Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2005

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number: 000-50855

Auxilium Pharmaceuticals, Inc.

(Exact name of registrant as specified in its charter)

| DELAWARE | 23-3016883 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

40 Valley Stream Parkway Malvern, PA | 19355 | |

| (Address of principal executive offices) | (Zip Code) | |

(484) 321-5900

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Securities Exchange Act of 1934:

None

Securities registered pursuant to Section 12(g) of the Securities Exchange Act of 1934:

Common Stock, Par Value $0.01 Per Share

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant, based on the last sale price for such stock on the NASDAQ National Market as of June 30, 2005, was approximately $58.2 million.

As of March 27, 2006, the number of shares outstanding of the issuer’s common stock, $0.01 par value per share, was 29,291,719.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive Proxy Statement for its Annual Meeting of Stockholders to be held on June 6, 2006, to be filed with the Securities and Exchange Commission, are incorporated by reference into Part III of this Form 10-K.

Table of Contents

AUXILIUM PHARMACEUTICALS, INC.

FORM 10-K

December 31, 2005

TABLE OF CONTENTS

| Page | ||||

| PART I | ||||

| Item 1. | 3 | |||

| Item 1A. | 28 | |||

| Item 1B. | 54 | |||

| Item 2. | 54 | |||

| Item 3. | 54 | |||

| Item 4. | 54 | |||

| PART II | ||||

| Item 5. | 55 | |||

| Item 6. | 56 | |||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 57 | ||

| Item 7A. | 73 | |||

| Item 8. | 74 | |||

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 112 | ||

| Item 9A. | 112 | |||

| Item 9B. | 115 | |||

| PART III | ||||

| Item 10. | 116 | |||

| Item 11. | 116 | |||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 116 | ||

| Item 13. | 116 | |||

| Item 14. | 116 | |||

| PART IV | ||||

| Item 15. | 117 | |||

| 118 | ||||

| 119 | ||||

Exhibit 31.1 | 123 | |||

Exhibit 31.2 | 124 | |||

Exhibit 32 | 125 | |||

2

Table of Contents

This Report on Form 10-K contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, that involve risks and uncertainties. All statements other than statements of historical information provided herein are forward-looking statements and may contain projections relating to financial results, economic conditions, trends and known uncertainties. These statements are not guarantees of future performance or events. Our actual results may differ materially from those discussed in the Report. You should review the “Risk Factors” section, of this Report for a discussion of the important factors that could cause actual results to differ materially from those described in or implied by the forward-looking statements contained in this Report. Readers are cautioned not to place undue reliance on these forward-looking statements, which reflect management’s analysis, judgment, belief or expectation only as of the date hereof. We undertake no obligation to publicly reissue these forward-looking statements to reflect events or circumstances that arise after the date hereof.

PART I

| ITEM 1. | Business |

Company Overview

Company Description

We are a specialty pharmaceutical company with a focus on developing and marketing products for urology, sexual health and other indications within specialty markets. We currently have a sales and marketing organization of approximately 120 people. Our only marketed product, Testim®, is a proprietary, topical 1% testosterone once-a-day gel indicated for the treatment of hypogonadism. Hypogonadism is defined as reduced or absent secretion of testosterone which can lead to symptoms such as loss of libido, adverse changes in body composition, irritability and poor concentration. We reported revenues in 2005 of $42.8 million, an increase of 58.5% over the $27.0 million reported in 2004. According to National Prescription Audit data from IMS Health, Inc. or IMS, a pharmaceutical market research firm, Testim’s share of total prescriptions for the gel segment of the testosterone replacement therapy, or TRT, market was 16.3% for the month of December 2005, compared with 11.5% for the month of December 2004. For the full year 2005, Testim’s share of total prescriptions for the TRT market was 13.8%, versus 10.0% for the full year 2004.

We target diseases with unmet medical needs that we believe can be addressed by more innovative, effective or easy to use products. Our current product pipeline includes:

| • | Five projects in clinical development; |

| • | Two pain product candidates in pre-clinical development; and |

| • | Rights to six additional pain product candidates, options to additional indications for our injectable enzyme and other products for urology and sexual health. |

Our lead project is AA4500, an injectable enzyme. We have an option to license all non-topical uses of AA4500, and we currently are pursuing three indications: Dupuytren’s Disease, Peyronie’s Disease and Adhesive Capsulitis, or Frozen Shoulder Syndrome. We believe that AA4500 has completed Phase II of development for the treatment of Dupuytren’s Disease and is in Phase II of development for the treatment of Peyronie’s Disease and Frozen Shoulder Syndrome. Each of these disease states is characterized by patients suffering the debilitating effects and deformities of scar tissue. AA4500 was identified for in-licensing because of its application for the treatment of Peyronie’s Disease, which is a plaque or hard scar on the shaft of the penis that causes substantial distortion of the penis upon erection. Men suffering from Peyronie’s Disease are often unable to engage in sexual intercourse due to the deformity of their erection.

In the process of pursuing AA4500 for the treatment of Peyronie’s Disease, we saw completed clinical work and an opportunity to pursue AA4500 for the treatment of Dupuytren’s Disease. Dupuytren’s Disease results

3

Table of Contents

when a patient has excess scar tissue that collects at the tendons in the hand. Typically it results in forming a “cord” affecting the ring and small finger, causing the finger to contract, leaving the patient unable to fully extend the affected finger(s).

AA4500 was identified as a potential treatment for Frozen Shoulder Syndrome by the licensor of AA4500. We exercised our option to expand our license for AA4500 to include its application for the treatment of Frozen Shoulder Syndrome based on the results of a Phase II clinical trial conducted by the licensor of AA4500 which suggests that local injection of AA4500 is well-tolerated and may be effective in patients suffering from Frozen Shoulder Syndrome. Frozen Shoulder Syndrome is a disease of diminished shoulder motion, characterized by restriction in both active and passive range of motion of the shoulder joint.

We have in-licensed a platform technology for the delivery of hormones and pharmaceutical products through the oral mucosal membrane. AA2600, is a TRT for the treatment of hypogonadism that utilizes this transmucosal film technology. We believe AA2600 has completed Phase II of development and expect to commence Phase III trials early in the second quarter of 2006.

We also have a project, which we refer to as AA4010, and referred to erroneously as AA2010 in a press release issued and during our earnings conference call on March 7, 2006, in Phase I of development for the treatment for overactive bladder using the same transmucosal film delivery system. Overactive bladder is a medical condition affecting both men and women characterized by urinary urgency and increased frequency of urination.

We have two pain products using our transmucosal film delivery system in pre-clinical development. We also have rights to six additional pain products and products for hormone replacement and urologic disease using our transmucosal film delivery system.

Company Strategy

Our goal is to build a leading specialty pharmaceutical company by focusing on disease states that can be addressed through sales to predominantly specialist audiences, such as urologists, endocrinologists, certain targeted primary care physicians and subsets of orthopedic surgeons. We have an experienced development and regulatory team that has a proven track record. We intend to draw upon our track record and experience to successfully develop our product candidates. Our strategy will focus on optimizing Testim’s commercial success, developing and commercializing AA4500 and products utilizing our transmucosal film technology platform.

