). As a result, the Funds’ investment adviser (the “Manager”), previously an indirect wholly-owned subsidiary of Citigroup, has become a wholly-owned subsidiary of Legg Mason. Completion of the sale caused the Funds’ existing investment management contract to terminate. The Funds’ shareholders previously approved a new investment management contract between the Funds and the Manager, which became effective on December 1, 2005.

On or about April 7, 2006, the Smith Barney Multiple Discipline Trust will be renamed Legg Mason Partners Variable Portfolios IV.

Information About Your Fund

As you may be aware, several issues in the mutual fund industry have recently come under the scrutiny of federal and state regulators. The Portfolios’ Manager and some of its affiliates have received requests for information from various government regulators regarding market timing, late trading, fees, and other mutual fund issues in connection with various investigations. The regulators appear to be examining, among other things, the Funds’ response to market timing and shareholder exchange activity, including compliance with prospectus disclosure related to these subjects. The Portfolios have been informed that the Manager and its affiliates are responding to those information requests, but are not in a position to predict the outcome of these requests and investigations.

Smith Barney Multiple Discipline Trust III

Important information concerning the Portfolios and their Manager with regard to recent regulatory developments is contained in the Notes to Financial Statements included in this report.

As always, thank you for your confidence in our stewardship of your assets. We look forward to helping you continue to meet your financial goals.

Sincerely,

R. Jay Gerken, CFA

Chairman, President and Chief Executive Officer

February 1, 2006

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| | |

i | | Gross domestic product is a market value of goods and services produced by labor and property in a given country. |

| |

ii | | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| |

iii | | The federal funds rate is the interest rate that banks with excess reserves at a Federal Reserve district bank charge other banks that need overnight loans. |

| |

iv | | The S&P 500 Index is an unmanaged index of 500 stocks that is generally representative of the performance of larger companies in the U.S. |

| |

v | | The Russell Midcap Index measures the performance of the 800 smallest companies in the Russell 1000 Index whose average market capitalization was approximately $4.7 billion as of 6/24/05. |

| |

vi | | The Russell 1000 Index measures the performance of the 1,000 largest companies in the Russell 3000 Index, which represents approximately 92% of the total market capitalization of the Russell 3000 Index. |

| |

vii | | The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 8% of the total market capitalization of the Russell 3000 Index. |

| |

viii | | The Russell 3000 Value Index measures the performance of those Russell 3000 Index companies with lower price-to-book ratios and lower forecasted growth values. (A price-to-book ratio is the price of a stock compared to the difference between a company’s assets and liabilities.) |

| |

ix | | The Russell 3000 Growth Index measures the performance of those Russell 3000 Index companies with higher price-to-book ratios and higher forecasted growth values. |

IV Smith Barney Multiple Discipline Trust

Manager Overview

Multiple Discipline Portfolio — All Cap Growth and Value

Special Shareholder Notice

On or about April 7, 2006, the Multiple Discipline Portfolio — All Cap Growth and Value will be renamed Legg Mason Partners Variable Multiple Discipline Portfolio — All Cap Growth and Value.

Q. What were the overall market conditions during the Fund’s reporting period?

A. A resilient U.S. economy provided a positive backdrop for the stock market in 2005. Businesses across America did their part, as corporate profit growth was expected to exceed 10% for the third consecutive year. However, this did not translate into superior stock market returns, as the S&P 500 Indexi gained a relatively modest 4.91% in 2005. After trading in a fairly narrow range for much of the period, there were hopes that a year-end rally, similar to what occurred in 2003 and 2004, would propel stocks higher. However, after strong gains in November, the market treaded water in December as investor sentiment weakened due to fears of continued rate hikes by the Federal Reserve Boardii. Looking more closely at the stock market’s returns in 2005, among the Dow Jones industrial categories, oil & gas stocks generated the best returns, followed at a distance by utilities, and health care companies. In contrast, telecommunications, consumer services, and consumer goods stocks produced weak returns.

Performance Update1

For the 12 months ended December 31, 2005 shares of the Multiple Discipline Portfolio — All Cap Growth and Value returned 5.25%. In comparison, the Fund’s unmanaged benchmarks, the Russell 3000 Indexiii and the S&P 500 Index, returned 6.12% and 4.91%, respectively, for the same period. The Fund’s Lipper Variable Multi-Cap Core Funds Category Average2 returned 6.66%.

Q. What were the most significant factors affecting Fund performance?

What were the leading contributors to performance?

A. The Fund’s outperformance versus the S&P 500 Index benchmark was predominantly the result of overweight positions in the information technology and health care sectors, as well as its positioning in consumer staples stocks.

In terms of individual holdings, the Fund’s largest contributors to performance were Texas Instruments Inc., a company that designs and supplies digital signal processors, SanDisk Corp., a company that produces flash memory data storage products, bio - -

| 1 | | The Fund is an underlying investment option of various variable annuity and variable life insurance products. The Fund’s performance returns do not reflect the deduction of initial sales charges and expenses imposed in connection with investing in variable annuity or variable life insurance contracts, such as administrative fees, account charges, and surrender charges, which, if reflected, would reduce the performance of the Fund. Past performance is no guarantee of future results. |

| 2 | | Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the 12-month period ended December 31, 2005, including the reinvestment of distributions, including returns of capital, if any, calculated among the 167 funds in the Fund’s Lipper category. |

Smith Barney Multiple Discipline Trust 2005 Annual Report 1

technology giant Genentech Inc., UnitedHealth Group Inc., a diversified health and well-being services company, and Grant Prideco Inc., a supplier of drill pipe and equipment.

What were the leading detractors from performance?

A. Areas that detracted from relative results included the Fund’s overweights in consumer discretionary stocks and underweights in the industrial and utilities sectors.

The largest detractors for the period were Comcast Corp., a cable and internet communications company, Biogen Idec Inc., a biotechnology company focusing on drug research and supply, computer giant Dell Inc., Liberty Media Corp., a holding company that specializes in electronic retailing, media, communications and entertainment, and media conglomerate Walt Disney Co.

Q. Were there any significant changes to the Fund during the reporting period?

A. There was no change in MDF sleeve weightings, nor was there a specific net change in sector or market weightings.

Thank you for your investment in the Multiple Discipline Portfolio—All Cap Growth and Value. As ever, we appreciate that you have chosen us to manage your assets and we remain focused on seeking to achieve the Fund’s investment goals.

Sincerely,

| | |

| |  |

| Roger Paradiso | | Kirstin Mobyed |

| Coordinating Portfolio Manager | | Co-Coordinating Portfolio Manager |

February 1, 2006

2 Smith Barney Multiple Discipline Trust 2005 Annual Report

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

Portfolio holdings and breakdowns are as of December 31, 2005 and are subject to change and may not be representative of the portfolio manager’s current or future investments. The Fund’s top ten holdings (as a percentage of net assets) as of this date were: Texas Instruments Inc. (2.7%), Comcast Corp., Special Class A Shares (2.3%), Biogen Idec Inc. (2.2%), Microsoft Corp. (2.2%), Johnson & Johnson (2.2%), Pfizer Inc. (2.1%), Merrill Lynch & Co. Inc. (2.1%), Cisco Systems Inc. (2.0%), Time Warner Inc. (1.9%) and Home Depot (1.9%). Please refer to pages 23 through 27 for a list and percentage breakdown of the Fund’s holdings.

