UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

| Investment Company Act file number | | |

Nuveen Preferred & Income Securities Fund

(Exact name of registrant as specified in charter)

333 West Wacker Drive

Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Mark L. Winget

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code:

(312) 917-7700

Date of fiscal year end:

July 31

Date of reporting period:

July 31, 2022

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

Closed-End Funds

31 July 2022

Nuveen Closed-End Funds

| | |

| JPC | | Nuveen Preferred & Income Opportunities Fund |

| JPI | | Nuveen Preferred and Income Term Fund |

| JPS | | Nuveen Preferred & Income Securities Fund |

| JPT | | Nuveen Preferred and Income Fund (formerly Nuveen Preferred and Income 2022 Term Fund) |

| NPFD | | Nuveen Variable Rate Preferred & Income Fund |

Nuveen makes things e-simple.

It only takes a minute to sign up for

e-Reports.

Once enrolled, you’ll receive an

e-mail

as soon as your Nuveen Fund information is ready—no more waiting for delivery by regular mail. Just click on the link within the

e-mail

to see the report and save it on your computer if you wish.

Free e-Reports right to your email!

If you receive your Nuveen Fund dividends and statements from your financial professional or brokerage account.

or

www.nuveen.com/client-access

If you receive your Nuveen Fund dividends and statements directly from Nuveen.

NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE

| | | | |

| | | 4 | |

| |

| | | 5 | |

| |

| | | 7 | |

| |

| | | 14 | |

| |

| | | 16 | |

| |

| | | 20 | |

| |

| | | 30 | |

| |

| | | 31 | |

| |

| | | 33 | |

| |

| | | 66 | |

| |

| | | 67 | |

| |

| | | 68 | |

| |

| | | 71 | |

| |

| | | 72 | |

| |

| | | 79 | |

| |

| | | 97 | |

| |

| | | 139 | |

| |

| | | 141 | |

| |

| | | 142 | |

| |

| | | 144 | |

| |

| | | 155 | |

3

Chair’s Letter to Shareholders

Dear Shareholders,

The question of whether economies are moving toward normalization or recession has dominated financial markets in 2022. Persistently high inflation has made the outcome more unpredictable, as it has dampened consumer sentiment, pushed central banks into raising interest rates more aggressively and contributed to considerable turbulence in the markets this year.

Inflation has surged partially due to COVID supply chain bottlenecks and exacerbated by Russia’s war in Ukraine and recent lockdowns across China to contain a large-scale COVID-19 outbreak. This has necessitated increasingly forceful responses from the U.S. Federal Reserve (Fed) and other central banks, who have signaled their intentions to slow inflation while tolerating slower economic growth. As anticipated, the Fed began the rate hiking cycle in March 2022, raising its short-term rate by 0.25% from near zero for the first time since the pandemic was declared two years ago. Larger increases of 0.50% in May and 0.75% in June, July and September 2022 followed, bringing the target fed funds rate to a range of 3.00% to 3.25%. Additional rate hikes are expected in the remainder of this year, although Fed officials will closely monitor inflation data along with other economic measures and modify their rate setting policy based upon these factors. U.S. gross domestic product growth has now contracted for two consecutive quarters, according to government estimates, as consumer and business activity has slowed in part due to higher prices and borrowing costs. However, the still strong labor market suggests not all areas of the economy are weakening in unison.

While markets will likely continue fluctuating with the daily headlines, we encourage investors to keep a long-term perspective. To learn more about how well your portfolio is aligned to your time horizon, risk tolerance and investment goals, consider reviewing it with your financial professional.

On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Terence J. Toth

Chair of the Board

September 23, 2022

4

For Shareholders of

Nuveen Preferred & Income Opportunities Fund (JPC)

Nuveen Preferred and Income Term Fund (JPI)

Nuveen Preferred & Income Securities Fund (JPS)

Nuveen Preferred and Income Fund (JPT)

Nuveen Variable Rate Preferred & Income Fund (NPFD)

Fund Restructuring for Nuveen Preferred and Income Fund (JPT)

On January 19, 2022, shareholders of Nuveen Preferred and Income Fund (JPT) approved a proposal to restructure the fund (the “restructuring”). The restructuring allowed shareholders the opportunity to maintain their investment in JPT and its exposure to a leveraged strategy focused on preferred and other income producing securities in lieu of the scheduled termination of the fund. The effectiveness of the restructuring was contingent on the success of the fund’s tender offer.

On January 20, 2022, JPT conducted a tender offer, which allowed shareholders to offer up to 100% of their shares for repurchase for cash at a price per share equal to 100% of the net asset value (“NAV”) per share determined on the date the tender offer expired.

JPT’s tender offer expired on February 17, 2022. In the tender offer 2,454,617 shares were tendered, representing approximately 36% of JPT’s common shares outstanding. Properly tendered shares were repurchased at $23.2613 per share, which was the NAV of the fund as of the close of ordinary trading on the New York Stock Exchange on February 17, 2022.

As a result of the successful completion of the tender offer, the restructuring of the JPT was completed and on February 28, 2022 the following changes became effective.

| | • | | JPT’s declaration of trust was amended to eliminate the term of the fund. |

| | • | | JPT’s investment policies were amended to permit investment in contingent capital securities (CoCos). |

| | • | | JPT’s name changed to Nuveen Preferred and Income Fund. |

| | • | | Nuveen Fund Advisors, LLC, the investment adviser to the fund, will waive 50% of the fund’s net management fees beginning February 8, 2022 and continuing over the first year following the elimination of the term. |

More details about JPT’s restructuring is available on www.nuveen.com/cef.

Additional Market Disruption Risk

In late February 2022, Russia launched a large scale military attack on Ukraine. The invasion significantly amplified already existing geopolitical tensions among Russia, Ukraine, Europe, NATO and other western nations, including the U.S. In response to the military action by Russia, various countries, including the U.S., the United Kingdom, and European Union issued broad-ranging economic sanctions against Russia. Such sanctions included, among other things, a prohibition on doing business with certain Russian companies, large financial institutions, officials and oligarchs; a commitment by certain countries and the European Union to remove selected Russian banks from the Society for Worldwide Interbank Financial Telecommunications (“SWIFT”), the electronic banking network that connects banks globally; and restrictive measures to prevent the Russian Central Bank from undermining the impact of the sanctions.

Additional sanctions may be imposed in the future. Such sanctions may adversely impact, among other things, the Russian economy and various sectors of the global economy, including but not limited to, the financials, energy, metals and mining, engineering and defense sectors. The sanctions and any related boycotts, tariffs, and financial restrictions

5

imposed on Russia’s government, companies and certain individuals may cause a decline in the value and liquidity of Russian securities; weaken the value of the ruble; downgrade the country’s credit rating; freeze Russian securities and/or funds invested in prohibited assets and impair the ability to trade in Russian securities and/or other assets; and have other adverse consequences on the Russian government, economy, companies and region. Further, several large corporations and U.S. states have announced plans to divest interests or otherwise curtail business dealings with certain Russian businesses.

The ramifications of the hostilities and sanctions, however, may not be limited to Russia and Russian companies but may spill over to and negatively impact other regional and global economic markets (including Europe and the United States), companies in other countries (particularly those that have done business with Russia) and on various sectors, industries and markets for securities and commodities globally, such as oil and natural gas. Accordingly, the actions discussed above and the potential for a wider conflict could increase financial market volatility, cause severe negative effects on regional and global economic markets, industries, and companies and have a negative effect on your Fund’s investments and performance beyond any direct exposure to Russian issuers or those of adjoining geographic regions. In addition, Russia may take retaliatory actions and other countermeasures, including cyberattacks and espionage against other countries and companies around the world, which may negatively impact such countries and the companies in which your Fund invests.

The extent and duration of the military action or future escalation of such hostilities, the extent and impact of existing and future sanctions, market disruptions and volatility, and the result of any diplomatic negotiations cannot be predicted. These and any related events could have a significant impact on Fund performance and the value of an investment in the Fund.

6

Portfolio Managers’ Comments

Nuveen Preferred & Income Opportunities Fund (JPC)

Nuveen Preferred and Income Term Fund (JPI)

Nuveen Preferred & Income Securities Fund (JPS)

Nuveen Preferred and Income Fund (JPT)

(formerly Nuveen Preferred and Income 2022 Term Fund

)

Nuveen Variable Rate Preferred & Income Fund (NPFD)

Nuveen Asset Management, LLC (NAM), an affiliate of Nuveen Fund Advisors, LLC, the Funds’ investment adviser, is the

sub-adviser

for the Nuveen Preferred & Income Opportunities Fund (JPC), Nuveen Preferred and Income Term Fund (JPI), Nuveen Preferred and Income Fund (JPT) and Nuveen Variable Rate Preferred & Income Fund (NPFD). The Funds’ portfolio managers are Douglas M. Baker, CFA and Brenda A. Langenfeld, CFA. The Nuveen Preferred & Income Securities Fund (JPS) is

sub-advised

by a team of specialists at Spectrum Asset Management, Inc. (Spectrum), a wholly owned subsidiary of Principal Global Investors Holding Company (U.S.), LLC. The portfolio managers for JPS are Mark Lieb and Phil Jacoby.

