QuickLinks -- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on March , 2004

Registration No. 333-112991

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Noveon International, Inc.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) | 2891 (Primary Standard Industrial Classification Code Number) | 13-4143923 (I.R.S. Employer Identification Number) |

9911 Brecksville Road

Cleveland, Ohio 44141

(216) 447-5000

(Address, including zip code, and telephone number, including

area code, of registrant's principal executive offices)

Christopher R. Clegg, Esq.

Senior Vice President, General Counsel and Secretary

Noveon International, Inc.

9911 Brecksville Road

Cleveland, Ohio 44141

(216) 447-5000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||

| Jean E. Hanson, Esq. Fried, Frank, Harris, Shriver & Jacobson LLP One New York Plaza New York, New York 10004 (212) 859-8000 | Peter M. Labonski, Esq. Latham & Watkins LLP 885 Third Avenue New York, NY 10022-4802 (212) 906-1200 | |

Approximate date of commencement of proposed sale to public:As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. o

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MARCH , 2004

Shares

Noveon International, Inc.

Common Stock

Prior to this offering there has been no public market for our common stock. The initial public offering price of the common stock is expected to be between $ and $ per share. We have applied to list our common stock on The New York Stock Exchange under the symbol "NOV."

We are selling shares of common stock and the selling stockholders are selling shares of common stock. We will not receive any of the proceeds from the shares of common stock sold by the selling stockholders.

The underwriters have an option to purchase a maximum of additional shares to cover over-allotments of shares.

Investing in our common stock involves risks. See "Risk Factors" on page 11.

| | Price to Public | Underwriting Discounts and Commissions | Proceeds to Noveon International | Proceeds to Selling Stockholders | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Per Share | $ | $ | $ | $ | ||||||||

| Total | $ | $ | $ | $ | ||||||||

Delivery of the shares of common stock will be made on or about , 2004.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Joint Book-Running Managers | ||||

Credit Suisse First Boston | Deutsche Bank Securities | UBS Investment Bank | ||

| Goldman, Sachs & Co. | Merrill Lynch & Co. |

The date of this prospectus is , 2004.

[PICTURES AND DESCRIPTIONS TO COME]

| PROSPECTUS SUMMARY | 1 | |

| RISK FACTORS | 11 | |

| CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS | 22 | |

| USE OF PROCEEDS | 23 | |

| DIVIDEND POLICY | 23 | |

| CAPITALIZATION | 24 | |

| DILUTION | 25 | |

| SELECTED CONSOLIDATED FINANCIAL AND OTHER DATA | 27 | |

| MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 32 | |

| BUSINESS | 55 | |

| MANAGEMENT | 71 | |

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS | 84 | |

| PRINCIPAL AND SELLING STOCKHOLDERS | 87 | |

| DESCRIPTION OF OUR INDEBTEDNESS | 90 | |

| DESCRIPTION OF CAPITAL STOCK | 93 | |

| SHARES ELIGIBLE FOR FUTURE SALE | 96 | |

| CERTAIN UNITED STATES FEDERAL TAX CONSIDERATIONS FOR NON-UNITED STATES HOLDERS | 98 | |

| UNDERWRITING | 101 | |

| LEGAL MATTERS | 106 | |

| EXPERTS | 106 | |

| WHERE YOU CAN FIND MORE INFORMATION | 107 | |

| INDEX TO CONSOLIDATED FINANCIAL STATEMENTS | F-1 |

You should rely only on the information contained in this document or to which we have referred you. We have not authorized anyone to provide you with information that is different. This document may only be used where it is legal to sell these securities. The information in this document may only be accurate on the date of this document.

This prospectus includes market share and industry data and forecasts that we obtained from internal company surveys, market research, consultant surveys, publicly available information and industry publications and surveys. Industry surveys, publications, consultant surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but there can be no assurance as to the accuracy and completeness of such information. We have not independently verified any of the data from third-party sources nor have we ascertained the underlying economic assumptions relied upon therein. Similarly, internal company surveys, industry forecasts and market research, which we believe to be reliable based upon management's knowledge of the industry, have not been verified by any independent sources. In addition, we do not know what assumptions regarding general economic growth were used in preparing the forecasts we cite. Except where otherwise noted, references to North America include only the United States and Canada, and statements as to our position relative to our competitors or as to market share refer to the most recent available data.

Dealer Prospectus Delivery Obligation

Until , 2004, all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealer's obligation to deliver a prospectus when acting as an underwriter and with respect to unsold allotments or subscriptions.

In this prospectus, "Noveon International, Inc.," "Noveon International," "Noveon," the "Company," "we," "us" or "our" refer to Noveon International, Inc. (formerly known as Noveon Holdings, Inc.) and its subsidiaries, except where the context makes clear that the reference is only to Noveon International, Inc. itself and not its subsidiaries. Any references to the "Company," "we," "us" or "our" as of a date prior to February 28, 2001, the date of the completion of our acquisition of the Performance Materials Segment from the Goodrich Corporation (formerly known as The B.F.Goodrich Company), are to the Performance Materials Segment of the Goodrich Corporation, the predecessor to Noveon, Inc. Any references to "Goodrich" are to the Goodrich Corporation. Any references to "Noveon, Inc." are to Noveon, Inc., our wholly owned operating subsidiary.

Unless otherwise indicated, the information in this prospectus does not give effect to a -for-one stock split of our common stock, which will occur immediately prior to the completion of this offering.

Our Business

We are a leading global producer and marketer of technologically advanced specialty materials and chemicals used in a broad range of consumer and industrial applications. We have a number of high growth, industry-leading product franchises marketed under some of the industry's most recognized brand names including Carbopol®, TempRite®, Estane® and Hycar®. These global brands are complemented by a diverse portfolio of historically stable, cash-generating businesses. We have a significant presence in many niche product categories, where customers value our long-standing ability to provide need-specific formulations and solutions. Our products and services enhance the value of customers' end-products by improving performance, providing essential product attributes, lowering cost, simplifying processing or making them more environmentally friendly.

Through our worldwide network of 29 strategically located manufacturing facilities, we serve more than 7,000 customers operating in over 25 industries. In 2003, we generated sales of $1,135.9 million, a net loss of $7.9 million, net cash provided by operating activities of $118.0 million and Adjusted EBITDA of $201.3 million. We derived approximately 59% of our sales from the United States, 21% of our sales from Europe and 20% of our sales from the rest of the world in 2003. Our margins, combined with our strong cash flow from operations, ongoing capital efficiency efforts and available cash, provide us with significant flexibility to capitalize on future growth opportunities.

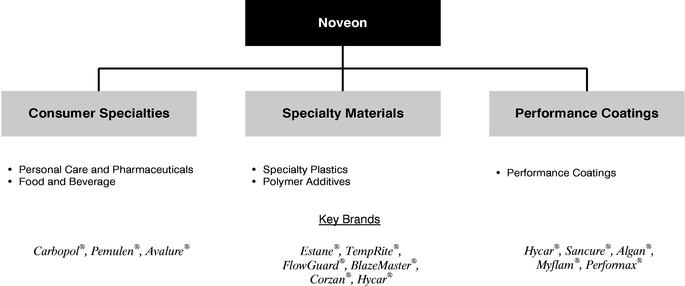

Consistent with our focus on industries and end-use applications, we have organized our business into three segments: Consumer Specialties, Specialty Materials and Performance Coatings.