Optimizing Testim’s Commercial Success. Testim has demonstrated an ability to capture market share in the gel segment of the TRT market. We believe that we can continue to increase sales of Testim by capturing market share from competitive products, expanding the use of TRT through increased physician and patient awareness and benefiting from the on-going demographic changes that could create additional patient candidates for treatment with this product.

| • | Increase Testim market penetration. Through on-going evaluation of physician targeting and greater sales efficiencies, we intend to improve the effectiveness of our sales force. We will continue to work with accredited education groups, thought leaders and professional organizations to further educate physicians about diagnosis and the benefits of TRT, including Testim. In April 2005, we entered into a co-promotion agreement with Oscient Pharmaceuticals Corporation, or Oscient, for the promotion and sale of Testim in the U.S. Oscient commenced promotion of Testim in June 2005 and now details Testim with approximately 300 sales representatives to primary care physicians. Prior to our agreement with Oscient, many of these primary care physicians were not accessible to our specialty sales force. We also have entered into two collaborations with partners for the international commercialization of Testim. Bayer, Inc., or Bayer, plans to market Testim in Canada, and Ipsen Farmaceutica, B.V., or Ipsen, has begun to market Testim in Europe. |

4

Table of Contents

| • | Expand market opportunities for Testim. There are some conditions where low testosterone levels may have an impact on the underlying disease. In the fourth quarter of 2004, we began a clinical study of hypogonadal men with Type II diabetes to evaluate the impact of testosterone normalization on blood glucose control. If the results show that Testim contributes to improvement of glycemic control of hypogonadal men with Type II diabetes, we believe that more physicians and patients will understand that maintaining normalized levels of testosterone has positive health consequences beyond sexual health issues |

| • | Capture the benefits of an aging population.According to the U.S. Census Bureau, there were 30.4 million men aged 45 to 64 and 13.2 million men aged 65 to 84 in 2000, and these figures are expected to increase to 39.5 million and 15.1 million, respectively, by 2010. According to a 2001 article published inThe Journal of Clinical Endocrinology & Metabolism, hypogonadism affects approximately 20% of all U.S. men age 50 and older. As a result, we expect to see an increase in the number of potential patients over the coming years. We expect the percentage of men with hypogonadism seeking and receiving treatment will also increase because we believe men from the baby boom generation are more health conscious and expect to have a higher quality of life in their older years than their predecessors. |

Developing and Commercializing AA4500.We believe that AA4500 represents a significant opportunity for us, and we are devoting what we believe to be the appropriate resources to the development and pre-commercialization of this product. For Dupuytren’s and Peyronie’s Diseases, we believe there is a large unmet medical need for a non-surgical solution to these debilitating diseases and that the data that we have seen to date in our well-controlled Phase II studies is encouraging. The product has received orphan drug designation in the U.S. for both indications, and our preliminary market research leads us to believe that urologists and orthopedic surgeons would be very likely to use the product to delay or avoid surgery. As an alternative to surgery we expect that the product could offer a pharmaco-economic advantage for the payers and patients. We have exclusive worldwide rights to develop, market and sell products containing AA4500, other than dermal formulations labeled for topical administration, for the treatment of Dupytren’s and Peyronie’s Diseases and, as of December 2005, Frozen Shoulder Syndrome.

Developing and Commercializing Transmucosal Film Technology.We believe delivery of pharmaceuticals across the mucosal membrane of the mouth offers important advantages to patients, including the possibility to achieve therapeutic benefits with significantly lower doses of drug, and the possibility of a convenient, once or twice daily dosing regimen.

We believe that the dosage form that we are developing for AA2600 will address many of the issues that previous buccal tablets have encountered. Specifically, our product for delivery of testosterone is very thin and is applied to the gum above the back teeth, compared to the buccal tablet which has a much higher profile and is placed above the front teeth. Our product candidate has a coating on the outside that prevents the cheek from sticking to the film and also seals the drug substance. In our recently completed Phase II trial, 97% of patients stated that the dosage form was desirable (49%) or acceptable (48%). Our market research leads us to believe that there is a percentage of hypogonadal men who do not like to use a topical gel on a daily basis for their therapy. We believe that a transmucosal film would provide a viable treatment alternative for these patients, as well as those patients who require increased doses of a gel formulation to achieve therapeutic benefit.

5

Table of Contents

Testim Opportunity

Hypogonadism market

Hypogonadism , or low testosterone, is a disorder that affects millions of men in the U.S. According to a 2001 article published inThe Journal of Clinical Endocrinology & Metabolism, hypogonadism affects approximately 20% of the U.S. male population over age 50. We estimate there is a similar percentage of affected men in Europe. Hypogonadism also affects a high percentage of men with certain co-morbidities regardless of age. The documented associations include: Type II Diabetes (33%)1, HIV (30%)2, Erectile Dysfunction (18%)3 and up to 74% of men being treated with high doses of opioids for chronic pain4. The effects of low testosterone lead to symptoms such as low energy, diminished libido, irritability and poor concentration. According to a recent study the impact of these symptoms on an afflicted person can be high.

TRT is the standard treatment for hypogonadism. According to IMS the total prescriptions within the TRT market have grown from .97 million to 2.39 million prescriptions (146%) between 2000 and 2005. Before 2000, the TRT market consisted of oral, injectable and patch therapies. In 2000 the first topical gel was introduced, and this product segment has been the driver of much of the total growth in the TRT market. According to IMS, the gel segment accounted for approximately 69% of the total prescriptions in the TRT market in the fourth quarter of 2005. Despite this growth, estimates of the U.S. Food and Drug Administration, or FDA, indicate that only 5% of men with hypogonadism currently receive TRT. According to our physician research, this low diagnosis rate stems primarily from low patient and physician awareness of the symptoms, treatment options and monitoring requirements.

| 1 | Dhindsa S. et al.J. Clin Endocrinology Metab. 2004 |

| 2 | Dobs A.S.Clin Endocrinol Metab. 1998 |

| 3 | Bodie J. et al.J. Urol. 2003 |

| 4 | Daniell H.W.J. Pain 2002 |

6

Table of Contents

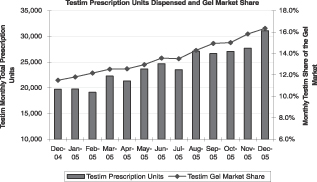

Testim has captured a significant portion of the gel prescription growth since its launch in early 2003, and Testim held a 16.3% prescription share of this market in December 2005. For the calendar year 2005, prescriptions of Testim grew by 70,100 compared to 2004. Despite its market leader status, the other gel in this market grew only by 17,000 prescriptions over the same period. Injectable formulations of TRT also grew (15,800 prescriptions), but the number of prescriptions for all other formulations (patches, orals, and buccals) dropped year over year.

|  |

Source: IMS

We believe Testim’s growth has been due to Testim’s favorable clinical profile and increased sales and marketing efforts in 2005. Our sales organization of nearly 100 representatives promotes Testim to urologists, endocrinologists and key primary care physicians. In April 2005, we contracted with Oscient in order to utilize their then 250-person salesforce to expand our promotional reach to a much larger audience of primary care physicians. Oscient had increased its sales force to approximately 300 by the end of 2005. We believe this effort has helped to improve physician awareness of hypogonadism and to differentiate Testim.

Testim is a proprietary, topical 1% testosterone once-a-day gel that treats hypogonadism by restoring testosterone blood levels back to normal for a 24-hour period following application. Testim is packaged in convenient, easy-to-open, single-use tubes. Patients apply Testim once per day to the upper arms and shoulders, enabling Testim’s active ingredient, testosterone, to be absorbed through the skin and into the bloodstream.

Clinical data supporting the advantages of Testim. We have designed and conducted our clinical trials to provide prescribing physicians with comprehensive information regarding Testim’s benefits. Since 2001, we have completed 13 clinical studies involving 1,600 patients including the largest placebo controlled study (n=400) ever conducted to evaluate the benefits and risks of TRT. We conducted five of these studies using Testim and other TRT products, including a transdermal patch and the other commercial gel. The results from these five studies, taken together, demonstrate that in patients with hypogonadism, testosterone levels directly correlate with patient symptom improvement.

