FORM 6 - K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Pursuant to Rule 13a - 16 or 15d - 16 of

the Securities Exchange Act of 1934

As of April 27, 2010

TENARIS, S.A.

(Translation of Registrant's name into English)

TENARIS, S.A.

46a, Avenue John F. Kennedy

L-1855 Luxembourg

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or 40-F.

Form 20-F ü Form 40-F

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12G3-2(b) under the Securities Exchange Act of 1934.

Yes __ No ü

If “Yes” is marked, indicate below the file number assigned to the registrant in connection

with Rule 12g3-2(b): 82-

The attached material is being furnished to the Securities and Exchange Commission pursuant to Rule 13a-16 and Form 6-K under the Securities Exchange Act of 1934, as amended. This report contains Tenaris' notice of Annual General Meeting of Shareholders and the Shareholder Meeting Brochure and Proxy Statement and the Company’s 2009 annual report (which includes the Company’s consolidated financial statements for the years ended December 31, 2009, 2008 and 2007 and the Company’s annual accounts as at December 31, 2009, together with the independent auditors’ reports and the Board of Directors’ management report and certification).

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

Date: April 27, 2010

Tenaris, S.A.

By: /s/ Cecilia Bilesio

Cecilia Bilesio

Corporate Secretary

Dear Tenaris Shareholder and ADR Holder,

I am pleased to invite you to attend the Annual General Meeting of Shareholders of the Company. The meeting will be held on Wednesday, June 2, 2010, at 46A, Avenue John F. Kennedy L-1855 Luxembourg and will begin promptly at 11:00 a.m. (Central European Time).

At the Annual General Meeting, you will have the opportunity to hear a report on the Company’s business, financial condition and results of operation and to vote on various matters, including the approval of the Company’s consolidated financial statements, the election of the members of the Board of Directors and the appointment of the independent auditors.

The Notice and Agenda for the meeting, the Shareholder Meeting Brochure and Proxy Statement and the Company’s 2009 annual report (which includes the Company’s consolidated financial statements for the years ended December 31, 2009, 2008 and 2007, and the Company’s annual accounts as at December 31, 2009, together with the independent auditors’ reports and the Board of Directors’ management report and certifications), are available free of charge at the Company's registered office in Luxembourg and on our website at www.tenaris.com/investors. They may also be obtained upon request, by calling (352) 26-47-89-78 (if you are in Luxembourg), 1-800-555-2470 (if you are in the United States), or +1-267-468-0786 (if you are in any other jurisdiction).

Even if you only own a few shares or ADRs, I hope that you will exercise your right to vote at the meeting. You can vote your shares personally or by proxy. If you choose to vote by proxy, you may use the enclosed dedicated proxy form. If you are a holder of ADRs, please see the letter from THE BANK OF NEW YORK MELLON, depositary bank, for instructions on how to exercise your vote by proxy.

Yours sincerely,

Paolo Rocca

Chairman and Chief Executive Officer

April 23, 2010

Re: TENARIS S.A.

| To: | Registered Holders of American Depositary Receipts (“ADRs”) |

| for ordinary shares, US$1 Par Value (the “Shares”), of |

| Tenaris S.A. (the “Company”): |

The Company has announced that its Annual General Meeting of Shareholders (the “Meeting”) will be held on June 2, 2010, at 11:00 a.m. (Central European Time). The Meeting will take place at 46A, Avenue John F. Kennedy L-1855 Luxembourg. A copy of the Company’s Notice of Annual General Meeting of Shareholders, including the agenda for the Meeting, is enclosed.

The Notice of Annual General Meeting of Shareholders, the Shareholder Meeting Brochure and Proxy Statement, and the Company’s 2009 annual report (which includes the Company’s consolidated financial statements for the years ended December 31, 2009, 2008 and 2007, and the Company’s annual accounts as at December 31, 2009, together with the independent auditors’ reports and the Board of Directors’ management report and certifications), are available on the Company’s website at www.tenaris.com/investors and may also be obtained upon request, by calling 1-800-555-2470 (if you are in the United States) or +1-267-468-0786 (if you are outside the United States). These materials are provided to allow the Shares represented by your ADRs to be voted at the Meeting.

Each holder of ADRs as of each of April 23, 2010, and May 17, 2010, is entitled to instruct THE BANK OF NEW YORK MELLON, as Depositary (the “Depositary”), as to the exercise of the voting rights pertaining to the Shares represented by such holder’s ADRs. Although voting instructions are sent to ADR holders and proxy materials are available on the Company’s website beginning on April 23, 2010, only those holders of record at each of April 23, 2010, and May 17, 2010, will be entitled to provide the Depositary with voting instructions. Notwithstanding that holders of ADRs must have held ADRs on each such date, in order to avoid the possibility of double vote, only those positions on May 17, 2010, will be counted for voting instruction purposes. Eligible ADR holders who desire to give voting instructions with respect to their Shares represented by their ADRs must complete, date and sign a proxy form and return it to the Depositary at THE BANK OF NEW YORK MELLON, Proxy Processing P.O. Box 3549, S. Hackensack, NJ 07606-9249, U.S.A. If the Depositary receives properly completed instructions by 5:00 p.m., New York City time, on May 27, 2010, then it shall vote, or cause to be voted, the Shares represented by such ADRs in the manner prescribed by the instructions. However, if by 5:00 p.m., New York time, on May 27, 2010, the Depositary receives no instructions from the holder of ADRs, or the instructions received by the Depositary are not in proper form, then the Depositary shall deem such ADR holder to have instructed the Depositary to vote the Shares represented by any such ADRs in favor of any proposals or recommendations of the Company, for which purposes the Depositary shall issue a proxy to a person appointed by the Company to vote such Shares represented by such ADRs in favor of any proposals or recommendations of the Company (including any recommendation by the Company to vote such Shares represented by such ADRs on any given issue in accordance with the majority shareholder vote on that issue). No proxy shall be given, and no instruction shall be deemed given, with respect to any matter as to which the Company informs the Depositary that (i) it does not wish such proxy given, (ii) it has knowledge that substantial opposition exists with respect to the action to be taken at the Meeting, or (iii) the matter materially and adversely effects the rights of the holders of ADRs.

Any holder of ADRs entitled to provide the Depositary with voting instructions in respect of the Shares represented by its ADRs, is also entitled to revoke any instructions which it has previously given to the Depositary by filing with the Depositary a written revocation or duly executed instructions bearing a later date at any time prior to 5:00 p.m., New York time, on May 27, 2010. No instructions, revocations or revisions thereof shall be accepted by the Depositary after that time.

IF YOU WANT YOUR VOTE TO BE COUNTED, THE DEPOSITARY MUST RECEIVE YOUR VOTING INSTRUCTIONS PRIOR TO 5:00 P.M. (NEW YORK CITY TIME) ON MAY 27, 2010.

THE BANK OF NEW YORK MELLON

Depositary

April 23, 2010

New York, New York

Tenaris S.A.

Société Anonyme Holding

46A, avenue John F. Kennedy

L-1855, Luxembourg

RCS Luxembourg B 85 203

Notice of the Annual General Meeting of Shareholders to be held on June 2, 2010

Notice is hereby given to holders of ordinary shares (the “Shares”) of Tenaris S.A. (the “Company”) that the Annual General Meeting of Shareholders (the “Meeting”) will be held on June 2, 2010, at 11:00 a.m. (Central European Time). The Meeting will be held at 46A, avenue John F. Kennedy L-1855 Luxembourg. In the Meeting, shareholders will vote with respect to the items listed below under the heading “Annual General Meeting of Shareholders”.

Agenda

Annual General Meeting of Shareholders

| 1. | Consideration of the Board of Directors’ management report and certifications and the independent auditors’ reports on the Company’s consolidated financial statements for the years ended December 31, 2009, 2008 and 2007, and the Company’s annual accounts as at December 31, 2009. |

| 2. | Approval of the Company’s consolidated financial statements for the years ended December 31, 2009, 2008 and 2007. |

| 3. | Approval of the Company’s annual accounts as at December 31, 2009. |

| 4. | Allocation of results and approval of dividend payment for the year ended December 31, 2009. |

| 5. | Discharge of the members of the Board of Directors for the exercise of their mandate during the year ended December 31, 2009. |

| 6. | Election of members of the Board of Directors. |

| 7. | Compensation of members of the Board of Directors. |

| 8. | Appointment of the independent auditors for the fiscal year ending December 31, 2010 and approval of their fees. |

| 9. | Authorisation to the Company, or any subsidiary, to from time to time purchase, acquire or receive shares of the Company, in accordance with Article 49-2 of the Luxembourg law of 10 August 1915 and with applicable laws and regulations. |

| 10. | Authorisation to the Board of Directors to cause the distribution of all shareholder communications, including its shareholder meeting and proxy materials and annual reports to shareholders, by such electronic means as is permitted by any applicable laws or regulations. |

Pursuant to the Company’s Articles of Association, resolutions at the Meeting will be passed by a simple majority of the votes cast, irrespective of the number of Shares present or represented.

