Washington, D.C. 20549

WINTON FUTURES FUND, L.P. (US)

c/o ALTEGRIS PORTFOLIO MANAGEMENT, INC.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer," “accelerated filer" and “smaller reporting company" in Rule 12b-2 of the Exchange Act.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

Not Applicable.

None.

ITEM 1: BUSINESS

(a) General Development of Business

Winton Futures Fund, L.P. (US) (d/b/a Altegris Winton Futures Fund, L.P.) (the “Partnership”) is a limited partnership organized under the Colorado Uniform Limited Partnership Act in March 1999. The Partnership’s business is the speculative trading and investment in international futures, options and forward markets (“Commodity Interests”). The Partnership commenced its trading and investment operations in November 1999. Under the Partnership’s First Amended Agreement of Limited Partnership (the “Limited Partnership Agreement”), Altegris Portfolio Management, Inc. (d/b/a Altegris Funds), an Arkansas corporation (“Altegris Funds” or the “General Partner”), serves as general partner of the Partnership and has sole responsibility for management and administration of all aspects of the Partnership’s business. Investors purchasing limited partnership interests (the “Interests”) in the Partnership (“Limited Partners” and together with the General Partner, “Partners”) have no rights to participate in the management of the Partnership.

Altegris Funds is registered with the Commodity Futures Trading Commission (“CFTC”) as a Commodity Pool Operator (“CPO”), and is a member of National Futures Association (“NFA”). Winton Capital Management Limited, a United Kingdom Company, acts as the Partnership’s trading advisor (��Advisor”). The Advisor is registered with the CFTC as a Commodity Trading Advisor and is authorized and regulated by the United Kingdom’s Financial Services Authority. Effective as of December 31, 2010, Altegris Funds became a wholly-owned subsidiary of Genworth Financial, Inc. (“Genworth”). Genworth became a principal of Altegris Funds and Altegris Futures, L.L.C. (“Altegris Futures”), an affiliate of the General Partner, in January 2011.

Altegris Investments, Inc. (“Altegris”), an affiliate of the General Partner, serves as a selling agent of the Interests and acted as the Partnership’s introducing broker until January 1, 2011, when Altegris Futures replaced Altegris as the Partnership’s introducing broker (“Introducing Broker”). Altegris Futures is registered with the CFTC as an Introducing Broker.

The Partnership’s term will end upon the first to occur of the following: December 31, 2035; receipt by the General Partner of an election to dissolve the Partnership at a specified time by Limited Partners owning more than 50% of the Interests then outstanding, notice of which is sent by registered mail to the General Partner not less than ninety (90) days prior to the effective date of such dissolution; withdrawal (including withdrawal after suspension of trading), admitted or court decreed insolvency or dissolution of the General Partner; termination of the Partnership pursuant to the terms of the Limited Partnership Agreement; or any event that makes it unlawful for the existence of the Partnership to be continued or requiring termination of the Partnership.

The Partnership is not required to be, and is not, registered under the Investment Company Act of 1940, as amended.

As of February 28, 2011, the aggregate net asset value of the Interests in the Partnership before redemptions was $757,212,460. The Partnership operates on a calendar fiscal year and has no subsidiaries.

The Partnership offers three “classes” of Interests: Class A, Class B and Institutional Interests (each, a “Class of Interest”). The Classes of Interests differ from each other only in the fees that they pay and the applicable investment minimums.

(b) Financial Information About Segments

The Partnership’s business constitutes only one segment for financial reporting purposes — i.e., a speculative “commodity pool.” The Partnership does not engage in sales of goods or services. Financial information regarding the Partnership’s business is set forth in the Partnership’s financial statements, included herewith.

(c) Narrative Description of Business

The Partnership is designed to produce long-term capital appreciation through growth, and not current income. Altegris Funds has selected the Advisor to trade one of the Advisor’s proprietary trading models, the Winton Diversified Program (the “Program”), on behalf of the Partnership. The Advisor currently has the authority to trade the Program on behalf of the Partnership in all the easily accessible and liquid commodity interests (comprising international futures, options and forward markets) that it practically can, which currently consists mainly of commodity interests that are futures, options and forward contracts and certain OTC products, such as swaps in the following areas: stock indices, bonds, short term interest rates, currencies, precious and base metals, grains, livestock, energy and agricultural products.

The Advisor’s investment technique in trading the Program consists of trading a portfolio of approximately 120 diversified, highly liquid financial instruments traded across numerous futures markets, and may also include certain OTC instruments and government securities, employing a computerized, technical, principally trend-following trading system. This system tracks the daily price movements and other data from these markets around the world, and carries out certain computations to determine each day how long or short the portfolio should be to maximize profit within a certain range of risk. If rising prices are anticipated, a long position will be established; a short position will be established if prices are expected to fall.

The trading methods applied by the Advisor to trade the Program on behalf of the Partnership are proprietary, complex and confidential. As a result, the following explanation is of necessity general in nature and not intended to be exhaustive. The Advisor plans to continue the research and development of its trading methodology and, therefore, retains the right to revise any methods or strategy, including the technical trading factors used, the commodity interests traded and/or the money management principles applied.

The Program traded by the Advisor pursues a technical trend-following system. Technical analysis refers to analysis based on data intrinsic to a market, such as price and volume. This is to be contrasted with fundamental analysis which relies on factors external to a market, such as supply and demand. The Program uses no fundamental factors.

A trend-following system is one that attempts to take advantage of the observable tendency of the markets to trend (that is, to move from one price point to another, either higher or lower over a period of time), and to tend to make exaggerated movements in both upward and downward directions as a result of such trends. These exaggerated movements are largely explained as a result of the influence of crowd psychology or the herd instinct, amongst market participants.

The Advisor developed the Program by relating the probability of the size and direction of future price movements with certain indicators derived from past price movements which characterize the degree of trending of each market at any time.

The Program follows a primarily non-discretionary system. This means that trading signals are automatically generated by its models and, except in extreme situations, are followed to the letter. The Advisor has found that the absence of discretion promotes greater consistency in performance and lessens the opportunity for less reliable anecdotal evidence and personal judgment to influence decision-making. In unusual market situations, the Advisor reserves the right to deviate from its automatic system.

The Advisor will select the type of order to be used in executing each trade on behalf of the Partnership and may use any type of order permitted by the exchange on which the order is placed. The Advisor may place individual orders for each account it trades, or a block order for all accounts it trades, in which the same commodity interest is being cleared through the same clearing broker. In the latter instance, the Advisor will allocate trades to individual accounts using a proprietary algorithm. The aim of this algorithm is to achieve an average price for transactions as close as mathematically possible for each account. This takes the form of an optimization process where the objective is to minimize the variation in the average traded price for each account. On occasion, it may direct the clearing broker for the accounts to employ a neutral order allocation system to assign trades. Partial fills will be allocated in proportion to account size.

The trading strategy and account management principles of the Program described above are factors upon which the Advisor will base its trading decisions. Such principles may be revised from time to time by the Advisor as it deems advisable or necessary. Accordingly, no assurance is given that all of these factors will be considered with respect to every trade or recommendation made on behalf of the Partnership or that consideration of any of these factors in a particular situation will lessen the risk of loss or increase the potential for profits.

It is expected that between 5% and 50% of the Partnership’s assets generally will be held as initial margin or option premiums (in cash or U.S. Treasury Department (“Treasury”) securities) in the Partnership’s brokerage accounts at its clearing broker, Newedge USA, LLC (“Newedge USA”), a futures commission merchant (“FCM”), and/or Newedge Alternative Strategies, Inc. (“NAST”) (which may from time to time execute spot and other over-the-counter foreign exchange transactions as a counterparty to the Partnership), and available for trading by the Advisor in Commodity Interests on behalf of the Partnership. Interest on Partnership assets held at Newedge USA in cash or Treasury securities will be credited to the Partnership as described under “Charges.” Depending on market factors, the amount of margin or option premiums held at Newedge USA could change significantly, and all of the Partnership’s assets are available for use as margin. The Partnership may also retain other brokers and/or dealers from time to time to clear or execute a portion of Partnership trades made by the Advisor.

