ANNUAL INFORMATION FORM

YEAR ENDED JUNE 30, 2011

September 22, 2011

TABLE OF CONTENTS

| DOCUMENTS INCORPORATED BY REFERENCE | i |

| BASIS OF PRESENTATION | i |

| FORWARD-LOOKING STATEMENTS | i |

| GLOSSARY OF TERMS AND PROPER NAMES | iv |

| CORPORATE STRUCTURE | 7 |

| GENERAL DEVELOPMENT OF THE BUSINESS | 8 |

| RISK FACTORS | 29 |

| DIRECTORS AND SENIOR MANAGEMENT | 41 |

| MAJOR SHAREHOLDERS AND RELATED PARTY TRANSACTIONS | 49 |

| AUDIT FEES | 56 |

| INDEPENDENCE OF EXPERTS | 57 |

| LEGAL PROCEEDINGS | 57 |

| TRANSFER AGENT AND REGISTRAR | 57 |

| MATERIAL CONTRACTS | 57 |

| ADDITIONAL INFORMATION | 58 |

DOCUMENTS INCORPORATED BY REFERENCE

The following documents are incorporated by reference in, and form part of, this Annual Information Form (“AIF”):

| · | the audited consolidated balance sheets as at June 30, 2010 and June 30, 2011 and the audited consolidated statements of earnings and retained earnings and changes in financial position for each of the years in the three year period ended June 30, 2011 (collectively, the “Financial Statements”); and |

| · | management’s discussion and analysis of financial condition and results of operations for the year ended June 30, 2011 (the “MD&A”). |

All of the documents referred to above have been filed on SEDAR (System for Electronic Document Analysis and Retrieval) and are available to the public at www.sedar.com. Further information may also be found on the Company’s website at www.ymbiosciences.com.

BASIS OF PRESENTATION

Except where the context otherwise requires, all references in this AIF to the “Company”, “YM”, “we”, “us”, “our” or similar words or phrases are to YM Biosciences Inc. and its subsidiaries, taken together. In this AIF, references to “US$” are to U.S. dollars and references to “C$” or “$” are to Canadian dollars. Unless otherwise indicated, the statistical and financial data contained in this AIF are presented as at June 30, 2011.

FORWARD-LOOKING STATEMENTS

This AIF, including any documents incorporated by reference, contains “forward-looking statements” within the meaning of the United States federal securities laws. The words “may”, “believe”, “will”, “anticipate”, “expect”, “estimate”, “project”, “future” and other expressions that are predictions of or indicate future events and trends and that do not relate to historical matters identify forward-looking statements. The forward-looking statements in this AIF, including any documents incorporated by reference, include, among others, statements with respect to:

| · | our expected expenditure and accumulated deficit levels; |

| · | our intentions with respect to acquiring or investing in production facilities; |

| · | production quantities; |

| · | our ability to obtain sufficient supplies of our products; |

| · | our ability to identify licensable products or research suitable for licensing and commercialization; |

| · | the locations of our clinical trials; |

| · | our intention to license products from multiple jurisdictions; |

| · | our ability to obtain necessary funding on favourable terms or at all; |

| · | our potential sources of funding; |

| · | our business strategy; |

| · | our drug development plans; |

| · | our ability to obtain licenses on commercially reasonable terms; |

- i -

| · | the effect of third party patents on our commercial activities; |

| · | our intentions with respect to developing manufacturing, marketing or distribution programs; |

| · | our expectations with respect to the views toward our products held by potential partners; |

| · | our plans for generating revenue; |

| · | our plans for increasing expenditures for the development of certain products; |

| · | our strategy for protecting our intellectual property; |

| · | the success of trial results, the timing for the receipt thereof, and the efficacy of our products; |

| · | the sufficiency of our financial resources to support our activities and our prospective pivotal trials; and |

| · | our plans for future clinical trials and for seeking clinical clearance. |

Reliance should not be placed on forward-looking statements, as they involve known and unknown risks, uncertainties and other factors that may cause the actual results to differ materially from the anticipated future results expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially from those set forward in the forward-looking statements include, but are not limited to:

| · | our ability to obtain, on satisfactory terms or at all, the capital required for research, product development, operations and marketing; |

| · | general economic, business and market conditions; |

| · | our ability to successfully and timely complete clinical studies; |

| · | product development delays and other uncertainties related to new product development; |

| · | our ability to attract and retain business partners and key personnel; |

| · | the risk of our inability to profitably commercialize our products; |

| · | the risk that our product trials will not yield positive results or that we will not support regulatory market approvals for our products; |

| · | the extent of any future losses; |

| · | the risk of our inability to establish or manage manufacturing, development or marketing collaborations; |

| · | the risk of delay of, or failure to obtain, necessary regulatory approvals and, ultimately, product launches; |

| · | dependence on third parties for successful commercialization of our products; |

| · | inability to obtain development product in sufficient quantity or at standards acceptable to health regulatory authorities to complete clinical trials or to meet commercial demand; |

| · | the risk of the termination or conversion to non-exclusive licenses or our inability to enforce our rights under our licenses; |

| · | our ability to obtain patent protection and protect our intellectual property rights; |

| · | commercialization limitations imposed by intellectual property rights owned or controlled by third parties; |

| · | uncertainty related to intellectual property liability rights and liability claims asserted against us; |

- ii -

| · | the uncertainty of recovery of advances to subsidiaries; |

| · | the impact of competitive products and pricing; |

| · | future levels of government funding; and |

| · | additional risks and uncertainties, many of which are beyond our control, referred to elsewhere in this AIF. See “Risks Factors”. |

Except as required by law, we undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise.

- iii -

GLOSSARY OF TERMS AND PROPER NAMES

This glossary contains general terms used in the discussion of the biopharmaceutical industry, as well as specific technical terms used in the descriptions of our technology and business.

Adjuvant: Substance added to a vaccine to enhance its immunogenicity (i.e. its ability to stimulate an immune response). May also mean “at the time of surgery” as in “treatment with another agent of its type at, or close to, the time of surgery”.

Amgen: Amgen Incorporated

ASCO: The American Society of Clinical Oncology

ASH: The American Society of Hematology

AstraZeneca: AstraZeneca PLC

Board: board of directors of YM

BMS: Bristol Myers Squibb

Cancer Vaccine: Vaccines or candidate vaccines designed to treat cancer. Active immunotherapy

CIM: Cuba’s Centro de Immunologia Molecular

CIMAB: CIMAB S.A., a Cuban company responsible for commercializing products developed at CIM

CIMYM and CIMYM BioSciences: CIMYM BioSciences Inc., an 80% owned joint venture subsidiary of YM

CIMYM (Barbados): CIMYM Inc., a predecessor company to CIMYM BioSciences, incorporated under the laws of Barbados

CNS: Central Nervous System

Clinical Trial Application (“CTA”): previously known as an Investigational New Drug application which must be filed and accepted by the regulatory agency, Health Canada, before each phase of human clinical trials may begin

Cytopia means Cytopia Limited, acquired by YM effective January 29, 2010

Cytotoxic: Having capacity to kill cells

Daiichi: Daiichi Pharmaceutical Co. Ltd. or Daiichi Sankyo Co., Ltd.

EGFR: A protein known as Epidermal Growth Factor Receptor

EMA (formerly EMEA): The European Medicines Agency - the European health regulatory authority

Eximias: Eximias Pharmaceutical Corporation

FAK: Focal Adhesion Kinase – a kinase target in cancer drug development

FDA: U.S. Food and Drug Administration

FMS: Feline McDonough Strain – a kinase target in cancer in other disease conditions

Genentech: Genentech Incorporated

- iv -

Glioma: A form of brain cancer involving the malignant transformation of a glial cell

GMP: good manufacturing practices, i.e. guidelines established by the governments of various countries, including Canada and the U.S., to be used as a standard in accordance with the World Health Organization’s Certification Scheme on the quality of pharmaceutical products

HER-1: Tumors expressing/producing the EGF receptor

Humanized: The process whereby an antibody derived from murine cells is altered to resemble a human antibody

ImClone: ImClone Systems Incorporated

Incyte: Incyte Corporation

IND: Investigational New Drug application which must be filed and accepted by the FDA before each phase of human clinical trials may begin

Irinotecan: An approved chemotherapeutic agent

In vivo: In the living body or organism. A test performed on a living organism

JAK: Janus Kinase – therapeutic targets for drugs known as JAK1, 2 or 3 inhibitors, specific kinases on the kinome

K: thousand

Ligand: Used herein to describe a protein or peptide that binds to a particular receptor

M: million

M&A: mergers and acquisitions

Merck: Merck KGaA

Metastatic: A term used to describe a cancer where tumor cells have migrated from the primary tumor to a secondary site (e.g. from prostate to bone)

MD&A: Management’s discussion and analysis of financial condition and results of operations for the year ended June 30, 2011

Myelofibrosis: A debilitating and potentially fatal disorder that causes anemia, enlargement of the spleen (splenomegaly), cachexia and constitutional symptoms such as bone pain, night sweats, itching and fatigue.

