Exhibit 99.1

ALAMOS GOLD INC.

Suite 2200 – 130 Adelaide Street West

Toronto, Ontario M5H 3P5

416-368-9932

ANNUAL INFORMATION FORM

for the year ended December 31, 2012

March 28, 2013

| ANNUAL INFORMATION FORM - 2012 |

ALAMOS GOLD INC.

ANNUAL INFORMATION FORM

TABLE OF CONTENTS

| Page | ||||

PRELIMINARY NOTES | 4 | |||

GLOSSARY | 7 | |||

CORPORATE STRUCTURE | 13 | |||

Name and Incorporation | 13 | |||

Intercorporate Relationships | 13 | |||

GENERAL DEVELOPMENT OF THE BUSINESS | 14 | |||

Three-Year History | 14 | |||

NARRATIVE DESCRIPTION OF THE BUSINESS | 17 | |||

The Mulatos Mine | 17 | |||

Aĝi Daĝi and Kirazli Projects | 19 | |||

Uses of Gold | 20 | |||

Sales and Refining | 20 | |||

Employees | 20 | |||

Risk Factors | 20 | |||

SALAMANDRA CONCESSIONS & MULATOS MINE IN MEXICO | 29 | |||

Project Description and Location | 29 | |||

Access, Climate, Communication, Power | 31 | |||

History | 32 | |||

Mineralization | 32 | |||

Exploration | 33 | |||

Logging, Sampling Methodology, Sample Preparation, Analysis, Sample Custody | 43 | |||

Modelling and Estimation | 44 | |||

Metallurgy | 46 | |||

Mineral Resources | 46 | |||

Mineral Reserves | 50 | |||

Qualified Person(s) Disclosure | 52 | |||

Mining Operations | 52 | |||

Outlook | 54 | |||

AĞI DAĞI & KIRAZLI PROJECTS IN TURKEY | 55 | |||

Project Description and Location | 55 | |||

Access, Climate, Communication, Power | 57 | |||

History | 57 | |||

Geological Setting | 57 | |||

Engineering and Development Work | 58 | |||

Mineralization | 58 | |||

Exploration Work Summary – 2011 and 2012 | 59 | |||

Logging, Sampling Methodology, Sample Preparation, Analysis, Sample Custody | 63 | |||

Modelling and Estimation | 64 | |||

| 2 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

Metallurgy | 65 | |||

Mineral Resource | 66 | |||

Qualified Person(s) Disclosure | 68 | |||

Outlook | 68 | |||

DIVIDENDS | 69 | |||

DESCRIPTION OF CAPITAL STRUCTURE | 69 | |||

Common Shares | 69 | |||

MARKET FOR SECURITIES | 70 | |||

Trading Price and Volume | 70 | |||

PRIOR SALES | 70 | |||

DIRECTORS AND OFFICERS | 71 | |||

Cease Trade Orders or Bankruptcies | 72 | |||

Penalties or Sanctions | 73 | |||

Conflicts of Interest | 73 | |||

AUDIT COMMITTEE | 74 | |||

Composition of the Audit Committee | 74 | |||

Relevant Education and Experience | 74 | |||

Reliance on Certain Exemptions | 74 | |||

Reliance on the Exemption in Subsection 3.3(2) or Section 3.6 | 74 | |||

Reliance on Section 3.8 | 74 | |||

Audit Committee Oversight | 74 | |||

Pre-approval Policies and Procedures | 74 | |||

External Auditor Service Fees (Category) | 75 | |||

INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 75 | |||

TRANSFER AGENT AND REGISTRAR | 75 | |||

LEGAL PROCEEDINGS | 75 | |||

MATERIAL CONTRACTS | 75 | |||

INTERESTS OF EXPERTS | 75 | |||

ADDITIONAL INFORMATION | 75 | |||

| 3 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

ANNUAL INFORMATION FORM

(“AIF”)

ALAMOS GOLD INC.

(the “Company”)

PRELIMINARY NOTES

Effective Date of Information

The information in this AIF is current as of March 28, 2012, unless otherwise stated herein.

Currency and Exchange Rates

All dollar amounts in this AIF are expressed in United States dollars, unless otherwise indicated (“CAD” denotes Canadian dollars). The following table sets forth the value of the Canadian dollar expressed in United States dollars on December 31 of each year and the average, high and low exchange rates during the year indicated based on the noon rate of exchange as reported by the Bank of Canada:

Canadian Dollars into United States Dollars | 2012 | 2011 | 2010 | |||||||||

Closing | $ | 1.0051 | $ | 0.9833 | $ | 1.0054 | ||||||

Average | $ | 0.9937 | $ | 1.0114 | $ | 0.9710 | ||||||

High | $ | 1.0299 | $ | 1.0583 | $ | 1.0054 | ||||||

Low | $ | 0.9599 | $ | 0.9430 | $ | 0.9278 | ||||||

The noon rate of exchange on March 27, 2013, as reported by the Bank of Canada for the conversion of Canadian dollars into United States dollars was CAD$1.017 equals US$1.000.

Imperial Equivalents

For ease of reference, the following factors for converting metric measurements to imperial equivalents are provided:

To Convert From Metric | To Imperial | Multiply by | ||||

Hectares | Acres | 2.471 | ||||

Metres | Feet (ft.) | 3.281 | ||||

Kilometres (km.) | Miles | 0.621 | ||||

Tonnes | Tons (2000 pounds) | 1.102 | ||||

Grams/tonne | Ounces (troy/ton) | 0.029 | ||||

Forward-Looking Statements

This AIF contains forward-looking statements within the meaning of the United States Securities Exchange Act of 1934, as amended (the “Exchange Act”), and applicable Canadian securities laws, concerning the Company’s plans for its properties and other matters. All statements other than statements of historical fact included in this AIF, including, without limitation, statements regarding forecast gold production, gold grades, recoveries, waste-to-ore ratios, total cash costs, potential mineralization and reserves, exploration results, and future plans and objectives of the Company, are forward-looking statements that involve various risks and uncertainties. These forward-looking

| 4 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

statements include, but are not limited to, statements with respect to mining and processing of mined ore, achieving projected recovery rates, anticipated production rates and mine life, operating efficiencies, costs and expenditures, changes in mineral resources and conversion of mineral resources to proven and probable reserves, and other information that is based on forecasts of future operational or financial results, estimates of amounts not yet determinable, and assumptions of management.

Exploration results that include geophysics, sampling, and drill results on wide spacings may not be indicative of the occurrence of a mineral deposit. Such results do not provide assurance that further work will establish sufficient grade, continuity, metallurgical characteristics and economic potential to be classed as a category of mineral resource. A mineral resource that is classified as “inferred” or “indicated” has a great amount of uncertainty as to its existence and economic and legal feasibility. It cannot be assumed that any or part of an “indicated mineral resource” or “inferred mineral resource” will ever be upgraded to a higher category of resource. Investors are cautioned not to assume that all or any part of mineral deposits in these categories will ever be converted into proven and probable reserves.

Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as “expects” or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “estimates” or “intends”, or stating that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved) are not statements of historical fact and may be “forward-looking statements”. Forward-looking statements are subject to a variety of risks and uncertainties that could cause actual events or results to differ from those reflected in the forward-looking statements.

There can be no assurance that forward-looking statements will prove to be accurate and actual results and future events could differ materially from those anticipated in such statements. Important factors that could cause actual results to differ materially from the Company’s expectations include risks related to the on-going business of the Company, including risks related to international operations; the actual results of current exploration activities; conclusions of economic evaluations and changes in project parameters as plans continue to be refined as well as future prices of gold and silver, as well as those risk factors described in the section entitled “Risk Factors” in this AIF. Although the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements.

