Exhibit 99.1

ONCOR

Fourth Quarter And Year End 2014 Investor Call

March 3, 2015

Oncor Electric Delivery

Forward Looking Statements

This presentation contains forward-looking statements, which are subject to various risks and uncertainties. Discussion of risks and uncertainties that could cause actual results to differ materially from management’s current projections, forecasts, estimates and expectations is contained in filings made by Oncor Electric Delivery Company LLC (Oncor) with the Securities and Exchange Commission (SEC). Specifically, Oncor makes reference to the section entitled “Risk Factors” in its annual and quarterly reports. In addition to the risks and uncertainties set forth in Oncor’s SEC filings, the forward-looking statements in this presentation could be affected by, among other things: prevailing governmental policies and regulatory actions; legal and administrative proceedings and settlements, including the exercise of equitable powers by courts; any impacts on us as a result of the bankruptcy proceedings involving Energy Future Holdings Corp. and certain of its subsidiaries; weather conditions and other natural phenomena; acts of sabotage, wars or terrorist or cyber security threats or activities; economic conditions, including the impact of a recessionary environment; unanticipated population growth or decline, or changes in market demand and demographic patterns; changes in business strategy, development plans or vendor relationships; unanticipated changes in interest rates or rates of inflation; unanticipated changes in operating expenses, liquidity needs and capital expenditures; inability of various counterparties to meet their financial obligations to Oncor, including failure of counterparties to perform under agreements; general industry trends; hazards customary to the industry and the possibility that Oncor may not have adequate insurance to cover losses resulting from such hazards; changes in technology used by and services offered by Oncor; significant changes in Oncor’s relationship with its employees; changes in assumptions used to estimate costs of providing employee benefits, including pension and other post-retirement employee benefits, and future funding requirements related thereto; significant changes in critical accounting policies material to Oncor; commercial bank and financial market conditions, access to capital, the cost of such capital, and the results of financing and refinancing efforts, including availability of funds in the capital markets and the potential impact of disruptions in US credit markets; circumstances which may contribute to future impairment of goodwill, intangible or other long-lived assets; financial restrictions under Oncor’s revolving credit facility and indentures governing its debt instruments; Oncor’s ability to generate sufficient cash flow to make interest payments on its debt instruments; actions by credit rating agencies; and Oncor’s ability to effectively execute its operational strategy. Any forward-looking statement speaks only as of the date on which it is made, and Oncor undertakes no obligation to update any forward-looking statement to reflect events or circumstances after the date on which it is made or to reflect the occurrence of unanticipated events.

Regulation G

This presentation includes certain non-GAAP financial measures. A reconciliation of these measures to the most directly comparable GAAP measures is included in this presentation, which is available on Oncor’s website, www.oncor.com, in the Investor section, and also filed with the SEC.

Oncor Electric Delivery 1

4th Quarter And Year End 2014 Investor Call Agenda

Financial Overview

David Davis

Chief Financial Officer

Operational Review

Bob Shapard

Chairman and CEO

Q&A

Oncor Electric Delivery 2

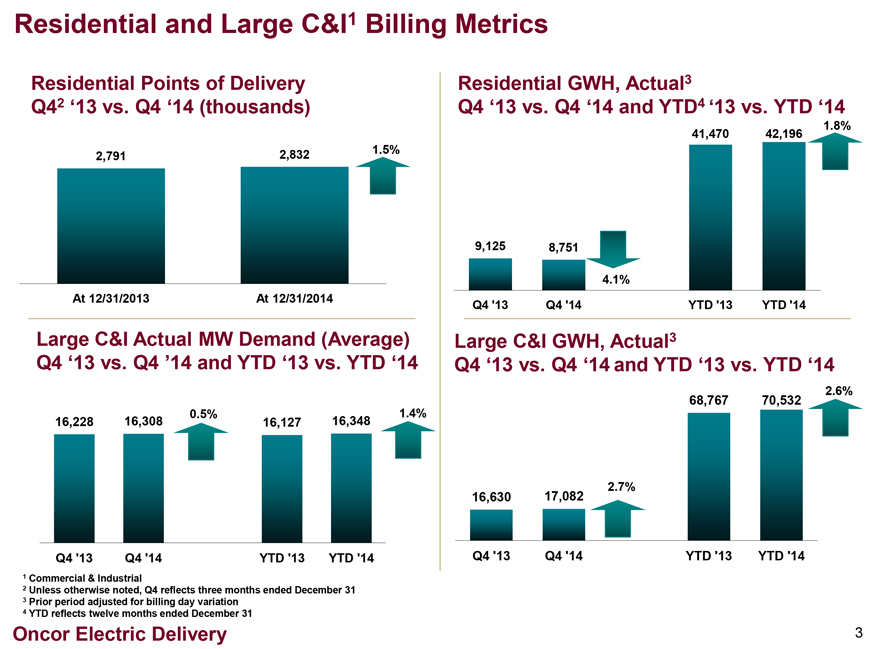

Residential and Large C&I1 Billing Metrics

Residential Points of Delivery Q42 ‘13 vs. Q4 ‘14 (thousands)