The mention of sector breakdowns is for informational purposes only and should not be construed as a recommendation to purchase or sell any securities. The information provided regarding such sectors is not a sufficient basis upon which to make an investment decision. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies discussed should consult their financial professional. Portfolio holdings are subject to change at any time and may not be representative of the portfolio manager’s current or future investments. The Fund’s top five sector holdings (as a percentage of net assets) as of December 31, 2005 were: Health Care (19.1%), Information Technology (17.8%), Consumer Discretionary (17.8%), Financials (13.6%) and Industrials (9.1%). The Fund’s portfolio composition is subject to change at any time.

RISKS: Diversification does not assure against loss. The Fund may invest in small- and mid-cap companies that may involve a higher degree of risk and volatility than investments in large-cap companies. The Fund may use derivatives, such as options and future, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on Fund performance. Please see the Fund���s prospectus for more information on these and other risks.

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| i | | The S&P 500 Index is an unmanaged index of 500 stocks that is generally representative of the performance of larger companies in the U.S. |

| ii | | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| iii | | The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represent approximately 98% of the U.S. equity market. |

Smith Barney Multiple Discipline Trust 2005 Annual Report 3

Fund at a Glance (unaudited)

Multiple Discipline Portfolio — All Cap Growth and Value

4 Smith Barney Multiple Discipline Trust 2005 Annual Report

Historical Performance (unaudited)

Multiple Discipline Portfolio — All Cap Growth and Value

Value of $10,000 Invested in Shares of the Multiple Discipline Portfolio — All Cap Growth and Value vs. Russell 3000 Index† (October 2002 — December 2005)

| † | | Hypothetical illustration of $10,000 invested in shares of the Multiple Discipline Portfolio — All Cap Growth and Value on October 1, 2002 (commencement of operations), assuming reinvestment of all distributions, including returns of capital, if any, at net asset value through December 31, 2005. The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represent approximately 98% of the U.S. equity market. The Index is unmanaged and is not subject to the same management and trading expenses of a mutual fund. Please note that an investor cannot invest directly in an index. |

The performance shown above represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns do not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. To obtain performance data current to the most recent month-end, please visit our website at www.citigroupam.com.

| | | |

| Average Annual Total Returns* (unaudited) | |

Twelve Months Ended 12/31/05 | | 5.25 | % |

|

|

10/1/02** through 12/31/05 | | 14.92 | |

|

|

| | | |

| Cumulative Total Return* (unaudited) | |

10/1/02** through 12/31/05 | | 57.12 | % |

|

|

| * | | Assumes reinvestment of all distributions, including returns of capital, if any, at net asset value. All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns do not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| ** | | Commencement of operations. |

Smith Barney Multiple Discipline Trust 2005 Annual Report 5

Manager Overview

Multiple Discipline Portfolio — Large Cap Growth and Value

Special Shareholder Notice

On or about April 7, 2006, the Multiple Discipline Portfolio — Large Cap Growth and Value will be renamed Legg Mason Partners Variable Multiple Discipline Portfolio — Large Cap Growth and Value.

Q. What were the overall market conditions during the Fund’s reporting period?

A. A resilient U.S. economy provided a positive backdrop for the stock market in 2005. Businesses across America did their part, as corporate profit growth was expected to exceed 10% for the third consecutive year. However, this did not translate into superior stock market returns, as the S&P 500 Indexi gained a relatively modest 4.91% in 2005. After trading in a fairly narrow range for much of the period, there were hopes that a year-end rally, similar to what occurred in 2003 and 2004, would propel stocks higher. However, after strong gains in November, the market treaded water in December as investor sentiment weakened due to fears of continued rate hikes by the Federal Reserve Boardii. Looking more closely at the stock market’s returns in 2005, among the Dow Jones industrial categories, oil & gas stocks generated the best returns, followed at a distance by utilities, and health care companies. In contrast, telecommunications, consumer services, and consumer goods stocks produced weak returns.

Performance Update1

For the 12 months ended December 31, 2005 shares of the Multiple Discipline Portfolio—Large Cap Growth and Value returned 3.55%. In comparison, the Fund’s unmanaged benchmarks, the Russell 1000 Indexiii and the S&P 500 Index, returned 6.27% and 4.91%, respectively, for the same period. The Fund’s Lipper Variable Large-Cap Core Funds Category Average2 returned 5.77%.

Q. What were the most significant factors affecting Fund performance?

What were the leading contributors to performance?

A. Areas that were positive contributors to relative results included overweights in the consumer staples and health care sectors. In addition, the Fund’s positioning in telecommunication services enhanced relative performance versus the benchmark.

In terms of individual holdings, the Fund’s largest contributors to performance were Genentech Inc., a biotechnology company that discovers, develops, manufactures, and commercializes multiple biotherapeutic and biotechnology products, Texas Instruments Inc., a technology firm that seeks to meet customers’ real world signal processing requirements, Gillette Co., a company that manufactures and sells a variety of consumer products throughout the world, Amgen Inc., a global biotechnology company, and financial services company Merrill Lynch & Co. Inc.

| 1 | | The Fund is an underlying investment option of various variable annuity and variable life insurance products. The Fund’s performance returns do not reflect the deduction of initial sales charges and expenses imposed in connection with investing in variable annuity or variable life insurance contracts, such as administrative fees, account charges, and surrender charges, which, if reflected, would reduce the performance of the Fund. Past performance is no guarantee of future results. |

| 2 | | Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the 12-month period ended December 31, 2005, including the reinvestment of distributions, including returns of capital, if any, calculated among the 220 funds in the Fund’s Lipper category. |

6 Smith Barney Multiple Discipline Trust 2005 Annual Report

What were the leading detractors from performance?

A. The Fund lagged the Russell 1000 benchmark due largely to an underweight in the energy sector and overweight in the information technology sector. The Fund’s holdings in materials stocks also detracted from results.

The largest detractors for the period were Lexmark International Inc., a developer, manufacturer, and supplier of printing solutions for homes and offices, computer company Dell Inc., Time Warner Inc., an Internet-powered media and communications company, Comcast Corp., which is involved in the development, management and operation of broadband cable networks and Walt Disney Co., a diversified worldwide entertainment company.

Q. Were there any significant changes to the Fund during the reporting period?

A. There was no change in MDF sleeve weightings, nor was there a specific net change in sector or market weightings.

Thank you for your investment in the Multiple Discipline Portfolio—Large Cap Growth and Value. As ever, we appreciate that you have chosen us to manage your assets and we remain focused on seeking to achieve the Fund’s investment goals.

