Filed by Alamos Gold Inc.

Pursuant to Rule 425 under the Securities Act of 1933, as amended

Subject Company: Aurizon Mines Ltd.

Commission File Number: 333-186004

Date: January 29, 2013

ALAMOS GOLD INC.

January 2013 Corporate Presentation

Forward-Looking Statements and Disclaimer

Forward-Looking Statements

Certain statements contained in this presentation are forward-looking statements, including within the meaning of the United States Securities Exchange Act of 1934, as amended, and the rules and regulations promulgated thereunder. All statements other than statements of historical fact included herein, including, without limitation, statements regarding forecast gold production, gold grades, recoveries, waste-to-ore ratios, total cash costs, potential mineralization and reserves, exploration results, and future plans and objectives of Alamos Gold Inc. (“Alamos”), are forward-looking statements that involve various risks and uncertainties. These forward-looking statements include, but are not limited to, statements with respect to mining and processing of mined ore, achieving projected recovery rates, anticipated production rates and mine life, operating efficiencies, costs and expenditures, changes in mineral resources and conversion of mineral resources to proven and probable reserves, and other information that is based on forecasts of future operational or financial results, estimates of amounts not yet determinable and assumptions of management.

Exploration results that include geophysics, sampling, and drill results on wide spacings may not be indicative of the occurrence of a mineral deposit. Such results do not provide assurance that further work will establish sufficient grade, continuity, metallurgical characteristics and economic potential to be classed as a category of mineral resource. A mineral resource that is classified as “inferred” or “indicated” has a great amount of uncertainty as to its existence and economic and legal feasibility. It cannot be assumed that any or part of an “indicated mineral resource” or “inferred mineral resource” will ever be upgraded to a higher category of resource. Investors are cautioned not to assume that all or any part of mineral deposits in these categories will ever be converted into proven and probable reserves.

Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as “expects” or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “estimates” or “intends”, or stating that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved) are not statements of historical fact and may be “forward-looking statements”. Forward-looking statements are subject to a variety of risks and uncertainties that could cause actual events or results to differ from those reflected in the forward-looking statements.

There can be no assurance that forward-looking statements will prove to be accurate and actual results and future events could differ materially from those anticipated in such statements. Important factors that could cause actual results to differ materially from Alamos’ expectations include risks related to the offer, fluctuations in the value of the consideration; integration issues; the effect of the offer on the market price of Alamos common shares; the exercise of dissent rights in connection with a compulsory acquisition or subsequent acquisition transaction; the liquidity of the Aurizon Mines Ltd. (“Aurizon”) common shares; risks associated with Aurizon becoming a majority-owned subsidiary of Alamos; differences in Aurizon common shareholder interests; the reliability of the information regarding Aurizon; change of control provisions; risks associated with obtaining governmental and regulatory approvals; failure to maintain effective internal controls; the liquidity of Alamos common shares on the New York Stock Exchange; and the effect of the offer on non-Canadian holders of Aurizon common shares, and risks related to the on-going business of Alamos, including risks related to international operations; the actual results of current exploration activities; conclusions of economic evaluations and changes in project parameters as plans continue to be refined as well as future prices of gold and silver, as well as those risk factors described in the section entitled “Risk Factors Related to the Offer” that is included in Alamos’ take-over bid circular dated January 14, 2013 and in the section entitled “Risk Factors” that is included in Alamos’ annual information form dated March 29, 2012. Although Alamos has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements.

Disclaimers

This presentation is presented in conjunction with Alamos’ Registration Statement on Form F-10 (the “Registration Statement”) and Tender Offer Statement on Schedule TO (the “Tender Offer Statement”) as filed with the United States Securities and Exchange Commission (the “SEC”). The securities registered pursuant to the Registration Statement are not offered for sale in any jurisdiction in which such offer or sale is not permitted. You should only rely on the information contained in the offer and circular (the “Offer and Circular”) in each of the Registration Statement and the Tender Offer Statement. The information included in this presentation is only a summary and you should read the entire Offer and Circular carefully. The Registration Statement and the Tender Offer Statement are available on the SEC’s website at www.sec.gov.

This presentation does not constitute an offer to buy or the solicitation of an offer to sell any of the securities of Alamos or Aurizon.

Each of Alamos and Aurizon prepare its disclosure in accordance with the requirements of securities laws in effect in Canada, which differ from the requirements of U.S. securities laws. Terms relating to mineral resources in this presentation are defined in accordance with National Instrument 43-101—Standards of Disclosure for Mineral Projects under the guidelines set out in the Canadian Institute of Mining, Metallurgy, and Petroleum Standards on Mineral Resources and Mineral Reserves. The SEC permits mining companies, in their filings with the SEC, to disclose only those mineral deposits that a company can economically and legally extract or produce. Alamos and Aurizon may use certain terms, such as “measured mineral resources”, “indicated mineral resources”, “inferred mineral resources” and “probable mineral reserves” that the SEC does not recognize (these terms may be used in this presentation and are included in the public filings of each of Alamos and Aurizon, which have been filed with the SEC and the securities commissions or similar authorities in Canada).

All figures in US$ unless otherwise indicated.

3 |

ALAMOS GOLD INC.

TSX.AGI

We Expect Alamos to Remain…

• A leader in growing low-cost production

• A financially strong company

• A leader in delivering shareholder value

Since its inception, Alamos has focused successfully on these three areas. They will remain fundamental to the Company’s growth.

3 |

ALAMOS GOLD INC.

TSX.AGI

A Strong Company Positioned to Lead

• Low-cost, mid-tier gold producer

• Met production guidance and increased production by 32% in 2012 to 200,000 ounces at a cash operating cost (pre-5% royalty) of $360/oz

• Production guidance of 180,000-200,000 ounces Au in 2013; cash cost guidance of $415-$435/oz (pre-5% royalty)

• Mexico (Sonora State): own and operate the Mulatos Mine

• Acquired in 2003 for about $10 million; initial production in 2005

• Turkey (Çannakale): advanced-stage development projects

• Acquired in 2010 for $90 million; fast-tracking production for 2014

4 |

ALAMOS GOLD INC.

