UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21188

PIMCO California Municipal Income Fund III

(Exact name of registrant as specified in charter)

1633 Broadway, New York, New York 10019

(Address of principal executive offices) (Zip code)

Lawrence G. Altadonna —1633 Broadway, New York, New York 10019

(Name and address of agent for service)

Registrant’s telephone number, including area code: 212-739-3371

Date of fiscal year end: September 30, 2012

Date of reporting period: September 30, 2012

Item 1. REPORT TO SHAREHOLDERS

Annual Report

September 30, 2012

PIMCO Municipal Income Fund III

PIMCO California Municipal Income Fund III

PIMCO New York Municipal Income Fund III

Contents

| | | | | | |

| 9.30.12 | | PIMCO Municipal Income Funds III Annual Report | | | 1 | |

Hans W. Kertess

Chairman

Brian S. Shlissel

President & CEO

Dear Shareholder:

The municipal bond market benefitted from attractive valuations and strong demand during the fiscal twelve-month reporting period ended September 30, 2012. Longer-term, lower credit municipals were particularly favorable during the reporting period.

For the fiscal twelve-month period ended September 30, 2012:

| • | | PIMCO Municipal Income Fund III returned 23.34% on net asset value (“NAV”) and 33.20% on market price. |

| • | | PIMCO California Municipal Income Fund III returned 21.38% on NAV and 31.62% on market price. |

| • | | PIMCO New York Municipal Income Fund III returned 17.20% on NAV and 26.56% on market price. |

In contrast, the Barclays Municipal Bond Index increased a tax-advantaged 8.32% during the reporting period. The broad taxable bond market, represented by the Barclays U.S. Aggregate Index, rose 5.16%.

Twelve-Month Period in Review through September 30, 2012

The fiscal twelve-month reporting period began with gross domestic product (“GDP”), the value of goods and services produced in the country, the broadest measure of economic activity and the principal indicator of economic performance, expanding at an annual pace of 1.3%. GDP growth accelerated to an annual rate of 4.1% between October and December 2011. This momentum reversed during the first and second quarters of 2012 as GDP eased to a 2.0% and 1.3% annual pace respectively. Economic data released during the third quarter of 2012 indicated that the growth rate would be similarly tepid during that quarter.

The Federal Reserve (the “Fed”) revealed that it would launch a third round of “quantitative easing.” The Fed agreed to purchase $40 billion of mortgage securities each month for the foreseeable future. The objective is to lower already record low mortgage rates in an effort to boost the housing market. The Fed also indicated that it would continue “Operation Twist”, the program involving the selling of debt obligations with short-term maturities and the purchase of debt obligations with longer-term maturities.

The Fed also announced that it expected to keep the Fed Funds interest rate in the 0.0% to 0.25% range through 2015, longer than previously stated.

| | | | |

| 2 | | PIMCO Municipal Income Funds III Annual Report | | 9.30.12 |

Yields on U.S. Treasury bonds dropped to all-time lows during the twelve-month fiscal reporting period. At one point, the yield on the benchmark 10-year Treasury bond fell to 1.43%. It ended the period at 1.65% as of September 30, 2012. These low yields reflect market uncertainty over a variety of issues, notably the European Union’s ongoing fiscal crisis and the ongoing political standoff in Washington with respect to future levels of taxes and spending. Since municipal bond yields tend to track comparable Treasury bonds, municipal yields declined accordingly.

The Road Ahead

The credit and economic environment for municipal bonds is expected to remain challenging. Economic growth has been modest and overall tax revenues remain low, despite improving fiscal conditions of state and local governments. This suggests that municipal securities will remain under pressure.

The political standoff in Washington regarding future levels of taxes and spending is also a matter of

concern. Currently, federal taxes are scheduled to increase, and sharp spending cuts are planned to begin in January 2013. The prospect of higher taxes, reduced spending, or both, is likely to have a detrimental effect on the already-modest economic recovery. The potential for higher taxes, however, may increase the appeal of tax-advantaged products such as municipal securities.

For specific information on the Funds and their performance, please review the following pages. If you have any questions regarding the information provided, we encourage you to contact your financial advisor or call the Funds’ shareholder servicing agent at (800) 254-5197. In addition, a wide range of information and resources is available on our website, www.allianzinvestors.com/closedendfunds.

Together with Allianz Global Investors Fund Management LLC, the Funds’ investment manager, and Pacific Investment Management Company LLC (“PIMCO”), the Funds’ sub-adviser, we thank you for investing with us.

We remain dedicated to serving your investment needs.

Sincerely,

| | |

Hans W. Kertess Chairman | |

Brian S. Shlissel President & Chief Executive Officer |

Receive this report electronically and eliminate paper mailings. To enroll, go to www.allianzinvestors.com/ edelivery.

| | | | | | |

| 9.30.12 | | PIMCO Municipal Income Funds III Annual Report | | | 3 | |

PIMCO Municipal Income Funds III Fund Insights

September 30, 2012 (unaudited)

For the 12-month period ended September 30, 2012, PIMCO Municipal Income III (“Municipal III”) returned 23.34% on net asset value (“NAV”) and 33.20% on market price.

For the 12-month period ended September 30, 2012, PIMCO California Municipal Income III (“California Municipal III”) returned 21.38% on NAV and 31.62% on market price.

For the 12-month period ended September 30, 2012, PIMCO New York Municipal Income III (“New York Municipal III”) returned 17.20% on NAV and 26.56% on market price.

The municipal bond market generated strong results during the 12-month reporting period ended September 30, 2012. While there were several periods of weakness within the municipal market, these proved to be only temporary setbacks. In fact, the overall municipal market, as measured by the Barclays Municipal Bond Index (the “Benchmark”), posted positive returns during nine of the twelve months of the period. Supporting the market were strengthening municipal fundamentals, including rising tax revenues, as well as overall modest new issuance. In addition, investor demand was generally strong as investors sought higher incremental yield in the low interest rate environment. All told, during the 12-month period the Benchmark returned 8.32%. In comparison, the overall taxable fixed income market, as measured by the Barclays U.S. Aggregate Index, rose 5.16% during the period.

Municipal III and New York Municipal III benefited from positively emphasizing revenue bonds versus general obligation bonds. This contributed to results as revenue bonds outperformed general obligation bonds during the reporting period.

The Funds had an overweighting to the Tobacco and Healthcare sectors. This was beneficial as these sectors outperformed the Benchmark for the fiscal year ended September 30, 2012. Municipal III and New York Municipal III benefited from an overweighting to the strong performing Corporate-backed sector. California Municipal III was rewarded for an overweighting to the Education sector. Municipal III’s underweighting to Education and Special Tax sectors detracted from performance. California Municipal III’s underweighting to the Lease-backed sector was detrimental to returns as this sector outperformed.

During the reporting period, a shorter duration than that of the Benchmark detracted from all three Funds’ performance, as municipal yields declined during the 12-month period. In addition, a short Treasury position through the use of futures by California Municipal III and New York Municipal III was a drag on returns as a result of the declining interest rate environment.

Each fund utilized payer interest rate swaps to manage duration. This detracted from performance due to the falling interest rate environment. The Funds’ utilization of Treasury futures to manage the portfolios’ duration did not have a meaningfully impact on performance.

| | | | |

| 4 | | PIMCO Municipal Income Funds III Annual Report | | 9.30.12 |

PIMCO Municipal Income Funds III Performance & Statistics

September 30, 2012 (unaudited)

Municipal III:

| | | | | | | | |

| Total Return(1): | | Market Price | | | NAV | |

1 Year | | | 33.20% | | | | 23.34% | |

5 Year | | | 5.53% | | | | 2.84% | |

Commencement of Operations (10/31/02) to 9/30/12 | | | 6.05% | | | | 4.79% | |

Market Price/NAV Performance:

Commencement of Operations (10/31/02) to 9/30/12

| | | | |

| Market Price/NAV: | | | |

Market Price | | | $13.31 | |

NAV | | | $11.02 | |

Premium to NAV | | | 20.78% | |

Market Price Yield(2) | | | 6.31% | |

Leverage Ratio(3) | | | 38.24% | |

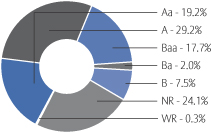

Moody’s Rating

(as a % of total investments)

California Municipal III:

| | | | | | | | |

| | |

| Total Return(1): | | Market Price | | | NAV | |

1 Year | | | 31.62% | | | | 21.38% | |

5 Year | | | 3.63% | | | | 0.63% | |

Commencement of Operations (10/31/02) to 9/30/12 | | | 4.46% | | | | 3.65% | |

Market Price/NAV Performance:

Commencement of Operations (10/31/02) to 9/30/12

| | | | |

| Market Price/NAV: | | | |

Market Price | | | $11.68 | |

NAV | | | $10.23 | |

Premium to NAV | | | 14.17% | |

Market Price Yield(2) | | | 6.16% | |

Leverage Ratio(3) | | | 41.39% | |

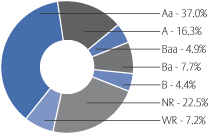

Moody’s Rating

(as a % of total investments)

| | | | | | |

| 9.30.12 | | PIMCO Municipal Income Funds III Annual Report | | | 5 | |

PIMCO Municipal Income Funds III Performance & Statistics

September 30, 2012 (unaudited)

New York Municipal III:

| | | | | | | | |

| Total Return(1): | | Market Price | | | NAV | |

1 Year | | | 26.56% | | | | 17.20% | |

5 Year | | | 1.90% | | | | –1.56% | |

Commencement of Operations (10/31/02) to 9/30/12 | | | 2.98% | | | | 2.39% | |

Market Price/NAV Performance:

Commencement of Operations (10/31/02) to 9/30/12

| | | | |

| Market Price/NAV: | | | |

Market Price | | | $10.66 | |

NAV | | | $9.65 | |

Premium to NAV | | | 10.47% | |

Market Price Yield(2) | | | 5.91% | |

Leverage Ratio(3) | | | 42.97% | |

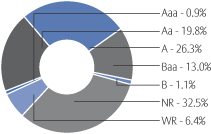

Moody’s Rating

(as a % of total investments)

(1) Past performance is no guarantee of future results. Total return is calculated by determining the percentage change in NAV or market price (as applicable) in the specified period. The calculation assumes that all income dividends and capital gain distributions, if any, have been reinvested. Total return does not reflect broker commissions or sales charges in connection with the purchase or sale of Fund shares. Total return for a period of more than one year represents the average annual total return.

Performance at market price will differ from results at NAV. Although market price returns typically reflect investment results over time, during shorter periods returns at market price can also be influenced by factors such as changing views about the Funds, market conditions, supply and demand for each Fund’s shares, or changes in each Fund’s dividends.

An investment in the Funds involves risk, including the loss of principal. Total return, market price, market price yield and NAV will fluctuate with changes in market conditions. This data is provided for information purposes only and is not intended for trading purposes. Closed-end funds, unlike open-end funds, are not continuously offered. There is a one time public offering and once issued, shares of closed-end funds are traded in the open market through a stock exchange. NAV is equal to total assets attributable to common shareholders less total liabilities divided by the number of common shares outstanding. Holdings are subject to change daily.

(2) Market Price Yield is determined by dividing the annualized current monthly dividend per common share (comprised of net investment income) by the market price per common share at September 30, 2012.

