| OMB APPROVAL OMB Number: Expires: 3235-0063 April 30, 2012 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended:December 31, 2009

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____________________________ to_____________________________

Commission file number:0-49942

STRATECO RESOURCES INC.

(Exact name of registrant as specified in its charter)

| QUÉBEC, CANADA | N/A |

| State or other jurisdiction of | (I.R.S. Employer |

| incorporation or organisation | Identification No.) |

1

225 GAY-LUSSAC, BOUCHERVILLE, QUÉBEC, CANADA, J4B 7K1

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code:(450) 641-0775

Securities registered pursuant to Section 12(g) of the Act:

| Title of each class | Name of each exchange on which registered |

| ________________________ | Toronto Stock Exchange in Canada (RSC) |

| (Title of class) | Frankfurt in Germany:(RF9) |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes[ ] No[ ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes[ ] No[ ]

Note– Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the

Exchange.

2

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13

or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter

period that the registrant was required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days

[X]Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web

site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation

S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit and post such files).

[X] No [ ]Yes

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this

chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive

proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K.[ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer,

or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting

company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [X] | |

| Non-accelerated filer [ ] | (Do not check if a smaller reporting company) | Smaller reporting company [ ] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

[ ] Yes [X] No

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference

to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the

last business day of the registrant’s most recently completed second fiscal quarter.

As of the last business day of the registrant’s most recently completed second financial quarter as of June 30, 2009, the

common share was last sold at the price of CAN$0.92 per share for and aggregate market value with 119,266,462 common

shares outstanding of CAN$109,725,117.

APPLICABLE ONLY TO REGISTRANTS INVOLVED IN BANKRUPTCY

PROCEEDINGS DURING THE PRECEDING FIVE YEARS:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or

15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

[ ]Yes [ ] No

(APPLICABLE ONLY TO CORPORATE REGISTRANTS)

3

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest

practicable date.

As of March 10, 2010, 122,695,906 common shares were outstanding

4

DOCUMENTS INCORPORATED BY REFERENCE

(1) Part

Item 8: Financial Statements of an exploration stage company

The Company, an exploration stage company, incorporates for reference to the present document the Strateco Resources Inc. audited financial statements for the fiscal year ending December 31, 2009 and audited financial statements for the fiscal year ending December 31, 2008 that include the report of U.S. GAAP reconciliation atNote 23. These financial statements follow the signature page of the present document.

INDEX:

5

PART I

Item 1. Business

All amounts mentioned in this following section are in Canadian dollars.

The Company was incorporated under theCanada Business Corporations Actby articles of incorporation dated April 13, 2000.

The Company is primarily engaged in the exploration of mining properties with a view to commercial production. It does not currently have any mines in production. The Company has a portfolio of five wholly-owned mining properties, as well as an interest in or options on three mining properties in Quebec, Canada. These properties comprise 1,068 claims for a total area of 56,747 hectares (567 km2). The Company’s activities are focused on the development of the MATOUSH PROJECT, which consists of four uranium properties.

Recovery of the cost of mining assets is subject to the discovery of economically recoverable reserves, the Company's ability to obtain the financing required to pursue exploration and development of its properties, and profitable future production or the proceeds from the sale of its properties. The Company must periodically obtain new funds in order to pursue its activities. While it has always succeeded in doing so to date, there can be no assurance that it will continue to do so in the future.

The Company is involved in exploration of uranium and to its cognizance; there exists no competition between companies involved in that kind of exploration. The main business of the Company is to discover by exploration as much as possible of resources of uranium to eventually become a producer of uranium and to sell this uranium at the market value. Most of the companies cooperate with each other, exchange or trade equipment, consultant services and knowledge regarding the complex requirements of health and safety standards, permits and governmental authorizations, methods of exploration or production. Since most companies in Canada involved in exploration or production of uranium are public companies all technical information is publicly disclosed as well.

However, in the mining industry in Canada in general, a certain competition may exist when a company needs to retain and to hire geologists and mining technicians which are difficult to find in Québec or in Canada The Company was however able up to now to recruit in Europe and in Québec and to retain qualified personnel and consultants.

Another aspect of competition for the whole mining industry in general is the acquisition of claims and many factors may influence their value. But once the interest in the claims of the property is acquired by the Company or is subject to an agreement, the claims of the property and the adjacent claims as well, are protected by the agreement as an interest area. For the moment the Company holds sufficient mining claims to pursue its objectives.

The Company had initiated voluntarily an Environmental Impact Study for the MATOUSH PROJECT through a specialized firm, Golder Associates in 2007, at approximate costs of $268,000 during the year 2007, that represented less than 1.5% of the Company’s expenses in exploration in the approximate amount of $18.7M.

As of December 31, 2008, the Company has spent a sum of $1,193,640 for environmental impact studies and had paid to a management company the sum of $20,420 for the services on a permanent basis of an environmental manager in the months of November and December 2008 to prepare the environmental requirements in view of the underground exploration program. This total amount of $1,214,060 represented only 5.40% of the Company's expenses in exploration in the amount of $22,317,849.

6

For the fiscal year ended December 31, 2009, the Company has spent an approximate amount of $976,000 to obtain environmental permits and licenses, to comply with environmental obligations of different levels of government and to retain though a management company, the services of the environmental manager throughout the year. This approximate amount represents approximately 5.6% of the explorations expenses of the company for that year. Compliance with Environmental Laws at the Federal, provincial and local levels, for as long as the Company remains at the exploration stage for uranium, does not require material capital expenditures for the Company.

The Company has no employees and only a few consultants since it has a Services Agreement with BBH Géo-Management Inc. that provides employees and consultants in management, secretarial, geology, operations, legal affairs, investor relations, technical and environmental matters and professional services as fully disclosed inItem 7 of Management’s Discussion and Analysis of Financial Condition and Results of Operation -Related-Party Transactions andItem 10-Executive Compensation.”

Financing

On October 1st, 2008, the Company closed a non-brokered private placement of flow-through common shares with two funds for aggregate gross proceeds of $8,000,001.75. The private placement consists of 4,102,565 flow-through common shares issued at a price of $1.95 per share. The flow-through proceeds have been used by the Company before December 31, 2009 to incur eligible exploration expenses on its MATOUSH PROJECT located in Quebec, Canada and described in details inItem 2. Properties

On December 8, 2009, the Company completed a flow-through private placement of $2.5Million with one insider holding more than 10% of the share capital of the Company, through one fund and one accredited investor that are related, for an aggregate amount of $2.4M and another accredited investor for an amount of $100,000 for a total flow-through financing of $2,500,000. This private placement was made with two (3) subscribers from the Province of Ontario in Canada. The Company issued in this private placement a total of 2,500,000 flow-through common shares at the price of $1.00 per share.

The flow-through proceeds will be used by the Company to incur eligible exploration expenses on its MATOUSH PROJECT including MATOUSH, MATOUSH EXTENSION, ECLAT and PACIFIC BAY-MATOUSH properties and also on the MISTASSINI property, all located in Quebec, Canada and described in details inItem 2. Properties.The Company paid an amount of $100,000 as Finder’s fees.

Subscribers of flow through common shares are entitled to tax rebates in Canada and in the Province of Quebec when the holder is a resident of Quebec because the Company renounce to the credits to which it would be entitled in favor of the subscribers. The Company engages itself to spend the flow-through financing amounts on exploration expenses eligible to tax credits on or before December 31, 2010.

All the securities issued pursuant to the placement were subject to a hold period of four months and one day from the date of closing.

On January 27, 2010, the Company closed a non-brokered private placement for a total financing of $15 million. The financing was subscribed by Sentient Executive GP III Limited on behalf of two funds from Cayman Islands (“Sentient”), an equity fund that manages natural resource sector investments (“Sentient”).

Pursuant to the private placement, Sentient subscribed for 100,000 units at a price of $0.95 per unit for an amount of $95,000. Each unit consists of one common share (a "share") of the Company and one-half of one warrant. Each warrant entitles its holder to purchase one share of the Company for $1.00 during a 24-month period following the closing and for $1.05 during the subsequent period of 24 to 36 months after the closing (“warrant”). On closing, the Company issued a total of 100,000 shares and 50,000 warrants in consideration of the subscription price of the units.

Sentient also subscribed for 14,905 convertible notes maturing on February 27, 2015, for an amount of $14,905,000. Each tranche of $1,000 in notes is accompanied by 527 warrants, for a total of 7,844,737 warrants with the same exercise conditions as the warrants included in the units.

Until the maturity date of the notes, Sentient has the option of converting the notes into 1,053 shares per tranche of $1,000 based on a conversion price of $0.95 per share, for a total of 15,689,474 shares.

7

The Company paid Sentient transaction fees equal to 5% of the gross proceeds of the private placement. These transaction fees in the amount of $750,000 were paid through the issuance at closing of 789,474 units, being 789,474 shares and 394,737 warrants with the same exercise conditions as the warrants included in the units.