TSX.AGI

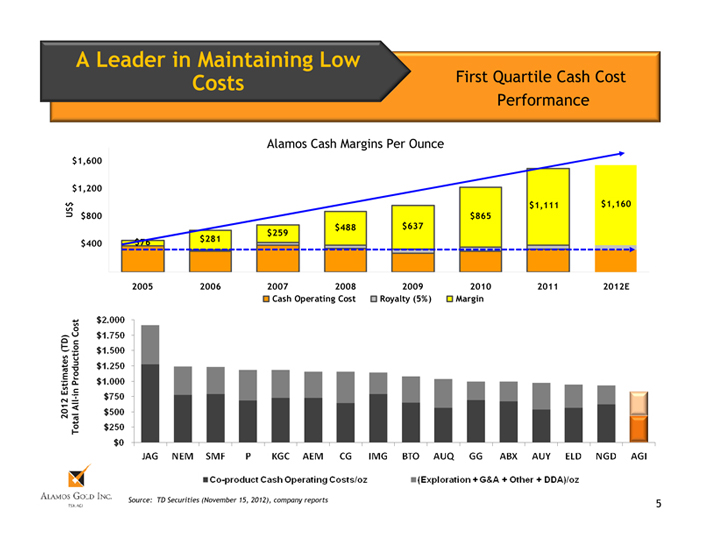

A Leader in Maintaining Low

Costs First Quartile Cash Cost Performance

Alamos Cash Margins Per Ounce

$1,600

$1,200

US $ $1,111 $1,160 $800 $865 $259 $488 $637

$76 $281 $400

2005 2006 2007 2008 2009 2010 2011 2012E Cash Operating Cost Royalty (5%) Margin

Cost (TD) Production Estimates in All-2012 Total

Source: TD Securities (November 15, 2012), company reports 5

Co-product Cash Operating Costs/oz

(Exploration+G&A+Other+DDA)/oz

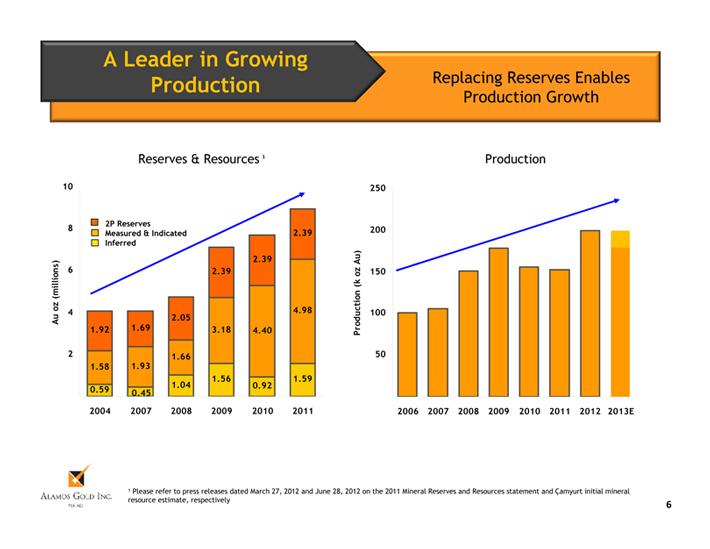

A Leader in Growing

Production Replacing Reserves Enables Production Growth

Reserves & Resources 1 Production

10 250

2P Reserves

8 | 200 |

Measured & Indicated 2.39 Inferred

2.39 Au)

6 | 2.39 oz 150 (k (millions) oz |

4 | 2.05 4.98 100 Au |

1.92 1.69 3.18 4.40 Production

2 | 1.66 50 |

1.58 1.93

1.56 1.59

1.04 0.92

0.59 0.45

2004 2007 2008 2009 2010 2011 2006 2007 2008 2009 2010 2011 2012 2013E

1 Please refer to press releases dated March 27, 2012 and June 28, 2012 on the 2011 Mineral Reserves and Resources statement and Çamyurt initial mineral resource estimate, respectively

Mexico: Mulatos Mine

Record Production in 2012

• Open-pit, heap leach operation (100% ownership)

• 17,000 tpd throughput capacity

• 500 tpd gravity mill for Escondida high-grade ore

• Commenced operation in Q1 2012

• Achieving design throughput and budgeted grades

• Large exploration package (30,325 ha /117 sq. miles)

• ~40,000 m drill program in 2012 (completed)

• +72,000 m drill program planned in 2013

7 |

ALAMOS GOLD INC.

TSX.AGI

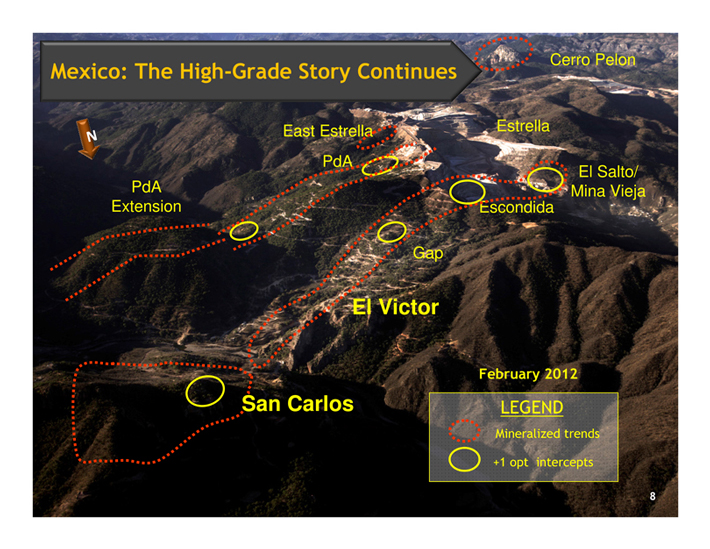

Cerro Pelon

Mexico: The High-Grade Story Continues

N East Estrella Estrella PdA

El Salto/ PdA Mina Vieja Extension Escondida

Gap

El Victor

February 2012

San Carlos LEGEND

Mineralized trends

+1 opt intercepts

8 |

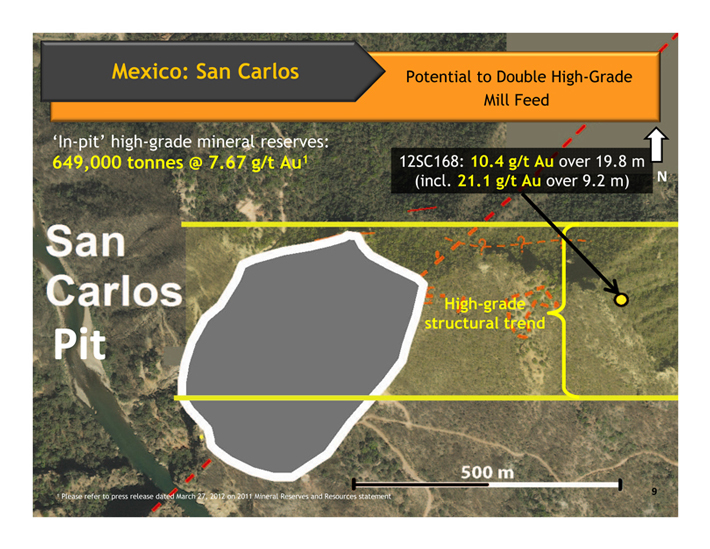

Mexico: San Carlos Potential to Double High-Grade Mill Feed

‘In-pit’ high-grade mineral reserves:

649,000 tonnes @ 7.67 g/t Au1 12SC168: 10.4 g/t Au over 19.8 m

(incl. 21.1 g/t Au over 9.2 m) N

High-grade structural trend

Pit

9

1 | Please refer to press release dated March 27, 2012 on 2011 Mineral Reserves and Resources statement |

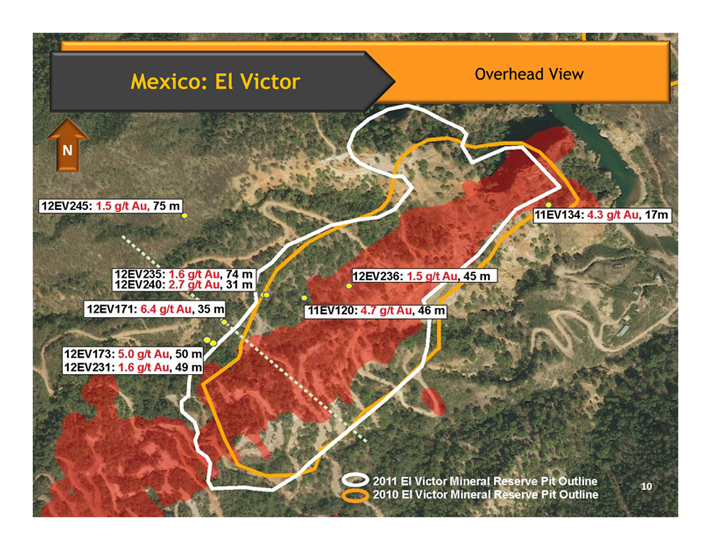

San carlos

Mexico:

El

Victor

Overhead

View

N

10

2011 EI victor Mineral Reserve Pit Outline

2010 EI Victor Mineral Reserve Pit Outline

12EV245: 1.5g/t Au, 75 m

11EV134: 4.3 g/t Au,17m

12EV235: 1.6 g/t Au, 74 m

12EV240: 2.7 g/t Au, 31m

12EV236: 1.5 g/t Au, 45m

12EV171: 6.4 g/t Au, 35m

12EV173: 5.0 g/t Au, 50m

12EV231: 1.6 g/t Au, 49m

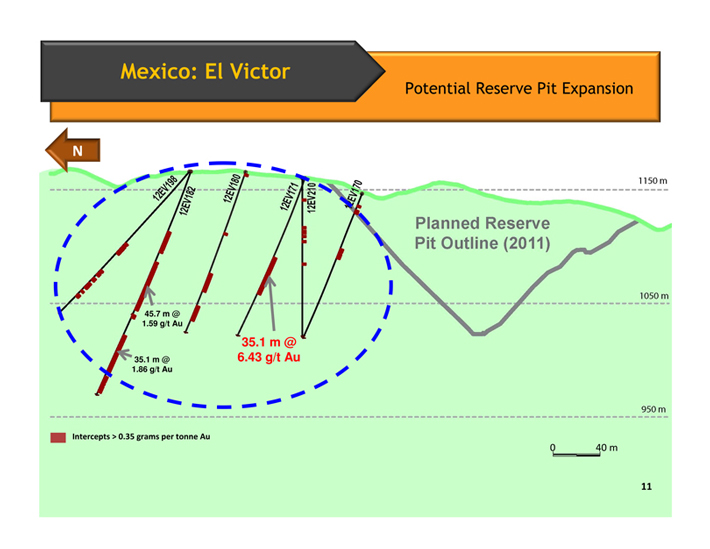

Mexico: El Victor

Potential Reserve Pit Expansion

N

45.7 m @ 1.59 g/t Au

35.1 m @

35.1 m @ 6.43 g/t Au

1.86 g/t Au

Intercepts > 0.35 grams per tonne Au

0 40 m

11

Planned Reserve Pit outline (2011)

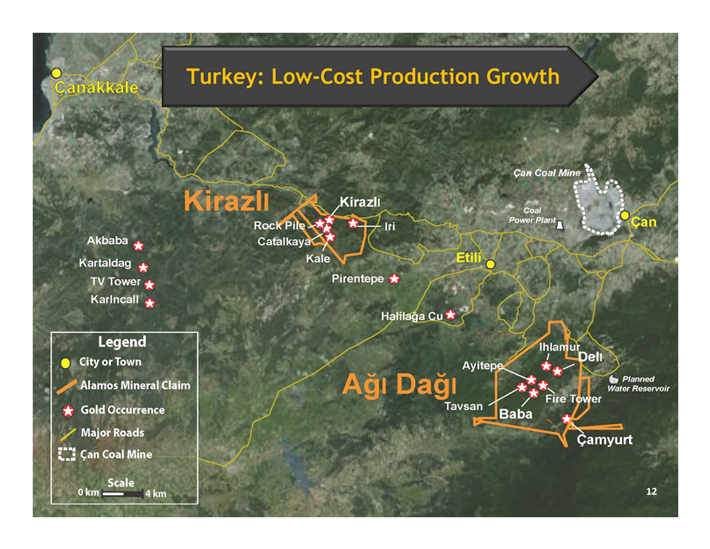

Turkey: Low-Cost Production Growth

12

Cannakkale

Akkaba

Kartaldag

TV Tower

Karincall

Legend

City or Town

Alamos Mineral Claim

Gold Occurrence

Major Roads

Can Coal Mine

Kirazli

Kirazli

Rock pile

Catalkaya

Kale

Iri

Pirentepe

Halilaga Cu

Agi Dagi

Can Coal Mine Coal Power plant Can

Ayitepe

Ihlamur deli

Baba

Tavsan

Fire Tower

Palnned Water Reservoir

Camyurt

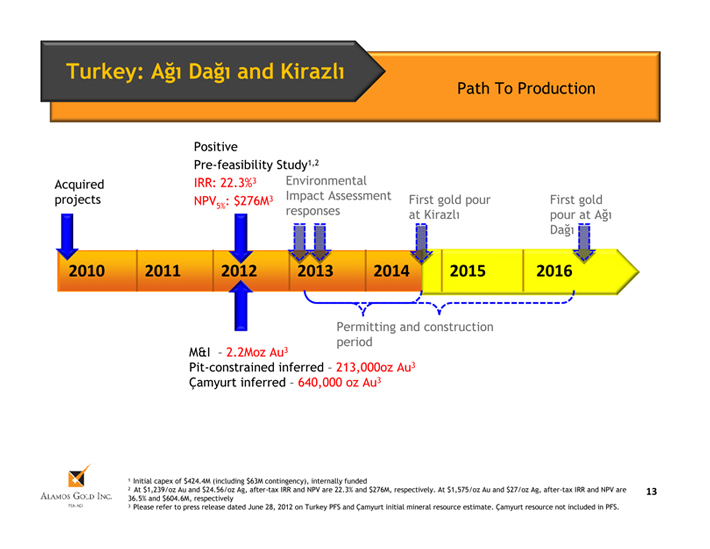

Turkey: Ağ? Dağ? and Kirazl?

Path To Production

Positive

Pre-feasibility Study1,2

Acquired IRR: 22.3%3 Environmental projects 3 Impact Assessment First gold pour First gold NPV : $276M

5% responses at Kirazl? pour at Ağ? Dağ?

2010 2011 2012 2013 2014 2015 2016

Permitting and construction M&I – 2.2Moz Au3 period Pit-constrained inferred – 213,000oz Au3 Çamyurt inferred – 640,000 oz Au3

1 | Initial capex of $424.4M (including $63M contingency), internally funded |

2 At $1,239/oz Au and $24.56/oz Ag, after-tax IRR and NPV are 22.3% and $276M, respectively. At $1,575/oz Au and $27/oz Ag, after-tax IRR and NPV are 13

36.5% and $604.6M, respectively

3 Please refer to press release dated June 28, 2012 on Turkey PFS and Çamyurt initial mineral resource estimate. Çamyurt resource not included in PFS.

ALAMOS GOLD INC.

TSX.AGI

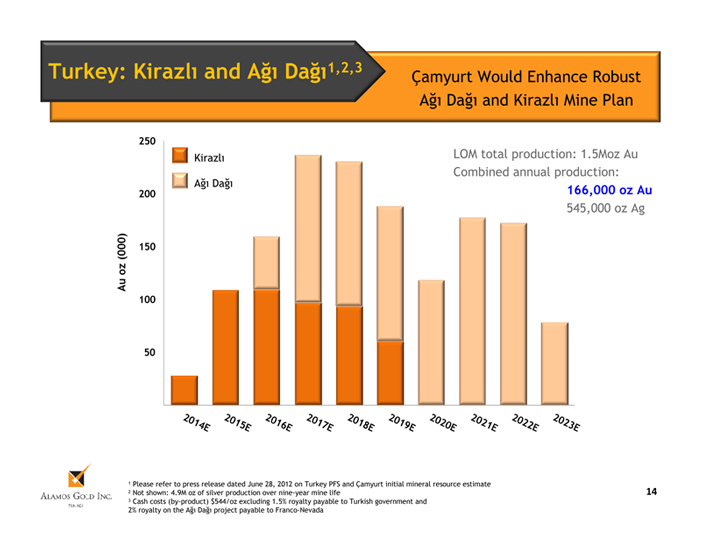

Turkey: Kirazl? and Ağ? Dağ?1,2,3

Çamyurt Would Enhance Robust Ağ? Dağ? and Kirazl? Mine Plan

250

Kirazl? LOM total production: 1.5Moz Au Combined annual production:

Ağ? Dağ?