Mineral Reserve and Resource Estimates

Unless otherwise indicated, all resource and reserve estimates included in this AIF have been prepared in accordance with National Instrument 43-101 -Standards of Disclosure for Mineral Projects(“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) -CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended. NI 43-101 is a rule developed by the Canadian Securities Administrators, which established standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. The terms “mineral reserve”, “proven mineral reserve” and “probable mineral reserve” are Canadian mining terms as defined in accordance with NI 43-101 and the CIM standards. These definitions differ from the definitions in SEC Industry Guide 7 (“SEC Industry Guide 7”) under the United States Securities Act of 1933, as amended, and the Exchange Act. Under SEC Industry Guide 7 standards, a “final” or “bankable” feasibility study is required to report reserves, the three-year historical average price is used in any reserve or cash flow analysis to designate reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority.

In addition, the terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are defined in and required to be disclosed by NI 43-101 and the CIM standards; however, these terms are not defined terms under SEC Industry Guide 7 and are normally not permitted to be used in reports and registration statements filed with the SEC. Investors are cautioned not to assume that all or any part of mineral deposits in these categories will ever be converted into reserves. “Inferred mineral resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be

| 5 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre–feasibility studies, except in rare cases. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable. Disclosure of “contained ounces” in a resource is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers to report mineralization that does not constitute “reserves” by SEC standards as in place tonnage and grade without reference to unit measures.

| 6 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

GLOSSARY

In this AIF unless otherwise defined or unless there is something in the subject matter or context inconsistent therewith, the following terms have the meanings set forth herein or therein:

| “Ag” | Silver. | |

| “Aği Daği and Kirazli Projects” | Advanced-stage gold development projects located in the Çanakkale province in the Biga Peninsula of northwestern Turkey. The Aği Daği property (the “Aği Daği Project” or “Aği Daği”) consists of 10,525 hectares of mineral tenure in eleven (11) contiguous licences. The Kirazli property (the “Kirazli Project” or “Kirazli”) is situated 25 kilometres to the northwest of the Aği Daği property and consists of 1,541 hectares of mineral tenure in two (2) contiguous licenses. | |

| “Alamos Minerals” | Alamos Minerals Ltd., a company which amalgamated with National Gold on February 21, 2003 to form the Company. | |

| “Au” | Gold. | |

| “Çamyurt Project” | An early-stage development mineral project located approximately three km southeast of the Company’s Aği Daği Project. | |

| “Company” or “Alamos” | Alamos Gold Inc., including, unless the context otherwise requires, the Company’s subsidiaries. | |

| “Cu” | Copper. | |

| “dacite” | The extrusive (volcanic) equivalent of quartz-diorite. | |

| “dome” | An uplift or anticlinal structure, either circular or elliptical in outline, in which the rocks dip gently away in all directions. | |

| “dore” | Unrefined gold and silver bullion bars, which will be further refined to almost pure metal. | |

| “EIA” | Environmental Impact Assessment report. | |

| “Ejido” | Mulatos Ejido, a local community of people who own the surface rights to an area of land covering all of the known mineral deposits in the Mulatos area of the Salamandra Concessions. | |

| “feasibility study” | A comprehensive study of a deposit in which all geological, engineering, operating, economic and other relevant factors are considered in sufficient detail that it could reasonably serve as the basis for a final decision by a financial institution to finance the development of the deposit for mineral production. | |

| “Fronteer” | Fronteer Development Group Inc., the 40% vendor of the Aği Daği and Kirazli Projects. | |

| “Fronteer Teck Agreement” | The share purchase agreement among Teck, Fronteer, the Company, Teck Madencilik Sanayi Ticaret A.S., Fronteer Investment Inc. and Fronteer Eurasia Madencilik Anonim Sirketi dated December 7, 2009 pursuant to which the Company acquired all of the issued and outstanding shares in the capital of Kuzey Biga Madencilik Sanayi Ticaret A.Ş, Doğu Biga Madencilik Sanayi Ticaret A.Ş and Alamos Eurasia Madencilik A.Ş, Turkish subsidiaries of Fronteer and Teck which were the vendors of the Aği Daği and Kirazli Projects. | |

| “grade” | Term used to indicate the concentration of an economically desirable mineral or element in its host rock as a function of its relative mass. With gold, this term may be expressed as grams per tonne (g/t) or ounces per tonne (opt). | |

| “HQ diameter” | 2.4 inch diameter drill hole. | |

| 7 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

| “IFRS” | International financial reporting standards, the accounting principles used by the Company. | |

| “indicated resource” or “indicated mineral resource” | That part of a mineral resource for which quantity, grade or quality, densities, shape and physical characteristics can be estimated with a level of confidence sufficient to allow the appropriate application of technical and economic parameters, to support mine planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough for geological and grade continuity to be reasonably assumed. | |

| “inferred resource” or “inferred mineral resource” | That part of a mineral resource for which quantity and grade or quality can be estimated on the basis of geological evidence and limited sampling and reasonably assumed, but not verified, geological and grade continuity. The estimate is based on limited information and sampling gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes. | |

| “Kennecott” | Kennecott Minerals Company. | |

| “Kennecott Assignment Agreement” | An assignment agreement between Royal Gold and Kennecott dated January 5, 2006 whereby Kennecott assigned its 30% interest in the Placer Kennecott Royalty to Royal Gold. | |

| “km” | Kilometres. | |

| “leaching” | The separation, selective removal or dissolving-out of soluble constituents from a rock or ore body by the natural actions of percolating solutions. | |

| “m” | Metres. | |

| “the Mine” or “the Mulatos Mine” | The Mulatos Mine consists of an open pit heap leach operation located within the Company’s Salamandra Concessions in Sonora, Mexico. | |

| “Mineral Reserve” | The economically mineable part of a measured or indicated mineral resource demonstrated by at least a preliminary feasibility study. The study must include adequate information on mining, processing, metallurgical, economics and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified. A mineral reserve includes diluting materials and allowances for losses that occur when the material is mined and processed. | |

| “M3” or “M3 Engineering” | M3 Engineering and Technology Corporation. | |

| “M3 July 14, 2004 Report” | A technical report prepared for the Company by M3 Engineering entitled “Technical Report – the Estrella Pit Development Mulatos Sonora Mexico” dated June 17, 2004 (as revised July 14, 2004) which incorporates a summary of technical information from the 2004 Feasibility Study. | |

| “measured resource” or “measured mineral resource” | That part of a mineral resource for which quantity, grade or quality, densities, shape, physical characteristics are so well established that they can be estimated with confidence sufficient to allow the appropriate application of technical and economic parameters, to support production planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough to confirm both geological and grade continuity. | |

| “Minera San Augusto” | Minera San Augusto, S.A. de C.V., owned 70% by Placer Dome and 30% by Kennecott, and the original vendor of the Salamandra Concessions. | |

| 8 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

| “mineral resource” | A concentration or occurrence of natural, solid, inorganic or fossilized organic material in or on the earth’s crust in such form and quantity and of such grade or quality that it has reasonable prospects for economic extraction. The location, quantity, grade, geological characteristics and continuity of a mineral resource are known, estimated or interpreted from specific geological evidence and knowledge. The term “mineral resource” covers mineralization and natural material of intrinsic economic interest which has been identified and estimated through exploration and sampling and within which mineral reserves may subsequently be defined by the consideration and application of technical, economic, legal, environmental, socio-economic and governmental factors. The phrase “reasonable prospects for economic extraction” implies a judgment by the Qualified Person in respect of the technical and economic factors likely to influence the prospect of economic extraction. A mineral resource is an inventory of mineralization that under realistically assumed and justifiable technical and economic conditions might become economically extractable. The term “mineral resource” used in this AIF is a Canadian mining term as defined in accordance with NI 43-101 under the guidelines set out in the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) Standards on Mineral Resource and Mineral Reserves Definitions and guidelines adopted by the CIM Council on August 20, 2000 (the “CIM Standards”). | |

