Filed by Alamos Gold Inc.

Pursuant to Rule 425 under the Securities Act of 1933, as amended

Subject Company: Aurizon Mines Ltd.

Commission File Number: 333-186004

Date: January 15, 2013

Offer for Aurizon

January 14, 2013

ALAMOS GOLD INC.

Forward-Looking Statements and Disclaimers

Forward-Looking Statements

Certain statements contained in this presentation are forward-looking statements, including within the meaning of the United States Securities Exchange Act of 1934, as amended, and the rules and regulations promulgated thereunder. All statements other than statements of historical fact included herein, including, without limitation, statements regarding forecast gold production, gold grades, recoveries, waste-to-ore ratios, total cash costs, potential mineralization and reserves, exploration results, and future plans and objectives of Alamos Gold Inc. (“Alamos”), are forward-looking statements that involve various risks and uncertainties. These forward-looking statements include, but are not limited to, statements with respect to mining and processing of mined ore, achieving projected recovery rates, anticipated production rates and mine life, operating efficiencies, costs and expenditures, changes in mineral resources and conversion of mineral resources to proven and probable reserves, and other information that is based on forecasts of future operational or financial results, estimates of amounts not yet determinable and assumptions of management.

Exploration results that include geophysics, sampling, and drill results on wide g may not be indicative of the occurrence of a mineral deposit. Such results do not provide assurance that further work will establish sufficient grade, continuity, metallurgical characteristics and economic potential to be classed as a category of mineral resource. A mineral resource that is classified as “inferred” or “indicated” has a great amount of uncertainty as to its existence and economic and legal feasibility. It cannot be assumed that any or part of an “indicated mineral resource” or “inferred mineral resource” will ever be upgraded to a higher category of resource. Investors are cautioned not to assume that all or any part of mineral deposits in these categories will ever be converted into proven and probable reserves.

Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as “expects” or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “estimates” or “intends”, or stating that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved) are not statements of historical fact and may be “forward-looking statements”. Forward-looking statements are subject to a variety of risks and uncertainties that could cause actual events or results to differ from those reflected in the forward-looking statements.

There can be no assurance that forward-looking statements will prove to be accurate and actual results and future events could differ materially from those anticipated in such statements. Important factors that could cause actual results to differ materially from Alamos’ expectations include risks related to the offer, fluctuations in the value of the consideration; integration issues; the effect of the offer on the market price of Alamos common shares; the exercise of dissent rights in connection with a compulsory acquisition or subsequent acquisition transaction; the liquidity of the Aurizon Mines Ltd. (“Aurizon”) common shares; risks associated with Aurizon becoming a majority-owned subsidiary of Alamos; differences in Aurizon common shareholder interests; the reliability of the information regarding Aurizon; change of control provisions; risks associated with obtaining governmental and regulatory approvals; failure to maintain effective internal controls; the liquidity of Alamos common shares on the New York Stock Exchange; and the effect of the offer on non-Canadian holders of Aurizon common shares, and risks related to the on-going business of Alamos, including risks related to international operations; the actual results of current exploration activities; conclusions of economic evaluations and changes in project parameters as plans continue to be refined as well as future prices of gold and silver, as well as those risk factors described in the section entitled “Risk Factors Related to the Offer” that is included in Alamos’ take-over bid circular dated January 14, 2013 and in the section entitled “Risk Factors” that is included in Alamos’ annual information form dated March 29, 2012. Although Alamos has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements.

Disclaimers

This presentation is presented solely in conjunction with Alamos’ Registration Statement on Form F-10 (the “Registration Statement”) and Tender Offer Statement on Schedule TO (the “Tender Offer Statement”) as filed with the United States Securities and Exchange Commission (the “SEC”). The securities registered pursuant to the Registration Statement are not offered for sale in any jurisdiction in which such offer or sale is not permitted. You should only rely on the information contained in the offer and circular (the “Offer and Circular”) in each of the Registration Statement and the Tender Offer Statement. The information included in this presentation is only a summary and you should read the entire Offer and Circular carefully.

This presentation does not constitute an offer to buy or the solicitation of an offer to sell any of the securities of Alamos or Aurizon

Each of Alamos and Aurizon prepare its disclosure in accordance with the requirements of securities laws in effect in Canada, which differ from the requirements of U.S. securities laws. Terms relating to mineral resources in this presentation are defined in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects under the guidelines set out in the Canadian Institute of Mining, Metallurgy, and Petroleum Standards on Mineral Resources and Mineral Reserves. The SEC permits mining companies, in their filings with the SEC, to disclose only those mineral deposits that a company can economically and legally extract or produce. Alamos and Aurizon may use certain terms, such as “measured mineral resources”, “indicated mineral resources”, “inferred mineral resources” and “probable mineral reserves” that the SEC does not recognize (these terms may be used in this presentation and are included in the public filings of each of Alamos and Aurizon, which have been filed with the SEC and the securities commissions or similar authorities in Canada).

