QuickLinks -- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on October 14, 2009

Registration No. 333-162115

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

AMENDMENT NO. 2 TO

FORM F-10

REGISTRATION STATEMENT UNDER

THE SECURITIES ACT OF 1933

DRAGONWAVE INC.

(Exact name of Registrant as specified in its charter)

| Canada (Province or other Jurisdiction of Incorporation or Organization) | 4812 (Primary Standard Industrial Classification Code Number) | Not Applicable (I.R.S. Employer Identification Number, if applicable) |

411 Legget Drive, Suite 600, Ottawa, Ontario, Canada, K2K 3C9, (613) 599-9991

(Address and telephone number of Registrant's principal executive offices)

Corporation Service Company, 2711 Centerville Road, Suite 400, Wilmington, Delaware, 19808, (800) 927-9800

(Name, address (including zip code) and telephone number (including area code) of agent for service in the United States)

Copies to:

| Peter Allen DragonWave Inc. 411 Legget Drive, Suite 600 Ottawa, Ontario, K2K 3C9 Canada (613) 599-9991 | Andrea Johnson Fraser Milner Casgrain LLP 99 Bank Street, Suite 1420 Ottawa, Ontario, K1P 1H4 Canada (613) 783-9600 | Craig Andrews Matthew Leivo DLA Piper LLP (US) 4635 Executive Drive, Suite 1100 San Diego, CA 92121 USA (858) 677-1400 | Martin Langlois Ian G. Putnam Stikeman Elliott LLP 5300 Commerce Court West 199 Bay Street Toronto, Ontario, M5L 1B9 Canada (416) 869-5500 | Andrew Foley Edwin S. Maynard Paul, Weiss, Rifkind, Wharton & Garrison LLP 1285 Avenue of the Americas New York, New York 10019-6064 USA (212) 373-3000 |

Approximate date of commencement of proposed sale of the securities to the public:

As soon as practicable after this registration statement becomes effective

Province of Ontario, Canada

(Principal jurisdiction regulating this offering)

It is proposed that this filing shall become effective (check appropriate box below):

| A. | ý | upon filing with the Commission, pursuant to Rule 467(a) (if in connection with an offering being made contemporaneously in the United States and Canada). | ||||

B. | o | at some future date (check the appropriate box below) | ||||

1. | o | pursuant to Rule 467(b) on (date) at (time) (designate a time not sooner than 7 calendar days after filing). | ||||

2. | o | pursuant to Rule 467(b) on (date) at (time) (designate a time 7 calendar days or sooner after filing) because the securities regulatory authority in the review jurisdiction has issued a receipt or notification of clearance on (date). | ||||

3. | o | pursuant to Rule 467(b) as soon as practicable after notification of the Commission by the Registrant or the Canadian securities regulatory authority of the review jurisdiction that a receipt or notification of clearance has been issued with respect hereto. | ||||

4. | o | after the filing of the next amendment to this Form (if preliminary material is being filed). | ||||

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to the home jurisdiction's shelf prospectus offering procedures, check the following box. o

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered | Amount to be Registered(1) | Proposed maximum offering price per share(2) | Proposed maximum aggregate offering price(2) | Amount of registration fee(3) | ||||

|---|---|---|---|---|---|---|---|---|

| Common Shares | 14,918,145 | U.S.$11.32 | U.S.$168,873,401 | U.S.$9,423.14 | ||||

- (1)

- Includes 1,945,845 common shares that the underwriters have the option to purchase to cover over-allotments, if any, as well as associated rights to purchase common shares pursuant to the Registrant's Shareholder Rights Plan Agreement dated January 29, 2009.

- (2)

- Estimated solely for the purpose of calculating the amount of the registration fee pursuant to Rule 457 of the Securities Act of 1933, based on the average of the high and low prices of the Registrant's common shares on the Toronto Stock Exchange on October 13, 2009 converted into U.S.��dollars at the U.S.-Canadian dollar exchange rate of U.S.$1.00 = C$1.0275 on October 13, 2009. Includes 1,945,845 common shares that the underwriters have the option to purchase to cover over-allotments, if any, as well as associated rights to purchase common shares pursuant to the Registrant's Shareholder Rights Plan Agreement dated January 29, 2009.

- (3)

- Of this amount, $6,326.49 previously paid.

PART I

INFORMATION REQUIRED TO BE DELIVERED TO OFFEREES OR PURCHASERS

EXPLANATORY NOTE RELATED TO CANADIAN PROSPECTUS ALTERNATIVE PAGES

This registration statement contains two forms of prospectus: one to be used in connection with the offering of securities described herein in the United States (the "U.S. Prospectus") and one to be used connection with the offering of such securities in Canada (the "Canadian Prospectus"). The U.S. Prospectus and the Canadian Prospectus are identical except for the cover page, the table of contents and the back page, and except that the Canadian Prospectus includes sections titled "Eligibility For Investment", "Purchasers' Contractual Right of Action", "Purchasers' Statutory Rights" and auditors' consents, certificate of corporation and certificate of the underwriters. The form of the U.S. Prospectus is included herein and is supplemented by the alternate pages to be used in the Canadian Prospectus. Each of the alternate pages for the Canadian Prospectus included herein is labeled "Alternative Page for Canadian Prospectus."

I-1

[ALTERNATIVE PAGE FOR CANADIAN PROSPECTUS]

This short form prospectus has been filed under procedures in all the provinces of Canada, except the province of Quebec, that permit certain information about these securities to be determined after the short form prospectus has become final and that permit the omission of that information from this prospectus. The procedures require the delivery to purchasers of a supplemented PREP prospectus containing the omitted information within a specified period of time after agreeing to purchase any of these securities.All of the information contained in the supplemented PREP prospectus that is not contained in this short form base PREP prospectus will be incorporated by reference into this short form base PREP prospectus as of the date of the supplemented PREP prospectus.

No securities regulatory authority has expressed an opinion about these securities and it is an offence to claim otherwise. This short form prospectus constitutes a public offering of these securities only in those jurisdictions where they may be lawfully offered for sale and therein only by persons authorized to sell such securities in those jurisdictions.

Information contained herein is subject to completion or amendment. DragonWave Inc. has filed a registration statement on Form F-10 with the U.S. Securities and Exchange Commission, under the United States Securities Act of 1933, as amended, with respect to the sale of these securities. These securities may not be sold nor may offers to buy be accepted prior to the time the registration statement becomes effective. This short form prospectus shall not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of these securities in any U.S. state in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such U.S. state.

Information has been incorporated by reference in this short form prospectus from documents filed with securities commissions or similar authorities in Canada. Copies of the documents incorporated herein by reference may be obtained on request without charge from the Secretary of DragonWave Inc. at 411 Legget Drive, Suite 600, Ottawa, Ontario, Canada, K2K 3C9, telephone: (613) 599-9991; facsimile: (613) 599-4225 and are also available electronically atwww.sedar.com.

This offering of securities is made by a Canadian issuer that is permitted, under a multi-jurisdictional disclosure system ("MJDS") adopted by the United States and Canada, to prepare this short form prospectus in accordance with Canadian disclosure requirements. Purchasers of the Offered Shares (as defined below) should be aware that such requirements are different from those of the United States. Consolidated financial statements contained and incorporated herein have been prepared in accordance with Canadian generally accepted accounting principles, and may be subject to Canadian auditor and independence standards, and thus may not be comparable to financial statements of United States companies. Information regarding the impact upon our consolidated financial statements of significant differences between Canadian and United States generally accepted accounting principles is contained in (a) note 20 (entitled "Reconciliation with United States Generally Accepted Accounting Principles") presented in the consolidated financial statements comprising DragonWave Inc.'s (i) amended audited consolidated financial statements for the fiscal years ended February 28, 2009 and February 29, 2008 (together with the auditors' report thereon dated April 17, 2009 except as to note 20 which is as of August 25, 2009) and (ii) amended unaudited consolidated financial statements for the three month period ended May 31, 2009 which are contained elsewhere and are incorporated by reference in this short form prospectus and (b) note 13 (entitled "Reconciliation with United States Generally Accepted Accounting Principles") presented in the unaudited consolidated financial statements for the three and six months ended August 31, 2009 which are incorporated by reference in this short form prospectus.

Prospective investors should be aware that the acquisition of the securities described herein may have tax consequences in both the United States and Canada. This short form prospectus or any applicable prospectus supplement may not describe these tax consequences fully for investors who are resident in, or citizens of either Canada or the United States. You should consult your tax advisor about the potential tax consequences that may be applicable in your particular circumstances.

FINAL SHORT FORM BASE PREP PROSPECTUS

| New Issue and Secondary Offering | October 14, 2009 |

DragonWave Inc.

