UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-21233

PARADIGM FUNDS

(Exact name of registrant as specified in charter)

Nine Elk Street, Albany, NY 12207-1002

(Address of principal executive offices) (Zip code)

Robert A. Benton

Nine Elk Street, Albany, NY 12207-1002

(Name and address of agent for service)

Registrant's telephone number, including area code: (518) 431-3500

Date of fiscal year end: December 31

Date of reporting period: June 30, 2012

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e -1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Paradigm Funds

Paradigm Value Fund

Paradigm Select Fund

Paradigm Opportunity Fund

Paradigm Micro-Cap Fund

For Investors Seeking Long-Term Capital Appreciation

SEMI-ANNUAL REPORT

June 30, 2012

| Table of Contents | |

| PARADIGM FUNDS | |

| Letter to Shareholders | 2 |

| Sector Allocation | 6 |

| Performance Information | 8 |

| Schedules of Investments | 10 |

| Statements of Assets and Liabilities | 20 |

| Statements of Operations | 20 |

| Statements of Changes in Net Assets | 22 |

| Financial Highlights | 24 |

| NOTES TO FINANCIAL STATEMENTS | 26 |

| DISCLOSURE OF EXPENSES | 31 |

| ADDITIONAL INFORMATION | 33 |

2012 Semi-Annual Report 1

Letter to Shareholders

Dear Fellow Shareholder:

The markets in 2012 followed the pattern of the previous two years: a strong first quarter followed by a challenging second quarter. To our regret, the Paradigm Funds were not immune to this pattern. We trailed the benchmark indices in the second quarter primarily because the markets' focus on macro factors resulted in sharp swings in sentiment that often ignored positive long-term individual company fundamentals of the Funds’ holdings. Our philosophy has always been to invest in what we know. We look for undervalued securities with strong financials, proven management teams, and the ability to weather difficult conditions over the long term. Macro concerns about an overall slowdown in the global economy hit our holdings disproportionately hard in the second quarter, with our holdings demonstrating more sensitivity than we anticipated despite their sound financials. Several stock-specific events also negatively impacted performance in the short term but did not change our long-term assessment of intrinsic value. We have taken advantage of these disconnects by selectively adding to high-conviction positions at what we consider to be even more attractive valuations.

In addition to a difficult market environment, the companies in our small-cap universe (although primarily exposed only to the US) still had to navigate against a backdrop of international turmoil, which continued to roil the equity markets. The two key global concerns were the ongoing Eurozone sovereign debt crisis and reports of an economic slowdown in China. In June alone, noteworthy events included a surprise rate cut in China, the Spanish bank bailout, Greek elections, and the Eurozone ESM announcement.

Moreover, in the US the chief new concern in the second quarter was the deceleration of the US economic recovery. The recovery we had seen gaining traction in 2011 and early 2012 began to falter in the second quarter. Decelerating growth continued throughout the quarter, with the weaker trends of April and May persisting into June. Unemployment levels remained at 8.2%, while the most recent ISM data slipped into contractionary territory, below 50. Nonetheless, we still believe that the prospects for a double-dip recession remain unlikely despite this reduced traction.

On a positive note, we finally began to see improvements in US housing demand, with recent strength reported across pending home sales, home prices, new home sales, and permits. Furthermore, the higher oil prices of the first quarter have receded sharply. As we write this letter, oil prices are down 25% since May, and gasoline prices are at a 6-month low of $3.36, which should alleviate another potential headwind for consumer sentiment and spending.

As we look out to the second half of 2012, however, we believe that the prevailing uncertainty across so many fronts will remain an overhang for the equity markets. As a slowing global economy casts a shadow on companies' growth prospects, there is no doubt that this will weigh on corporate guidance for the second half. Moreover, until US elections are behind us this fall and there is some clarity on fiscal and tax policy, we expect the US economy will remain somewhat stagnant. This policy gridlock has the potential to delay or diminish corporate spending decisions, in terms of hiring, capital expenditures, and strategic growth plans. Adding this to the continued "risk-off" sentiment for equities leads us to believe that the markets will remain challenged for the near-term, barring a deus ex machi-na event such as an announcement of additional Fed stimulus in the form of QE3, or language intimating at least the increased probability of it.

The offset to the above investment concerns is quite clear to us. We believe that valuations are excessively low for many of the names in our universe and that a good deal of the negative sentiment is already priced in. For example, a recent J.P. Morgan report highlighted that equities have a 2.3% average dividend yield, versus a 4.0% yield for the equivalent corporate bonds. This is the narrowest spread since 1976, lending further credibility to the discounted valuation of the equity markets at present.

Given the above cross-currents, we clearly feel the need to be defensive in our posture as we strive to drive performance for our clients. Thus, we continue to seek out those companies that can demonstrate solid growth even in challenging times. Moreover, we are focused on companies that have underlying support to their share prices across a variety of metrics, including free cash flow yields, net cash on the balance sheet, and active share

2012 Semi-Annual Report 2

repurchase programs. This approach does not deviate from our historical emphasis on company fundamentals with a catalyst. Rather, we simply see this as a prudent tactic for the near-term, given unpredictable markets and economies.

We remain believers in equity markets as a compelling source of returns. While it is impossible to predict short-term market conditions, we believe that markets ultimately value companies for their financial strength and growth prospects. We remain confident that taking the longer view will reward our investors over time.

Paradigm Value Fund Portfolio Commentary

The Paradigm Value Fund appreciated 3.20% in the six months ended June 30, 2012, compared to an increase of 8.23% for its benchmark, the Russell 2000 Value Index. Over the past three years on an annualized basis, the Fund appreciated 15.04% versus 17.43% for the benchmark. Over the past five years on an annualized basis, the Fund appreciated 1.45% versus a decline of 1.05% for the benchmark. Since inception (January 1, 2003), the Fund has generated an annualized return of 14.32%, compared to 9.03% for the Russell 2000 Value Index.

The Fund's top three performing companies for the first half of 2012 were Lender Processing Services, Foot Locker, and Regal Entertainment. Lender Processing Services, a provider of mortgage and consumer loan processing services, rallied after a foreclosure settlement was reached between the country's five largest banks and 49 states' attorneys. Foot Locker, a leading retailer of athletic footwear and apparel and a top performer in 2011, continued its operational success and capitalized on the positive athletic footwear cycle. The company delivered 65% earnings growth in 2011 and 37% in the first quarter of 2012. Lastly, Regal Entertainment, the largest theater operator in the United States, has benefited from favorable box office trends in 2012. Regal is a steady cash flow generator and has paid out substantial dividends over the last decade.

The Fund's bottom three performing companies for the first half of 2012 were Brightpoint, Schnitzer Steel, and Deckers Outdoor Corporation. Brightpoint, a provider of supply chain solutions to the wireless industry, experienced an unexpected reduction in demand and lost a meaningful logistics customer. Schnitzer Steel is a recycler of scrap metal. The industry has been hit hard by a combination of a slowdown in overseas purchases of recycled metals and increased competition for scrap in the US. Deckers Outdoor Corporation, a producer and marketer of footwear and accessories including the Ugg and Teva brands, experienced reduced demand for its products which management attributed primarily to the mild winter. Margins were also negatively impacted by elevated sheepskin costs.

Paradigm Select Fund Portfolio Commentary

The Paradigm Select Fund appreciated 3.74% in the six months ended June 30, 2012, compared to an increase of 8.31% for its benchmark, the Russell 2500 Index. Over the past three years on an annualized basis, the Fund appreciated 16.59% versus 19.06% for the benchmark. Over the past five years on an annualized basis, the Fund appreciated 1.79% versus 1.18% for the benchmark. Since inception (January 1, 2005), the Fund has generated an annualized return of 6.72%, compared to 5.05% for the Russell 2500 Index.

The Fund's top three performing companies for the first half of 2012 were Sunoco, Lender Processing Services, and Westlake Chemical. Sunoco, a provider of transportation fuels and new purchase in 2012, announced plans to be acquired by Energy Transfer Partners. Lender Processing Services, a provider of mortgage and consumer loan processing services, rallied after the bank foreclosure settlement was reached between the country's five largest banks and 49 states' attorneys. Westlake Chemical, a fully integrated manufacturer of petrochemicals and polymers, rallied as ethane prices, a key feedstock for the company, dropped in line with natural gas prices.

The Fund's bottom three performing companies for the first half of 2012 were Brightpoint, Deckers Outdoor Corporation, and QLogic. Brightpoint, a provider of supply chain solutions to the wireless industry, experienced an unexpected reduction in demand and lost a meaningful logistics customer. Deckers Outdoor Corporation, a producer and marketer of footwear and accessories including the Ugg and Teva brands, experienced reduced demand for its products due to the mild winter. Margins were also negatively impacted by

2012 Semi-Annual Report 3

elevated sheepskin costs. QLogic, a provider of data storage and network solutions, provided a softer-than-expected outlook for the June quarter due to a pause in the server cycle ahead of new server launches. We believe that the stock is a compelling value at 10x 2012 earnings, with cash on the balance sheet that represents 40% of the market capitalization of the company.

Paradigm Opportunity Fund Portfolio Commentary

The Paradigm Opportunity Fund appreciated 3.71% in the six months ended June 30, 2012, compared to an increase of 8.53% for its benchmark, the Russell 2000 Index. Over the past three years on an annualized basis, the Fund appreciated 15.68% versus 17.80% for the benchmark. Over the past five years on an annualized basis, the Fund appreciated 0.38% versus 0.54% for the benchmark. Since inception (January 1, 2005), the Fund has generated an annualized return of 4.53%, compared to 4.12% for the Russell 2000 Index.

The Fund's top three performing companies for the first half of 2012 were Regal Entertainment Group, Venoco, and Foot Locker. Regal Entertainment, the largest theater operator in the United States, has benefited from favorable box office trends in 2012. Regal is a steady cash flow generator and has paid out substantial dividends over the last decade. Venoco, an oil and gas exploration and production company, rallied after Venoco's Board recommended that shareholders accept the Chairman's offer to take the company private at a substantial premium. Foot Locker, a leading retailer of athletic footwear and apparel and a top performer in 2011 as well, continued to execute operationally and capitalize on the positive athletic footwear cycle. The company delivered 65% earnings growth in 2011 and 37% in the first quarter of 2012.

The Fund's bottom three performing companies for the first half of 2012 were QLogic, Magellan Health Services, and Endo Health Solutions. QLogic, a provider of data storage and network solutions, provided a softer-than-expected outlook for the June quarter due to a pause in the server cycle ahead of new server launches based on the Romley platform. We believe that the stock is a compelling value at 10x 2012 earnings, with cash on the balance sheet that represents 40% of the market capitalization of the company. Endo Health Solutions, a provider of branded and generic pharmaceuticals, medical devices and services, reported mixed first-quarter results due to supply disruptions for two key products. These issues were resolved, and we believe that the company's long-term prospects are favorable. Magellan Health, a provider of specialty managed health solutions, also reported mixed first-quarter results due to higher cost trends in its behavioral health segment and new business start-up costs. We also believe these issues are transitory and that prospects remain favorable for the company.