| “MON” or “Minas de Oro Nacional” | Minas de Oro Nacional, S.A. de C.V. (formerly, O.N.C. de Mexico, S.A. de C.V.), a Mexican corporation which is a wholly-owned subsidiary of the Company. | |

| “National Gold” | National Gold Corporation, a British Columbia company which amalgamated with Alamos Minerals on February 21, 2003 to form the Company. | |

| “net smelter return royalty/Net Smelter Royalty” | A payment made by a producer of metals based on the value of the gross metal production from the property, less deduction of certain limited costs including, but not necessarily limited to, smelting, refining, transportation and insurance costs. | |

| “New Surface Agreement” | A surface rights agreement dated May 27, 2004 between Minas de Oro Nacional and the Ejido regarding a lease of surface rights required to perform different mining works and activities and to set up infrastructure for the Company’s exploration and exploitation of certain mining concessions on the Salamandra Concessions. The New Surface Agreement supersedes the 1995 Surface Agreement. | |

| “NYSE” | New York Stock Exchange. | |

| “NI 43-101” | National Instrument 43-101 – Standards of Disclosure for Mineral Projects. A rule developed by the Canadian Securities Administrators (an umbrella group of Canada’s provincial and territorial securities regulators) that governs public disclosure by mining and mineral exploration issuers. The rule establishes certain standards for all public disclosure of scientific and technical information concerning mineral projects. | |

| “NQ diameter” | 1.75 inch diameter drill hole. | |

| “ore” | A natural aggregate of one or more minerals which, at a specified time and place, may be mined and sold at a profit, or from which some part may be profitably separated. | |

| “ounces” or “oz” | A measure of weight in gold and other precious metals, correctly troy ounces, which weigh 31.2 grams as distinct from an imperial ounce which weighs 28.4 grams. | |

| “Placer” or “Placer Dome” | Placer Dome Inc., which was acquired by Barrick Gold Corporation (“Barrick”) and amalgamated with Barrick in 2006. | |

| 9 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

| “Placer Assignment Agreement” | An assignment agreement between Royal Gold and Barrick dated October 1, 2008 whereby Barrick assigned its 70% interest in the Placer Kennecott Royalty to Royal Gold. | |

| “Placer Kennecott Royalty” or “Royal Gold Royalty” | A royalty that is currently payable to Royal Gold pursuant to the Kennecott Assignment Agreement and the Placer Assignment Agreement. Under the RTE Agreement, a royalty payable to Tenedoramex and Kennecott on an aggregate basis and divided between them, beginning on the date of commencement of commercial production until such time as the first 2,000,000 ounces of gold have been mined, processed and sold (or deemed sold) from the Salamandra Concessions:

i. 2% of the Net Smelter Returns (as defined in the RTE Agreement) in respect of all Products (as defined in the RTE Agreement) mined and sold (or deemed sold) by Minas de Oro Nacional from the Salamandra Concessions; and

ii. the applicable percentage based on the average Gold Price (as defined in the RTE Agreement) as published in the Wall Street Journal for the calendar quarter in which the royalty is payable of the Net Smelter Returns in respect of all silver and gold Products (as defined in the RTE Agreement) mined and sold (or deemed sold) by Minas de Oro Nacional from the Salamandra Concessions as follows: | |

Gold Price Range | Net Smelter Return Royalty 100% Basis | |||

US$0.00/oz to US$299.99/oz | 1.0 | % | ||

US$300.00/oz to US$324.99/oz | 1.5 | % | ||

US$325.00/oz to US$349.99/oz | 2.0 | % | ||

US$350.00/oz to US$374.99/oz | 3.0 | % | ||

US$375.00/oz to US$399.99/oz | 4.0 | % | ||

US$400.00/oz or higher | 5.0 | % | ||

The term “Products” (as defined in the RTE Agreement) means ores, minerals, or other commercially valuable products, except any fraction thereof comprising or deemed to comprise Gold and Silver Products, mined from the Salamandra Concessions.

The term “Gold and Silver Products” (as defined in the RTE Agreement) means ores, minerals, or other commercially valuable products containing gold or silver mined from the Salamandra Concessions, provided that where such products contain a combination of gold and silver and other commercially viable metals or minerals, Gold and Silver Products shall be deemed to comprise that fraction of such products as represents the proportionate commercial value of the gold and silver contained in such products, with the remaining fraction of such products deemed to be Products. | ||

| “ppm” | parts per million. | |

| “ppb” | parts per billion. | |

| “PQ diameter” | 3.2-inch drill hole diameter. | |

| “preliminary feasibility study” | A comprehensive study of the viability of a mineral project that has advanced to a stage where the mining method, in the case of underground mining, or the pit configuration, in the case of an open pit, has been established and an effective method of mineral processing has been determined, and includes a financial analysis based on reasonable assumptions of technical, engineering, legal, operating, economic, social, and environmental factors and the evaluation of other relevant factors which are sufficient for a Qualified Person, acting reasonably, to determine if all or part of the Mineral Resource may be classified as a Mineral Reserve. | |

| “probable mineral reserve” | The economically mineable part of an indicated and, in some circumstances, a measured mineral resource demonstrated by at least a preliminary feasibility study. This study must include adequate information on mining, processing, metallurgical, economics and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified. | |

| 10 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

| “proven mineral reserve” or “proven reserve” | The economically mineable part of a measured mineral resource demonstrated by at least a preliminary feasibility study. This study must include adequate information on mining, processing, metallurgical, economics and other relevant factors that demonstrate, at the time of reporting, that economic extraction is justified. | |

“QA/QC” | Quality assurance/quality control. | |

| “Qualified Person” | Conforms to that definition under NI 43-101 for an individual:

(a) is an engineer or geoscientist with a university degree, or equivalent accreditation, in an area of geoscience, or engineering, relating to mineral exploration or mining;

(b) has at least five years of experience in mineral exploration, mine development or operation or mineral project assessment, or any combination of these, that is relevant to his or her professional degree or area of practice;

(c) has experience relevant to the subject matter of the mineral project and the technical report;

(d) is in good standing with a professional association; and

(e) in the case of a professional association in a foreign jurisdiction, has a membership designation that: (i) requires attainment of a position of responsibility in their profession that requires the exercise of independent judgment; and (ii) requires a favourable confidential peer evaluation of the individual’s character, professional judgement, experience, and ethical fitness or a recommendation for membership by at least two peers, and demonstrated prominence or expertise in the field of mineral exploration or mining. | |

Royal Gold | Royal Gold Inc. is a royalty holding company that acquired the 30% Kennecott portion of the Placer Kennecott Royalty effective January 5, 2006, and acquired the other 70% of the royalty from Barrick effective October 1, 2008. | |

“RQD” | Rock quality designation. | |

“RTE Agreement” | A royalty agreement between Minas de Oro Nacional and Minera San Augusto dated March 23, 2001 describing, among other things, the Placer Kennecott Royalty. | |

| “Salamandra Concessions” | The Salamandra group of mineral concessions held by the Company’s Mexican subsidiary, Minas de Oro Nacional, currently comprising an area of approximately 30,536 hectares in 44 concessions located in the State of Sonora, Mexico. | |

| “Scoping Study or Preliminary Economic Assessment” | A technical report prepared for the Company by KD Engineering entitled “Technical report on the Aği Daği- Kirazli Gold Project, Çanakkale Province, Republic of Turkey” dated March 12, 2010 and filed atwww.sedar.com on March 29, 2010. | |

| “Technical Report Kirazli & Aği Daği Gold Project” | On August 9, 2012, Alamos filed with the Canadian securities regulatory authorities a technical report pursuant to NI 43-101F1 with respect to the Kirazli Project and the Aği Daği Project entitled “NI 43-101 Technical Report Kirazli & Aği Daği Gold Project” dated July 31, 2012 with an effective date of June 30, 2012. | |

| “Technical Report Update (2012) - Mulatos Mine” | On January 14, 2013, Alamos filed with the Canadian securities regulatory authorities a technical report pursuant to NI 43-101F1 with respect to the Mulatos Mine entitled “Minas de Oro Nacional, S.A. de C.V. – Mulatos Project – Technical Report Update (2012)” dated December 21, 2012. | |