We continue to conduct clinical studies to enhance the Testim data and to address the full patient population that could benefit from its use. For example, we completed a study in over 600 patients in December 2003 that demonstrated that overall sexual function and mood improves significantly by the end of the first week of Testim treatment. We have also initiated a large, multi-centered, placebo controlled study to determine the impact of Testim therapy and testosterone normalization within hypogonadal men who have type II diabetes. A retrospective analysis of our initial studies revealed the fact that the subset of hypogonadal men who had type II diabetes not

7

Table of Contents

only received the typical benefits of testosterone therapy, but also a significant decrease in fasting glucose levels versus placebo. This promising data and the high prevalence of hypogonadism within men with type II diabetes led to the initiation of the more robust, prospective, placebo controlled study.

Cost effectiveness and convenience. We believe, based on clinical data regarding testosterone levels in patients, market feedback from physicians, and the results of our clinical trials, that a higher percentage of patients are treated with only one tube of Testim per day (one dose per day) compared to the other commercial gel. In a recent retrospective pharmacy analysis conducted by Verispan analyzing 12 month usage patterns in over 40,000 patients, we learned that 95% of the Testim treated patients utilized a daily 5 gram dose at month 3 and 97% utilized this dose at month 12. We believe that one tube of Testim per day is an advantage for patients because of less volume of drug to apply, and for payors, because of lower cost.

Broad prescription coverage. Currently, we have broad third-party payor reimbursement for Testim and are covered by the majority of reimbursement plans. Our efforts to achieve third-party payor coverage have expanded as we grow our national accounts group. Testim has advantaged or parity coverage status compared to the other commercial gel with managed care plans covering over 150 million lives. Advantaged coverage generally means lower co-pays for patients.

AA4500 Opportunity

AA4500 is an injectable enzyme we in-licensed from BioSpecifics Technologies Corp., or BioSpecifics. Under our agreement with BioSpecifics, we were granted exclusive worldwide rights to develop, market and sell certain products containing AA4500. Our licensed rights concern the development of products, other than dermal formulations labeled for topical administration. Currently, we are developing AA4500 for the treatment of Dupuytren’s Disease, Peyronie’s Disease and Frozen Shoulder Syndrome. We may expand our agreement with BioSpecifics, at our option, to cover other indications as they are developed by us or BioSpecifics.

Dupuytren’s Disease

Disease state and market: Dupuytren’s Disease is a condition that affects the connective tissue that lies beneath the skin in the palm. The disease is progressive in nature. Typically, painful nodules typically develop in the palm as collagen deposits accumulate. As the disease progresses, the collagen deposits form a cord that stretches from the palm of the hand to the base of the finger. Once this cord develops, the patient’s fingers contract and the function of the hand is impaired. Currently, surgery is the only effective treatment. According toDupuytren’s Disease by Leclercq published in 2000, Dupuytren’s Disease is common in Caucasians with diabetes, epilepsy, alcoholism or HIV. It is most common in men and the incidence increases with age. In most patients (65%) the disease affects both hands, and recurrence after surgical treatment is common (as high as 50% over a patient’s lifetime). Due to the recurrent nature of the disease, multiple corrective surgeries are often required, which become increasingly complex. AA4500 is injected directly into the cord and the procedure is performed on an out-patient basis. We believe AA4500 as a treatment for Dupuytren’s Disease represents an attractive and addressable market for us as a specialty pharmaceutical company.

R&D status: Based on Phase II data previously published inThe Journal of Hand Surgery in 2002 utilizing a mean of three injections of AA4500 resulted in a 90% success for the joint closest to the palm, known as the MP joint, and 70% for the middle joint in the fingers, known as the PIP joint. On average patients required 1.5 injections of AA4500. We believe that Phase III studies for AA4500 as a treatment for Dupuytren’s Disease will commence in the middle of 2006.

Peyronie’s Disease

Disease state and market: Peyronie’s Disease is characterized by a plaque or hard lump that occurs on the penis. It begins as a localized inflammation, which progresses to a hardened scar on the shaft of the penis that

8

Table of Contents

reduces flexibility and causes the penis to bend during erection. This may cause pain on erection and a deformity that may prevent sexual intercourse altogether. Our market research indicates that, aside from the physical consequences, depression and loss of self-esteem are common in men with Peyronie’s Disease. According to a 2004 article by Mulhall et. al. inThe Journal of Urology, it is currently believed that Peyronie’s Disease is caused by vascular trauma or injury to the penis. Generally, Peyronie’s Disease is treated by urologists. Some physicians have used injections of Verapamil or Interferon or oral administration of para-aminobenzoic acid with minimal success. Surgical treatment may be an option for some patients, although complications as well as loss of penile length can occur.

AA4500 is injected on an out-patient basis into the plaque causing the penile curvature. Early Phase II clinical work with AA4500 in patients with Peyronie’s Disease indicates that the product reduces scar tissue size, thereby improving the curvature of the penis, and in some cases, restoring the ability to have sexual intercourse. Additional dose optimization studies will be needed.

R&D status: Although previous Stage II studies by the licensor of the product indicate possible effectiveness of AA4500 in this disease state, we believe there is an opportunity to reduce the number of injections required. Therefore, we expect to commence a Phase IIb dose ranging study for AA4500 as a treatment for Peyronie’s Disease in the second half of 2006.

Frozen Shoulder Syndrome

Disease state and market: Frozen Shoulder Syndrome is a disorder of diminished shoulder motion, characterized by restriction in both active and passive range of motion of the shoulder joint. Frozen Shoulder Syndrome usually affects patients aged 40-70 years. According toHarrison’s Principles of Internal Medicine, it is estimated that 3% of people develop Frozen Shoulder Syndrome over their lifetime and that women tend to be affected more frequently than men. The condition may affect both shoulders, either simultaneously or in sequence, in up to 16% of patients. Recurrence of Frozen Shoulder Syndrome is common within five years of the onset of the disorder. According to Dahan et. al. in the 2005 eMedicine article “Adhesive Capsulitis,” a higher incidence of Frozen Shoulder Syndrome exists among patients with diabetes (10-20%) compared to the general population (2-5%) and incidence among patients with insulin-dependent diabetes is even higher (36%), with an increased frequency of bilateral shoulder involvement. The most common treatment for Frozen Shoulder Syndrome is extensive physical therapy, corticosteroids and/or arthroscopy. Drugs are used to control pain, but none have been demonstrated to have an impact on Frozen Shoulder Syndrome. Likewise, medications have not been shown to affect the duration of the disorder or the severity or duration of joint contracture.

R&D status: Our licensor has conducted a Phase II clinical trial using AA4500 for the treatment of Frozen Shoulder. Three different doses of the enzyme were compared to placebo in this prospective, randomized, 60-subject trial. The results from this trial suggest that local injection of the enzyme is well-tolerated and may be effective in patients suffering from Frozen Shoulder Syndrome. Additional studies are needed to assess the optimal dose and dosing regimen of AA4500 for this indication.