The Paradigm Micro-Cap Fund

The Paradigm Micro-Cap Fund appreciated 3.86% in the six months ended June 30, 2012, compared to an increase of 13.01% for the Russell Microcap Index. Over the past three years on an annualized basis, the Fund appreciated 12.59% versus 16.71% for the benchmark.

The Fund's top three performing companies for the first half of 2012 were Brown Shoe Co., Obagi Medical, and TGC Industries. Brown Shoe Co., a footwear wholesaler and retailer, returned 41% during the first half. The company posted strong quarterly earnings that significantly exceeded Street expectations. The earnings beat was driven by stronger-than-expected sales growth, which management attributed to continuing strength in the athletic shoe cycle and favorable spring weather. Obagi Medical, a specialty pharmaceutical skin-care company, reported strong sales and profits for the first quarter, and increased its share buyback plan. Moreover, the resolution of its Texas regulatory issues and the presence of an activist investor urging that the company pursue strategic alternatives also resulted in a lift for the shares. TGC Industries is a seismic data acquisition company. Driven by seasonal strength in Canada and an improvement in the seismic data market, the company announced strong revenue and earnings growth for the first quarter and initiated a quarterly dividend.

The Fund's bottom three performers for the first half of 2012 were Brightpoint, Dawson Geophysical, and Dynamics Research Corp. Brightpoint, a provider of supply chain solutions to the wireless industry, experienced an unexpected reduction in demand and lost a

2012 Semi-Annual Report 4

meaningful logistics customer. However, the company has subsequently received a takeover offer at a substantial premium. Dawson Geophysical, a seismic data acquisition company, announced strong first-quarter earnings results and margin improvement, but signaled a more cautious second-quarter outlook reflecting less certain customer demand. We believe that the company's clean balance sheet, strong free cash flow, and low valuation on an EV/EBITDA basis present a strong support for the shares. Dynamics Research, a provider of technology management solutions for government programs, lowered its 2012 guidance following an in-line first quarter, as the deferral of government procurement decisions and program cuts dampened its outlook. The stock now trades at historically low multiples, and we continue to monitor the company's progress in the face of ongoing defense budget uncertainty.

Sincerely,

Candace King Weir | Amelia F. Weir |

2012 Semi-Annual Report 5

Paradigm Funds (Unaudited)

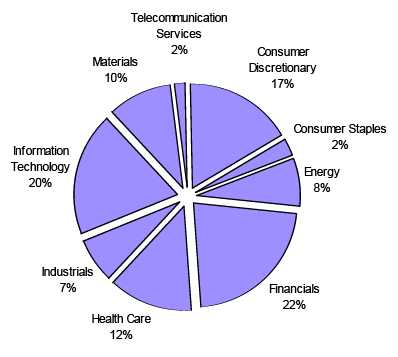

PARADIGM VALUE FUND

Sector Allocation (Unaudited)

(As a Percentage of Equity Securities Held)

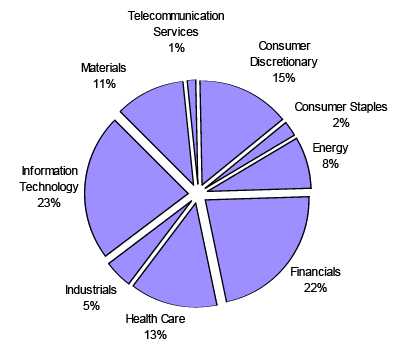

PARADIGM SELECT FUND

Sector Allocation (Unaudited)

(As a Percentage of Equity Securities Held)

2012 Semi-Annual Report 6

Paradigm Funds (Unaudited)

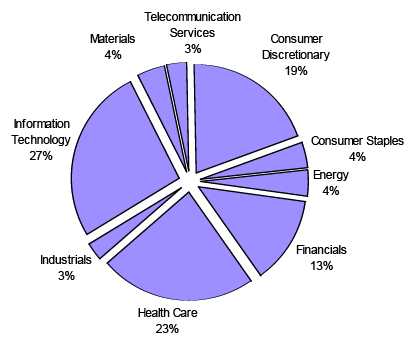

PARADIGM OPPORTUNITY FUND

Sector Allocation (Unaudited)

(As a Percentage of Equity Securities Held)

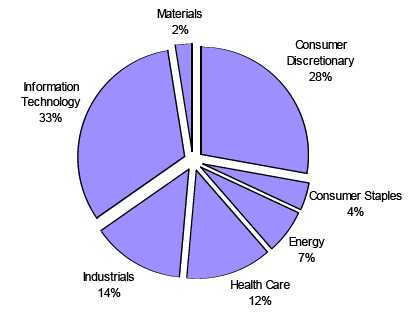

PARADIGM MICRO-CAP FUND

Sector Allocation (Unaudited)

(As a Percentage of Equity Securities Held)

2012 Semi-Annual Report 7

Paradigm Value Fund (Unaudited)

PERFORMANCE INFORMATION

Average Annual Rate of Return (%) for The Periods Ended June 30, 2012.

June 30, 2012 NAV $54.22

| Since | ||||||||

| 1 Year(A) | 3 Years(A) | 5 Years(A) | Inception(A) | |||||

| Paradigm Value Fund | (4.66)% | 15.04% | 1.45% | 14.32% | ||||

| Russell 2000® Value Index(B) | (1.44)% | 17.43% | (1.05)% | 9.03% |

(A) 1 Year, 3 Years, 5 Years and Since Inception returns include change in share prices and in each case includes reinvestment of any dividends and capital gain distributions. The inception date of the Paradigm Value Fund was January 1, 2003.

(B) The Russell 2000® Value Index (whose composition is different from the Fund) is an unmanaged index of small-capitalization stocks with lower price-to-book ratios and lower forecasted growth values than the total population of small-capitalization stocks.

For purposes of the table, it is assumed that all dividends and distributions were reinvested.

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS. INVESTMENT RETURN AND PRINCIPAL VALUE WILL FLUCTUATE SO THAT SHARES, WHEN REDEEMED, MAY BE WORTH MORE OR LESS THAN THEIR ORIGINAL COST. RETURNS DO NOT REFLECT THE DEDUCTION OF TAXES THAT A SHAREHOLDER WOULD PAY ON FUND DISTRIBUTIONS OR THE REDEMPTION OF FUND SHARES. CURRENT PERFORMANCE MAY BE LOWER OR HIGHER THAT THE PERFORMANCE DATA QUOTED. TO OBTAIN PERFORMANCE DATA CURRENT TO THE MOST RECENT MONTH END, PLEASE CALL 1-800-239-0732 OR VISIT OUR WEBSITE AT www.paradigm-funds.com.

Paradigm Select Fund (Unaudited)

PERFORMANCE INFORMATION

Average Annual Rate of Return (%) for The Periods Ended June 30, 2012.

June 30, 2012 NAV $31.36

| Since | ||||||||

| 1 Year(A) | 3 Years(A) | 5 Years(A) | Inception(A) | |||||

| Paradigm Select Fund | (0.90)% | 16.59% | 1.79% | 6.72% | ||||

| Russell 2500® Index(B) | (2.29)% | 19.06% | 1.18% | 5.05% |

(A) 1 Year, 3 Years, 5 Years and Since Inception returns include change in share prices and in each case includes reinvestment of any dividends and capital gain distributions. The inception date of the Paradigm Select Fund was January 1, 2005.

(B) The Russell 2500® Index (whose composition is different from the Fund) measures the performance of the small to mid-cap segment of the U.S. equity universe, commonly referred to as "mid" cap. The Russell 2500 Index is a subset of the Russell 3000® Index. It includes approximately 2,500 of the smallest securities based on a combination of their market cap and current index membership.

For purposes of the table, it is assumed that all dividends and distributions were reinvested.

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS. INVESTMENT RETURN AND PRINCIPAL VALUE WILL FLUCTUATE SO THAT SHARES, WHEN REDEEMED, MAY BE WORTH MORE OR LESS THAN THEIR ORIGINAL COST. RETURNS DO NOT REFLECT THE DEDUCTION OF TAXES THAT A SHAREHOLDER WOULD PAY ON FUND DISTRIBUTIONS OR THE REDEMPTION OF FUND SHARES. CURRENT PERFORMANCE MAY BE LOWER OR HIGHER THAT THE PERFORMANCE DATA QUOTED. TO OBTAIN PERFORMANCE DATA CURRENT TO THE MOST RECENT MONTH END, PLEASE CALL 1-800-239-0732 OR VISIT OUR WEBSITE AT www.paradigm-funds.com.

2012 Semi-Annual Report 8

Paradigm Opportunity Fund (Unaudited)

PERFORMANCE INFORMATION

Average Annual Rate of Return (%) for The Periods Ended June 30, 2012.

June 30, 2012 NAV $25.97

| Since | ||||||||

| 1 Year(A) | 3 Years(A) | 5 Years(A) | Inception(A) | |||||

| Paradigm Opportunity Fund | (3.69)% | 15.68% | 0.38% | 4.53% | ||||

| Russell 2000® Index(B) | (2.08)% | 17.80% | 0.54% | 4.12% |

(A) 1 Year, 3 Years, 5 Years and Since Inception returns include change in share prices and in each case includes reinvestment of any dividends and capital gain distributions. The inception date of the Paradigm Opportunity Fund was January 1, 2005.

(B) The Russell 2000® Index (whose composition is different from the Fund) consists of the smallest 2,000 companies in the Russell 3000 Index (which represents approximately 98% of the investable U.S. equity market). The Index is an unmanaged index generally considered as the premier of small capitalization stocks.

For purposes of the table, it is assumed that all dividends and distributions were reinvested.

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS. INVESTMENT RETURN AND PRINCIPAL VALUE WILL FLUCTUATE SO THAT SHARES, WHEN REDEEMED, MAY BE WORTH MORE OR LESS THAN THEIR ORIGINAL COST. RETURNS DO NOT REFLECT THE DEDUCTION OF TAXES THAT A SHAREHOLDER WOULD PAY ON FUND DISTRIBUTIONS OR THE REDEMPTION OF FUND SHARES. CURRENT PERFORMANCE MAY BE LOWER OR HIGHER THAT THE PERFORMANCE DATA QUOTED. TO OBTAIN PERFORMANCE DATA CURRENT TO THE MOST RECENT MONTH END, PLEASE CALL 1-800-239-0732 OR VISIT OUR WEBSITE AT www.paradigm-funds.com.