MTD: Maximum tolerated dose

Monoclonal antibody (“mAb”): Antibodies of exceptional purity and specificity derived from hybridoma cells

Neoplastic: New and abnormal growth of tissue (neoplasm), which may be benign or cancerous

Novartis: Novartis International AG and subsidiaries

NSCLC: Non-small-cell lung cancer

OFAC: Office of Foreign Assets Control of the U.S. Department of the Treasury

Oncoscience: Oncoscience AG of Germany

Orphan Drug: A drug aimed at treating a condition with an incidence of less than 200,000 per year in the U.S. (often given a seven year market exclusivity by the FDA)

- v -

OSI: OSI Pharmaceuticals, Inc.

Overall Survival: For patients who have died, overall survival is calculated in months from the day of randomization to date of death. Otherwise, survival is censored at the last day the patient is known alive

PR: Partial Response, the shrinkage of a tumor measured by decrease by at least 30% as measured by a decrease in the sums of the longest diameter according to RECIST criteria

Passive Immunotherapy: Immunologically active material transferred into the patient as a passive recipient. Monoclonal antibodies are considered Passive Immunotherapy since antibodies are generated outside the body and given to the patient

Qualified Person(s) or QP: A technical term used in European Union pharmaceutical regulation (Directive 2001/83/EC for Medicinal products for human use); the regulations specify that no batch of medicinal product can be released for sale or supply prior to certification by a QP that the batch is in accordance with the relevant requirements (EudraLex, Volume 4, Chapter 1). The QP is typically a licensed pharmacist, biologist or chemist (or a person with another permitted academic qualification) who has several years of experience working in pharmaceutical manufacturing operations and has passed examinations attesting to his or her knowledge.

RECIST: Response Evaluation Criteria in Solid Tumors, a U.S. standard

Roche: F.Hoffmann-LaRoche Ltd.

TGFα: Transforming growth factor alpha

Tyrosine kinase: An enzyme that catalyzes the phosphorylation of tyrosine residues in proteins with nucleotides as phosphate donors

U.S.: United States of America

VDA: Vascular Disrupting Agent – a molecule that impedes or reverses the formulation of capillaries that provide blood flow to tumours

YM Australia: YM BioSciences Australia Pty Ltd (formerly, Cytopia Research Pty Ltd), an indirect wholly-owned subsidiary of YM

YM USA: YM BioSciences USA Inc., a wholly-owned subsidiary of YM

- vi -

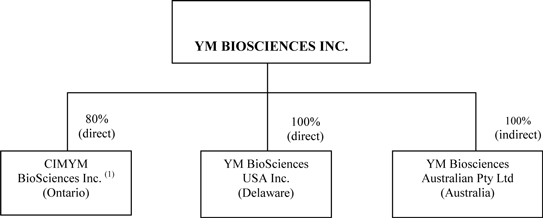

CORPORATE STRUCTURE

YM BioSciences Inc. was incorporated under the laws of the Province of Ontario on August 17, 1994 under the name “York Medical Inc.”. On February 7, 2001 we changed our name to “YM BioSciences Inc.” and on December 11, 2001 were continued into the Province of Nova Scotia under the Companies Act (Nova Scotia).

Our head office and principal place of business is 5045 Orbitor Drive, Building 11, Suite 400, Mississauga, Ontario, L4W 4Y4; telephone (905) 629-9761. Our registered head office is 1959 Upper Water Street, Suite 900, Halifax, Nova Scotia, B3J 2X2; telephone: (902) 420-3200.

We currently have the following material subsidiaries:

| (1) | Subject to current negotiations, ownership may become 70% mitigated by additional revenues to YM from a manufacturing royalty |

On June 30, 2006 CIMYM Inc., an Ontario corporation, was amalgamated under the laws of Ontario, Canada with CIMYM Inc., a Barbados corporation, to form CIMYM BioSciences Inc (CIMYM). CIMYM is 80% directly owned by the Company and 20% owned by CIMAB.

YM BioSciences USA Inc. (YM USA) was incorporated on November 23, 2005 under the laws of Delaware. YM US Operations Inc. was incorporated on April 10, 2006 under the laws of Delaware. On May 9, 2006 YM US Operations Inc. was merged with Eximias. On March 6, 2008 YM US Operations Inc. was merged into YM USA. YM USA is 100% directly owned by the Company.

On January 29, 2010 we acquired Cytopia Research Pty Ltd, an Australian company, through the acquisition of all of the issued and outstanding ordinary shares of Cytopia, an Australian company listed on the Australian Stock Exchange. YM issued to the Cytopia shareholders common shares of YM in consideration for their shares of Cytopia. On March 9, 2010, Cytopia Research Pty Ltd changed its name to “YM BioSciences Australia Pty Ltd.”. YM Australia is 100% indirectly owned by the Company.

We also have a wholly-owned subsidiary incorporated under the laws of Anguilla to facilitate the restructuring of our intellectual property ownership in order to generate tax efficiency.

7

GENERAL DEVELOPMENT OF THE BUSINESS

Business Overview

YM BioSciences Inc. is a drug development company advancing three clinical-stage hematology and cancer-related products: CYT387, a small molecule, dual inhibitor of the JAK1/JAK2 kinases; nimotuzumab, an EGFR-targeting monoclonal antibody; and CYT997, a vascular disrupting agent (VDA). We use our expertise to manage and perform, within our means, what we believe are value-enhancing activities in the development process of a drug, which include, but are not limited to, the design and conduct of clinical trials, the development and execution of strategies for the protection and maintenance of intellectual property rights, interaction with drug regulatory authorities internationally, and the securing of partners to assist in the development and commercialization processes. We do not have research laboratories of our own, and have acquired or in-licensed our current products and do not directly engage in early-stage research, avoiding the earlier risk and investment of time and capital that is generally required before a compound is identified as appropriate for drug development. We both conduct and out-source clinical trials and we out-source the manufacture of clinical materials to third parties.

We principally intend to co-develop and/or license the rights to manufacture or market our products in development to other pharmaceutical companies in exchange for license fees and royalty payments. We do not currently intend to manufacture or market products although we may, if the opportunity is available on terms that are considered attractive, participate in ownership of manufacturing facilities or retain marketing rights to specific products in certain market regions. We intend to continue to seek other in-licensing or acquisition opportunities in pursuing our business strategy.

We have three product candidates currently in clinical stages of development:

| · | CYT387 is an oral small molecule inhibitor of the kinase enzymes JAK1 and JAK2, which have been implicated in a family of hematological conditions known as myeloproliferative neoplasms, including myelofibrosis, and as well in numerous other disorders including indications in hematology, oncology and inflammatory diseases. We are currently evaluating CYT387 in a Phase I/II trial for the treatment of patients with myelofibrosis, a chronic debilitating disease in which a patient’s bone marrow is replaced by scar tissue, often rendering the patient anemic and suffering from significant symptoms. The trial was initiated at Mayo Clinic in November 2009 and subsequently has been expanded to include centers in the U.S., Canada and Australia. The U.S. Food and Drug Administration (FDA) has granted Orphan Drug Designation to CYT387 and the European Commission has granted Orphan Medicinal Product Designation to CYT387, both for the treatment of myelofibrosis. YM BioSciences retains full global commercialization rights to CYT387. |

| · | Nimotuzumab is a humanized monoclonal antibody targeting EGFR with an enhanced side-effect profile over currently marketed EGFR-targeting antibodies. Nimotuzumab is licensed to YM’s majority-owned joint venture, CIMYM BioSciences Inc., an Ontario corporation, for Western and Eastern Europe, North America, and Japan, as well as Australia, New Zealand, Israel and certain Asian and African countries. Certain of CIMYM’s rights to nimotuzumab have been sub-licensed to Daiichi-Sankyo Co. Ltd in Japan, Oncoscience AG in Europe, to Kuhnil Pharmaceutical Company for Korea and to Innogene Kalbiotech Ltd. of Singapore for certain Pacific-rim countries and certain African countries. These partners are currently evaluating the drug in several Phase II and III trials. Nimotuzumab reportedly has been approved in 27 countries that are outside of the major market territories for which CIMYM has a license. More than 15,500 patients have been reportedly treated with the drug to date in 35 countries. |

| · | CYT997, a small molecule microtubule polymerisation inhibitor, is being developed for the treatment of solid and other tumours in cancer patients. As well as being cytotoxic, it also acts as a vascular disrupting agent and is able to be administered orally as well as intravenously to patients, potentially allowing greater flexibility in dosing and patient convenience. We recently completed a Phase I/II trial of CYT997 given intravenously in combination with platinum chemotherapy in glioma patients and we will review the results to guide advancement of the oral formulation of the drug. |