2 |

|

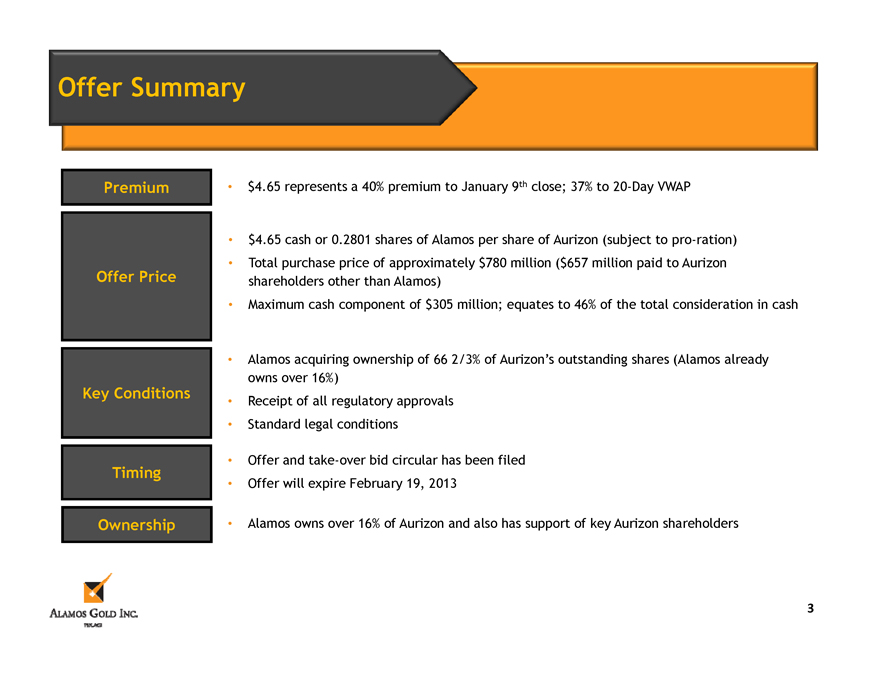

Offer Summary

Premium $4.65 represents a 40% premium to January 9th close; 37% to 20-Day VWAP

$4.65 cash or 0.2801 shares of Alamos per share of Aurizon (subject to pro-ration)

Total purchase price of approximately $780 million ($657 million paid to Aurizon

Offer Price shareholders other than Alamos)

Maximum cash component of $305 million; equates to 46% of the total consideration in cash

Alamos acquiring ownership of 66 2/3% of Aurizon’s outstanding shares (Alamos already

owns over 16%)

Key Conditions Receipt of all regulatory approvals

Standard legal conditions

Offer and take-over bid circular has been filed

Timing

Offer will expire February 19, 2013

Ownership Alamos owns over 16% of Aurizon and also has support of key Aurizon shareholders

3 |

|

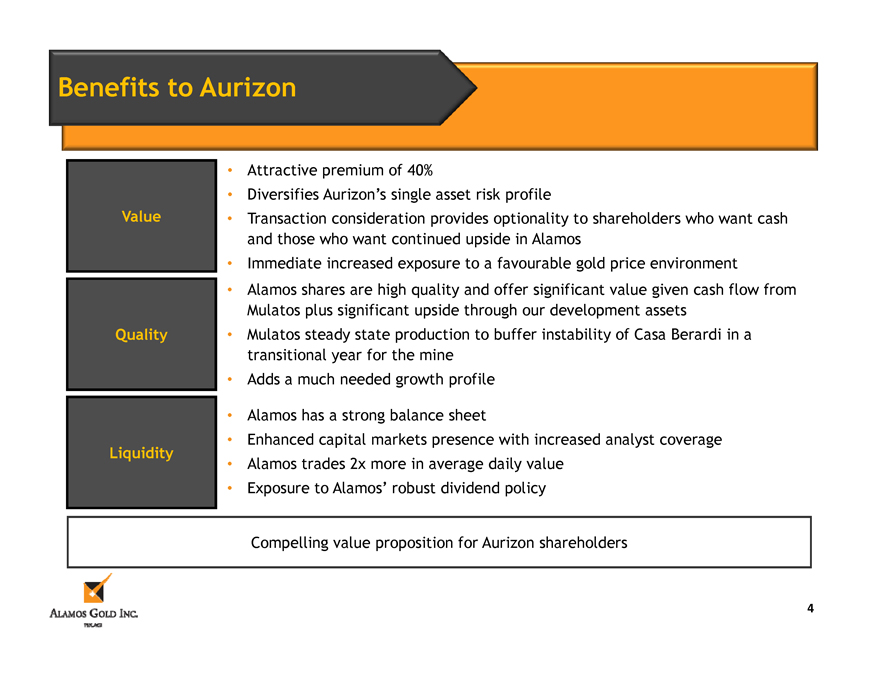

Benefits to Aurizon

Attractive premium of 40%

Diversifies Aurizon’s single asset risk profile

Value Transaction consideration provides optionality to shareholders who want cash