Paradigm Micro-Cap Fund (Unaudited)

PERFORMANCE INFORMATION

Average Annual Rate of Return (%) for The Period Ended June 30, 2012.

June 30, 2012 NAV $21.82

| Since | ||||||

| 1 Year(A) | 3 Years(A) | Inception(A) | ||||

| Paradigm Micro-Cap Fund | (2.28)% | 12.59% | 2.20% | |||

| Russell Microcap® Index(B) | (0.54)% | 16.71% | 0.32% | |||

| S&P 500® Index(C) | 5.45% | 16.40% | 0.55% |

(A) 1 Year, 3 Years and Since Inception returns include change in share prices and in each case includes reinvestment of any dividends and capital gain distributions. The inception date of the Paradigm Micro-Cap Fund was January 1, 2008. Effective December 27, 2011, the name of the Paradigm Intrinsic Value Fund was changed to the Paradigm Micro-Cap Fund.

(B) The Russell Microcap® Index measures the performance of the microcap segment of the U.S. equity market. Microcap stocks make up less than 3% of the U.S. equity market (by market cap) and consist of the smallest 1,000 securities in the small-cap Russell 2000® Index, plus the next smallest eligible securities by market cap. The Russell Microcap is completely reconstituted annually to ensure larger stocks do not distort performance and characteristics of the true microcap opportunity set. Effective December 27, 2011 the Fund changed its investment strategy. Under normal circumstances, the Micro-Cap Fund invests at least 80% of its net assets in common stocks of U.S. micro-cap companies. Therefore, the primary comparative index was changed from the S&P 500® Index to the Russell Microcap® Index.

(C)The S&P 500® Index (whose composition is different from the Fund) is an unmanaged index which measures the performance of 500 companies chosen by Standard & Poor’s to represent the large cap U.S. equity market. Effective December 27, 2011 the S&P 500® Index became the secondary comparison index. Previously the Russell 3000® Index was the secondary comparison index.

For purposes of the table, it is assumed that all dividends and distributions were reinvested.

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS. INVESTMENT RETURN AND PRINCIPAL VALUE WILL FLUCTUATE SO THAT SHARES, WHEN REDEEMED, MAY BE WORTH MORE OR LESS THAN THEIR ORIGINAL COST. RETURNS DO NOT REFLECT THE DEDUCTION OF TAXES THAT A SHAREHOLDER WOULD PAY ON FUND DISTRIBUTIONS OR THE REDEMPTION OF FUND SHARES. CURRENT PERFORMANCE MAY BE LOWER OR HIGHER THAT THE PERFORMANCE DATA QUOTED. TO OBTAIN PERFORMANCE DATA CURRENT TO THE MOST RECENT MONTH END, PLEASE CALL 1-800-239-0732 OR VISIT OUR WEBSITE AT www.paradigm-funds.com.

2012 Semi-Annual Report 9

| Paradigm Value Fund | |||||

| Schedule of Investments | |||||

| June 30, 2012 (Unaudited) | |||||

| Shares | Fair Value | % of Net Assets | |||

| COMMON STOCKS | |||||

| Agriculture Production - Crops | |||||

| 343,815 | Dole Food Company Inc. * | $ | 3,018,696 | 1.15 | % |

| Agriculture Production - Livestock & Animal Specialties | |||||

| 77,000 | Cal-Maine Foods, Inc. | 3,010,700 | 1.15 | % | |

| Apparel & Other Finished Products of Fabrics & Similar Material | |||||

| 146,200 | True Religion Apparel, Inc. * | 4,236,876 | 1.62 | % | |

| Chemical & Allied Products | |||||

| 62,548 | Innospec Inc. * | 1,852,046 | |||

| 236,000 | Olin Corp. | 4,930,040 | |||

| 6,782,086 | 2.59 | % | |||

| Computer Communications Equipment | |||||

| 375,525 | Emulex Corporation * | 2,703,780 | |||

| 456,000 | QLogic Corp. * | 6,242,640 | |||

| 8,946,420 | 3.41 | % | |||

| Construction - Special Trade Contractors | |||||

| 292,402 | Matrix Service Co. * | 3,312,915 | 1.26 | % | |

| Crude Petroleum & Natural Gas | |||||

| 342,044 | McMoRan Exploration Co. * | 4,333,697 | |||

| 589,775 | PetroQuest Energy Inc. * | 2,948,875 | |||

| 455,300 | Resolute Energy Corporation * | 4,357,221 | |||

| 11,639,793 | 4.44 | % | |||

| Drilling Oil & Gas Wells | |||||

| 99,100 | Atwood Oceanics Inc. * | 3,749,944 | 1.43 | % | |

| Electrical Work | |||||

| 146,100 | EMCOR Group Inc. | 4,064,502 | 1.55 | % | |

| Electronic Components & Accessories | |||||

| 653,100 | Vishay Intertechnology Inc.* | 6,158,733 | 2.35 | % | |

| Fabricated Plater Work (Boiler Shops) | |||||

| 197,938 | Global Power Equipment Group Inc. * | 4,322,966 | 1.65 | % | |

| Fire, Marine & Casualty Insurance | |||||

| 155,500 | Aspen Insurance Holdings Limited (Bermuda) | 4,493,950 | |||

| 198,500 | Montpelier Re Holdings Ltd. (Bermuda) | 4,226,065 | |||

| 8,720,015 | 3.33 | % | |||

| Footwear (No Rubber) | |||||

| 172,700 | Iconix Brand Group, Inc. * | 3,017,069 | 1.15 | % | |

| In Vitro & In Vivo Diagnostic Substances | |||||

| 250,200 | Myriad Genetics, Inc. * | 5,947,254 | 2.27 | % | |

| Industrial Inorganic Chemicals | |||||

| 10,275 | Tronox Inc. * | 1,240,398 | 0.47 | % | |

| Industrial Organic Chemicals | |||||

| 146,477 | Sensient Technologies Corp. | 5,380,100 | 2.05 | % | |

| Laboratory Analytical Instruments | |||||

| 127,875 | PerkinElmer Inc. | 3,299,175 | 1.26 | % | |

| Life Insurance | |||||

| 23,425 | National Western Life Insurance Co. Class A | 3,324,476 | 1.27 | % | |

| Metal Mining | |||||

| 98,100 | Richmont Mines Inc. * | 454,203 | 0.17 | % | |

| Motor Vehicle Parts & Accessories | |||||

| 150,700 | Superior Industries International Inc. | 2,466,959 | 0.94 | % | |

| Oil & Gas Field Services, NEC | |||||

| 71,600 | C&J Energy Services, Inc. * | 1,324,600 | 0.51 | % | |

| Orthopedic, Prosthetic & Surgical Appliances & Supplies | |||||

| 445,826 | Symmetry Medical, Inc. * | 3,825,187 | 1.46 | % | |

| * Non-Income Producing Securities. The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 10

| Paradigm Value Fund | |||||

| Schedule of Investments | |||||

| June 30, 2012 (Unaudited) | |||||

| Shares | Fair Value | % of Net Assets | |||

| COMMON STOCKS | |||||

| Pharmaceutical Preparations | |||||

| 179,300 | Endo Pharmaceuticals Holdings Inc. * | $ | 5,554,714 | 2.12 | % |

| Plastic Materials, Synth Resin/Rubber, Cellulos (No Glass) | |||||

| 314,800 | Chemtura Corp. * | 4,564,600 | 1.74 | % | |

| Retail - Apparel & Accessory Stores | |||||

| 223,400 | Express Inc. * | 4,059,178 | |||

| 92,475 | The Men's Wearhouse, Inc. | 2,602,247 | |||

| 6,661,425 | 2.54 | % | |||

| Retail - Family Clothing Stores | |||||

| 154,725 | American Eagle Outfitters, Inc. | 3,052,724 | 1.17 | % | |

| Retail - Miscellaneous Retail | |||||

| 175,875 | EZCORP Inc. Class A * | 4,126,027 | 1.57 | % | |

| Retail - Retail Stores, NEC | |||||

| 74,150 | IAC/InterActiveCorp. | 3,381,240 | 1.29 | % | |

| Retail - Shoe Stores | |||||

| 93,500 | Foot Locker, Inc. | 2,859,230 | 1.09 | % | |

| Retail - Variety Stores | |||||

| 86,400 | Big Lots Inc. * | 3,524,256 | 1.35 | % | |

| Rubber & Plastics Footwear | |||||

| 139,025 | Deckers Outdoor Corporation * | 6,118,490 | 2.34 | % | |

| Savings Institution, Federally Chartered | |||||

| 227,400 | Capitol Federal Financial | 2,701,512 | |||

| 285,012 | SI Financial Group, Inc. | 3,277,638 | |||

| 318,000 | United Financial Bancorp | 4,572,840 | |||

| 258,200 | Viewpoint Financial Group | 4,038,248 | |||

| 358,500 | Westfield Financial Inc. | 2,617,050 | |||

| 17,207,288 | 6.57 | % | |||

| Secondary Smelting & Refining of Nonferrous Metals | |||||

| 555,000 | Metalico Inc. * | 1,221,000 | 0.47 | % | |

| Security Brokers, Dealers & Flotation Companies | |||||

| 506,425 | Knight Capital Group Inc. Class A * | 6,046,715 | 2.31 | % | |

| Semiconductors & Related Devices | |||||

| 444,125 | Kulicke & Soffa Industries Inc. * (Singapore) | 3,961,595 | |||

| 165,200 | Microsemi Corporation * | 3,054,548 | |||

| 481,550 | TriQuint Semiconductor, Inc. * | 2,648,525 | |||

| 9,664,668 | 3.69 | % | |||

| Services - Business Services | |||||

| 25,700 | Lender Processing Services, Inc. | 649,696 | |||

| 514,677 | Premiere Global Services Inc. * | 4,318,140 | |||

| 4,967,836 | 1.90 | % | |||

| Services - Computer Integrated Systems Design | |||||

| 552,875 | Convergys Corp. * | 8,165,964 | 3.12 | % | |

| Services - Hospitals | |||||

| 182,750 | Magellan Health Services Inc. * | 8,284,057 | |||

| 68,000 | MEDNAX, Inc. * | 4,660,720 | |||

| 12,944,777 | 4.94 | % | |||

| Services - Motion Picture Theaters | |||||

| 586,055 | Regal Entertainment Group Class A | 8,064,117 | 3.08 | % | |

| Services - Prepackaged Software | |||||

| 515,300 | Actuate Corporation * | 3,571,029 | |||

| 318,025 | Compuware Corp. * | 2,957,633 | |||

| 6,528,662 | 2.49 | % | |||

| Special Industry Machinery | |||||

| 61,962 | Cymer, Inc. * | 3,652,660 | 1.39 | % | |

| * Non-Income Producing Securities. The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 11