Procedures for Attending the Meeting

Any shareholder registered in the Company’s share register on May 28, 2010 (the “Record Date”) shall be admitted to the Meeting and may attend the Meeting in person.

Any shareholder registered in the Company’s share register on the Record Date may also vote by proxy. To vote by proxy, holders of Shares must file a completed proxy form not later than 4:00 p.m. (local time) on the Record Date at any of the addresses indicated below or, in the case of Shares held in Mexico, with S.D. Indeval, S.A. de C.V. (Paseo de la Reforma #255, 2o. y 3er. piso Col. Cuauhtémoc, Mexico City).

Holders of Shares holding their Shares through fungible securities accounts wishing to attend the Meeting in person must present a certificate (issued by the financial institution or professional depositary holding such Shares) evidencing deposit of their Shares and certifying the number of Shares recorded in the relevant account as of the Record Date. Certificates certifying the number of Shares recorded in the relevant account as of a date other than the Record Date will not be accepted and such shareholders will not be admitted to the Meeting. Each certificate must (i) indicate the stock exchange on which the Shares evidenced by such certificate trade, and (ii) in case of certificates evidencing Shares trading on the Argentine or Italian stock exchanges, certify that such Shares have been blocked for trading until the date of the Meeting. Certificates must be filed not later than 4:00 p.m. (local time) on the Record Date, at any of the addresses indicated below or, in the case of Shares held through fungible securities accounts in Mexico, with S.D. Indeval, S.A. de C.V. (Paseo de la Reforma #255, 2o. y 3er. piso Col. Cuauhtémoc, Mexico City).

Holders of Shares holding their Shares through fungible securities accounts may also vote by proxy. To do so, holders of Shares must present a certificate (issued by the financial institution or professional depositary holding such Shares) evidencing deposit of their Shares and certifying the number of Shares recorded in the relevant account as of the Record Date. Certificates certifying the number of Shares recorded in the relevant account as of a date other than the Record Date will not be accepted and such shareholders will not be admitted to the Meeting. Each certificate must (i) indicate the stock exchange on which the Shares evidenced by such certificate trade, and (ii) in case of certificates evidencing Shares trading on the Argentine or Italian stock exchanges, certify that such Shares have been blocked for trading until the date of the Meeting. In addition, such holders of Shares wishing to vote by proxy must also present a completed proxy form. Such certificate and proxy form must be filed not later than 4:00 p.m. (local time) on the Record Date, at any of the addresses indicated below and, in the case of Shares held through fungible securities accounts in Mexico, with S.D. Indeval, S.A. de C.V. (Paseo de la Reforma #255, 2o. y 3er. piso Col. Cuauhtémoc, Mexico City).

In the event of Shares owned by a corporation or any other legal entity, individuals representing such entity who wish to attend the Meeting in person and vote at the Meeting on behalf of such entity, must present evidence of their authority to attend, and vote at, the Meeting by means of a proper document (such as a general or special power-of-attorney) issued by the respective entity. A copy of such power of attorney or other proper document must be filed not later than 4:00 p.m. (local time) on the Record Date, at any of the addresses indicated below. The original documentation evidencing the authority to attend, and vote at, the Meeting, or a notarized and legalized copy thereof, must be presented at the Meeting.

Luxembourg: 46A, Avenue John F. Kennedy

L-1855 Luxembourg

Attn: Adélia Soares

Argentina: c/o Siderca S.A.I.C.

Carlos María della Paolera 299, piso 16°

(C1001ADA) Buenos Aires

Attn: Horacio de las Carreras and/or Eleonora Cimino

Italy: c/o Dalmine S.p.A.

Piazza Caduti 6 luglio 1944 n. 1 24044

Dalmine (BG)

Attn: Marco Tajana and/or Teresa Gaini

Mexico: c/o Tubos de Acero de México, S.A.

Campos Elíseos 400-17

Col. Chapultepec Polanco

11560 México D.F.

Attn: Félix Todd and/or Cecilia Pérez Valencia

Those shareholders who have sold their Shares between the Record Date and the date of the Meeting cannot attend the Meeting or vote by proxy. In case of breach of such prohibition, criminal sanctions may apply.

Holders of American Depositary Receipts (“ADRs”) as of each of April 23, 2010, and May 17, 2010, are entitled to instruct THE BANK OF NEW YORK MELLON, as Depositary (the “Depositary”), as to the exercise of the voting rights pertaining to the Company’s Shares represented by such holder’s ADRs. Although voting instructions are sent to holders and proxy materials are available on the Company’s website beginning on April 23, 2010, only those holders of record as of each of April 23, 2010 and May 17, 2010, will be entitled to provide the Depositary with voting instructions. Notwithstanding that holders of ADRs must have held ADRs on each such date, in order to avoid the possibility of double vote, only those positions on May 17, 2010, will be counted for voting instruction purposes. Eligible ADR holders who desire to give voting instructions with respect of the Shares represented by their ADRs must complete, date and sign a proxy form and return it to the Depositary, at THE BANK OF NEW YORK MELLON, Proxy Processing P.O. Box 3549, S. Hackensack, NJ 07606-9249, U.S.A., by 5:00 p.m., New York City time, on May 27, 2010.

Under Luxembourg legislation implementing the EU Transparency Directive, investors in the Company’s securities should notify the Company and the Luxembourg Commission de Surveillance du Secteur Financier (CSSF) on an ongoing basis whenever their direct or indirect ownership or other control rights over shares of the Company’s capital or rights to vote such shares either reaches, exceeds or falls below any of the following thresholds: 5%, 10%, 15%, 20%, 25%, 33.33%, 50% and 66.66%. The total number of issued and outstanding shares and votes set forth in the second paragraph of the Shareholder Meeting Brochure and Proxy Statement should be used for purposes of determining whether an investor reaches or exceeds each such threshold. Any such notification shall be made as indicated in the Company’s website at www.tenaris.com/investors and in accordance with CSSF regulations. Failure to make such notification will cause the suspension of the exercise of voting rights relating to the shares exceeding the fraction that should have been notified.

The Shareholder Meeting Brochure and Proxy Statement (which contains reports on each item of the agenda for the Meeting, and further details on voting procedures) and the forms furnished by the Company in connection with the Meeting, may be obtained at any of the addresses indicated above or upon request by calling (352) 26-47-89-78 (if you are in Luxembourg), 1-800-555-2470 (if you are in the United States), or +1-267-468-0786 (if you are in any other jurisdiction), but also from the Depositary, Borsa Italiana SpA (Piazza degli Affari 6, 20123, Milan, Italy) and S.D. Indeval S.A. de C.V., as from April 23, 2010, between 10:00 a.m. and 5:00 p.m. (local time).

Copies of the Shareholder Meeting Brochure and Proxy Statement and the forms are also available at www.tenaris.com/investors. Copies of the Company’s 2009 annual report (including the Company’s consolidated financial statements for the years ended December 31, 2009, 2008 and 2007, and the Company’s annual accounts as at December 31, 2009, together with the independent auditors’ reports and management report and certifications, and the documents referred to in the preceding sentence) may also be obtained free of charge at the Company's registered office in Luxembourg or upon request by calling (352) 26-47-89-78 (if you are in Luxembourg), 1-800-555-2470 (if you are in the United States), or +1-267-468-0786 (if you are in any other jurisdiction).

Cecilia Bilesio

Secretary to the Board of Directors

April 23, 2010

Luxembourg

Tenaris S.A.

Société Anonyme Holding

46A, avenue John F. Kennedy

L-1855, Luxembourg

RCS Luxembourg B 85 203

Shareholder Meeting Brochure and Proxy Statement

Annual General Meeting of Shareholders to be held on June 2, 2010

This Shareholder Meeting Brochure and Proxy Statement is furnished by Tenaris S.A. (the “Company”) in connection with the Annual General Meeting of Shareholders (the “Meeting”) to be held, for the purposes set forth in the accompanying Notice of the Annual General Meeting of Shareholders (the “Notice”), on June 2, 2010, starting at 11:00 a.m., at 46A, avenue John F. Kennedy L-1855 Luxembourg.