and those who want continued upside in Alamos

Immediate increased exposure to a favourable gold price environment

Alamos shares are high quality and offer significant value given cash flow from

Mulatos plus significant upside through our development assets

Quality Mulatos steady state production to buffer instability of Casa Berardi in a

transitional year for the mine

Adds a much needed growth profile

Alamos has a strong balance sheet

Enhanced capital markets presence with increased analyst coverage

Liquidity Alamos trades 2x more in average daily value

Exposure to Alamos’ robust dividend policy

Compelling value proposition for Aurizon shareholders

4 |

|

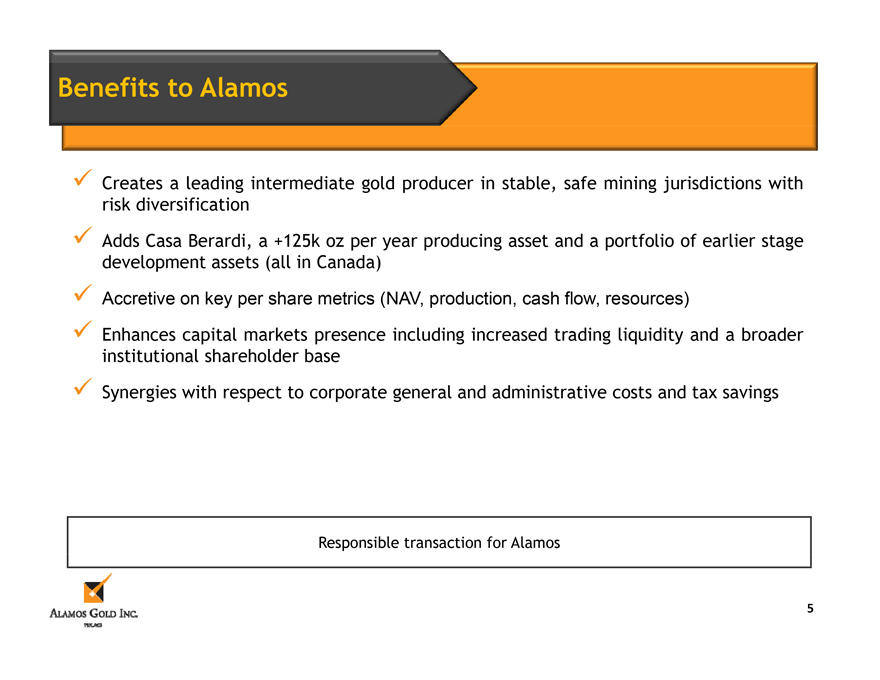

Benefits to Alamos

Creates a leading intermediate gold producer in stable, safe mining jurisdictions with risk diversification Adds Casa Berardi, a +125k oz per year producing asset and a portfolio of earlier stage development assets (all in Canada)

Accretive on key per share metrics (NAV, production, cash flow, resources)

Enhances capital markets presence including increased trading liquidity and a broader institutional shareholder base Synergies with respect to corporate general and administrative costs and tax savings

Responsible transaction for Alamos

5 |

|

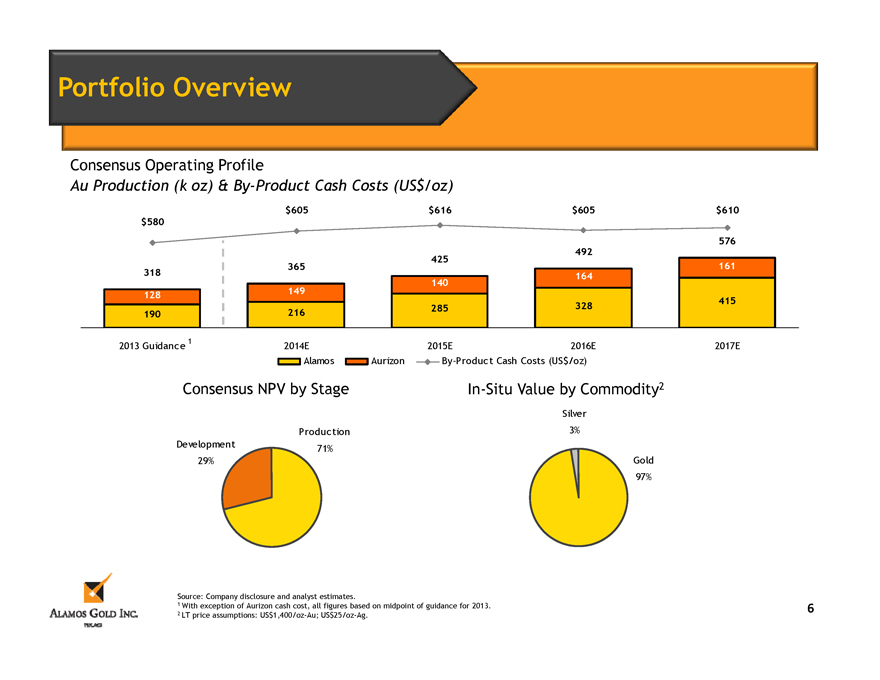

Portfolio Overview

Consensus Operating Profile

Au Production (k oz) & By-Product Cash Costs (US$/oz)

