Commercial Capital Bancorp (CCBI) Inactive

Filed: 27 Oct 03, 12:00am

This presentation may include forward-looking statements (related to the

plans, beliefs and goals of CCBI and its subsidiaries), which involve certain

risks and uncertainties that could cause actual results to differ materially from

those in the forward-looking statements. Such risks and uncertainties include,

but are not limited to, the following factors: competitive pressure in the

banking industry; changes in the interest rate environment; the health of the

economy, either nationally or regionally; the deterioration of credit quality,

which would cause an increase in the provision for possible loan and lease

losses; changes in the regulatory environment; changes in business conditions,

particularly in California real estate; volatility of rate sensitive deposits;

asset/liability matching risks and liquidity risks; and changes in the securities

markets. CCBI undertakes no obligation to revise or publicly release any

revision to these forward-looking statements.

Regulation FD

CCBI Highlights

Financial Position

September 30, 2003

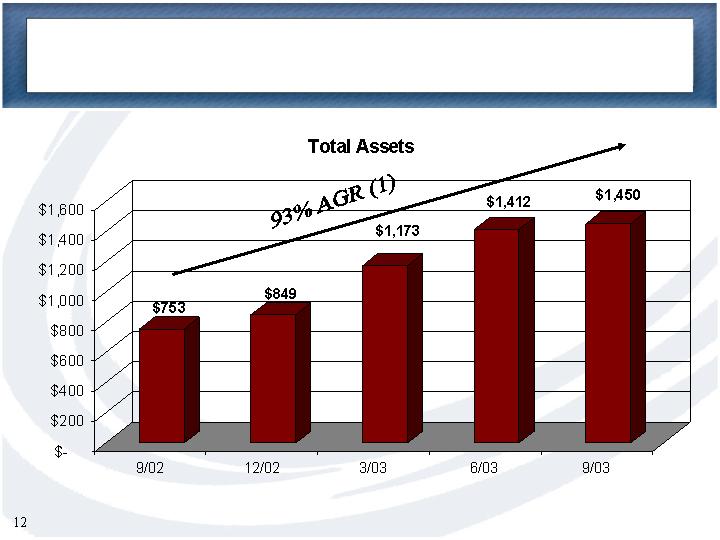

Total Assets

$1.45 billion

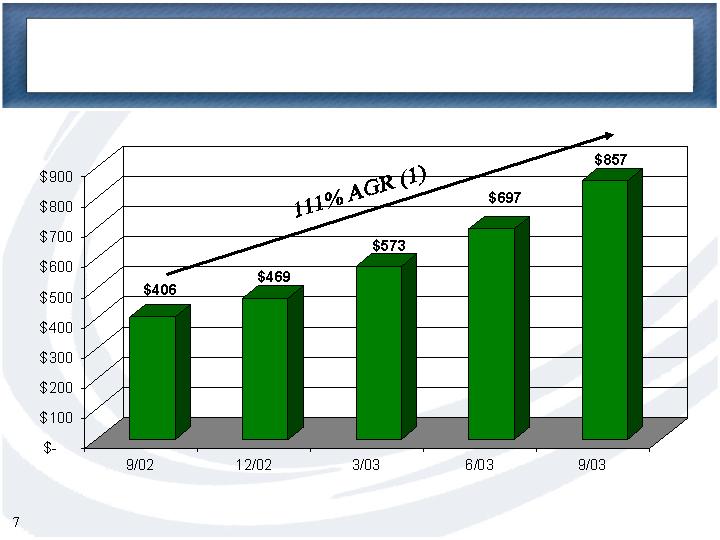

Loans Held for Investment

$857 million

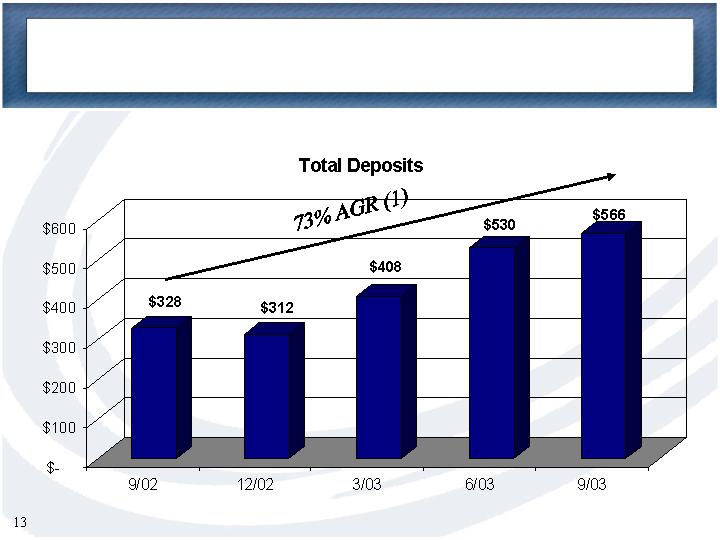

Deposits

$566 million

Equity

$96 million

Tangible Equity

$83 million

Quarter Ended

Quarter Ended