Sincerely,

| | |

| | |

| Roger Paradiso | | Kirstin Mobyed |

| Coordinating Portfolio Manager | | Co-Coordinating Portfolio Manager |

February 1, 2006

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

Portfolio holdings and breakdowns are as of December 31, 2005 and are subject to change and may not be representative of the portfolio manager’s current or future investments. The Fund’s top ten holdings (as a percentage of net assets) as of this date were: Merrill Lynch & Co. Inc. (3.5%), American International Group Inc. (3.3%), Microsoft Corp. (3.2%), Pfizer Inc. (3.1%), Time Warner Inc. (2.9%), Johnson & Johnson (2.6%), Amgen Inc. (2.5%), Texas Instruments Inc. (2.5%), General Electric Co. (2.0%) and Intel Corp. (2.0%). Please refer to pages 28 through 31 for a list and percentage breakdown of the Fund’s holdings.

The mention of sector breakdowns is for informational purposes only and should not be construed as a recommendation to purchase or sell any securities. The information provided regarding such sectors is not a sufficient basis upon which to make an investment decision. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies discussed should consult their financial professional. Portfolio holdings are subject to change at any time and may not be representative of the portfolio manager’s current or future investments. The Fund’s top five sector holdings (as a percentage of net assets) as of December 31, 2005 were: Financials (18.2%), Consumer Discretionary (16.5%), Health Care (16.1%), Information Technology (16.0%) and Consumer Staples (10.5%). The Fund’s portfolio composition is subject to change at any time.

RISKS: Diversification does not assure against loss. The Fund may use derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on fund performance. Please see the Fund’s prospectus for more information on these and other risks.

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| i | | The S&P 500 Index is an unmanaged index of 500 stocks that is generally representative of the performance of larger companies in the U.S. |

| ii | | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| iii | | The Russell 1000 Index measures the performance of the 1,000 largest companies in the Russell 3000 Index, which represents approximately 92% of the total market capitalization of the Russell 3000 Index. |

Smith Barney Multiple Discipline Trust 2005 Annual Report 7

Fund at a Glance (unaudited)

Multiple Discipline Portfolio — Large Cap Growth and Value

8 Smith Barney Multiple Discipline Trust 2005 Annual Report

Historical Performance (unaudited)

Multiple Discipline Portfolio — Large Cap Growth and Value

Value of $10,000 Invested in Shares of the Multiple Discipline Portfolio — Large Cap Growth and Value vs. Russell 1000 Index† (October 2002 — December 2005)

| † | | Hypothetical illustration of $10,000 invested in shares of the Multiple Discipline Portfolio — Large Cap Growth and Value on October 1, 2002 (commencement of operations), assuming reinvestment of all distributions, including returns of capital, if any, at net asset value through December 31, 2005. The Russell 1000 Index measures the performance of the 1,000 largest companies in the Russell 3000 Index, which represents approximately 92% of the total market capitalization of the Russell 3000 Index. The Index is unmanaged and is not subject to the same management and trading expenses of a mutual fund. Please note that an investor cannot invest directly in an index. |

The performance shown above represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns do not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. To obtain performance data current to the most recent month-end, please visit our website at www.citigroupam.com.

| | | |

| Average Annual Total Returns* (unaudited) | |

Twelve Months Ended 12/31/05 | | 3.55 | % |

|

|

10/1/02** through 12/31/05 | | 13.98 | |

|

|

| | | |

| Cumulative Total Return* (unaudited) | |

10/1/02** through 12/31/05 | | 53.00 | % |

|

|

| * | | Assumes reinvestment of all distributions, including returns of capital, if any, at net asset value. All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns do not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| ** | | Commencement of operations. |

Smith Barney Multiple Discipline Trust 2005 Annual Report 9

Manager Overview

Multiple Discipline Portfolio — Global All Cap Growth and Value

Special Shareholder Notice

On or about April 7, 2006, the Multiple Discipline Portfolio — Global All Cap Growth and Value will be renamed Legg Mason Partners Variable Multiple Discipline Portfolio — Global All Cap Growth and Value.

Q. What were the overall market conditions during the Fund’s reporting period?

A. A resilient U.S. economy provided a positive backdrop for the stock market in 2005. Businesses across America did their part, as corporate profit growth was expected to exceed 10% for the third consecutive year. However, this did not translate into superior stock market returns, as the S&P 500 Indexi gained a relatively modest 4.91% in 2005. After trading in a fairly narrow range for much of the period, there were hopes that a year-end rally, similar to what occurred in 2003 and 2004, would propel stocks higher. However, after strong gains in November, the market treaded water in December as investor sentiment weakened due to fears of continued rate hikes by the Federal Reserve Boardii. Looking more closely at the stock market’s returns in 2005, among the Dow Jones industrial categories, oil & gas stocks generated the best returns, followed at a distance by utilities, and health care companies. In contrast, telecommunications, consumer services, and consumer goods stocks produced weak returns.

Performance Update1

For the 12 months ended December 31, 2005 shares of the Multiple Discipline Portfolio—Global All Cap Growth and Value returned 6.54%. In comparison, the Fund’s unmanaged benchmarks, the Russell 3000 Index,iii the MSCI EAFE Index,iv the MSCI World Indexv and the S&P 500 Index, returned 6.12%, 13.54%, 9.49% and 4.91%, respectively, for the same period. The Fund’s Lipper Variable Large-Cap Core Funds Category Average2 returned 5.77%.

Q. What were the most significant factors affecting Fund performance?

What were the leading contributors to performance?

A. The Fund outperformed the Russell 3000 benchmark over the year, due largely to its positioning in the financials sector. The Fund’s overweight in the consumer staples and information technology sectors also enhanced results.

In terms of individual holdings, the Fund’s largest contributors to performance were UnitedHealth Group Inc., a diversified health and well-being services company,

| 1 | | The Fund is an underlying investment option of various variable annuity and variable life insurance products. The Fund’s performance returns do not reflect the deduction of initial sales charges and expenses imposed in connection with investing in variable annuity or variable life insurance contracts, such as administrative fees, account charges, and surrender charges, which, if reflected, would reduce the performance of the Fund. Past performance is no guarantee of future results. |

| 2 | | Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the 12-month period ended December 31, 2005, including the reinvestment of distributions, including returns of capital, if any, calculated among the 220 funds in the Fund’s Lipper category. |

10 Smith Barney Multiple Discipline Trust 2005 Annual Report

SanDisk Corp., which designs, develops and markets flash storage card products used in a wide variety of consumer electronics, Genentech Inc., a biotechnology company that discovers, develops, manufactures, and commercializes multiple biotherapeutic and biotechnology products, financial service company Lehman Brothers Holdings Inc. and Texas Instruments Inc., a technology firm that seeks to meet customers’ real world signal processing requirements.

What were the leading detractors from performance?

A. The Fund’s underweights in the industrials, energy and utilities sectors detracted from performance versus the benchmark.

The largest detractors for the period were Lexmark International Inc., a developer, manufacturer, and supplier of printing solutions for homes and offices, Biogen Idec Inc., a company that develops, manufactures and commercializes novel therapies, Comcast Corp., which is involved in the development, management and operation of broadband cable networks, computer company Dell Inc. and Liberty Media Corp., a holding company that, through its ownership of interests in subsidiaries and other companies, is primarily engaged in the electronic retailing, media, communications, and entertainment industries.

Q. Were there any significant changes to the Fund during the reporting period?

A. There was no change in MDF sleeve weightings, nor was there a specific net change in sector or market weightings.

Thank you for your investment in the Multiple Discipline Portfolio—Global All Cap Growth and Value. As ever, we appreciate that you have chosen us to manage your assets and we remain focused on seeking to achieve the Fund’s investment goals.