$605 $616 $605 $610

$580

576

492

425

365 161

318 164

140

128 149

415

190 216 285 328

2013 Guidance 1 2014E 2015E 2016E 2017E

Alamos Aurizon By-Product Cash Costs (US$/oz)

Consensus NPV by Stage In-Situ Value by Commodity2

Silver

Production 3%

Development 71%

29% Gold

97%

Source: Company disclosure and analyst estimates.

1 With exception of Aurizon cash cost, all figures based on midpoint of guidance for 2013.

2 LT price assumptions: US$1,400/oz-Au; US$25/oz-Ag.

6 |

|

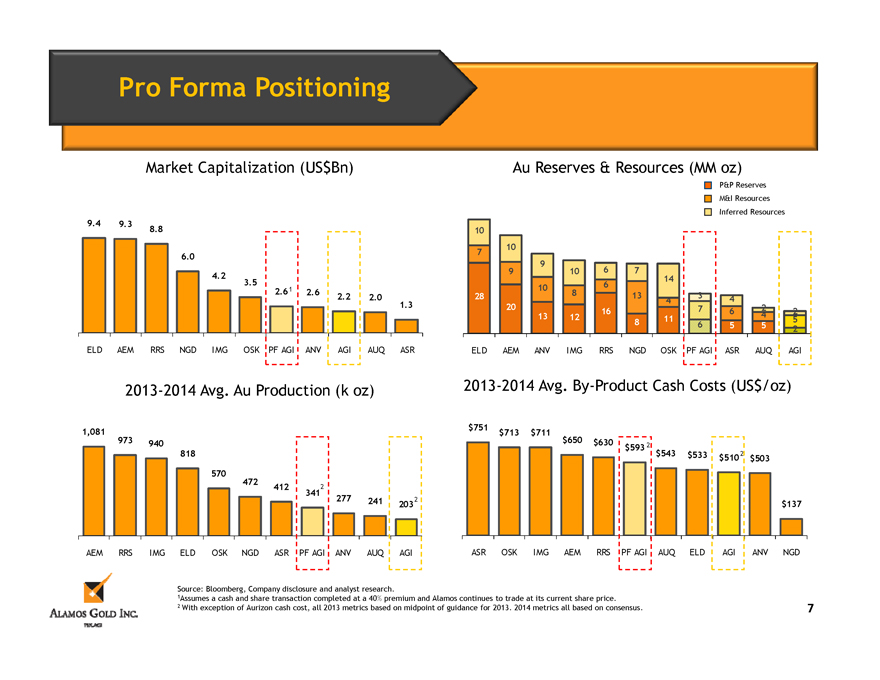

Pro Forma Positioning

Market Capitalization (US$Bn)

9.4 9.3

10.0 8.8

8.0 6.0

6.0 4.2

3.5

4.0 2.61 2.6 22. 20.

1.3

2.0

-

ELD AEM RRS NGD IMG OSK PF AGI ANV AGI AUQ ASR

Au Reserves & Resources (MM oz)

P&P Reserves

M&I Resources

Inferred Resources

10

7 |

| 10 |

9

9 10 6 7

6 14

10 8

28 13 4 3 4

20 13 12 16 11 7 6 4 2 2

8 |

| 6 55 2 5 |

ELD AEM ANV IMG RRS NGD OSK PF AGI ASR AUQ AGI

2013-2014 Avg. Au Production (k oz)

1,081

973 940

818

570

600 472 412 2

341

277 241 2032

AEM RRS IMG ELD OSK NGD ASR PF AGI ANV AUQ AGI

2013-2014 Avg. By-Product Cash Costs (US$/oz)

$751 $713 $711

$650 $630 $593 2

$543 $533 $510 2 $503

$137

ASR OSK IMG AEM RRS PF AGI AUQ ELD AGI ANV NGD

Source: Bloomberg, Company disclosure and analyst research.

1Assumes a cash and share transaction completed at a 40% premium and Alamos continues to trade at its current share price.

2 With exception of Aurizon cash cost, all 2013 metrics based on midpoint of guidance for 2013. 2014 metrics all based on consensus.