(3) Represents Floating Rate Notes Issued in tender option bond transactions and Preferred Shares (collectively “Leverage”) outstanding, as a percentage of total managed assets. Total managed assets refer to total assets (including assets attributable to Leverage) minus accrued liabilities (other than liabilities representing Leverage).

| | | | |

| 6 | | PIMCO Municipal Income Funds III Annual Report | | 9.30.12 |

PIMCO Municipal Income Fund III Schedule of Investments

September 30, 2012

| | | | | | | | |

Principal Amount (000s) | | | | | Value | |

| MUNICIPAL BONDS & NOTES – 97.0% | | | | |

| | | | Alabama – 2.2% | | | | |

| $ | 9,000 | | | Birmingham-Baptist Medical Centers Special Care Facs. Financing Auth. | | | | |

| | | | Rev., Baptist Health Systems, Inc., 5.00%, 11/15/30, Ser. A | | $ | 9,009,810 | |

| | 500 | | | Birmingham Special Care Facs. Financing Auth. Rev., | | | | |

| | | | Childrens Hospital, 6.00%, 6/1/39 (AGC) | | | 593,250 | |

| | 1,500 | | | Colbert Cnty. Northwest Health Care Auth. Rev., 5.75%, 6/1/27 | | | 1,465,065 | |

| | 1,000 | | | State Docks Department Rev., 6.00%, 10/1/40 | | | 1,149,710 | |

| | | | | | | | |

| | | | | | | 12,217,835 | |

| | | | | | | | |

| | | | Arizona – 6.5% | | | | |

| | | | Health Facs. Auth. Rev., | | | | |

| | | | Banner Health, | | | | |

| | 1,250 | | | 5.00%, 1/1/35, Ser. A | | | 1,333,500 | |

| | 900 | | | 5.50%, 1/1/38, Ser. D | | | 996,417 | |

| | 2,250 | | | Beatitudes Campus Project, 5.20%, 10/1/37 | | | 2,053,665 | |

| | | | Pima Cnty. Industrial Dev. Auth. Rev., | | | | |

| | 13,000 | | | 5.00%, 9/1/39 (h) | | | 13,613,600 | |

| | 750 | | | Tucson Electric Power Co., 5.25%, 10/1/40, Ser. A | | | 815,745 | |

| | 5,000 | | | Salt River Project Agricultural Improvement & Power Dist. Rev., 5.00%, 1/1/39, Ser. A (h) | | | 5,604,650 | |

| | 11,600 | | | Salt Verde Financial Corp. Rev., 5.00%, 12/1/37 | | | 12,726,824 | |

| | | | | | | | |

| | | | | | | 37,144,401 | |

| | | | | | | | |

| | | | California – 14.0% | | | | |

| | | | Bay Area Toll Auth. Rev., San Francisco Bay Area, | | | | |

| | 1,500 | | | 5.00%, 10/1/29 | | | 1,712,985 | |

| | 500 | | | 5.00%, 4/1/34, Ser. F-1 | | | 561,890 | |

| | 3,260 | | | 5.00%, 10/1/42 | | | 3,605,625 | |

| | | | Golden State Tobacco Securitization Corp. Rev., Ser. A-1, | | | | |

| | 4,600 | | | 5.125%, 6/1/47 | | | 3,543,564 | |

| | 7,120 | | | 5.75%, 6/1/47 | | | 6,070,156 | |

| | | | Health Facs. Financing Auth. Rev., | | | | |

| | 2,500 | | | Catholic Healthcare West, 6.00%, 7/1/39, Ser. A | | | 2,928,100 | |

| | | | Sutter Health, | | | | |

| | 600 | | | 5.00%, 11/15/42, Ser. A (IBC-NPFGC) | | | 630,912 | |

| | 1,500 | | | 6.00%, 8/15/42, Ser. B | | | 1,788,840 | |

| | 3,350 | | | Indian Wells Redev. Agcy., Tax Allocation, | | | | |

| | | | Whitewater Project, 4.75%, 9/1/34, Ser. A (AMBAC) | | | 3,044,044 | |

| | 130 | | | Los Angeles Unified School Dist., GO, 5.00%, 7/1/30, Ser. E (AMBAC) | | | 141,526 | |

| | 2,000 | | | M-S-R Energy Auth. Rev., 6.50%, 11/1/39, Ser. B | | | 2,607,300 | |

| | 1,580 | | | Municipal Finance Auth. Rev., Azusa Pacific Univ. Project, | | | | |

| | | | 7.75%, 4/1/31, Ser. B | | | 1,868,129 | |

| | | | | | |

| 9.30.12 | | PIMCO Municipal Income Funds III Annual Report | | | 7 | |

PIMCO Municipal Income Fund III Schedule of Investments

September 30, 2012 (continued)

| | | | | | | | |

Principal Amount (000s) | | | | | Value | |

| | | | California (continued) | | | | |

| $ | 1,250 | | | Palomar Pomerado Health, CP, 6.75%, 11/1/39 | | $ | 1,405,912 | |

| | 1,600 | | | San Marcos Unified School Dist., GO, 5.00%, 8/1/38, Ser. A | | | 1,800,240 | |

| | | | State, GO, | | | | |

| | 5,000 | | | 5.00%, 6/1/37 | | | 5,425,000 | |

| | 5,300 | | | 5.00%, 12/1/37 | | | 5,843,091 | |

| | 1,350 | | | 5.25%, 3/1/38 | | | 1,489,995 | |

| | 1,300 | | | 5.25%, 11/1/40 | | | 1,497,340 | |

| | 3,200 | | | 5.50%, 3/1/40 | | | 3,693,504 | |

| | 2,500 | | | 5.75%, 4/1/31 | | | 2,948,175 | |

| | 5,000 | | | 6.00%, 4/1/38 | | | 5,963,700 | |

| | | | Statewide Communities Dev. Auth. Rev., | | | | |

| | 1,000 | | | American Baptist Homes West, 6.25%, 10/1/39 | | | 1,090,870 | |

| | 2,205 | | | California Baptist Univ., 5.75%, 11/1/17, Ser. B (a)(d) | | | 2,533,347 | |

| | | | Methodist Hospital Project (FHA), | | | | |

| | 2,900 | | | 6.625%, 8/1/29 | | | 3,677,722 | |

| | 10,300 | | | 6.75%, 2/1/38 | | | 12,711,127 | |

| | 1,200 | | | Tobacco Securitization Auth. of Southern California Rev., 5.00%, 6/1/37, Ser. A-1 | | | 980,160 | |

| | | | | | | | |

| | | | | | | 79,563,254 | |

| | | | | | | | |

| | | | Colorado – 0.8% | | | | |

| | 500 | | | Confluence Metropolitan Dist. Rev., 5.45%, 12/1/34 | | | 403,295 | |

| | 500 | | | Health Facs. Auth. Rev.,

Evangelical Lutheran, 6.125%, 6/1/38, Ser. A (Pre-refunded @ $100, 6/1/14) (c) | | | 547,955 | |

| | 2,000 | | | Sisters of Charity of Leavenworth Health System, 5.00%, 1/1/40, Ser. A | | | 2,181,040 | |

| | 500 | | | Public Auth. for Colorado Energy Rev., 6.50%, 11/15/38 | | | 639,905 | |

| | 500 | | | Regional Transportation Dist. Rev., Denver Transportation Partners, 6.00%, 1/15/34 | | | 585,235 | |

| | | | | | | | |

| | | | | | | 4,357,430 | |

| | | | | | | | |

| | | | Connecticut – 0.3% | | | | |

| | 1,250 | | | Harbor Point Infrastructure Improvement Dist., Tax Allocation, 7.875%, 4/1/39, Ser. A | | | 1,427,862 | |

| | | | | | | | |

| | | | District of Columbia – 2.1% | | | | |

| | 10,000 | | | Water & Sewer Auth. Rev., 5.50%, 10/1/39, Ser. A (h) | | | 11,757,800 | |

| | | | | | | | |

| | | | Florida – 4.1% | | | | |

| | 3,480 | | | Brevard Cnty. Health Facs. Auth. Rev., Health First, Inc. Project, 5.00%, 4/1/34 | | | 3,602,774 | |

| | 500 | | | Broward Cnty. Airport System Rev., 5.375%, 10/1/29, Ser. O | | | 576,465 | |

| | 4,500 | | | Broward Cnty. Water & Sewer Utility Rev., 5.25%, 10/1/34, Ser. A (h) | | | 5,184,945 | |

| | 3,000 | | | Cape Coral Water & Sewer Rev., 5.00%, 10/1/41 (AGM) | | | 3,376,710 | |

| | 350 | | | Dev. Finance Corp. Rev., Renaissance Charter School, 6.50%, 6/15/21, Ser. A | | | 394,800 | |

| | 2,500 | | | Hillsborough Cnty. Industrial Dev. Auth. Rev., | | | | |

| | | | Tampa General Hospital Project, 5.25%, 10/1/34, Ser. B | | | 2,560,650 | |

| | | | |

| 8 | | PIMCO Municipal Income Funds III Annual Report | | 9.30.12 |

PIMCO Municipal Income Fund III Schedule of Investments

September 30, 2012 (continued)

| | | | | | | | |

Principal Amount (000s) | | | | | Value | |

| | | | Florida (continued) | | | | |

| $ | 3,895 | | | Sarasota Cnty. Health Facs. Auth. Rev., | | | | |

| | | | Sarasota-Manatee Jewish Housing Council, Inc. Project, 5.75%, 7/1/45 | | $ | 2,994,905 | |

| | 4,200 | | | State Board of Education, GO, 5.00%, 6/1/38, Ser. D (h) | | | 4,799,382 | |

| | | | | | | | |

| | | | | | | 23,490,631 | |

| | | | | | | | |

| | | | Georgia – 0.4% | | | | |

| | 1,750 | | | Fulton Cnty. Residential Care Facs. for the Elderly Auth. Rev., | | | | |

| | | | Lenbrook Project, 5.125%, 7/1/42, Ser. A | | | 1,679,002 | |

| | 400 | | | Medical Center Hospital Auth. Rev., Spring Harbor Green Island Project, 5.25%, 7/1/37 | | | 387,584 | |

| | | | | | | | |

| | | | | | | 2,066,586 | |

| | | | | | | | |

| | | | Hawaii – 0.3% | | | | |

| | 1,500 | | | Hawaii Pacific Health Rev., 5.50%, 7/1/40, Ser. A | | | 1,666,410 | |

| | | | | | | | |

| | | | Illinois – 5.7% | | | | |

| | 5,000 | | | Chicago, GO, 5.00%, 1/1/34, Ser. C (h) | | | 5,475,900 | |

| | | | Finance Auth. Rev., | | | | |

| | | | Leafs Hockey Club Project, Ser. A (b)(e), | | | | |

| | 1,000 | | | 5.875%, 3/1/27 | | | 339,500 | |

| | 625 | | | 6.00%, 3/1/37 | | | 209,831 | |

| | 400 | | | OSF Healthcare System, 7.125%, 11/15/37, Ser. A | | | 483,384 | |

| | 12,795 | | | Peoples Gas Light & Coke Co., 5.00%, 2/1/33 (AMBAC) | | | 12,864,733 | |

| | 1,000 | | | Swedish Covenant Hospital, 6.00%, 8/15/38, Ser. A | | | 1,125,110 | |

| | | | Univ. of Chicago, | | | | |

| | 165 | | | 5.25%, 7/1/41, Ser. 05-A | | | 165,147 | |

| | 5,000 | | | 5.50%, 7/1/37, Ser. B (h) | | | 5,918,250 | |

| | 5,000 | | | State Toll Highway Auth. Rev., 5.50%, 1/1/33, Ser. B | | | 5,568,800 | |

| | | | | | | | |

| | | | | | | 32,150,655 | |

| | | | | | | | |

| | | | Indiana – 1.1% | | | | |

| | 500 | | | Dev. Finance Auth. Rev., 5.00%, 3/1/30, Ser. B (AMBAC) | | | 500,430 | |