200 166,000 oz Au

545,000 oz Ag

(000) 150 oz Au

100

50

1 Please refer to press release dated June 28, 2012 on Turkey PFS and Çamyurt initial mineral resource estimate

2 Not shown: 4.9M oz of silver production over nine-year mine life 14

3 Cash costs (by-product) $544/oz excluding 1.5% royalty payable to Turkish government and 2% royalty on the Ağ? Dağ? project payable to Franco-Nevada

2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E

ALAMOS GOLD INC.

TSX.AGI

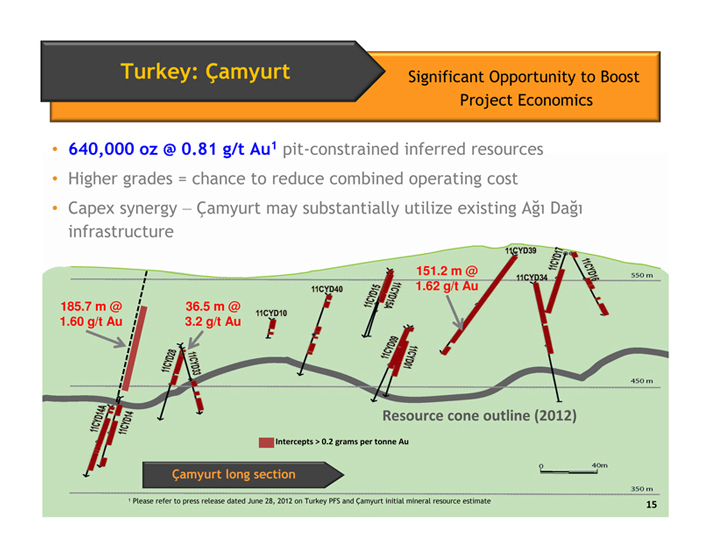

Turkey: Çamyurt Significant Opportunity to Boost Project Economics

• 640,000 oz @ 0.81 g/t Au1 pit-constrained inferred resources

• Higher grades = chance to reduce combined operating cost

• Capex synergy – Çamyurt may substantially utilize existing Ağ? Dağ? infrastructure

151.2 m @ 1.62 g/t Au 185.7 m @ 36.5 m @ 1.60 g/t Au 3.2 g/t Au

Resource cone outline (2012)

Intercepts > 0.2 grams per tonne Au

Çamyurt long section

1 Please refer to press release dated June 28, 2012 on Turkey PFS and Çamyurt initial mineral resource estimate

15

Succeeding in Turkey

An Alignment of Interests

Turkey Needs Mining

• Government calls mining a key to economic growth

• New Mining Law 2010; New Commercial Code 2012

• 2011 current account deficit 9.9% of GDP

• New investment system promotes foreign direct investment

• Tax incentive became law in June 2012

• Alamos expects to qualify for 80% reduction in corporate tax rate

• Corporate tax rate 4%, until savings cap of 40% of capex reached

• Earning our social license

• Generations have consumed substandard, unhealthy water (acidic; high alumina)

• Reservoir: process water for operations, potable water for communities

• Finalizing water protocol – planned commissioning in 2014; PFS Plan1: Capex $32M

16

ALAMOS GOLD INC.

TSX.AGI

A Financially Strong Company

St Robust, Clean Balance Sheet

Cash & Equivalents1 > US$350 million

Working Capital1 > US$370 million

Debt None

Gold Hedging None

Semi-Annual Dividend US$0.10/share

Shares Outstanding1 127.5 million Employee Options1 4.8 million Fully Diluted 132.3 million

Recent Share Price1 C$16.92

Market Capitalization C$2.16 billion

1 | Unaudited – management’s estimate as of January 11, 2013. 17 |

ALAMOS GOLD INC.

TSX.AGI

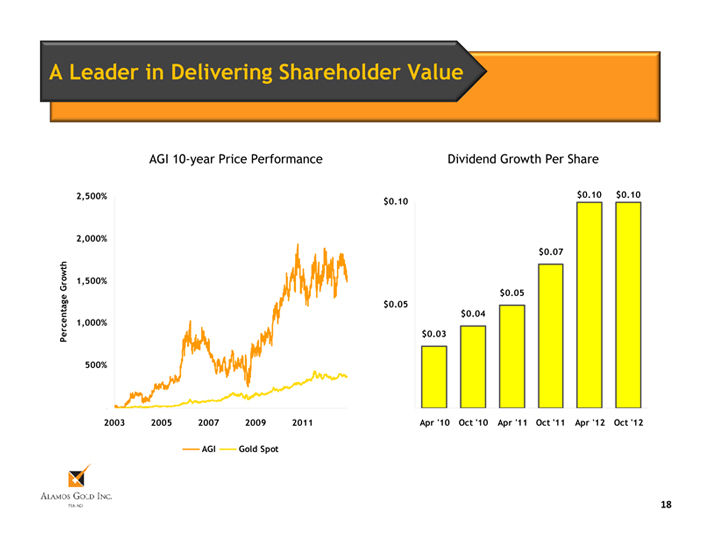

A Leader in Delivering Shareholder Value

AGI 10-year Price Performance Dividend Growth Per Share

2,500% $0.10 $0.10 $0.10

2,000%

$0.07 Growth 1,500%

$0.05

$0.05

$0.04 1,000% Percentage $0.03 500%

0% $0.00

2003 2005 2007 2009 2011 Apr ‘10 Oct ‘10 Apr ‘11 Oct ‘11 Apr ‘12 Oct ‘12

AGI Gold Spot

18

ALAMOS GOLD INC.

TSX.AGI

Appendices

19

ALAMOS GOLD INC.

