April 26, 2004

First Quarter 2004 Earnings Call

This presentation may include forward-looking statements related to the plans, beliefs

and goals of the Company, its subsidiaries, which involve certain risks and

uncertainties that could cause actual results to differ materially from those in the

forward-looking statements. Such risks and uncertainties include, but are not limited

to, the following factors: competitive pressure in the banking industry; changes in the

interest rate environment; the health of the economy, either nationally or regionally;

the deterioration of credit quality, which would cause an increase in the provision for

possible loan and lease losses; changes in the regulatory environment; changes in

business conditions, particularly in California real estate; volatility of rate sensitive

deposits; asset/liability matching risks and liquidity risks; changes in the securities

markets. The Company undertakes no obligation to revise or publicly release any

revision to these forward-looking statements.

Regulation FD

2

CCBI Highlights

3

Financial Position

March 31, 2004

Total Assets

$1.96 billion

Loans Held for Investment

$1.20 billion

Deposits

$736 million

Equity

$114 million

Tangible Equity

$101 million

Quarter Ended

Quarter Ended

Financial Results

3/31/2004

3/31/2003

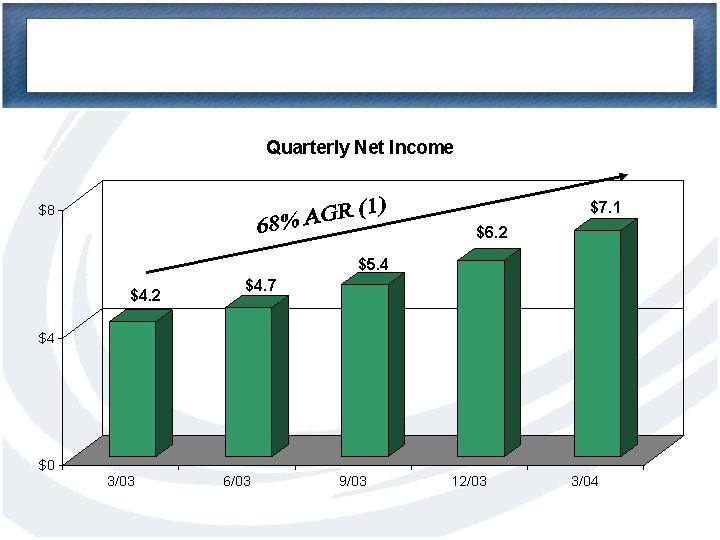

Net Income

$7.1 million

$4.2 million

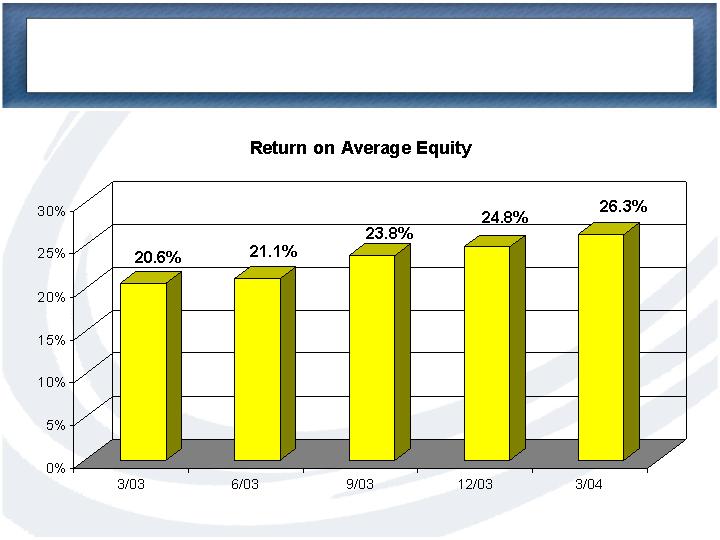

Return on Average Equity

26.30%

20.60%

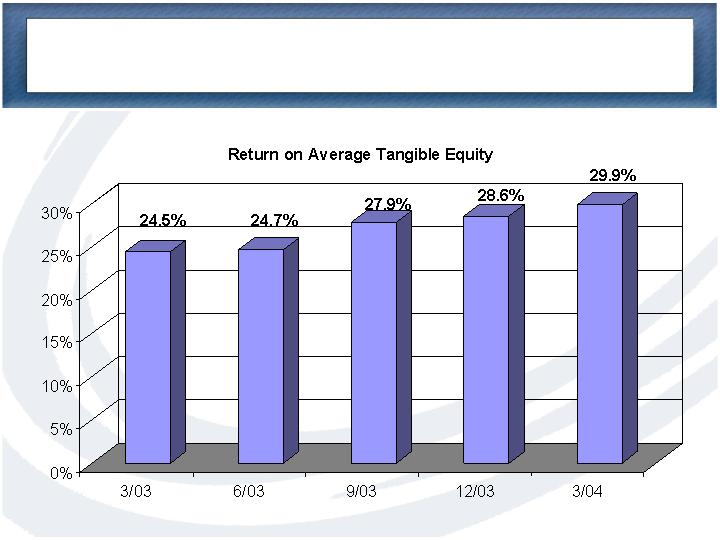

Return on Avg.Tang. Equity

29.91%

24.48%

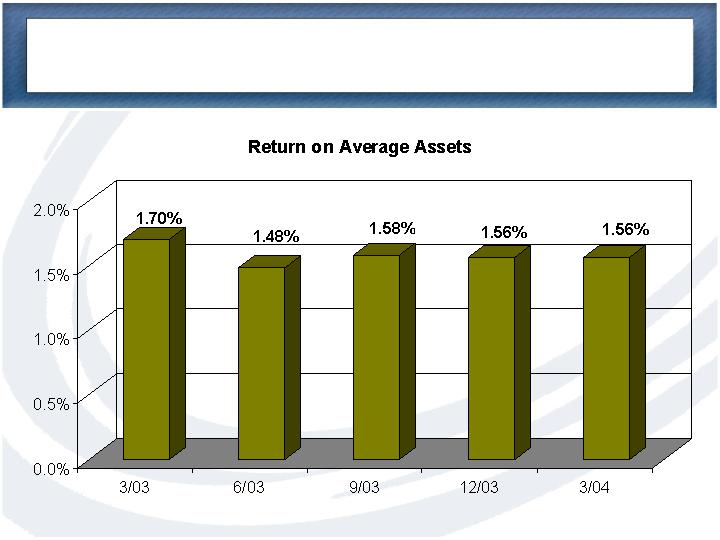

Return on Average Assets

1.56%

1.70%

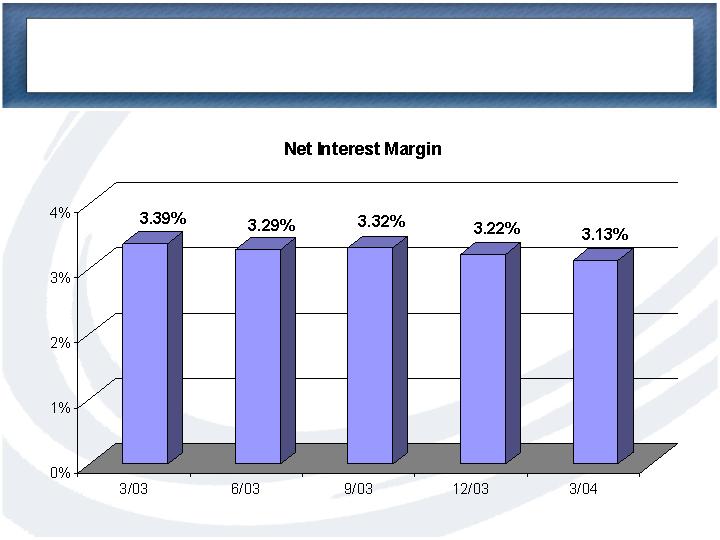

Net Interest Margin

3.13%

3.39%

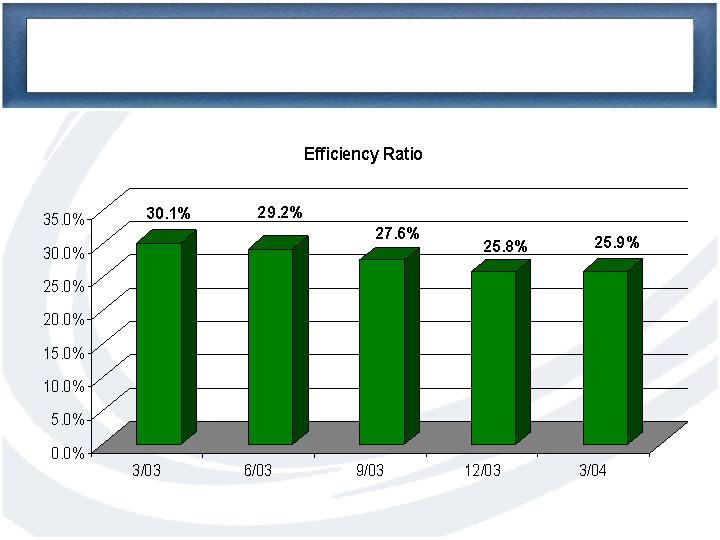

Efficiency Ratio

25.86%

30.08%