Sincerely,

| | |

| | |

| Roger Paradiso | | Kirstin Mobyed |

| Coordinating Portfolio Manager | | Co-Coordinating Portfolio Manager |

February 1, 2006

Smith Barney Multiple Discipline Trust 2005 Annual Report 11

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

Portfolio holdings and breakdowns are as of December 31, 2005 and are subject to change and may not be representative of the portfolio manager’s current or future investments. The Fund’s top ten holdings (as a percentage of net assets) as of this date were: UnitedHealth Group Inc. (2.1%), Pfizer Inc. (2.1%), Merrill Lynch & Co. Inc. (2.1%), Biogen Idec Inc. (2.0%), Microsoft Corp. (1.9%), American International Group Inc. (1.9%), Liberty Media Corp., Class A Shares (1.8%), Time Warner Inc. (1.7%), Johnson & Johnson (1.5%) and Texas Instruments Inc. (1.5%). Please refer to pages 32 through 37 for a list and percentage breakdown of the Fund’s holdings.

The mention of sector breakdowns is for informational purposes only and should not be construed as a recommendation to purchase or sell any securities. The information provided regarding such sectors is not a sufficient basis upon which to make an investment decision. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies discussed should consult their financial professional. Portfolio holdings are subject to change at any time and may not be representative of the portfolio manager’s current or future investments. The Fund’s top five sector holdings (as a percentage of net assets) as of December 31, 2005 were: Health Care (17.9%), Financials (16.3%), Consumer Discretionary (15.6%), Information Technology (14.5%) and Consumer Staples (8.2%). The Fund’s portfolio composition is subject to change at any time.

RISKS: Diversification does not assure against loss. The Fund may invest in small- and mid-cap companies that may involve a higher degree of risk and volatility than investments in large-cap companies. The Fund may use derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on fund performance. Foreign stocks are subject to certain risks of overseas investing not associated with domestic investing such as currency fluctuations and changes in political and economic conditions, which could result in significant market fluctuation. These risks are magnified in emerging markets. Please see the Fund’s prospectus for more information on these and other risks.

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| i | | The S&P 500 Index is an unmanaged index of 500 stocks that is generally representative of the performance of larger companies in the U.S. |

| ii | | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| iii | | The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represent approximately 98% of the U.S. equity market. |

| iv | | The MSCI EAFE Index is an unmanaged index of common stocks of companies located in Europe, Australasia and the Far East. |

| v | | The MSCI World Index is a market capitalization weighted equity index of over 1,500 stocks traded in 22 world markets. |

12 Smith Barney Multiple Discipline Trust 2005 Annual Report

Fund at a Glance (unaudited)

Multiple Discipline Portfolio — Global All Cap Growth and Value

Smith Barney Multiple Discipline Trust 2005 Annual Report 13

Historical Performance (unaudited)

Multiple Discipline Portfolio — Global All Cap Growth and Value

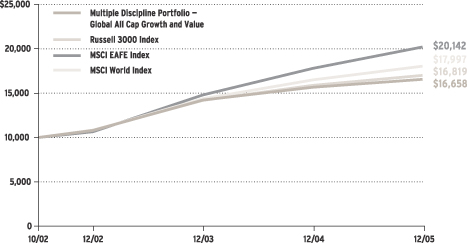

Value of $10,000 Invested in Shares of the Multiple Discipline Portfolio — Global All Cap Growth and Value vs. Russell 3000 Index, MSCI EAFE Index and MSCI World Index† (October 2002 — December 2005)

| † | | Hypothetical illustration of $10,000 invested in shares of the Multiple Discipline Portfolio — Global All Cap Growth and Value on October 1, 2002 (commencement of operations), assuming reinvestment of all distributions, including returns of capital, if any, at net asset value through December 31, 2005. The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represent approximately 98% of the U.S. equity market. The MSCI EAFE Index is an unmanaged index of common stocks of companies located in Europe, Australasia and the Far East. The MSCI World Index is a free float-adjusted market capitalization index that is designed to measure global developed market equity performance. The Indices are unmanaged and are not subject to the same management and trading expenses of a mutual fund. Please note that an investor cannot invest directly in an index. |

The performance shown above represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns do not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. To obtain performance data current to the most recent month-end, please visit our website at www.citigroupam.com.

| | | |

| Average Annual Total Returns* (unaudited) | |

Twelve Months Ended 12/31/05 | | 6.54 | % |

|

|

10/1/02** through 12/31/05 | | 17.01 | |

|

|

| | | |

| Cumulative Total Return* (unaudited) | |

10/1/02** through 12/31/05 | | 66.58 | % |

|

|

| * | | Assumes reinvestment of all distributions, including returns of capital, if any, at net asset value. All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns do not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| ** | | Commencement of operations. |

14 Smith Barney Multiple Discipline Trust 2005 Annual Report

Manager Overview

Multiple Discipline Portfolio — Balanced All Cap Growth and Value

Special Shareholder Notice

On or about April 7, 2006, the Multiple Discipline Portfolio — Balanced All Cap Growth and Value will be renamed Legg Mason Partners Variable Multiple Discipline Portfolio — Balanced All Cap Growth and Value.

Q. What were the overall market conditions during the Fund’s reporting period?

A. A resilient U.S. economy provided a positive backdrop for the stock market in 2005. Businesses across America did their part, as corporate profit growth was expected to exceed 10% for the third consecutive year. However, this did not translate into superior stock market returns, as the S&P 500 Indexi gained a relatively modest 4.91% in 2005. After trading in a fairly narrow range for much of the period, there were hopes that a year-end rally, similar to what occurred in 2003 and 2004, would propel stocks higher. However, after strong gains in November, the market treaded water in December as investor sentiment weakened due to fears of continued rate hikes by the Federal Reserve Boardii. Looking more closely at the stock market’s returns in 2005, among the Dow Jones industrial categories, oil & gas stocks generated the best returns, followed at a distance by utilities, and health care companies. In contrast, telecommunications, consumer services, and consumer goods stocks produced weak returns.

Performance Update1

For the 12 months ended December 31, 2005 shares of the Multiple Discipline Portfolio —Balanced All Cap Growth and Value returned 4.25%. In comparison, the Fund’s unmanaged benchmarks, the Russell 1000 Indexiii, the Russell 3000 Growth Indexiv, the Russell 3000 Value Indexv, the Lehman Brothers Intermediate Treasury Bond Indexvi and the S&P 500 Index, returned 6.27%, 5.17%, 6.85%, 1.56% and 4.91%, respectively, for the same period. The Fund’s Lipper Variable Balanced Funds Category Average2 returned 4.78%.

Q. What were the most significant factors affecting Fund performance?

What were the leading contributors to performance?

A. Areas generating solid relative returns included the Fund’s holdings in the information technology, health care and consumer staples sectors.