Transmucosal Film Technology

General Discussion of Technology

We are developing several product candidates using a new oral transmucosal drug delivery system based on patented technology licensed from Formulation Technologies, L.C.C., doing business as PharmaForm, or PharmaForm. The basis of this technology is a film that adheres to the upper gum. We have the exclusive worldwide right to use this technology platform in therapeutic products that contain hormones or that treat urologic disorders and in certain pain products. We currently have four product candidates using this technology:

| • | AA2600, which is our TRT for the treatment of hypogonadism for which we expect to commence Phase III trials early in the second quarter of 2006; |

9

Table of Contents

| • | AA4010, which is our therapy to treat overactive bladder in Phase I of development for which we expect to seek a partner to further develop the product; and |

| • | two pain product candidates in the pre-clinical phase of development for the management of pain. |

We believe the key benefits of these products candidates could include high absorption, potentially less frequent dosing for some therapeutic drugs and a relatively low cost of goods.

A2600 (Testosterone Replacement Film)

Disease state and market: We are developing AA2600 for the treatment of hypogonadism using the transmucosal film technology. This product candidate may provide an important line extension for the Testim brand. If approved, AA2600 will provide physicians with a novel alternative for the treatment of hypogonadism. We believe its benefits may include the fact that it is small, discrete and easy to use, without the need for drying time as with topical gels. It is our opinion that the most likely patient candidates for this treatment option are those that prefer a dosage form other than those currently available, i.e., gel, patch, injectable or buccal tablet.

R&D status: We have conducted four Phase I studies in Europe with AA2600 in 60 men with low testosterone. Our studies demonstrated that AA2600 was well tolerated and the drug was well absorbed with approximately 80% of the drug delivered and available to the body. AA2600 provided marked increased levels of the androgen within one hour of application. A Phase II proof-of-principle study was initiated in late 2004 in which hypogonadal men were treated for 14 days. In August 2005, we announced that data from the study showed that AA2600 increased serum testosterone levels in hypogonadal men. Furthermore, the data indicated that it was well tolerated and 97% of patients in the study rated the dosage form as desirable or acceptable.

AA4010 (Overactive Bladder Film)

Disease state and market: According to an article published inThe Journal of Urology in August 2002, overactive bladder affects an estimated 13 million people in the U.S. Based on data from the RxList, the internet drug index, we estimate sales of pharmaceutical products for overactive bladder exceeded $1.0 billion in 2004.

A leading oral treatment option for overactive bladder is oxybutynin in both immediate release, or IR, and extended release forms. The published side effects of these drugs are dry mouth, gastrointestinal disorders, difficulty in concentration and visual disturbances. We believe these side effects are impediments to their widespread adoption as a therapy. A recently introduced transdermal patch, which is applied once every three days, appears to have equivalent efficacy to oral medications such as oxybutynin IR but with better tolerability, except for skin reactions at patch application sites, according to an article published inThe Journal of Urology in August 2002.

Because of resources committed to AA4500 and AA2600, and the broad nature of the overactive bladder market, we may seek a partner to further develop this product candidate.

R&D status: We initiated the first Phase I study of AA4010 in December 2004 and commenced patient dosing in January 2005. The study was completed in June 2005 and recent pharmacokinetic results confirmed that oxybutinin is delivered through our licensed transmucosal film delivery system.

Pain Film

Disease state and market: According to the American Pain Foundation, an estimated 75 million Americans suffer from pain every year (50 million from chronic pain and 25 million from acute pain due to injuries or surgery). According to the American Pain Foundation, chronic pain, if left untreated, significantly impacts quality of life — affecting physical, psychological, social and spiritual sense of well-being. According to a 2003 article by Stewart et. al. in theJournal of the American Medical Associations, surveys from various pain

10

Table of Contents

organizations indicate that 1 in 3 American adults lose more than 20 hours of sleep each month due to pain and lost workdays due to pain add up to over 50 million per year. Estimates based on these surveys project that pain costs Americans $100 billion each year, of which $61 billion is attributed to lost productivity.

Pharmacological treatment of pain follows the principles of treatment of any condition. Guidelines from theNational Foundation For The Treatment Of Painindicate that the correct medicine must be selected; the proper doses prescribed; and the risks and side-effects must be carefully monitored and weighed against the benefits. Our efforts are focused around the specialty audience addressed by our sales force. The early products in the pain drug development program address “short-procedure” needs and associated pain management as well as break-through pain and possibly chronic pain in follow-on programs. For applicability of some or all of the eight pain products in areas beyond specialty markets, we are likely to take a partnering approach.

R&D status: In February 2005, we entered into an additional license agreement with PharmaForm, granting us the exclusive right to develop, manufacture and market eight compounds for the management of pain, including acute and chronic pain, using the transmucosal film delivery system. Laboratory scale formulations have been produced for the first two compounds and are currently being evaluated. We believe the next step will be to evaluate the readiness of the formulations for inclusion in Phase I.

Manufacturing

We currently use, and expect to continue to depend on, contract manufacturers to manufacture Testim. We may depend on contract manufacturers to manufacture any products for which we receive marketing approval, and to produce sufficient quantities of our product candidates for use in preclinical and clinical studies.

Testim is manufactured for us by DPT Laboratories, Ltd., or DPT, pursuant to a manufacturing and supply agreement that expires on December 31, 2010 , the terms of which are summarized below in“Material Agreements”.

Testosterone, a non-animal derived hormone, is currently available to us from only two sources. We purchase testosterone from both sources but do not have an agreement with either of these suppliers. We acquire CPD, a critical ingredient for the manufacture of Testim, from a single source. We endeavor to maintain what we believe is an adequate inventory of the key ingredients of Testim.

For AA4500, we are responsible, at our own cost and expense, for developing the formulation and finished dosage form of products and arranging for the clinical supply of products. As permitted under the terms of our agreement with BioSpecifics, we have qualified Cobra Biologics Ltd., or Cobra, as a supplier of AA4500 for use in our clinical trials. The terms of our agreement with Cobra are summarized below under“Material Agreements.”Pursuant to our agreement with Althea Technologies, Inc., or Althea, Althea will fill and lyophilize the AA4500 bulk substance produced by Cobra, manufacture placebo and produce sterile diluent. The terms of our agreement with Althea are summarized below under“Material Agreements.”

Under the terms of our agreement with BioSpecifics, BioSpecifics has the option, exercisable no later than six months after FDA approval of the first New Drug Application or Biologics License Application with respect to a product, to assume the right and obligation to supply, or arrange for the supply from a third party other than a back-up supplier qualified by us, of a specified portion of commercial product required by us. The terms of our agreement with BioSpecifics are summarized below under“Material Agreements.”

Our contract manufacturers are subject to an extensive governmental regulation process. Regulatory authorities in our markets require that drugs be manufactured, packaged and labeled in conformity with current good manufacturing practices, or cGMP. The cGMP requirements govern quality control of the manufacturing process and documentation policies and procedures. We have established an internal quality control and quality assurance program, including a set of standard operating procedures and specifications that we believe is cGMP-compliant.

11

Table of Contents

Material Agreements

We have entered into agreements for the in-licensing of technology and products and for the manufacture of our products. Additionally, we have secured collaboration partners for the sale of Testim in geographic locations where we do not have our own sales force and a co-promotion partner for the sale of Testim in the U.S. We intend to pursue other licensing agreements and collaborations in the future.

Bentley Pharmaceuticals

We entered into two separate license agreements with Bentley Pharmaceuticals, Inc., or Bentley, that give us access to Bentley’s patented transdermal gel technology. In May 2000, Bentley granted us an exclusive, worldwide, royalty-bearing license to make and sell products incorporating Bentley’s formulation technology that contains testosterone. The term of this agreement is determined on a country by country basis and extends until the later of patent right termination in a country or 10 years from the date of first commercial sale. We produce Testim under this license. Bentley has filed new patent applications in the U.S., Europe and Japan, which, if issued, could provide additional patent protection for Testim. In May 2001, Bentley granted us similar rights for a product containing another hormone, the term of which is perpetual. Under these agreements, we are required to make up-front and milestone payments to Bentley upon contract signing, the decision to develop the underlying product, and the receipt of FDA approval.