“Teck” | Teck Resources Limited, the 60% vendor of the Aği Daği and Kirazli Projects. | |

“Tenedoramex” | Tenedoramex S.A., a wholly owned subsidiary of Placer Dome and a 70% owner of Minera San Augusto. | |

“tpd” | Tonnes per day. | |

| 11 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

| “TSX” | The Toronto Stock Exchange. | |

| “TSXV” | The TSX Venture Exchange. | |

| “1995 Surface Agreement” | A surface rights agreement dated November 26, 1995 between Minera San Augusto and the Mulatos Ejido regarding a lease of surface rights required to perform different mining works and activities and to set up infrastructure for the Company’s exploration and exploitation of certain mining concessions on the Salamandra Concessions. | |

| “2004 Feasibility Study” | “Mulatos Feasibility Study Phase One - Estrella Pit” dated June 1, 2004, prepared by M3 Engineering containing a feasibility study of the Estrella zone within the Mulatos deposit on the Salamandra Concessions filed atwww.sedar.com on July 22, 2004. | |

| 12 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

CORPORATE STRUCTURE

Name and Incorporation

The name of the Company is “Alamos Gold Inc.”. The Company’s principal place of business is located at Suite 2200, 130 Adelaide Street West, Toronto, Ontario, Canada M5H 3P5, telephone: 416-368-9932, facsimile: 416-368-2934. The Company has administration offices in Hermosillo, Mexico and in Ankara, Turkey. The registered and records office of the Company is located at Suite 3350, Four Bentall Centre, 1055 Dunsmuir Street, P.O. Box 49222, Vancouver, British Columbia, Canada V7X 1L2.

Alamos was formed by the amalgamation of Alamos Minerals, a company incorporated under the laws of the Province of British Columbia, and National Gold Corporation, a company incorporated under the laws of the Province of Alberta, and continued into the Province of British Columbia under the formerCompany Act (British Columbia) on February 21, 2003, with the resulting amalgamated company continuing under the name “Alamos Gold Inc.”. TheBusiness Corporations Act (British Columbia) (the “BCBCA”) came into force on March 29, 2004, and on July 15, 2004, after obtaining shareholder approval, Alamos altered its Notice of Articles to increase its authorized capital from 1,000,000,000 common shares without par value to an unlimited number of common shares without par value and adopted new articles that take advantage of certain business flexibilities available under the BCBCA. Alamos is a public corporation that is listed on the TSX and the NYSE under the symbol “AGI” and has a quoted market value of approximately $1.78 billion as of the close of trading on March 27, 2013.

Intercorporate Relationships

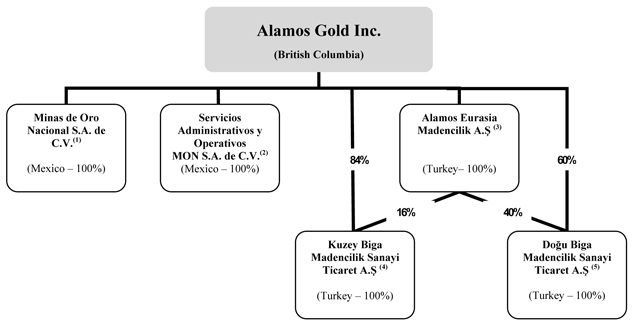

In this AIF, unless the context otherwise requires, the terms “we”, “us”, “our”, and similar terms as well as references to “Alamos” or the “Company” refer to Alamos Gold Inc. together with its subsidiaries. As at March 28, 2013, the following diagram sets forth the Company’s intercorporate relationships with its active subsidiaries including the jurisdiction of incorporation or organization and the Company’s respective percentage ownership of each subsidiary.

| (1) | The authorized share capital of Minas de Oro Nacional consists of 50,000 fixed shares and an unlimited number of variable shares. The issued and outstanding capital of MON consists of 50,000 fixed shares and 485,624,800 variable shares. All of the variable shares are registered in the name of the Company. One of the 50,000 outstanding fixed shares |

| 13 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

of MON is held for the benefit of the Company in the name of John McCluskey, the President and Chief Executive Officer of the Company. |

| (2) | One of the 50,000 outstanding shares of Servicios Administrativos y Operativos MON S.A. de C.V. is held for the benefit of the Company in the name of John McCluskey, the President and Chief Executive Officer of the Company. |

| (3) | Alamos Eurasia Madencilik A.S. (“Alamos Eurasia”) has authorized and issued and outstanding share capital of an aggregate of 547,003 shares. The shares of Alamos Eurasia are distributed with 546,999 to Alamos, and one share each is held for the benefit of the Company by the following officers of the Company: Jamie Porter, Manley Guarducci, Charles Tarnocai and Han Ilhan. |

| (4) | Kuzey Biga Madencilik Sanayi Ticaret A.Ş (“Kuzey Biga”) has authorized and issued and outstanding share capital of 39,492,842 shares. The shares of Kuzey Biga are distributed with 32,997,042 to Alamos, 6,495,500 shares to Alamos Eurasia, and 100 shares each held for the benefit of the Company by the following officers of the Company: Charles Tarnocai, Manley Guarducci and Han Ilhan. |

| (5) | Doğu Biga Madencilik Sanayi Ticaret A.Ş. (“Dogu Biga”) has authorized and issued and outstanding share capital of 8,113,000 shares. The shares of Dogu Biga are distributed with 4,867,600 to Alamos, 3,245,100 shares to Alamos Eurasia, and 100 shares each held for the benefit of the Company by the following officers of the Company: Charles Tarnocai, Manley Guarducci and Han Ilhan. |

GENERAL DEVELOPMENT OF THE BUSINESS

Three-Year History

Alamos is a mining company engaged in the mining and extraction of, and exploration for, precious metals, primarily gold. Alamos currently has one mine that is in production, the Mulatos Mine, located in the state of Sonora, Mexico. Alamos acquired the Mulatos Mine in February 2003. In January 2010, Alamos acquired the development-stage Aği Daği and Kirazli projects in the Biga district of northwestern Turkey. In 2011, Alamos discovered the Çamyurt project, which Alamos believes has the potential to become a viable stand-alone mining project. Camyurt is located approximately three kilometers from the Aği Daği Project.

In recent years, the focus at the Mulatos Mine has been on operational improvements designed to enhance the efficiency of the mine, and on exploration programs seeking to increase the Company’s reserves and resources. In 2012, the Mulatos Mine produced 200,000 ounces of gold, representing the fifth consecutive year in which the Mulatos Mine has produced in excess of 150,000 ounces of gold. In the fiscal year ended December 31, 2012, Alamos generated revenues of $329.4 million, compared to $227.4 million in 2011. As at December 31, 2012, Alamos had in excess of $350 million in cash and cash equivalents and short-term investments.

2010 Developments

On January 6, 2010, the Company acquired the Aği Daği and Kirazli Projects through the purchase of three Turkish companies from Teck and Fronteer. The Company paid a total of $40 million cash and issued an aggregate of 4 million common shares to Teck (as to 60%) and Fronteer (as to 40%) in total consideration. Aği Daği and Kirazli are advanced-stage development projects that are within the Biga Mineral District, an established gold-copper mineral district located in northwestern Turkey. The Company spent approximately $9 million in 2010 on development and exploration activities related to these projects.

On January 7, 2010 the Company reported record quarterly gold production for the fourth quarter of 2009 of 48,000 ounces and full year 2009 production of 178,500 ounces. The primary factor contributing to higher than expected production was higher recoveries, resulting from several operating enhancements implemented throughout the year.

On January 12, 2010 the Company announced that drilling activities in 2009 at the San Carlos project in close proximity to the Mulatos mine were successful at identifying high-grade mineralization, and that further work was planned to further delineate the deposit in 2010.