7 |

|

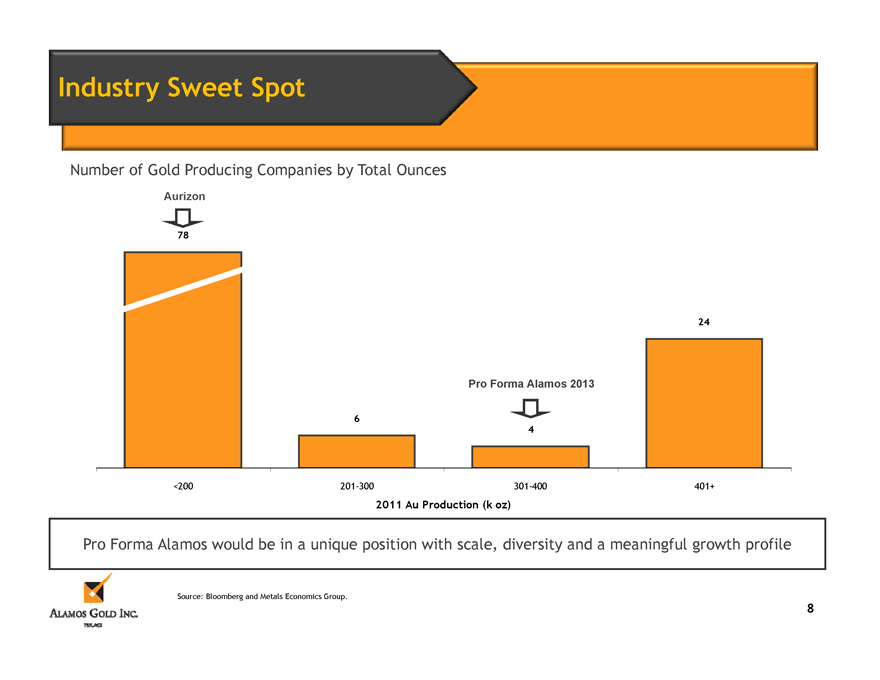

Industry Sweet Spot

Number of Gold Producing Companies by Total Ounces

Aurizon

78

24

Pro Forma Alamos 2013

6 |

|

4 |

|

<200 201-300 301-400 401+

2011 Au Production (k oz)

Pro Forma Alamos would be in a unique position with scale, diversity and a meaningful growth profile

Source: Bloomberg and Metals Economics Group.