In addition to our royalty obligations, to date, we have paid Bentley approximately $0.6 million of up-front payments and milestones under the in-license agreements. If all events under our in-license agreements with Bentley occur, we would be obligated to pay a maximum of approximately $1.0 million in milestone payments. The timing of these payments, if any, is uncertain.

DPT

Testim is manufactured for us by DPT under the terms of a manufacturing and supply agreement that we entered into in April 2002 as amended most recently on September 14, 2005. This agreement expires on December 31, 2010. During the term of the agreement, subject to our right to qualify and order Testim from a back-up supplier, and subject to DPT’s ability to qualify its Lakewood, New Jersey facility as a secondary site for the production of Testim, DPT is required to manufacture all of our worldwide commercial requirements of Testim. Prior to DPT’s qualification of the Lakewood facility, we are permitted to qualify a back-up supplier and order a specified amount of Testim each year from a back-up supplier. Upon DPT’s qualification of the Lakewood facility, we will no longer be permitted to order commercial supply of Testim from the back-up supplier. However, in the event that DPT is unable to meet our Testim supply requirements, Testim may be manufactured for us by a back-up supplier. The manufacturing fees paid to DPT are based upon the specified annual volume of Testim ordered by us. If we order less than a specified amount of Testim in any calendar year, the parties are required to negotiate to establish new manufacturing fees, with the understanding that DPT will continue to produce Testim for a specified minimum period in order to enable us to identify and utilize another supplier. DPT may terminate the agreement only upon our insolvency or bankruptcy or upon our breach of the agreement. We are in the process of qualifying an alternate contract manufacturer until DPT’s Lakewood, New Jersey facility has been qualified as a secondary site for the production of Testim.

BioSpecifics

In June 2004, we entered into a development and license agreement with BioSpecifics and amended the agreement in May 2005 and December 2005 (the BioSpecifics Agreement). Under the BioSpecifics Agreement, we were granted exclusive worldwide rights to develop, market and sell certain products containing BioSpecifics’ enzyme, which we refer to as AA4500. Our licensed rights concern the development of products, other than dermal formulations labeled for topical administration, and currently, our licensed rights cover the indications of Dupuytren’s and Peyronie’s Diseases and Frozen Shoulder Syndrome, for which we exercised our

12

Table of Contents

option in December 2005. We may further expand the BioSpecifics Agreement, at our option, to cover other indications as they are developed by us or BioSpecifics.

The BioSpecifics Agreement extends, on a country-by-country and product-by-product basis, for the longer of the patent life, the expiration of any regulatory exclusivity period or 12 years. We may terminate the BioSpecifics Agreement upon 90 days prior written notice.

We are responsible, at our own cost and expense, for developing the formulation and finished dosage form of products and arranging for the clinical supply of products. As permitted under the BioSpecifics Agreement, we have qualified Cobra as our primary supplier of clinical products under the agreement.

BioSpecifics has the option, exercisable no later than six months after FDA approval of the first New Drug Application or Biologics License Application with respect to a product, to assume the right and obligation to supply, or arrange for the supply from a third party other than a back-up supplier qualified by us, of a specified portion of our commercial product requirements. The BioSpecifics Agreement provides that we may withhold a specified amount of a milestone payment until (i) BioSpecifics executes an agreement, containing certain milestones, with a third party for the commercial manufacture of the product, (ii) BioSpecifics commences construction of a facility, compliant with cGMP, for the commercial supply of the product, or (iii) 30 days after BioSpecifics notifies us in writing that it will not exercise the supply option.

If BioSpecifics exercises the supply option, commencing on a specified date, BioSpecifics will be responsible for supplying either by itself or through a third party other than a back-up supplier qualified by us, a specified portion of the commercial supply of the product. If BioSpecifics does not exercise the supply option, we will be responsible for arranging for the entire commercial product supply. In the event BioSpecifics exercises the supply option, we and BioSpecifics are required to use commercially reasonable efforts to enter into a commercial supply agreement on customary and reasonable terms and conditions which are not worse than those with back-up suppliers qualified by us.

We must pay BioSpecifics on a country-by-country and product-by-product basis a specified percentage of net sales for products covered by the BioSpecifics Agreement. Such percentage may vary depending on whether BioSpecifics exercises the supply option. In addition, the percentage may be reduced if (i) BioSpecifics fails to supply commercial product supply in accordance with the terms of the BioSpecifics Agreement; (ii) market share of a competing product exceeds a specified threshold; or (iii) we are required to obtain a license from a third party in order to practice BioSpecifics’ patents without infringing such third party’s patent rights.

In addition to the payments set forth above, we must pay BioSpecifics an amount equal to a specified mark-up of the cost of goods sold for products sold by us that are not manufactured by or on behalf of BioSpecifics, provided that, in the event BioSpecifics exercises the supply option, no payment will be due for so long as BioSpecifics fails to supply the commercial supply of the product in accordance with the terms of the BioSpecifics Agreement.

Finally, we will be obligated to make contingent milestone payments upon the filing of regulatory applications and receipt of regulatory approval. Through December 31, 2005, we paid up-front and milestone payments under the BioSpecifics Agreement of $8.5 million. We could make up to an additional $5.5 million of contingent milestone payments under the BioSpecifics Agreement if all existing conditions are met. Additional milestone obligations will be due if we exercise an option to develop and license AA4500 for additional medical indications.

Cobra

In July 2005 we entered into an agreement with Cobra for the process development, scale up and manufacture of AA4500 for Phase II/III clinical trials (the Cobra Agreement). Accordingly, we will now rely on Cobra as our primary supplier of AA4500 for clinical trials.

13

Table of Contents

The Cobra Agreement is divided into five non-sequential stages with specific objectives, timelines, down payments and total payments that attach to each stage. We may terminate the Cobra Agreement at the completion of each stage if the objective or the timeline for such stage is not met. Through December 31, 2005, we incurred a total of $2.1 million under the Cobra Agreement. If all remaining stages are completed under the current Cobra Agreement, then we will pay Cobra an additional $2.4 million.

Althea

In order to prepare AA4500 for clinical trials, AA4500 bulk substance produced by Cobra must be filled and lyophilized, placebo must be manufactured and a sterile diluent must be produced (collectively, “pharmaceutical products”). On February 28, 2006, we entered into a Manufacturing and Clinical Supply Agreement with Althea to be effective as of January 17, 2006 that sets out the general terms and conditions under which Althea will produce these pharmaceutical products in bulk or finished dosage form for our development and/or clinical use only. At the time we executed the agreement, we and Althea entered into a project plan that provides the parameters for the production of the pharmaceutical products. Pursuant to the project plan we will supply bulk substance of AA4500 produced by Cobra to Althea which, in turn, will produce and deliver to us the pharmaceutical products. The agreement provides that we will pay Althea 50% of the total fees due to Althea upon signing of the project plan. Then, Althea will invoice us monthly for services completed during such month, and the balance of the fees will be invoiced upon delivery of the pharmaceutical products. Upon signing of the project plan in February 2006, we paid to Althea $174,000, and we expect to incur an additional $174,000 under this project plan in 2006.