U.S.$ •

12,972,300 Common Shares

This offering (the "Offering") is the initial public offering of the common shares (the "Common Shares") of DragonWave Inc. ("DragonWave", "we", "us", "our" or the "Company") in the United States and includes a new issue of Common Shares in Canada. The Offering consists of a treasury offering of 7,454,050 Common Shares (the "Treasury Shares") by us and a secondary offering by Enterprise Partners V, L.P., Enterprise Partners VI, L.P., Wesley Clover Corporation, Venture Coaches Fund L.P. and certain members of our management (collectively, the "Selling Shareholders") of an aggregate of 5,518,250 Common Shares (the "Secondary Shares", and together with the Treasury Shares, the "Offered Shares"). See "Selling Shareholders". The Offering is being made concurrently in Canada under the terms of this short form prospectus and in the United States under the terms of a registration statement on Form F-10 filed with the United States Securities and Exchange Commission (the "SEC"). Our outstanding Common Shares are listed and posted for trading on the Toronto Stock Exchange (the "TSX") under the symbol "DWI". The TSX has conditionally approved the listing of the Treasury Shares on the TSX. NASDAQ has conditionally approved the listing of the Treasury Shares and our outstanding Common Shares (including the Secondary Shares) on the NASDAQ Global Market under the trading symbol "DRWI". Listing will be subject to our fulfillment of all of the listing requirements of the TSX and NASDAQ, respectively on or before December 23, 2009. On October 13, 2009, the last trading day prior to the filing of this short form prospectus, the closing price of our Common Shares on the TSX was U.S.$10.98 or C$11.31 based on the prevailing U.S.-Canadian dollar exchange rate of U.S.$1.00 = C$1.0298 on October 13, 2009.

[ALTERNATIVE PAGE FOR CANADIAN PROSPECTUS]

The Offered Shares are being offered in Canada by Canaccord Capital Corporation, CIBC World Markets Inc., GMP Securities L.P., RBC Dominion Securities Inc., Dundee Securities Corporation and TD Securities Inc. (the "Canadian Underwriters") and in the United States by Canaccord Adams Inc., Piper Jaffray & Co., Pacific Crest Securities LLC, CIBC World Markets Corp., GMP Securities L.P., Dundee Securities Inc. and TD Securities (USA) LLC (together with the Canadian Underwriters, the "Underwriters"). See "Plan of Distribution".

Price: U.S.$ • per Common Share

| | Price to Public(1) | Underwriters' Fees(2) | Net Proceeds to Us(3)(4)(5) | Net Proceeds to the Selling Shareholders | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Per Common Share | U.S.$ • | U.S.$ • | U.S.$ • | U.S.$ • | |||||||||

Total | U.S.$ • | U.S.$ • | U.S.$ • | U.S.$ • | |||||||||

- (1)

- The public Offering price for the Offered Shares offered in the U.S. of U.S.$ • per Common Share is payable in U.S. dollars and the public Offering price of the Offered Shares offered in Canada of C$ • per Common Share is payable in Canadian dollars, except as may otherwise be agreed by the Underwriters. The U.S. dollar amount is the approximate equivalent of such Canadian dollar amount based on the prevailing U.S.-Canadian dollar exchange rate of U.S.$1.00 = C$ • on • .

- (2)

- The Underwriters will receive a fee of U.S.$ • (C$ • ) per Offered Share (5.75% of the price of the Offered Shares), that will be paid in the currency in which we and the Selling Shareholders receive payment for the Offered Shares. See "Plan of Distribution".

- (3)

- Before deducting expenses of the Offering estimated to be U.S.$ • (C$ • ). The expenses of the Offering will be paid solely by us, and the Selling Shareholders will not pay any portion of such expenses, as provided in the Underwriting Agreement (as defined herein). We have agreed to pay all of the expenses of the Offering since the sale of the Secondary Shares has not added materially to the expenses of the Offering. See "Plan of Distribution".

- (4)

- If the Over-Allotment Option (as defined below) is exercised in full, the total number of Offered Shares under the Offering will be 14,918,145, the total "Price to Public" will be U.S.$ • , the total "Underwriters' Fees" will be U.S.$ • , the total "Net Proceeds to Us" will be U.S.$ • (or C$ • , C$ • and C$ • respectively). The total Net Proceeds to the Selling Shareholders will be unaffected by the exercise of the Over-Allotment Option.

- (5)

- It is anticipated that the Private Investor Warrants (as defined herein) held by Enterprise Partners V. L.P. and Enterprise Partners VI, L.P. will be exercised on the Closing Date pursuant to the cashless exercise feature contained in such Private Investor Warrants. If the exercise of the Private Investor Warrants pursuant to the cashless exercise feature results in the issue of less than 114,366 Common Shares, the number of Treasury Shares offered will be increased by the difference between 114,366 and the total number of Common Shares issued pursuant to the exercise of the Private Investor Warrants held by Enterprise Partners V. L.P. and Enterprise Partners VI, L.P. In any event, the total number of Offered Shares will be no greater than 12,972,300. If the number of Treasury Shares is increased pursuant to the cashless exercise of the Private Investor Warrants, "Net Proceeds to Us" will increase and "Net Proceeds to the Selling Shareholders" will decrease.

There are certain risks associated with an investment in the Offered Shares which prospective purchasers should carefully review and consider. See "Risk Factors" beginning on page 11 of this short form prospectus.

We have granted to the Underwriters an option (the "Over-Allotment Option") allowing the Underwriters to purchase that number of Common Shares representing up to 15% of the Offered Shares sold pursuant to the Offering at the Offering price, for a period of 30 days following the Closing Date (as defined below), to cover over-allotments, if any, and for market stabilization purposes. See "Plan of Distribution". This short form prospectus qualifies both the grant of the Over-Allotment Option and the issuance of Common Shares if the Over-Allotment Option is exercised. A purchaser who acquires Common Shares forming part of the Underwriters' over-allocation position acquires those securities under this short form prospectus, regardless of whether the over-allocation position is ultimately filled through the exercise of the Over-Allotment Option or through secondary market purchases. See "Plan of Distribution".

Underwriters' Position | Maximum size | Exercise period | Exercise price | |||

|---|---|---|---|---|---|---|

Over-Allotment Option | 1,945,845 Common Shares | 30 days following the Closing Date | U.S.$ • per Common Share (C$ • per Common Share) |

Unless otherwise indicated, all information in this short form prospectus is presented without giving effect to the exercise of the Over-Allotment Option.

The Underwriters, as principals, conditionally offer the Offered Shares, subject to prior sale, if, as and when issued by us and if, as and when sold by the Selling Shareholders in accordance with the conditions contained in the Underwriting Agreement referred to under "Plan of Distribution" and subject to the approval of certain legal matters on our behalf by our Canadian counsel Fraser Milner Casgrain LLP and our U.S. counsel DLA Piper LLP (US) and on behalf of the Underwriters by the Underwriters' Canadian counsel Stikeman Elliott LLP and U.S. counsel Paul, Weiss, Rifkind, Wharton & Garrison LLP.

Subject to applicable laws, the Underwriters may, in connection with the Offering, effect transactions that stabilize or maintain the market price of the Common Shares at levels other than those which might otherwise prevail on the open market. Such transactions, if commenced, may be discontinued at any time.The Underwriters may offer the Offered Shares at lower prices than stated above. See "Plan of Distribution".

Subscriptions for the Offered Shares will be received subject to rejection or allotment, in whole or in part, and the right is reserved to close the subscription books at any time without notice. We expect to arrange for an instant deposit of the Offered Shares to or for the account of the Underwriters with The Depositary Trust Company on the date of closing, which is expected to take place on or about October 20, 2009 (the "Closing Date"). In any event, the Offered Shares are to be taken up by the Underwriters, if at all, on or before a date not later than 42 days after the date of the receipt of this final short form base PREP prospectus.

Two of the Selling Shareholders, Enterprise Partners V, L.P. and Enterprise Partners VI, L.P., are incorporated, continued or otherwise organized under the laws of a foreign jurisdiction. Mr. McCormack, a Selling Shareholder, is a U.S. citizen and resides in the U.S. Although such Selling Shareholders have appointed Fraser Milner Casgrain LLP, 99 Bank Street, Suite 1420, Ottawa, Ontario, K1P 1H4 as their agent for service of process in all of the provinces of Canada, except Quebec, it may not be possible for investors to enforce judgments obtained in Canada against such Selling Shareholders.

The enforcement by investors of civil liabilities under United States federal securities laws may be affected adversely by the fact that DragonWave is incorporated under the laws of Canada, that a majority of our officers and directors and experts are residents of Canada, that some or all of the Underwriters or experts named in the registration statement to which this short form prospectus relates are residents of a foreign country and that a substantial portion of our assets and said persons are located outside of the United States.

NEITHER THE SEC NOR ANY STATE OR CANADIAN SECURITIES COMMISSIONS OR SIMILAR REGULATORY AUTHORITY HAS APPROVED OR DISAPPROVED THE OFFERED SHARES OR PASSED UPON THE ACCURACY OR ADEQUACY OF THIS SHORT FORM PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENCE.

Our head and registered office is 411 Legget Drive, Suite 600, Ottawa, Ontario, Canada, K2K 3C9.