2,791 2,832 1.5%

At 12/31/2013 At 12/31/2014

Large C&I Actual MW Demand (Average) Q4 ‘13 vs. Q4 ’14 and YTD ‘13 vs. YTD ‘14

0.5% 1.4% 16,228 16,308 16,127 16,348

Q4 ‘13 Q4 ‘14 YTD ‘13 YTD ‘14

1 Commercial & Industrial

2 Unless otherwise noted, Q4 reflects three months ended December 31

3 Prior period adjusted for billing day variation

4 YTD reflects twelve months ended December 31

Residential GWH, Actual3

Q4 ‘13 vs. Q4 ‘14 and YTD4 ‘13 vs. YTD ‘14

41,470 42,196 1.8% 9,125 8,751 4.1%

Q4 ‘13 Q4 ‘14 YTD ‘13 YTD ‘14

Large C&I GWH, Actual3

Q4 ‘13 vs. Q4 ‘14 and YTD ‘13 vs. YTD ‘14

68,767 70,532 2.6% 2.7% 16,630 17,082

Q4 ‘13 Q4 ‘14 YTD ‘13 YTD ‘14

Oncor Electric Delivery

3

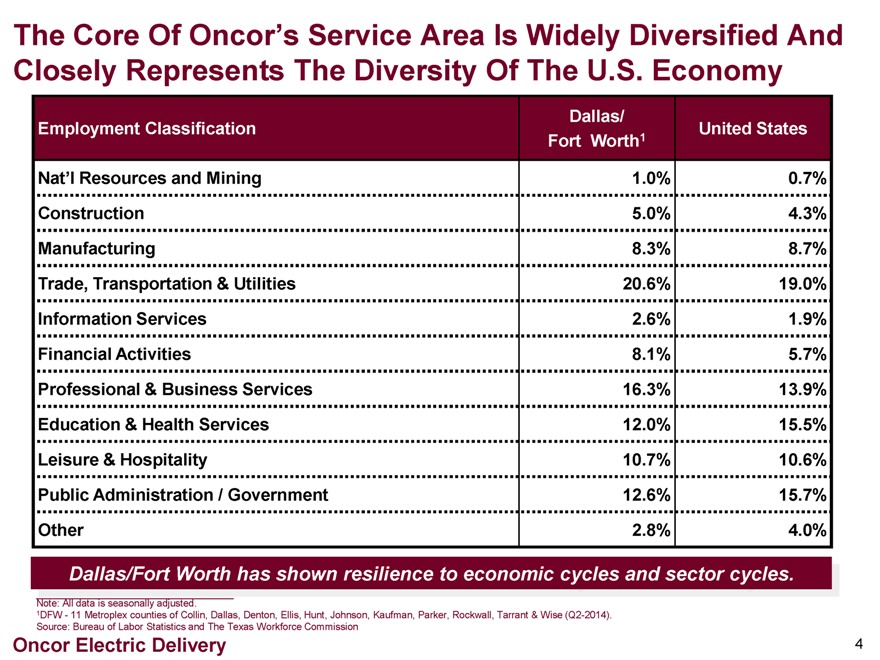

The Core Of Oncor’s Service Area Is Widely Diversified And Closely Represents The Diversity Of The U.S. Economy

Employment Classification Dallas/ Fort Worth1 United States

Nat’l Resources and Mining

1.0% 0.7%

Construction

5.0% 4.3%

Manufacturing

8.3% 8.7%

Trade, Transportation & Utilities

20.6% 19.0%

Information Services

2.6% 1.9%

Financial Activities

8.1% 5.7%

Professional & Business Services

16.3% 13.9%

Education & Health Services

12.0% 15.5%

Leisure & Hospitality

10.7% 10.6%

Public Administration / Government

12.6% 15.7%

Other 2.8% 4.0%

Dallas/Fort Worth has shown resilience to economic cycles and sector cycles.

Note: All data is seasonally adjusted.

1DFW-11 Metroplex counties of Collin, Dallas, Denton, Ellis, Hunt, Johnson, Kaufman, Parker, Rockwall, Tarrant & Wise (Q2-2014).

Source: Bureau of Labor Statistics and The Texas Workforce Commission

Oncor Electric Delivery

4

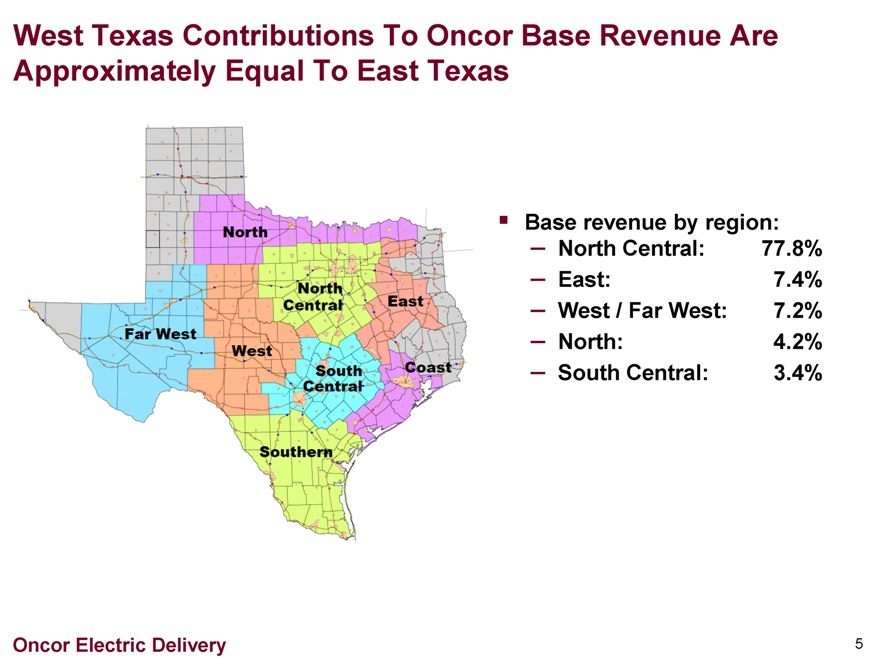

West Texas Contributions To Oncor Base Revenue Are Approximately Equal To East Texas

North

North Central

East

Far West

West South Central

Coast

Southern

Base revenue by region:

— North Central: 77.8%

— East: 7.4%

— West / Far West: 7.2%

— North: 4.2%

— South Central: 3.4%

Oncor Electric Delivery 5

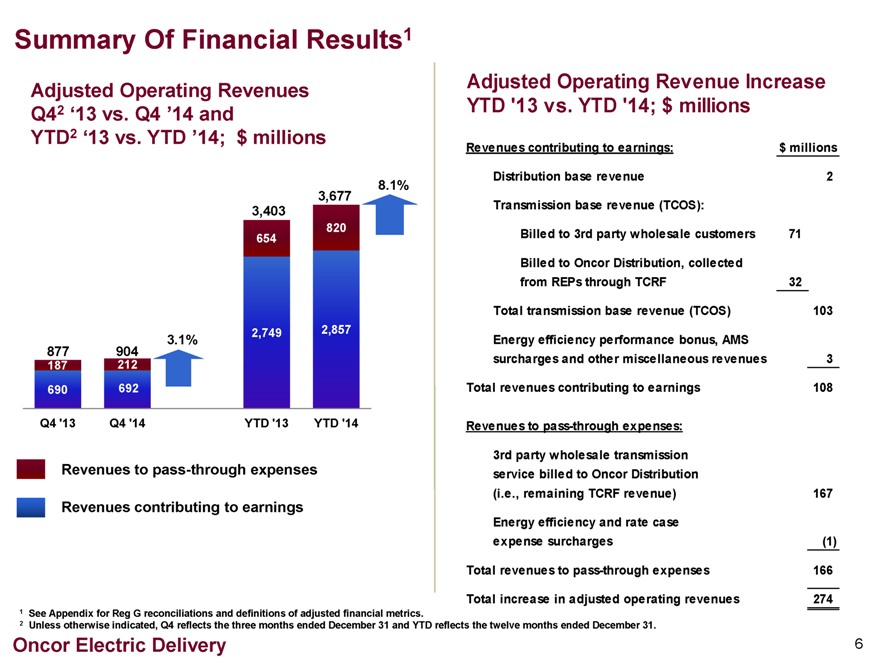

Summary Of Financial Results1

Adjusted Operating Revenues Q42 ‘13 vs. Q4 ’14 and YTD2 ‘13 vs. YTD ’14; $ millions

877 187 690 Q4 ‘13

904 212 692 Q4 ‘14

3.1%

3,403 654 2,749 YTD ‘13

3,677 820 2,857 YTD ‘14

8.1%

Revenues to pass-through expenses

Revenues contributing to earnings

Adjusted Operating Revenue Increase YTD ‘13 vs. YTD ‘14; $ millions

Revenues contributing to earnings: $ millions

Distribution base revenue 2

Transmission base revenue (TCOS):

Billed to 3rd party wholesale customers 71

Billed to Oncor Distribution, collected from REPs through TCRF 32

Total transmission base revenue (TCOS) 103

Energy efficiency performance bonus, AMS surcharges and other miscellaneous revenues 3

Total revenues contributing to earnings 108

Revenues to pass-through expenses:

3rd party wholesale transmission service billed to Oncor Distribution (i.e., remaining TCRF revenue) 167

Energy efficiency and rate case expense surcharges (1)

Total revenues to pass-through expenses 166

Total increase in adjusted operating revenues 274

1 See Appendix for Reg G reconciliations and definitions of adjusted financial metrics.

2 Unless otherwise indicated, Q4 reflects the three months ended December 31 and YTD reflects the twelve months ended December 31.

Oncor Electric Delivery

6

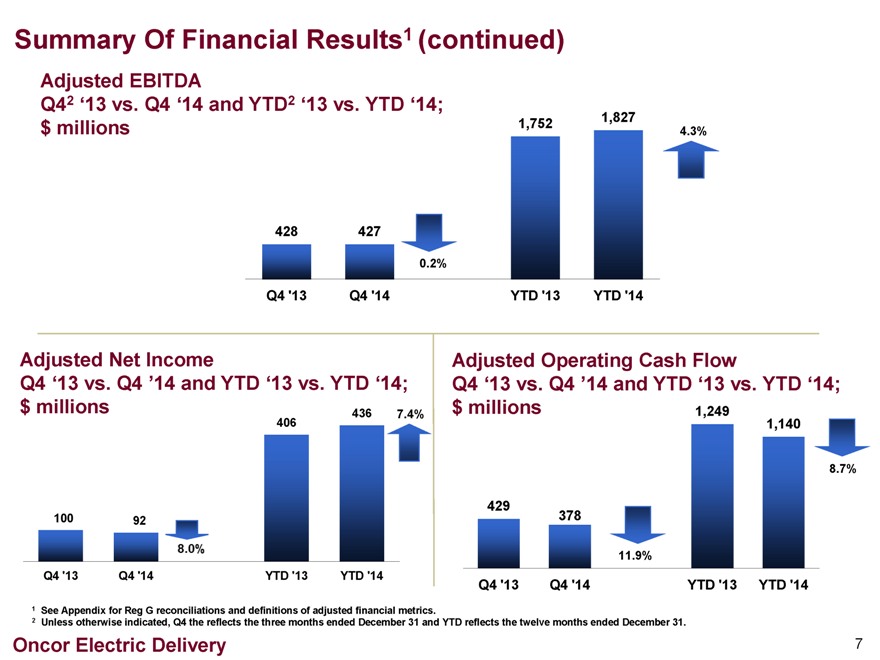

Summary Of Financial Results1 (continued)

Adjusted EBITDA

Q42 ‘13 vs. Q4 ‘14 and YTD2 ‘13 vs. YTD ‘14;

$ millions

428 Q4 ‘13

427 Q4 ‘14

0.2%

1,752 YTD ‘13

1,827 YTD ‘14

4.3%

Adjusted Net Income

Q4 ‘13 vs. Q4 ’14 and YTD ‘13 vs. YTD ‘14;

$ millions

406 436 7.4% 100 92 8.0% Q4 ‘13 Q4 ‘14 YTD ‘13 YTD ‘14

Adjusted Operating Cash Flow

Q4 ‘13 vs. Q4 ’14 and YTD ‘13 vs. YTD ‘14;

$ millions

1,249 1,140 8.7%

429 378 11.9%

Q4 ‘13 Q4 ‘14 YTD ‘13 YTD ‘14

1 See Appendix for Reg G reconciliations and definitions of adjusted financial metrics.

2 Unless otherwise indicated, Q4 the reflects the three months ended December 31 and YTD reflects the twelve months ended December 31.