1

Consumer Specialties is a global producer of specialty chemicals targeting the personal care, pharmaceutical and food and beverage industries. Key products in this segment include Carbopol® acrylic thickeners, film formers, fixatives, emollients, silicones, botanicals, active pharmaceutical ingredients and intermediates, benzoate preservatives, fragrances, synthetic food dyes and natural colorants. Primary end-uses in the personal care industry for Carbopol® acrylic thickeners include hair care, skin care and personal and oral hygiene products. In 2003, Consumer Specialties generated sales of $328.7 million, segment operating income of $47.0 million and Segment EBITDA of $73.1 million.

Specialty Materials is the largest global supplier of chlorinated polyvinyl chloride (CPVC) resins and compounds and reactive liquid polymers (RLP), sold under the respective trademarks TempRite® and Hycar®. Specialty Materials is also a leading producer of thermoplastic polyurethane (TPU) sold under the trademark Estane®. With respect to the markets in which we compete, Specialty Materials is a leading producer of cross-linked polyethylene compounds (PEX) sold under the trademark TempRite®. Applications for TempRite® resins and compounds include piping for residential and commercial plumbing and fire sprinkler systems. Applications for Estane® TPU include plastic film and sheet for various coatings processes. Applications for Hycar® RLP include engineering adhesives. Specialty Materials is also a leading North American producer of rubber and lubricant antioxidants and rubber accelerators. In 2003, Specialty Materials generated sales of $428.6 million, segment operating income of $75.8 million and Segment EBITDA of $110.6 million.

Performance Coatings is a leading global producer of high-performance polymers for specialty paper, printing and packaging, industrial and architectural specialty coatings and textile applications. Approximately 70% of Performance Coatings' sales are generated from our water-based acrylic polymers and compounds and polyurethane dispersions. We believe that we offer customized solutions to meet the specific needs of our customers sold under the trademarks Hycar®, Sancure®, Algan®, Performax® and Myflam®. In 2003, Performance Coatings generated sales of $378.6 million, segment operating income of $43.3 million and Segment EBITDA of $63.4 million.

Our Competitive Strengths

Leading Product Franchises. Approximately 65% of our 2003 EBITDA was generated by products that hold #1 or #2 global positions, including Carbopol® acrylic thickener, TempRite® CPVC, Estane® TPU and Hycar® acrylic emulsions. We have a proprietary technology position in each of these products within their respective industries, which contributed to above average industry growth rates. Carbopol® acrylic thickener volume for personal care and pharmaceuticals, measured in pounds sold, grew at a compound annual rate of approximately 8.5% per year between 1993 and 2003, while we estimate that the personal care industry grew at 3.5% during the same period. Between 1993 and 2003, volume, measured in pounds used, of our TempRite® resins and compounds grew at a compound annual rate of approximately 8.4% per year, 1.9 times the growth rate of U.S. residential construction during the same period.

Commitment to Innovation. We believe that innovation and new product development is critical to meeting our customers' needs and to fuel future growth. Our history of technological innovation includes the invention of Carbopol® acrylic thickener and the commercial development of TempRite® CPVC. Carbopol® acrylic thickener is the global leader in synthetic thickeners due to its efficient stabilizing properties and superior thickening capabilities. TempRite® CPVC is the industry standard for CPVC piping, which is a higher performance, lower cost alternative to copper and steel in household plumbing, fire sprinklers and other industrial applications. Our commitment to innovation is demonstrated by recent increases in research and development employment and spending. We have increased our research and development and technical service staff by 21%, or 64 positions, and spending has increased 21%, or $7.7 million, since 2001.

2

Customized Value-Added Products. We have developed many of our products in cooperation with our customers, often as a result of their specific needs, resulting in long-standing, loyal customer relationships. Our products generally represent a small percentage of our customers' production costs but are critical to end-product performance. In addition, many of our products are specified in our customers' formulations, resulting in significant barriers to changing suppliers. Specific examples include carbomer thickeners in personal care and pharmaceutical applications and FDA-approved polymers used in food packaging applications.

Strong Cash Flow. We generate strong cash flow from operations after capital expenditures. Since our inception in March 2001, we have generated $278.2 million in cash flow from operations after capital expenditures. Our ability to generate strong and stable cash flows is principally attributable to the diversity of our product lines, industry-leading margins, rigorous management of working capital and relatively low capital expenditures. Our strong cash flow will enable us to invest in targeted growth strategies and continue to reduce indebtedness thereby enhancing our ability to grow earnings.

Relentless Focus on Productivity Improvement. Our operating culture is based on continuing productivity improvement, maximizing operating efficiency and optimizing the use of capital resources across all production lines. Since we began operation as a stand-alone company in 2001, we have successfully implemented cost-saving initiatives that reduced our fixed manufacturing overhead by over $20 million, delayered our organization, reduced working capital, refocused our capital spending and introduced our Six Sigma productivity initiative.

Proven Management Team with Significant Equity Interest. We have a highly motivated senior management team with an average of approximately 20 years of experience in the specialty chemicals industry. Our senior management has instilled an entrepreneurial culture throughout our organization, successfully implemented leading productivity practices, reinvigorated our new product development efforts, and positioned us for strong future earnings growth and cash flow generation. As of February 29, 2004, our management and employees held outstanding shares and granted options representing approximately 9.3% of our equity.

Our Growth Strategy

Enter New Applications and End-Uses. We intend to build on our core product franchises and technology to expand our product offerings by modifying existing formulations to meet new end-use applications. For example, we pioneered the development of hand sanitizing gels by using the thickening and stabilizing properties of Carbopol® acrylic thickener to combine water and alcohol, and we broadened the use of Carbopol® acrylic thickeners into applications such as oven cleaners and alkaline batteries. We have also expanded our BlazeMaster® fire sprinkler opportunities by obtaining amendments to building codes, allowing us to participate in a broader spectrum of fire sprinkler applications, including dormitories and single and multi-family homes.

Expand Global Reach. We expect to continue to serve our existing multinational customers globally as they penetrate emerging regions and to target other customers in such regions. Our approach is to strategically add sales, marketing and research and development related personnel in selected regions and to follow with further infrastructure expansion as the markets for our customers' products develop. For example, in 2003 we acquired a controlling interest in a Thailand-based manufacturer of formulated botanical extracts used in personal care applications. This acquisition provides us with access to products that we plan to sell throughout our global distribution system. In addition, we began producing textile coating compounds and started construction of a TPU plant in China to service regional demand.

Extend Product Breadth. We expect to continue to expand our product offerings through both internal research and development and the acquisition of new formulations and products. For example,

3

in 2003, we developed and introduced Fixate™, a fixative used in hair care styling resins, allowing us to broaden our hair care application base. In addition, we acquired aliphatic TPU technologies and assets that allow us to enter high-value optical film and medical tubing applications. In 2004, we purchased Scher Chemicals, Inc., a manufacturer of emollients used in skin care, one of the largest and fastest growing applications in the personal care industry.

Continue Productivity Improvements. We expect to continue our successful cost-saving initiatives by pursuing operational efficiencies, optimizing available technologies, maintaining a lean organizational structure, reducing fixed costs, rationalizing capacity and efficiently managing capital spending. In 2002, we launched a Six Sigma initiative, which has been designed to further enhance our understanding of our customers' needs, our process capabilities and the total cost of maintaining quality. We have 21 employees trained as Six Sigma black belts throughout our Company. We are targeting an increase of 10 black belts per year. We believe this initiative is a natural extension of our productivity efforts and allows us to focus our activities on those areas expected to provide us with the highest customer impact and organizational productivity.

Actively Manage Business Portfolio. We plan to accelerate profitable growth through selected acquisitions of assets and technology that focus on high value niche applications and complement our current product offerings and capabilities. We have made 11 targeted strategic acquisitions since our inception. At the same time, we will consider selective divestitures to optimize our product portfolio and to strengthen our financial flexibility.