In this short form prospectus, unless otherwise specified or the context otherwise requires, all dollar amounts are expressed in Canadian dollars. All references to "dollars", "C$" or "$" are to Canadian dollars and all references to "U.S.$" are to United States dollars. See "Currency Presentation and Exchange Rate Information".

[ALTERNATIVE PAGE FOR CANADIAN PROSPECTUS]

| | Page | |

|---|---|---|

GENERAL MATTERS | iv | |

GLOSSARY OF TECHNICAL TERMS | v | |

CAUTION REGARDING FORWARD-LOOKING STATEMENTS | 1 | |

CURRENCY PRESENTATION AND EXCHANGE RATE INFORMATION | 2 | |

PROSPECTUS SUMMARY | 3 | |

OUR BUSINESS | 3 | |

THE OFFERING | 7 | |

SUMMARY CONSOLIDATED FINANCIAL INFORMATION | 9 | |

RISK FACTORS | 11 | |

OUR BUSINESS | 26 | |

DIRECTORS AND MANAGEMENT | 48 | |

INTERESTS OF MANAGEMENT AND OTHERS IN CERTAIN TRANSACTIONS | 54 | |

DESCRIPTION OF SECURITIES BEING DISTRIBUTED | 55 | |

CONSOLIDATED CAPITALIZATION | 56 | |

USE OF PROCEEDS | 57 | |

DIVIDEND POLICY | 57 | |

SELECTED CONSOLIDATED FINANCIAL INFORMATION | 58 | |

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 60 | |

OPTIONS AND WARRANTS TO PURCHASE SECURITIES | 84 | |

PRIOR SALES | 86 | |

TRADING PRICE AND VOLUME | 87 | |

PRINCIPAL SHAREHOLDERS | 87 | |

SELLING SHAREHOLDERS | 89 | |

PLAN OF DISTRIBUTION | 91 | |

DOCUMENTS INCORPORATED BY REFERENCE | 94 | |

AUDITORS, TRANSFER AGENT AND REGISTRAR | 95 | |

RECONCILIATION TO U.S. GAAP | 95 | |

CERTAIN CANADIAN FEDERAL INCOME TAX CONSIDERATIONS FOR NON-RESIDENTS OF CANADA | 96 | |

CERTAIN UNITED STATES FEDERAL INCOME TAX CONSIDERATIONS FOR U.S. HOLDERS | 97 | |

NASDAQ QUORUM REQUIREMENT | 101 | |

WHERE YOU CAN FIND MORE INFORMATION | 102 | |

ENFORCEABILITY OF CIVIL LIABILITIES | 102 | |

LEGAL MATTERS | 103 | |

EXPERTS | 103 | |

ELIGIBILITY FOR INVESTMENT | 104 | |

PURCHASERS' STATUTORY RIGHTS | 104 | |

PURCHASERS' CONTRACTUAL RIGHT OF ACTION | 104 | |

AUDITORS' CONSENT | 105 | |

AMENDED AUDITED CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEARS ENDED FEBRUARY 28, 2009 AND FEBRUARY 29, 2008 AND AMENDED CONSOLIDATED FINANCIAL STATEMENTS FOR THE THREE MONTH PERIOD ENDED MAY 31, 2009 | F-1 | |

CERTIFICATE OF THE COMPANY | C-1 | |

CERTIFICATE OF THE UNDERWRITERS | C-2 |

iii

Information contained herein is subject to completion or amendment. A registration statement related to these securities has been filed with the Securities and Exchange Commission. These securities may not be sold nor may offers to buy be accepted prior to the time the registration statement becomes effective. This prospectus shall not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of these securities in any State in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such State.

SUBJECT TO COMPLETION, DATED OCTOBER 14, 2009

Preliminary Prospectus

U.S.$ •

12,972,300 Common Shares

This offering (the "Offering") is the initial public offering of the common shares (the "Common Shares") of DragonWave Inc. ("DragonWave", "we", "us", "our" or the "Company") in the United States and includes a new issue of Common Shares in Canada. The Offering consists of a treasury offering of 7,454,050 Common Shares (the "Treasury Shares") by us and a secondary offering by Enterprise Partners V, L.P., Enterprise Partners VI, L.P., Wesley Clover Corporation and Venture Coaches Fund L.P. and certain members of our management (collectively, the "Selling Shareholders") of an aggregate of 5,518,250 Common Shares (the "Secondary Shares", and together with the Treasury Shares, the "Offered Shares"). See "Selling Shareholders". The Offering is being made concurrently in Canada under the terms of this short form prospectus and in the United States under the terms of a registration statement on Form F-10 filed with the United States Securities and Exchange Commission (the "SEC"). Our outstanding Common Shares are listed and posted for trading on the Toronto Stock Exchange (the "TSX") under the symbol "DWI". The TSX has conditionally approved the listing of the Treasury Shares on the TSX. NASDAQ has conditionally approved the listing of the Treasury Shares and our outstanding Common Shares (including the Secondary Shares) on the NASDAQ Global Market under the trading symbol "DRWI". Listing will be subject to our fulfillment of all of the listing requirements of the TSX and NASDAQ, respectively on or before December 23, 2009. On October 13, 2009, the last trading day prior to the filing of this short form prospectus, the closing price of our Common Shares on the TSX was U.S.$10.98 or C$11.31 based on the prevailing U.S.-Canadian dollar exchange rate of U.S.$1.00 = C$1.0298 on October 13, 2009.

Investing in our Common Shares involves a high degree of risk. Before investing, you should read "Risk Factors" beginning on page 11.

This offering of securities is made by a Canadian issuer that is permitted, under a multi-jurisdictional disclosure system ("MJDS") adopted by the United States, to prepare this prospectus in accordance with Canadian disclosure requirements. Prospective investors should be aware that such requirements are different from those of the United States. Financial statements included and incorporated herein have been prepared in accordance with Canadian generally accepted accounting principles, and may be subject to Canadian auditing and auditor independence standards, and thus may not be comparable to financial statements of United States companies.

Prospective investors should be aware that the acquisition of the securities described herein may have tax consequences in both the United States and Canada. This prospectus or any applicable prospectus supplement may not describe these tax consequences fully for investors who are resident in, or citizens of either Canada or the United States. You should consult your tax advisor about the potential tax consequences that may be applicable in your particular circumstances.

The enforcement by investors of civil liabilities under United States federal securities laws may be affected adversely by the fact that DragonWave is incorporated under the laws of Canada, that a majority of our officers and directors and experts are residents of Canada, that some or all of the underwriters or experts named in the registration statement to which this prospectus relates are residents of a foreign country and that a substantial portion of the assets of DragonWave and said persons are located outside of the United States.

NEITHER THE SEC NOR ANY STATE OR CANADIAN SECURITIES COMMISSIONS OR SIMILAR REGULATORY AUTHORITY HAS APPROVED OR DISAPPROVED THE OFFERED SHARES OR PASSED UPON THE ACCURACY OR ADEQUACY OF THIS PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

| | Price to Public(1) | Underwriters' Fees(2) | Net Proceeds to Us(3)(4) | Net Proceeds to the Selling Shareholders | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Per Common Share | U.S.$ • | U.S.$ • | U.S.$ • | U.S.$ • | |||||||||

Total | U.S.$ • | U.S.$ • | U.S.$ • | U.S.$ • | |||||||||

- (1)

- The public Offering price for the Offered Shares offered in the U.S. of U.S.$ • per Common Share is payable in U.S. dollars and the public Offering price of the Offered Shares offered in Canada of C$ • per Common Share is payable in Canadian dollars, except as may otherwise be agreed by the Underwriters. The U.S. dollar amount is the approximate equivalent of such Canadian dollar amount based on the prevailing U.S.-Canadian dollar exchange rate of U.S.$1.00 = C$ • on • , 2009.

- (2)

- The Underwriters will receive a fee of U.S.$ • (5.75%) of the price of the Offered Shares offered hereby, that will be paid in the currency in which we and the Selling Shareholders receive payment for the Offered Shares. See "Plan of Distribution".

- (3)

- Before deducting expenses of the Offering estimated to be U.S.$ • . The expenses of the Offering will be paid solely by us, and the Selling Shareholders will not pay any portion of such expenses, as provided in the Underwriting Agreement (as defined herein). We have agreed to pay all of the expenses of the Offering since the sale of the Secondary Shares has not added materially to the expenses of the Offering. See "Plan of Distribution".

- (4)

- If the Over-Allotment Option (as defined below) is exercised in full, the total number of Offered Shares under the Offering will be 14,918,145, the total "Price to Public" will be U.S.$ • , the total "Underwriters' Fees" will be U.S.$ • , the total "Net Proceeds to Us" will be U.S.$ • . The total Net Proceeds to the Selling Shareholders will be unaffected by the exercise of the Over-Allotment Option.