Oncor Electric Delivery

7

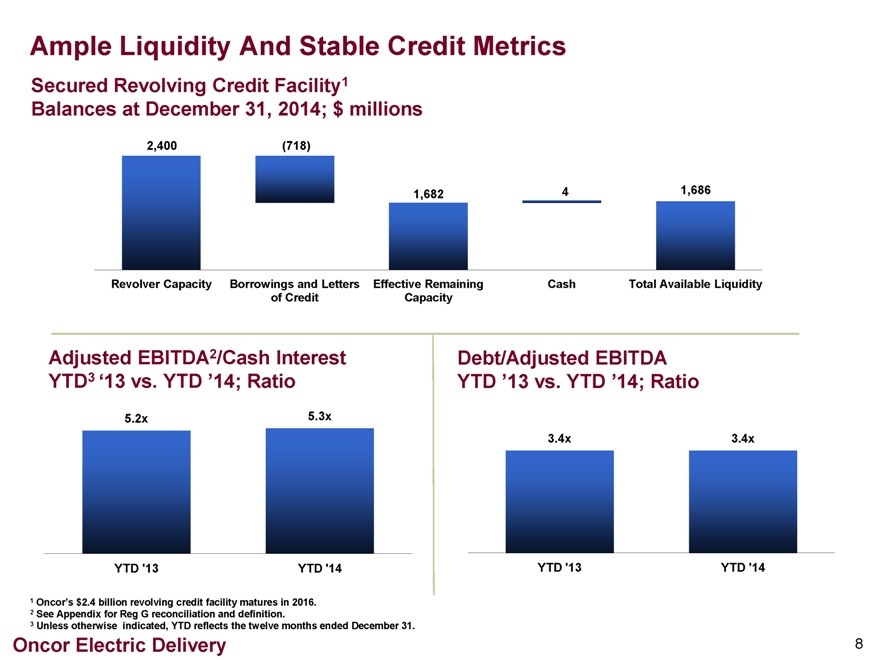

Ample Liquidity And Stable Credit Metrics

Secured Revolving Credit Facility1 Balances at December 31, 2014; $ millions

2,400 (718)

1,6824 1,686

Revolver Capacity Borrowings and Letters of Credit Effective Remaining Capacity Cash Total Available Liquidity

