QuickLinks -- Click here to rapidly navigate through this document

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

The following provides management's discussion and analysis ("MD&A") of DragonWave Inc.'s consolidated results of operations and financial condition for three and six months ended August 31, 2010. This MD&A is dated October 7, 2010 and should be read in conjunction with our unaudited consolidated interim financial statements for the three and six months ended August 31, 2010, including the notes thereto. For additional information and details, readers are referred to the audited annual consolidated financial statements, and corresponding note, and our MD&A for fiscal 2010, our Annual Information Form dated May 6, 2010 (the "AIF"), all of which are filed separately and are available atwww.sedar.com orhttp://www.sec.gov/edgar/searchedgar/companysearch.html.

The financial statements have been prepared in accordance with Canadian generally accepted accounting principles (GAAP) and are reported in US dollars. The information contained herein is dated as of October 7, 2010 and is current to that date, unless otherwise stated. Our fiscal year commences March 1 of each year and ends on the last day of February of the following year.

In this document, "we", "us", "our", "Company" and "DragonWave" all refer to DragonWave Inc. collectively with its subsidiaries, DragonWave Corp. and 4472314 Canada Inc. The content of this MD&A has been approved by our Board of Directors, on the recommendation of its Audit Committee.

Unless otherwise indicated, all currency amounts referenced in this MD&A are denominated in US dollars.

Forward-Looking Statements

This MD&A contains "forward-looking information" and "forward-looking statements" within the meaning of applicable Canadian and U.S. securities laws. All statements in this MD&A other than statements that are reporting results or statements of historical fact are forward-looking statements which involve assumptions and describe our future plans, strategies and expectations. Forward-looking statements are generally identifiable by use of the words "may", "will", "should", "continue", "expect", "anticipate", "estimate", "believe", "intend", "plan" or "project" or the negative of these words or other variations on these words or comparable terminology. Forward-looking statements include, without limitation, statements regarding our strategic plans and objectives, growth strategy, customer diversification and expansion initiatives, and the expected use of proceeds from financing activities. There can be no assurance that forward-looking statements will prove to be accurate and actual results or outcomes could differ materially from those expressed or implied in such statements. Important factors that could cause actual results or outcomes to differ materially from those discussed in the forward-looking statements are discussed in this MD&A under the heading "Risks and Uncertainties". Forward-looking statements are provided to assist external stakeholders in understanding management's expectations and plans relating to the future as of the date of this MD&A and may not be appropriate for other purposes. Readers are cautioned not to place undue reliance on forward-looking statements. Forward-looking statements are made as of the date of this MD&A and the Company does not undertake to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except to the extent expressly required by law.

2

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

Risks and Uncertainties

Our financial performance, achievements and results may be impacted by risks and uncertainties related to our business. These risks and uncertainties include, but are not limited to the following:

- •

- dependence on the development and growth of the market for high-capacity wireless communications services;

- •

- reliance on a small number of customers for a large percentage of revenue;

- •

- intense competition from several competitors;

- •

- competition from indirect competitors;

- •

- dependence on the ability to develop new products and enhance existing products;

- •

- a history of losses;

- •

- our ability to successfully manage growth;

- •

- quarterly revenue and operating results which are difficult to predict and can fluctuate substantially;

- •

- the impact of the general economic downturn on our customers;

- •

- disruption resulting from economic and geopolitical uncertainty;

- •

- ability to successfully effect acquisitions of products or businesses and other risks associated with acquisitions;

- •

- currency fluctuations;

- •

- exposure to credit risk for accounts receivable;

- •

- pressure on our pricing models;

- •

- the allocation of radio spectrum and regulatory approvals for our products;

- •

- our customers' ability to secure a license for applicable radio spectrum;

- •

- changes in government regulation or industry standards that may limit the potential market for our products;

- •

- dependence on establishing and maintaining relationships with channel partners;

- •

- reliance on outsourced manufacturing;

- •

- reliance on suppliers of components;

- •

- our ability to protect our own intellectual property and potential harm to our business if we infringe the intellectual property rights of others;

- •

- risks associated with software licensed by us;

- •

- a lengthy and variable sales cycle;

- •

- dependence on our ability to recruit and retain management and other qualified personnel;

- •

- exposure to risks resulting from international sales and operations, including the requirement to comply with export control and economic sanctions laws;

- •

- product defects, product liability claims, or health and safety risks relating to wireless products;

- •

- risks associated with possible loss of our foreign private issuer status, and

- •

- risks and expenses associated with being a public company in the U.S.

Readers are also referred to "Risk Factors" in the Company's AIF, which is available atwww.sedar.com andhttp://www.sec.gov/edgar/searchedgar/companysearch.html. Although we have attempted to identify important factors that could cause our actual results to differ materially from our expectations, intentions, estimates or forecasts, there may be other factors that could cause our results to differ from what we currently anticipate, estimate or intend. Recent unprecedented events in global financial and credit markets have resulted in high market price volatility and contraction in credit markets.

3

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

These on-going events could impact our business, financial condition and operating results in an unpredictable and possibly detrimental manner.

Change in Functional and Reporting Currency

Effective March 1, 2010, the Company adopted the US dollar (USD) as its functional and reporting currency, as a significant portion of its revenue, expenses, assets, liabilities and financing are denominated in USD. Prior to that date, the Company's operations were measured in Canadian dollars (CAD) and the consolidated financial statements were expressed in CAD. The Company followed the recommendations of the Emerging Issues Committee (EIC) of the Canadian Institute of Chartered Accountants (CICA), set out in EIC-130, "Translation method when the reporting currency differs from the measurement currency or there is a change in the reporting currency". In accordance with EIC-130, assets and liabilities as at March 1, 2010, were translated into USD using the exchange rate in effect on that date and equity transactions were translated at historical rates. As the change took place on the first day of the fiscal year, there was no income statement or cash flow translation required. For comparative purposes, historical financial statements have been restated in USD using the current rate method. Under this method, assets and liabilities are translated at the closing rate in effect at the end of these periods, revenues, expenses and cash flows are translated at the average rates in effect for these periods and equity transactions are translated at historical rates. Any exchange differences resulting from the translation are included in accumulated other comprehensive income presented in shareholders' equity.

