FORM 6 - K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Pursuant to Rule 13a - 16 or 15d - 16 of

the Securities Exchange Act of 1934

As of May 8, 2007

TENARIS, S.A.

(Translation of Registrant's name into English)

TENARIS, S.A.

46a, Avenue John F. Kennedy

L-1855 Luxembourg

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or 40-F.

Form 20-F þ Form 40-F___

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12G3-2(b) under the Securities Exchange Act of 1934.

Yes ___ Noþ

If “Yes” is marked, indicate below the file number assigned to the registrant in connection

with Rule 12g3-2(b): 82- .

The attached material is being furnished to the Securities and Exchange Commission pursuant to Rule 13a-16 and Form 6-K under the Securities Exchange Act of 1934, as amended. This report contains Tenaris' notice of Annual General Meeting and Extraordinary General Meeting of Shareholders and the Shareholder Meeting Brochure and Proxy Statement.

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

Date: May 8, 2007

Tenaris, S.A.

By: /s/ Cecilia Bilesio

Cecilia Bilesio

Corporate Secretary

Dear Tenaris Shareholder and ADR Holder,

I am pleased to invite you to attend the Annual General Meeting and an Extraordinary General Meeting of Shareholders of the Company. Both meetings will be held on Wednesday, June 6, 2007, at 46A, Avenue John F. Kennedy L-1855 Luxembourg. The Annual General Meeting will begin promptly at 11:00 a.m. (Central European Time), while the Extraordinary General Meeting will follow immediately thereafter.

At the Annual General Meeting, you will have the opportunity to hear a report on the Company’s business, financial condition and results of operation and to vote on various matters, including the approval of the Company’s financial statements, the election of the members of the board of directors and the appointment of the independent auditors. Subsequently, the Extraordinary General Meeting will decide to renew, for a further five years and otherwise on its current terms and conditions, the validity of the Company’s authorized share capital, and the authorization to the board of directors to issue shares within that limit.

The Notice and Agenda for both Meetings, the Shareholder Meeting Brochure and Proxy Statement and the Company’s 2006 annual report (which includes the Company’s financial statements for the year ended December 31, 2006, 2005 and 2004 in their consolidated and unconsolidated form, together with the board of directors’ and independent auditors reports), are available free of charge at the Company's registered office in Luxembourg and on our website at www.tenaris.com/investors. They may also be obtained upon request, by calling 1-800-990-1135 (if you are in the United States) or +1-201-680-6630 (if you are outside the United States).

Even if you only own a few shares or ADRs, I hope that you will exercise your right to vote at both Meetings. You can vote your shares personally or by proxy. If you choose to vote by proxy, you may use the enclosed dedicated proxy form. If you are a holder of ADRs, please see the letter from JPMorgan Chase Bank, N.A., depositary bank, for instructions on how to exercise your vote by proxy.

Yours sincerely,

Paolo Rocca

Chairman and Chief Executive Officer

April 27, 2007

1

JPMORGAN CHASE BANK, N.A.

4 New York Plaza, Floor 13

New York, NY 10004

Re: TENARIS S.A.

| To: | Registered Holders of American Depositary Receipts (“ADRs”) |

for Shares of Common Stock, US$1 Par Value (“Common Stock”), of Tenaris S.A. (the “Company”): |

The Company has announced that its Annual General Meeting of Shareholders will be held on June 6, 2007, at 11:00 a.m. (Central European Time), and that an Extraordinary General Meeting will be held immediately after conclusion of the Annual General Meeting. Both meetings will take place at 46A, Avenue John F. Kennedy L-1855 Luxembourg. A copy of the Company’s Notice of Annual General Meeting and Extraordinary General Meeting of Shareholders, including the agenda for such meetings, is enclosed.

The Notice of Annual General Meeting and Extraordinary General Meeting of Shareholders, the Shareholder Meeting Brochure and Proxy Statement, and the Company’s 2006 annual report (which includes the Company’s financial statements for the year ended December 31, 2006, 2005 and 2004 in their consolidated and unconsolidated form, together with the board of directors and independent auditors reports), are available on the website at www.tenaris.com/investors and may also be obtained upon request at 1-800-990-1135 (if you are in the United States) or +1-201-680-6630 (if you are outside the United States). These materials are provided to allow the shares represented by your ADRs to be voted at the meetings.

Each holder of ADRs as of April 30, 2007, which continues to hold such ADRs on May 22, 2007, is entitled to instruct JPMorgan Chase Bank, N.A., as Depositary (the “Depositary”), as to the exercise of the voting rights pertaining to the Company’s shares of Common Stock represented by such holder’s ADRs. Although voting instructions are sent to holders and proxy materials are available on the website beginning on May 5, 2007, only those Holders of record at each of April 30, 2007 and May 22, 2007 will be entitled to provide the Depositary with voting instructions. Notwithstanding that holders of ADRs must have held ADRs on each such date, in order to avoid the possibility of double vote, only those positions on May 22, 2007 will be counted for voting instruction purposes. Eligible ADR holders who desire to have their shares represented by their ADRs voted at the Meeting must complete, date and sign a proxy form and return it to JPMorgan Chase Bank, N.A., P.O. Box 3500, South Hakensack, NJ 07606-3500, U.S.A. If the Depositary receives properly completed instructions by 3:00 p.m., New York City time, on May 30, 2007, then it shall vote or cause to be voted the shares underlying such ADRs in the manner prescribed by the instructions. However, if by 3:00 p.m., New York time, on May 30, 2007, the Depositary receives no instructions from the holder of ADRs, or the instructions are not in proper form, then the Depositary shall deem such holder to have instructed the Depositary to vote the underlying shares of Common Stock of any such ADRs in favor of any proposals or recommendations of the Company, for which purposes the Depositary shall issue a discretionary proxy to a person appointed by the Company to vote such shares in favor of any proposals or recommendations of the Company (including any recommendation by the Company to vote such shares on any given issue in accordance with the majority shareholder vote on that issue). No instruction shall be deemed given and no discretionary proxy shall be given with respect to any matter as to which the Company informs the Depositary it does not wish such proxy given or if the proposal has, in the discretion of the Depositary, a materially adverse effect on the rights of the holders of ADRs.

Any holder of ADRs is entitled to revoke any instructions which it has previously given to the Depositary by filing with the Depositary a written revocation or duly executed instructions bearing a later date at any time prior to 3:00 p.m., New York time, on May 30, 2007. No instructions, revocations or revisions thereof shall be accepted by the Depositary after that time.

IF YOU WANT YOUR VOTE TO BE COUNTED, THE DEPOSITARY MUST RECEIVE YOUR VOTING INSTRUCTIONS PRIOR TO 3:00 P.M. (NEW YORK CITY TIME) ON MAY 30, 2007.

JPMORGAN CHASE BANK, N.A. | |

Depositary | |

| April 27, 2007 | |

| New York, New York | |

2

Tenaris S.A.

Société Anonyme Holding

46A, avenue John F. Kennedy

L-1855, Luxembourg

RCS Luxembourg B 85 203

Notice of the Annual General Meeting and Extraordinary General Meeting of Shareholders to be held on June 6, 2007

Notice is hereby given to holders of shares of common stock of Tenaris S.A. (the “Company”) that the Annual General Meeting of Shareholders will be held on June 6, 2007, at 11:00 a.m. (Central European Time), and that an Extraordinary General Meeting will be held immediately after conclusion of the Annual General Meeting. Both meetings will be held at 46A, avenue John F. Kennedy L-1855 Luxembourg. In the Annual General Meeting, shareholders will vote with respect to the items listed below under the heading “Annual General Meeting of Shareholders”. At the Extraordinary General Meeting, shareholders will vote with respect to the items listed below under the heading “Extraordinary General Meeting of Shareholders”.

Agenda

Annual General Meeting of Shareholders

| 1. | Consideration of the Board of Directors’ and independent auditor’s reports on the Company’s consolidated financial statements. Approval of the Company’s consolidated financial statements for the years ended December 31, 2006, 2005 and 2004. |

| 2. | Consideration of the Board of Directors’ and independent auditors’ reports on the Company’s annual accounts. Approval of the Company’s annual accounts as at December 31, 2006. |

| 3. | Allocation of results and approval of dividend payment. |

| 4. | Discharge to the members of the Board of Directors. |

| 5. | Election of the members of the Board of Directors. |

| 6. | Compensation of the members of the Board of Directors. |

| 7. | Authorisation to the Board of Directors to cause the distribution of all shareholder communications, including its shareholder meeting and proxy materials and annual reports to shareholders, by such electronic means as is permitted by any applicable laws or regulations. |

Appointment of the independent auditors and approval of their fees.Pursuant to the Company’s Articles of Association, resolutions at the Annual General Meeting of Shareholders will be passed by simple majority vote, irrespective of the number of shares present or represented.