With respect to Partnership assets not held at Newedge USA or NAST as described above, but deposited with Wilmington Trust Company (the “Custodian”), the portion not held in checking, money market or other bank accounts (and used to pay Partnership operating expenses) will be invested in liquid, high-quality short-term securities at the direction of the Custodian or its sub-advisor, Wilmington Trust Investment Management, LLC, an affiliate of the Custodian that is registered with the Securities and Exchange Commission (“SEC”) as an investment adviser. The Partnership’s custody and investment management agreement with the Custodian permits the Custodian to invest in U.S. government and agency securities, other securities or instruments guaranteed by the U.S. government or its agencies, CDs, time deposits, banker’s acceptances, commercial paper and repurchase agreements — subject in each case to specific diversification, credit quality and maturity limitations. The Custodian may use sub-advisers to attempt to increase yield enhancement. The General Partner may direct that a portion of Partnership assets be deposited with other custodians and retain other sub-advisers for the purpose of attempting to increase yield enhancement via other cash management arrangements.

The percentage of the Partnership’s assets deposited with these firms is also subject to change in the General Partner’s sole discretion. The Partnership’s assets will not be commingled with the assets of any other person. Depositing the Partnership’s assets with banks or Newedge USA, or other clearing brokers, as segregated funds is not commingling for these purposes.

The Partnership pays all of its ongoing liabilities, expenses and costs. Altegris Funds receives a management fee of 0.104% of the month-end net asset value, before deduction for any accrued incentive fees related to the current quarter (the “management fee net asset value”), of all Class A Interests (1.25% per annum), 0.104% of the month-end management fee net asset value of all Class B Interests (1.25% per annum) and 0.0625% of the month-end management fee net asset value of all Institutional Interests (0.75% per annum). The Advisor receives a management fee of 0.083% of the management fee net asset value of the month-end capital account balances of all Interests (1.0% per annum) and 20% of quarterly trading profits applicable to each Class of Interest.

Each selling agent selling Class A Interests receives 0.166% of the month-end net asset value of the Partnership apportioned to each Class A Interest sold by such selling agent (2% per annum) and may elect to receive 0.0417% of the month-end net asset value apportioned to any Institutional Interest sold by such selling (0.50% per annum).

Newedge USA and/or NAST paid Altegris during 2010 and will pay Altegris Futures from and after January 1, 2011 a portion of the brokerage commissions and transaction fees received from the Partnership as well as a portion of the interest income received on the Partnership’s assets. Monthly brokerage charges equal to the greater of (A) actual commissions of $9.75 per round-turn (higher for certain exchanges or commodities) multiplied by number of round-turn trades, which amount includes other transaction costs; or (B) an amount equal to 0.125% of the management fee net asset value of all Interest holders’ month-end capital account balances (1.50% annually). If actual monthly commissions and transaction costs in (A) above are less than the amount in (B) above, the Partnership will pay the difference to the Introducing Broker as payment for brokerage-related services. In any

month when the amount in (A) is greater than the amount in (B) above, the Partnership pays only the amount described in (A) above.

The Partnership generally pays its operating expenses as they are incurred. A fixed administrative fee is charged to Class A and Class B Interests and paid to Altegris Funds equal to 0.0275% of the management fee net asset value of the month-end capital account balance of all such Class A and Class B Interests (0.333% per annum).

(h) Regulation

The CFTC has delegated to NFA responsibility for the registration of “commodity trading advisors,” “commodity pool operators,” “futures commission merchants,” “introducing brokers” and their respective associated persons and “floor brokers” and “floor traders.” The Commodity Exchange Act requires commodity pool operators such as Altegris Funds, commodity trading advisors such as the Advisor and commodity brokers or FCMs such as Newedge USA and introducing brokers such as Altegris Futures to be registered and to comply with various reporting and record keeping requirements. CFTC regulations also require FCMs and certain introducing brokers to maintain a minimum level of net capital. In addition, the CFTC and certain commodities exchanges have established limits referred to as “speculative position limits” on the maximum net long or net short speculative positions that any person may hold or control in any particular futures or options contracts traded on U.S. commodities exchanges. All accounts owned or managed by the Advisor will be combined for position limit purposes. The Advisor could be required to liquidate positions held for the Partnership in order to comply with such limits. Any such liquidation could result in substantial costs to the Partnership. In addition, many futures exchanges impose limits beyond which the price of a futures contract may not trade during the course of a trading day, and there is a potential for a futures contract to hit its daily price limit for several days in a row, making it impossible for the Advisor to liquidate a position and thereby experiencing a dramatic loss. Currency forward contracts currently are not subject to regulation by any U.S. government agency.

In addition to such registration requirements, the CFTC and certain commodity exchanges have established limits on the maximum net long or net short position which any person may hold or control in particular commodities. Most exchanges also limit the changes in futures contract prices that may occur during a single trading day. In January 2011, the CFTC proposed a separate position limits regime for 28 so-called “exempt” (i.e. metals and energy) and agricultural futures and options contracts and their economically equivalent swap contracts. Position limits in spot months are proposed to be 25% of the official estimated deliverable supply of the underlying commodity and in a non-spot month a percentage of the average aggregate 12-month rolling open interest in all months (swaps and futures) for each contract. The General Partner believes that the proposed limits are sufficiently large that if adopted, they should not restrict the Partnership’s trading strategy.

Currency forward contracts are not currently subject to regulation by any United States (“U.S.”) Government agency. The Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Reform Act”) was enacted in July 2010. The Reform Act includes provisions that comprehensively regulate the over-the-counter derivatives markets for the first time. The Reform Act will mandate that a substantial portion of over-the-counter derivatives must be executed in regulated markets and submitted for clearing to regulated clearinghouses. The mandates imposed by the Reform Act may result in the Partnership bearing higher upfront and mark-to-market margin, less favorable trade pricing, and the possible imposition of new or increased fees with respect to any swaps entered into by the Partnership.

The Reform Act also amended the definition of “eligible contract participant,” and the CFTC is interpreting that definition in a such manner that the Partnership may no longer be permitted to engage in forward currency transactions by directly accessing the interbank market. Rather, when the Reform Act goes into effect in July 2011, the Partnership may be limited to engaging in “retail forex transactions” which could limit the Partnership’s potential forward currency counterparties to futures commission merchants and retail foreign exchange dealers. Limiting on the Partnership’s potential forward currency counterparties in this manner could lead to the Partnership bearing higher upfront and mark-to-market margin, less favorable trade pricing, and the possible imposition of new or increased fees. The “retail forex” markets could also be significantly less liquid than the interbank market. Moreover, the creditworthiness of the futures commission merchants and retail foreign exchange dealers with which the Partnership may be required to trade could be significantly weaker than the creditworthiness of the financial institutions with which the Partnership currently engages for its forward currency transactions. Although the impact

of requiring the Partnership to conduct forward currency transactions in the “retail” market could be substantial, the full scope is currently unknown and the ultimate effect could also be negligible.

The Partnership has no employees.

Financial Information About Geographic Areas

The Partnership has no operations in foreign countries although it trades on foreign exchanges and other non-U.S. markets. The Partnership does not engage in sales of goods or services.

ITEM 1A: RISK FACTORS

Not required.

ITEM 1B: UNRESOLVED STAFF COMMENTS

Not applicable.

ITEM 2: PROPERTIES

The Partnership does not own or use any physical properties in the conduct of its business. Employees of Altegris, a wholly owned subsidiary of Genworth Financial, Inc. as of December 31, 2010, perform all administrative services for the Partnership from offices at 1202 Bergen Parkway, Suite 212, Evergreen, Colorado 80439 or at 1200 Prospect St., Suite 400, La Jolla, California 92037.

ITEM 3: LEGAL PROCEEDINGS

The Partnership is not aware of any pending legal proceedings to which either the Partnership is a party or to which any of its assets are subject. The Partnership is not aware of any material legal proceedings involving Altegris Funds or its principals in an adverse position to the Partnership or in which the Partnership has adverse interests. The Partnership has no subsidiaries.

