Table of Contents

As filed with the Securities and Exchange Commission, via EDGAR, on December 8, 2003

REGISTRATION NO. 333-104000

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

POST-EFFECTIVE AMENDMENT NO. 1

TO

FORM S-11

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

American Financial Realty Trust

(Exact name of Registrant as specified in its Governing Instruments)

1725 The Fairway, Jenkintown, Pennsylvania 19046

(215) 887-2280

(Address, including Zip Code, and Telephone Number, including Area Code, of Registrant’s Principal Executive Offices)

Edward J. Matey Jr., Esquire

1725 The Fairway

Jenkintown, Pennsylvania 19046

(215) 887-2280

(Name, Address, including Zip Code, and Telephone Number, including Area Code, of Agent for Service)

with a copy to:

James W. McKenzie, Jr., Esquire

Justin W. Chairman, Esquire

Morgan, Lewis & Bockius LLP

1701 Market Street

Philadelphia, Pennsylvania 19103

(215) 963-5000

Approximate date of commencement of the proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box: ¨

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

PROSPECTUS

46,543,974 Common Shares

This prospectus relates to up to 46,543,974 common shares of beneficial interest of American Financial Realty Trust that the selling shareholders named in this prospectus may offer for sale from time to time. We are registering the common shares to provide the selling shareholders with registered securities, but this prospectus does not necessarily mean that the selling shareholders will offer or sell the shares. The selling shareholders named in this prospectus either currently own the common shares they are offering, or may acquire these common shares by converting units of limited partnership interest in our operating partnership, First States Group, L.P., into common shares. These units of limited partnership interest in our operating partnership may be converted by the selling shareholders into common shares at any time in accordance with our operating partnership’s partnership agreement. We are filing the registration statement of which this prospectus is a part pursuant to contractual obligations. We will not receive any of the proceeds from the sale of any common shares by the selling shareholders, but will incur expenses in connection with the offering.

The selling shareholders from time to time may offer and sell the shares held by them directly or through agents or broker-dealers on terms to be determined at the time of sale. These sales may be made on the New York Stock Exchange or other exchanges on which our common shares are then traded, in the over-the-counter market, in negotiated transactions or otherwise at prices and at terms then prevailing or at prices related to the then current market prices or at prices otherwise negotiated. To the extent required, the names of any agent or broker-dealer and applicable commissions or discounts and any other required information with respect to any particular offer will be set forth in a prospectus supplement which will accompany this prospectus. A prospectus supplement also may add, update or change information contained in this prospectus.

Certain selling shareholders named in this prospectus have agreed, subject to certain exceptions, not to sell the shares they are offering for 180 days after the date of the prospectus relating to our initial public offering, which was June 24, 2003. Lock-up agreements relating to 40,565,241 common shares, and 2,555,656 common shares that are issuable upon conversion of an equal number of units of our operating partnership, to be offered by selling shareholders named in this prospectus expired on August 8, 2003. See “Registration Rights and Lock-Up Agreements” beginning on page 140.

Our common shares trade on the New York Stock Exchange under the symbol “AFR.” The last reported sale price on December 5, 2003 was $16.12 per share.

See “Risk Factors” beginning on page 17 of this prospectus for certain risk factors relevant to an investment in our common shares, including, among others:

• We commenced operations in September 2002 and completed our initial public offering in June 2003, and our management has a very limited history of operating a REIT and little experience operating a public company. This limited experience may impede the ability of our management to execute our business plan successfully. • We expect to continue to experience rapid growth and may not be able to adapt our management and operational systems to respond to the acquisition and integration of additional properties, including those acquired since our initial public offering, without unanticipated disruption or expense. • If we are unable to complete our acquisitions under contract or to continue acquiring properties under our contracts with AmSouth Bank, Bank of America, N.A., KeyBank, N.A., and Wachovia Bank, N.A., or through agreements with other financial institutions and entities, our ability to execute our business plan and our operating results could be adversely affected. • Some of the properties that we acquire from financial institutions are vacant or partially vacant. We may incur substantial financial costs if we are unable to lease these properties to other financial institutions or we are forced to make significant capital expenditures to modify the properties for sale or lease to non-bank tenants. • We are dependent on Bank of America, N.A. and Wachovia Bank, N.A., our two largest tenants, for a significant portion of | our revenues, and failure of these tenants to perform their obligations or renew their leases may adversely affect our cash flow and ability to pay dividends at historical levels or at all. • Our formulated price contracts with financial institutions require us to purchase properties on an “as is” basis and, therefore, these properties may have significant problems that we discover after we acquire them and may have a fair market value below the amount that we pay for them. • We may experience conflicts of interest with members of our management or board of trustees, some of whom have a retained interest in our 123 South Broad Street property and own interests in our operating partnership, with respect to major transactions, including dispositions of our properties. • Since our inception, we have derived a majority of our revenues and income from interest income received from investments in residential mortgage-backed securities and other marketable investments. We may be unable to generate comparable revenues or income from our real estate investments going forward in accordance with our business plan. • Our board may alter our investment policies at any time without shareholder approval, and the alteration of these policies may adversely affect our financial performance. |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is December , 2003.

Table of Contents

| Page | ||

| 1 | ||

| 1 | ||

| 2 | ||

| 2 | ||

| 3 | ||

| 4 | ||

| 7 | ||

Private Placement, Formation Transactions and Initial Public Offering | 7 | |

| 8 | ||

| 8 | ||

| 9 | ||

| 10 | ||

| 10 | ||

| 11 | ||

| 12 | ||

| 17 | ||

| 17 | ||

| 27 | ||

| 30 | ||

| 34 | ||

Risks Related to Investments in Residential Mortgage-Backed Securities | ||

| 37 | ||

| 40 | ||

| 41 | ||

| 41 | ||

| 49 | ||

| 50 | ||

| 51 | ||

| 55 | ||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 66 | |

| 66 | ||

| 67 | ||

| 70 | ||

Comparison of Three Months Ended September 30, 2003 and 2002 | 71 | |

| 73 | ||

Comparison of Combined Year Ended December 31, 2002 and Year Ended December 31, 2001 | 76 | |

Comparison of Years Ended December 31, 2001 and December 31, 2000 | 79 | |

| 81 | ||

| 82 | ||

| 83 | ||

| 83 | ||

| 84 | ||

| 85 | ||

| 85 | ||

| 86 | ||

| 86 | ||

| 87 | ||

| 87 | ||

| 87 | ||

| 90 | ||

| 95 | ||

| 96 | ||

| 97 | ||

| 98 | ||

| 99 | ||

| 107 | ||

| 111 | ||

| 111 | ||

| 111 | ||

| 112 | ||

| 113 | ||

| 113 | ||

| 113 | ||

| 113 |

i

Table of Contents

| Page | ||

| 117 | ||

| 117 | ||

| 121 | ||

| 124 | ||

| 124 | ||

| 125 | ||

| 126 | ||

| 128 | ||

| 129 | ||

| 132 | ||

| 132 | ||

| 133 | ||

| 136 | ||

| 138 | ||

| 140 | ||

| 143 | ||

| 143 | ||

Benefits Received by Our Trustees and Executive Officers in Our Formation Transactions | 148 | |

| 148 | ||

| 149 | ||

| 149 | ||

| 150 | ||

| 150 | ||

| 150 | ||

| 150 | ||

| 151 | ||

| 151 | ||

| 151 | ||

| 153 | ||

CERTAIN PROVISIONS OF MARYLAND LAW AND OF OUR DECLARATION OF TRUST AND BYLAWS | 154 | |

| 154 | ||

| 154 | ||

| 154 | ||

| 155 | ||

| 156 | ||

| 156 | ||

| 157 | ||

| 157 | ||

| 157 | ||

| 157 | ||

| 158 | ||

| 159 | ||

| 159 | ||

| 159 | ||

| 159 | ||

| 160 | ||

| 161 | ||

| 161 | ||

| 161 | ||

| 161 | ||

| 162 | ||

| 162 | ||

| 164 | ||

| 174 | ||

| 175 | ||

| 176 | ||

| 179 | ||

| 181 | ||

| 181 | ||

| 181 | ||

| 182 | ||

INDEX TO FINANCIAL STATEMENTS AND FINANCIAL STATEMENT SCHEDULES | F-1 |

You should rely only on the information contained in this prospectus or to which we have referred you. We have not authorized anyone to provide you with information that is different. This prospectus may only be used where it is legal to sell these securities. The information in this prospectus may only be accurate on the date of this prospectus.

ii

Table of Contents

The following summary highlights information contained elsewhere in this prospectus. You should read the entire prospectus, including “Risk Factors,” before making a decision to invest in our common shares. In this prospectus, unless the context suggests otherwise, references to “the company,” “we,” “us” and “our” mean American Financial Realty Trust, including our operating partnership and other subsidiaries. Certain terms used in this prospectus are defined in the glossary beginning on page 182.