| Paradigm Value Fund | |||||

| Schedule of Investments | |||||

| June 30, 2012 (Unaudited) | |||||

| Shares | Fair Value | % of Net Assets | |||

| COMMON STOCKS | |||||

| Sporting & Athletic Goods, NEC | |||||

| 478,100 | Callaway Golf Co. | $ | 2,825,571 | 1.08 | % |

| Telegraph & Other Message Communications | |||||

| 97,450 | j2 Global, Inc. | 2,574,629 | 0.98 | % | |

| Telephone & Telegraph Apparatus | |||||

| 196,500 | Comverse Technology, Inc. * | 1,141,665 | 0.44 | % | |

| Transportation Services | |||||

| 103,700 | GATX Corp. | 3,992,450 | 1.52 | % | |

| Wholesale - Chemicals & Allied Products | |||||

| 93,831 | Innophos Holdings Inc. | 5,297,698 | 2.02 | % | |

| Wholesale - Machinery, Equipment & Supplies | |||||

| 126,192 | Applied Industrial Technologies | 4,650,175 | 1.77 | % | |

| Wholesale - Miscellaneous Durable Goods | |||||

| 63,857 | Schnitzer Steel Industries, Inc. Class A | 1,789,273 | 0.68 | % | |

| Total for Common Stocks (Cost $211,463,662) | $ | 238,820,921 | 91.14 | % | |

| REAL ESTATE INVESTMENT TRUSTS | |||||

| 933,400 | Anworth Mortgage Asset Corp. | 6,580,470 | |||

| 342,400 | MFA Financial, Inc. | 2,701,536 | |||

| 104,800 | Mid-America Apartment Communities Inc. | 7,151,552 | |||

| Total for Real Estate Investment Trusts (Cost $14,183,601) | 16,433,558 | 6.27 | % | ||

| MONEY MARKET FUNDS | |||||

| 5,342,948 | SEI Daily Income Treasury Government CL B 0.02% ** | 5,342,948 | 2.04 | % | |

| (Cost $5,342,948) | |||||

| Total Investment Securities | 260,597,427 | 99.45 | % | ||

| (Cost $230,990,211) | |||||

| Other Assets In Excess of Liabilities | 1,428,898 | 0.55 | % | ||

| Net Assets | $ | 262,026,325 | 100.00 | % | |

| * Non-Income Producing Securities. ** Variable Rate Security; the rate shown was the rate at June 30, 2012. The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 12

| Paradigm Select Fund | |||||

| Schedule of Investments | |||||

| June 30, 2012 (Unaudited) | |||||

| Shares | Fair Value | % of Net Assets | |||

| COMMON STOCKS | |||||

| Agriculture Production - Crops | |||||

| 12,452 | Dole Food Company Inc. * | $ | 109,328 | 0.98 | % |

| Agriculture Production - Livestock & Animal Specialties | |||||

| 2,800 | Cal-Maine Foods, Inc. | 109,480 | 0.99 | % | |

| Biological Products, (No Diagnostic Substances) | |||||

| 4,900 | Life Technologies Corporation * | 220,451 | 1.99 | % | |

| Chemical & Allied Products | |||||

| 2,000 | Innospec Inc. * | 59,220 | |||

| 7,800 | Olin Corp. | 162,942 | |||

| 222,162 | 2.00 | % | |||

| Computer & Office Equipment | |||||

| 5,700 | Lexmark International, Inc. | 151,506 | 1.36 | % | |

| Computer Communications Equipment | |||||

| 15,000 | Emulex Corporation * | 108,000 | |||

| 19,900 | QLogic Corp. * | 272,431 | |||

| 380,431 | 3.43 | % | |||

| Construction - Special Trade Contractors | |||||

| 10,700 | Matrix Service Co. * | 121,231 | 1.09 | % | |

| Crude Petroleum & Natural Gas | |||||

| 6,100 | Denbury Resources Inc. * | 92,171 | |||

| 22,200 | PetroQuest Energy Inc. * | 111,000 | |||

| 1,500 | Plains Exploration & Production Company * | 52,770 | |||

| 4,700 | Resolute Energy Corporation * | 44,979 | |||

| 2,700 | Whiting Petroleum Corp. * | 111,024 | |||

| 411,944 | 3.71 | % | |||

| Electrical Work | |||||

| 5,700 | EMCOR Group Inc. | 158,574 | 1.43 | % | |

| Electronic Components & Accessories | |||||

| 22,760 | Vishay Intertechnology Inc. * | 214,627 | 1.93 | % | |

| Fire, Marine & Casualty Insurance | |||||

| 509 | Alleghany Inc. * | 172,933 | |||

| 4,200 | American Financial Group Inc. | 164,766 | |||

| 6,000 | Aspen Insurance Holdings Limited (Bermuda) | 173,400 | |||

| 100 | Markel Corp. * | 44,170 | |||

| 9,300 | Montpelier Re Holdings Ltd. (Bermuda) | 197,997 | |||

| 753,266 | 6.79 | % | |||

| Footwear (No Rubber) | |||||

| 7,900 | Iconix Brand Group, Inc. * | 138,013 | 1.24 | % | |

| In Vitro & In Vivo Diagnostic Substances | |||||

| 11,200 | Myriad Genetics, Inc. * | 266,224 | 2.40 | % | |

| Industrial Inorganic Chemicals | |||||

| 450 | Tronox Inc. * | 54,324 | 0.49 | % | |

| Industrial Organic Chemicals | |||||

| 5,850 | Sensient Technologies Corporation | 214,871 | |||

| 3,600 | Westlake Chemical Corp. | 188,136 | |||

| 403,007 | 3.63 | % | |||

| Iron & Steel Foundries | |||||

| 800 | Precision Castparts Corp. | 131,592 | 1.19 | % | |

| Laboratory Analytical Instruments | |||||

| 5,100 | PerkinElmer Inc. | 131,580 | 1.19 | % | |

| Men's & Boy's Furnishings, Work Clothing & Allied Garments | |||||

| 2,680 | PVH Corp. | 208,477 | 1.88 | % | |

| * Non-Income Producing Securities. The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 13

| Paradigm Select Fund | |||||

| Schedule of Investments | |||||

| June 30, 2012 (Unaudited) | |||||

| Shares | Fair Value | % of Net Assets | |||

| COMMON STOCKS | |||||

| Mineral Royalty Traders | |||||

| 1,500 | Royal Gold, Inc. | $ | 117,600 | 1.06 | % |

| National Commercial Banks | |||||

| 17,800 | First Niagara Financial Group, Inc. | 136,170 | 1.23 | % | |

| Petroleum Refining | |||||

| 6,000 | Sunoco, Inc. | 285,000 | 2.57 | % | |

| Pharmaceutical Preparations | |||||

| 7,175 | Endo Pharmaceuticals Holdings Inc. * | 222,282 | 2.00 | % | |

| Plastic Materials, Synth Resin/Rubber, Cellulos (No Glass) | |||||

| 11,400 | Chemtura Corp. * | 165,300 | 1.49 | % | |

| Plastics Products | |||||

| 3,200 | AptarGroup Inc. | 163,360 | 1.47 | % | |

| Retail - Apparel & Accessory Stores | |||||

| 9,000 | Express Inc. * | 163,530 | |||

| 3,700 | The Men's Wearhouse, Inc. | 104,118 | |||

| 267,648 | 2.41 | % | |||

| Retail - Family Clothing Stores | |||||

| 6,300 | American Eagle Outfitters, Inc. | 124,299 | 1.12 | % | |

| Retail - Miscellaneous Retail | |||||

| 7,100 | EZCORP Inc. Class A * | 166,566 | 1.50 | % | |

| Retail - Retail Stores, NEC | |||||

| 2,900 | IAC/InterActiveCorp. | 132,240 | 1.19 | % | |

| Retail - Shoe Stores | |||||

| 3,700 | Foot Locker, Inc. | 113,146 | 1.02 | % | |

| Retail - Variety Stores | |||||

| 2,700 | Big Lots Inc. * | 110,133 | 0.99 | % | |

| Rubber & Plastics Footwear | |||||

| 6,125 | Deckers Outdoor Corporation * | 269,561 | 2.43 | % | |

| Savings Institution, Federally Chartered | |||||

| 14,000 | Capitol Federal Financial | 166,320 | 1.50 | % | |

| Security Brokers, Dealers & Flotation Companies | |||||

| 24,600 | Knight Capital Group Inc. Class A * | 293,724 | 2.65 | % | |

| Semiconductors & Related Devices | |||||

| 17,700 | Kulicke & Soffa Industries Inc. * (Singapore) | 157,884 | |||

| 9,600 | Marvell Technology Group Ltd. * (Bermuda) | 108,288 | |||

| 6,700 | Microsemi Corporation * | 123,883 | |||

| 19,300 | TriQuint Semiconductor, Inc. * | 106,150 | |||

| 496,205 | 4.47 | % | |||

| Services - Business Services | |||||

| 1,089 | Lender Processing Services, Inc. | 27,530 | |||

| 16,170 | Premiere Global Services Inc. * | 135,666 | |||

| 163,196 | 1.47 | % | |||

| Services - Computer Integrated Systems Design | |||||

| 22,200 | Convergys Corp. * | 327,894 | 2.95 | % | |

| Services - Hospitals | |||||

| 7,500 | Magellan Health Services Inc. * | 339,975 | |||

| 2,800 | MEDNAX, Inc. * | 191,912 | |||

| 531,887 | 4.79 | % | |||

| Services - Management Consulting Services | |||||

| 2,200 | FTI Consulting, Inc. * | 63,250 | 0.57 | % | |

| Services - Motion Picture Theaters | |||||

| 21,600 | Regal Entertainment Group Class A | 297,216 | 2.68 | % | |

| * Non-Income Producing Securities. The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 14

| Paradigm Select Fund | |||||

| Schedule of Investments | |||||

| June 30, 2012 (Unaudited) | |||||

| Shares | Fair Value | % of Net Assets | |||

| COMMON STOCKS | |||||

| Services - Prepackaged Software | |||||

| 13,000 | Compuware Corp. * | $ | 120,900 | 1.09 | % |

| Special Industry Machinery | |||||

| 2,700 | Cymer, Inc. * | 159,165 | 1.43 | % | |

| Telegraph & Other Message Communications | |||||

| 3,900 | j2 Global, Inc. | 103,038 | 0.93 | % | |

| Telephone & Telegraph Apparatus | |||||

| 9,000 | Comverse Technology, Inc. * | 52,290 | 0.47 | % | |

| Wholesale - Electronic Parts & Equipment, NEC | |||||

| 7,800 | Avnet, Inc. * | 240,708 | 2.17 | % | |

| Wholesale - Machinery, Equipment & Supplies | |||||

| 4,600 | Applied Industrial Technologies | 169,510 | 1.53 | % | |

| Wholesale - Miscellaneous Durable Goods | |||||

| 2,300 | Schnitzer Steel Industries, Inc. Class A | 64,446 | 0.57 | % | |

| Total for Common Stocks (Cost $8,994,264) | $ | 9,709,271 | 87.47 | % | |

| REAL ESTATE INVESTMENT TRUSTS | |||||

| 40,300 | Anworth Mortgage Asset Corp. | 284,115 | |||

| 32,300 | MFA Financial, Inc. | 254,847 | |||

| 4,200 | Mid-America Apartment Communities Inc. | 286,608 | |||

| Total for Real Estate Investment Trusts (Cost $767,062) | 825,570 | 7.44 | % | ||