Adjusted EBITDA2/Cash Interest

YTD3 ‘13 vs. YTD ’14; Ratio

5.2x 5.3x

YTD ‘13 YTD ‘14

Debt/Adjusted EBITDA

YTD ’13 vs. YTD ’14; Ratio

3.4x 3.4x

YTD ‘13 YTD ‘14

1 Oncor’s $2.4 billion revolving credit facility matures in 2016.

2 See Appendix for Reg G reconciliation and definition.

3 Unless otherwise indicated, YTD reflects the twelve months ended December 31.

Oncor Electric Delivery 8

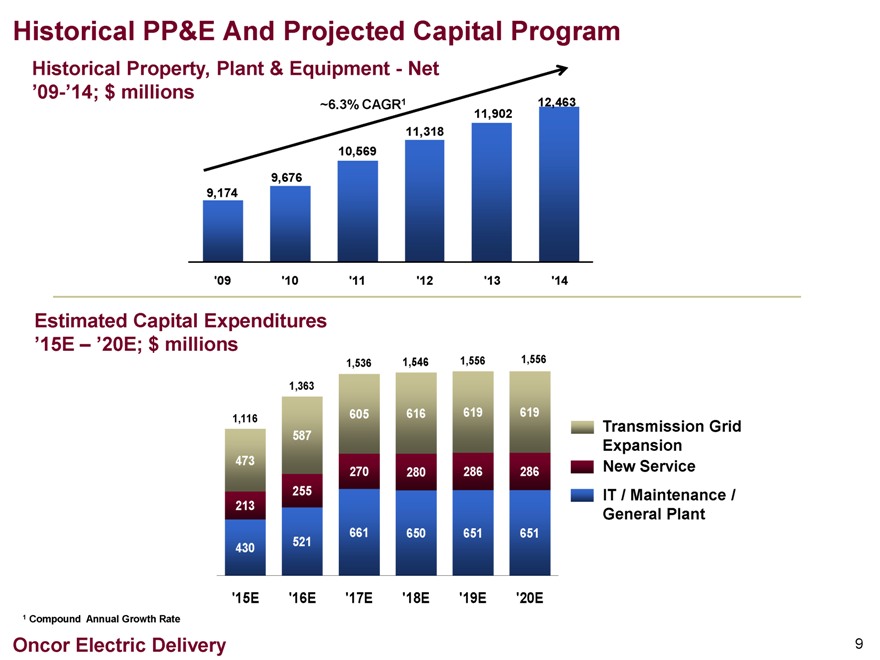

Historical PP&E And Projected Capital Program

Historical Property, Plant & Equipment - Net

’09-’14; $ millions ~6.3% CAGR1 12,463

11,902

11,318

10,569

9,676

9,174

‘09 ‘10 ‘11 ‘12 ‘13 ‘14

Estimated Capital Expenditures

’15E – ’20E; $ millions

1,536 1,546 1,556 1,556

1,363

1,116 587 605 616 619 619 Transmission Grid Expansion

473 270 280 286 286 New Service

213 255 661 650 651 651 IT / Maintenance / General Plant

430 521

‘15E ‘16E ‘17E ‘18E ‘19E ‘20E

1 Compound Annual Growth Rate

Oncor Electric Delivery

9

4th Quarter And Year End 2014 Investor Call Agenda

Financial Overview David Davis

Chief Financial Officer

Operational Review Bob Shapard

Chairman and CEO

Q&A

Oncor Electric Delivery 10

Key Drivers Of Capital Investment

Continued strong investment in transmission

Load growth

Reduction of grid congestion

Interconnection of new generation sources

Emerging physical security needs

Distribution investment to connect new customers

Consistent gross premise growth since 2009

Investments in infrastructure to maintain and improve reliability

Overhead and pole maintenance

Underground cable replacement and rehabilitation

Network equipment maintenance and planned replacements

Investments in technology to support business processes and operational efficiencies

Oncor Electric Delivery

11

Appendix -

Regulation G Reconciliations And Supplemental Data

Oncor Electric Delivery 12

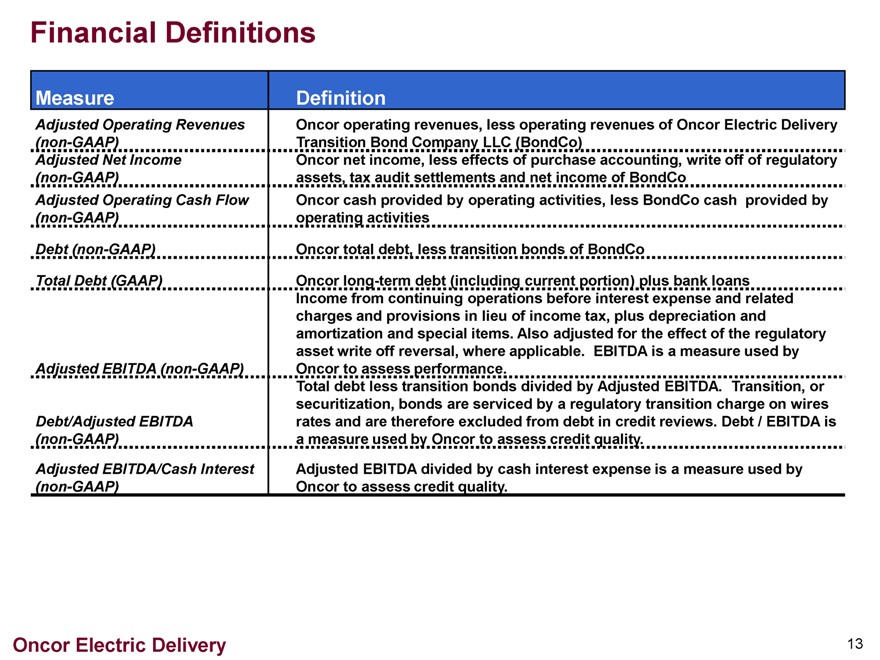

Financial Definitions

Measure Definition

Adjusted Operating Revenues Oncor operating revenues, less operating revenues of Oncor Electric Delivery

(non-GAAP) Transition Bond Company LLC (BondCo)

Adjusted Net Income Oncor net income, less effects of purchase accounting, write off of regulatory

(non-GAAP) assets, tax audit settlements and net income of BondCo

Adjusted Operating Cash Flow Oncor cash provided by operating activities, less BondCo cash provided by

(non-GAAP) operating activities

Debt (non-GAAP) Oncor total debt, less transition bonds of BondCo

Total Debt (GAAP) Oncor long-term debt (including current portion) plus bank loans

Income from continuing operations before interest expense and related

charges and provisions in lieu of income tax, plus depreciation and

amortization and special items. Also adjusted for the effect of the regulatory

asset write off reversal, where applicable. EBITDA is a measure used by

Adjusted EBITDA (non-GAAP) Oncor to assess performance.

Total debt less transition bonds divided by Adjusted EBITDA. Transition, or

securitization, bonds are serviced by a regulatory transition charge on wires

Debt/Adjusted EBITDA rates and are therefore excluded from debt in credit reviews. Debt / EBITDA is

(non-GAAP) a measure used by Oncor to assess credit quality.

Adjusted EBITDA/Cash Interest Adjusted EBITDA divided by cash interest expense is a measure used by

(non-GAAP) Oncor to assess credit quality.