ITEM 4: (REMOVED AND RESERVED)

PART II

ITEM 5: MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

(a) Market information

There is no trading market for the Interests, and none is likely to develop. Interests may be redeemed or transferred subject to the conditions imposed by the Limited Partnership Agreement.

(b) Holders

As of February 28, 2011 the Partnership had 8,363 holders of Interests.

(c) Dividends

Altegris Funds has sole discretion in determining what distributions, if any, the Partnership will make to its investors. To date no distributions or dividends have been paid on the Interests, and Altegris Funds has no present intention to make any.

(d) Securities Authorized for Issuance under Equity Compensation Plans

None.

(e) Recent Sales of Unregistered Securities; Use of Proceeds from Registered Securities

The Partnership did not sell any unregistered securities within the past three years which have not previously been included in the Partnership’s Quarterly Reports on Form 10-Q or in a Current Report on Form 8-K.

(f) Issuer Purchases of Equity Securities

Pursuant to the Limited Partnership Agreement, Limited Partners may redeem their Interests in the Partnership as of the end of any calendar month upon fifteen (15) days’ written notice to the General Partner. The redemption of capital from capital accounts by Limited Partners has no impact on the value of the capital accounts of other Limited Partners.

The following table summarizes Limited Partner redemptions during the fourth calendar quarter of 2010:

| Month Ended | | Amount Redeemed | |

| | | | |

| October 31, 2010 | | $ | 7,603,649 | |

| November 30, 2010 | | | 12,705,656 | |

| December 31, 2010 | | | 5,335,278 | |

| Total | | $ | 25,644,583 | |

ITEM 6: SELECTED FINANCIAL DATA

Not required.

ITEM 7: MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Reference is made to “Item 8. Financial Statements and Supplementary Data.” The information contained therein is essential to, and should be read in conjunction with, the following analysis.

(a) Liquidity

The Partnership’s assets are generally held as cash or cash equivalents, which are used to margin the Partnership’s futures positions and are sold to pay redemptions and expenses as needed. Other than any potential market-imposed limitations on liquidity, the Partnership’s assets are highly liquid and are expected to remain so. Market-imposed limitations, when they occur, can be due to limited open interest in certain futures markets or to daily price fluctuation limits, which are inherent in the Partnership’s futures trading. A portion of the Partnership’s assets not used for margin and held with the Custodian are invested in liquid, high quality securities. Through December 31, 2010 the Partnership experienced no meaningful periods of illiquidity in any of the markets traded by the Advisor on behalf of the Partnership.

(b) Capital Resources

The Partnership raises additional capital only through the sale of Interests and capital is increased through trading profits (if any) and interest income. The Partnership does not engage in borrowing.

The amount of capital raised for the Partnership should not have a significant impact on its operations, as the Partnership has no significant capital expenditure or working capital requirements other than for capital to pay trading losses, brokerage commissions and expenses. Within broad ranges of capitalization, the Partnership’s trading positions should increase or decrease in approximate proportion to the size of the Partnership.

The Partnership participates in the speculative trading of commodity futures contracts, options on futures contracts and forward contracts, substantially all of which are subject to margin requirements. The minimum amount of margin required for each contract is set from time to time in response to various market factors by the respective exchanges. Further, the Partnership’s FCMs and brokers may require margin in excess of minimum exchange requirements.

Contracts currently traded by the Advisor on behalf of the Partnership include exchange-traded futures contracts and over-the-counter forward currency contracts. The risks associated with exchange-traded contracts are generally perceived to be less than those associated with over-the-counter transactions because, in over-the-counter transactions, the Partnership must rely solely on the credit of its trading counterparties, whereas exchange-traded contracts are generally, but not universally, backed by the collective credit of the members of the exchange. The credit risk from counterparty non-performance associated with the Partnership’s over-the-counter forward currency transactions is the net unrealized gain on such contracts plus related collateral held by the counterparty.

The Partnership bears the risk of financial failure by Newedge USA, NAST (which may from time to time execute spot and other over-the-counter foreign exchange transactions as a counterparty to the Partnership) and/or other clearing brokers or counterparties with which the Partnership trades.

(c) Results of Operations

Performance Summary

The Partnership’s success depends primarily upon the Advisor’s ability to recognize and capitalize on market trends in the sectors of the global commodity futures markets in which it trades. The Partnership seeks to produce long-term capital appreciation through growth, and not current income. The past performance of the Partnership is not necessarily indicative of future results.

2010

During 2010, the Partnership achieved net realized and unrealized gains of $91,161,476 from its trading of commodity futures contracts including brokerage commissions of $9,080,039. The Partnership accrued total expenses of $34,714,623, including $14,074,548 in incentive fees, $11,527,983 in management fees paid to the General Partner, and $7,946,107 in service and professional fees. The Partnership earned $3,110,927 in interest

income during 2010. An analysis of the profits and losses generated from the Partnership’s commodity futures trading activities for each quarter during 2010 is set forth below.

Fourth Quarter 2010. The Partnership experienced a gain in October 2010 as stock markets continued their September rally. Government bonds slowed during the first week of the month before subsequently dropping. The main contributors to the positive performance during the month were futures contracts on stock indices, currencies, precious metals and agricultural markets. The falling US Dollar and buoyant gold price reversed mid-month before recovering a little towards month end as the Japanese yen continued to rise. The Partnership experienced a loss in November 2010. The Euro fell during the month helping the US Dollar to reverse its fall of the last two months. The Partnership established gains during the first week of the month as the US Dollar fell and stocks, bonds and commodity prices rose, although these price moves subsequently reversed. The month’s losses were focused in futures contracts on bonds and currencies, with precious metals showing a small gain. The Partnership experienced a gain in December 2010 as the Euro remained relatively steady after its previous month’s fall. U.S. equity markets rallied in contrast to the European equities, which have fallen this year.

Third Quarter 2010. The Partnership experienced a loss in July of 2010. Currency futures was the worst performing sector for the Partnership where losses were focused on the Euro. Trading in futures contracts on bonds, precious metals and agriculturals also contributed to losses for the month. Short term interest rate futures trading, driven by falls in US LIBOR rates, was the best performing sector during the month. The Partnership achieved a gain in August of 2010. Most of the month’s gains can be attributed to the bonds sector, with positive contributions from futures trading on interest rates, currencies and precious metals. Agricultural futures were the Partnership’s worst performing sector during August of 2010. The Partnership achieved a gain in September of 2010. The Partnership benefited from its long positions in agriculturals and precious metals as cotton futures hit a 15 year high and gold prices again set new highs. Crude oil ended the month close to where it started, while base metals and grains both moved higher. Losses were concentrated in the energy and fixed income futures markets. Gains in the Australian Dollar offset the Partnership’s losses in the Euro.

Second Quarter 2010. The Partnership achieved gains for the month of April of 2010 as US stock indices continued their ascent to end the month higher, while European stock indices declined. The Partnership’s best performing sector during the month was currencies, as it capitalized on the Euro’s steady decrease in value. In April, the Partnership introduced a small amount of currency forward trading on the Chinese Renminbi and the Taiwanese Dollar. The Partnership experienced a loss in May of 2010 as European economic concerns and the Euro’s decline continued to dominate the financial news. The Partnership’s currencies trading posted a positive performance during the month with short positions on the Euro and Pound covering the losses from the Partnership’s long positions on the Australian and Canadian Dollar. The Partnership’s worst performing sector was trading futures on equity indices, where long positions were hurt by the strong downward trend in equity indices. The Partnership achieved gains during the month of June of 2010 as yields on Greek, Portuguese and Spanish government bonds continued to rise. Fixed income markets were the Partnership’s strongest contributors during June, with US bonds also continuing to rise. Energies futures were the worst performing sector as the Partnership’s short positions suffered in the face of a rally in crude oil.