| MONEY MARKET FUNDS | |||||

| 524,367 | SEI Daily Income Treasury Government CL B 0.02% ** | 524,367 | 4.72 | % | |

| (Cost $524,367) | |||||

| Total Investment Securities | 11,059,208 | 99.63 | % | ||

| (Cost $10,285,693) | |||||

| Other Assets In Excess of Liabilities | 40,872 | 0.37 | % | ||

| Net Assets | $ | 11,100,080 | 100.00 | % | |

| * Non-Income Producing Securities. ** Variable Rate Security; the rate shown was the rate at June 30, 2012. The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 15

| Paradigm Opportunity Fund | |||||

| Schedule of Investments | |||||

| June 30, 2012 (Unaudited) | |||||

| Shares | Fair Value | % of Net Assets | |||

| COMMON STOCKS | |||||

| Agriculture Production - Crops | |||||

| 10,357 | Dole Food Company Inc. * | $ | 90,934 | 1.87 | % |

| Agriculture Production - Livestock & Animal Specialties | |||||

| 2,400 | Cal-Maine Foods, Inc. | �� | 93,840 | 1.93 | % |

| Biological Products, (No Diagnostic Substances) | |||||

| 3,500 | Life Technologies Corporation * | 157,465 | 3.24 | % | |

| Computer Communications Equipment | |||||

| 13,500 | Emulex Corporation * | 97,200 | |||

| 15,800 | QLogic Corp. * | 216,302 | |||

| 313,502 | 6.45 | % | |||

| Construction - Special Trade Contractors | |||||

| 9,300 | Matrix Service Co. * | 105,369 | 2.17 | % | |

| Crude Petroleum & Natural Gas | |||||

| 18,700 | PetroQuest Energy Inc. * | 93,500 | 1.92 | % | |

| Electrical Work | |||||

| 5,000 | EMCOR Group Inc. | 139,100 | 2.86 | % | |

| Industrial Organic Chemicals | |||||

| 5,250 | Sensient Technologies Corporation | 192,833 | 3.97 | % | |

| Laboratory Analytical Instruments | |||||

| 4,600 | PerkinElmer Inc. | 118,680 | 2.44 | % | |

| Orthopedic, Prosthetic & Surgical Appliances & Supplies | |||||

| 14,400 | Symmetry Medical, Inc. * | 123,552 | 2.54 | % | |

| Pharmaceutical Preparations | |||||

| 6,400 | Endo Pharmaceuticals Holdings Inc. * | 198,272 | 4.08 | % | |

| Retail - Apparel & Accessory Stores | |||||

| 8,000 | Express Inc. * | 145,360 | |||

| 3,300 | The Men's Wearhouse, Inc. | 92,862 | |||

| 238,222 | 4.90 | % | |||

| Retail - Family Clothing Stores | |||||

| 5,500 | American Eagle Outfitters, Inc. | 108,515 | 2.23 | % | |

| Retail - Miscellaneous Retail | |||||

| 6,300 | EZCORP Inc. Class A * | 147,798 | 3.04 | % | |

| Retail - Retail Stores, NEC | |||||

| 2,600 | IAC/InterActiveCorp. | 118,560 | 2.44 | % | |

| Retail - Shoe Stores | |||||

| 3,300 | Foot Locker, Inc. | 100,914 | 2.08 | % | |

| Retail - Variety Stores | |||||

| 2,400 | Big Lots Inc. * | 97,896 | 2.01 | % | |

| Security Brokers, Dealers & Flotation Companies | |||||

| 17,200 | Knight Capital Group Inc. Class A * | 205,368 | 4.22 | % | |

| Semiconductors & Related Devices | |||||

| 15,800 | Kulicke & Soffa Industries Inc. * (Singapore) | 140,936 | |||

| 5,900 | Microsemi Corporation * | 109,091 | |||

| 16,500 | TriQuint Semiconductor, Inc. * | 90,750 | |||

| 340,777 | 7.01 | % | |||

| Services - Business Services | |||||

| 16,700 | Premiere Global Services Inc. * | 140,113 | 2.88 | % | |

| Services - Computer Integrated Systems Design | |||||

| 19,800 | Convergys Corp. * | 292,446 | 6.02 | % | |

| * Non-Income Producing Securities. The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 16

| Paradigm Opportunity Fund | |||||

| Schedule of Investments | |||||

| June 30, 2012 (Unaudited) | |||||

| Shares | Fair Value | % of Net Assets | |||

| COMMON STOCKS | |||||

| Services - Hospitals | |||||

| 6,500 | Magellan Health Services Inc. * | $ | 294,645 | ||

| 2,700 | MEDNAX, Inc. * | 185,058 | |||

| 479,703 | 9.87 | % | |||

| Services - Motion Picture Theaters | |||||

| 19,700 | Regal Entertainment Group Class A | 271,072 | 5.58 | % | |

| Service - Prepackaged Software | |||||

| 11,400 | Compuware Corp. * | 106,020 | 2.18 | % | |

| Sporting & Athletic Goods, NEC | |||||

| 17,100 | Callaway Golf Co. | 101,061 | 2.08 | % | |

| Telegraph & Other Message Communications | |||||

| 3,400 | j2 Global, Inc. | 89,828 | 1.84 | % | |

| Total for Common Stocks (Cost $3,807,470) | $ | 4,465,340 | 91.85 | % | |

| REAL ESTATE INVESTMENT TRUSTS | |||||

| 3,600 | Mid-America Apartment Communities Inc. | 245,664 | |||

| Total for Real Estate Investment Trusts (Cost $164,861) | 245,664 | 5.05 | % | ||

| MONEY MARKET FUNDS | |||||

| 144,478 | SEI Daily Income Treasury Government CL B 0.02% ** | 144,478 | 2.98 | % | |

| (Cost $144,478) | |||||

| Total Investment Securities | 4,855,482 | 99.88 | % | ||

| (Cost $4,116,809) | |||||

| Other Assets In Excess of Liabilities | 6,026 | 0.12 | % | ||

| Net Assets | $ | 4,861,508 | 100.00 | % | |

| * Non-Income Producing Securities. ** Variable Rate Security; the rate shown was the rate at June 30, 2012. The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 17

| Paradigm Micro-Cap Fund | |||||

| Schedule of Investments | |||||

| June 30, 2012 (Unaudited) | |||||

| Shares | Fair Value | % of Net Assets | |||

| COMMON STOCKS | |||||

| Commercial Printing | |||||

| 10,000 | Consolidated Graphics, Inc. | $ | 290,500 | ||

| 40,000 | Quad/Graphics, Inc. | 575,200 | |||

| 865,700 | 5.34 | % | |||

| Commodity Contracts Brokers & Dealers | |||||

| 20,900 | MFC Industrial Ltd. (Canada) | 140,866 | 0.87 | % | |

| Communications Services, NEC | |||||

| 70,000 | Kratos Defense & Security Solutions, Inc. * | 408,800 | 2.52 | % | |

| Computer Peripheral Equipment, NEC | |||||

| 90,000 | RadiSys Corporation * | 565,200 | 3.48 | % | |

| Electromedical & Electrotherapeutic Apparatus | |||||

| 30,000 | Solta Medical, Inc. * | 87,900 | |||

| 40,000 | Syneron Medical Ltd. * (Israel) | 415,200 | |||

| 503,100 | 3.10 | % | |||

| Footwear, (No Rubber) | |||||

| 20,000 | Brown Shoe Co. Inc. | 258,200 | 1.59 | % | |

| Industrial Instruments for Measurement, Display and Control | |||||

| 60,000 | Rudolph Technologies Inc. * | 523,200 | 3.22 | % | |

| Instruments for Measuring & Testing of Electricity & Electric Signals | |||||

| 30,000 | Cohu, Inc. | 304,800 | 1.88 | % | |

| Millwood, Veneer, Plywood, & Structural Wood Members | |||||

| 10,100 | American Woodmark Corporation | 172,710 | 1.06 | % | |

| Miscellaneous Electrical Machinery, Equipment & Supplies | |||||

| 152,000 | Exide Technologies * | 510,720 | 3.15 | % | |

| Miscellaneous Furniture & Fixtures | |||||

| 20,000 | Knoll, Inc. | 268,400 | 1.65 | % | |

| Oil & Gas Field Exploration Services | |||||

| 20,000 | Dawson Geophysical Company * | 476,400 | |||

| 57,750 | TGC Industries Inc. * | 560,752 | |||

| 1,037,152 | 6.39 | % | |||

| Orthopedic, Prosthetic & Surgical Appliances & Supplies | |||||

| 17,467 | Exactech Inc. * | 292,922 | |||

| 100,000 | RTI Biologics, Inc. * | 376,000 | |||

| 668,922 | 4.12 | % | |||

| Paper Mills | |||||

| 20,000 | KapStone Paper and Packaging Corporation * | 317,000 | 1.95 | % | |

| Pharmaceutical Preparations | |||||

| 40,000 | Nature's Sunshine Products * | 604,000 | |||

| 30,000 | Obagi Medical Products, Inc. * | 458,100 | |||

| 1,062,100 | 6.55 | % | |||

| Printed Circuit Boards | |||||

| 60,000 | TTM Technologies, Inc. * | 562,800 | 3.47 | % | |

| Radio & Tv Broadcasting & Communications Equipment | |||||

| 100,000 | Harmonic Inc. | 426,000 | 2.63 | % | |

| Retail - Auto Dealers & Gasoline Stations | |||||

| 40,000 | West Marine Inc. * | 470,000 | 2.90 | % | |

| Retail - Catalog & Mail-Order Houses | |||||

| 17,000 | Insight Enterprises Inc. * | 286,110 | |||

| 4,750 | PC Connection, Inc. * | 50,445 | |||

| 336,555 | 2.07 | % | |||

| Retail - Family Clothing Stores | |||||

| 39,937 | Stein Mart Inc. * | 317,499 | 1.96 | % | |

| * Non-Income Producing Securities. The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 18