4

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

SELECTED FINANCIAL INFORMATION:

| | Three Months Ended | Six Months Ended | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | August 31, 2010 | August 31, 2009 | August 31, 2010 | August 31, 2009 | ||||||||||

REVENUE | 27,171 | 32,423 | 75,897 | 45,422 | ||||||||||

Cost of sales | 15,219 | 18,795 | 42,714 | 27,304 | ||||||||||

Gross profit | 11,952 | 13,628 | 33,183 | 18,118 | ||||||||||

| 44.0% | 42.0% | 43.7% | 39.9% | |||||||||||

EXPENSES | ||||||||||||||

Research and development | 3,733 | 3,236 | 8,431 | 5,701 | ||||||||||

Selling and marketing | 4,468 | 3,257 | 8,604 | 5,326 | ||||||||||

General and administrative | 2,607 | 1,661 | 5,183 | 2,664 | ||||||||||

Investment tax credits | — | (55 | ) | — | (104 | ) | ||||||||

| 10,808 | 8,099 | 22,218 | 13,587 | |||||||||||

Income from Operations | 1,144 | 5,529 | 10,965 | 4,531 | ||||||||||

Interest income | 76 | (5 | ) | 108 | 17 | |||||||||

Investment income | 62 | — | 13 | — | ||||||||||

Gain on sale of property, equipment and intangible assets | — | 32 | — | 32 | ||||||||||

Foreign exchange gain (loss) | 69 | 64 | 186 | (1,310 | ) | |||||||||

Net Income | 1,351 | 5,620 | 11,272 | 3,270 | ||||||||||

Income tax expense (recovery) | 126 | (125 | ) | 357 | (125 | ) | ||||||||

Net and Comprehensive Income | 1,225 | 5,745 | 10,915 | 3,395 | ||||||||||

Basic income per share | 0.03 | 0.20 | 0.30 | 0.12 | ||||||||||

Diluted income per share | 0.03 | 0.19 | 0.29 | 0.12 | ||||||||||

Basic weighted average shares outstanding | 35,978,213 | 28,620,162 | 36,447,553 | 28,594,700 | ||||||||||

Diluted weighted average shares outstanding | 36,690,926 | 29,675,696 | 37,345,767 | 29,281,050 | ||||||||||

5

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

| | As at August 31, 2010 | As at February 28, 2010 | |||||

|---|---|---|---|---|---|---|---|

Consolidated Balance Sheet Data: | |||||||

Cash and cash equivalents | 43,921 | 105,276 | |||||

Short Term Investments | 54,556 | 8,074 | |||||

Total Assets | 158,338 | 176,749 | |||||

Total liabilities | 18,473 | 37,903 | |||||

Total shareholder's equity | 139,865 | 138,846 | |||||

SELECTED CONSOLIDATED QUARTERLY FINANCIAL INFORMATION

The following table sets out selected financial information for each of our most recent eight fiscal quarters. In the opinion of management, this information has been prepared on the same basis as DragonWave's audited consolidated financial statements, and all necessary adjustments have been included in the amounts stated below to present fairly the unaudited quarterly results when read in conjunction with DragonWave's consolidated financial statements and related notes thereto.

| | FY09 | FY10 | FY11 | |||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Nov 28 2008 | Feb 28 2009 | May 31 2009 | Aug 31 2009 | Nov 30 2009 | Feb 28 2010 | May 31 2010 | Aug 31 2010 | ||||||||||||||||||

Revenue | 9,819 | 10,395 | 12,999 | 32,423 | 51,594 | 60,973 | 48,726 | 27,171 | ||||||||||||||||||

Gross Profit | 3,398 | 2,696 | 8,509 | 18,795 | 29,453 | 34,808 | 21,231 | 11,952 | ||||||||||||||||||

Gross Profit % | 35% | 26% | 35% | 42% | 43% | 43% | 44% | 44% | ||||||||||||||||||

Operating Expenses | 5,947 | 5,501 | 5,488 | 8,099 | 10,334 | 12,229 | 11,410 | 10,808 | ||||||||||||||||||

Income from operations | (2,549 | ) | (2,805 | ) | (988 | ) | 5,529 | 11,807 | 13,936 | 9,821 | 1,144 | |||||||||||||||

Net income (loss) for the period | (203 | ) | (1,972 | ) | (2,350 | ) | 5,745 | 11,647 | 12,802 | 9,690 | 1,225 | |||||||||||||||

Net income (loss) per share | ||||||||||||||||||||||||||

Basic | (0.01 | ) | (0.07 | ) | (0.08 | ) | 0.20 | 0.36 | 0.35 | 0.26 | 0.03 | |||||||||||||||

Diluted | (0.01 | ) | (0.07 | ) | (0.08 | ) | 0.19 | 0.34 | 0.34 | 0.26 | 0.03 | |||||||||||||||

Weighted average number of shares outstanding | ||||||||||||||||||||||||||

Basic | 28,555,716 | 28,536,427 | 28,569,238 | 28,620,162 | 32,604,077 | 36,461,643 | 36,916,893 | 35,978,213 | ||||||||||||||||||

Diluted | 28,555,716 | 28,536,427 | 28,569,238 | 29,675,696 | 34,085,934 | 37,914,614 | 37,930,704 | 36,690,926 | ||||||||||||||||||

Total Assets | 44,152 | 40,789 | 45,449 | 63,103 | 150,288 | 176,749 | 172,840 | 158,338 | ||||||||||||||||||

Historically, our operating results have fluctuated on a quarterly basis and we expect that quarterly financial results will continue to fluctuate in the future. The results of operations for interim periods should not be relied upon as an indication of the results to be expected or achieved in any future period or any fiscal year as a whole. Fluctuations in results relate to the growth in our revenue, and the project nature of the network installations of our end-customers. In addition, results may fluctuate as a result of the timing of staffing, infrastructure additions required to support growth, and material costs required to support design initiatives. Operating results may not follow past trends for other reasons, including strategic decisions by us such as acquisition of complementary products or businesses.

6

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

Overview

DragonWave is a leading provider of high-capacity Ethernet microwave solutions that drive next-generation IP networks. Our carrier-grade point-to-point Ethernet microwave systems transmit broadband voice, video and data, enabling service providers, government agencies, enterprises and other organizations to meet their increasing bandwidth requirements rapidly and affordably. The principal application of our products is wireless network backhaul.

In the second quarter of fiscal 2011, DragonWave recognized revenue of $27.2 million. This quarter's revenue represents a 16% decrease over the second quarter of fiscal 2010 and a 44% decrease from the first quarter of fiscal 2011. Gross margin reached 44.0% for the three months ended August 31, 2010, which represents a 2% increase over the same period in the previous fiscal year, and a 0.4% increase over the first quarter of fiscal 2011. This sales level combined with a strong margin performance has resulted in a second quarter operating profit of $1.1 million, this compares to an operating profit of $5.5 million for the same period in the previous fiscal year. Net and comprehensive income for the quarter decreased by $4.5 million from the same period in the previous year (Net income: second quarter fiscal 2011—$1.2 million; second quarter fiscal 2010—$5.7 million).