PharmaForm

In June 2003, we expanded our drug delivery technology portfolio by entering into a license agreement with PharmaForm. Under this agreement, as amended, we were granted an exclusive, worldwide, royalty-bearing license to develop, make and sell products that contain hormones or that are used to treat urologic disorders incorporating PharmaForm’s oral transmucosal film technology for which there is an issued patent in the U.S. The term of this license agreement is for the life of the licensed patents.

In February 2005, we entered into an additional license agreement with PharmaForm. Under this agreement, we were granted exclusive, worldwide royalty-bearing rights to develop, manufacture and market eight compounds using PharmaForm’s proprietary transmucosal film technology for the management of pain, including acute and chronic pain. The compounds that may be developed include opioids as well other types of analgesics. In 2005, we paid an up-front payment of $0.5 million and could make up to an additional $21.2 million in contingent milestone payments if all underlying events for these eight products occur. In addition, we will have on-going royalty payment obligations to PharmaForm. The timing of the remaining payments, if any, is uncertain.

To speed the development of products using the licensed technology from PharmaForm, we entered into a research and development agreement with PharmaForm on a fee for service basis. We will be the sole owner of any intellectual property rights developed in connection with this agreement. We incurred $2.3 million under the research and development agreement in 2005 and expect to incur $3.1 million in 2006.

Bayer

We entered into an exclusive marketing and distribution agreement with Bayer in December 2003 to commercialize Testim in Canada. This agreement is effective for the life of the Bentley patent. The expiration of the Bentley patent in Canada is January 5, 2010. In July 2005, an additional patent covering Testim issued in Canada, and this patent is included in our license from Bentley. This patent expires in 2023. Bayer has a large commercial presence in Canada that includes approximately 450 sales representatives. We filed for regulatory approval of Testim in Canada in March 2004 and will not be able to sell Testim in Canada until regulatory

14

Table of Contents

approval is granted. We have responded to questions raised by the Canadian authorities, and they are reviewing our responses as part of the approval process. The terms of this agreement require Bayer to purchase all Testim supply for Canada from us and to make up-front, milestone and royalty payments. The milestone payments are due upon contract signing, filing for regulatory approval in Canada, the first sale of Testim in Canada and upon achieving specified sales levels. The royalty payments are based on net product revenue and are similar to the royalty payments due to Bentley.

Ipsen

We entered into a license and distribution agreement with Ipsen in March 2004. This agreement is exclusive and royalty-bearing for the longer of ten years from the date of first commercial sale by country or the life of the Bentley patent, including any newly issued patents. The European patent that we license from Bentley for Testim expires in November 2006. Bentley has filed a new patent application in the U.S., Europe and Japan, which, if issued, could provide additional patent protection for Testim. Ipsen is a European pharmaceutical company with a worldwide commercial presence and a strong urology focus. Ipsen currently has operations in 110 countries and has approximately 3,700 employees. Under this agreement, we granted Ipsen an exclusive license to use and sell Testim on a worldwide basis outside the U.S., Canada, Mexico and Japan. The U.K. was the first country outside of the U.S. where regulatory approval to market Testim was obtained. A mutual recognition application based on the U.K. approval was initiated on March 30, 2004 in order to obtain additional European approvals. As of December 31, 2005, Testim was approved for marketing in the U.S., the U.K., Belgium, Denmark, Finland, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain and Sweden. In 2005, Testim was launched in Belgium, Denmark, Finland, Germany, Ireland, Netherlands, Spain, Sweden, and the U.K. Under the terms of our agreement, Ipsen will seek regulatory approval in those non-E.U. countries in which it wishes to sell our product. The terms of this agreement require Ipsen to purchase all Testim supply from us or exercise their conditional option for a technology transfer and to make up-front, milestone and royalty payments. Future milestone payments will be due upon regulatory approval, product launch in various countries and supply price reductions. The royalty payments are based on net product revenue and are similar to royalty payments due to Bentley.

We do not expect sales of Testim outside of the U.S. pursuant to our collaborations with Bayer and Ipsen to have a material impact on our revenues or profitability. We believe that the primary benefit of these agreements is the demonstration of our global development and commercialization capabilities to future licensors, as well as providing us with up-front and milestone payments and opportunities for manufacturing efficiencies through increased sales of Testim.

Through December 31, 2005, we have collected $11.9 million in up-front and milestone fees from Bayer and Ipsen. We can potentially collect up to an additional $5.7 million in milestone fees under the Ipsen collaboration and up to $1.7 million under the Bayer collaboration, if all underlying events occur. The timing of the above payments, if any, is uncertain.

Oscient Pharmaceuticals

In April 2005, we entered into a co-promotion agreement (the Oscient Agreement) with Oscient. The agreement provides that Oscient will have the exclusive right to co-promote Testim to primary care physicians in the U.S. using its 300-person sales force, while we will continue to promote Testim using our specialty sales force that calls on urologists, endocrinologists and select primary care physicians. The initial term of the Oscient Agreement ends on April 30, 2007. Oscient may extend the Oscient Agreement for two consecutive two-year periods provided that Oscient has met certain milestones for each extension. If these milestones are met and Oscient does not elect to terminate the Oscient Agreement, the first extension period will commence on January 1, 2007 and end on December 31, 2008 and the second extension period will commence effective January 1, 2009 and end on April 30, 2011.

15

Table of Contents

We and Oscient utilize a joint marketing and promotion plan which sets forth the responsibilities of both parties with respect to the marketing and promotion of Testim in the U.S. primary care physician market, and we share equally these promotional expenses. Each party will be responsible for the costs associated with its own sales force. The 2005 combined spending for marketing and promotion of Testim in the primary care physician market in the U.S. was $7.1 million, and we estimate that the total costs for 2006 will be approximately $11.0 million to 13.0 million. These costs will be shared equally.

Oscient will be compensated for its services based on a specified percentage of the gross profit from Testim sales attributable to primary care physicians in the U.S. that exceed a specified sales threshold (the Oscient co-promotion fees). All gross profit earned on sales to primary care physicians below the predetermined threshold and all gross profit earned on all sales to non primary care physicians are not subject to the terms of the Oscient Agreement. Once sales to primary care physicians have exceeded the predetermined sales threshold, the gross profit earned on such sales is available to be split between us and Oscient. Once all agreed upon promotional expenses are appropriately reimbursed to each party, the gross profit remaining will be divided according to agreed upon percentages. The specific percentages are based upon Testim sales levels above the threshold attributable to primary care physicians actually achieved. For the year ended December 31, 2005, we recorded $3.5 million of expense for the Oscient co-promotion fees.

The agreed upon promotional expenses for each year are reimbursable equally and simultaneously to each company through the profit split mechanism, except in 2005 when Oscient was disproportionately reimbursed its share of the promotional expenses through the profit split mechanism. As the agreed upon percentage of the gross profit available to be split in 2005 was insufficient to reimburse Oscient its share of the promotional expenses, that portion not reimbursed to Oscient will be carried over to 2006 and will be reimbursed through the 2006 profit split mechanism. Of the $3.5 million expense recorded by us for the year ended December 31, 2005, $0.6 million was due to this carry over reimbursement.

The Oscient Agreement may be terminated by either party upon the occurrence of certain termination events. We may be obligated to make termination payments in certain instances. Also, Oscient has been granted the exclusive option to co-promote any of our future product candidates that treat hypogonadism and contain testosterone as the active ingredient.

We will invoice and record in our financial statements all sales of Testim, including those sales to primary care physicians that exceed the specified threshold, as well as the gross profit earned on all sales. We will record our share of promotional expenses incurred and the Oscient co-promotion fees as “selling, general & administration” operating expenses in our consolidated statement of operations.