On March 16, 2010 the Company reported record annual earnings of $56.0 million ($0.52 per basic share), in addition to announcing a semi-annual dividend of $0.03 per share payable commencing on April 30, 2010 to shareholders of record on April 15, 2010.

| 14 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

On March 29, 2010, the Company released the Scoping Study which reported indicated and inferred resources at Aği Daği and Kirazli, and that the development of the Aği Daği and Kirazli Projects was economic at then current gold prices and supported a decision to proceed to the preliminary feasibility study stage. Highlights of the Scoping Study included total initial and sustaining capital costs (inclusive of a 27% contingency) of $234.7 million, and average annual production of approximately 135,000 ounces of gold and 621,600 ounces of silver over an estimated mine life of approximately 8 years at an average total cash cost of $314 per ounce (with silver accounted for as a by-product credit). The Scoping Study indicated the potential economic viability of the Aği Daği and Kirazli Projects, and as a result the Company decided to proceed to the preliminary feasibility study stage.

On March 31, 2010, the Company reported a 17% increase in proven and probable reserves at Mulatos to 2.39 million ounces. The Company also announced a 13% increase in measured and indicated resources (exclusive of reserves) to 1.88 million ounces and an 11% decline in inferred resources. In addition, the Company reported its intention to expand crushing throughput capacity through the addition of a screening plant between the secondary and tertiary crushers at an estimated total cost of $6.5 million with completion targeted for the third quarter of 2010. The Company implemented the screening plant in the third quarter of 2010 at a total cost of approximately $7.3 million.

Effective September 17, 2010, the Company announced a 17% increase to its semi-annual dividend from $0.03 to $0.035 per share. In addition, the Company reported that it had entered into surface right access agreements that would allow exploration activities to commence at the Company’s El Carricito exploration project, located approximately 20 km from the Mulatos Mine.

On December 9, 2010, the Company outlined its production guidance for 2011. Gold production for 2011 was forecast to be 160,000 to 175,000 ounces at a total cash cost (including the 5% royalty) of between $415 and $430 per ounce. Further, the Company reported plans to spend $48.1 million in capital in Mexico in 2011, focused primarily on production expansion. Development costs related to the Turkish projects were budgeted at $15 million, while exploration expenditures for both Mexico and Turkey were expected to total $18 million.

2011 Developments

On March 14, 2011, the Company reported a 43% increase to its semi-annual dividend to $0.05 per share payable on May 2, 2011 to shareholders of record on April 15, 2011.

On March 15, 2011, the Company reported its financial results for the fourth quarter and full year of 2010. The Company produced a total of 156,000 ounces of gold in 2010 at a total cash cost of $361 per ounce of gold sold. Revenues of $189.3 million increased 10% over 2009, and the Company achieved record annual earnings of $65.7 million ($0.57 per basic share), inclusive of a $0.11 per share gain on completion of the settlement agreement with Primero.

On March 24, 2011, the Company announced a 38% increase in measured and indicated resources, in addition to replacing proven and probable mineral reserves at the Mulatos Mine.

On June 16, 2011, the Company reported that drilling at the Çamyurt Project had delineated a mineralized zone that is continuous for at least 1,100 m along strike with potential to extend mineralization. An initial mineral resource estimate will be reported in the second quarter of 2012, and the Company believes that the Çamyurt Project has the potential to be a stand-alone mining project.

On September 14, 2011, the Company announced a 40% increase in its semi-annual dividend from $0.05 to $0.07 per common share, payable on October 28, 2011 to shareholders of record on October 14, 2011.

On September 16, 2011, the Company reported a 19% increase in measured and indicated resources at its Aği Daği and Kirazli Projects and provided an exploration update on the Çamyurt Project. Measured and indicated mineral resources at Aği Daği and Kirazli increased 19% to 1.96 million ounces of gold, reflecting a 19% increase in tonnes and no change in the average gold grade compared to the 2010 year-end estimate.

| 15 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

2012 Developments

On February 23, 2012 the Company reported its financial results for the fourth quarter and 2011 full year. The Company produced a total of 153,000 ounces in 2011 at a total cash cost of $368 per ounce of gold sold. Operating revenues of $227.4 million increased 20% over 2010, and the Company achieved annual earnings of $60.1 million ($0.51 per basic share). The Company also announced a 43% increase to its semi-annual dividend from $0.07 to $0.10 per share, payable on April 30, 2012 to shareholders of record on April 13, 2012.

In addition, the Company provided 2012 production guidance of between 200,000 and 220,000 ounces of gold at a cash operating cost (before 5% royalty) of between $365 and $390 per ounce. The increase in annual production was attributable to the start-up of the mill to process high-grade ore from the Escondida zone.

On March 27, 2012, the Company reported drill results from El Victor and provided its 2011 global mineral reserve and resource update, replacing mineral reserves mined out in 2011.

On June 28, 2012 the Company announced a positive preliminary feasibility study for Aği Daği and Kirazli, supporting a decision to proceed with permitting towards construction. The study contemplated total life of mine production of over 1.5 million ounces of gold and 4.9 million ounces of silver over a combined nine year life. Total pre-production capital expenditures are estimated to be approximately $424.4 million. At a $1,239 per ounce average gold price assumption, the after-tax net present value at a 5% discount rate was calculated to be $276 million. The Company also announced an initial inferred mineral resource for the Çamyurt project.

On August 9, 2012, Alamos filed with the Canadian securities regulatory authorities a technical report pursuant to NI 43-101F1 with respect to the Kirazli Project and the Aği Daği Project entitled “NI 43-101 Technical Report Kirazli & Aği Daği Gold Project” dated July 31, 2012 with an effective date of June 30, 2012.

Developments Subsequent to 2012 Year End

On January 8, 2013, Alamos issued a press release summarizing fourth quarter and full year 2012 production results from the Mulatos Mine as well as operating, development and exploration plans for 2013. In the fourth quarter of 2012, the Mulatos Mine produced a record 67,800 ounces of gold, 41% higher than the previous quarterly production record of 48,200 ounces. Full year 2012 gold production was 200,000 ounces, achieving production guidance. Gold production at the Mulatos Mine for 2013 is expected to be between 180,000 and 200,000 ounces at a cash operating cost (exclusive of the 5% royalty) between $415 and $435 per ounce of gold sold. Capital spending in Mexico in 2013 is budgeted at approximately $40.7 million, while development spending in Turkey is forecast to be approximately $69.3 million. Total exploration spending is budgeted to be $21.6 million, split evenly between Mexico and Turkey.

On January 14, 2013, Alamos filed with the Canadian securities regulatory authorities a technical report pursuant to NI 43-101F1 with respect to the Mulatos Mine entitled “Minas de Oro Nacional, S.A. de C.V. – Mulatos Project – Technical Report Update (2012)” dated December 21, 2012.

On January 14, 2013, Alamos announced an offer to acquire Aurizon Mines Ltd. (“Aurizon”) for approximately CAD$780 million in cash and shares (the “Offer”). Alamos reported that on the date of the Offer, Alamos owned 26,507,283 Aurizon shares, representing over 16% of the issued and outstanding Aurizon shares. On March 4, 2013, Aurizon announced that it had entered into an agreement to be acquired by Hecla Mining Ltd. (“Hecla”). Among the terms of Aurizon’s agreement with Hecla was a $27.2 million dollar “break fee” payable to Hecla in the event that (among other things) Aurizon acquired more than 33.32% of the outstanding Aurizon shares. Consequently, on March 19, 2013, the Company announced that it would not take up any Aurizon shares tendered to the Offer, and that it would let the Offer expire on March 19, 2013.

On February 13, 2013, the common shares of the Company commenced trading on the NYSE under the ticker symbol “AGI”.

| 16 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

On February 21, 2013, Alamos reported its fourth quarter and 2012 year-end financial results. The fourth quarter of 2012 was the best quarter in the Company’s history, from a financial perspective, with record revenues, cash flows and earnings.