| | | | Portage, Tax Allocation, Ameriplex Project, | | | | |

| | 1,000 | | | 5.00%, 7/15/23 | | | 1,025,540 | |

| | 775 | | | 5.00%, 1/15/27 | | | 786,943 | |

| | 2,800 | | | Vigo Cnty. Hospital Auth. Rev., Union Hospital, Inc., 7.50%, 9/1/22 | | | 3,653,440 | |

| | | | | | | | |

| | | | | | | 5,966,353 | |

| | | | | | | | |

| | | | Iowa – 0.1% | | | | |

| | | | Finance Auth. Rev., Deerfield Retirement Community, Inc., Ser. A, | | | | |

| | 120 | | | 5.50%, 11/15/27 | | | 113,173 | |

| | 575 | | | 5.50%, 11/15/37 | | | 518,650 | |

| | | | | | | | |

| | | | | | | 631,823 | |

| | | | | | | | |

| | | | | | |

| 9.30.12 | | PIMCO Municipal Income Funds III Annual Report | | | 9 | |

PIMCO Municipal Income Fund III Schedule of Investments

September 30, 2012 (continued)

| | | | | | | | |

Principal Amount (000s) | | | | | Value | |

| | | | Kentucky – 0.8% | | | | |

| | | | Economic Dev. Finance Auth. Rev., | | | | |

| $ | 1,000 | | | Catholic Healthcare Partners, 5.25%, 10/1/30 | | $ | 1,000,000 | |

| | 2,000 | | | Owensboro Medical Healthcare Systems, 6.375%, 6/1/40, Ser. A | | | 2,375,960 | |

| | 1,250 | | | Ohio Cnty. Pollution Control Rev., | | | | |

| | | | Big Rivers Electric Corp. Project, 6.00%, 7/15/31, Ser. A | | | 1,329,662 | |

| | | | | | | | |

| | | | | | | 4,705,622 | |

| | | | | | | | |

| | | | Louisiana – 1.6% | | | | |

| | | | Local Gov’t Environmental Facs. & Community Dev. Auth. Rev., | | | | |

| | 400 | | | Westlake Chemical Corp., 6.50%, 11/1/35, Ser. A-2 | | | 466,928 | |

| | | | Woman’s Hospital Foundation, Ser. A, | | | | |

| | 1,500 | | | 5.875%, 10/1/40 | | | 1,698,495 | |

| | 1,000 | | | 6.00%, 10/1/44 | | | 1,137,160 | |

| | | | Public Facs. Auth. Rev., Ochsner Clinic Foundation Project, | | | | |

| | 1,700 | | | 5.50%, 5/15/47, Ser. B | | | 1,794,707 | |

| | 2,000 | | | 6.50%, 5/15/37 | | | 2,396,800 | |

| | 1,345 | | | Tobacco Settlement Financing Corp. Rev., 5.875%, 5/15/39, Ser. 2001-B | | | 1,376,164 | |

| | | | | | | | |

| | | | | | | 8,870,254 | |

| | | | | | | | |

| | | | Maryland – 0.8% | | | | |

| | 1,000 | | | Economic Dev. Corp. Rev., 5.75%, 6/1/35, Ser. B | | | 1,086,930 | |

| | | | Health & Higher Educational Facs. Auth. Rev., | | | | |

| | 1,500 | | | Calvert Health System, 5.50%, 7/1/36 | | | 1,559,565 | |

| | 700 | | | Charlestown Community, 6.25%, 1/1/41 | | | 801,171 | |

| | 1,000 | | | Lifebridge Health, 6.00%, 7/1/41 | | | 1,162,310 | |

| | | | | | | | |

| | | | | | | 4,609,976 | |

| | | | | | | | |

| | | | Massachusetts – 1.3% | | | | |

| | | | Dev. Finance Agcy. Rev., | | | | |

| | 300 | | | Adventcare Project, 7.625%, 10/15/37 | | | 340,941 | |

| | | | Linden Ponds, Inc. Fac., | | | | |

| | 140 | | | zero coupon, 11/15/56, Ser. B (b) | | | 1,921 | |

| | 28 | | | 5.50%, 11/15/46, Ser. A-2 (b) | | | 18,957 | |

| | 529 | | | 6.25%, 11/15/39, Ser. A-1 | | | 408,439 | |

| | 4,910 | | | Housing Finance Agcy. Rev., 5.125%, 6/1/43, Ser. H | | | 4,917,512 | |

| | 1,600 | | | State College Building Auth. Rev., 5.50%, 5/1/39, Ser. A | | | 1,823,808 | |

| | | | | | | | |

| | | | | | | 7,511,578 | |

| | | | | | | | |

| | | | Michigan – 12.4% | | | | |

| | 1,500 | | | Detroit, GO, 5.25%, 11/1/35 | | | 1,650,030 | |

| | 9,320 | | | Detroit Sewage Disposal System Rev., 5.00%, 7/1/32, Ser. A (AGM) | | | 9,388,502 | |

| | | | |

| 10 | | PIMCO Municipal Income Funds III Annual Report | | 9.30.12 |

PIMCO Municipal Income Fund III Schedule of Investments

September 30, 2012 (continued)

| | | | | | | | |

Principal Amount (000s) | | | | | Value | |

| | | | Michigan (continued) | | | | |

| $ | 5,000 | | | Detroit Water and Sewerage Department Rev., 5.25%, 7/1/39, Ser. A | | $ | 5,341,700 | |

| | | | Detroit Water Supply System Rev., | | | | |

| | 16,000 | | | 5.00%, 7/1/34, Ser. A (NPFGC) | | | 16,189,280 | |

| | 7,555 | | | 5.00%, 7/1/34, Ser. B (NPFGC) | | | 7,644,376 | |

| | 5,000 | | | 5.25%, 7/1/41, Ser. A | | | 5,324,050 | |

| | 500 | | | Global Preparatory Academy Rev., 5.25%, 11/1/36 | | | 396,385 | |

| | 1,500 | | | Royal Oak Hospital Finance Auth. Rev., William Beaumont Hospital, 8.25%, 9/1/39 | | | 1,932,060 | |

| | | | State Hospital Finance Auth. Rev., | | | | |

| | 575 | | | Oakwood Group, 6.00%, 4/1/22, Ser. A (Pre-refunded @ $100, 4/1/13) (c) | | | 591,445 | |

| | 20,000 | | | Trinity Health, 5.375%, 12/1/30 (Pre-refunded @ $100, 12/1/12) (c) | | | 20,167,600 | |

| | 1,300 | | | State Univ. Rev., 6.173%, 2/15/50, Ser. A | | | 1,593,345 | |

| | | | | | | | |

| | | | | | | 70,218,773 | |

| | | | | | | | |

| | | | Minnesota – 0.0% | | | | |

| | 125 | | | Duluth Housing & Redev. Auth. Rev., 5.875%, 11/1/40, Ser. A | | | 127,691 | |

| | | | | | | | |

| | | | Missouri – 0.1% | | | | |

| | 250 | | | Jennings Rev., Northland Redev. Area Project, 5.00%, 11/1/23 | | | 245,035 | |

| | 500 | | | Manchester, Tax Allocation, Highway 141/Manchester Road Project, 6.875%, 11/1/39 | | | 534,095 | |

| | | | | | | | |

| | | | | | | 779,130 | |

| | | | | | | | |

| | | | New Hampshire – 0.4% | | | | |

| | 2,000 | | | Business Finance Auth. Rev., Elliot Hospital, 6.125%, 10/1/39, Ser. A | | | 2,266,200 | |

| | | | | | | | |

| | | | New Jersey – 6.1% | | | | |

| | 1,000 | | | Camden Cnty. Improvement Auth. Rev., Cooper Health Systems Group, 5.00%, 2/15/35, Ser. A | | | 1,024,140 | |

| | 300 | | | Economic Dev. Auth. Rev., Newark Airport Marriott Hotel, 7.00%, 10/1/14 | | | 300,927 | |

| | 4,500 | | | Economic Dev. Auth., Special Assessment, Kapkowski Road Landfill Project, 6.50%, 4/1/28 | | | 5,434,380 | |

| | 1,000 | | | Health Care Facs. Financing Auth. Rev., St. Peter’s Univ. Hospital, 5.75%, 7/1/37 | | | 1,052,760 | |

| | | | Tobacco Settlement Financing Corp. Rev., Ser. 1-A, | | | | |

| | 1,600 | | | 4.75%, 6/1/34 | | | 1,318,768 | |

| | 19,745 | | | 5.00%, 6/1/41 | | | 16,425,471 | |

| | 8,000 | | | Transportation Trust Fund Auth. Rev., 5.00%, 6/15/42, Ser. B | | | 9,066,160 | |

| | | | | | | | |

| | | | | | | 34,622,606 | |

| | | | | | | | |

| | | | New Mexico – 0.2% | | | | |

| | 1,000 | | | Farmington Pollution Control Rev., 5.90%, 6/1/40, Ser. D | | | 1,115,170 | |

| | | | | | | | |

| | | | | | |

| 9.30.12 | | PIMCO Municipal Income Funds III Annual Report | | | 11 | |

PIMCO Municipal Income Fund III Schedule of Investments

September 30, 2012 (continued)

| | | | | | | | |

Principal Amount (000s) | | | | | Value | |

| | | | New York – 12.2% | | | | |

| $ | 9,800 | | | Brooklyn Arena Local Dev. Corp. Rev., Barclays Center Project, 6.25%, 7/15/40 | | $ | 11,314,394 | |

| | 5,000 | | | Hudson Yards Infrastructure Corp. Rev., 5.75%, 2/15/47, Ser. A | | | 5,909,050 | |

| | 1,700 | | | Liberty Dev. Corp. Rev., Goldman Sachs Headquarters, 5.50%, 10/1/37 | | | 2,042,975 | |

| | 3,000 | | | Metropolitan Transportation Auth. Rev., 5.00%, 11/15/36, Ser. D | | | 3,368,460 | |

| | 1,150 | | | Nassau Cnty. Industrial Dev. Agcy. Rev., Amsterdam at Harborside, 6.70%, 1/1/43, Ser. A | | | 790,257 | |

| | 10,450 | | | New York City Industrial Dev. Agcy. Rev., Yankee Stadium, 7.00%, 3/1/49 (AGC) | | | 12,647,217 | |

| | | | New York City Municipal Water Finance Auth. Water & Sewer Rev. (h), | | | | |

| | 4,900 | | | 5.00%, 6/15/37, Ser. D | | | 5,360,208 | |

| | 4,000 | | | Second Generation Resolutions, 4.75%, 6/15/35, Ser. DD | | | 4,424,680 | |

| | | | New York Liberty Dev. Corp. Rev., | | | | |

| | 10,000 | | | 1 World Trade Center Project, 5.00%, 12/15/41 | | | 11,305,100 | |

| | 11,255 | | | 4 World Trade Center Project, 5.00%, 11/15/44 | | | 12,451,519 | |

| | | | | | | | |

| | | | | | | 69,613,860 | |

| | | | | | | | |

| | | | North Carolina – 1.4% | | | | |

| | 1,500 | | | Medical Care Commission Rev., Cleveland Cnty. Healthcare, 5.00%, 7/1/35, Ser. A (AMBAC) | | | 1,528,740 | |

| | 6,000 | | | New Hanover Cnty. Rev., New Hanover Regional Medical Center, 5.00%, 10/1/28 | | | 6,655,140 | |

| | | | | | | | |

| | | | | | | 8,183,880 | |

| | | | | | | | |

| | | | Ohio – 3.9% | | | | |

| | 500 | | | Allen Cnty. Catholic Healthcare Rev., Allen Hospital, 5.00%, 6/1/38, Ser. A | | | 538,500 | |

| | | | Buckeye Tobacco Settlement Financing Auth. Rev., Ser. A-2, | | | | |

| | 2,400 | | | 5.875%, 6/1/30 | | | 1,984,680 | |

| | 2,350 | | | 5.875%, 6/1/47 | | | 1,897,132 | |

| | 7,290 | | | 6.00%, 6/1/42 | | | 6,039,765 | |

| | 5,000 | | | 6.50%, 6/1/47 | | | 4,423,450 | |

| | 3,500 | | | Hamilton Cnty. Healthcare Rev.,

Christ Hospital Project, 5.00%, 6/1/42 | | | 3,708,880 | |

| | 500 | | | Higher Educational Fac. Commission Rev., Univ. Hospital Health Systems,