As we entered the second quarter of fiscal 2011 we focused our efforts on three key objectives; satisfying and working closely with our largest customer, pursuing our market and customer diversification agenda, and further reducing manufacturing costs.

Our Largest Customer

We communicated at the beginning of this quarter that we expected the demand from our largest customer to decrease as it implements its 2010 network plans and work toward the next phase of its build out plan. We were pleased with the level of demand from this customer as it strengthened throughout the quarter and ended up accounting for 59.3% of our sales in the second quarter of fiscal 2011.

Customer Diversification and New Market Entry

To continue to grow, we are focusing our efforts on diversifying our customer base and entering new markets. We are using a number of strategies to achieve this objective including dedicating resources to key accounts, opening offices in various regions of the world, investigating more partnerships and considering acquisitions which will support our focus on customer diversification and new market entry.

DragonWave had a second customer which accounted for more than 10% of revenue in the three month period ended August 31, 2010. This customer is located in Eastern Europe and its project is expected to continue to benefit our revenue stream in the third quarter, though to a lesser degree.

Internationally the level of bid activity is high. We have dedicated sales resources located in Canada, the United States, England, France, Singapore, Pakistan, Dubai and Australia. We continue to believe their proximity to customers and knowledge of local customs and language increases our ability to respond to opportunities wherever they present themselves. As one example of the international opportunity, the Indian regulator has completed the 3G and 4G spectrum auction and therefore network build activity is expected to ramp up in this region. DragonWave is currently investigating the best approach to address this emerging market.

7

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

With our existing U.S. market share we are well positioned to respond to prospects in North America as well and recent Request for Proposal (RFP) activity indicates this market continues to provide good potential for customer expansion. In particular, we see the United States as an exciting market as several major players have announced plans to build nation-wide networks there. In Canada, we recently announced a partnership with Execulink Telecom to provide affordable broadband internet access to residential and small-business customers in southern Ontario.

As previously reported, another element of our growth strategy involves developing alliances with other companies to expand our customer reach. In February, 2010 we announced that we had signed an original equipment manufacturer (OEM) agreement with a world leader in mobile communications. In the second quarter of fiscal 2011 we began to make our first shipments into Japan which leveraged this agreement.

Although there continues to be uncertainty in the financial markets internationally, the growth in demand for greater user bandwidth is continuing unabated. Internationally, carriers are beginning to seek solutions which can address the growing demand for network capacity, in a more cost effective and reliable fashion than previous solutions afforded. DragonWave feels that packet based microwave technologies will be well positioned to capture a sizable portion of the available backhaul market for reasons including cost, time to implementation, capacity and scalability.

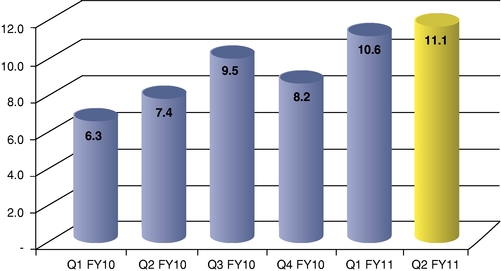

Revenue from Customers Excluding the Largest Customer

Q1 FY2010 to Q2 FY2011

(USD millions)

8

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

Continued Focus on Cost Reduction and Product Innovation

We were very pleased to be in a position to ship the first units of our recently launched Quantum product, in the second quarter of fiscal 2011. The Horizon Quantum represents a product offering which can deliver high capacity and ultra-low latency combined with carrier-class reliability. At the same time, our design efforts have been focusing on choices which enable DragonWave to manufacture our products for a lower cost. The cost advantage of our newer designs is one of the contributing factors to our margins remaining above 40% despite the reduction in sales volumes. Our manufacturing strategy for the entire Horizon product line centres around the increasing use of contract manufacturers, not only for product assembly, but for final test as well; functions historically performed at DragonWave. In the second quarter of fiscal 2011 we continued this emphasis with the implementation of our training and qualification program to manufacture both Compact and Quantum in Malaysia.

Share Repurchase

On April 9, 2010, the Toronto Stock Exchange (the "TSX") accepted the Company's notice of intention to repurchase up to 3,508,121 common shares (10 percent of the Company's issued and outstanding common shares) through a normal course issuer bid ("NCIB"). The NCIB was effective April 13, 2010 and will expire April 12, 2011. Daily purchases over the facilities of the NASDAQ are limited to 25% of the average daily trading volume of the common shares on NASDAQ other than pursuant to block purchase exemptions. Daily purchases over the facilities of the TSX are limited to 25% of the average daily trading volume of the common shares on TSX other than pursuant to block purchase exemptions. Except in the case of an exempt purchase, the prices that the Company will pay for the common shares purchased will be the market price of the shares at the time of acquisition.

During the three months ended August 31, 2010, the Company acquired 1,691,149 common shares pursuant to the NCIB at prevailing market prices. These shares were purchased for cancellation at an aggregate cost of $9.7 million of which $8.2 million was charged to share capital, based on the historical weighted per share value at the date of purchase, and the balance of $1.5 million was charged to deficit. During the six months ended August 31, 2010, the Company has acquired 1,865,549 common shares pursuant to the NCIB at prevailing market prices. These shares were purchased for cancellation at an aggregate cost of $10.7 million of which $9.0 million was charged to share capital, based on the historical weighted per share value at the date of purchase, and the balance of $1.7 million was charged to deficit.

9

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

Revenue and Expenses

Revenue

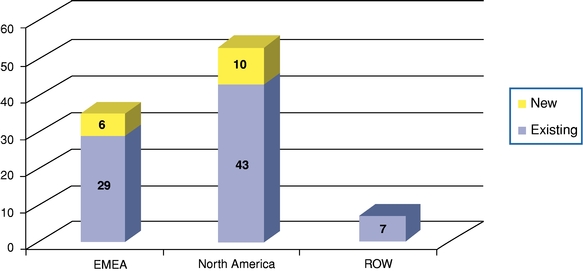

We evaluate revenue performance over three main geographic regions. These regions are North America; Europe, the Middle East and Africa ("EMEA"); and Rest of World ("ROW"). The following table sets out the portion of new customers and existing customers we shipped to in the second quarter of fiscal 2011.

Number of Customers Shipped to in the Quarter Ended August 31, 2010

Number of Customers Shipped to in the Six Months Ended August 31, 2010

10

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

The ability for the Company to attract new customers in multiple geographic regions is evident from the chart above. We believe that our growth strategy hinges, in part, on new customer acquisition and on our ability to penetrate markets both inside and outside of North America wherever the wireless backhaul market is expanding.