As of April 23, 2010, there were issued and outstanding 1,180,536,830 ordinary shares, US$1 par value each, of the Company (the “Shares”), including the Shares (the “Deposited Shares”) deposited with various agents for THE BANK OF NEW YORK MELLON, as depositary (the “Depositary”), under the Amended and Restated Deposit Agreement, dated as of February 28, 2008 (the “Deposit Agreement”), among the Company, the Depositary and all holders from time to time of American Depositary Receipts (the “ADRs”) issued thereunder. The Deposited Shares are represented by American Depositary Shares, which are evidenced by the ADRs (one ADR equals two Deposited Shares). Each Share entitles the holder thereof to one vote at the Meeting.

Any shareholder registered in the Company’s share register on May 28, 2010 (the “Record Date”) shall be admitted to the Meeting and may attend the Meeting in person. Any shareholder registered in the Company’s share register on the Record Date may also vote by proxy. To vote by proxy, holders of Shares must file a completed proxy form not later than 4:00 p.m. (local time) on the Record Date at any of the addresses indicated in the Notice.

Holders of Shares holding their Shares through fungible securities accounts wishing to attend the Meeting in person must present a certificate (issued by the financial institution or professional depositary holding such Shares) evidencing deposit of their Shares and certifying the number of Shares recorded in the relevant account as of the Record Date. Certificates certifying the number of Shares recorded in the relevant account as of a date other than the Record Date will not be accepted and such shareholders will not be admitted to the Meeting. Each certificate must (i) indicate the stock exchange on which the Shares evidenced by such certificate trade, and (ii) in case of certificates evidencing Shares trading on the Argentine or Italian stock exchanges, certify that such Shares have been blocked for trading until the date of the Meeting. Certificates must be filed not later than 4:00 p.m. (local time) on the Record Date, at any of the addresses indicated in the Notice.

Holders of Shares holding their Shares through fungible securities accounts may also vote by proxy. To do so, such holders of Shares must present a certificate (issued by the financial institution or professional depositary holding such Shares) evidencing deposit of their Shares and certifying the number of Shares recorded in the relevant account as of the Record Date. Certificates certifying the number of Shares recorded in the relevant account as of a date other than the Record Date will not be accepted and such shareholders will not be admitted to the Meeting. Each certificate must (i) indicate the stock exchange on which the Shares evidenced by such certificate trade, and (ii) in case of certificates evidencing Shares trading on the Argentine or Italian stock exchanges, certify that such Shares have been blocked for trading until the date of the Meeting. In addition, such holders of Shares must also present a completed proxy form. Such certificate and proxy form must be filed not later than 4:00 p.m. (local time) on the Record Date, at any of the addresses indicated in the Notice.

In the event of Shares owned by a corporation or any other legal entity, individuals representing such entity who wish to attend the Meeting in person and vote at the Meeting on behalf of such entity, must present evidence of their authority to attend, and vote at, the Meeting by means of a proper document (such as a general or special power-of-attorney) issued by the respective entity. A copy of such power of attorney or other proper document must be filed not later than 4:00 p.m. (local time) on the Record Date, at any of the addresses indicated in the Notice. The original documentation evidencing the authority to attend, and vote at, the Meeting, or a notarized and legalized copy thereof, must be presented at the Meeting.

Each holder of ADRs as of each of April 23, 2010, and May 17, 2010, is entitled to instruct the Depositary, as to the exercise of the voting rights pertaining to the Shares represented by such holder’s ADRs. Although voting instructions are sent to holders and proxy materials are available at the Company’s website beginning on April 23, 2010, only those holders of record as of each of April 23, 2010 and May 17, 2010, will be entitled to provide the Depositary with voting instructions. Notwithstanding that holders of ADRs must have held ADRs on each such date, in order to avoid the possibility of double vote, only those positions on May 17, 2010, will be counted for voting instruction purposes. Eligible holders of ADRs who wish to give voting instructions in respect of the Shares represented by their ADRs must complete, date and sign a proxy form and return it to the Depositary, at THE BANK OF NEW YORK MELLON, Proxy Processing P.O. Box 3549, S. Hackensack, NJ 07606-9249, U.S.A. If the Depositary receives properly completed instructions by 5:00 p.m., New York City time, on May 27, 2010, then it shall vote or cause to be voted the Shares underlying such ADRs in the manner prescribed by the instructions. However, if by 5:00 p.m., New York time, on May 27, 2010, the Depositary receives no instructions from the holder of ADRs, or the instructions are not in proper form, then the Depositary shall deem such ADR holder to have instructed the Depositary to vote the Shares represented by any such ADRs in favor of any proposals or recommendations of the Company, for which purposes the Depositary shall issue a proxy to a person appointed by the Company to vote such Shares represented by such ADRs in favor of any proposals or recommendations of the Company (including any recommendation by the Company to vote such underlying shares on any given issue in accordance with the majority shareholder vote on that issue). No proxy shall be given, and no instruction shall be deemed given, with respect to any matter as to which the Company informs the Depositary that (i) it does not wish such proxy given (ii) it has knowledge that substantial opposition exists with respect to the action to be taken at the Meeting, or (iii) the matter materially and adversely effects the rights of the holders of ADRs. Any holder of ADRs entitled to provide the Depositary with voting instructions in respect of the Shares represented by its ADRs, is also entitled to revoke any instructions which it has previously given to the Depositary by filing with the Depositary a written revocation or duly executed instructions bearing a later date at any time prior to 5:00 p.m., New York time, on May 27, 2010. No instructions, revocations or revisions thereof shall be accepted by the Depositary after that time.

Holders of ADRs maintaining non-certificated positions must follow voting instructions given by their broker or custodian bank.

Due to regulatory differences and market practices in each country where the Company’s Shares or ADRs are listed, holders of Shares traded on the Argentine and Italian stock exchanges who have requested admission to the Meeting, or who have issued a voting proxy, must have their Shares blocked for trading until the date of the Meeting, while holders of Shares traded in the Mexican stock exchange and holders of ADRs traded in the New York stock exchange need not have their Shares or ADRs, as the case may be, blocked for trading. However, the votes of holders of Shares traded in the Mexican stock exchange who sell their Shares between May 27, 2010, and June 1, 2010, shall be disregarded for voting purposes.

Under Luxembourg legislation implementing the EU Transparency Directive, investors in the Company’s securities should notify the Company and the Luxembourg Commission de Surveillance du Secteur Financier (CSSF) on an ongoing basis whenever their direct or indirect ownership or other control rights over shares of the Company’s capital or rights to vote such shares either reaches, exceeds or falls below any of the following thresholds: 5%, 10%, 15%, 20%, 25%, 33.33%, 50% and 66.66%. The total number of issued and outstanding shares and votes set forth in the second paragraph of this Shareholder Meeting Brochure and Proxy Statement should be used for purposes of determining whether an investor reaches or exceeds each such threshold. Any such notification shall be made as indicated in the Company’s website at www.tenaris.com/investors and in accordance with CSSF regulations. Failure to make such notification will cause the suspension of the exercise of voting rights relating to the shares exceeding the fraction that should have been notified.

The Meeting will appoint a chairperson pro tempore to preside the Meeting. The chairperson pro tempore will have broad authority to conduct the Meeting in an orderly and timely manner and to establish rules for shareholders who wish to address the Meeting; the chairperson may exercise broad discretion in recognizing shareholders who wish to speak and in determining the extent of discussion on each item of the agenda.

Pursuant to the Company’s Articles of Association, resolutions at the Meeting will be passed by simple majority of the votes cast, irrespective of the number of Shares present or represented.

The Meeting is called to address and vote on the following agenda:

Annual General Meeting of Shareholders

1. Consideration of the Board of Directors’ management report and certifications and the independent auditors’ reports on the Company’s consolidated financial statements for the years ended December 31, 2009, 2008 and 2007, and the Company’s annual accounts as at December 31, 2009.

The Board of Directors recommends a vote FOR approval of the Board of Directors’ management report and certifications and the independent auditors’ reports on the Company’s consolidated financial statements for the years ended December 31, 2009, 2008 and 2007, and the Company’s annual accounts as at December 31, 2009. The Board of Directors’ management report on such consolidated financial statements -which has been combined with its management report on the Company’s annual accounts- management’s certifications and the independent auditors’ reports to such consolidated financial statements and annual accounts are included in the Company’s 2009 annual report, a copy of which is available on the Company’s website at www.tenaris.com/investors and may also be obtained upon request, by calling (352) 26-47-89-78 (if you are in Luxembourg), 1-800-555-2470 (if you are in the United States), or +1-267-468-0786 (if you are in any other jurisdiction).