| Paradigm Micro-Cap Fund | |||||

| Schedule of Investments | |||||

| June 30, 2012 (Unaudited) | |||||

| Shares | Fair Value | % of Net Assets | |||

| COMMON STOCKS | |||||

| Retail - Furniture Stores | |||||

| 44,000 | Haverty Furniture Companies Inc. | $ | 491,480 | 3.03 | % |

| Retail - Hobby, Toy & Game Shops | |||||

| 60,000 | Build-A-Bear Workshop, Inc. * | 286,800 | 1.77 | % | |

| Retail - Retail Stores, NEC | |||||

| 25,000 | Kirkland's Inc. * | 281,250 | 1.73 | % | |

| Retail - Shoe Stores | |||||

| 25,000 | Finish Line Inc. | 522,750 | 3.22 | % | |

| Retail - Women's Clothing Stores | |||||

| 300,000 | Coldwater Creek Inc. * | 165,000 | |||

| 70,000 | Wet Seal Inc. Class A * | 220,500 | |||

| 385,500 | 2.38 | % | |||

| Semiconductors & Related Devices | |||||

| 20,000 | Finisar Corporation | 299,200 | |||

| 80,000 | Photronics, Inc. * | 488,000 | |||

| 787,200 | 4.85 | % | |||

| Services - Computer Integrated Systems Design | |||||

| 30,000 | Dynamics Research Corp. * | 174,300 | 1.07 | % | |

| Services - Personal Services | |||||

| 10,000 | Steiner Leisure Limited * (Bahamas) | 464,100 | 2.86 | % | |

| Special Industry Machinery (No Metalworking Machinery) | |||||

| 15,000 | Kadant Inc. * | 351,750 | 2.17 | % | |

| Surgical & Medical Instruments | |||||

| 100,000 | Alphatec Holdings, Inc. * | 184,000 | 1.13 | % | |

| Telephone & Telegraph Apparatus | |||||

| 30,000 | Oplink Communications, Inc. * | 405,900 | 2.50 | % | |

| Wholesale - Electronic Parts & Equipment, NEC | |||||

| 80,000 | Brightpoint, Inc. * | 432,800 | |||

| 35,000 | Richardson Electronics Ltd. | 431,550 | |||

| 864,350 | 5.33 | % | |||

| Women's, Misses', and Juniors Outerwear | |||||

| 40,000 | bebe stores, inc. | 234,800 | 1.45 | % | |

| Total for Common Stocks (Cost $15,462,250) | $ | 15,153,904 | 93.39 | % | |

| MONEY MARKET FUNDS | |||||

| 572,486 | SEI Daily Income Treasury Government CL B 0.02% ** | 572,486 | 3.53 | % | |

| (Cost $572,486) | |||||

| Total Investment Securities | 15,726,390 | 96.92 | % | ||

| (Cost $16,034,736) | |||||

| Other Assets In Excess of Liabilities | 499,898 | 3.08 | % | ||

| Net Assets | $ | 16,226,288 | 100.00 | % | |

| * Non-Income Producing Securities. ** Variable Rate Security; the rate shown was the rate at June 30, 2012. The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 19

| Paradigm Funds | ||||||

| Statements of Assets and Liabilities (Unaudited) | Value | Select | ||||

| June 30, 2012 | Fund | Fund | ||||

| Assets: | ||||||

| Investment Securities at Fair Value* | $ | 260,597,427 | $ | 11,059,208 | ||

| Receivable for Fund Shares Sold | 133,051 | 33,458 | ||||

| Receivable for Securities Sold | 1,991,528 | 18,626 | ||||

| Dividends Receivable | 120,728 | 3,380 | ||||

| Interest Receivable | 239 | 12 | ||||

| Total Assets | 262,842,973 | 11,114,684 | ||||

| Liabilities: | ||||||

| Payable for Fund Shares Redeemed | 386,408 | - | ||||

| Payable for Securities Purchased | 113,675 | 4,372 | ||||

| Payable to Advisor | 316,565 | 10,232 | ||||

| Total Liabilities | 816,648 | 14,604 | ||||

| Net Assets | $ | 262,026,325 | $ | 11,100,080 | ||

| Net Assets Consist of: | ||||||

| Paid In Capital | $ | 233,771,732 | $ | 10,267,206 | ||

| Accumulated Undistributed Net Investment Income (Loss) | (182,142 | ) | 3,254 | |||

| Accumulated Realized Gain (Loss) on Investments - Net | (1,170,481 | ) | 56,105 | |||

| Unrealized Appreciation (Depreciation) in Value of Investment Securities - Net | 29,607,216 | 773,515 | ||||

| Net Assets | $ | 262,026,325 | $ | 11,100,080 | ||

| Net Asset Value and Offering Price (Note 2) | $ | 54.22 | $ | 31.36 | ||

| * Investments at Identified Cost | $ | 230,990,211 | $ | 10,285,693 | ||

| Shares Outstanding (Unlimited number of shares | 4,832,997 | 353,905 | ||||

| authorized without par value) | ||||||

| Statements of Operations (Unaudited) | ||||||

| For the six month period ended June 30, 2012 | ||||||

| Investment Income: | ||||||

| Dividends | $ | 1,807,609 | $ | 60,545 | ||

| Interest | 1,433 | 58 | ||||

| Total Investment Income | 1,809,042 | 60,603 | ||||

| Expenses: | ||||||

| Investment Advisor Fees | 2,447,705 | 74,805 | ||||

| Total Expenses | 2,447,705 | 74,805 | ||||

| Less: Expenses Waived | (456,521 | ) | (17,456 | ) | ||

| Net Expenses | 1,991,184 | 57,349 | ||||

| Net Investment Income (Loss) | (182,142 | ) | 3,254 | |||

| Realized and Unrealized Gain (Loss) on Investments: | ||||||

| Net Realized Gain (Loss) on Investments | 2,117,141 | 98,777 | ||||

| Net Change in Unrealized Appreciation (Depreciation) on Investments | 5,525,041 | 84,513 | ||||

| Net Realized and Unrealized Gain (Loss) on Investments | 7,642,182 | 183,290 | ||||

| Net Increase (Decrease) in Net Assets from Operations | $ | 7,460,040 | $ | 186,544 | ||

| The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 20

| Paradigm Funds | ||||||

| Statements of Assets and Liabilities (Unaudited) | Opportunity | Micro-Cap | ||||

| June 30, 2012 | Fund | Fund | ||||

| Assets: | ||||||

| Investment Securities at Fair Value* | $ | 4,855,482 | $ | 15,726,390 | ||

| Cash | 253 | - | ||||

| Receivable for Fund Shares Sold | 98 | - | ||||

| Receivable for Securities Sold | 12,409 | 510,442 | ||||

| Dividends Receivable | 1,595 | 5,364 | ||||

| Interest Receivable | 5 | 13 | ||||

| Total Assets | 4,869,842 | 16,242,209 | ||||

| Liabilities: | ||||||

| Payable for Securities Purchased | 3,498 | - | ||||

| Payable to Advisor | 4,836 | 15,921 | ||||

| Total Liabilities | 8,334 | 15,921 | ||||

| Net Assets | $ | 4,861,508 | $ | 16,226,288 | ||

| Net Assets Consist of: | ||||||

| Paid In Capital | $ | 4,121,330 | $ | 16,001,405 | ||

| Accumulated Undistributed Net Investment Income (Loss) | (10,512 | ) | (40,516 | ) | ||

| Accumulated Realized Gain (Loss) on Investments - Net | 12,017 | 573,745 | ||||

| Unrealized Appreciation (Depreciation) in Value of Investment Securities - Net | 738,673 | (308,346 | ) | |||

| Net Assets | $ | 4,861,508 | $ | 16,226,288 | ||

| Net Asset Value and Offering Price (Note 2) | $ | 25.97 | $ | 21.82 | ||

| * Investments at Identified Cost | $ | 4,116,809 | $ | 16,034,736 | ||

| Shares Outstanding (Unlimited number of shares | 187,194 | 743,730 | ||||

| authorized without par value) | ||||||

| Statements of Operations (Unaudited) | ||||||

| For the six month period ended June 30, 2012 | ||||||

| Investment Income: | ||||||

| Dividends (Net of foreign withholding taxes** of $0 and $788, respectively) | $ | 23,722 | $ | 37,733 | ||

| Interest | 15 | 95 | ||||

| Total Investment Income | 23,737 | 37,828 | ||||

| Expenses: | ||||||

| Investment Advisor Fees | 48,295 | 78,344 | ||||

| Total Expenses | 48,295 | 78,344 | ||||

| Less: Expenses Waived | (14,046 | ) | - | |||

| Net Expenses | 34,249 | 78,344 | ||||

| Net Investment Income (Loss) | (10,512 | ) | (40,516 | ) | ||

| Realized and Unrealized Gain (Loss) on Investments: | ||||||

| Net Realized Gain (Loss) on Investments | 69,868 | 689,839 | ||||

| Net Change in Unrealized Appreciation (Depreciation) on Investments | 111,325 | (858,279 | ) | |||

| Net Realized and Unrealized Gain (Loss) on Investments | 181,193 | (168,440 | ) | |||

| Net Increase (Decrease) in Net Assets from Operations | $ | 170,681 | $ | (208,956 | ) | |

| ** Foreign withholding taxes on foreign dividends have been provid- ed for in accordance with the Funds’ understanding of the applica- ble country's tax rules and rates. The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 21

| Paradigm Funds | ||||||||||||

| Statements of Changes in Net Assets | Value Fund | Select Fund | ||||||||||

| (Unaudited) | (Unaudited) | |||||||||||

| 1/1/2012 | 1/1/2011 | 1/1/2012 | 1/1/2011 | |||||||||

| to | to | to | to | |||||||||

| 6/30/2012 | 12/31/2011 | 6/30/2012 | 12/31/2011 | |||||||||

| From Operations: | ||||||||||||

| Net Investment Income (Loss) | $ | (182,142 | ) | $ | (787,755 | ) | $ | 3,254 | $ | 13,610 | ||

| Net Realized Gain (Loss) on Investments | 2,117,141 | 6,680,547 | 98,777 | 198,161 | ||||||||

| Change in Net Unrealized Appreciation (Depreciation) | 5,525,041 | (21,135,754 | ) | 84,513 | (209,355 | ) | ||||||

| Increase (Decrease) in Net Assets from Operations | 7,460,040 | (15,242,962 | ) | 186,544 | 2,416 | |||||||

| From Distributions to Shareholders: | ||||||||||||

| Net Investment Income | - | - | - | (14,165 | ) | |||||||

| Net Realized Gain from Security Transactions | - | (3,448,769 | ) | - | - | |||||||

| Total Distributions to Shareholders | - | (3,448,769 | ) | - | (14,165 | ) | ||||||