The Company plans to use the net proceeds of the private placement to finance exploration work, primarily for the acquisition of materials and infrastructure for its MATOUSH uranium PROJECT, which comprises THE MATOUSH, MATOUSH EXTENSION, ECLAT AND PACIFIC-BAY MATOUSH PROPERTIES in Quebec’s Otish Mountains in Canada located in Quebec, Canada and described in details inItem 2: Properties.

All the securities issued pursuant to the placement were subject to a hold period of four months and one day from the date of closing.

Item 1A: Risk Factors.

Exploration and Mining

The Company is at an exploration stage.Exploration and mining activities are subject to a high level of risk. Few exploration properties reach the production stage. Unusual or unexpected formations, fires, power failures, labour conflicts, floods, rockbursts, subsidence, landslides and the inability to locate the appropriate or adequate manpower, machinery or equipment are all risks associated with mining activities and the execution of exploration programs.

The development of resource properties is subject to many factors, including the cost of mining, variations in the material mined, fluctuations in the commodities and exchange markets, the cost of processing equipment and other factors such as aboriginal claims, government regulations including in particular regulations on royalties, authorized production, importation and exportation of natural resources and environmental protection. Depending on the price of the natural resources produced, the Company may decide not to undertake or continue commercial production. Most exploration projects do not result in the discovery of ore.

The probability of an individual prospect ever having reserves that meet the requirements of Industry Guide 7 is extremely remote. In all probabilities, the majority of the properties do not contain any reserves and any funds spent on exploration will probably be lost.

Even if the Company completes the current exploration program and it is successful in identifying a mineral deposit, the Company will have to spend substantial funds on further drilling and engineering studies before the Company knows if it has a commercially viable mineral deposit, a reserve.

Environmental and Other Regulations

Current, possible or future environmental legislation, regulations and measures may entail unforeseeable additional costs, capital expenditures, restrictions or delays in the Company's activities. The requirements of the environmental regulations and standards are constantly re-evaluated and may be considerably increased, which could seriously hamper the Company or its ability to develop its properties economically. Before a property can enter into production, the Company must obtain regulatory and environmental approvals. There can be no assurance that such approvals will be obtained or that they will be obtained in a timely manner. The cost related to assessing changes in government regulations may reduce the profitability of the operation or altogether prevent a property from being developed. The Company considers that it is in material compliance with the existing environmental legislation.

Financing and Development

The Company has incurred losses to date and does not presently have the financial resources required to finance all of its planned exploration and development programs. Development of the Company's properties therefore depends on its ability to obtain the additional financing required. There can be no assurance that

8

the Company will succeed in obtaining the required funding. Failure to do so may lead to substantial dilution of its interests (existing or proposed) in its properties. Furthermore, the Company has limited experience in developing a resource property, and its ability to do so depends on the services of experienced people or in the signature of agreements with major resource companies that can produce such expertise.

Commodities Prices

The market for uranium, gold, diamond, base metals or other mineral discovered can be affected by factors beyond the Company's control. Commodities prices have fluctuated widely, particularly in recent years. The impact of these factors cannot be accurately predicted.

Uninsured Risks

The Company could become liable for subsidence, pollution and other risks against which it cannot insure itself or chooses not to insure itself due to the high cost of premiums or for some other reason. Payment of such liabilities could decrease or even eliminate the funds available for exploration and mining activities.

Item 1B: Unresolved Staff Comments

The Company did not receive any comments from the U.S. Securities and Exchange Commission during the fiscal year to which the present report relates.

Item 2: Properties. All amounts mentioned in this following section are in Canadian dollars.

The following technical data has been read and revised by Jean-Pierre Lachance, Geo., Executive Vice President of Strateco Resources Inc., and David A. Ross, P.Geo., Senior geologist at Scott Wilson Roscoe Postle Associates Inc. (Scott Wislon RPA) who are qualified persons as defined under Canadian National Instrument 43-101 (NI 43-101).

At December 31, 2009, the Company had a portfolio of five wholly owned mining properties and interests or options on three mining properties in Quebec covering more than 56,747 hectares. Of these eight (8) properties, the Company explores actively for uranium on five (5) of them.

The table below represents the number of claims, the surface area for each property held by the Company as of December 31, 2009, the kind of minerals subject to exploration on this property, the interests of the Company in each property and applicable royalties:

| Number of claims | Surface Area in Hectares | Company’s Interest (I) and Options (O) | Percentage | Exploration(1) | Royalties | |

| MATOUSH PROJECT | ||||||

| Matoush | 25 | 1,328.46 | I | 100% | U3O8 | 2% NSR Yellow Cake(2) |

| MatoushExtension | 198 | 10,503.85 | I | 100% | U3O8 | - |

| Eclat | 90 | 4,786.90 | I(3) | 100% | U3O8 | 2% NSR(3) |

| Pacific-Bay-Matoush | 277 | 14,576.33 | O(4) | 60% | U3O8 | 2% Yellow Cake(4) |

| MISTASSINI | 171 | 9,114.47 | O(5) | 60% | U3O8 | 2% Yellow Cake(5) |

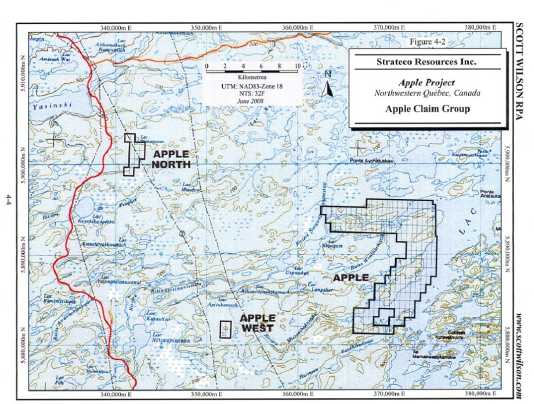

| APPLE | 194 | 9,928.13 | I | 100% | U3O8 | 2% NSR(6) |

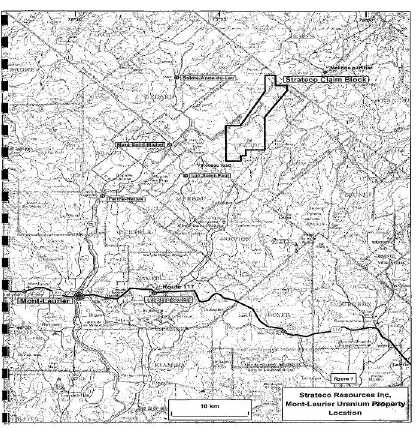

| MONT-LAURIERURANIUM | 80 | 4,710.35 | I | 100% | U3O8 | |

| QUÉNONISCA | 33 | 1,798.77 | I(7) | 50% | ZN,PB,CU,AG | |

| TOTAL | 1,068 | 56,747.26 | ||||

9

(1) | Exploration for uranium: U O and base metals exploration: ZN, PB, CU and AG;3 8 |

| |

| (2) | This Royalty will be payable by the Company to Ditem Explorations Inc.; upon production; |

| |

| (3) | The Company holds a 100% interest in all minerals other than diamonds in the ECLAT PROPERTY since June 15, 2009. This Royalty will be payable, upon production, in favour of the Vija Ventures Corporation on all minerals other than diamonds and 2% portion in favour of Vija Ventures Corporation of all gross proceeds from the sale or disposition of carbon emission rights tied to the production of uranium from the property; |

| |

| (4) | The Company detains an option to acquire a 60% interest in the PACIFIC BAY-MATOUSH PROPERTY over a period of 4 years ending in 2011. Only Pacific Bay Minerals Ltd. its successors and assigns will be responsible to pay this Yellow Cake Royalty to Pierre Angers, upon production; |

| |

| (5) | The Company detains an option over a period of 3 years ending in 2011 to acquire an interest of 60% on uranium rights only, on the Mistassini Property. This Royalty will be payable upon production by the parties to the option and joint venture agreement in favour of Northern Superior Resources Inc; |

| |

| (6) | This Yellow Cake Royalty will be payable on all minerals, in favour of Virginia Mines Inc., upon production, subject to buyback right of the Company to purchase one percent (1%) NSR against a cash payment of one million dollars (CAN$1,000,000). |

| |

| (7) | The Company and SOQUEM, each holds a 50% interest in this property. Upon production, each partner is entitled to its share of the production but if the interest of one party is of 10% or less it must transfer its interest to the other party and will hold thereafter a 1% NSR royalty. |

10

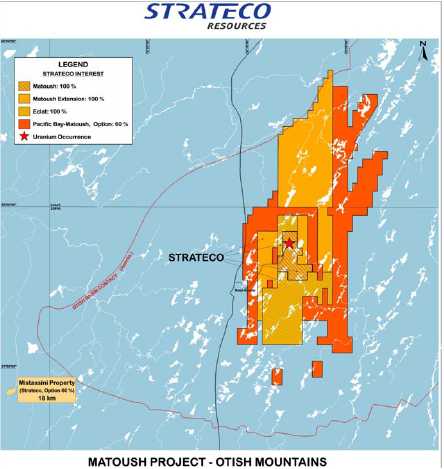

The map inFigure 1belowrepresentsthe regional location of all properties and projects of the Company as of March 2010 in the Province of Québec, Canada:

Following is the order for the Company’s discussion of its eight (8) properties:

SUMMARY OF URANIUM EXPLORATION ANALYTICAL PROCEDURES

| A. | MATOUSH PROJECT | ||

| A.1 | MATOUSH PROPERTY | ||

MT-34 ZONE

MT-006 ZONE

TECHNICAL REPORTS

SCOPING STUDY

| A.2 | MATOUSH EXTENSION PROPERTY | |

| A.3 | ECLAT PROPERTY | |

| A.4 | PACIFIC-BAY-MATOUSH PROPERTY | |

| A.5 | PERMITS AND LICENSE |

| B. | MISTASSINI PROPERTY | |

| C. | APPLE PROPERTY | |

| D. | MONT-LAURIER PROPERTY | |

| E. | QUÉNONISCA PROPERTY |

11

The Company is mainly involved in exploration work for uranium on properties described in details in subsectionsItem 2: Properties subsections AthroughD, so the Company will present at the outset, a briefSummary ofUranium Exploration analytical proceduresin the following paragraphs and a detailed description of these procedures at the end of thisItem 2-Noteentitled:Detailed Uranium Exploration Analytical procedures.