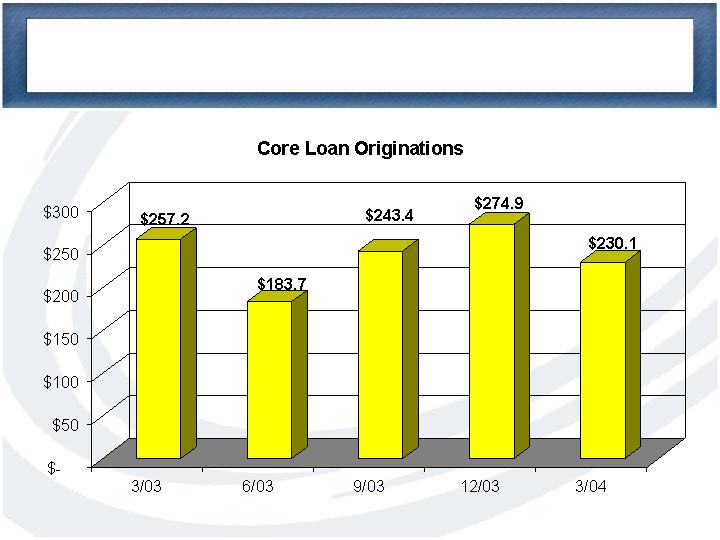

Total Loan Originations

$259 million

$267 million

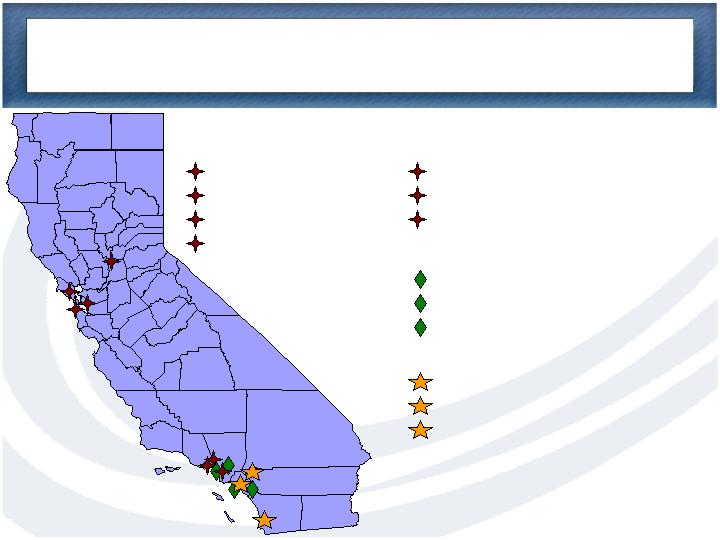

CCBI’s Growing Franchise Presence

Northern California

Loan Offices

Sacramento

Corte Madera

Burlingame

Oakland

Southern California

Loan Offices

Woodland Hills

Encino

West Los Angeles

Banking Offices

Rancho Santa Margarita

Beverly Hills (Summer 2004)

Newport Coast (2005)

Banking & Loan Offices

Irvine (Headquarters)

La Jolla

Riverside

4

Asset Quality of Multi-family Loans

Noncurrent Loans/

Nationwide

Total Loans

(1)

Multi-family

0.13%

Single family

0.84%

Commercial Real Estate

0.87%

Construction and Land Loans

0.85%

Business Loans

1.21%

Consumer

0.87%

Multi-family Loans

CCBI

0.00%

Western Region Thrifts

0.05%

Nationwide Thrifts

0.13%

(1) Based upon 12/31/03 Thrift Financial Reports for nationwide savings institutions