6.75%, 1/15/39, Ser. 2009-A (Pre-refunded @ $100, 1/15/15) (c) | | | 572,335 | |

| | 2,500 | | | Lorain Cnty. Hospital Rev., Catholic Healthcare, | | | | |

| | | | 5.375%, 10/1/30 (Pre-refunded @ $100, 10/1/12) (c) | | | 2,500,000 | |

| | 500 | | | Montgomery Cnty. Rev., Miami Valley Hospital, 6.25%, 11/15/39, Ser. A | | | 534,875 | |

| | | | | | | | |

| | | | | | | 22,199,617 | |

| | | | | | | | |

| | | | Pennsylvania – 2.3% | | | | |

| | 1,000 | | | Allegheny Cnty. Hospital Dev. Auth. Rev., Univ. of Pittsburgh Medical Center, 5.625%, 8/15/39 | | | 1,130,620 | |

| | | | |

| 12 | | PIMCO Municipal Income Funds III Annual Report | | 9.30.12 |

PIMCO Municipal Income Fund III Schedule of Investments

September 30, 2012 (continued)

| | | | | | | | |

Principal Amount (000s) | | | | | Value | |

| | | | Pennsylvania (continued) | | | | |

| $ | 4,000 | | | Berks Cnty. Municipal Auth. Rev., Reading Hospital Medical Center, 5.00%, 11/1/44, Ser. A | | $ | 4,388,960 | |

| | | | Cumberland Cnty. Municipal Auth. Rev., Messiah Village Project, Ser. A, | | | | |

| | 750 | | | 5.625%, 7/1/28 | | | 792,240 | |

| | 670 | | | 6.00%, 7/1/35 | | | 711,614 | |

| | 1,000 | | | Dauphin Cnty. General Auth. Rev., Pinnacle Health System Project, 6.00%, 6/1/36, Ser. A | | | 1,130,220 | |

| | 1,250 | | | Harrisburg Auth. Rev., Harrisburg Univ. of Science, 6.00%, 9/1/36, Ser. B (e) | | | 988,600 | |

| | 100 | | | Luzerne Cnty. Industrial Dev. Auth. Rev., Pennsylvania American Water Co., 5.50%, 12/1/39 | | | 111,561 | |

| | 500 | | | Philadelphia Water & Sewer Rev., 5.25%, 1/1/36, Ser. A | | | 556,080 | |

| | 3,000 | | | Turnpike Commission Rev., 5.125%, 12/1/40, Ser. D | | | 3,284,400 | |

| | | | | | | | |

| | | | | | | 13,094,295 | |

| | | | | | | | |

| | | | Puerto Rico – 1.0% | | | | |

| | | | Sales Tax Financing Corp. Rev., | | | | |

| | 2,400 | | | 5.00%, 8/1/40, Ser. A (AGM) (h) | | | 2,532,288 | |

| | 3,000 | | | 5.375%, 8/1/38, Ser. C | | | 3,212,250 | |

| | | | | | | | |

| | | | | | | 5,744,538 | |

| | | | | | | | |

| | | | South Carolina – 1.3% | | | | |

| | 1,000 | | | Greenwood Cnty. Rev., Self Regional Healthcare, 5.375%, 10/1/39 | | | 1,092,090 | |

| | 5,305 | | | Jobs-Economic Dev. Auth. Rev., Bon Secours Health System, 5.625%, 11/15/30, Ser. B | | | 5,336,140 | |

| | 800 | | | State Ports Auth. Rev., 5.25%, 7/1/40 | | | 896,512 | |

| | | | | | | | |

| | | | | | | 7,324,742 | |

| | | | | | | | |

| | | | Tennessee – 0.5% | | | | |

| | 1,250 | | | Claiborne Cnty. Industrial Dev. Board Rev., Lincoln Memorial Univ. Project, 6.625%, 10/1/39 | | | 1,416,687 | |

| | 1,000 | | | Johnson City Health & Educational Facs. Board Rev., | | | | |

| | | | Mountain States Health Alliance, 6.00%, 7/1/38, Ser. A | | | 1,160,890 | |

| | | | | | | | |

| | | | | | | 2,577,577 | |

| | | | | | | | |

| | | | Texas – 8.5% | | | | |

| | 1,300 | | | Dallas Rev., Dallas Civic Center, 5.25%, 8/15/38 (AGC) | | | 1,445,288 | |

| | 3,000 | | | Harris Cnty. Cultural Education Facs. Finance Corp. Rev., Baylor College of Medicine, 5.00%, 11/15/37 | | | 3,247,470 | |

| | | | North Harris Cnty. Regional Water Auth. Rev., | | | | |

| | 5,500 | | | 5.25%, 12/15/33 | | | 6,129,255 | |

| | 5,500 | | | 5.50%, 12/15/38 | | | 6,137,230 | |

| | | | | | |

| 9.30.12 | | PIMCO Municipal Income Funds III Annual Report | | | 13 | |

PIMCO Municipal Income Fund III Schedule of Investments

September 30, 2012 (continued)

| | | | | | | | |

Principal Amount (000s) | | | | | Value | |

| | | | Texas (continued) | | | | |

| | | | North Texas Tollway Auth. Rev., | | | | |

| $ | 3,000 | | | 5.00%, 1/1/38 | | $ | 3,277,020 | |

| | 600 | | | 5.50%, 9/1/41, Ser. A | | | 717,030 | |

| | 10,800 | | | 5.625%, 1/1/33, Ser. A | | | 12,238,560 | |

| | 700 | | | 5.75%, 1/1/33, Ser. F | | | 773,409 | |

| | 2,000 | | | Sabine River Auth. Pollution Control Rev., TXU Energy, 5.20%, 5/1/28, Ser. C (b) | | | 205,140 | |

| | 3,000 | | | Tarrant Cnty. Cultural Education Facs. Finance Corp. Rev., | | | | |

| | | | Baylor Health Care Systems Project, 6.25%, 11/15/29 | | | 3,643,830 | |

| | | | Texas Municipal Gas Acquisition & Supply Corp. I Rev., | | | | |

| | 150 | | | 5.25%, 12/15/26, Ser. A | | | 167,733 | |

| | 8,100 | | | 6.25%, 12/15/26, Ser. D | | | 9,950,121 | |

| | 500 | | | Wise Cnty. Rev., Parker Cnty. Junior College Dist., 8.00%, 8/15/34 | | | 578,750 | |

| | | | | | | | |

| | | | | | | 48,510,836 | |

| | | | | | | | |

| | | | Virginia – 0.3% | | | | |

| | 1,000 | | | Fairfax Cnty. Industrial Dev. Auth. Rev., Inova Health Systems, 5.50%, 5/15/35, Ser. A | | | 1,145,120 | |

| | 1,000 | | | James City Cnty. Economic Dev. Auth. Rev., United Methodist Homes, 5.50%, 7/1/37, Ser. A | | | 825,660 | |

| | | | | | | | |

| | | | | | | 1,970,780 | |

| | | | | | | | |

| | | | Washington – 3.7% | | | | |

| | | | Health Care Facs. Auth. Rev., | | | | |

| | 500 | | | Kadlec Regional Medical Center, 5.50%, 12/1/39 | | | 529,600 | |

| | 1,000 | | | Seattle Cancer Care Alliance, 7.375%, 3/1/38 | | | 1,236,950 | |

| | 18,685 | | | Tobacco Settlement Auth. Rev., 6.50%, 6/1/26 | | | 19,462,296 | |

| | | | | | | | |

| | | | | | | 21,228,846 | |

| | | | | | | | |

| | | | West Virginia – 0.2% | | | | |

| | 1,000 | | | Hospital Finance Auth. Rev., Highland Hospital, 9.125%, 10/1/41 | | | 1,216,680 | |

| | | | | | | | |

| | | | Wisconsin – 0.4% | | | | |

| | | | Health & Educational Facs. Auth. Rev., | | | | |

| | 1,000 | | | Aurora Health Care, Inc., 5.625%, 4/15/39, Ser. A | | | 1,103,410 | |

| | 1,000 | | | Prohealth Care, Inc., 6.625%, 2/15/39 | | | 1,186,320 | |

| | | | | | | | |

| | | | | | | 2,289,730 | |

| | | | | | | | |

| | | | Total Municipal Bonds & Notes (cost- $497,537,744) | | | 551,223,421 | |

| | | | | | | | |

| | | | | | | | |

| VARIABLE RATE NOTES (a)(d)(f)(g) – 3.0% | | | | |

| | | | California – 0.4% | | | | |

| | 1,675 | | | Los Angeles Community College Dist., GO, 13.80%, 8/1/33, Ser. 3096 | | | 2,308,569 | |

| | | | | | | | |

| | | | Florida – 1.1% | | | | |

| | 5,000 | | | Greater Orlando Aviation Auth. Rev., 9.44%, 10/1/39, Ser. 3174 | | | 6,031,600 | |

| | | | | | | | |

| | | | Texas – 1.5% | | | | |

| | 6,500 | | | JPMorgan Chase Putters/Drivers Trust, GO, 9.386%, 2/1/17, Ser. 3480 | | | 8,729,500 | |

| | | | | | | | |

| | | | Total Variable Rate Notes (cost-$13,078,420) | | | 17,069,669 | |

| | | | | | | | |

| | | | Total Investments (cost-$510,616,164) – 100.0% | | $ | 568,293,090 | |

| | | | | | | | |

| | | | |

| 14 | | PIMCO Municipal Income Funds III Annual Report | | 9.30.12 |

PIMCO Municipal Income Fund III Schedule of Investments

September 30, 2012 (continued)

| | | | | | |

| Industry classification of portfolio holdings as a percentage of total investments at September 30, 2012 was as follows: | |

| Revenue Bonds: | | | | | | |

Health, Hospital, Nursing Home Revenue | | 24.8% | | | | |

Tobacco Settlement Funded | | 11.2 | | | | |

Water Revenue | | 10.6 | | | | |

Natural Gas Revenue | | 7.0 | | | | |

Sewer Revenue | | 4.7 | | | | |

Recreational Revenue | | 4.3 | | | | |

Miscellaneous Revenue | | 4.2 | | | | |

Port, Airport & Marina Revenue | | 3.7 | | | | |

College & University Revenue | | 3.5 | | | | |

Highway Revenue Tolls | | 3.4 | | | | |

Industrial Revenue | | 2.7 | | | | |

Lease (Appropriation) | | 2.4 | | | | |

Local or Government Housing | | 1.6 | | | | |

Electric Power & Lighting Revenue | | 1.6 | | | | |

Miscellaneous Taxes | | 1.0 | | | | |

Sales Tax Revenue | | 1.0 | | | | |

Transit Revenue | | 0.7 | | | | |

Ad Valorem Property Tax | | 0.1 | | | | |

Tax Increment/ Allocation Revenue | | 0.0 | | | | |

| | | | | | |

| Total Revenue Bonds | | | | | 88.5 | % |

| General Obligation Bonds | | | | | 9.1 | |

| Tax Allocation | | | | | 1.2 | |

| Special Assessments | | | | | 1.0 | |

| Certificates of Participation | | | | | 0.2 | |

| | | | | | |

| Total Investments | | | | | 100.0 | % |

| | | | | | |

| | | | | | |

| 9.30.12 | | PIMCO Municipal Income Funds III Annual Report | | | 15 | |

PIMCO California Municipal Income Fund III Schedule of Investments

September 30, 2012

| | | | | | | | |

Principal

Amount

(000s) | | | | | Value | |

| CALIFORNIA MUNICIPAL BONDS & NOTES – 95.5% | | | | |

| $ | 1,250 | | | Bay Area Toll Auth. Rev., San Francisco Bay Area, | | | | |

| | | | 5.00%, 4/1/34, Ser. F-1 | | $ | 1,404,725 | |

| | 1,000 | | | Cathedral City Public Financing Auth., Tax Allocation, | | | | |

| | | | 5.00%, 8/1/33, Ser. A (NPFGC) | | | 975,910 | |

| | 1,150 | | | Ceres Redev. Agcy., Tax Allocation, | | | | |

| | | | Project Area No. 1, 5.00%, 11/1/33 (NPFGC) | | | 1,152,898 | |

| | 2,000 | | | Chula Vista Rev., San Diego Gas & Electric, 5.875%, 2/15/34, Ser. B | | | 2,363,280 | |