NARRATIVE DESCRIPTION OF THE BUSINESS

The Company is a gold mining company engaged in exploration, mine development, and the mining and extraction of precious metals, primarily gold. The Company’s primary asset is the Mulatos Mine and its 30,536 hectares of Salamandra Concessions in the state of Sonora, Mexico, that were acquired on February 21, 2003, by way of amalgamation of National Gold and Alamos Minerals. In addition, on January 6, 2010 the Company acquired the development-stage Aği Daği and Kirazli Projects in the Biga district of northwestern Turkey. In 2011, the Company discovered the Çamyurt Project, located approximately 3 kilometers from the Aği Daği Project, which the Company believes has the potential to become a stand-alone mining project.

The Mulatos Mine

General

The Salamandra Concessions are located in the State of Sonora, Mexico. The Mulatos deposit is located in the Salamandra Concessions and has been developed into the Mulatos Mine. Mineral rights for all concessions comprising the Salamandra Concessions are controlled by Minas de Oro Nacional, a Mexican company wholly owned by the Company.

Portions of the Salamandra Concessions originally acquired from Placer Dome are subject to the Royal Gold Royalty which applies to the first two million ounces of gold mined, processed or sold from the Mulatos Mine. As at December 31, 2012, the royalty had been paid or accrued on approximately 1,004,000 ounces of applicable gold production.

2004 Feasibility Study and M3 July 14, 2004 Report

On June 1, 2004, M3 Engineering and M3 Mexicana Hermosillo Sonora Mexico and Consultants, independent consultants to the Company, completed the 2004 Feasibility Study recommending development of the Estrella Pit portion of the Mulatos deposit. Subsequently, the Company engaged M3 Engineering and M3 Mexicana Hermosillo Sonora Mexico and Consultants to prepare an independent technical report based on the 2004 Feasibility Study, which is available for review on the SEDAR website at www.sedar.com under the Company’s issuer profile.

Technical Report (Update) – Mulatos Mine

On January 14, 2013, Alamos filed with the Canadian securities regulatory authorities a technical report pursuant to NI 43-101F1 with respect to the Mulatos Mine entitled “Minas de Oro Nacional, S.A. de C.V. – Mulatos Project – Technical Report Update (2012)” dated December 21, 2012.

Mine Construction

The Company began construction of the Mulatos Mine, beginning with the Estrella Pit portion, in the third quarter of 2004 and Phase I of the Estrella Pit portion of the Mulatos Mine was completed in January 2006 at a cost of approximately $74 million. Although the 2004 Feasibility Study plan called for a 10,000 tpd crushing operation, the Company sized the major components of the Mulatos Mine, including the crusher/conveyor and the gold recovery plant, to handle a mining and processing operation with a capacity of approximately 15,000 tpd. In 2005, an expansion budget of $20 million was approved to increase the scale of mining operations from the 2004 Feasibility Study level of 10,000 tpd.

Since 2005, the Mulatos Mine has undergone significant expansion, particularly with respect to crushing capacity. At the start of 2010, the Company commissioned a closed circuit crushing system designed to improve the size consistency of stacked ore. In October 2010, the Company added a scalping screen plant to the crushing circuit

| 17 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

designed to increase throughput. Continued modifications to the crushing circuit aimed at increasing crusher throughput have been implemented throughout 2011 and early 2012. Average daily crusher throughput in 2012 was 16,000 tpd, up from 14,100 tpd in 2011. In 2013, the Company expects average daily crusher throughput to increase to approximately 17,500 tonnes per day.

In addition to the existing heap leach operations at the Mulatos Mine, between 2009 and 2012, the Company has developed the Escondida high-grade zone at an approximate cost of $61 million and constructed a mill to process high-grade ore from Escondida at a cost of $20 million.

Pre-commercial Operations

The Mulatos Mine began operations in 2005 as a run-of-mine conventional open-pit heap-leach operation with a gold recovery plant consisting of a carbon-in-column circuit. Although not specified in the 2004 Feasibility Study, the Company operated temporarily on a run-of-mine basis to take advantage of gold prices at levels significantly above those considered in the 2004 Feasibility Study. Run-of-mine ore was stacked directly on the leach pad in the period from June 2005 to June 2006. No additional run-of-mine material was stacked on the leach pad effective July 1, 2006, as the crusher was operating near capacity and gold recoveries from crushed ore are significantly higher than recoveries from run-of-mine ore.

Commercial Operations

The Company announced commercial production at the Mulatos Mine on April 1, 2006. The Mine operates 365 days a year. Daily production may be affected to some extent by adverse weather, but it would be unusual for adverse weather to cause complete mine stoppage for an extended period. The Company has acquired the surface rights necessary to carry on its current operations, but may be required to secure additional rights should the Company decide to pursue mining activities outside of the currently permitted concessions. The Company complies with all relevant environmental laws.

Gold is produced on site as dore containing approximately 60-80% gold by weight. The dore is sent to a refinery for final processing prior to sale. Refined gold is sold to several counterparties at market prices. Processing chemicals and materials are generally readily available as is diesel fuel, however, the cost of these products delivered to the site has increased significantly from the feasibility levels. In 2011, the Company experienced short-term disruption of its cyanide supply as a result of its primary cyanide supplier experiencing a flood. Cyanide shipments were reduced in the second quarter of 2011, resulting in lower than planned production in the second and third quarters of the year. Regular cyanide shipments resumed late in the second quarter and gold production deferred as a result of the cyanide supply disruption was produced in the fourth quarter of the year. Alternate cyanide suppliers have been sourced and contingency plans are in place in the event that a similar shortage occurs in the future.

Cost levels have increased significantly from the life-of-mine average cash operating cost of $174 per ounce indicated in the 2004 Feasibility Study which excluded the Royal Gold Royalty and were based on a gold price of $350 per ounce. Unit operating costs are affected by mine operating efficiencies, the waste-to-ore ratio, the cost of mining and processing materials, labour costs, the grade of ore mined and recoveries achieved. Certain costs such as lime, cyanide and diesel fuel have increased in price substantially since the 2004 Feasibility Study was prepared.

In the year ended December 31, 2006, its first year of partial commercial production, the Mulatos Mine produced 101,170 ounces of gold at a cash operating cost of $294 per ounce of gold sold. Since then the Company has implemented a number of operational improvements contributing to higher levels of gold production. In the year-ended December 31, 2012, the Company produced 200,000 ounces of gold at a cash operating cost of $355 per ounce.

Total gold sales revenues for 2012 amounted to $329.4 million (2011 - $234.7 million). The Company’s product, gold and to a lesser extent, silver, is sold to several qualified counterparties for a price that is readily quoted and fluctuates daily. The Company can sell all of its refined metal at the quoted price or contract for a fixed price for future delivery. At December 31, 2012, the Company had no forward gold sales or other gold hedge positions outstanding.

| 18 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

Aği Daği and Kirazli Projects

The Aği Daği and Kirazli gold projects are located on the Biga Peninsula of northwestern Turkey. Aği Daği is located approximately 50 km southeast of Çanakkale and Kirazli is located approximately 25 km northwest of Aği Daği. Çanakkale is the largest centre on the Biga Peninsula with a population of approximately 97,000. Infrastructure in close proximity to the project is excellent and well-serviced with paved roads, transmission lines, and electricity generating facilities.