5

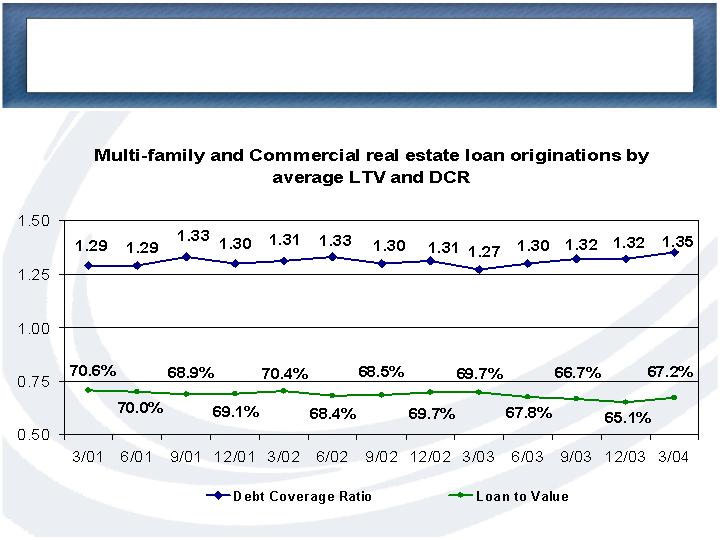

LTV and DCR of March 31, 2004 Portfolio

6

Multi-Family

Loan to Value

68%

Debt Coverage Ratio

1.29:1

Commercial RE

Loan to Value

65%

Debt Coverage Ratio

1.47:1

Values are weighted average ratios, at origination

Consistent Underwriting

7

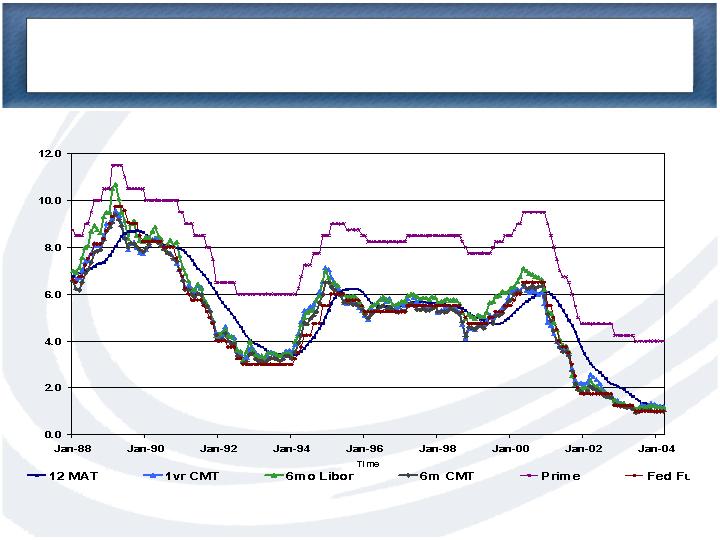

Interest Rate Comparison

(Interest Rate, in percent)

CCBI’s loan rates adjust based on 12MAT, 1yr CMT, 6mo LIBOR, 6mo CMT and Prime, plus a margin