Extraordinary General Meeting of Shareholders

1. The renewal of the validity period of the Company’s authorized share capital for a period starting on the date of the general meeting of shareholders and ending on the fifth anniversary of the date of the publication in the Mémorial of the deed recording the minutes of such meeting and of the authorisation to the Board to issue shares from time to time within the limits of such authorised share capital against contribution in cash, in kind or by way of incorporation of reserves, at an amount that may not be less than the par value and may include such issue premium as the Board shall decide, while reserving to existing shareholders the preferential right to subscribe for such newly issued shares, except:

3

a. in circumstances in which the shares are issued for a consideration other than cash;

b. with respect to shares issued as compensation to directors, officers, agents, or employees of the Company, its subsidiaries or affiliates; and

c. with respect to shares issued to satisfy conversion or option rights created to provide compensation to directors, officers, agents or employees of the Company, its subsidiaries or affiliates.

Any shares to be issued for the purposes set forth in (b) and (c) may not exceed 1.5% of the Company’s issued share capital.

2. The waiver of any preferential subscription rights of existing shareholders provided for by law and the authorisation to the Board to suppress any preferential subscription rights of existing shareholders, each time with respect to issuances of shares under (a), (b) and (c) above, and the acknowledgement and approval of the report of the Board on the authorised share capital and the proposed waiver and authorisation to the Board with respect to such issuances

Pursuant to the Company’s Articles of Association, an extraordinary general meeting of shareholders convened to consider the renewal of the validity period of the Company’s authorised share capital and the waiver of, suppression of, and authorisation to suppress or limit, preferential subscription rights by the Company’s existing shareholders may only validly vote on such amendment on the first call if at least half of the share capital is present or represented. If the required quorum is not met, a second meeting may be convened by means of notices published twice, not less than twenty (20) days apart and in any case twenty (20) days before the meeting, in the Mémorial C, Recueil des Sociétés et Associations (Luxembourg Official Gazette), two Luxembourg newspapers and such other publications as are required under article 19 of the Company’s Articles of Association. The second meeting may validly decide on the matter, regardless of the quorum present or represented. In each case, resolutions may only be passed by a two-thirds majority of the votes of the shareholders present or represented.

4

Procedures for Attending the Meetings

Holders of shares wishing to attend the meetings must obtain an admission ticket by depositing their certificates representing their common stock, not later than 4:00 p.m. (local time) on June 1st, 2007, at the Company’s office in Luxemburg or at the offices of any of the Company’s subsidiaries set forth below:

| Luxembourg: | 46A, Avenue John F. Kennedy |

| L-1855 Luxembourg | |

| Argentina: | Carlos María della Paolera 299, piso 16° |

| (C1001ADA) Buenos Aires | |

| Attn: Horacio de las Carreras and/or Eleonora Cimino | |

| Italy: | c/o Dalmine S.p.A. |

| Piazza Caduti 6 luglio 1944 n. 1 24044 | |

| Dalmine (BG) | |

| Attn: Marco Tajana and/or Teresa Gaini | |

| Mexico: | c/o Tubos de Acero de México S.A. |

| Campos Eliseos 400-17 | |

| Col. Chapultepec Polanco | |

| 11560 Mexico D.F. | |

| Attn: Félix Todd and/or Luis Armando Leviaguirre |

Holders of shares through fungible securities accounts wishing to attend the meetings must present a certificate (issued by the financial institution or professional depositary holding such shares) evidencing such deposit and certifying the number of shares recorded in the relevant account as of June 1st, 2007. Such certificate must be filed no later than 4:00 p.m. (local time) on June 1st, 2007, at any of the addresses indicated above and, in the case of shares held in Mexico, with S.D. Indeval, S.A. de C.V. (Paseo de la Reforma #255, 2o. y 3er. piso Col. Cuauhtémoc, Mexico City).

Holder of shares as of June 1st, 2007, may also vote by proxy. To vote by proxy, holders must file the required certificate and a completed proxy form not later than 4:00 p.m. (local time) on June 1st, 2007 with any of the addresses indicated above or, in the case of shares held in Mexico, with S.D. Indeval, S.A. de C.V, in Mexico City.

Holders of American Depositary Receipts (“ADRs”) as of April 30, 2007, which continue to hold such ADRs on May 22, 2007, are entitled to instruct JPMorgan Chase Bank, N.A., as Depositary (the “Depositary”), as to the exercise of the voting rights pertaining to the Company’s shares of Common Stock represented by such holder’s ADRs. Although voting instructions are sent to holders and proxy materials are available at our website beginning on May 5, 2007, only those holders of ADRs as of each of April 30, 2007 and May 22, 2007 will be entitled to provide the Depositary with voting instructions. Notwithstanding that holders of ADRs must have held ADRs on each such date, in order to avoid the possibility of double vote, only those positions on May 22, 2007, will be counted for voting instruction purposes. Eligible ADR holders who desire to vote at the Meeting must complete, date and sign a proxy form and return it to JPMorgan Chase Bank, N.A. (the “Depositary”), P.O. Box 3500, South Hakensack, NJ 07606-3500, U.S.A., by 3:00 p.m., New York City time, on May 30, 2007.

5

The Shareholder Meeting Brochure and Proxy Statement (which contains reports on each item of the agenda for the meetings, and further details on voting procedures) and the forms furnished by the Company in connection with the meetings, may be obtained at any of the addresses indicated above, but also from the Depositary, Borsa Italiana SpA (Piazza degli Affari 6, 20123, Milan, Italy) and S.D. Indeval S.A. de C.V., as from May 5, 2007, between 10:00 a.m. and 5:00 p.m. (local time).

Copies of the Shareholder Meeting Brochure and Proxy Statement and the forms are also available at www.tenaris.com/investors. Copies of the Company’s 2006 annual reports (including the Company’s financial statements for the years ended 2006, 2005 and 2004, the Board of Directors and independent auditors reports, and the documents referred to in the preceding sentence) may also be obtained free of charge at the Company's registered office in Luxembourg.

Cecilia Bilesio

Secretary to the Board of Directors

April 27, 2007

Luxembourg

6

Tenaris S.A.

Société Anonyme Holding

46A, avenue John F. Kennedy

L-1855, Luxembourg

RCS Luxembourg B 85 203

Shareholder Meeting Brochure and Proxy Statement

Annual General Meeting and Extraordinary General Meeting of Shareholders to be held on June 6, 2007

This Shareholder Meeting Brochure and Proxy Statement is furnished by Tenaris, S.A. (the “Company”) in connection with the Annual General Meeting of Shareholders and the Extraordinary General Meeting of Shareholders to be both held, for the purposes set forth in the accompanying Notice of the Annual General Meeting and Extraordinary General Meeting of Shareholders (the “Notice”), on June 6, 2007 starting at 11:00 a.m., at 46A, avenue John F. Kennedy L-1855 Luxembourg.

As of April 27, 2007, there were issued and outstanding 1,180,536,830 shares of common stock, US$1 par value, of the Company (the “Common Stock”), including shares of Common Stock (the “Deposited Shares”) deposited with Fortis Bank Luxembourg S.A., as agent for JPMorgan Chase Bank, N.A., as depositary (the “Depositary”), under the Deposit Agreement, dated as of November 11, 2002, as amended on April 3, 2006 (the “Deposit Agreement”) among the Company, the Depositary and all holders from time to time of American Depositary Receipts (the “ADRs”) issued thereunder. The Deposited Shares are represented by American Depositary Shares), which are evidenced by the ADRs (one ADR equals two Deposited Shares).

Each holder of shares of Common Stock is entitled to one vote per share. Holders of shares that hold shares through fungible securities accounts and wish to attend the Meetings must present a certificate (issued by the financial institution or professional depositary holding such shares) evidencing such deposit and certifying the number of shares recorded in the relevant account on June 1st, 2007. Such certificate must be filed no later than 4:00 p.m. (local time) on June 1st, 2007, at any of the addresses indicated in the Notice, or, in the case of shares held in Mexico, with S.D. Indeval, S.A. de C.V., in Mexico City.