In terms of individual equity holdings, the Fund’s largest contributors to performance were Texas Instruments Inc., a company that designs and supplies digital signal processors, SanDisk Corp. which develops flash memory data storage products, biotechnology giant Genentech Inc., Amgen Inc., a leading human therapeutics and biotechnology company, and UnitedHealth Group Inc., a health care service company.

| 1 | | The Fund is an underlying investment option of various variable annuity and variable life insurance products. The Fund’s performance returns do not reflect the deduction of initial sales charges and expenses imposed in connection with investing in variable annuity or variable life insurance contracts, such as administrative fees, account charges, and surrender charges, which, if reflected, would reduce the performance of the Fund. Past performance is no guarantee of future results. |

| 2 | | Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the 12-month period ended December 31, 2005, including the reinvestment of distributions, including returns of capital, if any, calculated among the 105 funds in the Fund’s Lipper category. |

Smith Barney Multiple Discipline Trust 2005 Annual Report 15

What were the leading detractors from performance?

A. The equity portion of the Fund lagged the Russell 3000 benchmark due largely to underweight positions in the energy and industrial sectors. In addition, its positioning in the financials sector detracted from results.

The largest equity detractors for the period were Comcast Corp., a cable and internet communications company, computer giant Dell Inc., Pfizer Inc., a research-based, global pharmaceutical company, Liberty Media Corp., a holding company that specializes in electronic retailing, media, communications and entertainment, and media conglomerate Walt Disney Co.

Q. Were there any significant changes to the Fund during the reporting period?

A. There was no change in MDF sleeve weightings, nor was there a specific net change in sector or market weightings.

Thank you for your investment in the Multiple Discipline Portfolio—Balanced All Cap Growth and Value. As ever, we appreciate that you have chosen us to manage your assets and we remain focused on seeking to achieve the Fund’s investment goals.

Sincerely,

| | |

| | |

| Roger Paradiso | | Kirstin Mobyed |

| Coordinating Portfolio Manager | | Co-Coordinating Portfolio Manager |

February 1, 2006

16 Smith Barney Multiple Discipline Trust 2005 Annual Report

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

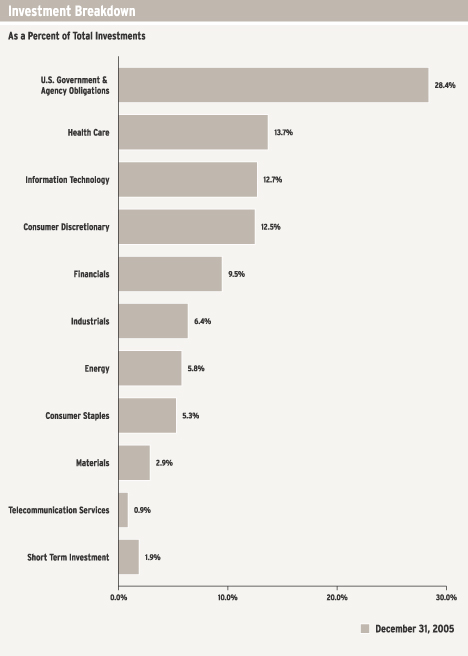

Portfolio holdings and breakdowns are as of December 31, 2005 and are subject to change and may not be representative of the portfolio manager’s current or future investments. The Fund’s top ten holdings (as a percentage of net assets) as of this date were: Federal Home Loan Mortgage Corp., 3.500% due 9/15/07 (5.8%), Federal National Mortgage Association, 3.375% due 12/15/08 (5.8%), United States Treasury Notes, 4.000% due 4/15/10 (4.3%), United States Treasury Notes, 4.625% due 5/15/06 (2.9%), United States Treasury Notes, 4.250% due 8/15/14 (2.6%), United States Treasury Notes, 5.000% due 2/15/11 (2.0%), Texas Instruments Inc. (1.9%), Biogen Idec Inc. (1.6%), Microsoft Corp. (1.6%) and Comcast Corp., Special Class A Shares (1.5%). Please refer to pages 38 through 43 for a list and percentage breakdown of the Fund’s holdings.

The mention of sector breakdowns is for informational purposes only and should not be construed as a recommendation to purchase or sell any securities. The information provided regarding such sectors is not a sufficient basis upon which to make an investment decision. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies discussed should consult their financial professional. Portfolio holdings are subject to change at any time and may not be representative of the portfolio manager’s current or future investments. The Fund’s top five sector holdings (as a percentage of net assets) as of December 31, 2005 were: U.S. Government & Agency Obligations (28.3%), Health Care (13.7%), Information Technology (12.6%), Consumer Discretionary (12.5%) and Financials (9.5%). The Fund’s portfolio composition is subject to change at any time.

RISKS: Diversification does not assure against loss. The Fund may invest in small- and mid-cap companies that may involve a higher degree of risk and volatility than investments in large-cap companies. Interest rates typically cause the prices of fixed income securities to decline and may reduce the value of the Fund’s share price. The Fund may use derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on Fund performance. Please read the prospectus, which describes these and other investment risks in greater detail. Please see the Fund’s prospectus for more information on these and other risks.

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| i | | The S&P 500 Index is an unmanaged index of 500 stocks that is generally representative of the performance of larger companies in the U.S. |

| ii | | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| iii | | The Russell 1000 Index measures the performance of the 1,000 largest companies in the Russell 3000 Index, which represents approximately 92% of the total market capitalization of the Russell 3000 Index. |

| iv | | The Russell 3000 Growth Index measures the performance of those Russell 3000 Index companies with higher price-to-book ratios and higher forecasted growth values. |

| v | | The Russell 3000 Value Index measures the performance of those Russell 3000 Index companies with lower price-to-book ratios and lower forecasted growth values. (A price-to-book ratio is the price of a stock compared to the difference between a company’s assets and liabilities.) |

| vi | | The Lehman Brothers Intermediate Treasury Bond Index is an unmanaged index of U.S. Treasury bonds with maturities between one and ten years. |

Smith Barney Multiple Discipline Trust 2005 Annual Report 17

Fund at a Glance (unaudited)

Multiple Discipline Portfolio — Balanced All Cap Growth and Value

18 Smith Barney Multiple Discipline Trust 2005 Annual Report

Historical Performance (unaudited)

Multiple Discipline Portfolio — Balanced All Cap Growth and Value

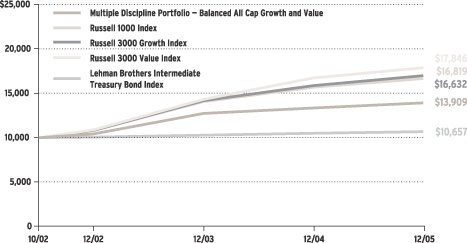

Value of $10,000 Invested in Shares of the Multiple Discipline Portfolio — Balanced All Cap Growth and Value vs. Russell 1000 Index, Russell 3000 Growth Index, Russell 3000 Value Index and Lehman Brothers Intermediate Treasury Bond Index† (October 2002 — December 2005)

| † | | Hypothetical illustration of $10,000 invested in shares of the Multiple Discipline Portfolio — Balanced All Cap Growth and Value on October 1, 2002 (commencement of operations), assuming reinvestment of all distributions, including returns of capital, if any, at net asset value through December 31, 2005. The Russell 1000 Index measures the performance of the 1,000 largest companies in the Russell 3000 Index, which represents approximately 92% of the total market capitalization of the Russell 3000 Index. The Russell 3000 Growth Index measures the performance of those Russell 3000 Index companies with higher price-to-book ratios and higher forecasted growth values. (A price-to-book ratio is the price of a stock compared to the difference between a company’s assets and liabilities). The Russell 3000 Value Index measures the performance of those Russell 3000 Index companies with lower price-to-book ratios and lower forecasted growth values. The Lehman Brothers Intermediate Treasury Bond Index is an unmanaged index of U.S. Treasury bonds with maturities between one and ten years. The Indices are unmanaged and are not subject to the same management and trading expenses of a mutual fund. Please note that an investor cannot invest directly in an index. |

The performance shown above represent past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Investment return and principal value or an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. To obtain performance data current to the most recent month-end, please visit our website at www.citigroupam.com.