Competition

We face competition in North America, Europe and elsewhere from larger pharmaceutical companies, specialty pharmaceutical companies and biotechnology firms, universities and other research institutions and government agencies that are developing and commercializing pharmaceutical products. Many of our competitors have substantially greater financial, technical and human resources than we have and may, subsequently, develop products that are more effective, safer or less costly than any that have been or are being developed by us or that are generics. Our success will depend on our ability to acquire, develop and commercialize products and our ability to establish and maintain markets for Testim or any products for which we receive marketing approval.

AndroGel

The primary competition for Testim in the TRT market is AndroGel, marketed by Solvay Pharmaceuticals, Inc., or Solvay. Solvay has the advantage of having launched AndroGel three years prior to Testim as well as

16

Table of Contents

having a sales force of approximately 300 individuals. During 2005, Solvay and ICOS Corporation, or ICOS, co-promoted AndroGel. ICOS has reported that it will not continue to co-promote AndroGel in 2006. According to IMS, as of December 31, 2005, AndroGel accounted for 83.7% of the gel prescriptions, although this share declined each quarter in 2005, while Testim’s share of the gel market increased.

Other Delivery Options

Testim also competes with other TRTs such as injectables, patches, orals and a buccal tablet. The injectables have maintained presence in the market due to the low cost compared to the transdermal options. There are also a significant number of patients who prefer getting a shot every two to three weeks instead of utilizing a daily application of another product. Physicians perceive the disadvantage of the injectables as being the fact that many patients’ testosterone levels rise past the normal barrier of 1000 ng/dl which leads to a wide flux of levels in a patient and the potential for side effects such as gynecomastia. Androderm is a transdermal testosterone patch marketed by Watson Pharmaceuticals. Androderm is the leading patch product and accounted for approximately 10% of total TRT prescriptions in December of 2005. The number of Androderm prescriptions is decreasing. We believe this trend may be due to the high number of patients who experience skin rash. Oral therapy has decreased substantially in recent years. We believe this trend may be due to the concern of inconsistent testosterone levels and the chance for liver toxicity. The buccal therapy retains less than 1% share in the market.

Generic Competition

In July 2003, Watson Pharmaceuticals, or Watson, and Par Pharmaceuticals, or Par, filed abbreviated new drug applications, or ANDAs, with the FDA to be approved as generics for AndroGel. In response to these ANDAs, Solvay filed patent infringement lawsuits against these two companies to block the approval and marketing of the generic products. Any generic for AndroGel will not be a generic substitute for Testim. On November 1, 2004, Par Pharmaceuticals’ partner, Paddock Laboratories, or Paddock, received tentative approval of its ANDA from the FDA, and on January 12, 2006, Watson received approval of its ANDA from the FDA. In January 2006, the thirty-month stay in each patent action expired. We believe that Watson was the first to file an ANDA with FDA and, therefore, Watson, not Par/Paddock, is entitled to launch first with six-month exclusivity. As a result, Watson will have to decide whether to (1) launch before a final outcome in the patent litigation and risk treble damages if its product is found to infringe the Solvay patent or (2) wait for the final outcome of the litigation before launch. Any generic for AndroGel will not be a generic for Testim, since Testim is BX rated (or non-substitutable) with Androgel. However if one of the companies chooses to market its product, this would likely result in increased competition for Testim, most likely, at lower prices. Other pharmaceutical companies may develop generic versions of any products that we commercialize that are not subject to patent protection or other proprietary rights. Governmental and other cost containment pressures may result in physicians writing prescriptions for these generic products.

Future Delivery Options

In addition to potential generic competition, several other pharmaceutical companies have TRT products in development that may be approved for marketing in the U.S. Cellegy Pharmaceuticals Inc. submitted a new drug application, or NDA, to the FDA for the approval of a 2% testosterone gel that the FDA rejected in 2003. In addition, BioSante Pharmaceuticals Inc. licensed a testosterone gel in 2000 which is currently reported to be in late stage development. MacroChem Corp. has also developed a testosterone gel that is currently in Phase I studies. Ardana plc, a U.K. company, has announced plans to develop a testosterone cream for the U.S. market. Other new treatments are being sought for TRT, including a new isomer of an old product for centrally mediated treatment of primary hypogonadism as well as a new class of drugs called Selective Androgen Receptor Modulators, or SARMs. These products are in the early stages of development and their future impact on the treatment of testosterone deficiency is unknown.

17

Table of Contents

It has also been made public that Indevus Pharmaceuticals, Inc. has licensed a long acting testosterone injection that is currently marketed in Europe under the name of Nebido. We believe that this product could be launched in the U.S. in late 2007 or early 2008. This product may enhance compliance with some patients and should be considered as competition to Testim if it were to launch. Another potential introduction into the marketplace is an oral therapy, called Androxal, from Zonagen, Inc., or Zonagen. This molecule is designed to restore normal testosterone production in males rather than externally replacing testosterone like the current alternatives. According to Zonagen, an NDA may be filed for this product in 2008.

Finally, we face extensive competition in the acquisition or in-licensing of pharmaceutical products to enhance our portfolio of products. A number of more established companies, which have strategies to in-license or acquire products, may have competitive advantages as may other emerging companies taking similar or different approaches to product acquisitions. In addition, a number of established research-based pharmaceutical and biotechnology companies may acquire products in late stages of development to augment their internal product lines. These established companies may have a competitive advantage over us due to their size, resources and experience.

Government Regulation

Government authorities in the U.S., at the federal, state, and local level, and foreign countries extensively regulate, among other things, the following areas relating to our products and product candidates:

| • | research and development; |

| • | testing, manufacture, labeling and distribution; |

| • | advertising, promotion, sampling and marketing; and |

| • | import and export. |

All of our products require regulatory approval by government agencies prior to commercialization. In particular, human therapeutic products are subject to rigorous preclinical and clinical trials to demonstrate safety and efficacy and other approval procedures of the FDA and similar regulatory authorities in foreign countries. Various federal, state, local, and foreign statutes and regulations also govern testing, manufacturing, labeling, distribution, storage and record-keeping related to such products and their promotion and marketing. The process of obtaining these approvals and the compliance with federal, state, local, and foreign statutes and regulations require the expenditure of substantial time and financial resources. In addition, the current regulatory and political environment at FDA could lead to increased testing and data requirements which could impact regulatory timelines and costs.

We have received marketing approval for Testim for the indication of hypogonadism in the U.S., the U.K., Belgium, Denmark, Finland, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain and Sweden. Approval in the specified European countries was via the Mutual Recognition Procedure. We have applied for marketing approval for Testim in Canada. We have responded to questions raised by the Canadian authorities as part of the approval process. In Europe, Testim was launched in Belgium, Denmark, Finland, Germany, Ireland, Netherlands, Spain, Sweden, and the UK in 2005. None of our other product candidates has received marketing approval.

U.S. Government Regulation

In the U.S., the FDA regulates drugs under the Federal Food, Drug, and Cosmetic Act and implementing regulations. If we fail to comply with the applicable requirements at any time during the product development process, approval process, or after approval, we may become subject to administrative or judicial sanctions. These sanctions could include:

| • | refusal to approve pending applications; |

18

Table of Contents

| • | withdrawals of approvals; |

| • | clinical holds; |

| • | warning letters; |

| • | product recalls and product seizures; and |

| • | total or partial suspension of our operations, injunctions, fines, civil penalties or criminal prosecution. |

Any agency enforcement action could have a material adverse effect on us.