Financial Results

09/30/2003

09/30/2002

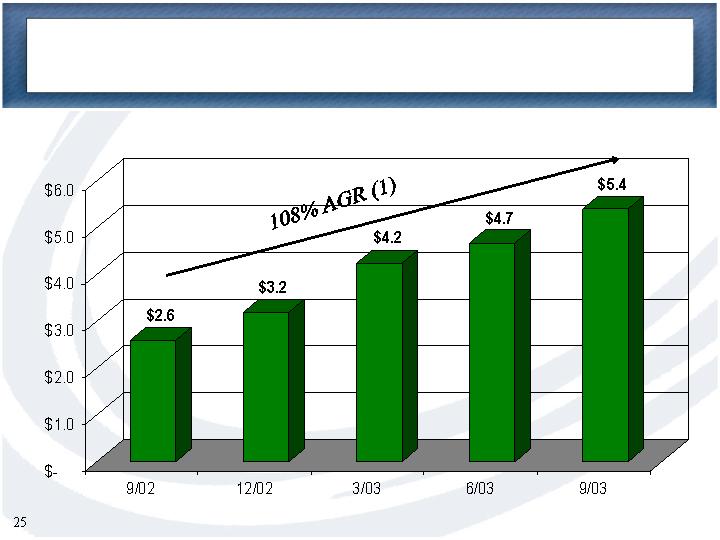

Net Income

$5.4 million

$2.6 million

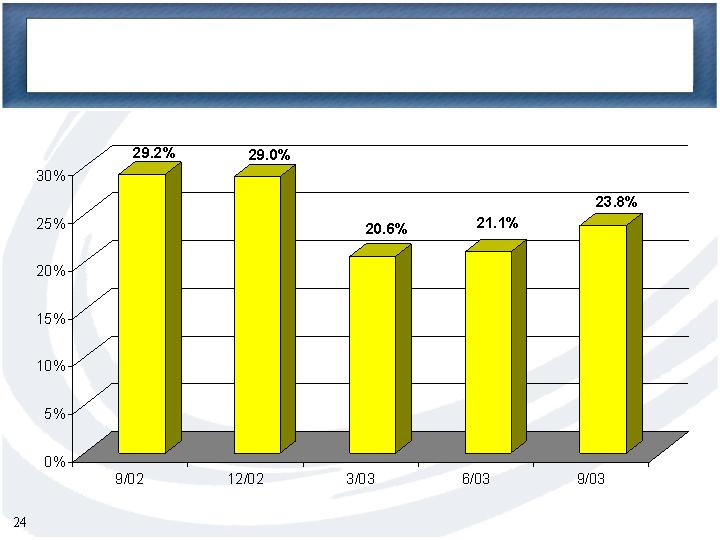

Return on Average Equity

23.84%

29.19%

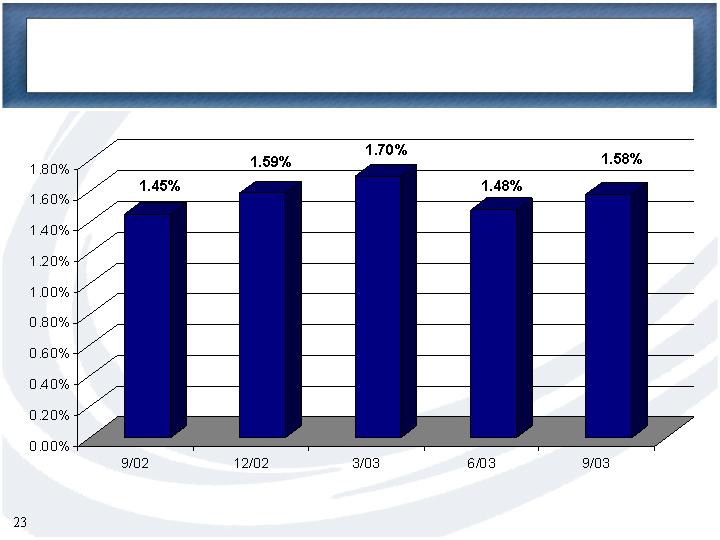

Return on Average Assets

1.58%

1.45%

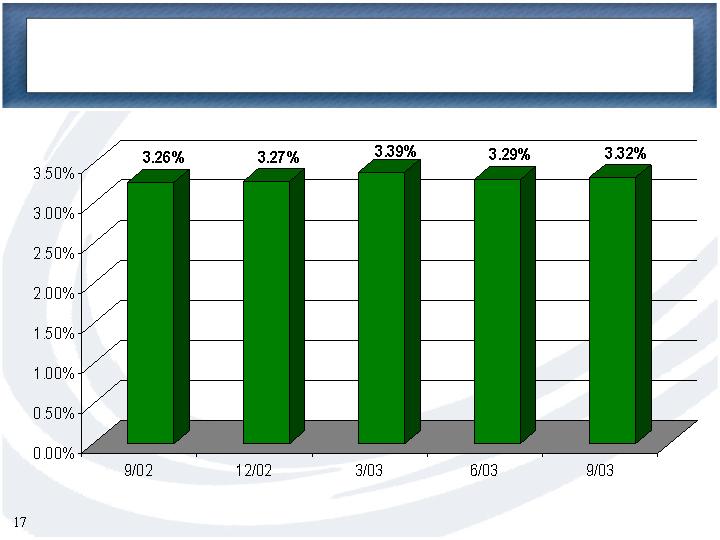

Net Interest Margin

3.32%

3.26%

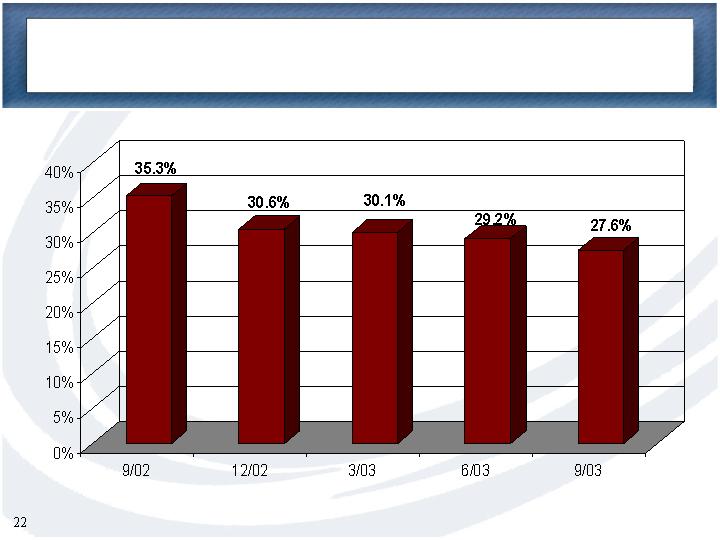

Efficiency Ratio

27.55%

35.32%

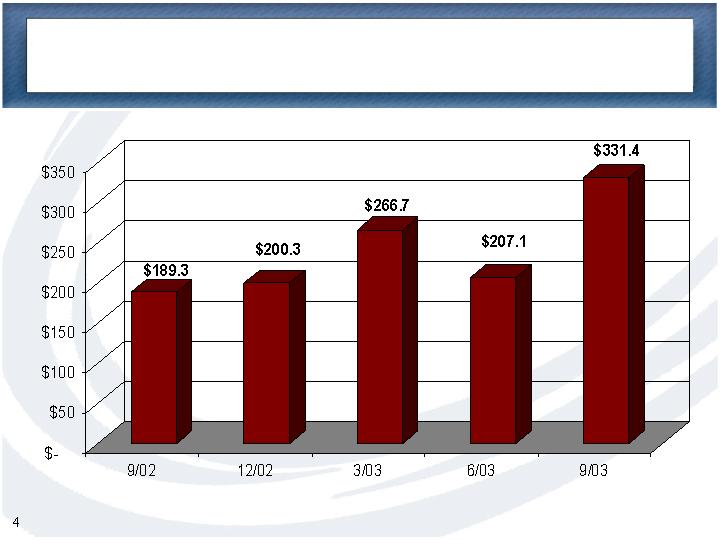

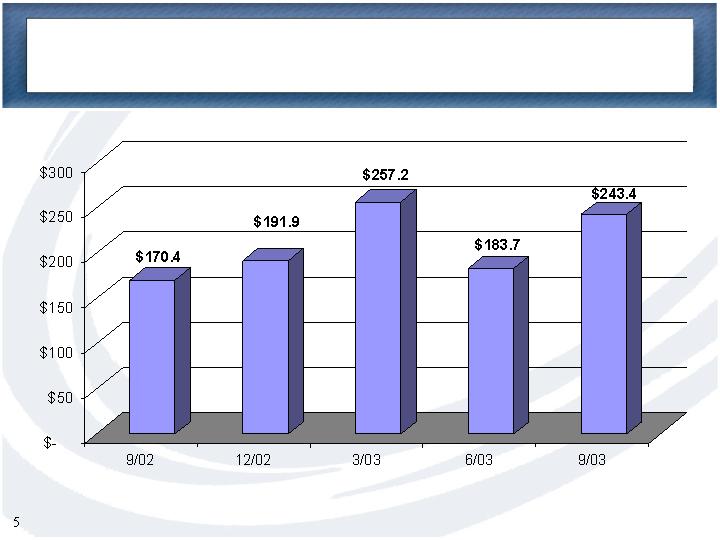

Total Loan Originations

$331 million

$189 million

($ in millions)

Record Total Loan Originations

($ in millions)

Core Loan Originations

Core Loan Originations Retained

($ in millions)