Holders of shares as of June 1st, 2007, may also vote by proxy. To vote by proxy, such holders must file the requisite certificate and a completed proxy form not later than 4:00 p.m. (local time), on June 1st, 2007, at any of the addresses indicated in the Notice, or, in the case of shares held in Mexico, with S.D. Indeval, S.A. de C.V., in Mexico City.

Each holder of ADRs as of April 30, 2007, which continues to hold such ADRs on May 22, 2007, is entitled to instruct JPMorgan Chase Bank, N.A., as Depositary (the “Depositary”), as to the exercise of the voting rights pertaining to the Company’s shares of Common Stock represented by such holder’s ADRs. Although voting instructions are sent to holders and proxy materials are available at our website beginning on May 5, 2007, only those Holders of record as of each of April 30, 2007 and May 22, 2007 will be entitled to provide the Depositary with voting instructions. Notwithstanding that holders of ADRs must have held ADRs on each such date, in order to avoid the possibility of double vote, only those positions on May 22, 2007 will be counted for voting instruction purposes. Eligible holders of ADRs who desire to have their shares represented by their ADRs voted at the Meeting must complete, date and sign a proxy form and return it to JPMorgan Chase Bank, N.A., P.O. Box 3500, South Hakensack, NJ 07606-3500, U.S.A. If the Depositary receives properly completed instructions by 3:00 p.m., New York City time, on May 30, 2007, then it shall vote or cause to be voted the shares underlying such ADRs in the manner prescribed by the instructions. However, if by 3:00 p.m., New York time, on May 30, 2007, the Depositary receives no instructions from the holder of ADRs, or the instructions are not in proper form, then the Depositary shall deem such holder to have instructed the Depositary to vote the underlying shares of Common Stock of any such ADRs in favor of any proposals or recommendations of the Company, for which purposes the Depositary shall issue a discretionary proxy to a person appointed by the Company to vote such shares in favor of any proposals or recommendations of the Company (including any recommendation by the Company to vote such shares on any given issue in accordance with the majority shareholder vote on that issue). No instruction shall be deemed given and no discretionary proxy shall be given with respect to any matter as to which the Company informs the Depositary it does not wish such proxy given or if the proposal has, in the discretion of the Depositary, a materially adverse effect on the rights of the holders of ADRs. Any holder of ADRs is entitled to revoke any instructions which it has previously given to the Depositary by filing with the Depositary a written revocation or duly executed instructions bearing a later date at any time prior to 3:00 p.m., New York time, on May 30, 2007. No instructions, revocations or revisions thereof shall be accepted by the Depositary after that time.

7

Due to regulatory differences and market practices in each country where the Company’s shares or ADRs are listed, the holders of shares traded on the Argentine and Italian stock exchanges who have requested admission to the meetings, or who have issued a voting proxy, must have their shares blocked for trading until the date of the meetings, while holders of shares traded in the Mexican stock exchange and holders of ADRs traded in the New York stock exchange need not have their shares or ADRs, as the case may be, blocked for trading. However, the votes of holders of shares traded in the Mexican stock exchange who sell their shares between May 30, 2007 and June 6, 2006, shall be disregarded.

The meetings will appoint a chairperson pro tempore to preside over them. The chairperson pro tempore will have broad authority to conduct the meetings in an orderly and timely manner and to establish rules for shareholders who wish to address either meeting; the chairperson may exercise broad discretion in recognizing shareholders who wish to speak and in determining the extent of discussion on each item of the agenda.

Pursuant to the Company’s Articles of Association, resolutions at the Annual General Meeting of Shareholders will be passed by majority vote, irrespective of the number of shares present or represented. The extraordinary general meeting of shareholders convened to consider the renewal of the validity period of the Company’s authorized share capital, and the waiver of, suppression of, and authorisation to suppress or limit, preferential subscription rights by the Company’s existing shareholders may only validly meet on the first call if at least half of the share capital is present or represented. If the required quorum is not met, a second meeting may be convened by means of notices published twice, not less than twenty (20) days apart and in any case twenty (20) days before the meeting, in the Mémorial C, Recueil des Sociétés et Associations (Luxembourg Official Gazette), two Luxembourg newspapers and such other publications as are required under article 19 of the Company’s Articles of Association. The second meeting may validly decide on the matter, regardless of the quorum present or represented. In each case, resolutions may only be passed by a two-thirds majority of the votes of the shareholders present or represented.

8

The meetings are called to address and vote on the following agenda:

Annual General Meeting of Shareholders

1. Consideration of the Board of Directors’ and Independent Auditor’s Reports on the Company’s Consolidated Financial Statements. Approval of the Company’s Consolidated Financial Statements for the Years Ended December 31, 2006, 2005 and 2004.

The Board of Directors recommends a vote FOR approval of the Company’s consolidated financial statements for the fiscal years ended December 31, 2006, 2005 and 2004, after due consideration of the reports from each of the Board of Directors and the independent auditors on such consolidated financial statements. The consolidated balance sheet of the Company and its subsidiaries at December 31, 2006, 2005 and 2004 and the related consolidated statement of income, consolidated statement of changes in shareholders’ equity, consolidated cash flow statement and notes to the consolidated financial statements, the independent auditors’ report on such consolidated financial statements and management’s discussion and analysis on the Company’s results of operations and financial condition are included in the Company’s 2006 annual report, a copy of which is available on our website at www.tenaris.com/investors and may also be obtained upon request at 1-800-990-1135 (if you are in the United States) or +1-201-680-6630 (if you are outside the United States).

2. Consideration of the Board of Directors’ and Independent Auditors’ Reports on the Company’s annual accounts. Approval of the Company’s annual accounts as at December 31, 2006.

The Board of Directors recommends a vote FOR approval of the Company’s annual accounts as of, and for the fiscal year ended, December 31, 2006, after due consideration of the report from each of the Board of Directors and the independent auditors on such annual accounts. These documents are included in the Company’s 2006 annual report, a copy of which is available on our website at www.tenaris.com/investors and may also be obtained upon request at 1-800-990-1135 (if you are in the United States) or +1-201-680-6630 (if you are outside the United States).

3. Allocation of Results and Approval of Dividend Payment.

The Board of Directors recommends a vote FOR approval of a dividend payable in U.S. dollars on June 21, 2007, in the amount of US$0.30 per share of Common Stock currently issued and outstanding and US$0.60 per ADR currently issued and outstanding. All of the aggregate amount of US$354,161,049 to be distributed as dividends are to be paid from profits of the year ended December 31, 2006. The balance of the fiscal year’s profits will be allocated to the Company’s retained earnings account.

Upon approval of this resolution, it is proposed that the Board of Directors determine, in its discretion, the terms and conditions of the dividend payment, including the applicable record date.

4. Discharge to the Members of the Board of Directors.

In accordance with applicable Luxembourg law and regulations, it is proposed that, upon approval of the Company’s accounts for the year ended December 31, 2006, the members of Board of Directors be discharged of any responsibilities in connection with the management of the Company’s affairs during such year.

9

5. Election of the Board of Directors’ Members.

The Company’s Articles of Association provide for the annual election by the holders of Common Stock of a Board of Directors of not less than five and not more than fifteen members. Members of the Board of Directors have a term of office of one year, but may be reappointed.

Under applicable U.S. laws and regulations, effective on July 15, 2005, the Company is required to have an audit committee comprised solely of directors who are independent.

The present Board of Directors of the Company consists of nine Directors. Three members of the Board of Directors (Messrs. Jaime Serra Puche, Amadeo Vázquez y Vázquez and Roberto Monti) qualify as independent members under the Company’s Articles of Association and applicable law.

It is proposed that the size of the Board of Directors be increased to ten members, with (1) the current nine members of the Board of Directors being re-elected, and (2) Mr. Carlos Condorelli (presently, the Company’s chief financial officer) be also appointed as a member of the Board of Directors.