Smith Barney Multiple Discipline Trust 2005 Annual Report 19

Historical Performance (unaudited) (continued)

| | | |

| Average Annual Total Returns* (unaudited) | | | |

Twelve Months Ended 12/31/05 | | 4.25 | % |

|

|

10/1/02** through 12/31/05 | | 10.69 | |

|

|

| | | |

| Cumulative Total Return* (unaudited) | | | |

10/1/02** through 12/31/05 | | 39.09 | % |

|

|

| * | | Assumes reinvestment of all distributions, including returns of capital, if any, at net asset value. All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns do not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| ** | | Commencement of operations. |

20 Smith Barney Multiple Discipline Trust 2005 Annual Report

Fund Expenses (unaudited)

Example

As a shareholder of the Funds, you may incur two types of costs: (1) transaction costs, including front-end and back-end sales charges (loads) on purchase payments, reinvested distributions, including returns of capital, if any; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested on July 1, 2005 and held for the six months ended December 31, 2005.

Actual Expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

| | | | | | | | | | | | | | | |

| Based on Actual Total Return(1) | | | | | | | | | |

| | | | | |

| | | Actual

Total

Return(2) | | | Beginning

Account

Value | | Ending

Account

Value | | Annualized

Expense

Ratio | | | Expenses

Paid During

the Period(3) |

All Cap Growth and Value | | 7.13 | % | | $ | 1,000.00 | | $ | 1,071.30 | | 0.97 | % | | $ | 5.06 |

|

Large Cap Growth and Value | | 5.15 | | | | 1,000.00 | | | 1,051.50 | | 1.01 | | | | 5.22 |

|

Global All Cap Growth and Value | | 8.58 | | | | 1,000.00 | | | 1,085.80 | | 0.92 | | | | 4.84 |

|

Balanced All Cap Growth and Value | | 5.29 | | | | 1,000.00 | | | 1,052.90 | | 0.97 | | | | 5.02 |

|

| (1) | | For the six months ended December 31, 2005. |

| (2) | | Assumes reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Total returns do not reflect expenses associated with the separate account such as administrative fees, account charges and surrender charges which, if reflected, would reduce the total returns. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| (3) | | Expenses (net of voluntary fee waiver) are equal to each Fund’s respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 365. |

Smith Barney Multiple Discipline Trust 2005 Annual Report 21

Fund Expenses (unaudited) (continued)

Hypothetical Example for Comparison Purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Funds and other funds. To do so, compare the 5.00% hypothetical example relating to the Fund with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, this table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | |

| Based on Hypothetical Total Return(1) | | | | | | | | | |

| | | | | |

| | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | Ending

Account

Value | | Annualized

Expense

Ratio | | | Expenses

Paid During

the Period(2) |

All Cap Growth and Value | | 5.00 | % | | $ | 1,000.00 | | $ | 1,020.31 | | 0.97 | % | | $ | 4.94 |

|

Large Cap Growth and Value | | 5.00 | | | | 1,000.00 | | | 1,020.11 | | 1.01 | | | | 5.14 |

|

Global All Cap Growth and Value | | 5.00 | | | | 1,000.00 | | | 1,020.56 | | 0.92 | | | | 4.69 |

|

Balanced All Cap Growth and Value | | 5.00 | | | | 1,000.00 | | | 1,020.31 | | 0.97 | | | | 4.94 |

|

| (1) | | For the six months ended December 31, 2005. |

| (2) | | Expenses (net of voluntary fee waiver) are equal to each Fund’s respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 365. |

22 Smith Barney Multiple Discipline Trust 2005 Annual Report

Schedules of Investments (December 31, 2005)

ALL CAP GROWTH AND VALUE

| | | | | |

| | |

| Shares | | Security | | Value |

| | | | | | |

| COMMON STOCKS — 98.3% |

| CONSUMER DISCRETIONARY — 17.8% |

| Auto Components — 0.5% |

| 50,000 | | Lear Corp. | | $ | 1,423,000 |

|

| Hotels, Restaurants & Leisure — 1.2% |

| 66,945 | | Expedia Inc.* | | | 1,604,001 |

| 55,935 | | McDonald’s Corp. | | | 1,886,129 |

|

| | | Total Hotels, Restaurants & Leisure | | | 3,490,130 |

|

| Internet & Catalog Retail — 1.4% |

| 41,500 | | Amazon.com Inc.* | | | 1,956,725 |

| 66,945 | | IAC/InterActiveCorp.* | | | 1,895,213 |

|

| | | Total Internet & Catalog Retail | | | 3,851,938 |

|

| Leisure Equipment & Products — 1.1% |

| 108,740 | | Hasbro Inc. | | | 2,194,373 |

| 64,940 | | Mattel Inc. | | | 1,027,351 |

|

| | | Total Leisure Equipment & Products | | | 3,221,724 |

|

| Media — 10.7% |

| 92,340 | | Cablevision Systems Corp., New York Group, Class A Shares* | | | 2,167,220 |

| 21,500 | | Clear Channel Communications Inc. | | | 676,175 |

| 248,545 | | Comcast Corp., Special Class A Shares* | | | 6,385,121 |

| 32,377 | | Discovery Holding Co., Class A Shares* | | | 490,511 |

| 224,000 | | Interpublic Group of Cos. Inc.* | | | 2,161,600 |

| 6,938 | | Liberty Global Inc., Class A Shares* | | | 156,105 |

| 6,938 | | Liberty Global Inc., Series C Shares* | | | 147,086 |

| 433,779 | | Liberty Media Corp., Class A Shares* | | | 3,413,841 |

| 2,687 | | Live Nation* | | | 35,200 |

| 155,590 | | News Corp., Class B Shares | | | 2,584,350 |

| 120,000 | | Pearson PLC, Sponsored ADR | | | 1,424,400 |

| 316,535 | | Time Warner Inc. | | | 5,520,370 |

| 219,230 | | Walt Disney Co. | | | 5,254,943 |

|

| | | Total Media | | | 30,416,922 |

|

| Specialty Retail — 2.9% |

| 41,000 | | Bed Bath & Beyond Inc.* | | | 1,482,150 |

| 94,160 | | Charming Shoppes Inc.* | | | 1,242,912 |

| 132,234 | | Home Depot Inc. | | | 5,352,832 |

|

| | | Total Specialty Retail | | | 8,077,894 |

|

| | | TOTAL CONSUMER DISCRETIONARY | | | 50,481,608 |

|

| CONSUMER STAPLES — 7.6% |

| Beverages — 2.3% |

| 79,463 | | Coca-Cola Co. | | | 3,203,153 |

| 11,000 | | Molson Coors Brewing Co., Class B Shares | | | 736,890 |

| 44,013 | | PepsiCo Inc. | | | 2,600,288 |

|

| | | Total Beverages | | | 6,540,331 |

|

See Notes to Financial Statements.