8

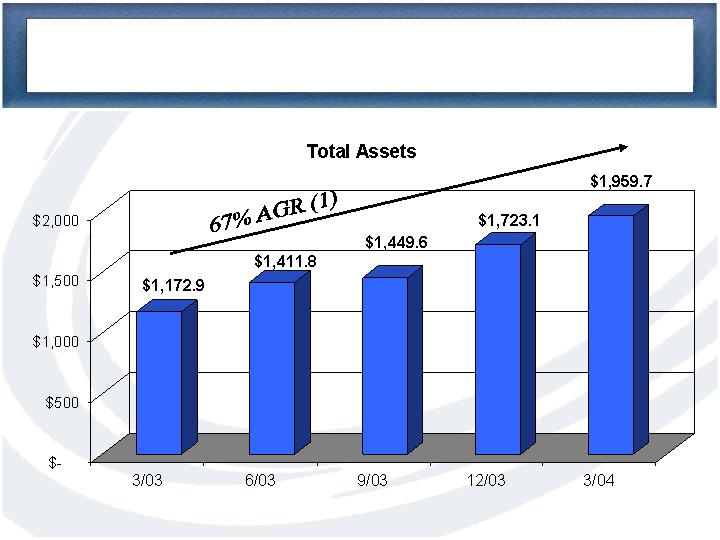

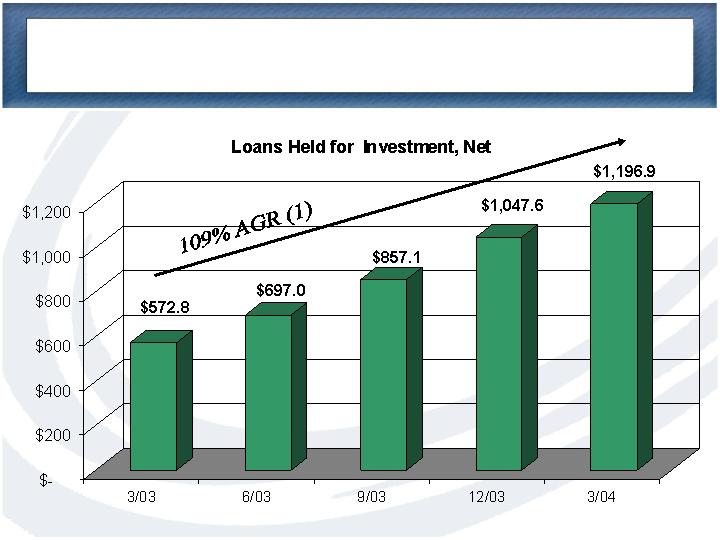

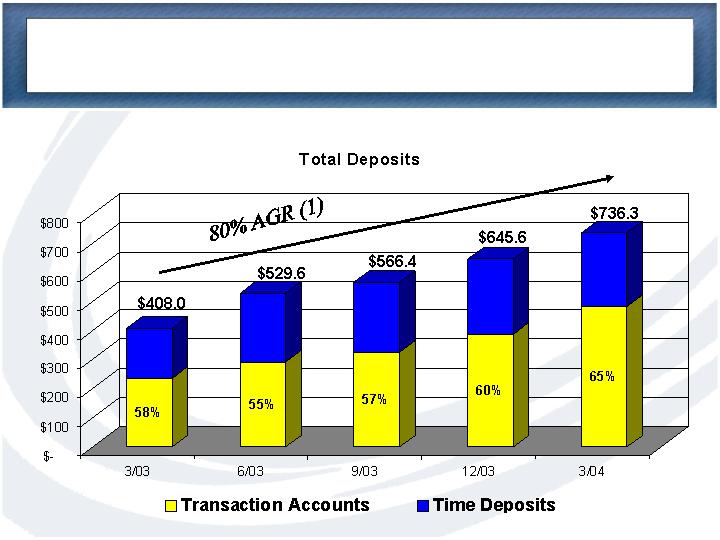

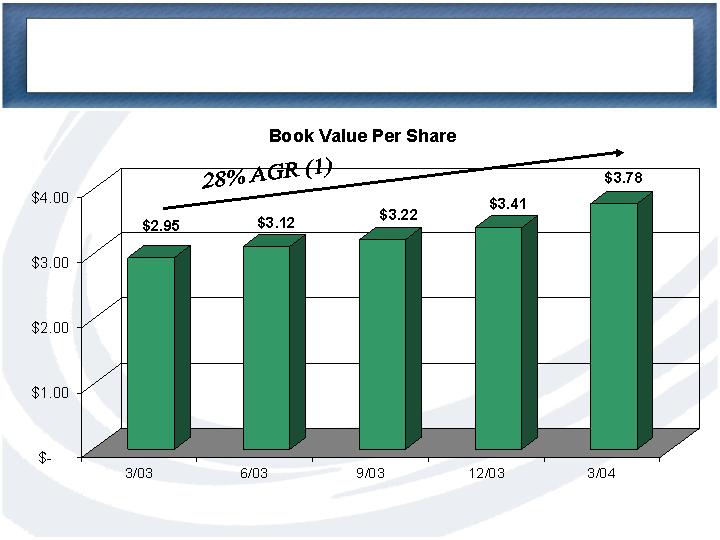

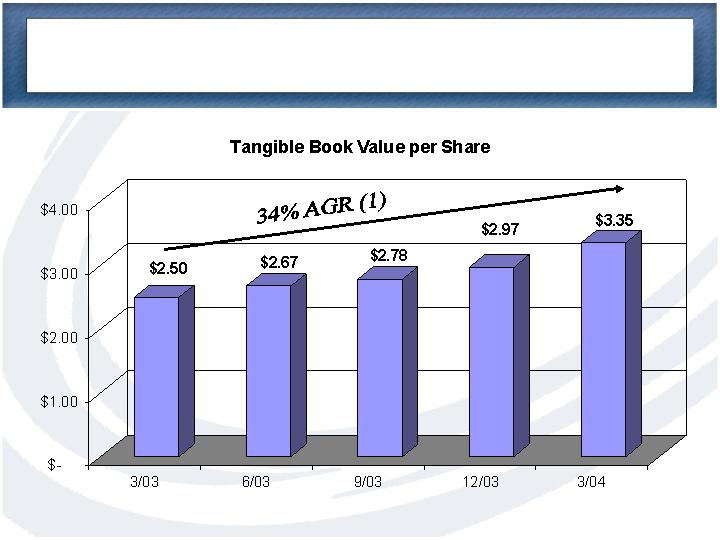

(1) AGR – Annual Growth Rate: 3/03 to 3/04

($ in millions)

Balance Sheet Growth