- (5)

- It is anticipated that the Private Investor Warrants (as defined herein) held by Enterprise Partners V, L.P. will be exercised on the Closing Date pursuant to the cashless exercise feature contained in such Private Investor Warrants. If the exercise of the Private Investor Warrants pursuant to the cashless exercise feature results in the issue of less than 114,366 Common Shares, the number of Treasury Shares offered will be increased by the difference between 114,366 and the total number of Common Shares issued pursuant to the exercise of the Private Investor Warrants held by Enterprise Partners V, L.P. and Enterprise Partners VI, L.P. In any event, the total number of Offered Shares will be no greater than 12,972,300. If the number of Treasury Shares is increased pursuant to the cashless exercise of the Private Investor Warrants, "Net Proceeds to Us" will increase and "Net Proceeds to the Selling Shareholders" will decrease.

Joint Bookrunners

| Canaccord Adams | Piper Jaffray |

| Pacific Crest Securities |

CIBC GMP Securities L.P. RBC Capital Markets Dundee Securities Inc. TD Securities

Two of the Selling Shareholders, Enterprise Partners V, L.P. and Enterprise Partners VI, L.P., are incorporated, continued or otherwise organized under the laws of a foreign jurisdiction. Mr. McCormack, a Selling Shareholder, is a U.S. citizen and resides in the U.S. Although such Selling Shareholders have appointed Fraser Milner Casgrain LLP, 99 Bank Street, Suite 1420, Ottawa, Ontario, K1P 1H4, as their agent for service of process in all of the provinces of Canada, except Quebec, it may not be possible for investors to enforce judgments obtained in Canada against such Selling Shareholders.

The Offered Shares are being offered in Canada by Canaccord Capital Corporation, CIBC World Markets Inc., GMP Securities L.P., RBC Dominion Securities Inc., Dundee Securities Corporation and TD Securities Inc. (the "Canadian Underwriters") and in the United States by Canaccord Adams Inc., Piper Jaffray & Co., Pacific Crest Securities LLC, CIBC World Markets Corp., GMP Securities L.P., Dundee Securities Inc. and TD Securities (USA) LLC (together with the Canadian Underwriters, the "Underwriters"). See "Plan of Distribution".

Information has been incorporated by reference in this prospectus from documents filed with the SEC. Copies of the documents incorporated herein by reference may be obtained on request without charge from the Secretary of DragonWave Inc. at 411 Legget Drive, Suite 600, Ottawa, Ontario, Canada, K2K 3C9, telephone: (613) 599-9991; facsimile: (613) 599-4225 and are also available electronically at www.sedar.com and www.sec.gov.

We have granted to the Underwriters an option (the "Over-Allotment Option") allowing the Underwriters to purchase that number of Common Shares representing up to 15% of the Offered Shares sold pursuant to the Offering at the Offering price, for a period of 30 days following the Closing Date (as defined below), to cover over-allotments, if any, and for market stabilization purposes. See "Plan of Distribution". This prospectus qualifies both the grant of the Over-Allotment Option and the issuance of Common Shares if the Over-Allotment Option is exercised. A purchaser who acquires Common Shares forming part of the Underwriters' over-allocation position acquires those securities under this prospectus, regardless of whether the over-allocation position is ultimately filled through the exercise of the Over-Allotment Option or through secondary market purchases. See "Plan of Distribution".

Underwriters' Position | Maximum size | Exercise period | Exercise price | |||

|---|---|---|---|---|---|---|

| Over-Allotment Option | 1,945,845 Common Shares | 30 days following the Closing Date | U.S.$ • per Common Share |

Unless otherwise indicated, all information in this prospectus is presented without giving effect to the exercise of the Over-Allotment Option.

The Underwriters, as principals, conditionally offer the Offered Shares, subject to prior sale, if, as and when issued by us and if, as and when sold by the Selling Shareholders in accordance with the conditions contained in the Underwriting Agreement referred to under "Plan of Distribution" and subject to the approval of certain legal matters on our behalf by our Canadian counsel Fraser Milner Casgrain LLP and our U.S. counsel DLA Piper LLP (US) and on behalf of the Underwriters by the Underwriters' Canadian counsel Stikeman Elliott LLP and U.S. counsel Paul, Weiss, Rifkind, Wharton & Garrison LLP.

Subject to applicable laws, the Underwriters may, in connection with the Offering, effect transactions that stabilize or maintain the market price of the Common Shares at levels other than those which might otherwise prevail on the open market. Such transactions, if commenced, may be discontinued at any time.The Underwriters may offer the Offered Shares at lower prices than stated above. See "Plan of Distribution".

Subscriptions for the Offered Shares will be received subject to rejection or allotment, in whole or in part, and the right is reserved to close the subscription books at any time without notice. We expect to arrange for an instant deposit of the Offered Shares to or for the account of the Underwriters with The Depositary Trust Company on the date of closing, which is expected to take place on or about October 20, 2009 (the "Closing Date"). In any event, the Offered Shares are to be taken up by the Underwriters, if at all, on or before a date not later than 42 days after the date of the receipt of the final prospectus.

Our head and registered office is 411 Legget Drive, Suite 600, Ottawa, Ontario, Canada, K2K 3C9.

In this prospectus, unless otherwise specified or the context otherwise requires, all dollar amounts are expressed in Canadian dollars. All references to "dollars", "C$" or "$" are to Canadian dollars and all references to "U.S.$" are to United States dollars. See "Currency Presentation and Exchange Rate Information".

| | Page | |

|---|---|---|

GENERAL MATTERS | iv | |

GLOSSARY OF TECHNICAL TERMS | v | |

CAUTION REGARDING FORWARD-LOOKING STATEMENTS | 1 | |

CURRENCY PRESENTATION AND EXCHANGE RATE INFORMATION | 2 | |

PROSPECTUS SUMMARY | 3 | |

OUR BUSINESS | 3 | |

THE OFFERING | 7 | |

SUMMARY CONSOLIDATED FINANCIAL INFORMATION | 9 | |

RISK FACTORS | 11 | |

OUR BUSINESS | 26 | |

DIRECTORS AND MANAGEMENT | 48 | |

INTERESTS OF MANAGEMENT AND OTHERS IN CERTAIN TRANSACTIONS | 54 | |

DESCRIPTION OF SECURITIES BEING DISTRIBUTED | 55 | |

CONSOLIDATED CAPITALIZATION | 56 | |

USE OF PROCEEDS | 57 | |

DIVIDEND POLICY | 57 | |

SELECTED CONSOLIDATED FINANCIAL INFORMATION | 58 | |

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 60 | |

OPTIONS AND WARRANTS TO PURCHASE SECURITIES | 84 | |

PRIOR SALES | 86 | |

TRADING PRICE AND VOLUME | 87 | |

PRINCIPAL SHAREHOLDERS | 87 | |

SELLING SHAREHOLDERS | 89 | |

PLAN OF DISTRIBUTION | 91 | |

DOCUMENTS INCORPORATED BY REFERENCE | 94 | |

AUDITORS, TRANSFER AGENT AND REGISTRAR | 95 | |

RECONCILIATION TO U.S. GAAP | 95 | |

CERTAIN CANADIAN FEDERAL INCOME TAX CONSIDERATIONS FOR NON-RESIDENTS OF CANADA | 96 | |

CERTAIN UNITED STATES FEDERAL INCOME TAX CONSIDERATIONS FOR U.S. HOLDERS | 97 | |

NASDAQ QUORUM REQUIREMENT | 101 | |

WHERE YOU CAN FIND MORE INFORMATION | 102 | |

ENFORCEABILITY OF CIVIL LIABILITIES | 102 | |

LEGAL MATTERS | 103 | |

EXPERTS | 103 | |

AMENDED AUDITED CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEARS ENDED FEBRUARY 28, 2009 AND FEBRUARY 29, 2008 AND AMENDED CONSOLIDATED FINANCIAL STATEMENTS FOR THE THREE MONTH PERIOD ENDED MAY 31, 2009 | F-1 |

iii

Documents incorporated by reference in this short form prospectus include market share information and industry data and forecasts obtained from independent industry publications and surveys. References in such documents to research reports, surveys or articles should not be construed as depicting the complete findings of the entire referenced report, survey or article. The information in any such report, survey or article is not incorporated by reference in this short form prospectus. Although we believe these sources are reliable, we have not independently verified any of the data nor ascertained the underlying economic assumptions relied upon in such reports, surveys or articles. Some data is also based on our estimates, which are derived from our review of our internal surveys, as well as independent sources. We cannot and do not provide any assurance as to the accuracy or completeness of such information. Market forecasts, in particular, are likely to be inaccurate, especially over long periods of time.

Investors should rely only on the information contained in or incorporated by reference in this short form prospectus. Neither we, nor the Selling Shareholders, nor the Underwriters have authorized any other person to provide investors with different information.

Readers should not assume that the information contained in this short form prospectus is accurate as of any date other than the date on the front of this short form prospectus, unless otherwise noted herein or as required by law. It should be assumed that the information appearing in this short form prospectus and the documents incorporated by reference herein is accurate only as of their respective dates. Our business, financial condition, results of operations or prospects may have changed since those dates.

Certain terms and phrases used in this short form prospectus are defined in the "Glossary of Technical Terms".