Other Information

We commenced operations on March 1, 2001 through the acquisition on February 28, 2001 of the Performance Materials Segment of Goodrich. The total purchase price was $1,386.5 million before fees and expenses. The textile dyes and drug delivery system businesses that were operated as part of the Performance Materials Segment of Goodrich were not part of the acquisition.

PMD Investors I LLC and PMD Investors II LLC, collectively referred to in this prospectus as PMD, are entities owned by investor groups led by AEA Investors LLC, the successor company of AEA Investors Inc., referred to in this prospectus as AEA. DLJ Merchant Banking Partners III, LP and affiliated funds are affiliates of Credit Suisse First Boston LLC. DLJ Merchant Banking Partners III, LP and its affiliated funds that hold shares of our common stock are collectively referred to as DLJ Merchant Banking in this prospectus. MidOcean Capital/PMD Investors, LLC is referred to as MidOcean in this prospectus. We have no independent operations or investments other than our investment in Noveon, Inc.

We and Noveon, Inc. were capitalized as follows:

- •

- PMD, DLJ Merchant Banking and MidOcean contributed $355.0 million of cash as equity to us, which we in turn contributed to Noveon, Inc. Of this amount, PMD contributed $155.0 million, DLJ Merchant Banking contributed $150.0 million and MidOcean contributed $50.0 million. The price paid per share of our common stock by PMD, DLJ Merchant Banking and MidOcean, after giving effect to a -for-one stock split of our common stock, that will occur immediately prior to the completion of this offering, was $ ;

- •

- We issued a $172.0 million seller note to Goodrich, which was subsequently sold by Goodrich in March 2003 to various holders in a private placement; and

- •

- Noveon, Inc. issued $275.0 million of senior subordinated notes and borrowed $635.0 million under senior credit facilities. The credit facilities are secured by substantially all of our assets, substantially all of the assets of Noveon, Inc. and its domestic subsidiaries, 100% of the capital stock of its direct and indirect restricted domestic subsidiaries and 65% of the capital stock of its first tier foreign subsidiaries. In addition, the credit facilities are guaranteed by us and each of the direct and indirect material domestic subsidiaries of Noveon, Inc.

Our principal executive offices are located at 9911 Brecksville Road, Cleveland, Ohio 44141 and our telephone number is 216-447-5000. Our website is located at www.noveoninc.com. Information contained on our website does not constitute a part of this prospectus.

4

| Common stock offered: | ||||

By us | shares ( shares if the underwriters' over-allotment option is fully exercised). | |||

By the selling stockholders | shares ( shares if the underwriters' over-allotment option is fully exercised). | |||

Total | shares ( shares if the underwriters' over-allotment option is fully exercised). | |||

Common stock outstanding after the offering | shares. | |||

Use of proceeds | We estimate that our net proceeds from the sale of the shares offered by us, after deducting estimated expenses and underwriting discounts and commissions of $ million, will be approximately $ million (approximately $ million if the underwriters' over-allotment option is fully exercised). We intend to use substantially all of the net proceeds from this offering and the proposed concurrent senior notes offering to repay approximately $ million of our debt obligations outstanding under the seller note, including call premiums and accrued interest, to repay a portion of our term loans and to make total payments of $ million in connection with the management and advisory services agreements, which are being terminated. We will not receive any proceeds from the sale of shares by the selling stockholders. See "Use of Proceeds." | |||

Proposed NYSE symbol | "NOV." | |||

Risk Factors | See "Risk Factors" beginning on page 11 of this prospectus for a discussion of factors that you should carefully consider before deciding to invest in shares of our common stock. | |||

We are contemplating the issuance of debt securities in connection with this offering. Any offering of debt securities concurrently with this offering would not be a condition to the completion of this offering.

Unless we specifically state otherwise, the information in this prospectus does not take into account the sale of up to shares of common stock, which the underwriters have the option to purchase from us and the selling stockholders to cover over-allotments, and an aggregate of shares of common stock reserved for issuance under outstanding stock options and under our Employee Stock Purchase Plan. Options to purchase shares of common stock will be outstanding upon completion of this offering, of which options to purchase shares will be exercisable upon completion of this offering at a weighted average exercise price of $ per share.

5

SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA

The following table presents summary financial data at the dates and for the periods indicated. The data for the years ended December 31, 1999 and 2000 and the two months ended February 28, 2001 are derived from the audited consolidated historical financial statements of the Performance Materials Segment of Goodrich. The data for the ten months ended December 31, 2001 and the years ended December 31, 2002 and 2003 are derived from our audited consolidated financial statements. The unaudited, as adjusted, summary financial data for the year ended December 31, 2003 include the impact of this offering and application of the net proceeds therefrom as if such transactions occurred at the beginning of the period presented. The information set forth below should be read in conjunction with the consolidated financial statements and the related notes and "Management's Discussion and Analysis of Financial Condition and Results of Operations" and other financial information included elsewhere in this prospectus.

| | Performance Materials Segment of Goodrich | Noveon International, Inc. | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | | Two Months Ended February 28 2001 | Ten Months Ended December 31 2001 | | | |||||||||||||

| | Years Ended December 31 | Years Ended December 31 | |||||||||||||||||

| | 1999 | 2000 | 2002 | 2003 | |||||||||||||||

| | (dollars in millions) | ||||||||||||||||||

| Statement of Operations Data: | |||||||||||||||||||

| Sales | $ | 1,217.7 | $ | 1,167.7 | $ | 187.0 | $ | 876.4 | $ | 1,069.3 | $ | 1,135.9 | |||||||

| Cost of sales | 832.2 | 819.5 | 137.3 | 628.1 | 726.8 | 809.4 | |||||||||||||

| Gross profit | 385.5 | 348.2 | 49.7 | 248.3 | 342.5 | 326.5 | |||||||||||||

| Selling and administrative expenses | 218.2 | 201.1 | 35.2 | 160.5 | 202.8 | 204.8 | |||||||||||||

| Amortization expense | 24.6 | 24.4 | 4.0 | 26.5 | 13.9 | 14.7 | |||||||||||||

| Restructuring and severance costs | 37.3 | 40.5 | — | 3.1 | 6.1 | 13.2 | |||||||||||||

| Operating income | 105.4 | 82.2 | 10.5 | 58.2 | 119.7 | 93.8 | |||||||||||||

| Interest (income) expense—net | (0.5 | ) | (4.4 | ) | (0.6 | ) | 92.6 | 99.6 | 90.9 | ||||||||||

| Other expense (income)—net | 1.5 | 0.4 | 1.5 | 0.7 | (10.0 | ) | 1.1 | ||||||||||||

| Income (loss) before income taxes and cumulative effect of accounting change | 104.4 | 86.2 | 9.6 | (35.1 | ) | 30.1 | 1.8 | ||||||||||||

| Income tax expense | 42.3 | 35.9 | 4.0 | 4.6 | 6.4 | 9.2 | |||||||||||||

| Income (loss) before cumulative effect of accounting change | 62.1 | 50.3 | 5.6 | (39.7 | ) | 23.7 | (7.4 | ) | |||||||||||

| Cumulative effect of accounting change—net of tax | — | — | — | — | — | (0.5 | ) | ||||||||||||

| Net income (loss) | $ | 62.1 | $ | 50.3 | $ | 5.6 | $ | (39.7 | ) | $ | 23.7 | $ | (7.9 | ) | |||||