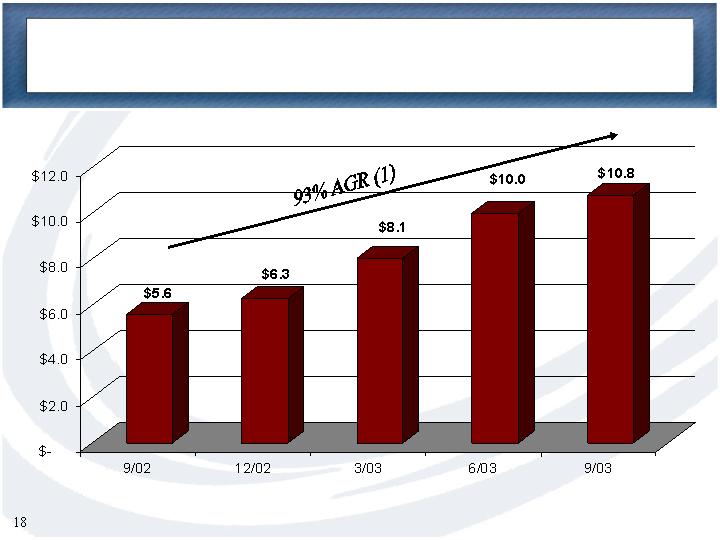

Record Growth in Loans Held for Investment

(1) AGR – Annual Growth Rate: 9/02 to 9/03

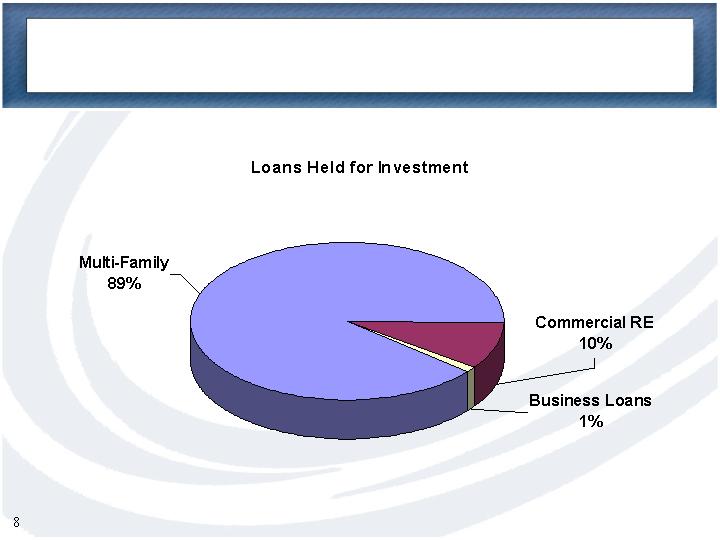

Loan Portfolio Mix

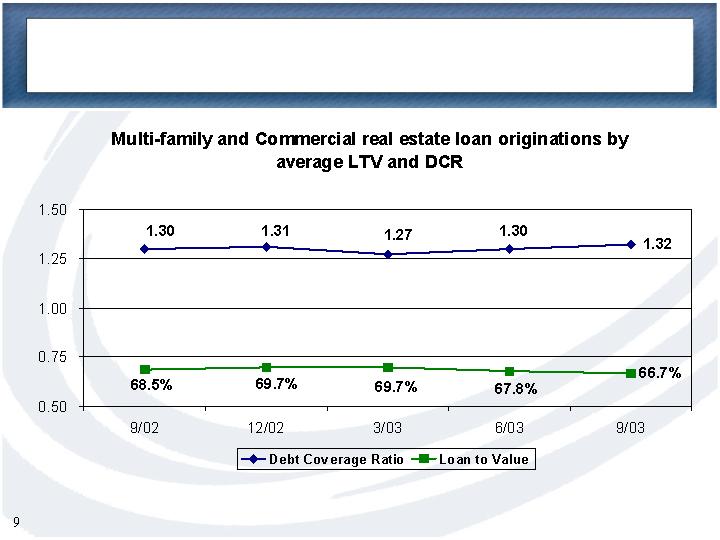

Consistent Underwriting

Asset Quality of Multi-family Loans

Non-Accrual Loans/

Nationwide

Total Loans

(1)

Multi-family

0.19%

Single family

0.84%

Commercial Real Estate

1.14%

Construction

1.15%

Business Loans

1.96%

Consumer

0.66%

Multi-family Loans

CCBI

0.00%

Western Region Thrifts

0.13%

Nationwide Thrifts

0.19%

(1) Based upon 6/30/03 Thrift Financial Reports for nationwide savings institutions

($ in millions)

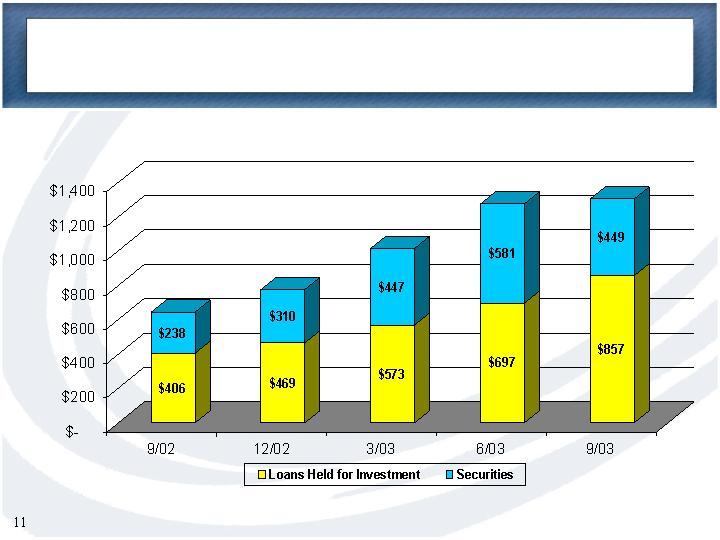

Loans to Securities Mix

($ in millions)

Balance Sheet Transition

(1) AGR – Annual Growth Rate: 9/02 to 9/03

($ in millions)