Set forth below is summary biographical information of each of the candidates:

| 1. | Mr. Roberto Bonatti. Mr. Bonatti is a member of our board of directors. Mr. Bonatti has been involved in Techint Group businesses, specifically in the engineering and construction and corporate sectors, throughout his career. He was first employed by the Techint Group in 1976, as deputy resident engineer in Venezuela. In 1984, he became a director of San Faustín, and, since 2001, he has served as its president. In addition, Mr. Bonatti currently serves as president of Techint Compañía Técnica Internacional S.A.C.I. of Argentina and Tecpetrol S.A. of Argentina and as a director of Tenaris, Siderca and Siderar. Mr. Bonatti is an Italian citizen. |

| 2. | Mr. Carlos Condorelli.- Mr. Condorelli currently serves as our chief financial officer, a position that he assumed in October 2002. He is also a board member of Ternium. He began his career within the Techint group in 1975 as an analyst in the accounting and administration department of Siderar. He has held several positions within Tenaris and other Techint group companies, including finance and administration director of Tubos de Acero de México, S.A. (“Tamsa”) and president of the board of directors of Empresa Distribuidora La Plata S.A., or Edelap, an Argentine utilities company. Mr. Condorelli is an Argentine citizen. |

| 3. | Mr. Carlos Manuel Franck. Mr. Franck is a member of our board of directors. He is president of Santa María S.A.I.F., Inverban S.A. vice president of Siderca SAIC and a member of the board of directors of Techint Financial Corporation N.V., Industrial Investments Inc., Siderar S.A., Tecpetrol S.A. and Tecgas N.V. He has financial, planning and control responsibilities in subsidiaries of San Faustín N.V. Mr. Franck is an industrial engineer and an Argentine citizen. |

| 4. | Mr. Bruno Marchettini. Mr. Marchettini has retired from executive positions, but continues to be the referent advisor in steel technology matters for the Techint Group. He is member of the board of directors of San Faustín N.V., Ternium S.A. and Siderar SA.I.C. Mr. Marchettini is an Italian citizen. |

| 5. | Mr. Roberto Monti*. Mr. Monti is a non-executive chairman of Trefoil Limited., member of the board of directors of Petrobras Energia, Transocean Offshore Drilling and of John Wood Group PLC. Served as vice president of Exploration and Production of Repsol YPF and chairman and CEO of YPF. He was also president of Dowell, a subsidiary of Schlumberger and president of Schlumberger Wire & Testing division for East Hemisphere Latin America. Mr. Monti is an Argentine citizen. |

10

| 6. | Mr. Gianfelice Mario Rocca. Mr. Rocca is chairman of the board of directors of San Faustín, a member of the board of directors of I.I.I. Industrial Investments Inc., Tenaris S.A., Dalmine S.p.A., Tamsa. and Ternium S.A., president of the Humanitas Group and president of the board of directors of Techint Compagnia Tecnica Internazionale S.p.A., Techint S.A. de C.V. In addition, he sits on the board of directors or executive committees of several companies, including Sirti S.p.A., Ras, RCS Quotidiani, Fastweb and Buzzi Unicem. He is vice president of Confindustria, the leading association of Italian industrialists. He is a member of the European Advisory Board of the Harvard Business School, the Trilateral Commission. Mr. Rocca graduated in Physics cum laude at the University of Milan and holds a postgraduate degree from the Harvard Business School. Mr. Rocca is an Italian citizen. |

| 7. | Mr. Paolo Rocca. Mr. Rocca is chairman of our board of directors and our chief executive officer. He is also chairman of the board of directors of Tamsa and of Dalmine, S.p.A. and vice president of Confab Industrial S.A. He is also chairman of the board of Ternium S.A. and director and vice president of San Faustín N.V. and director of Techint Financial Corporation N.V. Mr. Rocca is member of the Executive Committee of the IISI (International Iron and Steel Institute) and member of the International Advisory Committee of the NYSE (New York Stock Exchange) Mr. Rocca is an Italian citizen. |

| 8. | Mr. Jaime Serra Puche*. Mr. Serra Puche is chairman of SAI Consultores, and a member of the board of directors of Chiquita Brands International, The Mexico Fund, Vitro and Grupo Modelo. Mr. Serra Puche served as Mexico’s Undersecretary of Revenue, Secretary of Trade and Industry, and Secretary of Finance. He led the negotiation and implementation of NAFTA. Mr. Serra Puche is a Mexican citizen. |

| 9. | Mr. Amadeo Vázquez y Vazquez*. Mr. Vázquez y Vázquez is a director of Gas Natural Ban, S.A., third vice president of Cámara Argentina de Comercio, communications advisor of Departamento de Infraestructura de la Unión Industrial Argentina, and Vocal of the Executive Committee of Asociación Empresaria Argentina. He was also chairman of the board of directors of Telecom Argentina S.A. Mr. Vázquez y Vázquez is an Argentine citizen. |

| 10. | Mr. Guillermo F. Vogel. Mr. Vogel is vice chairman of Tamsa, vice chairman of the American Iron & Steel Institute, chairman of the North American Steel Council, chairman of Grupo Collado, vice chairman of Estilo y Vanidad S.A. de C.V. and a Director of the North American Competitiveness Council, the International Iron and Steel Institute and HSBC (México) being also a member of its audit committee . Mr. Vogel is a Mexican citizen. |

* Independent directors

Each elected director will hold office until the next annual general meeting of shareholders. Under the current Company’s Articles of Association, such meeting is required to be held on June 4, 2008.

The Company’s Board of Directors met nine times during 2006. On January 31, 2003, the Board of Directors created an Audit Committee pursuant to Article 11 of the Articles of Association. As permitted under applicable laws and regulations, the Board of Directors does not have any executive, nominating or compensation committee, or any committees exercising similar functions.

11

6. Compensation of the Members of the Board of Directors.

It is proposed that each of the members of the Board of Directors receive an amount of US$ 70,000 as compensation for their services during the fiscal year 2007. It is further proposed that the Chairman of the Audit Committee receive an additional fee of US$10,000 and that the other members of the Board of Directors who are members of such Committee receive an additional fee of US$50,000.

7. Authorisation to the Board of Directors to Cause the Distribution of all Shareholder Communications, Including its Shareholder Meeting and Proxy Materials and Annual Reports to Shareholders, by Such Electronic Means as is Permitted by any Applicable Laws or Regulations.

In order to expedite shareholder communications and ensure their timely delivery, the Board of Directors recommends that it be authorized to cause the distribution of all shareholder communications, including its shareholder meeting and proxy materials and annual reports to shareholders (either in the form of a separate annual report containing financial statements of the Company and its consolidated subsidiaries or in the form of a Form 20-F or similar document, as filed with the securities authorities or stock markets) by such electronic means as are permitted or required by any applicable laws or regulations (including any interpretations thereof), including, without limitation, by posting such communication on the Company's web site, or by sending an email with attachment in a widely used format or with a hyperlink to the applicable filing by the Company on the website of the above referred authorities or stock markets, or by any other existing or future electronic means of communication.

8. Appointment of Independent Auditors and Approval of their Fees.

Based on the recommendation from the Audit Committee, the Board of Directors recommends a vote FOR the appointment of PricewaterhouseCoopers (acting, in connection with the Company’s annual accounts required under Luxembourg law, through PricewaterhouseCoopers S.àr.l., Réviseur d'entreprises, and, in connection with the Company’s annual and interim financial statements required under the laws of any other relevant jurisdiction, through Pricewaterhouse & Co. S.R.L.) as the Company’s independent auditors for the fiscal year ending December 31, 2007, to be engaged until the next annual general meeting that will be convened to resolve on the 2007 accounts.

In addition, the Board of Directors recommends a vote FOR approval of an amount up to US$5’083,000 payable to the independent auditors as fees for audit services and audit related services to be rendered during the fiscal year ending December 31, 2007 and to authorise the Audit Committee to increase the independent auditors’ fees should it conclude that circumstances would merit any such change. Such fees cover the audit of the Company’s consolidated financial statements and its annual accounts, the audit of the Company’s internal controls over financial reporting as mandated by the Sarbanes-Oxley Act of 2002, and other services.