6

| | Year Ended December 31, 2003 | |||

|---|---|---|---|---|

| | (dollars in millions, except share information) (unaudited) | |||

| As Adjusted Data(1): | ||||

| Income (loss) before cumulative effect of accounting change | $ | |||

| Cumulative effect of accounting change—net of tax | ||||

| Net income (loss) | $ | |||

Basic earnings per share: | ||||

| Income (loss) before cumulative effect of accounting change | $ | |||

| Cumulative effect of accounting change—net of tax | ||||

| Net income (loss) | $ | |||

| Diluted earnings per share: | ||||

| Income (loss) before cumulative effect of accounting change | $ | |||

| Cumulative effect of accounting change—net of tax | ||||

| Net income (loss) | $ | |||

Weighted-average shares outstanding: | ||||

| Basic | ||||

| Diluted | ||||

| | Performance Materials Segment of Goodrich | Noveon International, Inc. | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | | Two Months Ended February 28 2001 | Ten Months Ended December 31 2001 | | | |||||||||||||

| | Years Ended December 31 | Years Ended December 31 | |||||||||||||||||

| | 1999 | 2000 | 2002 | 2003 | |||||||||||||||

| | (dollars in millions) | ||||||||||||||||||

| Other Data: | |||||||||||||||||||

| Net cash provided (used) by operating activities | $ | 156.1 | $ | 180.9 | $ | (31.6 | ) | $ | 153.9 | $ | 143.7 | $ | 118.0 | ||||||

| Net cash (used) by investing activities | (97.3 | ) | (75.3 | ) | (7.6 | ) | (1,218.7 | ) | (79.7 | ) | (88.7 | ) | |||||||

| Net cash (used) provided by financing activities | (54.4 | ) | (100.2 | ) | 37.5 | 1,188.4 | (112.3 | ) | (1.2 | ) | |||||||||

| EBITDA(2) | 190.8 | 168.5 | 23.4 | 140.5 | 214.4 | 184.1 | |||||||||||||

| EBITDA margin(3) | 15.7 | % | 14.4 | % | 12.5 | % | 16.0 | % | 20.1 | % | 16.2 | % | |||||||

| Adjusted EBITDA(4) | $ | 228.1 | $ | 209.0 | $ | 23.4 | $ | 146.9 | $ | 211.8 | $ | 201.3 | |||||||

| Adjusted EBITDA margin(5) | 18.7 | % | 17.9 | % | 12.5 | % | 16.8 | % | 19.8 | % | 17.7 | % | |||||||

| Depreciation and amortization | $ | 86.9 | $ | 86.7 | $ | 14.4 | $ | 83.0 | $ | 84.7 | $ | 91.4 | |||||||

| Capital expenditures | 79.6 | 64.0 | 7.6 | 28.5 | 52.3 | 56.6 | |||||||||||||

7

| | Performance Materials Segment of Goodrich | Noveon International, Inc | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | December 31 | December 31, 2003 | |||||||||||||||

| | 1999 | 2000 | 2001 | 2002 | Actual | As Adjusted(1) | |||||||||||

| | (dollars in millions) | ||||||||||||||||

| Balance Sheet Data: | |||||||||||||||||

| Cash and cash equivalents | $ | 10.6 | $ | 15.7 | $ | 124.0 | $ | 79.5 | $ | 116.8 | |||||||

| Goodwill | 342.1 | 307.0 | 346.9 | 367.3 | 416.0 | ||||||||||||

| Identifiable intangible assets—net | 60.9 | 58.9 | 192.0 | 182.1 | 172.9 | ||||||||||||

| Total assets | 1,430.6 | 1,359.2 | 1,664.8 | 1,634.5 | 1,757.6 | ||||||||||||

| Total debt | 42.7 | 30.0 | 1,083.9 | 992.7 | 1,030.3 | ||||||||||||

| Goodrich investment | 950.9 | 910.4 | — | — | — | ||||||||||||

| Stockholders' equity | — | — | 309.1 | 346.5 | 412.3 | ||||||||||||

- (1)

- The as adjusted balance sheet data assumes the sale by us of (i) shares in this offering at an assumed initial offering price of $ per share (the midpoint of the range) and (ii) $ million of % senior notes due 20 in a concurrent offering, and the application of the proceeds of these offerings (a) to the total payment of $ million of our debt obligations outstanding under the seller note including premiums and accrued interest, (b) to repay a portion of our term loans and (c) to the total payments of $ million to be paid in connection with the management and advisory services agreements, which are being terminated. The as adjusted statement of operations data reflect a reduction in interest expense of $ million, and a reduction of selling and administrative expenses of $4.0 million in connection with the termination of the management and advisory services agreements for the year ended December 31, 2003. The as adjusted statement of operations data and per share data do not reflect the payments of $ million to be paid in connection with the management and advisory services agreements, and the call premiums associated with the repayment of a portion of the seller note. See "Use of Proceeds" and "Certain Relationships and Related Transactions—Management and Advisory Services Agreements."

- (2)

- EBITDA is defined as net income (loss) before cumulative effect of accounting change, income tax expense, interest (income) expense, depreciation and amortization. We present EBITDA because we consider it an important supplemental measure of our performance and believe it is frequently used by securities analysts, investors and other interested parties in the evaluation of companies in our industry, many of which present EBITDA when reporting their results.

- •

- EBITDA does not reflect our cash expenditures, or future requirements, for capital expenditures or contractual commitments;

- •

- EBITDA does not reflect changes in, or cash requirements for, our working capital needs;

- •

- EBITDA does not reflect the significant interest expense or cash requirements necessary to service interest or principal payments on our debts;

- •

- Although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and EBITDA does not reflect any cash requirements for such replacements; and

We also use EBITDA because our credit agreement and our indenture use EBITDA with additional adjustments to measure our compliance with covenants such as interest coverage, leverage ratio and debt incurrence and because compensation agreements with our employees use EBITDA with additional adjustments as a performance measure.

EBITDA has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our financial results prepared in accordance with generally accepted accounting principles, or GAAP. Some of these limitations are:

8

- •

- Other companies in our industry may calculate EBITDA differently than we do, limiting its usefulness as a comparative measure.

Because of these limitations, EBITDA should not be considered as a measure of discretionary cash available to us to invest in the growth of our business. We compensate for these limitations by relying primarily on our GAAP results and using EBITDA and Adjusted EBITDA only supplementally. See the Consolidated Statement of Cash Flows included in our financial statements located elsewhere in this prospectus.

- (3)

- EBITDA margin is defined as EBITDA as a percentage of sales.

- (4)

- We present Adjusted EBITDA as a further supplemental measure of our performance. Adjusted EBITDA data is an important metric used by management with respect to both the performance of our fundamental business activities as well as our ability to meet future debt service, capital expenditures and working capital needs. We prepare Adjusted EBITDA by adjusting EBITDA to eliminate the impact of the gain on the early extinguishment of debt, the payments in connection with the management and advisory services agreements, which are being terminated, and restructuring and severance costs. We consider these items to be one-time costs and gains and not indicative of our ongoing operating performance. You are encouraged to evaluate each adjustment and the reasons we consider them appropriate for supplemental analysis. As an analytical tool, Adjusted EBITDA is subject to all of the limitations applicable to EBITDA. In addition, in evaluating Adjusted EBITDA, you should be aware that in the future we may incur expenses similar to the adjustments in this presentation. Our presentation of Adjusted EBITDA should not be construed as an implication that our future results will be unaffected by unusual or non-recurring items.

Adjusted EBITDA is calculated by adding to EBITDA certain items of expense and deducting from EBITDA certain items of income that we believe are not indicative of our future performance consisting of (i) gain on early extinguishment of debt, (ii) management and advisory fees and (iii) restructuring and severance costs.