(1) AGR – Annual Growth Rate: 9/02 to 9/03

Deposit Growth

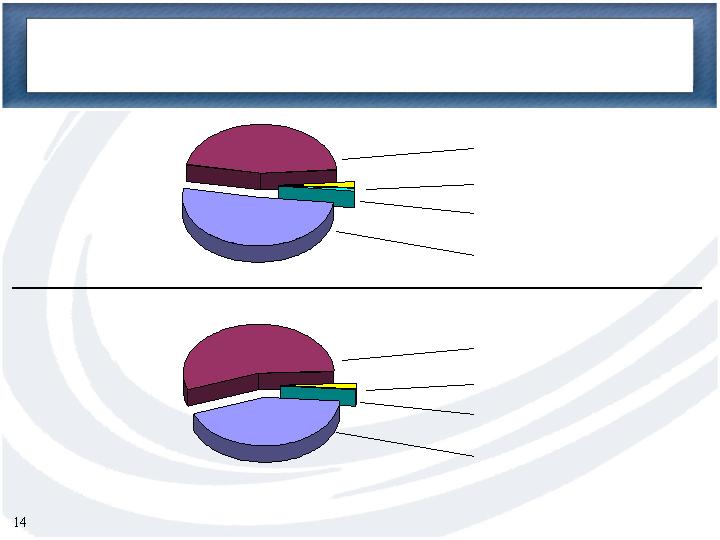

Deposit Composition

at 9/30/2002

Deposit Composition

at 9/30/2003

43% Certificates of Deposit

Maturing Deposit Mix

‹1% Savings Accounts

2% Demand Deposits

55% Money Market

51% Certificates of Deposit

1% Savings Accounts

2% Demand Deposits

46% Money Market

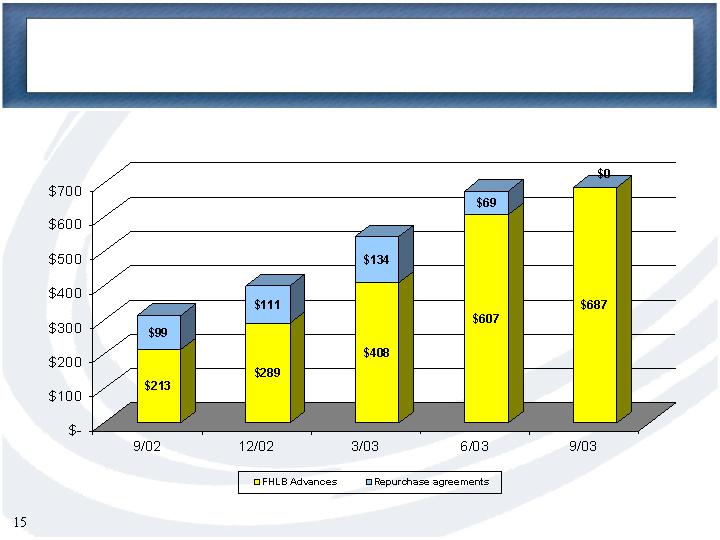

FHLB Advances to Repo Mix

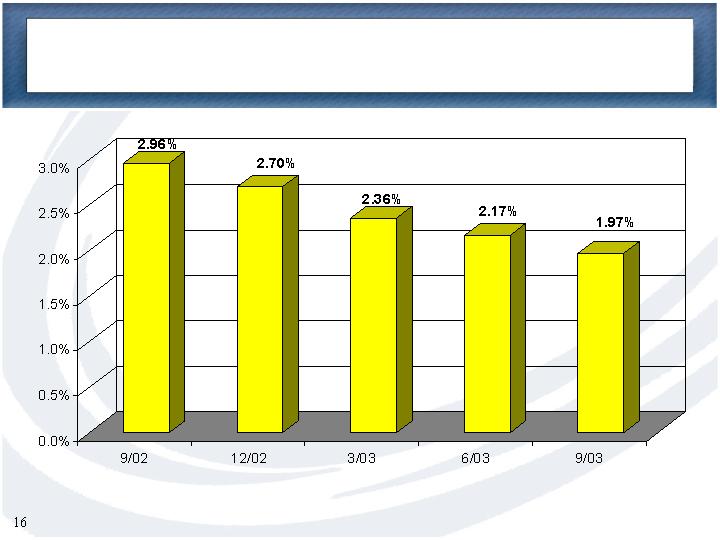

Cost of Funds

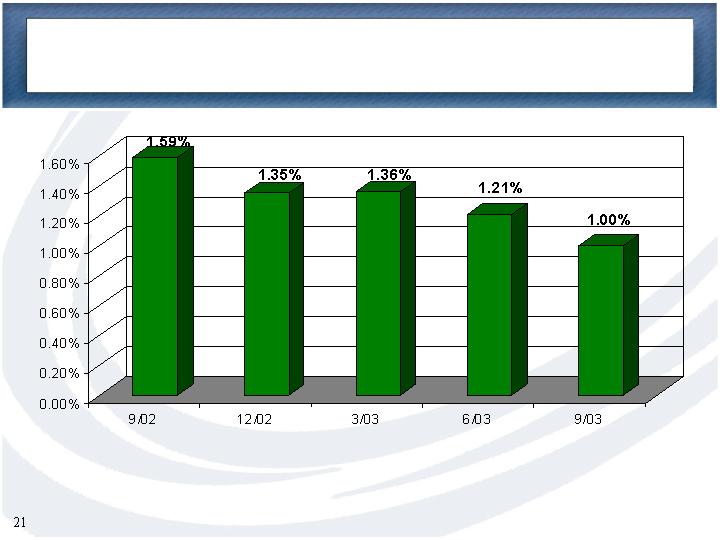

Net Interest Margin

($ in millions)