9

Balance Sheet Growth Generated Internally

($ in millions)

10

Historic Driver of Balance Sheet Growth

11

($ in millions)

Balance Sheet Growth

(1) AGR – Annual Growth Rate: 3/03 to 3/04

12

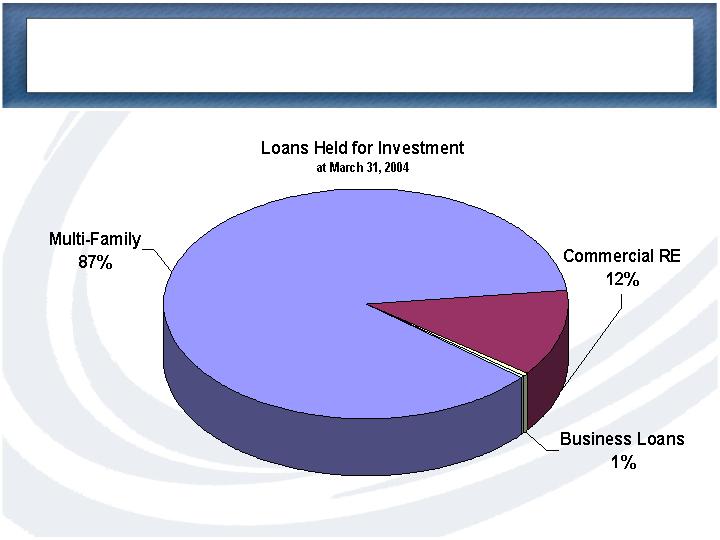

Loan Portfolio Mix

13

($ in millions)