The following table reconciles net income (loss) to EBITDA and EBITDA to Adjusted EBITDA for the periods indicated:

| | Performance Materials Segment of Goodrich | Noveon International, Inc. | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Years Ended December 31 | Two Months Ended February 28 2001 | Ten Months Ended December 31 2001 | Years Ended December 31 | |||||||||||||||

| | 1999 | 2000 | 2002 | 2003 | |||||||||||||||

| | (dollars in millions) | ||||||||||||||||||

| Net income (loss) | $ | 62.1 | $ | 50.3 | $ | 5.6 | $ | (39.7 | ) | $ | 23.7 | $ | (7.9 | ) | |||||

| Cumulative effect of accounting change—net of tax | — | — | — | — | — | 0.5 | |||||||||||||

| Income tax expense | 42.3 | 35.9 | 4.0 | 4.6 | 6.4 | 9.2 | |||||||||||||

| Interest (income) expense—net | (0.5 | ) | (4.4 | ) | (0.6 | ) | 92.6 | 99.6 | 90.9 | ||||||||||

| Depreciation and amortization | 86.9 | 86.7 | 14.4 | 83.0 | 84.7 | 91.4 | |||||||||||||

| EBITDA | 190.8 | 168.5 | 23.4 | 140.5 | 214.4 | 184.1 | |||||||||||||

| Gain on early extinguishment of debt | — | — | — | — | (12.4 | ) | — | ||||||||||||

| Management and advisory fees | — | — | — | 3.3 | 3.7 | 4.0 | |||||||||||||

| Restructuring and severance costs | 37.3 | 40.5 | — | 3.1 | 6.1 | 13.2 | |||||||||||||

| Adjusted EBITDA | $ | 228.1 | $ | 209.0 | $ | 23.4 | $ | 146.9 | $ | 211.8 | $ | 201.3 | |||||||

9

EBITDA and Adjusted EBITDA presented in this table are measures of our performance that are not required by, or presented in accordance with, GAAP. EBITDA and Adjusted EBITDA are not measurements of our financial performance under GAAP and should not be considered as alternatives to net income or any other performance measures derived in accordance with GAAP or as an alternative to net cash provided by operating activities as a measure of liquidity.

Segment EBITDA is defined as operating income of a segment plus depreciation and amortization. The following table reconciles segment operating income to Segment EBITDA:

| | Consumer Specialties | Specialty Materials | Performance Coatings | ||||||

|---|---|---|---|---|---|---|---|---|---|

| | Year Ended December 31, 2003 | ||||||||

| | (dollars in millions) | ||||||||

| Segment operating income | $ | 47.0 | $ | 75.8 | $ | 43.3 | |||

| Depreciation and amortization | 26.1 | 34.8 | 20.1 | ||||||

| Segment EBITDA | $ | 73.1 | $ | 110.6 | $ | 63.4 | |||

- (5)

- Adjusted EBITDA margin is defined as Adjusted EBITDA as a percentage of sales.

10

You should carefully consider the risks described below, as well as other information included in this prospectus, before making an investment decision. The risks described below summarize the material risks involved in investing in our common stock but are not the only ones we face. Our business, results of operations or financial condition could be materially and adversely affected by any of these risks. The value of your investment may decrease due to any of these risks.

Increases in raw material prices and reductions in availability of raw material supplies could disrupt our operations.

We use a substantial amount of a variety of specialty and commodity chemicals in our manufacturing processes. These raw materials are generally available from numerous independent suppliers. We typically purchase our major raw materials on a contract basis in order to insure that we receive minimum required volumes. Our most significant raw materials include toluene, ethyl and butyl acrylate, glacial acrylic acid, chlorine, MDI, PTMEG, aniline, acetone, PVC, styrene and ethylene glycol, although we do purchase approximately 1,500 other materials. Some of the raw materials that we use are derived from petrochemical-based feedstocks, such as crude oil and natural gas. There have been historical periods of rapid and significant movements in the prices of these feedstocks both upward and downward. Any significant variations in the cost and availability of our specialty and commodity materials may negatively impact our business, financial condition or results of operations. We typically do not enter into hedging arrangements with respect to raw materials. We selectively pass changes in the prices of raw materials to our customers from time to time. However, we cannot always do so, and any limitation on our ability to pass through any price increases could disrupt our operations.

Competition and consolidation in our industry may put downward pressure on our prices and margins.

We operate in a highly competitive and consolidating environment. We compete with a wide variety of product materials and specialty chemicals manufacturers. Some of our competitors are larger, have greater financial resources and have less debt than we do. As a result, these competitors may be better able to withstand a change in conditions within our industry, a change in the prices of raw materials or a change in the economy as a whole. In addition, we could be subject to adverse results caused by our competitors' pricing decisions. Current and future consolidation among our competitors and customers may cause loss of market share as well as put downward pressure on pricing. These competitors may also be able to maintain significantly greater operating and financial flexibility than we do. Additionally, a number of our niche product applications are customized or sold for highly specialized uses. Competitors that have greater financial, technological, manufacturing and marketing resources than we do and that do not currently market similar products may do so in the future. Increased competition could put downward pressure on our prices and margins.

Our business has cyclical exposure, which may reduce demand for our products.

A substantial portion of our sales is attributable to products and markets that historically have been cyclical and sensitive to relative changes in supply and demand and general economic conditions. The demand for our products depends, in part, upon the general economic conditions of the industries of our customers. Downward economic cycles in our customers' industries may reduce sales of our products. It is not possible to predict accurately the factors that will affect demand for our products in the future.

11

Our indebtedness, including the senior notes proposed to be issued concurrently with this offering, could restrict our operations and make us more vulnerable to adverse economic conditions.

We now have, and after this offering and the proposed concurrent senior notes offering, will continue to have, a significant amount of indebtedness. As of December 31, 2003, our total debt was $1,030.3 million. On an as adjusted basis, as if we had completed this offering and the proposed concurrent senior notes offering, and used the net proceeds therefrom as described in "Use of Proceeds," our total debt would have been $ million, on December 31, 2003. For the year ended December 31, 2003, we made cash principal and interest payments totaling $67.1 million, excluding the non-cash accretion of interest on the seller note, which we will repay with the proceeds of this offering. Holding all other variables constant, if interest rates increased or decreased by 1%, interest expense for the year ended December 31, 2003 would have increased or decreased by approximately $3.8 million. In addition, we have guaranteed Noveon, Inc.'s outstanding obligations of $594.9 million, including letters of credit, and maximum obligations of aggregate principal amount of $714.1 million, under our credit facilities. Our total debt could increase, as we have a total borrowing capacity of $125.0 million under our credit facilities, of which $119.2 million was available as of December 31, 2003, net of $5.8 million of outstanding letters of credit. Furthermore, the terms of the indentures governing Noveon, Inc.'s outstanding senior subordinated notes and our senior notes proposed to be issued concurrently with this offering allow us and our subsidiaries to incur additional amounts of indebtedness, including up to $65.0 million at any time under various baskets, and unlimited additional borrowings, so long as we satisfy a fixed charge coverage ratio after giving effect to those borrowings. Based on this fixed charge coverage ratio in the senior subordinated notes indenture, as of December 31, 2003, we could have incurred an additional $478.0 million of indebtedness.