Smith Barney Multiple Discipline Trust 2005 Annual Report 23

Schedules of Investments (December 31, 2005) (continued)

| | | | | |

| | |

| Shares | | Security | | Value |

| | | | | | |

| Food & Staples Retailing — 1.4% |

| 65,700 | | Safeway Inc. | | $ | 1,554,462 |

| 51,500 | | Wal-Mart Stores Inc. | | | 2,410,200 |

|

| | | Total Food & Staples Retailing | | | 3,964,662 |

|

| Food Products — 2.4% |

| 61,500 | | Kraft Foods Inc., Class A Shares | | | 1,730,610 |

| 68,700 | | Unilever PLC, Sponsored ADR | | | 2,756,244 |

| 36,040 | | Wm. Wrigley Jr. Co. | | | 2,396,300 |

|

| | | Total Food Products | | | 6,883,154 |

|

| Household Products — 1.5% |

| 73,841 | | Procter & Gamble Co. | | | 4,273,917 |

|

| | | TOTAL CONSUMER STAPLES | | | 21,662,064 |

|

| ENERGY — 7.9% | | | |

| Energy Equipment & Services — 2.7% | | | |

| 23,000 | | Baker Hughes Inc. | | | 1,397,940 |

| 31,640 | | GlobalSantaFe Corp. | | | 1,523,466 |

| 33,046 | | Grant Prideco Inc.* | | | 1,457,989 |

| 91,900 | | Weatherford International Ltd.* | | | 3,326,780 |

|

| | | Total Energy Equipment & Services | | | 7,706,175 |

|

| Oil, Gas & Consumable Fuels — 5.2% | | | |

| 42,260 | | Anadarko Petroleum Corp. | | | 4,004,135 |

| 31,820 | | BP PLC, Sponsored ADR | | | 2,043,480 |

| 19,800 | | Chevron Corp. | | | 1,124,046 |

| 66,780 | | Exxon Mobil Corp. | | | 3,751,033 |

| 33,620 | | Murphy Oil Corp. | | | 1,815,144 |

| 84,300 | | Williams Cos. Inc. | | | 1,953,231 |

|

| | | Total Oil, Gas & Consumable Fuels | | | 14,691,069 |

|

| | | TOTAL ENERGY | | | 22,397,244 |

|

| FINANCIALS — 13.6% | | | |

| Capital Markets — 4.5% | | | |

| 10,000 | | Goldman Sachs Group Inc. | | | 1,277,100 |

| 29,002 | | Lehman Brothers Holdings Inc. | | | 3,717,186 |

| 86,804 | | Merrill Lynch & Co. Inc. | | | 5,879,235 |

| 34,530 | | State Street Corp. | | | 1,914,343 |

|

| | | Total Capital Markets | | | 12,787,864 |

|

| Consumer Finance — 1.8% | | | |

| 56,145 | | American Express Co. | | | 2,889,222 |

| 77,520 | | MBNA Corp. | | | 2,104,668 |

|

| | | Total Consumer Finance | | | 4,993,890 |

|

| Diversified Financial Services — 1.2% | | | |

| 10,329 | | Ameriprise Financial Inc. | | | 423,489 |

| 76,332 | | JPMorgan Chase & Co. | | | 3,029,617 |

|

| | | Total Diversified Financial Services | | | 3,453,106 |

|

See Notes to Financial Statements.

24 Smith Barney Multiple Discipline Trust 2005 Annual Report

Schedules of Investments (December 31, 2005) (continued)

| | | | | |

| | |

| Shares | | Security | | Value |

| | | | | | |

| Insurance — 4.1% | | | |

| 20,315 | | Ambac Financial Group Inc. | | $ | 1,565,474 |

| 73,985 | | American International Group Inc. | | | 5,047,997 |

| 681 | | Berkshire Hathaway Inc., Class B Shares* | | | 1,999,075 |

| 31,785 | | Chubb Corp. | | | 3,103,805 |

|

| | | Total Insurance | | | 11,716,351 |

|

| Thrifts & Mortgage Finance — 2.0% | | | |

| 44,145 | | MGIC Investment Corp. | | | 2,905,624 |

| 70,000 | | PMI Group Inc. | | | 2,874,900 |

|

| | | Total Thrifts & Mortgage Finance | | | 5,780,524 |

|

| | | TOTAL FINANCIALS | | | 38,731,735 |

|

| HEALTH CARE — 19.1% | | | |

| Biotechnology — 8.4% | | | |

| 2,746 | | Alkermes Inc.* | | | 52,504 |

| 65,945 | | Amgen Inc.* | | | 5,200,423 |

| 138,655 | | Biogen Idec Inc.* | | | 6,285,231 |

| 94,590 | | Chiron Corp.* | | | 4,205,471 |

| 27,752 | | Genentech Inc.* | | | 2,567,060 |

| 23,550 | | Genzyme Corp.* | | | 1,666,869 |

| 65,000 | | ImClone Systems Inc.* | | | 2,225,600 |

| 183,120 | | Millennium Pharmaceuticals Inc.* | | | 1,776,264 |

|

| | | Total Biotechnology | | | 23,979,422 |

|

| Health Care Providers & Services — 1.5% |

| 69,260 | | UnitedHealth Group Inc. | | | 4,303,816 |

|

| Pharmaceuticals — 9.2% |

| 72,290 | | Abbott Laboratories | | | 2,850,395 |

| 28,000 | | Eli Lilly & Co. | | | 1,584,520 |

| 74,580 | | Forest Laboratories Inc.* | | | 3,033,914 |

| 43,130 | | GlaxoSmithKline PLC, Sponsored ADR | | | 2,177,202 |

| 103,224 | | Johnson & Johnson | | | 6,203,763 |

| 25,000 | | Novartis AG, Sponsored ADR | | | 1,312,000 |

| 258,016 | | Pfizer Inc. | | | 6,016,933 |

| 61,610 | | Wyeth | | | 2,838,373 |

|

| | | Total Pharmaceuticals | | | 26,017,100 |

|

| | | TOTAL HEALTH CARE | | | 54,300,338 |

|

| INDUSTRIALS — 9.1% | | | |

| Aerospace & Defense — 3.2% |

| 21,000 | | Boeing Co. | | | 1,475,040 |

| 71,960 | | Honeywell International Inc. | | | 2,680,510 |

| 30,186 | | L-3 Communications Holdings Inc. | | | 2,244,329 |

| 64,590 | | Raytheon Co. | | | 2,593,289 |

|

| | | Total Aerospace & Defense | | | 8,993,168 |

|

| Airlines — 0.7% |

| 129,830 | | Southwest Airlines Co. | | | 2,133,107 |

|

See Notes to Financial Statements.