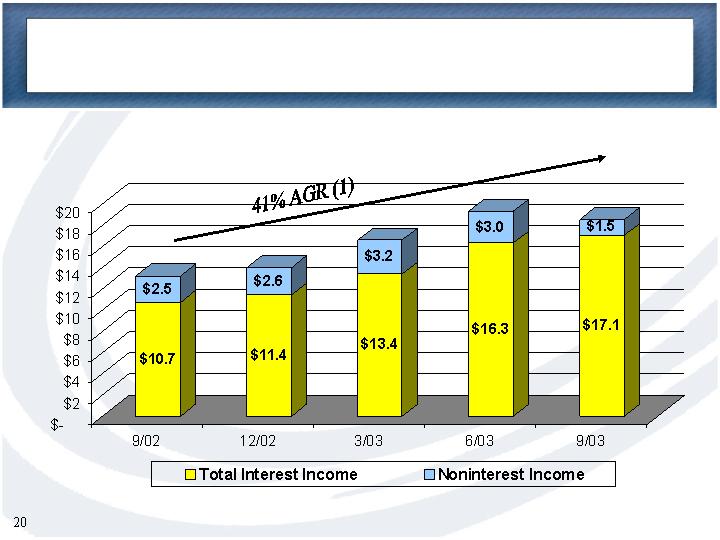

Net Interest Income

(1) AGR – Annual Growth Rate: 9/02 to 9/03

Noninterest Income to Total Revenue

Total Revenue Composition

($ in millions)

(1) AGR – Annual Growth Rate: 9/02 to 9/03

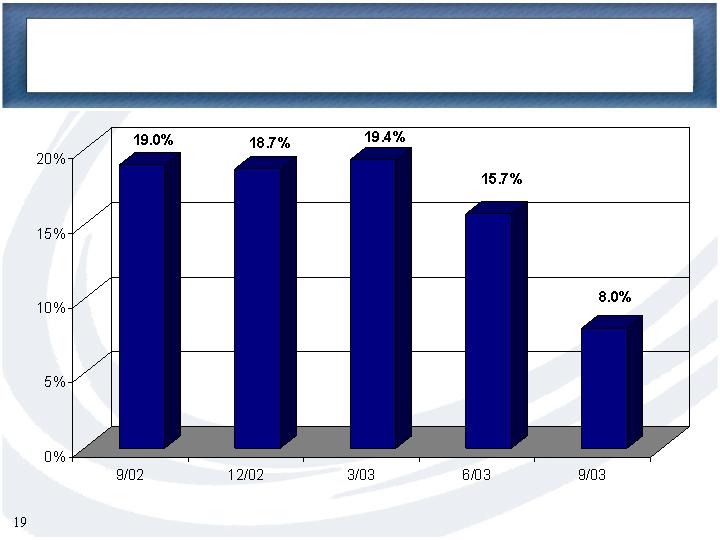

G&A to Average Assets

Efficiency Ratio

Return on Average Assets

Return on Average Equity

($ in millions)