First Quarter 2010. January of 2010 started with the Partnership up by mid month, followed by a sharp sell-off in equity markets, which wiped out earlier gains. These losses were centered in the long equity futures positions, with gains in short term interest rate futures providing only a partial cushion. In February of 2010, the euro reacted to concerns over Greek sovereign debt by continuing its fall against the U.S. dollar, while equity markets reversed their initial drop to end the month virtually flat. U.S. and European bonds were volatile during the month. The Partnership’s gains were concentrated in currency and interest rate futures with stock index futures also posting modest gains. March of 2010 saw the euro rally for the first two weeks of the month, before reversing to make new lows for the year. U.S. equity markets put in a strong performance with the majority of the Partnership’s gains coming from equity index futures trading. The bond markets continued their volatility, making the sector the worst performing of the month. Weakness in the euro and British pound meant that strong gains were made in currencies, with crops and base metals also delivering a positive performance.

2009

During 2009, the Partnership achieved net realized and unrealized losses of $22,281,070 from its trading of commodity futures contracts including brokerage commissions of $5,636,378. The Partnership accrued total expenses of $13,656,913, including $546,869 in incentive fees, $7,310,067 in management fees paid to the General Partner, and $5,183,957 in service and professional fees. The Partnership earned $3,044,150 in interest income during 2009. An analysis of the profits and losses generated from the Partnership’s commodity futures trading activities for each quarter during 2009 is set forth below.

Fourth Quarter 2009. The Partnership experienced a loss during October as equity markets opened the month with a selloff, then rallied to make new highs for the year, before falling back to where they started the month. Crude oil briefly increased, gold made new highs and grains experienced some strong upward moves, while the U.S. Dollar continued its fall against the Euro. November was generally a good month for the Partnership with the continuation of a number of longer term trends. The general theme was the rallying of asset prices and the U.S. Dollar falling. Equity markets made new highs for the year, bonds rallied and gold put in a stellar performance to reach an all-time high. The Partnership made gains in equities, precious metals, currencies and fixed income markets and ended up for the month. A number of longer term trends reversed in December, which saw the Partnership give back some of November’s gains. Surprise employment numbers published early in the month helped the U.S. Dollar reverse its near year-long decline. Global stock markets moved higher, however, gold gave up most of the previous month’s gains, and there were similar sharp reversals in bonds and short term interest rates.

Third Quarter 2009. The Partnership experienced a loss in July 2009 as initial economic pessimism, driven by weaker than expected employment data, was reversed mid-month by strong earnings announcements in the U.S. Crude started the month by falling, but swiftly bounced back, mirroring the rally in stocks. Against a background of uncertainty in the fixed income markets, the Partnership’s returns were dominated by losses in the equity and bond sectors, with short-term interest rates posting modest gains. The Partnership’s currency positions continued to bring some diversification to the Partnership’s portfolio. August 2009 saw continued signs of economic recovery, with a further stream of positive data being released. The Federal Reserve Board again committed to leaving interest rates near zero while the Bank of England moved to continue its program of quantitative easing. The U.S. equity markets were up from lows set in March of 2009 and the Advisor’s stock index systems were slow to reverse their short positions, meaning that the Partnership gave back a portion of last year’s gain in stock indices. The global stock indices continued their strong rally into September 2009, while gold came close to its all time high, as the effective nationalization of debt by Governments created a fear of future inflation in debtor economies. Currencies were the strongest performing sector in September of 2009 as the Partnership benefited from the falling exchange rates of the U.S. Dollar. Short-term interest rates registered further gains and became the Partnership’s best performing sector for the nine months ended September 30, 2009.

Second Quarter 2009. The Partnership experienced a loss in April 2009 as trading conditions returned to something approaching normality, with daily ranges more constrained and volatility in decline. The main story for April 2009 was the continued rally of global equities, where the Partnership continued to retain a slightly increased but still relatively small short exposure. There was little offset from the other sectors, with bond yields increasing as sentiment on the economic situation became slightly more upbeat. Currency markets were also in flux, and the Partnership experiencing losses similar to what it experienced in the equity sectors during the month. Commodities also started a decline towards month-end as the very recent scare over swine flu began to impact the markets. The Partnership was down modestly in May 2009, a month that saw further signs of stability return to the financial system and liquidity continuing to improve to levels not seen since September 2008. However, the Partnership’s long and short exposures during the month were not synchronized to its advantage as the markets reacted to the new sense of relative confidence. Equities rallied during the month, while 10-year bond yields rose, resulting in mixed signals for the Partnership’s portfolio positions. Also, the Partnership’s exposure in the commodities such as the energy and agricultural sectors was also muddled. The Partnership was again down modestly in June 2009, as equities initially rallied, but fell back and ended flat as markets such as Russia fell 20% from their highs during the month. Commodities, in particular base metals, also rallied initially but retreated. The Partnership’s returns were dominated by volatile interest rate moves during June 2009, with losses in the debt and interest rate sectors. Against these losses, however, crops did well with a positive contribution to Partnership performance during the month.

First Quarter 2009. January of 2009 saw a wave of consistently poor economic numbers, with unemployment rising, Government debt increasing and recessionary conditions around the globe. In January, futures markets were volatile and the Partnership profited primarily in currencies, with the U.S. Dollar and Japanese

Yen remaining strong, while the Pound Sterling remained under pressure. Elsewhere in the portfolio, there were small losses in bonds and small profits in equities, while liquidity remained favorable. Throughout February, the situation in global financial and commodity markets worsened and no regions, countries, sectors or companies appeared immune from recessionary conditions. With volatility levels still elevated, the portfolio continued its low margin exposure with small profits made in short equities (due to falling stock indices in February). Gyrating currency markets caused small losses mainly attributable to weakening of the U.S. Dollar at month-end. The continued plunge in demand for commodities in February, combined with increasing inventories, kept a lid on prices. Crude oil and grain prices came under renewed price pressure, and the only sector to see higher prices was precious metals. Small gains were achieved from a small long position in gold, and the Partnership benefited primarily from being short grains. March proved a difficult month for the Partnership and losses were experienced in bond and equity futures, while the Partnership’s long exposure in the U.S. Dollar was damaged by both the increasing United States debt and rumors of the U.S. Dollar being sidelined as the reserve currency. The Japanese Yen position also suffered. The commodities sector was mixed in March, with the main features being vacillations in gold prices and a rally in energy. Small returns were derived in crude oil as it started to find some strength.

2008

During 2008, the Partnership achieved net realized and unrealized gains of $41,907,106 from its trading of commodity futures contracts including brokerage commissions of $499,445. The Partnership accrued total expenses of $13,589,300, including $8,685,185 in incentive fees, $2,474,653 in management fees paid to the General Partner, and $2,429,462 in service and professional fees. The Partnership earned $3,801,283 in interest income during 2008. An analysis of the profits and losses generated from the Partnership’s commodity futures trading activities for each quarter during 2008 is set forth below.

Fourth Quarter 2008. The Partnership experienced a fairly good month in October 2008, which was a remarkable month in the financial markets; disastrous for many traditional managers and some hedge funds, but generally favorable to commodity futures traders. Profits came mainly from short positions in falling equity indices and long positions in the U.S. Dollar, particularly versus the Canadian Dollar and Pound Sterling. November 2008 saw a certain amount of continuity from the previous two months, with continued government and central bank initiatives, both individual and collective, attempting to prevent further failures and stimulate economies. The markets continued to trend, with equity indices down, bond indices up and commodity markets trading lower. Exposure to bonds accounted for about half of November’s profits, as 10-year yields fell from 4.36% to an incredible 3.32%. The other half was derived from positions in the energy, interest rate and equity sectors. Continued gains were experienced in December 2008, as 10-year note yields in the US fell, which once again helped performance in the bond sector. The energy sector was the stand out performer for the Partnership in December, as crude oil prices declined sharply, whereas currency markets were more erratic resulting in a slight overall loss in that sector. Equity index returns were more or less flat for the month.