TSX.AGI

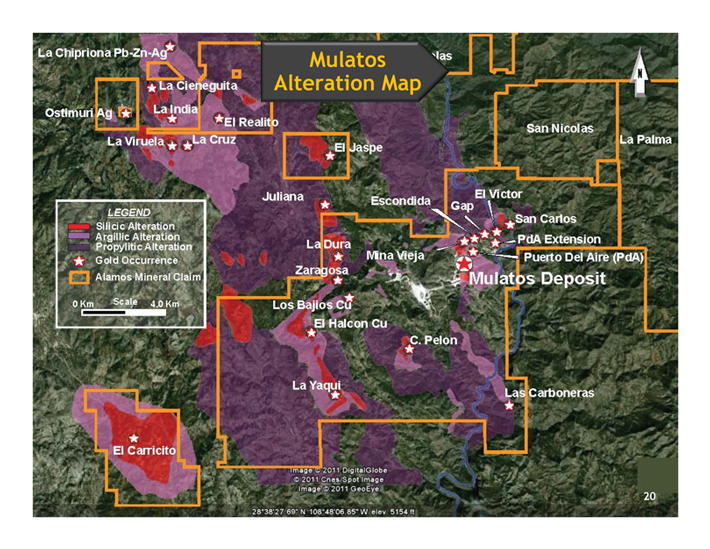

Mulatos Alteration Map

20

La chipriona Pb-Zn-Ag

Ostimuri Ag

La Cieneguita

La India

EI Realito

La Cruz

La Viruela

LEGEND

Sillcic Alteration

Argillic Alteration

Propyitic Alteration

Gold Occurrence

Alamos Mineral Claim

EI Carricito

EI jaspe

Juliana

La Dura Zaragosa

Los Bajios Cu

EI halcon Cu

La Yaqui

San Nicolas La Palma

EI Victor

Gap San Carlos PdA Extension

Image 2011 digitalglobe

2011 Cness/Spot image

Image 2011 GeoEye

28 38 27 69 N 108 48 06 85 W elev 5154 ft

San Carlos

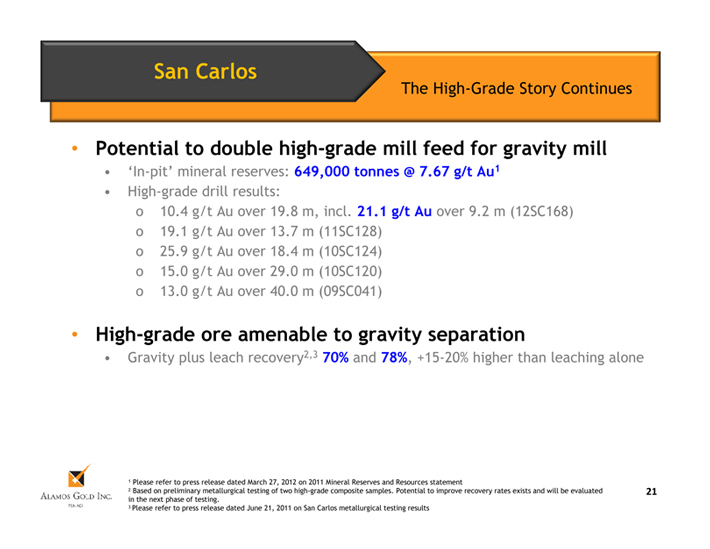

The High-Grade Story Continues

• Potential to double high-grade mill feed for gravity mill

• ‘In-pit’ mineral reserves: 649,000 tonnes @ 7.67 g/t Au1

• High-grade drill results: o 10.4 g/t Au over 19.8 m, incl. 21.1 g/t Au over 9.2 m (12SC168) o 19.1 g/t Au over 13.7 m (11SC128) o 25.9 g/t Au over 18.4 m (10SC124) o 15.0 g/t Au over 29.0 m (10SC120) o 13.0 g/t Au over 40.0 m (09SC041)

• High-grade ore amenable to gravity separation

• Gravity plus leach recovery2,3 70% and 78%, +15-20% higher than leaching alone

1 | Please refer to press release dated March 27, 2012 on 2011 Mineral Reserves and Resources statement |

2 Based on preliminary metallurgical testing of two high-grade composite samples. Potential to improve recovery rates exists and will be evaluated 21 in the next phase of testing.

3 | Please refer to press release dated June 21, 2011 on San Carlos metallurgical testing results |

ALAMOS GOLD INC.

TSX.AGI

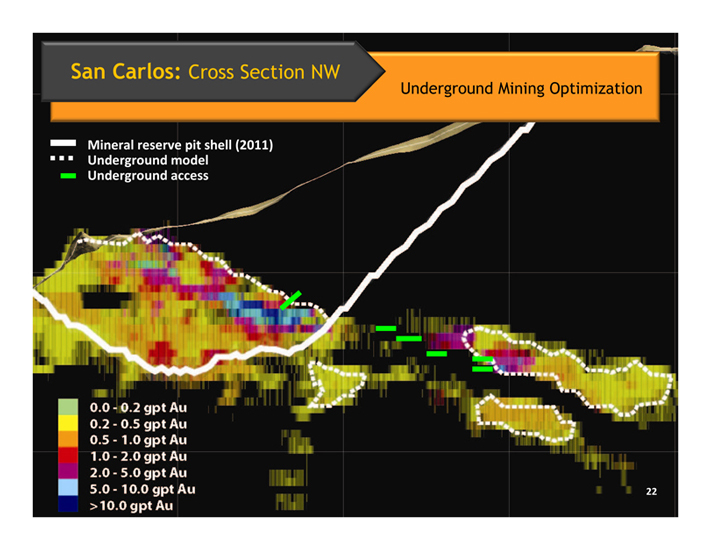

San Carlos: Cross Section NW

Underground Mining Optimization

Mineral reserve pit shell (2011) Underground model Underground access

22

0.0—0.2 | gpt Au |

0.2— 0.5 gpt Au

0.5—1.0 gpt Au

1.0—2.0 gpt Au

2.0 – 5.0 gpt Au

5.0 – 10.00 gpt Au

> 10.0 gpt Au

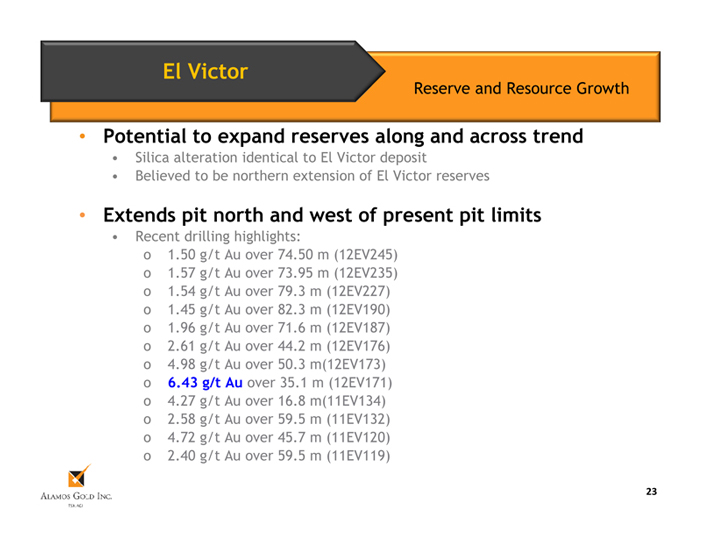

El Victor

Reserve and Resource Growth

• Potential to expand reserves along and across trend

• Silica alteration identical to El Victor deposit

• Believed to be northern extension of El Victor reserves

• Extends pit north and west of present pit limits

• Recent drilling highlights: o 1.50 g/t Au over 74.50 m (12EV245) o 1.57 g/t Au over 73.95 m (12EV235) o 1.54 g/t Au over 79.3 m (12EV227) o 1.45 g/t Au over 82.3 m (12EV190) o 1.96 g/t Au over 71.6 m (12EV187) o 2.61 g/t Au over 44.2 m (12EV176) o 4.98 g/t Au over 50.3 m(12EV173) o 6.43 g/t Au over 35.1 m (12EV171) o 4.27 g/t Au over 16.8 m(11EV134) o 2.58 g/t Au over 59.5 m (11EV132) o 4.72 g/t Au over 45.7 m (11EV120) o 2.40 g/t Au over 59.5 m (11EV119)

23

ALAMOS GOLD INC.