The table below breaks down the revenue earned by region for the three and six month periods ending August 31, 2010 and compares these figures to the same periods in the prior fiscal year. The table clearly shows that sales into Europe, the Middle East and Africa continue to grow.

| | Three Months Ended | Six Months Ended | |||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | August 31, 2010 | August 31, 2009 | August 31, 2010 | August 31, 2009 | |||||||||||||||||||||

| | $'s | % | $'s | % | $'s | % | $'s | % | |||||||||||||||||

North America | 20,299 | 74% | 29,099 | 90% | 63,215 | 83% | 39,573 | 87% | |||||||||||||||||

Europe, Middle East, and Africa | 6,420 | 24% | 2,708 | 8% | 11,868 | 16% | 5,175 | 12% | |||||||||||||||||

Other | 452 | 2% | 616 | 2% | 814 | 1% | 674 | 1% | |||||||||||||||||

Total Revenue | 27,171 | 100% | 32,423 | 100% | 75,897 | 100% | 45,422 | 100% | |||||||||||||||||

Cost of Sales and Expenses

A large component of our cost of sales is the cost of product purchased from outsourced manufacturers. In addition to the cost of product payable to outsourced manufacturers, we incur expenses associated with final configuration, testing, logistics and warranty activities. Final test and assembly for the links sold by us is carried on both at our premises and that of our contract manufacturers'. We use primarily the services of two outsourced manufacturers with locations in North America and Malaysia.

Research and development costs relate mainly to the compensation of our engineering group and the material consumption associated with prototyping activities.

Selling and marketing expenses include the remuneration of sales staff, travel and trade show activities and customer support services.

General and administrative expenses relate to the remuneration of related personnel, professional fees associated with tax, accounting and legal advice, and insurance costs.

Occupancy and information systems costs are related to our leasing costs and communications networks and are accumulated and allocated, based on headcount, to all functional areas in our business. Our facilities are leased from a related party that is controlled by one of our directors and shareholders. Our management believes the terms of the lease reflect fair market terms and payment provisions.

11

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

Comparison of the three and six months ended August 31, 2010 and August 31, 2009

Revenue

| Three months ended August 31 | Six months ended August 31 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009 | 2010 | 2009 | ||||||||

| $ | 27,171 | $ | 32,423 | $ | 75,987 | $ | 45,422 | ||||

Revenue for the second quarter of fiscal 2011 decreased by $5.3 million compared with the three month period ended August 31, 2009. On a year to date basis, revenue is $30.6 million higher, when compared with the six month period ended August 31, 2009.

The primary drivers for the changes are as follows:

Changes to Revenue: Three months ended August 31, 2010 vs Three months ended August 31, 2009

North American national carrier | (9.2 | ) | ||

New Customers in Europe | 5.3 | |||

Regional Carriers and Distributors in EMEA | (1.0 | ) | ||

Regional Carriers and Distributors in ROW | (0.7 | ) | ||

Other New Customers | 0.6 | |||

Regional Carriers and Distributors in North America | (0.2 | ) | ||

Canadian national carrier | (0.1 | ) | ||

Total | (5.3 | ) | ||

12

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

Changes to Revenue: Six months ended August 31, 2010 vs Six months ended August 31, 2009

North American national carrier | 23.1 | |||

New Customers in Europe | 5.7 | |||

Regional Carriers and Distributors in ROW | 0.8 | |||

Canadian national carrier | 0.6 | |||

New Customers in North America | 0.6 | |||

Regional Carriers and Distributors in North America | 0.2 | |||

Other New Customers | 0.2 | |||

Other | (0.6 | ) | ||

Total | 30.6 | |||

Gross Profit

| Three months ended August 31 | Six months ended August 31 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009 | 2010 | 2009 | ||||||||

| $ | 11,952 | $ | 13,628 | $ | 33,183 | $ | 18,118 | ||||

| 44.0% | 42.0% | 43.7% | 39.9% | ||||||||

Our gross margin climbed to 44.0% for the three month period ended August 31, 2010. This represents a 2.0% increase over the same period in the previous fiscal year. The margin improved as well over the first quarter by 0.4%. On a year to date basis the margin improved by 3.8%, rising to 43.7% for the six month period ended August 31, 2010. The strong margin in this quarter was driven the product mix that we sold in the quarter coupled with the continuing reduction in our manufacturing costs. On a year to date basis, the favourable economics afforded by our manufacturing strategyis the most significant factor contributing to our improved margin results. The Company believes that the gross margin is at the high end of the achievable level based on current technology, manufacturing strategies and pricing pressures.

Research and Development

| Three months ended August 31 | Six months ended August 31 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009 | 2010 | 2009 | ||||||||

| $ | 3,733 | $ | 3,236 | $ | 8,431 | $ | 5,701 | ||||

Research and development ("R&D") expenses increased by $0.5 million for the three month period ended August 31, 2010 when compared with the same period in the prior fiscal year. On a year to date basis, R&D spending increased by $2.7 million when compared to the six month period ended August 31, 2009.

A number of factors have contributed to the increased spending in R&D. First, the Company expanded its R&D organization which resulted in compensation and other headcount associated spending

13

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

increasing year over year (Second quarter increase—$ 0.2 million; year to date increase—$2.0 million). As well, material spending associated with prototype builds for products still in the design phase, and depreciation on R&D equipment used in the design process increased (Second quarter increase—$ 0.2 million; year to date increase—$0.6 million). Finally, travel and other miscellaneous costs have risen (Second quarter increase—$ 0.1 million; year to date increase—$0.1 million)

Selling and Marketing

| Three months ended August 31 | Six months ended August 31 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009 | 2010 | 2009 | ||||||||

| $ | 4,468 | $ | 3,257 | $ | 8,604 | $ | 5,326 | ||||

Sales and marketing expenses increased $1.2 million in the three months ended August 31, 2010 relative to the same three month period in the previous fiscal year. Expenses increased by $3.3 million when comparing the six month period ended August 31, 2010 to the same period in fiscal 2010.

In focusing our efforts on expanding our customer base, and in taking the necessary steps to properly support our existing customers globally, our sales, marketing and customer support organizations have all grown over the past year. Compensation costs connected with this headcount growth resulted in higher spending (Second quarter increase—$1.2 million; year to date increase—$2.2 million). Higher variable compensation associated with revenue performance accounted for a portion of the variance as well (Second quarter decrease—$0.3 million; year to date increase—$0.4 million). Finally, travel costs, marketing initiatives and spending related to new offices outside of North America accounted for the remaining difference (Second quarter increase—$0.3 million; year to date increase—$0.7 million).