Here the Funds’ portfolio management teams review economic and market conditions, key investment strategies and the Funds’ performance for the twelve-month reporting period July 31, 2022. For more information on the Funds’ investment objectives and policies, please refer to the Shareholder Update section of the report.

What factors affected the economy and the markets during the twelve-month annual reporting period ended July 31, 2022?

After recovering from the pandemic in 2021, the U.S. economy weakened in the first half of 2022. Overall, 2021 gross domestic product (GDP) grew by 5.7% as the economy reopened with the help of $5.3 trillion in crisis-related aid from the federal government, low borrowing rates for businesses and individuals, an increase in

COVID-19

vaccinations and improved treatments for

COVID-19.

However, in early 2022, China’s

COVID-19

lockdown and the Russia-Ukraine war worsened existing pandemic-related supply chain disruptions. Inflation increased more than expected during the first half of 2022, putting pressure on global central banks to respond with more aggressive measures.

The U.S. Federal Reserve (Fed) began an interest rate hiking cycle in March 2022 with a 0.25% hike to the target federal funds rate, followed by larger increases of 0.50% in May 2022, 0.75% in June 2022 and another 0.75% in July 2022. Overall, the Fed raised the target federal funds rate from near zero at the start of 2022 to a range of 2.25% to 2.50% by July 2022. Subsequent to the end of the reporting period, the Fed raised the policy interest rate another 0.75% in September 2022 to a range of 3.00% to 3.25%. Interest rate, stock and bond price volatility increased as markets considered whether the Fed could cool inflation without putting the economy into a recession. Additionally, the U.S. dollar appreciated significantly relative to major world currencies beginning in March of 2022, serving as a headwind to the profits of international companies and U.S. domestic companies with overseas earnings. The dollar’s appreciation was driven in part by the Fed’s increasingly forceful response to inflation compared with other central banks, the relatively better prospects of the U.S. economy and “safe-haven” flows from investors uncertain about geopolitical and global economic conditions.

By

mid-year,

inflation and higher borrowing costs appeared to be dampening consumer confidence and consumer spending. Also, two consecutive quarters of negative U.S. GDP growth added to recession risks. U.S. GDP fell by an annual rate of 0.6% in the second quarter of 2022, according to the second estimate from the U.S. Bureau of Economic

7

Portfolio Managers’ Comments

(continued)

Analysis. This followed a 1.6% annualized GDP decrease in the first quarter of 2022. However, the labor market, another key gauge of the economy’s health, has remained resilient. As of July 2022, the U.S. unemployment rate fell to 3.5%, its

pre-pandemic

low, and the economy has now recovered the 22 million jobs lost since the beginning of the pandemic.

The preferred market struggled during the reporting period, with all segments of the market posting negative returns that were driven by a combination of wider credit spreads and higher U.S. Treasury rates. $1,000 par preferred securities were top performers, followed by $25 par securities and contingent capital securities (“CoCos”). Securities that have coupons with reset features also fared better than fixed-rate coupons during the same period. Those structures are predominately found in the $1,000 par and CoCo segments.

Nuveen Preferred & Income Opportunities Fund (JPC)

What key strategies were used to manage the Fund during the twelve-month reporting period ended July 31, 2022?

The Fund seeks to provide high current income and secondarily, total return, by investing at least 80% of its managed assets in preferred and other income producing securities, including hybrid securities such as contingent capital securities (CoCos). The Fund invests up to 20% opportunistically in other securities, primarily income-oriented securities such as corporate and taxable municipal debt and common equity. Additionally, at least 50% is invested in securities that are rated investment grade at the time of purchase or, if unrated, judged to be of comparable quality by the Fund’s investment management team. The Fund uses leverage.

The investment management team incorporated several active themes within the Fund relative to the JPC Blended Benchmark, including an overweight to $1,000 par preferred securities and securities that have coupons with reset features (floating rate,

rate,

an underweight to CoCos and a corresponding overweight to U.S.-domiciled issuers. The investment management team increased the Fund’s exposure to CoCos beginning in the second quarter of 2022. However, given the anticipated impact of the Russia-Ukraine war on the European economy, the Fund shifted its allocation to core Western European countries and reduced exposure to periphery European countries. The Fund was strategically overweight in the more highly regulated bank and insurance sectors, so investors could benefit from the added scrutiny of regulatory oversight resulting in higher required capital levels.

How did the Fund perform during the twelve-month reporting period ended July 31, 2022?

For the twelve-month reporting period ended July 31, 2022, JPC outperformed the JPC Blended Benchmark. For the purposes of this Performance Commentary, references to relative performance are in comparison to the JPC Blended Benchmark. Effective April 1, 2022, the JPC Blended Benchmark was updated to consist of: 1) 60% ICE BofA U.S. All Capital Securities Index and 2) 40% ICE USD Contingent Capital Index (CDLR). Benchmark performance prior to April 1, 2022 reflects the JPC Blended Benchmark’s previous composition of: 1) 50% ICE BofA Fixed Rate Preferred Securities Index, 2) 30% ICE BofA U.S. All Capital Securities Index, and 3) 20% ICE USD Contingent Capital Index (CDLR).

The Fund’s outperformance was driven by an overweight to $1,000 par preferred securities, which gave the Fund greater exposure to securities that have coupons with reset features. These investments generally demonstrate lower sensitivity to interest rates. During the reporting period, these structures outperformed securities with fixed-rate coupons. The Fund’s relatively shorter leverage-adjusted duration was also accretive to performance. Historically, the investment management team has limited emerging markets exposure in the portfolio and the Fund held no securities from Russian, Ukrainian or Belarusian-domiciled issuers during the reporting period. Conversely, the JPC Blended Benchmark began 2022 with approximately a 1.4% weighting in US dollar denominated CoCos issued by Russian banks, whose prices dropped to zero by the end of the first quarter of 2022. While the absolute exposure to these securities was modest in the JPC Blended Benchmark, their price performance had a meaningful impact on the benchmark performance during the first quarter of 2022. The Fund’s lack of exposure was accretive to relative performance. The

8

Fund’s overweight exposure to Land O’ Lakes Inc. and CHS Inc. contributed to performance. Both of these consumer

non-cyclical

sector holdings outperformed the broader market that encountered headwinds due to uncertainty surrounding the global economy. The Fund continues to hold both positions.

Partially offsetting the outperformance was the Fund’s use of leverage through bank borrowings and reverse repurchase agreements, which significantly detracted from relative performance during the reporting period. However, the Fund’s use of leverage was accretive to overall common share income. Leverage is discussed in more detail in the Fund Leverage section of this report.

In addition to the use of leverage, the Fund’s modest overweight to consumer cyclicals detracted from performance as the market began to price in an economic slowdown and the sector underperformed the JPC Blended Benchmark during the second quarter of 2022. An underweight to the utilities sector also detracted from performance as that sector outperformed the JPC Blended Benchmark. Finally, the Fund’s overweight exposure to Deutsche Bank AG and General Motors Financial Co Inc. both detracted from performance. Deutsche Bank underperformed due to concerns about Russian exposure. Capital levels remain strong and the Fund continues to hold the position. An overweight to General Motors hindered performance due to increased economic uncertainty. The Fund continues to maintain an overweight given the company’s solid long-term fundamentals.

The Fund sold interest rate futures during the reporting period to manage its exposure to various points along the yield curve, with a net effect of decreasing the Fund’s overall interest rate sensitivity. During the reporting period, the interest rate futures had a negligible impact on relative performance.

Nuveen Preferred and Income Term Fund (JPI)

What key strategies were used to manage the Fund during the twelve-month reporting period ended July 31, 2022?

The Fund seeks to provide a high level of current income and total return by investing at least 80% of its managed assets in preferred and other income-producing securities, including hybrid securities such as contingent capital securities, with a focus on securities issued by financial and insurance firms. At least 50% of its managed assets are rated investment grade at the time of purchase or, if unrated, judged to be of comparable quality by the Fund’s investment management team.