TSX.AGI

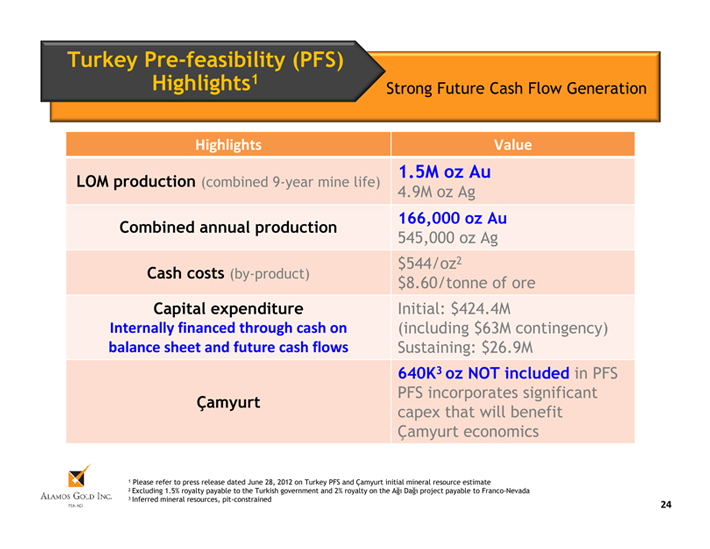

Turkey Pre-feasibility (PFS) Highlights1

Strong Future Cash Flow Generation

Highlights Value

1.5M oz Au

LOM production (combined 9-year mine life)

4.9M oz Ag

166,000 oz Au Combined annual production

545,000 oz Ag $544/oz2

Cash costs (by-product)

$8.60/tonne of ore

Capital expenditure Initial: $424.4M

Internally financed through cash on (including $63M contingency) balance sheet and future cash flows Sustaining: $26.9M

640K3 oz NOT included in PFS PFS incorporates significant

Çamyurt capex that will benefit Çamyurt economics

1 | Please refer to press release dated June 28, 2012 on Turkey PFS and Çamyurt initial mineral resource estimate |

2 Excluding 1.5% royalty payable to the Turkish government and 2% royalty on the Ağ? Dağ? project payable to Franco-Nevada

3 | Inferred mineral resources, pit-constrained 24 |

ALAMOS GOLD INC.

TSX.AGI

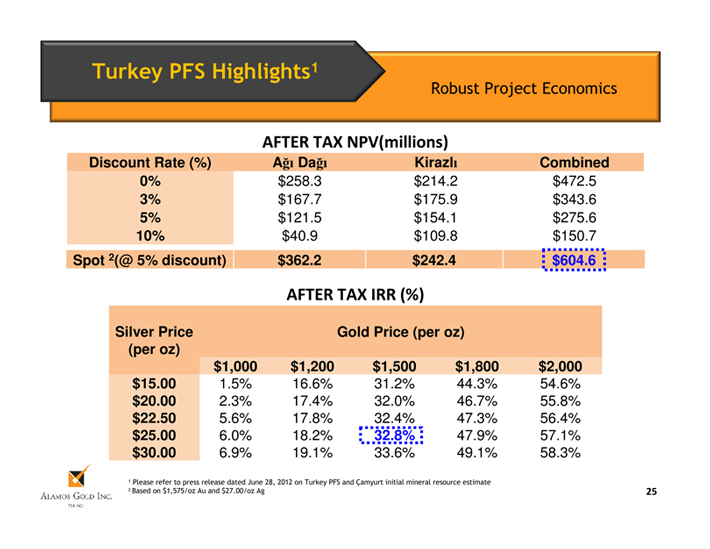

Turkey PFS Highlights1

Robust Project Economics

AFTER TAX NPV(millions)

Discount Rate (%) Ağ? Dağ? Kirazl? Combined

0% $258.3 $214.2 $472.5

3% $167.7 $175.9 $343.6

5% $121.5 $154.1 $275.6 10% $40.9 $109.8 $150.7

Spot 2(@ 5% discount) $362.2 $242.4 $604.6

AFTER TAX IRR (%)

Silver Price Gold Price (per oz) (per oz) $1,000 $1,200 $1,500 $1,800 $2,000 $15.00 1.5% 16.6% 31.2% 44.3% 54.6% $20.00 2.3% 17.4% 32.0% 46.7% 55.8% $22.50 5.6% 17.8% 32.4% 47.3% 56.4% $25.00 6.0% 18.2% 32.8% 47.9% 57.1% $30.00 6.9% 19.1% 33.6% 49.1% 58.3%

1 | Please refer to press release dated June 28, 2012 on Turkey PFS and Çamyurt initial mineral resource estimate |

2 | Based on $1,575/oz Au and $27.00/oz Ag 25 |

ALAMOS GOLD INC.

TSX.AGI

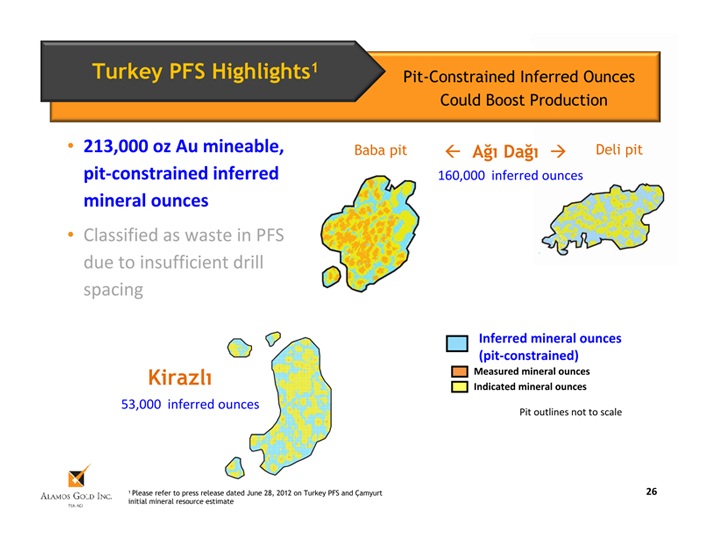

Turkey PFS Highlights1

Pit-Constrained Inferred Ounces Could Boost Production

• 213,000 oz Au mineable, Baba pit _ Ağ? Dağ? _ Deli pit pit-constrained inferred 160,000 inferred ounces mineral ounces

• Classified as waste in PFS due to insufficient drill spacing

Inferred mineral ounces (pit-constrained)

Kirazl? Measured mineral ounces Indicated mineral ounces

53,000 inferred ounces

Pit outlines not to scale

1 | Please refer to press release dated June 28, 2012 on Turkey PFS and Çamyurt 26 initial mineral resource estimate |

ALAMOS GOLD INC.