Oncor Electric Delivery

13

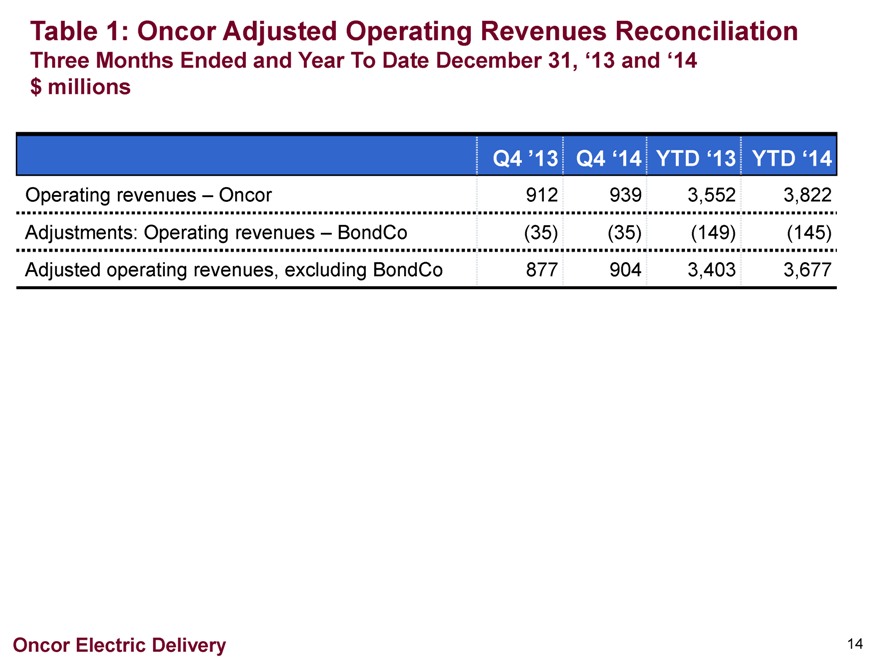

Table 1: Oncor Adjusted Operating Revenues Reconciliation

Three Months Ended and Year To Date December 31, ‘13 and ‘14 $ millions

Q4 ’13 Q4 ‘14 YTD ‘13 YTD ‘14

Operating revenues – Oncor 912 939 3,552 3,822

Adjustments: Operating revenues – BondCo (35) (35) (149) (145)

Adjusted operating revenues, excluding BondCo 877 904 3,403 3,677

Oncor Electric Delivery

14

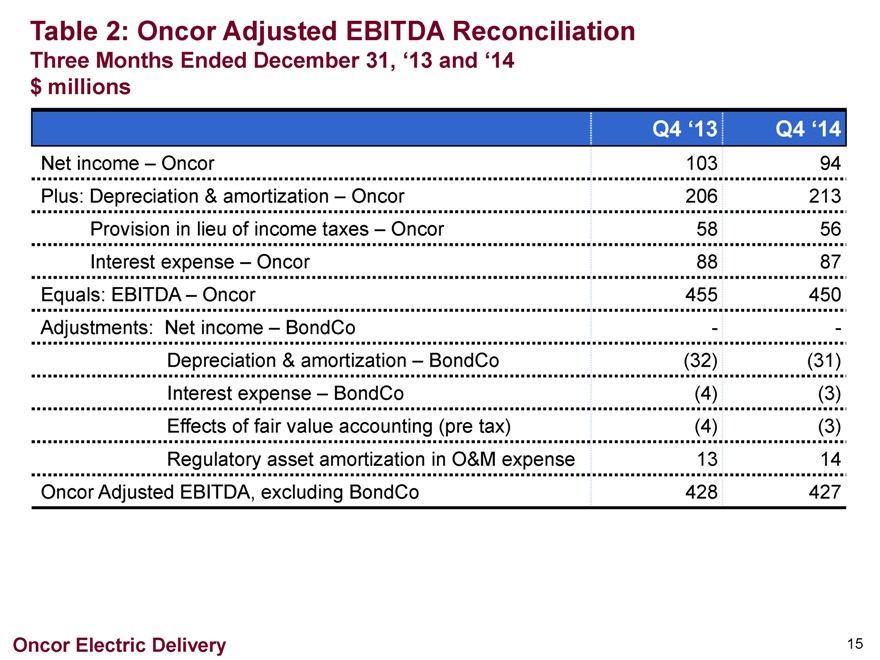

Table 2: Oncor Adjusted EBITDA Reconciliation

Three Months Ended December 31, ‘13 and ‘14 $ millions

Q4 ‘13 Q4 ‘14

Net income – Oncor 103 94

Plus: Depreciation & amortization – Oncor 206 213

Provision in lieu of income taxes – Oncor 58 56

Interest expense – Oncor 88 87

Equals: EBITDA – Oncor 455 450

Adjustments: Net income – BondCo - -

Depreciation & amortization – BondCo (32) (31)

Interest expense – BondCo (4) (3)

Effects of fair value accounting (pre tax) (4) (3)