We are a self-managed, self-administered REIT and are the only public REIT focused primarily on acquiring and operating properties leased to regulated financial institutions. We were formed in Maryland in May 2002, commenced operations on September 10, 2002 and completed an initial public offering of our common shares on June 30, 2003. As banks continue to divest their corporate real estate, we believe that our contractual relationships, our growing visibility within the banking industry and our flexible acquisition and lease structures position us for continued growth. We seek to lease our properties to banks and other financial institutions using long-term net leases with terms ranging from 10 to 20 years, resulting in stable risk-adjusted returns on our capital.

Our innovative approach is designed to provide banks and other financial institutions with operational flexibility and the benefits of reduced real estate exposure. We seek to become the preferred landlord of leading banks and other financial institutions through the development of mutually beneficial relationships and by offering flexible acquisition structures and lease terms. We believe that our recent transactions with Bank of America, N.A., Wachovia Bank, N.A., KeyBank, N.A. and AmSouth Bank demonstrate our ability to cultivate mutually beneficial relationships with leading financial institutions.

We acquire both core and underutilized real estate from banks through our three acquisition structures:

Sale Leaseback Transactions. Under this structure, we acquire properties and lease them back to the seller pursuant to a triple net or bond net lease, under which rent is based largely upon the property’s purchase price and the tenant’s credit;

Formulated Price Contracts. Pursuant to these agreements, we acquire or assume leasehold interests in the surplus bank branches of a financial institution at a formulated price. This price is typically based on the fair market value of the property as determined through an independent appraisal process, which values the property based on its highest and best use and its alternative use, and then applies a negotiated discount; and

Specifically Tailored Transactions. These transactions, which typically relate to the acquisition of office buildings and often include a partial sale leaseback with the seller, apply leasing and pricing structures that we tailor to meet the seller’s specific needs.

Of the 586 properties that we owned as of October 31, 2003, we acquired 332 properties containing approximately 8.8 million rentable square feet in sale leaseback transactions, 163 properties containing approximately 808,000 rentable square feet under formulated price contracts, and 91 properties containing approximately 7.0 million rentable square feet in specifically tailored transactions.

We completed a private placement of common shares in September 2002, in which we raised net proceeds of approximately $378.6 million. At that time, we acquired our initial properties in our formation transactions, which are described below under “Our Business and Properties—Our Formation.” On June 30, 2003, we completed an initial public offering of our common shares pursuant to which we sold 64,142,500 common shares at $12.50 per share, and raised an aggregate of approximately $741.5 million in net proceeds, after deducting underwriters’ discounts and commissions and offering expenses. See “Our Business and Properties—Our Initial Public Offering.” We used approximately $370.0 million of these proceeds to fund the equity portion of the

1

Table of Contents

purchase price of a portfolio of 158 office buildings, consisting of 8.1 million rentable square feet, which were sold to us by Bank of America, N.A. for an aggregate purchase price of approximately $770.0 million.

As of October 31, 2003, our portfolio consisted of 367 bank branches and 219 office buildings, containing an aggregate of approximately 16.5 million rentable square feet.

Until September 10, 2002, when we acquired our initial properties and operating companies through the formation transactions, we had no historical operations. Our executive offices are located at 1725 The Fairway, Jenkintown, Pennsylvania 19046. Our telephone number is (215) 887-2280.

According to the Federal Deposit Insurance Corporation, or FDIC, commercial banks and savings institutions that are FDIC-insured owned approximately $92.5 billion in operating real estate assets as of December 31, 2002. We have identified two major trends in the banking industry. First, we believe that banks and other financial institutions will continue to sell properties, lease some or all of the space back from the acquiror and reinvest the proceeds from these sales into their primary operating businesses. Second, we anticipate that continued consolidation within the banking industry will create an environment in which larger banks will sell surplus bank branches that other banks will seek to lease as they expand their market presence.

We believe that our business strategy and operating model distinguish us from developers and other owners, operators and acquirors of real estate in a number of ways, including:

| • | Banking Industry Focus. The extensive real estate holdings of the banking industry present us with the opportunity to continue to grow our portfolio in the future. We believe that consolidation activity, the sale of underutilized real estate and other trends in the banking industry are likely to continue to result in acquisition opportunities for us. |

| • | Limited Competition. We believe that we are the first real estate company that acquires the full range of real estate from banks and other financial institutions utilizing our unique formulated price contract structure as well as sale leasebacks and specifically tailored transactions. Most of our acquisitions have not resulted from a competitive bidding process. We believe that our strategy affords us a competitive advantage over more traditional real estate companies in acquiring real estate owned by banks and other financial institutions. |

| • | High Credit Quality Tenants. Our tenant base consists principally of banks and other financial institutions that are highly regulated. As of October 31, 2003, 87.8% of our contractual rent from our current portfolio will be derived from financial institutions in the aggregate and 83.3% from financial institutions with current credit ratings of A or better as reported by Standard & Poor’s. |

| • | Diversified Real Estate Strategy. Our portfolio is diversified geographically and by asset type within the banking industry. As of October 31, 2003, our portfolio included both small and large office buildings, as well as bank branches, leased to 405 different tenants in 27 states and Washington, D.C., including our two largest tenants, Bank of America, N.A. and Wachovia Bank, N.A. Assuming we complete our acquisitions under contract, our portfolio will include properties in 28 states and Washington, D.C. Our business strategy includes traditional principles of diversification that we believe will help to insulate us from regional changes in economic conditions and the financial condition of specific tenants. |

| • | External Growth Opportunities. We believe that our existing relationships with financial institutions, our growing visibility in the banking industry and our flexible acquisition structures will continue to provide us with opportunities to acquire properties that meet our portfolio criteria. |

2

Table of Contents

| • | Internal Growth Opportunities. Through our specifically tailored transactions, we often acquire properties at prices based on the rental income being generated at the time of acquisition. These prices reflect the underutilized space and below market rents at those properties. We also acquire vacant bank branches under our formulated price contracts based on independent appraisals using a valuation methodology that values the property based on its highest and best use and its alternative use, and then applies a negotiated discount. Through our active management and leasing efforts, we believe that we are well-positioned to maximize the value of the underutilized real estate we acquire. In addition, we strive to increase cash flow from these properties by obtaining leases with scheduled rent increases. |

| • | Stable Risk-Adjusted Returns. We typically enter into long-term triple net or bond net leases with our tenants, many of which are the sellers of the properties. As of October 31, 2003, the weighted average lease term of our leases is 13.6 years based on contractual rent. In addition, we anticipate that approximately 87.3% of the contractual rent from our leases as of October 31, 2003, will be generated from triple net and bond net leases where we are not responsible for operating expenses. We believe that these types of leases generate consistent and predictable returns, protecting us from market fluctuations and increases in operating expenses. |