| From Capital Share Transactions: | ||||||||||||

| Proceeds From Sale of Shares | 67,304,113 | 199,045,263 | 3,782,232 | 4,955,030 | ||||||||

| Proceeds from Redemption Fees (Note 2) | 7,533 | 129,958 | 783 | 77 | ||||||||

| Shares Issued on Reinvestment of Dividends | - | 3,384,204 | - | 14,125 | ||||||||

| Cost of Shares Redeemed | (47,594,489 | ) | (204,517,840 | ) | (799,196 | ) | (944,604 | ) | ||||

| Net Increase (Decrease) from Shareholder Activity | 19,717,157 | (1,958,415 | ) | 2,983,819 | 4,024,628 | |||||||

| Net Increase (Decrease) in Net Assets | 27,177,197 | (20,650,146 | ) | 3,170,363 | 4,012,879 | |||||||

| Net Assets at Beginning of Period | 234,849,128 | 255,499,274 | 7,929,717 | 3,916,838 | ||||||||

| Net Assets at End of Period | $ | 262,026,325 | $ | 234,849,128 | $ | 11,100,080 | $ | 7,929,717 | ||||

| Accumulated Undistributed Net Investment Income (Loss) | $ | (182,142 | ) | $ | - | $ | 3,254 | $ | - | |||

| Share Transactions: | ||||||||||||

| Issued | 1,216,165 | 3,563,706 | 116,258 | 161,670 | ||||||||

| Reinvested | - | 64,155 | - | 465 | ||||||||

| Redeemed | (853,042 | ) | (3,796,093 | ) | (24,563 | ) | (31,750 | ) | ||||

| Net Increase (Decrease) in Shares | 363,123 | (168,232 | ) | 91,695 | 130,385 | |||||||

| Shares Outstanding Beginning of Period | 4,469,874 | 4,638,106 | 262,210 | 131,825 | ||||||||

| Shares Outstanding End of Period | 4,832,997 | 4,469,874 | 353,905 | 262,210 | ||||||||

| The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 22

| Paradigm Funds | |||||||||||||

| Statements of Changes in Net Assets | Opportunity Fund | Micro-Cap Fund | |||||||||||

| (Unaudited) | (Unaudited) | ||||||||||||

| 1/1/2012 | 1/1/2011 | 1/1/2012 | 1/1/2011 | ||||||||||

| to | to | to | to | ||||||||||

| 6/30/2012 | 12/31/2011 | 6/30/2012 | 12/31/2011 | ||||||||||

| From Operations: | |||||||||||||

| Net Investment Income (Loss) | $ | (10,512 | ) | $ | (37,003 | ) | $ | (40,516 | ) | $ | (7,121 | ) | |

| Net Realized Gain (Loss) on Investments | 69,868 | 494,674 | 689,839 | 197,926 | |||||||||

| Change in Net Unrealized Appreciation (Depreciation) | 111,325 | (537,492 | ) | (858,279 | ) | (40,694 | ) | ||||||

| Increase (Decrease) in Net Assets from Operations | 170,681 | (79,821 | ) | (208,956 | ) | 150,111 | |||||||

| From Distributions to Shareholders: | |||||||||||||

| Net Investment Income | - | - | - | - | |||||||||

| Net Realized Gain from Security Transactions | - | (37,186 | ) | - | - | ||||||||

| Total Distributions to Shareholders | - | (37,186 | ) | - | - | ||||||||

| From Capital Share Transactions: | |||||||||||||

| Proceeds From Sale of Shares | 252,104 | 14,626 | 9,428,825 | 5,073,670 | |||||||||

| Proceeds from Redemption Fees (Note 2) | - | - | - | - | |||||||||

| Shares Issued on Reinvestment of Dividends | - | 37,186 | - | - | |||||||||

| Cost of Shares Redeemed | (51,892 | ) | (383,396 | ) | (19,906 | ) | (1,645,185 | ) | |||||

| Net Increase (Decrease) from Shareholder Activity | 200,212 | (331,584 | ) | 9,408,919 | 3,428,485 | ||||||||

| Net Increase (Decrease) in Net Assets | 370,893 | (448,591 | ) | 9,199,963 | 3,578,596 | ||||||||

| Net Assets at Beginning of Period | 4,490,615 | 4,939,206 | 7,026,325 | 3,447,729 | |||||||||

| Net Assets at End of Period | $ | 4,861,508 | $ | 4,490,615 | $ | 16,226,288 | $ | 7,026,325 | |||||

| Accumulated Net Investment Income (Loss) | $ | (10,512 | ) | $ | - | $ | (40,516 | ) | $ | - | |||

| Share Transactions: | |||||||||||||

| Issued | 9,803 | 555 | 410,230 | 251,925 | |||||||||

| Reinvested | - | 1,476 | - | - | |||||||||

| Redeemed | (1,920 | ) | (15,760 | ) | (899 | ) | (80,132 | ) | |||||

| Net Increase (Decrease) in Shares | 7,883 | (13,729 | ) | 409,331 | 171,793 | ||||||||

| Shares Outstanding Beginning of Period | 179,311 | 193,040 | 334,399 | 162,606 | |||||||||

| Shares Outstanding End of Period | 187,194 | 179,311 | 743,730 | 334,399 | |||||||||

| The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 23

| Paradigm Value Fund | ||||||||||||||||||

| Financial Highlights - Paradigm Value Fund | ||||||||||||||||||

| (Unaudited) | ||||||||||||||||||

| Selected data for a share outstanding | 1/1/2012 | 1/1/2011 | 1/1/2010 | 1/1/2009 | 1/1/2008 | 1/1/2007 | ||||||||||||

| throughout the period: | to | to | to | to | to | to | ||||||||||||

| 6/30/2012 | 12/31/2011 | 12/31/2010 | 12/31/2009 | 12/31/2008 | 12/31/2007 | |||||||||||||

| Net Asset Value - Beginning of Period | $ | 52.54 | $ | 55.09 | $ | 42.75 | $ | 32.51 | $ | 49.27 | $ | 48.55 | ||||||

| Net Investment Income (Loss) (a) | (0.04 | ) | (0.15 | ) | (0.07 | ) | 0.16 | (0.22 | ) | (0.40 | ) | |||||||

| Net Gains (Loss) on Securities (Realized and Unrealized) | 1.72 | (1.64 | ) | 12.49 | 10.07 | (16.52 | ) | 2.84 | ||||||||||

| Total from Investment Operations | 1.68 | (1.79 | ) | 12.42 | 10.23 | (16.74 | ) | 2.44 | ||||||||||

| Distributions (From Net Investment Income) | - | - | (0.09 | ) | - | - | - | |||||||||||

| Distributions (From Capital Gains) | - | (0.78 | ) | - | - | (0.07 | ) | (1.73 | ) | |||||||||

| Total Distributions | 0.00 | (0.78 | ) | (0.09 | ) | 0.00 | (0.07 | ) | (1.73 | ) | ||||||||

| Proceeds from Redemption Fee (Note 2) | 0.00 | + | 0.02 | 0.01 | 0.01 | 0.05 | 0.01 | |||||||||||

| Net Asset Value - End of Period | $ | 54.22 | $ | 52.54 | $ | 55.09 | $ | 42.75 | $ | 32.51 | $ | 49.27 | ||||||

| Total Return (b) | 3.20 | % ** | (3.22 | )% | 29.08 | % | 31.50 | % | (33.88 | )% | 5.03 | % | ||||||

| Ratios/Supplemental Data | ||||||||||||||||||

| Net Assets - End of Period (Thousands) | $ | 262,026 | $ | 234,849 | $ | 255,499 | $ | 123,043 | $ | 85,018 | $ | 116,247 | ||||||

| Before Reimbursement | ||||||||||||||||||

| Ratio of Expenses to Average Net Assets | 1.85 | % *** | 1.83 | % | 1.89 | % | 1.98 | % | 1.99 | % | 2.02 | % | ||||||

| After Reimbursement | ||||||||||||||||||

| Ratio of Expenses to Average Net Assets (c) ++ | 1.50 | % *** | 1.50 | % | 1.50 | % | 1.63 | % | 1.99 | % | 2.02 | % | ||||||

| Ratio of Net Investment Income (Loss) to Average | ||||||||||||||||||

| Net Assets (c) ++ | -0.14 | % *** | -0.26 | % | -0.14 | % | 0.43 | % | -0.52 | % | -0.78 | % | ||||||

| Portfolio Turnover Rate | 21.40 | % ** | 83.95 | % | 81.17 | % | 69.85 | % | 67.84 | % | 59.75 | % | ||||||

| Paradigm Select Fund | ||||||||||||||||||

| Financial Highlights - Paradigm Select Fund | ||||||||||||||||||

| (Unaudited) | ||||||||||||||||||

| Selected data for a share outstanding throughout the period: | 1/1/2012 | 1/1/2011 | 1/1/2010 | 1/1/2009 | 1/1/2008 | 1/1/2007 | ||||||||||||

| to | to | to | to | to | to | |||||||||||||

| 6/30/2012 | 12/31/2011 | 12/31/2010 | 12/31/2009 | 12/31/2008 | 12/31/2007 | |||||||||||||

| Net Asset Value - Beginning of Period | $ | 30.24 | $ | 29.71 | $ | 23.82 | $ | 18.53 | $ | 27.91 | $ | 26.48 | ||||||

| Net Investment Income (Loss) (a) | 0.01 | 0.06 | (0.05 | ) | 0.08 | 0.03 | (0.06 | ) | ||||||||||

| Net Gains (Loss) on Securities (Realized and Unrealized) | 1.11 | 0.52 | 6.01 | 5.28 | (9.41 | ) | 1.54 | |||||||||||

| Total from Investment Operations | 1.12 | 0.58 | 5.96 | 5.36 | (9.38 | ) | 1.48 | |||||||||||

| Distributions (From Net Investment Income) | - | (0.05 | ) | (0.07 | ) | (0.07 | ) | - | - | |||||||||

| Distributions (From Capital Gains) | - | - | - | - | - | (0.05 | ) | |||||||||||

| Total Distributions | - | (0.05 | ) | (0.07 | ) | (0.07 | ) | - | (0.05 | ) | ||||||||

| Proceeds from Redemption Fee (Note 2) | - + | - + | - + | - + | - | - | ||||||||||||

| Net Asset Value - End of Period | $ | 31.36 | $ | 30.24 | $ | 29.71 | $ | 23.82 | $ | 18.53 | $ | 27.91 | ||||||

| Total Return (b) | 3.74 | % ** | 1.97 | % | 25.03 | % | 28.92 | % | (33.61 | )% | 5.57 | % | ||||||