General and Administrative

| Three months ended August 31 | Six months ended August 31 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009 | 2010 | 2009 | ||||||||

| $ | 2,607 | $ | 1,661 | $ | 5,183 | $ | 2,664 | ||||

General and administrative expenses increased by $0.9 million for the three months ended August 31, 2010 when compared to the same three month period in the previous fiscal year. On a year to date basis, spending increased by $2.5 million compared to same six month period in the prior fiscal year.

The increase in spending in the quarter can be primarily attributed to higher compensation costs related to an increase in resources in a variety of areas (Second quarter increase—$0.3 million; year to date increase—$1.1 million). We are now listed on both the NASDAQ and the TSX, a change from the first half of fiscal 2010, and this change has also contributed to higher head office costs associated with professional fees and travel (Second quarter increase—$0.7 million; year to date increase—$1.1 million). Finally, insurance, business taxes and miscellaneous other costs have differed between fiscal 2011 and fiscal 2010 (Second quarter decrease—$0.1 million; year to date increase—$0.3 million).

14

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

Investment Tax Credits

| Three months ended August 31 | Six months ended August 31 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009 | 2010 | 2009 | ||||||||

| $ | — | $ | (55 | ) | $ | — | $ | (104 | ) | ||

In prior years we were able to claim benefits under the Ontario Innovation Tax Credit program. During the fourth quarter of fiscal 2010, it was determined that the higher revenue and asset levels of the consolidated company would eliminate the entitlement to claim any benefit in Canada.

Interest Income/(Loss) (Net)

| Three months ended August 31 | Six months ended August 31 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009 | 2010 | 2009 | ||||||||

| $ | 76 | $ | (5 | ) | $ | 108 | $ | 17 | |||

Interest rates on investments are extremely low at present. As a result, despite the Company's healthy cash position, interest income earned by the Company in the three and six month periods ended August 31, 2010 was relatively low.

Investment Gain

| Three months ended August 31 | Six months ended August 31 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009 | 2010 | 2009 | ||||||||

| $ | 62 | $ | — | $ | 13 | $ | — | ||||

In the first six months of fiscal 2011 we made short term investments which carried a fixed yield and term to maturity. Because these investments are reflected on the balance sheet at their market value, and the interest rates decreased between the date they were purchased and August 31, 2010, an unrealized investment gain was booked to reflect the increase in the market value of the investments.

A portion of the Company's available cash resources have been invested in low risk investment vehicles with a variety of maturity dates to maximize our returns while ensuring our cash is easily accessed for the Company's business priorities and that our risk is kept at a minimum.

15

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

Foreign Exchange Gain (Loss)

| Three months ended August 31 | Six months ended August 31 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009 | 2010 | 2009 | ||||||||

| $ | 69 | $ | 64 | $ | 186 | $ | (1,310 | ) | |||

The small foreign exchange gain recognized in the second quarter of fiscal 2011 resulted from the translation of monetary accounts denominated in currencies other than the USD at August 31, 2010 in an environment where the USD was becoming relatively weaker. When comparing the gain and loss between the two years it is important to bear in mind that on March 1, 2010 the Company began to report in USD. Prior to that date all USD financial assets were re-valued to reflect the fair value in CAD. As at August 31, 2010 only 4% of our cash, 6% of our trade receivables, and 70% of our financial liabilities are held in currencies other than the USD. As a result the foreign exchange gain (loss) resulting from such revaluations has been minimized.

Income Taxes Expense (Recovery)

| Three months ended August 31 | Six months ended August 31 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009 | 2010 | 2009 | ||||||||

| $ | 126 | $ | (125 | ) | $ | 357 | $ | (125 | ) | ||

Income tax expense relates primarily to DragonWave's wholly owned U.S. subsidiary, where available net operating losses are not sufficient to offset taxable income. In Canada, DragonWave has utilized its tax carry-forward balances to eliminate current taxes.

We have a number of tax carry-forward pools (including loss carry-forwards and scientific research and experimental development expenses), primarily in Canada, available to us to reduce future taxable income. At the end of fiscal 2010, the total of these carry-forwards was $51,677 for use in fiscal 2011 and future years. Except for benefits recorded in respect of U.S. operating losses and timing differences, income tax benefits relating to these carryforwards have not been recognized in the consolidated financial statements as recognition requirements under the liability method of accounting for income taxes were not met.

Liquidity and Capital Resources

As at August 31, 2010, we had a credit line in place with a major U.S.-based bank which allows borrowing to support working capital requirements of up to $17.0 million and capital expenditure requirements of up to $3 million.

16

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

The table below outlines selected balance sheet accounts and key ratios:

| | As at August 31, 2010 | As at February 28, 2010 | ||||||

|---|---|---|---|---|---|---|---|---|

Key Balance Sheet Amounts and Ratios: | ||||||||

Cash and Cash Equivalents | 43,921 | 105,276 | ||||||

Short Term Investments | 54,556 | 8,074 | ||||||

Working Capital | 133,727 | 133,343 | ||||||

Long Term Assets | 8,611 | 7,605 | ||||||

Long Term Liabilities | 2,473 | 2,102 | ||||||

Working Capital Ratio | 9.4 : 1 | 4.7 : 1 | ||||||

Days Sales Outstanding in accounts receivable | 67 days | 47 days | ||||||

Inventory Turnover | 1.6 times | 5.7 times | ||||||

Cash and Cash Equivalents, and Short Term Investments

As at August 31, 2010, the Company had $98.5 million in cash and cash equivalents plus short term investments ("Cash") representing a $14.9 million decrease from the Cash balance at February 28, 2010. There were three primary drivers for the decrease; the repurchase of shares which reduced cash by $10.3 million, the payment for capital equipment of $3.1 million, and the usage of cash from operations of $1.5 million, which resulted from the payment of trade accounts payables for inventory shipped.

Working Capital

Changes in working capital | February 28, 2010 to August 31, 2010 | |||

|---|---|---|---|---|

Beginning Working Capital Balance(current assets—current liabilities) | 133,343 | |||

Cash and cash equivalents & short term investments | (14,873 | ) | ||

Trade Receivables | (8,272 | ) | ||

Other receivables | (870 | ) | ||

Inventory | 3,598 | |||

Prepaid Expenses | 1,098 | |||

Current Income Tax Asset | (98 | ) | ||

Accounts Payable and accrued liabilities | 20,704 | |||

Taxes Payable | 742 | |||

Deferred Revenue | (1,645 | ) | ||

Net Change in Working Capital | 384 | |||

Ending Working Capital Balance | 133,727 | |||

Working capital is calculated as the difference between our current assets and current liabilities. Our working capital balance increased to $133.7 million between February 28, 2010 and August 31, 2010. One

17

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

of the most significant impacts related to the decrease in accounts payable (which benefits working capital), and the increase in inventory. This was partially offset by a decrease in accounts receivable, and the increase deferred revenue (which as a liability reduces working capital).