The investment management team incorporated several active themes within the Fund relative to the JPI Blended Benchmark that included an overweight to $1,000 par preferred securities and securities that have coupons with reset features (floating rate,

rate,

an underweight to CoCos and a corresponding overweight to U.S.-domiciled issuers. Given the anticipated impact of the Russian-Ukrainian war on the European economy, the investment management team modestly reduced the Fund’s CoCos exposure and correspondingly added to its preferred securities allocation. Within the CoCos allocation, the investment management team was more defensive given its relatively greater concern for the European economy. As a result, the team rotated some of the Fund’s exposure out of periphery European countries and added exposure to core Western European countries. The Fund was strategically overweight the more highly regulated bank and insurance sectors, so investors could benefit from the added scrutiny of regulatory oversight resulting in higher required capital levels.

How did the Fund perform during the twelve-month reporting period ended July 31, 2022?

For the twelve-month reporting period ended July 31, 2022, JPI underperformed the JPI Blended Benchmark. The JPI Blended Benchmark consists of: 1) 60% ICE BofA U.S. All Capital Securities Index and 2) 40% ICE USD Contingent Capital Index (CDLR). For the purposes of this Performance Commentary, references to relative performance are in comparison to the JPI Blended Benchmark.

9

Portfolio Managers’ Comments

(continued)

The Fund’s use of leverage through bank borrowings and reverse repurchase agreements significantly detracted from relative performance during the reporting period. However, the Fund’s use of leverage was accretive to overall common share income. Leverage is discussed in more detail in the Fund Leverage section of this report.

In addition to the use of leverage, the Fund’s longer leverage-adjusted duration for most of the reporting period and an underweight to the utilities sector detracted from relative performance. Also, the Fund’s overweight to Deutsche Bank AG and SBL Holdings both detracted from relative results. Deutsche Bank underperformed due to concerns about Russian exposure. Capital levels remain strong and the Fund continues to hold the position. SBL Holdings underperformance was related to selling pressure during the reporting period. The Fund continues to hold the position based on its solid credit metrics.

Partially offsetting the Fund’s relative detractors were overweight exposures to the consumer

non-cyclical

sector, $1,000 par preferred securities, and securities that have coupons with reset features, as well as selection within the CoCos allocation that contributed favorably to the Fund’s relative results. The Fund’s overweight exposure to Land O’ Lakes Inc. and CHS Inc. also contributed to performance. Both of these consumer

non-cyclical

sector holdings outperformed the broader market that encountered headwinds given uncertainty surrounding the global economy. The Fund continues to hold both positions.

The Fund sold interest rate futures during the reporting period to manage its exposure to various points along the yield curve, with a net effect of decreasing the Fund’s overall interest rate sensitivity. During the reporting period, the interest rate futures contributed to relative performance.

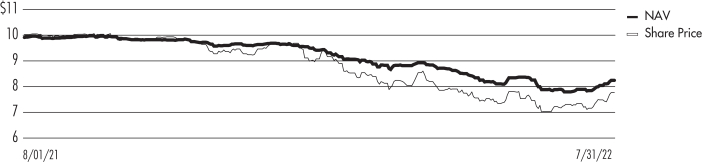

Nuveen Preferred & Income Securities Fund (JPS)

What key strategies were used to manage the Fund during the twelve-month reporting period ended July 31, 2022?

The Fund primarily seeks to offer high current income consistent with capital preservation. The Fund invests at least 80% of its managed assets in preferred and other income-producing securities, including hybrid securities such as contingent capital securities. At least 50% is invested in securities that are rated investment grade. The Fund uses leverage.

The investment management team incorporated several strategies relative to the JPS Blended Benchmark, including an overweight to $1,000 par preferred securities and CoCos. The Fund was also underweight securities with a duration of at least 10 years and overweight securities with a duration of one to three years. As interest rates are expected to be elevated for some time, the Fund maintained an overall shorter-duration profile relative to the JPS Blended Benchmark.

How did the Fund perform during this twelve-month reporting period ended July 31, 2022?

For the twelve-month reporting period ended July 31, 2022, JPS underperformed the JPS Blended Benchmark. The JPS Blended Benchmark consists of: 1) 60% ICE BofA U.S. All Capital Securities Index, and 2) 40% ICE USD Contingent Capital Index (CDLR). For the purposes of this Performance Commentary, references to relative performance are in comparison to the JPS Blended Benchmark.

The Fund’s use of leverage through bank borrowings and reverse repurchase agreements significantly detracted from relative performance during the reporting period. However, the Fund’s use of leverage was accretive to overall common share income. Leverage is discussed in more detail in the Fund Leverage section of this report.

In addition to the use of leverage, the Fund’s overweight to securities with a duration of one to three years detracted from relative performance. Although these securities had short-duration profiles, they underperformed because of the significant flattening on the front end of the yield curve. The longer-duration junior subordinated debt of MetLife and Nationwide Financial also detracted from performance. Longer-duration securities underperformed driven by rising interest rates during the reporting period. The Fund continues to hold these issues because the credits are stable and the current income has remained above market levels.

10

Partially offsetting some of the Fund’s underperformance was an underweight to securities with a duration of at least 10 years. As previously mentioned, longer-duration securities underperformed driven by rising interest rates during the reporting period. The Fund’s allocation to Bank of America Corp. perpetual preferred and PNC Financial Services Group Inc. PRP $25 par preferred also contributed to performance. The floating rate features of both holdings contributed to their outperformance. The Fund continues to maintain its allocation to Bank of America Corp. and PNC Financial Services Group.

Nuveen Preferred and Income Fund (JPT)

(formerly Nuveen Preferred and Income 2022 Term Fund

)

What key strategies were used to manage the Fund during the twelve-month reporting period ended July 31, 2022?

The Fund seeks to provide a high level of current income and total return. The Fund provides access to both the exchange-traded and

preferred securities markets, seeking to capitalize on price discrepancies that may occur between these two markets. The Fund also has the flexibility to opportunistically invest in preferred securities with various coupon structures, including

structures, which may help reduce interest rate risk and enhance performance in a rising rate environment. The Fund invests at least 80% of its managed assets in preferred and other income-producing securities, including hybrid securities such as contingent capital securities (CoCos). The Fund may invest without limit in below investment grade securities but no more than 10% in securities rated below

B-/B3

at the time of investment. Up to 40% of its managed assets may be in securities issued by companies located anywhere in the world, but no more than 10% in securities of issuers in emerging markets countries, and 100% in U.S. dollar-denominated securities. The Fund uses leverage.

During the reporting period, the investment management team incorporated several active themes within the Fund relative to the JPT Blended Benchmark, including: an overweight to $1,000 par preferred securities; an overweight to securities that have coupons with reset features (floating rate,

rate,

and an underweight to CoCos with a corresponding overweight to U.S.-domiciled issuers. On February 28, 2022, JPT’s investment policies were amended to permit investment in CoCos. Following the policy change, the investment management team increased exposure to CoCo securities. However, given the anticipated impact of the Russian-Ukrainian war on the European economy, the Fund shifted its allocation to core Western European countries and reduced exposure to periphery European countries. In terms of sector exposure, the Fund was strategically overweight in the highly regulated bank and insurance sectors, so investors could benefit from the added scrutiny of regulatory oversight resulting in higher required capital levels.

How did the Fund perform during the twelve-month reporting period ended July 31, 2022?

For the twelve-month reporting period ended July 31, 2022, JPT performed in line with the JPT Blended Benchmark. For the purposes of this Performance Commentary, references to relative performance are in comparison to the JPT Blended Benchmark. Effective February 28, 2022, the JPT Blended Benchmark was updated to consist of: 1) 60% ICE BofA U.S. All Capital Securities Index, and 2) 40% ICE USD Contingent Capital Index (CDLR). Benchmark performance prior to February 28, 2022 consisted of the ICE BofA U.S. All Capital Securities Index.

Contributors to the Fund’s relative performance included overweight exposure to the consumer

non-cyclical

sector, $1,000 par preferred securities and securities that have coupons with reset features, as well as selection within the CoCo allocation. The Fund’s overweight to $1,000 par preferred securities gave the Fund greater exposure to securities that have coupons with reset features. These structures generally demonstrate lower sensitivity to interest rates and during the reporting period, they outperformed securities with fixed-rate coupons. Historically, the investment management team has limited emerging markets exposure in the portfolio and the Fund held no securities from Russian, Ukrainian or Belarusian domiciled issuers during the reporting period. Conversely, the JPT Blended Benchmark began 2022 with approximately a 1.4% weighting in USD CoCos issued by Russian banks, whose prices dropped to zero by the end of

11

Portfolio Managers’ Comments

(continued)

the first quarter of 2022. While the absolute exposure was modest in the JPT Blended Benchmark, the price performance had a meaningful impact during the first quarter of 2022. The Fund’s lack of exposure was accretive to relative performance. The Fund’s overweight exposure to Land O’ Lakes Inc. and CHS Inc. also contributed to performance. Both of these consumer

non-cyclical

sector holdings outperformed the broader market that encountered headwinds due to uncertainty surrounding the global economy. The Fund continues to hold both positions.