Third Quarter 2008. A loss in July of 2008 occurred as volatility returned to the commodity markets, with both the energy and grain sectors experiencing dramatic price fluctuations, and grain sectors falling significantly. The Partnership again experienced losses in August, although less dramatically than in the previous month. Profits were realized from a long bias in fixed income sectors, but suffered in the currency sector as the long-standing negative trend in the U.S. dollar reversed. With these two financial sectors offsetting each other, the net decline in August came from commodities – primarily crude oil, precious metals and grains. In September, the Partnership experienced a small net decline amidst high volatility, and sizeable losses in some sectors were offset by sizeable profits elsewhere in the portfolio. Losses in September were recorded in commodities and currencies as the dollar’s violent rally and accompanying commodity sell off continued to inflict damage on residual exposures. These were almost offset by erratic declines in stock indices and renewed strength in government bonds worldwide.

Second Quarter 2008. April 2008 saw performance dip slightly negative, although energy was a stand out performer, with the crude oil, unleaded gasoline and natural gas markets all contributing. It was also a profitable month in grains. However, the U.S. Dollar became somewhat range-bound while equities rallied against the Partnership’s overall small net short position. Low exposure to considerable gyrations in short-term interest rates had little effect, but long-term bonds proved less successful. Performance was positive in May of 2008, following small declines in March and April. Five out of the nine sectors traded showed positive returns. The continued boom in crude oil prices dominated the month, and gold in particular resumed its uptrend, as did a number of base metals.

Grains were mixed, tending to net against each other. Small profits in short-term interest rates and currencies were offset by equivalent losses in bonds and equities. The Partnership’s position in equities remained small during the period. June of 2008 saw a sharp decline in global equity markets, as a technical bear market looked to be in place in the United States. However, the Partnership was well positioned to benefit from these conditions, with equity indices accounting for nearly half the month’s positive return. Commodity markets, in particular crude oil and grains, made significant contributions for the month.

First Quarter 2008. January of 2008 saw a sharp decline in equities mirrored by rises in bonds and interest rate futures. The Partnership’s exposure to the equity indices was small and decreased during the month, and was more than offset by long positions in interest rate futures that were the source of a major portion of the Partnership’s profits. Sharply lower U.S. interest rates and rises in gold and agricultural and other commodity also benefited the portfolio’s established long positions, while offsetting losses were recorded in the energy sector. Commodity markets experienced renewed strength in February. The Partnership’s long positions in grains, metals and energy all made positive contributions, while the U.S. Dollar renewed its overall decline towards the end of the month, causing the Partnership to profit from its long exposure to the Euro. The Partnership lost ground in March against a background of acute and rising volatility across many markets and tightened liquidity. Profits in March came from the currency and grain sectors, while intra-month spikes in gold and energy prices caused losses for the Partnership’s metal and energy sector positions. Trading in most other sectors was flat, with losing sectors effectively cancelling out profitable ones.

(d) Off-Balance Sheet Arrangements

The Partnership does not engage in off-balance sheet arrangements with other entities.

(e) Contractual Obligations

Not required.

(f) Critical Accounting Estimates

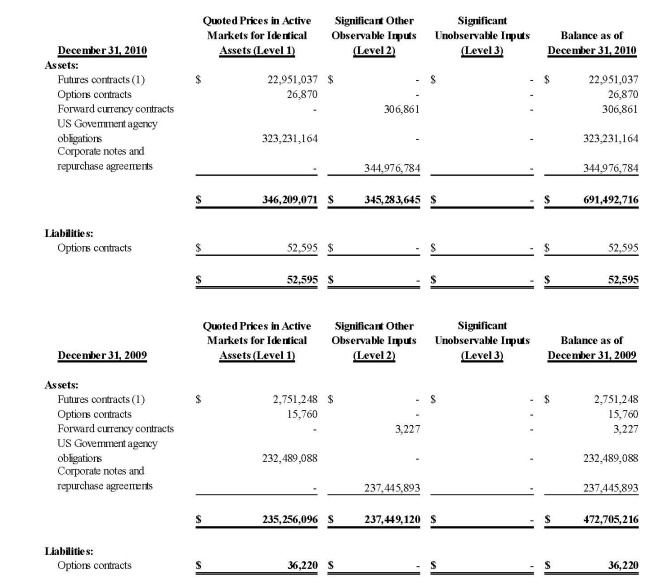

Altegris Funds believes that the Partnership's most critical accounting estimates relate to the valuation of the Partnership's assets. Futures and options on futures contracts are valued using the primary exchange’s closing price. Forward currency contracts are stated at fair value using spot currency rates provided by Newedge USA, LLC and adjusted for interest rates and other typical adjustment factors. United States government agency securities are generally valued based on quoted prices in active markets. Corporate notes and repurchase agreements are generally valued at cost given their short duration from the time of purchase. Security transactions are recorded on the trade date. Realized gains and losses from security transactions are determined using the identified cost method. Assets and liabilities denominated in currencies other than the U.S. dollar are translated into U.S. dollars at the rates in effect at the date of the statement of financial condition. Income and expense items denominated in currencies other than the U.S. dollar are translated into U.S. dollars at the rates in effect during the period. Gains and losses resulting from the translation to U.S. dollars are reported in income currently.

The Partnership’s financial statements are presented in accordance with accounting principles generally accepted in the United States of America, which require the use of certain estimates made by the Partnership’s management. Actual results could differ from those estimates. Based on the nature of the business and operations of the Partnership, Altegris Funds believes that the estimates utilized in preparing the Partnership’s financial statements are appropriate and reasonable, however actual results could differ from these estimates. The estimates used do not provide a range of possible results that would require the exercise of subjective judgment. Altegris Funds further believes that, based on the nature of the business and operations of the Partnership, no other reasonable assumptions relating to the application of the Partnership’s critical accounting estimates other than those currently used would likely result in materially different amounts from those reported.

ITEM 7A: QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Not required.

ITEM 8: FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

Financial statements required by this item are included herewith following the Index to Financial Statements and are incorporated by reference into this Item 8.

Because the Partnership is a Smaller Reporting Company, as defined by Rule 229.10(f)(1), the supplementary financial information required by Item 302 of Regulation S-K is not required.

ITEM 9: CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

None.

ITEM 9A: CONTROLS AND PROCEDURES

(a) The General Partner, with the participation of the General Partner’s principal executive officer and principal financial officer, has evaluated the effectiveness of the design and operation of its disclosure controls and procedures with respect to the Partnership as of the end of the period covered by this annual report, and, based on their evaluation, has concluded that these disclosure controls and procedures are effective.

(b) Management’s Annual Report on Internal Control over Financial Reporting

Altegris Funds, the general partner of the Partnership is responsible for the management of the Partnership. Management of Altegris Funds (“Management”) is responsible for establishing and maintaining adequate internal control over financial reporting. The internal control over financial reporting is designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles.

The Partnership’s internal control over financial reporting includes those policies and procedures that:

| | • | | Pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the Partnership; |

| | | | |

| | • | | Provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that the Partnership’s transactions are being made only in accordance with authorizations of Management and; |

| | | | |

| | • | | Provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use or disposition of the Partnership’s assets that could have a material effect on the financial statements. |

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Management assessed the effectiveness of the Partnership’s internal control over financial reporting as of December 31, 2010. In making this assessment, Management used the criteria set forth in Internal Control — Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (“COSO”). As a result of this assessment and based on the criteria in the COSO framework, management has concluded that, as of December 31, 2010, the Partnership’s internal control over financial reporting was effective.

(c) Changes in Internal Control over Financial Reporting

There were no changes in the Partnership’s internal control over financial reporting during the quarter ended December 31, 2010 that have materially affected, or are reasonably likely to materially affect, its internal control over financial reporting.

ITEM 9B: OTHER INFORMATION

None.

PART III

ITEM 10: DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

(a) Identification of Directors and Executive Officers

(i) The Partnership has no officers, directors, or employees. The Partnership’s affairs are managed by Altegris Funds (although it has delegated trading and investment authority to the Advisor and administrative duties to Altegris. Altegris Funds is owned by Genworth Financial Inc., and its directors and executive officers are Jon C. Sundt, Robert J. Amedeo, Matthew C. Osborne, Richard G. Pfister, Kenneth I. McGuire, and Gurinder S. Ahluwalia.