The days sales outstanding in accounts receivable, ("DSO"), as at August 31, 2010 was 67 days. This calculation was 20 days higher than the DSO of 47 days at February 28, 2010. We evaluate DSO by determining the number of days of sales in the ending accounts receivable balance with reference to the most recent monthly sales, rather than average yearly or quarterly values

Inventory turnover for August 31, 2010 was 1.6 times for the three month period then ended, a decrease from the number of turns calculated at February 28, 2010. Turnover is calculated with reference to the most recent monthly standard cost of goods sold and is based on the period ending inventory balance of production related inventory (net of labour and overhead allocations).

Cash Inflows and Outflows:

| | Quarter Ended | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Aug 31 2009 | Nov 30 2010 | Feb 28 2010 | May 31 2010 | Aug 31 2010 | |||||||||||

Beginning Cash (incl Short Term Investments) | 20,048 | 19,466 | 98,356 | 113,350 | 115,825 | |||||||||||

Normal Operations | ||||||||||||||||

Net Income (Loss) | 5,745 | 11,647 | 12,802 | 9,690 | 1,225 | |||||||||||

Changes in Non-Cash Working Capital | (5,528 | ) | 1,183 | 710 | (5,034 | ) | (10,290 | ) | ||||||||

Capital Asset Purchases | (1,368 | ) | (2,820 | ) | (1,120 | ) | (2,225 | ) | (917 | ) | ||||||

Line of Credit/Option proceeds & other | 33 | (543 | ) | 1,694 | 147 | 64 | ||||||||||

Non Cash items included in Net Income | 536 | 808 | 908 | 951 | 1,839 | |||||||||||

Total Cash (Used) / Generated | (582 | ) | 10,275 | 14,994 | 3,529 | (8,079 | ) | |||||||||

NASDAQ IPO/(Share Repurchase) | — | 68,615 | — | (1,054 | ) | (9,269 | ) | |||||||||

Ending Cash (incl Short Term Investments) | 19,466 | 98,356 | 113,350 | 115,825 | 98,477 | |||||||||||

Cash Used in Operating Activities

The positive impact to cash of the net income of $1.2 million, ($3.1 million when adjusted for non-cash items) for the three months ended August 31, 2010 was offset by the growth in non-cash working capital of $10.3 million, and the purchase of capital equipment for $0.9 million.

Investing Activities (Purchase of Capital Assets)

We are continuing to invest in capital equipment to support engineering programs as well as the manufacturing and test capabilities associated with current and new products. For the three months ended August 31, 2010, the cash impact of the investments in capital equipment amounted to $0.9 million.

18

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

Financing Activities

During the three months ended August 31, 2010 we repurchased 1,691,149 shares for a total cost of $9.7 million. As at August 31, 2010, $0.4 million is included in accounts payable and accrued liabilities related to these purchases. See "Share Repurchases."

We disclosed our expectations regarding the use of net proceeds ($70.5 million CAD) of the offering of our common shares which was completed on October 20, 2009 (the "Offering") in our supplemented short form PREP prospectus dated October 14, 2009. The following table summarizes progress to the end of FY2010 against the use of net proceeds disclosed in the prospectus, other than proceeds which were described as being allocated to working capital:

Description of Expected Use of Proceeds | Amount of Net Proceeds | Status as at August 31, 2010 | |||

|---|---|---|---|---|---|

Strengthen our balance sheet | $ | 27.4 million | As of August 31, 2010 the Company had $98.5 million in Cash on its balance sheet, consisting of net proceeds of the Offering that have not yet been allocated as well as cash flow from operations. | ||

Fund efforts to increase sales penetration in regions outside of North America | $ | 13.7 million | Between October 14, 2009 and August 31, 2010 the Company expended approximately $2.9 million to fund efforts to increase sales penetration outside of North America. | ||

Provide source of funding for potential future acquisitions | $ | 6.8 million | As at August 31, 2010 the Company had not made any acquisitions. | ||

In addition to cash raised through financing activities, we have generated substantial cash flows from operations which are also allocated to the foregoing uses, as described in the table, as well as to fund operations and other initiatives. As disclosed in the Offering prospectus, management has broad discretion in how it uses the net proceeds received from financing activities. We may re-allocate the net proceeds of the Offering from time to time having consideration to our strategy relative to the market and other conditions in effect at the time, including those factors discussed above under the heading "Risks and Uncertainties". As discussed our current focus is on diversifying our customer base through a strategy that includes product innovation, expansion of our geographic markets, OEM arrangements and mergers and acquisitions, and we expect that our available funds will be used to support these and related initiatives as well as other elements of our growth strategy.

Liquidity and Capital Resource Requirements

Based on our recent performance, current revenue expectations, and funds raised through the financing activities of the previous year, our management believes cash resources will be available to satisfy working capital needs for at least the next 12 months.

19

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

Commitments as at August 31, 2010

Future minimum operating lease payments as at August 31, 2010 per fiscal year are as follows:

Fiscal Year | $(000's) | |||

|---|---|---|---|---|

2011 | 560 | |||

2012 | 783 | |||

2013 | 92 | |||

2014 | 14 | |||

Thereafter | — | |||

Total | 1,449 | |||

In the normal course of its business activities, the Company is subject to claims and legal actions. The Company recognizes a provision for estimated loss contingencies when it is probable that a liability has been incurred and the amount of the loss can be reasonably estimated. In management's opinion, adequate provisions have been made for all current and future claims.

Outstanding Share Data

The common shares of the Corporation are listed on the TSX under the symbol DWI and on the NASDAQ under the symbol DRWI.

| | Outstanding | Exercise Price Range | Weighted Avg Exercise Price | ||||||

|---|---|---|---|---|---|---|---|---|---|

Common shares | 35,112,860 | n/a | n/a | ||||||

DRWI on NASDAQ on August 31, 2010 | $ | 5.86 | |||||||

Market Capitalization | $ | 205,761,360 | |||||||

Stock option—common shares | 2,041,429 | CAD 1.34—CAD 13.74 | CAD 4.70 | ||||||

Warrants—common share | 72,573 | $3.34—$8.53 | $5.80 | ||||||

The information presented is at August 31, 2010.