Item 2: SUMMARY OF URANIUM EXPLORATION ANALYTICAL PROCEDURES:

Summary of Sampling Methods, Quality Assurance and Quality Control

The sampling program at MATOUSH PROJECT, including all aspects of Quality Assurance and Quality Control (“QA/QC”), is supervised by the Company’s Chief Geologist, Jonathan Lafontaine, P. Geo., who is a Qualified Person as defined under Canadian National Instrument 43-101 (“NI 43-101”).

Drill core is hydraulically split on-site by dedicated personnel and samples are collected over 30 cm to 3 m intervals based on geology. All reported samples are split with hydraulic splitter. Samples are individually bagged and tagged and shipped as per transportation protocols. Blanks, duplicates, and standards are randomly inserted in the sample shipment within the sample number sequence.

Prior to shipping, sealed sample bags are stored in a locked facility. Samples are shipped via air to Témiscamie float plane base, trucked to Chibougamau and from there sent by courier to the Geo-analytical Laboratories at the Saskatchewan Research Council (“SRC”) in Saskatoon, in the Province of Saskatchewan in Canada. The laboratory is accredited by the Standards Council of Canada as an ISO/IEC 17025 Laboratory for Mineral Analysis Testing. On arrival at SRC, samples are sorted into lots according to radioactivity level and prepped and analyzed in that order. Samples are dried and jaw crushed to 60% passing -2 mm and 100 g to 200 g sub sample split out using a riffler. The sub-sample is pulverized to 90% passing 106 microns using a ring and puck grinding mill. The mills are cleaned between samples using steel wool and compressed air.

After sample preparation, SRC analyzes for U3O8content by several means. ICP 4-3R (partial digestion) and fluorimetry are used on samples with U3O8less than 100 PPM. ICP 4-3 (total digestion) is employed on samples with normal to high radioactivity, hence for the majority of the samples submitted. Samples with greater than 1,000 PPM U3O8are also subjected to an Aqua Regia digestion before determination of wt% U3O8also by ICP. The Company independently adds one blank sample and one quarter split duplicate each with every 14 samples. Results are reviewed on an ongoing basis.

In addition to chemical analysis, the Company employs a down-hole gamma probe instrument to estimate uranium grades. Prior to probing, the holes are washed to eliminate minor mineralization smearing or radon effects. Probe results, in cps units, are converted toeU3O8(equivalent U3O8) using well established algorithms specifically calibrated to the Matoush deposit. A calibration hole (MT-07-29), for which there are complete chemical analyses, is probed at least once per month to ensure the probe is calibrated accurately and functioning properly. Results are also compared with chemical analysis when received. Discrepancies in results are immediately investigated and corrected.

Analytical results are received and imported into the Company’s data base. Laboratory replicates and laboratory standards are checked. Internal duplicates, blanks and standards are checked. Analytical drift from expected results triggers re-analysis.

Results are also compared with estimated Grade and Thickness (“GT”) values from in-situ down-hole probing, and with counts per second (“CPS”) values logged during initial core logging procedures.

In the following text covering in details exploration works on the Company’s properties, the letter “e” in“eU3O8” represents theestimatedorequivalentvalue ofU3O8 as determined by down-hole calibratedgeophysical probing.

12

Further information on the various technical subjects relating to exploration work for uranium, namely the “eU3O8” and “CPS” nomenclatures, exploration program analysis methods, sampling techniques, quality control for the results obtained by the gamma probe and laboratory chemical analyses is available on the Company’s website atwww.stratecoinc.comin section “Investor Relations” subsection “Q/A and Q/C” and inthis annual report at Item 2 Properties-inthe Note: Detailed Uranium exploration analytical procedures.

Item 2 A: MATOUSH PROJECT

The map inFigure 2below represents the Company interests in different properties constituting the MATOUSH PROJECT including MATOUSH PROPERTY, MATOUSH EXTENSION PROPERTY, ECLAT PROPERTY and PACIFIC BAY-MATOUSH PROPERTY.

The MATOUSH PROJECT (See subsectionA) is located in the Otish Mountains in northern Quebec, Canada, about 275 kilometres north of Chibougamau, and consists of the wholly-owned MATOUSH PROPERTY (See subsectionA.1), the wholly-owned MATOUSH EXTENSION PROPERTY (See subsectionA.2), the wholly-owned ECLAT PROPERTY (See subsectionA.3) and PACIFIC-BAY-MATOUSH PROPERTY in which the Company has an option to earn a 60% interest (See subsectionA.4). The MATOUSH PROJECT currently comprises 590 claims for a total area of 32,195.54 hectares (321 km2).

13

The project is accessible by air, and in winter by the Eastmain winter road, which runs about seven kilometres to the west of the Project. The winter road has been upgraded over a 142-km length to allow access to the camp and transport of equipment and fuel required for 2009. The winter road repair work was carried out as planned. The contract was awarded toEntreprises CARSA Inc. for a second consecutive year. Repair work began in mid-December 2008 and maintenance was ongoing until March 20, 2009. In addition to various materials and a shovel excavator 700,000 litres of fuel and four new 50,000-litre fuel tanks were transported to the site. The four drills belonging to Major Drilling Group International Inc. that were on site were taken away and replaced by two new drills.

The workers and consultants benefit from a 50 persons camp completed in 2007, with all modern commodities.

The technical data in the following text is based on a report entitled:Technical Report on the Mineral Resources Update for the Matoush Uranium Project Central Quebec, Canada, dated September 16, 2008, prepared in accordance withNational Instrument 43-101 respecting standards of disclosure for mineral projects (“NI 43-101”). This data has also been reviewed by the authors of the report, David A. Ross, M. Sc. P. Geo. and R. Barry Cook, P. Eng. of Scott Wilson RPA. The technical data in the following text is also based on a memorandum entitledMatoush Mineral Resource Update, dated September 18, 2009, and reviewed by David A. Ross, M. Sc. P. Geo. of Scott Wilson RPA. The technical data based on recent information has been reviewed by Jean-Pierre Lachance, Executive Vice President of the Company. All three are qualified persons as defined inNI 43-101.

Cautionary Note to U.S. Investors concerning estimates of Measured and Indicated Resources.This section uses the terms “measured” and “indicated resources”.We advise U.S. investors that while those terms are recognized and required by Canadian regulations, the U.S. Securities and Exchange Commission does not recognize them. U.S. investors are cautioned not to assume that any part or all of mineral deposits in these categories will ever be converted into reserves.

Cautionary Note to U.S. Investors concerning estimates of Inferred Resources. This section uses the term “inferred resources”.We advise U.S. investors that while this term is recognized and required by Canadian regulations, the U.S. Securities and Exchange Commission does not recognize it. “Inferred resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of anInferred Mineral Resourcewill ever be upgraded to a higher category. Under Canadian rules, estimates ofInferred Mineral Resourcesmay not form the basis of feasibility or pre-feasibility studies, except in rare cases.U.S. investors are cautioned not to assume that part or all of an inferred resource exists, or is economically or legally minable.

In 2008, the Company began a 40,000-metre drilling program on the MATOUSH PROJECT and planned a budget of $22 million in exploration works. The Company carried out an extensive drilling program on its wholly-owned MATOUSH PROPERTY, located in the Otish Mountains, 275 km north of Chibougamau and the Company obtained interesting drill results. The potential and size of the newMT-22 mineralized zone was confirmed, as well as the extension of theAM-15 zone at depth.

In the second quarter of 2008, drilling was primarily focused on the newMT-34 mineralized zone that lies in the depth extension of theAM-15 zone, as well as on theMT-22 mineralized zone.

Third quarter of 2008, exploration work on the MATOUSH PROJECT essentially consisted of drilling and prospecting. A total of 16,837 metres were drilled in 52 holes. Of this total, 15,327 metres (45 holes) were drilled on the MATOUSH PROPERTY and the remaining 1,510 metres (7 holes) on the PACIFIC BAY-MATOUSH PROPERTY.