Unless indicated otherwise, all information in this short form prospectus is presented without giving effect to the exercise of the Over-Allotment Option.

Information contained on our website, www.dragonwaveinc.com, is not part of this short form prospectus and is not incorporated herein by reference and may not be relied upon by prospective purchasers for the purpose of determining whether to invest in the Offered Shares offered under this short form prospectus.

iv

"2G": refers to the second generation family of standards for mobile wireless communications, based on GSM or CDMA technologies.

"3G+": refers to the third generation family of standards for wireless communication for mobile voice and data communications established by the International Telecommunications Union ("ITU") as well as fourth generation (4G) standards still being defined. 3G+ includes such advanced all-IP wireless networking technologies as HSPA, WiMAX and LTE. The 3G+ family of standards enable concurrent use of voice and other data services such as enhanced multimedia (Internet, email, video and other data) at broadband transmission speed, and roaming capability. 3G+ networks enable network operators to offer users a wider range of more advanced services while achieving greater network capacity through improved spectral efficiency.

"ATPC": is an acronym for "automatic transmit power control", a technique used to reduce the level of radio signal interference between communications systems. The ATPC reduces transmitter power during clear weather when the path attenuation is low and increases transmitter power during rain, when the path attenuation increases.

"backhaul": refers to the means by which information (or data) is carried from a radio access network wireless base station or other collection point to a core network node, from which it can be transported over the high capacity fiber optic network.

"broadband": refers to a telecommunication technology in which a wide band of frequencies is available to transmit information. Where a wide band of frequencies is available, information can be multiplexed and sent on many different frequencies or channels within the band concurrently. This allows more information to be transmitted in a given amount of time.

"CCTV": is an acronym for "closed circuit television", the use of video cameras to transmit a signal to a specific place, on a limited set of monitors. More generally, CCTV refers to the use of video for surveillance applications.

"CDMA": is an acronym for "code division multiple access", a channel access method utilized by various radio communications technologies.

"DEMS": is an acronym for "digital electronic messaging services", a wireless service providing local broadband data transmission.

"DS3": is an acronym for "digital signal 3", a high-speed TDM circuit for data connectivity equivalent in bandwidth to 28 T1 lines (45 Mbps).

"DSL": is an acronym for "digital subscriber line", a technology for bringing high-bandwidth Internet connectivity to homes and small businesses over ordinary copper telephone lines.

"E1": refers to a 2.0 Mbps point-to-point dedicated digital circuit typically provided by the telephone companies. This is a standard interface used mostly outside the United States.

"EDGE": refers to Enhanced Data rates for GSM Evolution, a digital mobile communications technology that allows increased data transmission rates and improved data transmission reliability. EDGE is generally classified as a '2.75G' mobile wireless technology.

"Ethernet": refers to a common method of networking computers in a local area network (or LAN) and is specified in an IEEE standard, IEEE 802.3.

"EV-DO": refers to Evolution-Data Optimized, a 3G+ wireless radio broadband data standard based upon the CDMA access scheme that enables faster speeds than are available in early CDMA networks or other 2G services, such as GPRS or EDGE. EV-DO was designed as an evolution of the CDMA2000 standard that would support high data rates and could be deployed alongside a wireless carrier's voice services. "1xEV-DO Rev A" and "EV-DO Rev B" refer to different revisions of this CDMA-based technology.

"FOMA": is an acronym for "freedom of mobile multimedia access", the brand name of a CDMA-based 3G+ telecommunications service offered by the Japanese telecommunications service provider NTT DoCoMo. FOMA is an implementation of UMTS and was one of the world's first 3G+ services to commence operation.

v

"FPGA": is an acronym for "field-programmable gate array", a semiconductor device that can be configured by the customer or designer after manufacturing. FPGAs are programmed to specify how the chip will work. FPGAs can be used to implement any logical function that an application-specific integrated circuit (or ASIC) could perform, but the ability to update the functionality after shipping offers advantages for many applications.

"Gbps": is an acronym for "billions of bits per second" or "gigabits per second", a measure of bandwidth (the total information flow over a given time) on a telecommunications medium.

"GHz": is an abbreviation of "gigahertz", frequencies in the billions of cycles per second range. In radio communications, GHz is used to define the size of radio bands in the electromagnetic spectrum.

"Gigabit Ethernet" or "GigE": refers to a transmission technology based on the Ethernet protocol used in LANs which provides a data rate of 1 billion bits per second (one gigabit).

"GPRS": is an acronym for "general packet radio service", a packet-oriented mobile data service available to users of the 2G cellular communication systems GSM, as well as in certain 3G+ technologies and network standards.

"GSM": is an acronym for "global system for mobile communications", a cellular network technology and the most common standard for mobile phones globally.

"HSDPA": is an acronym for "high speed download packet access", a 3G+ mobile telephony communications protocol in the HSPA family, which allows networks based on UMTS to increase data capacity and increase transfer rates.

"HSPA" is an acronym for "high speed packet access", a family of high-speed 3G+ digital data services provided by cellular carriers worldwide based on GSM technology. HSPA service works with HSPA handsets as well as laptops and other portable devices with HSPA modems. The two established standards of HSPA are HSDPA and HSUPA.

"HSUPA": is an acronym for "high speed upload packet access", a 3G+ mobile telephony protocol in the HSPA family that improves the performance of uplink dedicated transport channels to increase uplink data capacity and increase transfer rates.

"IEEE": is an acronym for "Institute of Electrical and Electronics Engineers", a U.S.-based organization of engineers, scientists and students involved in electrical, electronics, and related fields. IEEE also functions as a publishing house and standards making body.

"IF": is an acronym for "intermediate frequency", a frequency between the base band and RF frequency that is used in communications between a modem and a radio.

"IP" or "Internet Protocol": refers to a standardized method of transporting information across the Internet in packets of digital data.

"ISM": is an acronym for "industrial, scientific and medical", a part of the radio spectrum that can be used for specific applications such as point-to-point communications without a license in most countries.

"LMDS": is an acronym for "local multipoint distribution systems", a system for broadband fixed microwave wireless transmission direct from a local antenna to homes and businesses within line-of-sight.

"LTE" is an acronym for "long term evolution", an advanced 3G+ all-IP technology for both GSM and CDMA cellular service providers for which initial deployments are expected in the 2010 time frame. Approved in 2008, LTE is expected to enable typical download speeds of approximately 6 Mbps, a considerably higher bandwidth than HSPA (evolved from GSM) and EV-DO (evolved from CDMA) technologies.

"Mbps": is an acronym for "millions of bits per second" or "megabits per second", a measure of bandwidth (the total information flow over a given time) on a telecommunications medium.

"MHz": is an abbreviation of "megahertz", frequencies in the millions of cycles per second range. In radio communications, MHz is used to define the size of radio bands in the electromagnetic spectrum.

"ms": is an abbreviation of "millisecond".

vi

"multiplexer": refers to a device that can send several signals over a single line. The signals are then separated by a similar device at the other end of the link.

"native Ethernet": refers to systems that are designed to transport Ethernet directly rather than adapting Ethernet to existing SONET/SDH or PDH transport systems.

"PDA": is an acronym for "personal digital assistant", a lightweight handheld consumer electronic device that performs basic computing tasks such as diary and personal database management.

"PDH": is an acronym for "plesiochronous digital hierarchy", the data rates and formats used in telecommunications equipment and described in International Telecommunications Standard G 920. Common data rates include 1.5 Mbps (or T1) and 2.0 Mbps (or E1).

"points of presence": refers to a site that houses a service provider's telecommunication equipment such as a switching system or a facility node.

"pseudowire technology": refers to technology that allows a communications service provider or network operator to package any network service, legacy or emerging, and send it into the network in a format that both preserves the service's original features and delivers the values of end-to-end OAM&P (operations, administration, maintenance and provisioning), statistical multiplexing, and unified management.

"RF": is an acronym for "radio frequency", the range of electromagnetic frequencies above the audio range and below visible light. All broadcast transmissions, from AM radio to satellites, fall into this range, which is between 30 kilohertz and 300 GHz.

"SDH": is an acronym for "synchronous digital hierarchy", the data rates and formats used in telecommunications equipment and described in International Telecommunications Union standard G.823. Common data rates include 155 Mbps (or STM1) and 622 Mbps (or STM4).

"SNMP": is an acronym for "simple network management protocol", a protocol for exchanging management information and commands across a network between a management computer and a managed device.

"SONET": is an acronym for "synchronous optical network", the data rates and formats used in telecommunications equipment and described in American National Standards Institute standard GR-253-CORE. Common data rates include 155 Mbps (or OC3) and 622 Mbps (or OC12).

"T1": refers to a 1.544 Mbps point-to-point dedicated digital circuit provided by telephone companies.

"Tbps": is an acronym for "tera bits per second", a measure of bandwidth (the total information flow over a given time) on a telecommunications medium.

"TDM": is an acronym for "time division multiplexing", a scheme in which numerous signals are combined for transmission on a single communications line or channel.

"topology": refers to the physical or logical connectivity of a network.