8

In addition, we own approximately 4,000 pre-clinical molecules resulting from the merger of Cytopia into YM and from YM sponsored research. The molecules are at different stages of development:

| · | YM is currently evaluating a number of JAK inhibitor candidates in preclinical testing, with the goal of identifying a candidate suitable for clinical testing as a therapeutic for the treatment of chronic inflammatory diseases, such as rheumatoid arthritis. |

| · | Prior to the merger of Cytopia into YM, Cytopia entered into a global joint research and licensing collaboration in 2006 with Novartis for the discovery of JAK3 inhibitors. In 2008, Cytopia entered into an early stage collaboration with Cancer Therapeutics CRC Pty Ltd to discover FAK inhibitors for the treatment of cancer. Cancer Therapeutics CRC had the responsibility to conduct lead optimization studies with the goal of identifying FAK inhibitors that meets pre-agreed upon criteria. YM has the option to buy-back rights to the FAK inhibitors should the compounds pass internal review. In 2011, YM entered into an early stage collaboration and license with SYN│thesis Medchem Pty Ltd. to identify inhibitors of the FMS kinase for the treatment of particular tumor types including metastatic cancers. As with the Cancer Therapeutics CRC arrangement, YM has a buy-back right should the identified compounds pass internal review. |

We have three additional licenses to products that are not in clinical development and are not subject to expenditure: tesmilifene, for which all development activities were terminated in 2007.

We also own AeroLEF®, a proprietary formulation of both free and lipsome-encapsulated fentanyl administered by pulmonary inhalation, which was being developed for the treatment of severe and moderate acute pain including cancer pain. On August 4, 2010, we announced the discontinuation of further expenditures on AeroLEF-related activities.

We continue to evaluate opportunities to expand and diversify our development portfolio through licensing, acquisition or M&A activity. There are no proposed undisclosed material transactions that have progressed to a state where the Company believes that the likelihood of the Company completing such a transaction is high.

A description of our principal capital expenditures and divestitures and a description of acquisitions of material assets are found in our MD&A and in the notes to our Financial Statements incorporated herein by reference.

Business Strategy

We are principally focused on the development of products for the treatment of hematological and cancer or cancer-related conditions. Our strategy is to in-license rights to promising products or acquire such products, optimize them as required, and further develop those products by conducting and managing clinical research trials and progressing the products toward regulatory approval. We principally intend to co-develop and/or license the rights to manufacture or market our products in development to other pharmaceutical companies in exchange for license fees and royalty payments. We do not currently intend to manufacture or market products although we may, if the opportunity is available on terms that are considered attractive, participate in ownership of manufacturing facilities or retain marketing rights to specific products in certain market regions. We intend to continue to seek other in-licensing or acquisition opportunities in pursuing our business strategy.

The main elements of our business strategy are described below:

Identification of Product Candidates: We directly perform scientific evaluation and market assessment of biopharmaceutical products and research developed by scientific/academic institutions and other biopharmaceutical companies. As part of this process, we evaluate the related scientific research and pre-clinical and clinical research, if any, and the intellectual property rights for such products and research, with a view to determining the therapeutic and commercial potential of the applicable product candidates.

9

In-Licensing or Acquisition: Upon identifying a promising biopharmaceutical product, we seek to negotiate the acquisition of the product or the company owning the product or license the rights for the product from the holder of those rights, the developer or researcher. The terms of such licenses vary, but generally our goal is to secure licenses that permit us to engage in further development, clinical trials, intellectual property protection (on behalf of the licensor or otherwise) and further licensing of manufacturing and marketing rights to any resulting products. This process of securing license rights to products is commonly known as “in-licensing”.

Further Development: Upon in-licensing or acquiring a product, our strategy is to apply our skills and expertise to progress the products toward regulatory approval and commercial production and sale in major markets. These activities include implementing intellectual property protection and registration strategies, performing, or having performed for us, pre-clinical research and testing, product optimization, formulating or reformulating drug products, manufacturing and scale-up of manufacturing, making regulatory submissions, performing or managing clinical trials in target jurisdictions and undertaking or managing the collection, collation and interpretation of clinical and field data and the submission of such data to the relevant regulatory authorities in compliance with applicable protocols and standards.

Out-Licensing and Commercialization: We generally plan to further license manufacturing and marketing rights to our licensed products to other pharmaceutical firms. This is commonly known as “out-licensing”. Under our business model, licensees would be expected, to the extent necessary, to participate wholly or partially in the remaining clinical and ancillary development required to obtain final regulatory approval for the product. The sharing of development expenses between the licensee and licensor is commonly known as “co-development”. We expect that out-licensing/co-development would result in a pharmaceutical company or other licensee marketing or manufacturing the product in return for licensing fees in addition to royalties on any sales of the product. Management believes this model is consistent with current biotechnology and pharmaceutical industry licensing practices. In addition, although out-licensing is a primary strategy of ours, we may retain certain co-development or marketing rights to particular products, indications or territories. To date, we have out-licensed the development and marketing rights to nimotuzumab in Europe, South Korea, Japan and several jurisdictions in South East Asia and Africa to four separate companies. We have also licensed certain rights to early stage drug discovery preclinical programs to three organizations and have retained rights of first refusal to in-license back these programs upon the accomplishment of pre-specified milestones. See “Business Overview - Licensing Arrangements - Out-Licensing”.

We actively search for new product opportunities using the expertise and relationships of our management, board and advisors, and through the monitoring of the academic and biotechnology environments in hematology, oncology and certain other therapeutic areas. Our staff analyze and evaluate opportunities on a regular basis. We intend to seek other in-licensing or acquisition opportunities in pursuing our business strategy.

Cancer and the Cancer Therapeutic Market

According to the International Agency for Research on Cancer (IARC), cancer remains the leading cause of death in developed countries and second worldwide. There were approximately 12 million new cancer cases and seven million cancer deaths worldwide in 2008, with 20-26 million new cases and 13-17 million deaths projected for 2030 (World Cancer Report 2008).

Globally, according to the World Health Organization, the cancers which cause the most deaths are lung (1.4 million), stomach (866,000), liver (653,000), colon (677,000) and breast (548,000). According to the American Cancer Society, it is estimated that 1.59 million new cancer cases will be diagnosed in the U.S. in 2011 and 571,950 will die from the disease, while in Canada, according to the Canadian Cancer Society, there will be an estimated 177,800 new cases of cancer and 75,000 deaths from cancer in 2011. Cancer is the second leading cause of disease-related death in North America behind cardiovascular disease, which it is predicted to surpass in the next few years. The principal reasons for this projection appear to be the aging population, environmental issues related to industrial development and improvements in the treatment of cardiovascular disease. North America, Europe and Japan are currently the principal markets for cancer therapies because of the established healthcare and payer systems.

10

Surgery, radiation and chemotherapy remain the principal effective treatments for cancer. Chemotherapy is defined broadly as the use of medicine or drugs to treat cancer. Chemotherapy include treatment with both classical cytotoxic drugs such as cisplatin and paclitaxel, as well as the new generation of targeted therapy drugs such as erlotinib and sorafenib, which are designed to target and interfere with specific proteins, enzymes or processes involved in cancer growth and proliferation. Targeted therapy represents the new generation of cancer therapy that utilizes drugs to more precisely identify and attack cancer cells, while usually causing less damage to normal healthy cells than chemotherapy. Targeted therapy is a growing part of many cancer treatment regimens and is the dominant focus of current cancer research and drug development worldwide.