The Company prospected in the Laurent Martin area, 5.0 km to the east of theAM-15 lens, where a train of boulders including one that returned nearly 60,000 counts per second had been identified during prospection in summer 2007.

In the fourth quarter 2008, drilling continued on the MATOUSH PROJECT in the northern and southern extensions of well defined lenses and also along the Matoush fault with the objective to identify new mineralised lenses.

Twenty three drillings have been completed for a total of 9,517 metres during the fourth quarter 2008. These drillings explored at the North of theMT-22 lens and the south of theMT-34 lens.

14

In 2008, a total of 119 holes were drilled on the MATOUSH PROJECT for a total of 59,603 meters leading tothe delineation of Indicated mineral resources of 3.73M poundsU3O8and Inferred mineral Resources of 13.070 Mpounds U3O8as reported inItem 2: Properties-Technical Reports of Form 10K for the year ended December 31,8.

All exploration drill holes results for the year 2009, longitudinal sections as well as photos of the mineralized intersections can be seen on the company’s website atwww.stratecoinc.com.

In 2009, the Company continued to focus its efforts on the exploration and development of its uranium project, the MATOUSH PROJECT, using advanced exploration methods. The Company drilled 75 holes on its various properties for a total of 35,026 metres of drilling, including 34,240 metres on the MATOUSH PROJECT. Most notably, the holes drilled on the MATOUSH PROJECT resulted in the doubling of theindicated mineral resourceto 7.46 million pounds of U3O8at the high grade of 0.78% U3O8.

The true width of the mineralized intersections of the holes drilled in 2009 has not yet been determined.

In order to describe the exploration work in 2009 conducted on its uranium properties in details, the Company must include in this annual report a description of the techniques used and required for exploration work, namely: (i) analytical procedures used in the exploration program; (ii) sampling methods; (iii) quality assurance and control (including information on the use of the letter“e”ineU3O8, which represents theestimatedorequivalentU3O8value determined using a calibrated spectral or gamma probe); (iv) the methodology for the use of the gamma probe; and,finally, (v) a comparison of eU3O8and U3O8 results.

This technical description can be found in theNOTEfollowing theItem 2: Propertiesand in theQA/QCsection under theAbout Stratecotab on the Company’s website, atwww.stratecoinc.com.

In 2009, 68 holes totalling 34,240 metres were drilled on the MATOUSH PROJECT as a whole. Drilling was distributed as follows: 26,144 metres in 44 holes on the MATOUSH PROPERTY; 4,375 metres in 11 holes on the ECLAT property, and 3,721 metres in 13 holes on the PACIFIC BAY-MATOUSH property. No drilling was done on the MATOUSH EXTENSION property. In all, 160,216 metres (378 holes) have been drilled on the MATOUSH PROJECT since exploration began in 2006.

The 2009 drilling program began in early February on the MATOUSH PROJECT, with two drills in operation. One drill was assigned to drilling on the southern extension of the MT-34 zone, about 1 km away from that zone, with the goal of identifying a new lens at a depth of between -400 and - -650 metres. The second drill was first mobilized on the PACIFIC BAY-MATOUSH property to drill 1,500 metres in the Rabbit Ears South area, and was then moved in early March to an area of the ECLAT property 9.5 km south of the MT-34 zone, near Hole EC-08-01, which returned very interesting results in the winter of 2008.

Drilling was temporarily suspended during the spring thaw, from April 27 to May 27. Drilling then resumed, with two drills operating on the properties, as well as one helicopter-borne drill for holes drilled on the MISTASSINI and PACIFIC BAY-MATOUSH properties. Besides the exploration holes, five geotechnical holes totalling 526 metres were drilled as part of the preparatory work for the underground exploration program. The 2009 drilling program ended on November 26.

The MATOUSH PROJECT remains the Company’s priority in the pursuit of its objective to become the first Québec Company to advance a uranium exploration project to the underground exploration stage.

Item 2: A1. MATOUSH PROPERTY

The Company owns a 100% interest in this uranium property representing for the moment the main focus of the MATOUSH PROJECT located about 275 km north of Chibougamau, in the Otish Mountains, in Québec, Canada (SeeFigure 1for regional location of the MATOUSH PROPERTY).

15

Location and Access

This property is accessible by air, and in winter by the Eastmain winter road, which runs about seven kilometres to the west of the property.

Mining Claims

The property consists of 25 claims covering an area of 1,328.46 hectares.

A letter of intent dated May 12, 2005 provided for the Company to earn a 51% interest from Ditem Explorations Inc. ("Ditem"), which owned then a 100% interest in the MATOUSH PROPERTY, in consideration of payments totalling $125,000 over two years, including $5,000 on signature of the agreement; $750,000 in exploration work over three years, including $200,000 the first year; and the issuance of 600,000 common shares of the Company over two years. The Beaver Lake Area project, which lied approximately 20 kilometres to the west, was also covered by this initial agreement.

A new letter of intent was signed with Ditem on February 21, 2006, giving the Company a 100% interest in the MATOUSH PROPERTY under the following terms: The Company paid $10,000 at the execution of the letter of intent and within five days following approval of the transaction by regulatory authorities, the Company paid to Ditem $140,000 and issued to Ditem 400,000 common shares. The shares were subject to a resale restriction of four months plus a day. Ditem became entitled upon production to a 2% NSR, as defined by industry standards. The claims in the Beaver Lake area have not been renewed by the Company upon acquisition of this 100% interest in the MATOUSH PROPERTY.

Uranium Potential

The Otish Mountains area is well known for its uranium potential, particularly due to exploration conducted by Uranerz Exploration and Mining (“Uranerz”) and Cogema in the late 1970s and early 1980s.

The results of exploration conducted by Uranerz in the early 1980s before uranium prices tumbled, as well as those obtained by the Company in 2006, 2007, 2008 and 2009, indicated that the MATOUSH PROPERTY had a very good potential.

Uranerz only explored a 900-metre section of the Matoush structure, which had been traced over 3,900 metres on this property. The Matoush structure was discovered in the early 1980s by the German company. In 1984, Uranerz drilled 23 holes, including HoleAM-15, which returned a 16-metre intersection at a vertical depth of 200 metres grading 0.95%U3O8 or over 20 pounds of U3O8 per tonne of ore, a very high grade by today’s standards. Due to low uranium prices from 1985 to 2005, the uranium potential of the MATOUSH PROPERTY was not explored any further. Uranerz exploration work results dated from the late 1970s and early 1980s and preceded the Canadian National Instrument 43-101 (“NI 43-101”)

Cautionary Note:A qualified person has not done sufficient work to classify the historical estimate by Uranerz as current mineral resources or mineral reserves. The Company does not consider resources or reserves of an historical estimate to be mineral resources or mineral reserves, as these categories are defined in articles 1.2 and 1.3 of the NI 43-101, as amended. The investor or reader should not rely upon this historical estimate.

This exploration work by Uranerz served however as the Company's point of departure for exploration of the MATOUSH PROPERTY.

The holes drilled on the MATOUSH PROPERTY indicated that the uranium mineralization was closely linked to the fuschite and tourmaline alteration on both sides of a gabbros dike in the sediments. The alteration envelope associated with the Matoush structure was symmetrical, with an average thickness of 40 metres. Typically, adjacent to and moving outward from the dike was first a tourmaline zone, then a chlorite-fuschite-muscovite zone and a limonite-hematite zone.

In 2009, the Company carried out surface exploration on 26,144 metres in 44 holes of surface drilling on the property.

16

Given the structural context at MATOUSH PROPERTY, various zones of varying grade and thickness were outlined using a smaller drill grid.

It should be noted that the southern extension of theAM-15zone was tested in the winter of 2006-2007 along theACF unitthat hosts theAM-15resources.

Detailed geological interpretation of theAM-15zone as part of the NI 43-101 resource estimate in September 2007 revealed that theAM-15zone dips about 200to the south and that the mineralization appears to continue in the underlying CBF unit. Drilling carried out on the lake ice showed clearly that theAM-15zone continues at depth toward the south.

The five holes drilled in the less porous, 75-metre thick intermediate CBF unit all intersected the fault zone, with variable thicknesses and grades thataveraged 0.08% eU3O8over 4.2metres. The mineralization extends to the lowerCBFcontact, and the goal was to explore the underlyingACFunit in the extension of theAM-15zone plunge.

The potential of this major mineralized zone was supported by the marked presence of fuschite alteration and the absence of dykes in the three most northern holes (MT-08-001,MT-08-003,MT-07-129), which returned the best intersections. Drilling on theAM-15lens had shown that the best intersections corresponded to the intensity of the fuschite alteration and the absence of dykes.

The drill results resulted in an initial resource estimate for theAM-15zone in September 2007, discovery of a new zone (MT-22) and confirmation of the extension of theAM-15zone at depth. On September 27, 2007, Scott Wilson Roscoe Postle Associates Inc. (Scott Wilson RPA) completed a NI 43-101 technical report on the MATOUSH PROPERTY, including a resource estimate on theAM-15core zone.