TSX.AGI

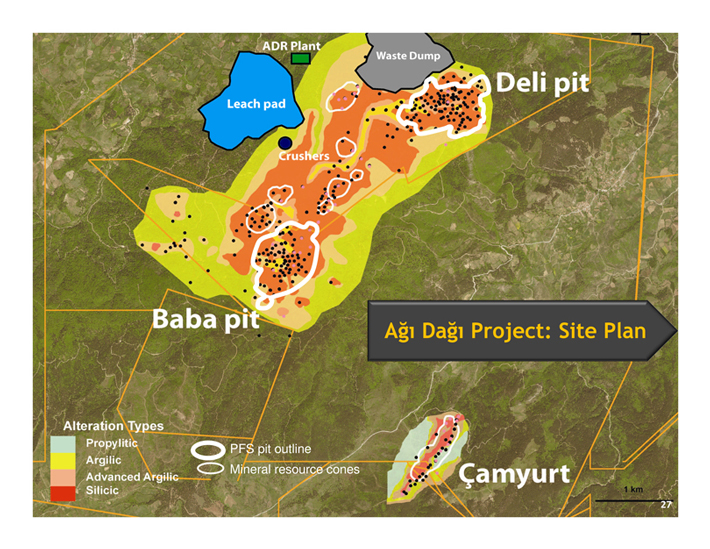

Ağ? Dağ? Project: Site Plan

PFS pit outline

Mineral resource cones

27

ADR plant

Waster Dump

Leach pad Deli pit

Crushers

Baba pit

Agi Dagi Project: Site Plan

Alternation Types

Propylitic

Argilic

Advanced Argilic

Slicic

PFS pit outline

Mineral resource cones Camyurt

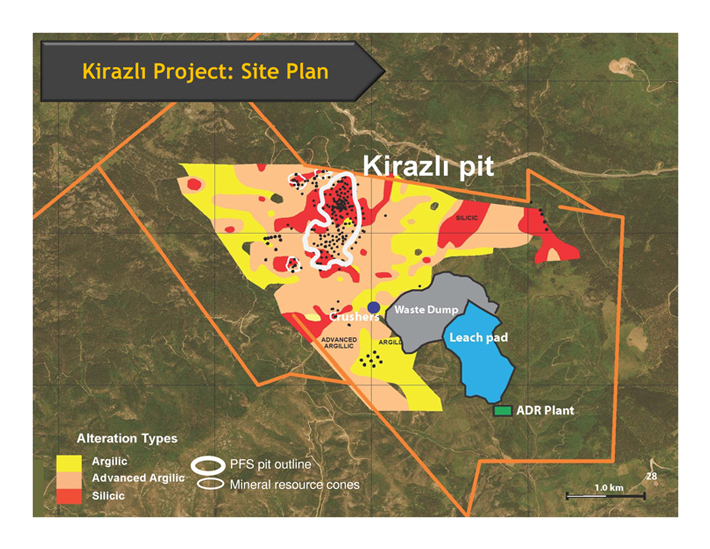

Kirazl? Project: Site Plan

PFS pit outline

Mineral resource cones 28

Kirazli Pit

Crushers waste dump Leach pad

ADVNACED ARGILLIC ARGILL

ADR Plant

Alteration Types

Argilic

Advanced Argilic

Silicic

PFS pit outline

Mineral resource cones

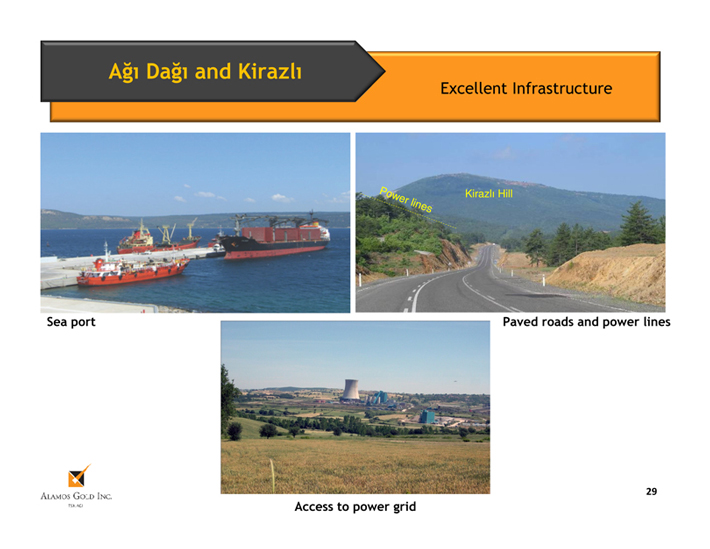

Ağ? Dağ? and Kirazl?

Excellent Infrastructure

Pow Kirazl? Hill

er li nes

Sea port Paved roads and power lines

29

Access to power grid

ALAMOS GOLD INC.

TSX.AGI

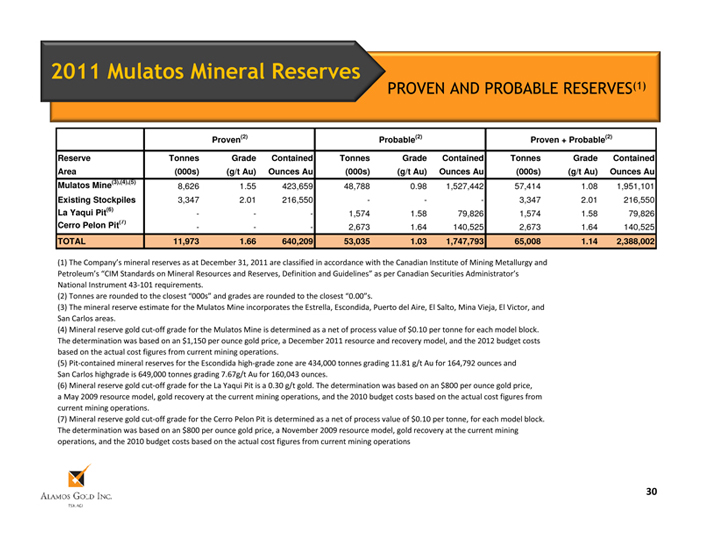

2011 Mulatos Mineral Reserves

PROVEN AND PROBABLE RESERVES(1)

Proven(2) Probable(2) Proven + Probable(2)

Reserve Tonnes Grade Contained Tonnes Grade Contained Tonnes Grade Contained Area (000s) (g/t Au) Ounces Au (000s) (g/t Au) Ounces Au (000s) (g/t Au) Ounces Au Mulatos Mine(3),(4),(5)

8,626 1.55 423,659 48,788 0.98 1,527,442 57,414 1.08 1,951,101 Existing Stockpiles 3,347 2.01 216,550——3,347 2.01 216,550

La Yaqui Pit(6)

——1,574 1.58 79,826 1,574 1.58 79,826 Cerro Pelon Pit(7)——2,673 1.64 140,525 2,673 1.64 140,525

TOTAL 11,973 1.66 640,209 53,035 1.03 1,747,793 65,008 1.14 2,388,002

(1) The Company’s mineral reserves as at December 31, 2011 are classified in accordance with the Canadian Institute of Mining Metallurgy and Petroleum’s “CIM Standards on Mineral Resources and Reserves, Definition and Guidelines” as per Canadian Securities Administrator’s National Instrument 43-101 requirements.

(2) | Tonnes are rounded to the closest “000s” and grades are rounded to the closest “0.00“s. |

(3) The mineral reserve estimate for the Mulatos Mine incorporates the Estrella, Escondida, Puerto del Aire, El Salto, Mina Vieja, El Victor, and San Carlos areas.

(4) Mineral reserve gold cut-off grade for the Mulatos Mine is determined as a net of process value of $0.10 per tonne for each model block. The determination was based on an $1,150 per ounce gold price, a December 2011 resource and recovery model, and the 2012 budget costs based on the actual cost figures from current mining operations.

(5) Pit-contained mineral reserves for the Escondida high-grade zone are 434,000 tonnes grading 11.81 g/t Au for 164,792 ounces and San Carlos highgrade is 649,000 tonnes grading 7.67g/t Au for 160,043 ounces.

(6) Mineral reserve gold cut-off grade for the La Yaqui Pit is a 0.30 g/t gold. The determination was based on an $800 per ounce gold price, a May 2009 resource model, gold recovery at the current mining operations, and the 2010 budget costs based on the actual cost figures from current mining operations.