According to “Evaluate Pharma and Defined Health’s July 2011 Insight Briefing”, the current oncology pharmaceutical market is estimated to be approximately US$75-80 billion. Unlike other therapeutic areas such as cardiovascular, CNS or respiratory diseases where revenue from drug sales are forecasted to decline or remain flat over the next five years, sales of oncology drugs are forecasted to surpass US$100 billion in the next five years. Much of the current drug sales in oncology are from targeted therapy agents. In 2010, seven targeted therapy agents contributed 81% of the US$33.8 billion of sales from the top 10 oncology drugs. Approval of new oncology indications for existing targeted therapy and approval of new targeted therapy agents are forecast to drive growth in the oncology market over the next five years. In 2016, nine targeted therapy agents are predicted to contribute 93% of the estimated US$42.7 billion of sales from the top 10 oncology drugs.

Cancer is often grouped into two categories: solid tumour (cancer of an organ) and haematological malignancies (cancer of the blood). Solid tumour has traditionally dominated the oncology market with >90% of new cancer diagnosis in the U.S. being solid tumour. However, in recent years, agents for the treatment of haematological disorder and malignancies have played an increasing role in the oncology market. Recently approved drugs for treating haematological disorder and malignancies were priced at two times the price per treatment for solid tumour agents approved during the same period. For oncology drugs launched in recent years, the average annual treatment costs for haematological malignancies was US$61,000 versus US$21,000 for solid tumours. Of the top 10 blockbuster drugs in oncology, five are approved for the treatment of haematological disorders and malignancies. There are significant market opportunities in haematological malignancies as well as in solid tumours.

Product Portfolio

CYT387

Overview

CYT387 is a dual inhibitor of the kinases JAK1 and JAK2 in clinical development initially for the treatment of myeloproliferative neoplasms and prospectively other diseases where inhibition of JAK1 and JAK2 activity may have therapeutic benefit, such as various cancers. See “General Development of the Business – Intellectual Property” for a list of our CYT patent claims.

| Product type | Small molecule pyrimidine kinase inhibitor |

| Initial Indication | Treatment of myeloproliferative neoplasms |

| Development Status | International (PCT) patent application filed March 2008. Patent application is in regional/national phase in various jurisdictions. Maximum patent term ends March 2028 (subject to possible extension). |

| Project Status | Dosing in Phase I/II clinical studies commenced in November 2009; Interim data reported at ASH 2010 and ASCO 2011. Enrolment of 166 patients was completed in September 2011. |

11

CYT387 is a small molecule based on a pyrimidine scaffold that belongs to the class of drugs known as kinase inhibitors. These drugs inhibit the action of enzymes called kinases, which are known to be over-active in certain diseases. CYT387 selectively inhibits the kinases JAK1 and JAK2, two kinases which are excessively active in a number of diseases including certain cancers and myeloproliferative neoplasms (or myeloproliferative disorders) such as polycythemia vera (PV), essential thrombocythemia (ET) and myelofibrosis (MF). The selectivity and potency profile of CYT387 is a potential advantage over other JAK inhibitors currently in development.

In preclinical studies CYT387 has been shown to possess a favourable selectivity and potency profile in a range of in-vitro screens using both isolated enzyme and cell-based assay systems. In particular, using cells isolated from patients with myeloproliferative neoplasms, CYT387 was shown to block the action of the hyperactive JAK2 mutant enzyme present in patients with this disease, leading to a decrease in cells possessing the disease-driving mutation.

In an in-vivo model of myeloproliferative disorders, CYT387 was shown to effect significant disease reversal as observed by a reduction in spleen size and a decrease in red-blood cell production, both returning to normal levels. Furthermore, the compound caused a return of blood cell production to the bone marrow as well as leading to a decrease in systemic inflammation, as measured by the decrease of certain markers (cytokines) in the circulation. In preclinical cancer studies, CYT387 has been shown to decrease the proliferation of certain cancer cells and to block the action of signalling molecules known to drive cancer cell growth.

Clinical Development

CYT387 has undergone preclinical safety studies in preparation for clinical studies in patients. A preclinical data package has been reviewed by the FDA, which permitted commencement of a clinical study in patients with myelofibrosis.

A Phase I/II study was initiated in November 2009 at Mayo Clinic, Rochester MN, USA, with Dr. Ayalew Tefferi, a recognized key opinion leader in myeloproliferative neoplasms, as study chair. The Phase I/II open-label, non-randomized, dose-escalation study is being conducted in three phases: a Dose Escalation Phase (n=21) to determine the safety and tolerability of CYT387, and to identify a maximum tolerated dose for CYT387; a Dose Confirmation Phase (n=39) which enrolled a cohort expansion at 150mg and 300mg QD, and a Dose Expansion Phase (n=106, ongoing) which recently completed enrolment at multiple study sites at doses of 150mg and 300mg QD and 150mg BID. The Core Study consists of nine 28-day treatment cycles. Patients who achieve stable disease or better and tolerate the drug well may continue to receive CYT387 beyond the initial nine cycles in an Extension Phase of the study.

ASCO 2011 Phase I/II Study Interim Results

Subject Characteristics: The results presented at ASCO 2011 were for the first 60 patients enrolled in the Dose Escalation and Dose Confirmation Phases. Fifty-five percent of the patients were red-cell transfusion-dependent. The trial also enrolled patients who had received previous therapies, including other JAK inhibitors and/or pomalidomide. The median follow-up time for the first 60 patients since study start was then 10.1 months (range 5.8-17.4; ongoing).

Interim Safety Results: CYT387 was very well tolerated in myelofibrosis patients. The majority of reported non-hematological adverse events were mild to moderate and no Grade 4 events were reported. Observed treatment-emergent non-hematological adverse effects included transient lightheadedness/dizziness, mild peripheral neuropathy and asymptomatic abnormalities in liver/pancreas-related laboratory tests. To date, 34 of 35 patients who had completed the Core Study had continued into the Extension Phase. Including the Extension Phase, 11 patients (18%) had discontinued the study, only one for drug-related reasons, for an overall retention rate of 82%.

12

Treatment-emergent hematological adverse events included infrequent neutropenia (Grade 3/4: n=3 (5%)) and anemia (Grade 3/4: n=1 (3%)). The minimum platelet count required for study entry was 50,000/µL. Only 6 out of 44 patients (14%) with baseline platelets >100,000/ µL reported Grade 3/4 thrombocytopenia. Overall, 16 (27%) of the first 60 patients reported Grade 3/4 thrombocytopenia.

Interim Spleen Response: All evaluable patients reported demonstrable spleen responses. Of the 52 patients evaluable for spleen response, 24 (46%) achieved a response per IWG-MRT. The median duration of spleen response was then 7.7 months (range 5.3 – 16.6, ongoing). The median time to spleen response was 0.4 months (range 0.2 – 4.7, ongoing). A loss of spleen response was seen in only one subject; 96% maintained a spleen response.

In the Dose Escalation and Dose Confirmation Phases, 32 of 52 patients (62%) achieved more than a 50% maximal decrease in spleen size from baseline to date, with 92% achieving at least a 25% decrease. In the Expansion Phase, subjects had thus far displayed a spectrum of spleen reductions similar to those observed in the Dose Escalation and Dose Confirmation Phases.

Interim Constitutional Symptoms Response: The majority of patients reporting constitutional symptoms at baseline demonstrated a Complete Resolution or Marked Improvement of their symptoms, including pruritus, night sweats and bone pain.

Interim Anemia Response: Of the 42 patients evaluable for anemia response, 21 (50%) had achieved a response per IWG-MRT. Of the 33 patients who were transfusion dependent at baseline, 19 (58%) became transfusion independent per IWG-MRT. All anemia responses persisted for a minimum of 12 weeks. Of the 19 patients who became transfusion-independent, the median duration of transfusion-free period was then 7.5 months (range 4.1-15.7, ongoing). None of the 19 patients had lost transfusion independence. Single episodes of transfusion were required by 6 patients after a median transfusion-free period of 5.9 months (range 4.1-9.5) due to infection (n=3), withholding of drug (n=1), or unexplained (n=2).

In all 60 patients, and in the anemia evaluable group, mean hemoglobin levels showed a sustained overall improvement. Representative examples of individual subject hemoglobin curves demonstrated a clear and pronounced treatment-related increase in hemoglobin, sustained over time. In the Expansion Phase, early multicenter data were consistent with previous observations, with several subjects already becoming transfusion independent.