8 |

|

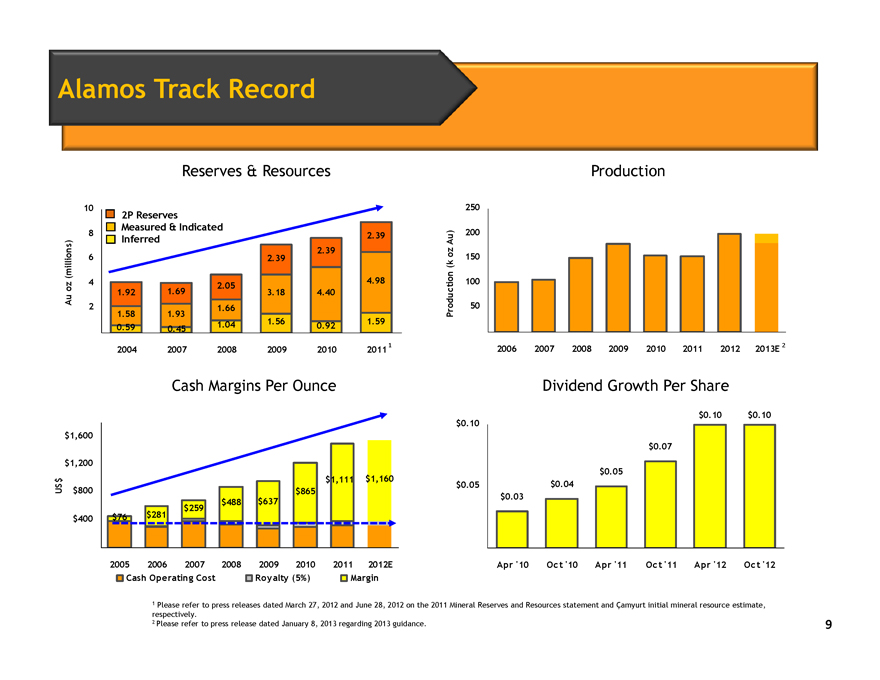

Alamos Track Record

Reserves & Resources

10

2P Reserves

Measured & Indicated

8 |

| Inferred 2.39 |

2.39

(millions) 6 2.39

oz 4 2.05 4.98

1.92 1.69 3.18 4.40

Au 2 1.66

1.58 1.93

0.59 0.45 1.04 1.56 0.92 1.59

2004 2007 2008 2009 2010 2011 1

Production

250

Au) 200

oz 150

(k

uction 100

Prod 50

2006 2007 2008 2009 2010 2011 2012 2013E 2

Cash Margins Per Ounce

$1,600

$1,200

$ $1,111 $1,160

US $800 $865

$259 $488 $637

$400 $76 $281

2005 2006 2007 2008 2009 2010 2011 2012E

Cash Operating Cost Royalty (5%) Margin

Dividend Growth Per Share

$ 0.10 $ 0.10

$ 0.10

$ 0.07

$ 0.05

$ 0.05 $ 0.04

$ 0.03

Apr ‘10 Oct ‘10 Apr ‘11 Oct ‘11 Apr ‘12 Oct ‘12

1 Please refer to press releases dated March 27, 2012 and June 28, 2012 on the 2011 Mineral Reserves and Resources statement and Çamyurt initial mineral resource estimate, respectively.

2 |

| Please refer to press release dated January 8, 2013 regarding 2013 guidance. |

9

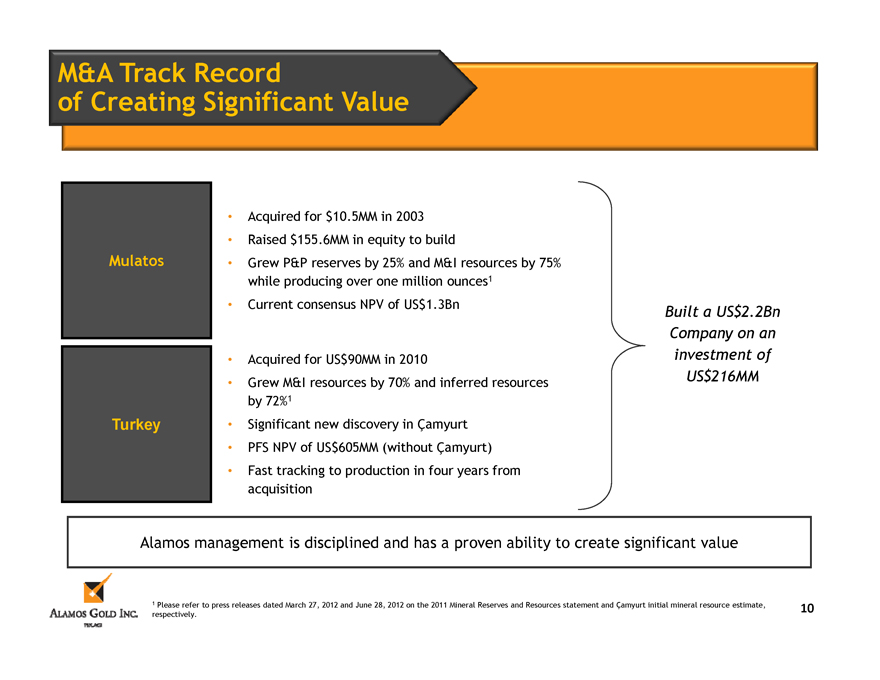

M&A Track Record of Creating Significant Value

Mulatos

Acquired for $10.5MM in 2003 Raised $155.6MM in equity to build

Grew P&P reserves by 25% and M&I resources by 75% while producing over one million ounces1 Current consensus NPV of US$1.3Bn

Turkey

Acquired for US$90MM in 2010

Grew M&I resources by 70% and inferred resources by 72%1 Significant new discovery in Çamyurt PFS NPV of US$605MM (without Çamyurt) Fast tracking to production in four years from acquisition

Built a US$2.2Bn Company on an investment of US$216MM

Alamos management is disciplined and has a proven ability to create significant value

1 Please refer to press releases dated March 27, 2012 and June 28, 2012 on the 2011 Mineral Reserves and Resources statement and Çamyurt initial mineral resource estimate, respectively.

10

Transaction Summary

Creates a leading intermediate gold producer

Two producing mines in safe jurisdictions

Robust, near-term growth pipeline

Larger, more liquid investment with increased cash flow

Strong balance sheet with no hedging

Continued basis for a strong dividend policy

11

Jo Mira Clodman

Vice President, Investor Relations 416.368.9932 x 401 jmclodman@alamosgold.com

12

ALAMOS GOLD INC.