Quarterly Net Income

(1) AGR – Annual Growth Rate: 9/02 to 9/03

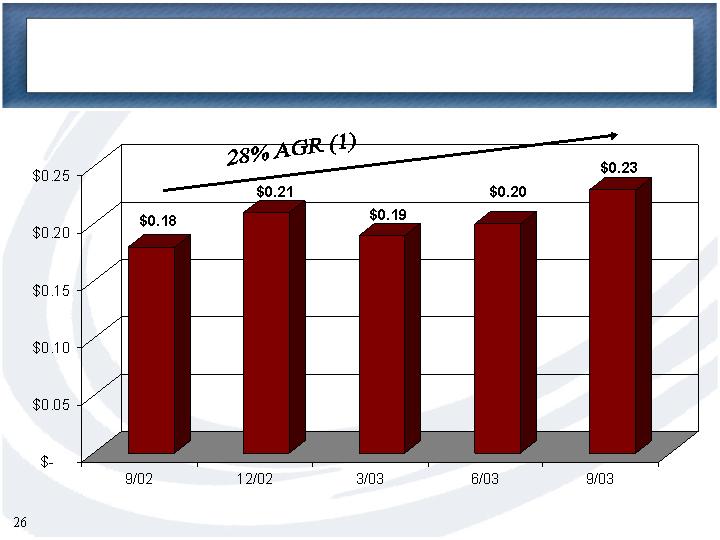

Diluted Earnings per Share

(1) AGR – Annual Growth Rate: 9/02 to 9/03

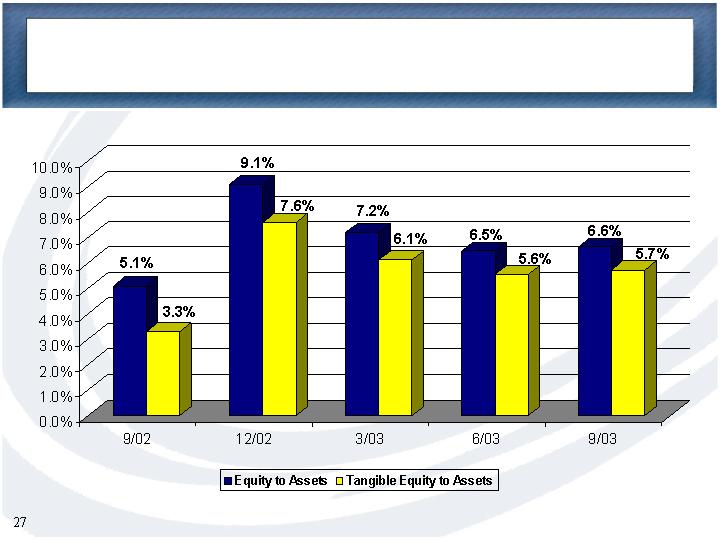

Consolidated Capital Ratios

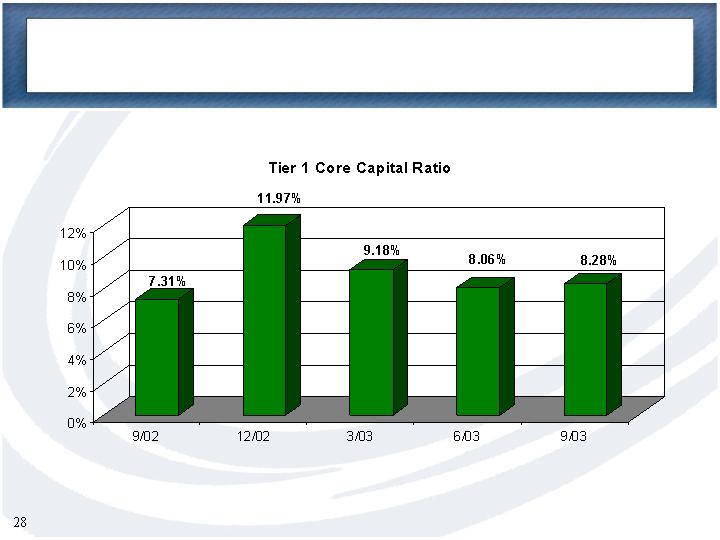

Bank Capital Ratio

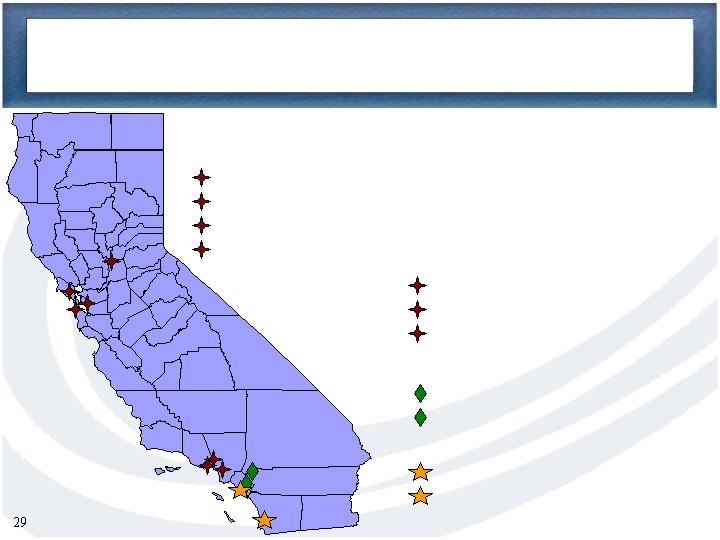

Growing Franchise Presence

Northern California

Loan Offices

Sacramento

Corte Madera (Marin County)

Burlingame

Oakland

Southern California

Loan Offices

Woodland Hills

Encino (Opened Aug. ’03)

West Los Angeles

Banking Offices

Rancho Santa Margarita

Riverside

Banking & Loan Offices

Irvine (Headquarters)

La Jolla (Opened Sept. ’03)

CCB was the fastest growing bank in California over

the 36 months ended 6/30/03, (source www.fdic.gov).

4th largest multi-family originator in CA with 2.7%

market share for the 12 months ended 6/30/03, (source:

Dataquick Information Systems).

Consistent High Quality Growth