Funding Asset Growth

(1) AGR – Annual Growth Rate: 3/03 to 3/04

14

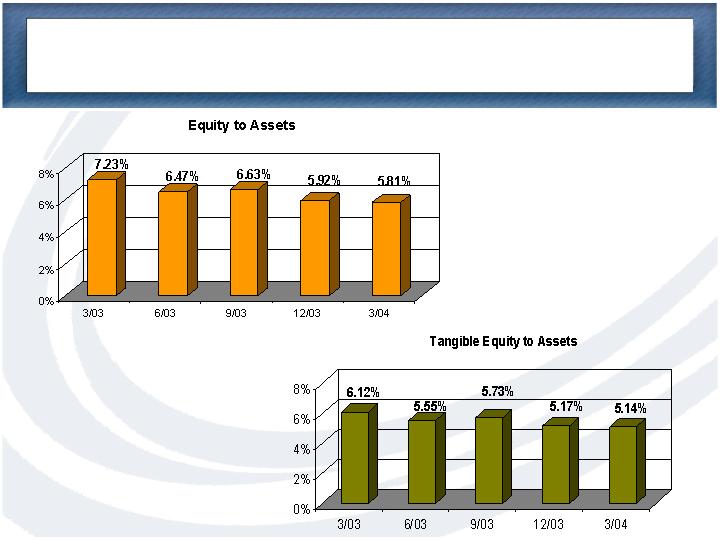

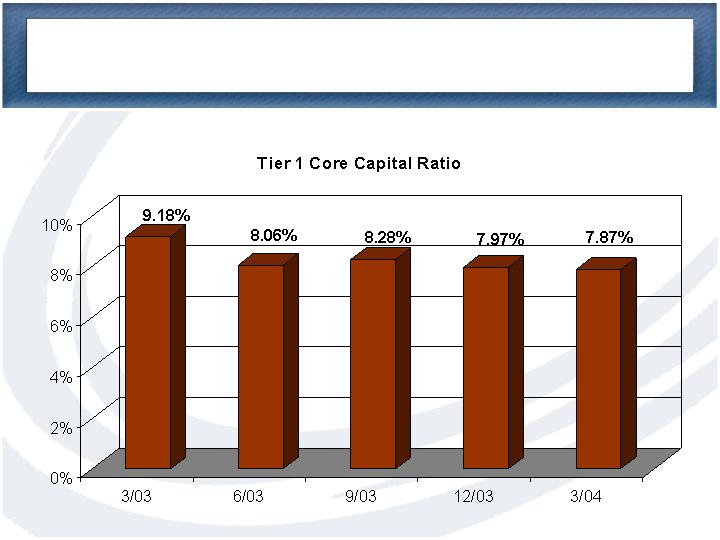

Capital Ratios

15

Bank Capital Ratio

16

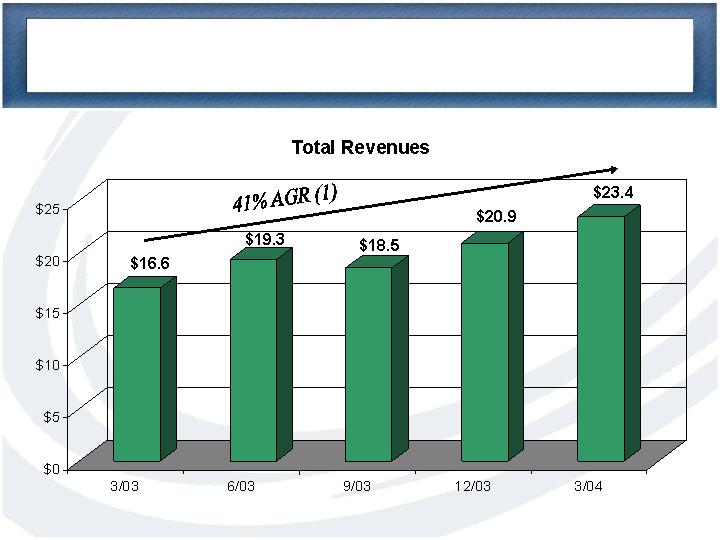

Operating Performance

($ in millions)

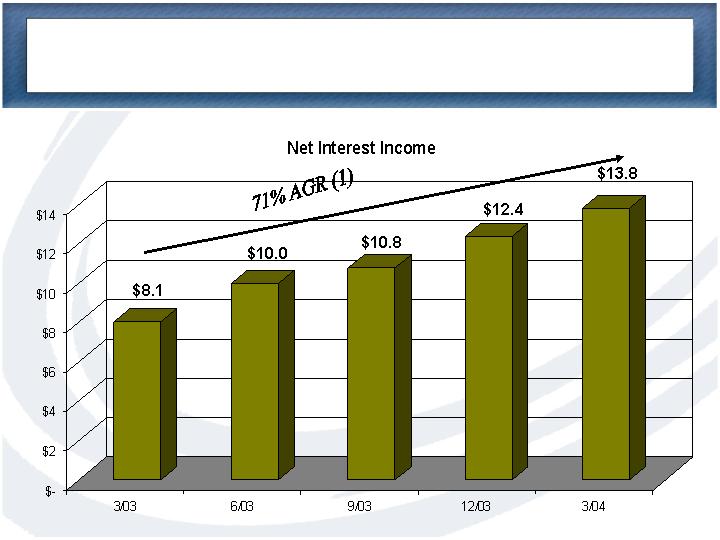

(1) AGR – Annual Growth Rate: 3/03 to 3/04

17

($ in millions)