The Fund sold interest rate futures during the reporting period to manage its exposure to various points along the yield curve, with a net effect of decreasing the Fund’s overall interest rate sensitivity. During the reporting period, the interest rate futures contributed to relative performance.

Serving to partially offset the contributors was the Fund’s use of leverage through bank borrowings, which significantly detracted from relative performance during the reporting period. However, the Fund’s use of leverage was accretive to overall common share income. Leverage is discussed in more detail in the Fund Leverage section of this report.

In addition to the use of leverage, the Fund’s relatively longer leverage-adjusted duration for most of the reporting period detracted from relative performance. The Fund’s modest overweight to consumer cyclicals detracted from performance as the market began to price in an economic slowdown and the sector underperformed the JPT Blended Benchmark during the second quarter of 2022. An underweight to the utilities sector also detracted from performance as that sector outperformed the JPT Blended Benchmark. Finally, the Fund’s overweight exposure to Deutsche Bank and SBL Holdings both detracted from performance. Deutsche Bank underperformed due to concerns about Russian exposure. Capital levels remain strong and the Fund continues to hold the position. SBL Holdings underperformance was related to selling pressure during the reporting period. The Fund continues to hold the position based on its solid credit metrics.

Nuveen Variable Rate Preferred & Income Fund (NPFD)

What key strategies were used to manage the Fund during the abbreviated reporting period since the Fund’s commencement on December 15, 2021 through July 31, 2022?

The Fund seeks to provide a high level of current income and total return by investing in primarily investment grade, variable rate preferred securities and other variable rate income-producing securities from high quality, highly regulated companies such as banks, utilities and insurance companies. All, or almost all, of the Fund’s distributions of net investment income are expected to be treated as qualified dividend income (QDI) which is generally taxed at a lower rate than interest and ordinary dividend income, assuming holding period and certain other requirements are met.

The Fund may invest up to 20% of managed assets in contingent capital securities or contingent convertible securities (CoCos) and up to 15% in companies located in emerging market countries but may only invest in U.S. dollar denominated securities. More than 25% of managed assets are invested in securities of companies in the financial services sector. The Fund uses leverage and has a

12-year

term with the potential to convert to perpetual.

The overwhelming majority of the

invest-up

period was via the secondary market in attractive opportunities in both U.S.-domiciled and

non-U.S.-domiciled

issuers, including CoCos. Positioning favored highly regulated sectors such as banks and insurance. Given the anticipated impact of the Russian/Ukrainian war on the European economy, the investment management team slightly reduced the Fund’s CoCos exposure beginning in February 2022 and correspondingly added to its preferred securities allocation. Within the CoCos allocation, the team rotated some exposure out of periphery European countries and added exposure to core Western European countries.

How did the Fund perform during the abbreviated reporting period since the Fund’s commencement on December 15, 2021 through July 31, 2022?

For the abbreviated reporting period since the Fund’s commencement on December 15, 2021 through July 31, 2022, NPFD underperformed the NPFD Blended Benchmark. The NPFD Blended Benchmark consists of: 1) 80% ICE Variable

12

Rate Preferred & Hybrid Securities Index, and 2) 20% ICE USD Contingent Capital Index (CDLR). For the purposes of this Performance Commentary, references to relative performance are in comparison to the NPFD Blended Benchmark.

The Fund’s use of leverage through bank borrowings and reverse repurchase agreements significantly detracted from relative performance during the reporting period. However, the Fund’s use of leverage was accretive to overall common share income. Leverage is discussed in more detail in the Fund Leverage section of this report.

In addition to the use of leverage, the Fund’s longer leverage-adjusted effective duration and modest steepening bias detracted from relative performance. The Fund’s overweight to consumer cyclicals detracted from performance as the market began to price in an economic slowdown during the second quarter of 2022 and the sector underperformed the benchmark. The Fund’s overweight exposure to SBL Holdings and General Motors also detracted from performance. SBL Holdings underperformance was related to selling pressure during the reporting period. The Fund continues to hold based on its solid credit metrics. An overweight to General Motors hindered performance due to increased economic uncertainty. The Fund continues to maintain an overweight given the company’s solid long-term fundamentals.

Partially offsetting the Fund’s relative detractors was the Fund’s lack of exposure to Russian-domiciled issuers. The investment management team has limited emerging markets exposure in the Fund and held no securities from Russian, Ukrainian or Belarusian-domiciled issuers during the reporting period. Conversely, the NPFD Blended Benchmark began 2022 with an estimated 0.7% weighting in USD CoCos issued by Russian banks, whose prices dropped to zero by the end of the first quarter of 2022 and resulted in removal from the index. While the absolute exposure was modest in the NPFD Blended Benchmark, the price performance had a meaningful impact. Overweight positions in the insurance and consumer

non-cyclical

sectors contributed favorably to the Fund’s relative performance versus the NPFD Blended Benchmark. These sectors outperformed the NPFD Blended Benchmark since the Fund’s inception. The Fund’s overweight exposure to CHS Inc. and NuStar Energy LP contributed to performance. Within the consumer

non-cyclical

sector, CHS Inc. outperformed the broader market, which encountered headwinds due to uncertainty surrounding the global economy. Nustar Energy was a strong performer tracking higher oil prices during the reporting period. The Fund continues to hold both positions.

The Fund sold interest rate futures during the reporting period to manage its exposure to various points along the yield curve, with a net effect of decreasing the Fund’s overall interest rate sensitivity. During the reporting period, the interest rate futures had a negligible impact on relative performance.

13

IMPACT OF THE FUNDS’ LEVERAGE STRATEGIES ON PERFORMANCE

One important factor impacting the returns of the Funds’ common shares relative to their comparative benchmarks was the Funds’ use of leverage through bank borrowings, Taxable Fund Preferred Shares (TFP) for JPS and reverse repurchase agreements for JPC, JPI, JPS and NPFD. The Funds use leverage because our research has shown that, over time, leveraging provides opportunities for additional income. The opportunity arises when short-term rates that a Fund pays on its leveraging instruments are lower than the interest the Fund earns on its portfolio securities that it has bought with the proceeds of that leverage. This has been particularly true in the recent market environment where short-term rates have been low by historical standards.

However, use of leverage can expose Fund common shares to additional price volatility. When a Fund uses leverage, the Fund’s common shares will experience a greater increase in their net asset value if the securities acquired through the use of leverage increase in value, but will also experience a correspondingly larger decline in their net asset value if the securities acquired through leverage decline in value. All this will make the shares’ total return performance more variable, over time.

In addition, common share income in levered funds will typically decrease in comparison to unlevered funds when short-term interest rates increase and increase when short-term interest rates decrease. In recent quarters, fund leverage expenses have generally tracked the overall movement of short-term tax-exempt interest rates. While fund leverage expenses are somewhat higher than their all-time lows, leverage nevertheless continues to provide the opportunity for incremental common share income, particularly over longer-term periods.

The Funds’ use of leverage significantly detracted from relative performance during the reporting period. However, the Funds’ use of leverage was accretive to overall common share income.

JPC, JPI and JPS continued to use interest rate swap contracts to partially hedge the interest cost of leverage. During the period, these interest rate swaps contributed to the relative performance of JPC, JPI and JPS.