2. Approval of the Company’s consolidated financial statements for the years ended December 31, 2009, 2008 and 2007.

The Board of Directors recommends a vote FOR approval of the Company’s consolidated financial statements for the years ended December 31, 2009, 2008 and 2007, after due consideration of the Board of Directors’ management report and certifications and the independent auditor’s reports on such consolidated financial statements. The consolidated balance sheets and the related consolidated statements of income, of cash flows and of changes in equity and the notes to such consolidated financial statements are included in the Company’s 2009 annual report, a copy of which is available on the Company’s website at www.tenaris.com/investors and may also be obtained upon request, by calling (352) 26-47-89-78 (if you are in Luxembourg), 1-800-555-2470 (if you are in the United States), or +1-267-468-0786 (if you are in any other jurisdiction).

3. Approval of the Company’s annual accounts as at December 31, 2009.

The Board of Directors recommends a vote FOR approval of the Company’s annual accounts as at December 31, 2009, after due consideration of the of the Board of Directors’ management report and certifications and the independent auditor’s reports on such annual accounts. The balance sheet, the profit and loss account and the notes to such annual accounts are included in the Company's 2009 annual report, a copy of which is available on our website at www.tenaris.com/investors and may also be obtained upon request, by calling (352) 26-47-89-78 (if you are in Luxembourg), 1-800-555-2470 (if you are in the United States), or +1-267-468-0786 (if you are in any other jurisdiction).

4. Allocation of results and approval of dividend payment for the year ended December 31, 2009.

The Board of Directors recommends a vote FOR approval of a dividend in U.S. dollars, in the amount of US$0.34 per Share currently issued and outstanding and US$0.68 per ADR currently issued and outstanding. As required by Luxembourg law, this dividend includes the interim dividend of US$0.13 per Share (US$0.26 per ADR) paid on November 26, 2009. Accordingly, if this dividend proposal is approved, the Company will make a dividend payment on June 24, 2010, in the amount of US$ 0.21 per Share currently issued and outstanding and US$ 0.42 per ADR currently issued and outstanding.

The aggregate amount of US$ 153,469,787.90 distributed as interim dividend on November 26, 2009, was paid from reserves of earnings from the nine-month period ended September 30, 2009. The aggregate amount of US$ 247,912,734.30 to be distributed as dividend on June 24, 2010, is to be paid from profits earned during the year ended December 31, 2009. The balance of the fiscal year’s profits will be allocated to the Company’s retained earnings account.

Upon approval of this resolution, it is proposed that the Board of Directors be authorized to determine or amend, in its discretion, the terms and conditions of the dividend payment.

5. Discharge to the members of the Board of Directors for the exercise of their mandate during the year ended December 31, 2009.

In accordance with applicable Luxembourg law and regulations, it is proposed that, upon approval of the Company’s annual accounts as at December 31, 2009, the members of the Board of Directors be discharged from any liability in connection with the management of the Company’s affairs during such year.

6. Election of the members of the Board of Directors.

The Company’s Articles of Association provide for the annual election by the shareholders of a Board of Directors of not less than five and not more than fifteen members. Members of the Board of Directors have a term of office of one year, but may be reappointed.

Under the Company’s Articles of Association and applicable U.S. laws and regulations, effective as of July 15, 2005, the Company is required to have an Audit Committee comprised solely of directors who are independent.

The present Board of Directors of the Company consists of ten directors. Three members of the Board of Directors (Messrs. Jaime Serra Puche, Amadeo Vázquez y Vázquez and Roberto Monti) qualify as independent directors under the Company’s Articles of Association and applicable law and are members of the Audit Committee.

It is proposed that the number of members of the Board of Directors be maintained at ten and that all of the current members of the Board of Directors be re-elected.

Set forth below is summary biographical information of each of the candidates:

| 1. | Roberto Bonatti. Mr. Bonatti is a member of the Company’s board of directors. He is a grandson of Agostino Rocca, founder of the Techint group, a group of companies controlled by San Faustin N.V. (“San Faustin”).Throughout his career in the Techint group he has been involved specifically in the engineering and construction and corporate sectors. He was first employed by the Techint group in 1976, as deputy resident engineer in Venezuela. In 1984, he became a director of San Faustin, and since 2001 he has served as its president. In addition, Mr. Bonatti currently serves as president of Tecpetrol S.A. (“Tecpetrol”) and Techint Compañia Técnica Internacional S.A.C.I. He is also a member of the board of directors of Ternium S.A. (“Ternium”), Siderca S.A.I.C. (“Siderca”) and Siderar S.A.I.C. (“Siderar”). Mr. Bonatti is an Italian citizen. |

| 2. | Carlos Condorelli. Mr. Condorelli is a member of the Company’s board of directors. He served as our chief financial officer from October 2002 until September 2007. He is also a board member of Ternium. He began his career within the Techint group in 1975 as an analyst in the accounting and administration department of Siderar. He has held several positions within Tenaris and other Techint group companies, including finance and administration director of Tubos de Acero de México, S.A. (“Tamsa”) and president of the board of directors of Empresa Distribuidora La Plata S.A., or Edelap, an Argentine utilities company. Mr. Condorelli is an Argentine citizen. |

| 3. | Carlos Franck. Mr. Franck is a member of the Company’s board of directors. He is president of Santa María S.A.I.F. and Inverban S.A., vice president of Siderca and a member of the board of directors of Techint Financial Corporation N.V., III Industrial Investments Inc., Siderar, Tecpetrol and Tecgas N.V. He has financial, planning and control responsibilities in subsidiaries of San Faustin. He serves as a member of the Board in the Di Tella University. Mr. Franck is an Argentine citizen. |

| 4. | Roberto Monti. Mr. Monti is a member of the Company’s board of directors. He is the non-executive chairman of Trefoil Limited and a member of the board of directors of Petrobras Energia. He has served as vice president of Exploration and Production of Repsol YPF and chairman and CEO of YPF. He was also president of Dowell, a subsidiary of Schlumberger and president of Schlumberger Wire & Testing division for East Hemisphere Latin America. Mr. Monti is an Argentine citizen. |

| 5. | Gianfelice Mario Rocca. Mr. Rocca is a member of the Company’s board of directors. He is a grandson of Agostino Rocca. He is chairman of the board of directors of San Faustin, a member of the board of directors of Ternium, president of the Humanitas Group and president of the board of directors of Techint Compagnia Tecnica Internazionale S.p.A. and Tenova S.p.A. In addition, he sits on the board of directors or executive committees of several companies, including Allianz S.p.A and Buzzi Unicem. He is vice president of Confindustria, the leading association of Italian industrialists. He is a member of the Advisory Board of Allianz Group, the Trilateral Commission and the European Advisory Board of the Harvard Business School. Mr. Rocca is an Italian citizen. |

| 6. | Paolo Rocca. Mr. Rocca is chairman of the Company’s board of directors and our chief executive officer. He is a grandson of Agostino Rocca. He is also chairman of the board of directors of Tamsa. He is also chairman of the board of directors of Ternium, director and vice president of San Faustin and director of Techint Financial Corporation N.V. Mr. Rocca is the chairman of the World Steel Association and member of the International Advisory Committee of the NYSE Euronext (New York Stock Exchange). Mr. Rocca is an Italian citizen. |

| 7. | Jaime Serra Puche. Mr. Serra Puche is a member of the Company’s board of directors. He is chairman of SAI Consultores, a Mexican consulting firm, and a member of the board of directors of Chiquita Brands International, the Mexico Fund, Grupo Vitro and Grupo Modelo. Mr. Serra Puche served as Mexico’s Undersecretary of Revenue, Secretary of Trade and Industry, and Secretary of Finance. He led the negotiation and implementation of NAFTA. Mr. Serra Puche is a Mexican citizen. |

| 8. | Alberto Valsecchi. Mr. Valsecchi is a member of the Company’s board of directors. He served as our chief operating officer from February 2004 until July 2007. He joined the Techint group in 1968 and has held various positions within Tenaris and other Techint group companies. He has retired from his executive positions. He is also a member of the board of directors of San Faustin and has been elected as the chairman of the board of directors of Dalmine, a position he assumed in May 2008. Mr. Valsecchi is an Italian citizen. |

| 9. | Amadeo Vázquez y Vázquez. Mr. Vázquez y Vázquez is a member of the Company’s board of directors. He is an independent member of the board of directors of Gas Natural Ban S.A. He is a member of the Asociación Empresaria Argentina, and of the Fundación Mediterránea, and he is a member of the Advisory Board of the Fundación de Investigaciones Económicas Latinoamericanas. He served as CEO of the Banco Río de la Plata S.A. until August 1997 and was also the chairman of the board of directors of Telecom Argentina S.A. until April 2007. Mr. Vázquez y Vázquez is a Spanish and Argentine citizen. |

| 10. | Guillermo Vogel. Mr. Vogel is a member of the Company’s board of directors. He is vice chairman of Tamsa, chairman of Grupo Collado S.A.B. de C.V, vice chairman of Estilo y Vanidad S.A. de C.V. and member of the board of directors of Alfa S.A.B. de C.V., the American Iron and Steel Institute, the North American Steel Council, the Universidad Panamericana and the IPADE. In addition, he is a member of the board of directors and of the investment committee of the Corporación Mexicana de Inversiones de Capital and a member of the board of directors and the audit committee of HSBC (México). Mr. Vogel is a Mexican citizen. |

Each elected director will hold office until the next Annual General Meeting of Shareholders. Under the current Company’s Articles of Association, such meeting is required to be held on June 1st, 2011.