| | 550 | | | City & Cnty. of San Francisco, Capital Improvement Projects, CP, | | | | |

| | | | 5.25%, 4/1/31, Ser. A | | | 616,671 | |

| | 1,415 | | | Contra Costa Cnty. Public Financing Auth., Tax Allocation, | | | | |

| | | | 5.625%, 8/1/33, Ser. A | | | 1,390,195 | |

| | | | Educational Facs. Auth. Rev. (h), | | | | |

| | 9,800 | | | Claremont McKenna College, 5.00%, 1/1/39 | | | 10,784,998 | |

| | 10,000 | | | Univ. of Southern California, 5.00%, 10/1/39, Ser. A | | | 11,342,000 | |

| | 1,695 | | | El Dorado Irrigation Dist. & El Dorado Cnty. Water Agcy., CP, | | | | |

| | | | 5.75%, 8/1/39, Ser. A (AGC) | | | 1,835,600 | |

| | | | Golden State Tobacco Securitization Corp. Rev., | | | | |

| | 11,000 | | | 5.00%, 6/1/45 (AMBAC-TCRS) | | | 11,241,010 | |

| | 4,000 | | | 5.00%, 6/1/45, Ser. A (FGIC-TCRS) | | | 4,087,640 | |

| | 13,865 | | | 5.75%, 6/1/47, Ser. A-1 | | | 11,820,606 | |

| | | | Health Facs. Financing Auth. Rev., | | | | |

| | | | Adventist Health System, Ser. A, | | | | |

| | 500 | | | 5.00%, 3/1/33 | | | 506,225 | |

| | 4,000 | | | 5.75%, 9/1/39 | | | 4,495,880 | |

| | | | Catholic Healthcare West, Ser. A, | | | | |

| | 1,935 | | | 6.00%, 7/1/34 | | | 2,080,493 | |

| | 4,000 | | | 6.00%, 7/1/39 | | | 4,684,960 | |

| | 450 | | | Children’s Hospital of Los Angeles, 5.25%, 7/1/38 (AGM) | | | 476,964 | |

| | 500 | | | Children’s Hospital of Orange Cnty., 6.50%, 11/1/38, Ser. A | | | 610,480 | |

| | 6,000 | | | Cottage Health System, 5.00%, 11/1/33, Ser. B (NPFGC) | | | 6,065,040 | |

| | 1,300 | | | Scripps Health, 5.00%, 11/15/36, Ser. A | | | 1,434,771 | |

| | 2,900 | | | Stanford Hospital, 5.25%, 11/15/40, Ser. A-2 | | | 3,322,327 | |

| | | | Sutter Health, | | | | |

| | 1,000 | | | 5.00%, 8/15/35, Ser. D | | | 1,122,370 | |

| | 5,000 | | | 5.00%, 8/15/38, Ser. A | | | 5,361,550 | |

| | 500 | | | 5.00%, 11/15/42, Ser. A (IBC-NPFGC) | | | 525,760 | |

| | 1,200 | | | 6.00%, 8/15/42, Ser. B | | | 1,431,072 | |

| | 500 | | | Lancaster Redev. Agcy., Tax Allocation, 6.875%, 8/1/39 | | | 564,405 | |

| | | | |

| 16 | | PIMCO Municipal Income Funds III Annual Report | | 9.30.12 |

PIMCO California Municipal Income Fund III Schedule of Investments

September 30, 2012 (continued)

| | | | | | | | |

Principal

Amount

(000s) | | | | | Value | |

| $ | 150 | | | Lancaster Redev. Agcy. Rev., Capital Improvements Projects, | | | | |

| | | | 5.90%, 12/1/35 | | $ | 162,921 | |

| | 5,020 | | | Long Beach Airport Rev., 5.00%, 6/1/40, Ser. A | | | 5,437,714 | |

| | 5,600 | | | Long Beach Bond Finance Auth. Rev., | | | | |

| | | | Long Beach Natural Gas, 5.50%, 11/15/37, Ser. A | | | 6,382,096 | |

| | 5,000 | | | Long Beach Unified School Dist., GO, 5.75%, 8/1/33, Ser. A | | | 5,900,450 | |

| | | | Los Angeles Department of Water & Power Rev., | | | | |

| | 6,000 | | | 4.75%, 7/1/30, Ser. A-2 (AGM) (h) | | | 6,386,940 | |

| | 10,000 | | | 5.00%, 7/1/39, Ser. A (h) | | | 11,088,700 | |

| | 1,500 | | | 5.00%, 7/1/43, Ser. B | | | 1,736,685 | |

| | | | Los Angeles Unified School Dist., GO, | | | | |

| | 9,580 | | | 4.75%, 1/1/28, Ser. A (NPFGC) (Pre-refunded @ $100, 7/1/13) (c) | | | 9,903,325 | |

| | 10,000 | | | 5.00%, 1/1/34, Ser. I (h) | | | 11,330,000 | |

| | 550 | | | Malibu, City Hall Project, CP, 5.00%, 7/1/39, Ser. A | | | 597,085 | |

| | 1,000 | | | Manteca Financing Auth. Sewer Rev., 5.75%, 12/1/36 | | | 1,131,910 | |

| | 5,000 | | | Metropolitan Water Dist. of Southern California Rev., | | | | |

| | | | 5.00%, 7/1/37, Ser. A (h) | | | 5,697,450 | |

| | 2,980 | | | Modesto Irrigation Dist., Capital Improvement Projects, CP, | | | | |

| | | | 5.00%, 7/1/33, Ser. A (NPFGC) | | | 3,004,734 | |

| | 3,000 | | | Montebello Unified School Dist., GO, 5.00%, 8/1/33 (AGM) | | | 3,291,570 | |

| | 1,700 | | | M-S-R Energy Auth. Rev., 6.50%, 11/1/39, Ser. B | | | 2,216,205 | |

| | 955 | | | Municipal Finance Auth. Rev., Azusa Pacific Univ. Project, | | | | |

| | | | 7.75%, 4/1/31, Ser. B | | | 1,129,154 | |

| | 5,000 | | | Oakland, GO, 5.00%, 1/15/33, Ser. A (NPFGC) (Pre-refunded @ $100, 1/15/13) (c) | | | 5,068,100 | |

| | 3,900 | | | Orange Unified School Dist., CP, 4.75%, 6/1/29 (NPFGC) | | | 3,900,000 | |

| | 1,250 | | | Peralta Community College Dist., GO, 5.00%, 8/1/39, Ser. C | | | 1,362,937 | |

| | 1,250 | | | Pollution Control Financing Auth. Rev., | | | | |

| | | | American Water Capital Corp. Project, 5.25%, 8/1/40 (a)(d) | | | 1,300,075 | |

| | 1,950 | | | Poway Unified School Dist., Special Tax, 5.125%, 9/1/28 | | | 1,983,891 | |

| | 5,000 | | | Riverside, CP, 5.00%, 9/1/33 (AMBAC) (Pre-refunded @ $100, 9/1/13) (c) | | | 5,217,900 | |

| | 500 | | | Rocklin Unified School Dist. Community Facs. Dist., Special Tax, | | | | |

| | | | 5.00%, 9/1/29 (NPFGC) | | | 506,205 | |

| | 3,250 | | | Sacramento Municipal Utility Dist. Rev., | | | | |

| | | | 5.00%, 8/15/33, Ser. R (NPFGC) (Pre-refunded @ $100, 8/15/13) (c) | | | 3,377,191 | |

| | 6,250 | | | San Diego Cnty. Water Auth., CP, 5.00%, 5/1/38, Ser. 2008-A (AGM) | | | 6,773,875 | |

| | 12,075 | | | San Diego Community College Dist., GO, | | | | |

| | | | 5.00%, 5/1/28, Ser. A (AGM) (Pre-refunded @ $100, 5/1/13) (c) | | | 12,410,202 | |

| | 4,000 | | | San Diego Public Facs. Financing Auth. Sewer Rev., | | | | |

| | | | 5.25%, 5/15/39, Ser. A | | | 4,541,480 | |

| | 2,200 | | | San Diego Regional Building Auth. Rev., | | | | |

| | | | Cnty. Operations Center & Annex, 5.375%, 2/1/36, Ser. A | | | 2,473,372 | |

| | | | | | |

| 9.30.12 | | PIMCO Municipal Income Funds III Annual Report | | | 17 | |

PIMCO California Municipal Income Fund III Schedule of Investments

September 30, 2012 (continued)

| | | | | | | | |

Principal

Amount

(000s) | | | | | Value | |

| $ | 1,000 | | | San Francisco Public Utilities Commission Water Rev., 5.00%, 11/1/43 | | $ | 1,147,450 | |

| | 1,500 | | | San Jose Hotel Tax Rev., Convention Center Expansion, 6.50%, 5/1/36 | | | 1,791,615 | |

| | 12,200 | | | San Marcos Public Facs. Auth., Tax Allocation, | | | | |

| | | | 5.00%, 8/1/33, Ser. A (FGIC-NPFGC) | | | 12,371,410 | |

| | 1,000 | | | San Marcos Unified School Dist., GO, 5.00%, 8/1/38, Ser. A | | | 1,125,150 | |

| | 500 | | | Santa Clara Cnty. Financing Auth. Rev., | | | | |

| | | | El Camino Hospital, 5.75%, 2/1/41, Ser. A (AMBAC) | | | 547,685 | |

| | 1,200 | | | Santa Cruz Cnty. Redev. Agcy., Tax Allocation, Live Oak/Soquel Community, | | | | |

| | | | 7.00%, 9/1/36, Ser. A | | | 1,421,016 | |

| | 4,425 | | | South Tahoe JT Powers Financing Auth. Rev., | | | | |

| | | | South Tahoe Redev. Project, 5.45%, 10/1/33, Ser. 1-A | | | 4,425,398 | |

| | 7,300 | | | State, GO, 6.00%, 4/1/38 | | | 8,707,002 | |

| | | | State Public Works Board Rev., | | | | |

| | 2,000 | | | California State Univ., 6.00%, 11/1/34, Ser. J | | | 2,370,200 | |

| | 2,050 | | | Univ. CA M.I.N.D. Inst., 5.00%, 4/1/28, Ser. A | | | 2,086,756 | |