You should carefully consider the matters discussed in the section “Risk Factors” beginning on page 17 prior to deciding whether to invest in our common shares. Some of these risks include:

| • | we commenced operations in September 2002 and completed our initial public offering in June 2003, and our management has a very limited history of operating a REIT and little experience operating a public company. This limited experience could impede the ability of our management to execute our business plan successfully; |

| • | we expect to continue to experience rapid growth and may not be able to adapt our management and operational systems to respond to the acquisition and integration of additional properties, including those acquired since our initial public offering, without unanticipated disruption or expense; |

| • | if we are unable to complete, or experience significant delays in completing, our acquisitions under contract, our ability to pay dividends to our shareholders at historical levels or at all will be adversely affected; |

| • | if we are unable to continue acquiring properties under our contracts with AmSouth Bank, Bank of America, N.A., KeyBank, N.A. and Wachovia Bank, N.A., or through agreements with other financial institutions and entities, our ability to execute our business plan and our operating results could be adversely affected; |

| • | we may be unable to lease our properties, or may incur substantial costs in connection with the leasing of our properties, which may adversely affect our financial condition and results of operations; |

| • | we are dependent upon significant tenants, including Bank of America, N.A. and Wachovia Bank, N.A., that may be difficult or costly to replace. The loss of either of these tenants could have a material adverse effect on our financial condition and results of operations; |

| • | our formulated price contracts with financial institutions require us, with limited exceptions, to purchase properties on an “as is” basis and, therefore, these properties may have significant problems that we discover only after we acquire them and may have a fair market value below the amount that we pay for them; |

| • | we may experience conflicts of interest with members of our management or board of trustees, some of whom have a retained interest in our property at 123 South Broad Street, Philadelphia, PA and own interests in our operating partnership, with respect to major transactions, including dispositions of our properties; |

3

Table of Contents

| • | since our inception, we have derived a majority of our revenues and income from interest income received from investments in our residential mortgage-backed securities and from other marketable investments. We may be unable to generate comparable revenues or income from our real estate investments going forward in accordance with our business plan; |

| • | any of our investment policies and strategies may be amended or waived by our board of trustees at any time without shareholder approval, and the alteration of these policies may adversely affect our financial performance; |

| • | our use of debt financing and our substantial existing debt obligations may decrease our cash flow and put us at a competitive disadvantage; |

| • | if there is a decline in either of the two major trends in the banking industry that we rely upon for our growth, including the continued sale leaseback of real estate by banks and other financial institutions and the continued consolidation within the banking industry, we may be unable to successfully execute our business plan or expand our operations; and |

| • | we invest in investment grade securities, including, among others, residential mortgage-backed securities, as part of our short-term cash management strategy and are exposed to the risks inherent in investing in these instruments. |

As of October 31, 2003, we owned or held leasehold interests in 586 properties located in 27 states and Washington, D.C. containing an aggregate of approximately 16.5 million rentable square feet. As of that date, the aggregate contractual rent expected from our properties was approximately $168.3 million. The following table describes our portfolio as of October 31, 2003:

Our Portfolio as of October 31, 2003

Properties | Number of Buildings | Rentable Square Feet | Occupancy | Percentage of Contractual Rent | ||||||

Office buildings | 219 | 14,642,408 | 89.1 | % | 83.2 | % | ||||

Bank branches | 367 | 1,892,642 | 84.4 | 16.8 | ||||||

Total | 586 | 16,535,050 | 88.5 | % | 100.0 | % | ||||

Weighted Average Remaining Lease Term(1) | Percentage of 2003 Contractual Rent | Percentage of 2003 Contractual Rent | ||||||

Total properties | 13.6 years | 87.8 | % | 87.3 | % |

| (1) | Weighted based on Contractual Rent. |

4

Table of Contents

The following table presents information as of October 31, 2003, regarding the acquisitions we have completed, including the properties we acquired in our formation transactions and excluding properties that we have sold:

Completed Transactions

Seller | Property Type | Acquisition Structure | Closing Date | Number of Buildings | Rentable Square Feet | Purchase Price(1)(2) | ||||||||

| (in thousands) | ||||||||||||||

Formation Transactions | All | Specifically Tailored | Sept. 10, 2002 | 84 | 1,467,939 | $ | 190,697 | |||||||

Wachovia Bank | Bank branches | Formulated Price | Dec. 10, 2002 | 18 | 119,383 | 19,662 | ||||||||

Bank of America | Office buildings | Specifically Tailored | Dec. 16, 2002 | 16 | 528,361 | 33,070 | ||||||||

AmSouth Bank | Bank branches | Formulated Price | Dec. 20, 2002 | 6 | 15,600 | 806 | ||||||||

Dana Commercial Credit | Office buildings | Sale Leaseback | Jan. 9, 2003 | 16 | 3,759,634 | 335,893 | ||||||||

Wachovia Bank | Bank branches | Formulated Price | Feb. 5, 2003 | 5 | 15,519 | 2,836 | ||||||||

AmSouth Bank | Bank branch | Formulated Price | Feb. 12, 2003 | 1 | 2,817 | 268 | ||||||||

Wachovia Bank | Bank branches | Formulated Price | Feb. 19, 2003 | 7 | 20,107 | 4,826 | ||||||||

Bank of America | Office buildings | Specifically Tailored | Mar. 20, 2003 | 1 | 15,278 | 768 | ||||||||

Pitney Bowes—Wachovia | Office buildings | Sale Leaseback | Mar. 31, 2003 | 15 | 635,218 | 85,206 | ||||||||

| Bank branches | Sale Leaseback | Mar. 31, 2003 | 72 | 437,077 | 59,155 | |||||||||

Finova Capital—BB&T | Office buildings | Sale Leaseback | Apr. 15, 2003 | 3 | 201,897 | 16,948 | ||||||||

| Bank branches | Sale Leaseback | Apr. 15, 2003 | 7 | 48,911 | 4,161 | |||||||||

Bank of America | Bank branches | Formulated Price | May 1, 2003 | 4 | 30,260 | 1,257 | ||||||||

Wachovia | Bank branches | Formulated Price | May 8, 2003 | 1 | 2,972 | 347 | ||||||||

Wachovia | Bank branches | Formulated Price | June 6, 2003 | 4 | 21,587 | 1,083 | ||||||||

Bank of America | Office buidings | Sale Leaseback | June 30, 2003 | 90 | 3,043,777 | 317,138 | ||||||||

| Office buildings | Specifically Tailored | June 30, 2003 | 68 | 5,011,499 | 456,888 | |||||||||

Bank of America | Office buildings | Specifically Tailored | July 10, 2003 | 1 | 28,094 | 1,721 | ||||||||

Wachovia | Bank branches | Formulated Price | July 17, 2003 | 1 | 4,530 | 622 | ||||||||

Bank of America | Bank branches | Formulated Price | August 18, 2003 | 2 | 9,018 | 518 | ||||||||

Citigroup | Bank branches | Formulated Price | August 28, 2003 | 18 | 109,124 | 9,323 | ||||||||

Wachovia | Bank branches | Formulated Price | August 29, 2003 | 11 | 67,649 | 3,718 | ||||||||

Single acquisitions (non-bank sellers) | Formulated Price | August 2003 | 2 | 5,228 | 493 | |||||||||

Pitney Bowes—Key Bank | Bank branches | Sale Leaseback | September 16, 2003 | 31 | 153,950 | 36,444 | ||||||||

Pitney Bowes—Bank of America | Bank branches | Sale Leaseback | September 25, 2003 | 97 | 479,418 | 89,233 | ||||||||

First Charter Bank | Bank branches | Formulated Price | September 29, 2003 | 2 | 5,935 | 1,014 | ||||||||

Wachovia | Bank branches | Formulated Price | September 30, 2003 | 2 | 31,210 | 1,997 | ||||||||

First States Wilmington, LP | Office buildings | Specifically Tailored | September 30, 2003 | 1 | 263,058 | 49,106 | ||||||||

Total | 586 | 16,535,050 | $ | 1,725,198 | (3) | |||||||||

| (1) | Includes all acquisition costs. |

| (2) | Excludes other non-real estate assets acquired. |

| (3) | Includes value of acquired intangible assets. |

Included in the completed transactions above is our acquisition on June 30, 2003 from Bank of America, N.A. of a portfolio of 27 large office buildings and 131 small office buildings containing an aggregate of approximately 8.1 million rentable square feet. The aggregate purchase price for the properties was approximately $770.0 million, approximately $370.0 million of which we funded using a portion of the proceeds from our initial public offering, with the remainder financed through a bridge loan in the amount of $400 million that we obtained from German

5

Table of Contents

American Capital Corporation. We currently expect that three of the properties will not be occupied by Bank of America, N.A. by June 30, 2004. If we are unable to lease these three properties to other financial institutions, we will attempt to sell them. These properties represent approximately 2.7% of the aggregate rentable square feet in the portfolio. Bank of America, N.A. has initially leased an aggregate of approximately 64.7% of the rentable square feet in this portfolio with an initial lease term of 20 years. Excluding the three unoccupied sites, the Bank of America, N.A. lease constitutes approximately 67.7% of the remaining rentable square feet for the initial 20 year lease term. Bank of America, N.A. has the option to renew this lease for up to six successive five year terms. In the case of a renewal, the rent will be the fair market rental value of the premises, as determined in accordance with the lease. Bank of America, N.A.’s obligations under this lease are unconditionally guaranteed by its parent, Bank of America Corporation.