In June 2012, the Company published a preliminary feasibility study summary of the Aği Daği and Kirazli projects. The highlights are summarized below:

| • | Total life of mine production of 1.5 million ounces of gold and 4.9 million ounces of silver. |

| • | Annual combined gold production is expected to peak in 2017 at 237,000 ounces, and will average 166,000 ounces per year over the nine year combined mine life. |

| • | First gold production from the Kirazli project in 2014, followed by gold production from Aği Daği in 2016. |

| • | Mine life of seven years for Aği Daği and five years for Kirazli. |

| • | Pre-production capital expenditures of $424.4 million. |

| • | Average life of mine cash operating costs of $544 per ounce sold, total cash costs per ounce sold of $579. |

| • | At a $1,239 per ounce gold price assumption, after-tax net present value (“NPV”) at a 5% discount rate of $275.6 million and after-tax internal rate of return (“IRR”) of 22.3%. |

| • | At a gold price of $1,575 per ounce, after-tax NPV at a 5% discount rate increases to $604.6 million and after-tax IRR of 36.5%. |

In addition, the Company reported an initial inferred mineral resource estimate of 640,000 ounces at Çamyurt. Inclusion of the Çamyurt resource in a development scenario represents a major opportunity to further enhance the economic potential of the Company’s Turkish projects.

The preliminary feasibility study for Aği Daği and Kirazli incorporates significant capital spending on infrastructure that is expected to benefit the economics of the Çamyurt project. The average grade of the resources at Çamyurt is substantially higher than at the Aği Daği and Kirazli projects. As a result, once Çamyurt is factored into the Company’s development plan, it is expected to reduce cash costs per ounce on a combined project basis, as well as enhance combined project economics.

The Company has submitted the final environmental impact assessment (“EIA”) report for Kirazli, and expects a response from the Turkish Government in the first quarter of 2013. The final Aği Daği EIA is expected to be submitted in the first quarter of 2013, with a response expected in the second quarter. Permitting and construction activities are expected to take up to 18 months once the EIAs are approved.

In 2012, total expenditures in Turkey were $22.4 million, of which $18.9 million was capitalized. Investments were focused on exploration, engineering and permitting work. The Company had up to nine drill rigs operating at a cost of $9.1 million in 2012, focused on condemnation, geotechnical and exploration drilling.

| 19 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

Uses of Gold

The two principal uses of gold are bullion investment and product fabrication. Within the fabrication category there are a wide variety of end uses, the largest of which is the manufacture of jewellery. Other fabrication purposes include official coins, electronics, dentistry, medallions and other industrial and decorative uses.

Sales and Refining

Gold can be readily sold on numerous markets throughout the world and its market price can be readily ascertained at any time. Because there are a large number of available gold purchasers, the Company is not dependent upon the sale of gold to any one customer.

The Company’s gold production is currently refined to market delivery standards by Johnson Mathey at a refinery in Salt Lake City, Utah. The Company believes that, because of the availability of alternate refiners, the inability of one of the Company’s refiners to process the Company’s product would not have a material adverse effect on the Company.

Employees

As of December 31, 2012, the Company had 20 full-time employees at its Toronto corporate head office. Each of these full time employees is employed under a contract for services directly with the Company. In addition, the Company’s Mexican subsidiary, Servicios Administrativos y Operativos MON, S.A. de C.V. (“SAO”) provides labour-related services for operations at the Salamandra Concessions and at the administrative offices of Minas de Oro Nacional in Hermosillo, Mexico. As of December 31, 2012, SAO had 550 full-time employees. The Company has sourced most of its labour pool, including skilled mining personnel, from the state of Sonora in Mexico. Competition for highly qualified miners has become intense as more mines are being brought into production in the area and worldwide. In addition, the Company has approximately 60 full-time administrative, engineering and exploration personnel in Turkey.

Risk Factors

The financing, exploration, development and mining of any of the Company’s properties is subject to a number of risk factors, including the price of gold, laws and regulations, political conditions, currency fluctuations, hiring qualified people and obtaining necessary services in jurisdictions where the Company operates. The current trends relating to these factors are generally favourable but could change at any time and negatively affect the Company’s operations and business.

The following is a brief discussion of those distinctive or special characteristics of the Company’s operations and industry that may have a material impact on, or constitute risk factors in respect of the Company’s operations and future financial performance. Additional risks not currently known by the Company, or that the Company currently deems immaterial, may also impair the Company’s operations.

The Company’s operating and development properties are located in Mexico and Turkey and are subject to changes in economic and political conditions and regulations in those countries

The economics of the mining and extraction of precious metals are affected by many factors, including the costs of mining and processing operations, variations of grade of ore discovered or mined, fluctuations in metal prices, foreign exchange rates and the prices of goods and services, and such other factors as government regulations, including regulations relating to royalties, allowable production, importing and exporting goods and services and environmental regulations. Depending on the price of minerals discovered and potentially mined, the Company may determine that it is neither profitable nor competitive to acquire or develop properties, or to continue mining activities.

The Company’s mineral properties are located in Mexico and Turkey. Economic and political conditions in Mexico and Turkey could adversely affect the business activities of the Company. These conditions are beyond the

| 20 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

Company’s control, and there can be no assurances that any mitigating actions by the Company will be effective. In the past, both Mexico and Turkey have been subject to political instability, changes and uncertainties which may cause changes to existing governmental regulations affecting mineral exploration and mining activities. The potential implications of political volatility in Mexico or Turkey cannot be accurately predicted. The mineral interests of the Company and the ultimate ability to generate cash flow and profits from operations may be affected by political or economic stability. Associated risks include, but are not limited to: terrorism, corruption, military repression, extreme fluctuations in currency exchange rates and high rates of inflation. Changes in regulations or political attitudes are beyond the control of the Company and may materially adversely affect its business, financial condition and results of operations.

The Company’s mineral exploration and mining activities in both Mexico and Turkey may be adversely affected in varying degrees by changing government regulations relating to the mining industry or shifts in political conditions that increase the costs related to the Company’s activities or to the cost of maintaining its properties. Operations may also be affected to varying degrees by changes in government regulations with respect to restrictions on production, price controls, export controls, income taxes, royalties, and expropriation of property, environmental legislation and mine safety. The effect of these factors cannot be accurately predicted. Economic instability in Mexico could result from current global economic conditions and could contribute to currency volatility and potential increases to income tax rates, both of which could significantly impact the Company’s profitability. Turkey is seeking membership to the European Union (“EU”) and is progressing to conform to EU standards through strengthening its political and economic framework, including through improved stability and transparency. However, Turkey has historically experienced, and to some degree continues to experience, heightened levels of political and economic instability due to regional geopolitical instability. These conditions may be exacerbated by current global economic conditions. This instability may have a material adverse effect on the Company’s properties, business and results of operations.

The Company’s activities are subject to extensive laws and regulations governing worker health and safety, employment standards, waste disposal, protection of historic and archaeological sites, mine development, protection of endangered and protected species and other matters. Specifically, the Company’s activities related to its Mulatos Mine and the Salamandra Concessions are subject to regulation by theMexican Department of Economy - Direccion General of Mines (“DGM”), the environmental protection agency of Mexico (“SEMARNAP”),Comisión Nacional del Aqua(“CONAGUA”),which regulates water rights, and the Mexican Mining Law. Mexican regulators have broad authority to shut down and/or levy fines against facilities that do not comply with regulations or standards. The Company’s exploration and development activities in Turkey are subject to regulation by the General Directorate of Forestry of the Ministry of Environment and Forestry (“MIGEM”). The judiciary in Turkey has substantial discretion to impose injunctions and other legal sanctions.

The Company will be unable to undertake its required drilling and other development work on its properties if all necessary permits and licenses are not granted

A number of approvals, licenses and permits are required for various aspects of exploration and mine development. The Company is uncertain if all necessary permits will be maintained or obtained on acceptable terms or in a timely manner. Future changes in applicable laws and regulations or changes in their enforcement or regulatory interpretation could negatively impact current or planned exploration and development activities within the Salamandra Concessions, the Aği Daği and Kirazli Projects or any other projects with which the Company becomes involved. Any failure to comply with applicable laws and regulations or failure to obtain or maintain permits, even if inadvertent, could result in the interruption of production, exploration or development, or material fines, penalties or other liabilities. It remains uncertain if the Company’s existing permits may be affected in the future or if the Company will have difficulties in obtaining all necessary permits it requires for its proposed or existing mining activities.