The Company’s Board of Directors met eleven times during 2009. On January 31, 2003, the Board of Directors created an Audit Committee pursuant to Article 11 of the Company’s Articles of Association. As permitted under applicable laws and regulations, the Board of Directors does not have any executive, nominating or compensation committee, or any committees exercising similar functions.

7. Compensation of the members of the Board of Directors.

It is proposed that each of the members of the Board of Directors receive an amount of US$70,000 as compensation for their services during the fiscal year 2010. It is further proposed that the members of the Board of Directors who are members of the Audit Committee receive an additional fee of US$50,000 and that the Chairman of such Audit Committee receive, further, an additional fee of US$10,000.

8. Appointment of the independent auditors for the fiscal year ending December 31, 2010, and approval of their fees.

Based on the recommendation from the Audit Committee, the Board of Directors recommends a vote FOR the appointment of PricewaterhouseCoopers (acting, in connection with the Company’s annual accounts and annual consolidated financial statements required under Luxembourg law, through PricewaterhouseCoopers S.àr.l., Réviseur d'entreprises, and, in connection with the Company’s annual and interim consolidated financial statements required under the laws of any other relevant jurisdiction, through Pricewaterhouse & Co. S.R.L.) as the Company’s independent auditors for the fiscal year ending December 31, 2010, to be engaged until the next Annual General Meeting of Shareholders that will be convened to decide on the 2010 accounts.

In addition, the Board of Directors recommends a vote FOR approval of the independent auditors’ fees for audit, audit-related and other services to be rendered during the fiscal year ending December 31, 2010, broken-down into five currencies (Argentine Pesos, Euro, Mexican Pesos, Brazilian reais and U.S. Dollars), up to a maximum amount for each currency equal to AR$7,533,962, €472,297, MX$4,237,309, BR$345,000 and US$1,408,735. Such fees would cover the audit of the Company’s consolidated financial statements and annual accounts, the audit of the Company’s internal controls over financial reporting as mandated by the Sarbanes-Oxley Act of 2002, other audit-related services, and other services rendered by the independent auditors. For information purposes, based on the exchange rate between the U.S. Dollar and each applicable other currency as of December 14, 2009, the aggregate amount of fees for audit, audit-related and other services to be rendered by the independent auditors during the fiscal year ending December 31, 2010, is equivalent to US$4,611,249. The Board of Directors also recommends that its Audit Committee be authorised to approve any increase or reallocation of the independent auditors’ fees as may be necessary, appropriate or desirable under the circumstances.

9. Authorisation to the Company, or any subsidiary, to from time to time purchase, acquire or receive shares of the Company, in accordance with Article 49-2 of the Luxembourg law of 10 August 1915 and with applicable laws and regulations.

It is recommended that the authorisation to the Company and to the Company’s subsidiaries to acquire, from time to time, Shares, including Shares represented by ADRs (collectively, “Securities”) granted by the General Meeting of Shareholders held on June 3, 3009, be cancelled and that a new authorization be granted to the Company and to the Company’s subsidiaries to purchase, acquire or receive, from time to time, Securities, on the following terms and conditions:

| 1. | Purchases, acquisitions or receptions of Securities may be made in one or more transactions as the Board of Directors or the board of directors or other governing bodies of the relevant entity, as applicable, considers advisable. |

| 2. | The maximum number of Securities acquired pursuant to this authorization may not exceed 10% of the Company’s issued and outstanding Shares or, in the case of acquisitions made through a stock exchange in which the Securities are traded, such lower amount as may not be exceeded pursuant to any applicable laws or regulations of such market. The number of Securities acquired as a block may amount to the maximum permitted amount of purchases. |

| 3. | The purchase price per share to be paid in cash may not exceed 125% (excluding transaction costs and expenses), nor may it be lower than 75% (excluding transaction costs and expenses), in each case of the average of the closing prices of the Company’s Securities in the stock exchange through which the Company’s Securities are acquired, during the five trading days in which transactions in the Securities were recorded in such stock exchange preceding (but excluding) the day on which the Company’s Securities are acquired. For over-the-counter or off-market transactions, the purchase price per ADR to be paid in cash may not exceed 125% (excluding transaction costs and expenses), nor may it be lower than 75% (excluding transaction costs and expenses), in each case of the average of the closing prices of the Company’s ADRs in the New York Stock Exchange during the five trading days in which transactions in ADRs were recorded in the New York Stock Exchange preceding (but excluding) the day on which the Company’s ADRs are acquired; and, in the case of acquisition of Securities, other than in the form of ADRs, such maximum and minimum purchase prices shall be calculated based on the number of underlying Shares represented by such ADRs. Compliance with maximum and minimum purchase price requirements in any and all acquisitions made pursuant to this authorization (including, without limitation, acquisitions carried out through the use of derivative financial instruments or option strategies) shall be determined on and as of the date on which the relevant transaction is entered into, irrespective of the date on which the transaction is to be settled. |

| 4. | The above maximum and minimum purchase prices shall, in the event of a change in the par value of the Shares, a capital increase by means of a capitalization of reserves, a distribution of Shares under compensation or similar programs, a stock split or reverse stock split, a distribution of reserves or any other assets, the redemption of capital, or any other transaction impacting on the Company’s equity be adapted automatically, so that the impact of any such transaction on the value of the Shares shall be reflected. |

| 5. | The acquisitions of Securities may not have the effect of reducing the Company’s net assets below the sum of the Company’s capital stock plus its undistributable reserves. |

| 6. | Only fully paid-up Securities may be acquired pursuant to this authorisation. |

| 7. | The acquisitions of Securities may be carried out for any purpose, as may be permitted under applicable laws and regulations, including without limitation to reduce the share capital of the Company, to offer such shares to third parties in the context of corporate mergers or acquisitions of other entities or participating interests therein, for distribution to the Company’s or the Company’s subsidiaries’ directors, officers or employees or to meet obligations arising from convertible debt instruments. |

| 8. | The acquisitions of Securities may be carried out by any and all means, as may be permitted under applicable laws and regulations, including through any stock exchange in which the Company’s Securities are traded, through public offers to all shareholders of the Company to buy Securities, through the use of derivative financial instruments or option strategies, or in over the counter or off-market transactions or in any other manner. |

| 9. | The acquisitions of Securities may be carried out at any time, during the duration of the authorisation, including during a tender offer period, as may be permitted under applicable laws and regulations. |

| 10. | The authorisation granted to acquire Securities shall be valid for such maximum period as may be provided for under applicable Luxembourg law as in effect from time to time (such maximum period being, as of to date, 5 years). |

| 11. | The acquisitions of Securities shall be made at such times and on such other terms and conditions as may be determined by the Board of Directors or the board of directors or other governing bodies of the relevant entity, provided that, any such purchase shall comply with Article 49-2 et.seq. of the Luxembourg Law of 10 August 1915 on commercial companies, as amended (or any successor law) and, in the case of acquisitions of Securities made through a stock exchange in which the Company’s Securities are traded, with any applicable laws and regulations of such market. |

It is recommended that the Meeting grant this authorization and further grant all powers to the Board of Directors and to the board of directors or other governing bodies of the Company’s subsidiaries, in each case with powers to delegate in accordance with applicable laws, the Company’s Articles of Association or the articles of association of other applicable organizational documents of the relevant Company’s subsidiary, to decide on and implement this authorisation, to define, if necessary, the terms and procedures for carrying out any purchase, acquisition or reception of Securities, and, in particular, to place any stock exchange orders, conclude any agreements, including for keeping registers of purchases and sales of Securities, make any declarations to the applicable regulatory authorities, carry out all formalities and, generally, do all such other acts and things as may be necessary, appropriate or desirable under the circumstances. The Board of Directors is expressly authorized to delegate to its Chairman, with the latter having the option to sub-delegate to any other person(s), the performance of the actions entrusted to the Board of Directors, pursuant to, or in connection with, this authorisation.