Scott Wilson RPA prepared the initial mineral resource estimate for theAM-15core zone at MATOUSH PROPERTY using drill-hole data available as of September 27, 2007. This technical report concluded that,Indicated mineral resourceswere estimated to total201,000 tonnes grading 0.79%U3O8 containing 3.48million pounds ofU3O8. Inferred mineral resources were estimated to total 65,000 tonnes grading 0.43%U3O8 containing 0.62million pounds.

Results of this resource estimate have been described in details inForm 10-KSB for the year ended December 31, 2007 at Item 2 Properties-MATOUSH PROPERTY.

Through geophysical surveys and several drill holes on the MATOUSH PROPERTY, the Company also established the presence of the Matoush fault and sedimentary horizonsACF-3(AM-15zone) andACF-4(MT-22andMT-34zones) on a distance of over 15 km, including a mineralized section located by HoleEC-08-01, 8.5 km south of theAM-15zone. This hole intersected0.15% eU3O8over 2.1metres at a vertical depth of 550 metresin theACF-4. These ACF horizons of coarse sediments represent a favourable context for uranium precipitation.

Two holes drilled in theACF-4(MT-08-019andMT-08-027) proved encouraging, both in terms of geological context and the potential size of the mineralized body and showed a fault offset that is a prime site for uranium precipitation.

During the second quarter of 2008, the drill results confirmed the potential in uranium sought by the Company, especially on theMT-34zone, which lies in theACF-4, as does theMT-22zone.

Extensive surface exploration and airborne VLF geophysics were carried out during the summer 2008 on MATOUSH PROPERTY.

During the third quarter of 2008, the exploration holes drilled in the northern extension of theAM-15zone (600 m to the north) and theMT-22zone (200 m to the north) resulted in the identification of a new fault, the Coonishish fault. This fault lies about 200 m east of the Matoush fault and is sub parallel to it. Two sections spaced at approximately 75 metres were drilled to determine the fault’s strike and dip and assess its uranium potential. The task proved relatively arduous, as the Coonishish fault is cut by other siliceous, clayey faults. From an exploration perspective, the results

17

were compelling, as the genesis model allowed the confirmation of a second system detached from the Matoush fault. The Coonishish fault was intersected in almost all the layers:ACF 1,2and3andCBF 1,2and3. Only one hole has intercepted mineralization to date, with the notable presence of fuschite alteration, which remains a key element for exploration. HoleMT-08-084returned an intersection of0.04%eU3O8over 2.0metres.

Exploration work

MT-22 ZONE

The newMT-22mineralized zone discovered by the Company in 2007 on the MATOUSH PROPERTY lies under theAM-15zone and is parallel to its plunge. TheMT-22lens drilled on a grid of approximately 100 m, lies at a vertical depth of between -300 m and -650 m and over a length of 450 m, between sections 31+50S and 27+00S and remained open to the north over its full height (350 m) (see longitudinal section on the Company’s website:www.stratecoinc.com). Given the known structural context of MATOUSH PROPERTY, several lenses with various grades and thicknesses were expected from drilling on a tighter grid and were also expected to return significant grades at the intersection with the Matoush fault.

In comparison, theAM-15zone is 50 metres high and 300 metres long, contained anestimated resourceof 4.1million pounds of U3O8according to theTechnical Report on the Matoush Uranium Project Central Quebec, CanadaNI 43-101of Scott Wilson RPA dated September 27, 2007.

Between November 2007 and March 2008, more than 25 holes had been drilled on this newMT-22zone. Good results on theMT-22zone were obtained in the two last holes drilled in 2007,MT-07-129andMT-07-130, and were located 80 metres apart at the same depth, -350 metres. HoleMT-07-129, which intersected8.3 metres at 0.24%eU3O8, including 3.7metres at 0.51%eU3O8, was encouraging, particularly as the alterationhalo in this hole isidentical to that of theAM-15zone.

The holes drilled in the first quarter of 2008 on theMT-22zone proved positive, with impressive intersections that confirm the importance of this major new zone. The best intersections included HoleMT-08-003, with2.86%eU3O8 over 5.8 metres including 4.48% eU3O8over 3.4metres and Hole MT-08-013 with 0.52% eU3O8over 7.2metres.

In February 2008 the Company intersected a new high grade section at the North End of theMT-22lens and in March 2008, the Company realised that theMT-22mineralized zone on the MATOUSH PROPERTY, discovered at depth under theAM-15zone, was proving to be major and planned for 50,000 metres of drilling during the year 2008 on this property.

During the second quarter of 2008, drilling on theMT-22mineralized zone, continued on a 50-metre grid in preparation for the next resource estimate. The results for this zone were conclusive. The best results were obtained in holesMT-08-022,028,036and043. HoleMT-08-022intersected0.37% eU3O8 over 18.4m, including 1.16% eU3O8 over 5.3m. Hole MT-08-027, drilled in early April 2008, returned an exceptionally wide mineralized section of 63 metres downhole, representing a true width of about 23 metres. The hole intersected 0.05% eU3O8 over 63.2 metres, including 0.13% eU3O8over 8.0metres showing a strong potential for this sector. Hole MT-08-028 intersected 0.47% eU3O8 over 41.6m, including 2.40% eU3O8 over 7.0m. Hole MT-08-036 intersected 0.41% eU3O8over 7.5m, including 1.25%eU3O8 over 2.0m, and Hole MT-08-043 intersected 2.45% eU3O8 over 10.5 m, including an high-grade section of 2.0 m at 8.97% eU3O8.

The most interesting holes drilled up to the end of the second quarter of 2008 on theMT-22zone are indicated in bold in the following table:

18

| Core | ||||||||||

| Az. | Angle | From | To | length | % | Max. | ||||

| Hole | Collar | (º) | (º) | (m) | (m) | (m) | eU3O8 | cps | lb/tonne | |

| East | North | |||||||||

| MT-08-001 | 13+46E | 27+00S | 264 | -45 | 707.2 | 709.5 | 2.3 | 0.62 | 20,000 | 13.64 |

| MT-08-003 | 12+40E | 26+50S | 273 | -45 | 573.5 | 580.3 | 6.8 | 2.43 | 65,000 | 53.46 |

| Including | 576.6 | 580.0 | 3.4 | 4.48 | 98.56 | |||||

| MT-08-013 | 12+15E | 27+42S | 264 | -60 | 467.1 | 474.3 | 7.2 | 0.52 | 8,300 | 11.44 |

| Including | 469.5 | 471.5 | 2.0 | 1.21 | 26.62 | |||||

| MT-08-015 | 12+78E | 26+52S | 276 | -63 | 565.8 | 567.1 | 1.3 | 0.85 | 10,000 | 18.70 |

| 584.6 | 591.3 | 6.7 | 0.47 | 10.34 | ||||||

| MT-08-018 | 12+75E | 26+50S | 262 | -65 | 636.9 | 638.1 | 1.2 | 0.90 | 25,000 | 19.80 |

| MT-08-020 | 11+55E | 28+70S | 267 | -64 | 455.3 | 463.6 | 8.30 | 0.31 | 1,900 | 6.82 |

| MT-08-022 | 11+70E | 28+05S | 267 | -62 | 450.5 | 468.9 | 18.40 | 0.37 | 14,200 | 8.14 |

| Including | 451.9 | 457.2 | 5.30 | 1.16 | 25.52 | |||||

| MT-08-028 | 12+15E | 27+40S | 284 | -59 | 409.9 | 451.5 | 41.6 | 0.47 | 56,000 | 10.34 |

| Including | 431.2 | 438.2 | 7.0 | 2.40 | 52.80 | |||||

| MT-08-035 | 13+12E | 25+46S | 264 | -55 | 520.6 | 523.4 | 2.8 | 0.63 | 12.6 | |

| MT-08-036 | 11+72E | 28+07S | 277 | -70 | 556.9 | 564.4 | 7.5 | 0.41 | 8.2 | |

| Including | 562.4 | 564.4 | 2.0 | 1.25 | 25.0 | |||||

| MT-08-043 | 12+13E | 27+39S | 272 | -61 | 475.0 | 485.0 | 10.5 | 2.45 | 49.0 | |

| Including | 481.5 | 483.5 | 2.0 | 8.97 | 179.4 | |||||

| MT-08-046 | 12+13E | 27+39S | 280 | -67 | 565.0 | 576.5 | 11.5 | 0.26 | 5.2 | |

| Including | 565.0 | 567.6 | 2.6 | 0.81 | 16.2 | |||||

| MT-07-022 | 13+25E | 31+50S | 273 | -53 | 769.3 | 769.9 | 0.6 | 1.18* | 8,600 | 25.96 |

| 830.8 | 832.2 | 1.4 | 0.31* | 6.83 | ||||||

| MT-07-101 | 12+40E | 30+60S | 275 | -48 | 524.1 | 526.6 | 2.5 | 0.25 | 5,900 | 5.50 |

| MT-07-116 | 14+81E | 28+96S | 275 | -49 | 797.6 | 798.9 | 1.3 | 0.72 | 32,000 | 15.84 |

| MT-07-120 | 15+64E | 28+03S | 275 | -45 | 840.2 | 840.8 | 0.6 | 0.36 | 5,000 | 7.92 |

| MT-07-126 | 13+94E | 30+80S | 275 | -45 | 753.5 | 760.8 | 7.3 | 0.10 | 5,800 | 2.20 |

| MT-07-129 | 11+93E | 28+65S | 269 | -47 | 491.6 | 499.9 | 8.3 | 0.24 | 6,400 | 5.28 |

| Including | 496.2 | 499.9 | 3.7 | 0.51 | 11.22 | |||||

| MT-07-130 | 11+93E | 28+65S | 280 | -47 | 499.3 | 504.3 | 5.0 | 0.11 | 1,020 | 2.42 |

| Including | 499.3 | 501.0 | 1.7 | 0.24 | 5.28 |

* Grades determined by chemical analysis

The true width of the mineralized sections has not yet been determined.