| Ratios/Supplemental Data | ||||||||||||||||||

| Net Assets - End of Period (Thousands) | $ | 11,100 | $ | 7,930 | $ | 3,917 | $ | 2,710 | $ | 2,031 | $ | 11,109 | ||||||

| Before Reimbursement | ||||||||||||||||||

| Ratio of Expenses to Average Net Assets | 1.50 | % *** | 1.50 | % | 1.50 | % | 1.50 | % | 1.50 | % | 1.50 | % | ||||||

| After Reimbursement | ||||||||||||||||||

| Ratio of Expenses to Average Net Assets ++ | 1.15 | % *** | 1.20 | % | 1.50 | % | 1.50 | % | 1.50 | % | 1.50 | % | ||||||

| Ratio of Net Investment Income/(Loss) to Average | ||||||||||||||||||

| Net Assets ++ | 0.07 | % *** | 0.21 | % | -0.20 | % | 0.42 | % | 0.13 | % | -0.23 | % | ||||||

| Portfolio Turnover Rate | 18.30 | % ** | 58.40 | % | 65.77 | % | 65.57 | % | 47.71 | % | 64.68 | % | ||||||

| ** Not Annualized. *** Annualized. (a) Per share amount calculated using the average shares method. (b) Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund assuming reinvestment of dividends. Returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or redemption of Fund shares. (c) Includes dividend expense on securities sold short and interest expense of 0.00% for the six months ended 6/30/2012, and 0.00%, 0.00%, 0.00%, 0.00% (Amount calculated less than 0.005%) and 0.02% for the years ended 12/31/2011 - 2007, respectively. + Amount calculated is less than $0.005. ++ Such percentages reflect an expense waiver by the Advisor (for Value since 2009 and for Select since 2011). |

| The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 24

| Paradigm Opportunity Fund | |||||||||||||||||||

| Financial Highlights - Paradigm Opportunity Fund | |||||||||||||||||||

| (Unaudited) | |||||||||||||||||||

| Selected data for a share outstanding throughout the period: | 1/1/2012 | 1/1/2011 | 1/1/2010 | 1/1/2009 | 1/1/2008 | 1/1/2007 | |||||||||||||

| to | to | to | to | to | to | ||||||||||||||

| 6/30/2012 | 12/31/2011 | 12/31/2010 | 12/31/2009 | 12/31/2008 | 12/31/2007 | ||||||||||||||

| Net Asset Value - Beginning of Period | $ | 25.04 | $ | 25.59 | $ | 20.29 | $ | 13.79 | $ | 22.94 | $ | 23.21 | |||||||

| Net Investment Income (Loss) (a) | (0.06 | ) | (0.20 | ) | (0.12 | ) | (0.01 | ) | (0.13 | ) | (0.04 | ) | |||||||

| Net Gains (Loss) on Securities (Realized and Unrealized) | 0.99 | (0.14 | ) | 5.42 | 6.51 | (9.02 | ) | 0.47 | |||||||||||

| Total from Investment Operations | 0.93 | (0.34 | ) | 5.30 | 6.50 | (9.15 | ) | 0.43 | |||||||||||

| Distributions (From Net Investment Income) | - | - | - | - | - | - | |||||||||||||

| Distributions (From Capital Gains) | - | (0.21 | ) | - | - | - | (0.70 | ) | |||||||||||

| Total Distributions | - | (0.21 | ) | - | - | - | (0.70 | ) | |||||||||||

| Proceeds from Redemption Fee (Note 2) | - | - | - + | - | - + | - | |||||||||||||

| Net Asset Value - End of Period | $ | 25.97 | $ | 25.04 | $ | 25.59 | $ | 20.29 | $ | 13.79 | $ | 22.94 | |||||||

| Total Return (b) | 3.71 | % ** | (1.34 | )% | 26.12 | % | 47.14 | % | (39.89 | )% | 1.85 | % | |||||||

| Ratios/Supplemental Data | |||||||||||||||||||

| Net Assets - End of Period (Thousands) | $ | 4,862 | $ | 4,491 | $ | 4,939 | $ | 3,693 | $ | 2,425 | $ | 5,613 | |||||||

| Before Reimbursement | |||||||||||||||||||

| Ratio of Expenses to Average Net Assets | 2.00 | % *** | 2.00 | % | 2.00 | % | 2.00 | % | 2.00 | % | 2.00 | % | |||||||

| After Reimbursement | |||||||||||||||||||

| Ratio of Expenses to Average Net Assets (c) | 1.42 | % *** | 1.50 | % | 1.50 | % | 1.50 | % | 1.50 | % | 1.50 | % | |||||||

| Ratio of Net Investment Income/(Loss) to Average | |||||||||||||||||||

Net Assets (c) | -0.44 | % *** | -0.76 | % | -0.56 | % | -0.04 | % | -0.67 | % | -0.17 | % | |||||||

| Portfolio Turnover Rate | 16.58 | % ** | 65.44 | % | 96.20 | % | 135.62 | % | 164.89 | % | 169.26 | % | |||||||

| Paradigm Micro-Cap Fund | |||||||||||||||

| Financial Highlights - Paradigm Micro-Cap Fund | |||||||||||||||

| (Unaudited) | |||||||||||||||

| Selected data for a share outstanding throughout the period: | 1/1/2012 | 1/1/2011 | 1/1/2010 | 1/1/2009 | 1/1/2008* | ||||||||||

| to | to | to | to | to | |||||||||||

| 6/30/2012 | 12/31/2011 | 12/31/2010 | 12/31/2009 | 12/31/2008 | |||||||||||

| Net Asset Value - Beginning of Period | $ | 21.01 | $ | 21.20 | $ | 17.99 | $ | 13.98 | $ | 20.00 | |||||

| Net Investment Income (Loss) (a) | (0.07 | ) | (0.04 | ) | (0.01 | ) | 0.14 | 0.15 | |||||||

| Net Gains (Loss) on Securities (Realized and Unrealized) | 0.88 | (d) | (0.15 | ) | 3.33 | 3.98 | (6.17 | ) | |||||||

| Total from Investment Operations | 0.81 | (0.19 | ) | 3.32 | 4.12 | (6.02 | ) | ||||||||

| Distributions (From Net Investment Income) | - | - | (0.11 | ) | (0.11 | ) | - | ||||||||

| Distributions (From Capital Gains) | - | - | - | - | - | ||||||||||

| Total Distributions | - | - | (0.11 | ) | (0.11 | ) | - | ||||||||

| Proceeds from Redemption Fee (Note 2) | - | - | - | - + | - | ||||||||||

| Net Asset Value - End of Period | $ | 21.82 | $ | 21.01 | $ | 21.20 | $ | 17.99 | $ | 13.98 | |||||

| Total Return (b) | 3.86 | % ** | (0.90 | )% | 18.44 | % | 29.44 | % | (30.10 | )% | |||||

| Ratios/Supplemental Data | |||||||||||||||

| Net Assets - End of Period (Thousands) | $ | 16,226 | $ | 7,026 | $ | 3,448 | $ | 2,575 | $ | 1,620 | |||||

| Ratio of Expenses to Average Net Assets | 1.25 | % *** | 1.25 | % | 1.25 | % | 1.25 | % | 1.25 | % | |||||

| Ratio of Net Investment Income/(Loss) to Average Net Assets | -0.64 | % *** | -0.20 | % | -0.08 | % | 0.92 | % | 0.86 | % | |||||

| Portfolio Turnover Rate | 28.31 | % ** | 126.43 | % ++ | 77.78 | % | 79.35 | % | 70.57 | % | |||||

| * Commencement of operations. ** Not Annualized. *** Annualized. (a) Per share amount calculated using the average shares method. (b) Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund assuming reinvestment of dividends. Returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or redemption of Fund shares. (c) Such percentages reflect an expense waiver by the Advisor. (d) Realized and unrealized gains and losses per share in this caption are balancing amounts necessary to reconcile the change in the net asset value for the period, and may not reconcile with the aggregate gains and losses in the Statement of Operations due to share transactions for the period. + Amount calculated is less than $0.005. ++ The Fund's portfolio turnover rate increased due to the change in the Fund's principal investment strategy to invest (under normal circumstances) at least 80% of its net assets in the common stocks of U.S. micro-cap companies effective December 27, 2011. |

| The accompanying notes are an integral part of these financial statements. |

2012 Semi-Annual Report 25

NOTES TO FINANCIAL STATEMENTS

PARADIGM FUNDS

June 30, 2012

(Unaudited)

1.) ORGANIZATION

The Paradigm Funds (the "Trust”) is an open-end management investment company organized in Ohio as a business trust on September 13, 2002 that may offer shares of beneficial interest in a number of separate series, each series representing a distinct fund with its own investment objectives and policies. The Paradigm Value Fund (“Value”) commenced operations on January 1, 2003. The Paradigm Value Fund's investment objective is long-term capital appreciation. The Paradigm Opportunity Fund (“Opportunity”) and Paradigm Select Fund (“Select”) both commenced operations on January 1, 2005 with long-term capital appreciation as their objective. The Paradigm Micro-Cap Fund (“Micro-Cap”) commenced operations on January 1, 2008. Effective December 27, 2011, the name of the Paradigm Intrinsic Value Fund was changed to the Paradigm Micro-Cap Fund. The Paradigm Micro-Cap Fund's investment objective is long-term capital appreciation. Under normal circumstances, the Micro-Cap Fund invests at least 80% of its net assets in the common stocks of U.S. micro-cap companies. Prior to December 27, 2011, the principal investment strategy of the Fund was to invest primarily in the common stocks of small, mid or large capitalization companies that the Advisor believed had the potential for capital appreciation. Value, Opportunity, Select and Micro-Cap are all diversified funds. The advisor to Value, Opportunity, Select and Micro-Cap (each a “Fund” and collectively the “Funds”) is Paradigm Funds Advisor LLC (the “Advisor”).

2.) SIGNIFICANT ACCOUNTING POLICIES

SECURITY VALUATION: All investments in securities are recorded at their estimated fair value, as described in Note 3.

SECURITY TRANSACTIONS AND OTHER: Security transactions are recorded based on a trade date. Dividend income is recognized on the ex-dividend date. Interest income is recognized on an accrual basis. The Funds use the highest cost basis in computing gain or loss on sale of investment securities. Discounts and premiums on fixed income securities purchased are amortized over the lives of the respective securities. Withholding taxes on foreign dividends have been provided for in accordance with the Funds’ understanding of the applicable country’s tax rules and rates. The Funds may invest in real estate investment trusts (“REITs”) that pay distributions to their shareholders based on available funds from operations. It is common for these distributions to exceed the REITs taxable earnings and profits resulting in the excess portion of such distribution to be designated as return of capital. Distributions received from REITs are generally recorded as dividend income and, if necessary, are reclassified annually in accordance with tax information provided by the underlying REITs.