In addition to the portion of the premises subject to the 20 year lease, Bank of America, N.A. currently occupies approximately 847,000 rentable square feet that it may rent at a reduced rate for up to 12 months after the commencement of the lease. Bank of America, N.A. is required to notify us, within 12 months after the commencement of the 20 year lease, whether it intends to vacate this square footage or add it to the lease at a fair market rate or at the rate established by the 20 year lease, depending on the length of the term selected. Approximately 10.1% of the rentable square feet in the portfolio is currently leased to third parties. Bank of America will pay us approximately $44.0 million in annual base rent under the 20 year lease for this portfolio, plus their portion of the operating expenses associated with the leased space, excluding the 847,000 rentable square feet that is occupied on a reduced basis.

We have also engaged in the following financing transactions:

| • | On April 30, 2003, we obtained a $100.0 million credit facility from a syndicate of lenders, including Bank of America, N.A., UBS AG, Cayman Islands Branch, and Wachovia Bank, N.A. The credit facility has a term of three years, bears interest at an annual rate of LIBOR plus 1.25%, and will be secured by a pledge of membership interests in a special purpose entity that is the borrower under the facility, as well as, when applicable, an assignment of leases and rents that would only be recorded in the event of a default. Availability under this credit facility will be determined based on the net present value of the monthly base rent payments on the properties securing the loan. Only properties under bond net leases with terms of at least five years, and with tenants having senior corporate debt with a minimum credit rating of A- or better, may be used to secure our obligations under this credit facility by the borrower. This credit facility was terminated in October 2003. |

| • | On April 30, 2003, we completed a long-term financing through Lehman Brothers Bank, FSB for an aggregate principal amount of $80.0 million. We have issued to Lehman Brothers Bank a total of 64 promissory notes secured by leases on 64 properties that are leased to Wachovia Bank, N.A. We utilized $75.0 million of this $80.0 million financing to fund the repayment of a bridge loan from Bank of America, N.A. The notes have been issued in two series. The notes in the first series relate to 23 properties, are due on June 10, 2023, bear interest at a fixed annual rate of 5.496% and are secured by mortgages on, and assignments of leases and rents for, properties to which the notes relate. The notes in the second series relate to the remaining 41 properties, are due on September 10, 2010, bear interest at a fixed annual rate of 4.066% and are secured by mortgages on, and assignments of leases and rents for, the properties to which the notes relate. Lehman Brothers Bank will securitize the notes through an offering of lease-backed pass through certificates to one or more institutional investors. |

| • | On May 23, 2003, we completed a long-term financing arranged through Banc of America Securities LLC for an aggregate principal amount of $200.0 million. In connection with this financing, we have issued a note for the full principal amount of the loan to Wells Fargo Bank Northwest, N.A., as trustee for a group of institutional investors. This note is due on January 10, 2011, bears interest at a fixed annual rate of 4.04%, and is secured by mortgages on, and an assignment of leases and rents for, 14 office buildings acquired from a wholly owned subsidiary of Dana Commercial Credit Corporation. We utilized the proceeds of this financing to fund the repayment of a bridge loan from Bank of America, N.A. |

6

Table of Contents

| • | On October 1, 2003, we completed a long-term financing with an affiliate of Deutsche Bank Securities Inc. for an aggregate principal amount of $440.0 million. This financing was entered into to refinance a bridge loan we obtained on June 30, 2003 from an affiliate of Deutsche Bank to finance a portion of our acquisition of 158 properties from Bank of America, N.A. in a specifically tailored transaction. |

The note payable on the long-term financing bears interest through November 30, 2003 at the variable rate payable under the bridge note and then changes to an effective interest rate of 5.78%, including the amortization of the corresponding interest rate swap agreement that was terminated in connection with consummating the long-term financing. The long-term financing matures on December 31, 2013 and has a balloon payment due of $369,910. Interest only payments will be made during the initial 20 months of the term. The long-term financing is secured by a first lien mortgage and an assignment of rents and leases on certain properties acquired in the related purchase of properties from Bank of America.

The bridge loan bore interest at the rate of 30-day LIBOR (1.12% at September 30, 2003) plus 1.50% and required interest-only payments through the maturity date of December 31, 2003.

| • | On July 18, 2003, we completed a financing with Deutsche Bank Securities Inc., acting on behalf of Deutsche Bank AG, Cayman Islands Branch, for a $300.0 million warehouse facility. Borrowings under this facility will be extended in a series of advances, each of which will be used to acquire a specific property. Borrowings under this facility may be used only to acquire properties that may be financed on a long-term basis through credit-tenant lease or conduit commercial mortgage-backed securities financing. Advances under this facility will be made in the aggregate principal amount of up to 80% of the lesser of either (i) the maximum amount of subsequent debt financing that can be secured by the properties that we acquire with borrowings under this facility or (ii) the acquisition cost of those properties. This facility has a term of three years and bears interest at an annual rate of LIBOR plus either (x) with respect to conduit properties, 1.75%, or (y) with respect to credit tenant lease properties, an amount, ranging from 1.25% to 2.50%, based on the credit rating of the tenant(s) in the property being purchased with the proceeds of the specific advance. We paid a fee of 1.25% of the total availability in connection with this facility, including $500,000 paid upon signing the commitment. We have not received any advances under this warehouse facility to date. |

As of October 31, 2003, we do not have any acquisitions under contract.

Recent Developments

On November 26, 2003, we entered into a definitive agreement with an affiliate of GE Pension Trust to acquire Bank of America Plaza, a 750,000 square foot Class A office building located in St. Louis, Missouri. The total purchase price, exclusive of any debt prepayment and closing costs, will be approximately $82.0 million. The property is approximately 96.0% leased to high credit tenants, including Bank of America, which leases approximately 467,000 square feet and IBM, which leases approximately 155,000 square feet. Other tenants include PricewaterhouseCoopers and KeyBank. Total 2004 projected net operating income will be approximately $7.6 million. We anticipate closing this acquisition by the end of 2003.

Private Placement, Formation Transactions and Initial Public Offering

We sold 40,263,441 common shares on September 10, 2002, in a private placement, and completed the sale of an additional 501,800 common shares on October 7, 2002 pursuant to the exercise by Friedman, Billings, Ramsey & Co., Inc. of its option to purchase additional shares. These sales resulted in aggregate net proceeds of

7

Table of Contents

approximately $378.6 million. On September 10, 2002, in our formation transactions, we acquired from our predecessor entities and other related parties 87 bank branches and six office buildings containing approximately 1.5 million rentable square feet. We also acquired American Financial Resources Group, Inc., or AFRG, Strategic Alliance Realty Group, LLC and several other affiliated entities in order to obtain the capacity to provide our properties with asset management, leasing, property management and accounting and finance services. In connection with these transactions, we assumed contracts and letters of intent to purchase additional properties, subject to satisfactory completion of our due diligence, from financial institutions such as Bank of America, N.A., KeyBank, N.A. and Wachovia Bank, N.A., having a potential aggregate gross purchase price of approximately $256.0 million. The aggregate purchase price for the 93 properties, the acquired entities and assumed contracts and letters of intent was approximately $230.5 million.

In addition, on June 30, 2003, we sold 64,142,500 common shares in an underwritten initial public offering at $12.50 per share. In connection with this offering, we received proceeds of approximately $741.5 million, after deducting underwriters’ discounts and commissions and offering expenses. In addition, in connection with our initial public offering, a selling shareholder also sold 200,000 common shares.