These equivalent uranium values were generated by the Gamma probe.

During the third quarter of 2008, five holes (3,096 metres) were drilled for the definition of theMT-22zone on the MATOUSH PROPERTY. Two holes (MT-08-061and064) were drilled in theMT-22zone to provide geological information within the mineral resource envelope. The three other holes (MT-08-077,079and080) were drilled within the envelope in the northern extension of theMT-22zone between the -400 m and -450 m levels. The holeMT-08-077 intersected0.80% eU3O8 over 7.0m, including 2.07% eU3O8 over 2.2m.

19

The holes in the northern part were drilled from 500 metres to 1 km from theMT-22zone, between sections 18+00S and 22+00S, from near surface to -425 metres. These holes failed to intersect any new zones. However, three of the four holes drilled on section 20+00S intercepted very strong fuschite alteration, which represented a favourable environment for the deposition of uranium mineralization. The best result was obtained in HoleMT-08-098, which returned a grade of0.06%eU3O8over 2.8metres in theACF 3.

These results were not part of the resource estimate of September 2008 since the cut-off date of this technical Report was July 25, 2008 (SeeItem 2:sub-sectionA-1,entitled:TECHNICAL REPORTS).

All the results ofMT-22zone can be viewed on the longitudinal section on the Company’s website, atwww.stratecoinc.com.

MT-34 ZONE

During the winter of 2006-2007, theSouthern Extensionof theAM-15zone was drilled along theACFhorizon hosting theAM-15estimated resources.

Detailed geological interpretation of theAM-15zone revealed that the zone dipped about 200to the south, and that the mineralization appeared to continue in the underlyingCBFunit. Drilling to be carried out on the lake ice began at the end of January 2008. The holes drilled show clearly that theAM-15zone continues at depth toward the south. The goal was then to explore the underlyingACFlayer, the same unit that hosted theMT-22zone to the north.

In 2008, the Company explored and outlined theSouthern Extensionof theAM-15zone at depth. This new zone had returned impressive core lengths with lower U3O88 grades than theAM-15andMT-22zones. However, it should be noted that exploration of this area had just begun, and based on theMT-22zone model, there were likely high-grade zone in theACFat depths of between - -300 and -650 metres.

Five holes were drilled in theCBFunit, and intersected values similar to those seen in the sameCBFunit above theMT-22zone.

This drilling on theSouthern ExtensionofAM-15led to the discovery of a new mineralized zone, theMT-34lens, on the Company’s MATOUSH PROPERTY at the end of April 2008.

Drilled in this new area at the end of the first quarter of 2008, holesMT-08-019andMT-08-027(see table above) revealed a major displacement of the Matoush fault between the two holes. HoleMT-08-034was planned on the basis of this observation.

The understanding of the geology and mineralization obtained from three years of work led to the discovery of this new, high-grade uranium zone and could likely result in the discovery of other mineralized zones. In fact, work by the Company has shown that the high-grade areas of theAM-15andMT-22uranium zones are associated with horizontal displacement of the Matoush fault.

The new zone, namedMT-34, was intersected by HoleMT-08-034at a vertical depth of 370 metres, south of theAM-15andMT-22zones. The HoleMT-08-034was the most interesting hole drilled by the Company at that time on the MATOUSH PROPERTY (the location of HoleMT-08-034can be seen atwww.stratecoinc.com).

HoleMT-08-034had intersected mineralization over a54.4 -metresection of drill core and gradedan average of0.69%eU3O8, including a 28.0 -metre section grading at an average of 1.32% eU3O8 (29 lbs/tonne) and a 4.80 -metre section with a grade of 6.13% eU3O8 (135 lbs/tonne). The true width of the mineralized sections had not yetbeen determined. The equivalent uranium values were generated by the Gamma probe.

Following HoleMT-08-034, 11 other holes were drilled in theMT-34area to test the extensions of this new mineralized zone. The results were conclusive, showing a high-grade core within theMT-34zone. HoleMT-08-047intersected a10.0 -metre mineralized zone grading an average of 2.24%eU3O8, including a 3.0 -metre sectiongrading 3.20%eU3O8 at a vertical depth of 454 metres, about 70 metres south of hole MT-08-034.

20

The most interesting hole drilled on theMT-34 zonewere: HoleMT-08-047, at a vertical depth of 454 metres about 70 metres south ofMT-08-034, which intersected a10.0 -metremineralized section grading an average of2.24%eU3O8, including 3.0metres with a grade of 3.20% eU3O8.

Two other holes drilled between holesMT-08-034andMT-08-047on a40-metre gridin preparation for the next resource estimate confirmed the potential of this new zone.Hole MT-08-050intersected the mineralized zoneover 21.6 metres averaging 0.44% eU3O8, including1.8metres grading 1.88%eU3O8,while holeMT-08-053intersected an11.4 -metremineralized sectionaveraging 2.02%eU3O8, including 5.2m grading 4.38% eU3O8.

The most interesting results for holes drilled on theMT-34zone are indicated in bold in the following table:

| Hole | Collar | Az. (º) | Angle (º) | From (m) | To (m) | Core Length (m) | % eU3O8 | lb/tonne | |

| East | North | ||||||||

| MT-08-034 | 9+86E | 33+48S | 268 | -67 | 383.5 | 437.9 | 54.4 | 0.69 | 13.8 |

| Including | 383.3 | 411.3 | 28.0 | 1.32 | 26.4 | ||||

| Including | 397.8 | 402.6 | 4.8 | 6.13 | 122.6 | ||||

| MT-08-037 | 10+55E | 32+08S | 262 | -61 | 380.2 | 399.3 | 19.1 | 0.10 | 2.0 |

| Including | 396.2 | 399.3 | 3.1 | 0.22 | 4.4 | ||||

| MT-08-041 | 11+48E | 34+75S | 277 | -51 | 557.8 | 564.8 | 7.0 | 0.13 | 2.6 |

| MT-08-047 | 12+42E | 32+97S | 259 | -46 | 616.3 | 626.3 | 10.0 | 2.24 | 44.8 |

| Including | 619.3 | 622.3 | 3.0 | 3.20 | 64.0 | ||||

The true width of the mineralized sections has not yet been determined.

The equivalent uranium values were generated by the Gamma probe.

HolesMT-08-062andMT-08-068, drilled to an approximate depth of -450 m about 190 m north of the heart of theMT-34zone, returned interesting results, with respective intersections of1.86% eU3O8over 3.1m (including 2.3% eU3O8over 2.3m)and0.05%eU3O8over 1.39m. In the depth extension, holeMT-08-058(-530 m) returned a notable intersection of0.03%eU3O8 over 19.3m, including 0.13% U3O8 over 1.6m. HoleMT-08-069(-580 m) returned0.19%eU3O8 over 1.0m. (The hole pierce points and results can be seen on longitudinal section on the Company’s website atwww.stratecoinc.com).

HoleMT-08-105intersected0.06%eU3O8 over 3.5metresand HoleMT-08-107intersected0.02%eU3O8 over 7.1 metres,including 0.10% eU3O8over0.9metres.

Finally, six holes were drilled in theMT-34zone extensions, particularly the southern extension. The best hole wasMT-08-083, which returned 0.16%eU3O8 over 7.7metres, including 0.37% eU3O8 over 1.2metres. Drilling ended on December 5, 2008.

With the exception of HoleMT-08-062, these holes were not part of the resource estimate as of July 25, 2008 (See followingItem 2 A.1, sub-section entitled:TECHNICAL REPORTS).

As of April, 2009, the 30,000-metre exploration drilling program which started in February 2009 had already resulted in the discovery of two new mineralized zones on the Company’s MATOUSH PROJECT.

HoleMT-006, drilled in April 2009, is located on section 46+00S, 1.0 km south of theMT-34core zone. The new mineralized zone was intersected by HoleMT-09-006, which returned an 8.9 -metre intersection grading 0.21% eU3O8, including 1.1 metres at 0.96% eU3O8. This intersection is strongly altered in fuschite with the presence of pitchblende and uranophanes, and is similar in size, grade and alteration to intersections near theMT-34andMT-22core zones.