12

Extraordinary General Meeting of Shareholders

1. The renewal of the validity period of the company’s authorized Share Capital for a period starting on the date of the General Meeting of Shareholders and ending on the fifth anniversary of the date of the publication in the Mémorial of the deed recording the minutes of such meeting and of the authorisation to the Board to issue shares from time to time within the limits of such authorised Share Capital against contribution in cash, in kind or by way of incorporation of reserves, at an amount that may not be less than the par value and may include such issue premium as the Board shall decide, while reserving to existing shareholders the preferential right to subscribe for such newly issued shares, except:

a. In circumstances in which the shares are issued for a consideration other than cash;

b. With respect to shares issued as compensation to directors, officers, agents, or employees of the company, its subsidiaries or affiliates; and

c. With respect to shares issued to satisfy conversion or option rights created to provide compensation to directors, officers, agents or employees of the company, its subsidiaries or affiliates.

Any shares to be issued for the purposes set forth in (b) and (c) may not exceed 1.5% of the company’s issued share capital.

2. The waiver of any preferential subscription rights of existing shareholders provided for by law and the authorisation to the Board to suppress any preferential subscription rights of existing shareholders, each time with respect to issuances of shares under (a), (b) and (c) above, and the acknowledgement and approval of the report of the Board on the authorised Share Capital and the proposed waiver and authorisation to the Board with respect to such issuances.

The Board of Directors believes that the proposed renewal of the validity period of the Company’s authorized share capital, the authorisation to the Board of Directors to issue shares within the authorized share capital and the waiver of, suppression of, and authorisation to suppress or limit, preferential subscription rights by the Company’s existing shareholders is in the best interests of the Company and its shareholders and accordingly recommends a vote FOR this proposal.

Shareholders are reminded that the authorized share capital, the authorisation to the Board of Directors to issue shares within the authorized share capital and the exceptions set forth under (a), (b) and (c) are currently contained in the Company’s Articles of Association and are therefore simply renewed.

The Board of Directors is of the opinion that the successful implementation and development of the Company and its group’s long term strategy will depend, among other factors, on the Company’s ability to grow through acquisitions or other investments on the best possible terms, and that the existence of the preferential subscription rights provided for by Luxembourg law for the benefit of existing shareholders will seriously reduce the flexibility of the Company to finance through issuances of shares its operations and potential growth; in addition, the preferential subscription rights procedure contemplated by the Luxembourg law would, in some cases, risk delaying increases in share capital and issuances of new shares at times when timing would be of the essence.

13

Accordingly, the Board of Directors believes it to be in the Company’s best interest that the Board of Directors be authorized to negotiate and conclude acquisitions, investments, joint venture and other transactions using shares or rights to shares (either at or below market price, and including by way of incorporation of reserves) of the Company’s capital as acquisition currency. Similarly, the Board of Directors believes that the interest of the Company requires that maximum flexibility be granted so that the Company be able to react quickly and without delay to any suitable acquisition, investment, joint venture or other strategic proposals or projects and/or to secure financing in connection thereto by issuing or offering to issue shares for consideration other than cash.

The Board of Directors also believes that the interest of the Company requires that the Board be authorized to issue such shares or rights thereto either at or below market price, as it may be necessary or convenient in light of the facts and circumstances of the transaction in question or its strategic significance.

The Board of Directors further believes that in order for the Company and its group to maximize its ability to attract and retain valuable directors, managers, officers, agent or employees, it is in the best interest of the Company to retain the flexibility to elect to offer to such persons shares or conversion, option or similar plans or incentive programs permitting the subscription of shares in the Company. Such plans and programs, by serving the purpose of facilitating the recruitment or retention of key employees and executives, would enable the Company and its group to secure, further strengthen and develop its market position and continue the implementation of the Company’s long term strategy.

Accordingly, the Board of Directors believes that issuances of shares as compensation to, or to satisfy conversion or option rights created to provide compensation to directors, officers, agents or employees of the Company, its subsidiaries or its affiliated companies should be made by the Board upon such terms and conditions as it deems fit and without reserving preferential subscription rights to existing shareholders; provided, however, that any such issuances shall be limited to 1.5% of the Company’s issued share capital from time to time.

The Company anticipates that the next Annual General Meeting of Shareholders will be held on June 4, 2008. Any holder of shares who intends to present a proposal to be considered at the next Annual General Meeting must submit the proposal in writing to the Company at any of the offices indicated in the Notice not later than 4:00 P.M. (local time) on March 31, 2008, or in accordance with the procedures set forth under applicable Luxembourg law, in order for such proposal to be considered for inclusion on the agenda for the 2008 annual general meeting of shareholders.

PricewaterhouseCoopers are the Company’s independent auditors. A representative of the independent auditors will be present at the Meetings to respond to questions.

Cecilia Bilesio

Secretary to the Board of Directors

14

Annual Report 2006 | ||

| Company profile | ||

| Leading indicators | ||

| Chairman’s letter | ||

| Business review | ||

| Communities and environment review | ||

| Corporate governance | ||

| Board of directors and executive officers | ||

| Operating and financial review | ||

| Consolidated financial statements | ||

| Report and audited annual accounts of Tenaris S.A. | ||

| (Luxembourg GAAP) | ||

| Corporate information | ||

Cautionary statement

Some of the statements contained in this Annual Report are “forward-looking statements”. Forward-looking statements are based on management’s current (February 2007) assumptions and involve known and unknown risks that could cause actual results, performance or events to differ materially from those expressed or implied by those statements. These risks include, but are not limited to, risks arising from uncertainties as to future oil and gas prices and their impact on the investment programs by oil and gas companies.

Certain figures included in this Annual Report have been subject to rounding adjustments. Accordingly, figures shown as totals in tables may not be the sum of the figures that precede them, and percentages in the text may not total 100% or may not be the sum of the percentages that precede them.

15

Company profile

Tenaris is the leading supplier of tubes and related services for the world’s energy industry, as well as for other industrial applications. Our mission is to deliver value to our customers through product development, manufacturing excellence, and supply chain management. We minimize risk for our customers and help them reduce costs, increase flexibility and improve time-to-market. Our employees around the world are committed to continuous improvement by sharing knowledge across a single global company.

16

Leading indicators

| 2006 | 2005 | 2004 | ||||||||

| SALES VOLUMES (thousands of metric tons) | ||||||||||

| Seamless pipes | 2,919 | 2,870 | 2,646 | |||||||

| Welded pipes | 578 | 501 | 316 | |||||||

Total steel pipes | 3,497 | 3,371 | 2,963 | |||||||

| PRODUCTION VOLUMES (thousands of metric tons) | ||||||||||

| Seamless pipes | 3,013 | 2,842 | 2,631 | |||||||

| Welded pipes | 642 | 476 | 366 | |||||||

Total steel pipes | 3,655 | 3,318 | 2,997 | |||||||

| FINANCIAL INDICATORS (millions of USD) | ||||||||||

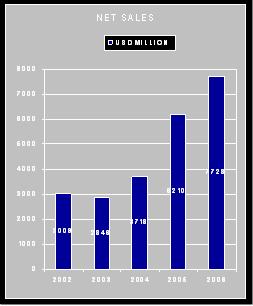

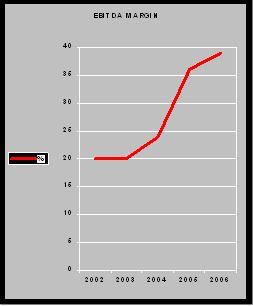

| Net sales | 7,728 | 6,210 | 3,718 | |||||||

| Operating income | 2,792 | 1,946 | 806 | |||||||

| EBITDA (1) | 3,047 | 2,160 | 891 | |||||||

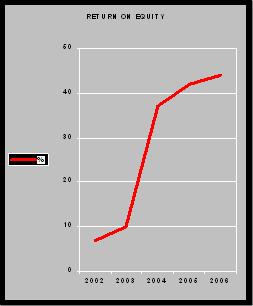

| Net income | 2,059 | 1,387 | 805 | |||||||

| Cash flow from operations | 1,811 | 1,295 | 98 | |||||||

| Capital expenditures | 441 | 284 | 183 | |||||||

| BALANCE SHEET (millions of USD) | ||||||||||

| Total assets | 12,595 | 6,706 | 5,662 | |||||||

| Total financial debt | 3,651 | 1,010 | 1,259 | |||||||

| Net financial debt (2) | 2,095 | 183 | 828 | |||||||

| Total liabilities | 6,894 | 2,930 | 3,001 | |||||||

| Shareholders’ equity including minority interest | 5,702 | 3,776 | 2,661 | |||||||

| PER SHARE / ADS DATA (USD per share / per ADS) (3) | ||||||||||

Number of shares outstanding (4) (thousands of shares) | 1,180,537 | 1,180,537 | 1,180,537 | |||||||

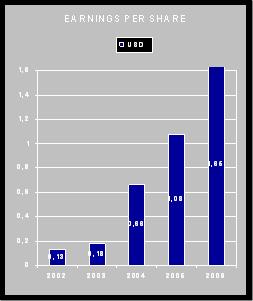

| Earnings per share | 1.65 | 1.08 | 0.66 | |||||||

| Earnings per ADS | 3.3 | 2.16 | 1.33 | |||||||

| Dividends per share (5) | 0.3 | 0.3 | 0.17 | |||||||

| Dividends per ADS (5) | 0.6 | 0.6 | 0.34 | |||||||

| ADS Stock price at year-end | 49.89 | 22.9 | 9.78 | |||||||

| Number of employees (4) | 21,751 | 17,693 | 16,447 | |||||||

(1) Defined as operating income plus depreciation and amortization charges taken before non-recurring gains derived from the Fintecna arbitration award in 2004.