Some of our executives and trustees have interests that may conflict with our interests and result in them receiving personal benefits from this offering. Our executives have been granted restricted common shares that will be effective upon completion of this offering. Nicholas S. Schorsch, our President and Chief Executive Officer, Jeffrey C. Kahn, our Senior Vice President—Acquisitions and Dispositions, and Shelley D. Schorsch, our Senior Vice President—Corporate Affairs and the spouse of Nicholas S. Schorsch, all own interests in First States Wilmington, L.P., which owned the Three Beaver Valley Road property in Wilmington, Delaware. We exercised our option to acquire this property on September 30, 2003 using proceeds of our initial public offering. The exercise price of the option was approximately $51.8 million, of which $44.8 million consisted of the assumption of debt. The determination to exercise this option was made by members of our board of trustees who did not have any interest in First States Wilmington, L.P. The executive officers and trustees who have an interest in First States Wilmington, L.P. also own a majority of the 11% minority interest in First States Partners II, L.P., which owns our 123 South Broad Street property.

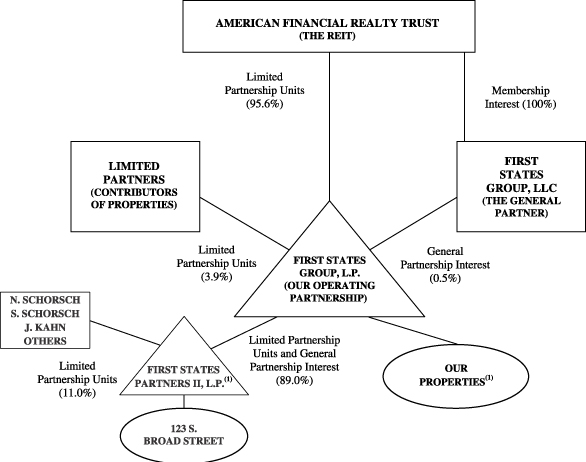

Through our wholly owned subsidiary, First States Group, LLC, we are the sole general partner of our operating partnership, First States Group, L.P. We own the general partnership interest and limited partnership units of our operating partnership representing approximately 96.1% of the total partnership interests as of September 30, 2003, including the 0.5% general partnership interest. The remaining holders of limited partnership units may convert their units into common shares on a one-for-one basis, subject to adjustments for stock splits, dividends, recapitalizations and similar events. At our option, in lieu of issuing common shares upon conversion of units, we may redeem the units tendered for conversion for a cash amount equal to the value of the common shares. We expect that, when limited partnership unitholders elect to convert their units, we will typically issue common shares and not redeem the units for cash. Holders of units have received and will receive distributions equivalent to the dividends we pay to holders of our common shares. We conduct all of our business through our operating partnership, and hold all of our interests in properties in limited liability companies or limited partnerships that are wholly owned subsidiaries of our operating partnership, except that we own 89.0% of First States Partners II, L.P., which owns our 123 South Broad Street property. As the sole owner of the general partner of our operating partnership, we have the exclusive power to manage and conduct our operating partnership’s business, subject to the limitations described in the Amended and Restated Agreement of Limited Partnership of our operating partnership. See “Partnership Agreement” beginning on page 159.

8

Table of Contents

The following chart illustrates our structure:

| (1) | We own 100% of the entities that directly own our properties, except that we own 89% of First States Partners II, L.P., which owns 100% of our 123 South Broad Street property, which accounts for approximately 8.0% of our contractual rent as of October 31, 2003. The remaining 11% of First States Partners II, L.P. is owned by various holders, including the members of our management and board of trustees listed above, who own a majority of the 11% minority interest. Our ownership of First States Partners II, L.P. and the ownership of the 11% minority interest are described in more detail under “Certain Relationships and Related Transactions.” |

Registration Rights and Lock-Up Agreements

Resale Registration Statement

In connection with registration rights agreements we entered into in September 2002 with the purchasers of common shares in our September 2002 private placement and the holders of units of our operating partnership, we agreed to file the registration statement of which this prospectus is a part, referred to as the resale registration statement.

| • | Common Shareholders. The resale registration statement includes 42,088,008 common shares issued in connection with private placements of our common shares completed in September 2002 and at the time of the merger of our predecessor entities into our company as part of our formation transactions. |

9

Table of Contents

| • | Operating Partnership Unitholders. The resale registration statement also includes 4,455,966 common shares issuable upon the conversion of an equal number of units of our operating partnership, which units were issued to certain individuals and entities who contributed our initial properties in connection with our formation transactions. |

Lock-Up Agreements

| • | Trustees, Executive Officers and Certain Other Parties. Pursuant to the underwriting agreement for our initial public offering, we, our trustees, our executive officers at the time of the offering and Friedman, Billings, Ramsey Group, Inc., the successor-by-merger to FBR Asset Investment Corporation and an affiliate of Friedman, Billings, Ramsey & Co., Inc., are restricted from, without the prior written consent of both Banc of America Securities LLC and Friedman, Billings, Ramsey & Co., Inc., directly or indirectly offering, selling, contracting to sell, pledging or otherwise transferring, disposing of or hedging our common shares or securities convertible into or exchangeable for common shares for a period of 180 days following the date of the prospectus relating to our initial public offering, which was June 24, 2003. These restrictions affect an aggregate of 5,742,198 common shares, and 2,195,452 common shares issuable upon the conversion of an equal number of units of our operating partnership. |

| • | Other Common Shareholders. The holders of up to 40,565,241 common shares issued in our September 2002 private placement that are being registered under the resale registration statement were restricted from, without the prior written consent of both Banc of America Securities LLC and Friedman, Billings, Ramsey & Co., Inc., directly or indirectly offering, selling, contracting to sell or otherwise disposing of or hedging their common shares covered by the resale registration statement for 45 days following the date of the prospectus relating to our initial public offering, which was June 24, 2003. This lock-up period expired on August 8, 2003. |

| • | Operating Partnership Unitholders. The holders of the 2,555,656 common shares that are issuable upon the conversion of an equal number of units of our operating partnership not owned by our trustees, executive officers or certain other parties mentioned above, which shares are being registered under the resale registration statement, were restricted from, without the prior written consent of both Banc of America Securities LLC and Friedman, Billings, Ramsey & Co., Inc., directly or indirectly offering, selling, contracting to sell or otherwise disposing of or hedging their common shares covered by the resale registration statement for 45 days following the date of the prospectus relating to our initial public offering, which was June 24, 2003. This lock-up period expired on August 8, 2003. |

This prospectus relates to up to 46,543,974 common shares that the selling shareholders named in this prospectus may offer for sale from time to time. The selling shareholders named in this prospectus either currently own the common shares they are offering, or may acquire these common shares upon the conversion of their units of limited partnership interest in our operating partnership, First States Group, L.P., into common shares.

We will not receive any proceeds from the sale by the selling shareholders of the common shares being offered by this prospectus. We have agreed, however, to pay various expenses relating to registration of these common shares under applicable securities laws.

10

Table of Contents

Dividend Policy and Distributions

We intend to distribute to our shareholders each year all or substantially all of our REIT taxable income so as to avoid paying corporate income tax and excise tax on our earnings and to qualify for the tax benefits accorded to REITs under the Internal Revenue Code of 1986, as amended. The actual amount and timing of distributions, however, will be at the discretion of our board of trustees and will depend upon actual results of operations and a number of other factors discussed in the section “Dividend Policy and Distributions” on page 50, including:

| • | the timing of the investment of the proceeds of our initial public offering; |

| • | the rent received from our tenants; |

| • | the ability of our tenants to meet their other obligations under their leases; and |

| • | our operating expenses. |

For the period from September 10, 2002 through December 31, 2002, we declared our initial dividend of $0.22 per common share, payable to shareholders of record on December 31, 2002. We distributed this dividend on January 20, 2003.

On March 21, 2003, we declared a dividend of $0.25 per common share, payable with respect to the quarter ended March 31, 2003, to shareholders of record on March 31, 2003. We distributed this dividend on April 17, 2003.

On May 21, 2003, we declared a dividend of $0.25 per common share, payable with respect to the quarter ending June 30, 2003, to shareholders of record on June 10, 2003. We distributed this dividend on July 18, 2003.

On September 17, 2003, we declared a dividend of $0.25 per common share, payable with respect to the quarter ended September 30, 2003, to shareholders of record on September 30, 2003. We distributed this dividend on October 15, 2003.