21

Hole | Collar | Az. | Angle (º) | From (m) | To | Vertical | Length | eU3O8 | |

| East | North | (º) | (m) | Depth (m) | (m)* | (%) | |||

| MT-09-006 | 11+01E | 43+92S | 249 | -64 | 601.0 | 609.9 | 555 | 8.9 | 0.21 |

| Including | 603.0 | 604.1 | 1.1 | 0.96 | |||||

*Core length

The true width of the mineralized sections has not yet been determined.

The equivalent uranium grades are obtained using a spectral probe.

As of the end of May 2009, the Company resumed exploration drilling campaign that had been halted temporarily at the end of April 2009 for the spring break-up. This campaign was part of the 30,000-metre exploration drilling program which started in February 2009, on the Company’s wholly-owned MATOUSH PROPERTY.

MT-006 ZONE

Drilling continued with one of two drills, in HoleMT-09-011which was interrupted at a depth of 180 metres and is located on the newMT-006zone discovered in April 2009. TheMT-006zone is located on section 46+00S, 1.0 km south of theMT-34core zone. HoleMT-09-006returned an8.9 -metre intersection grading 0.21%eU3O8including1.1 metres at 0.96% eU3O8. Thisintersection is strongly altered in fuschite with the presence of pitchblende anduranophanes and is similar in size, grade and alteration to intersections near theMT-34andMT-22core zones.

As for the second drill mobilized for geotechnical drilling as part of preliminary work for the underground drilling program, it went back to exploration drilling in the first week of June 2009.

Before going back to theMT-006zone, the drill made a stop in the sector of the high gradeMT-34lens, where holeMT-08-034had intersected1.32% eU3O8 on 28.0metresincluding6.13%eU3O8 on 4.8metres. Two strategic drill holes were carried out in order to expand already delineated mineral resources.

On theMT-34zone,indicatedmineral resourcesare estimated to total88,000 tonnes grading 0.97%U3O8containing1,890,000 poundsU3O8andinferred resourcesthat were estimated to total527,000 tonnes grading 0.55%U3O8containing6,350,000 poundsU3O8These results came from the NI 43-101resource estimateupdatedby Scott Wilson RPAin September 2008.

As of July 2009, one of the two drills in operation on the MATOUSH PROPERTY, wholly-owned by the Company, had been assigned to theMT-34zone area. Due to the high grades obtained in HoleMT-34(1.36% U3O8 over 27.50 m including 6.03% U3O8 over 4.80 m) relative to the other grades and thicknesses for the zone, the influence of HoleMT-34in the September 2008 resource estimate done by Scott Wilson RPA was voluntarily limited. Furthermore, because a 50 m x 70 m drill grid was used in the area of HoleMT-34in 2008, this resource could not be categorized as anindicated resource.

The four holes drilled in June and the fifth hole allowed the totalMT-34zone resource to be increased and a portion of the resource to be upgraded frominferredtoindicated.

Scott Wilson RPA was retained to prepare an update of the resource estimate for theMT-34zone. The memorandum is entitled:Matoush Mineral Resources Update, dated September 18, 2009 prepared by David A. Ross, M.Sc. P. Geo of Scott Wilson RPA and is further detailed inItem 2 A.1, sub-section entitled:TECHNICAL REPORTS

Four holes (MT-09-012,014,016and019) were drilled in the upper part of theMT-34zone in June 2009. Three of the four holes intersected high grades over considerable intervals.

HoleMT-09-019, with a pierce point in the upper part of theACF-4near the contact with the CBF, 35 m north of HoleMT-08-051(0.40% eU3O8 over 5.1 m), intersected 0.26%eU3O8 over 14.1metres, including a section of0.95%eU3O8 over 2.8m. HoleMT-09-017was drilled on the same section, but was abandoned due to excessive deviation. HoleMT-09-014returned an intersection of0.08%eU3O8over 5.1m. This hole lies at the lower limit of theMT-34zone. HoleMT-09-020was drilled to test the extension of HoleMT-08-034up dip from theMT-34zone

22

in the direction of the upper part of theACF-4.Another hole was planned on theMT-34zone at a vertical depth of -470 m between holesMT-08-047andMT-08-055, alongside theMT-34zone in an area where no resources were estimated.

| Hole | Collar | Az. (º) | Angle (º) | From (m) | To (m) | Vert. Depth (m) | Length (m)* | eU3O8 (%) | |

| Easting | Northing | ||||||||

| MT-09-012 | 12+18E | 34+76S | 286.5 | -47.6 | 507.0 | 532.7 | 383.4 | 25.7 | 0.61 |

| including | 509.9 | 517.3 | 383.4 | 7.4 | 1.30 | ||||

| MT-09-014 | 12+54E | 33+72S | 273 | -48.2 | 554.5 | 559.6 | 405.8 | 5.1 | 0.08 |

| MT-09-016 | 12+20E | 34+76S | 287.5 | -45.9 | 506.0 | 532.9 | 376.8 | 26.9 | 0.42 |

| including | 507.9 | 520.8 | 376.8 | 12.9 | 0.66 | ||||

| including | 508.2 | 509.5 | 376.8 | 1.3 | 2.41 | ||||

| MT-09-019 | 12+09E | 34+76S | 287.5 | -45.6 | 486.9 | 501.0 | 345.4 | 14.1 | 0.25 |

| including | 495.1 | 497.9 | 345.4 | 2.8 | 0.95 | ||||

*Core length

The true width of the mineralized sections has not yet been determined.

The equivalent uranium grades are obtained using a spectral probe.

All exploration drill holes results of 2009 and longitudinal sections can be seen on the company’s website atwww.stratecoinc.com.

The drill results for the first quarter of 2009 were promising, particularly south of theMT-34zone. HoleMT-09-006, drilled 1 km away from the heart of theMT-34zone on Section 46 + 00S, intersected a 8.9 -metre zone strongly altered in fuschite with the presence of pitchblende and uranophanes. This intersection graded0.27% U3O8over 9.5 metres, including 0.97% U3O8over 1.2metres.

The four completed holes (MT-09-011,013,015and018)all intercepted the Matoush fault, with anomalous uranium values.

In the second quarter, another eight holes were drilled in theMT-006area on a 100-metre grid to test the continuity of the HoleMT-09-006intersection. The best hole wasMT-09-009, drilled to a vertical depth of -600 metres along the presumed plunge ofMT-09-006, 100 metres away. It intersected0.11%U3O8 over 2.4metresat the level of the fault.

Early in June, one of the two drills in operation on the MATOUSH PROPERTY was assigned to theMT-34zone area. Due to the high grades obtained in HoleMT-08-034(1.36% U3O8 over 27.5 m including 6.03% U3O8 over 4.8 m) relative to the other grades and thicknesses for the zone, the influence of HoleMT-08-034in the September 2008 resource estimate done by Scott Wilson RPA was voluntarily limited.

Furthermore, because a 50 m x 70 m drill grid was used in the area ofMT-08-034in 2008, this resource could not be categorized as anindicated resource.

Four holes were drilled in the upper part of the MT-34 zone in June 2009. Three of the four holes intersected high grades over considerable intervals.

HoleMT-09-012, whose pierce point lies just a few metres from HoleMT-08-50due to strong deviation, returned an intersection of 0.69% U3O8 over 25.5 metres, including 1.44% U3O8 over 7.2 metres.

HoleMT-09-016, whose pierce point lies midway between holes MT-08-050 andMT-08-34, returned an intersection of 0.56% U3O8 over 25.8 metres, including 0.94% U3O8 over 12.5 metres, while HoleMT-08-050previously intersected 0.49% U3O8 over 21.3m, including 1.99% U3O8over 2.0m.

23

On or about the end of July 2009, the Company discovered a uranium high grade intersection in the extension of theMT-34lens.

In fact, holeMT-09-022has intersected 0.99% eU3O8over 30.6 metres including 5.98% eU3O8over 4.5 metres.

This drill hole, with a pierce point located on section 34+85S at a vertical depth of 456 metres in the extension on theMT-34lens, is one of the best holes drilled to date by the Company on its wholly-owned MATOUSH PROPERTY.

The pierce point ofMT-09-022is located outside of the resources estimated by Scott Wilson RPA published in September 2008 and as such its results are interesting.

Another drill hole was planned at the same elevation, 50 metres south ofMT-09-022, to fill in the gap between holesMT-09-022andMT-08-062located 100 metres apart.

The true width of the mineralized sections has not yet been determined.

Location of pierce point of HoleMT-09-022can be seen on theMT-34longitudinal section available on the Company’s website atwww.stratecoinc.com.

As of July, 2009, 20,000 metres of the planned 30,000 metres of exploration drilling in 2009 had been completed.

At the end of September 2009, the Company increased its 2009 surface exploration program from 30,000 metres to 35,000 metres of drilling.

In the third quarter of 2009, drilling continued steadily on the MATOUSH PROPERTY, with two drills in operation. One drill (1419) was dedicated to definition drilling on theMT-34zone to improve data quality in preparation for a new resource estimate. The second drill (1420) was essentially used for exploration drilling on the southern extension of theMT-34zone (widely-spaced holes).