Phase II BID Study

On the basis of promising safety and pharmacokinetic data obtained in the initial phases of our ongoing Phase I/II study, we introduced a twice-daily dosing schedule into the Dose Expansion Phase of this trial. Our initial findings from this cohort suggest that CYT387 has promising activity whether dosed once or twice daily. In order to fully explore the BID dosing regimen, YM will initiate a complementary Phase II BID in calendar Q3, 2011 enrolling approximately 60 patients to augment the data from our Phase I/II trial. The BID study will facilitate further investigation of the spleen, constitutional symptom and anemia responses observed to date. The trial is expected to initiate enrolment for the trial is expected to be initiated in calendar Q3, 2011 and is scheduled to recruit approximately 60 patients across six sites in North America.

In total, these two trials will enrol more than 230 patients and will provide the basis upon which we will design a Phase III trial anticipated to begin in mid-2012 that leverages CYT387’s unique and promising therapeutic profile to maximize its clinical utility in the treatment of myelofibrosis.

Regulatory Matters

The U.S. Food and Drug Administration (FDA) has granted Orphan Drug Designation to CYT387 for the treatment of myelofibrosis. The European Commission has also granted Orphan Medicinal Product Designation to CYT387 for the treatment of myelofibrosis. These designations are typically granted to medicines intended for the treatment of rare, life-threatening or chronically-debilitating conditions. Developers of medicines that have been designated as orphan drugs may receive fee reductions, protocol assistance, as well as periods of marketing exclusivity once authorized.

13

Intended Market and Commercialization Status

CYT387 is an orally-administered, selective, small molecule, ATP-competitive inhibitor of both JAK1 and JAK2. Both receptors and the JAK-STAT pathway have been implicated in myeloproliferative disorders such as myelofibrosis, in hematological malignancies such as multiple myeloma, leukemia and lymphoma and in solid tumours such as NSCLC, head and neck cancer and hepatocellular carcinoma.

The initial development and registration strategy for CYT387 is in myelofibrosis, the most serious neoplastic condition among the myeloproliferative disorders. Myelofibrosis is a debilitating and potentially fatal disorder that causes anemia, enlargement of the spleen (splenomegaly), cachexia and constitutional symptoms such as bone pain, night sweats, itching and fatigue. Myelofibrosis can also transform into acute myelogenous leukemia and shorten survival. Primary myelofibrosis presents as myelofibrosis without any other etiology, while secondary myelofibrosis (post-polycythemia vera and post-essential thrombocythemia myelofibrosis) are progressions of polycythemia vera (PV) and essential thrombocythemia (ET). The prevalence of primary myelofibrosis in the U.S. is around 18,000 – 20,000 and secondary myelofibrosis around 13,000 – 15,000. The prevalence of primary myelofibrosis in the E.U. is around 30,000 – 32,000 and secondary myelofibrosis around 14,000 – 16,000. Treatment options to date have been limited or unsatisfactory. Primary and secondary myelofibrosis represents an unmet medical need with significant commercial opportunity.

Beyond myeloproliferative disorders, indication and market expansion opportunities exist within hematological malignancies. The JAK receptor has been implicated in hematological malignancies such as multiple myeloma, leukemia and lymphoma. The anemia responses observed with CYT387 may be of benefit in treating myelodysplastic syndrome (MDS) patients with anemia. Small molecule inhibitors of the JAK receptor have been reported to be effective anticancer agents in in vitro and in vivo preclinical models. The combination of CYT387 with other cancer drugs represents additional opportunities for developing new therapies in various solid tumour indications.

Considerable interest has been shown by pharmaceutical companies in JAK inhibitors, particularly with their broader potential applicability for cancer and other indications. A significant arrangement reported in November 2009 was the out-licensing of ex-U.S. rights by Incyte to Novartis of a JAK1/JAK2 inhibitor for myelofibrosis and other cancers. In December 2009, Incyte reportedly licensed worldwide rights to another JAK1/2 inhibitor for inflammatory disease indications to Eli Lilly Corporation. Onyx Pharmaceuticals and Singapore based S*Bio announced an agreement to develop and commercialise the S*Bio JAK2 inhibitors and in June 2010 Sanofi-Aventis acquired TargeGen, Inc. reportedly principally for TargeGen’s JAK2 molecule. In general, there continues to be strong interest within the pharmaceutical industry in establishing development and commercialization partnerships for novel agents. Examples of recently established collaborations include Celgene and Acceleron partnerships to develop ACE536, a protein therapeutic for the treatment of anemia, and Array Biopharma and Genentech partnerships to develop ARRY-575, a small molecule CHK1 inhibitor for the treatment of cancer.

Competitive Position

There are currently five small molecule JAK inhibitors in active clinical development in hematology and oncology: INCB18424, CYT387, TG101348, SB1518 and AZD1480. Clinical trials with INCB18424, CYT387, TG101348 and SB1518 have been conducted in myelofibrosis and other myeloproliferative disorders. Clinical trials with AZD1480 have been conducted in other oncology indications. These five inhibitors have differing selectivity against the family of four JAK receptors (JAK1, 2, 3 and TYK2) as well as other kinases. CYT387 and INCB18424 are dual JAK1 and JAK2 inhibitors, while TG101348, SB1518 and AZD1480 are described as JAK2 inhibitors, with FLT3 activity reported for TG101348 and SB1518. Emerging preclinical and clinical data in myeloproliferative disorder such as myelofibrosis strongly suggest that appropriate dual inhibition of JAK1 and JAK2 is necessary to obtain optimal benefit from treatment with JAK inhibitors. Inhibition of FLT3, as observed in the selectivity profile of TG101348 and SB1518, is undesirable as it could translate into undesirable toxicity such as gastrointestinal toxicity, which has been reported in the clinical trials of these two compounds. There are other JAK inhibitors with differing selectivity against the family of four JAK receptors currently in development for inflammatory related diseases.

14

Nimotuzumab

Overview

Nimotuzumab is a humanized MAb targeting the EGF receptor (EGFR). The EGFR is present in high concentrations on the surface of many cancer cells and it is postulated that the binding of ligands to this receptor is important in the continuing growth of cancer cells. Nimotuzumab appears to block this binding resulting in the potential for inhibition of cell growth or, possibly, cell destruction by the immune system. Improved tumour responses or clinical benefit have been reported when EGFR targeting agents are combined with other anti-cancer treatments. Nimotuzumab is being developed to be administered alone or in combination with other anti-cancer treatments.

Clinical Experience and Development Pathway

Nimotuzumab is reported to have been administered to approximately 15,500 cancer patients worldwide and shown to be well tolerated. The product has been cleared for use in numerous clinical trials by various regulatory agencies including the EMA, Health Canada and the FDA.

During Fiscal 2011, CIMYM made the decision to focus its involvement with nimotuzumab to supporting the development and commercialization activities of its partners, which have advanced the drug into late-stage clinical development.

Daiichi Sankyo Co., Ltd., CIMYM’s licensee for nimotuzumab in Japan, advised it had previously initiated a randomized Phase II trial with nimotuzumab in second line gastric cancer together with Kuhnil Pharma Co. Ltd., CIMYM’s licensee in South Korea. Data from this trial was presented in January 2011 at the ASCO Gastrointestinal Cancers Symposium, and demonstrated evidence of an improvement in Progression Free Survival in a subset of patients who were EGFR-positive. Daiichi also has advised it has launched a Phase II trial in first-line NSCLC for which recruitment has been completed, with data expected to be reported at a scientific conference in the calendar third quarter of 2011.

Oncoscience AG (OSAG), CIMYM’s licensee for Europe, reported updated data from a single-arm Phase III trial of nimotuzumab as first-line therapy in combination with radiotherapy for diffuse intrinsic pontine glioma (DIPG) at the annual international pediatric oncology forum, SIOP, held in Boston in October 2010. Data from a series of 13 patients with DIPG that studied the combination of nimotuzumab plus vinorelbine and radiation was presented at ASCO 2011. Updated safety data from a Phase III trial in adult glioma patients was presented along with preliminary efficacy analyses at ASCO 2011. CIMYM has been advised by OSAG that final efficacy data from the adult glioma trial may be released in the second half of calendar 2011, once a biomarker correlation study has been completed. OSAG also advises they continue to recruit patients into a Phase IIb/III trial in pancreatic cancer.