Off-Balance Sheet Arrangements

We lease space for our headquarters in Ottawa, Ontario, Canada. Our R&D, services and support, and general and administrative groups operate from our headquarters. We also lease warehouse space in Ottawa, Ontario, Canada. Both leases expire in November 2011. We lease additional warehouse space on a month by month basis. Our rental costs including operating expenses total $92 thousand per month. In April, 2008 we signed a lease agreement in England. The lease expires in April, 2013 and rental costs including operating costs total $8 thousand per month.

We use an outsourced manufacturing model whereby most of the component acquisition and assembly of our products is executed by third parties. Generally, we provide the supplier with a purchase order

20

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

90 days in advance of expected delivery. We are responsible for the financial impact of any changes to the product requirements within this period. We have purchase orders in place currently for raw materials and manufactured products in addition to capital expenses and services. All purchase orders reflect our current view on revenue and cash flow.

Financial Instruments

Under Canadian generally accepted accounting principles, financial instruments are classified into one of the following categories: held for trading, held-to-maturity, available-for-sale, loans and receivables, or other liabilities.

Fair Value

The following table summarizes the carrying values of the Company's financial instruments:

| | August 31, 2010 | February 28, 2010 | |||||

|---|---|---|---|---|---|---|---|

Held-for-trading(1) | 98,477 | 113,350 | |||||

Loans and receivables(2) | 20,920 | 28,990 | |||||

Other financial liabilities(3) | 11,833 | 31,269 | |||||

- (1)

- Includes cash, cash equivalents, and short term investments

- (2)

- Includes trade receivables and other receivables which are financial in nature

- (3)

- Includes accounts payable and accrued liabilities which are financial in nature

Cash and cash equivalents, short term investments, trade receivables, other receivables, line of credit, accounts payable and accrued liabilities are short term financial instruments whose fair value approximates the carrying amount given that they will mature shortly. As at the balance sheet date, there are no significant differences between the carrying value of these items and their estimated fair values.

Interest rate risk

Cash and cash equivalents with variable interest rates expose the Company to interest rate risk on these financial instruments. The Company pays interest on its line of credit at the bank's prime rate of interest plus 1%, and has interest rate risk exposure due to changes in the bank's prime rate. The line of credit was not utilized as at August 31, 2010.

Credit risk

In addition to trade receivables and other receivables, the Company is exposed to credit risk on its cash and cash equivalents, and short term investments in the event that its counterparties do not meet their obligations. The Company does not use credit derivatives or similar instruments to mitigate this risk and, as such, the maximum exposure is the full carrying value or face value of the financial instrument. The Company minimizes credit risk on cash and cash equivalents and short term investments by transacting with only reputable financial institutions.

21

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

Foreign exchange risk

The following table summarizes the currency distribution of the Company's financial instruments in US dollars, as at August 31, 2010:

| | August 31, 2010 | February 28, 2010 | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | US Dollars | CDN Dollars | Other Currency | US Dollars | CDN Dollars | Other Currency | |||||||||||||

Held-for-trading | 96% | 3% | 1% | 86% | 13% | 1% | |||||||||||||

Loans and receivables | 94% | 5% | 1% | 93% | 6% | 1% | |||||||||||||

Other financial liabilities | 30% | 70% | 0% | 65% | 35% | 0% | |||||||||||||

Foreign exchange risk arises because of fluctuations in exchange rates. The Company does not currently use derivative financial instruments to mitigate this risk.

If the US dollar had appreciated 1 percent against all foreign currencies at August 31, 2010, with all other variables held constant, the impact of this foreign currency change on the Company's foreign denominated financial instruments would have resulted in a reduction of after-tax net income of $34 thousand for the three and six month periods ended August 31, 2010 (three and six month periods ended August 31, 2009—$72 thousand), with an equal and opposite effect if the US dollar had depreciated 1 percent against all foreign currencies at August 31, 2010.

Liquidity risk

A risk exists that the Company will not be able to meet its financial obligations as they become due. Based on the Company's recent performance, current revenue expectations and strong current ratio, management believes that liquidity risk is low.

Transactions with Related Parties

The Company leases premises from a real estate company controlled by a member of the Board of Directors. During the three and six months ended August 31, 2010, the Company paid $0.4 million and $0.7 million respectively (three and six months ended August 31, 2009—$0.2 million and $0.4 million respectively), relating to the rent, operating costs, and leasehold improvements associated with this real estate, and the value owing for net purchases at August 31, 2010 was nil (February 28, 2010—$70 thousand). These amounts have been allocated amongst various expense accounts, except for leasehold improvements which have been allocated to property, equipment and intangible assets.

The Company also purchased products and services from a company controlled or significantly influenced by a Board member. Total net product and services purchased for the three and six month periods ended August 31, 2010 was nil and $2.7 million respectively (three and six months ended August 31, 2009—$4.7 million and $6.6 million respectively). The majority of the purchases have been recorded in inventory and ultimately in cost of sales. This company ceased to be a related party on May 28, 2010.

All transactions are in the normal course of business and have been recorded at the exchange amount.

22

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

Description of Credit Facilities

Bank Line of Credit

As at August 31, 2010, the Company had drawn $nil (February 28, 2010—$nil), on an operating credit facility with a limit of $17.0 million (February 28, 2010—$10.0 million). Interest is calculated at the bank's prime rate of interest plus 1% (February 28, 2010—1.75%) and resulted in a weighted average effective rate of nil for the three and six months ended August 31, 2010 (three and six months ended August 31, 2009—4.59% and 4.25% respectively). An amount of $0.3 million has been reserved against the operating line of credit to secure letters of credit to support performance guarantees. The Company has provided a general security agreement on trade receivables. The Company was in compliance with the financial covenants included in the lending agreement as at August 31, 2010.

The Company has drawn $nil (February 28, 2010—$nil) on a capital expenditure facility with a limit of $3.0 million (February 28, 2010 $3. 0 million).

Controls and Procedures

In compliance with the Canadian Securities Administrators' National Instrument 52-109—Certification of Disclosure in Issuers' Annual and Interim Filings, we have filed certificates signed by our Chief Executive Officer ("CEO") and Chief Financial Officer ("CFO") that, among other things, report on the design and effectiveness of disclosure controls and procedures and the design and effectiveness of internal controls over financial reporting. These reports were filed for the three months ended August 31, 2010 and the twelve months ended February 28, 2010. During the three month and six month periods ending August 31, 2010 no significant changes in internal controls occurred.

Commencing with our fiscal year ended February 28, 2011, we will be required to satisfy the requirements of Section 404 of the Sarbanes-Oxley Act ("SOX"). SOX requires an annual assessment by management of the effectiveness of our internal control over financial reporting and an attestation report by our independent auditors addressing this assessment.