11

Table of Contents

Summary Selected Financial Information

The summary selected financial information presented below under the captions “Operating Information” and “Balance Sheet Information” as of December 31, 2002 and for the period from September 10, 2002 to December 31, 2002 are derived from the consolidated financial statements of American Financial Realty Trust. The financial information as of December 31, 2001 and for the period January 1, 2002 to September 9, 2002 and for each of the years in the three year period ended December 31, 2001 are derived from the combined financial statements of our predecessor entities, which consisted of American Financial Resource Group, Inc. and its wholly owned subsidiaries, First States Management Corp., First States Properties, Inc., Strategic Alliance Realty LLC, First States Properties, L.P., First States Partners, L.P., Chester Court Realty, LP., Dresher Court Realty, L.P., First States Partners II, L.P., First States Partners III, L.P., First States Holdings, L.P., and the general partner of each of these partnerships, and which are deemed to be our predecessor entities for accounting purposes. These financial statements have been audited by KPMG LLP, our independent auditor. The summary selected financial information presented below as of September 30, 2003, and for the nine month period ended September 30, 2003 and the period from January 1, 2002 to September 9, 2002 and the period from September 10, 2002 to December 31, 2002 are derived from the unaudited consolidated financial statements of American Financial Realty Trust and our predecessor entities, respectively, and include all adjustments, consisting of normal recurring adjustments, which we consider necessary for a fair presentation of our financial condition and results of operations as of such date and for such periods under generally accepted accounting principles. The consolidated balance sheets as of September 30, 2003 and December 31, 2002 and the combined balance sheet as of December 31, 2001, and the related consolidated statements of operations, shareholders’ equity and comprehensive income (loss) and cash flows for nine month period ended September 30, 2003 and for the period from September 10, 2002 to December 31, 2002, and the related combined statements of operations, owners’ net investment and cash flows for the period January 1, 2002 to September 9, 2002 and for each of the years in the two year period ended December 31, 2001, and the report thereon, are included elsewhere in this prospectus. The summary selected financial information presented below as of and for the year ended December 31, 1998 is derived from the unaudited combined financial statements of our predecessor entities and includes adjustments, consisting of normal recurring adjustments, which we consider necessary for a fair presentation of our financial condition and results of operations as of such date and for such period under generally accepted accounting principles. The unaudited pro forma Balance Sheet Information of American Financial Realty Trust as of December 31, 2002 and the unaudited pro forma Operating Information for the nine month period ended September 30, 2003 and the year ended December 31, 2002 reflects the historical financial information adjusted to give effect to recently completed transactions, including our initial public offering, and our acquisitions under contract.

The historical financial statements of our predecessor entities represent the combined financial condition and results of operations of the entities that previously owned our initial properties and operating companies, as well as several properties and an entity controlled by Nicholas S. Schorsch, our President, Chief Executive Officer and Vice Chairman of our board of trustees, or by his wife, Shelley D. Schorsch, our Senior Vice President—Corporate Affairs, that we did not acquire in connection with our formation transactions. See “Our Business and Properties—Our Formation.” In addition, the historical financial information for our predecessor entities included herein and set forth elsewhere in this prospectus reflects our predecessor entities’ corporate investment strategy. Historically, our predecessor entities often funded new acquisitions by selling properties, a strategy which we discontinued when we became a REIT. Accordingly, historical financial results are not indicative of our future performance. In addition, since the financial information presented below is only a summary and does not provide all of the information contained in our financial statements, including related notes, you should read “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” the financial statements, including related notes and the Independent Auditors’ Report, which refers to the adoption of Statement of Financial Accounting Standards No.144, Accounting for the Impairment or Disposal of Long-Lived Assets and to the fact that the consolidated financial information for American Financial Realty Trust is presented on a different cost basis than that of the Predecessor and, therefore, is not comparable, and “Unaudited Pro Forma Consolidated Financial Information,” each contained elsewhere in this prospectus. Pro forma information has been compiled from historical financial and other information, but does not purport to represent what our financial position or results of operations actually would have been had the transactions occurred on the dates indicated, or to project our financial performance for any future period.

12

Table of Contents

Nine Months Ended September 30, | Pro Forma Year Ended December 31, 2002 | September 10, 2002 to December 31, 2002 | ||||||||||||||||||||||

| Pro Forma 2003 | 2003 | Predecessor January 1, 2002 to | ||||||||||||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||

Operating Information: | ||||||||||||||||||||||||

Revenues: | ||||||||||||||||||||||||

Rental income | $ | 111,634 | $ | 62,028 | $ | 17,869 | $ | 149,057 | $ | 8,338 | ||||||||||||||

Operating expense reimbursements | 49,465 | 18,336 | 5,577 | 72,400 | 2,813 | |||||||||||||||||||

Interest income | 2,362 | 2,362 | 105 | 2,456 | 2,351 | |||||||||||||||||||

Other income | 1,342 | 724 | 822 | 1,919 | 37 | |||||||||||||||||||

Total revenues | 164,803 | 83,450 | 24,373 | 225,832 | 13,539 | |||||||||||||||||||

Expenses: | ||||||||||||||||||||||||

Property operating expenses | 72,453 | 28,660 | 7,198 | 101,103 | 3,828 | |||||||||||||||||||

General and administrative expenses | 19,470 | 13,026 | 4,695 | 20,805 | 3,645 | |||||||||||||||||||

Interest expense | 32,651 | 19,748 | 9,745 | 46,898 | 3,421 | |||||||||||||||||||

Depreciation and amortization | 54,605 | 30,050 | 5,822 | 73,996 | 2,911 | |||||||||||||||||||

Total expenses | 179,179 | 91,484 | 27,460 | 242,802 | 13,805 | |||||||||||||||||||

Income (loss) before investment income and expenses, net realized gain (loss) on sales of properties and investments, minority interest and discontinued operations | (14,376 | ) | (8,034 | ) | (3,087 | ) | (16,970 | ) | (266 | ) | ||||||||||||||

Interest income from residential mortgage-backed securities, net | (5,822 | ) | 9,016 | — | — | 16,385 | ||||||||||||||||||

Interest expense on reverse repurchase agreements | (817 | ) | (4,355 | ) | — | — | 6,578 | |||||||||||||||||

Net interest income on residential mortgage-backed securities | (5,005 | ) | 4,661 | — | — | 9,807 | ||||||||||||||||||

Net gain (loss) on sales of properties, net | — | — | — | 715 | 715 | |||||||||||||||||||

Realized gain (loss) on sales of investments, net | (9,241 | ) | (9,241 | ) | — | (280 | ) | (280 | ) | |||||||||||||||

Income (loss) from continuing operations before minority interest | (28,622 | ) | (12,614 | ) | (3,087 | ) | (16,535 | ) | 9,976 | |||||||||||||||

Minority interest | 1,251 | 1,190 | — | 723 | (849 | ) | ||||||||||||||||||

Income (loss) from continuing operations | (27,371 | ) | (11,424 | ) | (3,087 | ) | (15,812 | ) | 9,127 | |||||||||||||||

Discontinued operations: | ||||||||||||||||||||||||

Income (loss) from operations | — | (1,788 | ) | (865 | ) | — | (211 | ) | ||||||||||||||||

Gains on disposals | — | 3,927 | 9,609 | — | 28 | |||||||||||||||||||

Income (loss) from discontinued operations | — | 2,139 | 8,744 | — | (183 | ) | ||||||||||||||||||

Net income (loss) | $ | (27,371 | ) | $ | (9,285 | ) | $ | 5,657 | $ | (15,812 | ) | $ | 8,944 | |||||||||||

Basic earnings (loss) per share: | ||||||||||||||||||||||||

From continuing operations | $ | (0.25 | ) | $ | (0.19 | ) | $ | (0.15 | ) | $ | 0.22 | |||||||||||||

From discontinued operations |

| — |

|

| 0.04 |

|

| — |

| — | ||||||||||||||

Total basic earnings (loss) per share | $ | (0.25 | ) | $ | (0.15 | ) | $ | (0.15 | ) | $ | 0.22 | |||||||||||||

Diluted earnings (loss) per share: | ||||||||||||||||||||||||

From continuing operations | $ | (0.25 | ) | $ | (0.19 | ) | $ | (0.15 | ) | $ | 0.21 | |||||||||||||

From discontinued operations | — | 0.03 | — | — | ||||||||||||||||||||

Total diluted earnings (loss) per share | $ | (0.25 | ) | $ | (0.16 | ) | $ | (0.15 | ) | $ | 0.21 | |||||||||||||