(2) Defined as borrowings less cash and cash equivalents and other current investments.

(3) As of April 26, 2006, the ratio of ADS to ordinary shares was changed from 1:10 to 1:2.

(4) As of December 31.

(5) Proposed or paid in respect of the year.

17

Chairman’s letter

Dear Shareholders,

2006 was a momentous year for Tenaris. Earnings, cash flow from operations and investments in operations reached record levels. After many years of exclusion from the US market, we made a decisive move to establish ourselves as the leading player in North America through the acquisition of Maverick Tube Corporation, concluded in October, and the pending acquisition of Hydril Company, announced earlier this month. In China, we started up our first industrial operation in the country with a premium connection threading and coupling facility at Qingdao, with which we will consolidate our position as a supplier of products for complex drilling operations in this large and growing market.

In Romania, we completed the integration of the Donasid steel shop we acquired in 2005 into our European operations and bought out the remaining minority interests in Silcotub. In Italy, we began commissioning our new power generation facility at Dalmine and concluded the sale of a 75% participation in Dalmine Energie, our energy trading business, establishing a partnership with E.ON, one of Europe’s leading energy companies. In Russia, we penetrated the market for pipes for complex drilling operations with sales of our TenarisBlue® premium connections for use in Gazprom’s Astrakhan and Orenburg fields and for Lukoil’s Narianmar operations. In the Middle East, we were able to draw on our long-standing experience in the region and comprehensive range of products to more than double sales as the market took off.

The acquisition of Maverick transforms our position in North America, the world’s largest market for pipes used in the drilling, completion and production of oil and gas, accounting for over 40% of all OCTG products consumed worldwide. That of Hydril would accelerate the transformation by making us the leader in premium connection technology for complex applications. More than one-third of our sales will be in this region. We are building a solid regional platform to provide customers here the service, quality and technology that our global customers are used to receiving elsewhere in the world. In a market where demand for standard products for mature fields complements that for specialized products for some of the most innovative offshore and non-conventional drilling operations anywhere in the world, we will supply a full range of products to cover all the applications of our customers, all made to a single, exacting, quality standard.

Our capital investment program is advancing as planned. We are increasing the capacity of our globally integrated industrial system to deliver the specialized products used in the world’s most demanding applications with new heat treatment, premium threading and R&D and inspection facilities. With Hydril, we would further enhance our capabilities in this area and would be able to offer an unparalleled range of premium connections to our customers worldwide. Our investments in R&D continue to increase as we develop and test new products and improve mill processes. In November, we opened a new R&D center in Veracruz, expanding our global network of research centers.

Global demand for oil and gas continues to grow. Decline rates at producing oil and gas fields are higher than in the past as the fields mature. To keep pace with global demand and offset decline rates, investment is increasing in the exploration and development of new fields in complex operating environments requiring the use of specialized products and services. The capacity of the offshore drilling fleet is set to see a strong increase to service new deepwater projects, as is the number of rigs drilling wells of depths greater than 15,000 feet.

As global capacity in the tubular sector increases to meet higher demand from the oil and gas industry and other sectors, Tenaris is consolidating its position as industry leader and laying solid foundations for further growth. Our unique global positioning, our focus on manufacturing high quality products for use in the most complex applications, our ability to deliver a full range of products with integrated supply chain services under long-term agreements, our decisive move to expand in North America, all serve to differentiate us from our competitors.

We will continue to work hard to reinforce our competitive position and to build on the expansion and transformation we have managed over the past 15 years. With 29 industrial centers in 12 countries and 21,800 employees, we are engaged in a project integrating industrial, R&D, systems and management operations to cement the common identity of a global enterprise, while at the same time contributing to the sustainable development of the local communities where we have our roots.

Our financial results reflect the benefits of a strong market and the positioning we have built over a long period. Net sales for the year rose to USD 7.7 billion and EBITDA to USD 3.0 billion. Earnings per share rose 52% to USD 1.65, or USD 3.30 per ADS, following on from last year’s 63% growth. As we are investing to position the company for further growth, we propose to maintain the dividend at last year’s level and pay USD 0.30 per share (USD 0.60 per ADS) in June.

We welcome all the new employees who have joined us this year. The expansion in North America and the new operation in China add further diversity to our workforce and will strengthen it. The integration process is under way and is adding to the high workload of a demanding market. I want to thank all of our employees for their commitment and unstinting efforts and also express my thanks to our customers, suppliers and shareholders for their continuous support and confidence in Tenaris.

February 28, 2007

Paolo Rocca

18

Business review

Market background and outlook

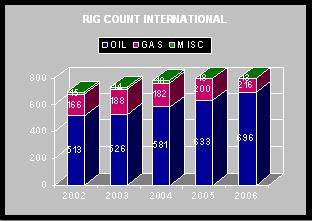

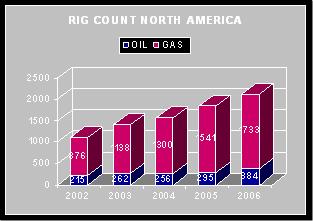

In 2006, global demand for oil and gas continued to rise reflecting economic growth and the importance of oil and gas in the energy matrix. Encouraged by continuing high levels of oil and gas prices, oil and gas companies throughout the world continued to increase their level of spending and drilling activity to offset declining rates of production from mature fields and to explore and develop new reserves. The international count of active drilling rigs, as published by Baker Hughes, rose steadily quarter on quarter throughout the year to average 952 during the fourth quarter, showing an increase of 9% compared to the same quarter of the previous year matching the average increase for the year overall compared to 2005.

The corresponding percentage annual rig count increases in the US and Canadian markets, which are more sensitive to North American natural gas prices, were 19% and 3% respectively. For the fourth quarter, however, the Canadian rig count registered a 23% decline compared to the fourth quarter of 2005. The US rig count, although up 16% over the fourth quarter of 2005, was flat compared to the third quarter of 2006.

We estimate that global apparent consumption of OCTG (oil country tubular goods) in 2006 grew approximately 14% compared to 2005, and will continue to grow in 2007.

However, the rate of growth is expected to slow from the high rates of the past three years and we are likely to see downwards inventory adjustments in North America.

Demand from the energy sector for specialized pipe products, including premium connections, used in complex drilling and other high-performance applications, is expected to match the growth of the overall OCTG market.

Favorable market conditions and increased demand for our specialized pipe products, including premium connections, helped us to record sales growth and an increase in operating margin for our tubular products and services (Tubes) segment in the first nine months of the year. The consolidation of the energy products division of Maverick within this segment during the fourth quarter resulted in an increase in sales but a reduction in the operating margin from the previous quarter. For 2007, we expect to record further growth in sales in our Tubes segment due to the consolidation of Maverick for the full year and to maintain, or improve, the segment operating margin from that recorded in the fourth quarter of 2006 as we make progress in integrating welded OCTG and line pipe products under our sales strategy for North America.

Demand for our large diameter pipes for pipeline projects in South America in 2006 was affected by delays in the implementation of major gas pipeline infrastructure projects in Brazil and Argentina. This resulted in a substantial decline in sales and margins in our Projects segment from those recorded in 2005, notwithstanding an increase in sales for pipeline projects in North America and Africa. With orders in hand for the delayed projects in Brazil and Argentina and deliveries expected to begin at the end of the first quarter, we expect a significant increase in sales and improved margins in 2007 for our Projects segment, assuming there are no further delays to deliveries to these projects.