Appendix:

Supplemental Materials

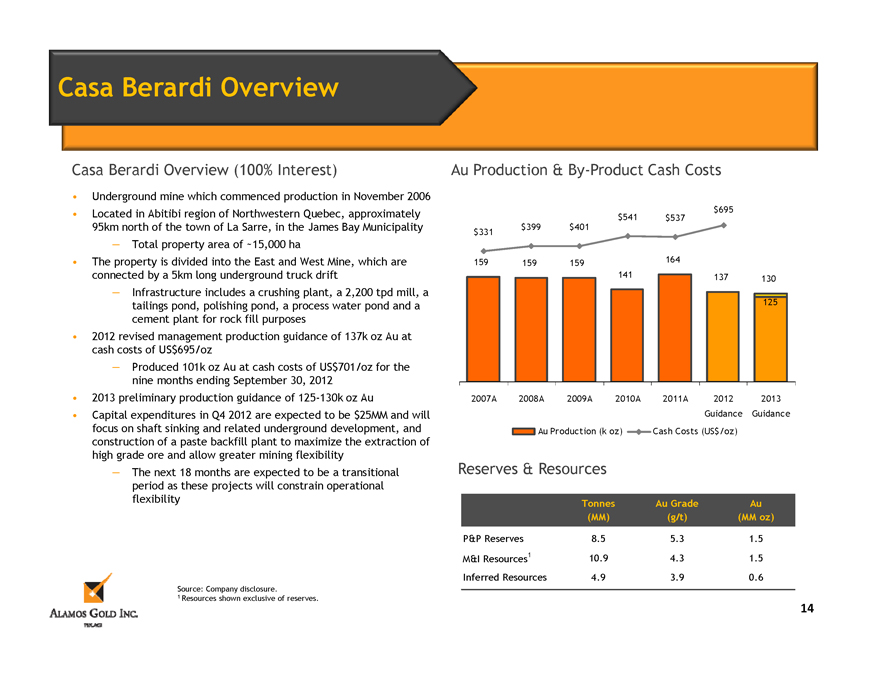

Casa Berardi Overview

Casa Berardi Overview (100% Interest)

Underground mine which commenced production in November 2006

Located in Abitibi region of Northwestern Quebec, approximately 95km north of the town of La Sarre, in the James Bay Municipality

– Total property area of ~15,000 ha

The property is divided into the East and West Mine, which are connected by a 5km long underground truck drift

– Infrastructure includes a crushing plant, a 2,200 tpd mill, a tailings pond, polishing pond, a process water pond and a cement plant for rock fill purposes

2012 revised management production guidance of 137k oz Au at cash costs of US$695/oz

– Produced 101k oz Au at cash costs of US$701/oz for the nine months ending September 30, 2012

2013 preliminary production guidance of 125-130k oz Au

Capital expenditures in Q4 2012 are expected to be $25MM and will focus on shaft sinking and related underground development, and construction of a paste backfill plant to maximize the extraction of high grade ore and allow greater mining flexibility

– The next 18 months are expected to be a transitional period as these projects will constrain operational flexibility

Source: Company disclosure.

1 Resources shown exclusive of reserves.

Au Production & By-Product Cash Costs

$695

$541 $537

$331 $399 $401

159 159 159 164

141 137 130

125

2007A 2008A 2009A 2010A 2011A 2012 2013

Guidance Guidance

Au Production (k oz) Cash Costs (US$/oz)

Reserves & Resources

Tonnes Au Grade Au

(MM) (g/t) (MM oz)

P&P Reserves 8.5 5.3 1.5

M&I Resources1 10.9 4.3 1.5

Inferred Resources 4.9 3.9 0.6

14

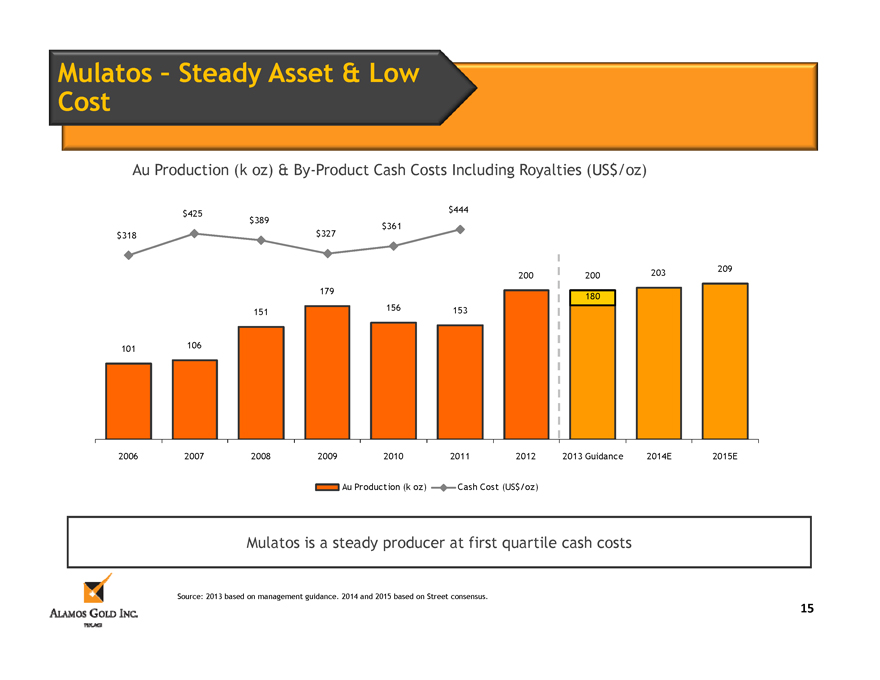

Mulatos – Steady Asset & Low Cost

Au Production (k oz) & By-Product Cash Costs Including Royalties (US$/oz)