Operating Performance

(1) AGR – Annual Growth Rate: 3/03 to 3/04

18

Operating Performance

19

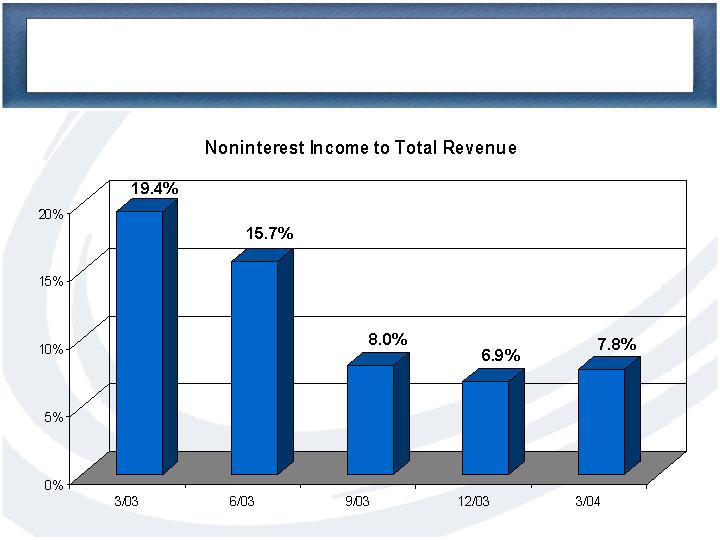

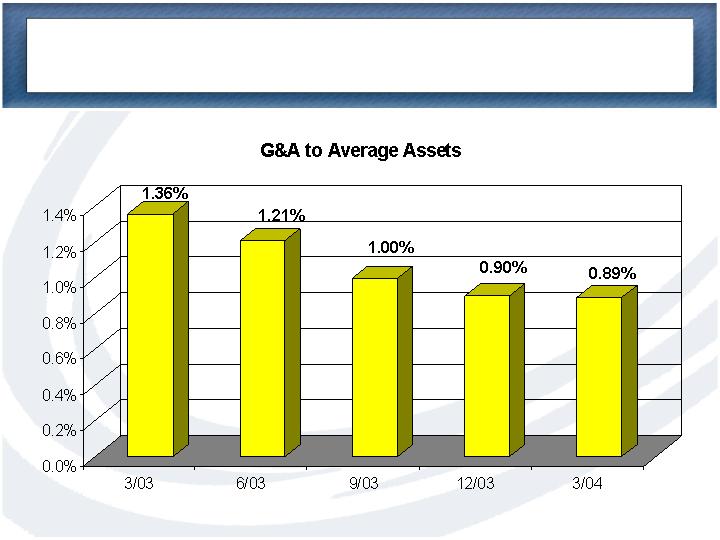

Operating Performance Ratios

20

Operating Performance Ratios

21

($ in millions)

Earnings Performance

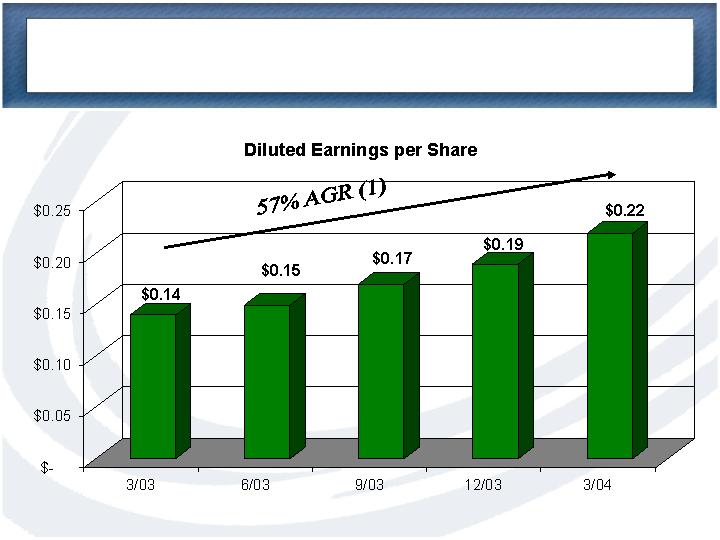

(1) AGR – Annual Growth Rate: 3/03 to 3/04.

22

Operating Performance

23

Profitability Ratios

24

Profitability Ratios

25

Profitability Ratios

26

Profitability Ratios

(1) AGR – Annual Growth Rate: 3/03 to 3/04.

27

Profitability Ratios

(1) AGR – Annual Growth Rate: 3/03 to 3/04.

28

Earnings Performance

(1) AGR – Annual Growth Rate: 3/03 to 3/04.

29

CCB was the fastest growing savings institution in

California over the 36 months ended 12/31/03, (source

www.fdic.gov).

3rd largest multi-family originator in CA with 2.9%

market share for the 12 months ended 12/31/03, (source:

Dataquick Information Systems).

Leading Loan Originator & High Growth Bank

30

NASDAQ: “CCBI”

April 26, 2004