Regulatory asset amortization in O&M expense 13 14

Oncor Adjusted EBITDA, excluding BondCo 428 427

Oncor Electric Delivery 15

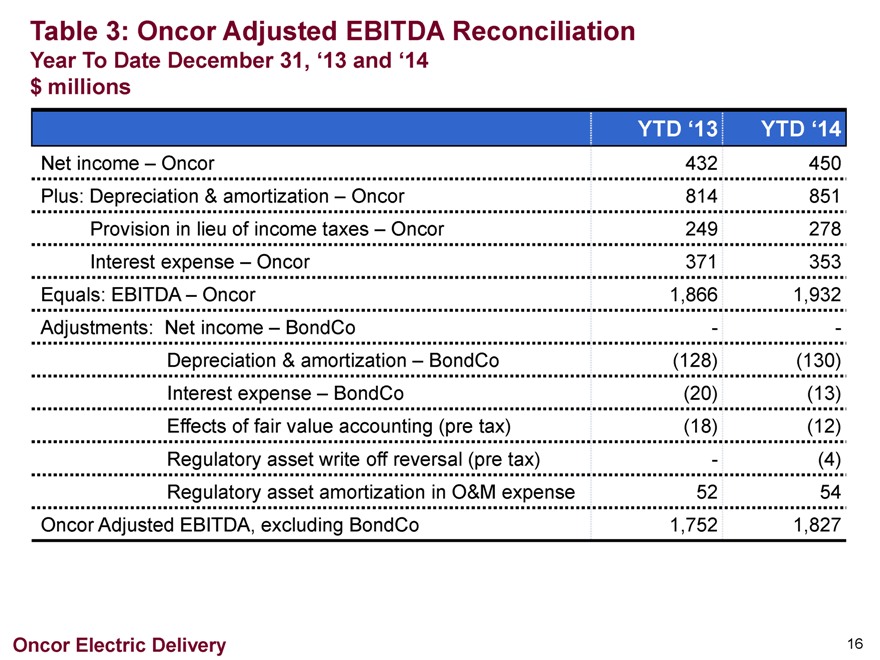

Table 3: Oncor Adjusted EBITDA Reconciliation

Year To Date December 31, ‘13 and ‘14 $ millions

YTD ‘13 YTD ‘14

Net income – Oncor 432 450

Plus: Depreciation & amortization – Oncor 814 851

Provision in lieu of income taxes – Oncor 249 278

Interest expense – Oncor 371 353

Equals: EBITDA – Oncor 1,866 1,932

Adjustments: Net income – BondCo - -

Depreciation & amortization – BondCo (128) (130)

Interest expense – BondCo (20) (13)

Effects of fair value accounting (pre tax) (18) (12)

Regulatory asset write off reversal (pre tax) - (4)

Regulatory asset amortization in O&M expense 52 54

Oncor Adjusted EBITDA, excluding BondCo 1,752 1,827

Oncor Electric Delivery

16

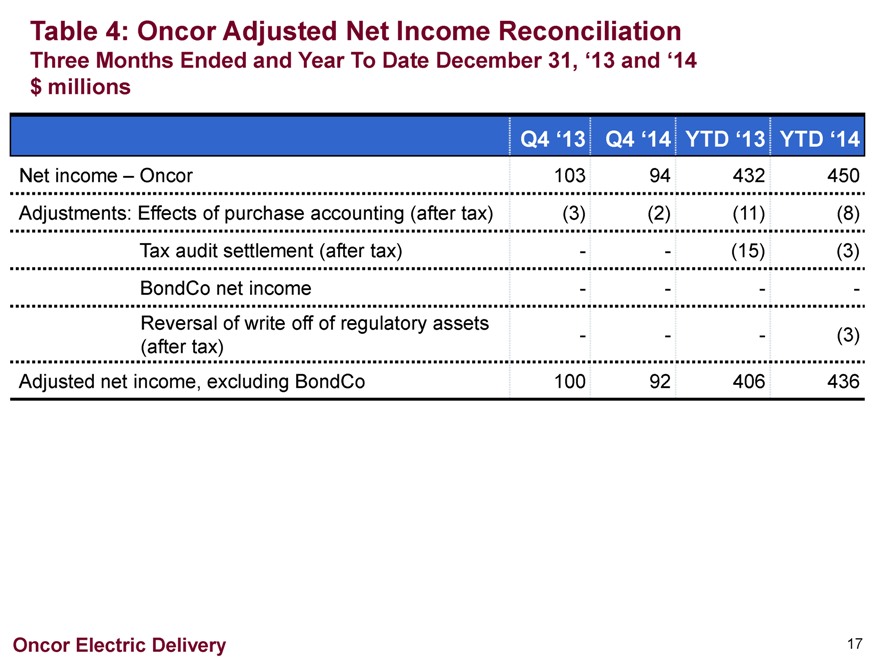

Table 4: Oncor Adjusted Net Income Reconciliation

Three Months Ended and Year To Date December 31, ‘13 and ‘14 $ millions

Q4 ‘13 Q4 ‘14 YTD ‘13 YTD ‘14

Net income – Oncor 103 94 432 450

Adjustments: Effects of purchase accounting (after tax) (3) (2) (11) (8)

Tax audit settlement (after tax) - - (15) (3)

BondCo net income - - - -

Reversal of write off of regulatory assets - - - (3)

(after tax)

Adjusted net income, excluding BondCo 100 92 406 436

Oncor Electric Delivery 17

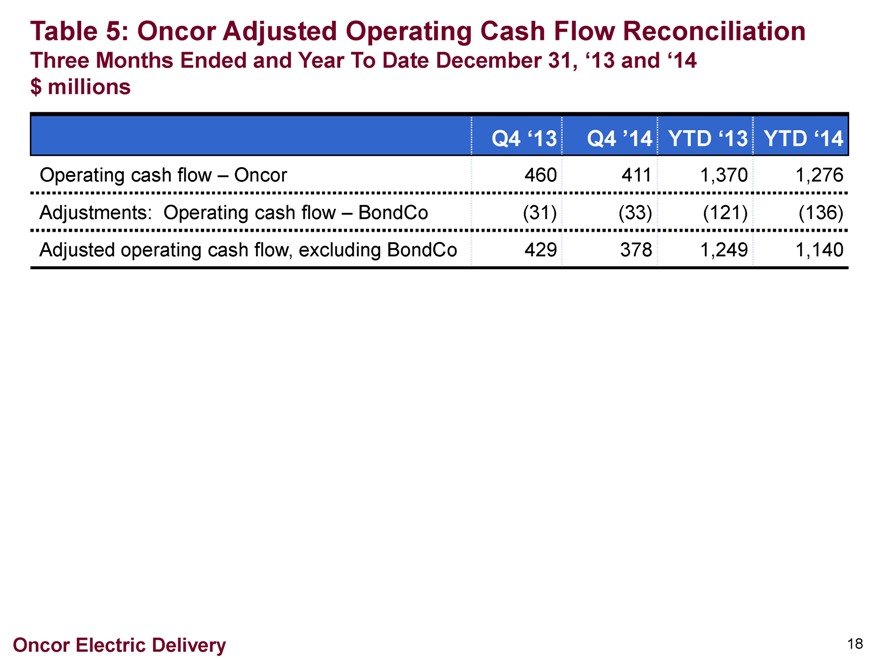

Table 5: Oncor Adjusted Operating Cash Flow Reconciliation

Three Months Ended and Year To Date December 31, ‘13 and ‘14 $ millions

Q4 ‘13 Q4 ’14 YTD ‘13 YTD ‘14

Operating cash flow – Oncor 460 411 1,370 1,276

Adjustments: Operating cash flow – BondCo (31) (33) (121) (136)