"UMTS": is an acronym for "universal mobile telecommunications system", a 3G+ mobile telecommunications technology and standard specified by the 3rd Generation Partnership Project (or 3GPP) and the ITU-IMT-2000.

"VLAN": is an acronym for "virtual local area network", a group of hosts with a common set of requirements that communicate as if they were attached to the broadcast domain, regardless of their physical location. A VLAN has the same attributes as a physical local area network, but allows for end stations to be grouped together even if they are not located on the same network switch. In a VLAN, network reconfiguration can be performed through software instead of physically relocating devices.

"VoIP": is an acronym for "voice over internet protocol", a category of hardware and software that enables the use of the Internet as the transmission medium for telephone calls.

"WiFi": is an acronym for "wireless fidelity", a set of product compatibility standards for wireless local area networks (or WLANs) based on the IEEE 802.11 standard. WiFi operates in unlicensed frequency bands.

"WiMAX": is an acronym for "worldwide interoperability for microwave access", a set of product compatibility standards for wireless metropolitan-area networks based on the IEEE 802.16 standard.

vii

The following is a summary of the principal features of this Offering and should be read together with the more detailed information and financial data contained elsewhere in this short form prospectus, including the documents incorporated by reference in this short form prospectus. Prospective purchasers should carefully consider, among other things, the matters discussed in "Risk Factors" beginning on page 11 of this short form prospectus.

CAUTION REGARDING FORWARD-LOOKING STATEMENTS

This short form prospectus contains or incorporates by reference certain information that may constitute "forward-looking information" and "forward-looking statements" within the meaning of applicable Canadian and United States securities laws. All forward looking information and forward-looking statements are necessarily based on a number of estimates and assumptions that are inherently subject to significant business, economic and competitive uncertainties and contingencies. All statements other than statements which are reporting results as well as statements of historical fact set forth or incorporated herein by reference, are forward-looking statements that may involve a number of known and unknown risks, uncertainties and other factors; many of which are beyond our ability to control or predict. Forward-looking statements include, without limitation, statements regarding strategic plans, future production, sales and revenue estimates, cost estimates and anticipated financial results, capital expenditures and objectives. These statements relate to analysis and other information that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements.

Forward-looking statements, which involve assumptions and describe our future plans, strategies and expectations, are generally identifiable by use of the words "may", "will", "should", "continue", "expect", "anticipate", "estimate", "believe", "intend", "plan" or "project" or the negative of these words or other variations on these words or comparable terminology. There can be no assurance that such statements will prove to be accurate and actual results and future events could differ materially from those anticipated in such statements. The following are some of the important factors that could cause actual results or outcomes to differ materially from those discussed in the forward-looking statements:

- •

- our dependence on the development and growth of the market for high-capacity wireless communications services;

- •

- our reliance on a small number of customers for a large percentage of revenue;

- •

- intense competition from several competitors;

- •

- competition from indirect competitors;

- •

- our dependence on our ability to develop new products and enhance existing products;

- •

- our history of losses;

- •

- our ability to successfully manage growth;

- •

- quarterly revenue and operating results which are difficult to predict and can fluctuate substantially;

- •

- the impact of the general economic downturn on our customers;

- •

- disruption resulting from economic and geopolitical uncertainty;

- •

- currency fluctuations;

- •

- our exposure to credit risk for accounts receivable;

- •

- pressure on our pricing models;

- •

- the allocation of radio spectrum and regulatory approvals for our products;

- •

- the ability of our customers to secure a license for applicable radio spectrum;

- •

- changes in government regulation or industry standards that may limit the potential market for our products;

1

- •

- our dependence on establishing and maintaining relationships with channel partners;

- •

- our reliance on outsourced manufacturing;

- •

- our reliance on suppliers of components;

- •

- our ability to protect our own intellectual property and potential harm to our business if we infringe the intellectual property rights of others;

- •

- risks associated with software licensed by us;

- •

- a lengthy and variable sales cycle;

- •

- our dependence on ability to recruit and retain management and other qualified personnel;

- •

- our exposure to risks resulting from our international sales and operations, including the requirement to comply with export control and economic sanctions laws;

- •

- our ability to successfully effect acquisitions of products or businesses; and

- •

- product defects, product liability claims, or health and safety risks relating to wireless products.

Although we have attempted to identify important factors that could cause our actual results to differ materially from expectations, intentions, estimates or forecasts, there may be other factors that could cause our results to differ from what we currently anticipate, estimate or intend. Recent unprecedented events in global financial and credit markets have resulted in high market price volatility and contraction in credit markets. These on-going events could impact forward-looking statements contained in this short form prospectus and in the documents incorporated herein by reference in an unpredictable and possibly detrimental manner. In light of these risks, uncertainties and assumptions, the forward-looking events described in this short form prospectus and the documents incorporated by reference might not occur or might not occur when stated.

Forward-looking statements made in a document incorporated by reference in this short form prospectus are made as at the date of the original document and have not been updated by us except as expressly provided for in this short form prospectus. Except as required under applicable securities legislation, we undertake no obligation to publicly update or revise forward-looking statements, whether as a result of new information, future events or otherwise.

CURRENCY PRESENTATION AND EXCHANGE RATE INFORMATION

In this short form prospectus, unless otherwise specified or the context otherwise requires, all dollar amounts are expressed in Canadian dollars. All references to "dollars", "C$" or "$" are to Canadian dollars and all references to "U.S.$" are to United States dollars. For the amounts referenced under "Use of Proceeds" and "Plan of Distribution", the rate of exchange was U.S.$1.00=C$ • or C$1.00=U.S.$ • , each based on the Bank of Canada's noon exchange rate for • .

The following table sets out (1) the high and low rate of exchange for one Canadian dollar in U.S. dollars during the indicated periods, (2) the average of the rate of exchange on the last business day of each month during those periods, and (3) the exchange rate in effect as at the end of each of those periods, each based on the noon rate published by the Bank of Canada.

| | High | Low | Average | End of Period | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Three Month Periods ended August 31, | ||||||||||||||