As of July 31, 2022, the Funds’ percentages of leverage are as shown in the accompanying table.

| | | | | | | | | | | | | | | | | | | | |

| | | JPC | | | JPI | | | JPS | | | JPT | | | NPFD | |

| Effective Leverage* | | | 37.28 | % | | | 36.72 | % | | | 38.09 | % | | | 33.59 | % | | | 36.46 | % |

| Regulatory Leverage* | | | 32.38 | % | | | 30.85 | % | | | 31.18 | % | | | 33.59 | % | | | 27.04 | % |

| * | Effective leverage is a Fund’s effective economic leverage, and includes both regulatory leverage and the leverage effects of reverse repurchase agreements, certain derivative and other investments in a Fund’s portfolio that increase the Fund’s investment exposure. Regulatory leverage consists of preferred shares issued or borrowings of a Fund. Both of these are part of a Fund’s capital structure. A Fund, however, may from time to time borrow on a typically transient basis in connection with its day-to-day operations, primarily in connection with the need to settle portfolio trades. Such incidental borrowings are excluded from the calculation of a Fund’s effective leverage ratio. Regulatory leverage is subject to asset coverage limits set forth in the Investment Company Act of 1940. |

14

THE FUNDS’ LEVERAGE

As noted previously, the Funds employ leverage through the use of bank borrowings. The Funds’ bank borrowing activities are as shown in the accompanying table.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Current Reporting Period | | | | | | Subsequent to the Close of the Reporting Period | |

| Fund | | Outstanding

Balance as of

August 1, 2021 | | | Draws | | | Paydowns | | | Outstanding

Balance as of

July 31, 2022 | | | Average Balance

Outstanding | | | | | | Draws | | | Paydowns | | | Outstanding

Balance as of

September 23, 2022 | |

| JPC | | $ | 462,700,000 | | | $ | 10,700,000 | | | $ | (50,000,000 | ) | | $ | 423,400,000 | | | $ | 455,111,644 | | | | | | | $ | — | | | $ | (150,000,000 | ) | | $ | 273,400,000 | |

| JPI | | $ | 234,800,000 | | | $ | 1,200,000 | | | $ | (20,000,000 | ) | | $ | 216,000,000 | | | $ | 231,129,315 | | | | | | | $ | 9,400,000 | | | $ | — | | | $ | 225,400,000 | |

| JPS | | $ | 873,300,000 | | | $

| —

|

| | $ | (374,000,000 | ) | | $ | 499,300,000 | | | $ | 829,047,945 | | | | | | | $ | — | | | $ | — | | | $ | 499,300,000 | |

| JPT | | $ | 47,000,000 | | | $

| —

|

| | $

| —

|

| | $ | 47,000,000 | | | $ | 47,000,000 | | | | | | | $ | — | | | $ | — | | | $ | 47,000,000 | |

| NPFD | | $

| —

|

| | $ | 210,200,000 | | | $ | (21,600,000 | ) | | $ | 188,600,000 | | | $ | 197,116,832 | * | | | | | | $ | — | | | $ | (33,800,000 | ) | | $ | 154,800,000 | |

| * | For the period January 11, 2022 (initial draw) through July 31, 2022. |

Refer to Notes to Financial Statements, Note 9 – Borrowing Arrangements and Reverse Repurchase Agreements for further details.

Reverse Repurchase Agreements

As noted previously, JPC, JPI, JPS and NPFD used reverse repurchase agreements, in which the Funds sell to a counterparty a security that it holds with a contemporaneous agreement to repurchase the same security at an agreed-upon price and date. The Funds’ transactions in reverse repurchase agreements are as shown in the accompanying table.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Current Reporting Period | | | | | | Subsequent to the Close of the Reporting Period | |

| Fund | | Outstanding

Balance as of

August 1, 2021 | | | Sales | | | Purchases | | | Outstanding

Balance as of

July 31, 2022 | | | Average Balance

Outstanding | | | | | | Sales | | | Purchases | | | Outstanding

Balance as of

September 23, 2022 | |

| JPC | | $ | 121,000,000 | | | $ | 3,500,000 | | | $ | (22,400,000 | ) | | $ | 102,100,000 | | | $ | 115,558,630 | | | | | | | $ | — | | | $ | — | | | $ | 102,100,000 | |

| JPI | | $ | 56,500,000 | | | $ | 8,500,000 | | | $ | — | | | $ | 65,000,000 | | | $ | 64,426,301 | | | | | | | $ | — | | | $ | — | | | $ | 65,000,000 | |

| JPS | | $ | 275,000,000 | | | $ | — | | | $

| —

|

| | $ | 275,000,000 | | | $ | 275,000,000 | | | | | | | $ | — | | | $ | — | | | $ | 275,000,000 | |

| NPFD | | $

| —

|

| | $ | 120,000,000 | | | $ | (16,598,000 | ) | | $ | 103,402,000 | | | $ | 107,266,712 | ** | | | | | | $ | 52,197,000 | | | $ | (103,402,000 | ) | | $ | 52,197,000 | |

| ** | For the period January 5, 2022 (initial purchase of reverse repurchase agreements) through July 31, 2022. |

Refer to Notes to Financial Statements, Note 9 – Borrowing Arrangements and Reverse Repurchase Agreements for further details.

Taxable Fund Preferred Shares

As noted previously, in addition to bank borrowings, JPS also issued TFP. The Fund’s transactions in TFP are as shown in the accompanying table.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Current Reporting Period | | | | | | Subsequent to the Close of the Reporting Period | |

Outstanding

Balance as of

August 1, 2021 | | | Issuance | | | Redemptions | | | Outstanding

Balance as of

July 31, 2022 | | | Average Balance

Outstanding | | | | | | Issuance | | | Redemptions | | | Outstanding

Balance as of

September 23, 2022 | |

| | $ — | | | | $270,000,000 | | | | $ — | | | | $270,000,000 | | | | $270,000,000 | * | | | | | | | $ — | | | | $ — | | | | $270,000,000 | |

| * | For the period July 14, 2022 (first issuance date of shares) through July 31, 2022. |

Refer to Notes to Financial Statements, Note 5 – Fund Shares and Note 11 - Subsequent Events for further details on TFP.

15

COMMON SHARE DISTRIBUTION INFORMATION

The following information regarding the Funds’ distributions is current as of July 31, 2022. Each Fund’s distribution levels may vary over time based on each Fund’s investment activity and portfolio investment value changes.

During the current reporting period, each Fund’s distributions to common shareholders were as shown in the accompanying table.

| | | | | | | | | | | | | | | | | | | | |

| | | Per Common Share Amounts | |

| Monthly Distributions (Ex-Dividend Date) | | JPC | | | JPI | | | JPS | | | JPT | | | NPFD | |

| August 2021 | | $ | 0.0530 | | | $ | 0.1305 | | | $ | 0.0505 | | | $ | 0.1185 | | | $ | — | |

| September | | | 0.0530 | | | | 0.1305 | | | | 0.0505 | | | | 0.1185 | | | | — | |

| October | | | 0.0530 | | | | 0.1305 | | | | 0.0505 | | | | 0.1185 | | | | — | |

| November | | | 0.0530 | | | | 0.1305 | | | | 0.0505 | | | | 0.1185 | | | | — | |

| December | | | 0.0530 | | | | 0.1305 | | | | 0.0505 | | | | 0.1185 | | | | — | |

| January | | | 0.0530 | | | | 0.1305 | | | | 0.0505 | | | | 0.1185 | | | | — | |

| February | | | 0.0530 | | | | 0.1305 | | | | 0.0505 | | | | 0.1185 | | | | 0.1380 | |

| March | | | 0.0530 | | | | 0.1305 | | | | 0.0505 | | | | 0.1350 | | | | 0.1380 | |

| April | | | 0.0530 | | | | 0.1305 | | | | 0.0475 | | | | 0.1350 | | | | 0.1380 | |

| May | | | 0.0530 | | | | 0.1305 | | | | 0.0475 | | | | 0.1350 | | | | 0.1380 | |

| June | | | 0.0530 | | | | 0.1305 | | | | 0.0475 | | | | 0.1350 | | | | 0.1380 | |

| July 2022 | | | 0.0530 | | | | 0.1305 | | | | 0.0435 | | | | 0.1255 | | | | 0.1380 | |

| Total Distributions | | $ | 0.6360 | | | $ | 1.5660 | | | $ | 0.5900 | | | $ | 1.4950 | | | $ | 0.8280 | |

| | | | | |

| Current Distribution Rate* | | | 7.76 | % | | | 7.64 | % | | | 6.72 | % | | | 7.43 | % | | | 8.29 | % |

| * | Current distribution rate is based on the Fund’s current annualized monthly distribution divided by the Fund’s current market price. The Fund’s monthly distributions to its shareholders may be comprised of ordinary income, net realized capital gains and, if at the end of the fiscal year the Fund’s cumulative net ordinary income and net realized gains are less than the amount of the Fund’s distributions, a return of capital for tax purposes. |

NPFD declared its first distribution of $0.1380 during January 2022, for shareholders of record on February 15, 2022 and payable on March 1, 2022. Each Fund seeks to pay regular monthly dividends out of its net investment income at a rate that reflects its past and projected net income performance. To permit each Fund to maintain a more stable monthly dividend, the Fund may pay dividends at a rate that may be more or less than the amount of net income actually earned by the Fund during the period. Distributions to common shareholders are determined on a tax basis, which may differ from amounts recorded in the accounting records. In instances where the monthly dividend exceeds the earned net investment income, the Fund would report a negative undistributed net ordinary income. Refer to Note 6 – Income Tax Information for additional information regarding the amounts of undistributed net ordinary income and undistributed net long-term capital gains and the character of the actual distributions paid by the Fund during the period.