Critical Accounting Policies and Estimates

Business Combinations

In January 2009, the Canadian Accounting Standards Board issued a new standard for business combinations, CICA 1582, "Business Combinations," which is substantially converged with IFRS. The revised Canadian standard is effective for years beginning on or after January 1, 2011, with earlier adoption permitted. An entity adopting this section for a fiscal year beginning before January 1, 2011 shall disclose that fact and also is required to adopt CICA 1601, "Consolidated Financial Statements" and CICA 1602, "Non-Controlling Interests" effective at the same time. The Company has adopted CICA Handbook Sections 1582, "Business Combinations," 1601, "Consolidated Financial Statements" and 1602, "Non-Controlling Interests" with effect from March 1, 2010. For the three and six month periods ended August 31, 2010, the Company has not entered into any business combinations.

23

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

Inventory

We value inventory at the lower of cost and market. We calculate the cost of raw materials on a standard cost basis, which approximates average cost. Market is determined as net realizable value for finished goods, raw materials and work in progress. Indirect manufacturing costs and direct labour expenses are allocated systematically to the total production inventory.

Revenue recognition

We derive revenue from the sale of our broadband wireless backhaul equipment which includes embedded software and a license to use said software and extended product warranties. We consider software to be incidental to the product. Services range from installation and training to basic consulting. We recognize revenue when persuasive evidence of an arrangement exists, delivery has occurred and there are no significant remaining vendor obligations, collection of receivables is reasonably assured and the fee is fixed and determinable. Where final acceptance of the product is specified by the customer, revenue is deferred until acceptance criteria have been met. Additionally, our business agreements may contain multiple elements. Accordingly, we are required to determine the appropriate accounting, including whether the deliverables specified in a multiple element arrangement should be treated as separate units of accounting for revenue recognition purposes, the fair value of these separate units of accounting and when to recognize revenue for each element. For arrangements involving multiple elements, we allocate revenue to each component of the arrangement using the residual value method, based on vendor-specific objective evidence of the fair value of the undelivered elements. These elements may include one or more of the following: advanced replacement, extended warranties, training, and installation. We allocate the arrangement fee, in a multiple-element transaction, to the undelivered elements based on the total fair value of those undelivered elements, as indicated by vendor-specific objective evidence. This portion of the arrangement fee is deferred. The difference between the total arrangement fee and the amount deferred for the undelivered elements is recognized as revenue related to the delivered elements. In some instances, a group of contracts or agreements with the same customer may be so closely related that they are, in effect, part of a single multiple element arrangement and, therefore, we would allocate the corresponding revenue among the various components, as described above.

We generate revenue through direct sales and sales to distributors. Revenue on stocking orders sold to distributors is not recognized until the end-user is identified.

We evaluate arrangements that include services such as training and installation to determine whether those services are essential to the functionality of other elements of the arrangement. When services are considered essential, revenue allocable to the other elements is deferred until the services have been performed. When services are not considered essential, the revenue allocable to the services is recognized as the services are performed.

We recognize revenue associated with extended warranty and advanced replacement rateably over the life of the contract.

We recognize revenue from engineering services or development agreements according to the specific terms and acceptance criteria as services are rendered.

24

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

We accrue estimated potential product liability as warranty costs when revenue on the sale of equipment is recognized. We calculate warranty costs on a percentage of revenue per month based on current actual warranty costs and return experience.

We record shipping and handling costs borne by us in costs of sales. Shipping and handling costs charged to customers are recorded as revenue, if billed at the time of shipment. Costs charged to customers after delivery are recorded in cost of sales.

Research and development

Our research costs are expensed as incurred. Our development costs other than property and equipment are expensed as incurred unless they meet generally accepted accounting criteria for deferral and amortization. Development costs incurred prior to establishment of technological feasibility do not meet these criteria, and are expensed as incurred. Government assistance and investment tax credits relating to ongoing R&D costs are recorded as a recovery of the related R&D expenses, where such assistance is reasonably assured.

Income taxes

Income taxes are accounted for using the liability method of accounting for income taxes. Under this method, future tax assets and liabilities are determined based on differences between the tax and accounting basis of assets and liabilities as well as for the benefit of losses available to be carried forward to future years for tax purposes that are more likely than not to be realized. Future tax assets and liabilities are measured using substantively enacted tax rates that apply to taxable income in the years in which temporary differences are expected to be recovered or settled. Future tax assets are recognized only to the extent, in the opinion of management, it is more likely than not that the future tax assets will be realized in the future.

We periodically review our provisions for income taxes and the valuation allowance to determine whether the overall tax estimates are reasonable. When we perform our quarterly assessments of the provision and valuation allowance, it may be determined that an adjustment is required. This adjustment may have a material impact on our financial position and results of operations.

Future Accounting Changes

In 2006, Canada's Accounting Standards Board ratified a strategic plan that will result in Canadian GAAP, as used by public companies, being evolved and converged with International Financial Reporting Standards ("IFRS") over a transitional period to be complete by 2011 (second quarter of fiscal 2012). We will be required to report using the converged standards effective for interim and annual financial statements relating to fiscal years beginning on or after January 1, 2011. Canadian GAAP will be converged with IFRS through a combination of two methods: as current joint-convergence projects of the United States' Financial Accounting Standards Board and the International Accounting Standards Board are agreed upon, they will be adopted by Canada's Accounting Standards Board and may be introduced in Canada before the complete changeover to IFRS; and standards not subject to a joint-convergence project will be exposed in an omnibus manner for introduction at the time of the complete changeover to IFRS.

25

![]()

DragonWave Inc.

Management's Discussion and Analysis

For the three and six months ended August 31, 2010

Tables are expressed in USD $000's except share and per share amounts

The International Accounting Standards Board currently has projects underway that should result in new pronouncements that continue to evolve IFRS.

Transition to US GAAP vs. IFRS

On October 1, 2010, the Canadian Securities Administrators approved National Instrument ("NI") 52-107Acceptable Accounting Principles and Auditing Standards. The policy comes into force on January 1, 2011. NI 52-107 permits Canadian public companies which are also SEC registrants the option to prepare their financial statements under US GAAP. Under this policy there will be no requirement to provide a reconciliation of the US GAAP financial statements to IFRS. DragonWave has carefully considered the implications of conversion to IFRS compared to US GAAP. We have determined that it is in the best interests of the company and the readers of our financial information to begin to provide US GAAP, rather than IFRS compliant financial statements in fiscal 2012. DragonWave already provides a US GAAP reconciliation to Canadian GAAP, and the differences are considered to be minor. Differences relate to the calculation of stock based compensation, and are fully explained in note 15 to the unaudited financial statements for the three and six months ended August 31, 2010. We will continue to assess the relative merits of providing IFRS compliant financial statements in the future.

26