The closely-spaced holes drilled on theMT-34zone returned very good results overall, confirming and increasing confidence in the geological continuity and high grades, as can be seen by the increase in theindicated resourceand grades in the new September 2009 update of the resource estimate.

The 2009 drilling program continued with two drills working on the property. One of these was assigned to systematic drilling on a 200-metre grid to locate new mineralized zones in the southern extension of theMT-34zone, in the upper part of theACF-4stratigraphic unit.

The Company plans to carry out 60,000 metres of surface drilling per year in 2010 and 2011, in parallel with underground exploration work. The results of the surface drilling program should allow the maximum capacity of the Matoush ore processing plant to be established.

In 2011, the Company plans to begin the environmental studies required for mill and tailings pond construction. These studies are required to obtain a mine construction permit.

In addition to the definition drilling, the results for the 12 exploration holes drilled to the south of theAM-15zone in theACF-3and south of theMT-34zone in the upperACF-4confirmed the new-zone discovery potential. Of the three holes drilled approximately 400 metres south of theAM-15zone in theACF-3(MT-09-30, 031, 032), HoleMT-09-030proved the most encouraging, with a mineralized intersection of3.9 metres grading 0.26%U3O8. The nine holes drilled in theACF-4over a distance of 1,800 metres along strike, relatively loosely spaced at about 200 metres, all intersected the Matoush fault and an alteration halo typical of the one around the mineralized zones. The three last holes (MT-09-035to038), drilled in virgin ground, proved the most interesting, with intersections of0.17% U3O8 over 2.0 metresin HoleMT-09-035and 0.48%U3O8 over 4.2 metresin HoleMT-09-036.

24

The 2009 drilling program continued, with two drills working on the property. One of these is assigned to systematic drilling on a 200-metre grid to locate new mineralized zones in the southern extension of theMT-34zone, in the upper part of theACF-4stratigraphic unit. The two most recent holes confirmed mineralization to the south. HoleMT-09-035, drilled 1.0 km south of the edge of the current mineral resources, intersected the mineralized zoneover2.9 metres grading 0.12%eU3O8,lying characteristically at the contact of the Matoush fault. Hole MT-09-036 wasdrilled 200 metres further south fromMT-09-035, and intersected a4.7 -metre section of mineralization grading0.26%eU3O8(see longitudinal sections atwww.stratecoinc.com).

These results confirm the very important potential for increasing the resource on the MATOUSH and ECLAT PROPERTIESover an 11.1 kmdistance along the Matoush fault, to the south of the mineralized envelope hosting the resources. As previously reported, two holes drilled 200 metres apart, last winter in the upper part of theACF-4(EC-09-05 and EC-09-06) more than 6 km south of HoleMT-09-036returned very good results (0.12% eU3O8 over 2.6 metres and 0.11% eU3O8 over 2.1 metres).

TECHNICAL REPORTS

Mineral Resource and Mineral Reserve Estimates

Cautionary Note to U.S. Investors concerning estimates of Measured and Indicated Resources.This section uses the terms “measured” and “indicatedresources”. We advise U.S. investors that while those terms are recognized and required by Canadian regulations, the U.S. Securities and Exchange Commission does not recognize them. U.S. investors are cautioned not to assume that any part or all of mineral deposits in these categories will ever be converted into reserves.

Cautionary Note to U.S. Investors concerning estimates of Inferred Resources. This section uses the term “inferred resources.”We advise U.S. investors that while this term is recognized and required by Canadian regulations, the U.S. Securities and Exchange Commission does not recognize it. “Inferred resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases.U.S. investors are cautioned not to assume that part or all of an inferred resource exists, or is economically or legally minable.

1. Mineral Resource Classification, Category and Definition

The Canadian Institute of Mining, Metallurgy and Petroleum (CIM) guideline for resource classification includes the following definitions which are pertinent to the classification of the Matoush Property resource:

AMineral Resourceis a concentration or occurrence of natural, solid, inorganic or fossilized organic material in or on the Earth’s crust in such form and quantity and of such a grade or quality that it has reasonable prospects for economic extraction. The location, quantity, grade, geological characteristics and continuity of a mineral resource are known, estimated or interpreted from specific geological evidence and knowledge.

AnInferred Mineral Resourceis that part of a mineral resource for which quantity and grade or quality can be estimated on the basis of geological evidence and limited sampling and reasonably assumed, but not verified, geological and grade continuity. The estimate is based on limited information and sampling gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes.

AnIndicated Mineral Resourceis that part of a mineral resource for which quantity, grade or quality, densities, shape and physical characteristics can be estimated with a level of confidence sufficient to allow the appropriate application of technical and economic parameters, to support mine planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration and testing information gathered through

25

appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough for geological and grade continuity to be reasonably assumed.

TheTechnical Report on the Mineral Resources Update for the Matoush Uranium Project Central Quebec, Canada, NI 43-101resource estimate completed by Scott Wilson Roscoe Postle Associates Inc. ("Scott Wilson RPA") on September 16, 2008, assessed the resources for the MATOUSH PROJECT of theAM-15,MT-22andMT-34zones. On September 18, 2008, the Company deposited on SEDAR, (www.sedar.com), this technical report prepared by Mr. R. Barry Cook, P.Eng. and Mr. David A. Ross, P.Geo.of Scott Wilson RPA, who are qualified persons pursuant to NI 43-101.

Scott Wilson RPA has updated the NI 43-101 Resource estimate for the MATOUSH PROJECT using drill hole data available as of July 25, 2008, at a cut-off grade of 0.05% U3O8,Indicated mineral resourceswere estimated to total250 thousand tonnes grading 0.68% U3O8containing 3.73 million pounds U3O8. Inferred mineral resources were estimated to total1.3 million tonnes grading 0.44% U3O8containing13.07 million poundsU3O8.The MineralResourcesare contained within three zones:AM-15,MT-22andMT-34.

This resource estimate showed, as of August 2008, with the data as of July 25, 2008, an increase of 300% from the last technical report pursuant to NI 43-101 dated September 27, 2007.

Scott Wilson RPA concluded that there is also potential for unconformity-type uranium deposits on the MATOUSH PROPERTY.

There are no mineral reserves estimated at MATOUSH PROJECT. See longitudinal section onwww.stratecoinc.com.

Table 1 - Mineral Resource Estimate for Matoush, July 25, 2008

| Tonnes | Grade | Pounds U3O8 | |

| (x 1,000) | (% U3O8) | (x 1,000) | |

| Indicated | |||

| AM-15 | 162 | 0.52 | 1,840 |

| MT-34 | 88 | 0.97 | 1,890 |

| Total Indicated | 250 | 0.68 | 3,730 |

| Inferred | |||

| AM-15 | 16 | 0.14 | 50 |

| MT-22 | 801 | 0.38 | 6,680 |

| MT-34 | 527 | 0.55 | 6,350 |

| Total Inferred | 1,344 | 0.44 | 13,070 |

Notes:

| 1. | CIM Definitions were followed for Mineral Resources. | |

| 2. | The cut-off grade of 0.05% U3O8was estimated using a price of US$55/lb and assumed operating costs. | |

| 3. | Wireframes at 0.05% U3O8and a minimum true thickness of 1.5 metres were used to constrain the grade interpolation. | |

| 4. | High U3O8grades were cut to 9% prior to compositing to two metre lengths | |

| 5. | Several blocks less than 0.05% U3O8were included for continuity or to expand the lenses to the minimum thickness. | |

| 6. | Totals may not sum correctly due to rounding. |

The Matoush drill holes included 257 diamond core holes totalling more than 98,000 m. A set of cross sections and plan views were interpreted to construct three-dimensional wireframe models at a cut-off grade of 0.05% U3O8, and a minimum true thickness of 1.5metres. High U3O8 values were cut to 9% U3O8 prior to compositing to two metres. Variogram parameters were interpreted from two metres composited U3O8 values. Block model U3O8 grades within the wireframe models were estimated by ordinary kriging. More than 98% of the U3O8 values in the drill hole database used in the grade estimate were derived from chemical analysis. The remaining values, from 27 of the most recent drill holes, were derived from gamma-probe data.

26

Classification into theIndicatedandInferredcategories was guided by the drill hole density, interpreted variogram ranges and the apparent continuity of the mineralized zones.

TheInferredcategory had a general drilling grid of approximately 50 metres by 50 metres up to 70 metres.

On September 18, 2009, Scott Wilson RPA has updated the NI 43-101-compliant resource estimate for the MATOUSH PROJECT based on drill results available as of September 1st, 2009 and using similar methods as applied in the previous estimate (Scott Wilson RPA, Sept. 2008). At a cut-off grade of 0.10% U3O8, the indicated mineral resources are now estimated at436,000 tonnesgrading0.78% U3O8containing 7.46 million poundsU3O8, and theinferred mineral resources are estimated at 1.16 million tonnes grading 0.50% U3O8containing 12.78 million poundsU3O8. These resources lie in the AM-15, MT-34 and MT-22 zones, and extend over a strike-length of 1.4 km. The Matoush structure has been traced 11 km to the south and 2.5 km to the north.