| | | | Statewide Communities Dev. Auth. Rev., | | | | |

| | 500 | | | American Baptist Homes West, 6.25%, 10/1/39 | | | 545,435 | |

| | | | California Baptist Univ., | | | | |

| | 1,300 | | | 5.50%, 11/1/38, Ser. A | | | 1,347,697 | |

| | 500 | | | 6.50%, 11/1/21 | | | 610,985 | |

| | | | Catholic Healthcare West, | | | | |

| | 1,015 | | | 5.50%, 7/1/31, Ser. D | | | 1,135,917 | |

| | 1,015 | | | 5.50%, 7/1/31, Ser. E | | | 1,135,917 | |

| | 4,500 | | | Kaiser Permanente, 5.00%, 3/1/41, Ser. B | | | 4,768,650 | |

| | 1,000 | | | Lancer Student Housing Project, 7.50%, 6/1/42 | | | 1,147,990 | |

| | 7,300 | | | Los Angeles Jewish Home, 5.50%, 11/15/33 (CA Mtg. Ins.) | | | 7,421,253 | |

| | 15,000 | | | Memorial Health Services, 5.50%, 10/1/33, Ser. A (Pre-refunded @ $100, 4/1/13) (c) | | | 15,394,200 | |

| | | | Methodist Hospital Project (FHA), | | | | |

| | 2,000 | | | 6.625%, 8/1/29 | | | 2,536,360 | |

| | 7,200 | | | 6.75%, 2/1/38 | | | 8,885,448 | |

| | 3,100 | | | St. Joseph Health System, 5.75%, 7/1/47, Ser. A (FGIC) | | | 3,451,416 | |

| | 1,800 | | | Sutter Health, 6.00%, 8/15/42, Ser. A | | | 2,146,608 | |

| | 11,000 | | | Trinity Health, 5.00%, 12/1/41 | | | 12,310,650 | |

| | 2,000 | | | Univ. of California Irvine E. Campus, 5.375%, 5/15/38 | | | 2,168,340 | |

| | 3,505 | | | Statewide Communities Dev. Auth., The Internext Group, CP, 5.375%, 4/1/30 | | | 3,513,727 | |

| | | | Tobacco Securitization Agcy. Rev., | | | | |

| | | | Alameda Cnty., | | | | |

| | 8,100 | | | 5.875%, 6/1/35 | | | 8,099,757 | |

| | 7,000 | | | 6.00%, 6/1/42 | | | 6,999,370 | |

| | 2,000 | | | Kern Cnty., 6.125%, 6/1/43, Ser. A | | | 1,999,900 | |

| | | | |

| 18 | | PIMCO Municipal Income Funds III Annual Report | | 9.30.12 |

PIMCO California Municipal Income Fund III Schedule of Investments

September 30, 2012 (continued)

| | | | | | | | |

Principal

Amount

(000s) | | | | | Value | |

| $ | 5,000 | | | Tobacco Securitization Auth. of Southern California Rev., | | | | |

| | | | 5.00%, 6/1/37, Ser. A-1 | | $ | 4,084,000 | |

| | 2,950 | | | Torrance Rev., Torrance Memorial Medical Center, | | | | |

| | | | 5.50%, 6/1/31, Ser. A | | | 2,956,165 | |

| | 5,000 | | | Univ. of California Rev., 5.00%, 5/15/42, Ser. G | | | 5,748,700 | |

| | | | West Basin Municipal Water Dist., CP, | | | | |

| | 650 | | | 5.00%, 8/1/30, Ser. A (NPFGC) | | | 675,734 | |

| | 350 | | | 5.00%, 8/1/30, Ser. A (NPFGC) (Pre-refunded @ $100, 8/1/13) (c) | | | 354,834 | |

| | 2,000 | | | Western Municipal Water Dist. Facs. Auth. Rev., | | | | |

| | | | 5.00%, 10/1/39, Ser. B | | | 2,224,020 | |

| | 1,000 | | | Westlake Village, CP, 5.00%, 6/1/39 | | | 1,056,010 | |

| | 2,500 | | | William S. Hart Union High School Dist., Special Tax, | | | | |

| | | | 6.00%, 9/1/33, Ser. 2002-1 | | | 2,521,200 | |

| | 2,750 | | | Woodland Finance Auth. Rev., 5.00%, 3/1/32 (XLCA) | | | 2,818,585 | |

| | | | | | | | |

| | | | Total California Municipal Bonds & Notes (cost-$321,654,115) | | | 360,062,547 | |

| | | | | | | | |

| | | | | | | | |

| OTHER MUNICIPAL BONDS & NOTES – 4.2% | | | | |

| | | | Indiana – 1.3% | | | | |

| | 5,000 | | | Vigo Cnty. Hospital Auth. Rev., Union Hospital, Inc., 5.75%, 9/1/42 (a)(d) | | | 5,106,750 | |

| | | | | | | | |

| | | | New Jersey – 0.2% | | | | |

| | 1,000 | | | Tobacco Settlement Financing Corp. Rev., 4.75%, 6/1/34, Ser. 1-A | | | 824,230 | |

| | | | | | | | |

| | | | New York – 1.0% | | | | |

| | 3,300 | | | New York City Municipal Water Finance Auth. Water & Sewer Rev., | | | | |

| | | | 5.00%, 6/15/37, Ser. D (h) | | | 3,609,936 | |

| | | | | | | | |

| | | | Ohio – 0.6% | | | | |

| | 2,000 | | | American Municipal Power-Ohio, | | | | |

| | | | Inc. Rev., Fremont Energy Center Project, 5.00%, 2/15/42, Ser. B | | | 2,215,840 | |

| | | | | | | | |

| | | | Puerto Rico – 1.1% | | | | |

| | | | Sales Tax Financing Corp. Rev., | | | | |

| | 1,535 | | | 5.00%, 8/1/46, Ser. C | | | 1,650,509 | |

| | 2,200 | | | 5.25%, 8/1/43, Ser. A-1 | | | 2,335,432 | |

| | | | | | | | |

| | | | | | | 3,985,941 | |

| | | | | | | | |

| | | | Total Other Municipal Bonds & Notes (cost-$12,589,603) | | | 15,742,697 | |

| | | | | | | | |

| | | | | | | | |

| CALIFORNIA VARIABLE RATE NOTES (a)(d)(f)(g) – 0.3% | | | | |

| | 1,000 | | | Los Angeles Community College Dist., GO,

13.80%, 8/1/33, Ser. 3096 (cost-$996,673) | | | 1,378,250 | |

| | | | | | | | |

| | | | Total Investments (cost-$335,240,391) – 100.0% | | $ | 377,183,494 | |

| | | | | | | | |

| | | | | | |

| 9.30.12 | | PIMCO Municipal Income Funds III Annual Report | | | 19 | |

PIMCO California Municipal Income Fund III Schedule of Investments

September 30, 2012 (continued)

| | | | | | |

| Industry classification of portfolio holdings as a percentage of total investments at September 30, 2012 was as follows: | |

| Revenue Bonds: | | | | | | |

Health, Hospital, Nursing Home Revenue | | 26.4% | | | | |

Tobacco Settlement Funded | | 13.0 | | | | |

College & University Revenue | | 9.1 | | | | |

Electric Power & Lighting Revenue | | 6.1 | | | | |

Water Revenue | | 4.2 | | | | |

Natural Gas Revenue | | 2.9 | | | | |

Lease (Abatement) | | 2.1 | | | | |

Sewer Revenue | | 1.5 | | | | |

Port, Airport & Marina Revenue | | 1.4 | | | | |

Tax Increment/ Allocation Revenue | | 1.2 | | | | |

Sales Tax Revenue | | 1.1 | | | | |

Local or Government Housing | | 0.7 | | | | |

Hotel Occupancy Tax | | 0.5 | | | | |

Highway Revenue Tolls | | 0.4 | | | | |

| | | | | | |

| Total Revenue Bonds | | | | | 70.6 | % |

| General Obligation Bonds | | | | | 16.1 | |

| Certificates of Participation | | | | | 7.3 | |

| Tax Allocation | | | | | 4.7 | |

| Special Tax | | | | | 1.3 | |

| | | | | | |

| Total Investments | | | | | 100.0 | % |

| | | | | | |

| | | | |

| 20 | | PIMCO Municipal Income Funds III Annual Report | | 9.30.12 |

PIMCO New York Municipal Income Fund III Schedule of Investments

September 30, 2012

| | | | | | | | |

Principal

Amount

(000s) | | | | | Value | |

| NEW YORK MUNICIPAL BONDS & NOTES – 91.2% | | | | |

| $ | 1,000 | | | Brooklyn Arena Local Dev. Corp. Rev., | | | | |

| | | | Barclays Center Project, 6.375%, 7/15/43 | | $ | 1,160,350 | |

| | 1,500 | | | Chautauqua Cnty. Industrial Dev. Agcy. Rev., | | | | |

| | | | Dunkirk Power Project, 5.875%, 4/1/42 | | | 1,689,195 | |

| | 730 | | | Dutchess Cnty. Industrial Dev. Agcy. Rev., | | | | |

| | | | Elant Fishkill, Inc., 5.25%, 1/1/37, Ser. A | | | 632,866 | |

| | 800 | | | East Rochester Housing Auth. Rev., | | | | |

| | | | St. Mary’s Residence Project, 5.375%, 12/20/22, Ser. A (GNMA) | | | 832,472 | |

| | 4,000 | | | Hudson Yards Infrastructure Corp. Rev., 5.75%, 2/15/47, Ser. A | | | 4,727,240 | |

| | | | Liberty Dev. Corp. Rev., | | | | |

| | 1,050 | | | Bank of America Tower at One Bryant Park Project, 6.375%, 7/15/49 | | | 1,213,317 | |

| | | | Goldman Sachs Headquarters, | | | | |

| | 1,810 | | | 5.25%, 10/1/35 | | | 2,139,022 | |

| | 2,400 | | | 5.50%, 10/1/37 | | | 2,884,200 | |

| | 1,500 | | | Long Island Power Auth. Rev., 5.75%, 4/1/39, Ser. A | | | 1,778,715 | |

| | | | Metropolitan Transportation Auth. Rev., | | | | |

| | 5,220 | | | 5.00%, 11/15/32, Ser. A (FGIC-NPFGC) | | | 5,384,900 | |

| | 500 | | | 5.00%, 11/15/34, Ser. B | | | 564,665 | |

| | 3,000 | | | Monroe Cnty. Industrial Dev. Corp. Rev.,

Unity Hospital Rochester Project, 5.50%, 8/15/40 (FHA) (h) | | | 3,488,490 | |

| | 500 | | | Nassau Cnty. Industrial Dev. Agcy. Rev.,

Amsterdam at Harborside, 6.70%, 1/1/43, Ser. A | | | 343,590 | |

| | 2,695 | | | New York City, GO, | | | | |

| | | | 5.00%, 3/1/33, Ser. I (Pre-refunded @ $100, 3/1/13) (c) | | | 2,747,687 | |

| | | | New York City Industrial Dev. Agcy. Rev., (AGC), | | | | |

| | 600 | | | Pilot Queens Baseball Stadium, 6.50%, 1/1/46 | | | 701,976 | |

| | 2,200 | | | Yankee Stadium, 7.00%, 3/1/49 | | | 2,662,572 | |

| | | | New York City Municipal Water Finance Auth. Water & Sewer Rev., | | | | |

| | | | Second Generation Resolutions, | | | | |

| | 5,000 | | | 4.75%, 6/15/35, Ser. DD (h) | | | 5,530,850 | |

| | 1,500 | | | 5.00%, 6/15/39, Ser. GG-1 | | | 1,708,125 | |

| | 2,000 | | | New York City Transitional Finance Auth. Rev., | | | | |

| | | | 5.00%, 5/1/39, Ser. F-1 | | | 2,300,240 | |

| | 3,450 | | | New York City Trust for Cultural Res. Rev., | | | | |

| | | | Wildlife Conservation Society, 5.00%, 2/1/34 (FGIC-NPFGC) | | | 3,548,566 | |