19

|  |

Summary of results

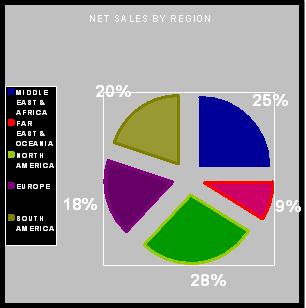

Our 2006 annual results reflect a further year of strong growth at Tenaris. They benefited from a strong market and the positioning we have built up over a number of years. Earnings per share grew 52% following growth of 63% in 2005. Demand for our high quality tubular products and services from the oil and gas industry remained firm throughout the year, particularly in the Middle East and Africa where sales more than doubled. Following the recent integration of Maverick, sales in 2007 are expected to grow strongly in North America.

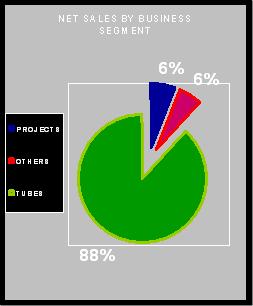

Net sales rose by 24%. Sales of tubular products and services rose by 33%, accounting for 88% of total sales. Sales of pipes for pipeline projects declined by 43% pursuant to delays in the implementation of pipeline projects in Brazil and Argentina. Operating income rose by 44% to USD 2,792 million, or 36% of net sales, compared to USD 1,946 million, or 31% of net sales in 2005, with sales from our tubular products and services segment accounting for 96% of operating income.

Cash flow from operations rose 40% to USD 1,811 million in 2006 compared to USD 1,295 million in 2005. However, following the acquisition of Maverick in October, net debt rose to USD 2,095 million at December 31, 2006 compared to USD 183 million at December 31, 2005. Capital expenditures rose to USD 441 million in 2006 from USD 284 million in 2005 as we stepped up investments in finishing lines and heat treatment facilities for specialized products and advanced with the construction of a power generation facility in Italy.

Oilfield services

We supply a comprehensive range of high-quality seamless and welded casing and tubing, premium connections, coiled tubing and accessories for use in the most demanding oil and gas drilling and well completion activities. Using our unique network of manufacturing, service and distribution and R&D facilities, we focus on reducing costs for our customers through integrated supply chain management and developing industry-leading products.

Sales of our TenarisBlue® premium connections continued to grow strongly during 2006. Now accounting for as much as 30% of our premium connection sales, it is firmly established in the Middle East and North African markets and was a major factor in the growth of our sales of tubes in this region. We successfully introduced it in the USA where sales to Newfield for their operations in Oklahoma were followed by sales to Anadarko and Wagner and Brown. We also introduced it in Russia where the technology was instrumental in the selection by Gazprom of Tenaris to supply advanced tubular products to their Astrakhan, Orenburg and Kuban operations as well as by Lukoil to supply pipes for their Narianmar project.

Other customers using TenarisBlue® premium connections for the first time included the local operations of BP, Shell and Burlington in Algeria; Sonangol, the national oil company of Angola; ADCO, the national oil company in UAE; PDVSA in Venezuela; the local operations of ConocoPhillips in Nigeria; ChevronTexaco in Australia; Shell in Egypt; Talisman in Malaysia, and ENI in Norway.

To keep pace with this growing customer base, we expanded our global network of licensed repair shops for the TenarisBlue® thread. Meanwhile, the range of more complex drilling operations where it is used is continuously being extended. For example, ConocoPhillips successfully used our TN 110 SS proprietary pipe grade with TenarisBlue® premium connections for an advanced drilling with casing drilling program offshore in the North Sea.

We also made progress with the introduction of our new connections, the TenarisBlue® Near Flush, an integral connection for use in slim wells, and the TenarisBlue® SAGD, a connection specially designed for use with slotted liners. Customers for the TenarisBlue® Near Flush connection include the Norwegian operations of ConocoPhillips and ENIRepsa, the Saudi joint venture drilling deep gas wells. The TenarisBlue® SAGD is used extensively in oil sands operations in Canada but we were successful in introducing it in Oman where Occidental is using it in the Mukhaizna heavy oil development .Our new R&D center in Veracruz will enable us to accelerate the customer testing and qualification process for these and other new products, particularly in larger diameter sizes.

We work with many customers under long-term framework agreements. Although the terms of these agreements vary, our aim is to provide a secure source and comprehensive range of tubular products backed up by integrated logistical and technical assistance services. During the year we renewed our agreement with Pemex in Mexico, extended our agreement with Repsol to cover the whole of Latin America, and renewed our agreements with ENI (global), Shell (Europe), ExxonMobil (Nigeria), AgipKCO (Kazakhstan) and ChevronTexaco (global). In Egypt, we opened a new service base at Alexandria. From here, we are providing pipe management services to Petrobel, IEOC and other operators under framework agreements.

|  |

20

Pipeline services

We supply an extensive range of seamless and welded line pipe products, complete with coatings and accessories for use in onshore, offshore and deepwater pipelines, with on-site, ready-for-installation delivery. Our focus is on providing the risers, flowlines and subsea tubular components for the deepwater and ultra deepwater markets where we are a major player in the Gulf of Mexico, West Africa, Far East, United Kingdom and Scandinavia.

As the industry moves further into frontier deepwater exploration and production projects, increasingly stringent technical requirements are required for our products. We are promoting and participating in joint industry programs with customers to research and develop the new product capabilities for use in the critical environments envisaged for future projects. These programs include development of weldable seamless X100 steel pipe, research into fatigue corrosion in sour environments, and research into tensile strain limit design models for pipelines.

In a market where products have become more demanding and delivery schedules more complex, we have begun discussing long-term agreements with some customers. We concluded agreements with Aramco, the leading player in the Middle East, and ChevronTexaco, a leading global player in deepwater projects. Under our agreement with ChevronTexaco, we supplied risers and flowlines to the Blind Faith project in the Gulf of Mexico and we are working with them in West Africa for projects such as Tombua Landana.

One of the most important projects of the year for Tenaris in this segment was the supply of 40,000 tons to the Akpo deepwater project in West Africa. This involved a wide dimensional range and a full package of deepwater solutions, including steel catenary risers, flowlines, oil offloading lines, export lines and line pipe for the topsides of the field development project in a water depth of 1,300 to 1,400 meters. The project tested our industrial capabilities to the full.

|  |

21

Process & power plant services

We provide comprehensive material planning, supply chain management services and on-time delivery of quality products to enable customers in the process and power plant industry to meet the demanding needs of major refinery, petrochemical and power plant contracts.

Downstream project activity remained strong during the year but new projects are taking longer to move forward due to rising costs, geopolitical uncertainties and the backlog of work at the leading engineering companies. As in last year, the focus of activity was the Middle East with gas processing projects to the fore. In addition, investment in major refinery projects around the world is picking up.

Major projects during the year included the Khursaniyah and Hawiyah NGL recovery programs in Saudi Arabia. These oil and gas processing facilities will support the Abu Hadriya, Fadhili and Khursaniyah oil fields and will boost oil production capacity in the Kingdom by some 2.3 million barrels per day by 2009. We worked closely with Snamprogetti and Bechtel and supplied 50,000 tons of pipes during the year for these developments.

In other projects in the Middle East, we are supplying pipes for the main projects to expand LNG processing capacity in Qatar. We are working closely with the Chiyoda-Technip joint venture on the RasGas 6 and 7, QatarGas II and QatarGas III and IV LNG trains. These projects will produce over 45 million tons per year of LNG, more than 25% of total global LNG capacity. In the UAE, we are working closely with Bechtel on the Offshore Gas Development III and the Asab Gas Development II projects that are part of a development to meet local gas demand in Abu Dhabi.

We are participating in two large refinery projects. In India, we are working with Bechtel to supply pipes for the expansion of Reliance’s Jamnagar refinery. This expansion would add 580,000 barrels per day of heavier crude processing capacity to the 660,000 barrels per day existing capacity and make Jamnagar the world’s largest single site refinery. In Vietnam we are working with the EPC consortium to supply pipes for PetroVietnam’s Dung Quat refinery. This refinery will be the first in Vietnam and would meet 40% of local demand with an annual capacity of 6.5 million metric tons.

|  |

22

Industrial & automotive services

We provide a wide variety of seamless pipe products for industrial applications with a focus on segments such as automotive components, hydraulic cylinders, gas cylinders and architectural structures where we can add value with our specialist product development and supply chain management expertise. Sales are concentrated in Europe, particularly Italy where our mill has traditionally served this market, but we also have significant sales in North America, the Far East and Mercosur.