10. Authorisation to the Board of Directors to cause the distribution of all shareholder communications, including its shareholder meeting and proxy materials and annual reports to shareholders, by such electronic means as is permitted by any applicable laws or regulations.

In order to expedite shareholder communications and ensure their timely delivery, the Board of Directors recommends that it be authorised to cause the distribution of all shareholder communications, including its shareholder meeting and proxy materials and annual reports to shareholders (either in the form of a separate annual report containing financial statements of the Company and its consolidated subsidiaries or in the form of an annual report on Form 20-F or similar document, as filed with the securities authorities or stock markets) by such electronic means as are permitted or required by any applicable laws or regulations (including any interpretations thereof), including, without limitation, by posting such communication on the Company's website, or by sending electronic communications (emails) with attachment(s) in a widely used format or with a hyperlink to the applicable filing by the Company on the website of the above referred authorities or stock markets, or by any other existing or future electronic means of communication as is or may be permitted by any applicable laws or regulations.

In this resolution the Company seeks authorisation under Article 16 of the Luxembourg Transparency Law of 11 January 2008 to give, send or supply information (including any notice or other document) that is required or authorised to be given, sent or supplied to a shareholder by the Company whether required under the Company’s Articles of Association or by any applicable law or any other rules or regulations to which the Company may be subject, by making such information (including any notice or other document) available on the Company’s website or through other electronic means.

* * * * *

The Company anticipates that the next Annual General Meeting of Shareholders will be held on June 1, 2011. Any holder of Shares who intends to present a proposal to be considered at the next Annual General Meeting of Shareholders is requested to submit its proposal in writing to the Company at any of the offices indicated in the Notice not later than 4:00 P.M. (local time) on March 31, 2011, or in accordance with the procedures set forth under applicable Luxembourg law, in order for such proposal to be considered for inclusion on the agenda for the 2011 Annual General Meeting of Shareholders.

PricewaterhouseCoopers are the Company’s independent auditors. A representative of the independent auditors will be present at the meeting to respond to questions.

Cecilia Bilesio

Secretary to the Board of Directors

TENARIS S.A.

ANNUAL REPORT 2009

TABLE OF CONTENTS

| COMPANY PROFILE | 2 |

| LETTER FROM THE CHAIRMAN | 3 |

| MANAGEMENT REPORT | 5 |

| Leading indicators | 7 |

| Information on Tenaris | 8 |

| TenarisHydril | 13 |

| Tenaris in numbers | 16 |

| Principal Risks and Uncertainties | 18 |

| Operating and Financial Review and Prospects | 20 |

| Recent Developments | 30 |

| Environmental Regulation | 30 |

| Related Party Transactions | 30 |

| Corporate Governance | 30 |

| MANAGEMENT CERTIFICATION | 41 |

| FINANCIAL INFORMATION | 42 |

| Consolidated Financial Statements | 42 |

| Tenaris S.A. Annual Accounts (Luxembourg GAAP) | 105 |

| CORPORATE INFORMATION | 121 |

company profile

Tenaris is a leading supplier of tubes and related services for the world’s energy industry and certain other industrial applications. Our mission is to deliver value to our customers through product development, manufacturing excellence and supply chain management. We minimize risk for our customers and help them reduce costs, increase flexibility and improve time-to-market. Our employees around the world are committed to continuous improvement by sharing knowledge across a single global organization.

2

Letter From The Chairman

Dear Shareholders,

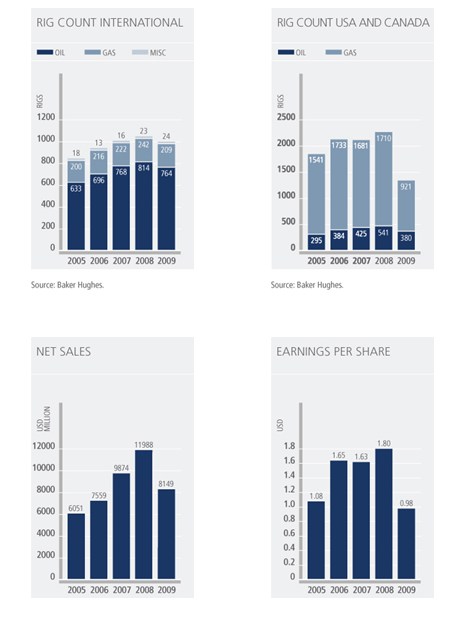

In 2009, we felt the impact of the global economic and financial crisis on demand for our products and services. Pipe shipments were down 41% compared to 2008. Tenaris responded well, adjusting production levels, reducing working capital and structural costs, while continuing with our investments to strengthen our positioning in a more competitive marketplace. Our employees made remarkable efforts to support the difficult adjustment that we had to execute, when our average level of plant utilization fell to around 40 % of that in 2008.

Our results for the year reflect a good performance in spite of the difficult comparison with the exceptional results of the previous years. With an EBITDA of $2.3 billion on net sales of $8.1 billion and a strong balance sheet with $0.7 billion in net cash, we are well positioned for the recovery of demand which we are starting to see particularly in North America and in the Middle East.

In the US market, attractive oil prices and the exploitation of leases for productive shale gas drilling is leading activity higher although rising natural gas production levels and falling prices may limit the extent of the recovery. At the same time, OCTG inventories have adjusted to more normal levels after reaching unsustainable levels following the surge in Chinese imports that took place in the second half of 2008 and first half of 2009.

In the Middle East, reactivation in Iraq and the development of deep and sour gas reserves in various parts of the region is driving activity. Meanwhile, the adjustment of inventory levels continued in the region in 2009 and inventories of premium products are now relatively low. We also expect activity levels to increase in other regions as oil and gas companies increase or maintain their budgets for exploration and production activity while drilling costs have come down.

The investments we have under way position us well for the recovery. In the US, we have been investing to transform the quality performance of our mills and we are completing new tubing and finishing facilities. We are currently ramping up production to meet the increase in demand. The construction of our new rolling mill in Veracruz is on schedule and we expect to begin operations in October. Following the agreement we concluded with the unions and the government in December in Italy, we will now go forward with a significant investment at our Dalmine mill aimed at increasing product differentiation and improving industrial efficiency.

With new production capacity continuing to come into the market all over the world and global demand for OCTG unlikely to recover the level seen in 2008 any time soon, the competitive environment over the coming years is expected to be fierce. We are pleased, however, that the governments of the US, Canada and the European Union have recognized the injury, and threat thereof, to local industrial production from subsidized Chinese imports.

A clear priority is to be close to our customers. Over the past few years, we have been building up local production and service capabilities in various key markets around the world. Over the past year, we have integrated into Tenaris, the heat treatment and premium finishing operations we acquired in Indonesia and have established a strong local presence. In May, we will start production at our new premium finishing facility in Saudi Arabia and the recruiting and training of local personnel is well under way. We will now reinforce this priority by making Dubai the center of our oil and gas commercial operations of the Eastern hemisphere.

Notwithstanding a more difficult competitive environment, the fundamentals of our business remain solid. We are capable of differentiating our products and services consistently from those of our competitors, in an environment in which the demand for more sophisticated products for complex applications is increasing. The decline in market prices that started towards the end of 2008 has largely taken its course and the raw material cost dynamics are starting to be reflected in price increases. We remain confident that Tenaris will continue to perform strongly.

3

We propose, however, to adjust the dividend payout to bring it more in line with the level of results we had this year. Accordingly, we are proposing a dividend of US$0.34 per share (US$0.68 per ADS), which includes the interim dividend of US$0.13 per share (US$0.26 per ADS) paid in November. The balance of the dividend will be payable in June.

As we went into 2009, the economic and financial crisis was still unfolding and there was considerable uncertainty as to the depth and course it would take. I wish to thank our employees for their extraordinary commitment and sense of responsibility in responding to the crisis and for their efforts to sustain and enhance the competitive position of the company. I also thank our customers, suppliers and shareholders for their continuing support and confidence in Tenaris.