Jon C. Sundt (age 48) is the President, CEO and a director of Altegris Funds (October 2004 to present), having also served as a Vice President from July 2002 to October 2004. Mr. Sundt has also been (1) the President, CEO and a director of Altegris Investments, Inc. (Altegris) (July 2002 to present), a current broker-dealer affiliate of Altegris Funds, and formerly an IB and CTA; (2) a manager and the President and CEO of Altegris Advisors, L.L.C. (Advisors), an affiliate of Altegris Funds and an SEC-registered investment adviser (February 2010 to present); (3) a manager and the President and CEO of Altegris Futures, L.L.C. (Altegris Futures), an IB and an affiliate of Altegris Funds (September 2010 to present); (4) a manager and the President and CEO of Altegris Clearing Solutions, L.L.C. (formerly known as Altegris Partners, L.L.C.) (Clearing Solutions), an IB and CTA and an affiliate of Altegris Funds (December 2008 to present); and (5) a manager and the President and CEO of Altegris Services, L.L.C. (Services), an administrative and operations affiliate of Altegris Funds (May 2010 to present). Mr. Sundt became a principal of Altegris Funds in July 2002. Mr. Sundt attended the University of California, San Diego.

Robert J. Amedeo (age 56) has served as a director of Altegris Funds since July 2002. He has also been a Vice President of Altegris Funds (October 2004 to January 2011), and President of Altegris Funds (July 2002 to October 2004), and he currently serves as Executive Vice President (January 2011 to present). Mr. Amedeo has also been (1) an Executive Vice President and director of Altegris; (2) a manager and Executive Vice President of Advisors (February 2010 to present); (3) a manager and Executive Vice President of Clearing Solutions (December 2008 to present); (4) a manager and Executive Vice President of Services (May 2010 to present); and (5) a manager and Executive Vice President of Altegris Futures (September 2010 to present). In addition to his responsibilities as an officer and director of Altegris Funds and Altegris, Mr. Amedeo has pursued business development projects for the companies and their affiliates. Mr. Amedeo is a graduate of Northwestern University and received a Juris Doctor degree from DePaul University. Mr. Amedeo is currently Chairman of the NFA’s CPO/CTA Advisory Committee.

Matthew C. Osborne (age 45) has served as a director of Altegris Funds since July 2002. He has also served as a Vice President of Altegris Funds (July 2002 to January 2011), and currently serves as Executive Vice President (January 2011 to present). Mr. Osborne has also been (1) an Executive Vice President, Chief Investment Officer and a director of Altegris (July 2002 to May 2010); (2) a manager and Executive Vice President of Advisors (February 2010 to present); (3) a manager and Executive Vice President of Clearing Solutions (December 2008 to present); (4) a manager and Executive Vice President of Services (February 2010 to present); and (5) a manager and Executive Vice President of Altegris Futures (September 2010 to present).

Richard G. Pfister (age 38) has served as a director of Altegris Funds since October 2004. He has also served as a Vice President (October 2004 to January 2011) and currently serves as Executive Vice President (January 2011 to present). Mr. Pfister has also served as (1) an Executive Vice President and director of Altegris (October 2004 to present); (2) a manager and Executive Vice President of Clearing Solutions (December 2008 to present); and (3) a manager and Executive Vice President of Altegris Futures (September 2010 to present). Mr. Pfister graduated from the University of San Diego and holds the Chartered Alternative Investments Analyst (CAIA) designation.

Kenneth I. McGuire (age 52) became the Chief Operating Officer of Altegris Funds in May 2010 and is a principal of Altegris Funds (June 2010 to present). Mr. McGuire also serves as Chief Operating Officer for Advisors (February 2010 to present), and Services (May 2010 to present). His duties within the Altegris Companies include supervision of personnel in the software development, information technology, fund operations and futures operations businesses of the Altegris Companies. During the past five years, Mr. McGuire was employed by The Bank of New York Mellon, an asset management and securities services company, as a Managing Director (April 2006 to October 2009). Mr. McGuire was employed within BNY Mellon Alternative Investment Services, serving as Product Manager for that unit’s Single Manager Hedge Fund services. Mr. McGuire was a Strategic Advisor with Harvest Technology, a boutique investment technology consultancy (May 2005 to April 2006). Mr. McGuire graduated Magna Cum Laude from Hofstra University with a degree in Computer Science/Mathematics and received his MBA with a concentration in Management from Adelphi University.

Gurinder S. Ahluwalia (age 46) became a Director and principal of Altegris Funds in January 2011. Mr. Ahluwalia has served as President and CEO of Genworth Financial Wealth Management (GFWM), an investment advisory firm (June 2009 to present), as Co-Chairman of GFWM (July 2008 to June 2009), and as Vice Chairman of AssetMark Investment Services, Inc. (“AssetMark”) (August 2006 to July 2008). GFWM was created by the 2008 combination of two affiliated investment advisory firms: AssetMark and Genworth Financial Asset Management, Inc. (“GFAM”). Mr. Ahluwalia has also served in the capacities as: (i) President, Chairman and a Trustee of Genworth Financial Asset Management Funds, a mutual fund complex (February 2004 to present); (ii) a Trustee of the Genworth Variable Insurance Trust, a mutual fund offered through variable insurance products (July 2008 to present); and (iii) as a Director on the Boards of GFWM (August 2008 to present), GFAM (January 2004 to August 2008), Genworth Financial Trust Company (“GFTC”), an Arizona chartered trust company and custodian (January 2004 to present), Centurion Financial Advisors, Inc. (“CFA”), an investment advisory firm (January 2004 to present), and Centurion Capital Group, Inc., an intermediate holding company for CFA, GFWM and GFTC (January 2004 to present). In addition, Mr. Ahluwalia has since July 2006 served as a Vice President of Genworth, the publicly traded global financial security company and parent company of Altegris Funds and its direct affiliates, as well as the ultimate parent holding company for all other Genworth affiliated companies. Mr. Ahluwalia holds a B.S. in Computer Science from New York University, a B.E. in Electrical Engineering from Cooper Union, and an M.S. in Electrical Engineering from the New Jersey Institute of Technology.

None of the individuals listed above currently serves as a director of a public company.

(ii) Identification of Certain Significant Employees

None.

(iii) Family Relationships

None.

(iv) Business Experience

See above.

(v) Involvement in Certain Legal Proceedings.

None.

(vi) Promoters and Control Persons

Not Applicable.

(b) Section 16(a) Beneficial Ownership Reporting Compliance

Altegris Funds, Jon C. Sundt, Robert J. Amedeo, Matthew C. Osborne and Richard G. Pfister each filed initial reports on Form 3 after the Interests became registered under Section 12 of the Securities Exchange Act of

1934. Gurinder Ahluwalia filed an initial report on Form 3 after being appointed a director of Altegris Funds in January 2011.

(c) Code of Ethics

The Partnership has no employees, officers or directors and is managed by Altegris Funds. Altegris Funds has adopted a Code of Ethics that applies to its principal executive officers and certain other persons associated with Altegris Funds. A copy of this Code of Ethics may be obtained at no charge by written request to Altegris Funds, 1202 Bergen Parkway, Suite 212, Evergreen, Colorado 80439. Richard G. Pfister previously filed a Form 5 on March 31, 2010, a late filing, and will file a Form 5 in April, 2011, also a late filing. No subsequent filings on Form 4 or Form 5 have been required as there have been no changes in beneficial ownership of the Partnership that would trigger Form 4 or Form 5 filing requirements during the period.

(d) Corporate Governance

Not applicable.