Smith Barney Multiple Discipline Trust 2005 Annual Report 25

Schedules of Investments (December 31, 2005) (continued)

| | | | | |

| | |

| Shares | | Security | | Value |

| | | | | | |

| Electrical Equipment — 1.1% |

| 42,285 | | Emerson Electric Co. | | $ | 3,158,689 |

|

| Industrial Conglomerates — 2.7% |

| 99,200 | | General Electric Co. | | | 3,476,960 |

| 148,621 | | Tyco International Ltd. | | | 4,289,202 |

|

| | | Total Industrial Conglomerates | | | 7,766,162 |

|

| Machinery — 1.4% |

| 37,882 | | Caterpillar Inc. | | | 2,188,443 |

| 64,200 | | Pall Corp. | | | 1,724,412 |

|

| | | Total Machinery | | | 3,912,855 |

|

| | | TOTAL INDUSTRIALS | | | 25,963,981 |

|

| INFORMATION TECHNOLOGY — 17.8% | | | |

| Communications Equipment — 3.4% |

| 338,675 | | Cisco Systems Inc.* | | | 5,798,116 |

| 155,500 | | Lucent Technologies Inc.* | | | 413,630 |

| 82,220 | | Motorola Inc. | | | 1,857,350 |

| 92,210 | | Nokia Oyj, Sponsored ADR | | | 1,687,443 |

|

| | | Total Communications Equipment | | | 9,756,539 |

|

| Computers & Peripherals — 2.5% |

| 83,780 | | Dell Inc.* | | | 2,512,562 |

| 19,435 | | International Business Machines Corp. | | | 1,597,557 |

| 195,843 | | Maxtor Corp.* | | | 1,359,151 |

| 25,300 | | SanDisk Corp.* | | | 1,589,346 |

|

| | | Total Computers & Peripherals | | | 7,058,616 |

|

| Electronic Equipment & Instruments — 0.6% |

| 50,790 | | Agilent Technologies Inc.* | | | 1,690,799 |

|

| Internet Software & Services — 0.7% |

| 50,000 | | Yahoo! Inc.* | | | 1,959,000 |

|

| Semiconductors & Semiconductor Equipment — 6.8% |

| 80,000 | | Applied Materials Inc. | | | 1,435,200 |

| 829 | | Cabot Microelectronics Corp.* | | | 24,314 |

| 45,136 | | Cree Inc.* | | | 1,139,233 |

| 141,490 | | Intel Corp. | | | 3,531,590 |

| 180,162 | | Micron Technology Inc.* | | | 2,397,956 |

| 31,900 | | Novellus Systems Inc.* | | | 769,428 |

| 236,035 | | Taiwan Semiconductor Manufacturing Co., Ltd., Sponsored ADR | | | 2,339,107 |

| 236,710 | | Texas Instruments Inc. | | | 7,591,290 |

|

| | | Total Semiconductors & Semiconductor Equipment | | | 19,228,118 |

|

| Software — 3.8% |

| 42,900 | | Advent Software Inc.* | | | 1,240,239 |

| 25,820 | | Autodesk Inc. | | | 1,108,969 |

| 30,000 | | Electronic Arts Inc.* | | | 1,569,300 |

| 70,000 | | Micromuse Inc.* | | | 692,300 |

| 240,230 | | Microsoft Corp. | | | 6,282,015 |

|

| | | Total Software | | | 10,892,823 |

|

| | | TOTAL INFORMATION TECHNOLOGY | | | 50,585,895 |

|

See Notes to Financial Statements.

26 Smith Barney Multiple Discipline Trust 2005 Annual Report

Schedules of Investments (December 31, 2005) (continued)

| | | | | | | |

| | |

| Shares | | Security | | Value | |

| | MATERIALS — 4.1% | | | | |

| | Chemicals — 1.8% | |

| | 29,600 | | Dow Chemical Co. | | $ | 1,297,072 | |

| | 46,000 | | E.I. du Pont de Nemours & Co. | | | 1,955,000 | |

| | 62,180 | | Engelhard Corp. | | | 1,874,727 | |

|

|

|

| | | | Total Chemicals | | | 5,126,799 | |

|

|

|

| | Containers & Packaging — 0.2% | |

| | 48,500 | | Smurfit-Stone Container Corp.* | | | 687,245 | |

|

|

|

| | Metals & Mining — 1.0% | |

| | 97,495 | | Alcoa Inc. | | | 2,882,927 | |

|

|

|

| | Paper & Forest Products — 1.1% | |

| | 44,975 | | Weyerhaeuser Co. | | | 2,983,642 | |

|

|

|

| | | | TOTAL MATERIALS | | | 11,680,613 | |

|

|

|

| | TELECOMMUNICATION SERVICES — 1.3% | | | | |

| | Diversified Telecommunication Services — 0.7% | |

| | 64,440 | | Verizon Communications Inc. | | | 1,940,933 | |

|

|

|

| | Wireless Telecommunication Services — 0.6% | |

| | 82,860 | | Vodafone Group PLC, Sponsored ADR | | | 1,779,004 | |

|

|

|

| | | | TOTAL TELECOMMUNICATION SERVICES | | | 3,719,937 | |

|

|

|

| | | | TOTAL INVESTMENTS BEFORE SHORT-TERM INVESTMENT

(Cost — $248,603,196) | | | 279,523,415 | |

|

|

|

| | |

Face

Amount | | | | | |

| | SHORT-TERM INVESTMENT — 1.9% | | | | |

| | Repurchase Agreement — 1.9% | | | | |

| $ | 5,431,000 | | State Street Bank & Trust Co. dated 12/30/05, 3.050% due 1/3/06; Proceeds at maturity — $5,432,841; (Fully collateralized by U.S. Treasury Bond, 5.250% due 2/15/29; Market value — $5,545,022) (Cost — $5,431,000) | | | 5,431,000 | |

|

|

|

| | | | TOTAL INVESTMENTS — 100.2% (Cost — $254,034,196#) | | | 284,954,415 | |

| | | | Liabilities in Excess of Other Assets — (0.2)% | | | (573,993 | ) |

|

|

|

| | | | TOTAL NET ASSETS — 100.0% | | $ | 284,380,422 | |

|

|

|

| * | | Non-income producing security. |

| # | | Aggregate cost for federal income tax purposes is $254,141,963. |

| | |

Abbreviation used in this schedule:

|

| ADR — American Depositary Receipt |

See Notes to Financial Statements.

Smith Barney Multiple Discipline Trust 2005 Annual Report 27

Schedules of Investments (December 31, 2005) (continued)

LARGE CAP GROWTH AND VALUE

| | | | | |

| | |

| Shares | | Security | | Value |

| | | | | | |

| COMMON STOCKS — 94.3% |

| CONSUMER DISCRETIONARY — 16.5% |

| Hotels, Restaurants & Leisure — 1.8% |

| 14,750 | | Expedia Inc.* | | $ | 353,411 |

| 8,220 | | McDonald’s Corp. | | | 277,178 |

|

| | | Total Hotels, Restaurants & Leisure | | | 630,589 |

|

| Household Durables — 0.8% |

| 11,490 | | Newell Rubbermaid Inc. | | | 273,232 |

|