Our current and future indebtedness could have important consequences to you. For example, it could:

- •

- impair our ability to make investments and obtain additional financing for working capital, capital expenditures, acquisitions or general corporate or other purposes;

- •

- limit our ability to use operating cash flow in other areas of our business because we must dedicate a substantial portion of these funds to make principal and interest payments on our indebtedness;

- •

- limit our ability to borrow funds that may be necessary to operate or expand our business;

- •

- put us at a competitive disadvantage to competitors that have less debt;

- •

- increase our vulnerability to interest rate increases; and

- •

- hinder our ability to adjust to rapidly changing economic and industry conditions.

Our ability to meet our debt service and other obligations may depend in significant part on the extent to which we can successfully implement our business strategy. We may not be able to implement, or realize the benefits of, our business strategy.

We may incur more indebtedness, which could exacerbate the risks described above.

We may be able to incur additional indebtedness in the future. As described above, under our credit facilities, we have additional borrowing capacity of up to $125.0 million, of which $119.2 million was available as of December 31, 2003, net of $5.8 million of outstanding letters of credit. Additionally, the terms of the indentures relating to Noveon, Inc.'s senior subordinated notes and our proposed % senior notes do not prohibit us or our subsidiaries from incurring indebtedness, although the indentures do contain limitations on additional indebtedness. If new indebtedness is added to our current levels of indebtedness, the risks described above could increase.

12

We may not be able to generate sufficient cash flow to meet our debt service obligations.

Our ability to generate sufficient cash flow from operations to make scheduled payments on our debt obligations will depend on our future financial performance, which will be affected by a range of economic, competitive and business factors, many of which are outside of our control. If we do not generate sufficient cash flow from operations to satisfy our debt obligations, including payments on Noveon, Inc.'s senior subordinated notes and our proposed % senior notes, we may have to undertake alternative financing plans, such as refinancing or restructuring our debt, selling assets, reducing or delaying capital investments or seeking to raise additional capital. We may not have sufficient availability under the restricted payments test in the indenture governing Noveon, Inc.'s senior subordinated notes to make scheduled payments on our proposed % senior notes. Our inability to generate sufficient cash flow to satisfy our debt obligations, to refinance our obligations on commercially reasonable terms, or to successfully complete alternative financing plans, could have an adverse effect on our business, financial condition, results, operations and prospects. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources."

The debt agreements of our subsidiaries contain, and any future financing agreements we enter into may contain, restrictions that will limit our ability to finance operations and capital needs or engage in other business activities.

Our debt agreements contain covenants that, among other things, restrict our ability to:

- •

- incur additional indebtedness (including guarantees);

- •

- make some acquisitions;

- •

- pay dividends and make other restricted payments;

- •

- issue certain types of stock;

- •

- engage in some transactions with affiliates;

- •

- enter into sale and leaseback transactions;

- •

- make loans and investments; and

- •

- enter into new lines of business.

In addition, our credit facilities require Noveon, Inc. to comply with specified financial covenants including maintenance of net worth, limitations on capital expenditures, minimum interest coverage ratios and maximum leverage ratios.

Our ability to meet these covenants and requirements in the future may be affected by events beyond our control, including prevailing economic, financial and industry conditions. Our breach or failure to comply with any of these covenants could result in a default under our credit facilities or the indenture governing our senior subordinated notes. If we default under our credit facilities, the lenders could cease to make further extensions of credit, cause all of our outstanding debt obligations under these credit facilities to become due and payable, require us to apply all of our available cash to repay indebtedness under these credit facilities, prevent us from making debt service payments on any other indebtedness we owe and/or proceed against the collateral granted to them to secure repayment of those amounts. The credit facilities are secured by substantially all of our assets, substantially all of the assets of Noveon, Inc. and its domestic subsidiaries, 100% of the capital stock of its direct and indirect restricted domestic subsidiaries and 65% of the capital stock of its first tier foreign subsidiaries. If the indebtedness under our credit facilities or our outstanding senior subordinated notes is accelerated, we may not have sufficient assets to repay amounts due under these existing debt agreements or on other debt securities then outstanding. See "Description of Our Indebtedness."

13

Environmental regulations may cause us to incur significant costs and liabilities.

Our operations are subject to extensive environmental laws and regulations by foreign, federal, state and local authorities. These include laws and regulations pertaining to pollution, the protection of human health and the environment, air emissions, wastewater discharges, occupational safety and health, the generation, handling, treatment, remediation, use, storage and release, and exposure to hazardous substances and wastes. We have incurred, and will continue to incur, costs and capital expenditures in complying with these laws and regulations and to obtain and maintain all necessary permits. Any failure by us to comply with such laws and regulations could subject us to significant future fines, penalties and other liabilities.

A majority, but not all, of our properties have been the subject of environmental site assessments performed by outside environmental consultants and our environmental engineers to determine the level of environmental risk. However, not all potential instances of either environmental non-compliance or soil and groundwater contamination may have been identified, even at those sites where environmental site assessments have been conducted. Accordingly, we may discover previously unknown environmental conditions and the cost of remediating such conditions could be material.

Several of our facilities have environmental cleanups that are currently in process and for which Goodrich provided an indemnity. In addition to Goodrich's indemnity, there are several other indemnities provided from other third parties such as past owners of the facilities. However, if Goodrich or the third party indemnitors become unable to, or otherwise do not, comply with their respective indemnity obligations in the future, we could become subject to significant liabilities.

Estimates that are particularly sensitive to future changes include contingent liabilities recorded for environmental remediation. Estimated future environmental remediation costs are subject to change due to such factors as the unknown magnitude of cleanup costs, the unknown time and extent of such remedial actions that may be required, and the determination of our liability in proportion to that of other responsible parties.

In addition, environmental laws and regulations, and their interpretations, are constantly evolving and it is impossible to predict accurately the effect that changes in these laws and regulations, or their interpretation, may have upon our business, financial condition or results of operations. Should environmental laws and regulations, or their interpretations become more stringent, the costs of compliance could increase. If we cannot pass along future costs to our customers, any increases may have an adverse effect on our business, financial condition or results of operations. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies and Estimates—Environmental Liabilities" and "Business—Health, Safety and Environmental Matters."

International social, political and economic conditions may adversely affect our operating performance.

Our international operations are subject to risks, including currency exchange controls, labor unrest, regional economic uncertainty, political instability, terrorism, expropriation of property, restrictions on the transfer of funds into or out of a country, trade restrictions, export duties, taxes and quotas, domestic and foreign customs and tariffs, and current and changing regulatory environments. These events could have an adverse effect on our international operations in the future by reducing the demand for our products, increasing the prices at which we can sell our products or otherwise having an adverse effect on our operating performance.

Currency translation risk and currency transaction risk may adversely affect our results of operations.

The financial condition and results of operations of each foreign operating subsidiary are reported in the relevant local currency and then translated to U.S. dollars at the applicable currency exchange rate for inclusion in our financial statements. Exchange rates between these currencies and U.S. dollars in recent years have fluctuated significantly and may do so in the future. For the year ended December 31, 2003, we generated approximately 31% of our sales in foreign currencies, and we

14

incurred approximately 28% of our total costs in foreign currencies. Significant changes in the value of the euro relative to the U.S. dollar could also have an adverse effect on our financial condition and results of operations and our ability to meet interest and principal payments on euro-denominated debt, including borrowings under our credit facilities, and U.S. dollar- denominated debt, including the senior subordinated notes and borrowings under the credit facilities. In addition to currency translation risks, we incur currency transaction risk whenever one of our operating subsidiaries enters into either a purchase or a sales transaction using a different currency from the currency in which it receives revenues. See "Management's Discussion and Analysis of Financial Condition and Results of Operations." Given the volatility of exchange rates, we may not be able to effectively manage our currency translation and/or transaction risks, and any volatility in currency exchange rates may have an adverse effect on our financial condition or results of operations.