April 22, 2010

Paolo Rocca

4

Management Report

CERTAIN DEFINED TERMS

Unless otherwise specified or if the context so requires:

| · | References in this annual report to “the Company” refer exclusively to Tenaris S.A., a Luxembourg joint stock corporation (société anonyme holding). |

| · | References in this annual report to “Tenaris”, “we”, “us” or “our” refer to Tenaris S.A. and its consolidated subsidiaries. See Accounting Policies A, B and L to our audited consolidated financial statements included in this annual report. |

| · | References in this annual report to “San Faustin” refer to San Faustin N.V., a Netherlands Antilles corporation and the Company’s controlling shareholder. |

| · | “Shares” refers to ordinary shares, par value $1.00 of the Company. |

| · | “ADSs” refers to the American Depositary Shares, which are evidenced by American Depositary Receipts. |

| · | “tons” refers to metric tons; one metric ton is equal to 1,000 kilograms, 2,204.62 pounds, or 1.102 U.S. (short) tons. |

| · | “billion” refers to one thousand million, or 1,000,000,000. |

| · | “dollars”, “U.S. dollars”, “US$” or “$” each refers to the United States dollar |

PRESENTATION OF CERTAIN FINANCIAL AND OTHER INFORMATION

Accounting Principles

We prepare our consolidated financial statements in conformity with International Financial Reporting Standards, as issued by the International Accounting Standards Board and adopted by the European Union, or IFRS.

We publish consolidated financial statements expressed in U.S. dollars. Our consolidated financial statements included in this annual report are those for the years ended December 31, 2009, 2008 and 2007.

Rounding

Certain monetary amounts, percentages and other figures included in this annual report have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables may not be the arithmetic aggregation of the figures that precede them, and figures expressed as percentages in the text may not total 100% or, as applicable, when aggregated may not be the arithmetic aggregation of the percentages that precede them.

CAUTIONARY STATEMENT CONCERNING FORWARD-LOOKING STATEMENTS

This annual report and any other oral or written statements made by us to the public may contain “forward-looking statements”. Forward looking statements are based on management’s current views and assumptions and involve known and unknown risks that could cause actual results, performance or events to differ materially from those expressed or implied by those statements.

We use words such as “aim”, “will likely result”, “will continue”, “contemplate”, “seek to”, “future”, “objective”, “goal”, “should”, “will pursue”, “anticipate”, “estimate”, “expect”, “project”, “intend”, “plan”, “believe” and words and terms of similar substance to identify forward-looking statements, but they are not the only way we identify such statements. This annual report contains forward-looking statements, including with respect to certain of our plans and current goals and expectations relating to Tenaris’s future financial condition and performance. Sections of this annual report that by their nature contain forward-looking statements include, but are not limited to, “Business Overview”, “Principal Risks and Uncertainties”, and “Operating and Financial Review and Prospects”. In addition to the risks related to our business discussed under “Principal Risks and Uncertainties”, other factors could cause actual results to differ materially from those described in the forward-looking statements. These factors include, but are not limited to:

5

| · | our ability to implement our business strategy or to grow through acquisitions, joint ventures and other investments; |

| · | our ability to price our products and services in accordance with our strategy; |

| · | trends in the levels of investment in oil and gas exploration and drilling worldwide; |

| · | general macroeconomic and political conditions in the countries in which we operate or distribute pipes; and |

| · | our ability to absorb cost increases and to secure supplies of essential raw materials and energy. |

By their nature, certain disclosures relating to these and other risks are only estimates and could be materially different from what actually occurs in the future. As a result, actual future gains or losses that may affect our financial condition and results of operations could differ materially from those that have been estimated. You should not place undue reliance on the forward-looking statements, which speak only as of the date of this annual report. Except as required by law, we are not under any obligation, and expressly disclaim any obligation, to update or alter any forward-looking statements, whether as a result of new information, future events or otherwise.

6

Leading indicators

| 2009 | 2008 | 2007 | ||||||||||

| SALES VOLUMES (thousands of metric tons) | ||||||||||||

| Tubes-Seamless | 1,970 | 2,818 | 2,818 | |||||||||

| Tubes-Welded | 346 | 1,057 | 965 | |||||||||

| Tubes-Total | 2,316 | 3,875 | 3,783 | |||||||||

| Projects-Welded | 334 | 591 | 474 | |||||||||

| Total –Tubes+Projects | 2,650 | 4,466 | 4,257 | |||||||||

| PRODUCTION VOLUMES (thousands of metric tons) | ||||||||||||

| Tubes-Seamless | 1,770 | 3,005 | 2,836 | |||||||||

| Tubes-Welded | 249 | 999 | 909 | |||||||||

| Tubes-Total | 2,019 | 4,004 | 3,745 | |||||||||

| Projects-Welded | 291 | 548 | 499 | |||||||||

| Total –Tubes+Projects | 2,310 | 4,552 | 4,244 | |||||||||

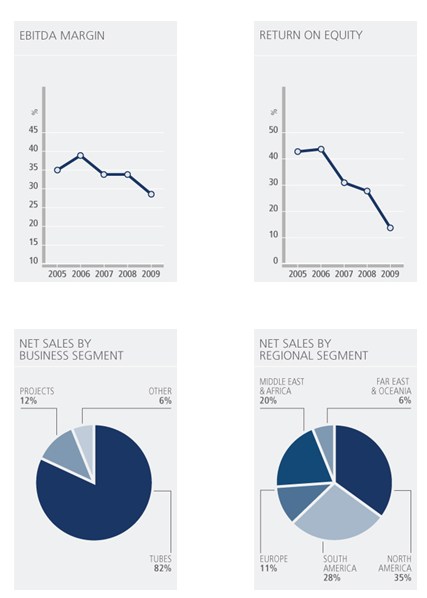

| FINANCIAL INDICATORS (millions of US$) | ||||||||||||

| Net sales | 8,149 | 11,988 | 9,874 | |||||||||

| Operating income | 1,814 | 3,126 | 2,917 | |||||||||

| EBITDA (1) | 2,318 | 4,044 | 3,401 | |||||||||

| Net income | 1,208 | 2,276 | 2,076 | |||||||||

| Cash flow from operations | 3,064 | 1,465 | 2,021 | |||||||||

| Capital expenditures | 461 | 443 | 448 | |||||||||

| BALANCE SHEET (millions of US$) | ||||||||||||

| Total assets | 13,483 | 15,101 | 15,245 | |||||||||

| Total financial debt | 1,447 | 2,977 | 4,020 | |||||||||

| Net financial debt/ (cash) (2) | (676 | ) | 1,392 | 2,970 | ||||||||

| Total liabilities | 3,762 | 6,399 | 7,715 | |||||||||

| Shareholders’ equity including minority interest | 9,721 | 8,702 | 7,530 | |||||||||

| PER SHARE / ADS DATA (US$ PER SHARE / PER ADS) | ||||||||||||

| Number of shares outstanding (3) (thousands of shares) | 1,180,537 | 1,180,537 | 1,180,537 | |||||||||

| Earnings per share | 0.98 | 1.80 | 1.63 | |||||||||

| Earnings per ADS | 1.97 | 3.60 | 3.26 | |||||||||

| Dividends per share (4) | 0.34 | 0.43 | 0.38 | |||||||||

| Dividends per ADS (4) | 0.68 | 0.86 | 0.76 | |||||||||

| ADS Stock price at year-end | 42.65 | 20.98 | 44.73 | |||||||||

| Number of employees (3) | 22,591 | 23,873 | 23,372 | |||||||||

| 1. | Defined as operating income plus depreciation, amortization and impairment charges. |

| 2. | Defined as borrowings less cash and cash equivalents and other current investments. |

| 3. | As of December 31. |

| 4. | Proposed or paid in respect of the year. |

7

Information on Tenaris

Overview

We are a leading global manufacturer and supplier of steel pipe products and related services for the world’s energy industry as well as for other industrial applications. Our customers include most of the world’s leading oil and gas companies as well as engineering companies engaged in constructing oil and gas gathering, transportation, processing and power generation facilities. Our principal products include casing, tubing, line pipe, and mechanical and structural pipes.