ITEM 11: EXECUTIVE COMPENSATION

The Partnership has no officers, directors, or employees. None of the principals, officers, or employees of Altegris Funds or Altegris receives compensation from the Partnership. All persons serving in the capacity of officers or executives of Altegris Funds, the General Partner of the Partnership, are compensated by Altegris and/or an affiliate in respect of their respective positions with such entities. Altegris Funds receives a monthly management fee equal to 1/12 of 1.25% of the management fee net asset value of the month-end capital account balances attributable to Class A and Class B Interests and equal to 1/12 of 0.75% of the management fee net asset value of the month-end capital account balances attributable to Institutional Interests. Altegris Funds also receives a monthly administrative fee equal to 1/12 of 0.333% of the management fee net asset value of the month-end capital account balances attributable to Class A and Class B Interests.

Altegris receives continuing monthly compensation from the Partnership equal to 1/12 of 2% of the month-end net asset value of Class A Interests sold by Altegris.

During 2010, Altegris received, and from January 1, 2011, Altegris Futures, in its capacity as Introducing Broker to the Partnership, receives compensation for brokerage-related services. The Partnership will pay monthly brokerage charges equal to the greater of (A) actual commissions of $9.75 per round-turn (higher for certain exchanges or commodities) multiplied by number of round-turn trades, which amount includes other transaction costs; or (B) an amount equal to 0.125% of the management fee net asset value of all Interest holders’ month-end capital account balances (1.50% annually). If actual monthly commissions and transaction costs in (A) above are less than the amount in (B) above, the Partnership will pay the difference to the Introducing Broker as payment for brokerage-related services. In any month when the amount in (A) is greater than the amount in (B) above, the Partnership will pay only the amount described in (A) above.

The Partnership has no other compensation arrangements. There are no compensation plans or arrangements relating to a change in control of the Partnership or Altegris Funds. On December 31, 2010 Altegris Funds was acquired by Genworth Financial, Inc. in a transaction reported on Form 8-K on January 6, 2011.

ITEM 12: SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS

| (a) | Security ownership of certain beneficial owners |

Not applicable.

| (b) | Security Ownership of Management |

The Partnership has no officers or directors. Under the terms of the Limited Partnership Agreement, the Partnership’s affairs are managed by Altegris Funds, which has delegated discretionary authority over the Partnership’s trading to the Advisor. As of February 28, 2011, Altegris Funds’ general partner interest in the Partnership was valued at $3,588, which constituted approximately 0% of the Partnership’s total assets. As of February 28, 2011, the following directors and executive officers of Altegris Funds owned Interests in the Partnership.

| Class | Name and Address | | Value of Interests | | | Percentage Ownership | |

| | | | Held Directly | | | Held Indirectly | | | Held Directly | | | Held Indirectly | |

| Institutional | Jon C. Sundt 1200 Prospect Street, Suite 400 La Jolla, CA 92037 | | | | | $ | 25,852 | * | | | | | | 0.00003 | % |

| Institutional | Robert J. Amedeo 1200 Prospect Street, Suite 400 La Jolla, CA 92037 | | $ | 303,117 | | | | | | | | 0.0004 | % | | | | |

| Institutional | Richard G. Pfister 1200 Prospect Street, Suite 400 La Jolla, CA 92037 | | $ | 24,880 | | | $ | 5,357 | * | | | 0.00003 | % | | | 0.000007 | % |

* Held via a family trust.

None.

ITEM 13: CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE

The Partnership does not engage in any transactions with Altegris Funds or its affiliates other than in respect of the services and payment of fees therefor described above in Item 1.

The Partnership paid to Altegris Funds monthly management fees totaling $11,527,938 for the year ended December 31, 2010. The Partnership paid to Altegris Funds administrative fees totaling $1,166,030 for the year ended December 31, 2010.

The Partnership paid to Altegris monthly continuing compensation of $1,094,158 for the year ended December 31, 2010. In addition, Altegris, in its former capacity as the Introducing Broker for the Partnership, received from the Partnership’s clearing broker (i.e., Newedge USA) the following compensation: (i) a portion of the brokerage commissions paid by the Partnership to Newedge USA, and of the interest income earned on Partnership’s assets held at Newedge USA, equal to $1,149,725 for the year ended December 31, 2010. Altegris Futures, in its capacity as Introducing Broker, receives from the Partnership, monthly brokerage charges as described in Item 11. For the year ended December 31, 2010 the Partnership paid monthly brokerage charges of $7,108,761. As of December 2010, the Partnership anticipates, but has not yet commenced entry into, spot and other foreign exchange over-the-counter transactions with NAST as principal counterparty. Upon commencement of such transactions between the Partnership and NAST, Altegris, in its capacity as Introducing Broker for the Partnership, will receive a portion of the transaction fees received by NAST.

The Partnership has not and does not make any loans to the General Partner, its affiliates, their respective officers, directors or employees or the immediate family members of any of the foregoing, or to any entity, trust or other estate in which any of the foregoing has any interest, or to any other person.

None of the General Partner, its affiliates, their respective officers, directors and employees or the immediate family members of any of the foregoing, or any entity trust or other estate in which any of the foregoing has any interest has, to date, sold any asset, directly or indirectly, to the Partnership.

The Partnership has no directors, officers or employees and is managed by the General Partner. The General Partner is managed by certain of its principals, none of whom is independent of the General Partner.

ITEM 14: PRINCIPAL ACCOUNTING FEES AND SERVICES

The following table sets forth the fees billed to the Partnership for professional audit services provided by Spicer Jeffries LLP, the Partnership’s independent registered public accountant, for the audit of the Partnership’s annual financial statements for the years ended December 31, 2010 and 2009.

| FEE CATEGORY | 2010 | 2009 |

| | | |

| Audit Fees | $82,500* | $82,500 |

| Audit-Related Fees | - | - |

| Tax Fees | 17,500 | 17,500 |

| All Other Fees | - | - |

| | | |

| TOTAL FEES | $100,000 | $100,000 |

_________________

* Amount expected to be billed for 2010 services.

Audit Fees consist of fees paid to Spicer Jeffries LLP for (i) the audit of Winton Futures Fund, L.P. (US)’s annual financial statements included in the annual report on Form 10-K, and review of financial statements included in the quarterly reports on Form 10-Q and filed on Winton Futures Fund, L.P. (US)’s current reports on Form 8-K; and (ii) services that are normally provided by the Independent Registered Public Accountants in connection with statutory and regulatory filings of registration statements.

Tax Fees consist of fees paid to Spicer Jeffries LLP for professional services rendered in connection with tax compliance and Partnership income tax return filings.

The board of directors of Altegris Funds pre-approves the engagement of the Partnership’s auditor for all services to be provided by the auditor.

PART IV

ITEM 15: EXHIBITS, FINANCIAL STATEMENT SCHEDULES

The financial statements and balance sheets required by this Item are included herewith, beginning after the signature page hereof, and are incorporated into this Item 15.

The following documents (unless otherwise indicated) are filed herewith and made part of this registration statement.

| Exhibit Designation | Description |

| *3.1 | Certificate of Formation of Winton Futures Fund, L.P. (US) |

| | |

| *4.1 | First Amended Agreement of Limited Partnership of Winton Futures Fund, L.P. (US) |

| | |

| *10.1 | Advisory Contract between Winton Futures Fund, L.P. (US), Rockwell Futures Management, Inc.** and Winton Capital Management Limited and Amendment thereto dated June 1, 2008 |

| | |

| *10.2 | Introducing Broker Clearing Agreement between Fimat USA, LLC*** and Altegris Investments, Inc. |

| | |

| *10.3 | Form of Selling Agency Agreement |

| | |

| 31.01 | Rule 13a-14(a)/15d-14(a) Certification |

| | |

| 32.01 | Section 1350 Certification |

______________________

* This exhibit is incorporated by reference to the exhibit of the same number and description filed with the Partnership’s Registration Statement (File No. 000-53348) filed on July 30, 2008 on Form 10-12G under the Securities Exchange Act of 1934.