$425 $444

$389 $361

$318 $327

200 200 203 209

179 180

151 156 153

101 106

2006 2007 2008 2009 2010 2011 2012 2013 Guidance 2014E 2015E

Au Production (k oz) Cash Cost (US$/oz)

Mulatos is a steady producer at first quartile cash costs

Source: 2013 based on management guidance. 2014 and 2015 based on Street consensus.

15

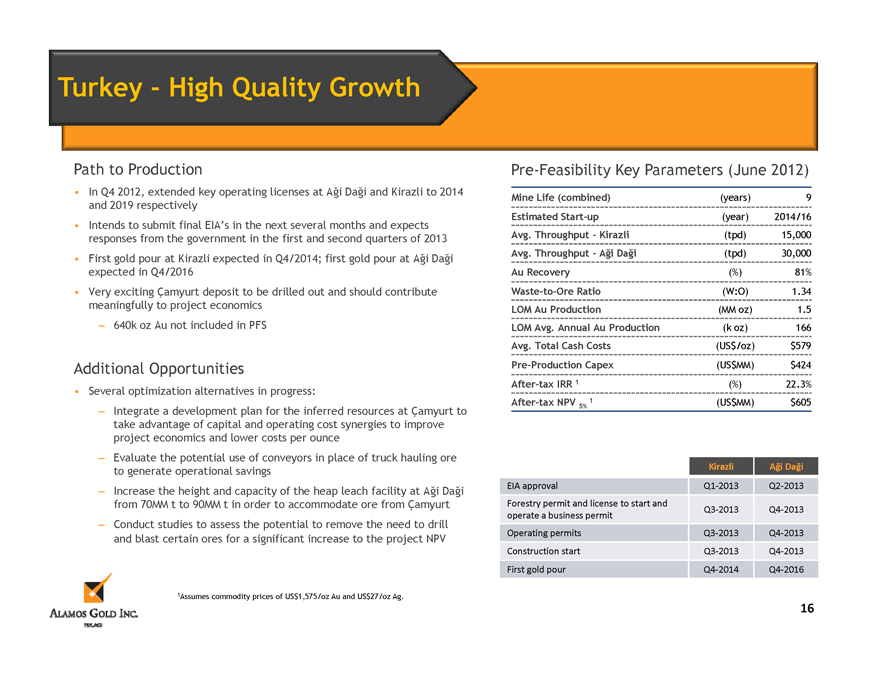

Turkey - High Quality Growth

Path to Production

In Q4 2012, extended key operating licenses at Aği Daği and Kirazli to 2014

and 2019 respectively

Intends to submit final EIA’s in the next several months and expects

responses from the government in the first and second quarters of 2013

First gold pour at Kirazli expected in Q4/2014; first gold pour at Aği Daği

expected in Q4/2016

Very exciting Çamyurt deposit to be drilled out and should contribute

meaningfully to project economics

– 640k oz Au not included in PFS

Additional Opportunities

Several optimization alternatives in progress:

– Integrate a development plan for the inferred resources at Çamyurt to take advantage of capital and operating cost synergies to improve project economics and lower costs per ounce

– Evaluate the potential use of conveyors in place of truck hauling ore to generate operational savings

– Increase the height and capacity of the heap leach facility at Aği Daği from 70MM t to 90MM t in order to accommodate ore from Çamyurt

– Conduct studies to assess the potential to remove the need to drill and blast certain ores for a significant increase to the project NPV

Pre-Feasibility Key Parameters (June 2012)

Mine Life (combined) (years) 9

Estimated Start-up (year) 2014/16

Avg. Throughput - Kirazli (tpd) 15,000

Avg. Throughput - Aği Daği (tpd) 30,000

Au Recovery (%) 81%

Waste-to-Ore Ratio (W:O) 1.34

LOM Au Production (MM oz) 1.5

LOM Avg. Annual Au Production (k oz) 166

Avg. Total Cash Costs (US$/oz) $579

Pre-Production Capex (US$MM) $424

After-tax IRR 1 (%) 22.3%

(US$MM) After-tax NPV 5% 1 $605

Kirazli AğiDaği

EIA approval Q1-2013 Q2-2013

Forestry permit and license to start and

Q3-2013 Q4-2013

operate a business permit

Operating permits Q3-2013 Q4-2013

Construction start Q3-2013 Q4-2013

First gold pour Q4-2014 Q4-2016

1Assumes commodity prices of US$1,575/oz Au and US$27/oz Ag.

16