The patents and confidentiality agreements we rely on to protect our intellectual property may be challenged or rendered unenforceable, which could result in a competitive disadvantage.

Protection of our proprietary processes, methods and compounds and other technology is important to our business. Consequently, we rely on enforcement and protection of our patents. While a presumption of validity exists with respect to patents issued to us in U.S. and non-U.S. jurisdictions, our patents may be challenged, invalidated, circumvented, infringed upon or rendered unenforceable. Furthermore, any pending patent application filed by us may not result in an issued patent, and if patents are issued to us, those patents may not provide meaningful protection against competitors or against competitive technologies.

We also rely upon unpatented proprietary manufacturing expertise, continuing technological innovation and other trade secrets, as well as trademarks, to develop and maintain our competitive position. While we generally enter into confidentiality agreements with our employees and third parties to protect our intellectual property, these agreements may be breached, may not provide meaningful protection for our trade secrets or proprietary manufacturing expertise or may not provide for adequate remedies in the event of an unauthorized use or disclosure of our trade secrets and manufacturing expertise. In addition, others may obtain knowledge of our trade secrets through independent development or other access by legal means. The failure of our patents, the failure to enforce our patents, or the failure of our confidentiality agreements to protect our processes, equipment, technology, trade secrets and proprietary manufacturing expertise, methods and compounds, or the failure to maintain and protect our trademark rights, could result in a competitive disadvantage.

In the future, we may have to rely on litigation to enforce our intellectual property rights and contractual rights. In addition, we may face claims of infringement that could interfere with our ability to use technology or other intellectual property rights that are material to our business operations. If litigation that we initiate is unsuccessful, we may not be able to protect the value of some of our intellectual property. In the event a claim of infringement against us is successful, we may be required to pay royalties or license fees to continue to use technology or other intellectual property rights that we have been using or we may be unable to obtain necessary licenses from third parties at a reasonable cost or within a reasonable time. Any litigation of this type, whether successful or unsuccessful, could result in substantial costs to us and diversions of some of our resources. Our products and services may potentially infringe on the intellectual property rights of third parties and our intellectual property rights may not have the value we believe them to have, which could result in a competitive disadvantage or adversely affect our business.

We may be unable to respond effectively to technological changes in our industry, which could put us at a competitive disadvantage.

Our future business success will depend upon our ability to maintain and enhance our technological capabilities, develop and market products and applications that meet changing customer needs and successfully anticipate or respond to technological changes on a cost-effective and timely

15

basis. Our inability to anticipate, respond to or utilize changing technologies could put us at a competitive disadvantage.

As part of our strategy to enter new applications and end users and to expand our global reach, we have acquired, and may continue to acquire, other entities. If we make acquisitions in the future, we may experience problems integrating new businesses and assets and allocating management resources.

Identifying, acquiring and integrating businesses requires substantial management, financial and other resources and may pose several risks, some or all of which could have a material adverse effect on our business, financial condition or results of operations. These risks include:

- •

- unforeseen operating difficulties and expenditures;

- •

- difficulties in assimilation of acquired personnel, operations and technologies;

- •

- the need to manage a significantly larger and more geographically dispersed business;

- •

- increased indebtedness;

- •

- diversion of management's attention from ongoing development of our business or other business concerns;

- •

- potential loss of customers;

- •

- failure to retain key personnel of the acquired business; and

- •

- the use of substantial amounts of our available cash and/or credit facilities.

Our production facilities are subject to operating risks that may adversely affect our operations.

We are dependent on the continued operation of our production facilities. These production facilities are subject to hazards associated with the manufacturing, handling, storage and transportation of chemical materials and products, including pipeline leaks and ruptures, explosions, fires, inclement weather and natural disasters, mechanical failure, unscheduled downtime, labor difficulties, transportation interruptions, remediation complications, chemical spills, discharges or releases of toxic or hazardous substances or gases, storage tank leaks and other environmental risks. These hazards can cause personal injury and loss of life, severe damage to, or destruction of, property and equipment and environmental damage, fines and liabilities and could have an adverse effect on our business, financial condition or results of operations. In addition, some of our production facilities are co-located at sites where our neighbors face the same operational risks and, in some cases, they provide critical supplies and/or services, and any disruption in those supplies and/or services could affect our operations.

Our production facilities are of the type that may attract terrorist attacks, and any attack may disrupt our operations and cause us to incur significant costs and liabilities.

Uncertainty surrounding the possibility and scope of terrorist attacks may impact our operations in unpredictable ways, including the possibility that our chemical production facilities may become direct targets, or indirect casualties, of possible terrorist attacks. While our production facilities are under a heightened level of security, this level of security may be insufficient to prevent a terrorist attack. The resulting damage would be difficult to assess, may be severe and could include loss of life and property damage. Available insurance coverage may not be sufficient to cover all of the damage incurred or may be prohibitively expensive. In addition, some of our production and other facilities are co-located at sites where our neighbors may be potential targets of terrorist attacks. The resulting collateral damage may be significant and substantial.

Certain of our employees are covered by collective bargaining agreements, and the failure to renew these agreements could result in labor disruptions and increased labor costs.

Approximately 24% of our domestic employees at seven of our U.S. sites are organized by labor unions with collective bargaining agreements that are subject to renegotiation, with five of these

16

agreements expiring in 2004 and 2005. While we believe our present labor relations to be satisfactory, our failure to renew these agreements on reasonable terms as the current agreements expire could result in labor disruptions and increased labor costs.

Present and future litigation may adversely affect our results of operations.

We are a defendant in lawsuits that result from, and are incidental to, the conduct of our business. These suits concern, and future suits may concern, issues, including product liability, contract disputes, labor-related matters, environmental proceedings, property damage, personal injury matters and patent infringement. It is not feasible to predict the outcome of all pending or future suits and claims, and the ultimate resolution of these matters could have an adverse effect upon our business, financial condition or results of operations.

We are subject to government regulation that may adversely affect our results of operations.

We are subject to regulation by many U.S. and non-U.S. supranational, national, federal, state and local governmental authorities. In some circumstances, before we may sell some of our products, these authorities must approve these products, our manufacturing processes and facilities. We are also subject to ongoing reviews of our products and manufacturing processes.

In order to obtain regulatory approval of various new products, we must, among other things, demonstrate to the relevant authority that the product is safe and effective for its intended uses and that we are capable of manufacturing the product in accordance with current regulations. The process of seeking approvals can be costly, time consuming and subject to unanticipated and significant delays, and approvals may not be granted to us on a timely basis, if at all. Any delay in obtaining, or any failure to obtain or maintain, these approvals would adversely affect our ability to introduce new products and to generate revenue from those products.

New laws and regulations may be introduced in the future that could result in additional compliance costs, seizures, confiscation, recall or monetary fines, any of which could prevent or inhibit the development, distribution and sale of our products. If we fail to comply with applicable laws and regulations, we may be subject to civil remedies, including fines, injunctions, recalls, seizures or revocation of regulatory approvals, which could have an adverse effect on our business, financial condition or results of operations.

Goodwill impairment may unpredictably affect our results of operations in the future.

In June 2001, the Financial Accounting Standards Board issued Statement of Financial Accounting Standards, or SFAS, No. 141, "Business Combinations," and SFAS No. 142, "Goodwill and Intangible Assets," effective for fiscal years beginning after December 15, 2001. Under the rules, goodwill (and intangible assets deemed to have indefinite lives) may no longer be amortized and are subject to annual impairment tests in accordance with SFAS No. 142. Other intangible assets continue to be amortized over their remaining useful lives. We adopted SFAS No. 142 in our first quarter of 2002. During the second quarter of 2002, we performed the first of the required impairment tests of goodwill as of January 1, 2002. During the fourth quarters of 2003 and 2002, we performed our annual impairment tests of goodwill. We have determined that no goodwill impairment had occurred.