| | 4,000 | | | New York Liberty Dev. Corp. Rev., | | | | |

| | | | 4 World Trade Center Project, 5.75%, 11/15/51 | | | 4,717,680 | |

| | 1,000 | | | Niagara Falls Public Water Auth. Water & Sewer Rev., | | | | |

| | | | 5.00%, 7/15/34, Ser. A (NPFGC) | | | 1,009,970 | |

| | 400 | | | Onondaga Cnty. Rev., Syracuse Univ. Project, 5.00%, 12/1/36 | | | 459,160 | |

| | | | | | |

| 9.30.12 | | PIMCO Municipal Income Funds III Annual Report | | | 21 | |

PIMCO New York Municipal Income Fund III Schedule of Investments

September 30, 2012 (continued)

| | | | | | | | |

Principal

Amount

(000s) | | | | | Value | |

| $ | 600 | | | Port Auth. of New York & New Jersey Rev., | | | | |

| | | | JFK International Air Terminal, 6.00%, 12/1/36 | | $ | 702,864 | |

| | | | State Dormitory Auth. Rev., | | | | |

| | 1,000 | | | 5.00%, 3/15/38, Ser. A | | | 1,144,850 | |

| | 2,250 | | | Jewish Board Family & Children, 5.00%, 7/1/33 (AMBAC) | | | 2,264,715 | |

| | 3,000 | | | Lutheran Medical Hospital, 5.00%, 8/1/31 (FHA-NPFGC) | | | | |

| | | | (Pre-refunded @ $100, 2/1/13) (c) | | | 3,046,740 | |

| | 250 | | | NYU Hospitals Center, 6.00%, 7/1/40, Ser. A | | | 292,803 | |

| | 3,740 | | | St. Barnabas Hospital, 5.00%, 2/1/31, Ser. A (AMBAC-FHA) | | | 3,750,472 | |

| | 1,200 | | | Teachers College, 5.50%, 3/1/39 | | | 1,328,004 | |

| | 500 | | | The New School, 5.50%, 7/1/40 | | | 573,505 | |

| | 2,500 | | | Univ. Dormitory Facs., 5.00%, 7/1/42, Ser. A | | | 2,862,775 | |

| | 620 | | | Winthrop Univ. Hospital Assoc., 5.50%, 7/1/32, Ser. A | | | 627,855 | |

| | 2,500 | | | Winthrop-Nassau Univ., 5.75%, 7/1/28 | | | 2,540,275 | |

| | 750 | | | State Environmental Facs. Corp. Rev., 4.75%, 6/15/32, Ser. B | | | 820,185 | |

| | 1,600 | | | State Thruway Auth. Rev., 5.00%, 1/1/42, Ser. I | | | 1,801,536 | |

| | | | State Urban Dev. Corp. Rev., | | | | |

| | 2,400 | | | 5.00%, 3/15/35, Ser. B | | | 2,587,440 | |

| | 2,200 | | | 5.00%, 3/15/36, Ser. B-1 (h) | | | 2,537,040 | |

| | 2,000 | | | Triborough Bridge & Tunnel Auth. Rev., 5.25%, 11/15/34, Ser. A-2 (h) | | | 2,382,580 | |

| | 1,400 | | | Troy Capital Res. Corp. Rev., Rensselaer Polytechnic Institute | | | | |

| | | | Project, 5.125%, 9/1/40, Ser. A | | | 1,547,826 | |

| | 2,000 | | | Warren & Washington Cntys. Industrial Dev. Agcy. Rev., | | | | |

| | | | Glens Falls Hospital Project, 5.00%, 12/1/35, Ser. A (AGM) | | | 2,042,920 | |

| | 600 | | | Westchester Cnty. Healthcare Corp. Rev., 6.125%, 11/1/37, Ser. C-2 | | | 704,436 | |

| | 100 | | | Yonkers Economic Dev. Corp. Rev., | | | | |

| | | | Charter School of Educational Excellence Project, 6.00%, 10/15/30, Ser. A | | | 105,063 | |

| | | | | | | | |

| | | | Total New York Municipal Bonds & Notes (cost-$77,584,875) | | | 85,889,732 | |

| | | | | | | | |

| | | | | | | | |

| OTHER MUNICIPAL BONDS & NOTES – 8.8% | | | | |

| | | | District of Columbia – 0.2% | | | | |

| | 175 | | | Tobacco Settlement Financing Corp. Rev., 6.50%, 5/15/33 | | | 200,653 | |

| | | | | | | | |

| | | | Ohio – 1.1% | | | | |

| | 1,250 | | | Buckeye Tobacco Settlement Financing Auth. Rev., | | | | |

| | | | 5.875%, 6/1/47, Ser. A-2 | | | 1,009,113 | |

| | | | | | | | |

| | | | Puerto Rico – 6.8% | | | | |

| | 580 | | | Children’s Trust Fund Rev., 5.625%, 5/15/43 | | | 580,058 | |

| | | | Sales Tax Financing Corp. Rev., | | | | |

| | 4,000 | | | 5.00%, 8/1/40, Ser. A (AGM) (h) | | | 4,220,480 | |

| | 500 | | | 5.25%, 8/1/43, Ser. A-1 | | | 530,780 | |

| | 1,000 | | | 5.375%, 8/1/38, Ser. C | | | 1,070,750 | |

| | | | | | | | |

| | | | | | | 6,402,068 | |

| | | | | | | | |

| | | | |

| 22 | | PIMCO Municipal Income Funds III Annual Report | | 9.30.12 |

PIMCO New York Municipal Income Fund III Schedule of Investments

September 30, 2012 (continued)

| | | | | | | | |

Principal

Amount

(000s) | | | | | Value | |

| | | | U.S. Virgin Islands – 0.6% | | | | |

| $ | 500 | | | Public Finance Auth. Rev., 6.00%, 10/1/39, Ser. A | | $ | 559,840 | |

| | | | | | | | |

| | | | Washington – 0.1% | | | | |

| | 135 | | | Tobacco Settlement Auth. Rev., 6.625%, 6/1/32 | | | 140,292 | |

| | | | | | | | |

| | | | Total Other Municipal Bonds & Notes (cost-$7,613,595) | | | 8,311,966 | |

| | | | | | | | |

| | | | | | | | |

| | | | Total Investments (cost-$85,198,470) – 100.0% | | $ | 94,201,698 | |

| | | | | | | | |

| | | | | | |

| Industry classification of portfolio holdings as a percentage of total investments at September 30, 2012 was as follows: | |

| Revenue Bonds: | | | | | | |

Health, Hospital, Nursing Home Revenue | | 21.8% | | | | |

Industrial Revenue | | 11.2 | | | | |

Water Revenue | | 9.6 | | | | |

Income Tax Revenue | | 9.1 | | | | |

Recreational Revenue | | 7.8 | | | | |

College & University Revenue | | 7.2 | | | | |

Transit Revenue | | 6.3 | | | | |

Sales Tax Revenue | | 6.2 | | | | |

Miscellaneous Revenue | | 5.6 | | | | |

Miscellaneous Taxes | | 5.0 | | | | |

Highway Revenue Tolls | | 2.5 | | | | |

Tobacco Settlement Funded | | 2.1 | | | | |

Electric Power & Lighting Revenue | | 1.9 | | | | |

Port, Airport & Marina Revenue | | 0.8 | | | | |

| | | | | | |

| Total Revenue Bonds | | | | | 97.1 | % |

| General Obligation Bonds | | | | | 2.9 | |

| | | | | | |

| Total Investments | | | | | 100.0 | % |

| | | | | | |

| | | | | | |

| 9.30.12 | | PIMCO Municipal Income Funds III Annual Report | | | 23 | |

PIMCO New York Municipal Income Funds Notes to Schedules of Investments

September 30, 2012 (continued)

| (a) | | Private Placement – Restricted as to resale and may not have a readily available market. Securities with an aggregate value of $19,603,016 and $7,785,075, representing 3.4% and 2.1% of total investments in Municipal III and California Municipal III, respectively. | |

| (c) | | Pre-refunded bonds are collateralized by U.S. Government or other eligible securities which are held in escrow and used to pay principal and interest and retire the bonds at the earliest refunding date (payment date) and/or whose interest rates vary with changes in a designated base rate (such as the prime interest rate). | |

| (d) | | 144A – Exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, typically only to qualified institutional buyers. Unless otherwise indicated, these securities are not considered to be illiquid. | |

| (f) | | Inverse Floater – The interest rate shown bears an inverse relationship to the interest rate on another security or the value of an index. The interest rate disclosed reflects the rate in effect on September 30, 2012. | |

| (g) | | Variable Rate Notes – Instruments whose interest rates change on specified date (such as a coupon date or interest payment date) and/or whose interest rates vary with changes in a designated base rate (such as the prime interest rate). The interest rate disclosed reflects the rate in effect on September 30, 2012. | |

| (h) | | Residual Interest Bonds held in Trust – Securities represent underlying bonds transferred to a separate securitization trust established in a tender option bond transaction in which each Fund acquired the residual interest certificates. These securities serve as collateral in a financing transaction. | |

Glossary:

| | | | | | |

| AGC | | | - | | | insured by Assured Guaranty Corp. |

| AGM | | | - | | | insured by Assured Guaranty Municipal Corp. |

| AMBAC | | | - | | | insured by American Municipal Bond Assurance Corp. |

| CA Mtg. Ins. | | | - | | | insured by California Mortgage Insurance |

| CP | | | - | | | Certificates of Participation |

| FGIC | | | - | | | insured by Financial Guaranty Insurance Co. |

| FHA | | | - | | | insured by Federal Housing Administration |

| GNMA | | | - | | | insured by Government National Mortgage Association |

| GO | | | - | | | General Obligation Bond |

| IBC | | | - | | | Insurance Bond Certificate |

| NPFGC | | | - | | | insured by National Public Finance Guarantee Corp. |

| TCRS | | | - | | | Temporary Custodian Receipts |

| XLCA | | | - | | | insured by XL Capital Assurance |

| | | | | | |

| 24 | | PIMCO Municipal Income Funds III Annual Report | | 9.30.12 | | See accompanying Notes to Financial Statements |

PIMCO Municipal Income Funds III Statements of Assets and Liabilities

September 30, 2012

| | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | | | Municipal III | | | | | California

Municipal III | | | | | New York

Municipal III | |

| | | | | | |

Assets: | | | | | | | | | | | | | | | | | | |

Investments, at value (cost-$510,616,164, $335,240,391

and $85,198,470, respectively) | | | | | $568,293,090 | | | | | | $377,183,494 | | | | | | $94,201,698 | |

Cash | | | | | 3,813,897 | | | | | | 2,281,267 | | | | | | 425,181 | |

Interest receivable | | | | | 9,034,307 | | | | | | 5,606,274 | | | | | | 1,078,109 | |

Prepaid expenses and other assets | | | | | 36,679 | | | | | | 26,117 | | | | | | 14,627 | |

Total Assets | | | | | 581,177,973 | | | | | | 385,097,152 | | | | | | 95,719,615 | |

| | | | | | |

| Liabilities: | | | | | | | | | | | | | | | | | | |

Payable for Floating Rate Notes issued | | | | | 32,121,219 | | | | | | 33,623,688 | | | | | | 8,932,500 | |

Dividends payable to common and preferred shareholders | | | | | 2,275,232 | | | | | | 1,320,810 | | | | | | 297,064 | |

Investment management fees payable | | | | | 289,615 | | | | | | 185,366 | | | | | | 45,748 | |

Interest payable | | | | | 76,701 | | | | | | 77,969 | | | | | | 14,320 | |

Accrued expenses and other liabilities | | | | | 276,266 | | | | | | 293,229 | | | | | | 102,880 | |

Total Liabilities | | | | | 35,039,033 | | | | | | 35,501,062 | | | | | | 9,392,512 | |