All monthly dividends paid by each Fund during the current reporting period were paid from net investment income. If a portion of the Fund’s monthly distributions is sourced or comprised of elements other than net investment income, including capital gains and/or a return of capital, shareholders will be notified of those sources. For financial reporting purposes, the per share amounts of each Fund’s distributions for the reporting period are presented in this report’s Financial Highlights. For income tax purposes, distribution information for each Fund as of its most recent tax year end is presented in Note 6 – Income Tax Information within the Notes to Financial Statements of this report.

16

NUVEEN CLOSED-END FUND DISTRIBUTION AMOUNTS

The Nuveen Closed-End Funds’ monthly and quarterly periodic distributions to shareholders are posted on www.nuveen.com and can be found on Nuveen’s enhanced closed-end fund resource page, which is at https://www.nuveen.com/resource-center-closed-end-funds, along with other Nuveen closed-end fund product updates. To ensure timely access to the latest information, shareholders may use a subscribe function, which can be activated at this web page (https://www.nuveen.com/subscriptions).

COMMON SHARE EQUITY SHELF PROGRAMS

During the current reporting period, JPC and JPS were authorized by the Securities and Exchange Commission to issue additional common shares through an equity shelf program (Shelf Offering). Under these programs, JPC and JPS, subject to market conditions, may raise additional capital from time to time in varying amounts and offering methods at a net price at or above each Fund’s NAV per common share. The maximum aggregate offering under these Shelf Offerings, are as shown in the accompanying table.

| | | | | | | | |

| | | JPC | | | JPS | |

| Maximum aggregate offering | | | Unlimited | | | | Unlimited | |

During the current reporting period, JPS and JPC sold common shares through their Shelf Offerings at a weighted average premium to its NAV per common share as shown in the accompanying table.

| | | | | | | | |

| | | JPC | | | JPS | |

| Common shares sold through shelf offering | | | 1,185,860 | | | | 921,252 | |

| Weighted average premium to NAV per common share sold | | | 1.18 | % | | | 1.16 | % |

Refer to Notes to Financial Statements, Note 5 – Fund Shares for further details of Shelf Offerings and each Fund’s transactions.

COMMON SHARE REPURCHASES

During August 2022 (subsequent to the close of the reporting period), the Funds’ Board of Trustees reauthorized an open-market common share repurchase program for JPC, JPI, JPS and JPT and authorized an open-market common share repurchase for NPFD, allowing each Fund to repurchase an aggregate of up to approximately 10% of its outstanding common shares.

During the current reporting period, the Funds did not repurchase any of their outstanding common shares. As of July 31, 2022 (and since the inception of the Funds’ repurchase programs), each Fund has cumulatively repurchased and retired its outstanding common shares as shown in the accompanying table.

| | | | | | | | | | | | | | | | |

| | | JPC | | | JPI | | | JPS | | | JPT | |

| Common shares cumulatively repurchased and retired | | | 2,826,100 | | | | 0 | | | | 38,000 | | | | 0 | |

| Common shares authorized for repurchase | | | 10,380,000 | | | | 2,275,000 | | | | 20,475,000 | | | | 680,000 | |

TENDER OFFER

The Fund’s Board of Trustees authorized JPT to conduct a tender offer pursuant to which the Fund offered to purchase up to 100% of JPT’s outstanding shares for cash on a pro rata basis at a price per share equal to 100% of the NAV per share, as determined on the date the tender offer expires.

On January 19, 2022, Nuveen announced the Fund’s tender offer, which commenced on January 20, 2022 and expired on February 17, 2022. In the tender offer, 2,454,617 common shares were tendered, representing approximately 36% of the Fund’s common shares outstanding, and therefore the Fund repurchased these outstanding shares from participating shareholders.

17

During the current reporting period, JPT repurchased and retired their common shares, through the tender offer, at a price per share and a discount per share as shown in the accompanying table.

| | | | |

| Common shares repurchased and retired through tender offer | | | 2,454,617 | |

| Tender offer price per common share | | $ | 23.2613 | |

| Tender offer discount per common share | | | 0.00 | % |

Refer to Notes to Financial Statements, Note 5 – Fund Shares, Tender Offer for further details on the tender offer.

OTHER COMMON SHARE INFORMATION

As of July 31, 2022, the Funds’ common share prices were trading at a premium/(discount) to their common share NAV and trading at an average premium/(discount) to NAV during the current reporting period, as follows.

| | | | | | | | | | | | | | | | | | | | |

| | | JPC | | | JPI | | | JPS | | | JPT | | | NPFD | |

| Common share NAV | | $ | 8.41 | | | $ | 21.26 | | | $ | 8.25 | | | $ | 21.16 | | | $ | 21.06 | |

| Common share price | | $ | 8.20 | | | $ | 20.51 | | | $ | 7.77 | | | $ | 20.26 | | | $ | 19.98 | |

| Premium/(Discount) to NAV | | | (2.50 | )% | | | (3.53 | )% | | | (5.82 | )% | | | (4.25 | )% | | | (5.13 | )% |

| Average premium/(discount) to NAV | | | (3.26 | )% | | | (1.46 | )% | | | (3.90 | )% | | | (2.46 | )% | | | (3.52 | )% |

18

THIS PAGE INTENTIONALLY LEFT BLANK

19

| | |

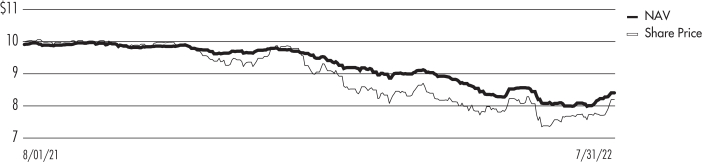

| | Nuveen Preferred & Income Opportunities Fund Performance Overview and Holding Summaries as of July 31, 2022 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of July 31, 2022*

| | | | | | | | | | | | |

| | | Average Annual | |

| | | | | | | | | | |

| JPC at Common Share NAV | | | (9.05)% | | | | 2.04% | | | | 6.02% | |

| JPC at Common Share Price | | | (11.91)% | | | | 2.32% | | | | 6.58% | |

| ICE BofA U.S. All Capital Securities Index | | | (9.18)% | | | | 2.96% | | | | 5.29% | |

| JPC Blended Benchmark | | | (9.64)% | | | | 2.77% | | | | 4.62% | |

| * | For purposes of Fund performance, relative results are measured against the JPC Blended Benchmark. Effective April 1, 2022, the Fund’s Blended Benchmark was updated to consist of: 1) 60% ICE BofA U.S. All Capital Securities Index and 2) 40% ICE USD Contingent Capital Index (CDLR). From December 31, 2013 through March 31, 2022, the Fund’s Blended Benchmark consists of: 1) 50% ICE BofA Fixed Rate Preferred Securities Index, 2) 30% ICE BofA U.S. All Capital Securities Index and 3) 20% ICE USD Contingent Capital Index (CDLR). Through December 30, 2013, the JPC Blended Benchmark’s consists of: 1) 82.5% ICE BofA Fixed Rate Preferred Securities Index and 2) 17.5% Bloomberg Capital Securities Index. Refer to the Glossary of Terms Used in this report for further details on the Fund’s Blended Benchmark compositions. |

Performance data shown represents past performance and does not predict or guarantee future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment. Performance for indexes that were created after the Fund’s inception are linked to the Fund’s previous benchmark.