Weighted average common shares outstanding (basic) | 64,153 | 107,782 | 42,168 | |||||||||||||||||||||

Weighted average common shares outstanding (diluted) | 68,611 | 112,237 | 46,938 | |||||||||||||||||||||

Dividends/distributions declared for shareholders per share and operating partnership unitholders per unit | — | $ | 0.75 | — | $ | 0.22 | ||||||||||||||||||

13

Table of Contents

Pro Forma September 30, | September 30, 2003 | December 31, 2002 | |||||||

| (unaudited) | (unaudited) | ||||||||

| (in thousands) | |||||||||

Balance Sheet Information: | |||||||||

Real estate investments, at cost | $ | 1,611,457 | $ | 1,611,457 | $ | 250,544 | |||

Cash and cash equivalents | 184,053 | 184,053 | 60,842 | ||||||

Marketable investments and accrued interest | 85,088 | 85,088 | 144,326 | ||||||

Residential mortgage-backed securities portfolio | — | — | 1,116,119 | ||||||

Intangible assets, net | 141,802 | 141,802 | 2,413 | ||||||

Total assets | 2,075,555 | 2,075,555 | 1,605,165 | ||||||

Mortgage notes payable | 467,689 | 467,689 | 149,886 | ||||||

Bridge and other notes payable | 400,000 | 400,000 | — | ||||||

Reverse repurchase agreements | — | — | 1,053,529 | ||||||

Total debt | 867,689 | 867,689 | 1,203,415 | ||||||

Value of assumed lease obligations, net | 51,780 | 51,780 | 1,268 | ||||||

Total liabilities | 1,025,394 | 1,025,394 | 1,231,990 | ||||||

Minority interest | 38,525 | 38,525 | 36,513 | ||||||

Shareholders’ equity | 1,011,636 | 1,011,636 | 336,662 | ||||||

Total liabilities and shareholders’ equity | 2,075,555 | 2,075,555 | 1,605,165 | ||||||

Nine Months | Predecessor | September 10, 2002 to December 31, 2002 | ||||||||||||||

January 1, 2002 to | ||||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||

| (in thousands) | ||||||||||||||||

Other Information: | ||||||||||||||||

Funds from operations (unaudited)(1) | $ | 16,952 | $ | — | $ | 12,496 | ||||||||||

Adjusted funds from operations (unaudited)(2) | 48,353 | — | 12,436 | |||||||||||||

Cash flows: | ||||||||||||||||

From operating activities | 77,389 | 2,382 | 12,594 | |||||||||||||

From investing activities | (3,595 | ) | 12,413 | (1,378,288 | ) | |||||||||||

From financing activities | 49,417 | (13,176 | ) | 1,426,536 | ||||||||||||

| (1) | Funds from operations (FFO) represents net income (loss) before minority interest in our operating partnership (computed in accordance with generally accepted accounting principles, or GAAP), excluding gains (or losses) from debt restructuring, including gains (or losses) on sales of property, plus real estate related depreciation and amortization (excluding amortization of deferred costs) and after adjustments for unconsolidated partnerships and joint ventures. Our calculation of funds from operations may differ from the methodology for calculating funds from operations utilized by other equity REITs and, accordingly, may not be comparable to other REITs. Further, funds from operations does not represent amounts available for management’s discretionary use because of needed capital replacement or expansion, debt service obligations or other commitments or uncertainties. Funds from operations should not be considered as an alternative for net income as a measure of profitability nor is it comparable to cash flow provided by operating activities determined in accordance with GAAP. |

| (2) | Adjusted funds from operations (AFFO) is a computation made by analysts and investors to measure a real estate company’s cash flow generated from operations. AFFO is generally calculated by subtracting from or adding to FFO (i) normalized recurring expenditures that are capitalized by the REIT and then amortized, |

14

Table of Contents

but which are necessary to maintain a REIT’s properties and its revenue stream (e.g., leasing commissions and tenant improvement allowances), (ii) straightlining of rents and (iii) amortization of deferred costs. |

Set forth below is a reconciliation of our calculations of FFO and AFFO to net income:

| Nine Months Ended September 30, 2003 | September 10, 2002 to December 31, 2002 | |||||||

(in thousands, except per share data) | ||||||||

Funds from operations: | ||||||||

Net income (loss) | $ | (9,285 | ) | $ | 8,944 |

| ||

Minority interest in operating partnership |

| (1,013 | ) |

| 938 |

| ||

Depreciation and amortization |

| 27,310 |

|

| 2,629 |

| ||

Non real estate depreciation |

| (60 | ) |

| (15 | ) | ||

Funds from operations | $ | 16,952 |

| $ | 12,496 |

| ||

Funds from operations per share (diluted) | $ | .24 |

| $ | 0.27 |

| ||

Adjusted funds from operations: | ||||||||

Funds from operations | $ | 16,952 |

| $ | 12,496 |

| ||

Straightline rental income |

| 16,320 |

|

| (592 | ) | ||

Straightline rent expense |

| 64 |

|

| 44 |

| ||

Tenant improvements and leasing commissions |

| (592 | ) |

| (369 | ) | ||

Amortization of deferred costs, including the value of in-place leases, customer relationship value and financing costs |

| 4,796 |

|

| 398 |

| ||

Amortization of fair market rental adjustment, net |

| (142 | ) |

| (36 | ) | ||

Amortization of deferred compensation |

| 1,714 |

|

| 215 |

| ||

Realized (gain) loss on sale of investments, net |

| 9,241 |

|

| 280 |

| ||

Adjusted funds from operations | $ | 48,353 |

| $ | 12,436 |

| ||

| Predecessor | ||||||||||||||||||||

January 1, 2002 to September 9, 2002 | Year Ended December 31, | |||||||||||||||||||

| 2001 | 2000 | 1999 | 1998 | |||||||||||||||||

| �� | (unaudited) | |||||||||||||||||||

| (in thousands) | ||||||||||||||||||||

Operating Information: | ||||||||||||||||||||

Revenues: | ||||||||||||||||||||

Rental income | $ | 17,314 | $ | 25,815 | $ | 13,483 | $ | 5,837 | $ | 1,365 | ||||||||||

Operating expense reimbursements | 5,577 | 7,663 | 2,085 | 875 | 29 | |||||||||||||||

Interest income | 105 | 188 | 485 | 482 | 92 | |||||||||||||||

Other income | 822 | 582 | 1,173 | 748 | 789 | |||||||||||||||

Total revenues | 23,818 | 34,248 | 17,226 | 7,942 | 2,275 | |||||||||||||||

Expenses: | ||||||||||||||||||||

Property operating expenses | 7,200 | 9,770 | 5,194 | 2,403 | 211 | |||||||||||||||

General and administrative expenses | 4,695 | 8,212 | 7,185 | 3,686 | 810 | |||||||||||||||

Interest expense | 9,737 | 14,071 | 6,042 | 2,410 | 507 | |||||||||||||||

Depreciation and amortization | 5,849 | 8,468 | 3,082 | 1,003 | 542 | |||||||||||||||

Total expenses | 27,481 | 40,521 | 21,503 | 9,502 | 2,070 | |||||||||||||||

Income (loss) before net gains on sale of properties | (3,663 | ) | (6,273 | ) | (4,277 | ) | �� | (1,560 | ) | 205 | ||||||||||

Net gain on sale of properties | — | 4,107 | 8,934 | 4,468 | — | |||||||||||||||

Income (loss) from continuing operations | (3,663 | ) | (2,166 | ) | 4,657 | 2,908 | 205 | |||||||||||||

Discontinued operations: | ||||||||||||||||||||

Income (loss) from operations | (180 | ) | (114 | ) | 499 | 165 | (6 | ) | ||||||||||||

Gains on disposals | 9,500 | — | — | — | — | |||||||||||||||

Income (loss) from discontinued operations | 9,320 | (114 | ) | 499 | 165 | (6 | ) | |||||||||||||

Net income (loss) | $ | 5,657 | $ | (2,280 | ) | $ | 5,156 | $ | 3,073 | $ | 199 | |||||||||