Preferred Shares ($0.00001 par value and $25,000 liquidation preference per share applicable to an aggregate of 7,560, 5,000 and 1,280 shares issued and outstanding, respectively) | | | | | 189,000,000 | | | | | | 125,000,000 | | | | | | 32,000,000 | |

Net Assets Applicable to Common Shareholders | | | | | $357,138,940 | | | | | | $224,596,090 | | | | | | $54,327,103 | |

| | | | | | |

| Composition of Net Assets Applicable to Common Shareholders: | | | | | | | | | | | | | | | | | | |

Common Shares: | | | | | | | | | | | | | | | | | | |

Par value ($0.00001 per share) | | | | | $324 | | | | | | $220 | | | | | | $56 | |

Paid-in-capital in excess of par | | | | | 457,380,551 | | | | | | 308,901,832 | | | | | | 79,174,051 | |

Undistributed net investment income | | | | | 3,817,545 | | | | | | 5,860,568 | | | | | | 1,935,488 | |

Accumulated net realized loss | | | | | (161,738,310) | | | | | | (132,091,831) | | | | | | (35,784,307) | |

Net unrealized appreciation of investments | | | | | 57,678,830 | | | | | | 41,925,301 | | | | | | 9,001,815 | |

Net Assets Applicable to Common Shareholders | | | | | $357,138,940 | | | | | | $224,596,090 | | | | | | $54,327,103 | |

Common Shares Issued and Outstanding | | | | | 32,402,125 | | | | | | 21,951,128 | | | | | | 5,630,985 | |

Net Asset Value Per Common Share | | | | | $11.02 | | | | | | $10.23 | | | | | | $9.65 | |

| | | | | | | | |

| See accompanying Notes to Financial Statements | | 9.30.12 | | PIMCO Municipal Income Funds III Annual Report | | | 25 | |

PIMCO Municipal Income Funds III Statements of Operations

Year ended September 30, 2012

| | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | | | Municipal III | | | | | California

Municipal III | | | | | New York

Municipal III | |

| | | | | | |

Investment Income: | | | | | | | | | | | | | | | | | | |

Interest | | | | | $31,121,148 | | | | | | $20,695,207 | | | | | | $5,197,424 | |

| | | | | | |

| Expenses: | | | | | | | | | | | | | | | | | | |

Investment management fees | | | | | 3,409,237 | | | | | | 2,193,233 | | | | | | 543,907 | |

Interest expense | | | | | 356,541 | | | | | | 304,314 | | | | | | 70,753 | |

Auction agent fees and commissions | | | | | 307,800 | | | | | | 191,699 | | | | | | 53,016 | |

Custodian and accounting agent fees | | | | | 103,854 | | | | | | 78,931 | | | | | | 48,850 | |

Audit and tax services | | | | | 80,336 | | | | | | 63,866 | | | | | | 45,103 | |

Shareholder communications | | | | | 55,770 | | | | | | 30,112 | | | | | | 19,207 | |

Trustees’ fees and expenses | | | | | 48,616 | | | | | | 29,585 | | | | | | 7,742 | |

Transfer agent fees | | | | | 42,497 | | | | | | 41,871 | | | | | | 40,930 | |

New York Stock Exchange listing fees | | | | | 25,722 | | | | | | 21,309 | | | | | | 21,071 | |

Legal fees | | | | | 12,208 | | | | | | 6,652 | | | | | | 12,212 | |

Insurance expense | | | | | 11,095 | | | | | | 7,438 | | | | | | 2,679 | |

Miscellaneous | | | | | 11,966 | | | | | | 11,982 | | | | | | 11,031 | |

Total Expenses | | | | | 4,465,642 | | | | | | 2,980,992 | | | | | | 876,501 | |

Less: investment management fees waived | | | | | (194,179) | | | | | | (125,057) | | | | | | (31,080) | |

custody credits earned on cash balances | | | | | (2,254) | | | | | | (4,178) | | | | | | (1,190) | |

Net Expenses | | | | | 4,269,209 | | | | | | 2,851,757 | | | | | | 844,231 | |

| | | | | | |

Net Investment Income | | | | | 26,851,939 | | | | | | 17,843,450 | | | | | | 4,353,193 | |

| | | | | | |

| Realized and Change In Unrealized Gain (Loss): | | | | | | | | | | | | | | | | | | |

Net realized gain (loss) on: | | | | | | | | | | | | | | | | | | |

Investments | | | | | (1,407,521) | | | | | | 861,734 | | | | | | 527,953 | |

Futures contracts | | | | | 273,273 | | | | | | (310,285) | | | | | | (107,072) | |

Swaps | | | | | (2,252,916) | | | | | | (3,997,978) | | | | | | (526,064) | |

Net change in unrealized appreciation/depreciation of: Investments | | | | | 43,496,985 | | | | | | 22,188,286 | | | | | | 3,409,069 | |

Swaps | | | | | 3,672,956 | | | | | | 4,663,255 | | | | | | 637,653 | |

Net realized and change in unrealized gain on investments, futures contracts and swaps | | | | | 43,782,777 | | | | | | 23,405,012 | | | | | | 3,941,539 | |

Net Increase in Net Assets Resulting from Investment Operations | | | | | 70,634,716 | | | | | | 41,248,462 | | | | | | 8,294,732 | |

Dividends on Preferred Shares from Net Investment Income | | | | | (459,781) | | | | | | (303,346) | | | | | | (78,584) | |

Net Increase in Net Assets Applicable to Common Shareholders Resulting from Investment Operations | | | | | $70,174,935 | | | | | | $40,945,116 | | | | | | $8,216,148 | |

| | | | | | |

| 26 | | PIMCO Municipal Income Funds III Annual Report | | 9.30.12 | | See accompanying Notes to Financial Statements |

[THIS PAGE INTENTIONALLY LEFT BLANK]

| | | | | | |

| 9.30.12 | | PIMCO Municipal Income Funds III Annual Report | | | 27 | |

PIMCO Municipal Income Funds III Statements of Changes in Net Assets

Applicable to Common Shareholders

| | | | | | | | | | | | |

| | |

| | | | | Municipal III | |

| | | | | Year ended

September 30, 2012 | | | | | Year ended

September 30, 2011 | |

Investment Operations: | | | | | | | | | | | | |

Net investment income | | | | | $26,851,939 | | | | | | $28,086,793 | |

Net realized loss on investments, futures contracts and swaps | | | | | (3,387,164) | | | | | | (4,849,640) | |

Net change in unrealized appreciation/depreciation of investments, futures contacts and swaps | | | | | 47,169,941 | | | | | | (14,805,435) | |

Net increase in net assets resulting from investment operations | | | | | 70,634,716 | | | | | | 8,431,718 | |

Dividends on Preferred Shares from Net Investment Income | | | | | (459,781) | | | | | | (651,323) | |

Net increase in net assets applicable to common shareholders

resulting from investment operations | | | | | 70,174,935 | | | | | | 7,780,395 | |

Dividends to Common Shareholders from Net Investment Income | | | | | (27,184,685) | | | | | | (27,072,603) | |

| | | | |

| Common Share Transactions: | | | | | | | | | | | | |

Reinvestment of dividends | | | | | 1,127,973 | | | | | | 1,473,126 | |

Total increase (decrease) in net assets applicable to common shareholders | | | | | 44,118,223 | | | | | | (17,819,082) | |

| | | | |

| Net Assets Applicable to Common Shareholders: | | | | | | | | | | | | |

Beginning of year | | | | | 313,020,717 | | | | | | 330,839,799 | |

End of year (including undistributed net investment income of $3,817,545 and $4,610,072; $5,860,568 and $4,108,834; $1,935,488 and $1,204,306; respectively) | | | | | $357,138,940 | | | | | | $313,020,717 | |

| | | | |

Common Shares Issued in Reinvestment of Dividends | | | | | 101,480 | | | | | | 146,402 | |

| | | | | | |

| 28 | | PIMCO Municipal Income Funds III Annual Report | | 9.30.12 | | See accompanying Notes to Financial Statements |

PIMCO Municipal Income Funds III Statements of Changes in Net Assets

Applicable to Common Shareholders (continued)

| | | | | | | | | | | | | | | | | | |

| | | |

| California Municipal III | | | | | New York Municipal III | |

Year ended

September 30, 2012 | | | | Year ended

September 30, 2011 | | | | | Year ended

September 30, 2012 | | | | | Year ended

September 30, 2011 | |

| | | | | | | | | | | | | | | | | | | |

| $17,843,450 | | | | | $16,886,814 | | | | | | $4,353,193 | | | | | | $3,847,375 | |

| (3,446,529) | | | | | (8,192,235) | | | | | | (105,183) | | | | | | (1,231,817) | |

26,851,541 | | | | | (4,941,083) | | | | | | 4,046,722 | | | | | | (2,130,334) | |

| 41,248,462 | | | | | 3,753,496 | | | | | | 8,294,732 | | | | | | 485,224 | |

| (303,346) | | | | | (428,181) | | | | | | (78,584) | | | | | | (110,402) | |

40,945,116 | | | | | 3,325,315 | | | | | | 8,216,148 | | | | | | 374,822 | |

| (15,785,355) | | | | | (15,719,522) | | | | | | (3,543,427) | | | | | | (3,527,553) | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| 687,943 | | | | | 825,372 | | | | | | 164,219 | | | | | | 243,118 | |

| 25,847,704 | | | | | (11,568,835) | | | | | | 4,836,940 | | | | | | (2,909,613) | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| 198,748,386 | | | | | 210,317,221 | | | | | | 49,490,163 | | | | | | 52,399,776 | |

$224,596,090 | | | | | $198,748,386 | | | | | | $54,327,103 | | | | | | $49,490,163 | |

| | | | | | | |

| 70,417 | | | | | 94,251 | | | | | | 17,760 | | | | | | 28,553 | |

| | | | | | | | |

| See accompanying Notes to Financial Statements | | 9.30.12 | | PIMCO Municipal Income Funds III Annual Report | | | 29 | |

PIMCO California Municipal Income Fund III Statement of Cash Flows

Year ended September 30, 2012

| | | | | | |

| | |

Decrease in Cash from: | | | | | | |

| | |

| Cash Flows provided by Operating Activities: | | | | | | |

Net increase in net assets resulting from investing operations | | | | | $41,248,462 | |

| | |

| Adjustments to Reconcile Net Increase in Net Assets Resulting from Investment Operations to Net Cash provided by Operating Activities: | | | | | | |

Purchases of long-term investments | | | | | (35,428,608) | |

Proceeds from sales of long-term investments | | | | | 36,742,385 | |

Sales of short-term portfolio investments, net | | | | | 5,571,780 | |

Net change in unrealized appreciation/depreciation of investments, futures contacts and swaps | | | | | (26,229,645) | |

Net realized loss on investments, futures contracts and swaps | | | | | 2,821,617 | |

Net amortization/accretion on investments | | | | | (1,592,752) | |

Decrease in interest receivable | | | | | 13,571 | |

Payments for futures contracts transactions | | | | | (310,285) | |

Increase in prepaid expenses and other assets | | | | | (4,002) | |

Net cash used for swap transactions | | | | | (4,179,560) | |

Increase in investment management fees payable | | | | | 26,604 | |

Decrease in accrued expenses and other liabilities | | | | | (19,306) | |

Net cash provided by operating activities | | | | | 18,660,261 | |

| | |

| Cash Flows used of Financing Activities: | | | | | | |

Cash dividends paid (excluding reinvestment of dividends of $687,943) | | | | | (15,394,462) | |

Cash retirement on issuance of Floating Rate Notes | | | | | (6,706,700) | |

Net cash used for financing activities | | | | | (22,101,162) | |

Net decrease in cash | | | | | (3,440,901) | |