Innogene Kalbiotech PTE Ltd. (IGK), a CIMYM licensee, has reported receiving marketing approval for nimotuzumab in the Philippines and Indonesia. In January 2009, the National Cancer Centre of Singapore (NCCS) announced that it was launching a worldwide Phase III, 710-patient trial of nimotuzumab in the post-operative or adjuvant setting in head and neck cancer in cooperation with IGK. This trial is in addition to an ongoing NCCS Phase II trial in locally advanced head and neck cancer, and the initiation of a Phase II trial in cervical cancer reportedly also being conducted by IGK.

Following a management review of CIMYM’s two randomized, Phase II, double-blind trials of nimotuzumab in patients with brain metastasis from non-small cell lung cancer (NSCLC) and for the palliative treatment of NSCLC, CIMYM decided in calendar Q2 2011 to close these studies to further enrolment due to slow rates of patient accrual and the projected timelines and costs anticipated to complete these studies. A Phase II, second-line, single-arm study in children with progressive DIPG has concluded recruitment at multiple sites in the U.S., Canada, and Israel and results from the trial have been submitted for publication and are expected to be reported in the second half of calendar 2011.

15

Regulatory Matters

In July 2004, nimotuzumab was designated an orphan drug for glioma by EMA.

In November 2004, nimotuzumab was designated an orphan drug for glioma by the FDA in the U.S.

In September 2006, YM USA received a Special License from OFAC for the importation of nimotuzumab for a U.S. trial in pediatric pontine glioma.

In October 2007, CIMYM was advised that an application for marketing approval for nimotuzumab was submitted to EMA.

In March 2008, a Withdrawal Assessment Report on the withdrawal by the applicant of an application for marketing approval for nimotuzumab to the EMA was published by the EMA citing that the benefit/risk balance for the drug in that application was negative.

In June 2008, CIMYM was advised that nimotuzumab was designated an orphan drug for pancreatic cancer by EMA.

In August 2009, YM USA received an expected but important clearance from the U.S. Treasury Department to extend our U.S. clinical program for nimotuzumab, permitting us to conduct trials in any solid tumor indication.

Nimotuzumab has also been reported to have received marketing approval in 27 countries, none of which are in the major-market territories for which CIMYM has a license.

Marketing

Nimotuzumab is licensed by CIMYM from a Cuban source, CIMAB, and as such is likely to be prohibited from sale in the U.S. unless OFAC issues a license or the U.S. embargo against Cuba is lifted. YM USA has received a Special License from OFAC to import nimotuzumab for clinical trials. YM USA made an application to OFAC for a license to commercialize nimotuzumab in the U.S. and the proposed terms are under review by the relevant agencies of both the U.S. and Cuban governments. YM USA will continue ongoing activities focused on securing this license.

Competitive Position

To our knowledge, other companies that are involved in the development of monoclonal antibody cancer therapeutics directly related to our efforts include Amgen, Genmab, ImClone/BMS and Merck KGaA, amongst others.

We understand that AstraZeneca and Astellas (formerly OSI), in concert with Genentech and Roche have small molecules designed to target the tyrosine kinase domains of EGF receptors.

We understand that Iressa®, previously approved as third-line monotherapy in locally-advanced or metastatic NSCLC, is undergoing a revision of registration in various countries. In Europe, the EMA recently approved Iressa® for the treatment of locally advanced or metastatic NSCLC with activating mutations of EGFR across all lines of therapy. The situation in the U.S. is unclear, but in 2011, AstraZeneca withdrew its regulatory application for Iressa® in the U.S. for use in patients with the activating mutation. Since 2005, the FDA has severely restricted access to Iressa® due to failure to show survival improvements following the drug’s registration under accelerated approval.

Astellas reported that it has positive survival data in a Phase III monotherapy study in refractory lung cancer. Tarceva® monotherapy is now approved for the treatment of patients with locally advanced or metastatic NSCLC. In addition, Tarceva® in combination with gemcitabine is approved for the first-line treatment of patients with locally advanced, unresectable or metastatic pancreatic cancer. Tarceva® also recently won FDA and European Union approval as a monotherapy maintenance treatment in patients with advanced NSCLC with stable disease after platinum-based initial chemotherapy. Recently Tarceva® received approval in Europe for use in NSCLC patients with activating EGFr mutation.

16

Astella’s product, Tarceva®, is in co-development with Roche and Genentech and is reported to be in numerous trials in various indications, including Phase III trials in ovarian cancer, colorectal cancer, hepatocellular cancer, head and neck cancer, NSCLC (1st line and adjuvant) and metastasis of the brain. See “Competition”.

We understand that Erbitux®, developed by ImClone/BMS and Merck, is approved in the U.S., Canada, Japan, Germany, Austria, Australia, Switzerland and numerous other jurisdictions for metastatic colorectal cancer in combination with irinotecan in irinotecan-refractory patients, in locally or regionally advanced squamous cell carcinoma of the head and neck in combination with radiation therapy, and in the U.S. for secondline therapy in squamous cell carcinoma of the head and neck progressing after platinum-based therapy. Erbitux® is approved in the U.S. for advanced NSCLC but the marketing application was rejected by the EMA. In a recent study in patients with earlier stage colorectal cancer, Erbitux® failed to prevent cancer recurrence compared with chemotherapy alone. Erbitux® is being further developed in other indications, and management believes it is reasonable to expect that the drug will be registered for additional indications in the future.

We understand that Vectibix®, developed by Amgen, is approved for third line monotherapy in colorectal cancer in irinotecan-refractory patients, and in Europe for the same indication but restricted to patients with the wild-type KRAS gene.

We understand that the market for Erbitux® and Vectibix® has recently been further restricted in the U.S. in colorectal cancer to patients with the wild-type KRAS gene.

CYT997

Overview

CYT997 is a novel, anticancer agent that belongs to the class of anticancer agents known as vascular disrupting agents (VDAs) which are designed to destroy pathological blood vessels created by growing tumours. The compound causes these blood vessels to collapse, thereby starving the tumour mass of oxygen and nutrients leading to tumor regression.

Unlike most other VDAs, CYT997 can be administered both intravenously as well as by oral capsule or tablet doses, potentially increasing its ease of use for patients and doctors. The oral form of CYT997 should also allow innovative dosing regimes whereby CYT997 may be given at a chronic, low dose to inhibit the tumor regrowth seen post-treatment with other agents.

Cytopia completed a Phase I intravenous infusion study for CYT997 in September 2007 and a Phase I oral study in December 2008. A single-arm intravenous Phase Ib/II study in patients with relapsed glioblastoma multiforme was recently closed to enrolment and data from the trial will be evaluated to guide further development of the oral formulation of the drug, which will involve additional preclinical testing and manufacturing development.

See “General Development of the Business – Intellectual Property” for a list of our CYT 997 patent claims.

| Product type | Small molecule microtubule polymerisation inhibitor and vascular disrupting agent |

| Initial Indication | Treatment of solid tumours |

| Development Status | International (PCT) patent application filed December 2004. Patent granted in South Africa and Australia. Under examination/awaiting examination in various jurisdictions. Maximum patent term ends December 2024 (subject to possible extension). |

17

| Project Status | A single-arm intravenous Phase Ib/II study in patients with relapsed glioblastoma multiforme was recently closed to enrolment with data anticipated from the study in calendar H2 2011 |

Preclinical Experience

A variety of cancer models have been used in order to evaluate the mechanism of action and vascular-disrupting activity of CYT997.

CYT997 has shown potent activity against a diverse panel of 21 different human, mouse and rat cancer cell lines including cancer cell lines with over-expressed resistance mechanisms. CYT997 was shown to dose-dependently inhibit the polymerisation of tubulin and block cancer cell division, confirming that this molecule targeted microtubules.

The compound significantly reduced primary tumour burden in a number of engrafted cancer models in mice. Importantly, CYT997 exerted a significant antivascular effect in tumours resulting in decreased blood flow and damage to tumour blood vessels. Tumour death was subsequently observed. The compound acts synergistically with other anticancer agents including 5-flurouracil and cisplatin.

CYT997 entered a formal clinical-trial enabling toxicology programme in 2004. These studies indicated that the drug is generally well tolerated with anticancer activity evident at doses below a maximum tolerated dose.

Clinical Program

| (a) | Phase I intravenous infusion study |

Dosing in this study concluded in September 2007.