Future events could cause the impairment of goodwill associated with any of our reporting units. Any resulting impairment loss may have a material adverse impact on our results of operations in any future period in which we record a charge for it. In addition, a significant impairment of goodwill may cause Noveon, Inc. to be in default under the net worth covenant of our credit facilities.

17

Risks Related to this Offering

We are controlled by PMD, DLJ Merchant Banking and MidOcean, whose interests may conflict with ours and those of our other stockholders.

Following this offering, PMD, DLJ Merchant Banking and MidOcean will own, in the aggregate, approximately % of our outstanding common stock and pursuant to a stockholders agreement among us, PMD, DLJ Merchant Banking and MidOcean, dated as of November 28, 2000, as amended from time to time, they will continue to control us. Accordingly, they will be able to:

- •

- elect our entire Board of Directors;

- •

- control our management and policies; and

- •

- determine, without the consent of our other stockholders, the outcome of any corporate transaction or other matter submitted to our stockholders for approval, including mergers, consolidations and the sale of all or substantially all of our assets.

The stockholders agreement provides PMD, DLJ Merchant Banking and MidOcean with various corporate governance rights, so long as specific stock ownership levels are maintained, including the right to designate each member of our Board of Directors.

They will also be able to prevent or cause a change in control of us and amend our certificate of incorporation and by-laws at any time. Pursuant to the stockholders agreement, we have entered into management agreements with each of AEA, DLJ Merchant Banking and MidOcean. In addition, we have entered into an advisory services agreement with Credit Suisse First Boston LLC. These management and advisory services agreements will be terminated upon completion of this offering and the obligations due thereunder will be satisfied with a portion of the proceeds from this offering.

Moreover, because we are contolled by PMD, DLJ Merchant Banking and MidOcean, we are a "controlled company" for purposes of The New York Stock Exchange. Among other things, this means that our compensation and nominating committees are not required to be independent, and that a majority of our Board of Directors is not required to be independent.

Our ability to take advantage of specific business opportunities is limited by our amended and restated certificate of incorporation, under which we renounce any interest or expectancy in certain business opportunities presented to any of PMD, DLJ Merchant Banking, MidOcean or their respective affiliates. Therefore, if any of PMD, DJL Merchant Banking, MidOcean or their respective affiliates becomes aware of a potential transaction that may be a corporate opportunity for any of them or us, they will have no duty to communicate or offer this corporate opportunity to us.

The interests of PMD, DLJ Merchant Banking and MidOcean may conflict with our interests and those of our other stockholders, including purchasers of the common stock in this offering.

There has been no active trading market for our common stock, and an active trading market may not develop.

Prior to this offering, there has been no public market for our common stock. We have applied to list our common stock on The New York Stock Exchange. We do not know if an active trading market will develop for our common stock or how the common stock will trade in the future, which may make it more difficult for you to sell your shares. Negotiations between the underwriters and us will determine the initial public offering price. You may not be able to resell your shares at or above the initial public offering price due to fluctuations in the market price of our common stock.

18

If our stock price fluctuates after the initial offering, you could lose a significant part of your investment.

The market price could be subject to wide fluctuations in response to a number of factors, most of which we cannot control, including:

- •

- changes in securities analysts' recommendations and estimates of our financial performance;

- •

- the public's reaction to our press releases, announcements and our filings with the Securities and Exchange Commission;

- •

- fluctuations in stock market prices and volumes, particularly among securities of chemical companies;

- •

- changes in market valuations of similar companies;

- •

- additions or departures of key personnel;

- •

- commencement or involvement in litigation;

- •

- announcements by us or our competitors of strategic alliances, significant contracts, new technologies, acquisitions, commercial relationships, joint ventures or capital commitments;

- •

- variations in our quarterly results of operations or cash flows or those of other chemical companies;

- •

- changes in our pricing policies or pricing policies of our competitor;

- •

- future issuances and sales of our common stock; and

- •

- changes in general conditions in the U.S. economy, financial markets or the chemical industry.

In recent years, the stock market has experienced extreme price and volume fluctuations. This volatility has had a significant effect on the market price of securities issued by many companies for reasons unrelated to the operating performance of these companies.

Additionally, because Credit Suisse First Boston LLC is considered to be our affiliate, it is unlikely that it will be permitted under the rules of The New York Stock Exchange to solicit, or make recommendations regarding, the purchase or sale of our common stock. This could affect the liquidity of, the trading markets for, or investor interest in, our common stock, which could adversely affect the price at which it trades.

An aggregate of approximately million shares of our common stock will become eligible for resale in the public market 180 days from the date of the preliminary prospectus, and future sales of our common stock may cause our stock price to decline.

Sales of substantial amounts of our common stock in the public market after the completion of this offering, or the perception that these sales could occur, could adversely affect the market price of our common stock and could materially impair our future ability to raise capital through offerings of our common stock. An aggregate of shares of our common stock will be outstanding after completion of this offering. Of these, only the shares offered by this prospectus will be freely tradable without restriction or further registration.

In connection with this offering, we and our executive officers, directors, other senior management and each of PMD, DLJ Merchant Banking and MidOcean (who together hold shares out of the shares of our common stock outstanding as of December 31, 2003), will agree not to sell or transfer any shares of our common stock (other than to us) for 180 days from the date of the preliminary prospectus without the prior written consent of each of Credit Suisse First Boston LLC, Deutsche Bank Securities Inc. and UBS Securities LLC. See "Underwriting."

19

PMD, DLJ Merchant Banking and MidOcean each have demand rights to cause us to file, at our expense, a registration statement under the Securities Act covering resales of their shares. These shares will represent approximately % of our outstanding common stock after this offering. They will agree not to exercise their demand registration right until 180 days from the date of the preliminary prospectus without the prior written consent of each of Credit Suisse First Boston LLC, Deutsche Bank Securities Inc. and UBS Securities LLC. These shares may also be sold under Rule 144 of the Securities Act, depending on their holding period and subject to significant restrictions in the case of shares held by persons deemed to be our affiliates.

We entered into a management stockholders agreement with our executive officers and other senior management who hold shares of our common stock. The agreement restricts the transfer of shares held by these executive officers except in certain circumstances. These transfer restrictions expire on the earlier of a sale of our Company or the second anniversary of this offering.

In addition, after this offering, we also intend to register shares of our common stock for issuance under our stock option plans. As of December 31, 2003, options to purchase shares of our common stock were issued and outstanding, of which options to purchase shares were vested. Assuming all option shares are exercised immediately upon eligibility, purchasers of common stock in this offering will experience dilution of $ per share.

It is uncertain what effect, if any, market sales of shares held by any stockholder or the availability of these shares for future sale will have on the market price of our common stock. See "Shares Eligible for Future Sale" and "Underwriting" for a more detailed description of the restrictions on selling shares of our common stock after this offering.

Purchasers of our common stock will experience substantial dilution in the net tangible book value per share of their investment.

The initial public offering price per share exceeds our net tangible book value per share. If you participate in this offering, you will pay a price per share that substantially exceeds the book value of our tangible assets, after subtracting our liabilities. New investors will contribute % of our total capitalization, but will own only % of the shares outstanding. You may incur additional dilution if holders of options to purchase common stock, whether currently outstanding or subsequently granted, exercise their options following this offering. See "Dilution" for more information.

We do not currently intend to pay dividends on our common stock.