In order to maintain mining concessions in good standing under the new Turkish mining law, concession holders must advance their projects efficiently, including by obtaining the necessary permits prior to stipulated deadlines. The Company has implemented plans to obtain all necessary permits prior to the relevant deadlines. While the Company is confident in its ability to meet all required deadlines or milestones so as to maintain its concessions in good standing, there is risk that the relevant Turkish permitting and licensing authorities will not respond in a timely manner. If these deadlines are not met, the Company believes that extensions to deadlines for obtaining the required approvals and permits could be negotiated so that the concessions would remain in good standing. However, there is

| 21 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

no guarantee that the Company will be able to obtain the approvals and permits as planned or, if unable to meet such deadlines, that negotiations for an extension will be successful in order to maintain its concessions in good standing. If the concessions were to expire, this could have a material adverse impact on the Company and its ability to control and develop its Turkish projects.

The business of exploration for minerals and mining involves a high degree of risk, as few properties that are explored are ultimately developed into producing mines

The Company is engaged in exploration, mine development and the mining and production of precious metals, primarily gold, and is exposed to a number of risks and uncertainties that are common to other companies in the same business. Unusual or unexpected ground movements, fires, power outages, labour disruptions, flooding, cave-ins, landslides and the inability to obtain suitable adequate machinery, equipment or labour are risks involved in the operation of mines and the conduct of exploration programs. The Company has relied on and may continue to rely upon consultants and others for mine operating and exploration expertise. Few properties that are explored are ultimately developed into producing mines. Substantial expenditures are required to establish ore reserves through drilling, to develop metallurgical processes to extract the metal from the ore and in the case of new properties, to develop the mining and processing facilities and infrastructure at any site chosen for mining. Although substantial benefits may be derived from the discovery of a major mineral deposit, the Company may not be able to raise sufficient funds for development. The economics of developing mineral properties is affected by many factors including the cost of operations, variations in the grade of ore mined, fluctuations in metal markets, costs of mining and processing equipment and such other factors as government regulations, including regulations relating to royalties, allowable production, importing and exporting of minerals and environmental protection. Where expenditures on a property have not led to the discovery of mineral reserves, spent costs will not usually be recoverable.

Estimates of mineral reserves and resources may not be realized

The mineral reserves and resources estimates contained in this AIF are only estimates and no assurance can be given that any particular level of recovery of minerals will be realized or that an identified resource will ever qualify as a commercially mineable (or viable) deposit which can be legally and economically exploited. The Company relies on laboratory-based recovery models to project estimated ultimate recoveries by ore type at optimal crush sizes. Actual gold recoveries in a commercial heap leach operation may exceed or fall short of projected laboratory test results. In addition, the grade of mineralization ultimately mined may differ from the one indicated by the drilling results and the difference may be material. Production can be affected by such factors as permitting regulations and requirements, weather, environmental factors, unforeseen technical difficulties, unusual or unexpected geological formations, inaccurate or incorrect geologic, metallurgical or engineering work, and work interruptions, among other things. Short-term factors, such as the need for an orderly development of deposits or the processing of new or different grades, may have an adverse effect on mining operations or the results of those operations. There can be no assurance that minerals recovered in small scale laboratory tests will be duplicated in large scale tests under on-site conditions or in production scale operations. Material changes in proven and probable reserves or resources, grades, waste-to-ore ratios or recovery rates may affect the economic viability of projects. The estimated proven and probable reserves and resources described herein should not be interpreted as assurances of mine life or of the profitability of future operations.

The Company has engaged expert independent technical consultants to advise it on, among other things, mineral reserves and resources and project engineering at its Mulatos Mine in Mexico. The Company has also engaged expert independent technical consultants to advise it on these matters at its Aği Daği and Kirazli Projects in Turkey. The Company believes that these experts are competent and that they have and will carry out their work in accordance with all internationally recognized industry standards. If, however, the work conducted and to be conducted by these experts is ultimately found to be incorrect or inadequate in any material respect, the Company may experience delays and increased costs.

Problems with title to mineral properties could have a negative impact on the Company’s future operations

The acquisition of the right to exploit mineral properties is a detailed and time-consuming process. Although the Company is satisfied it has taken reasonable measures to acquire unencumbered rights to explore on and exploit its

| 22 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

mineral reserves on the Salamandra Concessions in Mexico and the Aği Daği and Kirazli Projects in Turkey, no assurance can be given that such claims are not subject to prior unregistered agreements or interests or to undetected or other claims or interests which could be material and adverse to the Company. While the Company has used its best efforts to ensure title to all its properties and secured access to surface rights, these titles or rights may be disputed, which could result in costly litigation or disruption of operations.

Problems with surface access to exploration projects or minerals could have a negative impact on the Company’s exploration programs and future operations

The Company has entered into certain land lease agreements in Mexico with the Ejido and with individual land possessors for the purpose of conducting exploration activities. From time to time, a land possessor may dispute the Company’s surface access rights, and as a result the Company may be barred from its legal temporary occupation rights. Surface access issues have the potential to result in the delay of planned exploration programs, and these delays may be significant. The Company expects that it will be able to resolve these issues; however, there can be no assurance that this will be the case.

The Company strives to maintain good relations with the local community in Mexico by providing employment opportunities and other economic and social benefits. The Company has entered into the New Surface Agreement with the Ejido. In addition, the Company has entered into agreements with individual Ejido members for the surface rights to which they have been assigned. The transfers of title to these surface rights have been registered in Mexico.

The Company is also in negotiations with Ejido and non-Ejido members in Mexico, as a group and individually, to relocate the existing community of Mulatos, and to acquire additional surface rights. Negotiations with the Ejido are time consuming and can be challenging and uncertain. There are financial and other considerations associated with the negotiating process including the filing of complaints or the commencement of legal proceedings by Ejido members, or attempts to impede road access by blockades and other actions to affect access to the Mulatos Mine or otherwise affect operations which could result in significant downtime and associated costs, or suspension of operations and loss of production. With the assistance of experienced legal advisors and the input from State and local government officials, the Company expects that it will be able to acquire its land-use requirements at a reasonable cost; however, there can be no assurance that this will be the case. The Company also expects that any actions taken by Ejido or non-Ejido members to interrupt or otherwise impede mine operations will be addressed by the appropriate State and Federal government authorities.

In 2008, the Company entered into a land purchase agreement with certain landowners in Mexico, under which the Company made a payment of $1.25 million to secure temporary occupation rights to specified land. An additional payment of approximately $1 million (based on current foreign exchange rates) is payable once the land has been vacated and is transferred to the Company. The probability and timing of this additional payment is currently unknown to the Company.

During 2010, the Ejido filed a complaint with the Agrarian Court to nullify the 2008 land purchase agreement. On June 13, 2012, the Agrarian Court rendered a decision on the merits in favor of MON, dismissing the action filed by the plaintiff Ejido, and acquitting all of the defendants named in the lawsuit, including MON. The Company has at all times remained committed to fulfilling all of its obligations under the 2008 land purchase agreement.

Additional future property acquisition, relocation benefits, legal and related costs may be material. The Company cannot currently determine the expected timing, outcome of negotiations or costs associated with the relocation of the remaining property owners and possessors and potential land acquisitions.

The Company may need to enter into negotiations with landowners and other groups in the local community in Turkey in order to conduct future exploration and development work on the Aği Daği and Kirazli Projects. There is no assurance that future discussions and negotiations will result in agreements with landowners and other local community groups in Turkey or if such agreements will be on terms acceptable to the Company so that the Company can continue to conduct exploration and development work on these projects.

| 23 | ALAMOS GOLD INC |

| ANNUAL INFORMATION FORM - 2012 |

Development projects are uncertain and it is possible that actual capital and operating costs and economic returns will differ significantly from those estimated for a project prior to production