Adjusted operating cash flow, excluding BondCo 429 378 1,249 1,140

Oncor Electric Delivery

18

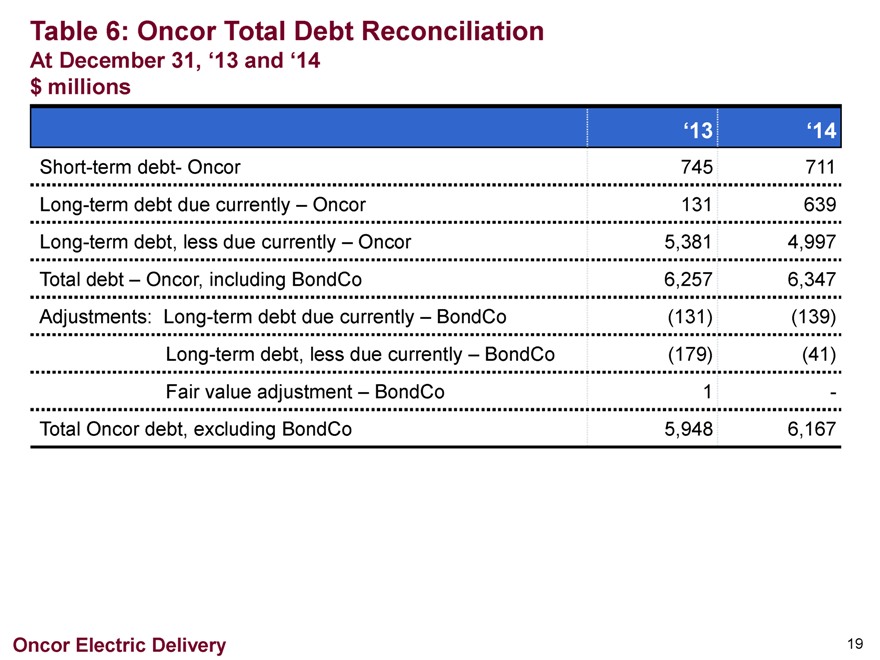

Table 6: Oncor Total Debt Reconciliation

At December 31, ‘13 and ‘14 $ millions

‘13 ‘14

Short-term debt- Oncor 745 711

Long-term debt due currently – Oncor 131 639

Long-term debt, less due currently – Oncor 5,381 4,997

Total debt – Oncor, including BondCo 6,257 6,347

Adjustments: Long-term debt due currently – BondCo (131) (139)

Long-term debt, less due currently – BondCo (179) (41)

Fair value adjustment – BondCo 1 -

Total Oncor debt, excluding BondCo 5,948 6,167

Oncor Electric Delivery

19

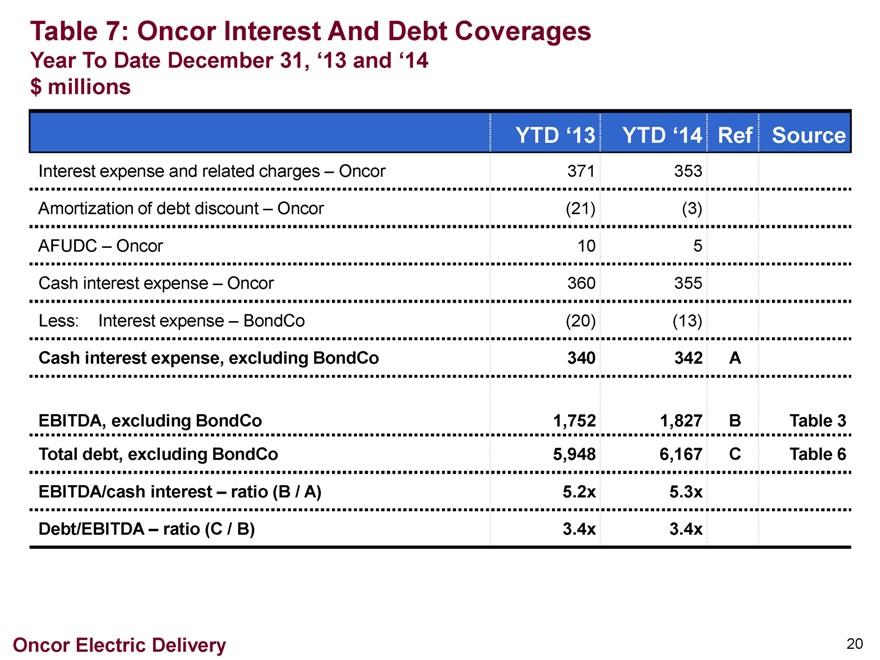

Table 7: Oncor Interest And Debt Coverages

Year To Date December 31, ‘13 and ‘14 $ millions

YTD ‘13 YTD ‘14 Ref Source

Interest expense and related charges – Oncor 371 353

Amortization of debt discount – Oncor (21) (3)

AFUDC – Oncor 10 5

Cash interest expense – Oncor 360 355

Less: Interest expense – BondCo (20) (13)

Cash interest expense, excluding BondCo 340 342 A

EBITDA, excluding BondCo 1,752 1,827 B Table 3

Total debt, excluding BondCo 5,948 6,167 C Table 6

EBITDA/cash interest – ratio (B / A) 5.2x 5.3x

Debt/EBITDA – ratio (C / B) 3.4x 3.4x

Oncor Electric Delivery

20