Currently there is a substantial amount of congressional and administration review of the FDA and the regulatory approval process for drug candidates in the U.S. As a result, there may be significant changes made to the regulatory approval process in the U.S.

The steps required before a drug may be marketed in the U.S.include:

| • | preclinical laboratory tests, animal studies and formulation studies; |

| • | submission to the FDA of an investigational new drug exemption, or IND, which must become effective before human clinical trials may begin; |

| • | execution of adequate and well-controlled clinical trials to establish the safety and efficacy of the product for each indication for which approval is sought; |

| • | submission to the FDA of a new drug application (NDA), or biologics license application (BLA); |

| • | satisfactory completion of an FDA inspection of the manufacturing facility or facilities at which the product is produced to assess compliance with cGMP; and |

| • | FDA review and approval of the NDA or BLA, or any supplements thereto, including, if applicable, a determination of its controlled substance schedule. |

Preclinical studies generally are conducted in laboratory animals to evaluate the potential safety and activity of a product. Violation of the FDA’s good laboratory practices regulations can, in some cases, lead to invalidation of the studies, requiring these studies to be replicated. In the U.S., drug developers submit the results of preclinical trials, together with manufacturing information and analytical and stability data, to the FDA as part of the IND, which must become effective before clinical trials can begin in the U.S. An IND becomes effective 30 days after receipt by the FDA unless before that time the FDA raises concerns or questions about the proposed clinical trials outlined in the IND. In that case, the IND sponsor and the FDA must resolve any outstanding FDA concerns or questions before clinical trials can proceed. If these concerns or questions are unresolved, the FDA may not allow the clinical trials to commence.

19

Table of Contents

Clinical trials involve the administration of the investigational product candidate or approved products to human subjects under the supervision of qualified investigators. Clinical trials are conducted under protocols detailing, among other things, the objectives of the study, the parameters to be used in assessing the safety and the effectiveness of the drug. Typically, clinical evaluation involves a time-consuming and costly three-phase sequential process, but the phases may overlap. Each trial must be reviewed, approved and conducted under the auspices of an independent institutional review board, and each trial must include the patient’s informed consent. The following sets forth a brief description of the typical phases of clinical trials:

Phase I | Refers typically to closely monitored clinical trials and includes the initial introduction of an investigational new drug into human patients or healthy volunteer subjects. Phase I clinical trials are designed to determine the safety, metabolism and pharmacologic actions of a drug in humans, the potential side effects of the product candidates associated with increasing drug doses and, if possible, to gain early evidence of the product candidate’s effectiveness. Phase I trials also include the study of structure-activity relationships and mechanism of action in humans, as well as studies in which investigational drugs are used as research tools to explore biological phenomena or disease processes. During Phase I clinical trials, sufficient information about a drug’s pharmacokinetics and pharmacological effects should be obtained to permit the design of well-controlled, scientifically valid Phase II studies. The total number of subjects and patients included in Phase I clinical trials varies, but is generally in the range of 20 to 80 people. | |

Phase II | Refers to controlled clinical trials conducted to evaluate appropriate dosage and the effectiveness of a drug for a particular indication or indications in patients with a disease or condition under study and to determine the common short-term side effects and risks associated with the drug. These clinical trials are typically well-controlled, closely monitored and conducted in a relatively small number of patients, usually involving no more than several hundred subjects. Phase II studies can be sequenced as Phase IIa or Phase IIb. | |

Phase III | Refers to expanded controlled and uncontrolled clinical trials. These clinical trials are performed after preliminary evidence suggesting effectiveness of a drug has been obtained. Phase III clinical trials are intended to gather additional information about the effectiveness and safety that is needed to evaluate the overall benefit-risk relationship of the drug and to provide an adequate basis for physician labeling. Phase III trials usually include from several hundred to several thousand subjects. | |

Phase IV | Refers to trials conducted after approval of a new drug and which explore approved uses and approved doses of the product. These trials must also be approved and conducted under the auspices of an institutional review board. Phase IV studies may be required as a condition of approval. | |

Clinical testing may not be completed successfully within any specified time period, if at all. The FDA closely monitors the progress of each of the first three phases of clinical trials that are conducted in the U.S. and may, at its discretion, reevaluate, alter, suspend or terminate the testing based upon the data accumulated to that point and the FDA’s assessment of the risk/benefit ratio to the patient. The FDA can also provide specific guidance on the acceptability of protocol design for clinical trials. The FDA or we may suspend or terminate clinical trials at any time for various reasons, including a finding that the subjects or patients are being exposed to an unacceptable health risk. The FDA can also request additional clinical trials be conducted as a condition to product approval. During all clinical trials, physicians monitor the patients to determine effectiveness and to observe and report any reactions or other safety risks that may result from use of the drug candidate.

Assuming successful completion of the required clinical trial, drug developers submit the results of preclinical studies and clinical trials, together with other detailed information including information on the

20

Table of Contents

chemistry, manufacture and control of the product, to the FDA, in the form of an NDA or BLA, requesting approval to market the product for one or more indications. In most cases, the NDA/BLA must be accompanied by a substantial user fee. The FDA reviews an NDA/BLA to determine, among other things, whether a product is safe and effective for its intended use.

Before approving an application, the FDA will inspect the facility or facilities where the product is manufactured. The FDA will not approve the application unless cGMP compliance is satisfactory. The FDA will issue an approval letter if it determines that the application, manufacturing process and manufacturing facilities are acceptable. If the FDA determines that the application, manufacturing process or manufacturing facilities are not acceptable, it will outline the deficiencies in the submission and will often request additional testing or information. Notwithstanding the submission of any requested additional information, the FDA ultimately may decide that the application does not satisfy the regulatory criteria for approval and refuse to approve the application by issuing a “not approvable” letter.

The testing and approval process requires substantial time, effort and financial resources, which may take several years to complete. The FDA may not grant approval on a timely basis, or at all. We may encounter difficulties or unanticipated costs in our efforts to secure necessary governmental approvals, which could delay or preclude us from marketing our products. Furthermore, the FDA may prevent a drug developer from marketing a product under a label for its desired indications or place other conditions, including restrictive labeling, on distribution as a condition of any approvals, which may impair commercialization of the product. After approval, some types of changes to the approved product, such as adding new indications, manufacturing changes and additional labeling claims, are subject to further FDA review and approval.

If the FDA approves the new drug application or biologics application, the drug can be marketed to physicians to prescribe in the U.S. After approval, the drug developer must comply with a number of post-approval requirements, including delivering periodic reports to the FDA (i.e., annual reports), submitting descriptions of any adverse reactions reported, biological product deviation reporting, and complying with drug sampling and distribution requirements. The holder of an approved NDA/BLA is required to provide updated safety and efficacy information and to comply with requirements concerning advertising and promotional labeling. Also, quality control and manufacturing procedures must continue to conform to cGMP after approval. Drug manufacturers and their subcontractors are required to register their facilities and are subject to periodic unannounced inspections by the FDA to assess compliance with cGMP which imposes procedural and documentation requirements relating to manufacturing, quality assurance and quality control. Accordingly, manufacturers must continue to expend time, money and effort in the area of production and quality control to maintain compliance with cGMP and other aspects of regulatory compliance. The FDA may require post-market testing and surveillance to monitor the product’s safety or efficacy, including additional studies to evaluate long-term effects.

In addition to studies requested by the FDA after approval, a drug developer may conduct other trials and studies to explore use of the approved drug for treatment of new indications, which require submission of a supplemental or new NDA and FDA approval of the new labeling claims. The purpose of these trials and studies is to broaden the application and use of the drug and its acceptance in the medical community.