Daily Common Share NAV and Share Price

Growth of an Assumed $10,000 Investment as of July 31, 2022 - Common Share Price

20

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| $1,000 Par (or similar) Institutional Preferred | | | 78.3% | |

| Contingent Capital Securities | | | 50.7% | |

| $25 Par (or similar) Retail Preferred | | | 28.2% | |

| Corporate Bonds | | | 0.7% | |

| Repurchase Agreements | | | 0.6% | |

| Other Assets Less Liabilities | | | 1.0% | |

| Net Assets Plus Borrowings and Reverse Repurchase Agreements, including accrued interest | | | 159.5% | |

| Borrowings | | | (47.9)% | |

| Reverse Repurchase Agreements, including accrued interest | | | (11.6)% | |

| Net Assets | | | 100% | |

(% of total investments)

| | | | |

| Banks | | | 47.4% | |

| Insurance | | | 14.4% | |

| Capital Markets | | | 13.5% | |

| Food Products | | | 4.7% | |

| Diversified Financial Services | | | 3.7% | |

| Trading Companies & Distributors | | | 2.7% | |

| Oil, Gas & Consumable Fuels | | | 2.5% | |

| Other | | | 10.8% | |

| Repurchase Agreements | | | 0.3% | |

| Total | | | 100% | |

(% of total investments)

| | | | |

| United States | | | 60.5% | |

| United Kingdom | | | 12.2% | |

| Switzerland | | | 7.6% | |

| France | | | 5.3% | |

| Spain | | | 2.4% | |

| Netherlands | | | 2.2% | |

| Canada | | | 2.0% | |

| Australia | | | 1.7% | |

| Germany | | | 1.5% | |

| Ireland | | | 1.4% | |

| Bermuda | | | 1.1% | |

| Other | | | 2.1% | |

| Total | | | 100% | |

Top Five Issuers

(% of total long-term

investments)

| | | | |

| UBS Group AG | | | 4.4% | |

| HSBC Holdings PLC | | | 3.6% | |

| Citigroup Inc | | | 3.3% | |

| Credit Suisse Group AG | | | 3.2% | |

| Barclays PLC | | | 2.9% | |

Portfolio Credit Quality

(% of total long-term fixed-income investments)

| | | | |

| A | | | 0.1% | |

| BBB | | | 65.6% | |

| BB or Lower | | | 32.3% | |

| N/R (not rated) | | | 2.0% | |

| Total | | | 100% | |

| 1 | See the Portfolio of Investments for the remaining industries/sectors comprising “Other” and not listed in the Portfolio Composition above. |

| 2 | Includes 2.0% (as a percentage of total investments) in emerging market countries. |

21

| | |

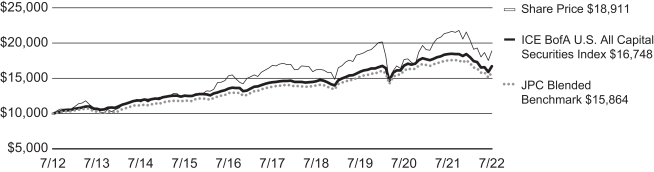

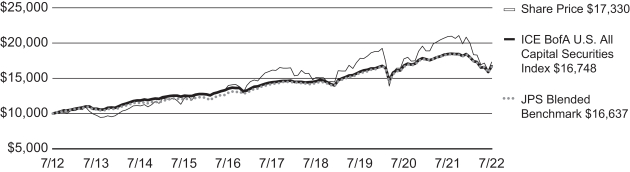

| | Nuveen Preferred and Income Term Fund Performance Overview and Holding Summaries as of July 31, 2022 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of July 31, 2022*

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

| JPI at Common Share NAV | | | (10.41)% | | | | 2.74% | | | | 6.56% | |

| JPI at Common Share Price | | | (16.35)% | | | | 2.86% | | | | 5.80% | |

| ICE BofA U.S. All Capital Securities Index | | | (9.18)% | | | | 2.96% | | | | 5.29% | |

| JPI Blended Benchmark | | | (9.48)% | | | | 3.16% | | | | 4.82% | |

| * | For purposes of Fund performance, relative results are measured against the JPI Blended Benchmark. The Fund’s Blended Benchmark consists of: 1) 60% ICE BofA U.S. All Capital Securities Index and 2) 40% ICE USD Contingent Capital Index (CDLR). Through December 30, 2013, the Fund’s Blended Benchmark consists of: 1) 65% ICE BofA Fixed Rate Preferred Securities Index and 2) 35% Bloomberg Capital Securities Index. Refer to the Glossary of Terms Used in this report for further details on the Fund’s Blended Benchmark compositions. |

Performance data shown represents past performance and does not predict or guarantee future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Daily Common Share NAV and Share Price

Growth of an Assumed $10,000 Investment as of July 31, 2022 - Common Share Price

22

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| $1,000 Par (or similar) Institutional Preferred | | | 74.7% | |

| Contingent Capital Securities | | | 51.1% | |

| $25 Par (or similar) Retail Preferred | | | 29.8% | |

| Corporate Bonds | | | 0.7% | |

| Repurchase Agreements | | | 1.0% | |

| Other Assets Less Liabilities | | | 0.8% | |

| Net Assets Plus Borrowings and Reverse Repurchase Agreements, including accrued interest | | | 158.1% | |

| Borrowings | | | (44.6)% | |

| Reverse Repurchase Agreements, including accrued interest | | | (13.5)% | |

| Net Assets | | | 100% | |

(% of total investments)

| | | | |

| Banks | | | 45.6% | |

| Insurance | | | 14.4% | |

| Capital Markets | | | 13.2% | |

| Diversified Financial Services | | | 4.9% | |

| Food Products | | | 4.9% | |

| Other | | | 16.4% | |

| Repurchase Agreements | | | 0.6% | |

| Total | | | 100% | |

(% of total investments)

| | | | |

| United States | | | 59.2% | |

| United Kingdom | | | 12.4% | |

| Switzerland | | | 7.6% | |

| France | | | 5.4% | |

| Spain | | | 2.3% | |

| Netherlands | | | 2.3% | |

| Canada | | | 2.2% | |

| Australia | | | 2.2% | |

| Germany | | | 1.6% | |

| Bermuda | | | 1.2% | |

| Ireland | | | 1.2% | |

| Other | | | 2.4% | |

| Total | | | 100% | |

Top Five Issuers

(% of total long-term

investments)

| | | | |

| UBS Group AG | | | 4.5% | |

| HSBC Holdings PLC | | | 3.6% | |

| Citigroup Inc | | | 3.2% | |

| Credit Suisse Group AG | | | 3.1% | |

| Barclays PLC | | | 2.9% | |

Portfolio Credit Quality

(% of total long-term fixed-income

investments)

| | | | |

| A | | | 0.2% | |

| BBB | | | 64.9% | |

| BB or Lower | | | 32.7% | |

| N/R (not rated) | | | 2.2% | |

| Total | | | 100% | |

| 1 | See the Portfolio of Investments for the remaining industries/sectors comprising “Other” and not listed in the Portfolio Composition above. |

| 2 | Includes 2.1% (as a percentage of total investments) in emerging market countries. |

23

| | |

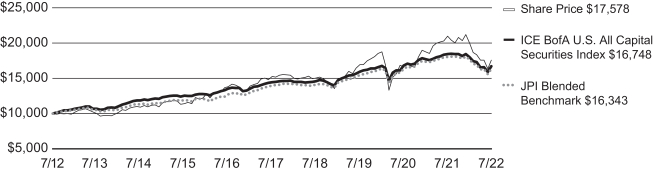

| | Nuveen Preferred & Income Securities Fund Performance Overview and Holding Summaries as of July 31, 2022 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of July 31, 2022*

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

| JPS at Common Share NAV | | | (11.16)% | | | | 2.21% | | | | 6.18% | |

| JPS at Common Share Price | | | (17.04)% | | | | 1.41% | | | | 5.65% | |

| ICE BofA U.S. All Capital Securities Index | | | (9.18)% | | | | 2.96% | | | | 5.29% | |

| JPS Blended Benchmark | | | (9.48)% | | | | 3.16% | | | | 5.23% | |

| * | For purposes of Fund performance, relative results are measured against the JPS Blended Benchmark. The Fund’s Blended Benchmark consists of: 1) 60% ICE BofA U.S. All Capital Securities Index and 2) 40% ICE USD Contingent Capital Index (CDLR). Through to December 30, 2013, the Fund’s Blended Benchmark consists of: 1) 55% ICE BofA Fixed Rate Preferred Securities Index and 2) 45% Bloomberg Capital Securities Tier-1 Index. Refer to the Glossary of Terms Used in this report for further details on the Fund’s Blended Benchmark compositions. |

Performance data shown represents past performance and does not predict or guarantee future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment. Performance for indexes that were created after the Fund’s inception are linked to the Fund’s previous benchmark.