The primary objectives of this study were to investigate the safety and tolerability of CYT997 when administered as a 24 hour infusion every three weeks to advanced cancer patients with a diverse range of solid tumors. Secondary objectives included the determination of CYT997 pharmacokinetics; the determination of dose-limiting toxicities (DLTs) and the recommended dose for future studies.

In total, 31 patients with diverse advanced solid tumours were treated in this study. A total of 98 cycles of CYT997 were administered over 12 dose levels (7 - 358 mg/m2).

Approximately 80% of patients achieved stable disease of six or more weeks' duration as a best response. However, there were no complete or partial responses in tumour size for the 22 evaluable study participants. Seven patients completed six cycles (approximately 4.5 months) of CYT997 therapy and two patients continued to receive CYT997 after leaving the clinical study. These patients experienced disease stabilisation for a period in excess of five months.

CYT997 dihydrochloride doses up to 202 mg/m2 were generally well tolerated. Dose-limiting toxicities observed at higher doses included two Grade 3 QTc prolongation events in two patients and a Grade 4 dyspnoea in one other patient. All toxicities were reversible.

Magnetic resonance imaging (MRI) of patient tumours was conducted in 11 patients. Seven of these subjects experienced significant alterations in tumour blood perfusion suggestive of an antivascular effect by CYT997. Other markers of antivascular activity were also significantly altered in some patients.

CYT997 pharmacokinetic parameters were dose-linear across the thirty-fold dosing range.

Data from this study therefore suggests that CYT997 disrupted tumour vasculature and showed preliminary evidence of anti-tumour activity at doses that were well tolerated by patients. The recommended dose for further clinical evaluation was 202mg/m2.

18

| (b) | Phase I oral capsule study |

Dosing in this study concluded in December 2008.

The primary objectives of the study were to establish the dose-limiting toxicities (DLTs) and maximum tolerated dose (MTD) of CYT997 given as an oral capsule dose. Secondary objectives included the determination of CYT997 pharmacokinetics; the determination of dose-limiting toxicities (DLTs) and the recommended dose for future studies.

In total, 21 patients were treated with a total of 56 cycles of CYT997 over 8 dose levels (15 - 164 mg/m2). No objective responses by RECIST criteria were observed however extended disease stabilisation of greater than six weeks was noted in 12 patients. Dose-limiting toxicities of a Grade 4 pulmonary sepsis resulting in patient death in one patient and two Grade 3/4 asthenic (fatigue) events in two other patients were observed.

Significant alterations in tumour blood perfusion were observed by DCE-MRI in most of the nine evaluable patients assessed by this method. Further pharmacodynamic analysis is currently ongoing.

Similar to the case with IV administration, pharmacokinetic analysis demonstrated that exposure to CYT997 increased in approximate proportion to the oral dose. The findings of this clinical trial suggest that CYT997 exerts an antivascular effect when administered orally. Data from this study will be used to guide future clinical development of the oral form of the compound.

| (c) | Phase Ib/II single-arm study in relapsed glioblastoma multiforme |

The primary objectives of the study are to assess the safety and tolerability of escalating doses of CYT997 when given in combination with standard carboplatin therapy (Phase Ib component) and estimate the progression-free survival at 6 months (PFS-6) utilising the dose of CYT997 identified in the Phase Ib component of this study (Phase II component). Preliminary data from YM’s current Phase I/II trial of CYT997 given IV in combination with platinum chemotherapy in glioma patients are expected in calendar H1 2012. Enrolment into this study was closed in Q1 2011.

| (d) | Phase II single-arm study in relapsed multiple myeloma |

The primary objective of this study was to determine the overall response rate to CYT997 therapy using World Health Organisation (WHO) criteria. Secondary objectives include estimation of the time-to-progression, number of cycles of CYT997 required to achieve maximal response, overall survival and safety and tolerability. Enrolment into this study was ended in September, 2008 as a strategic decision, with five patients having been enrolled.

Potential market

Vascular disrupting agents are a new class of anti-cancer drugs that show potential in treating a variety of solid tumour cancer. Solid tumour requires blood vessel or vasculature to deliver oxygen and nutrients to enable it to survive, grow and spread. The growth of new vessel to the tumour is known as angiogenesis. A number of angiogenesis inhibitors have been approved for the treatment of several types of solid tumour cancers. Tumour-vascular disrupting agents represent another approach at attacking the cancer via its vasculature or blood vessels. Unlike angiogenic agents, which prevent blood vessel formation, vascular disrupting agents shut down the tumour’s established network of blood vessels. Total suppression of blood flow in the tumour causes ischemia in tumour tissue and necrosis at the tumour’s core. Complementary treatment with chemotherapy or radiation to target the viable rim of malignant cells remaining at the periphery of the tumour improves the likelihood of a successful treatment.

19

A number of vascular disrupting agents have been evaluated in various clinical trials. In contrast to other vascular disrupting agents, CYT997 may be administered orally. Previous vascular disrupting agents were administered intravenously at high doses and in a non-continuous dosing schedule. Such infrequent dosing schedules result in rapid tumour revascularization while high doses may cause spikes in circulating pro-angiogenic endothelial precursors cells that also may restore tumour vasculature. Oral administration of an agent such as CYT997 may allow for more frequent and convenient dosing schedules as a single agent or in combination with other chemotherapy or radiation therapy. Oral administration of CYT997 at low, minimally toxic doses at frequent intervals may have safety and efficacy advantages compared to previous agents by allowing for a more continuous disruption of the tumour vasculature. Other potential advantages of an orally administered vascular targeting agent include improved patient convenience and combination with other orally administered anticancer drugs, CYT997 has the potential for treating a variety of solid tumour both as a single agent and in combination with chemotherapy or radiation therapy.

Manufacturing

Overview

Manufacturing of CYT387 and CYT997 occurs at the contract manufacturing organization (CMO) Aptuit Laurus, located in the province of Andhra Pradesh, India.

The R&D Centre is located in ICICI Knowledge Park, Hyderabad on nine acres. The R&D facility is approximately 160,000 sq. ft. including 50 laboratories and a 25,000 sq. ft. Pilot Plant/Scale-up facility inclusive of 30 reactors ranging in capacity from 2 - 250 litres. There is a dedicated space for the handling of oncology, highly potent and cytotoxic compounds with dedicated corresponding laboratories. The facility and systems maintain compliance to ICH Q7. The Hyderabad facility was inspected in February 2011 by the FDA and was found to be compliant and with No. 483 issued.

The API Commercial facility is located on 34 acres at Visakhapatnam (Vizag) with the a total of 380,000 sq. ft. of plant space including 100 reactors with volumes ranging between 250 – 7500 litres. This site also has a dedicated block for oncology/highly potent compounds. The Vizag facility has multiple class 100,000 suites for powder processing and has an additional nine acres of land available for future expansion. Export of material from Aptuit Laurus is made from Hyderabad as Vizag does not have an International shipping port or International airport.

There is an independent Quality Unit, headed by the VP of Corporate Quality having oversight for Quality Assurance, Quality Control and Regulatory Affairs. The Quality Management System is centralized and managed at the Hyderabad facility and the systems are commonly shared between the sites. The Quality Management System has been assessed against the provisions of ISO 9001:2008, complies with the applicable ICH guidelines and adheres to cGMP and GLP. The sites Regulatory status is as follows:

| · | U.S. FDA approval for both Hyderabad and Vizag |

| · | TGA approval for both Hyderabad and Vizag |

| · | MHRA approval for Vizag |

Quality Assurance commands oversight and control on the client’s Intellectual Property. There are comprehensive guidelines and SOPs in place for handling Intellectual Property, including use of project codes, limited access to information via the project leader, information redacted for external viewing during audits and use of shared drives verses transferring information over the internet. The Hyderabad facility has issued 9 Drug Master Files (DMFs) that are compliant to ICH Q7.

CYT387 manufacturing:

CYT387 API is manufactured under cGMP at the commercial API facility located in Visakhapatnam. The current production scale for Phase II material is undertaken in a campaign fashion comprised of 2 x 10 kg batches. The API is currently under an ongoing stability program in accordance with ICH guidelines.

20

CYT387 drug product manufacturing consists of direct encapsulation of unformulated API using either a manual fill-finish process at Penn Pharmaceutical Services Ltd. located at Tredegar, Gwent, UK, or a semi-automated fill finish process at Patheon UK Limited, Kingfisher Drive Swindon, UK. Both facilities are set up and responsible for QC testing and QA/QP release of drug product in adherence with cGMP. The drug product is currently under separate stability programs at both facilities in accordance with ICH guidelines.