2009 | 0.9358 | 0.8580 | 0.8981 | 0.9118 | ||||||||||

2008 | 0.9987 | 0.9365 | 0.9738 | 0.9411 | ||||||||||

Three Month Periods ended May 31, | ||||||||||||||

2009 | 0.9123 | 0.7692 | 0.8246 | 0.9123 | ||||||||||

2008 | 1.0161 | 0.9729 | 0.9949 | 1.0058 | ||||||||||

Fiscal Years Ended | ||||||||||||||

February 28, 2009 | 1.0161 | 0.7711 | 0.9133 | 0.7870 | ||||||||||

February 29, 2008 | 1.0905 | 0.8467 | 0.9588 | 1.0206 | ||||||||||

2

PROSPECTUS SUMMARY

OUR BUSINESS

Overview

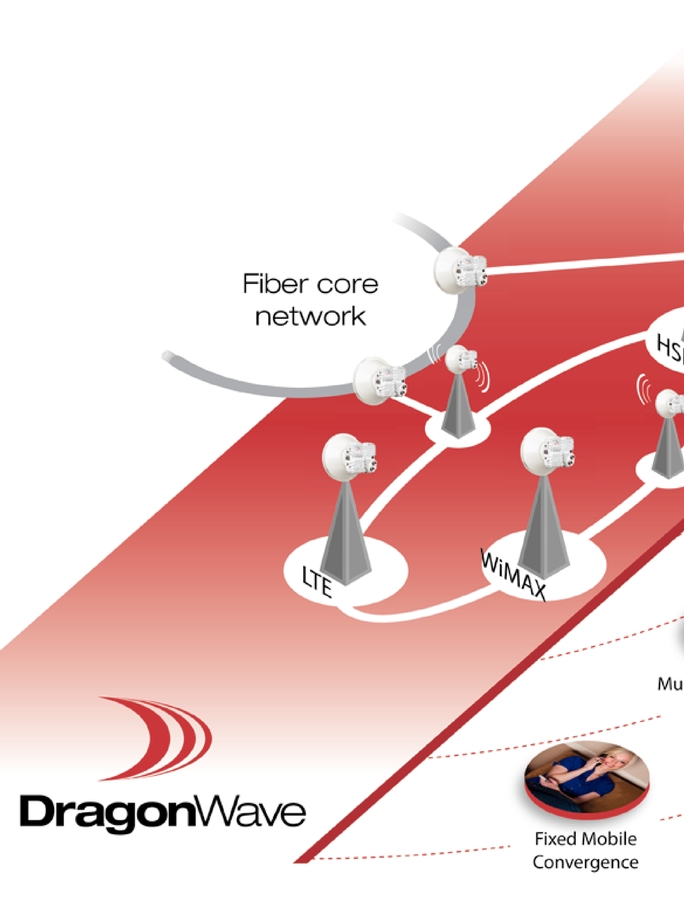

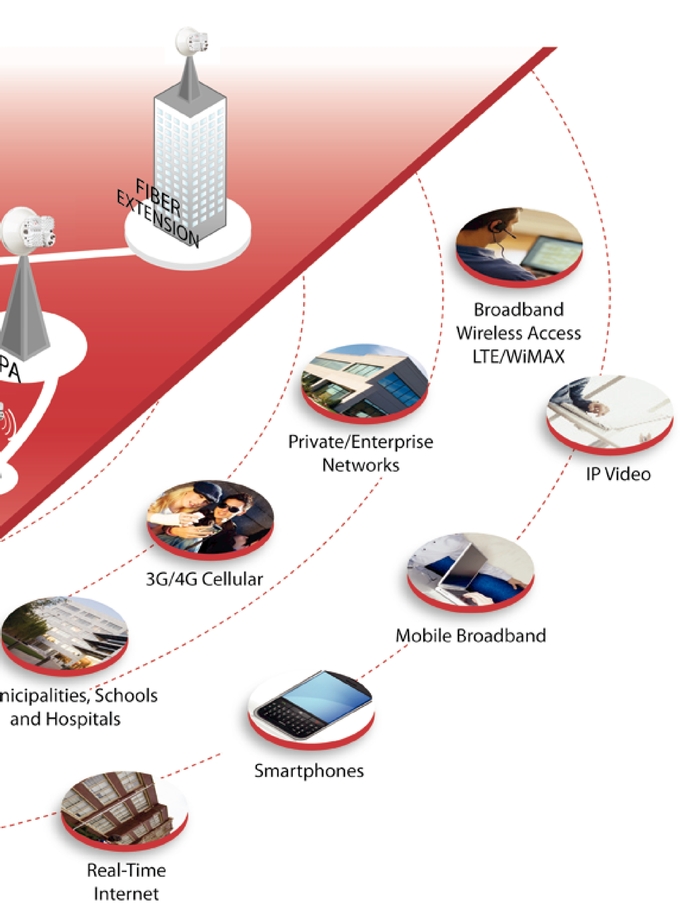

We are a leading provider of high-capacity Ethernet microwave equipment used in emerging IP networks. We design, develop, market and sell proprietary, carrier-grade microwave networking equipment, or links, that wirelessly transmit broadband voice, video and other data between two points. Our Ethernet microwave links, which are based on a native Ethernet platform, function as a wireless extension to an existing fiber optic core telecommunications network. Our products principally perform the backhaul function in a communication service provider's network, connecting high traffic points of aggregation such as high-capacity wireless base stations (3G+ wireless networks, including HSPA, WiMAX and LTE-based systems) and large `out of territory' enterprises to nodes on the fiber optic core network.

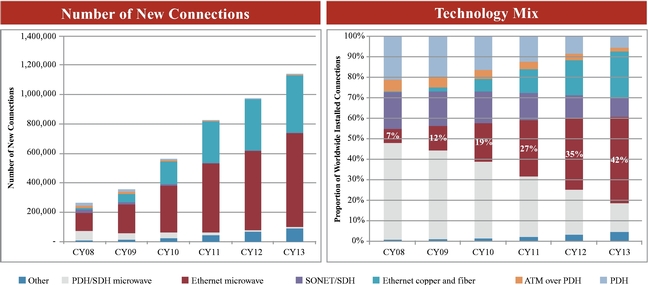

We target principally the global wireless communications service provider market and, in particular, service providers offering high-capacity wireless communication services, including 3G+ wireless service providers. At the end of our most recent fiscal year, we had shipped approximately 9,500 product units and our customer base included more than 250 customers worldwide in 56 countries. Our customers include Clearwire Corporation ("Clearwire"), which has launched the world's most advanced mobile WiMAX deployment, as well as Globalive Wireless Management Corp. ("Globalive"), which has selected our products for deployment in Globalive's North American 3G+ (HSPA) cellular network in support of its wireless services offered in the Canadian market under the brand name WIND. Based on our review of published United States Federal Communications Commission ("FCC") data, in 2008 we had the largest U.S. market share, at 32%, in combined 6, 11, 18 and 23 GHz links, and in 2008 we increased our market share in the U.S. market for 18 and 23 GHz bands to 46%.

Our revenue for the three months ended May 31, 2009 was $16.0 million, representing an increase of 49% or $5.2 million compared to the same period in the previous fiscal year. Revenue growth was driven by the acceleration of network deployment by Clearwire, as well as by overall increased sales activity. In the fiscal year ended February 28, 2009, our revenue was $43.3 million, representing an increase of 7.3% or $2.9 million compared to the previous fiscal year.

Industry Background

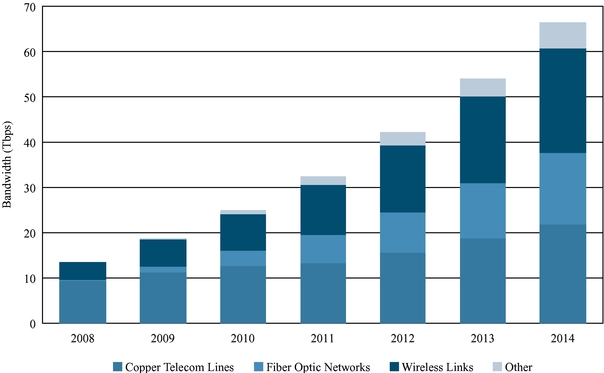

There are two key trends driving the increased demand for our products: increased demand for backhaul capacity and IP convergence. Demand for backhaul capacity is predicted to experience strong growth. According to a 2009 research report prepared by ABI Research titled "Mobile Backhaul — Global Market Analysis and Forecast (CAPEX and Lease Revenue Opportunities for Carrier Ethernet, Microwave, MPLS-TE, PBB-TE, TDM and Cable Backhaul Solutions)" (the "ABI Report"), global demand for backhaul capacity is expected to grow by almost five times from 2008 to 2014 (from 13.51 Tbps in 2008 to 66.49 Tbps in 2014), representing a compound annual growth rate of 30%. We believe the following factors are key drivers of demand for increased backhaul capacity:

- •

- Increasing Functionality of Mobile Devices and Capacity at the Edge of Wireless Networks. Access technologies currently being deployed or planned, including WiMAX, HSPA and LTE, in concert with the availability of sophisticated mobile devices, including smartphones, data cards and netbooks, significantly increase bandwidth demand per user within mobile networks.

- •

- Shift in Demand from Voice to Multimedia Content and Services in Mature Markets. Service providers in areas with mature subscriber bases are attempting to increase average revenue per user, or ARPU, by offering data services such as e-mail, web browsing, music and video downloading and other Internet related services, as well as mobile video services.

- •

- Increasing Demand for Wireless Coverage in Emerging Markets. As early broadband and wireless markets have matured, growth of broadband and wireless subscribers is shifting to emerging markets in developing countries and rural areas. In rural areas of the United States, some deployments are expected

3

- •

- Increase in Global Wireless Communications Subscribers. According to the ABI Report, the number of cellular subscribers globally is expected to increase from more than 4 billion at the end of 2008 to approximately 5.9 billion by the end of 2014.

- •

- Global Investment in Wireless Access Network Spectrum. There have been numerous auctions around the world of radio spectrum that is used in wireless access networks. The purchasers of this spectrum require backhaul solutions such as ours.

to receive government funding or other support through the U.S.$7.2 billion rural broadband stimulus package.

With the dramatic increase in mobile data, service providers are increasingly looking to integrate all communications traffic, including voice, video and other data traffic, onto a single, unified IP-based network. IP convergence enables service providers to carry more volume and types of data on a single network, improving efficiency, lowering network costs and giving service providers the ability to offer more advanced services. Advanced wireless networks such as certain 3G+ networks will utilize IP-based platforms and are expected to utilize the superior backhaul efficiencies of carrier-grade Ethernet equipment that supports scalability, high-availability, legacy TDM traffic support and service management.

Our Solutions

We believe our Ethernet microwave links are an attractive alternative to other backhaul solutions such as leased lines and fiber optic cable deployments. The key characteristics of our solutions are as follows:

- •

- Ethernet Microwave. Our products are based on a native Ethernet design which delivers high efficiency, low latency and full support for Ethernet data transport features. The advantages of Ethernet are lower price points when compared to SONET or SDH alternatives, more efficient transport due to the ability to perform statistical multiplexing, traffic priority management and fine bandwidth control.

- •

- High-Capacity and Scalable. Our products feature Gigabit Ethernet transport with link speeds up to 4 Gbps. The capacity of our Ethernet microwave links can be remotely controlled using our Flex software to match network demands without the need for site visits to upgrade hardware.

- •

- High Availability. Our products deliver 99.999% availability using Ethernet networking through a combination of equipment reliability and network level redundancy, including support for ring / mesh architectures. Our proprietary rapid link shutdown feature provides SONET-like failover speeds with low-cost Ethernet switching.

- •

- Cost Competitive. Our proprietary surface mount designs and manufacturing processes enable us to offer a cost competitive product compared with those that rely on conventional microwave manufacturing techniques. We deliver scalable bandwidth managed in 10 Mbps increments, providing our customers with an attractive `pay as you grow' approach.