Daily Common Share NAV and Share Price

Growth of an Assumed $10,000 Investment as of July 31, 2022 - Common Share Price

24

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| $1,000 Par (or similar) Institutional Preferred | | | 79.0% | |

| Contingent Capital Securities | | | 54.3% | |

| $25 Par (or similar) Retail Preferred | | | 17.3% | |

| Corporate Bonds | | | 4.7% | |

| Convertible Preferred Securities | | | 1.8% | |

| Investment Companies | | | 1.1% | |

| Repurchase Agreements | | | 1.8% | |

| Other Assets Less Liabilities | | | 1.4% | |

| Net Assets Plus Borrowings, Reverse Repurchase Agreements, including accrued interest and Taxable Fund Preferred Shares, net of deferred offering costs | | | 161.4% | |

| Borrowings | | | (29.4)% | |

| Reverse Repurchase Agreements, including accrued interest | | | (16.2)% | |

| Taxable Fund Preferred, net of deferred offering costs | | | (15.8)% | |

| Net Assets | | | 100% | |

(% of total investments)

| | | | |

| Banks | | | 53.2% | |

| Capital Markets | | | 14.9% | |

| Insurance | | | 14.7% | |

| Electric Utilities | | | 3.0% | |

| Other | | | 12.3% | |

| Repurchase Agreements | | | 1.2% | |

| Investment Companies | | | 0.7% | |

| Total | | | 100% | |

(% of total investments)

| | | | |

| United States | | | 54.6% | |

| United Kingdom | | | 11.4% | |

| France | | | 10.3% | |

| Switzerland | | | 9.0% | |

| Finland | | | 3.0% | |

| Spain | | | 2.1% | |

| Canada | | | 1.6% | |

| Netherlands | | | 1.3% | |

| Norway | | | 1.3% | |

| Australia | | | 1.2% | |

| Japan | | | 1.1% | |

| Other | | | 3.1% | |

| Total | | | 100% | |

Top Five Issuers

(% of total long-term

investments)

| | | | |

| Bank of America Corp | | | 4.3% | |

| UBS Group AG | | | 3.9% | |

| Credit Suisse Group AG | | | 3.5% | |

| BNP Paribas SA | | | 3.4% | |

| Barclays PLC | | | 3.4% | |

Portfolio Credit Quality

(% of total long-term fixed-income investments)

| | | | |

| A | | | 7.5% | |

| BBB | | | 79.1% | |

| BB or Lower | | | 13.4% | |

| Total | | | 100% | |

| 1 | See the Portfolio of Investments for the remaining industries/sectors comprising “Other” and not listed in the Portfolio Composition above. |

| 2 | Includes 0.0% (as a percentage of total investments) in emerging market countries. |

25

| | |

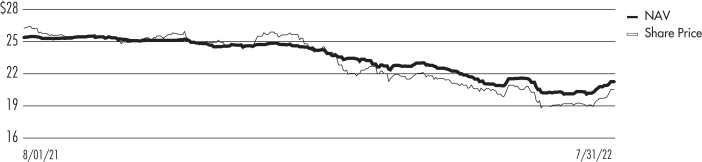

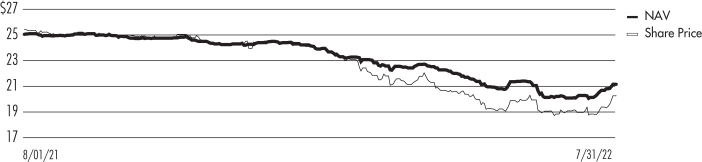

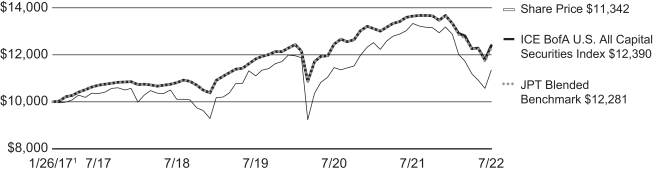

| | Nuveen Preferred and Income Fund Performance Overview and Holding Summaries as of July 31, 2022 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of July 31, 2022*

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | Since

Inception | |

| JPT at Common Share NAV | | | (9.81)% | | | | 2.33% | | | | 3.32% | |

| JPT at Common Share Price | | | (14.88)% | | | | 1.84% | | | | 2.31% | |

| ICE BofA U.S. All Capital Securities Index | | | (9.18)% | | | | 2.96% | | | | 3.97% | |

| JPT Blended Benchmark | | | (9.98)% | | | | 2.78% | | | | 3.80% | |

| * | For purposes of Fund performance, relative results are measured against the JPT Blended Benchmark. Effective February 28, 2022, the Fund’s Blended Benchmark consists of: 1) 60% ICE BofA U.S. All Capital Securities Index and 2) 40% ICE USD Contingent Capital Index (CDLR). Prior to February 28, 2022, the Fund’s performance was measured against the ICE BofA U.S. All Capital Securities Index. Refer to the Glossary of Terms Used in this report for further details. |

Since inception returns are from 1/26/17. Performance data shown represents past performance and does not predict or guarantee future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Daily Common Share NAV and Share Price

Growth of an Assumed $10,000 Investment as of July 31, 2022 - Common Share Price

| 1 | Value on 1/26/17 is $24.63, which represents the Fund’s public offering price less sales load. |

26

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| $1,000 Par (or similar) Institutional Preferred | | | 75.1% | |

| Contigent Capital Securities | | | 44.9% | |

| $25 Par (or similar) Retail Preferred | | | 25.5% | |

| Corporate Bonds | | | 3.9% | |

| Repurchase Agreements | | | 0.2% | |

| Other Assets Less Liabilities | | | 1.0% | |

| Net Assets Plus Borrowings | | | 150.6% | |

| Borrowings | | | (50.6)% | |

| Net Assets | | | 100% | |

Top Five Issuers

(% of total long-term investments)

| | | | |

| UBS Group AG | | | 4.5% | |

| HSBC Holdings PLC | | | 4.0% | |

| Citigroup Inc | | | 3.3% | |

| Barclays PLC | | | 3.0% | |

| Credit Suisse Group AG | | | 3.0% | |

(% of total investments)

| | | | |

| Banks | | | 44.6% | |

| Insurance | | | 15.0% | |

| Capital Markets | | | 13.5% | |

| Food Products | | | 5.2% | |

| Diversified Financial Services | | | 4.8% | |

| Trading Companies & Distributors | | | 3.1% | |

| Other | | | 13.7% | |

| Repurchase Agreements | | | 0.1% | |

| Total | | | 100% | |

Portfolio Credit Quality

(% of total long-term

fixed-income investments)

| | | | |

| A | | | 0.2% | |

| BBB | | | 65.3% | |

| BB or Lower | | | 33.1% | |

| N/R (not rated) | | | 1.4% | |

| Total | | | 100% | |

(% of total investments)

| | | | |

| United States | | | 58.5% | |

| United Kingdom | | | 11.8% | |

| Switzerland | | | 7.5% | |

| France | | | 5.8% | |

| Spain | | | 2.2% | |

| Ireland | | | 2.2% | |

| Germany | | | 2.2% | |

| Netherlands | | | 2.2% | |

| Canada | | | 2.2% | |

| Australia | | | 1.9% | |

| Bermuda | | | 1.6% | |

| Other | | | 1.9% | |

| Total | | | 100% | |

| 1 | See the Portfolio of Investments for the remaining industries/sectors comprising “Other” and not listed in the Portfolio Composition above. |

| 2 | Includes 2.6% (as a percentage of total investments) in emerging market countries. |

27

| | |

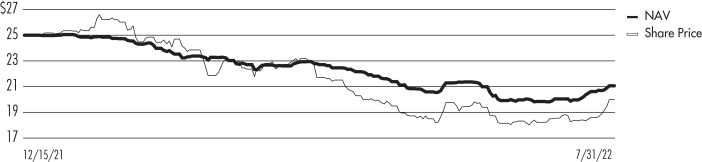

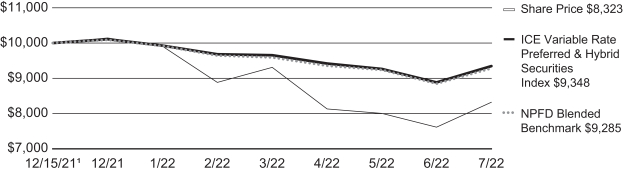

| | Nuveen Variable Rate Preferred & Income Fund Performance Overview and Holding Summaries as of July 31, 2022 |

Refer to Glossary of Terms Used in this Report for further definition of terms used in this section.

Cumulative Total Returns as of July 31, 2022*

| | | | |

| | | Since

Inception | |

| NPFD at Common Share NAV | | | (12.48)% | |

| NPFD at Common Share Price | | | (16.77)% | |

| ICE Variable Rate Preferred & Hybrid Securities Index | | | (6.52)% | |

| NPFD Blended Benchmark | | | (7.15)% | |

| * | For purposes of Fund performance, relative results are measured against the NPFD Blended Benchmark. The Fund’s Blended Benchmark consists of: 1) 80% ICE Variable Rate Preferred & Hybrid Securities Index and 2) 20% ICE USD Contingent Capital Index (CDLR). |