(7) Mineral reserve gold cut-off grade for the Cerro Pelon Pit is determined as a net of process value of $0.10 per tonne, for each model block. The determination was based on an $800 per ounce gold price, a November 2009 resource model, gold recovery at the current mining operations, and the 2010 budget costs based on the actual cost figures from current mining operations

30

ALAMOS GOLD INC.

TSX.AGI

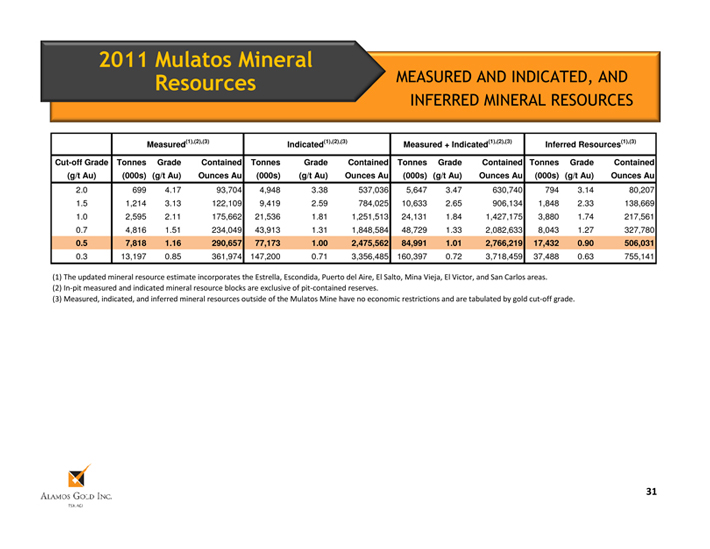

2011 Mulatos Mineral

Resources MEASURED AND INDICATED, AND INFERRED MINERAL RESOURCES

Measured(1),(2),(3) Indicated(1),(2),(3) Measured + Indicated(1),(2),(3) Inferred Resources(1),(3)

Cut-off Grade Tonnes Grade Contained Tonnes Grade Contained Tonnes Grade Contained Tonnes Grade Contained (g/t Au) (000s) (g/t Au) Ounces Au (000s) (g/t Au) Ounces Au (000s) (g/t Au) Ounces Au (000s) (g/t Au) Ounces Au

2.0 699 4.17 93,704 4,948 3.38 537,036 5,647 3.47 630,740 794 3.14 80,207 1.5 1,214 3.13 122,109 9,419 2.59 784,025 10,633 2.65 906,134 1,848 2.33 138,669 1.0 2,595 2.11 175,662 21,536 1.81 1,251,513 24,131 1.84 1,427,175 3,880 1.74 217,561 0.7 4,816 1.51 234,049 43,913 1.31 1,848,584 48,729 1.33 2,082,633 8,043 1.27 327,780

0.5 7,818 1.16 290,657 77,173 1.00 2,475,562 84,991 1.01 2,766,219 17,432 0.90 506,031

0.3 13,197 0.85 361,974 147,200 0.71 3,356,485 160,397 0.72 3,718,459 37,488 0.63 755,141

(1) The updated mineral resource estimate incorporates the Estrella, Escondida, Puerto del Aire, El Salto, Mina Vieja, El Victor, and San Carlos areas. (2) In-pit measured and indicated mineral resource blocks are exclusive of pit-contained reserves.

(3) Measured, indicated, and inferred mineral resources outside of the Mulatos Mine have no economic restrictions and are tabulated by gold cut-off grade.

31

ALAMOS GOLD INC.

TSX.AGI

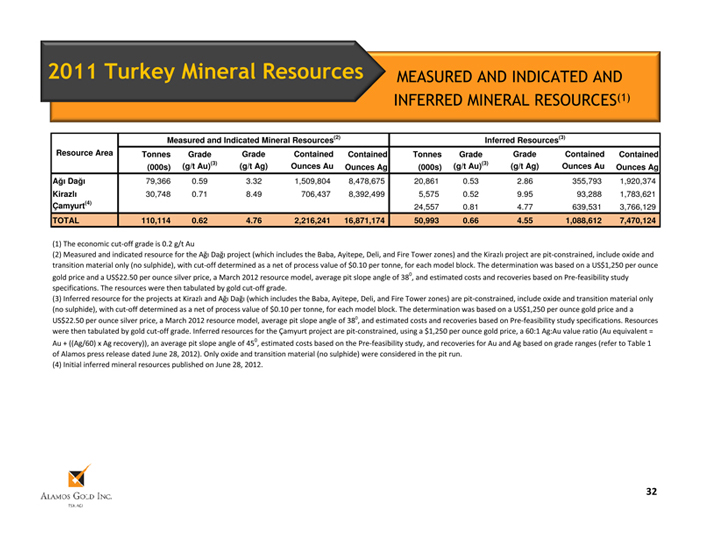

2011 Turkey Mineral Resources MEASURED AND INDICATED AND

INFERRED MINERAL RESOURCES(1)

Measured and Indicated Mineral Resources(2) Inferred Resources(3)

Resource Area Tonnes Grade Grade Contained Contained Tonnes Grade Grade Contained Contained (g/t Au)(3) (g/t Ag) Ounces Au (g/t Au)(3) (g/t Ag) Ounces Au (000s) Ounces Ag (000s) Ounces Ag Ağ? Dağ? 79,366 0.59 3.32 1,509,804 8,478,675 20,861 0.53 2.86 355,793 1,920,374 Kirazl? 30,748 0.71 8.49 706,437 8,392,499 5,575 0.52 9.95 93,288 1,783,621

Çamyurt(4)

24,557 0.81 4.77 639,531 3,766,129

TOTAL 110,114 0.62 4.76 2,216,241 16,871,174 50,993 0.66 4.55 1,088,612 7,470,124

(1) | The economic cut-off grade is 0.2 g/t Au |

(2) Measured and indicated resource for the Ağ? Dağ? project (which includes the Baba, Ayitepe, Deli, and Fire Tower zones) and the Kirazl? project are pit-constrained, include oxide and transition material only (no sulphide), with cut-off determined as a net of process value of $0.10 per tonne, for each model block. The determination was based on a US$1,250 per ounce

0

gold price and a US$22.50 per ounce silver price, a March 2012 resource model, average pit slope angle of 38 , and estimated costs and recoveries based on Pre-feasibility study specifications. The resources were then tabulated by gold cut-off grade.

(3) Inferred resource for the projects at Kirazl? and Ağ? Dağ? (which includes the Baba, Ayitepe, Deli, and Fire Tower zones) are pit-constrained, include oxide and transition material only (no sulphide), with cut-off determined as a net of process value of $0.10 per tonne, for each model block. The determination was based on a US$1,250 per ounce gold price and a US$22.50 per ounce silver price, a March 2012 resource model, average pit slope angle of 380, and estimated costs and recoveries based on Pre-feasibility study specifications. Resources were then tabulated by gold cut-off grade. Inferred resources for the Çamyurt project are pit-constrained, using a $1,250 per ounce gold price, a 60:1 Ag:Au value ratio (Au equivalent =

0

Au + ((Ag/60) x Ag recovery)), an average pit slope angle of 45 , estimated costs based on the Pre-feasibility study, and recoveries for Au and Ag based on grade ranges (refer to Table 1 of Alamos press release dated June 28, 2012). Only oxide and transition material (no sulphide) were considered in the pit run.

(4) | Initial inferred mineral resources published on June 28, 2012. |

32

ALAMOS GOLD INC.

TSX.AGI

Jo Mira Clodman

Vice President, Investor Relations 416.368.9932 x 401 jmclodman@alamosgold.com