** Rockwell Futures Management, Inc. is now Altegris Portfolio Management, Inc.

*** Fimat USA, LLC is now Newedge USA, LLC.

SIGNATURES

Pursuant to the requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Dated: March 31, 2011 | WINTON FUTURES FUND, L.P. (US) By: ALTEGRIS PORTFOLIO MANAGEMENT, INC. |

| | By: /s/ Jon C. Sundt Name: Jon C. Sundt Title: Principal Executive and Principal Financial Officer |

Pursuant to the requirements of the Securities Exchange Act of 1934, this report has been signed below by the following persons on behalf of the General Partner of the Registrant and in the capacities and on the date indicated.

| Dated: March 31, 2011 | |

| | By: /s/ Jon C. Sundt Name: Jon C. Sundt Title: Executive Officer, Principal Financial Officer and majority of the board of directors, or equivalent thereof, of Altegris Portfolio Management, Inc. |

WINTON FUTURES FUND, L.P. (US)

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

_______________

| NOTE 1 - | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) |

Financial Derivative Instruments (continued)

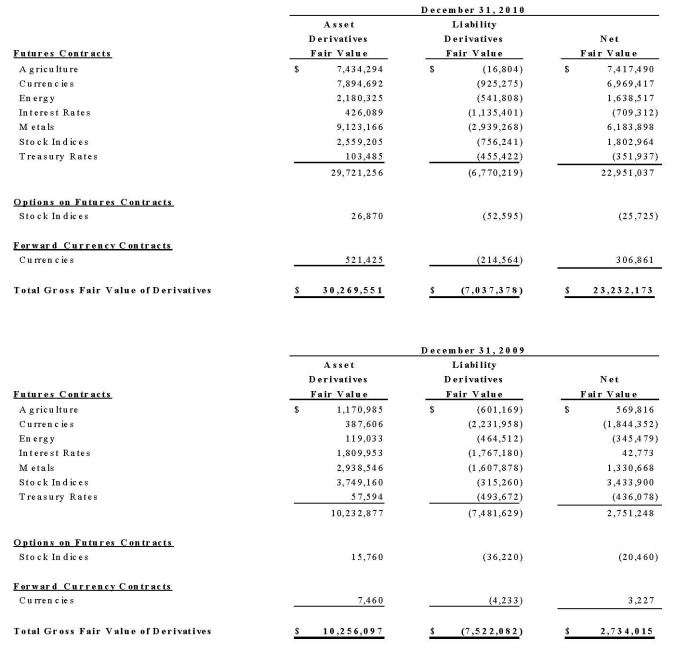

The number of contracts closed for futures contracts and options on futures contracts represents the number of contracts closed during the years ended December 31, 2010 and 2009 in the applicable category.

Reclassifications

Certain amounts in the 2009 and 2008 financial statements were reclassified to conform with the 2010 presentation.

Recently Issued Accounting Pronouncement

In January 2010, the FASB issued Accounting Standards Update No. 2010-06 (ASU 2010-06) entitled Fair Value Measurements and Disclosures (Topic 820) – Improving Disclosures about Fair Value Measurements. ASU 2010-06 amends the Fair Value Measurements and Disclosures Topic of the Codification to add new disclosure requirements about transfers into and out of Levels 1 and 2 and separate disclosures about purchases, sales, issuances and settlements in the reconciliation for fair value measurements using significant unobservable inputs (Level 3). It also clarifies existing disclosure requirements relating to the levels of disaggregation for fair value measurement and inputs and valuation techniques used to measure fair value. ASU 2010-06 is effective for interim and annual reporting periods beginning after December 15, 2009, except for disclosures about purchases, sales, issuances, and settlements in the roll forward of activity in Level 3 fair value measurements, which are effective for fiscal years beginning after December 15, 2010, and for interim periods within those fiscal years. The adoption of ASU 2010-06 did not have a material impact on the Partnership’s financial statements.

| NOTE 2 - | AGREEMENTS AND RELATED PARTIES |

Advisory Contract

The Partnership's trading activities are conducted pursuant to an advisory contract with Winton Capital Management, Limited ("Advisor"). The Partnership pays the Advisor a quarterly incentive fee of 20% of the trading profits (as defined). However, the quarterly incentive fee is payable only on cumulative profits achieved from commodity trading (as defined).

WINTON FUTURES FUND, L.P. (US)

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

_______________

| NOTE 2 - | AGREEMENTS AND RELATED PARTIES (CONTINUED) |

Advisory Contract (continued)

Effective July 1, 2008, the Advisor receives from the Partnership a monthly management fee equal to 0.083% (1.00% annually) for Class A, Class B, and Institutional Interests of the Partnership's management fee net asset value (as defined). In addition, the General Partner has assigned a portion of its management fees earned to the Advisor. Total management fees earned by the Advisor for the years ended December 31, 2010, 2009 and 2008 were $5,287,476, $3,266,333 and $933,820, respectively.

Brokerage Agreements

Newedge USA, LLC is the Partnership’s commodity broker (the “Clearing Broker”), pursuant to the terms of a brokerage agreement. The Partnership pays brokerage commissions to the Clearing Broker for clearing trades on its behalf.

General Partner Management Fee

The General Partner receives from the Partnership a monthly management fee equal to 0.0625% (0.75% annually) for Original Class A, 0.146% (1.75% annually) for Original Class B, and currently 0.0417% to 0.125% (0.50% to 1.5% annually) for Special Interests of the Partnership's management fee net asset value (as defined). Effective July 1, 2008, the General Partner receives from the Partnership a monthly management fee equal to 0.104% (1.25% annually) for Class A and Class B, and 0.0625% (0.75% annually) for Institutional Interests of the Partnership's management fee net asset value (as defined). The General Partner may declare any Limited Partner a “Special Limited Partner” and the management fees or incentive fees charged to any such partner may be different than those charged to other Limited Partners.

Total management fees earned by the General Partner, net of such management fees assigned to the Advisor, for the years ended December 31, 2010, 2009 and 2008 were $6,240,462, $4,043,734 and $1,540,833, respectively. Management fees payable to the General Partner as of December 31, 2010 and 2009 were $606,442 and $446,310, respectively.

Administrative Fee

Effective July 1, 2008, the General Partner receives from the Partnership a monthly administrative fee equal to 0.0275% (0.33% annually) of the Partnership's management fee net asset value (as defined) attributable to Class A and Class B Interests.

WINTON FUTURES FUND, L.P. (US)

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

_______________

| NOTE 2 - | AGREEMENTS AND RELATED PARTIES (CONTINUED) |

Service Fees

Original Class A Interests and Class A Interests pay selling agents an ongoing payment of 0.166% of the month-end net asset value (2% annually) of the value of interests sold by them which are outstanding at month end as compensation for their continuing services to the Limited Partners. Effective March 1, 2009 selling agents may, at their option, elect to receive the service fee for the sale of Institutional Interests.

Institutional Interests may pay selling agents, if the selling agent so elects, an ongoing payment of 0.0417% (0.50% annually) of the value of Institutional Interests sold by them which are outstanding at month end as compensation for their continuing services to the Limited Partners holding Institutional Interests.

Related Party

Altegris Investments, Inc. (“Altegris”), an affiliate of the General Partner, is registered as a broker-dealer with the SEC and an independent introducing broker registered with the Commodity Futures Trading Commission. Altegris has entered into a selling agreement with the Partnership where it receives 2% per annum as continuing compensation for interests sold by Altegris that are outstanding at month end. Altegris, as the Partnership’s introducing broker, also receives a portion of the commodity brokerage commissions paid by the Partnership to the Clearing Broker and interest income retained by the Clearing Broker. For the years ended December 31, 2010, 2009 and 2008, commissions, interest income and continuing compensation received by Altegris amounted to $9,352,644, $6,358,789 and $1,807,841, respectively.

Effective March 1, 2009, the Partnership pays to its clearing brokers and Altegris, at a minimum, brokerage charges at a flat rate of 0.125% (1.5% annually) of the Partnership’s management fee net asset value (as defined). Brokerage charges may exceed the flat rate described above, depending on commission and trading volume levels, which may vary.

WINTON FUTURES FUND, L.P. (US)

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

_______________

| NOTE 2 - | AGREEMENTS AND RELATED PARTIES (CONTINUED) |