CYT997 manufacturing:

CYT997 API is manufactured under cGMP at the R& D center located in Hyderabad at a production scale is ~1.5 kg per batch. The API is under an ongoing stability program in accordance with ICH guidelines.

Nimotuzumab manufacturing:

The CIMYM license agreement with CIMAB requires that CIMAB will manufacture and supply, or will contract for the manufacture and supply of, commercial quantities of nimotuzumab in accordance with the current licensing agreements at such time and stage of product development as commercial quantities of these products are required. Product from CIMAB’s manufacturing plant has been cleared for use in clinical trials in Canada, Europe, the USA and Japan amongst others. Recent reports on inspections of the manufacturing plant by Qualified Persons confirmed that the plant operates according to GMP principles. In addition the facility was inspected and approved by the Darmstadt Regional Presidium in Germany that is responsible for approvals of biological manufacturing facilities in Germany. The Darmstadt approval included 300 and 500 litre fermenters and covered a period of two years that expired in January 2009, following which two inspections by Qualified Persons declared the facilities to be in accordance with GMP principles. Another inspection occurred in February 2011, from which CIMAB is awaiting a formal GMP certificate. Manufacturing is being improved and scaled up to support expansion of clinical and commercial supplies in CIMYM’s territory.

CIMAB, or a supplier contracted by CIMAB, manufactures and supplies the product to CIMYM. Should CIMAB agree to alternative manufacturing arrangements, such as a sub-licensee of CIMYM manufacturing the product, the loss of manufacturing benefits to CIMAB may be reflected in a lower license fee and royalty payable to CIMYM than if manufacturing remains with CIMAB. See “Business - Licensing Arrangements”.

Licensing Arrangements

In-Licensing

Licenses for CYT997 and CYT387

The principal intellectual property claims for CYT997 and CYT387 are owned, not licensed, although patent families have been in-licensed from the Research Foundation of State University of New York (“SUNY”) relating to the use of JAK2 inhibitors to treat cardiovascular conditions, and from the Ludwig Institute for Cancer Research relating to the JAK2 enzyme and gene, and JAK2 antibodies. The Ludwig license is exclusive and was subject to cash payments that have already been made. The SUNY license also is exclusive, and worldwide, and is subject to certain payments based on achievement of clinical milestones, and a royalty on net sales of product in the field covered by the SUNY patents. See “General Development of the Business – Intellectual property”.

Licenses for Nimotuzumab

In May 1995, CIMYM acquired an exclusive, sub-licensable license (as amended, the “1995 CIMYM License”) from CIMAB, acting on behalf of CIM, to products for passive immunotherapy of cancer directed toward EGF and EGFR as targets, including hR3, a humanized MAb targeting the EGFR. CIMAB is the company responsible for the commercialization of products developed at CIM. The 1995 CIMYM License is in respect of Europe, Canada, the U.S., Japan, Australia, Taiwan, Singapore, Thailand, Hong Kong, South Korea, Malaysia, Indonesia and the Philippines. As a term of the 1995 CIMYM License, CIMYM has a right of first refusal with respect to licensing any other products derived from the EGF and EGFR programs of CIMAB except its anti-EGFR monoclonal antibody for psoriasis in Europe.

21

Pursuant to the 1995 CIMYM License, in 1995 we incorporated CIMYM and assigned the 1995 CIMYM License to CIMYM. Pursuant to the terms of the 1995 CIMYM License, CIMAB acquired a 20% equity interest in CIMYM as partial consideration for the 1995 CIMYM License. In addition, YM and CIMYM, pursuant to the terms of the 1995 CIMYM License, paid US$2,750,000 for certain product development costs for nimotuzumab and US$330,000 for certain product development costs for RadioTheraCIM.

The terms of the 1995 CIMYM License provide for CIMYM to conduct or cause to be conducted pre-clinical and clinical trials to evaluate the licensed products and to work with CIMAB to select sites, develop protocols and instruct investigators for pre-clinical and clinical trials. CIMYM is to decide after the end of each stage of trials whether to proceed with further development or to terminate the 1995 CIMYM License with respect to that product. In addition, the 1995 CIMYM License provides that, where commercially reasonable, CIMYM shall file applications for regulatory approval to market the licensed products in the applicable territory. Pursuant to the 1995 CIMYM License, CIMAB has the right, subject to certain terms and conditions, to supply the related drug substances (i.e., nimotuzumab) for commercial sale. CIMAB shall sell the product manufactured by it in Cuba to CIMYM at 85% of the sales price that CIMYM sets for the sale of the product to sub-licensees, thereby entitling CIMYM to the 15% difference. CIMYM shall use commercially reasonable efforts to obtain a sub-license agreement in which CIMAB retains the right to manufacture the product. The CIMYM License shall be in force as long as any patents thereunder are valid, or until such time as the license agreement is terminated by either party because of a default by the other party, or by CIMYM with written notice within 90 days after the end of a stage of pre-clinical trials or after each stage of clinical trials.

As at June 30, 2011 we had advanced $76,730,809 million to CIMYM for the licensing and development of the products licensed by CIMYM. We have the right to recover all funds advanced to CIMYM. To the extent that the net revenues of CIMYM are less than or equal to the advanced amounts, we are entitled to recover such advances from 30% of the net revenues. These advances have been partially repaid from license fees paid by the licensees in Japan, Indonesia and Korea.

On June 30, 2006 CIMYM amalgamated with CIMYM (Barbados) to form CIMYM BioSciences Inc., an Ontario company. CIMAB owns a 20% equity interest in CIMYM BioSciences and is entitled to receive 10% of net revenues received by CIMYM. We have agreed to negotiate in good faith a further 10% equity interest in CIMYM BioSciences to CIMAB such that we would then own a 70% equity interest and CIMAB would own a 30% equity interest in CIMYM BioSciences. Such a change in the equity holdings would not affect the current economics of the license.

Nimotuzumab Sublicenses

In November 2003, CIMYM and CIMAB, licensed the rights for nimotuzumab (known as “Theraloc” in Europe) in most of Europe to Oncoscience. Under the terms of the agreement, CIMYM is entitled to receive up to US$30 million as a share of any amounts received by Oncoscience in relation to development or sublicensing of the product and as a royalty on initial net sales. After CIMYM has received US$30 million, CIMYM continues to receive royalties on net sales but at a lesser percentage. Oncoscience has agreed to use diligent and reasonable efforts to develop and commercially exploit nimotuzumab in the licensed territory. A non-material amount of royalties have been received as of the date hereof by CIMYM from Oncoscience from its Special Access Program but no sublicensing fees have been received by Oncoscience. This license agreement may be terminated by either party in the event of specified breaches and insolvency events. In addition, Oncoscience may terminate the agreement at any time on 90 days of notice.

In August 2005, CIMYM and CIMAB licensed development and marketing rights to Kuhnil Pharmaceutical Co., Ltd. for Korea. There was an initial fee to CIMYM on signing and it is entitled to receive additional milestone payments and royalties. The maximum aggregate amount of milestone payments payable under the Kuhnil license agreement is US$700,000.

22

In October 2005, CIMYM and CIMAB licensed development and marketing rights to Innogene Kalbiotech Private Limited (a wholly owned subsidiary of P.T. Kalbe Farma Tbk, Indonesia) for Indonesia, Malaysia, the Philippines and Singapore and certain African countries including South Africa. The initial fee to CIMYM BioSciences on signing was U$1,000,000 and it is entitled to receive additional milestone payments and royalties. The maximum aggregate amount of milestone payments payable under the Innogene license agreement is US$3,800,000.

In July 2006, CIMYM and CIMAB licensed development and marketing rights for nimotuzumab in Japan to Daiichi Pharmaceutical Co., Ltd. (“Daiichi”), a wholly owned subsidiary of Daiichi Sankyo Co., Ltd., one of Japan’s largest pharmaceutical companies. Under the agreement, CIMYM received an up-front payment of US$14.5 million and milestone payments at certain states of development for each of a number of indications as well as payments based on supply of nimotuzumab and sales performance in the territory. The maximum aggregate amount of milestone payments payable under the Daiichi license agreement is US$21,400,000. Daiichi is developing nimotuzumab for the Japanese market in several cancer indications.

Licenses for Early Stage Drug Discovery and Preclinical Programs