15

Table of Contents

| Predecessor | ||||||||||||||||

| December 31, | ||||||||||||||||

| 2001 | 2000 | 1999 | 1998 | |||||||||||||

| (unaudited) | ||||||||||||||||

| (in thousands) | ||||||||||||||||

Balance Sheet Information: | ||||||||||||||||

Real estate investments, at cost | $ | 177,578 | $ | 172,518 | $ | 37,495 | $ | 22,372 | ||||||||

Cash and cash equivalents | 1,597 | 1,806 | 321 | 305 | ||||||||||||

Short-term investments | 546 | 14 | 6,359 | 7,949 | ||||||||||||

Total assets | 183,760 | 182,186 | 48,807 | 31,824 | ||||||||||||

Mortgage notes payable | 158,587 | 158,700 | 48,728 | 32,397 | ||||||||||||

Line of credit borrowings | 3,791 | 396 | 400 | — | ||||||||||||

Other indebtedness | 4,754 | 5,093 | 75 | — | ||||||||||||

Total debt | 167,132 | 164,189 | 49,203 | 32,397 | ||||||||||||

Total liabilities | 174,611 | 169,670 | 51,245 | 32,759 | ||||||||||||

Owners’ net investment | 9,149 | 12,516 | (2,438 | ) | (935 | ) | ||||||||||

Total liabilities and owners’ net investment | 183,760 | 182,186 | 48,807 | 31,824 | ||||||||||||

| Predecessor | ||||||||||||||||||||

January 1, 2002 to September 9, 2002 | Year Ended December 31, | |||||||||||||||||||

| 2001 | 2000 | 1999 | 1998 | |||||||||||||||||

| (unaudited) | ||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||

Other Information: | ||||||||||||||||||||

Cash flows: | ||||||||||||||||||||

From operating activities | $ | 2,382 | $ | 4,587 | $ | 112 | $ | (274 | ) | $ | (414 | ) | ||||||||

From investing activities | 12,413 | (5,745 | ) | (116,748 | ) | (11,708 | ) | (30,322 | ) | |||||||||||

From financing activities | (13,176 | ) | 949 | 118,121 | 11,998 | 31,041 | ||||||||||||||

16

Table of Contents

An investment in our common shares involves a number of risks. The risks described below represent the material risks you should carefully consider before making an investment decision. If any of these risks occurs, our business, financial condition, liquidity and results of operations could be materially and adversely affected, in which case the price of our common shares could decline significantly and you could lose all or a part of your investment.

Risks Related to Our Business and Properties

We have recently experienced and expect to continue to experience rapid growth and may not be able to adapt our management and operational systems to respond to the acquisition and integration of additional properties without unanticipated disruption or expense.

We are currently experiencing a period of rapid growth. Since our private placement of common shares in September 2002 and through October 31, 2003, we have acquired 586 properties, excluding properties that we both acquired and disposed of during that period, containing approximately 16.5 million rentable square feet for an aggregate purchase price of approximately $1,725.2 million, including the initial properties we acquired in the formation transactions at the time of our private placement. As a result of the rapid growth of our portfolio, we cannot assure you that we will be able to adapt our management, administrative, accounting and operational systems, or hire and retain sufficient operational staff to integrate these properties into our portfolio and manage any future acquisitions of additional properties without operating disruptions or unanticipated costs. Acquisition of any additional portfolio of properties would generate additional operating expenses that we would be required to pay. As we acquire additional properties, we will be subject to risks associated with managing new properties, including tenant retention and mortgage default. Our failure to successfully integrate any future acquisitions into our portfolio could have a material adverse effect on our results of operations and financial condition and our ability to pay dividends to shareholders at historical levels or at all.

We commenced operations in September 2002 and completed our initial public offering in June 2003, and our management has a very limited history of operating a REIT and little experience operating a public company, and may therefore have difficulty in successfully and profitably operating our business. This limited experience may impede the ability of our management to execute our business plan successfully.

We have recently been organized and have a brief operating history. We will be subject to the risks generally associated with the formation of any new business. In addition, we recently completed the initial public offering of our common shares on June 30, 2003. Our management has limited experience operating a REIT and in managing a publicly owned company. Therefore, you should be especially cautious in drawing conclusions about the ability of our management team to execute our business plan.

If we are unable to acquire additional properties through our relationships with financial institutions, our ability to execute our business plan and our operating results could be adversely affected.

One of our key business strategies is to capitalize on our relationships with financial institutions and, through our agreements with these institutions, to acquire additional bank branches and other properties. Our current agreements with AmSouth Bank, Bank of America, N.A., KeyBank, N.A. and Wachovia Bank, N.A. may be terminated upon 90 days notice by AmSouth Bank, Bank of America and KeyBank and by Wachovia Bank immediately upon written notice. We cannot assure you that these banks will maintain their respective agreements with us. If they do not, we may be unable to acquire desirable bank branches and other properties and execute our business strategy. In addition, these financial institutions may not have any surplus properties under these agreements in the future and, therefore, may have no obligation to sell to us any additional properties. If we are unable to acquire additional properties from financial institutions, we may be unable to execute our business plan, which could have a material adverse effect on our operating results and financial condition and our ability to pay dividends to shareholders at historical levels or at all.

17

Table of Contents

Since our inception, we have derived a majority of our revenues and income from interest income from investments in residential mortgage-backed securities and other investments in marketable investment grade securities. We may be unable to generate comparable revenues or income from our real estate investments in accordance with our business plan.

The majority of our revenues and income since we commenced operations in September 2002 has been generated from interest income from investments in residential mortgage-backed securities and other short-term investments, as opposed to revenues and income generated from our real estate investments in accordance with our business plan. Given our limited operating history, we cannot assure you that we will be able to implement our business plan successfully and derive a comparable level of our revenues or income from our current properties or properties that we may acquire in the future.

If we are unable to acquire additional properties from banks as a result of changes in banking laws and regulations or trends in the banking industry, we may be unable to execute our business plan and our operating results could be adversely affected.

Changes in current laws and regulations governing banks’ ability to invest in real estate beyond that necessary for the transaction of bank business and in current trends in the banking industry also may affect banks’ strategies with respect to the ownership and disposition of real estate. These banks may decide, based on these changes or other reasons, to retain much of their real estate, sell their bank branches to another financial institution, redevelop properties or otherwise determine not to sell properties to us. In addition, if our relationships with financial institutions deteriorate or we are unable to maintain these relationships or develop additional relationships, we may be unable to acquire additional properties. We cannot assure you that we will be able to maintain our current rate of growth by negotiating and acquiring properties acceptable to us in the future. If we are unable to acquire additional properties from financial institutions, we may be unable to execute our business plan, which could have a material adverse effect on our operating results and financial condition and our ability to pay dividends to shareholders at historical levels or at all.

Our agreements with financial institutions require us, with limited exceptions, to purchase properties on an “as is” basis and, therefore, the value of these properties may decline if we discover problems with the properties after we acquire them.

Our agreements with financial institutions require us to purchase properties on an “as is” basis. We may receive limited representations, warranties and indemnities from the sellers in connection with our acquisition of properties. If we discover issues or problems related to the physical condition of a property, zoning, compliance with ordinances and regulations or other significant problems after we acquire the property, we typically have no recourse against the seller and the value of the property may be less than the amount we paid for such property. We may incur substantial costs in repairing a property that we acquire or in ensuring its compliance with governmental regulations. These capital expenditures would reduce cash available for distribution to our shareholders. In addition, we may be unable to rent these properties on terms favorable to us, or at all.

Our use of debt financing and our substantial existing debt obligations may decrease our cash flow and put us at a competitive disadvantage.

We have incurred, and may in the future incur, debt to fund the acquisition of properties. As of September 30, 2003, we had approximately $867.7 million of outstanding indebtedness. On May 27, 2003, we began to repay our outstanding indebtedness under reverse repurchase agreements, a process which we completed in June 2003, and terminated a related hedging arrangement, which resulted in a loss of approximately $10.2 million in the quarter ending June 30, 2003. Increases in interest rates on our existing indebtedness would increase our interest expense, which could harm our cash flow and our ability to pay dividends. If we incur additional indebtedness, debt service requirements would increase accordingly, which could further adversely affect our financial condition and results of operations, cash available for distribution and equity value. In addition, increased leverage could increase the risk of our default on debt obligations, which could ultimately result in loss of properties through foreclosure.

18

Table of Contents