- •

- Support for Legacy Networking Standards. Our Service Delivery Unit, or SDU, supports pseudowire, a technology that emulates the essential attributes of legacy TDM services over an IP switched network. Our SDU allows our customers to continue offering revenue-generating legacy services, while making a smooth transition to more efficient IP-based networks.

- •

- Network Management and Planning. Our products use industry standard simple network management protocol, or SNMP, rather than costly, proprietary network management systems. This significantly reduces the cost to service providers of integrating our product into their networks. We also offer deployment planning services to assist our customers in the design of their networks and the deployment of our products.

Clearwire Relationship

Clearwire is an alternative mobile network operator using pre-WiMAX and WiMAX 802.16 E-2005 technology to deliver mobile, fixed and nomadic Internet services to its subscribers in the United States and

4

Europe in the 2.5 GHz and 3.5 GHz frequency bands, respectively. In 2008, Clearwire Corporation was formed through the combination of Clearwire LLC and certain Sprint WiMAX network and 2.5 GHz assets and operations. These wireless assets were combined with investments from Intel Capital Corp., Google Inc., Comcast Corp., Time Warner Cable Inc. and Bright House Networks LLC. Clearwire has since announced plans to launch WiMAX networks in more than 80 markets, with the objective of expanding coverage to 120 million subscriber points of presence by the end of 2010. Clearwire has also announced that as of March, 2009, it had markets covering 75 million people under development and construction, with some of these markets launching later in 2009 and others in 2010. Clearwire also stated in March, 2009 that it was working on the long lead time low-cost site acquisition zoning and permitting work for the markets covering the remaining 45 million people over the course of 2009, and most recently announced (in August, 2009) that it has more than 20,000 cell sites under development. Clearwire has deployed wireless networks in multiple markets across North America using our Ethernet microwave links, and we are currently the primary supplier of licensed microwave equipment to Clearwire.

Our Growth Strategy

Our objective is to strengthen our position as a global leader in high-capacity Ethernet microwave communication equipment that enables the transition by wireless service providers to high-capacity all-IP networks. In order to accomplish this goal, we aim to leverage our technological leadership, broaden our market penetration, and demonstrate competitiveness for deployment with key customers in multiple radio access network types such as WiMAX, HSPA and LTE. The specific elements of our growth strategy are as follows:

- •

- Continue Product Development Investment. We believe that our growth to date has been, in large part, due to our product development focus on high-capacity Ethernet microwave equipment. We intend to continue to develop products to address market requirements in various applications and geographic markets around the world.

- •

- Expand Geographical Reach. We intend to build on our leading U.S. market share and our current international market penetration to expand our geographical reach. This multi-faceted strategy includes increasing global direct sales activities, expanding our distributor, value added reseller ("VAR") and original equipment manufacturer ("OEM") arrangements around the globe and investing in training and tools for our international distribution partners.

- •

- Capitalize on Broadband Stimulus Funding. The U.S. government has recently announced substantial funding of new rural broadband initiatives under the American Recovery and Reinvestment Act of 2009 totaling U.S.$7.2 billion in grants and loans. We believe that broadband stimulus funding of rural projects represents a significant opportunity for us to develop new and expanded markets for our backhaul transport solutions.

- •

- Continue to Focus on Operational Excellence and Deliver Effective Customer Service and Support. We intend to continue to focus on improving product quality, reducing delivery time, reducing costs, streamlining manufacturing processes and optimizing inventories. This focus on operational excellence has allowed us to significantly reduce our manufacturing costs and shorten our delivery time.

- •

- Review Selective Strategic Acquisitions. We intend to selectively review opportunities to acquire companies or technologies that complement our existing product portfolio and market reach.

Recent Developments

On September 14, 2009, we introduced Horizon Quantum, our newest product designed to provide significantly increased bandwidth capacity of up to 4 Gbps per link in a half-rack-unit device incorporating a bandwidth accelerator feature that enables superior spectral efficiency by up to a factor of 2.5 times as compared to conventional systems. Shipments of Horizon Quantum are scheduled to commence by the end of 2009.

5

Corporate Information

We were incorporated on February 24, 2000 by a Certificate and Articles of Incorporation issued under theCanada Business Corporations Act. Our head and registered office is 411 Legget Drive, Suite 600, Ottawa, Ontario, Canada, K2K 3C9.

Unless otherwise noted or the context otherwise indicates, the terms "DragonWave", "we", "us", "our" and the "Company" refer to DragonWave Inc. and its wholly-owned subsidiaries DragonWave Corp. and 4472314 Canada Inc.

This short form prospectus contains company names, logos, trade names, trademarks and service marks of DragonWave and other organizations, all of which are the property of their respective owners.

6

Common Shares offered by us: | 7,454,050 Common Shares | |

Common Shares offered by the Selling Shareholders: | 5,518,250 Common Shares | |

Offering price: | U.S.$ • (C$ • ) per Common Share | |

Size of Offering: | U.S.$ • (C$ • Common Shares) | |

Common Shares Outstanding Assuming Completion of the Offering: | 36,209,978 Common Shares. This represents immediate dilution of 21% for existing holders of Common Shares. The number of Common Shares and the dilution calculation assume the exercise of the Private Investor Warrants (as defined herein) held by Enterprise Partners V, L.P. and Enterprise Partners VI, L.P. but assume no exercise of the Underwriters' Over-Allotment Option or any other options or warrants described in "Options and Warrants to Purchase Securities". See "Consolidated Capitalization". | |

Offering Type: | Offering in the U.S. under the MJDS and in each of the provinces of Canada, except the province of Quebec. | |

Use of Proceeds: | We expect to use the net proceeds of the sale of the Treasury Shares as follows: | |

(i) as to approximately U.S.$ • (C$ • ) (40% of the net proceeds), to strengthen our balance sheet in preparation for new mobile broadband network deployments and to better position us to be selected as an equipment vendor for large network service providers; | ||

(ii) as to approximately U.S.$ • (C$ • ) (30% of the net proceeds), to fund working capital requirements associated with accelerating sales and production of our products; | ||

(iii) as to approximately U.S.$ • (C$ • ) (20% of the net proceeds), to continue to fund our efforts to increase sales penetration in regions outside North America, including increasing global direct sales activity, expanding our distribution, VAR and OEM network, and providing training and support to strengthen the systems engineering and support organizations of our VARs and OEMs. We also plan to invest in human resources and supporting infrastructure to support this effort; and | ||

(iv) as to the balance, to provide an available source of funding for potential future acquisition opportunities. | ||

Over-Allotment Option: | We have granted the Underwriters an option to purchase up to an additional 1,945,845 Common Shares (equal to 15% of the Offered Shares) at the Offering price, exercisable during the period ending 30 days after the closing of this Offering to cover over-allotments, if any, and for market stabilization purposes. See "Plan of Distribution". | |

Dividend Policy: | We have never paid dividends and do not anticipate paying dividends in the foreseeable future. See "Dividend Policy". |

7

| Selling Shareholders: | Enterprise Partners V, L.P., Enterprise Partners VI, L.P., Wesley Clover Corporation, Venture Coaches Fund L.P. and certain members of our management (namely, Peter Allen, Erik Boch, David Farrar, Russell Frederick, Brian McCormack and Alan Solheim). | |

Listing: | The outstanding Common Shares are listed and posted for trading on the TSX under the symbol "DWI". The TSX has conditionally approved the listing of the Treasury Shares on the TSX. NASDAQ has conditionally approved the listing of the Treasury Shares and our outstanding Common Shares (including the Secondary Shares) on the NASDAQ Global Market under the trading symbol "DRWI". Listing will be subject to our fulfillment of all of the listing requirements of the TSX and NASDAQ, respectively, on or before December 23, 2009. | |

Risk Factors: | An investment in Common Shares is speculative and involves a high degree of risk. Each purchaser should carefully consider the information set out under "Risk Factors" beginning on page 11 and the other information in this short form prospectus before purchasing Common Shares. |

The number of Common Shares to be offered by us and the number of Common Shares to be outstanding are based on the number of Common Shares outstanding as of October 13, 2009 plus the number of Common Shares issuable on the exercise of the Private Investor Warrants held by Enterprise Partners V, L.P. and Enterprise Partners VI, L.P. Unless we specifically state otherwise, the information in this short form prospectus:

- •

- is based on the assumption that the Underwriters will not exercise the Over-Allotment Option;

- •

- excludes 2,175,917 Common Shares reserved for issuance upon the exercise of options outstanding as of October 13, 2009 at a weighted average exercise price of $2.93 per Common Share; and

- •

- excludes 137,654 Common Shares reserved for issuance upon the exercise of warrants outstanding as of October 13, 2009 (other than the Private Investor Warrants held by Enterprise Partners V, L.P. and Enterprise Partners VI, L.P. which will be exercised in connection with this Offering) at a weighted average exercise price of $5.25 per Common Share.

See "Options and Warrants to Purchase Securities".

8

SUMMARY CONSOLIDATED FINANCIAL INFORMATION