Overall, market conditions were good in 2006, particularly in the segment of gas cylinders and hollows for gas cylinders, in which Tenaris is the global market leader. We registered 15% growth in sales in this segment led by strong demand from China and India. We have been working on materials with ultra-high tensile strength (>1.100 Mega Pascal) and with excellent toughness properties at low temperatures (-50 °C) in order to meet demand for lighter gas cylinders with improved safety protection.

In the automotive segment, demand for our high-end components such as tubular components for airbags continues to grow, as well as output at our facility in Veracruz which was up 57% year on year. We developed and introduced a new prototype component using an ultra-high strength steel grade in collaboration with the design teams of established airbag inflator manufacturers. Nevertheless, overall sales to the automotive sector declined due to a phase-out from certain under-performing product lines, where we are facing intense competition from producers of general purpose tubes and alternative technologies.

In the hydraulic cylinder segment, we concluded a five-year contract with Caterpillar in the USA to provide multi-customized tubular components for hydraulic cylinders used in the excavators manufactured at the Joliet facility in Illinois for the NAFTA market. We are building a dedicated component centre at our Romanian mill for this project.

Sales of tubes for general mechanical applications declined primarily due to mill capacity constraints reflecting a strong demand for other product categories and the repositioning of mill capacity in Japan and Europe to oil and gas product applications. Competition in this sector, particularly in our main market in Europe, remains fierce as low-priced products continue to enter the market from countries such as China.

23

R&D: expanding the global network

In November 2006, we inaugurated a new Research & Development Center at our plant in Veracruz, Mexico. Built at a cost of USD 14 million, the center is the latest addition to our global R&D network that also includes research centers in Argentina, Japan and Italy.

Strategically located near the Gulf of Mexico, the center conducts research in four main areas: welding technology, fracture mechanics, process engineering and metallurgy and materials. In this last area, research is focused on the development of value-added OCTG products, line pipe and risers for deep and ultra-deep water applications. The center’s full scale testing laboratory possesses some of the most sophisticated equipment found in the world for testing tubes and threads.

Worldwide, more than 200 scientists and engineers, more than half of whom hold PhDs or Master’s degrees, work in Tenaris R&D centers. At the largest of these centers, the Centro de Investigación Industrial (CINI), located at our mill in Campana, Argentina, research is conducted in a wide range of areas: steel metallurgy, computational mechanics, surfaces and coating chemistry, metal forming and furnace technology, among others. The center in Japan specializes in high alloy products and process technology.

In Italy, research is conducted primarily through the industry-supported Centro Sviluppo Materiali, in Rome. However, we are constructing a new research center at our mill in Dalmine which will be opened in mid-2007. This will focus on industrial and automotive applications.

Through our global network of R&D centers, we work with more than 60 universities and research institutions worldwide which conduct basic and applied research for us and for industry consortia in which we participate. This combination of internal and external expertise provides us with the means to develop the value-added products and improved production processes that are vital to our future growth.

24

Communities and environment review

Tenaris’s growth has been made possible by adhering to certain values that guide the Company’s internal management and its relationships with customers, suppliers and the communities where the Company is present. These values are centered on a conviction that industry plays a key role in promoting lasting and equitable economic growth for societies and that Tenaris will add value to its operations as well as to the wider community by interacting with employees and others in accordance with that conviction.

Consistent with this vision, Tenaris strives to build partnerships, both internally and externally, that foster growth and opportunity for all involved. The importance we place on such relationships is manifested in our commitment to protecting the health and safety of our employees, maintaining transparent relations with customers and suppliers and collaborating with government and non-governmental organizations in the communities in which we operate.

Valuing education, we invest continuously in the development of our own workforce and support a wide variety of educational initiatives at primary, secondary and university level. Through a revitalized Global Trainee Program, where many in Tenaris’s senior management began, Tenaris recruits recent university graduates and develops them to be tomorrow’s senior management.

Much of the training that both Global Trainees (GTs) and other Tenaris employees receive, is focused on developing their engineering skills and knowledge of the company’s core industrial processes, and is delivered through the TenarisUniversity Industrial School. At a time when demand for skilled engineers is high, especially in our own industry, we believe that this emphasis on attracting and developing people that have the requisite education and skills is critical to our future growth.

In our community relations we stress support for academic excellence. In Argentina and Mexico we are carrying out a series of projects aimed at improving the quality of primary and secondary education in schools close to our plants in Campana and Veracruz. Drawing on the expertise of UNESCO and international experts as well as local universities and the active participation of school officials, students and their families, we take an integrated approach including investment in infrastructure, the provision of school supplies and scholarships.

In the area of higher education we continue to support the Roberto Rocca Education Program, which Tenaris co-founded in 2005. Designed to encourage the study of engineering in selected countries, the program in 2006 awarded 400 Scholarships to undergraduate students, and seven Fellowships for doctoral studies at leading international universities. As is the case with all of our community projects, we seek to reward merit and initiative by granting Scholarships and Fellowships only to those students who combine academic excellence with outstanding personal qualities.

The prevention of illness and disease is another key area for community action for Tenaris. In Mexico we instituted a breast cancer screening program for our employees and family members. Once the preliminary round of screening is completed, the program will be extended to the rest of the community around our plant in Veracruz. In Canada we contributed one million Canadian dollars towards a community fund for the construction of a maternal and child health center in Sault Ste. Marie.

In all of our community programs we seek to promote social integration and leverage our own contribution by partnering with other governmental and non-governmental organizations in projects that involve the active participation of the project’s beneficiaries. This was the approach we took in Mexico in the program “For a dignified home,” which involves the construction of 280 homes and a community center for low-income families in Veracruz.

25

The program, which gives special consideration to families in which a family member is physically handicapped, is co-sponsored by the city of Veracruz and other organizations. The construction work is complemented by job training and other activities designed to facilitate the beneficiaries’ integration in the broader Veracruz community and the development of micro-enterprises.

With more than 20,000 employees drawn from dozens of countries, we view the diversity of our workforce as one of our strengths. The combination of rational analysis and diversity of ideas and cultures will continue to play an instrumental role in the growth of Tenaris. Thus, we make a continuous effort to foster respect among employees for language, cultural and gender differences and are committed to broadening this diversity at all levels of the Company.

This belief in the benefits of diversity is also reflected in our support for cultural institutions. Working closely with the Fundación Proa in Buenos Aires and the Associazione per la Galleria d ’Arte Moderna e Contemporanea in Bergamo and through agreements with the Museum of Fine Arts in Houston and cultural institutions in Brazil, Mexico and Japan, we promote cultural exchanges in our local communities through art exhibits, seminars and other initiatives. Among the highlights in 2006 was the first edition of the Latin Wave Film Festival we sponsored at the Museum of Fine Arts in Houston. The three-day event, co-organized by Fundación Proa, featured films from Argentina, Brazil, Colombia, Mexico and Venezuela.

This year in Italy, we celebrated the 100th anniversary of our Dalmine mill. The activities included an open day when more than 12,000 people from the surrounding community visited our industrial facilities and attended a concert.

|  |

26

Health, safety and the environment

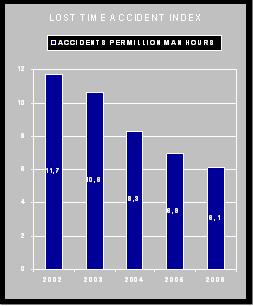

Tenaris is committed to protecting the health and safety of its employees and the communities in which it operates, as well as to minimizing its own impact on the environment and supporting broader industry and public efforts to protect the environment. In accordance with the principle of sustainable development, our efforts in this area are focused on improving the efficiency of our operations, reducing energy consumption, minimizing waste, recycling and employee training.

We continue to work on the implementation and improvement of our integrated Health, Safety and Environment (HSE) management system. Based on international standards such as ISO 14000 and OHSA 18000, the system applies eco-efficiency and integral safety concepts to all of our operations. Following the introduction of an integrated IT safety and environmental tool, we are able to record, track and analyze safety and environment accidents and incidents at all of our plants.