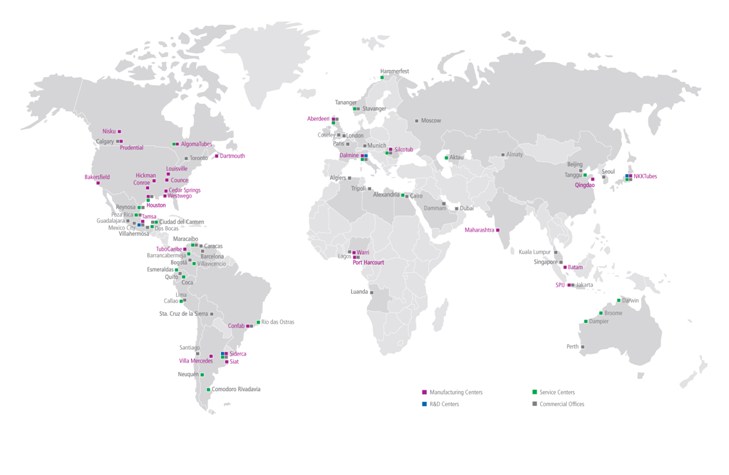

Over the last two decades, we have expanded our business globally through a series of strategic investments. We now operate an integrated worldwide network of steel pipe manufacturing, research, finishing and service facilities with industrial operations in North and South America, Europe, Asia and Africa and a direct presence in most major oil and gas markets.

Our business is organized in two main business segments: Tubes and Projects.

| · | Tubes includes our operations that consist in the production, distribution and sale of seamless and welded tubular products and related services mainly for energy and select industrial applications. |

| · | Projects includes our operations that consist in the production, distribution and sale of welded pipes mainly used in the construction of major pipeline projects. |

A third business segment (Others) includes all other business activities and operating segments that are not required under IFRS to be separately reported, such as the production, distribution and sale of sucker rods, welded steel pipes for electric conduits, industrial equipment and raw materials that exceed our internal requirements.

History and Development of Tenaris

Tenaris began with the formation of Siderca S.A.I.C., or Siderca, the sole Argentine producer of seamless steel pipe products, by San Faustin’s predecessor in Argentina in 1948. Siat, an Argentine welded steel pipe manufacturer, was acquired in 1986. We grew organically in Argentina and then, in the early 1990s, began to evolve beyond this initial base into a global business through a series of strategic investments. These investments included the acquisition, directly or indirectly, of controlling or substantial interests in the following companies:

| · | Tubos de Acero de México S.A., or Tamsa, the sole Mexican producer of seamless steel pipe products (June 1993); |

| · | Dalmine S.p.A., or Dalmine, a leading Italian producer of seamless steel pipe products (February 1996); |

| · | Tubos de Acero de Venezuela S.A., or Tavsa, the sole Venezuelan producer of seamless steel pipe products (October 1998)1; |

| · | Confab Industrial S.A., or Confab, the leading Brazilian producer of welded steel pipe products (August 1999); |

| · | NKKTubes, a leading Japanese producer of seamless steel pipe products (August 2000); |

| · | Algoma Tubes Inc., or AlgomaTubes, the sole Canadian producer of seamless steel pipe products (October 2000); |

1 In 2009, the Venezuelan government announced the nationalization of Tavsa. For more information on the Tavsa nationalization process, see note 32 (b) “Processes in Venezuela-Nationalization of Venezuelan Subsidiaries” to our consolidated financial statements included in this annual report.

8

| · | S.C. Silcotub S.A., or Silcotub, a leading Romanian producer of seamless steel pipe products (July 2004); |

| · | Maverick Tube Corporation, or Maverick, a leading North American producer of welded steel pipe products with operations in the U.S., Canada and Colombia (October 2006); |

| · | Hydril Company, or Hydril, a leading North American manufacturer of premium connection products for oil and gas drilling production (May 2007); and |

| · | Seamless Pipe Indonesia Jaya, or SPIJ, an Indonesian OCTG processing business with heat treatment and premium connection threading facilities (April 2009). |

In addition, we have established a global network of pipe finishing, distribution and service facilities with a direct presence in most major oil and gas markets and a global network of research and development centers.

Business Overview

Our business strategy is to continue expanding our operations worldwide and further consolidate our position as a leading global supplier of high-quality tubular products and services to the energy and other industries by:

| · | pursuing strategic investment opportunities in order to strengthen our presence in local and global markets; |

| · | expanding our comprehensive range of products and developing new high-value products designed to meet the needs of customers operating in increasingly challenging environments; |

| · | securing an adequate supply of production inputs and reducing the manufacturing costs of our core products; and |

| · | enhancing our offer of technical and pipe management services designed to enable customers to optimize their selection and use of our products and reduce their overall operating costs. |

Pursuing strategic investment opportunities and alliances

We have a solid record of growth through strategic investments and acquisitions. We pursue selective strategic investments and acquisitions as a means to expand our operations and presence in selected markets, enhance our global competitive position and capitalize on potential operational synergies. For example, we are building new capacity at our seamless pipe facility in Mexico in order to enhance our ability to serve local and global markets. Our track record on companies’ acquisitions is described above (See “History and Development of Tenaris”).

9

Developing high-value products

We have developed an extensive range of high-value products suitable for most of our customers’ operations using our network of specialized research and testing facilities and by investing in our manufacturing facilities. As our customers expand their operations, we seek to supply high-value products that reduce costs and enable them to operate safely in increasingly challenging environments.

Securing inputs for our manufacturing operations

We seek to secure our existing sources of raw material and energy inputs, and to gain access to new sources, of low-cost inputs which can help us maintain or reduce the cost of manufacturing our core products over the long term.

Enhancing our offer of technical and pipe management services

We continue to enhance our offer of technical and pipe management services for our customers worldwide. Through the provision of these services, we seek to enable our customers to optimize their operations, reduce costs and to concentrate on their core businesses. They are also intended to differentiate us from our competitors and further strengthen our relationships with our customers worldwide through long-term agreements.

Our Competitive Strengths

We believe our main competitive strengths include:

| · | our global production, commercial and distribution capabilities, offering a full product range with flexible supply options backed up by local service capabilities in important oil and gas producing and industrial regions around the world; |

| · | our ability to develop, design and manufacture technologically advanced products; |

| · | our solid and diversified customer base and historic relationships with major international oil and gas companies around the world, and our strong and stable market shares in the countries in which we have manufacturing operations; |

| · | our human resources around the world with their diverse knowledge and skills; |

| · | our low-cost operations, primarily at state-of-the-art, strategically located production facilities with favorable access to raw materials, energy and labor, and 50 years of operating experience; and |

| · | our strong balance sheet. |

Business Segments

Our business is organized in two main business segments: Tubes and Projects.

| · | Tubes includes our operations that consist in the production, distribution and sale of seamless and welded tubular products and related services mainly for energy and select industrial applications. |

| · | Projects includes our operations that consist in the production, distribution and sale of welded pipes mainly used in the construction of major pipeline projects. |

A third business segment (Others) includes all other business activities and operating segments that are not required under IFRS to be separately reported, such as the production, distribution and sale of sucker rods, welded steel pipes for electric conduits, industrial equipment and raw materials that exceed our internal requirements.

Our Products

Our principal finished products are seamless and welded steel casing and tubing, line pipe and various other mechanical and structural steel pipes for different uses. Casing and tubing are also known as oil country tubular goods or OCTG. In our Projects business segment we also produce large diameter welded steel pipes for oil and gas pipelines. We manufacture our steel pipe products in a wide range of specifications, which vary in diameter, length, thickness, finishing, steel grades, threading and coupling. For most complex applications, including high pressure and high temperature applications, seamless steel pipes are usually specified and, for some standard applications, welded steel pipes can also be used.

10

Casing. Steel casing is used to sustain the walls of oil and gas wells during and after drilling.

Tubing. Steel tubing is used to conduct crude oil and natural gas to the surface after drilling has been completed.

Line pipe. Steel line pipe is used to transport crude oil and natural gas from wells to refineries, storage tanks and loading and distribution centers.

Mechanical and structural pipes. Mechanical and structural pipes are used by general industry for various applications, including the transportation of other forms of gas and liquids under high pressure.

Cold-drawn pipe. The cold-drawing process permits the production of pipes with the diameter and wall thickness required for use in boilers, superheaters, condensers, heat exchangers, automobile production and several other industrial applications.

Premium joints and couplings. Premium joints and couplings are specially designed connections used to join lengths of steel casing and tubing for use in high temperature or high pressure environments. A significant portion of our steel casing and tubing products are supplied with premium joints and couplings. We own an extensive range of premium connections, and following the integration of Hydril’s premium connections business, we market our premium connection products under the TenarisHydril brand name. In addition, we hold licensing rights to manufacture and sell the Atlas Bradford range of premium connections outside of the United States.

Coiled tubing. Coiled tubing is used for oil and gas drilling and well workovers and for subsea pipelines.